Dynamically Aggregating Diverse Information111We are grateful to Cuimin Ba, Yash Deshpande, Mira Frick, Drew Fudenberg, Boyan Jovanovic, Erik Madsen, George Mailath, Konrad Mierendorff, Lan Min, Jacopo Perego, Peter Norman Sørensen, Jakub Steiner, Philipp Strack and Can Urgun for helpful comments and suggestions. Xiaosheng Mu acknowledges the hospitality of Columbia University and the Cowles Foundation at Yale University, which hosted him during parts of this research. Annie Liang thanks National Science Foundation Grant SES-1851629 for financial support.

Abstract

An agent has access to multiple information sources, each of which provides information about a different attribute of an unknown state. Information is acquired continuously—where the agent chooses both which sources to sample from, and also how to allocate attention across them—until an endogenously chosen time, at which point a decision is taken. We provide an exact characterization of the optimal information acquisition strategy under weak conditions on the agent’s prior belief about the different attributes. We then apply this characterization to derive new results regarding: (1) endogenous information acquisition for binary choice, (2) strategic information provision by biased news sources, and (3) the dynamic consequences of attention manipulation.

1 Introduction

We study dynamic acquisition of information when a decision-maker has access to multiple sources of information, and limited resources with which to acquire that information. Our decision-maker seeks to learn a Gaussian state, and each information source is modeled as a diffusion process whose drift is an unknown “attribute” that contributes linearly to the state. Attributes are potentially correlated. This structure captures information acquisition in many economic settings, including for example:

-

•

A governor wants to learn the number of cases of a disease outbreak, and can acquire information about the incidence rate of the disease in different cities.

-

•

An investor wants to assess the value of an asset portfolio, and acquires information about the value of each asset included in the portfolio.

-

•

An analyst wants to forecast a macroeconomic variable such as GDP growth, and needs to aggregate recent economic activities across different industries and locations.

At every instant of continuous time, the decision-maker allocates a fixed budget of attention/resources across the information sources, where this allocation determines the precision of information extracted from each source. For example, the governor may have a limited number of tests to allocate across testing centers each day, where more tests lead to a more precise estimate of the incidence rate. The decision-maker acquires information until an endogenously chosen stopping time, at which point he makes a decision whose payoff depends on the unknown state.

Our contribution is to demonstrate that the optimal dynamic acquisition strategy can be explicitly characterized under weak conditions on the prior belief, and to explain what those conditions are. Under the optimal strategy, the decision-maker initially exclusively acquires information from the single most informative source, where “more informative” is evaluated with respect to his prior belief over the unknown attribute values. At fixed times, the decision-maker begins learning from additional sources, and divides attention over these new sources as well as the ones he was learning from previously. Eventually, the decision-maker acquires information from all sources using a final and constant mixture. Notably, the optimal information acquisition strategy is not only history-independent but also robust across all decision problems. This implies, for example, that one does not need to solve for the optimal stopping time and information acquisition strategy jointly in this problem—optimal information acquisition is independent of when the decision-maker stops. We make use of this implication in Section 5.1 to derive new results about the optimal stopping behavior in a binary choice problem.

To gain some intuitions for the optimal information acquisition strategy, it is useful to compare our problem with a simpler one, in which the decision-maker acquires information for a decision at a fixed end date. Since the payoff-relevant state and all sources of information are Gaussian in our setting, the Blackwell-optimal solution would then be to acquire information in any way that minimizes posterior variance of the state at the known end date (Blackwell, 1951; Hansen and Torgersen, 1974). We show that under certain conditions on the prior belief, it is possible to “string together” these solutions across different end dates using a single history-independent dynamic strategy, which thus minimizes posterior variance at every moment of time. Generalizing a result of Greenshtein (1996), we show that this strategy—which we call the “uniformly optimal” strategy—is best for every decision problem and every distribution over stopping times, including those that are endogenously chosen.

When a uniformly optimal strategy does not exist, the variance-minimizing strategies for some end dates are in conflict with one another. In these environments the decision-maker must trade off across possible end dates, where the optimal way of doing this in general depends on the stopping time distribution and details of the payoff function. Thus, the existence of a uniformly optimal strategy is key to guaranteeing the properties of history independence and robustness across decision problems that we have outlined for our solution.

The question of whether a uniformly optimal strategy exists turns out to relate to a classic problem in consumer theory regarding the normality of demand—i.e., whether a consumer’s demand for various goods is weakly increasing in income. In our setting, the decision-maker’s “utility function” is the negative of the posterior variance function, and his “income” is the budget constraint on attention. When a uniformly optimal strategy exists, this means that the decision-maker’s demand for information from each source is weakly increasing in his overall attention budget. One of our sufficient conditions for existence of a uniformly optimal strategy—“perpetual complementarity” of the different sources—directly connects to a known sufficient condition in the literature for normality of demand. We additionally utilize the specific structure of our problem to provide two new sufficient conditions, and show that all of these conditions can be simply stated in terms of the decision-maker’s prior belief. See Section 4 for further details.

Beyond the specific statements of the results, a main contribution of this paper is demonstrating that in the present framework (i) the study of endogenous information acquisition is quite tractable, permitting explicit and complete characterizations; and (ii) there is enough richness in the setting to accommodate various economically interesting questions (e.g., about the role of primitives such as correlation across attributes). This makes the characterizations useful for deriving new substantive results in settings motivated by particular economic questions. We illustrate this with three applications, where we use our main results to generalize (Application 1) and complement (Application 3) existing results in the literature, as well as to solve for the equilibrium in a new game between competing news sources (Application 2). In all three applications, we discover new economic insights.

Application 1: Binary Choice.

A large literature in economics and neuroscience (originating with Ratcliff and McKoon (2008)) considers a consumer’s decision process for choosing between two goods with unknown payoffs. Recently, Fudenberg et al. (2018) proposed a model in which a decision-maker endogenously allocates attention across learning about two normally distributed, but i.i.d., payoffs. This model is nested in our framework. We use our main result to generalize Fudenberg et al. (2018)’s Proposition 3 and Theorem 5 beyond i.i.d. payoffs to settings with (1) correlation in the payoffs and (2) asymmetry in the consumer’s initial knowledge about the two payoffs. These generalizations bring important realism to the setting, since correlation and asymmetry are common features of choice environments. We characterize the optimal attention allocation given an arbitrary normal prior about the payoffs, and show that Fudenberg et al. (2018)’s main economic insight regarding the relationship between choice speed and accuracy holds in this general setting.

Application 2: Biased News Sources.

In our next application, we consider a stylized game between a liberal and a conservative news source that report on a common unknown (e.g., the fiscal cost of a policy proposal), where their reporting is biased in opposite directions. The sources choose the size of their bias, as well as the informativeness of their reporting, and compete over readers’ attention. Using our characterization of information acquisition, we are able to derive the complete time path of readers’ attention allocations given the sources’ choices of precision and bias levels, which allows us to characterize equilibrium news provision in this model. One particular insight that emerges from this analysis is that incentives for bias not only lead to greater polarization in equilibrium, but also lead to lower-quality news provision (i.e., larger noise choices). This analysis contributes to a literature about how competition across news sources affects the quality of news (Gentzkow and Shapiro, 2008; Galperti and Trevino, 2020; Chen and Suen, 2019; Perego and Yuksel, 2020), where our work is distinguished in considering the role of the time path of information demand.

Application 3: Attention Manipulation.

Finally, we use our framework to study the dynamic consequences of a one-time attention manipulation. Recently, Gossner et al. (2020) studied this question in a model where a decision-maker chooses between goods with independent payoffs. Under some assumptions, they show that a one-time manipulation of attention towards a given good leads to persistently higher cumulative attention devoted to that good, and persistently lower cumulative attention to every other good. We derive a complementary result in our setting, focusing on how correlation across the unknown attributes affects the consequences of attention manipulation. We show that with two sources, Gossner et al. (2020)’s insights hold under flexible patterns of correlation. On the other hand, with more than two sources, the nature of correlation matters. We identify a property of the prior belief under which all sources provide substitutable information, and show that under this property (but not in general), attention manipulation leads to persistently higher attention for that source and lower attention for others.

1.1 Related Literature

Our work builds on a large literature regarding dynamic acquisition of information. One part of this literature considers choice between unconstrained information structures at entropic (or more generally, “posterior-separable”) costs, see e.g. Yang (2015), Steiner et al. (2017), Hébert and Woodford (2020), Morris and Strack (2019), and Zhong (2019).222It is interesting that Steiner et al. (2017) also showed how the solution to their dynamic problem reduces to a series of static optimizations, similar to our multi-stage characterization. However, their argument is based on the additive property of entropy and differs from ours. Under this modeling approach, the cost to acquiring information depends on the decision-maker’s current belief, and is often interpreted as a mental processing cost (Mackowiak et al., 2020). In contrast, a second set of papers—to which our paper belongs—models agents as dynamically allocating a fixed budget of resources across a prescribed (and finite) set of experiments, see e.g. Che and Mierendorff (2019), Mayskaya (2019), Fudenberg et al. (2018), Gossner et al. (2020), and Azevedo et al. (2020). These papers, and ours, assume that the cost of information is independent of what the decision-maker currently knows. We view such information costs as a better match for applications in which the cost to information acquisition is physical, e.g., a limit on the number of available COVID tests that can be administered in a given day.

Relative to this latter strand of literature, a distinguishing feature of our work is the presence of flexible correlation. Dynamic learning about correlated unknowns is generally intractable, so there has been relatively little work done in this area. An exception is a model introduced by Callander (2011), where the available signals are the realizations of a single Brownian motion path at different points, and the agent (or a sequence of agents) chooses myopically. This informational setting has since been extended by Garfagnini and Strulovici (2016), which considers the optimal experimentation strategy for a forward-looking agent with acquisition costs, and Bardhi (2020), which introduces a potential conflict between an agent acquiring the information and a principal making the decision. These models differ from ours in that agents can perfectly observe any of an infinite number of attributes, and the correlation structure across the attributes is derived from a primitive notion of similarity or distance. We show that in a different model with flexible correlation across a finite number of sources (and with noisy observations), it is sometimes possible to exactly characterize the optimal forward-looking solution.333Also related are Klabjan et al. (2014) and Sanjurjo (2017), which study learning about multiple attributes. Besides having noisy Gaussian signals, the main distinction of our informational setting is again that we allow for correlation across attributes and focus on what this correlation implies for the optimal learning strategy.

Our work additionally connects to a large literature on sequential sampling in statistics and operations research. Since the information acquisition decisions in our model are not directly linked to flow payoffs, our model does not fall under the classic multi-armed bandit framework (Gittins, 1979; Bergemann and Välimäki, 2008). This feature also distinguishes our results relative to a classic literature on “learning by experimentation” (Easley and Kiefer, 1988; Aghion et al., 1991; Keller et al., 2005). The “best-arm identification” problem (Bubeck et al., 2009; Russo, 2016) is more closely related to us, as it considers a decision-maker who samples for a number of periods before selecting an arm and receiving its payoff. Indeed, the special case of two arms with jointly normal payoffs is nested in our framework under the case of two attributes and equal payoff weights. Our Theorem 1 thus builds on a prior result of Frazier et al. (2008), which showed that myopic information acquisition—or the “knowledge gradient” policy in the language of that literature—is optimal when the two arms have independent normal payoffs. Our result generalizes Frazier et al. (2008)’s result by allowing for correlated payoffs and a broader class of decision problems.

The best-arm identification problem between three or more arms falls outside of our framework, since payoffs in that problem depend on a multi-dimensional unknown.444With two arms, the difference in their payoffs is a sufficient statistic for choosing which arm is better. Such reduction to a one-dimensional unknown is not available in the case of many arms. From a number of papers including Chick and Frazier (2012) and Ke and Villas-Boas (2019), it is well-understood that characterizing the optimal strategy in those problems is quite challenging (although Frazier et al. (2008) and Frazier et al. (2009) showed that the knowledge gradient policy performs well asymptotically). Our setting also involves multi-dimensional uncertainty, but we assume that the unknowns are linearly aggregated into a one-dimensional payoff-relevant variable. We show that under this restriction, exact characterization of the optimal strategy is feasible, and in fact it is the knowledge gradient policy (suitably defined in continuous time). We also discover new properties of the knowledge gradient policy in our continuous-time setting: In each of a finite number of stages, the policy attends to a fixed set of attributes with a constant ratio of attention, until this set expands and the next stage commences.

A key technical tool behind our characterization builds on a literature about the comparison of normal experiments. Following the classic work of Blackwell (1951), Hansen and Torgersen (1974) showed that in a static decision problem, different normal signals about a one-dimensional payoff-relevant state can be Blackwell-ranked based on how much they reduce the variance of the state. Greenshtein (1996) subsequently derived comparisons between deterministic sequences of conditionally independent normal signals about an unknown state. His Theorem 3.1 implies that one sequence Blackwell-dominates another if and only if it leads to lower posterior variances about the state at every time. Our Lemma 5 shows that Greenshtein (1996)’s characterization is valid in a more general setting, in which time is continuous, and the sequence of signals can be chosen in a history-dependent manner (i.e., the first signal’s realization can determine which signal is chosen next).

2 Model

An agent has access to information sources, each of which is a diffusion process that provides information about an unknown attribute . The random vector is jointly normal with a known prior mean vector and prior covariance matrix . We assume has full rank, so the attributes are linearly independent.

As we describe in more detail below, the agent’s decision depends on a payoff-relevant state . We assume the state is a linear combination of the attributes:

Assumption 1.

for known weights .

It is equivalent (up to a constant) to assume that the vector is jointly normal, and that there is no residual uncertainty about conditional on the attribute values.555If are jointly normal, then can be rewritten as a linear combination of the plus a residual term that is independent of each . The assumption of no residual uncertainty means that the residual term is a constant, returning Assumption 1 up to an additive constant (which can be normalized to zero in our problem). Because any attribute value can be replaced with its negative, assuming is without loss. For ease of exposition, we will further assume that each weight is strictly positive.

Time is continuous, and the agent has a unit budget of attention to allocate at every instant of time. Formally, at each , the agent chooses an attention vector subject to the constraints (attentions are positive) and (allocations respect the budget constraint).

Attention choices influence the diffusion processes observed by the agent in the following way:

| (1) |

Above, each is an independent Brownian motion, and the term is a standard normalizing factor to ensure constant informativeness per unit of attention devoted to each source. Thus, devoting units of time to observation of source is equivalent to observation of the normal signal , or independent observations of the standard normal signal . This formulation treats “attention” and “time” in the same way, in the sense that devoting attention to source for a unit of time provides the same amount of information about as devoting full attention to source for a unit of time. We also note that since all sources are assumed to be equally informative about their corresponding attributes, it is with loss to further normalize the payoff weights to be equal to one another.666In fact, our subsequent results indicate that the case of equal weights is special. For example, with two sources, the conclusions of Theorem 1 always hold when , but do not hold in general.

Remark 1.

As these comments suggest, there is a natural discrete-time analogue to our continuous-time model: At each period , the agent has a unit budget of precision to allocate across normal signals. Choice of attention vector results in one observation of the normal signal for each source . All of our main results have an immediate corollary in that model. See Section 6 for further discussion.

Let describe the relevant probability space, where the information that the agent observes up to time is the collection of paths (with representing the sample path of from time to time ). An information acquisition strategy is a map from into , representing how the agent divides attention at each instant as a function of the observed diffusion processes.777We assume that given the agent’s attention strategy, the stochastic differential equations in (1) have a solution. This is true for example if each is a deterministic function of (as in the optimal strategy that we describe in Theorems 1 and 2), or if satisfies standard Lipschitz conditions (see Section 6.1 of Yong and Zhou (1999)). In addition to allocating his attention, the agent chooses how long to acquire information for; that is, at each instant he determines (based on the history of observations) whether to continue acquiring information, or to stop and take an action. Formally, the agent chooses a stopping time , which is a map from into satisfying the measurability requirement for all .

At the endogenously chosen end time , the agent will choose from a set of actions and receive the payoff ), where is a known payoff function that depends on the stopping time , the action taken and the payoff-relevant state . This formulation allows for additively separable waiting costs, , as well as geometric discounting, . The agent’s posterior belief about at time determines the action that maximizes his expected flow payoff . We will only impose the following weak assumption on the payoff function:

Assumption 2.

Given any (normal) belief about , is decreasing in .

That is, we assume that holding fixed the agent’s belief at the time of decision, an earlier decision is better. In the case of , this assumption requires the waiting cost to be non-decreasing in ; in the case of , the assumption is that the optimal flow payoff is non-negative (which is satisfied, for example, if there is a default action that always yields zero payoff).

To summarize, the agent chooses his information acquisition strategy and stopping time to maximize In this paper we primarily focus on characterizing the optimal information acquisition strategy . In general the strategies and should be determined jointly, but our results will show that in many cases the optimal can be characterized independently from the choice of .

3 Main Results

In Section 3.1 we consider the case of two attributes, where we are able to derive a slightly stronger result. In Section 3.2 we characterize the optimal attention allocation strategy for any finite number of attributes. All proofs appear in the appendix, and we provide an extended explanation of these results in Section 4.

3.1 Two Attributes

Suppose there are two attributes and , and the payoff-relevant state is , with each . The agent’s prior over the unknown attributes is . Then the prior covariance between each attribute and the payoff-relevant state is , and we assume that these covariances satisfy the following relationship:

Assumption 3.

.

Since both variances are positive, this property holds if the covariance is not too negative relative to the size of either variance. If the weights on the two attributes are equal (i.e., ), this property holds for all prior beliefs over the attributes (since ). If the attributes are positively correlated (), then this property holds for all payoff weights and .

Theorem 1.

Suppose and Assumption 3 is satisfied. W.l.o.g. let . Define

Then an optimal information acquisition strategy is history-independent and hence can be expressed as a deterministic path of attention allocations . This path consists of two stages:

-

•

Stage 1: At all times , the agent optimally allocates all attention to attribute (that is, and ).

-

•

Stage 2: At all times , the agent optimally allocates attention in the constant proportion .

There are two stages of information acquisition. In the first stage, which ends at some time , the agent allocates all of his attention to the attribute with higher prior covariance with the payoff-relevant state. After time , he divides his attention across the attributes in a constant ratio, where the long-run instantaneous attention allocation is proportional to the weights . Note that depending on the agent’s stopping rule, Stage 2 of information acquisition may never be reached along some histories of the diffusion processes. But as long as the agent continues acquiring information, his attention allocations are as given above. In Online Appendix O.1, we show that under mild technical assumptions, the optimal attention strategy is in fact unique up to the stopping time (after which attention allocations obviously do not matter).

The characterization reveals that the optimal information acquisition strategy is completely determined from the prior covariance matrix and the payoff weight vector (the prior mean vector does not play a role). In particular, the strategy does not depend on details of the agent’s payoff function , including his time preferences. When the prior belief satisfies Assumption 3, the optimal information acquisition strategy is thus constant across different objectives and also across different stopping rules. Relatedly, as we demonstrate in Section 5.1, we can solve for the optimal stopping rule in this setting as if information acquisition were exogenously given by Theorem 1. In Online Appendix O.2.1, we provide an example to illustrate that these properties can fail when Assumption 3 is violated. Online Appendix O.2.2 further shows that for the case of two attributes, Assumption 3 is not only sufficient but also necessary for our characterization to hold independently of the agent’s payoff criterion.

Below we illustrate this optimal strategy using a few simple examples.

Example 1 (Independent Attributes).

Suppose and the payoff-relevant state is . Then, applying Theorem 1, the agent initially puts all attention towards learning . At time , his posterior covariance matrix is the identity matrix. After this time he optimally splits attention equally between the two attributes, which are now symmetrically distributed.

Example 2 (Correlated Attributes).

Suppose , and the payoff-relevant state is still . Applying Theorem 1, the agent initially puts all attention towards learning . At time , his posterior covariance matrix becomes . Compared to the previous example, it takes longer for the agent’s uncertainty about the two attributes to equalize, since information about also reduces the agent’s uncertainty about . After he optimally splits attention equally between the two attributes.

Example 3 (Unequal Payoff Weights).

Consider the prior belief given in the previous example, but suppose now that the payoff-relevant state is . As before, the agent initially puts all attention towards learning . Stage 1 ends at time , when the posterior covariance matrix is . Note that because of the asymmetry in the payoff weights, the agent’s posterior uncertainty about the two attributes is not the same at this switch point. As we will discuss in Section 4, however, the marginal values of learning about the two attributes are equal to one another at time . After this time, the agent optimally acquires information in the mixture .

3.2 Attributes

We now consider the case of multiple attributes. We provide three different sufficient conditions under which the optimal information acquisition strategy can be exactly characterized.

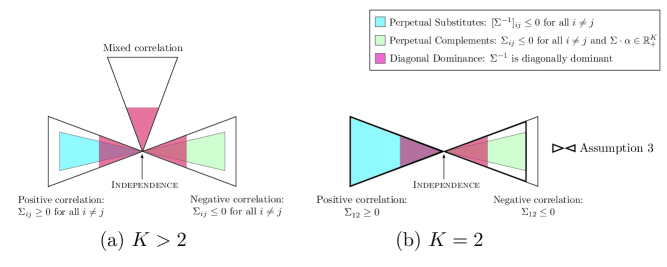

Assumption 4 (Perpetual Substitutes).

has non-positive off-diagonal entries.

Assumption 5 (Perpetual Complements).

has non-positive off-diagonal entries and has non-negative coordinates.

Assumption 6 (Diagonal Dominance).

is diagonally-dominant. That is, for all

These conditions, their relationship to one another, and their relationship to our previous Assumption 3 for the case of , are depicted in Figure 1. Assumption 4 generalizes a previous sufficient condition to more than two attributes. It requires that the partial correlation between any two attributes—controlling for all other attributes—is positive.888The partial correlation between attributes and under covariance matrix is equal to .,999Positive-definite matrices with non-positive off-diagonal entries are known as -matrices (Plemmons, 1977). It is well-known that the inverse of such matrices has positive entries everywhere. Thus Assumption 4 implies positive correlation , but is strictly stronger when . We mention that assuming for all does not guarantee Theorem 2 to hold. A counterexample with three sources is presented in Online Appendix O.2.3. Proposition 7 in Online Appendix O.3 shows that Assumption 4 is an if and only if condition for information from any pair of sources to be “perpetually substitutable.” By this we mean that the value of acquiring information from one source is decreasing in the amount of information from the other source, and that this property holds not only at time but also along any path of information acquisitions.

Assumption 5 imposes that all attributes are negatively correlated with one another, but that each attribute is initially positively correlated with the payoff-relevant state. Under this assumption, prior covariances are “mildly” negative. Proposition 8 in Online Appendix O.3 shows that Assumption 5 is an if and only if condition for information from any pair of sources to be perpetually complementary, in the sense that the value of acquiring information from one source is increasing in the amount of information from the other source, again along the entire path of information acquisitions.

The last Assumption 6 requires the inverse of the prior covariance matrix to be diagonally-dominant. Roughly speaking, this assumption allows for some pairs of attributes to be complements and other pairs to be substitutes, but puts an upper bound on the magnitude of any complementarity or substitution effects. When , Assumption 6 reduces to the simple condition , which is sufficient for our previous Assumption 3. For general , Assumption 6 is implied by a similar condition for all (see Appendix A.3) We explain the role of these assumptions in Section 4.

Theorem 2.

Suppose any of Assumption 4, 5, or 6 is satisfied.101010We point out that while Assumption 4, 5, and 6 are each sufficient for the theorem to hold, they are not in general necessary (unlike Assumption 3 in the case). Then, there exist times

and nested sets

such that an optimal information acquisition strategy is described by a deterministic path of attention allocations . This attention path consists of stages: For each , is constant at all times and supported on the sources in . In particular, the optimal attention allocation at any time is proportional to .

The full path of attention allocations (including the times , the nested sets , and the constant attention allocation at each stage ) can again be determined directly from the primitives and . In Appendix D, we provide an algorithm for computing this path. Theorem 2 thus tells us that the agent can reduce the dynamic information acquisition problem to a sequence of static problems, each of which involves finding the optimal constant division of attention for a fixed period of time (from to ). Moreover, as in the case, the optimal information acquisition strategy does not depend on the agent’s payoff function, and is history-independent.

We note that each of Assumption 4, 5, or 6 is “absorbing” in the following sense: If the prior covariance matrix satisfies any of these conditions, then so does any posterior covariance matrix. Propositions 7 and 8 respectively show that this is true for Assumptions 4 and 5, whereas diagonal dominance is absorbing because any information acquisition strategy only increases the diagonal entries of the precision matrix .111111By directly computing and at posterior beliefs, it can be shown that our previous Assumption 3 for the case of two attributes is also absorbing. The absorbing property implies that our characterization not only applies to the prior belief, but also to any posterior belief even if the history involves sub-optimal attention allocations. This feature enables us to study the effect of attention manipulation, an application that we pursue in Section 5.3.

Finally, we mention that starting from any prior belief (including those that fail all three of the sufficient conditions we have provided), so long as the agent does not stop learning about any attribute, his posterior belief must eventually satisfy Assumption 6.121212This is because any attention devoted to attribute simply increases the -th diagonal entry of the precision matrix . With sufficient attention devoted to each attribute, the posterior precision matrix must be diagonally-dominant. Theorem 2 applies at these posterior beliefs, implying in particular that the agent’s optimal attention allocation is eventually constant and proportional to the weight vector .

4 Explanation of Results

4.1 Fixed Stopping Time

Consider the simpler problem in which the agent makes a decision at an exogenously fixed and known time . Because normal signals can be completely Blackwell-ordered based on their precisions (Hansen and Torgersen, 1974), different mixtures over the sources can be compared based on how much they reduce the variance of the payoff-relevant state.

Formally, the agent’s past attention allocations integrate to a cumulative attention vector at time , describing how much attention has been paid to each attribute thus far. The agent’s posterior variance of is

| (2) |

where is the prior covariance matrix over the attribute values, and is the diagonal matrix with entries . This posterior variance depends solely on the payoff weights , the prior covariance matrix , and the cumulative acquisitions . It does not depend on the realizations of the diffusion processes or the order of information acquisitions. So the problem of optimizing for a fixed end date reduces to a static problem of optimally allocating units of attention.

Define the -optimal attention vector

to be the allocation of units of attention that minimizes posterior variance of , which is unique by Lemma 4 in the appendix. Every information acquisition strategy that cumulates to the attention vector at time is optimal for any decision problem at that time.

4.2 Uniformly Optimal Strategy: Definition

In general, the family of solutions corresponding to optimal allocation of units of attention does not determine the solution to the dynamic problem. To see this, suppose , so that the optimal way to allocate attention for a decision at time is to allocate it all to the second attribute, but , so that the optimal way to allocate attention for a decision at time is to allocate it all to the first attribute. Clearly these -optimal attention vectors are incompatible under a single dynamic strategy: Optimal attention allocation for a decision at time precludes achieving the optimal attention allocation for time . So when the agent faces the possibility of stopping at either time or (depending on the realizations of the diffusion processes), he must trade off between achieving more precise information about the payoff-relevant state at either time. The optimal resolution of this trade-off depends on the specific decision problem.

If, however, it were possible to continuously string together the -optimal attention vectors along the path of one information acquisition strategy, then such intertemporal trade-offs would not arise, and we might further conjecture such a strategy to be optimal for all stopping problems. This turns out to be true.

Definition 1.

Say that an information acquisition strategy is uniformly optimal if it is deterministic (i.e., history-independent) and its induced cumulative attention vector at each time is the -optimal vector .

A uniformly optimal strategy, by definition, minimizes posterior variance at every instant . A result of Greenshtein (1996) implies that such a strategy is best among all history-independent information acquisition strategies. In Lemma 5, we extend Greenshtein (1996)’s result to show that a uniformly optimal strategy is best among all strategies, including those that condition future attention allocations on past signal realizations. In brief, we first observe that compared to any alternative information acquisition strategy, the uniformly optimal strategy achieves the same precision of beliefs about the state at earlier times. We then use this observation to show that any decision rule (i.e., any stopping time and final action) achievable under the alternative strategy can be replicated under the uniformly optimal strategy in a way that makes the agent stop earlier, but maintains his belief at the time of stopping. This “replicating” decision rule, together with the uniformly optimal attention strategy, thus yields a higher expected payoff. We note that this proof relies crucially on the normal environment, which allows us to capture the agent’s uncertainty through the single statistic of posterior variance.

Thus, whenever a uniformly optimal strategy exists, it must be the optimal strategy in our problem.131313Our argument based on Blackwell comparisons gets to the optimal policy (i.e., attention allocation) without going through the HJB equation and value function, which may be difficult to solve for explicitly. It remains to show that under the assumptions we provided previously, a uniformly optimal strategy does exist, and has the structure described in Theorems 1 and 2.

4.3 Uniformly Optimal Strategy: Existence

Lemma 1 (Monotonicity).

A uniformly optimal strategy exists if and only if the -optimal attention vector weakly increases (in each coordinate) over time.

In words, a uniformly optimal strategy exists if and only if for every , the optimal allocation of units of attention devotes a (weakly) higher amount of attention to each source compared to the optimal allocation of units. Thus, monotonicity of and existence of a uniformly optimal strategy are equivalent.

Whether is monotone turns out to be closely related to a classic problem in consumer theory: Suppose a consumer has a utility function over consumption of units of each of goods, and let denote his Marshallian demand subject to the budget constraint . Then, the consumer’s demand is normal if each coordinate of increases with income . In our setting, we can set to be the negative of the posterior variance, so that minimizing is the same as maximizing . Our -optimal attention vector is then precisely the Marshallian demand, when prices are identically equal to and income is equal to . Thus, normality of the consumer’s demand under utility function is equivalent to existence of a uniformly optimal strategy.

A necessary and sufficient condition on for normality of demand is given in Alarie and Bronsard (1990) and Bilancini and Boncinelli (2010). When there are just two goods, demand is normal if and only if for . In our setting, this condition can be simplified to our Assumption 3, which as discussed is necessary and sufficient for a uniformly optimal strategy to exist when (although our proof of Theorem 1 is more direct, as it characterizes explicitly).

With many goods, this necessary and sufficient condition on is too complex to reduce to a statement on the primitives in our problem ( and ). However, a useful sufficient condition for normality of demand has been given by Chipman (1977) and more recently generalized by Quah (2007): If is concave and super-modular (also called “ALEP-complementary” to distinguish from Marshallian and Hicksian complementarity), then the consumer’s demand is normal. In our environment, is concave (see Lemma 3 in the appendix and the subsequent corollary). Super-modularity of requires the cross-partials of to be negative at every posterior belief, namely that the different sources are complements. Our Proposition 8 in Online Appendix O.3 shows that it is in fact possible to reduce supermodularity of to a condition on the prior belief only. This is our first sufficient condition in Assumption 5, “perpetual complementarity.”

Generalizing beyond this condition, we use the special form of to develop alternative sufficient conditions. Perhaps surprisingly, we show that if the sources are substitutes at every posterior belief (i.e., is sub-modular), then is also monotone. This “perpetual substitution” property, too, can be stated as a simple condition on the prior covariance matrix (our Assumption 4). Additionally, if correlation is not too strong—as implied by Assumption 6, which bounds the size of the covariances between the attributes relative to the size of their variances—then again we obtain monotonicity. In our proof of Theorem 2, we show that these three different economic conditions are each sufficient to imply the following technical property: At every moment of time, those attributes that covary most strongly with the payoff-relevant state all have positive covariance with (Lemma 8). As demonstrated in Lemma 9, this key technical property delivers the monotonicity of . Further exploration of our sufficient conditions, and whether they imply results for consumer demand theory beyond our specific setting, is an interesting topic for subsequent work.

4.4 Uniformly Optimal Strategy: Structure

When is indeed monotone in , the uniformly optimal strategy that achieves these vectors is simply the one that sets each attention allocation to be the time-derivative of . Under this strategy, the agent divides attention at every moment across those attributes that maximize the instantaneous marginal reduction of posterior variance . While the set of attributes is pinned down by first-order conditions, the precise mixture over those attributes is pinned down by second-order conditions, which ensure that this set of attributes continue to have equal and marginal values at future instants. Specifically, for each set of attributes, there is a unique linear combination that corresponds to the “learnable component” of given those attributes (formally, it is a projection of ). It turns out that at each stage, it is optimal to acquire information in a mixture proportional to the weights of this linear combination, thus producing an unbiased signal about the learnable component of . In the final stage, when the agent pays attention to every attribute—so that the learnable component of is itself—the optimal mixture is proportional to the payoff weights .

As beliefs about a set of attributes become more precise, their shared marginal value decreases continuously relative to the marginal value of learning about other attributes. Eventually the marginal value of learning about some other attribute “catches up” and joins the set of maximizers. This yields the nested-set property in Theorems 1 and 2.

5 Applications

The characterizations in Theorems 1 and 2 suggest that the study of dynamic information acquisition in our setting is quite tractable. We now apply this characterization to derive new results in a diverse set of applications.

In Section 5.1, we consider optimal attention allocation for choice between two goods and generalize recent results from Fudenberg et al. (2018). In Section 5.2 we develop a game between biased news sources, and characterize the degree of polarization and the quality of information in equilibrium. In Section 5.3, we consider the dynamic implications of a one-time attention manipulation, complementing a recent exercise in Gossner et al. (2020). The applications in Sections 5.1 and 5.3 show that we can use our main results to tractably introduce correlation in settings that have been previously studied under strong assumptions of independence. Our applications in Sections 5.1 and 5.2 show how our main results can be used as an intermediate step to derive results about other economic behaviors.

5.1 Application 1: Binary Choice

Building on a large literature regarding “binary choice” problems, Fudenberg et al. (2018) (henceforth FSS) recently proposed the uncertain drift-diffusion model: An agent has a choice between two goods with unknown payoffs and , and can learn about those payoffs before making a choice. The two payoffs are jointly normal and i.i.d.:

| (3) |

The agent observes two Brownian processes whose drifts are the unknown payoffs. He then chooses a stopping time to maximize the objective

where is a linear waiting cost.

FSS’s main economic insight is that earlier decision times are associated with more accurate decisions. Formally, let be the probability of choosing the higher-value good conditional on stopping at time . FSS’s Proposition 3 shows that is monotonically (weakly) decreasing over time. This comparative static is not obvious because two forces push in opposite directions: On the one hand, the agent has more information at later times, suggesting that later decisions may be more accurate. On the other hand, because the stopping time is endogenously chosen, the agent is more likely to stop earlier when the decision is easy (i.e., when one good’s value is much higher than the other). FSS’s result implies that this second force dominates.

FSS show moreover that this result is robust to endogenous attention allocation under a budget constraint. Specifically, suppose that at each moment of time, the agent has one unit of attention to allocate across learning either or . Then, FSS’s Theorem 5 shows that the agent optimally divides attention equally between learning about the two payoffs at every moment of time, similar to the exogenous process specified in their main model.

FSS’s model of endogenous attention and binary choice is nested within our framework. To map this setting back into our main model, define and . Then, since the payoff difference is a sufficient statistic for the agent’s decision, this problem corresponds to payoff-relevant state in our framework.

We now show that we can use our results to go beyond the case of independent and identically distributed payoffs (as imposed in the prior in (3)). Different from FSS, suppose that the agent’s prior over is normal with an arbitrary covariance matrix . Since the payoff weights are , our Theorem 1 applies and characterizes the agent’s optimal attention allocations over time given any . The following corollary is an immediate generalization of FSS’s Theorem 5:

Corollary 1.

Suppose . The agent’s optimal information acquisition strategy in this binary choice problem consists of two stages:

-

•

Stage 1: At all times

the agent optimally allocates all attention to .

-

•

Stage 2: At times , the agent optimally allocates equal attention to and .

Thus, when the agent is initially more uncertain about one of the two payoffs, he spends a period of time exclusively learning about that payoff. Starting at time , the agent divides attention equally across learning about the two goods, as in FSS’s i.i.d. case. From the closed-form expression for , it is straightforward to show that the length of the first stage is increasing in the asymmetry of initial uncertainty, and also increasing in the degree of correlation between the two payoffs.

We now use this characterization of optimal attention allocation to further generalize FSS’s main economic insight regarding the relationship between choice speed and accuracy.

Proposition 1.

For any , is weakly decreasing in . Thus, choice accuracy is weakly higher at earlier stopping times.

The logic of this result is as follows (see Online Appendix O.4 for detailed analysis). First, Corollary 1 implies that we can separate the problem of optimal stopping from the problem of optimal information acquisition. That is, we can take information as exogenously given by the process described in Corollary 1, and characterize properties of optimal stopping within this problem. In particular, Corollary 1 pins down the evolution of the agent’s posterior covariance matrix , which will be important for the subsequent arguments.

While is a deterministic process, the agent’s posterior expectation for the payoff difference evolves according to a random process . As in FSS, the symmetric stopping boundary at time is given by a function of the agent’s posterior covariance matrix ; that is, the agent optimally stops at time if and only if . Given these stopping boundaries, the choice accuracy conditional on stopping at time has the following simple form:

| (4) |

where is the agent’s posterior variance of at time , and is the normal c.d.f. function.

So it remains to understand how (4) evolves. There are two forces, which turn out to go in the same direction. First, uncertainty about the payoff difference decreases over time. As FSS already showed in the i.i.d. case, this effect weakly decreases the ratio . Roughly speaking, stopping at an earlier time when there is more residual uncertainty requires the agent to have received disproportionately stronger signals to forgo the option value. In our Lemma 16, we generalize this insight to arbitrary prior beliefs.

Second, our characterization in Corollary 1 reveals that the optimal attention strategy continuously reduces the asymmetry in uncertainty between the two attributes. We show in Lemma 15 that holding fixed uncertainty about the sum , asymmetry in uncertainty about the two attributes and allows the agent to learn faster; that is, the agent has lower posterior variance of at every future time compared to a symmetric prior.141414A simple informal argument is as follows. Given any prior, we can upper-bound the posterior variance under the optimal strategy by the posterior variance under a strategy that devotes equal attention to and at all times, which is equivalent to receiving the signals and over every unit of time. The information that those signals provide about the sum is at least as informative as the single signal , which is the sum of the previous two signals. Thus the agent learns about at least as fast as if he received the signal over every unit of time. When the prior is symmetric, then the equal-attention strategy considered above is optimal, and this lower bound on the speed of learning is tight. But when the prior is asymmetric, then the agent can improve upon this bound. This suggests that the agent can learn more quickly under an asymmetric prior than a symmetric one, holding fixed his prior uncertainty about . So asymmetric uncertainty increases the option value to waiting, and thus also the stopping boundary relative to the symmetric baseline. This effect, too, causes the ratio to decrease over time. Combining both effects yields the result that decreases over time.

5.2 Application 2: Biased News Sources

Next, we apply our results to study information provision in a setting with strategic information providers. Specifically, we are interested in how incentives for news bias interact with incentives for high-quality news provision.

To study this, we consider a stylized game in which a representative news reader seeks to learn a payoff-relevant unknown , for example the expected fiscal cost of a certain policy proposal. Two sources (a left-leaning and right-leaning news source) each report on , but bias their reporting in the direction helpful to their political party. We consider issues where the partisan implications are not precisely known by the general public (although they are understood by the sources)—for example, new limits on short selling in financial markets or trade deals with countries in Southeast Asia. We define to be the benefit to source 1’s party when the reader believes that is large (i.e., the cost of the policy is high). This benefit is a random variable from the perspective of the reader, and we assume it has distribution . The larger is, the less well understood the partisan implications of the issue are.

Source 1 biases its reporting of in the direction of , and source 2 biases away from it, but these sources can choose the intensity of their biases . The sources also choose the quality of their reporting, parametrized by , where a larger represents greater noise in the reporting. Specifically, we assume that a unit of time spent on source is informationally equivalent to a realization of

while a unit of time spent on source 2 is informationally equivalent to a realization of

Both choices and are fixed across time. For example, a source may develop a reputation for providing very biased information but having high-quality reporting.

We suppose that the reporters and editors at these news sources are subject to soft pressure to bias their reporting, and model the strength of those pressures by a payoff of for choice of bias intensity . The parameters and respectively determine the strength of incentives for bias, and the bliss point for bias intensity. We consider an interior bliss point to be realistic, since very biased sources lose credibility.

Sources are not explicitly incentivized to provide informative news, but will do so in equilibrium to attract attention from the news reader whose attention allocations we now describe. For any given choices of precisions and bias intensities, the reader’s optimal attention allocations can be derived from the characterization in Theorem 1. To apply this theorem, we can transform the current setting to our main model: Define and , so that a unit of time spent on each source produces an equally informative (standard normal) signal about . The payoff-relevant state can be rewritten as with payoff weights and . It can be checked that , so our Assumption 3 is satisfied and Theorem 1 holds.

The optimal path of attention allocations determines the discounted average attention paid to source , namely , where is a common discount rate for the sources.151515Note that in this formulation, we implicitly assume that the reader never stops information acquisition, which simplifies our subsequent analysis. However, can be interpreted as the limiting discounted average attention that source receives when the reader chooses an endogenous stopping time under vanishingly small information acquisition costs. Never stopping can also be justified in an extension of our main model where the agent faces multiple decisions across time (see Section 6). We use the discounted average attention as a reduced form for advertising revenue, where each news source receives a profit proportional to its viewership. Each source ’s total payoff is then the sum of discounted attention and the reward for bias intensity

The following proposition derives the equilibrium in this game between the two sources. For technical reasons, we require an assumption that the incentives for bias are not too weak.

Proposition 2.

Suppose .161616This assumption is imposed to guarantee the existence of a pure strategy equilibrium. Our analysis shows that is sufficient for existence, whereas a weaker condition is necessary. The unique pure strategy equilibrium is where

and

Given these equilibrium choices, the reader optimally devotes equal attention to the two sources at every moment.

The subsequent corollary regarding the informativeness of news in equilibrium follows immediately.171717It can be computed that when the sources choose and , the news reader’s posterior variance of the payoff-relevant state at time is . This confirms why is a sufficient statistic for equilibrium informativeness.

Corollary 2 (Informativeness of News).

The equilibrium noise level, ,

-

(a)

is increasing in the incentive for bias, , and the bias intensity bliss point, ;

-

(b)

is increasing in the prior uncertainty about partisan implications, ;

-

(c)

is decreasing in the discount rate, .

Part (a) says that incentives for greater bias not only increase polarization, which is expected, but also lead to a reduction in the quality of news. To understand this result, consider the incentives for source ’s choice of precision. Applying our characterization in Theorem 1, there are up to two stages of information acquisition: In Stage 1, if there is a strictly more informative source, then that source receives all viewership; in Stage 2, both sources receive a constant proportion of viewership. We show that, for any equal bias intensity choices , source ’s long-run share is , while source is chosen in Stage 1 if and only if its noise term is smaller (). Thus, sources face a trade-off between optimizing for greater long-run viewership—where a larger noise choice increases the long-run share—versus competing to be chosen in the short-run—which encourages smaller . Intuitively, more precise information improves the competitive value of a source at the beginning of time, but reduces the value of continual engagement with that source. In equilibrium, sources choose the same , thus washing out the first stage of information acquisition.

The size of this common noise level, however, depends on the incentives for bias. When sources provide biased news, the reader must attend to both sources to learn the truth. Polarized news sources thus live in symbiosis, where the extremity of bias on one side increases the value of information from the other. In the language of our paper, two sufficiently polarized news sources on opposite sides provide complementary information (while in contrast, two unbiased sources about provide fully substitutable information). The strength of complementarity increases monotonically with the degree of polarization.

Since the reader has stronger preferences for mixing over the two sources when they are complements, this means that the length of Stage 1 (when it exists) is decreasing in the degree of polarization. Thus, the more polarized the news sources are, the more emphasis these sources place on the long run, which in turn leads to lower quality news provision as we have discussed. This gives the conclusion in Part (a) of Corollary 2. In addition, larger prior uncertainty about implies higher value of de-biasing and thus also a shorter Stage 1, leading to Part (b).

Part (c) of Corollary 2 holds by very similar reasoning. Less patient news sources compete over short-run profits (i.e., being chosen in Stage 1), and thus prefer precise signals, while patient sources compete for long-run profits (i.e., long-run proportion), and thus prefer imprecise signals. So the less patient the sources are (larger ), the more precise their signals will be in equilibrium (smaller .

5.3 Application 3: Attention Manipulation

Our analyses have so far assumed that the agent has complete control over how to allocate his attention. In practice, businesses expend substantial effort to divert attention towards their products. Such “attention grabbing” often takes the form of a one-time intervention (e.g., an ad) rather than a continual shift in exposure, so the value of the attention diversion depends on how it shapes subsequent allocation of attention. Two questions thus naturally arise: 1) Does a one-time manipulation of attention towards a given source lead to a persistently higher amount of attention devoted to that source, or will the decision-maker quickly “compensate” for the manipulation? 2) What are the externalities on other sources—in particular, is it the case that manipulating attention towards one source decreases the amount of attention devoted to others?

Gossner et al. (2020) (henceforth GSS) recently studied this question in a model in which an agent sequentially learns about the quality of a number of goods by allocating attention to one good each period. One of their main results (Theorem 1) resolves the two questions posed above in the following way:

-

(1)

the cumulative amount of attention paid to that good remains persistently higher following the attention manipulation, and

-

(2)

the cumulative amount of attention paid to any other good remains persistently lower following the attention manipulation.

A key assumption in GSS is that the attention strategy used by the agent satisfies a version of Independence of Irrelevant Alternatives (IIA): Conditional on not focusing on the good to which attention is diverted, the agent’s belief about that good does not affect the relative probabilities of focusing on the remaining goods. Proposition 5 in Gossner et al. (2020) shows that when the agent adopts a class of “satisficing” stopping rules, the optimal attention strategy satisfies IIA for independent goods.181818This additional assumption on the stopping rule is not required in our setting, since we focus on the uniformly optimal attention strategy which is independent of stopping behavior.

We can use our framework and main characterization to study a related but different problem, where the agent learns about multiple attributes of an unknown (one-dimensional) payoff-relevant state, and—importantly—those attribute values can be correlated. Additionally, we differ from GSS by focusing on the optimal attention allocation strategy and how it is affected by attention manipulation. Outside of the special case of independent attributes, the optimal strategy in our setting fails IIA when there are more than two attributes. Nevertheless, we show GSS’s finding in (1) holds for flexible patterns of correlation, and the finding in (2) holds under an additional condition, which we make precise.

Formally, suppose attention is manipulated such that the agent only attends to source from time zero to time , where is fixed in this section. After time , the agent adopts the optimal attention strategy given his posterior belief at . The dynamic effect of the one-time attention manipulation is then understood by comparing the cumulative attention vectors under the optimal strategy and under the manipulated strategy. We assume throughout that our previous conditions on the prior covariance matrix apply (i.e., Assumption 3 if and Assumption 4, 5 or 6 if ).

Proposition 3.

Let be the earliest time at which cumulative attention towards source 1 exceeds under the baseline (unmanipulated optimal) strategy. Then, cumulative attention towards source 1 is strictly larger under the manipulated attention strategy at every moment of time , and equal to the baseline at all later times .

Thus, the finding in (1) holds under arbitrary correlation (so long as our characterizations apply): Attention manipulation towards source 1 has a persistent positive effect on the total amount of attention source 1 receives up to every future time. On the other hand, we show that this increase in cumulative attention vanishes in the long run, with the cumulative attention paid to source 1 under the baseline strategy “catching up” to the manipulated strategy by time .

The proof of this proposition is simple given our previous analysis. The cumulative attention vector under the optimal strategy is the -optimal vector defined as

| (5) |

where is the posterior variance function given by (2). On the other hand, the manipulated strategy induces the following constrained -optimal vector at any time :191919As discussed, the “absorbing property” of our sufficient conditions implies that our characterizations apply to the posterior belief at time after the agent has paid units of attention to source . Thus, the cumulative attention vector at time must minimize the posterior variance among feasible attention vectors following the manipulation. This leads to the constrained -optimal vector .

| (6) |

If , then the unconstrained -optimal vector satisfies the constraint in (6), so it coincides with the constrained -optimal vector . Moreover, as because our characterization says that source receives positive and constant attention at every instant in the final stage. Thus while initially source 1 must receive higher cumulative attention under the manipulated strategy, eventually the cumulative attention devoted to source 1 must be the same under the baseline and manipulated strategies. To show that is this switch point, note that implies (by definition of and monotonicity of ), in which case . And if , we have , so the manipulated amount of attention devoted to source 1 strictly exceeds that of the baseline strategy. This yields the result.

When there are only two attributes, Proposition 3 also delivers GSS’s second finding, namely that diversion of attention towards learning about one attribute weakly reduces cumulative attention towards learning about the remaining attribute at every moment of time. With more than two attributes, however, correlation between the attributes can overturn this result.

Example 4.

Suppose there are 3 attributes, the payoff-relevant state is , and the prior covariance matrix is

Since is diagonally-dominant, Theorem 2 applies.

Without attention manipulation, the optimal strategy devotes the first units of attention towards . At , the three sources have exactly equal marginal values (and equal payoff weights), so equal attention is optimal afterwards. Thus for and for .

Now suppose instead that the agent is forced to attend to source 1 for unit of time. Then after the first units of attention devoted towards , the agent optimally still begins by learning about . This lasts until , at which time source has the same marginal value as source . The second stage then involves learning about and using the constant attention ratio . The third stage begins at , after which equal attention across the three sources is optimal. It can be checked that the manipulation of attention towards source 1 weakly increases the cumulative attention towards source 2 at all times, and strictly so during the period .

Intuitively, in this example sources 1 and 2 provide complementary information (since ). Manipulating attention towards source 1 thus increases the marginal value of source 2, and the agent begins observing source 2 earlier than he would have otherwise. In contrast, we might expect that when all sources are substitutes with one another, attention manipulation to source 1 must decrease the amount of attention devoted to every other source. The challenge is understanding what the appropriate notion of “substitutes” is. This turns out to be the property given earlier in Assumption 4, which guarantees that each pair of attributes has a positive partial correlation coefficient.

Proposition 4.

Suppose all pairs of sources are substitutes (i.e., Assumption 4 is satisfied). Then cumulative attention towards every source is weakly smaller under the manipulated strategy than under the baseline strategy, at every moment of time.

This result complements GSS by demonstrating a class of correlated attributes for which manipulation of attention towards one reduces cumulative attention towards all others. Together with our previous Proposition 3, it shows that GSS’s Attention Theorem extends beyond their IIA assumption. Since our environment and GSS’s are non-nested, these results collectively point to the possibility of a more general set of sufficient conditions, which we leave to future work.

6 Discussion

Information acquisition is a classic problem within economics, but there are relatively few dynamic models that are simultaneously rich and tractable. In this paper we present a class of dynamic information acquisition problems whose solution can be explicitly characterized in closed-form. We show that a complete analysis is feasible if we assume: (1) Gaussian uncertainty, (2) a one-dimensional payoff-relevant state, and (3) correlation across the unknowns that satisfies certain assumptions (for example if correlation is not too strong). Given these restrictions, a great deal of generality can be accommodated in other aspects of the problem, such as the payoff function. The tractability of the solution and the flexibility of the environment open the door to interesting applications, a number of which we have illustrated here.

We conclude by briefly mentioning a few other potential extensions and variations.

Discrete Time. Although our main model is in continuous time, our results have direct analogues in a related discrete-time model. Specifically, for the model previously described in Remark 1, we have the following result: Suppose any of Assumption 4, 5, or 6 holds. Then at each period , the optimal allocation of precision is where for each , with being the optimal attention allocation for the continuous-time model as described in Theorem 2.202020In a companion piece, Liang et al. (2017), we discretize not only time but also information acquisitions: At each period , the agent has to choose one of standard normal signals, without the ability to allocate fractional precisions. The necessity of integer approximation complicates the characterization of the full sequence of signal choices. In that paper we instead provide conditions under which myopic acquisition is (eventually) optimal.

Exogenous Stopping. Although we have assumed that the agent endogenously chooses when to stop acquiring information, our results hold without modification if instead the end date arrives according to an arbitrary exogenous distribution. Additionally, in that alternative model, the optimal path of attention allocations is uniquely characterized by our results so long as the exogenous distribution of end date has full support.

Intertemporal Decision Problems. Our main model assumes that the agent takes only one action, which simplifies the exposition. But since our analysis based on the notion of uniform optimality is independent of details of the payoff function, it can be easily generalized to a setting where the agent takes actions at times . Our characterization of the optimal attention strategy extends for any (intertemporal) payoff function that is decreasing in the decision times .

Appendix A Preliminaries

A.1 Posterior Variance Function

Given units of attention devoted to learning about each attribute , the posterior variance of can be written in two ways:

Lemma 2.

It holds that

where is the diagonal matrix with entries .

This function extends to a rational function (quotient of polynomials) over all of , i.e., even if some are negative.

Proof.

The equality is well-known. To see that is a rational function, simply note that can be written as the adjugate matrix of divided by its determinant. Thus each entry of the posterior covariance matrix is a rational function in . ∎

Below we calculate the first and second derivatives of the posterior variance function :

Lemma 3.

Given a cumulative attention vector , define

which is a vector in . Then the first and second derivatives of are given by

Proof.

From Lemma 2 and the formula for matrix derivatives, we have

where is the -th coordinate vector in , and is the matrix with “1” in the -th entry and “0” elsewhere. For the second derivative, we compute that

as we desire to show. The last equality follows by writing , and using as well as . ∎

Corollary 3.

is decreasing and convex in whenever .

Proof.

By Lemma 3, the partial derivatives of are non-positive, so is decreasing. Additionally, its Hessian matrix is

which is positive semi-definite whenever . So is convex. ∎

We use these properties to show that for each , the -optimal vector is unique:

Lemma 4.

For each , there is a unique -optimal vector .

Proof.

Suppose for contradiction that two vectors and both minimize the posterior variance at time . Relabeling the sources if necessary, we can assume is positive for , negative for and zero for . Since , the cutoff indices satisfy .

For , consider the vector which lies on the line segment between and . Then by assumption we have . Since is convex, equality must hold. This means is a constant for . But is a rational function in , so its value remains the same constant even for or . In particular, consider the limit as . Then the -th coordinate of approaches for , approaches for and equals for .

For each , let us also consider the vector which takes the absolute value of each coordinate in . Note that as , has the same limit as . Thus by the second expression for (see Lemma 2), . For large , the first coordinates of are strictly larger than the corresponding coordinates of , and the remaining coordinates coincide. So the fact that is decreasing and implies for .

Consider the vector . By Lemma 3, for . Thus . Since and thus is not the zero vector, there exists s.t. . It follows that . But then the posterior variance would be reduced if we slightly decreased the first coordinate of (which is strictly positive since ) and increased the -th coordinate by the same amount. This contradicts the assumption that is a -optimal vector. Hence the lemma holds. ∎

A.2 Optimality and Uniform Optimality

The following result ensures that a strategy that minimizes the posterior variance uniformly at all times is an optimal strategy in any decision problem.

Lemma 5.

Suppose the payoff function satisfies Assumption 2, then a uniformly optimal attention strategy is dynamically optimal.

Proof.

Without loss of generality we may assume the prior mean of is zero; otherwise shift by a constant and modify the utility function accordingly. Let be the uniformly optimal attention strategy, and be the induced filtration. Given , the optimal stopping rule is a solution to

Note that the stochastic process of posterior means is a continuous martingale adapted to the filtration , with . Moreover, since information is Gaussian, the quadratic variation is simply , where is the posterior variance of at time under the strategy , and is the prior variance. By definition of uniform optimality, for each the random variable is deterministic and moreover smallest among possible posterior variances at time .

Thus, by the Dambis–Dubins–Schwartz Theorem (see Theorem 1.7 in Chapter V of Revuz and Yor (1999)), there exists a Brownian motion such that

This allows us to change variable from the time to the cumulative precision .

To formulate the resulting optimization problem, for each we denote by the time such that ; is a deterministic and increasing function of . Then, under the attention strategy , the agent’s optimal payoff can be rewritten as

| (7) |

In other words, instead of optimizing over stopping times adapted to , we can think of the agent choosing an optimal adapted to the Brownian motion .

We will show this payoff is greater than the optimal payoff under any other attention strategy . To do this, let be the induced filtration under . Similar to the above, we consider the stochastic process , adapted to . Applying the Dambis-Dubins-Schwartz Theorem again, there exists a Brownian motion such that

Here is the posterior variance under strategy , which is in general random but always satisfies . Note also that may not be the same process as .

Observe that for any we have . Thus the agent’s payoff under strategy is bounded above by

where we used Assumption 2. Now we can change variable again from to , and rewrite the payoff as

| (8) |

This is the same as the RHS of (7), since and are both Brownian motions. Hence the payoff under does not exceed the payoff under , completing the proof. ∎

We also have a simple converse result:

Lemma 6.

Fixing and . Suppose an information acquisition strategy is optimal for all payoff functions that satisfy Assumption 2, then it is uniformly optimal.

Proof.

Take an arbitrary time and consider the payoff function with , where for and very large for . Then the agent’s optimal stopping rule is to stop exactly at time . Since his information acquisition strategy is optimal for this payoff function, the induced cumulative attention vector must achieve -optimality. Varying yields the result. ∎

A.3 Sufficient Condition for Assumption 6

Lemma 7.

Suppose the prior covariance matrix satisfies for all . Then its inverse matrix satisfies for all , and is thus diagonally-dominant.

Proof.

By symmetry, we can focus on . Let for , and without loss assume has the greatest absolute value among . It suffices to show

From we have . Thus because . Rearranging yields

where the last inequality uses and for . The above inequality simplifies to

And since , we conclude that as desired. Note that is necessarily positive, thus . ∎

Appendix B Proof of Theorem 1

Define as in the statement of Theorem 1, and define to ease notation.

Given a cumulative attention vector , let be a shorthand for the diagonal matrix . Then by direct computation, we have

By Lemma 3, this implies the marginal values of the two sources are given by:

| (9) |

Note that Assumption 3 translates into . Under this assumption, we will characterize the -optimal vector and show it is increasing over time. Without loss assume , then is non-negative. Let . Then when we always have

since and . We also have

since and by assumption . Thus, (9) implies that at such attention vectors . So for any budget of attention , putting all attention to source minimizes the posterior variance . That is, for .

For , observe that (9) implies as well as . Thus the -optimal vector is interior (i.e., and are both strictly positive). The first-order condition , together with (9) and the budget constraint , yields the solution

Hence is indeed increasing in . The instantaneous attention allocations are the time-derivatives of , and they are easily seen to be described by Theorem 1. In particular, the long-run attention allocation to source is , which simplifies to . This completes the proof.

Appendix C Proof of Theorem 2

We will first prove the result under Assumption 6. The proof is similar under the alternative Assumption 4 or 5, and is presented at the end.

Given Lemma 5, it is sufficient to show that the -optimal vector is weakly increasing in , that its time-derivative is locally constant, and that the time-derivative has an expanding support set (as described in the theorem). The proof is divided into several sections below.

C.1 Technical Property of

We will use the following lemma regarding the marginal values of different sources:

Lemma 8.