Private Protocols for -Statistics in the Local Model and Beyond

Abstract

In this paper, we study the problem of computing -statistics of degree , i.e., quantities that come in the form of averages over pairs of data points, in the local model of differential privacy (LDP). The class of -statistics covers many statistical estimates of interest, including Gini mean difference, Kendall’s tau coefficient and Area under the ROC Curve (AUC), as well as empirical risk measures for machine learning problems such as ranking, clustering and metric learning. We first introduce an LDP protocol based on quantizing the data into bins and applying randomized response, which guarantees an -LDP estimate with a Mean Squared Error (MSE) of under regularity assumptions on the -statistic or the data distribution. We then propose a specialized protocol for AUC based on a novel use of hierarchical histograms that achieves MSE of for arbitrary data distribution. We also show that 2-party secure computation allows to design a protocol with MSE of , without any assumption on the kernel function or data distribution and with total communication linear in the number of users . Finally, we evaluate the performance of our protocols through experiments on synthetic and real datasets.

1 Introduction

The problem of collecting aggregate statistics from a set of users in a way that individual contributions remain private even from the data analysts has recently attracted a lot of interest. In the popular local model of differential privacy (LDP) (Duchi et al.,, 2013; Kairouz et al.,, 2014), users apply a local randomizer to their private input before sending it to an untrusted aggregator. In this context, most work has focused on computing quantities that are separable across individual users, such as sums and histograms (see Bassily and Smith,, 2015; Wang et al.,, 2017; Kulkarni et al.,, 2019; Cormode et al.,, 2018; Bassily et al.,, 2017, and references therein).

In this paper, we study the problem of privately computing -statistics of degree , which generalize sample mean statistics to averages over pairs of data points. Let be a set of data points drawn i.i.d. from an unknown ditribution over a (discrete or continuous) domain . The -statistic of degree with kernel , given by , is an unbiased estimate of with minimum variance (Hoeffding,, 1948). The class of -statistics covers many statistical estimates of interest, including sample variance, Gini mean difference, Kendall’s tau coefficient, Wilcoxon Mann-Whitney hypothesis test and Area under the ROC Curve (AUC) (Lee,, 1990; Mann and Whitney,, 1947; Faivishevsky and Goldberger,, 2008). They are also commonly used as empirical risk measures for machine learning problems such as ranking, clustering and metric learning (Kar et al.,, 2013; Clémençon et al.,, 2016).

Interestingly, private estimation of -statistics in the LDP model for arbitrary kernel functions and data distributions cannot be straightforwardly addressed by resorting to standard local randomizers such as the Laplace mechanism or randomized response. Indeed, one cannot apply the local randomizer to the terms of the sum based on the sensitivity of (as each term is shared across two users), and perturbing the inputs themselves can lead to large errors when passed through the (potentially discontinuous) function .

In this work, we design and analyze several protocols for computing -statistics with privacy and utility guarantees. More precisely:

-

1.

We introduce a generic LDP protocol based on quantizing the data into bins and applying -ary randomized response. We show that under an assumption on either the kernel function or the data distribution , the aggregator can construct an -LDP estimate of with a Mean Squared Error (MSE) of .

-

2.

For the case of the AUC on a domain of size , whose kernel does not satisfy the regularity assumption required by our previous protocol, we design a specialized protocol based on hierarchical histograms that achieves MSE under -LDP and under -LDP, for arbitrary data distribution.

-

3.

Under a slight relaxation of the local model in which we allow pairs of users and to compute a randomized version of with 2-party secure computation, we show that we can design a protocol with MSE of , without any assumption on the kernel function or data distribution and with constant communication for each of the users.

-

4.

To evaluate the practical performance of the proposed protocols, we present some experiments on synthetic and real datasets for the task of computing AUC and Kendall’s tau coefficient.

The paper is organized as follows. Section 2 gives some background on -statistics and local differential privacy. In Section 3 we present a generic LDP protocol based on randomizing quantized inputs. Section 4 introduces a specialized LDP protocol for computing the Area under the ROC Curve (AUC). In Section 5, we introduce a generic protocol which operates in a slightly relaxed version of the LDP model where users can run secure 2-party computation. We present some numerical experiments in Section 6, and conclude with a discussion of our results and future work in Section 7.

2 Background

In this section, we introduce some background on -statistics and local differential privacy.

2.1 -Statistics

2.1.1 Definition and Properties

Let be an (unknown) distribution over an input space and be a pairwise function (assumed to be symmetric for simplicity) referred to as the kernel. Given a sample of observations drawn from , we are interested in estimating the following population quantity:

| (1) |

Definition 1 (Hoeffding,, 1948).

The -statistic of degree with kernel is given by

| (2) |

is an unbiased estimate of . Denoting by and , its variance is given by (Hoeffding,, 1948; Lee,, 1990):

| (3) |

The above variance is of and is optimal among all unbiased estimators of that can be computed from . This incurs a complex dependence structure, as each data point appears in pairs. The statistical behavior of -statistics can be investigated using linearization techniques (Hoeffding,, 1948) and decoupling methods (de la Pena and Giné,, 1999), which provide tools to reduce their analysis to that of standard i.i.d. averages. One may refer to (Lee,, 1990) for asymptotic theory of -statistics, to (Van Der Vaart,, 2000) (Chapter 12 therein) and (de la Pena and Giné,, 1999) for nonasymptotic results, and to (Clémençon et al.,, 2008, 2016) for an account of -statistics in the context of machine learning and empirical risk minimization.

2.1.2 Motivating Examples

-statistics are commonly used as point estimators of various global properties of distributions, as well as in statistical hypothesis testing (Lee,, 1990; Mann and Whitney,, 1947; Faivishevsky and Goldberger,, 2008). They also come up as empirical risk measures in machine learning problems with pairwise loss functions such as bipartite ranking, metric learning and clustering. Below, we give some concrete examples of -statistics of broad interest to motivate our private protocols.

Gini mean difference. This is a classic measure of dispersion which is often seen as more informative than the variance for some distributions (Yitzhaki,, 2003). Letting , it is defined as

| (4) |

which is a -statistic of degree with kernel . Gini coefficient, the most commonly used measure of inequality, is obtained by multiplying by .

Remark 1.

The variance of a sample, obtained by replacing the absolute difference by the squared difference in (4), is also a -statistic. However we note that computing the variance can be achieved by computing two sums of locally computable variables ( and ), which can be done with existing LDP protocols.

Rényi-2 entropy. Also known as collision entropy, this provides a measure of entropy between Shannon’s entropy and min entropy which is used in many applications involving discrete distributions (see Acharya et al.,, 2015, and references therein). It is given by

| (5) |

The expression inside the log is a -statistic of degree with kernel .

Kendall’s tau coefficient. This statistic measures the ordinal association between two variables and is often used as a test statistic to answer questions such as “does a higher salary make one happier?”. In learning to rank applications, it is used to evaluate the extent to which a predicted ranking correlates with the (human-generated) gold standard (see e.g., Joachims,, 2002; Lapata,, 2006). Formally, assuming continuous variables for simplicity, let and . For any , the pairs and are said be concordant if or , and discordant otherwise. Let and be the number of concordant and discordant pairs in . Kendall rank correlation coefficient is defined as:

| (6) |

which is a -statistic of degree with kernel .111One can easily modify the kernel to account for ties.

Area under the ROC curve (AUC). In binary classification with class imbalance, the Receiver Operating Characteristic (ROC) gives the true positive rate with respect to the false positive rate of a predictor at each possible decision threshold. The AUC is a popular summary of the ROC curve which gives a single, threshold-independent measure of the classifier goodness: it corresponds to the probability that the predictor assigns a higher score to a randomly chosen positive point than to a randomly chosen negative one. AUCs are widely used as performance metrics in machine learning (Bradley,, 1997; Herschtal and Raskutti,, 2004), and have also been recently studied as fairness measures (Kallus and Zhou,, 2019; Vogel et al.,, 2020). Formally, let and where for each data point , is the score assigned to point and is its label. For convenience, let and and let and . The AUC is given by

| (7) |

where is an indicator variable outputting if the predicate is true and otherwise. Up to a factor, it is easy to see that is a -statistic of degree with kernel .

Machine learning with pairwise losses. Many machine learning problems involve loss functions that operate on pairs of points (Kar et al.,, 2013; Clémençon et al.,, 2016). This is the case for instance in metric learning (Bellet et al.,, 2015), bipartite ranking (Clémençon et al.,, 2008) and clustering (Clémençon,, 2014). Empirical risk minimization problems have therefore the following generic form:

| (8) |

where are model parameters. The objective function in (8), as well as its gradient, are -statistics of degree with kernels and respectively.

2.2 Local Differential Privacy

The classic centralized model of differential privacy assumed the presence of a trusted aggregator which processes the private information of individuals and releases a perturbed version of the result. The local model instead captures the setting where individuals do not trust the aggregator and randomize their input locally before sharing it. This model has received wide industrial adoption (Erlingsson et al.,, 2014; Fanti et al.,, 2016; Differential Privacy Team, Apple,, 2017; Ding et al.,, 2017).

Definition 2 (Duchi et al.,, 2013).

A local randomizer is -locally differentially private (LDP) if for all and all possible output in the range of :

The special case is called pure -LDP.

Most work in LDP aims to compute quantities that are separable across individual inputs, such as sums and histograms (see Bassily and Smith,, 2015; Wang et al.,, 2017; Kulkarni et al.,, 2019; Cormode et al.,, 2018; Bassily et al.,, 2017, and references therein). In contrast, our goal is to design LDP protocols for computing -statistics, where each term involves a pair of inputs.

3 Generic LDP Protocol from Quantization

| (9) |

Discrete inputs. We first consider the case of discrete inputs taking one of values. The possible values of the kernel function can be written as a matrix where . In this case, we can set the local randomizer to be -ary randomized response to generate a perturbed version of each input . Let denote the vector of length with a one in the -th position and elsewhere. For each perturbed input in one-hot encoding form we can deduce an unbiased estimate of . As the discrete -statistic is a linear function of each of these vectors, computing it on these unbiased estimates gives an unbiased estimate which can be written as:

and is itself a -statistic with kernel given by

where is the probability of returning the true input in -ary randomized response (see Eq. 9) and is the vector of length with every entry . Details and analysis of this process, leveraging Hoeffding’s decomposition of -statistics (Hoeffding,, 1948; Lee,, 1990), can be found in Section A.1 of the supplementary material. The resulting bounds on the variance of are summarized in the following theorem.

Theorem 1.

If for all , then

In order to achieve -LDP with a fixed this becomes,

Continuous inputs. For -statistics on discrete domains, e.g. Renyi-2 entropy, the above strategy can be applied directly. Possibly more importantly however, this then leads to a natural protocol for the continuous case. In this protocol (see Algorithm 1), the local randomizer proceeds by quantizing the input into bins (for instance using simple or randomized rounding) before applying the previous procedure.

There are two sources of error in this protocol. The first one is due to the randomization needed to satisfy LDP in the quantized domain as bounded in Theorem 1. The second source of error is due to quantization. In order to control this error in a nontrivial way, we rely on an assumption on the kernel function (namely, that it is Lipschitz) or the data distribution (namely, that it has Lipschitz density). Under these assumptions and using an appropriate variant of the kernel function on the quantized domain, we show that we can bound the error with respect to the original domain by a term in (see Section A.2 of the supplementary material). This leads to the following result.

Theorem 2.

For simplicity, assume bounded domain and kernel values for all . Let correspond to simple rounding, , and . Then Algorithm 1 satisfies -LDP. Furthermore:

-

•

If is -Lipschitz in each of its arguments, then is less than or equal to

-

•

If is -Lipschitz w.r.t. some measure , then is less than or equal to

Remark 2.

The use of simple rounding is not optimal in many situations. In the case of sum, and possibly of the Gini coefficient, it would be more accurate if randomized rounding were used instead of simple rounding. We leave this investigation for later work.

Setting so as to balance the quantization and estimation errors leads to the following corollary.

Corollary 1.

Under the conditions of Theorem 2, for and large enough , taking leads to , where corresponds to or depending on the assumption.

This result gives concrete error bounds for -statistics whose kernel is Lipschitz, for arbitrary data distributions. One important example is the Gini mean difference, whose corresponding kernel is -Lipschitz. On the other hand, for -statistics with non-Lipschitz kernels, the data distribution must be sufficiently smooth (if not, it is easy to construct cases that make the algorithm fail).

4 Locally Private AUC

In this section, we describe an algorithm for computing AUC (7), whose kernel is discontinuous and therefore non-Lipschitz. We assume to be an ordered domain of size , that is with each datum in . Note that all data is in practice discrete when represented in finite precision, so this is general. For simplicity of presentation we will assume that (i) for some integer , and (ii) that the classes of the data, the , are public.

Our solution for computing AUC in the local model relies on a hierarchical histogram construction that has been considered in previous works for private collection of high-dimensional data (Chan et al.,, 2012), heavy hitters (Bassily et al.,, 2017), and range queries (Kulkarni et al.,, 2019). A hierarchical histogram is essentially a tree data structure on top of a histogram where each internal node is labelled with the sum of the values in the interval covered by it (see Figure 1). That allows to answer any range query about by checking the value associated with nodes in the tree. We first define an exact version of such hierarchical histograms and explain how to compute AUC from one.

Notation on trees.

We represent a binary tree of depth with integer node labels as a total mapping from a prefix-closed set of binary strings of length at most to the integers. We refer to the -th node in level of the tree by the binary representation of padded to length from the left with zeros. With this notation, is the label of the root node, as we use to denote the empty string, (resp. ) is the integer label of the left (resp. right) child of the root of , and in general is the label of the node at path from the root, i.e. the label of the node reached by following left or right children from the root according to the value of ( indicates left and indicates right). Let be the -th node in the bottom level. For two binary strings we denote the prefix relation by , and their concatenation as .

Definition 3.

Let be a multiset, with . A hierarchical histogram of is a total mapping defined as . For simplicity, we denote by .

| \Tree[. [[. ] [. ] ] ] | = | \Tree[. [[. ] [. ] ] ] |

Algorithm. We use hierarchical histograms to compute AUC as follows. Let and be the samples of the positive and negative classes from which we want to estimate AUC. Let and be hierarchical histograms for and . Note that and . We can now define the unnormalized AUC, denoted UAUC, over hierarchical histograms recursively by letting be , if is a leaf, and otherwise setting:

Thus we have .

The above definition naturally leads to an algorithm that proceeds by traversing the trees top-down from the root , accumulating the products of counts from at nodes that correspond to entries in that are bigger than entries in . We now define a differentially private analogue. Later we will describe an efficient frequency oracle which can be used to compute an LDP estimate of a hierarchical histogram of values in a domain of size . This will provide the following necessary properties (i) is unbiased, (ii) , with defined as for some small constant (iii) the are pairwise independent and (iv) Each level of is independent of the other levels. Our private algorithm for computing an estimate of UAUC is then defined in terms of parameters and , and (bounding the variance of and respectively), and is a small number depending on , , and .

For a symbol we write to simultaneously refer to and . Let , i.e. and , and let . Our private estimate is defined as follows. If is a leaf then is , else if then it is given by

Otherwise, it is given recursively by

| (10) |

As before, this definition leads to an algorithm. Note that the only difference with its non-private analogue is that this procedure does not recurse into subtrees whose contribution to the UAUC is upper bounded sufficiently tightly. More concretely, the server starts by querying at the root, namely with . If is a leaf then we return as the AUC. Otherwise, the algorithm checks whether . If so, then the algorithm concludes that there is not much to gain in exploring the subtrees rooted at and , and returns as an estimate of . This estimate might seem equivalent to , but takes the previous form for a technical reason that is made clear in the proof. In this case we call a discarded node. On the other hand, if , the algorithm proceeds as its non-private analogue, accumulating the contribution to the UAUC from the direct subtrees of and recursing into nodes and . In this case we refer to as a recursed node. Thus every node will be either recursed, a leaf or there will be a discarded node such that . This is depicted in Figure 2.

Analysis. Note that our algorithm has two sources of error: (i) the one incurred by discarding nodes and (ii) the error in estimating the contribution to the UAUC of the recursed nodes. The threshold is carefully chosen to balance these two errors.

Let be the set of nodes recursed on at level . Our accuracy proof starts by bounding the expected value of (see Lemma 4 in Section B.1 of the supplementary) by a quantity that is independent of . We now describe a central argument to our accuracy proof, stated in the next theorem. Let be the contribution to the error by nodes in . Then, the total contribution to the error by recursed nodes is . A useful identity is , as we can bound , for any , in terms of (see detailed proof in the supplementary). Note that this identity follows from , with . The latter would hold if errors and were independent, since our frequency oracle is unbiased. However, errors at a given level are not independent of previous levels. However because the conditional expectation of with respect to the answers of the frequency oracles up to level is i.e. is a martingale difference sequence. The idea of conditioning on previous levels is used several times in our proofs, also to bound the error due to discarded nodes.

Next, we state our accuracy result, which is proven in detail in Section B.1 of the supplementary. Our proof tracks constants: this is important for practical purposes, and we show empirically in Section D.1 that our bound is in fact quite tight.

Theorem 3.

If and the following holds:

-

1.

i.e. frequency estimates are unbiased.

-

2.

i.e. MSE of frequency estimator is bounded by .

-

3.

For distinct with , and are independent i.e. the frequency estimates are pairwise independent.

-

4.

For all , the lists and are independent of each other.

Then, is given by

Instantiating .

So far, Theorem 3 does not yield a complete algorithm as it does not specify an algorithm for computing estimates of a hierarchical histogram that satisfy the conditions of Theorem 3. In Section B.2 of the supplementary, we show how to instantiate such an algorithm in a communication-efficient manner by combining ideas from Bassily et al., (2017), in particular the use of the Hadamard transform, with an modified version of the protocol from Kulkarni et al., (2019). This leads to the following result.

Theorem 4.

There is a one-round non-interactive protocol for computing AUC in the local model with MSE bounded by under -LDP and under -LDP. Every user submits one bit, and the server does computation and requires additional reconstruction space.

5 Generic Protocols from 2PC

So far, we have proposed a specialized LDP protocol for AUC, and a generic LDP protocol which requires some assumption on the kernel function or the data distribution to guarantee nontrivial error bounds. We conjecture that no LDP protocol can guarantee nontrivial error for arbitrary kernels and distributions, but we leave this as an open question for future work.

In this section, we slightly relax the model of LDP by allowing pairs of users and to compute a randomized version of their kernel value with 2-party secure computation (2PC). This gives rise to a computational differential privacy (CDP) model Mironov et al., (2009). Unsurprisingly, we show that in this model we can match the MSE of for computing regular (univariate) averages in the -LDP model by using advanced composition results (Dwork et al.,, 2010). However, such a protocol requires communication as all pairs of users need to compute via 2PC, and does not satisfy pure -DP.

Proposed protocol. To address these limitations, we propose that the aggregator asks only a (random) subset of pairs of users to submit their randomized kernel value . The idea is to trade-off between the error due to privacy (which increases as more pairs are used, due to budget splitting) and the subsampling error (for not averaging over all pairs). Given a positive integer (which should be thought of as a small constant independent of ) and assuming to be even for simplicity, we propose the following protocol:

-

1.

Subsampling: The aggregator samples independent permutations of the set of users . This defines a set of pairs .

-

2.

Perturbation: For each pair of users , users compute via 2PC and sends it to the aggregator.

-

3.

Aggregation: The aggregator computes an estimate of as a function of

Analysis. We have the following result for the Laplace mechanism applied to real-valued kernel functions (the extension to randomized response for discrete-valued kernels is straightforward). The proof relies on an exact characterization of the subsampling error by leveraging results on the variance of incomplete -statistics (Blom,, 1976), see Section C.1 of the supplementary for details.

Theorem 5 (2PC subsampling protocol with Laplace mechanism).

Let , and assume that the kernel has values in . Consider our subsampling protocol above with where , and the estimate computed as . Then the protocol satisfies -CDP, has a total communication cost of and

where and are defined as in (3).

The MSE in Theorem 5 is of . Remarkably, this shows that the variance of the estimate that uses all pairs is preserved when subsampling only pairs. This is made possible by the strong dependence structure in the terms of the original -statistic. As expected, rules a trade-off between the errors due to subsampling and to privacy: the larger , the smaller the former but the larger the latter (as each user must split its budget across pairs). The optimal value of depends on the kernel function and the data distribution (through and ) on the one hand, and the privacy budget on the other hand. This trade-off, along with the optimality of the proposed subsampling schemes, are discussed in more details Section C.1 of the supplementary material. In practice and as illustrated in our experiments, can be set to a small constant.

Implementing 2PC. Securely computing the randomized kernel value can be done efficiently for many kernel functions and local randomizers of interest, as the number of parties involved is limited to . We assume semi-honest parties (see Goldreich,, 2004, for a definition of this threat model). A suitable 2PC technique in this application are garbled circuits (Yao,, 1986; Lindell and Pinkas,, 2009; Evans et al.,, 2018), which are well-suited to compute Boolean comparisons as required in several of the kernels mentioned in Section 2.1.2. The circuits for computing the kernels can then be extended with output perturbation following ideas from Dwork et al., (2006) and Champion et al., (2019). We refer to Section C.2 of the supplement for details on design and complexity.

Remark 3 (Beyond 2PC).

One could further relax the model to allow multi-party secure computation with more than two parties, e.g. by extending the garbled circuit computing the kernel with secure aggregation over the pairs before performing output perturbation. This would recover the utility of centralized DP at the cost of much more computation and quadratic communication, which is not practical, as well as robustness. More interesting trade-offs may be achieved by securely aggregating small subsets of pairs. We leave the careful analysis of such extensions to future work.

6 Experiments

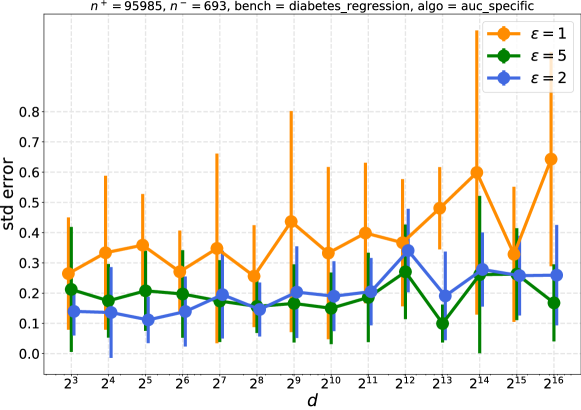

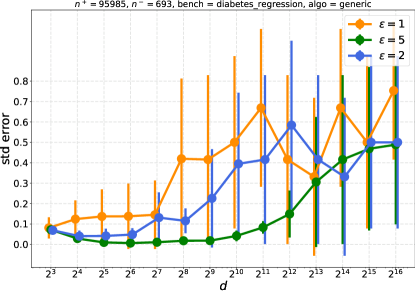

AUC. We use the Diabetes dataset (Strack et al.,, 2014) for the binary classification task of determining whether a patient will be readmitted in the next days after being discharged. We train a logistic regression model which is used to score data points in , and apply our protocol to privately compute AUC on the test set. Patients readmitted before days form the positive class. Class sizes are shown in Figure 3. Class information is not considered sensitive, as opposed to the score on private user data , which includes detailed medical information. Figure 3 shows the standard error achieved by our protocol for different values of the domain size . For each value of we run our protocol with inputs , where fp denotes a discretization into the domain . The plot shows that the protocol is quite robust to the choice of , and that increasing beyond does not improve results significantly. Recall that the error of our AUC protocol depends on the size of the smallest class, which is quite small here (only examples).

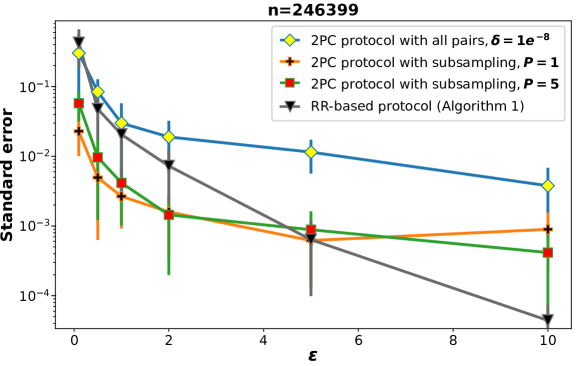

Kendall’s tau. We use the Tripadvisor dataset (Wang,, 2010). The dataset consists of discrete user ratings (from scale -1 to 5) for hotels in San Francisco over many service quality metrics such as room service, location, room cleanliness, front desk service etc. After discarding the records with missing values, we have over 246K records. Let be ratings given by user to the room () and the cleanliness (). The goal is to privately estimate the Kendall’s tau coefficient (KTC) between these two variables, whose true value is . We compare the privacy-utility trade-off of our randomized response protocol (Algorithm 1 without quantization, since inputs can take only values), our 2PC protocol based on subsampling, and the 2PC protocol that computes all pairs and relies on advanced composition (for which we set ). The 2PC primitive to compute is simulated. The results shown in Figure 4 show that the 2PC protocol with all pairs performs worst due to composition. The randomized response protocol performs slightly better, thanks to the small domain size. Finally, our 2PC protocol with subsampling achieves the lowest error by roughly an order of magnitude in high privacy regimes () while keeping the communication cost linear in . As predicted by our analysis, is best in high privacy regimes, where the error due to privacy dominates the subsampling error. We also see that can be used to reduce the overall error in low privacy regimes (for one can use an even larger to match the error of the randomized response protocol).

7 Concluding Remarks

In this paper, we tackled the problem of computing -statistics from private user data, covering many statistical quantities of broad interest which were not addressed by previous private protocols.

Relative merits of our protocols. Our three protocols are largely complementary, insofar as each of them is well-suited to specific situations. Our first protocol (quantization followed by randomized response) can gracefully handle cases where the kernel is Lipschitz or the data is discrete in a small domain. It may also work well for non-Lipschitz kernels when quantizing data into few bins does not lose too much information (e.g., when the data distribution is smooth enough). As the latter hypothesis is difficult to assess in advance, we argue that there can exist specialized protocols that work well for non-Lipschitz kernels on continuous data or large discrete domains. Our second protocol illustrates this for the case of AUC: we leverage a hierarchical histogram structure to scale much better with the number of bins than the first protocol (see Section D for experiments comparing these two protocols). Finally, if one is willing to slightly relax the LDP model to allow pairwise communication among users, and if the kernel can be computed efficiently via 2PC, our third protocol is expected to perform best in terms of accuracy.

Extension to higher degrees. While we focused on pairwise -statistics, our ideas can be extended to higher degrees. A prominent example is the Volume Under the ROC Surface, the generalization of the AUC to multi-partite ranking (Clémençon et al.,, 2013).

Future work. A promising direction for future work is to develop private multi-party algorithms for learning with pairwise losses (Kar et al.,, 2013; Clémençon et al.,, 2016) by combining private stochastic gradient descent for standard empirical risk minimization (Bassily et al.,, 2014; Shokri and Shmatikov,, 2015) and our protocols to compute the gradient estimates.

References

- Acharya et al., (2015) Acharya, J., Orlitsky, A., Suresh, A. T., and Tyagi, H. (2015). The Complexity of Estimating Rényi Entropy. In SODA.

- Bassily et al., (2017) Bassily, R., Nissim, K., Stemmer, U., and Thakurta, A. G. (2017). Practical locally private heavy hitters. In NIPS.

- Bassily and Smith, (2015) Bassily, R. and Smith, A. (2015). Local, private, efficient protocols for succinct histograms. In STOC.

- Bassily et al., (2014) Bassily, R., Smith, A. D., and Thakurta, A. (2014). Private Empirical Risk Minimization: Efficient Algorithms and Tight Error Bounds. In FOCS.

- Bellet et al., (2015) Bellet, A., Habrard, A., and Sebban, M. (2015). Metric Learning. Morgan & Claypool Publishers.

- Blom, (1976) Blom, G. (1976). Some properties of incomplete -statistics. Biometrika, 63(3):573–580.

- Bradley, (1997) Bradley, A. P. (1997). The use of the area under the ROC curve in the evaluation of machine learning algorithms. Pattern Recognition, 30(7):1145–1159.

- Champion et al., (2019) Champion, J., Shelat, A., and Ullman, J. (2019). Securely sampling biased coins with applications to differential privacy. IACR Cryptology ePrint Archive, 2019:823.

- Chan et al., (2012) Chan, T. H., Shi, E., and Song, D. (2012). Privacy-preserving stream aggregation with fault tolerance. In Financial Cryptography.

- Clémençon, (2014) Clémençon, S. (2014). A statistical view of clustering performance through the theory of U-processes. Journal of Multivariate Analysis, 124:42–56.

- Clémençon et al., (2016) Clémençon, S., Bellet, A., and Colin, I. (2016). Scaling-up Empirical Risk Minimization: Optimization of Incomplete U-statistics. Journal of Machine Learning Research, 13:165–202.

- Clémençon et al., (2008) Clémençon, S., Lugosi, G., and Vayatis, N. (2008). Ranking and empirical risk minimization of -statistics. The Annals of Statistics, 36(2):844–874.

- Clémençon et al., (2013) Clémençon, S., Robbiano, S., and Vayatis, N. (2013). Ranking data with ordinal labels: Optimality and pairwise aggregation. Machine Learning, 91(1):67–104.

- Cormode et al., (2018) Cormode, G., Kulkarni, T., and Srivastava, D. (2018). Marginal release under local differential privacy. In SIGMOD.

- Damgård et al., (2011) Damgård, I., Pastro, V., Smart, N. P., and Zakarias, S. (2011). Multiparty computation from somewhat homomorphic encryption. IACR Cryptology ePrint Archive, 2011:535.

- de la Pena and Giné, (1999) de la Pena, V. and Giné, E. (1999). Decoupling: from Dependence to Independence. Springer.

- Differential Privacy Team, Apple, (2017) Differential Privacy Team, Apple (2017). Learning with privacy at scale.

- Ding et al., (2017) Ding, B., Kulkarni, J., and Yekhanin, S. (2017). Collecting telemetry data privately. In NIPS.

- Duchi et al., (2013) Duchi, J. C., Jordan, M. I., and Wainwright, M. J. (2013). Local privacy and statistical minimax rates. In FOCS.

- Dwork et al., (2006) Dwork, C., Kenthapadi, K., McSherry, F., Mironov, I., and Naor, M. (2006). Our data, ourselves: Privacy via distributed noise generation. In EUROCRYPT.

- Dwork et al., (2010) Dwork, C., Rothblum, G. N., and Vadhan, S. (2010). Boosting and Differential Privacy. In FOCS.

- Erlingsson et al., (2014) Erlingsson, U., Pihur, V., and Korolova, A. (2014). Rappor: Randomized aggregatable privacy-preserving ordinal response. In CCS.

- Evans et al., (2018) Evans, D., Kolesnikov, V., and Rosulek, M. (2018). A pragmatic introduction to secure multi-party computation. Foundations and Trends in Privacy and Security, 2(2-3):70–246.

- Faivishevsky and Goldberger, (2008) Faivishevsky, L. and Goldberger, J. (2008). ICA based on a Smooth Estimation of the Differential Entropy. In NIPS.

- Fanti et al., (2016) Fanti, G., Pihur, V., and Erlingsson, Ú. (2016). Building a RAPPOR with the unknown: Privacy-preserving learning of associations and data dictionaries. In PoPETs.

- Goldreich, (2004) Goldreich, O. (2004). The Foundations of Cryptography - Volume 2, Basic Applications. Cambridge University Press.

- Goldreich et al., (1987) Goldreich, O., Micali, S., and Wigderson, A. (1987). How to play any mental game or A completeness theorem for protocols with honest majority. In STOC, pages 218–229. ACM.

- Herschtal and Raskutti, (2004) Herschtal, A. and Raskutti, B. (2004). Optimising area under the ROC curve using gradient descent. In ICML.

- Hoeffding, (1948) Hoeffding, W. (1948). A class of statistics with asymptotically normal distribution. Annals of Mathematics and Statistics, 19:293–325.

- Joachims, (2002) Joachims, T. (2002). Optimizing search engines using clickthrough data. In KDD.

- Kairouz et al., (2014) Kairouz, P., Oh, S., and Viswanath, P. (2014). Extremal mechanisms for local differential privacy. In NIPS.

- Kallus and Zhou, (2019) Kallus, N. and Zhou, A. (2019). The Fairness of Risk Scores Beyond Classification: Bipartite Ranking and the xAUC Metric. In NeurIPS.

- Kar et al., (2013) Kar, P., Sriperumbudur, B. K., Jain, P., and Karnick, H. (2013). On the Generalization Ability of Online Learning Algorithms for Pairwise Loss Functions. In ICML.

- Kulkarni et al., (2019) Kulkarni, T., Cormode, G., and Srivastava, D. (2019). Answering range queries under local differential privacy. In SIGMOD.

- Lapata, (2006) Lapata, M. (2006). Automatic Evaluation of Information Ordering: Kendall’s Tau. Computational Linguistics, 32(4):471–484.

- Lee, (1990) Lee, A. (1990). -statistics: Theory and practice. Marcel Dekker, Inc., New York.

- Lindell and Pinkas, (2009) Lindell, Y. and Pinkas, B. (2009). A proof of security of yao’s protocol for two-party computation. Journal of Cryptology, 22(2):161–188.

- Mann and Whitney, (1947) Mann, H. B. and Whitney, D. R. (1947). On a Test of Whether one of Two Random Variables is Stochastically Larger than the Other. Annals of Mathematical Statistics, 18(1):50–60.

- Mironov et al., (2009) Mironov, I., Pandey, O., Reingold, O., and Vadhan, S. P. (2009). Computational Differential Privacy. In CRYPTO.

- Shokri and Shmatikov, (2015) Shokri, R. and Shmatikov, V. (2015). Privacy-preserving deep learning. In CCS.

- Strack et al., (2014) Strack, B., DeShazo, J. P., Gennings, C., Olmo, J. L., Ventura, S., Cios, K. J., and Clore, J. N. (2014). Diabetes data. https://archive.ics.uci.edu/ml/datasets/diabetes+130-us+hospitals+for+years+1999-2008.

- Van Der Vaart, (2000) Van Der Vaart, A. W. (2000). Asymptotic Statistics. Cambridge University Press.

- Vogel et al., (2020) Vogel, R., Bellet, A., and Clémençon, S. (2020). Learning Fair Scoring Functions: Fairness Definitions, Algorithms and Generalization Bounds for Bipartite Ranking. arXiv preprint arXiv:2002.08159.

- Wang, (2010) Wang, H. (2010). Trip advisor data. http://www.preflib.org/data/combinatorial/trip/.

- Wang et al., (2017) Wang, T., Blocki, J., Li, N., and Jha, S. (2017). Locally differentially private protocols for frequency estimation. In USENIX Security Symposium.

- Yao, (1986) Yao, A. C. (1986). How to generate and exchange secrets (extended abstract). In FOCS.

- Yitzhaki, (2003) Yitzhaki, S. (2003). Gini’s Mean Difference: A Superior Measure of Variability for Non-Normal Distributions. Metron International Journal of Statistics, 61(2):285–316.

Appendix A Details and Proofs for Generic LDP Protocol

We start by introducing some notations. We denote by the number of bins of the quantization and by the quantization scheme such that for any data point , denotes the quantized version of (i.e., its image under ). Let denote the vector of length with a one in the -th position and elsewhere. A kernel function on the quantized domain is fully described by a matrix such that . We denote by the quantized analogue to the quantity .

The proposed protocol, described in Algorithm 1, applies generalized randomized response on data quantized with and uses this to compute an unbiased estimate of a quantized -statistic. The choice of the quantized kernel will be discussed below. Crucially, there are two sources of error in this protocol. More precisely, the mean squared error of the estimate returned by Algorithm 1 can be bounded as follows:

| (11) |

The first term corresponds to the error due to quantization, while the second one is the estimation error due to randomization needed to satisfy local differential privacy. The latter will increase with , thereby constraining to remain reasonably small. We will thus need to rely on assumptions on either the kernel or the data distribution to be able to control the error due to quantization.

In line with the error decomposition in (11), we conduct our analysis by considering the effect of sampling and randomization together. Therefore, we will not provide a direct bound on the error between our estimate and the U-statistic of the sample, but directly with respect to the population quantity . We now show how to control the two sources of error, which are easily combined to yield Theorem 2.

A.1 Bounding the Error of Randomized Response on Discrete Domain

In this part, we bound the second term in (11): we consider that the data is discrete () and derive error bounds for the estimate with respect to for a given kernel function . We propose to use the generalized randomized response mechanism as our local randomizer . We introduce some notations. Let be the probability of selecting a response uniformly at random, i.e. let , let be the vector of length with every entry . For convenience, we denote the data sample by . Note that these data points are drawn i.i.d. from a distribution over (which follows from and ) such that .

With these notations, we write the expected value of the discretized kernel computed directly on the randomized data points:

This is a biased estimator of due to the effect of the randomization. We correct for this by adding terms and scaling, leading to the estimator used in Algorithm 1:

This is an unbiased estimator of the population U-statistic, as for fixed and it is an unbiased estimator of . Averaging over all pairs of randomized inputs, we get the proposed estimator:

which is itself a U-statistic on the randomized sample. As this estimator is unbiased, its mean squared error is equal to its variance, for which the following lemma gives an exact expression.

Lemma 1.

The variance of is given by

Proof.

is a -statistic, hence its variance is given by (3) where and . We first simplify :

Similarly for , we have:

Substituting the values of and in the variance expression gives the result. ∎

Assuming a uniform bound on the values of allows a clear and simple bound on the variance.

Corollary 2.

If for all , then

Proof.

Under the boundedness of , the random variable takes values in and so has variance at most , whilst the random variable takes values in and so has variance at most . Substituting these into Lemma 1 gives the result. ∎

To achieve local differential privacy with parameter , should be taken to be . This leads directly to the following result.

Corollary 3 (Variance under randomized reponse).

Let and assume takes values in . We have:

where the approximation holds for small and .

The above result shows that for fixed the error incurred by this estimator is within a constant factor of the error due to the finite sample setting. As expected, should be reasonably small for the protocol to yield any utility.

A.2 Bounding the Error of Quantization

We now study the effect of quantization, which is needed to control the error due to privacy when the domain is continuous or has large cardinality. Recall that we quantize using a projection (assumed to be simple rounding for simplicity), and our goal is to approximate by , which we can privately estimate using the results of Section A.1.

The error incurred by the quantization can be written as follows:

| (12) |

To bound this quantization error, we need additional assumptions. We consider two options, each suggesting a different choice for the quantized kernel . We first consider a Lipschitz assumption on the original kernel function, for which the preferred quantized kernel minimizes the worst-case bound on (12). Then, we consider a smoothness assumption on the data distribution, leading to a quantized kernel that attempts to minimize the average-case error. We stress the fact that in some cases these quantized statistics will match or at least be very close, meaning that the particular choice of quantized kernel will not be crucial.

A.2.1 Assumption of Lipschitz Kernel Function

Our first assumption is motived by the fact that for all data distributions , the quantization error (12) can be bounded by

| (13) |

This bound is minimized by choosing the quantized kernel to be

| (14) |

which we will call the midpoint kernel. With this kernel we can define

which allows us to write the bound in equation 13 as

Note that this is itself a discrete -statistic over the population. The error can now be bounded through a bound on . A natural way to achieve this is to uniformly bound , which can be done by assuming that the kernel function is Lipschitz. This allows to control the error within each bin.

Lemma 2 (Quantization error for Lipschitz kernel functions).

Let and assume is -Lipschitz in each input. Let the set of bins be and let the quantization scheme perform simple rounding of inputs (affecting them to the nearest bin). Then we have .

Proof.

By the Lipschitz property of , we have that for all . Since the diameter of each bin is equal to , we have for all and the lemma follows. ∎

As desired, the quantization error decreases with . Note that the Lipschitz assumption is met in the important case of the Gini mean difference, while it does not hold for AUC and Kendall’s tau. Bounding is not the right approach for such kernels: indeed, for AUC, and so for data distributions with for some , the quantization error . In the next section, we consider generic kernel functions under a smoothness assumption on the data distributions.

Remark 4 (Empirical Estimation of ).

The quantization error is a discrete -statistic which can be estimated from the data collected to estimate . This provides a good empirical estimate of after the fact. However, as the data has to be collected before the estimate can be made it provides no guidance in choosing (this might be addressed by a multi-round protocol, which we leave for future work). The empirical assessment of may provide a tighter bound on the actual error than can be ascertained by the worst-case Lipschitz assumption.

A.2.2 Assumption of Smooth Data Distribution

We now consider a smoothness assumption on the data distribution . Specifically, we assume that the density with respect to a measure (which varies little on for all ) is -Lipschitz.

In this case, a more sensible choice of quantized kernel is given by

| (15) |

which we call the average kernel as the value of corresponds to the (normalized) expectation of , with respect to , over points and that are mapped to bin and respectively.

Under our smoothness assumption, the quantization error (12) can be bounded as follows.

Lemma 3 (Quantization error for smooth distributions).

Let and for all .222Similar arguments can be made in more general metric spaces. Assume that is -Lipschitz. Then we have , where is the maximum diameter of the quantization bins.

Proof.

For notational convenience, let us denote and for each . The absolute quantization error with quantized kernel (15) is given by:

| (16) |

Note that

and

Plugging these equations into (16) we get:

| (17) | ||||

| (18) | ||||

| (19) |

Summing over all and taking the square finally gives the result:

∎

The diameter of quantization bins is typically of order , hence the quantization error is of order . In practice, can simply be taken to be Lebesgue measure, hence computing (15) amounts to averaging the kernel function over all possible points that fall in the bins , and can be easily approximated by Monte Carlo sampling when one does not have a closed form expression for the integral.

Appendix B Details and Proofs for AUC Protocol

B.1 Proof of Theorem 3

We define as the set of nodes recursed on at level . Similarly, and for , let be the active nodes at level , i.e. those to be either recursed on or discarded. Then, the set of discarded nodes at level is defined as . Our algorithm has two main sources of error: (i) the one incurred on by discarded nodes, i.e. nodes in for whose intervals the algorithm uses a rough estimate, and (ii) the error in the estimating the contribution to the UAUC of the recursed nodes, i.e. nodes in .

The threshold is carefully chosen according to the error of the estimator to balance these two errors. In this way we translate error bounds for into error bounds for . Our proof starts by bounding the expected size of .

Lemma 4.

Consider the instantiation of Equation 10 with a frequency oracle for estimating satisfying , with , i.e. the estimate is unbiased and has uniformly bounded MSE. If , then for all ,

Proof.

Let , the sum of the positive estimated counts of active nodes at level .

Note that if then . In this case either, and thus , and thus , or and thus . In any of these cases .

Therefore

and thus

We bound as follows

We can now use this to bound the expression for .

| (20) |

We now need a bound on so we will proceed by induction.

Let . We take as the induction hypothesis, and as the base case.

The expression on the right hand side of inequality 20 is a monotonically increasing function of and has a fixed point

Finally we note that

and so

completing the proof. ∎

We are now ready to prove Theorem 3.

Proof of Theorem 3.

The estimation error at a given node can be written recursively as follows:

We will consider the error in two parts. Firstly, there is the contribution from those prefixes which we define by setting

and . Secondly, there is the contribution from the prefixes excluding their recursive subcalls which we define by setting

and . In bounding both of these we will make use of conditioning on i.e. the answers of the frequency oracles for layers up to .

We start by bounding . For any , we first show that is a martingale difference sequence i.e.

where the final equality holds because for all and and are independent. From this we can conclude that for

and thus

| (22) |

Next we shall bound . We start by writing out

By Equation 22 this becomes

After expanding the above and removing all the terms that are zero, because they are the expected value of the product of with something independent of it, we are left with

Subbing this into (22) and using Lemma 4 gives

To bound , first define and . We refer to the leaves in covered by a path as . Now note that

We now bound and separately. For a leaf node , let us denote by the unique node in that is a prefix of . We then have:

We can then bound

Thus

Furthermore by symmetry between and

Secondly we bound . Note that is a function of and so

Similarly to the bound on , we now apply the pairwise independence property and note that is an unbiased estimator of with variance bounded by . This results in

Noting that and that gives

By the Cauchy-Schwarz inequality we can conclude that,

Finally applying Cauchy-Schwarz again gives

∎

Remark 5.

The use of Cauchy-Schwarz to combine the separate errors in this proof is optimized for simplicity rather than minimizing the constants. At the expense of making the bound substantially more complicated a more precise analysis would reduce the bound. Gaining up to a factor of two in the case of very large and small compared to .

The value of in Theorem 3 can be chosen to minimize the error by taking it to solve which is approximately

This leads to the following corollary.

Corollary 4.

Let and then

Remark 6.

For fixed this is of the same order as the sampling error incurred in non-private AUC.

Algorithm variant.

An alternative algorithm assigns a value of zero to edges that it discards. For this algorithm a similar theorem holds by the same argument (actually a slightly simpler argument) the resulting error bound is

Note that the second term which is of leading order for a fixed fraction of is twice as large however the final term which is lower order is twenty-one times smaller. This lower order term might not be negligible in practice and so this algorithm should be considered. The corresponding choice of and bound on the final error is given by the following result.

Corollary 5.

Let and then

B.2 Instantiating the Private Hierarchical Histogram

Theorem 3 does not yield a complete algorithm as it only states that, if we had a differentially private algorithm for computing estimates of a hierarchical histogram that satisfy the conditions of Theorem 3, then we could solve AUC with the stated accuracy. In this section we instantiate such algorithm and show that, besides the required error guarantees, our proposal also has other nice properties, namely (i) it is one round, (ii) each user sends a single bit, and (iii) it is sublinear in processing space at the server.

B.2.1 Frequency Oracle

Relevant previous work on estimating hierarchical histograms in the local model includes the work of Bassily et al., (2017). While in that work the target problem is heavy hitters, their algorithm is similar to ours, as the server retrieves the heavy hitters by exploring a hierarchical histogram. Moreover their protocol – called TreeHist – has the nice properties listed above, as it is one round, every user sends a single bit and requires reconstruction space sublinear in . This satisfies the three above conditions. It is thus tempting to reuse the hierarchical histogram construction from Bassily et al., (2017). However, it does not satisfy the conditions of Theorem 3, as it is not guaranteed to be unbiased.

Alternative recent algorithms for constructing hierarchical histograms in the local model are presented in Kulkarni et al., (2019), with the motivation of answering range queries over a large domain. This proposal is much closer to what we need. However, it has some shortcomings: first, although it is one round, each user sends bits, and more importantly, it requires space space at the server, as it reconstructs the whole hierarchical histogram. However, one can tweak the protocol from Kulkarni et al., (2019) to overcome these limitations. We shall first split the users into groups (one for each level) and then for each level we shall apply the frequency oracle. Algorithm 2 and Algorithm 3 show the local randomizer (user side) and frequency oracle (server side) for each histogram.

Let be the true count of an index in a histogram. The following lemma is shown in Kulkarni et al., (2019).

Lemma 5.

The frequency oracle, Algorithm 3, run with users is unbiased and satisfies the following bound on the MSE.

| (23) |

Additionally we require the following lemma on the frequency oracle satisfies condition (3) in Theorem 3 which is given by the following lemma.

Lemma 6.

For distinct , and are independent i.e. the responses of the oracle are pairwise independent.

Proof.

As each user is independent of every other user it suffices to show that each user’s contribution to the two entries are independent. Suppose that a user has input , chooses index to report and let be a bit indicating that the user chose in Algorithm 2. That user’s contributions to the two estimates (scaled by ) are and . Note that we can consider and as elements of . Then and are distinct and . These two facts imply respectively that is independent of and that is uniformly distributed in . Thus the contributions are independent. ∎

B.2.2 Splitting Strategies

We will instantiate by running the frequency oracle above for each level of the hierarchy. The main choice remaining is how to determine which users contribute to each layer, we will consider two possibilities here. Firstly we can have everyone contribute to all layers, splitting their privacy budget. Alternatively, users can be split evenly across levels at random, each contributing to only one frequency oracle. Another possibility is to assign each user to a level independently and uniformly, this is similar to splitting them evenly though adds slightly more noise and is more complicated to analyse. In all cases, conditions 1 and 3 in Theorem 3 follow from Lemmas 5 and 6.

Splitting Privacy Budget Across Layers.

In the case of everyone contributing to all layers the privacy budget can be split using either basic or advanced composition. In either case condition 4 from Theorem 3 holds as the randomness for each layer is independent.

For pure differential privacy we must use basic composition. This allows us to run each frequency oracle can be run with a privacy budget of . Lemma 5 then gives a bound of on the mean squared error of each entry. While this is insufficient to establish condition 2 of Theorem 3, similar arguments can be used to prove that the algorithm built in this way achieves pure differential privacy at the cost of an factor in the MSE.

If we instead settle for -differential privacy, and assume for convenience that , advanced composition allows each frequency oracle to be run with privacy budget . Condition 2 in Theorem 3 then holds for some depending on and . This is the implementation and analysis that gives Theorem 3 as it is stated.

Splitting Users Across Layers.

When splitting users across levels the frequency oracles can each be run with privacy budget . However, each oracle will have only users and there is a subsampling error between the total sample and the input given to the frequency oracle. The squared error due to subsampling is thus Lemma 5 provides a bound on the MSE. This means that condition 2 of Theorem 3 holds. This would provide a version of Theorem 3 with pure differential privacy, however condition 4 from Theorem 3 fails to hold. Intuitively this is because if a user contributes to one level they can’t contribute to another level. There are still two things that can be proved about this version of the algorithm.

Firstly, it is still possible to prove a result like Theorem 3, but in which the MSE is times bigger. The proof of this result follows the same steps as that of Theorem 3 except that the martingale difference sequences argument must be replaced by a bound not assuming pairwise independence.

A second way of viewing this algorithm is to think of each input as being drawn independently from some population distribution and then compare the output to the AUC of that distribution. That is, given a pair of distributions , is obtained by sampling each value independently from . Denote and let . The fact that each of the users has an independent identically distributed input means that the contribution to each layer is independent, i.e. we can recover Theorem 3 with MSE replaced by . This alternative notion of is the correct notion to work with if the purpose of the deployment of the algorithm is to find the AUC of the population the sample is drawn from rather than just of the sample. This is likely to be the case in many applications.

Summary.

Table 1 summarizes the choices in the algorithm and analysis. The resulting orders of the MSE, corresponding to Theorem 4 are given in the final column.

| Splitting | Analysis | Error in |

|---|---|---|

| Privacy budget | Basic composition | |

| Privacy budget | Advanced composition | |

| Users | w.r.t. sample | |

| Users | w.r.t. population |

Appendix C Details and Proofs for 2PC Protocol

C.1 Proof of Theorem 5 and Discussion

Proof.

The -DP follows from the Laplace mechanism and the simple composition property of DP (observing that each input appears in exactly pairs in ).

It is easy to see that is unbiased, hence we only need to bound its variance. We will separate the part due to subsampling and the part due to privacy. To this end, we decompose into a noise-free term and a noisy term:

| (24) |

The noisy term is an average of independent Laplace random variables: its variance is equal to .

The quantity is known as an incomplete -statistic, whose variance is given by Blom, (1976):

| (25) |

where , , and are the number of members of which have exactly 1 (respectively 2) indices in common.

We first consider . Recall that is constructed from permutations of the set . As each index appears exactly once in each permutation, it suffices to consider the self pairs within permutations and the overlaps across pairs of permutations we get:

where is the number of pairs from the permutation that contain . The probability of a pair to appear in a given permutation is , hence using the independence between permutations we obtain:

For , using a similar reasoning we only have to consider overlaps across each pair of permutations, in which each index pair shares exactly one index with a single pair of another permutation, except when the pair appears twice, hence:

Putting everything together into (25) we get the desired result. ∎

Optimal value of .

The optimal value of depends on the kernel function, the data distribution and the privacy budget. Roughly speaking, setting larger than can be beneficial when is large compared to . On the other hand, when (which is the minimum value of , corresponding to the extreme case where the kernel can in fact be rewritten as a sum of univariate functions (Blom,, 1976)), simplifies to and is optimal. In practice and as illustrated in our experiments, should be set to a small constant.

Optimality of subsampling schemes.

The proposed subsampling strategy is simple to implement and leads to an optimal variance, up to an additive term of , among unbiased approximations based on pairs. Note that this additive term is when or , and is in general negligible compared to the dominating terms for small enough . Optimal variance could be achieved at the cost of a more involved sampling scheme.333In addition to having each data point appear the same number of times in , one must ensure that no pair appears more than once. Alternatively, sampling schemes that can be run independently by each user without global coordination (such as sampling other users uniformly at random) lead to a slight increase in variance as users are not guaranteed to appear evenly across the sampled pairs.

C.2 Implementing 2PC

MPC is a subfield of cryptography concerned with the general problem of computing on private distributed data in a way in which only the result of the computation is revealed to the parties, and nothing else. In this paper the number of parties is limited to , and the function to be computed is . There are several protocols that allow to achieve this goal, with different trade-offs in terms of security, round complexity, and also differing on how the functionality is represented. These alternatives include Yao’s garbled circuits (Yao,, 1986; Lindell and Pinkas,, 2009), the GMW protocol (Goldreich et al.,, 1987), and the SPDZ protocol (Damgård et al.,, 2011), among others. As some of the functions we are interested in involve comparisons (e.g., Gini mean difference and AUC), a Boolean representation is more suitable, as it will lead to a smaller circuit. Moreover, a constant round protocol is preferred in our setting, as as users might have limited connectivity. For this reason we choose garbled circuits as our protocol, for which (Evans et al.,, 2018) give a detailed description including crucial practical optimizations. Moreover, we assume semi-honest adversaries in the sequel (see Goldreich,, 2004, for a definition of this threat model).

Circuits for kernels.

We illustrate the main ideas on Gini mean difference and AUC. As circuits for floating point arithmetic are large, they are usually avoided in MPC, to instead rely on fixed point encodings. Hence, we assume that the parties have agreed on a precision, and hence are integers encoded in two’s complement.

For Gini mean difference we need our 2PC protocol to compute . Let be , let be the binary encoding of , where the bitwidth will be a constant such as or in practice, and let be the sign bit of replicated times. Then can be computed as and, thanks to the free-XOR optimization of garbled circuits (see Evans et al.,, 2018), the garble circuit evaluation requires only a subtraction and a summation, and thus is very efficient.

For AUC we need our 2PC protocol to compute , which requires a single comparison and thus a small number of binary gates to be evaluated in a garbled circuit.

Circuits for local randomizers.

The above circuits need to be extended with output perturbation corresponding to the Laplace and randomized response mechanisms discussed above. An important observation when designing efficient circuits for these tasks is the well-known fact that a random bit with bias , for any integer , can be generated from only two uniform random bits suffice, in expectation. Generating a uniformly random bit is easy (and extremely cheap using garbled circuits) in the semi-honest model: each party simply generates a random bit, and then inside the circuit a random bit is reconstructed as the XOR of two bits. As XORs are for free in garbled circuits this computation is very efficient. The problem of implementing differentially private mechanisms in MPC was discussed by Dwork et al., (2006), where the authors present small circuits for sampling from an exponential distribution requiring only a biased random bits, which can be constructed in parallel. Recently, Champion et al., (2019) proposed optimized constructions for several well-known differentially private mechanisms (including the geometric and Laplace mechanisms), and empirically showed their concrete efficiency.

Appendix D Additional Experiments

D.1 AUC Experiments on Synthetic Data

We illustrate the behavior of our AUC-specific LDP protocol of Section 4 on three synthetic datasets, and compare its performance with that of our generic LDP protocol of Section 3. For all datasets, we have inputs in each class (positive and negative) but the score values of inputs are distributed differently:

-

•

auc_one consists of two distinct inputs and each occurring times.

-

•

In ur, the score value of an input is drawn independently and uniformly from , regardless of its class.

-

•

ithdigit consists of two distinct inputs and each occurring times.

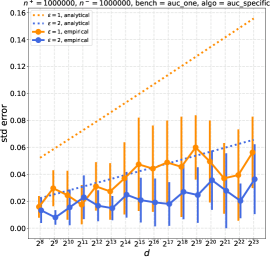

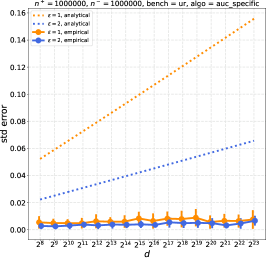

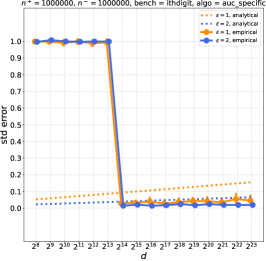

Figure 5 shows the error that our AUC-specific protocol incurs on the three datasets. On auc_one, our AUC-specific protocol incurs considerable error due to significant recursion error, , being incurred for every level. This example illustrates that our analysis for the AUC-specific protocol is not far from being tight. On ur, the error is much lower. This is because (i) the algorithm does not explore any of the lower sections of the tree and so no recursion error is incurred whilst exploring it, and (ii) within intervals that are discarded the points are uniformly distributed so the estimation of the AUC within that interval as a half is effective. Both of these effects will occur approximately whenever the data is smooth so one can expect the algorithm to do better in the case of smooth data than the analytic bounds indicate. Finally, on ithdigit, the protocol does not learn anything when the quantization is smaller or equal to , which is expected as all inputs are quantized to the same bin. However, we see that the protocol achieves low error for . Importantly, in all cases our AUC-specific protocol scales nicely with the size of the domain. This allows to be rather agnostic about the level of quantization needed for the problem at hand, which is often not known in advance.

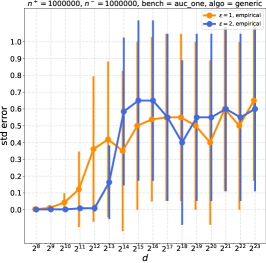

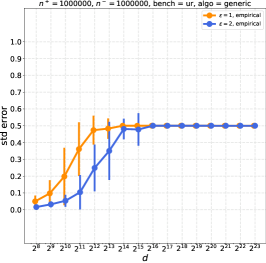

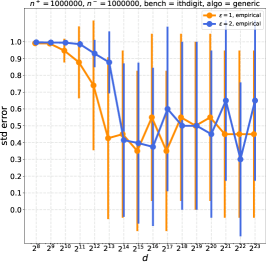

In contrast, we can see on Figure 6 that the generic protocol scales very poorly with the domain size due to the use of randomized response. On auc_one and ur, data can be quantized to a small domain without losing much relevant information, leading to good performance. In the case of ithdigit however, the generic protocol incurs very large error in all regimes: quantizing to small domain maps all inputs to the same bin, while quantizing to large domain leads to large error due to privacy.

D.2 Results of the Generic Protocol on Diabetes dataset

Figure 7 shows the results of our generic LDP protocol of Section 3 for the problem of computing the AUC on the Diabetes dataset (see Section 6 for results with the AUC-specific protocol). On this dataset, a fully trained logistic regression model yields scores of positive and negative points that are well separated. Hence, they can be quantized to a sufficiently small domain for the protocol to achieve small error.