Learning Sample-Specific Models with

Low-Rank Personalized Regression

Abstract

Modern applications of machine learning (ML) deal with increasingly heterogeneous datasets comprised of data collected from overlapping latent subpopulations. As a result, traditional models trained over large datasets may fail to recognize highly predictive localized effects in favour of weakly predictive global patterns. This is a problem because localized effects are critical to developing individualized policies and treatment plans in applications ranging from precision medicine to advertising. To address this challenge, we propose to estimate sample-specific models that tailor inference and prediction at the individual level. In contrast to classical ML models that estimate a single, complex model (or only a few complex models), our approach produces a model personalized to each sample. These sample-specific models can be studied to understand subgroup dynamics that go beyond coarse-grained class labels. Crucially, our approach does not assume that relationships between samples (e.g. a similarity network) are known a priori. Instead, we use unmodeled covariates to learn a latent distance metric over the samples. We apply this approach to financial, biomedical, and electoral data as well as simulated data and show that sample-specific models provide fine-grained interpretations of complicated phenomena without sacrificing predictive accuracy compared to state-of-the-art models such as deep neural networks.

1 Introduction

The scale of modern datasets allows an unprecedented opportunity to infer individual-level effects by borrowing power across large cohorts; however, principled statistical methods for accomplishing this goal are lacking. Standard approaches for adapting to heterogeneity in complex data include random effects models, mixture models, varying coefficients, and hierarchical models. Recent work includes the network lasso [11], the pliable lasso [32], personalized multi-task learning [37], and the localized lasso [38]. Despite this long history, these methods either fail to estimate individual-level (i.e. sample-specific) effects, or require prior knowledge regarding the relation between samples (e.g. a network). At the same time, as datasets continue to increase in size and complexity, the possibility of inferring sample-specific phenomena by exploiting patterns in these large datasets has driven interest in important scientific problems such as precision medicine [5, 24]. The relevance and potential impact of sample-specific inference has also been widely acknowledged in applications including psychology [9], education [12], and finance [1].

In this paper, we explore a solution to this dilemma through the framework of “personalized” models. Personalized modeling seeks to estimate a large collection of simple models in which each model is tailored—or “personalized”—to a single sample. This is in contrast to models that seek to estimate a single, complex model. To make this more precise, suppose we have samples , where denotes the response and are predictors. A traditional ML model would model the relationship between and with a single function parametrized by a complex parameter (e.g. a deep neural network). In a personalized model, we model each sample with its own function, allowing to be simple while varying with each sample. Thus, the model becomes . These models are estimated jointly with a single objective function, enabling statistical power to be shared between sub-populations.

The flexibility of using different parameter values for different samples enables us to use a simple model class (e.g. logistic regression) to produce models which are simultaneously interpretable and predictive for each individual sample. By treating each sample separately, it is also possible to capture heterogeneous effects within similar subgroups (an example of this will be discussed in Section 3.5). Finally, the parameters learned through our framework accurately capture underlying effect sizes, giving users confidence that sample-specific interpretations correspond to real phenomena (Fig 1). Whereas previous work on personalized models either seeks only the population’s distribution of parameters [34] or requires prior knowledge of the sample relationships [37, 38, 11], we develop a novel framework which estimates sample-specific parameters by adaptively learning relationships from the data. A Python implementation is available at http://www.github.com/blengerich/personalized_regression.

Motivating Example.

Consider the problem of understanding election outcomes at the local level. For example, given data on a particular candidate’s views and policy proposals, we wish to predict the probability that a particular locality (e.g. county, township, district, etc.) will vote for this candidate. In this example we focus on counties for concreteness. More importantly, in addition to making accurate predictions, we are interested in understanding and explaining how different counties react to different platforms. The latter information—in addition to simple predictive measures—is especially important to candidates and political consultants seeking advantages in major elections such as a presidential election. This information is also important to social and political scientists seeking to understand the characteristics of an electorate and how it is evolving. An application of this motivating example using personalized regression can be found in in Section 3.6.

One approach would be to build individual models for each county, using historical data from previous elections. Immediately we encounter several practical challenges: 1) By building independent models for each county, we fail to share information between related counties, resulting in a loss of statistical power, 2) Since elections are relatively infrequent, the amount of data on each county is limited, resulting in a further loss of power, and 3) To ensure that the models are able to explain the preferences of an electorate, we will be forced to use simple models (e.g. logistic regression or decision trees), which will likely have limited predictive power compared to more complex models. This simultaneous loss of power and predictive accuracy is characteristic of modeling large, heterogeneous datasets arising from aggregating multiple subpopulations. Crucially, in this example the total number of samples may be quite large (e.g. there are more than 3,000 US counties and there have been 58 US presidential elections), but the number of samples per subpopulaton is small. Furthermore, these challenges are in no way unique to this example: similar problems arise for examples in financial, biological, and marketing applications.

One way to alleviate these challenges is to model the th county using a regression model , where the are parameters that vary with each sample and are trained jointly using all of the data. This idea of personalized modeling allows us to train accurate models using only a single sample from each county—this is useful in settings where collecting more data may be expensive (e.g. biology and medicine) or impossible (e.g. elections and marketing). By allowing the parameter to be sample-specific, there is no longer any need for to be complex, and simple linear and logistic regression models will suffice, providing useful and interpretable models for each sample.

Alternative approaches and related work.

One natural approach to adapt to heterogeneity is to use mixture models, e.g. a mixture of regression [27] or mixture of experts model [10]. While mixture models present an intriguing way to increase power and borrow strength across the entire cohort, they are notoriously difficult to train and are best at capturing coarse-grained heterogeneity in data. Importantly, mixture models do not capture individual, sample-specific effects and thus cannot model heterogeneity within subgroups.

Furthermore, previous approaches to personalized inference [20, 37, 38, 11] assume that there is a known network or similarity matrix that encodes how samples in a cohort are related to each other. A crucial distinction between our approach and these approaches is that no such knowledge is assumed. Recent work has also focused on estimating sample-specific parameters for structured models [35, 14, 16, 20, 18]; in these cases, prior knowledge of the graph structure enables efficient testing of sample-specific deviations.

More classical approaches include varying-coefficient (VC) models [13, 30, 8], where the parameter is allowed to depend on additional covariates in some smooth way, and random effects models [15], where is modeled as a random variable. More recently, the spirit of the VC model has been adapted to use deep neural networks as encoders for complex covariates like images [2, 3] or domain adaptation [29, 26]. In contrast to our approach, which does not impose any regularity or structural assumptions on the model, these approaches typically require strong smoothness (in the case of VC) or distributional (in the case of random effects) assumptions.

Finally, locally-linear models estimated by recent work in model explanations [28] can be interpreted as sample-specific models. We make explicit comparisons to this approach in our experiments (Section 3), but we point out here that local explanations serve to interpret a black-box model—which may be incorrect—and not the true mechanisms underlying the data. This is clearly illustrated in Fig 1(c), where local linear approximations do a good job of explaining the behaviour of the underlying neural network, but nonetheless fail to capture the true regression coefficients. This tradeoff between inference and prediction is well-established in the literature.

2 Learning sample-specific models

For clarity, we describe the main idea using a linear model for each personalized model; extension to arbitrary generalized linear models including logistic regression is straightforward. In Section 3, we include experiments using both linear and logistic regression. A traditional linear model would dictate , where the are noise and the parameter is shared across different samples. We relax this model by allowing to vary with each sample, i.e.

| (1) |

Clearly, without additional constraints, this model is overparametrized—there is a -dimensional subspace of solutions to the equation in for each . Thus, the key is to choose a solution that simultaneously leads to good generalization and accurate inferences about the th sample. We propose two strategies for this: (a) a low-rank latent representation of the parameters and (b) a novel regularization scheme.

2.1 Low-rank representation

We constrain the matrix of personalized parameters to be low-rank, i.e. for some loadings and some dictionary . Letting denote the matrix of loadings, we have a low-rank representation of . The choice of is determined by the user’s desired latent dimensionality; for , using only instead of the of a full-rank solution can greatly improve computational and statistical efficiency. In addition, the low-rank formulation enables us to use distance in in Eq. (4) to restrict Euclidean distances between the : After normalizing the columns of , we have

| (2) |

This illustrates that closeness in the loadings implies closeness in parameters . This fact will be exploited to regularize (Section 2.2).

This use of a dictionary is common in multi-task learning [23] based on the assumption that tasks inherently use shared atomic representations. Here, we make the analogous assumption that samples arise from combinations of shared processes, so sample-specific models based on a shared dictionary efficiently characterize sample heterogeneity. Sparsity in can be realized by sparsity in ; for instance, effect sizes which are consistently zero across all samples can be created by zero vectors in the columns of . The low-rank formulation also implicitly constrains the number of personalized sparsity patterns; this can be adjusted by changing the latent dimensionality .

2.2 Distance-matching

Existing approaches [20, 37, 38, 11] assume that there is a known weighted network over samples such that . In other words, we have prior knowledge of which parameters should be similar. We avoid this strong assumption by instead assuming that we have additional covariates for which there exists some way to measure similarity that corresponds to similarity in the parameter space, however, we don’t have advance knowledge of this. More specifically, we regularize the parameters by requiring that similarity in corresponds to similarity in , i.e. , where is an unknown, latent metric on the covariates . In applications, the represent exogenous variables that we do not wish to directly model; for example, in our motivating example of an electoral analysis, this may include demographic information about the localities.

To promote similar structures in parameters as in covariates, we adapt a distance-matching regularization (DMR) scheme [17] to penalize the squared difference in implied distances. The covariate distances are modeled as a weighted sum:

| (3) |

where each () is a metric for a covariate. The positive vector represents a linear transformation of these “simple” distances into more useful latent distance functions. By using a linear parametrization for , we can interpret the learned effects by inspecting the weights assigned to each covariate.

By Eq. (2), in order for , it suffices to require . With this in mind, define the following distance-matching regularizer:

| (4) |

where . This regularizer promotes imitating the structure of covariate values in the regression parameters. By using instead of in the regularizer, calculation of distances is much more efficient when .

2.3 Personalized Regression

Let be a loss function, e.g. least-squares or logistic loss. For each sample of the training data, define a regularized, sample-specific loss by

| (5) |

where is a regularizer such as the penalty and is the distance-matching regularizer defined in Eq. (4). We learn and by minimizing the following composite objective:

| (6) |

where the second term regularizes the distance function with strength set by , and we recall that . The hyperparameter trades off sensitivity to prediction of the response variable against sensitivity to covariate structure.

Optimization.

We minimize the composite objective with subgradient descent combined with a specific initialization and learning rate schedule. An outline of the algorithm can be found in Alg. 1 below. In detail, we initialize by setting for a population model such as the Lasso or elastic net and then initialize and by factorizing with PCA. is a very small value used only to enable factorization by the PCA algorithm. Each personalized estimator is endowed with a personalized learning rate , which scales the global learning rate according to how far the estimator has traveled. In addition to working well in practice, this scheme guarantees that the center of mass of the personalized regression coefficients does not deviate too far from the intialization , even though the coefficients remain unconstrained. This property is discussed in more detail in Section 2.4.

Prediction.

Given a test point , we form a sample-specific model by averaging the model parameters of the nearest training points, according to the learned distance metric :

| (7a) | |||

where orders the indices in descending order of covariate distance. Increasing drives the test models toward the population model to control overfitting. In our experiments, we use .

We have intentionally avoided using to select so that interpretation of is not confounded by . In some cases, however, the sample predictors can provide additional insight to sample distances (e.g. [36]); we leave it to future work to examine how to augment estimations of sample distances by including distances between predictors.

Scalability.

Naïvely, the distance-matching regularizer has pairwise distances to calculate, however this calculation can be made efficient as follows. First, the terms involving remain unchanged during optimization, so that their computation can be amortized. This allows the use of feature-wise distance metrics which are computationally intensive (e.g. the output of a deep learning model for image covariates). Furthermore, these values are never optimized, so the distance metrics need not be differentiable. This allows for a wide variety of distance metrics, such as the discrete metric for unordered categorical covariates. Second, we streamline the calculation of nearest neighbors in two ways: 1) Storing in a spatial data structure and 2) Shrinking the hyperparameter used in (4). With these performance improvements, we are able to fit models to datasets with over 10,000 samples and 1000s of predictors on a Macbook Pro with 16GB RAM in under an hour.

2.4 Analysis

Initializing sample-specific models around a population estimate is convenient because the sample-specific estimates do not diverge from the population estimate unless they have strong reason to do so. Here, we analyze linear regression minimized by squared loss (e.g., ), though the properties extend to any predictive loss function with a Lipschitz-continuous subgradient.

Theorem 1.

Let us consider personalized linear regression with (i.e. regularization). Let be normalized such that , . Define , where is the current value of after iterations. Let the learning rate follow a multiplicative decay such that , where is the initial learning rate and is a constant decay factor. Then at iteration ,

| (8) |

That is, the center of mass of the personalized regression coefficients does not deviate too far from the initialization , even though the coefficients remain unconstrained. In addition, the distance-matching regularizer does not move the center of mass and the update to the center of mass does not grow with the number of samples. Proofs of these claims are included in Appendix A.

3 Experiments

We compare personalized regression (hereafter, PR) to four baselines: 1) Population linear or logistic regression, 2) A mixture regression (MR) model, 3) Varying coefficients (VC), 4) Deep neural networks (DNN). First, we evaluate each method’s ability to recover the true parameters from simulated data. Then we present three real data case studies, each progressively more challenging than the previous: 1) Stock prediction using financial data, 2) Cancer diagnosis from mass spectrometry data, and 3) Electoral prediction using historical election data. The results are summarized in Table 3 for easy reference.

We believe the out-of-sample prediction results provide strong evidence that any harmful overfitting of PR is outweighed by the benefit of personalized estimation. This agrees with famous results such as [31], where it is showed that optimal ensembles of linear models consist of overfitted atoms; see especially Eq. 12 and Fig. 2 therein.

3.1 Baselines

For each experiment, we use several baseline models to benchmark performance:

-

•

Population model. First, we use elastic net regularization [39] as a generalizable population estimator.

-

•

Mixture of regressions. To estimate a small collection of models, we use a standard mixture model optimized by expectation-maximization. Since this model does not share information between mixture components, the number of components must be much smaller than the number of samples.

-

•

Varying coefficient model. To estimate sample-specific models, we use an -regularized linear varying-coefficients model [13].

-

•

Deep neural network. Finally, to compare against models with large representational capacity, we include a neural network. This neural network contains 5 hidden layers, with layer sizes and nonlinearities treated as hyperparameters optimized for cross-validation loss by grid search. The final version contains 250 hidden nodes in each layer with sigmoid nonlinearities.

For the tasks with continuous outcomes, these are linear regression models; for classification tasks, these are logistic regression models.

3.2 Choice of hyperparameters

While the personalized regression approach estimates a large number of parameters, there are relatively few hyperparameters. Hyperparameters to be selected are: the strength of the traditional regression regularizer, the strength of the distance-matching regularizer, the diameter of the neighborhoods considered by the distance-matching regularizer, the strength of regularizer on , and the latent dimensionality. should be set equivalent to the used in the population estimator. requires some tuning and should be set such that the distance-matching regularizer contributes the a same order of magnitude on the total loss as does the predictive loss. should be set to reflect the user’s desired neighborhood of personalization; larger produces personalized estimates which reflect covariate distances even for very different samples, smaller improves computation speed but decreases the size of the neighborhoods of personalization. Finally, regularizes and should be set to reflect the user’s prior knowledge about the influence of each covariate on personalization.

For our experiments, we use the following hyperparameter values with PR:

-

•

Simulation. , , ,

-

•

Finance. , , ,

-

•

Cancer. , , ,

-

•

Election. , , ,

For all experiments, we dynamically set such that each point has on average 10 neighbors, and use the learning rate schedule of , . For each baseline described in Section 3.1, hyperparameter values were selected by cross-validation.

| Model | MSE | |||

|---|---|---|---|---|

| 2 | Pop. | 9.97 | 0.87 | 0.13 |

| MR | 9.86 | 0.88 | 0.12 | |

| VC | 14.55 | 0.76 | 0.22 | |

| DNN | 30.42 | 0.75 | 0.24 | |

| PR | 7.82 | 0.89 | 0.09 | |

| 10 | Pop. | 15.19 | 0.79 | 0.73 |

| MR | 14.81 | 0.80 | 0.70 | |

| VC | 23.86 | 0.69 | 1.09 | |

| DNN | 67.49 | 0.80 | 0.85 | |

| PR | 14.52 | 0.82 | 0.65 | |

| 25 | Pop. | 25.86 | 0.85 | 1.26 |

| MR | 25.75 | 0.86 | 1.20 | |

| VC | 38.77 | 0.66 | 3.05 | |

| DNN | 103.72 | 0.68 | 2.78 | |

| PR | 24.53 | 0.87 | 1.10 |

| Model | MSE | |||

|---|---|---|---|---|

| 100 | Pop. | 6.36 | 0.90 | 0.23 |

| MR | 6.48 | 0.90 | 0.23 | |

| VC | 10.75 | 0.78 | 0.50 | |

| DNN | 22.30 | 0.39 | 0.75 | |

| PR | 6.03 | 0.91 | 0.21 | |

| 500 | Pop. | 11.83 | 0.84 | 0.29 |

| MR | 11.78 | 0.84 | 0.30 | |

| VC | 19.06 | 0.74 | 0.49 | |

| DNN | 47.33 | 0.81 | 0.37 | |

| PR | 10.30 | 0.86 | 0.26 | |

| 2500 | Pop. | 33.03 | 0.87 | 0.26 |

| MR | 31.75 | 0.88 | 0.26 | |

| VC | 33.71 | 0.87 | 0.27 | |

| DNN | 102.88 | 0.88 | 0.29 | |

| PR | 26.11 | 0.90 | 0.21 |

3.3 Simulation Study

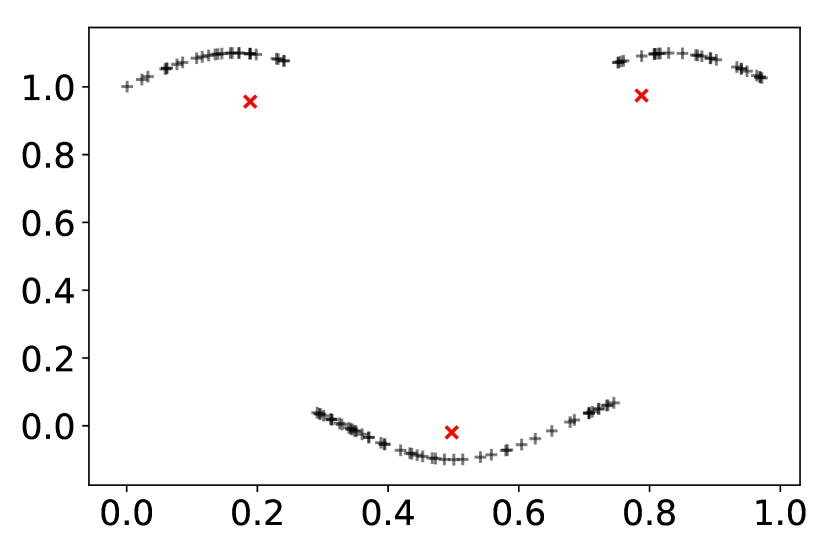

We first investigate the capacity of personalized regression to recover true effect sizes in simulation studies. For these experiments, we generate data according to , , , , , , . These experiments all use covariates. As shown in Fig. 1, this produces regression parameters with a discontinuous distribution.

The algorithms are given both and as input during training, and we use LIME [28] to generate local linear approximations to the DNN in order to estimate parameters for each sample. In this setting, there exists a discontinuous function which could output exactly the sample-specific regression models from the covariates. In this sense, the neural network is “correctly specified” for this dataset, testing how well locally-linear models approximate the true parameters. To estimate personalized models for the simulated dataset, we initialize the personalized estimations with a varying-coefficient model, and personalize according to the distance metric .

Results.

In Table 2, we report results for varying and in Table 2, we report results for varying . The values reported are: (1) the recovery error of the true regression parameters in the training set, with (mean std) values calculated over 20 experiments with different values of , (2) correlation coefficient of predictions on the test set, and (3) mean squared error of predictions on the test set.

As expected, the recovery error is much lower for PR, while the DNN shows competitive predictive error. The population estimator successfully recovers the mean effect sizes, but this central model is not accurate for any individual, resulting in poor performance both in recovering and in prediction. Similarly, both MR and VC perform poorly. As expected, the deep learning model excels at predictive error, however, the local linear approximations do not accurately recover the sample-specific linear models. In contrast, PR exhibits both the flexibility and the structure to learn the true regression parameters while retaining predictive performance.

3.4 Financial Prediction

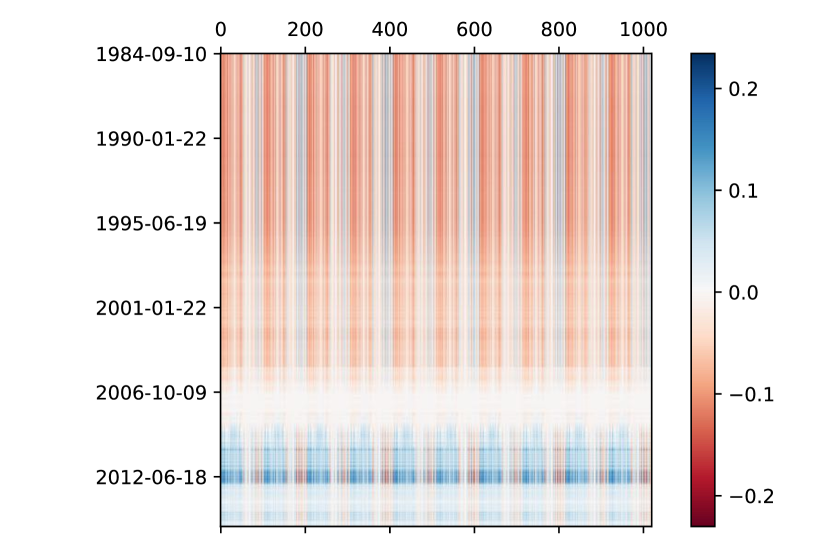

A common task in financial trading is to predict the price of a security at some point in the future. This is a challenging task made more difficult by nonstationarity—the interpretation of an event changes over time, and different securities may respond to the same event differently.

Data.

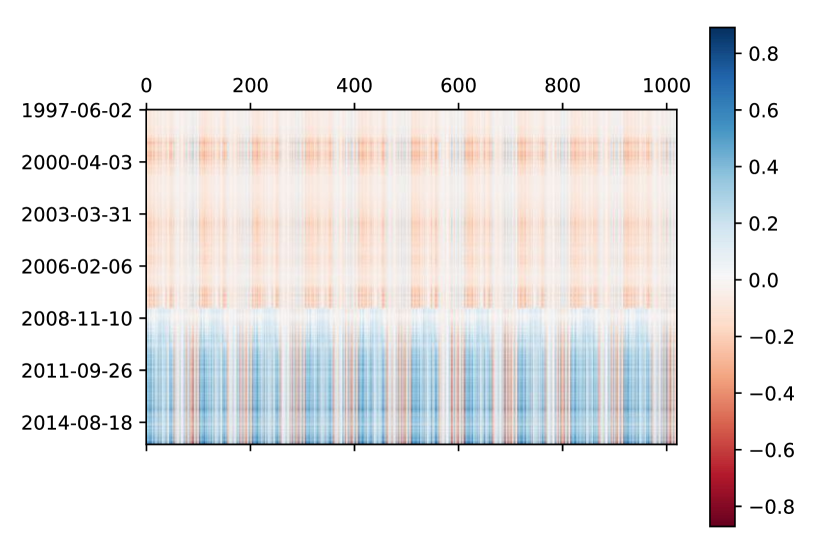

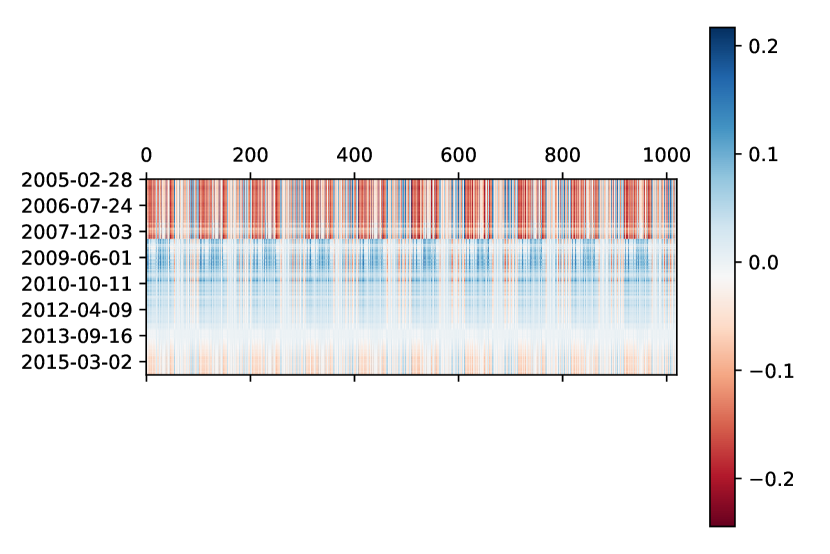

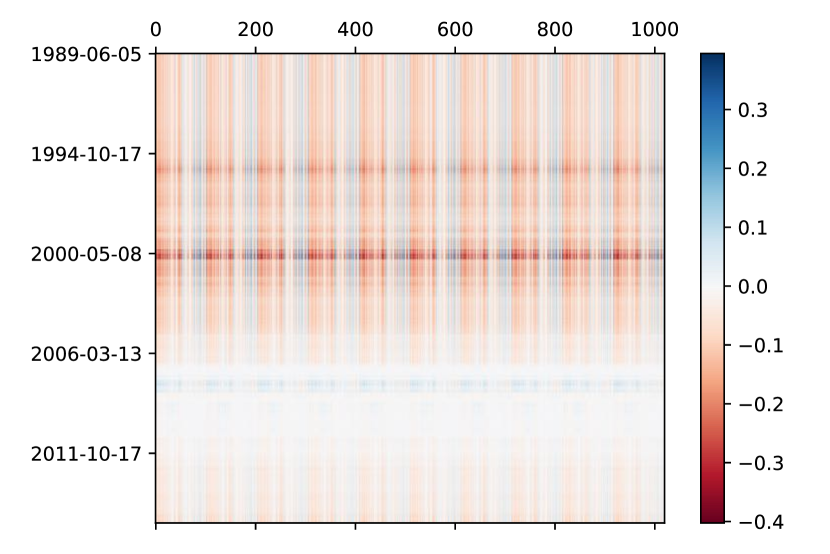

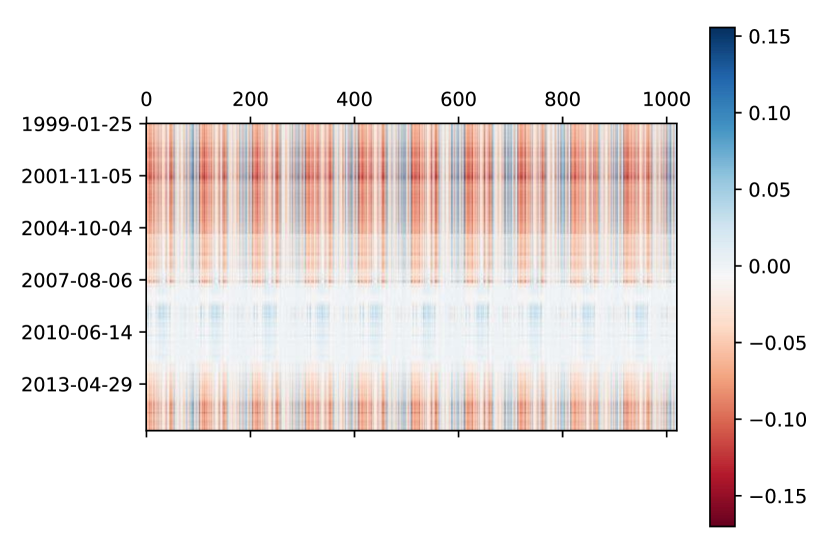

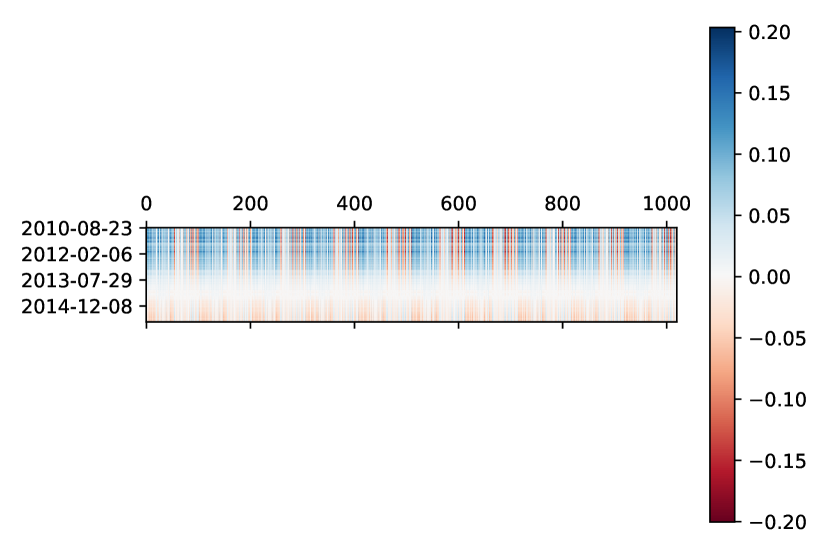

We built a dataset of security prices over a 30-year time frame by joining stock and ETF trading histories222https://www.kaggle.com/borismarjanovic/price-volume-data-for-all-us-stocks-etfs/version/3 to a database of global news headlines from Bloomberg [6] and Reddit333https://www.kaggle.com/aaron7sun/stocknews. We transform news headlines into continuous representations by tf-idf weighting averaging [4] of word embeddings under the GLoVE model [25] pre-trained on Wikipedia and Gigaword corpora444https://nlp.stanford.edu/projects/glove. After dimensionality reduction, this news dataset consists of a 50-dimensional vector for each date. The predictors consist of the trading history of the 24 securities over the previous 2 weeks as well as global news headlines from the same time period. The covariates consist of the date and security characteristics (name, region, and industry). The target is the price of this security 2 weeks after . We split the dataset into training and test sets at the 80th percentile date, which is approximately the beginning of 2011. To estimate personalized models for the financial dataset, we initialize the personalized estimators with the population model and personalize according to the distance for time and the discrete metric for the other covariates.

| Model | Financial | Cancer | Election | |||

|---|---|---|---|---|---|---|

| MSE | AUROC | Acc | MSE | |||

| Pop. | ||||||

| MR | ||||||

| VC | ||||||

| DNN | ||||||

| PR | ||||||

Results.

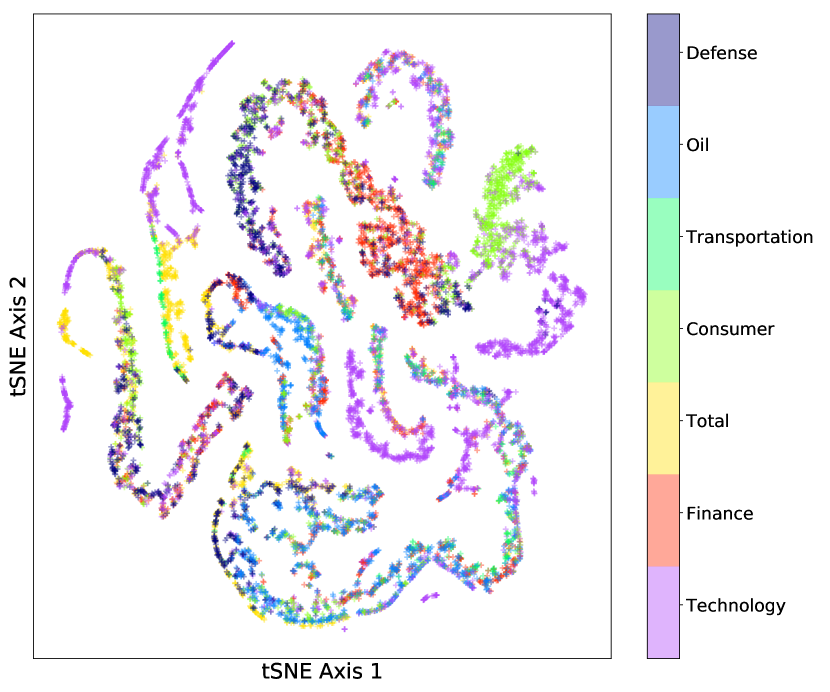

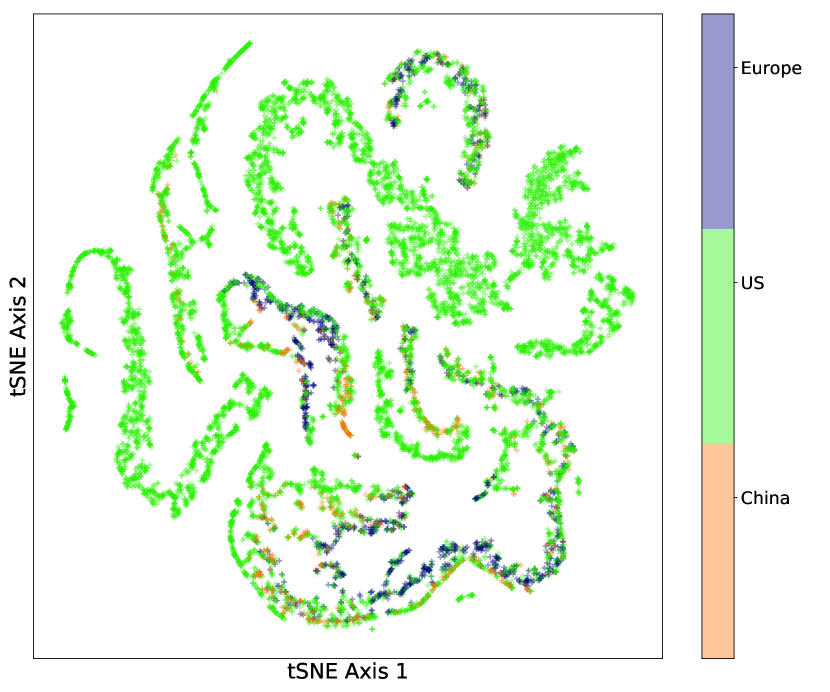

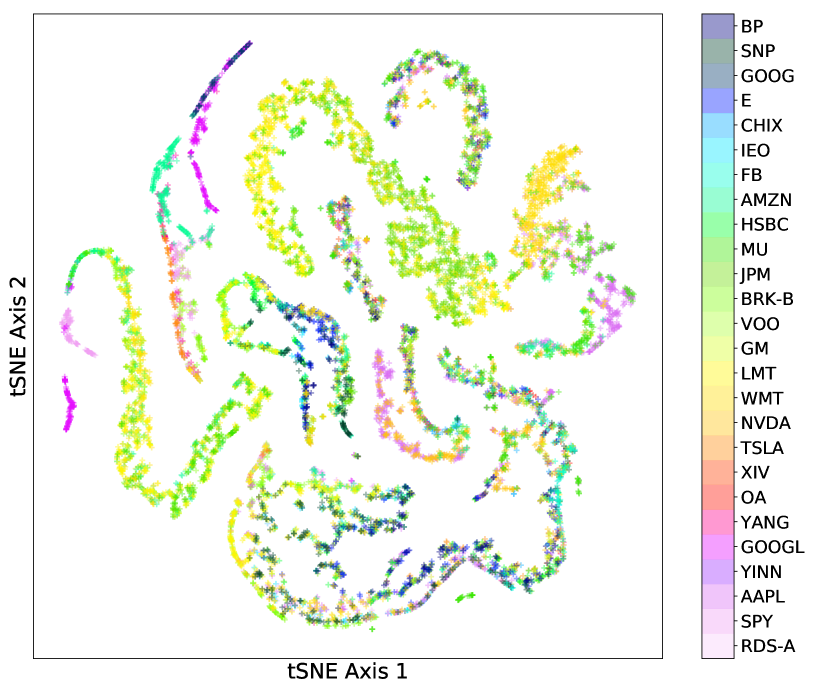

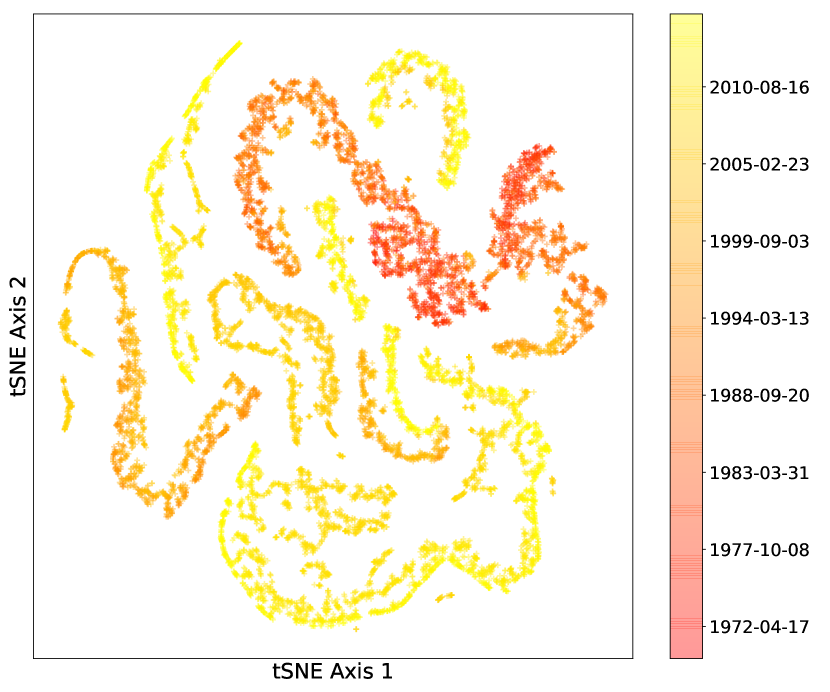

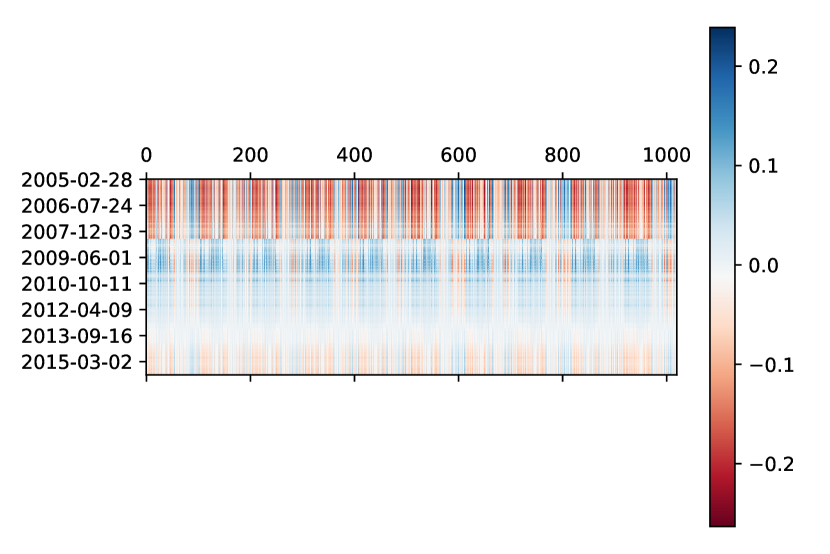

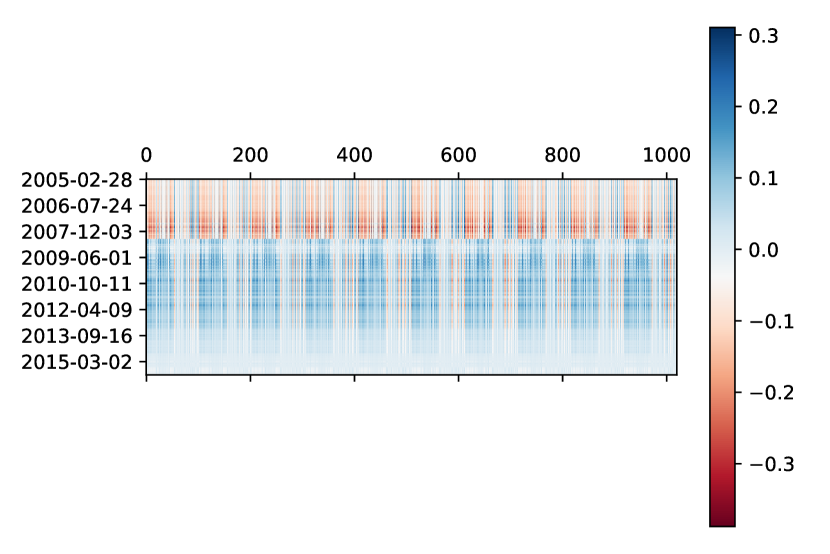

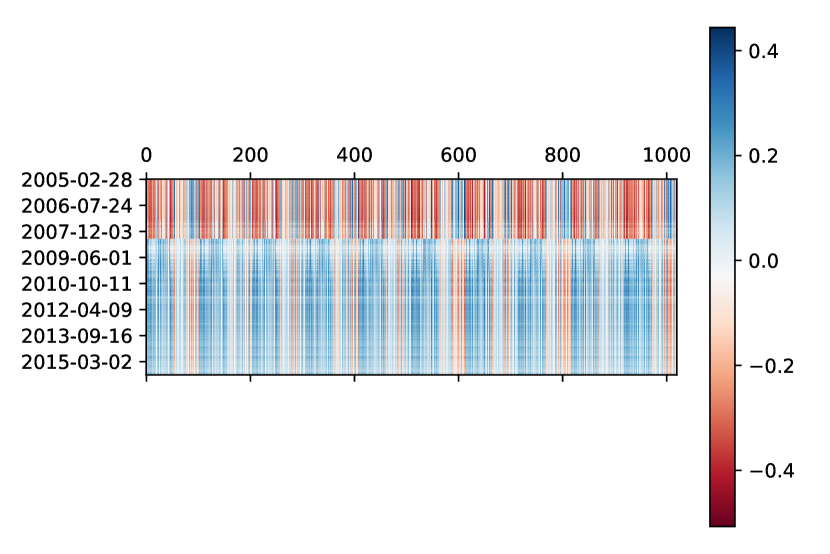

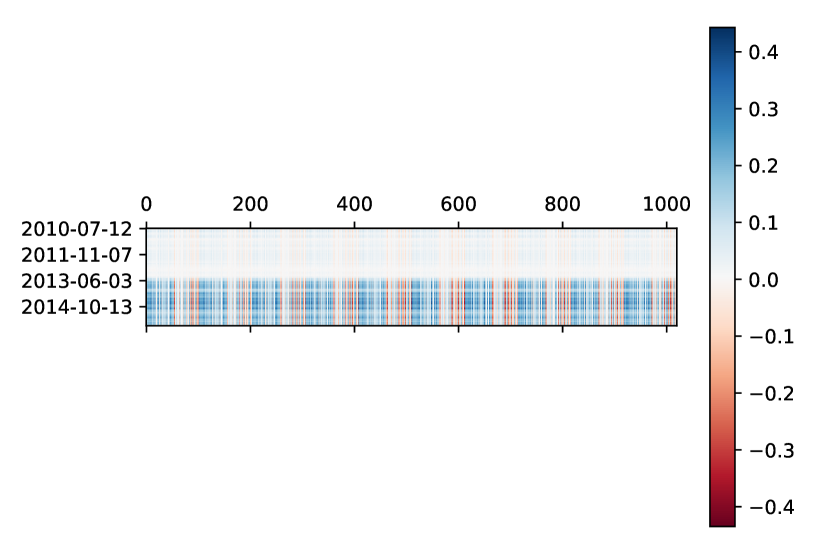

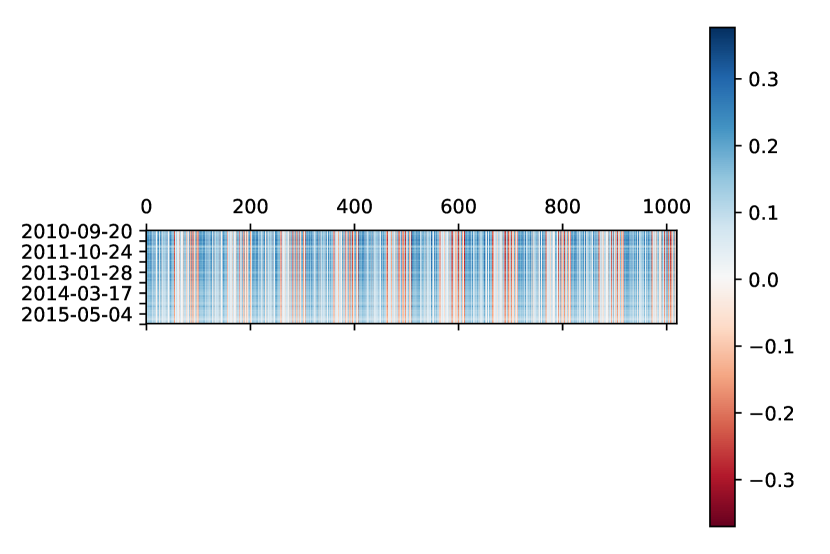

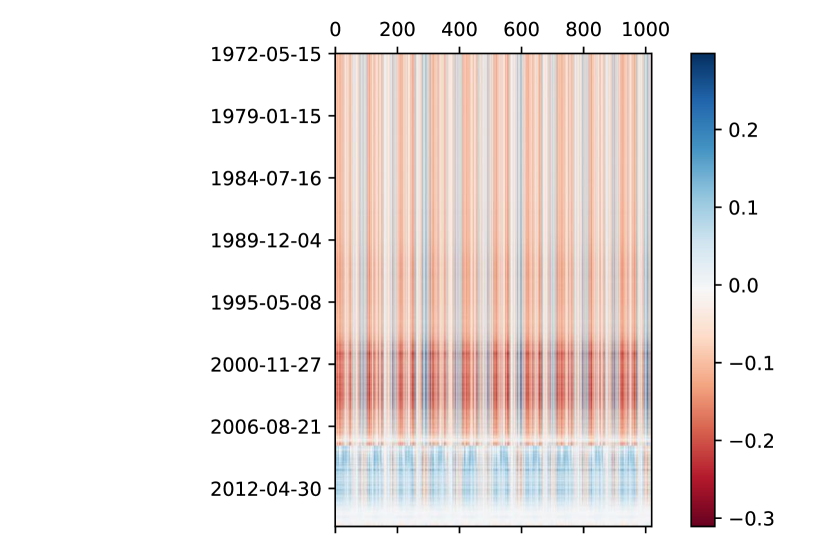

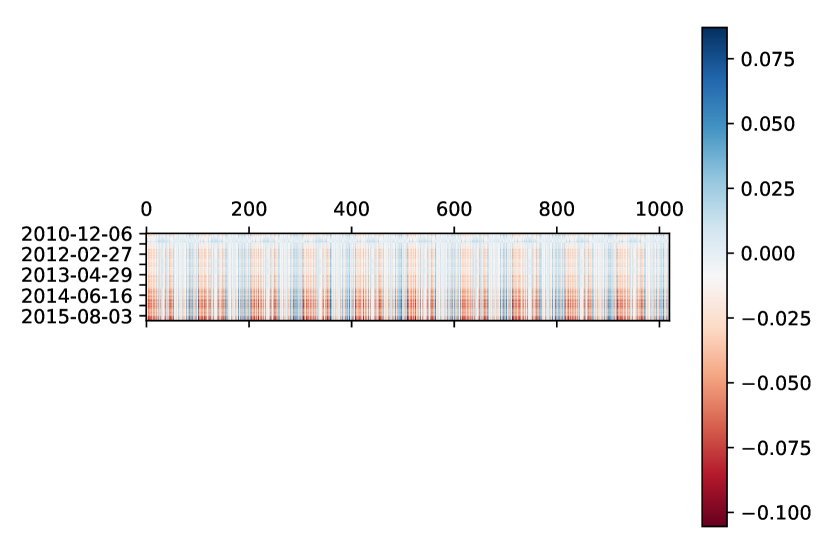

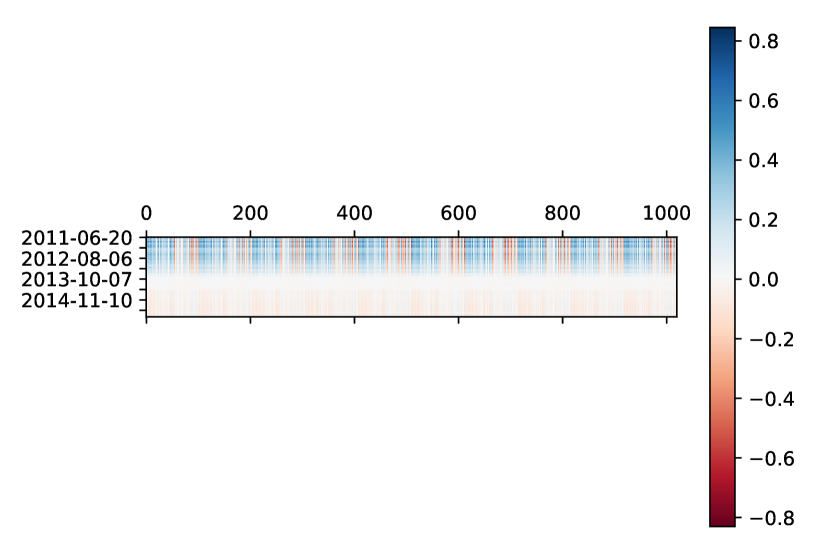

PR significantly outperforms baseline methods to predict price movements (Table 3). In contrast to standard models which average effects over long time periods and/or securities, PR summarizes gradual shifts in attention. Shown in Fig. 2 are visualizations of the model parameters, colored by each of the covariates used for personalization. The strongest clustering behavior is due to time (Fig. 2(d)). For instance, models fit to samples in the era of U.S. “stagflation" (1973-1975) are overlaid on models for samples in the early 1990s U.S. recession. In both of these cases, real equity prices declined against the background of high inflation rates. In contrast, the recessions marked by structural problems such as the Great Financial Crisis of 2008 are separated from the others. Within each time period, we also see that industries (Fig. 2(a)), regions (Fig. 2(b)), and securities (Fig. 2(c)) are strongly clustered.

3.5 Cancer Analysis

In cancer analysis, the challenges of sample heterogeneity are paramount and well-known. Increasing biomedical evidence suggests that patients do not fall into discrete clusters [21, 5], but rather each patient experiences a unique disease that should be approached from an individualized perspective [7]. Here, we investigate the capacity of PR to distinguish malignant from benign skin lesions using a dataset of desorption electrospray ionization mass spectrometry imaging (DESI-MSI) of a common skin cancer, basal cell carcinoma (BCC).

Data.

This dataset, from [22], contains 17,053 total samples from 17 patients. Each sample consists of 2,734 spectra intensities and is labeled with a binary outcome (0=benign, 1=malignant). Data from 9 patients are used to fit models, while data from 8 patients are held-out for evaluation. In this dataset, the only explicit covariate is the patient label. To produce covariates which are most useful for personalization, we augment the patient labels with 1500 of the predictive features compressed to 2 dimensions by t-SNE dimensionality reduction. These 1500 predictive features are excluded from the set of predictors for PR, while baseline methods use the entire set of features as predictors. We fit the personalized regression according to the distance function , , , where the first function checks if the patients are the same and the final two calculate distance in the continuous covariates.

Results.

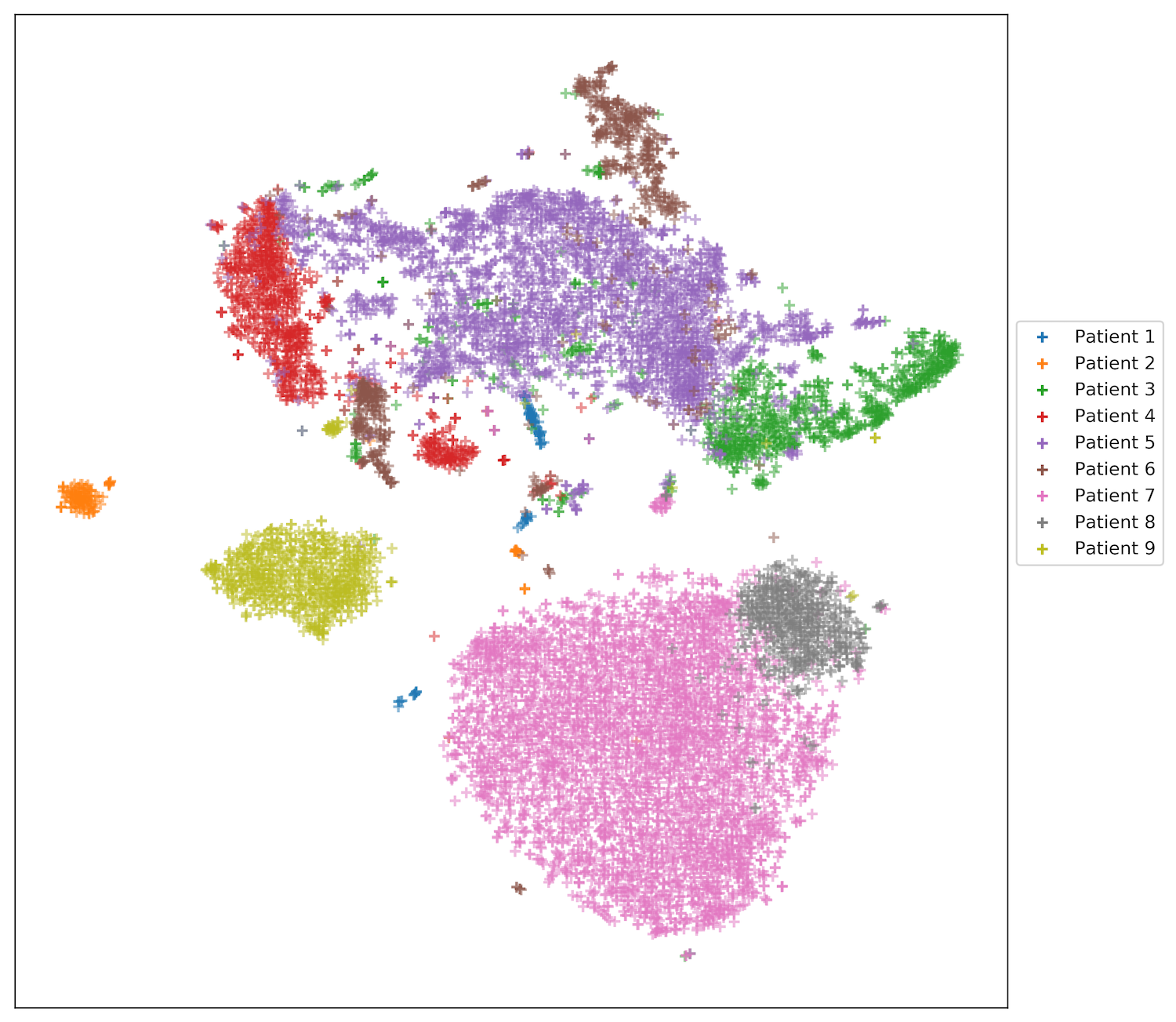

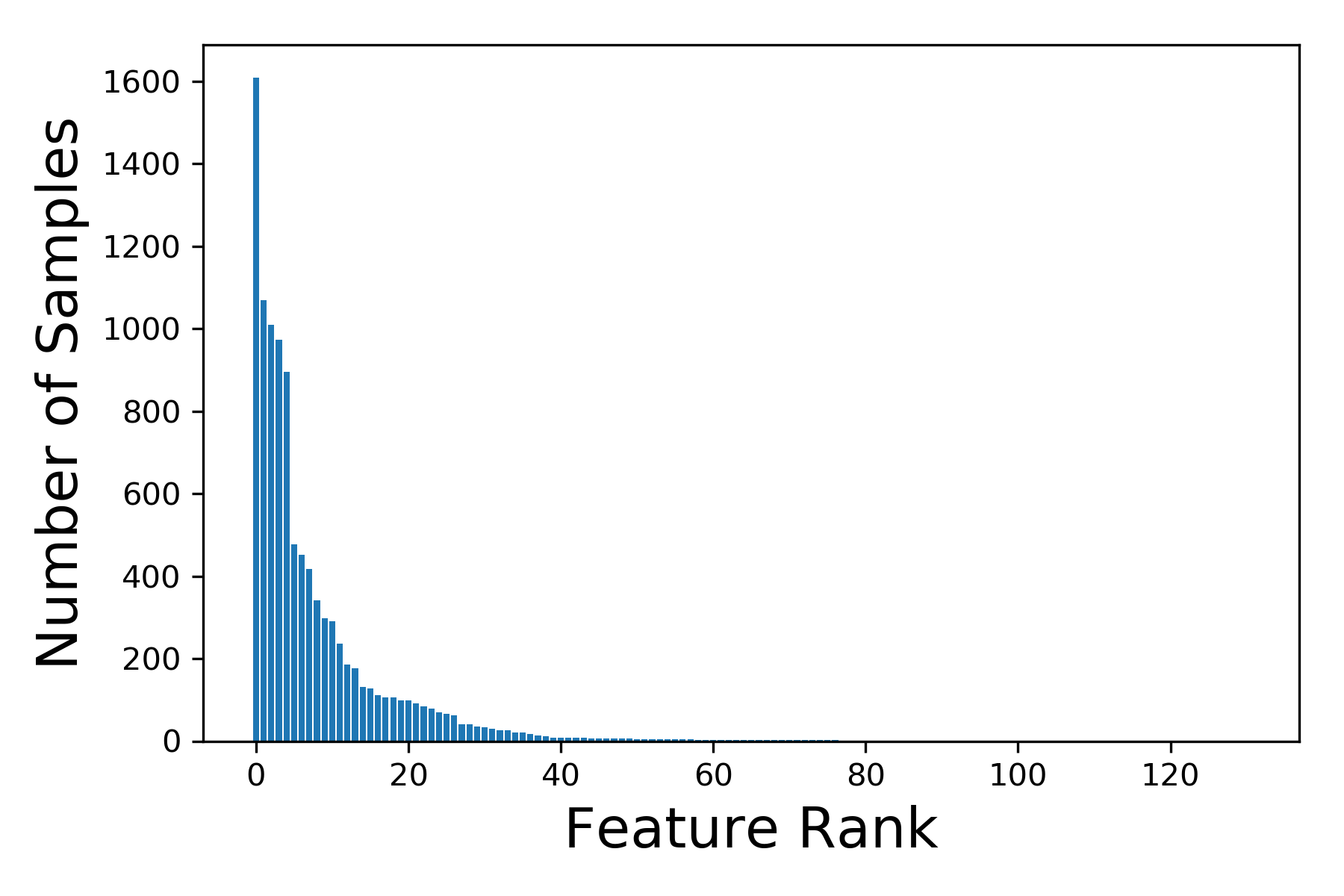

As shown in Table 3, PR produces the best predictions of tumor status amongst the methods evaluated. The substantial improvement over competing methods is likely due to the long tail of the distribution of characteristic features—we observe that the number of samples which assign the largest influence to each feature has a long tail (Fig. 3(b)). By summing the most important features for each instance, we can transform these sample-specific explanations into patient-specific explanations (Table S4). These explanations depict a clustering of patients in which there are 8 distinct subtypes (visualized in Fig. 3(a)). While we may hope that a mixture model could recover these patient clusters, actual mixture components are less accurate in prediction (Table 3), likely due to their independent estimation and reduced statistical power. Furthermore, this clustering by patient is incomplete—there is also significant heterogeneity in the models for each patient (Fig. 3(a)). This may point to the “mosaic" view of tumors, under which single tumors are comprised of multiple cell lines [19]. This example underscores the benefits of treating sample heterogeneity as fundamental by designing algorithms to estimate sample-specific models.

3.6 Presidential Election Analysis

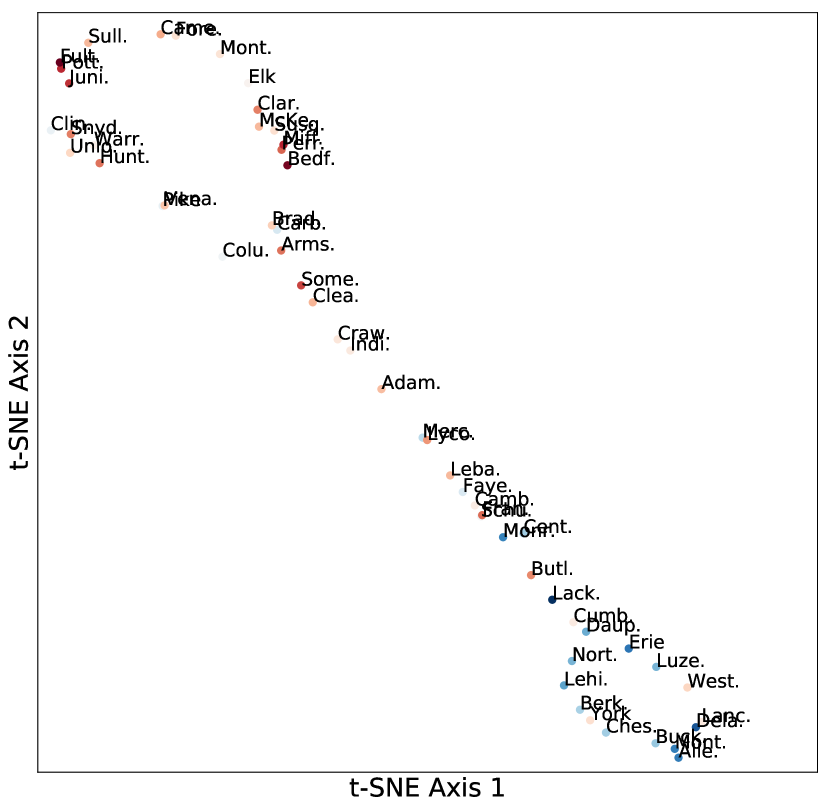

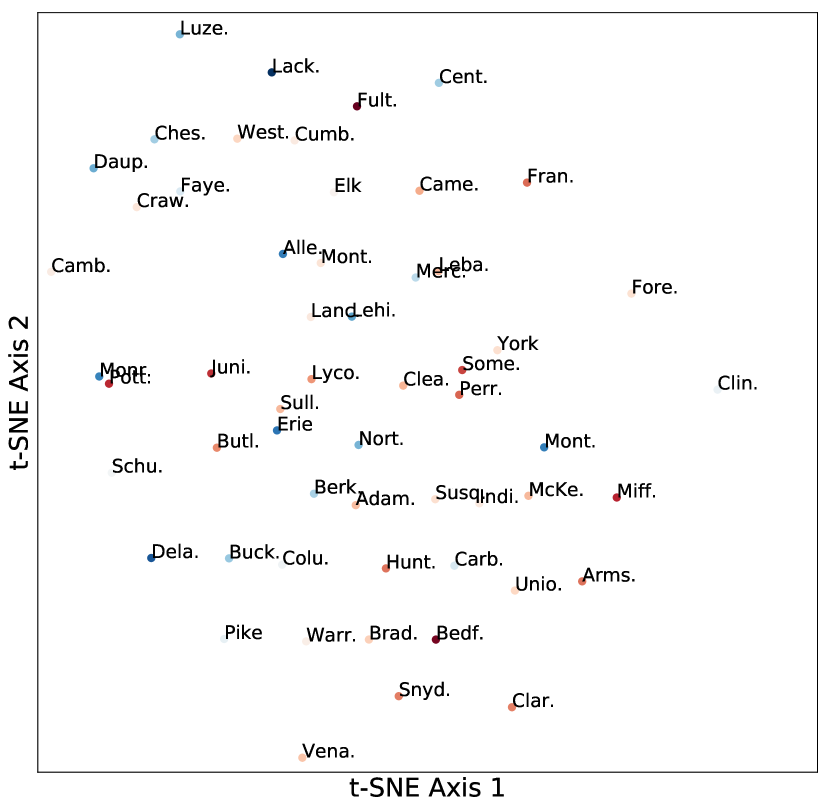

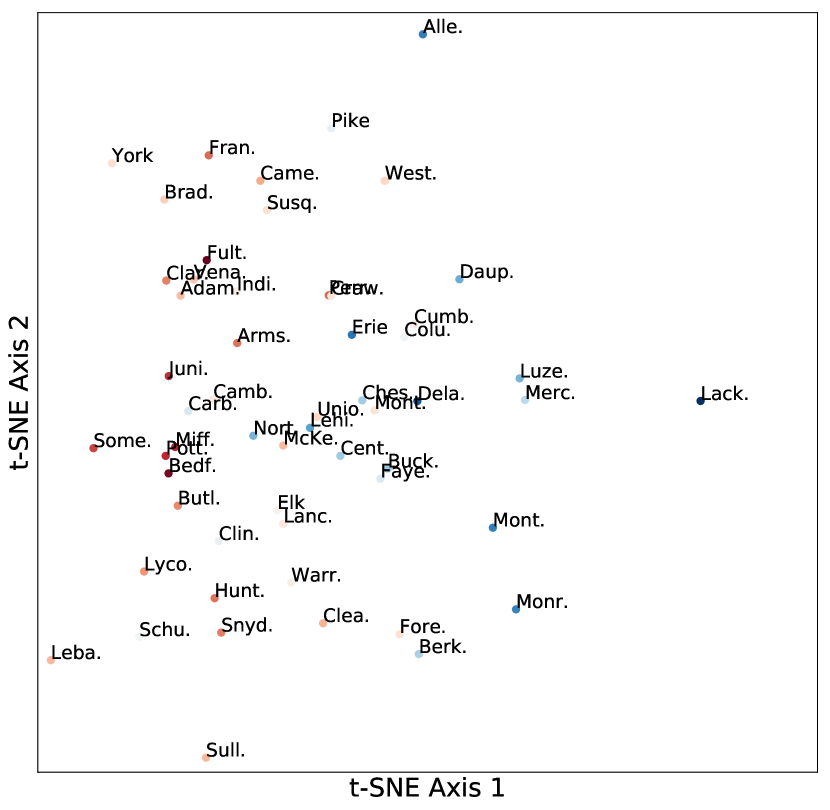

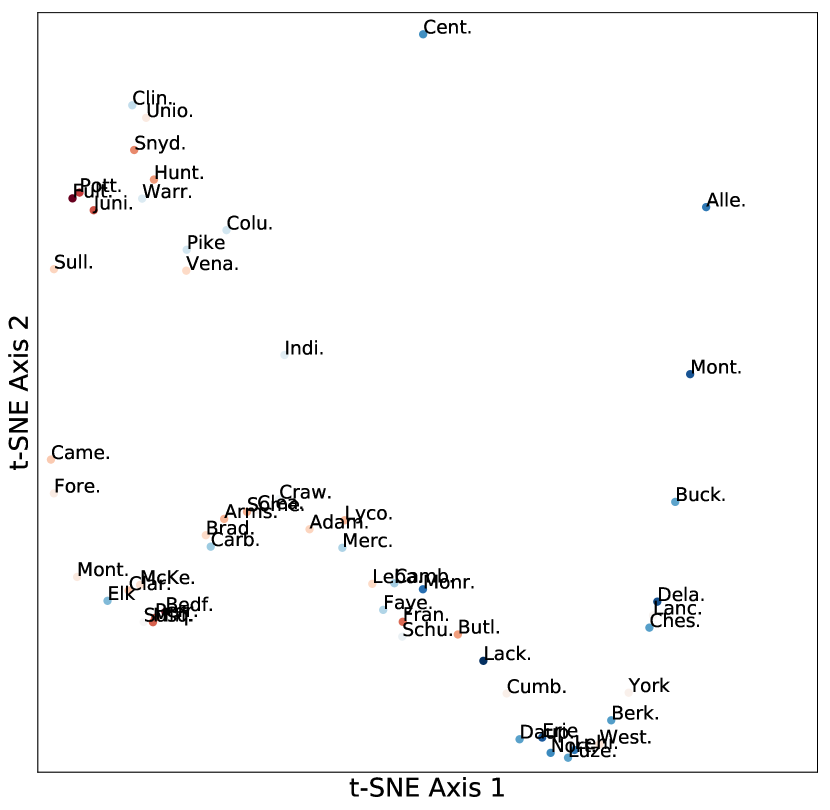

Our last experiment illustrates a practical use case for the example of modeling election outcomes discussed in Section 1. The goals are twofold: 1) To predict county-level election results, and 2) To explore the use of distinct regression models as embeddings of samples in order to better understand voting preferences at the county (i.e. sample-specific) level.

Data.

The election predictors are taken from the 2012 U.S. presidential election and consists of discrete representations of each candidate based on candidate positions compiled by ProCon.555https://2012election.procon.org/view.source-summary-chart.php Outcomes are the county-level vote proportions in the 2012 U.S. presidential election.666https://dataverse.harvard.edu/dataset.xhtml?persistentId=hdl:1902.1/21919 For the covariates , we used county demographic information from the 2010 U.S. Census.777https://www.census.gov/data/datasets/2016/demo/popest/counties-detail.html As the outcome varies across samples but the predictors remain constant, the personalized regression models must encode sample heterogeneity by estimating different regression parameters for different samples, thus creating county representations (“embeddings") which combine both voting and demographic data.

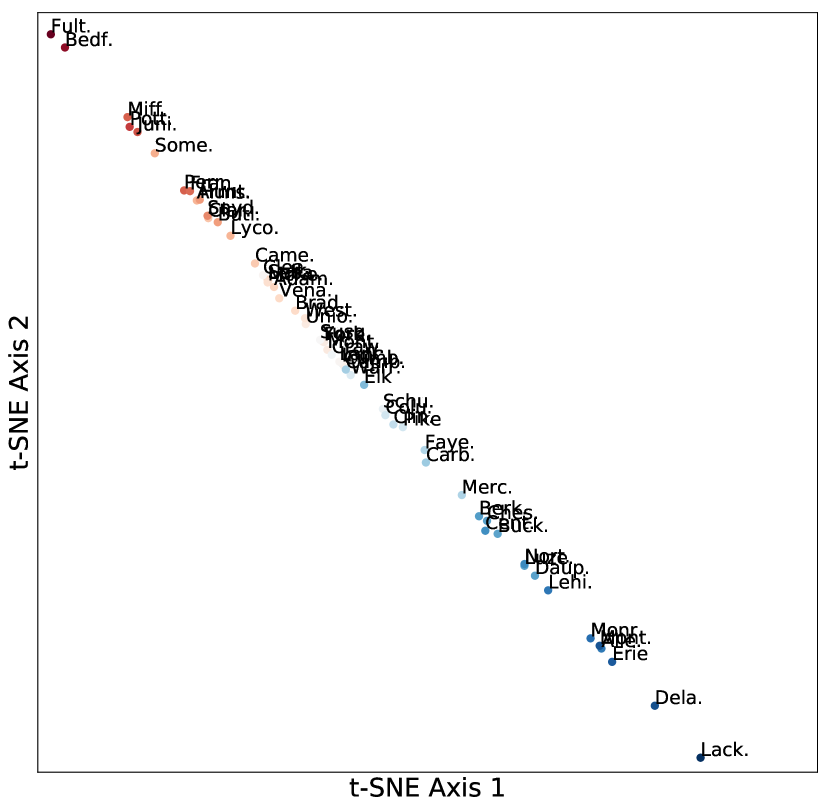

Results.

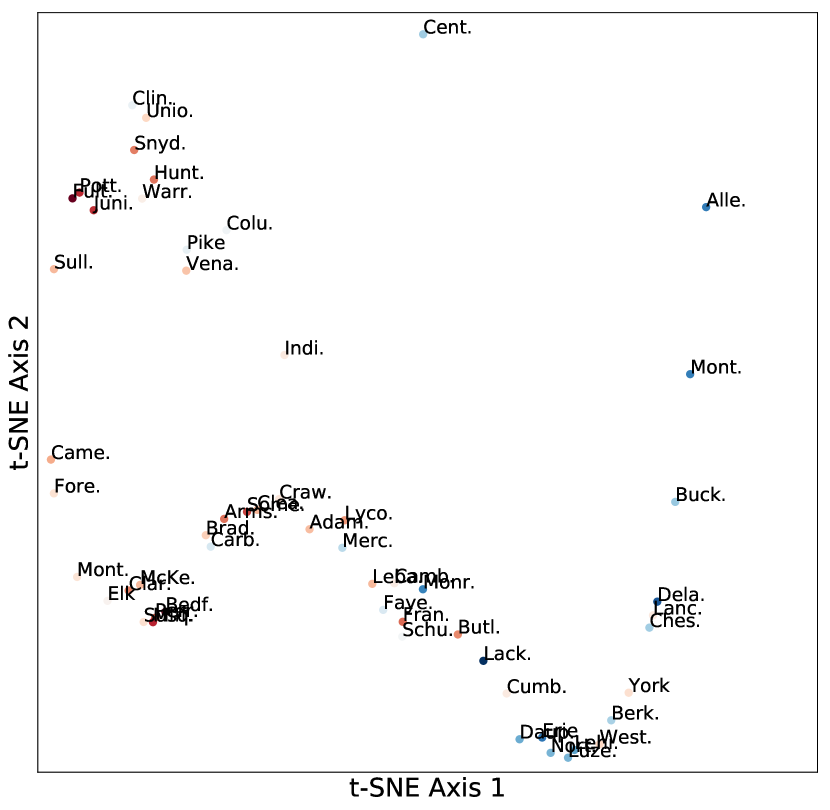

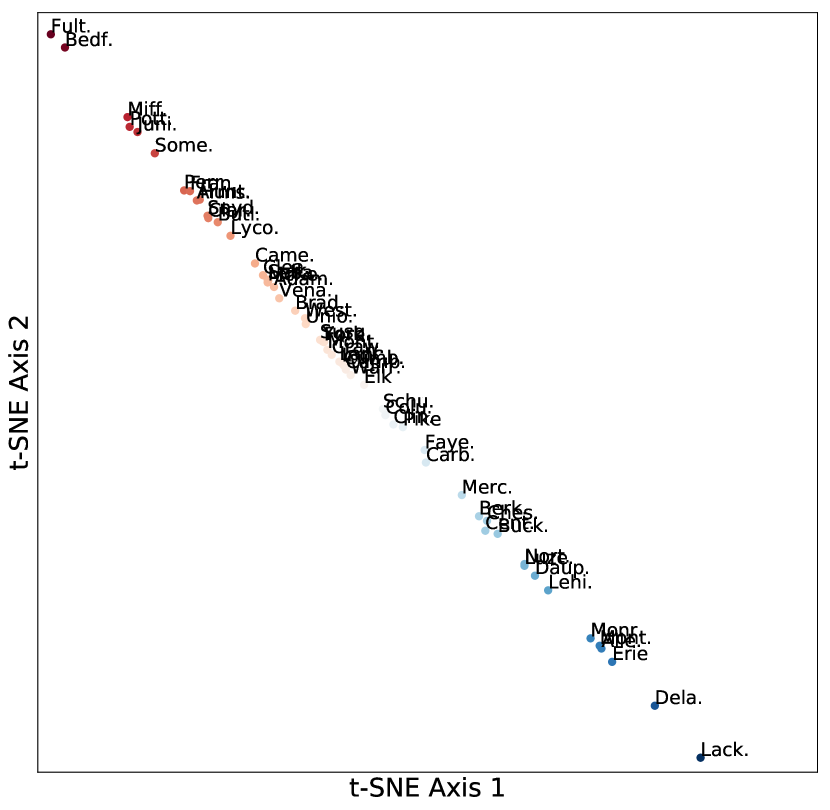

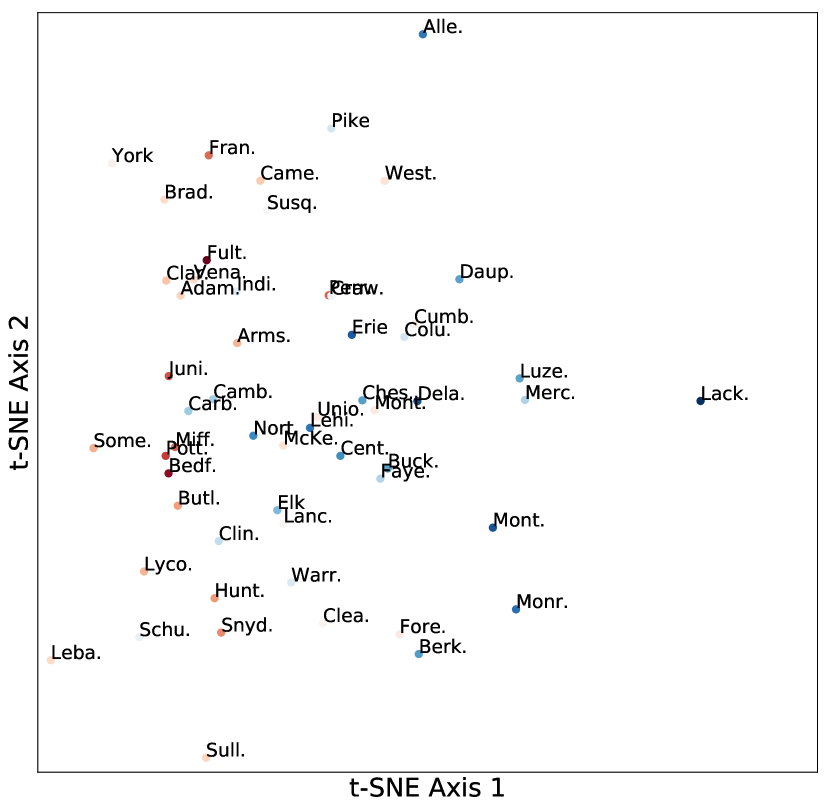

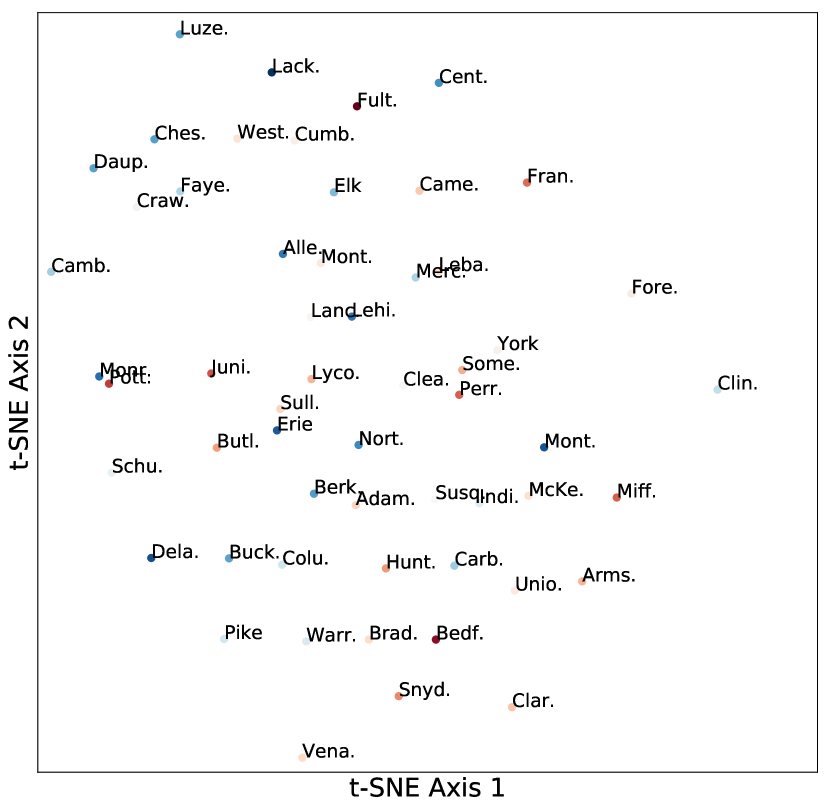

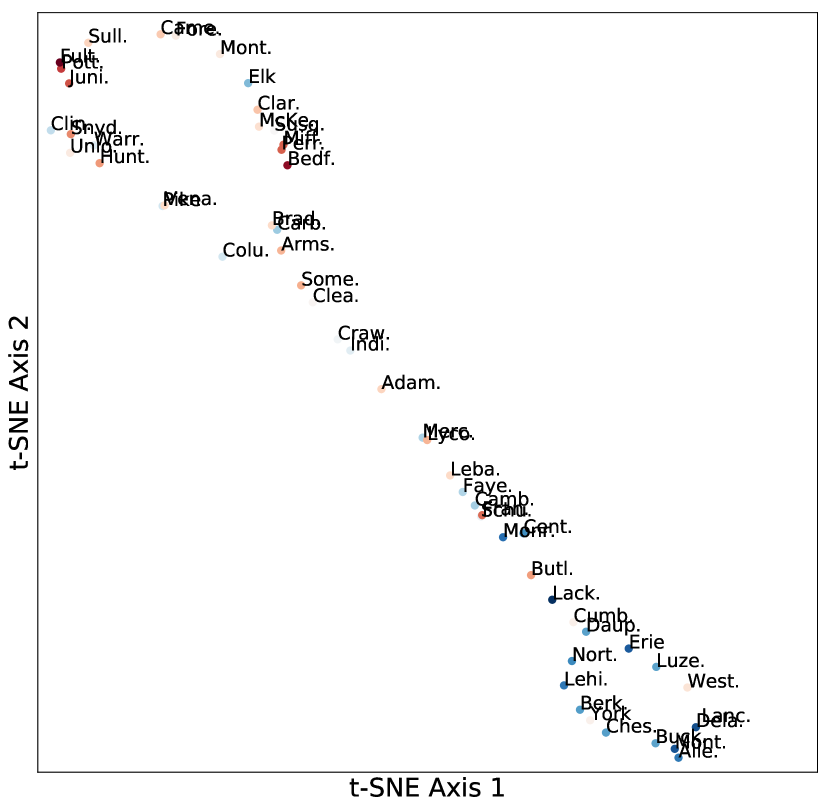

The out-of-sample predictive error is significantly reduced by personalization (Table 3). Representations of the personalized models for Pennsylvania counties are shown in Fig. 4, with a key to the abbrevations in Table S5. Generating county embeddings based solely on demographics produce embeddings which do not strongly correspond to voting patterns (Fig. 4(a)), while voting outcomes are near a one-dimensional manifold (Fig. 4(b)). In contrast, the personalized models produce a structure which interpolates between the two types of data (Fig. 4(e)). These trends are not captured by the baseline methods, such as the varying-coefficients model (Fig. 4(d)). In addition, concatenating the demographic and voting outcomes does not recover the same structure (Fig. 4(c)).

An interesting case is that of the Lackawanna and Allegheny counties. While these counties had similar voting results in the 2012 election, their embeddings are far apart due to the difference in demographics between their major metropolitan areas. This indicates that the county populations may be voting for different reasons despite similar demographics, a finding that is not discovered by jointly inspecting the demographic and voting data (Fig. 4(c)). Thus, sample-specific models can be used to understand the complexities of election results.

4 Discussion and Future Work

We have presented a framework to estimate collections of models by matching structure in sample covariates to structure in regression parameters. We showed that this framework accurately recovers sample-specific parameters, enabling collections of simple models to surpass the predictive capacity of larger, uninterpretable models. Our framework also enables fine-grained analyses which can be used to understand sample heterogeneity, even within groups of similar samples. Beyond estimating sample-specific models, we also believe it would be possible to adapt these ideas to improve standard models. For instance, the distance-matching regularizer may be applied to augment standard mixture models. It would also be interesting to consider extensions of this framework to more structured models such as personalized probabilistic graphical models. Overall, the success of these personalized models underscores the importance of directly treating sample heterogeneity rather than building increasingly-complicated cohort-level models.

Acknowledgments

We thank Maruan Al-Shedivat, Gregory Cooper, and Rich Caruana for insightful discussions.

This material is based upon work supported by NIH R01GM114311. Any opinions, findings and conclusions or recommendations expressed in this material are those of the author(s) and do not necessarily reflect the views of the National Institutes of Health.

References

- Ageenko et al. [2010] I. I. Ageenko, K. A. Doherty, and A. P. Van Cleave. Personalized lifetime financial planning tool, June 24 2010. US Patent App. 12/316,967.

- Al-Shedivat et al. [2017] M. Al-Shedivat, A. Dubey, and E. P. Xing. Contextual explanation networks. arXiv preprint arXiv:1705.10301, 2017.

- Al-Shedivat et al. [2018] M. Al-Shedivat, A. Dubey, and E. P. Xing. Personalized survival prediction with contextual explanation networks. arXiv preprint arXiv:1801.09810, 2018.

- Arora et al. [2017] S. Arora, Y. Liang, and T. Ma. A simple but tough-to-beat baseline for sentence embeddings. In International Conference on Learning Representations (ICLR), 2017.

- Buettner et al. [2015] F. Buettner, K. N. Natarajan, F. P. Casale, V. Proserpio, A. Scialdone, F. J. Theis, S. A. Teichmann, J. C. Marioni, and O. Stegle. Computational analysis of cell-to-cell heterogeneity in single-cell rna-sequencing data reveals hidden subpopulations of cells. Nature biotechnology, 33(2):155, 2015.

- Ding et al. [2015] X. Ding, Y. Zhang, T. Liu, and J. Duan. Deep learning for event-driven stock prediction. In IJCAI, pages 2327–2333, 2015.

- Dressman et al. [2007] H. K. Dressman, A. Berchuck, G. Chan, J. Zhai, A. Bild, R. Sayer, J. Cragun, J. Clarke, R. S. Whitaker, L. Li, et al. An integrated genomic-based approach to individualized treatment of patients with advanced-stage ovarian cancer. Journal of Clinical Oncology, 25(5):517–525, 2007.

- Fan and Zhang [1999] J. Fan and W. Zhang. Statistical estimation in varying coefficient models. Annals of Statistics, pages 1491–1518, 1999.

- Fisher et al. [2018] A. J. Fisher, J. D. Medaglia, and B. F. Jeronimus. Lack of group-to-individual generalizability is a threat to human subjects research. Proceedings of the National Academy of Sciences, 115(27):E6106–E6115, 2018. ISSN 0027-8424. doi: 10.1073/pnas.1711978115. URL https://www.pnas.org/content/115/27/E6106.

- Gormley et al. [2008] I. C. Gormley, T. B. Murphy, et al. A mixture of experts model for rank data with applications in election studies. The Annals of Applied Statistics, 2(4):1452–1477, 2008.

- Hallac et al. [2015] D. Hallac, J. Leskovec, and S. Boyd. Network lasso: Clustering and optimization in large graphs. In Proceedings of the 21th ACM SIGKDD international conference on knowledge discovery and data mining, pages 387–396. ACM, 2015.

- Hart [2016] S. A. Hart. Precision education initiative: Moving toward personalized education. Mind, Brain, and Education, 10(4):209–211, 2016. doi: 10.1111/mbe.12109. URL https://onlinelibrary.wiley.com/doi/abs/10.1111/mbe.12109.

- Hastie and Tibshirani [1993] T. Hastie and R. Tibshirani. Varying-coefficient models. Journal of the Royal Statistical Society. Series B (Methodological), pages 757–796, 1993.

- Jabbari et al. [2018] F. Jabbari, S. Visweswaran, and G. F. Cooper. Instance-specific bayesian network structure learning. In V. Kratochvíl and M. Studený, editors, Proceedings of the Ninth International Conference on Probabilistic Graphical Models, volume 72 of Proceedings of Machine Learning Research, pages 169–180, Prague, Czech Republic, 11–14 Sep 2018. PMLR. URL http://proceedings.mlr.press/v72/jabbari18a.html.

- Jiang [2007] J. Jiang. Linear and generalized linear mixed models and their applications. Springer Science & Business Media, 2007.

- Kuijjer et al. [2019] M. L. Kuijjer, M. G. Tung, G. Yuan, J. Quackenbush, and K. Glass. Estimating sample-specific regulatory networks. iScience, 14:226–240, 2019.

- Lengerich et al. [2018] B. J. Lengerich, B. Aragam, and E. P. Xing. Personalized regression enables sample-specific pan-cancer analysis. Bioinformatics, 34(13):i178–i186, 2018. doi: 10.1093/bioinformatics/bty250. URL http://dx.doi.org/10.1093/bioinformatics/bty250.

- Li et al. [2018] X. Li, S. Xie, P. McColgan, S. J. Tabrizi, R. I. Scahill, D. Zeng, and Y. Wang. Learning subject-specific directed acyclic graphs with mixed effects structural equation models from observational data. Frontiers in genetics, 9, 2018.

- Liu et al. [2011] C. Liu, J. C. Sage, M. R. Miller, R. G. Verhaak, S. Hippenmeyer, H. Vogel, O. Foreman, R. T. Bronson, A. Nishiyama, L. Luo, et al. Mosaic analysis with double markers reveals tumor cell of origin in glioma. Cell, 146(2):209–221, 2011.

- Liu et al. [2016] X. Liu, Y. Wang, H. Ji, K. Aihara, and L. Chen. Personalized characterization of diseases using sample-specific networks. Nucleic acids research, 44(22):e164–e164, 2016.

- Ma et al. [2018] S. Ma, S. Ogino, P. Parsana, R. Nishihara, Z. Qian, J. Shen, K. Mima, Y. Masugi, Y. Cao, J. A. Nowak, K. Shima, Y. Hoshida, E. L. Giovannucci, M. K. Gala, A. T. Chan, C. S. Fuchs, G. Parmigiani, C. Huttenhower, and L. Waldron. Continuity of transcriptomes among colorectal cancer subtypes based on meta-analysis. Genome Biology, 19(1):142, Sep 2018. ISSN 1474-760X. doi: 10.1186/s13059-018-1511-4. URL https://doi.org/10.1186/s13059-018-1511-4.

- Margulis et al. [2018] K. Margulis, A. S. Chiou, S. Z. Aasi, R. J. Tibshirani, J. Y. Tang, and R. N. Zare. Distinguishing malignant from benign microscopic skin lesions using desorption electrospray ionization mass spectrometry imaging. Proceedings of the National Academy of Sciences, 115(25):6347–6352, 2018. ISSN 0027-8424. doi: 10.1073/pnas.1803733115. URL https://www.pnas.org/content/115/25/6347.

- Maurer et al. [2013] A. Maurer, M. Pontil, and B. Romera-Paredes. Sparse coding for multitask and transfer learning. In ICML (2), pages 343–351, 2013.

- Ng et al. [2015] K. Ng, J. Sun, J. Hu, and F. Wang. Personalized predictive modeling and risk factor identification using patient similarity. AMIA Summits on Translational Science Proceedings, 2015:132, 2015.

- Pennington et al. [2014] J. Pennington, R. Socher, and C. Manning. Glove: Global vectors for word representation. In Proceedings of the 2014 conference on empirical methods in natural language processing (EMNLP), pages 1532–1543, 2014.

- Platanios et al. [2018] E. A. Platanios, M. Sachan, G. Neubig, and T. Mitchell. Contextual parameter generation for universal neural machine translation. arXiv preprint arXiv:1808.08493, 2018.

- Puig and Ginebra [2014] X. Puig and J. Ginebra. A bayesian cluster analysis of election results. Journal of Applied Statistics, 41(1):73–94, 2014.

- Ribeiro et al. [2016] M. T. Ribeiro, S. Singh, and C. Guestrin. Why should i trust you?: Explaining the predictions of any classifier. In Proceedings of the 22nd ACM SIGKDD international conference on knowledge discovery and data mining, pages 1135–1144. ACM, 2016.

- Rozantsev et al. [2018] A. Rozantsev, M. Salzmann, and P. Fua. Beyond sharing weights for deep domain adaptation. IEEE transactions on pattern analysis and machine intelligence, 41(4):801–814, 2018.

- Shyu et al. [1991] W. M. Shyu, E. Grosse, and W. S. Cleveland. Local regression models. In Statistical models in S, pages 309–376. Routledge, 1991.

- Sollich and Krogh [1996] P. Sollich and A. Krogh. Learning with ensembles: How overfitting can be useful. In Advances in neural information processing systems, pages 190–196, 1996.

- Tibshirani and Friedman [2017] R. Tibshirani and J. Friedman. A pliable lasso. arXiv preprint arXiv:1712.00484, 2017.

- Van Der Maaten [2014] L. Van Der Maaten. Accelerating t-sne using tree-based algorithms. The Journal of Machine Learning Research, 15(1):3221–3245, 2014.

- Vinayak et al. [2019] R. K. Vinayak, W. Kong, G. Valiant, and S. Kakade. Maximum likelihood estimation for learning populations of parameters. In International Conference on Machine Learning, pages 6448–6457, 2019.

- Visweswaran and Cooper [2010] S. Visweswaran and G. F. Cooper. Learning instance-specific predictive models. Journal of Machine Learning Research, 11(Dec):3333–3369, 2010.

- Wang et al. [2014] B. Wang, A. M. Mezlini, F. Demir, M. Fiume, Z. Tu, M. Brudno, B. Haibe-Kains, and A. Goldenberg. Similarity network fusion for aggregating data types on a genomic scale. Nature methods, 11(3):333, 2014.

- Xu et al. [2015] J. Xu, J. Zhou, and P.-N. Tan. Formula: Factorized multi-task learning for task discovery in personalized medical models. In Proceedings of the 2015 International Conference on Data Mining. SIAM, 2015.

- Yamada et al. [2016] M. Yamada, K. Takeuchi, T. Iwata, J. Shawe-Taylor, and S. Kaski. Localized lasso for high-dimensional regression. stat, 1050:20, 2016.

- Zou and Hastie [2005] H. Zou and T. Hastie. Regularization and variable selection via the elastic net. Journal of the Royal Statistical Society: Series B (Statistical Methodology), 67(2):301–320, 2005.

Appendix A Analysis

Initializing sample-specific models around a population estimate is convenient because the sample-specific estimations do not diverge from the population estimate unless they have strong reason to do so. Here, we analyze linear regression minimized by squared loss (e.g., ), though the properties extend to any predictive loss function with a Lipschitz-continuous subgradient.

We prove Theorem 1 by introducing two helpful lemmas. First, the distance-matching regularizer does not move the center of mass:

Lemma 2.

For any ,

Proof of Lemma 2.

Let . Then, for any symmetric , ,

| (9a) | ||||

| (9b) | ||||

| (9c) | ||||

| . So | ||||

| (9d) | ||||

| (9e) | ||||

This implies that the distance-matching regularizer has no effect on . An intuitive explanation is to visualize each as a collection of springs connecting estimator to each of the other estimators. While the springs will have some control over the pairwise distances, they cannot move the center of mass of any pair of particles and thus cannot adjust the center of mass of the system.

Second, the update to the center of mass does not grow with the number of samples:

Lemma 3.

At iteration , the update to the center of mass is bounded by:

| (10) |

Proof of Lemma 3.

The update to the barycenter at iteration is:

| (11a) | |||||

| (11b) | |||||

| by Lemma 2 | (11c) | ||||

where is the sub-gradient of used for optimization. Let where is the subgradient of used for optimization, with -Lipschitz continuous. Let be Lipschitz-continuous. Then

| (11d) | ||||

| (11e) | ||||

| (11f) | ||||

| (11g) | ||||

| (11h) |

where 11f holds because the population estimator was solved by a gradient descent algorithm resulting in . For , as used in our experiments, . For linear regression, . For normalized so that and , . With , we have the upper bound on the update:

Now we are ready to prove Theorem 1.

Appendix B Additional figures and discussion

B.1 Finance

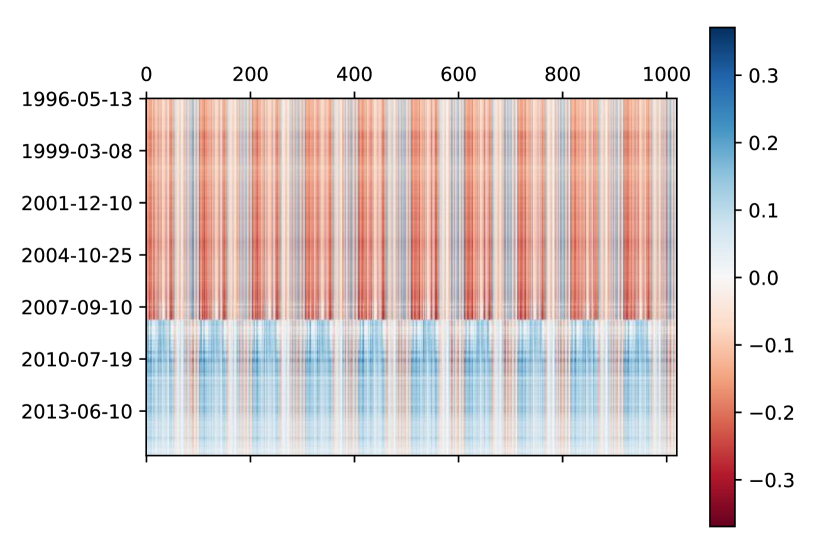

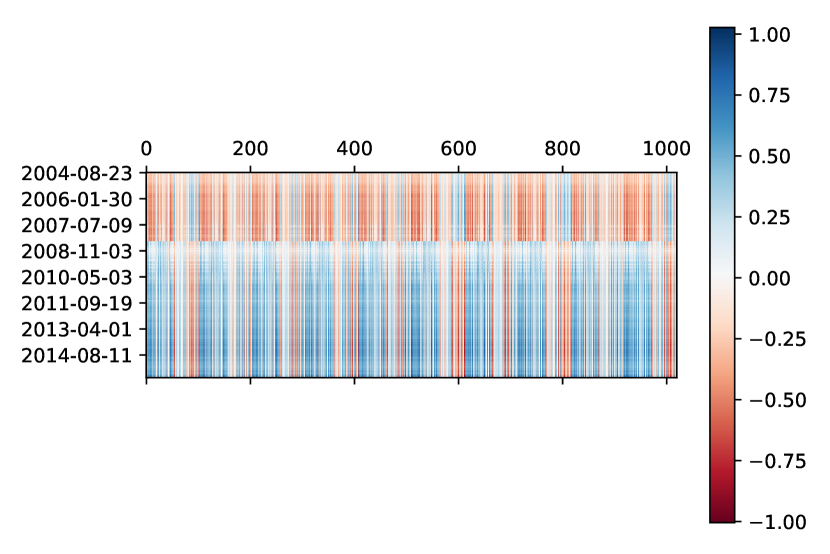

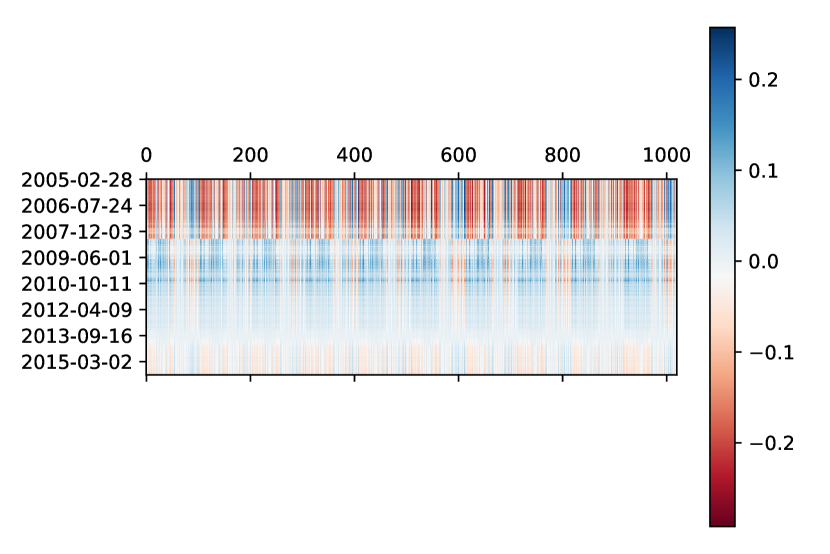

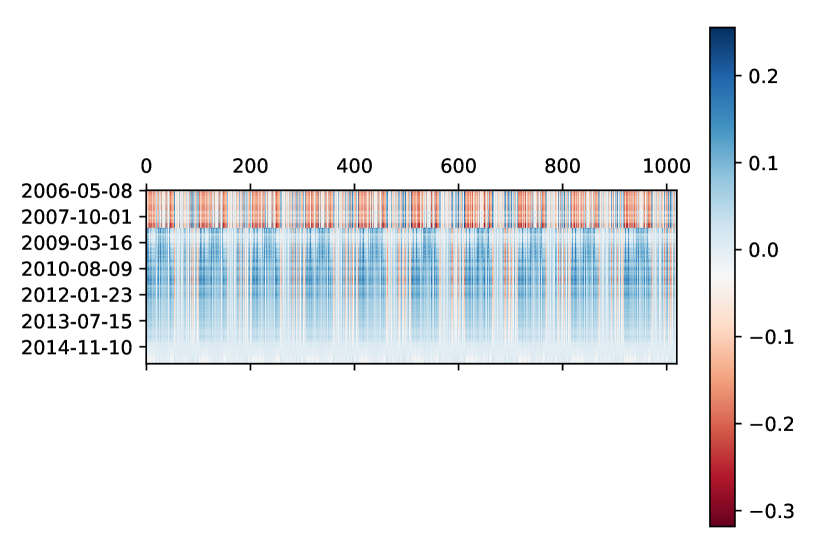

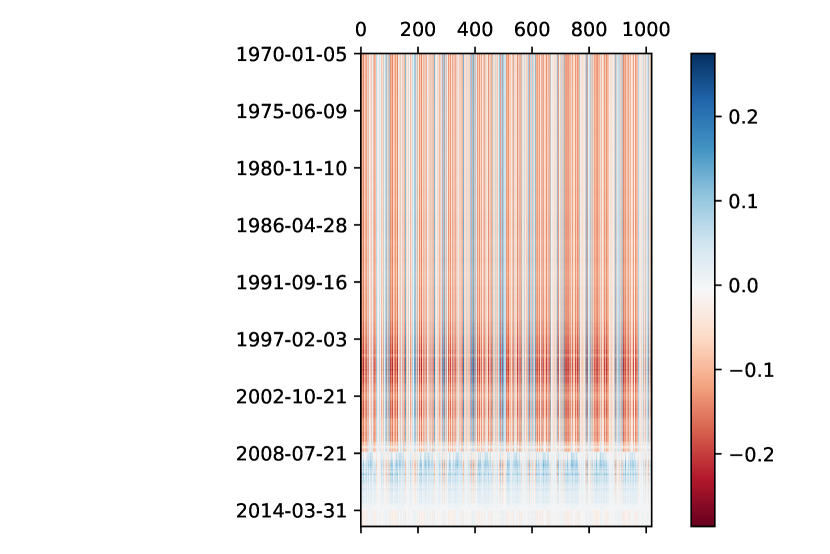

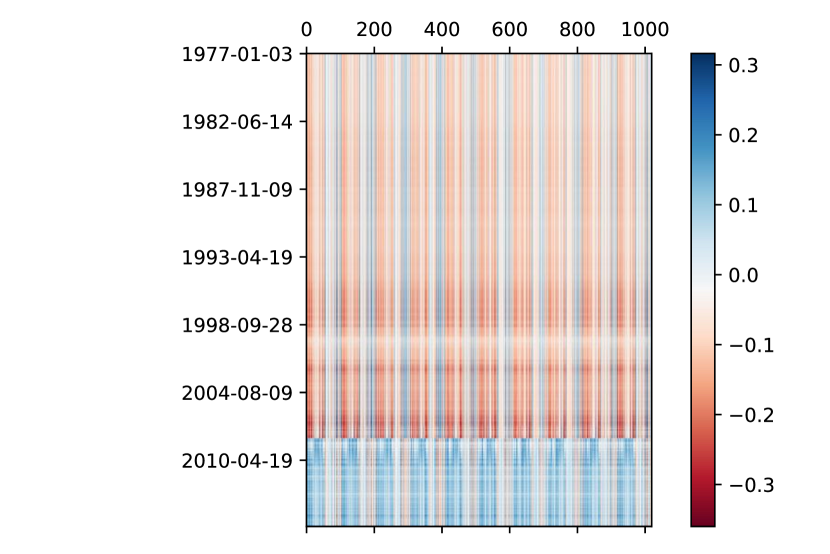

As described in the main text, we fit a variety of personalized models to a financial dataset of stock market price histories and world news headlines. To understand the relevance of each feature, we visualize the coefficients for each security in Fig. S6. The striped pattern is a result of the alternating arrangement of news and prices. In all securities, the effects of the Great Financial Crisis in 2008 are clear. Interestingly, other recessions do not seem to have similar lasting effects on parameter values, implying that these recessions had fewer structural effects than the Great Financial Crisis.

B.2 Cancer

By aggregating feature importance across each patient, we determine which feature is the most predictive of the sample labels for each patient (Table S4). We see that there are 9 different clusters, which are not accurately estimated by mixture models due to the sample heterogeneity within each mixture.

| Patient ID | Molecular Weight |

|---|---|

| 0 | 163.627 |

| 1 | 191.834 |

| 2 | 566.833 |

| 3 | 177.541 |

| 4 | 234.167 |

| 5 | 163.125 |

| 6 | 191.834 |

| 7 | 177.541 |

| 8 | 113.083 |

| 9 | 566.833 |

| 10 | 163.125 |

| 11 | 231.958 |

| 12 | 234.666 |

| 13 | 191.834 |

| 14 | 163.627 |

| 15 | 177.541 |

| 16 | 163.627 |

B.3 Election

As described in the main text, we fit personalized models to a dataset of election results. The patterns describe in the main text for the 2012 presidential election are replicated in the election of 2008 (Fig. S7).

| Abbreviation | Full Name |

|---|---|

| Alle. | Allegheny |

| Mont. | Montour |

| York | York |

| Faye. | Fayette |

| Adam. | Adams |

| Unio. | Union |

| Carb. | Carbon |

| Fore. | Forest |

| Perr. | Perry |

| Came. | Cameron |

| Pott. | Potter |

| Clin. | Clinton |

| Daup. | Dauphin |

| Merc. | Mercer |

| Fult. | Fulton |

| Cent. | Centre |

| Dela. | Delaware |

| Mont. | Montgomery |

| Warr. | Warren |

| Pike | Pike |

| Lehi. | Lehigh |

| Schu. | Schuylkill |

| Miff. | Mifflin |

| Susq. | Susquehanna |

| Juni. | Juniata |

| Bedf. | Bedford |

| Luze. | Luzerne |

| Brad. | Bradford |

| Lack. | Lackawanna |

| Some. | Somerset |

| Elk | Elk |

| Butl. | Butler |

| Erie | Erie |

| Lyco. | Lycoming |

| Sull. | Sullivan |

| Indi. | Indiana |

| Ches. | Chester |

| Monr. | Monroe |

| Nort. | Northampton |

| Craw. | Crawford |

| Arms. | Armstrong |

| Leba. | Lebanon |

| Cumb. | Cumberland |

| Camb. | Cambria |

| Hunt. | Huntingdon |

| West. | Westmoreland |

| Colu. | Columbia |

| Buck. | Bucks |

| Berk. | Berks |

| Clar. | Clarion |

| Vena. | Venango |

| Lanc. | Lancaster |

| Snyd. | Snyder |

| Fran. | Franklin |

| McKe. | McKean |

| Clea. | Clearfield |