Inversion of Convex Ordering: Local Volatility Does Not Maximize the Price of VIX Futures

Abstract.

It has often been stated that, within the class of continuous stochastic volatility models calibrated to vanillas, the price of a VIX future is maximized by the Dupire local volatility model. In this article we prove that this statement is incorrect: we build a continuous stochastic volatility model in which a VIX future is strictly more expensive than in its associated local volatility model. More generally, in this model, strictly convex payoffs on a squared VIX are strictly cheaper than in the associated local volatility model. This corresponds to an inversion of convex ordering between local and stochastic variances, when moving from instantaneous variances to squared VIX, as convex payoffs on instantaneous variances are always cheaper in the local volatility model. We thus prove that this inversion of convex ordering, which is observed in the SPX market for short VIX maturities, can be produced by a continuous stochastic volatility model. We also prove that the model can be extended so that, as suggested by market data, the convex ordering is preserved for long maturities.

Key words and phrases:

VIX, VIX futures, stochastic volatility, local volatility, convex order, inversion of convex ordering1. Introduction

For simplicity, let us assume zero interest rates, repos, and dividends. Let denote the market information available up to time . We consider continuous stochastic volatility models on the SPX index of the form

| (1.1) |

where denotes a standard one-dimensional -Brownian motion, is an -adapted process such that a.s. for all , and is the initial SPX price. By continuous model we mean that the SPX has no jump, while the volatility process may be discontinuous. The local volatility function associated to Model (1.1) is the function defined by

| (1.2) |

The associated local volatility model is defined by:

From [10], the marginal distributions of the processes and agree:

| (1.3) |

Let . By definition, the (idealized) VIX at time is the implied volatility of a 30 day log-contract on the SPX index starting at . For continuous models (1.1), this translates into

| (1.4) |

where (30 days). In the associated local volatility model, since by the Markov property of , , the VIX, denoted by , satisfies

| (1.5) |

Note that and have the same mean:

| (1.6) |

It has often been stated that, within the class of continuous stochastic volatility models calibrated to vanillas, the price of a VIX future is maximized by Dupire’s local volatility model. For example, in a general discussion in the introduction of [4] about the difficulty of jointly calibrating a stochastic volatility model to both SPX and VIX smiles, De Marco and Henry-Labordère approximate the VIX by the instantaneous volatility, i.e., and , and, using Jensen’s inequality and (1.3), they conclude that “within [the] class of continuous stochastic volatility models calibrated to vanillas, the VIX future is bounded from above by the Dupire local volatility model”:

Similarly, one would conclude that within the class of continuous stochastic volatility models calibrated to vanillas, the price of convex options on the squared VIX is minimized by the local volatility model: for any convex function , such as the call or put payoff function,

| (1.7) |

(The (correct) fact that had already been noticed by Dupire in [6].)

In this article, we prove that these statements are in fact incorrect. Even if 30 days is a relatively short horizon, it cannot be harmlessly ignored. VIX are implied volatilities (of SPX options maturing 30 days later), not instantaneous volatilities. We can actually build continuous stochastic volatility models, i.e., processes , such that

| (1.8) |

and, more generally, such that for any strictly convex function ,

| (1.9) |

(Our counterexample actually works for any .) Not only do we find one convex function such that (1.9) holds, we actually build a model in which (1.9) holds for any strictly convex function . Actually, we prove an inversion of convex ordering: Despite the fact that is smaller than in convex order for all (see (1.7)), is strictly larger than in convex order. Interestingly, Guyon [8] has reported that for short maturities , the market exhibits this inversion of convex ordering: the distribution of (computed with the market-implied Dupire local volatility) is strictly larger than the distribution of (implied from the market prices of VIX options) in convex order.

Guyon [9] has shown that, when the spot-vol correlation is large in absolute value, stochastic volatility models with fast enough mean reversion, as well as rough volatility models with small enough Hurst exponent, do exhibit this inversion of convex ordering. When mean reversion increases, the distribution of becomes more peaked, while the local volatility flattens but not as fast, and as a result it can be numerically checked that is strictly smaller than in convex order for short maturities. Interestingly enough, these models reproduce another characteristic of the SPX/VIX markets: that for larger maturities (say, 3–5 months) the two distributions become non-rankable in convex order, and for even larger maturities seems to become strictly larger than in convex order, i.e., the inversion of convex ordering vanishes as increases. However, it is very difficult to mathematically prove the inversion of convex ordering in these models. In order to get a proof of this inversion, our idea is to choose a more extreme model, in which the volatility process is such that is independent of , so that is almost surely constant, but also such that is not a.s. constant. In this case, since these two random variables have the same mean (recall (1.6)), is strictly smaller than in convex order, and (1.9) holds for any strictly convex function . In particular, applying (1.9) with yields (1.8).

Clearly, in order for to be non-constant, the local volatility cannot be constant as a function of , -a.e. in . There are many ways to achieve this, e.g., through volatility of volatility, and it is easy to numerically verify that (estimated from (1.5), e.g., using kernel regressions) is non-constant. However, the main mathematical difficulty here is to prove this result. To this end, we will consider models where the non-constant local volatility can be derived in closed form.

The remainder of the article is structured as follows. In Section 2 we derive a simple counterexample inspired by [2] where Beiglböck, Friz, and Sturm use a similar model to prove that local volatility does not minimize the price of options on realized variance. Then we generalize the counterexample in Section 3. Eventually in Section 4 we explain how the model can be extended so that, as suggested by market data, the convex ordering is preserved for long maturities.

2. A simple counterexample

Inspired by [2], we fix and consider the following volatility process:

| (2.1) |

where are three positive constants and denotes the result of a fair coin toss, independent of (e.g., known only at a time ).

Proposition 1.

Proof.

Let us denote

so that is given by or depending on the coin toss . Since is independent of , is a.s. constant:

Since this is also the mean of , to prove (1.9), it is enough to prove that is not a.s. constant.

Due to the very simple form of Model (2.1), we know the local volatility in closed form:

| (2.2) |

where is the density of the process with dynamics , , i.e.,

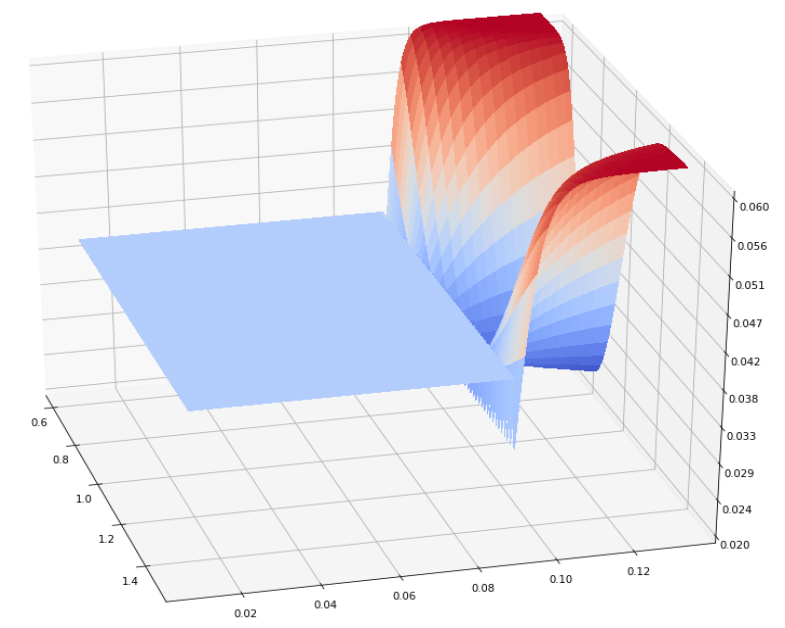

Figure 2.1 shows the shape of . Note in particular that takes values in and that

| (2.3) |

Let us define

| (2.4) |

so that . Note that

Since has support , in order to prove that is not a.s. constant, it is enough to prove that tends to when tends to . This follows from the next lemma. ∎

Proof.

Note that , where

so it is enough to prove that tends to when tends to . Let and . Let us denote , whose dynamics is given by

Since is bounded, it is easily checked that . Let . Then

| (2.5) |

We have

where

Recall that takes values in . From (2.5), for all . Obviously, for all . Moreover, it is easy to check that the convergence (2.3) is uniform w.r.t. : there exists such that

As a consequence, for all , . Finally,

We have thus proved that , hence , tends to when tends to . ∎

Remark 3.

Note that, if we fix and define

with only known at time , then we have built a model where the inversion of convex ordering holds for every short maturity .

3. Generalization

In this section, we generalize the example presented in Section 2, to show that the desired inversion of convex ordering can be obtained with a more interesting structure for the volatility. We fix , and define a càdlàg process on , which is independent of , the filtration generated by . We start by setting constant equal to for . This ensures that , and as a consequence is independent of for all , thus is constant:

We shall now define in , with the aim of having not constant. Let , and take values in . We denote by the law of on , the space of càdlàg functions on . Note that, for and , we recover the example of Section 2.

For every path , we denote by the evolution of the stock price for this realization of , that is

and by the density of the process , that is

The local volatility then takes the form

| (3.1) |

where

Lemma 4.

For all , the following limit holds for the local volatility:

| (3.2) |

where

| (3.3) |

Proof.

To study the limit of for , thanks to (3.1) and dominated convergence, we are reduced to consider the limit of . Note that

| (3.4) |

where

By Fatou’s lemma, as soon as , where

which in turn implies . On the other hand, if , then by dominated convergence , being bounded and bounded away from zero. Now equals zero when , and one when . This concludes the proof, noticing that

∎

Proposition 5.

Consider the stochastic volatility model (1.1). Let be constant equal to in , independent of in , admitting only finitely many paths, so that

| (3.5) |

with for all , . We assume the following non-degeneracy condition of in a neighborhood of : There exist and such that for all . Then, for all maturities , (1.9) holds. In particular, VIX futures are strictly more expensive than in the associated local volatility model.

With an abuse of notation, below we will write instead of , to ease readability.

Proof.

As in the example of Section 2, we consider the function

and note that our non-degeneracy assumption implies that

To prove the inversion of convex ordering for all maturities , we will show that , that is,

| (3.6) |

Since is discrete and the functions are continuous and bounded in , this interval divides in countably many intervals , , , such that, in each open interval , the function defined in (3.2) coincides with one or more paths of . To be more precise, for every , the sets defined in (3.3) coincide for every , say to a set , and

| (3.7) |

To show the convergence in (3.6), we split the interval into subintervals , . Since by dominated convergence

we are reduced to prove that for all ,

| (3.8) |

Fix and , and set . We split the interval into three subintervals

| (3.9) |

and we are going to show that converges uniformly to w.r.t. , for .

Let and note that the function depends on the paths and only through and , respectively. Therefore, from (3.4), we have

| (3.10) |

for any , which reduces to for . Now, it is easy to verify that, when tends to , converges to zero uniformly w.r.t. whenever and . In particular, there is such that, for all , , and , , thus

| (3.11) |

Since , we also have that, when tends to , converges to uniformly w.r.t. whenever and . This gives the existence of such that, for all , , , and ,

which by (3.10) implies

| (3.12) |

Note that in the present setting we have

from (3.7). Now (3.11) and (3.12) imply

| (3.13) |

which shows the claimed uniform convergence.

As in the proof of Lemma 2, we consider the log-price process , and we have , , since is bounded. Setting , we again obtain

| (3.14) |

We are going to show that

converges to zero for , by proving that for big enough this is smaller than the arbitrarily chosen . This in turn implies (3.8), being arbitrary, and concludes the proof of (3.6). In order to do that, we divide in three subintervals :

where we used the notation introduced in (3.9). Note that, since takes values in ,

and the same bound holds when taking the integral over . On the other hand, (3.14) implies

and (3.13) implies

for all . Altogether, for we have

This concludes the proof. ∎

4. Term-structure of convex ordering

In this section, we extend the model built in Section 3 in order to have the convex ordering preserved for long maturities, as suggested by market data. To this end, we set

| (4.1) |

where and is a Bernoulli random variable known in and independent of anything else. Say takes the value with probability and with probability , for some and . By Jourdain and Zhou [11], as long as the ratio is not too large, the stochastic differential equation (SDE) (4.1) admits a weak solution , which may not be unique. In the following we use the subscript or superscript to emphasize that a priori the corresponding quantities depend on the weak solution of (4.1).

Note that (4.1) implies that, whatever the weak solution, for . Therefore does not depend on the weak solution and is constant equal to for all maturities . We now want to show that, on the other hand, for any weak solution of (4.1), this is not true for . This will imply that is strictly smaller than in convex order for , thus there is no inversion of convex ordering for long maturities.

For any weak solution of (4.1), we set

Since is independent of , the conditional law of given and under agrees with the (unique) law of a weak solution to the SDE

living possibly on a different probability space (the weak uniqueness of the solution follows from [13, Theorem 3], given that [3, Proposition 5.1] ensures the existence of a measurable version of ). Being bounded and bounded away from zero, we deduce that, for , the conditional law of given and under admits a density , and that for all , which in turn implies that

| (4.2) |

Then, for , we have

Now, having constant (thus necessarily equal to ) corresponds to having , which is not possible given that takes values in , by (4.2). This shows that cannot be constant for any .

Remark 6.

To the best of our knowledge, uniqueness of a weak solution of (4.1) is still an open question. More generally, partial results on the existence of a weak solution of a calibrated stochastic local volatility (SLV) model of the form

| (4.3) |

have been obtained in [1, 11], but uniqueness has not been addressed. Note that Lacker et al. [12] have recently proved the weak existence and uniqueness of a stationary solution of a similar nonlinear SDE with drift, under some conditions. However, their result does not apply to the calibration of SLV models. Indeed, market-implied risk neutral distributions are strictly increasing in convex order and therefore no stationary solution can be a calibrated SLV model.

The possible absence of uniqueness of a weak solution of (4.1) or (4.3) is problematic, not only theoretically but also practically. It means that the price of a derivative in the calibrated SLV model may not be well defined. For example, in our case, the VIX may depend on . More generally, existence and uniqueness of (4.3) for general processes such as Itô processes remain a very challenging, open problem, despite the fact that these models are widely used in the financial industry, in particular thanks to the particle method of Guyon and Henry-Labordère [7].

Acknowledgements. We would like to thank Bruno Dupire and Vlad Bally for interesting discussions and helpful comments.

References

- [1] Abergel, F., Tachet, R. : A nonlinear partial integrodifferential equation from mathematical finance, Discrete Cont. Dynamical Systems, Serie A, 27(3):907–917, 2010.

- [2] Beiglböck, M., Friz, P., Sturm, S.: Is the minimum value of an option on variance generated by local volatility?, SIAM J. Finan. Math. 2:213–220, 2011.

- [3] Brunick, G., Shreve, S.: Mimicking an Itô process by a solution of a stochastic differential equation, The Annals of Applied Probability, 23(4):1584–1628, 2013.

- [4] De Marco, S., Henry-Labordère, P.: Linking vanillas and VIX options: A constrained martingale optimal transport problem, SIAM J. Finan. Math., 6:1171–1194, 2015.

- [5] Dupire, B.: Pricing with a smile, Risk, January, 1994.

- [6] Dupire, B.: Exploring Volatility Derivatives: New Advances in Modelling, presentation at Global Derivatives, Paris, 2005.

- [7] Guyon, J., Henry-Labordère, P., Being Particular About Calibration, Risk, January, 2012. Long version The smile calibration problem solved, SSRN preprint available at ssrn.com/abstract=1885032, 2011.

- [8] Guyon, J: On the Joint Calibration of SPX and VIX Options, presentation at Jim Gatheral’s 60th Birthday Conference, NYU, October 14, 2017.

- [9] Guyon, J: On the Joint Calibration of SPX and VIX Options, presentation at the Finance and Stochastics seminar, Imperial College, London, March 28, 2018.

- [10] Gyöngy, I.: Mimicking the One-Dimensional Marginal Distributions of Processes Having an Itô Differential, Probability Theory and Related Fields, 71, 501-516, 1986.

- [11] Jourdain, B., Zhou, A.: Fake Brownian motion and calibration of a Regime Switching Local Volatility model, preprint, available at arxiv.org/abs/1607.00077v1, 2016.

- [12] Lacker, D., Shkolnikov, M., Zhang, J.: Inverting the Markovian projection, with an application to local stochastic volatility models, preprint, 2019.

- [13] Veretennikov, A Yu: On the strong solutions of stochastic differential equations, Theory of Probability & Its Applications, 24(2):354–366, 1980.