Portfolio Cuts: A Graph-Theoretic Framework to Diversification

Abstract

Investment returns naturally reside on irregular domains, however, standard multivariate portfolio optimization methods are agnostic to data structure. To this end, we investigate ways for domain knowledge to be conveniently incorporated into the analysis, by means of graphs. Next, to relax the assumption of the completeness of graph topology and to equip the graph model with practically relevant physical intuition, we introduce the portfolio cut paradigm. Such a graph-theoretic portfolio partitioning technique is shown to allow the investor to devise robust and tractable asset allocation schemes, by virtue of a rigorous graph framework for considering smaller, computationally feasible, and economically meaningful clusters of assets, based on graph cuts. In turn, this makes it possible to fully utilize the asset returns covariance matrix for constructing the portfolio, even without the requirement for its inversion. The advantages of the proposed framework over traditional methods are demonstrated through numerical simulations based on real-world price data.

Index Terms— Financial signal processing, graph cut, graph signal processing, portfolio optimization, vertex clustering

1 Introduction

The introduction of modern portfolio theory by Harry Markowitz in 1952 [1] has marked the beginning of quantitative approaches to investing, with the underlying principle of diversification becoming the cornerstone of decision-making in finance and economics. The theory suggests an optimal strategy for the investment, which is based on the first- and second-order moments of the asset returns. This optimization task is referred to as the mean-variance optimization (MVO). Consider the vector, , which contains the returns of assets at a time , the -th entry of which is given by

| (1) |

where denotes the value of the -th asset at a time . The MVO asserts that the optimal vector of asset holdings, , is obtained through the following optimization problem

| (2) |

where is a vector of expected future returns, is the covariance matrix of returns, and is a Lagrange multiplier, also referred to as the risk aversion parameter. In practice, it is usually necessary to impose additional constraints on the values of .

The growth of computational power has naturally made MVO a ubiquitous tool for financial practitioners, however, to date the validity of its underlying theory remains perhaps the most debated topic in the field. Among a number of issues that make MVO unreliable in practice, a major caveat is the well established sensitivity of MVO to perturbations of the estimates of and [2, 3, 4], whereby small changes in the inputs may generate portfolio holdings with vastly different compositions. This is largely because the inputs to the MVO are statistical estimates of the moments of non-stationary return distributions, which typically yield portfolios that are far from truly optimal ones; these may even exhibit poor performance and excessive turnover.

It has been empirically demonstrated that the key parameter, the expected returns , can be rarely forecasted with sufficient accuracy. Consequently, various risk-based asset allocation approaches have been proposed, which drop the term altogether, with the optimization performed using only. The most important example is the minimum variance (MV) portfolio, formulated as

| (3) |

where , and the constraint, , enforces full investment of the capital. The optimal portfolio holdings then become

| (4) |

However, even in the absence of , the instability issues remain prominent, as the matrix inversion of required in (4) may lead to significant errors for ill-conditioned matrices.

Remark 1.

The numerical instability issues associated with MV portfolio optimisation leads to a counter-intuitive result, whereby the more collinear the asset returns the greater the need for diversification, and the more unstable the portfolio solution as the inversion of matrices with collinear rows/columns is notoriously unstable [5, 6]. Increasing the size of further complicates the problem as more data samples are required to yield a positive-definite estimate, i.e. at least independent and identically distributed (i.i.d.) observations of are needed. The severe impact of these challenges is highlighted by the fact that, in practice, even naive (equally-weighted) portfolios, i.e. , have been shown to outperform the mean-variance and risk-based optimization solutions [7].

These instability concerns have received substantial attention in recent years [8], and alternative procedures have been proposed to promote robustness by either incorporating additional portfolio constraints [9], introducing Bayesian priors [10] or improving the numerical stability of covariance matrix inversion [11]. A more recent approach has been to model assets using market graphs [12], that is, based on graph-theoretic techniques. Intuitively, a universe of assets can naturally be modelled as a network of vertices on a graph, whereby an edge between two vertices (assets) designates both the existence of a link and the degree of similarity between assets [13].

It is important to highlight that a graph-theoretic perspective offers an interpretable explanation for the underperformance of MVO techniques in practice. Namely, since the covariance matrix is dense, standard multivariate models implicitly assume full connectivity of the graph, and are therefore not adequate to account for the structure inherent to real-world markets [14, 15, 6]. Moreover, it can be shown that the optimal holdings under the MVO framework are inversely proportional to the vertex centrality, thereby over-investing in assets with low centrality [16, 17].

Intuitively, it would be highly desirable to remove unnecessary edges in order to more appropriately model the underlying structure between assets (graph vertices); this can be achieved through vertex clustering of the market graph [12]. Various portfolio diversification frameworks employ this technique to allocate capital within and across clusters of assets at multiple hierarchical levels. For instance, the hierarchical risk parity scheme [6] employs an inverse-variance weighting allocation which is based on the number of assets within each asset cluster. Similarly, the hierarchical clustering based asset allocation in [18] finds a diversified weighting by distributing capital equally among each of the cluster hierarchies.

Despite mathematical elegance and physical intuition, direct vertex clustering is an NP hard problem. Consequently, existing graph-theoretic portfolio constructions employ combinatorial optimization formulations [12, 19, 20, 21, 22, 23], which too become computationally intractable for large graph systems. To alleviate this issue, we employ the minimum cut vertex clustering method to introduce the portfolio cut. In this way, smaller graph partitions (cuts) can be evaluated quasi-optimally, using algebraic methods, and in an efficient and rigorous manner. The proposed approach is shown to enable creation of graph-theoretic capital allocation schemes, based on measures of connectivity which are inherent to the portfolio cut formulation. Finally, it is shown that the proposed portfolio construction employs full information contained in the asset covariance matrix, and without requiring its inversion, even in the critical cases of limited data lengths or singular covariance matrices.

2 Portfolio Cuts

We follow the notation in [24, 25], whereby a graph, , is defined as a set of vertices, , which are connected by a set of edges, . The existence of an edge between vertices and is designated by . The strength of graph connectivity of an -vertex graph can be represented by the weight matrix, , with the entries defined as

| (5) |

thus conveying information about the relative importance of the vertex (asset) connections. The degree matrix, , is a diagonal matrix with elements defined as

| (6) |

and, and such, it quantifies the centrality of each vertex in a graph. Another important descriptor of graph connectivity is the graph Laplacian matrix, , defined as

| (7) |

which serves as an operator for evaluating the curvature, or smoothness, of the graph topology.

2.1 Structure of market graph

A universe of assets can be represented as a set of vertices on a market graph [12], whereby the edge weight, , between vertices and is defined as the absolute correlation coefficient, , of their respective returns of assets and , that is

| (8) |

where is the covariance of returns between the assets and . In this way, we have if the assets and are statistically independent (not connected), and if they are statistically dependent (connected on a graph). Note that the resulting weight matrix is symmetric, .

2.2 Minimum cut based vertex clustering

Vertex clustering aims to group together vertices from the asset universe into multiple disjoint clusters, . For a market graph, assets which are grouped into a cluster, , are expected to exhibit a larger degree of mutual within-cluster statistical dependency than with the assets in other clusters, , . The most popular classical graph cut methods are based on finding the minimum set of edges whose removal would disconnect a graph in some “optimal” sense; this is referred to as minimum cut based clustering [26].

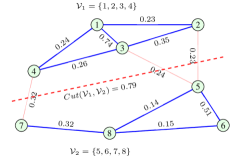

Consider an -vertex market graph, , which is grouped into disjoint subsets of vertices, and , with and . A cut of this graph, for the given clusters, and , is equal to a sum of all weights that correspond to the edges which connect the vertices between the subsets, and , that is

| (9) |

A cut which exhibits the minimum value of the sum of weights between the disjoint subsets, and , considering all possible divisions of the set of vertices, , is referred to as the minimum cut. Figure 1 provides an intuitive example of a graph cut.

Finding the minimum cut in (9) is an NP-hard problem, whereby the number of combinations to split an even number of vertices, , into any two possible disjoint subsets is given by .

Remark 2.

To depict the computational burden associated with this brute force graph cut approach, even for typical market graph with vertices (e.g. S&P 500 stock index), the number of combinations to split the vertices into two subsets is .

Within graph cuts, a number of optimization approaches may be employed to enforce some desired properties on graph clusters:

(i) Normalized minimum cut. The value of is regularised by an additional term to enforce the subsets, and , to be simultaneously as large as possible. The normalized cut formulation is given by [27]

| (10) |

where and are the respective numbers of vertices in the sets and . Since , the term reaches its minimum for .

(ii) Volume normalized minimum cut. Since the vertex weights are involved when designing the size of subsets and , then by defining the volumes of these sets as and , we arrive at [28]

| (11) |

Since , the term reaches its minimum for . Notice that vertices with a higher degree, , are considered as structurally more important than those with lower degrees. In turn, for market graphs, assets with a higher average statistical dependence to other assets are considered as more central.

Remark 3.

It is important to note that clustering results based on the two above graph cut forms are different. While the method (i) favours the clustering into subsets with (almost) equal number of vertices, the method (ii) favours subsets with (almost) equal volumes, that is, subsets with vertices exhibiting (almost) equal average statistical dependence to the other vertices.

2.3 Spectral bisection based minimum cut

To overcome the computational burden of finding the normalized minimum cut, we employ an approximative spectral solution which clusters vertices using the eigenvectors of the graph Laplacian, . The algorithm employs the second (Fiedler [29]) eigenvector of the graph Laplacian, , to yield a quasi-optimal vertex clustering on a graph. Despite its simplicity, the algorithm is typically accurate and gives a good approximation to the normalized cut [30, 31].

To relate the problem of the minimum cut in (10) and (11) to that of eigenanalysis of graph Laplacian, we employ an indicator vector, denoted by [24], for which the elements take sub-graph-wise constant values within each disjoint subset (cluster) of vertices, with these constants taking different values for different clusters of vertices. In other words, the elements of uniquely reflect the assumed cut of the graph into disjoint subsets .

For a general graph, we consider two possible solutions for the indicator vector, , that satisfy the subset-wise constant form:

(i) Normalized minimum cut. It can be shown that if the indicator vector is defined as [24]

| (12) |

then the normalized cut, in (10), is equal to the Rayleigh quotient of and , that is

| (13) |

Therefore, the indicator vector, , which minimizes the normalized cut also minimizes (13). This minimization problem, for the unit-norm form of the indicator vector, can also be written as

| (14) |

which can be solved through the eigenanalysis of , that is

| (15) |

After neglecting the trivial solution , (), since it produces a constant eigenvector, we next arrive at , ().

(ii) Volume normalized minimum cut. Similarly, by defining as

| (16) |

the volume normalized cut, in (11), takes the form of a generalised Rayleigh quotient of , given by [24]

| (17) |

The minimization of (17) can be formulated as

| (18) |

which reduces to a generalized eigenvalue problem of , given by

| (19) |

Therefore, the solution to (18) becomes the generalized eigenvector of the graph Laplacian that corresponds to its lowest non-zero eigenvalue, that is , ().

Remark 4.

The indicator vector, , converts the original, computationally intractable, combinatorial minimum cut problem into a manageable algebraic eigenvalue problem. However, the smoothest eigenvector, , of graph Laplacian is not subset-wise constant, and so such solution would be approximate but computationally feasible.

For the spectral solutions above, the membership of a vertex, , to either the subset or is uniquely defined by the sign of the indicator vector , that is

| (20) |

Notice that a scaling of by any constant would not influence the solution for clustering into subsets or .

Remark 5.

The value of the true normalized minimum cut in (10) has been shown to be bounded from below and above with constants which are proportional to the smallest non-zero eigenvalue, , of the graph Laplacian [32, 33]. Therefore, the eigenvalue serves as a measure of separability of a graph, whereby the larger the value of , the less separable the graph.

2.4 Repeated portfolio cuts

Although the above analysis has focused on the case with disjoint sub-graphs, it can be straightforwardly generalized to disjoint sub-graphs through the method of repeated bisection.

A single operation of the portfolio cut on the market graph, , produces two disjoint sub-graphs, and , as illustrated in Figure 2(a). Notice that in this way we construct a hierarchical binary tree structure, whereby the direct composition of the leaves of the network is equal to the original market graph, . We can then perform a subsequent portfolio cut operation on one of the leaves based on some criterion (e.g. the leaf with the greatest number of vertices or volume). Therefore, disjoint sub-graphs (leaves) can be obtained by performing the portfolio cut procedure times.

Remark 6.

Following Remark 5, the maximum number of portfolio cuts, , can be determined based on the value of the eigenvalue . For instance, the repeated portfolio cutting scheme may be terminated once the value of exceeds a predefined threshold.

Example 1.

Figure 2(a) illustrates the hierarchical structure resulting from portfolio cuts of a market graph, . The leaves of the resulting binary tree are given by (in red), whereby the number of disjoint sub-graphs is equal to . Notice that the union of the leaves equals to the original graph, i.e. .

2.5 Graph asset allocation schemes

We next propose intuitive asset allocation strategies, inspired by the work in [6, 18], which naturally builds upon the portfolio cut. The aim is to determine a diversified weighting scheme by distributing capital among the disjoint clusters (leaves) so that highly correlated assets within a given cluster receive the same total allocation, thereby being treated as a single uncorrelated entity.

By denoting the portion of the total capital allocated to a cluster by , we consider two simple asset allocation schemes:

(AS1) , where is the number of portfolio cuts required to obtain sub-graph ;

(AS2) ; where is the number of disjoint sub-graphs.

Remark 7.

An equally-weighted asset allocation strategy may now be employed within each cluster, i.e. every asset within the -th cluster, , will receive a weighting equal to .

Remark 8.

The weighting scheme in AS1 above is closely related to the strategy proposed in [18], while the scheme in AS2 is inspired by the generic equal-weighted (EW) allocation scheme [7]. These schemes are convenient in that they require no assumptions regarding the across-cluster statistical dependence. In addition, unlike the EW scheme, they implicitly consider the inherent market risks (asset correlation) by virtue of the portfolio cut formulation, which is based on the eigenanalysis of the market graph Laplacian, .

3 Numerical Example

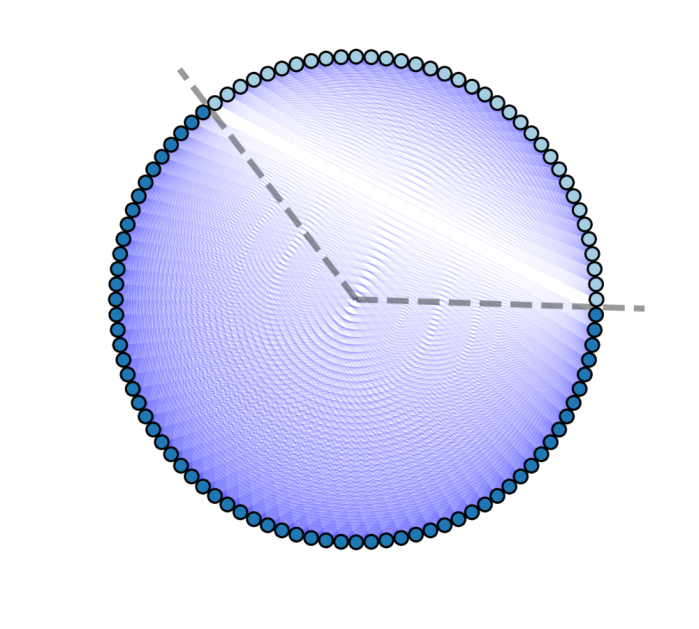

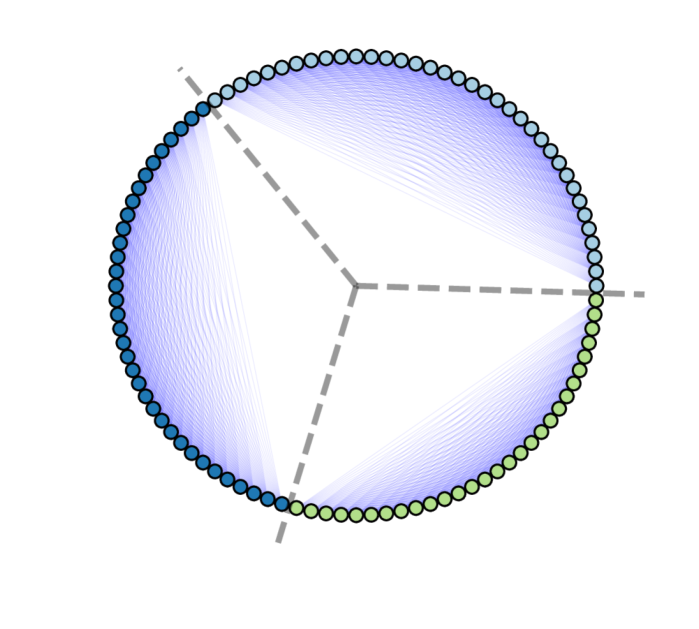

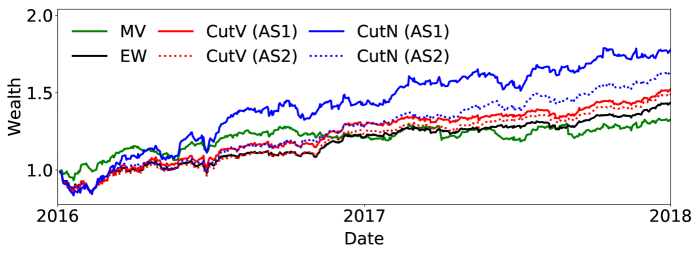

The performance of the portfolio cuts and the associated graph-theoretic asset allocation schemes was investigated using historical price data comprising of the most liquid stocks in the S&P 500 index, based on average trading volume, in the period 2014-01-01 to 2018-01-01. The data was split into: (i) the in-sample dataset (2014-01-01 to 2015-12-31) which was used to estimate the asset correlation matrix and to compute the portfolio cuts; and (ii) the out-sample (2016-01-01 to 2018-01-01), used to objectively quantify the profitability of the asset allocation strategies.

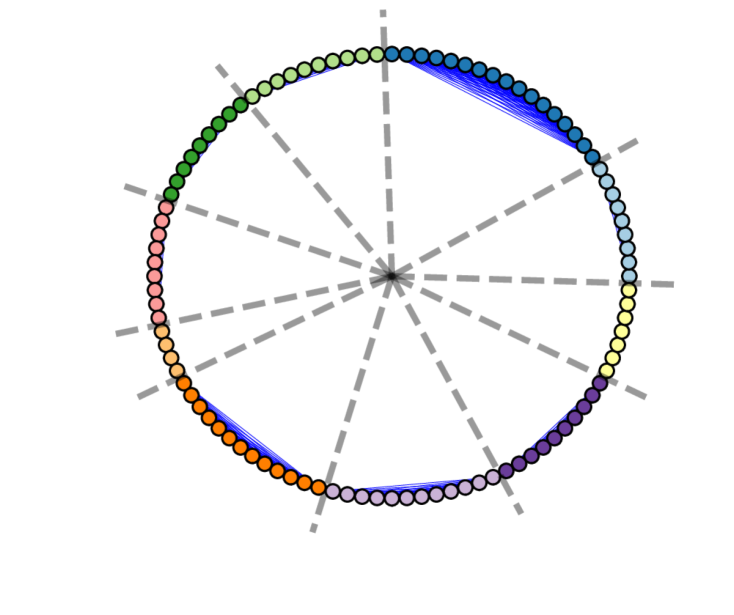

Figure 3 displays the -th iterations of the proposed normalised portfolio cut in (13), for , applied to the original -vertex market graph obtain from the in-sample data set.

Next, for the out-sample dataset, graph representations of the portfolio, for the number of cuts varying in the range , were employed to assess the performance of the asset allocation schemes described in Section 2.5. The standard equally-weighted (EW) and minimum-variance (MV) portfolios were also simulated for comparison purposes, with the results displayed in Figure 4.

Conforming with the findings in [6, 18], the proposed graph asset allocations schemes consistently delivered lower out-sample variance than the standard EW and MV portfolios, thereby attaining a higher Sharpe ratio, i.e. the ratio of the mean to the standard deviation of portfolio returns. This verifies that the removal of possibly spurious statistical dependencies in the “raw” format, through the portfolio cuts, allows for robust and flexible portfolio constructions.

| Cut Method | Allocation | ||||||

| CutV | AS1 | ||||||

| CutV | AS2 | ||||||

| CutN | AS1 | ||||||

| CutN | AS2 |

4 Conclusions

A graph-theoretic approach to portfolio construction has been introduced which employs the proposed portfolio cut paradigm to cluster assets using graph-specific techniques. The so derived graph asset allocation schemes have been shown to yield stable portfolio weights which are also robust to spurious asset correlations. Empirical analysis has demonstrated the advantages of the proposed framework over conventional portfolio optimization techniques, including a full utilization of the covariance matrix within the portfolio cut, without the requirement for its inversion. Finally, simulation results have demonstrated that the proposed framework allows for robust and flexible portfolio optimization, even in the critical cases of an ill-conditioned or singular asset covariance matrix.

References

- [1] H. Markowitz, “Portfolio Selection,” Journal of Finance, vol. 7, no. 1, pp. 77–91, 1952.

- [2] R. Michaud, “The Markowitz Optimization Enigma: Is Optimized Optimal?” Financial Analysts Journal, vol. 45, pp. 31–42, 1989.

- [3] ——, Efficient Asset Allocation: A Practical Guide to Stock Portfolio Optimization and Asset Allocation. Harvard Business School Press, 1998.

- [4] V. K. Chopra and W. T. Ziemba, “The Effects of Errors in Mean, Variances, and Covariances in Optimal Portfolio Choice,” Journal of Portfolio Management, vol. 19, no. 2, pp. 6–11, 1993.

- [5] D. Bailey and M. Lopez de Prado, “Balanced Baskets: A New Approach to Trading and Hedging Risks,” Journal of Investment Strategies, vol. 1, no. 4, pp. 21–62, 2012.

- [6] N. J. Calkin and M. Lopez de Prado, “Building Diversified Portfolios that Outperform Out of Sample,” The Journal of Portfolio Management, vol. 42, no. 4, pp. 59–69, 2016.

- [7] L. G. De Miguel, V. and R. R. Uppal, “Optimal Versus Naive Diversification: How Inefficient is the Portfolio Strategy?” Review of Financial Studies, vol. 22, pp. 1915–1953, 2009.

- [8] P. N. Kolm, R. Tutuncu, and F. J. Fabozzi, “60 Years of Portfolio Optimization: Practical Challenges and Current Trends,” European Journal of Operational Research, vol. 234, no. 2, pp. 356–371, 2014.

- [9] R. Clarke, H. De Silva, and S. Thorley, “Portfolio Constraints and the Fundamental Law of Active Management,” Financial Analysts Journal, vol. 58, pp. 48–66, 2002.

- [10] F. Black and R. Litterman, “Global Portfolio Optimization,” Financial Analysts Journal, vol. 48, no. 5, pp. 280–291, 1992.

- [11] O. Ledoit and M. Wolf, “Improved Estimation of the Covariance Matrix of Stock Returns With an Application to Portfolio Selection,” Journal of Empirical Finance, vol. 10, no. 5, pp. 603–621, 2003.

- [12] V. Boginski, S. Butenko, and P. M. Pardalos, “On Structural Properties of the Market Graph,” in Innovations in Financial and Economic Networks, A. Nagurney, Ed. Edward Elgar Publishers, 2003, pp. 29–45.

- [13] H. A. Simon, “The Architecture of Complexity,” In Proceedings of the American Philosophical Society, 1962.

- [14] N. J. Calkin and M. Lopez de Prado, “Stochastic Flow Diagrams,” Algorithmic Finance, vol. 3, no. 1–2, pp. 21–42, 2014.

- [15] ——, “The Topology of Macro Financial Flows: An Application of Stochastic Flow Diagrams,” Algorithmic Finance, vol. 3, no. 1, pp. 43–85, 2014.

- [16] G. Peralta and A. Zareei, “A Network Approach to Portfolio Selection,” Journal of Empirical Finance, vol. 38, no. A, pp. 157–180, 2016.

- [17] Y. Li, X. F. Jiang, Y. Tian, S. P. Li, and B. Zheng, “Portfolio Optimization Based on Network Topology,” Physica A, vol. 515, pp. 671–681, 2019.

- [18] T. Raffinot, “Hierarchical Clustering-Based Asset Allocation,” The Journal of Portfolio Management, vol. 44, no. 2, pp. 89–99, 2017.

- [19] V. Boginski, S. Butenko, and P. M. Pardalos, “Statistical Analysis of Financial Networks,” Computational Statistics & Data Analysis, vol. 48, no. 2, pp. 431–443, 2005.

- [20] ——, “Mining Market Data: A Network Approach,” Computers & Operations Research, vol. 33, no. 11, pp. 3171–3184, 2006.

- [21] A. A. Gunawardena, R. R. Meyer, and W. L. Dougan, “Optimal Selection of an Independent Set of Cliques in a Market Graph,” In Proceedings of the International Conference on Economics, Business and Marketing Management, pp. 281–285, 2012.

- [22] V. Boginski, S. Butenko, S. O., S. Trunkhanov, and J. Gil Lafuente, “A Network-Based Data Mining Approach to Portfolio Selection via Weighted Clique Relaxations,” Annals of Operations Research, vol. 216, pp. 23–34, 2014.

- [23] V. Kalyagin, A. Koldanov, P. Koldanov, and V. Zamaraev, “Market Graph and Markowitz Model,” in Optimization in Science and Engineering, T. M. Rassias, C. A. Floudas, and S. Butenko, Eds. Springer, 2014, pp. 293–306.

- [24] L. Stanković, D. P. Mandic, M. Daković, M. Brajović, B. Scalzo Dees, and T. Constantinides, “Graph Signal Processing – Part I: Graphs, Graph Spectra, and Spectral Clustering,” arXiv:1907.03467, 2019.

- [25] L. Stanković, D. P. Mandic, M. Daković, I. Kisil, E. Sejdić, and A. G. Constantinides, “Understanding the Basis of Graph Signal Processing via an Intuitive Example-Driven Approach,” IEEE Signal Processing Magazine, in press, 2019.

- [26] S. E. Schaeffer, “Graph clustering,” Computer Science Review, vol. 1, no. 1, pp. 27–64, 2007.

- [27] L. Hagen and A. B. Kahng, “New Spectral Methods for Ratio Cut Partitioning and Clustering,” IEEE Transactions on Computer-Aided Design of Integrated Circuits and Systems, vol. 11, no. 9, pp. 1074–1085, 1992.

- [28] J. Shi and J. Malik, “Normalized Cuts and Image Segmentation,” Departmental Papers (CIS), p. 107, 2000.

- [29] M. Fiedler, “Algebraic Connectivity of Graphs,” Czechoslovak Mathematical Journal, vol. 23, no. 2, pp. 298–305, 1973.

- [30] A. Y. Ng, M. I. Jordan, and Y. Weiss, “On Spectral Clustering: Analysis and an Algorithm,” In Proceedings of the Advances in Neural Information Processing Systems, pp. 849–856, 2002.

- [31] D. A. Spielman and S. H. Teng, “Spectral Partitioning Works: Planar Graphs and Finite Element Meshes,” Linear Algebra and its Applications, vol. 421, no. 2-3, pp. 284–305, 2007.

- [32] F. Chung, “Laplacians and the Cheeger Inequality for Directed Graphs,” Annals of Combinatorics, vol. 9, no. 1, pp. 1–19, 2005.

- [33] L. Trevisan, “Lecture Notes on Expansion, Sparsest Cut, and Spectral Graph Theory,” 2013.