Chen, Krishnamurthy and Wang

Robust Dynamic Assortment Optimization

Robust Dynamic Assortment Optimization in the Presence of Outlier Customers

Xi Chen \AFFStern School of Business, New York University, New York, NY 10012, \EMAILxchen3@stern.nyu.edu \AUTHORAkshay Krishnamurthy \AFFMicrosoft Research NYC, New York, NY 10011, \EMAILakshay.krishnamurthy@microsoft.com \AUTHORYining Wang \AFFWarrington College of Business, University of Florida, Gainesville, FL 32611, \EMAILyining.wang@warrington.ufl.edu

We consider the dynamic assortment optimization problem under the multinomial logit model (MNL) with unknown utility parameters. The main question investigated in this paper is model mis-specification under the -contamination model, which is a fundamental model in robust statistics and machine learning. In particular, throughout a selling horizon of length , we assume that customers make purchases according to a well specified underlying multinomial logit choice model in a -fraction of the time periods, and make arbitrary purchasing decisions instead in the remaining -fraction of the time periods. In this model, we develop a new robust online assortment optimization policy via an active elimination strategy. We establish both upper and lower bounds on the regret, and show that our policy is optimal up to logarithmic factor in when the assortment capacity is constant. We further develop a fully adaptive policy that does not require any prior knowledge of the contamination parameter . In the case of the existence a sub-optimality gap between optimal and sub-optimal products, we also established gap-dependent logarithmic regret upper bounds and lower bounds in both the known- and unknown- cases. Our simulation study shows that our policy outperforms the existing policies based on upper confidence bounds (UCB) and Thompson sampling.

Dynamic assortment optimization, gap-dependent analysis, regret analysis, robustness, active elimination

1 Introduction

A wide range of operations problems, ranging from assortment optimization to supply chain management, are built on an underlying probabilistic model. When real world outcomes follow this model, existing optimization techniques are able to provide accurate solutions. However, these model assumptions are only abstractions of reality and do not perfectly capture the sophisticated natural environment. In other words, these models are inherently mis-specified to a certain degree. Accordingly, model mis-specification and robust estimation have been an important topic in the statistics literature (Huber and Ronchetti 2011). However, this literature primarily focuses on estimation or prediction from a given dataset, which is insufficient for modern operations settings where decision making plays a vital role. Unfortunately, most decision-making policies are derived from optimization problems that explicitly rely on the probabilistic model, so they are inherently not robust to model mis-specification. Can we design robust policies for these operations problems?

This paper studies model mis-specification for an important problem in revenue management — dynamic assortment optimization, under a popular -contamination model (which will be introduced in the next paragraph). Assortment optimization has a wide range of applications in retailing and online advertising. Given a large number of substitutable products, the assortment optimization problem involves selecting a subset of products (a.k.a., an assortment) to offer a customer such that the expected revenue is maximized. To model customers’ choice behavior when facing a set of offered products, discrete choice models have been widely used, and one of the most popular such models is the multinomial logit model (MNL) (McFadden 1974). In dynamic assortment optimization, the customers’ choice behavior (e.g., mean utilities of products in an MNL) is not known a priori and must be learned online, which is often the case in practice, as historical data is often insufficient (e.g., fast fashion sale or online advertising). More specifically, the seller offers an assortment to each arriving customer for a finite time horizon , observes the purchase behavior of the customer and then updates the utility estimate. The goal of the seller is to maximize the cumulative expected revenue over periods. Due to its practical relevance, dynamic assortment optimization has received much attention in literature. (Caro and Gallien 2007, Rusmevichientong et al. 2010, Saure and Zeevi 2013, Agrawal et al. 2019, 2017).

All of these existing works assume that each arriving customer makes her purchase according to an underlying choice model. Yet, in practice, a small fraction of customers could make “outlier” purchases. To model such outlier purchases, we adopt a natural robust model in the statistical literature — the -contamination model (Huber 1964), which dates back to the 1960s and is perhaps the most widely used model in robust statistics. In the general setup of the -contamination model, we are given i.i.d. samples drawn from a distribution , where denotes the distribution of interest , parameterized by (e.g., a Gaussian distribution with mean ), and is an arbitrary contamination distribution. The parameter , which is usually very small, reflects the level at which contamination occurs, so a larger value means more observations are contaminated. The standard objective is to identify or estimate the parameter of the distribution of interest, in the presence of corrupted observations from . For the purpose of dynamic assortment optimization in the presence of outlier customers, the distribution represents the choice model for the majority of customers, which are “typical,” (with being the parameter of an underlying MNL choice model of interest), while the distribution corresponds to choice models of “outlier” customers and reflects the proportion of outlier customers. For dynamic assortment optimization, we also deviate from the standard parameter estimation objective and focus on designing online decision-making policies.

In the classical -contamination model, the “outlier distribution” stays stationary for all samples, To make the contamination model more practical in the online assortment optimization setting, we strengthen the model from two aspects:

-

1.

Instead of assuming a fixed corruption distribution for all outlier customers, we allow to change over different time periods (i.e., is the outlier distribution for customers at time period );

-

2.

Instead of assuming that each time is corrupted “uniformly at random”, we assume that outlier customers appear in at most time periods. The purchase pattern and arrivals of outlier customers can, however, be arbitrary and even adaptive to the assortment decisions or customer purchase activities prior to time period . The corrupted time periods and associated ’s are unknown to the seller.

This setting is much richer than the “random arrival setting” and more realistic in practice. Indeed, in a holiday season, consecutive time periods might contain anomalous or outlier purchasing behavior, which cannot be capture by “random corruption” in the original -contamination model. The details of our outlier customer model will be rigorously specified in Section 3.

The main goal of the paper is to develop a robust dynamic assortment policy under this -contaminated MNL. Our first observation is that popular policies in the literature including Upper-Confidence-Bounds (UCB) (Agrawal et al. 2019) and Thompson sampling (Agrawal et al. 2017) no longer work in this model. The reason is that these policies cannot use typical customers that arrive later in the selling period to correct for misleading customers that arrive early on, and hence even a small number of outlier customers can lead to poor performance. Further, while it is well known that randomization is crucial in any adversarial setting (see, e.g., Auer et al. (2002), Bubeck and Cesa-Bianchi (2012)) to hedge against outliers, UCB is a deterministic policy, while Thompson sampling provides very little randomization via posterior sampling. We explain these failures in more detail in Secs. 3 and 7 later in this paper.

To address the contaminated setting, we develop a novel active elimination algorithm for robust dynamic planning, which gradually eliminates those items that are not in the optimal assortment with high probability (see Algorithm 1). Compared to the existing methods mentioned above (Agrawal et al. 2019, 2017), our active elimination method has several important technical novelties. First, our active elimination policy implements the randomization in a much more explicit way by sampling from a carefully constructed small set of “active” products. Second, the existing UCB and Thompson sampling algorithms for MNL rely on an epoch-based strategy (i.e., repeatedly offering the same assortment until no purchase) to enable an unbiased estimation of utility parameters. This procedure is inherently fragile since the stopping time of an epoch relies on a single no-purchase activity, which can be easily manipulated by outlier customers; a few outliers can greatly affect the stopping times. The failure of such an epoch-based strategy implies that unbiased estimation of utility parameters is no longer possible. To overcome this challenge, we propose a new utility estimation strategy based on geometrically increasing offering time periods. We conduct a careful perturbation analysis to control the bias of these estimates, which leads to new confidence bounds for our active elimination algorithm (see Sec. 4 for more details).

We provide theoretical guarantees for our proposed robust policy via regret analysis and information-theoretic lower bounds. In particular, let be the selling horizon, the total number of products, and the cardinality constraint of an assortment (see Sec. 3). For the reasonable setting where is not too large, our active elimination algorithm (Algorithm 1) achieves regret when (or a reasonable upper bound of ) is known (see Theorem 4.1), where only suppresses factors. Compared to the lower bound (see Proposition 4.2), our upper bound is tight up to polynomial factors involving and other logarithmic factors. We also remark that the special case of reduces to the existing setting studied in (Agrawal et al. 2019, 2017, Chen and Wang 2018) in which no outlier customers are present. Compared to existing results, our regret bound is tight except for an additional factor, which represents the cost of being adaptive to outlier customers (see Sec. 4.2 for more discussions). We emphasize that in a typical assortment optimization problem, the capacity of an assortment is usually a small constant, especially relative to and .

The above result assumes that an upper bound on the outlier proportion is given as prior knowledge. While in some cases we may be able to estimate from historical data, this is not always possible, which motivates the design of fully adaptive policies that do not require as an input. Inspired by the “multi-layer active arm race” from the multi-armed bandits literature (Lykouris et al. 2018), we propose an adaptive robust dynamic assortment optimization policy in Algorithm 3. Our policy runs multiple “threads” of known- algorithms on a geometric grid of values in parallel, and, as we show, achieves regret, where suppresses and factors (see Theorem 5.1). Here, the (cumulative) regret is defined as the sum of the differences between the expected rewards (revenues) of the optimal assortment and the assortments the retailer offers at each time period. Algorithm 3 and its analysis in Sec. 5 provide more details.

Finally, in the case of well-separated problem instances (i.e. there is a large sub-optimality gap between optimal and sub-optimal assortments), built on the same proposed algorithm, we establish much improved regret upper bounds of when is known (see Theorem 6.2). When is unknown, the adaptive policy achieves the regret or , whichever is smaller (see Theorem 6.6). For both upper bounds in the well-separated case, the dependency on the time horizon is logarithmic when the corruption level is small. We also prove lower bounds on the regret when a sub-optimality gap of at least exists.

The rest of the paper is organized as follows. Sec. 2 introduces the related work. Sec. 3 describes the problem formulation. The first active elimination policy and the regret bounds are presented in Sec. 4, while the adaptive algorithm is presented in Sec. 5. The gap dependent regret analysis and -type regret bounds are provided in Sec. 6. Numerical illustration are provided in Sec. 7 with the conclusion in Sec. 8. The proof the lower bound result is provided in the appendix. Proofs of some technical lemmas are relegated to the supplementary material.

2 Related works

Static assortment optimization with known choice behavior has been an active research area since the seminal works by van Ryzin and Mahajan (1999) and Mahajan and van Ryzin (2001). Motivated by fast-fashion retailing, dynamic assortment optimization, which adaptively learns unknown customers’ choice behavior, has received increasing attention in the context of data-driven revenue management. The work by Caro and Gallien (2007) first studied dynamic assortment optimization problem under the assumption that demands for different products are independent. Recent works by Rusmevichientong et al. (2010), Saure and Zeevi (2013), Agrawal et al. (2019, 2017), Chen and Wang (2018), Wang et al. (2018) incorporated MNL models into dynamic assortment optimization and formulated the problem as an online regret minimization problem. In particular, for the standard MNL model, Agrawal et al. (2019) and Agrawal et al. (2017) developed UCB and Thompson sampling based approaches for online assortment optimization. Moreover, some recent work (Cheung and Simchi-Levi 2017, Chen et al. 2018, Oh and Iyengar 2019) study dynamic assortment optimization based on contextual MNL models, where the utility takes the form of an inner product between a feature vector and the coefficients. The present work focuses on the standard non-contextual MNL model, but a natural direction for future work is to extend our results to the contextual setting.

All works outlined above assume an underlying MNL choice model is correctly specified. However, model mis-specification is common in practice, and robust statistics, one of the most important branches in statistics, is a natural tool to address such mis-specification. The -contamination model, which was proposed by P. J. Huber (Huber 1964), is perhaps the most widely used robust model and has recently attracted much attention from the machine learning community (see, e.g., Chen et al. (2016), Diakonikolas et al. (2017, 2018) and reference therein). Despite this attention, online learning in the -contamination model or its generalizations is relatively unexplored. In the online setting, Esfandiari et al. (32018) studied online allocation under a mixing adversarial and stochastic model but the setting does not require any learning component. For online learning, the recent works of Lykouris et al. (2018), Gupta et al. (2019) studied the contaminated stochastic multi-armed bandit (MAB), but, due to the complex structure of discrete choice models, these results do not directly apply to our setting. Indeed, a straightforward analogy between assortment optimization and MAB is to treat each feasible assortment as an arm, but directly using this mapping will result in a large regret due to the exponentially many possible assortments.

In learning and decision-making settings, a few recent work investigate the impact of model mis-specification in revenue management, e.g., Cooper et al. (2006) for capacity booking problems and Besbes and Zeevi (2015) for dynamic pricing. In particular, Besbes and Zeevi (2015) show that a class of pricing policies based on linear demand functions perform well even when the underlying demand is not linear. Cooper et al. (2006) also identified some cases where simple decisions are optimal under mis-specification. However, our setting is quite different, as the widely used UCB and Thompson sampling policies are not robust under our model. On the other hand, our new active-elimination policy is robust to model mis-specification and additional achieves near-optimal regret when the model is well-specified.

3 Problem formulation

There are items, each associated with a known revenue parameter and an unknown utility parameter . At each time a customer arrives, for a total of time periods. The retailer then provides an assortment to the customer, subject to a capacity constraint . The customer then chooses at most one item to purchase, upon which the retailer collects a revenue of . If the customer chooses to purchase nothing (denoted by ), then the retailer collects no revenue.

At each time , the arriving customer is assumed to be one of the following two types:

-

1.

A typical customer makes purchases according to a multinomial-logit (MNL) choice model

(1) We assume that ;

-

2.

An outlier customer makes purchases according to an arbitrary unknown distribution (marginalized on ). can potentially change with .

We note that the MNL model in Eq. (1) together with the constraint that implies that “no purchase” is the most probable (or equally probable) outcome for a typical customer. This assumption has been made in operations literature, see, e.g., Agrawal et al. (2017). Such an assumption that for all is, however, only for the ease of presentation, and the assumption can be easily relaxed to for some known constant upper bound . With the relaxed boundedness condition, one can enlarge the constructed confidence intervals (see the definition in Algorithm 1) by multiplying a factor, and the other parts of our analysis/algorithms remain the same.

We consider the following -contamination model:

-

(A1)

(Bounded adversaries). The number of outlier customers throughout time periods does not exceed , where is a problem parameter;

-

(A2)

(Adaptive adversaries). The choice model for an outlier customer at time can be adversarially and adaptively chosen, based on the previous customers, offered assortments, and past purchasing activity.

A rigorous mathematical formulation is as follows: For any time period , let be the indicator variable of whether customer at time is an outlier ( if customer is an outlier and otherwise), be the assortment provided at time , be the purchasing activity of the customer. The protocol is formally defined as follows:

Definition 3.1 (Definition of protocol)

We define the following:

-

1.

An adaptive adversary consists of arbitrary measurable functions , where produces the type of the customer (typical or outlier) and the outlier distribution at time period , from the filtration ;

-

2.

An admissible policy consists of random functions , where produces a randomized assortment , at time period , from the filtration ;

-

3.

If then is realized according to model (1) conditioned on ; otherwise if then is realized according to model .

The objective of the retailer is to develop an admissible dynamic assortment optimization strategy that is competitive with a certain “benchmark” assortment. Unlike the classical setting, the definition of regret is a bit more complicated due to the presence of both typical and adversarial customers. To shed light on the subtle differences between different benchmark assortments, in this paper we consider two different types of cumulative regret, as introduced below. To simplify notations we use to denote the customer’s choice model at time . More specifically, is the “typical” model in Eq. (1) (denoted as ) if a typical customer arrives at time , and if an outlier customer arrives at time . We use to denote the expected revenue collected by offering assortment if the customer’s choice model is modeled by .

-

1.

The Typically-Optimal-Typically-Evaluated () regret is defined as

(2) where is the optimal assortment for typical customers;

-

2.

The Best-In-Hindsight () regret is defined as

(3)

The -regret uses the optimal assortment for typical customers as the benchmark. Furthermore, the -regret is always measured in the difference of expected revenue on typical customers, regardless of whether a typical or an outlier customer is present at time . On the other hand, the -regret measures the performance differences on the actual choice model of the incoming customers. In other words, it compares the performance of the dynamic assortment planning algorithm with the optimal assortment on both typical and outlier customers. The -regret also coincides with the “best stationary benchmark” regret considered in most fully adversarial multi-armed bandit problems.

There is an important relationship between these two definitions of regret, as characterized in the following statement.

Fact 1

.

Proof 3.2

Let be the optimal assortment for typical customers and be the assortment attaining the maximum in the definition of . Note that during time periods that , the . During time periods that , we have , because the expected revenue of any assortment under any choice model is at most one by normalization. Since there are outlier time periods, we have that .

Fact 1 shows that the difference between the -regret and the -regret is at most . Therefore, we shall focus solely on the -regret in terms of the upper bound, which always exhibits an additive term in the bounds. Such an upper bound implies the same regret bound for , up to a term of . For the lower bound, we consider the -regret which is standard in the literature.

4 An active-elimination policy

To motivate our policy, we first briefly explain why the popular Upper-confidence-bounds (UCB) and Thompson sampling fail in the presence of outlier customers. These algorithms are designed for the uncontaminated setting where , so the confidence bounds (in UCB policies) and posterior updates (in Thompson sampling policies) are designed under the assumption that all customers follow the same MNL model. Unfortunately, in the presence of outlier customers the confidence intervals are too narrow and the posterior updates are too aggressive. With these update strategies, a small number of outlier customers preferring items unpopular to typical customers could “swing” the algorithms’ parameter estimates, which can lead to the belief that these unpopular items are actually popular. This subsequently leads to poor exploration of the popular items, which eventually hurts performance. As a numerical demonstration, we construct a concrete setting in Sec. 7 where the performance of UCB and Thompson sampling policies degrades considerably in the presence of outlier customers.

We propose an active-elimination policy for dynamic assortment optimization in the presence of outlier customers. A pseudo-code description is given in Algorithm 1. While Algorithm 1 requires the knowledge of (or an upper bound , see Theorem 4.1) as input, we emphasize that such requirement can be completely removed by designing more complex policies, as we will show in Sec. 5. To highlight our main idea, we state Algorithm 1 upfront as the prior knowledge of simplifies both the algorithm and its analysis.

At a high level, Algorithm 1 operates in epochs with geometrically increasing lengths, and only performs item estimation or assortment updates between epochs. At any time , the algorithm maintains an active set of items consisting of all items that could potentially form a “good” assortment, and estimates of parameters for all active items in . For each time period in a single epoch , a random item is sampled from the current active item set and a “near-optimal” assortment is built, which must contain the target item . Once an epoch ends, parameter estimates of are updated and the active set is shrunk based on the updated estimates to exclude sub-optimal items. We will ensure that with high probability, the optimal assortment is always a subset of active sets for all epochs (see Lemma 4.6).

We now detail all notation used in Algorithm 1:

-

-

: the indices of epochs whose lengths increase geometrically ();

-

-

: the estimates of preference parameters (of typical customers) at epoch ;

-

-

: the subset of active items, which are to be explored uniformly at random in epoch ;

-

-

(see step 6): the estimated expected revenue of the optimal assortment calculated based on the active item subset and current preference estimates ;

-

-

(see step 5): an optimal assortment computed based on and , which must include the specific item ; this assortment is used to explore and estimate the the utility parameter of item ;

-

-

(see step 12): counters used in the estimate of ; note that for any supplied assortment , we only record the number of times a customer purchases item (accumulated by ), and the number of times a customer makes no purchases (accumulated by ); other purchasing activities (e.g., purchases of an item other than ) will not be recorded;

-

-

: length of confidence intervals used to eliminate items from ; its length depends on both the epoch index and the prior knowledge of the outlier proportion ;

In the rest of the section, we first give a brief description of how to compute in Line 5 efficiently. Then we detail the regret upper bound of Algorithm 1 and provide the the proof.

4.1 Solving the optimization problem

The implementation of most steps of Algorithm 1 is straightforward, except for the computation of the assortments , which require futher algorithmic development. This computation can be formulated as the following combinatorial optimization problem:

| (4) |

for a specific . This optimization problem is similar to the classical capacity-constrained assortment optimization (see, e.g., Rusmevichientong et al. (2010)), but the additional constraint in (4) yields a subtle difference. For the purpose of completeness, we provide an efficient optimization method with binary search for solving Eq. (4). Pseudo-code is provided in Algorithm 2.

For any , we want to check whether there exists , , such that , or equivalently . Re-organizing the terms, we only need to check whether there exists , such that . Because must hold, we only need to check whether there exists , such that

| (5) |

This can be accomplished by including all with the largest positive values of into the set of and check whether Eq. (5). If Eq. (5) holds, the current revenue value of can be obtained and otherwise the current value of cannot be obtained. We then solve the optimization problem by a standard binary search on . We also note that in Line 6 is a standard static capacitated assortment optimization, which can be solved efficiently (see Rusmevichientong et al. (2010)).

4.2 Regret analysis

The following theorem is our main regret upper bound result for Algorithm 1.

Theorem 4.1

Suppose and . Then there exists a universal constant such that, for sufficiently large , the -regret of Algorithm 1 is upper bounded by

Furthermore, if holds then the regret upper bound can be simplified to

| (6) |

To complement Theorem 4.1, we state the following proposition establishing some lower bounds for the different types of regret considered in this paper.

Proposition 4.2

Let be a universal constant and be any admissible policy. Suppose also .

-

1.

The -regret of on worst-case problem instances are at least ;

-

2.

For suppose there are outlier customers. Then the -regret of on worst-case problem instances is lower bounded by at least .

The first property of Proposition 4.2 is proved by simply setting and using existing lower bound results for dynamic assortment planning with no outlier customers (see, e.g., Chen and Wang (2018)). The proof of the second property is achieved by considering the two terms and separately. The complete proof of Proposition 4.2 is given in the supplementary material.

The claims in Proposition 4.2 leads to a challenging open problem on the -regret upper bound when , at which time the term would dominate the term (see Eq. (6)). In such cases, we conjecture that the optimal regret upper bounds would be , implying that our current result in Theorem 4.1 is sub-optimal when is very large. The question of achieving regret upper bound for all levels requires fully adversarial bandit algorithms for dynamic assortment optimization, which is very challenging and an open question as far as we know.

An important special case of Theorem 4.1 is , which reduces to the well-studied dynamic assortment optimization problem without outlier customers. For such settings, Agrawal et al. (2017, 2019) give algorithms with a regret upper bound of , which matches the lower bound of given in (Chen and Wang 2018) up to poly-logarithmic terms. Comparing their results to Theorem 4.1, we observe that our result at matches the regret bound except for an additional term of . This factor stems from our active elimination protocol and our technique for estimating the utility parameters, both of which are essential for handling outlier customers when . We believe removing this factor is technically quite challenging, and leave it as an interesting open question. We also note that the capacity constraint is typically a very small constant in practice, and hence an additional term is likely negligible.

Our regret upper bound in Theorem 4.1 also yields meaningful guarantees when is not zero. For example, with , meaning that out of customers are outliers, Theorem 4.1 provides an regret upper bound. This guarantee is non-trivial because it is sub-linear in , although it is larger than the standard bound for the uncontaminated setting. Thus, Theorem 4.1 reveals the trade-off and impact of a small proportion of outlier customers on the performance of dynamic assortment optimization algorithms/systems.

4.3 Proof sketch of Theorem 4.1

In this section we sketch the proof of Theorem 4.1. Key lemmas and their implications are given, while the complete proofs of the presented lemmas are deferred to the supplementary material accompanying this paper.

We first state a lemma that upper bounds the estimation error :

Lemma 4.3

Suppose and . With probability it holds for all satisfying and that , where

| (7) |

where is defined as , and .

Lemma 4.3 shows that, with high probability, the estimation error between and , the true preference parameter of item for typical customers, can be upper bounded by which is a function of , , , and . It should be noted that the definition of involves unknown quantities (mostly ) and hence cannot be directly used in an algorithm. The definition of in Algorithm 1, on the other hand, involves only known quantities and estimates. In Corollary 4.5, we will establish the connection between and .

Our next lemma derives how the estimated expected revenue deviates from the true value by using upper bounds on the estimation errors between and :

Lemma 4.4

For any , and , it holds that

The proof uses only elementary algebra.

Combining Lemmas 4.3 and 4.4, we show that the quantities defined in our algorithm serve as valid upper bounds on the estimation error between and :

Corollary 4.5

Our next lemma is an important structural lemma which states that, with high probability, any item in the optimal assortment is never excluded from active item sets for all epochs .

Lemma 4.6

If then with probability it holds that for all .

This structural lemma yields two important consequences: first, since “good” items remain within the active item subsets , each of the assortments computed at step 5 of Algorithm 1 will have relatively high expected revenue. Second, the fact that implies that the optimistic estimates will always be based on the expected revenue of the actual optimal assortment . This justifies the elimination step 7 in which we discard all items whose best assortment has significantly lower revenue than .

The proof of Lemma 4.6 is based on an inductive argument, which shows that if belongs to at the beginning of every epoch , then any item in will not be removed (with high probability) by step 7. The intuition for this is that the optimal assortment containing any is itself, whose revenue cannot be to far away from due to Lemmas 4.3 and 4.4. The complete proof of Lemma 4.6 is provided in the supplementary material.

Finally, our last technical lemma upper bounds the per-period regret incurred by Algorithm 1.

Lemma 4.7

Suppose holds for all . Then with probability , for every and , it holds that .

Given the established technical lemmas, we are now ready to give the proof of Theorem 4.1.

Proof 4.8

Let be the smallest integer such that . For all epochs , the induced cumulative regret can be upper bounded by

| (8) |

In the rest of this proof we upper bound the regret incurred from epochs . By Lemma 4.7, the regret incurred by a single time period in epoch is upper bounded by with high probability. The total regret accumulated in epoch is then upper bounded by . Hence, the regret accumulated on the entire time periods is upper bounded by

| (9) | |||

| (10) | |||

| (11) |

Here in Eq. (10), we apply Cauchy-Schwartz inequality. The final inequality holds because .

5 Adaptation to unknown outlier proportion

In this section we describe a more complex algorithm for robust dynamic assortment optimization where the outlier proportion is unknown a priori. Inspired by the “multi-layer active arm race” for multi-armed bandits, due to Lykouris et al. (2018), Algorithm 3 runs multiple “threads” of known- algorithms on a geometric grid of values in parallel, while carefully coordinating between the threads. The pseudo-code of the proposed adaptive algorithm is given in Algorithm 3.

We note that for two threads , we have , which implies that the confidence interval length is typically longer than . Therefore, the thread is less aggressive than the thread in terms of eliminating items, i.e., an item eliminated by thread may remain active in thread . More detailed explanations of key steps in Algorithm 3 are summarized below:

-

1.

Independence of threads: different threads , which correspond to different hypothetical values of (denoted as ), are largely independent from each other, maintaining their own parameter estimates , active item set and confidence intervals . Coordination among threads only appear in two steps in Algorithm 3: Step 8, which maintains a hierarchical “nested” structure of the active item sets among the threads, and Step 15, which provides update rules for by comparing the obtained optimistic assortment among different threads. Further details are given in subsequent bullets.

-

2.

Heterogeneous sampling of different threads: at each time period when a potential customer arrives, a random thread is selected to provide assortments. The random thread, however, is not selected uniformly at random but according to a specifically designed distribution, with the probability of selecting thread equals . Intuitively, such a sampling distribution “favors” the more aggressive threads with smaller hypothetical values.

This sampling scheme is motivated by the fact that threads with larger values typically incur large regret, because their elimination rules are conservative, so many sub-optimal items remain active for many rounds. The probability of choosing these threads with large values should be small to ensure low regret of the overall policy.

At the same time, threads corresponding to smaller values might also incur large regret, as their overly aggressive elimination rule might remove the optimal assortment from consideration. To avoid large regret from these threads, Step 15 coordinates amongst all of the threads and checks for inconsistencies, as we describe in the next bullet.

-

3.

Coordination and interaction among threads: as we mentioned in the first bullet, the coordination and interaction among different threads only happen in Steps 8 and 15 in Algorithm 3. In this bullet we discuss these two steps in detail.

Step 8 aims at maintaining a “nested” structure among the active subsets , such that for any at any epoch . We remark that such a nested structure should be expected even without this step, because thread is less aggressive than thread , in the sense that confidence intervals is typically longer than . Hence, one should expect that thread has a larger active set. Nevertheless, due to stochastic fluctuations such nested structures might be violated. Therefore, we explicitly enforce a nesting structure at the start of every epoch via Step 8.

Step 15 is a statistical test that tries to detect whether is small relative to the actual (unknown) outlier proportion . This test crucially ensures that we do not continue to select an overly aggressive thread, which, as we have mentioned, may incur large regret due to eliminating the optimal assortment . Step 15 detects such events by evaluating the optimistic assortment using the information from threads , which use less aggressive elimination rules. In detail, we check if the optimistic assortment is near optimal using the utility estimates and confidence intervals from thread . If the check fails and we see that is suboptimal, we know that thread has eliminated the optimal assortment from its active set , which subsequently lead to the conclusion that is too small. Then we terminate the current thread and restart the algorithm with .

We also remark on the time complexity of Algorithm 3. There are values on the -grid. At each time period , a thread is chosen. Then at most combinatorial optimization problems are solved and each combinatorial optimization takes time. Therefore, the total time complexity of the proposed algorithm is .

In the rest of this section we state our regret upper bound result for the adaptive Algorithm 3, as well as a sketch of its proof.

5.1 Regret analysis and proof sketch

We establish the following regret upper bound for Algorithm 3. We note that all the regret mentioned in this section is the -regret.

Theorem 5.1

Remark 5.2

In the statement of Theorem 5.1, means for some universal constant . For notational simplicity we did not work out the exact constant in the expression of .

The complete proof of Theorem 5.1 as well as the proofs of technical lemmas are relegated to the supplementary material. Here we sketch the key steps in the proof. The first step is the following lemma, which shows that for threads with , the optimal assortment is never removed from their active item sets with high probability.

Lemma 5.3

With probability it holds for all and that .

Lemma 5.3 is similar in spirit to the structural results established in Lemma 4.6 for Algorithm 1, but it is only applicable to thread with The remaining threads, with are too aggressive in their elimination strategy, so we cannot guarantee that for all . We will see how to upper bound the regret from these threads later in this section.

Our next lemma analyzes the Step 15 of the algorithm:

Lemma 5.4

If then with probability , Algorithm 3 will not be re-started.

At a high level, Lemma 5.4 states if step 15 is triggered (which causes and a re-start of the entire algorithm), the smallest hypothetical value must be below the actual value of . First, this ensure that the algorithm does not restart too often, but more importantly, it guarantees that the actual always falls between and throughout the entire selling period.

The proof of Lemma 5.4 is based on Lemma 5.3. In particular, the condition in Step 15 of Algorithm 3 compares the optimistic assortments in thread with estimates in threads , which have larger values. If, hypothetically, is larger than or equal to , then by Lemma 5.4, we know that for all , and therefore the estimated optimality of should be consistent in all threads . Hence, any inconsistency detected by step 15 must imply that , which justifies decreasing .

We now present two lemmas that upper bound the regret accumulated by different threads, which requires some new notation. For , let denote the cumulative regret incurred during the time periods in which thread is run. Clearly, the total regret incurred is upper bounded by . Using linearity of the expectation, it then suffices to upper bound for every . The next two lemmas provide these upper bounds for two different scenarios. For notational simplicity we use to hide factors.

Lemma 5.5

For all satisfying , .

Lemma 5.6

For all satisfying and any , it holds that

These two lemmas upper bound the total accumulated regret of threads , separately for the case of and . The case of is relatively straightforward to prove, since as shown in Lemma 5.3, so an argument similar to the proof of Theorem 4.1 applies. On the other hand, the case of is more difficult because might be eliminated in these threads. For Lemma 5.6, which considers this case, we carefully analyze the stopping rule in Step 15, essentially showing that the check in Step 15 will trigger as soon as the regret per-time period is too high for these threads. The complete proofs of both lemmas, as well as the complete proof of Theorem 5.1, are deferred to the supplementary material.

6 Instance gap-dependent analysis

Recall that is the optimal assortment. For any given item , let be the optimal assortment containing the specific item . Define the sub-optimality “gap” as

| (12) |

Intuitively, the sub-optimality gap defined in Eq. (12) measures how “well-defined” the optimal assortment is, in the sense that the inclusion of any non-optimal item would result in at least a drop of in expected revenue/reward, regardless of how other products in the assortment are selected. If a problem instance has a large sub-optimality gap parameter , it implies that the optimal assortment is easier to learn (since non-optimal products are easier to be ruled out) and therefore smaller cumulative regret is expected.

It is also worthwhile to compare the gap parameter defined in Eq. (12) with those defined in earlier works. In the work of Rusmevichientong et al. (2010), a non-parametric gap is defined as

where . It is clear that a strictly positive implies that all utility parameter are distinct. On the other hand, it is easy to construct problem instances with duplicate parameters (indicating that some products have the same utility/popularity for incoming customers) and zero , while our defined sub-optimality gap could still be strictly positive. Indeed, consider the following problem instance with products and capacity constraint, with and . It is easy to verify that in this problem instance , while .

In the remainder of this section, we will use the concept of sub-optimality gap defined in Eq. (12) to improve our regret upper bounds in Theorems 4.1 and 5.1, resembling type gap-dependent regret bounds in stochastic mutli-armed bandits. Both our Algorithms 1 and 3 remain unchanged, while the regret analysis is modified to take into consideration the parameter.

6.1 Gap-dependent analysis of Algorithm 1 (known corruption level)

We first consider Algorithm 1 designed for the setting in which a good upper bound on the true corruption level is known. The following lemma is the key lemma in the gap-dependent setting:

Lemma 6.1

Let be defined in Eq. (12) and suppose . Then with probability , for every epoch satisfying

| (13) |

for some universal constant , it holds that .

We note that in (13), is an upper bound estimate of . At a high level, Lemma 6.1 states that if is sufficiently large, the active product set only consists of the optimal assortment for typical customers . Intuitively, this is because when is large, the confidence bound is much shorter. When the confidence interval cannot cover the underlying sub-optimality gap , the non-optimal products will be automatically eliminated. A complete proof of Lemma 6.1 is given in the supplementary material.

With Lemma 6.1, we can prove the following theorem on gap-dependent regret upper bounds for Algorithm 1 with a known upper bound on .

Theorem 6.2

We remark that the term in the second term in the regret upper bound most likely arises from the doubling epochs used in our proposed active elimination algorithms, where the total number of epochs could be logarithmic in . It is an interesting open technical question to further improve the second term in (14) to be linear in , which should be possible at least in the case of (or its suitable upper bound ) being known.

6.2 Gap-dependent analysis of Algorithm 3 (unknown corruption level)

When the corruption level is unknown and no good estimate is available a priori, Algorithm 3 partitions the possible corruption levels into a logarithmic grid and runs Algorithm 1 on different levels of in parallel. To analyze its regret performance from a gap-dependent perspective, we again discuss the two cases of and separately.

In the case of (i.e., over-estimating the true corruption level ), Lemma 5.3 shows that with high probability the optimal assortment will not be removed from . Subsequently, Lemma 6.1 can be directly applied, with a union bound on the failure probability over , , as the following corollary:

Corollary 6.3

For and epoch recall the definitions that and , where is the sampling probability for thread and is the “normal” length epoch . Let be the smallest integer such that satisfies Eq. (13), or more specifically

| (15) |

where is a universal constant. Then for all , .

Subsequently, Lemma 5.5 leads to the following corollary:

Corollary 6.4

For all satisfying , , where is defined in Corollary 6.3.

We next consider the case of . Because the constraint is enforced in Algorithm 3 all the time, we know that implies with probability 1. Consequently, Lemma 5.6 implies the following:

Corollary 6.5

For all satisfying and any , it holds that where is defined in Corollary 6.3 for thread .

With Corollaries 6.3, 6.4 and 6.5 in place, we are ready to state our gap-dependent analysis for Algorithm 3 with unknown corruption level .

Theorem 6.6

Remark 6.7

An alternative upper bound of can also be proved, which could be larger or smaller than the one presented in Theorem 6.6 depending on the values of and .

Comparing Theorem 6.6 with Theorem 6.2, we notice an additional term in either the or the term in Theorem 6.2. Such a worsened dependency likely arises from the layered approach taken to address unknown values, which also delivered sub-optimal regret guarantees (compared to when is known a priori) in robust multi-armed bandit problems (Lykouris et al. 2018, Gupta et al. 2019).

6.3 A lower bound on gap-dependent regret

We complement our gap-depednent regret upper bound results in the previous sections by stating a lower bound on gap-dependent regret in dynamic assortment optimization with outlier customers.

Theorem 6.8

Let be constants independent of , satisfying and . Suppose also that can potentially change with , and that , . Then for sufficiently large , the worst-case -regret of any admissible policy is lower bounded by

where is a universal constant independent of and .

Remark 6.9

The lower bound result in Theorem 6.8 assumes the algorithm has full knowledge of the corruption level .

Remark 6.10

As Theorem 6.8 only concerns the -regret, a similar lower bound for the -regret can be established. More specifically, the lower bound in Proposition 4.2 still applies, because there is no additional constraints/assumptions imposed on outlier customers. Furthermore, the lower bound in Theorem 6.8 is obtained by simply setting , which applies to the -regret notion too. Hence, a lower bound of can be established for the -regret in the gap-dependent setting.

Comparing Theorem 6.8 to Theorem 6.2 (our regret upper bound with knowledge of ), we notice that the term matches the term in Theorem 6.8 up to polynomial dependency on and . As discussed in the works of Agrawal et al. (2019, 2017), in revenue management applications the capacity constraint is usually very small and therefore treated as a constant. On the other hand, there is a gap between the term in the upper bound and the term in the lower bound, particularly when is relatively large compared to . We are at the moment unsure which one is tight. However, in order for the lower bound to be tight, it requires fully-adversarial algorithms for dynamic assortment optimization, which has already been an open question as discussed before. Finally, the lower bound in Theorem 6.8 assumes the knowledge of the corruption level . The lower bound for cases when is unknown is significantly more complicated and could involve whether the upper bounds are tight in terms and the distinction between regret and pseudo-regret notions (Lykouris et al. 2018), which is out of the scope of this paper.

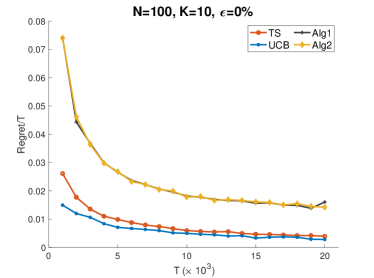

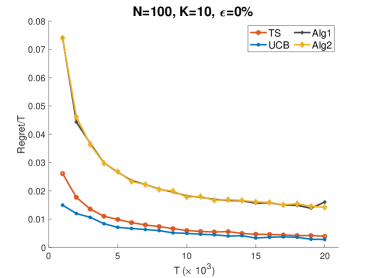

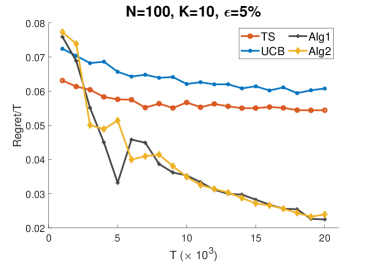

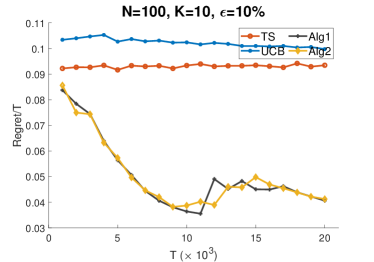

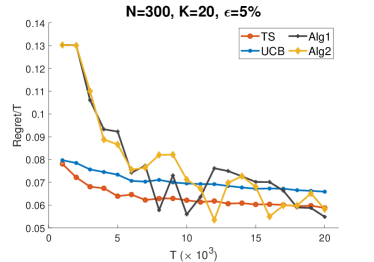

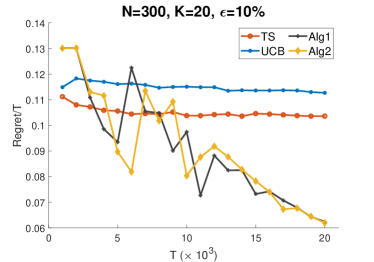

7 Numerical illustration

In this brief experimental section, we provide some numerical illustrations that demonstrate the robustness of our proposed policy and the benefits over existing non-robust approaches for dynamic assortment optimization, including Thompson Sampling (TS) (Agrawal et al. 2017) and Upper Confidence Bounds (UCB) (Agrawal et al. 2019). We construct the following data instance:

-

1.

out of items have revenue parameters and preference parameters ;

-

2.

For the other items, both their revenue and preference parameters are uniformly distribution on ;

-

3.

For the first time periods, the arriving customers are outliers with choice models , where is an MNL-parameterized choice model with preference parameters set as if and otherwise.

This instance reflects two important properties of outlier customers in practice, namely that they have significantly different preferences from typical customers, and that they arrive in consecutive time periods (e.g., during a holiday season). In particular, the instance consists of items with very high revenue, but very low preference parameters so that few customers will buy them. Under normal circumstances, a dynamic assortment optimization algorithm would identify the unpopularity of these items very quickly and stop recommending them. However, as the outlier customers prefer these items over the others, these items appear popular and profitable in the early time periods, which may mislead the algorithm. As these algorithms are highly unpopular in the latter time periods, a robust algorithm should not be severely impacted by these outlier customers.

For the baseline methods, the TS method is tuning-free with a non-informative prior on each item. For the UCB algorithm, we find the value in the multiplier () when constructing upper confidence bands that gives the best performance (in the original paper of Agrawal et al. (2019) for theoretical purposes). Each method is run for 100 independent trials and the mean average regret (i.e., the cumulative regret over ) is reported. The standard deviation of all the methods are sufficiently small and thus omitted for better visualization.

In Figure 1, we report the results for all methods under various settings of and . The experimental settings are chosen as , , and ranging from to . From Figure 1, we can see that when is strictly greater than 0, our proposed algorithms will stabilize at a mean regret level (0.02 to 0.06) that is much lower than the non-robust TS and UCB methods. More importantly, the average regret (i.e., cumulative regret divided by ) for our method decreases as a function of the time horizon, a phenomenon that does not happen for TS/UCB, especially when is large. This confirms that these latter two methods are not robust to outlier customers, and further confirms the effectiveness of our proposed algorithms for robust dynamic assortment optimization. For the no contamination case of , while our proposed algorithms perform slightly worse than the baselines, the decreasing rates of average regrets are the same. When there is no contamination, although the main term in our regret is still tight, there might be extra overhead in the regret bound through dependency on and factors.

8 Conclusions and Future Work

In this paper, we extend the -contamination model from statistics to the online decision-making setting and study the dynamic assortment optimization problem with outlier customers. We propose a new active elimination policy that is robust to adversarial corruptions and establish a near-optimal regret bound. We further develop an adaptive policy that does not require any prior knowledge of the corruption proportion .

The first interesting problem is to sharpen upper and lower regret bounds in the gap-dependent case. Moreover, it is technically interesting to further extend the paper to the fully adversarial MNL bandit setting. Beyond this technical question, we hope that this work inspires future work on model mis-specification in revenue management, which we believe is a practically important research direction. We look forward to pursuing this direction in future work.

References

- Agrawal et al. (2019) Agrawal S, Avadhanula V, Goyal V, Zeevi A (2019) MNL-bandit: A dynamic learning approach to assortment selection. Operations Research 67(5):1453–1485.

- Agrawal et al. (2017) Agrawal S, Avandhanula V, Goyal V, Zeevi A (2017) Thompson sampling for MNL-bandit. Proccedings of the Conference on Learning Theory (COLT).

- Auer (2002) Auer P (2002) Using confidence bounds for exploitation-exploration trade-offs. Journal of Machine Learning Research 3(Nov):397–422.

- Auer et al. (2002) Auer P, Cesa-Bianchi N, Freund Y, Schapire RE (2002) The nonstochastic multiarmed bandit problem. SIAM Journal on Computing 32(1):48–77.

- Auer and Ortner (2010) Auer P, Ortner R (2010) Ucb revisited: Improved regret bounds for the stochastic multi-armed bandit problem. Periodica Mathematica Hungarica 61(1-2):55–65.

- Besbes and Zeevi (2015) Besbes O, Zeevi A (2015) On the (surprising) sufficiency of linear models for dynamic pricing with demand learning. Management Science 61(4):723–739.

- Bubeck and Cesa-Bianchi (2012) Bubeck S, Cesa-Bianchi N (2012) Regret analysis of stochastic and nonstochastic multi-armed bandit problems. Foundations and Trends in Machine Learning 5(1):1–122.

- Caro and Gallien (2007) Caro F, Gallien J (2007) Dynamic Assortment with Demand Learning for Seasonal Consumer Goods. Management Science 53(2):276–292.

- Chen et al. (2016) Chen M, Gao C, Ren Z (2016) A general decision theory for huber’s -contamination model. Electronic Journal of Statistics 10(2):3752–3774.

- Chen and Wang (2018) Chen X, Wang Y (2018) A note on tight lower bound for mnl-bandit assortment selection models. Operations Research Letters 46(5):534–537.

- Chen et al. (2018) Chen X, Wang Y, Zhou Y (2018) Dynamic assortment optimization with changing contextual information. arXiv preprint arXiv:1810.13069 .

- Cheung and Simchi-Levi (2017) Cheung WC, Simchi-Levi D (2017) Thompson sampling for online personalized assortment optimization problems with multinomial logit choice models. Available at SSRN: https://papers.ssrn.com/?abstract_id=3075658 .

- Cooper et al. (2006) Cooper WL, de Mello TH, Kleywegt AJ (2006) Models of the spiral-down effect in revenue management. Operations Research 54(5):968–987.

- Diakonikolas et al. (2018) Diakonikolas I, Kamath G, Kane D, Li J, Moitra A, Stewart A (2018) Robustly learning a gaussian: Getting optimal error, efficiently. Proceedings of the ACM-SIAM Symposium on Discrete Algorithms.

- Diakonikolas et al. (2017) Diakonikolas I, Kamath G, Kane DM, Li J, Moitra A, Stewart A (2017) Being robust (in high dimensions) can be practical. Proceedings of the Interational Conference on Machine Learning.

- Esfandiari et al. (32018) Esfandiari H, Korula N, Mirrokni V (32018) Allocation with traffic spikes: Mixing adversarial and stochastic models. ACM Transactions on Economics and Computation 6(3–4):1–23.

- Even-Dar et al. (2006) Even-Dar E, Mannor S, Mansour Y (2006) Action elimination and stopping conditions for the multi-armed bandit and reinforcement learning problems. Journal of Machine Learning Research 7(Jun):1079–1105.

- Freedman (1975) Freedman DA (1975) On tail probabilities for martingales. The Annals of Probability 3(1):100–118.

- Gupta et al. (2019) Gupta A, Koren T, Talwar K (2019) Better algorithms for stochastic bandits with adversarial corruptions. Proceedings of the Conference on Learning Theory.

- Huber (1964) Huber PJ (1964) Robust estimation of a location parameter. The Annals of Mathematical Statistics 35(1):73–101.

- Huber and Ronchetti (2011) Huber PJ, Ronchetti EM (2011) Robust Statistics. Series in Probability and Statistics (Wiley).

- Lykouris et al. (2018) Lykouris T, Mirrokni V, Leme RP (2018) Stochastic bandits robust to adversarial corruptions. Proceedings of the ACM Symposium on Theory of Computing (STOC).

- Mahajan and van Ryzin (2001) Mahajan S, van Ryzin G (2001) Stocking retail assortments under dynamic consumer substitution. Operations Research 49:334–351.

- McFadden (1974) McFadden D (1974) Conditional logit analysis of qualitative choice behavior. Frontiers in Econometrics (Academic Press).

- Oh and Iyengar (2019) Oh MH, Iyengar G (2019) Multinomial logit contextual bandits. Reinforcement Learning for Real Life (RL4RealLife) Workshop in the International Conference on Machine Learning (ICML).

- Rusmevichientong et al. (2010) Rusmevichientong P, Shen ZJ, Shmoys D (2010) Dynamic assortment optimization with a multinomial logit choice model and capacity constraint. Operations Research 58(6):1666–1680.

- Saure and Zeevi (2013) Saure D, Zeevi A (2013) Optimal dynamic assortment planning with demand learning. Manufacturing & Service Operations Management 15(3):387–404.

- van Ryzin and Mahajan (1999) van Ryzin G, Mahajan S (1999) On the relationships between inventory costs and variety benefits in retail assortments. Management Science 45:1496–1509.

- Wang et al. (2018) Wang Y, Chen X, Zhou Y (2018) Near-optimal policies for dynamic multinomial logit assortment selection models. Proceedings of Advances in Neural Information Processing Systems (NeurIPS).

Supplementary Material: Additional Proofs

9 Proofs of the lower bounds

9.1 Proof of Proposition 4.2

Proposition 9.1 (restated)

There exists a universal constant such that, for any policy , its worst-case regret for problem instances with customers, items, assortment capacity constraint and outlier customers () is lower bounded by .

Proof 9.2

It suffices to prove that the maximum regret of the worst-case problem of any is lower bounded by , because . An lower bound has already been established in (Chen and Wang 2018) wit no outlier customers. Hence to prove Proposition 4.2 we only need to establish an regret lower bound.

Consider two problem instances and with shared revenue parameters and different preference parameters (for typical customers) , , such that for any assortment , , , where and are the optimal assortments under and , respectively. The existence and explicit construction of such problem instances can be found in (Chen and Wang 2018). Now consider the case in which all of the first customers are outliers, associated with the same outlier choice model under both and . Because the choice model of the outlier customers are the same, no algorithm can distinguish from during the first time periods with success probability larger than . Therefore, the worst-case regret (under and ) of any algorithm is at least , which is to be demonstrated.

10 Proofs of technical lemmas for Theorem 4.1

10.1 Proof of Lemma 4.3

Lemma 10.1 (restated)

Suppose and . With probability it holds for all satisfying and that , where

| (16) |

where is defined as , and .

Proof 10.2

Denote and let be the consecutive time periods during which assortments , are offered uniformly at random. Let also be the set of all time periods at epoch . For each and , define indicator variable if is offered at time and the no-purchase action is taken from the incoming customer, and otherwise. Similarly, define if is offered at time and the purchase of item , , is observed from the incoming customer. We then have, by definition, that,

| (17) |

Recall the definition that . Let and be the time periods corresponding to typical and outlier customers, respectively. The expectation of can subsequently be calculated as

Note that since at time is selected uniformly at random, the events “ is offered at time ” and “customer arriving at time is an outlier” are independent, which is crucial in the above derivation. Define . It is clear by definition that . Furthermore, because at most customers are outliers throughout the entire time periods, we know that and hence . Subsequently, we have

| (18) |

Similarly, for we have

| (19) |

where which also satisfies .

It is easy to verify that the partial sums form martingales where the filtration is , for both , because the decision of whether customer is an outlier is independent from the event . The variances of and (conditioned on the assortments offered in epoch ) can also be upper bounded as and . Subsequently, invoking Bernstein’s inequality (Lemma 15.1) with , and for , for , we have that

where

Let us now consider the case of . then admits the form of

Additionally, by Hoeffding’s inequality, it also holds that

| (20) |

Because , and with probability , we have that (with probability and a union bound)

Provided that

In the case of the definition of only decreases . A union bound over all and completes the proof of Lemma 4.3.

10.2 Proof of Lemma 4.4

Lemma 10.3 (restated)

For any , and , it holds that

Proof 10.4

Expanding the definitions of and , we have

10.3 Proof of Corollary 4.5

Corollary 10.5 (restated)

For every and , , conditioned on the success events on epochs up to , it holds that , where is defined in Algorithm 1.

Proof 10.6

Note that it suffices to prove the first inequality, because is a monotonically increasing function in . Also, we only need to consider the case of , as otherwise which trivially upper bounds . Invoking Lemma 4.4 and the upper bound in Lemma 4.3, we have (recall the definition that )

Here in the third inequality we use Cauchy-Schwarz inequality on ; more specifically, , as and , so that .

10.4 Proof of Lemma 4.6

Lemma 10.7 (restated)

If then with probability it holds that for all .

Proof 10.8

We use induction to prove this lemma. Let be the smallest integer such that . Because , the lemma clearly holds for . Next, conditioned on , we will prove that with probability .

Let be the solution of step (*) in Algorithm 1. If , then and hence . This means that . If , then because . If , we have

where the first inequality holds by Corollary 4.5, and the last inequality holds by monotonicity of . In both cases, it holds that

| (21) |

For any , let be the solution of () of Algorithm 1. Because by the induction hypothesis, we know that is a feasible solution to the optimization question of and therefore

| (22) |

Combining Eqs. (21,22) we have (with high probability) that , and hence . Repeat the argument for all we have proved that with high probability.

10.5 Proof of Lemma 4.7

Lemma 10.9 (restated)

Suppose holds for all . Then with probability , for every and , it holds that .

Proof 10.10

Because , we know that . Additionally, because , we have that with probability by invoking Corollary 4.5. Subsequently,

which is to be demonstrated.

11 Proofs of technical lemmas of Theorem 5.1

First, note that if , the term in Theorem 5.1 will be dominated by the term and is therefore not important. Hence, throughout the rest of this section we shall assume without loss of generality that , which also means that in the beginning.

11.1 Proof of Lemma 5.3

Lemma 11.1 (restated)

With probability it holds for all and that .

Proof 11.2

Because each thread is sampled at random with probability , the expected total number of outlier customers thread encounters is upper bounded by . Hence, by Bernstein’s inequality and the union bound, for , with probability at least the total number of outlier customers thread encounters is upper bounded by . In the rest of this proof, we will consider instead of merely , which only adds multiplicative factors to the regret bound in Theorem 5.1. With such considerations, for all satisfying , Lemma 4.3 and Corollary 4.5 in the previous proof of Theorem 4.1 would remain valid.

The rest of the proof is quite similar to the proof of Lemma 4.6, except we have to take into consideration the effect of Step 8 of Algorithm 3. The proof is again done via induction: at the first epoch we have and the lemma clearly holds. Now assume the lemma holds for some , we want to prove for all .

Fix arbitrary and assume by way of contradiction that . Then there exists such that . Additionally, because is the maximizer of for all , , it holds that . Let also be the assortment attaining (i.e., ). Then, invoking Corollary 4.5, we have with probability that

leading to the desired contradiction.

11.2 Proof of Lemma 5.4

Lemma 11.3 (restated)

If then with probability , Algorithm 3 will not be re-started.

Proof 11.4

We only need to prove that, if , then for any time period , the condition at step 14 of Algorithm 3 is satisfied with probability at most . Invoking Lemma 5.3, we know that with high probability holds for all and . Additionally, by algorithm design it is always guaranteed that for any , and therefore implies . Subsequently, invoking Corollary 4.5 we have with probability that

| (23) |

Since , by the construction of we know that . Let also be the assortment attaining (i.e., ). Then invoking Corollary 4.5 again, we have with probability that

| (24) |

Here Eq. (*) holds because . Combining Eqs. (23) and (24), we have

| (25) |

where the last inequality holds because by definition. On the other hand, with being the assortment attaining (i.e., ) and the fact that , invoking Corollary 4.5 we have with probability that

| (26) |

Combining Eqs. (25) and (26) we have with probability that

which is to be demonstrated.

11.3 Proof of Lemma 5.5

Lemma 11.5 (restated)

For all satisfying , .

Proof 11.6

Because , by Lemma 5.3 we know that for all with high probability. Then, invoking Lemma 4.7, the regret incurred by thread in a single time period is upper bounded by . Because thread is sampled with probability , the expected number of time periods thread is performed is . This completes the proof of Lemma 5.5.

11.4 Proof of Lemma 5.6

Lemma 11.7 (restated)

For all satisfying and any , it holds that

Proof 11.8

Fix arbitrary . According to step 14 of Algorithm 1, because the value of does not decrease, we must have for all assortments explored by thread in epoch . Because , we know that with high probability, and using the same argument as in the proof of Lemma 4.7 we have with high probability that

which serves as an upper bound of the regret thread incurs in a single time period it is performed. Therefore,

which is to be demonstrated.

11.5 Proof of Theorem 5.1

Because we restart Algorithm 3 whenever is reduced, and Lemma 5.4 shows that (with high probability) always holds. Note that it is possible for the value of to be far smaller than the actual outlier proportion . In the rest of this section we shall assume without loss of generality that, throughout a consecutive of time periods the value of does not change, and furthermore . The total regret over these time periods multiplying would then be an upper bound on the total regret over the entire time periods.

We first consider the regret incurred by thread with . By Lemma 5.5, the regret incurred by such a thread in epoch can be upper bounded by , because . Replacing by in the definition of , we have that

| (27) |

On the other hand, because of the sampling protocol in Algorithm 3 we have that

| (28) |

Subsequently,

| (29) |

Using Cauchy-Schwarz inequality and the concavity of , we have

| (30) |

Note that , where the last inequality holds because thanks to Lemma 5.4. Combining this fact with Eqs. (29,30), we have that

| (31) |

We next consider regret incurred by threads with . Let be the largest integer such that . Then by Lemma 5.6, the regret incurred by thread in epoch is upper bounded by

where the inequality holds because by definition. Using the same analysis in Eqs. (27), (28), (29) and (30), we have that

Because and , it is easy to verify that . Using the inequality we have that .

12 Proofs of technical lemmas for Theorem 6.2

12.1 Proof of Lemma 6.1

Lemma 12.1 (restated)

Let be defined in Eq. (12) and suppose . Then with probability , for every satisfying

| (32) |

for some universal constant , it holds that . Here is an upper bound estimate of .

Proof 12.2

Lemma 4.6 has already established that for all with probability . Hence we only need to prove that, with probability , any does not belong to for sufficiently large.

Consider arbitrary and assume by way of contradiction that . Define , where is the underlying true utility parameters. By definition of the gap parameter and the fact that (with high probability), we have that

| (33) |

According to Algorithm 1, means that . By Corollary 4.5, the optimality of and the fact that , we have that with probability that and . Subsequently,

Invoking Eq. (33) again , we obtain

| (34) |

On the other hand, plugging in the definition of we have that, if the condition in Eq. (13) holds, contradicting Eq. (34). This completes the proof of Lemma 6.1.

12.2 Proof of Theorem 6.2

Conditioned on the success event in Lemma 6.1 (with probability ), all epochs after the smallest satisfying Eq. (13) accumulate no regret. Therefore, to upper bound the cumulative regret of Algorithm 1, we can follow the analysis in the proof of Theorem 4.1 leading to Eq. (11) and replacing in Eq. (11) with , where is the smallest epoch whose satisfies Eq. (13). With the condition , the cumulative regret can be upper bounded by

| (35) |

Since and does not satisfy Eq. (13), we have that

| (36) |

Combing Eqs. (35) and (36), and noting that always holds, the regret of Algorithm 1 can be upper bounded by

| (37) |

where is a universal constant. Note that the term in Eq. (36) has been absorbed into the term because and therefore .

Finally we show how the second and the third terms in Eq. (37) are asymptotically dominated by the first and the fourth terms, thereby proving Theorem 6.2. For the second term, note that

thanks to the AM-GM inequality. For the third term in Eq. (37), invoking the AM-GM inequality again we have

This concludes the proof.

13 Proof of Theorem 6.6

We prove Theorem 6.6 by adding the regret incurred on each thread separately. First we consider for those . Because , Corollary 6.4 asserts that . Using the same derivation as in the proof of Theorem 6.2, we have that

where in the notation we omit terms and the last inequality holds because and and the fact that with high probability (Lemma 5.4).

Next consider any with . Let be the largest integer such that , or more specifically the unique index such that . By Corollary 6.5, we have that . By definition, . Subsequently,

Notice that and by definition. Subsequently,

where the second inequality holds by the AM-GM inequality. Theorem 6.6 is thus proved. The remark after Theorem 6.6 by applying the AM-GM inequality in a different way, or more specifically

14 Proof of Theorem 6.8

We first state our adversarial problem instances. The revenue parameters are set as . For typical customers, the choice model is parameterized by , , for all , where is an instance-dependent parameter and is a small perturbation parameter to be decided later. Such a problem instance is denoted as and the distribution it induces is denoted as . For outlier customers, they will always purchase the product with the smallest index (i.e., the probability of a no-purchase for outlier customers is zero).

Because of the additive nature of the lower bound, we only need to prove the -regret is lower bounded by and separately. For the first lower bound, one can simply plant a lower bound construction for gap-free capacitated dynamic assortment planning problems during the first time periods. By the work of Chen and Wang (2018), a gap-free lower bound of exists, where is the total number of time periods. Plugging in we complete the lower bound in Theorem 6.8.

In the rest of this proof we focus on the part of the lower bound, by simply setting . We first compute the sub-optimality gap of the problem instances to determine the appropriate values of .

Lemma 14.1

For each , , the sub-optimality gap defined in Eq. (12) satisfies .

Proof 14.2

Clearly, and for all , under problem instance . Let denote the expected revenue of assortment for typical customers. We then have

For , simply setting we obtain . Hence, the sub-optimality gap can be calculated as

where the last inequality holds because and .

From Lemma 14.1, clearly we should set to make being -gap problem instances. Because , we have that and therefore all problem instances are valid for .

Our next lemma upper bounds the Kullback-Leibner divergence between and on certain assortments.

Lemma 14.3

For assortment let denote the conditional distribution of purchase activities of typical customers with offered assortment and problem instance . Then for any and , , .

Proof 14.4

First note that if and then because the two distributions are exactly the same. Hence the KL-divergence is zero. In the rest of the proof we assume that either or .

Let , and . Denote and . For the no-purchase action we have

for , we have

for , we have

Invoking Lemma 3 from (Chen and Wang 2018), we have that

which is to be demonstrated.

Now consider arbitrary and sufficiently large . Define as the set of time periods during which product is offered in an assortment, and . We then have the following lemma lower bounding the -regret under and , respectively.

Lemma 14.5

Let and be expectations taken over the laws of and , respectively. Suppose . Then

Proof 14.6

The second inequality is obvious from the definition of the sub-optimality gap . To see the first inequality, note that under is . If for some , then this assortment suffers an instantaneous regret of ; if contains another , then this assortment suffers an additional instantaneous regret of since one product from the first products must be missed. Because , the lemma is proved.

Let and be parameters to be decided later. We will select such that, if the conclusion in Theorem 6.8 holds, then the -regret under is at most , or more specifically . By Markov’s inequality, this implies that

| (38) |

Next, let be the purchase activities realized during time periods at which product is offered as part of the assortment. Define also the log-likelihood ratio . We then have that, for any event ,

Hence, if , then , or equivalently . Using the law of total probability we have the following:

| (39) |

Now set for some sufficiently small universal constant and . If the -regret under exceeds then we have already proved Theorem 6.8. Otherwise, by Eq. (38) we have that

| (40) |

On the other hand, recall the definition that , we know that is the partial sum of a martingale and furthermore , thanks to Lemma 14.3. By setting to be sufficiently small, we have that . Because both and are constants not changing with , by the law of large numbers we have that

| (41) |

15 Tail inequalities

Lemma 15.1 (Bernstein’s inequality for martingale process Freedman (1975))

Let be centered random variables satisfying almost surely for all , and that for forms a martingale process. Then for any ,

As a corollary, for any ,

where .