Latent Dirichlet Analysis of Categorical Survey Responses

Abstract

Beliefs are important determinants of an individual’s choices and economic outcomes, so understanding how they comove and differ across individuals is of considerable interest. Researchers often rely on surveys that report individual beliefs as qualitative data. We propose using a Bayesian hierarchical latent class model to analyze the comovements and observed heterogeneity in categorical survey responses. We show that the statistical model corresponds to an economic structural model of information acquisition, which guides interpretation and estimation of the model parameters. An algorithm based on stochastic optimization is proposed to estimate a model for repeated surveys when responses follow a dynamic structure and conjugate priors are not appropriate. Guidance on selecting the number of belief types is also provided. Two examples are considered. The first shows that there is information in the Michigan survey responses beyond the consumer sentiment index that is officially published. The second shows that belief types constructed from survey responses can be used in a subsequent analysis to estimate heterogeneous returns to education.

Keywords: Information Acquisition, Mixture Models, Hierarchical Latent Class Models, Expectations

JEL Codes: D84, C21, C23

1 Introduction

An important part of economic analysis is understanding why economic outcomes differ across individuals. Heterogeneity in individual beliefs is presumed to be an important factor contributing to the observed differences. But, as beliefs are not easily observed directly, researchers often turn to surveys that solicit such information and report the qualitative responses in categorical form. For example, the Michigan Consumer Survey asks if individuals expect home prices to increase or decrease, and whether they believe business conditions are worse or better than the previous year. The Gallup Poll solicits sentiments towards politics, values and the environment, while the Bank of England Inflation Attitudes Survey tracks inflation expectations as categorical responses. Individuals’ views on stock valuations have been studied in Shiller, Kon-Ya, and Tsutsui (1996). In this paper, we use the term ‘beliefs’ to represent qualitative assessments about unknown or unrealized quantities. This encompasses such economic terms as ‘expectations’, which are beliefs about future values of specific variables such as inflation rates, ‘sentiments’, which are beliefs about current and future economic conditions in broad terms, as well as ‘attitudes’ and ‘self-assessments’, which are beliefs about health, wealth, and other socio-economic dimensions.

A distinctive feature of beliefs about the economy is that they are cross-sectionally correlated, presumably due to public information about the economy, but the correlation is not perfect, since individuals are heterogeneous. The goal is to design a methodology that is grounded in economic theory and can analyze heterogeneous and qualitative responses. Existing econometric methods designed for analyzing categorical data on beliefs are quite limited. Often, a single aggregated index is obtained by averaging the ordered survey responses. As discussed in Pesaran and Weale (2006), the application of this method is limited to datasets with variables that are closely related and easily ordered. More concerning is that this method provides an aggregate summary without modeling any heterogeneity, and thus cannot explain how beliefs differ. Yet, Manski (2004) and Dominitz and Manski (2004) document significant heterogeneity in beliefs even for events where individuals are unlikely to have private information. Manski (2004) suggests that the observed heterogeneity can be related to differences in the way individuals process public information, but did not make precise what the process might be. We suggest a model for this process.

We model heterogeneity in beliefs measured in surveys as coming from differences in individuals’ information choice. An example helps fix ideas. Suppose that we have survey responses for individuals grouped by the majority political affiliation (Democrat or Republican) for the county in which they live. The goal is to understand the heterogeneity in the survey responses given the observed group membership. Our economic model assumes that individuals have access to many news sources of public information such as CNN, ESPN, Discovery Channel, Fox News, etc. and can choose one news source to improve their naive belief about inflation. The model would predict that individuals living in a Republican-leaning county are more likely to (but do not always) choose Fox News, while those living in a Democrat-leaning county are more likely to (but do not always) choose CNN. To the extent that Fox News provides more coverage encouraging fiscal conservatism and the dangers of monetizing the deficit, this news source may leave its followers with a more pessimistic belief about future inflation. The information effect induced by Fox News is combined with an individual’s naive expectation to determine whether the individual is optimistic or pessimistic about inflation. In our economic model, an individual’s observed group membership does not directly determine heterogeneous beliefs, but it influences the source of information that the individual chooses to process, which in turn influences their sentiments.

Our economic model maps into a Bayesian hierarchical mixture model, also known as mixed membership model, that shares many similarities with Latent Dirichlet Allocation (LDA) of Blei, Ng, and Jordan (2003) for text data. Accordingly, we refer to our model as LDA-S. Mixed membership models are used in a variety of applications to cluster high-dimensional discrete data, including text, network, and genomic data. Our contribution is to show that a particular mixed-membership model can be motivated from an economic model in which belief heterogeneity is linked to group-level differences in processing of common information, and that this model can guide Bayesian model estimation, identification, and parameter interpretation. LDA-S uses multinomial distributions to explicitly take into account the categorical nature of the data. The hierarchical structure comes from the fact that the observed group membership affects the observed outcome through the unobserved choice of information source. The econometrician specifies a prior distribution for how group membership affects the choice of the information sources and another prior for how information affects the responses to the survey. The economic assumptions not only guide the choice of these priors, but also facilitate interpretation of the posterior estimates.

We derive two versions of the model: one for the static cross-section case, and one for the dynamic case when the belief formation process is time-dependent. To illustrate the economic insight gained from estimating heterogeneous types in qualitative survey data, our first example estimates a dynamic LDA-S model from the Michigan data to show that the estimated proportions of belief types are linked to macroeconomic factors like uncertainty and unemployment; this information is not apparent when working only with the aggregate consumer sentiment index currently published.

In the second example, we show that the estimated belief types can be used as estimates of fixed effects in subsequent regressions. We re-examine the estimation of returns to education considered in Card (1995). Using data from the National Longitudinal Survey of Young Men, we first estimate belief types using LDA-S. These estimates are then used to control for unobserved heterogeneity and estimate heterogeneous effects in a second step OLS regression of income on education. We find an important source of heterogeneity in returns to education relating to whether an individual believes ‘internal’ versus ‘external’ factors determine success.

2 Related Econometrics Literature

There are three types of categorical variables: nominal variables which represent unordered categories (such as zip code and NAICS codes), numerical (count) data, which represent ordered data such as age, and ordinal data (such as satisfaction metrics of excellent/good/bad) that are qualitative in nature. Ordinal data are said to be non-metrical when the distance between two categories has no interpretation. Survey data on categorical beliefs are often of this latter type.

There is a small existing literature on the methodology for analyzing qualitative survey data on beliefs. Carlson and Parkin (1975) uses a model with latent thresholds to derive aggregate probabilistic expectations from qualitative trichotomous responses on price expectations, assuming underlying quantitative inflation expectations are distributed normally. Structural modeling of categorical variables generally requires strong parametric assumptions for estimation of polychoric correlations, which is computationally burdensome and not easily scalable. For a discussion on these methods, see Ng (2015). Most often, a simple averaging method is used to aggregate qualitative beliefs data. For example, the Gallup Poll Weekly Economic Confidence Index is derived from averaging responses to two questions on the current and future state of the economy, where “good/excellent” or “getting better” is assigned a numeric value of 1 and “poor” or “getting worse” is assigned a numeric value of -1. Pesaran (1985) uses a weighted average instead. Neither of these methods capture heterogeneity in responses.

For analyzing other types of categorical survey data, a popular method among social scientists is the ‘asset index’ method of Filmer and Pritchett (2001a, b) used to summarize categorical data on asset ownership for households in developing countries. The method converts all categorical variables to binary variables, and applies PCA to the transformed matrix of responses. The method is simple, non-parametric and requires nothing more than the ability to compute a singular value decomposition. PCA has also been applied to a matrix of responses directly when the outcomes are ordered, so, in principle, all PCA-based methods can be used to analyze qualitative beliefs as well.

Despite its simplicity, applying the Filmer-Pritchett method to analyze categorical survey data has known drawbacks. In addition to conceptual issues concerning what the indices actually measure, as discussed in Davidson, Rutstein, Kiersten, Eldow, Wagstaff, and Amouzou (2007); Wittenberg and Leibbrandt (2017) and references therein, there are also methodological issues. Foremost is the problem that averaging methods ignore the fact that the distance between different categories may not be constant. Furthermore, converting multinomial outcomes to binary variables will introduce spurious negative correlations within the multiple columns that are mapped from a single question. These issues are discussed in Kolenikov and Angeles (2009); Vyas and Kumaranayake (2006); Lovaton, McCarthy, Kirdruang, Sharma, and Gondwe (2014), among others. These limitations motivate our analysis.

The framework we adopt is a hierarchical Bayesian latent class model. Latent class models were first introduced in Lazarsfeld (1950) to analyze dichotomous attributes based on a survey sample consisting of individuals who are assumed to belong to distinct classes. It was theorized in Goodman (1979) as a model for categorical variables. A multinomial latent class model for discrete data assumes that discrete survey data are generated by a finite mixture of multinomial distributions and that the mixture probabilities are the same for each individual. In contrast, the hierarchical latent class model allows for heterogeneous mixture probabilities. Although latent variable models are widely used in economic analysis, hierarchical latent variable models are far less common. The analysis of Moench, Ng, and Potter (2013) is for continuous data, while Catania and Mari (2020) considers count data.

Hierarchical models for categorical data are known in the statistics literature as mixed membership models. The first model in this class is the grade-of-membership model introduced in Woodbury, Clive, and Jr. (1978) that allows individual units to belong to multiple classes simultaneously. A Bayesian version of it was used in Erosheva (2002) to analyze disability data. As seen from the collection of papers in Airoldi, Blei, Erosheva, and Feinberg (2015), many specifications and assumptions are possible within models in the mixed membership class. Particularly popular is Latent Dirichlet Allocation (LDA) of Blei, Ng, and Jordan (2003) for modeling topics in documents, which is similar to the admixture (mixture of mixture) model independently developed in Pritchard, Stephens, and Donnelly (2000). Erosheva, Fienberg, and Lafferty (2004) develop a related mixed membership model where topics in scientific publications are associated with multiple multinomial distributions, one for words and one for references. Erosheva (2002) and Erosheva, Fienberg, and Joutard (2007) develop mixed-membership models as a unifying framework for the soft clustering of categorical data and show that every mixed membership model has a finite mixture representation. Applications include social networks as in Airoldi, Blei, Fienberg, and Xing (2008), voting patterns and political beliefs as in Gross and Manrique-Vallier (2014), and genetic studies, such as associating genotypes with diseases as in Falush, Stephens, and Pritchard (2003). Draca and Schwarz (2020) use a mixed membership model to analyze political ideology. Their adaptations to economic analysis remain quite limited, though LDA is getting increased attention. Recent applications include the analysis of CEO time usage in Bandiera, Hansen, Prat, and Sadun (2020), reducing the dimension of FOMC transcripts in Hansen, McMahon, and Prat (2018), and predicting consumer purchases in Ruiz, Athey, Blei, et al. (2020). Although there is a wide variety of mixed membership models available for various applications, it is not always clear to economists how to choose a model for a given situation and under what conditions the parameter estimates can be given an economic interpretation.

3 An Econometric Model of Beliefs Based on Information Acquisition

The goal of the econometric exercise is to explain the heterogeneity in survey responses using a model that (i) explicitly recognizes that many of the responses are in categorical form, (ii) allows the survey responses to have cross-section dependence; (iii) connects unobserved heterogeneity in individuals to observed heterogeneity in characteristics and responses, and (iv) provides an economic interpretation to the unobserved heterogeneity.

We will use an economic model of information acquisition to motivate the econometric analysis. There is extensive theoretical work on the role of information in shaping economic agents’ decisions. Costly information acquisition has been used as an amplifier of discrimination in the field experiment of Bartoš, Bauer, Chytilová, and Matějka (2016), and as a justification for ‘mistakes’ in choices in the theoretical analysis of Caplin and Dean (2015). Empirical work has also used costly information acquisition as a possible explanation for heterogeneous responses in the Michigan Survey data. In Carroll (2003), households occasionally update their inflation forecasts based on reports provided by the Survey of Professional Forecasters. Branch (2004) models individuals as econometricians, and assumes that heterogeneous responses are generated by households choosing between a set of costly econometric prediction methods. These models are designed for univariate continuous outcomes and as a result do not make precise how information acquisition affects qualitative beliefs.

3.1 LDA-S for Cross-Section Data

There are individuals indexed by , and each individual is a member of a group . There are discrete survey responses in the dataset, where each question has possible responses. Individuals choose a single response for each question by choosing the option most appropriate for question as indicated by a score function , which depends on the set of information an individual has processed.

The information acquisition model we consider is one of sequential choice and is motivated by Ruiz, Athey, Blei, et al. (2020) which recognizes that hierarchical models can be rationalized by economic models of myopic sequential choice. An individual chooses which of the sources of information, to consume by maximizing their utility, which incorporates a group affinity for each information source and an individual specific effect :

| (1) |

The chosen source of information determines an individual’s belief type. The observed heterogeneity of an individual’s group membership is linked to the unobserved heterogeneity of an individual’s belief type by a function where

The probability that an individual selects information source is the probability that for all .

The information source that is chosen influences the actual response that an individual makes. In the model, the actual response to survey question is optimal in the sense that it maximizes the individual’s score function for each response.

The score for each response has two components:

-

1.

An individual effect drawn independently for each , and from distribution .

-

2.

A type-specific information effect drawn independently for each from some distribution .

Here, is interpreted as the naive score that the individual assigns to the question in the absence of any information. If the information is uninformative and for all , then the individual selects the naive response with the maximum . In general, however, the acquired information that is shared by members of the same belief type will affect the response.

The expected choices induced by each information source can be described by a map . Precisely, is a random variable that gives the probability that an individual with information source believes that option is the appropriate response to question .

To complete the analysis, we assume that (a) is independent over with distribution and (b) is independent over and with distribution . The economic model has the following conditional independence properties:

Assumption S 1

The source of information chosen by individual is independent of the source of information chosen by individual conditional on each individual’s group membership and , so that

Assumption S 2

The group-specific mixtures are independent across groups, so .

Assumption S 3

Conditional on information source , is independent of for and , and is independent of an individual’s group membership . .

Assumption S 4

Conditional independence of belief types, so for , and conditional independence of beliefs and mixtures so that .

Property S1 follows from the two independence assumptions on and . As group-specific affinities for each information source are independent, S2 rules out the selection patterns of one group influencing the access to information of a second group. Since all dependence across questions in individual responses are channeled through the common information source, S3 rules out individual preferences that are correlated across questions and unrelated to the information source. The terms in the score function are independent of the parameters that determine an individual’s choice of information , which leads to S4. This completes the economic model.

The econometrician does not observe , , or their distributions ( and ), so treats the matrix as random. He proceeds with estimation by taking the features of the model S1-S4 as maintained assumptions. He specifies a prior on which are more likely through a Dirichlet distribution with hyperparameter , which is the conjugate prior to the multinomial . The econometrician also does not know the distributions and , so specifies a prior as to what sort of belief structures are more likely. Since each is a multinomial distribution, a Dirichlet prior with hyperparameter is used:

Thus, under the structure of the economic model, we arrive at the statistical model for LDA-S defined by the following equations:

Model LDA-S

| (2a) | ||||

| (2b) | ||||

| (2c) | ||||

| (2d) | ||||

where individuals are indexed by and categorical responses in the survey are indexed by Using and , we can write the joint distribution of the model as

3.2 Dynamic LDA-S

Many surveys on beliefs are conducted repeatedly, each time with a possibly different sample of individuals. The Michigan Survey of Consumers is perhaps the best known example as it has been in existence for over 50 years. The Bank of Canada interviews the business leaders of about 100 firms to gather perspectives on business outlook, while the Bank of England solicits attitudes towards inflation.

As in the static model, we will motivate with an example, one that attributes differences in economic sentiment to time of response and the outlook of business news. For the dynamic example, we group individuals by the time at which they respond to the survey, rather than the location in which they live. In each month, there are a variety of news articles that convey different sentiments, but only a few are relevant to the survey questions. For example, some articles might have an optimistic tone and others may have a pessimistic one. The model postulates that the individual survey response will depend on the prevalence of the article type at time (the time specific effect), as well as a random idiosyncratic preference for the article type (the individual specific effect). In the dynamic model, varies with time to allow the proportion of optimistic and pessimistic information about the economy to vary over time; during bad times, it is easier to access pessimistic news and incorporate that information into beliefs. An individual’s selection of news type determines their belief type, and is labeled . An individual who reads negative news on declining energy prices and bankrupt oil companies is more likely to respond to a survey indicating that they believe the economy is weak. An individual who selects the positive news source describing a booming tech industry with new product offerings and rising stock prices is more likely to respond to a survey indicating that they believe the economy is robust. This is represented by , which gives the expected responses of individuals who have absorbed different types of news sources.

We will continue to work with a matrix of survey response data but will refer to the dynamic model as LDA-DS, denoting the time at which an individual responds to the survey by . The choice described in Equation 1 is now:

| (3) |

In the static model, is assumed to be independent of for any . But, is meant to capture the net cost and benefit of accessing news type for individuals who form beliefs at time . Economic conditions tend to be persistent, so a high proportion of negative news in month is likely followed by pessimism in month . Thus, we now assume time dependence in the proportions of individuals of each belief type. As a consequence, while features S1, S3 and S4 of dynamic model are the same as in LDA-S (and now labeled DS1, DS3 and DS4), S2 needs to be replaced with the following:

Assumption DS2:

Mixture proportion is a first order Markov process. is independent of conditional on for . Let be lognormally distributed and satisfy , where for and ,

The econometrician now takes DS1 - DS5 as maintained assumptions. For and , the model is characterized by

| (4a) | |||||

| (4b) | |||||

| (4c) | |||||

| (4d) | |||||

| (4e) | |||||

The joint probability distribution of the dynamic hierarchical latent class model becomes

3.3 Relationship to Latent Class, Mixed Membership Models and NMF

We now describe how LDA-S and LDA-DS are related to existing models in both statistical and economic terms. Consider first a non-hierarchical Bayesian latent class (LC) model. To justify the absence of a group-specific effect would require that is the same for each individual. Under such a restriction, any observable heterogeneity is independent of an individual’s choice of information . This, however, would be inconsistent with the substantial evidence that heterogeneity in responses is related to heterogeneity in observed characteristics, such as group membership. For example, Manski (2004) finds gender and schooling type to be correlated with an individual’s optimism. Allowing an individual’s choice of information to depend on observed characteristic endows LDA-S with more flexibility.

The GoM (Grade of Membership) model of Erosheva (2002) is a mixed membership model, which has been applied to survey data on disabilities, health, and political ideology. The difference between GoM and LDA-S is that for GoM, the type assignment parameter is a matrix, but for LDA-S, is a vector. This means that in GoM, the response to each question is assigned its own class label, so each individual is a mixture over belief types. In both our economic model and LDA-S, we only have an assignment to a single belief type. This does not mean that a more sophisticated economic model cannot be written per se, but GoM cannot immediately be motivated by our model of information acquisition. Furthermore, the flexibility of GoM comes at a cost of many more parameters, and, in our experience, as further discussed in Section 4, GoM is more susceptible to the problem of non-uniqueness for a given prior and dataset. LDA-S allows information source selection probabilities to co-move yet also vary across individuals. Assuming that each individual is a member of only a single belief type but groups of individuals are mixtures over belief types simplifies interpretation and identification.

The model in the mixed-membership class closest to ours is LDA for estimating topics in a corpus of documents. In topics modeling, the singular value decomposition of a word-document frequency matrix is known as Latent Semantic Indexing (LSI). A probabilistic variation of it, known as pLSI, was developed in Hoffmann (1999) and Hofmann (2001). pLSI treats the document-specific mixture over topics as a fixed parameter and the documents as a fixed collection. LDA is the Bayesian version of pLSI, which treats document-specific mixtures over topics as random, as specified by a Dirichlet distribution. The appeal of LDA over pLSI is that documents which have not been observed can be analyzed.

LDA-S is an adaptation of LDA to survey response data. Instead of the frequency of word occurrences in documents, we analyze frequency of responses to questions in grouped individuals. In LDA, documents are modeled as mixtures over topics, which each involve different distribution over words. In LDA-S, we model survey responses as group-specific mixtures over belief types, each characterized by multinomial distributions over survey responses. A topic in LDA involves a single distribution over all words in the corpus. For each word , the outcome variable is simply the identity of that word, so . The joint likelihood for LDA can be factorized:

By contrast, LDA-S sets because in surveys we have survey questions and for individual we observe for . The belief types in the LDA-S model each specify multinomial distributions, one for each question response recorded in the columns of . So we may think of LDA-S as a multivariate variant of LDA with , but a simplified version of GoM since our is an vector instead of a matrix. A concise comparison of LDA-S to LDA is as follows:

| LDA-S for types in responses | LDA for topics in documents | |

| Data/outcome | response of to question | word in corpus |

| Outcome dimension | ||

| Outcomes per unit | responses in | word index of |

| # individuals in survey | # words appearing in corpus | |

| Frequency matrix | (group-response) | (document-word) |

| Latent size | information sources | topics |

| Mixture size | , number of groups | , number of documents |

| Class assignment | information source/belief type | assignment of word to topic |

| Membership | membership of individual in group | membership of word in doc |

| Mixture | group-specific mixture over types | document specific mixture over topics |

| Outcome distribution | for with | for with |

The dynamic version of LDA introduced by Blei and Lafferty (2006) incorporates dynamics into class proportions but also allows the topic distributions to evolve according to different documents that are observed over time. Modeling time dependence in would require the expected responses induced by each information source to change over time. While this is possible, it seems more appropriate to explain variations in survey responses by the variation in the proportion of belief types over time, while holding the beliefs for each type fixed.

Figure 1 presents a graphical view that concisely summarizes the differences in statistical conditional independence assumptions across models. Figure (a) shows the standard LC model. Figure (b) shows that LDA-S is the same as an LC model, except that (i) is now a descendant of rather than a common , which means is now independent of upon conditioning on a group-specific mixture, rather than an aggregate mixture . These changes from the basic model allow for more heterogeneity in the patterns of class assignment within the population. Comparing GoM in (d) to LDA-S in (b), the plate surrounding a row of is now -dimensional, and the -subscripted plate now incorporates both and since is now . Observe that in the LDA-S model, there is no link between and except through their common prior. But in LDA-DS there is a direct link between and . The rest of the model remains the same, so we assume that the time-specific mixture over belief types captures all the time dependence.

We close this section with two additional remarks. First, note that in LDA-S in (b) is -dimensional, but in LDA in (c) is not. This is not just a modeling choice but is in some sense necessary. Modeling the responses for each individual as one outcome would be necessary if we assumed there were correlation in individual responses across questions beyond what is induced by an individual’s belief type. However, this would require dealing with the joint distribution of responses for each individual, which would then be a multinomial distribution over all possible response permutations for a survey. For that is larger than a handful of questions, this is too high-dimensional.

Second, there are other interpretations of LDA that will also help in understanding LDA-S. Buntine (2002); Buntine and Jakulin (2012) show that LDA is a type of independent component analysis, while Canny (2004) shows that LDA is a type of factor analysis for discrete data. When the latent class assignments are integrated out, LDA can also be seen as factorizing the (document-term) matrix into two low rank matrices, one representing the probability of topics given document, and one representing probability of words given topics. In lieu of svd, it is also possible to obtain a non-negative matrix factorization (NMF) of into two rank matrices, and , both with non-negative entries. Ding, Li, and Peng (2006) show that NMF and PLSI solve the same objective function. In LDA-S, the discrete data is mapped into a (non-negative) frequency response matrix of dimension , . In our analysis, belief type is itself of interest, so we do not integrate it out. But if this were done, the frequency matrix , also known as contingency table, can also be seen as a product of two low rank matrices: . The matrix represents the probability of responses given belief type assignment and can be compared to a flattened version of the 3-dimensional matrix , while is the probability of belief type assignment for each group. Though the NMF approach is non-parametric and does not specify a probability distribution for the latent variables, the low rank factorization perspective is helpful in understanding the issues to be discussed in Section 4.

4 Implementation Issues

This section discusses three implementation issues: estimation of the model, the choice of the number of belief types , and identification for a given number of types .

4.1 Sampling Algorithms

An appeal of LDA is that the hierarchical structure makes the model interpretable and computationally feasible, and LDA-S inherits these appealing features. We can also exploit computational tools developed for estimating LDA, which is a heavily researched topic in the last two decades. LDA can be estimated using either MCMC or variational inference methods. The latter approximates posterior distributions using optimization techniques and is reviewed in Blei, Kucukelbir, and McAuliffe (2017).

For this paper, we will use MCMC methods, which are familiar to economists. In the static case, conjugacy of the Dirichlet distribution makes deriving a Gibbs sampler for posterior estimation quite simple. In each step of a Gibbs sampler, each variable is sampled from its conditional distribution, conditional on all other variables in the model.

-

1.

Sample conditional on , , and . The conditional distribution of is multinomial:

-

2.

Sample conditional on , , and . The conditional distribution of is Dirichlet, with:

where

-

3.

Sample conditional on , , and . The conditional distribution of is Dirichlet, with:

where .

Steps 1 and 2 of the Dynamic LDA-S sampler are the same as in LDA-S. But Step 3 is more complicated because the dynamic model does not have a conjugate prior distribution for the state mixtures . Blei and Lafferty (2006) specify a lognormal formulation for and use a variational Kalman Filter for estimation. Using a Metropolis-Hastings step to sample from the posterior of the lognormal distribution for would involve slow exploration of the posterior and is difficult to scale to datasets with a large number of respondents or time periods. Bradley, Holan, and Wikle (2018) and Linderman, Johnson, and Adams (2015) replace the lognormal formulation to improve sampling speed and convergence.

Rather than changing the formulation for the dynamics, we adapt recent advances in MCMC methods to improve sampling speed and convergence. We use a sampling approach similar to the one in Bhadury, Chen, Zhu, and Liu (2016), which is a method known as Stochastic Gradient Langevin Dynamics (SGLD) developed in Welling and Teh (2011) for learning Bayesian models from large scale datasets. In brief, SGLD works as follows. For parameter of interest , prior , and data , let the likelihood be . Instead of using the full sample gradient of the log posterior distribution to find the mode, SGLD updates at step according to

where and is the stepsize. The acronym SGLD comes from the fact that it (i) uses mini-batches of the data of size (the stochastic gradient part), and (ii) adds noise (the Langevin dynamics part). The SGLD method ensures that the parameters reach the maximum of the posterior distribution quickly, and once it reaches the MAP value, the sampling procedure enters a Langevin dynamics stage, where the noise added to the parameter updates result in exploration of the posterior distribution. Though the above defines a non-stationary Markov chain, Welling and Teh (2011) show that will converge to samples from the true posterior distribution with careful choice of the stepsize . In particular, must satisfy and . The MCMC draws not only give the posterior mode, but the entire posterior distribution.

To use this approach in our setting requires making precise the density of interest and its derivative. Let be the standard normal density function. The condition distribution of is proportional to:

Then, the SGLD step for is a combination of gradient descent towards the maximum of the posterior distribution and additional noise that ensures the full posterior distribution is explored. Our approach nonetheless differs from SGLD in one way. In the original paper, the gradient descent step is taken with respect to a random subsample of data (ie. the mini-batch). For many survey datasets and certainly applications considered in this paper, the number of respondents is small enough that we do not need to take subsamples when updating the parameters. Hence we use the batch size that equals the size of the dataset. In step of the Gibbs Sampler, for each ,

The first derivative is easily computed as follows:

where and .

We follow the literature and use a step size of at step with , and . Tuning these parameters to get fast convergence and good posterior exploration can be challenging. Welling and Teh (2011) show that as decreases, the acceptance probability approaches 1, so that a Metropolis-Hastings test is unnecessary as the acceptance probability is close to 1. The last part of the sampler for LDA-DS involves , which, conditional on all the other variables in the model, has an Inverse Gamma distribution. Let and . Then, .

4.2 Identification and Choice of Priors

Finite mixture models are susceptible to weak and under-identification, and the researcher must also be alert to label switching as the ordering of the estimated latent class is arbitrary. See Jasra, Holmes, and Stephens (2005) and Masyn (2013) for a recent review of the literature. Since LDA-S is a variation of LDA, and LDA is a finite mixture model, we begin with a discussion of identification issues concerning LDA. As noted earlier, LDA can be seen as a problem of finding a non-negative factorization of the matrix , but such a matrix factorization is not unique. Some applications of LDA do not require uniqueness, such as prediction of the content of new documents. It is nonetheless still useful to understand the two sources of non-uniqueness and how to deal with the problem. First, if a solution satisfies , then any positive definite producing and is also solution. For example, can be the permutation of a diagonal matrix with positive diagonal elements, so scaling and permuting the rows and columns of and can produce equivalent solutions. For uniqueness of the non-negative matrix factorization problem, see Gillis (2014), Moussaoui, Brie, and Idier (2005) Hoyer (2004), Huang, Sidiropoulous, and Swami (2014). More problematic is that there may be additional and matrices not obtained from rotations by . Imposing summing up constraints on the rows of and are not usually enough to tie down a unique LDA solution, so side conditions are needed. This is not surprising because the LDA is a mixture model known to be non-identifiable without further assumptions. The Bayesian approach is to impose non-exchangeable priors. For Dirichlet priors, Griffiths and Steyvers (2007) show that the posterior distributions of and in LDA have a mode of:

where is a matrix of word counts for each topic, and is a matrix of document counts for each topic. From this representation, it is clear that the prior only shrinks towards but does not restrict or to any particular value. See also Ke, Montiel-Olea, and Nesbitt (2019) for a discussion of how the choice of priors influence identification in LDA.

Like LDA, the LDA-S decomposition is not unique. Following the literature, we impose non-exchangeable priors to ensure that the same belief type is identified in each MCMC draw. Specifically, we assign a Dirichlet prior for the expected information choice conditional on group membership , and another Dirichlet prior for expected response choice conditional on information choice . The posterior expected values for and that emerge from steps 2 and 3 of the Gibbs Sampler are analogous to the two expressions for LDA just presented, with replaced by counts for the responses for a question and replaced by counts for each group.

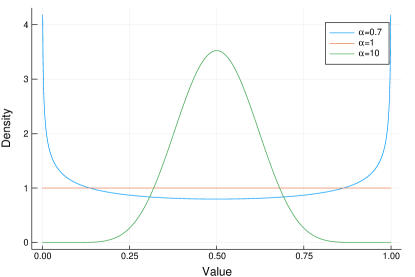

The choice of the hyperparameters for the Dirichlet distribution is important, but the economic model provides some guidance. For example, the prior for relates to assumptions about the underlying distributions that determine the preference for news sources, and . Consider as an example the case of two categories and a single group when the Dirichlet distribution for is also a Beta distribution. Figure 2 plots three cases: and . Values of are associated with values of that are on the corners of the simplex. This implies that the researcher believes that observed heterogeneity is tightly linked with unobserved heterogeneity, or that members of a group are likely to choose the same source of information. Values of are associated with values of in the center of the simplex, which implies that group membership is not highly correlated with unobserved heterogeneity. The case is an uninformative prior, with equal weight everywhere in the simplex. In the economic model, the unobserved heterogeneity is due to information choice. Hence specifying means that the researcher believes that the group specific cost of acquiring information is more variable than that of the individual specific benefit, so individuals in a certain group are likely to choose the same information. A similar discussion relates the prior for . Specifying a prior with would reflect the econometrician’s prior that all individuals who choose the same source of information are likely to respond the same way to each question. Although it is constant in this example, the hyperparameter vector need not be constant. The econometrician can specify higher probabilities on certain areas of the simplex of all possible beliefs over question responses.

In the examples that follow, we impose for all and , which is an uninformative prior for the relationship between group membership and information acquisition. We impose that for , and otherwise. Effectively, we assume that each information source is associated with a correctness score on one response that is higher than any other information source for at least one question in the survey. For example, for the Michigan Survey of Consumers, we assume that the first information source induces a higher probability on the first categorical response compared to other responses for all questions. The first question asks respondents about their financial condition compared to a year ago and the first categorical response to this question is ‘better now’. We thus interpret the first belief type estimated in multiple MCMC procedures to be the ‘optimistic’ one. The dynamic model has more parameters to estimate, , which has its own priors. Otherwise it is the same; we impose the same kind of prior restrictions on .

An additional issue relating to identification is that the frequency response matrix cannot have columns or rows that are near zero. This effectively rules out including questions with very rare responses; in some applications, responses are dropped or combined with more common responses. This condition, however, can be checked ahead of estimation.

4.3 The Choice of

Many solutions have been proposed to determine the number of latent classes in continuous data, but each has some shortcomings. Calculating the Bayes Factor for this type of hierarchical mixture model is computationally challenging due to the intractable integral over the parameter space required to compute the integrated likelihood. Other methods that integrate model selection into the MCMC procedure are complex and require specification of pseudo priors. Cross-validation is popular in the machine learning literature, but it is sensitive to the number of folds and the splits taken. Analyses on choosing the number of latent classes in discrete data are more limited. Early work by McHugh (1956) and Goodman (1974) provided insightful results for simple latent class models without a hierarchical structure. Simulation studies for hierarchical latent class models, such as those in Airoldi, Fienberg, Joutard, and Love (2006), have considered different criteria with no clear recommendation.

We use insights from both matrix factorization and statistical model selection to guide the choice of , the number of belief types induced by differing sources of information. We first check that there are enough ‘degrees of freedom’ for a non-negative matrix factorization of . This is a simple counting exercise: the number of independent observations in is ; the number of free parameters for and is, respectively, , and . This bound is based on counting entries in the frequency matrix alone. Additional information can loosen the bound. For example, Anandkumar, Foster, Hsu, Kakade, and Liu (2012) derived an algorithm that also uses third moments of the data to estimate LDA. To rule out under-identification would require , or

If , and , then the condition requires which is no longer a mixture model. However, if , and , the condition tolerates up to 4 classes. Though we are ultimately interested in parametric estimation of LDA-S, this algebraic result serves as a useful benchmark.

We run Monte-Carlo simulations to examine the implications of this identification condition in practice. Data are simulated using LDA-S as the DGP under two settings, one where the counting rule is satisfied and the others where it is violated. We evaluate the posterior mean of from the MCMC procedure. In the setting where the counting rule is satisfied, we find that the correlation between the posterior mean of and the true , averaged across 500 replications, approaches 1 as the sample size increases. This suggests that LDA-S is recovering the unique solution to the problem. On the other hand, when the model is underidentified and our counting rule fails, the model does not yield estimates that improve as the sample size increases because there are multiple solutions by design. This suggests that the counting rule is a useful check of identifiability.

In analysis of continuous data, it is well known from the Eckart-Young theorem that the best rank approximation of is spanned by the eigenvectors corresponding to the largest eigenvalues of . A similar idea can be expected to hold when is a function of discrete data. The eigenvalues of can be used to generate a scree plot. If has rank , there should be eigenvalues that are significantly larger than the rest. This can be used to guide the number of classes needed to explain a prescribed fraction of the variance of . Though this method is informal, it is useful in applications because this can be checked ahead of estimation.

In the applications below, we use the BIC to approximate the Bayes factor. Let be the maximum likelihood value of the data and be the set of parameters in the model. For a model with classes, where is the maximum likelihood value of the parameters and is the number of model parameters when the number of classes in the model is . We approximate the maximum likelihood value of the parameters using the posterior mean from the MCMC draws. The BIC considered is

where the sample size is the number of individuals. In simulations, this approximated BIC criterion reliably selects for models where the order condition for identification is met, even as we vary the form of the priors. Furthermore, the chosen by the BIC tends to coincide with the number of eigenvalues that explain over 90% of variation in .

5 Applications

This section consists of two parts. The first application estimates multiple types of respondents from the Michigan data using an LDA-S model. The goal is to show that while the proportion of optimistic respondents over time matches up well with the published index, the other predominant belief types in the data convey additional useful information on recession recovery and economic uncertainty. The second example uses the data analyzed in Card (1995) to illustrate how the estimated individual-level latent class belief types are linked to heterogeneous returns to education.

5.1 Heterogeneous Beliefs in Repeated Cross-Sections: The Michigan Data

The Michigan Index of Survey of Consumers (ICS) is a heavily watched indicator of consumer confidence. The index is constructed from monthly survey responses of approximately 500 telephoned respondents in continental U.S. Each month, an independent cross-section sample of households is drawn, and some are reinterviewed six months later. As explained on the official website of the survey, the ICS is constructed from five questions of the survey on the respondent’s opinion about current and future economic conditions as follows: (i) For compute the relative scores which is the percentage of respondents giving favorable replies to question , minus the percent giving unfavorable replies, plus 100; and (ii) After rounding each relative score to the nearest whole number, compute ICS = where 6.7558 is the value of the ICS in 1966 (the base period). The 2.0 is added to correct for sample design changes in the 1950s.

The ICS is an aggregate index and is often found to have little independent predictive power for real consumer spending. We will argue that there is unexploited information in the survey beyond the ICS, which requires applying a methodology that captures heterogeneity in responses. To make this point, we analyze 204,944 survey responses collected between January 1978 and May 2019. We do not model the repeated interviewing that occurs in the Michigan data. We use LDA-DS to analyze an additional 9 questions in the survey related to sentiment that are not incorporated in the ICS but have been asked since 1978. A challenge in using this data is missing values, as many survey respondents may not answer all questions. An appeal of LDA-DS is that it does not require each question to have similar response categories, and it does not require dropping or imputing responses that are incomplete, as long as they are not too rare in the sample.

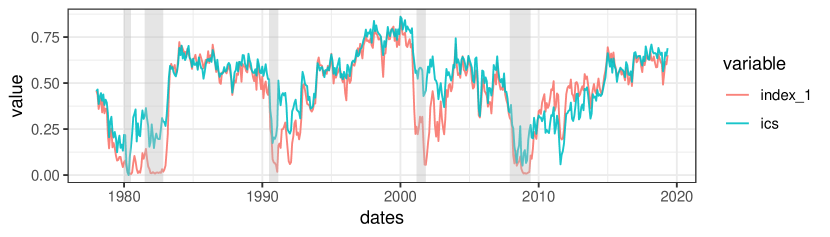

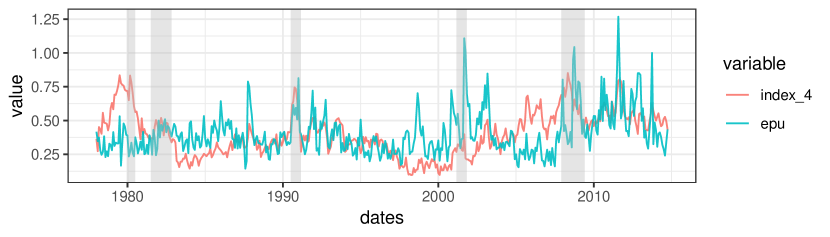

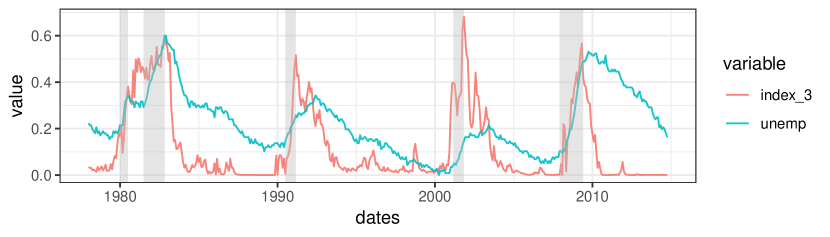

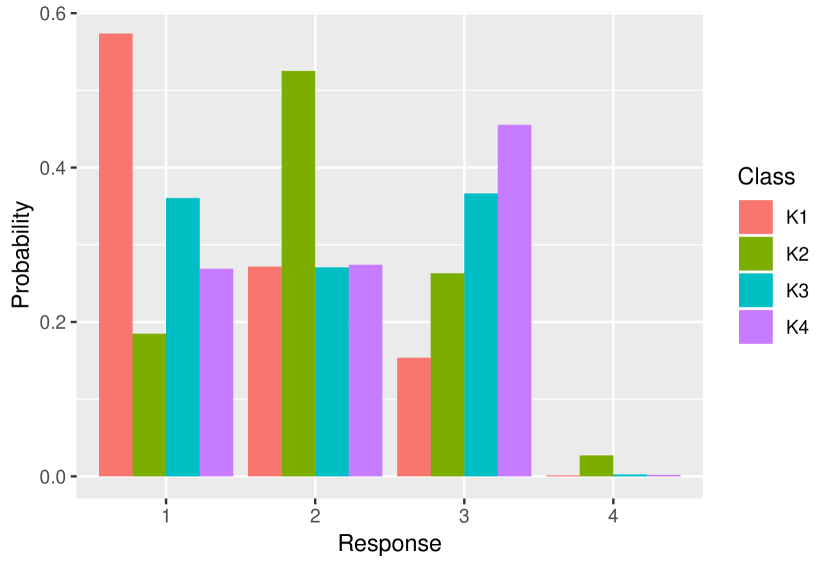

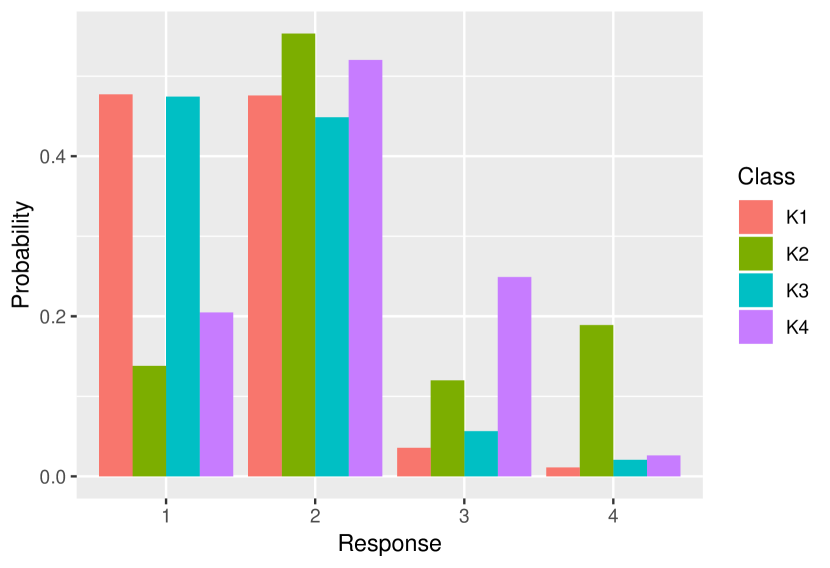

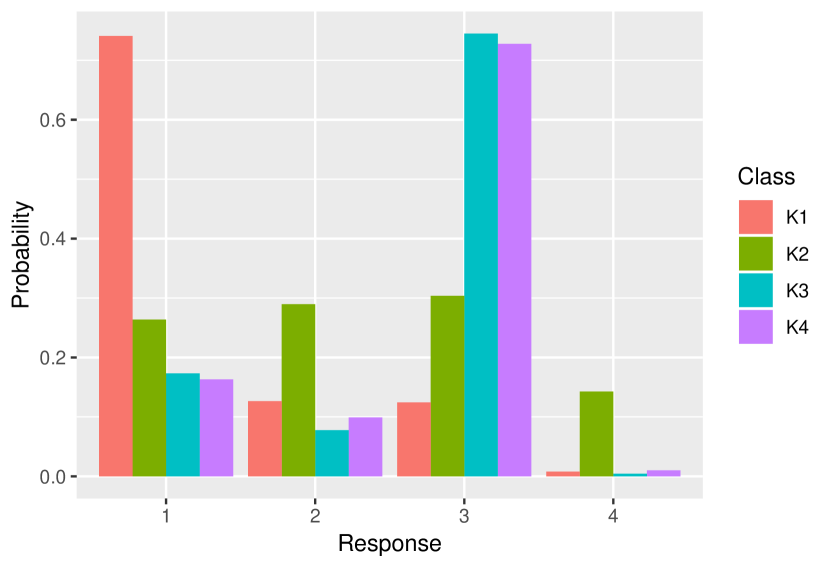

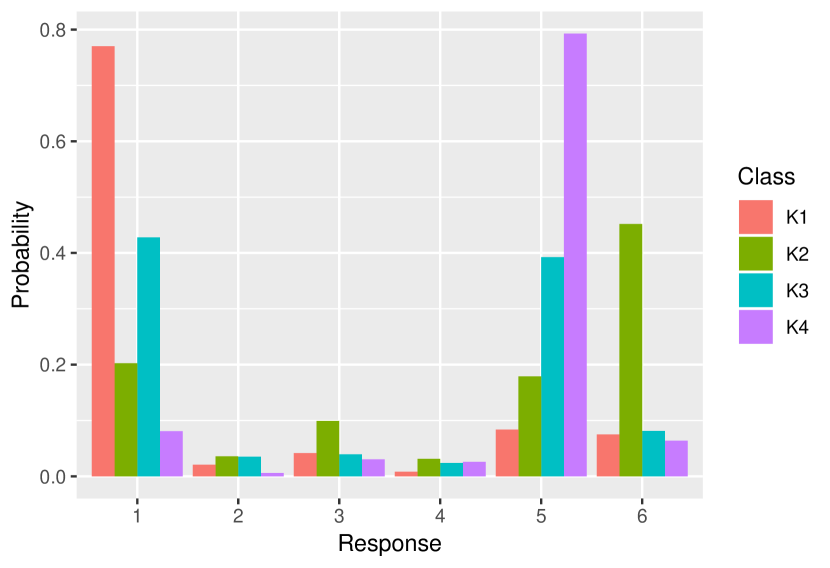

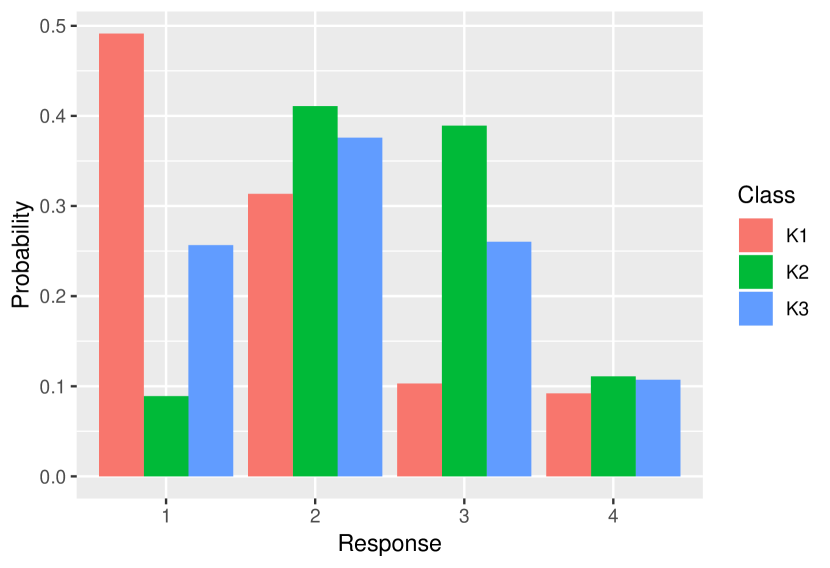

We estimate an LDA-DS model with types. Type 2 captures individuals who are uninformed and are likely to fill out the survey with lots of incomplete or missing responses. This decreases over time presumably due to changes in survey collection practices. We plot the type proportions in Figure 3 where , is the probability that an individual responding at time is assigned to type 1. A high corresponds to a high probability of responding optimistically to the survey questions on sentiment at time . As seen from Figure 3, this index is highly correlated with the rescaled Michigan ICS. Figure 3 also plots and with a rescaled news based uncertainty index and the unemployment rate. While often peaks before or at the beginning of the recession, peaks towards the end or after the recession. Examining the type-specific multinomial distributions, a few of which are plotted in Figure 4, suggests that Type 4 is associated with individuals who consume pessimistic news sources, and have a negative response to most questions, reflecting consumers’ sentiment that the economy is in bad shape and will continue to be so. This interpretation is supported by the correlation of with the news-based uncertainty index, which tracks the proportion of news that contain terms related to uncertainty. The probability of assignment to this ‘pessimism’ profile decreases when times are good in the economy and negative news is less available. In contrast, Type 3 can be understood as a recovery profile since the respondents believe they will likely be better off a year from now, in spite of a reasonably high probability that they have experienced bad times recently. This type is associated with turning points in unemployment. Estimating more complex forms of heterogeneity beyond an aggregate index is important for identifying and interpreting predominant types of beliefs among respondents to the Michigan survey and how these types relate to aggregate economic conditions.

5.2 Heterogeneous Beliefs and Returns to Education

In this subsection, we illustrate how the class assignments can be used to control for unobserved heterogeneity in subsequent regressions. It is well known that unobserved characteristics that are correlated with observed covariates will introduce bias in parameter estimates. With panel data, time-invariant characteristics can be controlled for by differencing or demeaning. These options are not available with cross-sectional data, and instrumental variable estimation is often used. Our approach is to use a high-dimensional set of auxiliary categorical information to control for omitted variable bias and to estimate interpretable heterogeneous effects in a parsimonious way.

Our application concerns estimating returns to education, and education research relies heavily on surveys that solicit subjective assessments. Using data from the National Longitudinal Survey of Young Men from 1966 to 1976, we consider the regression model

| (5) |

where is the outcome variable (income), is a covariate of interest (education), is a small set of important controls, is unobserved heterogeneity, and is not observed directly. , but . The parameter of interest is the return to education for the men in the sample. In Card (1995), includes covariates such as region, race, ability test scores, and parental education, and proximity to college is then used as an instrument, orthogonal to , to estimate returns to education .

We consider a scenario where a convincing instrumental variable is not available, but we have some auxiliary information about the qualitative beliefs of an individual to control for unobserved heterogeneity in belief type and to estimate heterogeneous effects that are based on an individual’s belief type. Our approach uses elements from Kasahara and Shimotsu (2009) and Bonhomme, Lamadon, and Manresa (2017). However, we not only cluster the data, but also give an economic interpretation to the latent class. We parameterize as a function of individual’s belief type:

We further assume that the slope parameters also depend on belief type, so that

Though is not observed, we can estimate these latent class probabilities if additional data on an individual’s beliefs are available. In addition to traditional economic questions on income and education, the U.S. National Longitudinal Survey asks other qualitative questions on beliefs and values. There are in fact hundreds of categorical variables available in the NLSYM survey waves that were not used in Card (1995). Therefore, in the first step, we estimate a model that allows the probabilities of class membership to vary by groups. In a second step we use the LDA-S posterior probabilities of membership in each belief type to generate an individual specific intercept, and interact type membership with the slope parameters. In a third step, returns to education are estimated by least squares regression of

| (6) |

where . If the belief type assignment provides a good proxy for the omitted variable , then the bias on should be reduced, and will be eliminated entirely if the belief type captures any relationship that has with , or with .

To illustrate, we use 2,830 of the original 3,010 men from Card (1995) who have Rotter questionnaire data available. We include (i) 11 variables from the 1976 survey wave that are part of the Rotter questionnaire, a locus of control psychological questionnaire that determined whether or not people believe individual choices determine outcomes or if external factors were to blame. We also include (ii) an additional 3 variables from the 1966 survey, on attitudes about high school and high school courses. It would be difficult to include all of these variables directly in the regression to measure heterogeneous effects without some method of clustering individuals, since the dimensionality of 14 categorical variables with many different response categories is high. LDA-S overcomes this problem since the information in the categorical variables for an individual is now summarized into interpretable belief type probabilities, which are low in dimension.

We estimate an LDA-S model with , where individuals are grouped by the four possible combinations of having a library card interacted with having a single mother at age 14. Table 1 contains the results for a replication of Card (1995)’s most basic OLS specification in column (1), as well as the results from estimating Equation 4 in column (2). The mean return to education does not change materially when an individual’s belief type is added as a control, which suggests that the estimated belief types are not affecting the bias of the OLS coefficient in this setting. This is similar to what is found in Card (1995), where the OLS coefficient changes little as additional controls are added beyond the basic specification.

However, there is meaningful heterogeneity in returns to education across belief types. The expected return to education for an individual with belief type 1 is 5.7%, while the return of an individual with belief type 2 is 7.9%. To interpret these differences, we examine . In Figure 5, we plot the posterior means of for the three questions that vary the most between belief type 1 and belief type 2, as measured by the Rao distance (see Rao (1945)), between and . Responses 1 and 2 to the survey questions are responses labelled ‘most internal’ and indicate the individual believes success is a matter of internal drive, persistence, and leadership ability. Responses 3 and 4 are labelled ‘most external’, and correspond to individuals believing success is a matter of luck, status, or other factors outside your control. Individuals assigned to type 1, who have higher mean income but lower returns to education, have absorbed information that has caused them to believe that work ethic and inherent ability leads to success with a higher probability than individuals assigned to type 2. This result is intuitive; individuals who believe that work ethic is important are more likely to make other choices that result in their success with or without a formal education, and so have a lower return to education than individuals who believe external factors determine their success.

The information that an individual absorbs and incorporates into their beliefs can be an important determinant of their economic choices and outcomes. Examining the returns to education for individuals surveyed in the NLSYM, we do not find evidence that controlling for an individual’s belief type reduces bias in the estimate of the mean return to education. However, we do find that belief types correspond to heterogeneous returns to education in a very intuitive way. Analyzing heterogeneity in qualitative beliefs can lead to important insights on the variation in the impact of education on economic outcomes.

6 Conclusion

This paper proposes a Bayesian hierarchical latent class approach to modeling categorical survey responses. We motivate the statistical model using an economic model of information acquisition. We illustrate using two applications how the estimated belief types can be useful in economic analysis of categorical survey data.

While traditional face-to-face and telephone surveys have declined, surveys can now be easily conducted through the internet and mobile phones. For example, web-based surveys have become an effective way to gauge various types of consumers sentiments during the covid19 pandemic. As Callegaro and Yang (2018) noted, Survey Monkey alone generates 90 million surveys per month worldwide. One can expect more data of this type to be available. LDA-S can be useful for interpreting and characterizing heterogeneity in such data. Given the close relation of LDA-S to the extensive computer science and statistics literature on mixed membership models, a variety of extensions are possible, including more complex forms of dynamics as in Fox and Jordan (2013), or integrating latent variable estimates in more complex causal analyses as suggested in Wang and Blei (2018).

For clarity and focus, the paper has used language, motivation, and applications appropriate for categorical survey data on beliefs. However, there are many other examples of categorical survey data that are used by economists and social scientists. For example, indicators of ownership of assets and housing characteristics from, for example, the Demographic and Health Surveys (DHS) and Living Standard Measurement Surveys (LSMS) are often the only source of data from which to build social and economic indicators to guide policies. The economic structural model used to derive and interpret LDA-S for qualitative beliefs data can be modified appropriately for other types of economic categorical data. LDA-S can be further extended within the mixed-membership framework to allow for more complex forms of dynamics as in Fox and Jordan (2013), or integrating latent variable estimates in more complex causal analyses as suggested in Wang and Blei (2018).

| Dependent variable: | ||

| LWAGE76 | LWAGE76 | |

| (1) | (2) | |

| BLACK | 0.187∗∗∗ | 0.182∗∗∗ |

| (0.018) | (0.018) | |

| EXP76 | 0.081∗∗∗ | 0.079∗∗∗ |

| (0.007) | (0.008) | |

| EXP762 | 0.216∗∗∗ | 0.208∗∗∗ |

| (0.034) | (0.038) | |

| SMSA76R | 0.168∗∗∗ | 0.167∗∗∗ |

| (0.016) | (0.016) | |

| REG76R | 0.125∗∗∗ | 0.127∗∗∗ |

| (0.016) | (0.016) | |

| ED76 | 0.072∗∗∗ | 0.074∗∗∗ |

| (0.004) | (0.004) | |

| Z1 | 0.24∗∗ | |

| (0.114) | ||

| Z2 | 0.084 | |

| (0.106) | ||

| ED76:Z1 | 0.0165∗ | |

| (0.009) | ||

| ED76:Z2 | 0.0053 | |

| (0.008) | ||

| Observations | 2,830 | 2,830 |

| R2 | 0.282 | 0.284 |

| Note: | ∗p0.1; ∗∗p0.05; ∗∗∗p0.01 | |

References

- (1)

- Airoldi, Blei, Erosheva, and Feinberg (2015) Airoldi, E., D. Blei, E. Erosheva, and S. Feinberg (eds.) (2015): Handbook of MIxed Membership Models and Their Applications, Chapman and Hall/CRC Handbooks of Modern Statistical Methods. CRC Press.

- Airoldi, Blei, Fienberg, and Xing (2008) Airoldi, E., D. Blei, S. Fienberg, and E. Xing (2008): “Mixed Membership Stochastic Blockmodels,” Journal of Machine Learning Research, 9, 1981–2014.

- Airoldi, Fienberg, Joutard, and Love (2006) Airoldi, E. M., S. E. Fienberg, C. Joutard, and T. M. Love (2006): “Discovering latent patterns with hierarchical Bayesian mixed-membership models and the issue of model choice,” in In Data Mining Patterns: New Methods and Applications. Citeseer.

- Anandkumar, Foster, Hsu, Kakade, and Liu (2012) Anandkumar, A., D. P. Foster, D. J. Hsu, S. M. Kakade, and Y.-K. Liu (2012): “A Spectral Algorithm for Latent Dirichlet Allocation,” in Advances in Neural Information Processing Systems, pp. 917–925.

- Bandiera, Hansen, Prat, and Sadun (2020) Bandiera, O., S. Hansen, A. Prat, and R. Sadun (2020): “CEO Behavior and Firm Performance,” Journal of Political Economy, 128:4, 1325–1369.

- Bartoš, Bauer, Chytilová, and Matějka (2016) Bartoš, V., M. Bauer, J. Chytilová, and F. Matějka (2016): “Attention discrimination: Theory and field experiments with monitoring information acquisition,” American Economic Review, 106(6), 1437–75.

- Bhadury, Chen, Zhu, and Liu (2016) Bhadury, A., J. Chen, J. Zhu, and S. Liu (2016): “Scaling Up Dynamic Topic Models,” in Proceedings of the 25th International Conference on World Wide Web, pp. 381–390.

- Blei, Ng, and Jordan (2003) Blei, D., A. Y. Ng, and M. I. Jordan (2003): “Latent Dirichlet Allocation,” Journal of Machine Learning Research, 3, 993–1022.

- Blei, Kucukelbir, and McAuliffe (2017) Blei, D. M., A. Kucukelbir, and J. D. McAuliffe (2017): “Variational Inference: A Review for Statisticians,” Journal of the American Statistical Association, 112(518), 859–877.

- Blei and Lafferty (2006) Blei, D. M., and J. D. Lafferty (2006): “Dynamic Topic Models,” in Proceedings of the 23rd International Conference on Machine Learning, pp. 113–120.

- Bonhomme, Lamadon, and Manresa (2017) Bonhomme, S., T. Lamadon, and E. Manresa (2017): “Discretizing Unobserved Heterogeneity,” Discussion paper, Becker Friedman Institute for Economics no. 2019-16.

- Bradley, Holan, and Wikle (2018) Bradley, J. R., S. H. Holan, and C. K. Wikle (2018): “Computationally Efficient Multivariate Spatio-Temporal Models for High-Dimensional Count-Valued Data,” Bayesian Analysis, 13(1), 253–310.

- Branch (2004) Branch, W. A. (2004): “The theory of rationally heterogeneous expectations: evidence from survey data on inflation expectations,” The Economic Journal, 114(497), 592–621.

- Buntine (2002) Buntine, W. (2002): “Variational Extensions to EM and Multinomial PCA,” in Machine Learning: ECML: Lecture Notes in Computer Science, vol. 2430. Springer, Berlin.

- Buntine and Jakulin (2012) Buntine, W., and A. Jakulin (2012): “Applying Discrete PCA in Data Analysis,” arXiv:1207.4124.

- Callegaro and Yang (2018) Callegaro, M., and Y. Yang (2018): “The Role of Surveys in the Era of Big Data,” in The Palgrace Handbook of Survey Research, pp. 175–192. Palgrave Macmillan.

- Canny (2004) Canny, J. (2004): “GaP: A Factor Model for Discrete Data,” in Proceedings of the 27th Annual International ACM SIGIR Conference on Research and Development in Information Retrieval, pp. 122–129.

- Caplin and Dean (2015) Caplin, A., and M. Dean (2015): “Revealed preference, rational inattention, and costly information acquisition,” American Economic Review, 105(7), 2183–2203.

- Card (1995) Card, D. (1995): “Using geographic variation in college proximity to estimate the return to schooling,” in Aspects of Labor Market Behavior: Essays in Honour of John Vanderkamp, pp. 201–222.

- Carlson and Parkin (1975) Carlson, J. A., and M. Parkin (1975): “Inflation expectations,” Economica, 42(166), 123–138.

- Carroll (2003) Carroll, C. D. (2003): “Macroeconomic expectations of households and professional forecasters,” the Quarterly Journal of economics, 118(1), 269–298.

- Catania and Mari (2020) Catania, L., and R. D. Mari (2020): “Hierarchical Markov Switching Models for Multivariate Integer-Valued Time Series,” Journal of Econometrics, Forthcoming.

- Davidson, Rutstein, Kiersten, Eldow, Wagstaff, and Amouzou (2007) Davidson, R. G., S. Rutstein, J. Kiersten, S. Eldow, A. Wagstaff, and A. Amouzou (2007): “Socio-Economic Differences in Health, Nutrition, and Population Within Developing Countries,” HNP, The World Bank.

- Ding, Li, and Peng (2006) Ding, C., T. Li, and W. Peng (2006): “Nonnegative Matrix Factorization and Probabilistic Latent Semantic Indexing: Equivalence, Chi-Square Statistic, and a Hybrid Method,” in AAAI Proceedings of the 21st National Confererence on Artificial Intelligence, pp. 342–347, Boston, Massachusetts.

- Dominitz and Manski (2004) Dominitz, J., and C. F. Manski (2004): “How Should We Measure Consumer Confidence?,” The Journal of Economic Perspectives, 18(2), 51–66.

- Draca and Schwarz (2020) Draca, M., and C. Schwarz (2020): “How Polarized are Citizens? Measuring Ideology from the Ground-Up,” mimeo, University of Warwick.

- Erosheva (2002) Erosheva, E. (2002): “Grade of Membership and Latent Structures with Application to Disability Survey Data,” Ph.D Thesis, Department of Statistics, Carneige Mellon University.

- Erosheva, Fienberg, and Lafferty (2004) Erosheva, E., S. Fienberg, and J. Lafferty (2004): “Mixed-membership models of scientific publications,” Proceedings of the National Academy of Sciences, 101, 5220–5227.

- Erosheva, Fienberg, and Joutard (2007) Erosheva, E. A., S. E. Fienberg, and C. Joutard (2007): “Describing Disability Through Individual-Level Mixture Models for Multivariate Binary Data,” The Annals of Applied Statistics, 1(2), 502–537.

- Falush, Stephens, and Pritchard (2003) Falush, D., M. Stephens, and J. Pritchard (2003): “Inference of Population Structure Using Multilocus Genotype Data: Linked Loci and Correlated Allele Frequencies,” Genetics, 164:4, 1567–1587.

- Filmer and Pritchett (2001a) Filmer, D., and L. Pritchett (2001a): “Estimating Wealth Effects Without Expenditure Data- Or Tears: An Application to Educational Enrollments in States of India,” Demography, 38:1, 115–132.

- Filmer and Pritchett (2001b) Filmer, D., and L. H. Pritchett (2001b): “Estimating Wealth Effects Without Expenditure Data - or Tears,” Demography, 38(1), 115–132.

- Fox and Jordan (2013) Fox, E. B., and M. I. Jordan (2013): “Mixed membership models for time series,” arXiv preprint arXiv:1309.3533.

- Gillis (2014) Gillis, N. (2014): “The Why and How of Nonnegative Matrix Factorization,” in Regularization, Optimization, Kernels, and Support Vector Machines: Learning and Pattern Recognition Series, pp. 257–291. Chapman and Hall/CRC.

- Goodman (1974) Goodman, L. (1974): “Exploratory Latent Structure Analysis Using Both Identifiable and Unidentifiable Models,” Biometrika, 61(2), 215–231.

- Goodman (1979) (1979): “On the Estimation of Parameters in Latent Structure Analysis,” Psychometrika, 44(1), 123–128.

- Griffiths and Steyvers (2007) Griffiths, T., and M. Steyvers (2007): “Topics in Semantic Representation,” Pyschological Review, 114(2), 211–244.

- Gross and Manrique-Vallier (2014) Gross, J. H., and D. Manrique-Vallier (2014): “A Mixed Membership Approach to Political Ideology,” in Handbook of Mixed Membership Models and its Applications, pp. 119–141. Chapman and Hall/CRC.

- Hansen, McMahon, and Prat (2018) Hansen, S., M. McMahon, and A. Prat (2018): “Transparency and Deliberation within the FOMC: A Computational Linguistics Approach,” Quarterly Journal of Economics, 133(2), 801–870.

- Hoffmann (1999) Hoffmann, T. (1999): “Probabilistic Latent Semantic Analysis,” Proceedings of the 15th Annual Conference on Uncertainty in Artificial Intelligence, pp. 289–296.

- Hofmann (2001) Hofmann, T. (2001): “Unsupervised Learning by Probabilistic Latent Semantic Analysis,” Machine Learning, 42, 177–196.

- Hoyer (2004) Hoyer, P. (2004): “Nonnegative Matrix Factorization with Sparseness Constraints,” Journal of Machine Learning Research, 5, 1457–1469.

- Huang, Sidiropoulous, and Swami (2014) Huang, K., N. Sidiropoulous, and A. Swami (2014): “Non-negative Matrix Factorization Revisited: Uniqueness and Algorithm for Symmetric Decomposition,” IEEE Transations of Signal Processing, 62:1, 211–224.

- Jasra, Holmes, and Stephens (2005) Jasra, A., C. C. Holmes, and D. Stephens (2005): “Markov Chain Monte Carlo Methods and the Label Switching Problem in Bayesian Mixture Modeling,” Statistical Science, 20, 50–67.

- Kasahara and Shimotsu (2009) Kasahara, H., and K. Shimotsu (2009): “Nonparametric Identification of Finite Mixture Models of Dynamic Discrete Choices,” Econometrica, 77(1), 135–175.

- Ke, Montiel-Olea, and Nesbitt (2019) Ke, S., J. Montiel-Olea, and J. Nesbitt (2019): “A Robust Machine Learning Algorithm for Text Analysis,” Working paper.

- Kolenikov and Angeles (2009) Kolenikov, S., and G. Angeles (2009): “Socioeconomic Status Measurement With Discrete Proxy Variables: Is Principal Component Analysis A Reliable Answer?,” Review of Income and Wealth, 55(1), 128–165.

- Lazarsfeld (1950) Lazarsfeld, P. (1950): “The Logical and Mathematical Foundation of Latent Structure Analysis,” in Measurement and Prediction, vol. 14, pp. 362–412.

- Linderman, Johnson, and Adams (2015) Linderman, B. S. W., M. J. Johnson, and R. P. Adams (2015): “Dependent Multinomial Models Made Easy: Stick Breaking with the Polya-Gamma Augmentation,” arXiv:1506.05843.

- Lovaton, McCarthy, Kirdruang, Sharma, and Gondwe (2014) Lovaton, D., A. McCarthy, P. Kirdruang, U. Sharma, and D. Gondwe (2014): “Water, Walls, and Bicycles: Wealth Index Composition Using Census Microdata,” Minnesota Population Center Working Paper 2014-7.

- Manski (2004) Manski, C. F. (2004): “Measuring Expectations,” Econometrica, 72(5), 1329–1376.

- Masyn (2013) Masyn, K. (2013): “Latent Class Analysis and Finite Mixture Modeling,” in The Oxford Handbook of Quantitative Methods, pp. 551–609.

- McHugh (1956) McHugh, R. (1956): “Efficient Estimation and Local Identification in Latent Class Analysis,” Psychometrika, 21(4), 331–347.

- Moench, Ng, and Potter (2013) Moench, E., S. Ng, and S. Potter (2013): “Dynamic Hierarchical Factor Models,” Review of Economics and Statistics, 95(5), 1811–1817, Columbia University, mimeo.

- Moussaoui, Brie, and Idier (2005) Moussaoui, S., D. Brie, and J. Idier (2005): “Non-Negative Source Separation: Range of Admissible Solutions and Conditions for Uniqueness of the Solution,” Proceedings of IEEE International Conference on Acoustic, Speech, and Signal Processing.

- Ng (2015) Ng, S. (2015): “Constructing Common Factors from Continuous and Categorical Data,” Econometric Reviews, 34(6-10), 1141–1171.

- Pesaran (1985) Pesaran, M. H. (1985): “Formation of inflation expectations in British manufacturing industries,” The Economic Journal, 95(380), 948–975.

- Pesaran and Weale (2006) Pesaran, M. H., and M. Weale (2006): “Survey expectations,” Handbook of economic forecasting, 1, 715–776.

- Pritchard, Stephens, and Donnelly (2000) Pritchard, J., M. Stephens, and P. Donnelly (2000): “Inference of Population Structure Using Multilocus Genotype Data,” Genetics, 155, 945–959.

- Rao (1945) Rao, C. R. (1945): “Information and the Accuracy Attainable in the Estimation of Statistical Parameters,” in Breakthroughs in Statistics, pp. 235–247. Springer.

- Ruiz, Athey, Blei, et al. (2020) Ruiz, F. J., S. Athey, D. M. Blei, et al. (2020): “Shopper: A probabilistic model of consumer choice with substitutes and complements,” Annals of Applied Statistics, 14(1), 1–27.

- Shiller, Kon-Ya, and Tsutsui (1996) Shiller, R. J., F. Kon-Ya, and Y. Tsutsui (1996): “Why did the Nikkei crash? Expanding the scope of expectations data collection,” The Review of Economics and Statistics, pp. 156–164.

- Vyas and Kumaranayake (2006) Vyas, S., and L. Kumaranayake (2006): “Constructing Socio-Economic Status Indices: How to use Principal Components,” Health and Policy Planning, 21(6), 459–468.

- Wang and Blei (2018) Wang, Y., and D. M. Blei (2018): “The blessings of multiple causes,” arXiv preprint arXiv:1805.06826.

- Welling and Teh (2011) Welling, M., and Y. W. Teh (2011): “Bayesian Learning via Stochastic Gradient Langevin Dynamics,” in Proceedings of the 28th International Conference on International Conference on Machine Learning, pp. 681–688.

- Wittenberg and Leibbrandt (2017) Wittenberg, M., and M. Leibbrandt (2017): “Measuring Inequality By Asset Indices: A General Approach with Application to South Africa,” Review of Income and Wealth, 63:4, 706–730.

- Woodbury, Clive, and Jr. (1978) Woodbury, M., J. Clive, and A. G. Jr. (1978): “Mathematical Typology: A Grade of Membership Technique for Obtaining Disease Definition,” Computers and Biomedical Research, 11, 277–298.