Noncompliance in randomized control trials without exclusion restrictions

Abstract

This study proposes a method to identify treatment effects without exclusion restrictions in randomized experiments with noncompliance. Exploiting a baseline survey commonly available in randomized experiments, I decompose the intention-to-treat effects conditional on the endogenous treatment status. I then identify these parameters to understand the effects of the assignment and treatment. The key assumption is that a baseline variable maintains rank orders similar to the control outcome. I also reveal that the change-in-changes strategy may work without repeated outcomes. Finally, I propose a new estimator that flexibly incorporates covariates and demonstrate its properties using two experimental studies.

Keywords: Causal inference, Change-in-Changes model, Exclusion restriction, Natural experiment, Principal stratification.

1 Introduction

Randomized assignment is a standard strategy to identify the average treatment effect under full compliance (i.e., when the assignment equals the associated treatment). By contrast, under noncompliance, an additional exclusion restriction is required to identify the associated treatment effects. Although an exclusion restriction requires that the assignment has no causal effect on the outcomes holding the treatment status fixed, this restriction may not always hold. In fact, the assignment itself may affect the outcomes for several reasons.

For randomized control trials (RCTs), I propose a strategy to identify the effects of a binary assignment and binary treatment without imposing an exclusion restriction. Specifically, I consider the intention-to-treat (ITT) effects decomposed by the treatment status. There are two key parameters to consider. First, I consider the ITT conditional on the treated under the assignment (ITTTA). The ITTTA is the combined effect of both the assignment and the treatment. It equals the average treatment effect on the treated (ATT), when the exclusion restriction holds under one-sided noncompliance, which prohibits the units from taking up the treatment without the assignment. Second, I consider the ITT conditional on the nontreated under the assignment (ITTNA). The ITTNA is solely the assignment’s own effect, often referred to as the assignment’s direct effect.

To identify the heterogeneous effects of whether to employ the treatment, the baseline strategies are to either use the assignment as an instrumental variable (IV) or the conditionally ignorable assumption for the treatment. In my strategy, I require neither the exogenous treatment nor valid IVs. Instead, I develop a natural experimental approach in RCTs with their typical feature, that is, the baseline survey. I use a continuous variable from the baseline survey as a proxy for the control outcome. Specifically, I develop a rank imputation strategy with new estimators based on a rank similarity assumption that appears in Chernozhukov and Hansen’s (2005) quantile IV model as well as in Athey and Imbens’s (2006) change-in-changes (CiC) model. I apply the method to microcredit and cash transfer experimental studies and demonstrate that the direct effect of the randomized assignment for the nontreated, the ITTNA, is an attractive and important parameter for estimating the combined effect of the assignment and the treatment, the ITTTA.

This study makes three major contributions to the literature. First, I propose a natural experimental strategy for RCTs by exploiting their typical feature, the baseline survey. Specifically, the first contribution concerns the parameter, called principal stratification by Frangakis and Rubin (2002), that appears when exploring for the causal effect mechanism. Causal inference with an invalid instrument for the treatment is the leading context in principal stratification. For example, Deuchert and Huber (2017), who examined the Vietnam draft lottery, documented that the exclusion restriction may be violated. Furthermore, most studies in this context exploit exclusion restrictions (Imbens and Angrist, 1994; Angrist et al., 1996) or conditional independence (Hirano et al., 2000).

As an alternative, several studies (Zhang and Rubin, 2003; Rubin, 2006; Flores and Flores-Lagunes, 2013; Mealli and Pacini, 2013) have proposed partial identification strategies exploiting monotone treatment response arguments (Manski, 1997; Manski and Pepper, 2000). In response to the above baseline strategies, the natural experimental approach has also emerged as a substitute recently. For instance, Deuchert et al. (2018) used a difference-in-differences (DiD) strategy to study the Vietnam war draft’s impact on political preferences. Specifically, the analysis allowed for the draft itself to have a direct impact on the preferences. Additionally, Huber et al. (2020) proposed a CiC strategy for the principal stratification and mediation analysis to study the impact of job training on mental health, using a randomized job training program in the United States called JOBS II. A unique feature of Huber et al. (2020) appears in their results without valid randomization. Specifically, they applied their strategy without valid randomization when examining the effect of paid maternity leave on labor income, using the Swiss Labour Force Survey.

Thus, I contribute to this stream of the literature by offering a unique natural experimental strategy that exploits the baseline survey with a continuous proxy variable. I impose restrictions on the proxy variable and the control outcome in their latent rankings, which are uniform random variables representing their underlying percentiles. I assume that the conditional distributions of the latent rankings for the proxy variable and control outcome are identical regardless of whether taking up a treatment. This restriction is called the rank similarity assumption, under which taking up a treatment may be endogenous. Although the strategy is consistent with Huber et al. (2020), my aims and imposed restrictions differ in two ways. First, Huber et al. (2020) required a structural model with a common latent rank variable unifying the different potential outcomes. Although the functional form is entirely flexible, it is a strong restriction in which a single unobserved variable governs all the potential outcome values during the same period. As I define the latent ranks as reduced-form representations for each potential outcome, I do not impose the structural model or the common latent rank variable. Second, to fully uncover the parameters, Huber et al. (2020) imposed latent rank restrictions not only on the control outcomes against the proxy but also on the treatment outcomes against the proxy. While the proxy variable and control outcome, which are both free of the intervention, are similar, it is challenging to relate the treatment outcomes to the proxy in general. Nonetheless, these stronger restrictions allow them to identify the mediation effects and principal stratification without randomization. Furthermore, it is difficult to disentangle the restrictions on the control and treatment outcomes because both are unified in the common latent rank, and the restrictions are imposed on the common latent rank variable. In my strategy, I do not impose any restrictions on the treated outcome, given the potential outcome model under randomization for the ITTTA and ITTNA. Instead, I only impose restrictions on the control outcomes. As these weaker restrictions prohibit us from identifying the other parameters in Huber et al. (2020), I impose fewer necessary restrictions on the potential outcomes to identify the parameters relating to the principal strata.

Overall, compared with Huber et al. (2020), who considered a richer mediation analysis under richer models and restrictions, the proposed strategy requires fewer model structures and less restrictive assumptions to identify the principal strata parameters. Therefore, this study complements Huber et al. (2020) by offering another option for applied researchers to trade off the strength of the restrictions and richness of the parameters. In general, one can use my strategy for minimal key parameters and Huber et al.’s (2020) if stronger restrictions are justified to study the causal effect mechanisms in depth.

As a second contribution, I find that the CiC strategy does not necessarily require repeated outcome measures for point identification. I demonstrate that the CiC strategy with binary or discrete outcomes can be used to identify the treatment effect when there is a continuous proxy variable in the baseline. My approach again differs from Huber et al. (2020), who considered an identification with continuous repeated outcomes. Many rank imputation approaches involve rank similarity or a stronger version, rank invariance (Juhn et al., 1993; DiNardo et al., 1996; Altonji and Blank, 1999; Chernozhukov and Hansen, 2005; Machado and Mata, 2005). An alternative copula restriction also reveals the identification of the conditional quantile treatment effects (Callaway et al. 2018), but the rank similarity approach is dominant. More recently, Han (2020) used the rank similarity assumption to identify dynamic treatment effects with nonseparable models and de Chaisemartin and D’Haultfoeuille (2017) studied the fuzzy design of CiC models under the assumption of an exclusion restriction.

Among these rank similarity-based approaches, Athey and Imbens’ (2006) CiC strategy is a natural experimental approach. As a generalization of the DiD model, a CiC strategy considers repeated outcome measures. For example, the underlying motivation in Athey and Imbens’ (2006) CiC strategy was to examine the issue in the standard DiD model, specifically because discrete outcomes may be predicted outside their supports. However, a CiC strategy with discrete repeated outcomes does not identify the parameters without stronger restrictions. Thus, I demonstrate that a CiC strategy may work without repeated outcomes. Specifically, I reveal the process of identifying the parameters of interest with discrete outcomes predicted from a continuous proxy variable. The key observation is that I do not need to invert the distribution function of the control outcome, allowing for a discrete outcome measure for point identification. Random assignment helps to justify this strategy. Particularly, randomization creates symmetry in the control outcome and proxy variable distributions across the units with and without the intervention. This symmetry allows us to directly compare the potential outcomes observed for units without an intervention versus units with an intervention, rather than going through the unifying structural functions. One can seek a proxy variable that is not necessarily the exact repeated measure because the structural function with the common latent rank in RCTs does not serve any essential role. This finding is particularly important in the context of RCTs because repeated measures may be unavailable. For example, an outcome such as timely graduation from a school cannot be repeated; conversely, the administrative records of test scores may be applicable as the graduation proxy. In this example, while the DiD does not apply, the rank imputation strategy may allow us to identify the assignment and treatment effects.

As the third contribution, I propose an estimator of the rank imputation strategy that is valid for any type of outcome measure and can flexibly incorporate covariates that have been compared with Athey and Imbens’ (2006) implementation. I demonstrate its desirable finite sample performance in clustered sampling as well as its robustness to nonlinear mean outcome functions that invalidate Athey and Imbens’ (2006) parametric implementation. Specifically, Athey and Imbens (2006) proposed a nonparametric estimator with discrete covariates, but the implementation with continuous covariates took a restrictive parametric form. Similarly, Melly and Santangelo (2015) suggested a semiparametric estimator with covariates, in response to the general theory used by Chernozhukov et al. (2013); however, the strategy is less appealing for a CiC model without quantile functions of repeated outcome measures. Alternatively, I propose another semiparametric estimator based on distribution regressions. In Appendices A.1 and A.2, I discuss the weak convergence of the empirical process for the proposed counterfactual estimator and the validity of the bootstrap inferences. I also adopt Davezies et al.’s (2018) results of cluster-robust weak convergence to accommodate the experimental studies with cluster dependencies. I demonstrate the estimators’ finite sample performance in simulations in Appendix E.1 and compared this with Athey and Imbens’ (2006) incorporation of covariates in Appendix E.2.

I apply the proposed estimator in the context of an experimental approach in development economics. In particular, I use the data from Crépon et al. (2015), who conducted a large-scale microcredit experiment in Morocco, to estimate the ITTTA, representing the intervention’s combined effects. In addition, I separately estimate the ITTNA, which is the direct effect of the assignment for the nontreated, finding that the corresponding IV point estimate is 2.2 times larger than my preferred ITTTA estimate. Nevertheless, the estimated effects are not statistically different because of the large standard errors. The signs and magnitudes of the suggested ITTTA and ITTNA estimates may imply the possibility of a small, but positive direct assignment effect, while the treatment itself should have a large positive impact. As a result, I demonstrate that the small direct effect may be heavily biased in the ATT’s IV point estimate, which should equal the ITTTA under the exclusion restriction. I also apply my strategy to Gertler et al.’s (2012) two-sided noncompliance experiment that studied the long-term impact of a cash transfer policy in Mexico. In particular, I evaluate their claim that the assignment’s long-term effect is mainly caused by productive animal investments (See Appendix F for the description of the latter’s application).

The rest of this paper is organized as follows. Section 2 introduces the notations and parameters of interest, Section 3 lists the formal identification assumptions illustrated in cases of one-sided noncompliance, and Section 4 demonstrates the estimation procedure with uniformly valid and cluster-robust bootstrap inferences. I apply the procedure to an experimental microcredit study in Section 5, discuss the framework in the case of two-sided noncompliance models in Section 6, and present my conclusions in Section 7.

2 Parameters of interest

Consider a standard model of potential outcomes. Let be a binary randomized assignment and be an observed outcome generated out of the potential outcomes. Assignment indexes the potential outcomes and , such that . Assignment ’s average effect

is the ITT. The ITT involves any assignment effects, including the associated treatment effect that assignment enables or enhances. Although this unconditional ITT represents assignment ’s average effect, a study’s eventual goal often regards the associated treatment rather than the assignment.

Assume that the binary assignment of introduces another binary treatment . The units, which are the experimental subjects, choose endogenously after assignment . If a unit is assigned to the control group (), then the treatment is not available (). The units with assignment may not comply with the associated treatment . Therefore, may be either or if the unit is in the treatment group .

Definition 2.1.

A design satisfies the one-sided noncompliance if

The following is an example of a one-sided noncompliance experiment.

Example 2.1.

Microcredit experiments are an example of investigations in which researchers are aware of and interested in an assignment’s direct impact. Specifically, Crépon et al. (2015) studied the effect of introducing microcredit in Morocco’s rural areas. They randomly assigned villages into treatment villages and control villages , and the microcredit treatment followed one-sided noncompliance.

With treatment , the observed outcome is

where is the outcome given the assignment and taking up the treatment ; is the outcome given the assignment , but not taking up the treatment ; and is the outcome of the control group, with and . The leading parameter of interest is the following ITT conditional on and ,

| (1) |

I define the left-hand side of (1) as the ITTTA, where the equality to the right-hand side of (1) holds under Definition 2.1. Specifically, under Definition 2.1, the ITTTA is the combined effect of the ATT,

and assignment ’s effect on the treated, net of treatment

The latter parameter is often called the direct effect of the treated in the principal stratification literature (Hirano et al., 2000; Frangakis and Rubin, 2002; Flores and Flores-Lagunes, 2013; Mealli and Pacini, 2013) and mediation analysis literature (Pearl, 2014). Examining if the ITTTA is significant confirms that experimental assignment operates through the expected channel of treatment since intention or treatment have impacts, at least for the intended units that comply with the intention. As an analogue parameter, I consider

| (2) |

and I define the left-hand side of (2) as the ITTNA, where the equality holds under Definition 2.1. This ITTNA, the direct effect of the nontreated, has an important policy implication because it indicates if assignment has a direct impact on the outcome without considering the treatment. The left-hand-side definitions of the ITTTA and ITTNA represent the same parameters of interest for both one-sided and two-sided noncompliance, while their underlying principal strata differ. Nevertheless, the above interpretation remains similar (see Section 6 for details). The distinction appears when we are interested in separating the net effect of from the ITTTA and ITTNA (see Section 3.3 for one-sided noncompliance and Section 6.3 for two-sided noncompliance).

In RCTs, is randomly assigned, but the treatment may be endogenous. For one-sided noncompliance, running a regression of on and without covariates may produce a biased estimate in the coefficient of due to selection bias (Angrist and Pischke, 2009). Namely,

Therefore, researchers often employ random assignment as the IV for taking up treatment . Under three conditions, (i) random assignment , (ii) relevancy , and (iii) the exclusion restriction , the IV estimator identifies the ITTTA, which equals to the ATT,

where the last equality, based on the exclusion restriction (iii), may not hold. In particular, assignment may affect the outcome for those who do not take up treatment .

Example 2.2.

Crépon et al. (2015) listed several reasons why giving access to assignment may have an impact even for those who do not borrow from the microcredit institution:

There are good reasons to believe that microcredit availability impacts not only on clients, but also on non-clients through a variety of channels: equilibrium effects via changes in wages or in competition, impacts on behavior of the mere possibility to borrow in the future, etc. (Crépon et al., 2015, p. 124)

This possibility of the direct impact of availability not only complicates identifying the heterogeneous treatment effects but also emphasizes the importance of the direct impact for understanding the consequences of microcredit intervention.

If the exclusion restriction is violated, then the IV estimator also becomes a biased ITTTA estimator:

The degree of bias depends on the take-up rate . If , then the magnitude of the bias is less than , but the IV point estimate may have been inflated in absolute value through divisions of the small probability when the take-up rate is low.

Researchers frequently avoid using the IV estimator and report the ITT estimate because of the former issue of bias in the IV estimator. However, the ITT does not reveal the impact that appears because of the treatment in addition to the assignment (i.e., ITTTA), nor the impact appearing solely by the assignment (i.e., ITTNA).

Throughout the paper, represents conditional distribution function of the random variable for each and . Also, represents conditional quantile function of the random variable for each and . In the following section, we focus on the case of one-sided noncompliance. Therefore, we propose an identification strategy for the ITTTA

and its quantile differences evaluated at each percentiles

as wel as the direct effect of the assignment for non-treated, the ITTNA

and its quantile differences evaluated at each percentiles

exploiting the baseline survey, which is the typical feature of the randomized control trials. See Section 6 for the parameters and their identifications in two-sided noncompliance cases.

Replce somewhere

2.1 Subgroup effects and mediation effects

One may wonder why my focus is on the quantity

For the evaluation of the treatment without any further manipulations available, we need to evaluate the outcome functions at the value of post-treatment variables as people choose under their assigned policy , i.e., . Therefore, the random variable

is the relevant treatment effect for every unit . For example, borrowing decisions and parental investments are not policy variables to be manipulated by the policy makers in the evaluation or the implementation of the micro credit treatment and the Head Start treatment. Thus, the parameters essential for evaluating these treatments are the overall average effect as the unconditional mean of the above

as well as the subgroup average for those assigned to treatment and took an action ,

We would be interested in far more variety of parameters for different purposes. It is true that obtaining the structural function

is desirable if we are interested in the causal effect of on the outcome which is by itself an important parameter for understanding the mechanisms behind the treatment effects, or evaluations of a policy with both and are manipulable treatments. However, identification of the structural functions require either a presence of a valid instrument (for example, Chernozhukov and Hansen, 2005) or an assumption that is exogenous to conditional on (for example, ImaiKeeleYamamoto10). These assumptions may be challenging for some randomized experiment. The identification of the structural functions enables us to identify

which is called the direct effect as opposed to the indirect effect

in the literature of the mediation analysis (Pearl09 and ImaiKeeleYamamoto10). These quantities are useful when the policy has two stages whereas policymakers may consider forceful manipulation of the second stage which was not randomized in the experiment. Such motivation is the best described in a dynamic treatment effect model (Robins1986, 1987, MurphyvanderLaanRobinsCPPRG01 or Murphy03). Consider a medical trial with initial randomized treatment and subsequent post-treatment medical treatment. In such a case, we need to know the net causal effects of both treatments since the manipulation of the second treatment is also a candidate treatment. For example, consider a medical trial of Swan-Ganz Catheterization as studied in BhattacharaShaikhVytlacil12. Such a treatment of Swan-Ganz Catheterization offers a criterion for doctors determining further medical treatment . In this context, the mediation effects are essential to the evaluation of the Catheterization since both offering Catheterization and offering post-Catheterization actions are manipulable, and essential for the evaluation of the effect of treatments and as a policy. Relevant parameters in such question require either exogenous assignment of dynamic treatments (Robins1986, 1987, MurphyvanderLaanRobinsCPPRG01 or Murphy03 in Biostatistics under sequential randomization assumption), or a particular form of instruments as in Econometrics.111Han18 studies identification of the dynamic treatment effects in the presence of an instrument satisfying two-way exclusion restrictions. HeckmanHumphriesVeramendi16 also studies the dynamic treatment effects using conditional independence assumption or, instrumental variables. While these parameters are out of scope of this paper, my approach requires neither assumptions.

3 Identification

In this section, I consider the identification assumptions for the ITTTA and ITTNA illustrated through one-sided noncompliance designs.

3.1 Identification assumption

If an individualistic assignment causes a direct effect by altering the behavior of units, then the potential outcomes, trivially defined as stable unit treatment value assumption (SUTVA) (Rubin, 1980), can be justified. If there are spillover or equilibrium effects from community-level interventions, then SUTVA may be violated for the individual observation units. To accommodate the direct effects stemming from strategic interactions, as equilibrium behavior in taking up a treatment, I weaken SUTVA to create unique equilibrium potential outcomes that may depend on community to which unit belongs.

Assumption 3.1.

Let be a set of observations , with common assignment . For every , and , there are unique maps for a treatment indicator and potential outcomes with the corresponding values in support of .

Throughout this study, I assume that a random sample of units from the population consists of identical units, representing either individuals or communities. For example, the ITTTA

is the mean comparison of potential outcomes and from identical communities with against for the same type of members who would apply the treatment if their communities belonged to the treatment group , namely, . Under Assumption 3.1, the take-up and non-take-up subgroups are stable and unique for a given draw of communities. Nonetheless, I do not observe these take-up or non-take-up members in these communities without assignment . Therefore, I need an additional identification restriction. Below, I omit the index from the potential outcomes to simplify the notations.

Hereafter, I consider RCTs with the two consecutive surveys of baseline and intervention. Let denote a variable observed in the baseline survey to ensure that works as a proxy for the control outcome of interest . Let denote a vector of other pretreatment covariates observed in the baseline survey. I assume that the random assignment of is successful for the potential outcomes and and the baseline variable .

Assumption 3.2.

and

This randomization assumption is sufficient to identify the following ITT

Remark 1.

Assumption 3.2 is stronger than necessary for the ITT in the independence of from . I label this assumption as random assignment because of the restriction on , notwithstanding its similarity to the conditional ignorability for observational data (see Remark 2 for the role of covariates ).

My identification strategy is to exploit certain similarities in the proxy variable and control outcome . However, these two random variables, and , may have different distribution functions. Thus, I restrict the rankings of and to ensure that they are similar. Throughout the study, represents the conditional distribution function of the random variable , and constitutes the conditional quantile function of .

Definition 3.1.

is a vector of baseline covariates and random variable , indexed by each , is termed a (conditional) latent rank variable for random variable if

where and .

The above definition is a key departure from other rank imputation strategies. Many approaches, including Athey and Imbens’ (2006) and Huber et al.’s (2020), have assumed that a structural model shares the same scalar latent rank across potential outcomes. Such a structural assumption possibly imposes an obscure restriction on the nature of the random variable, especially when the outcomes are not continuously distributed. On the one hand, it is difficult to avoid such an additional structure function with a common latent variable across outcomes without randomization, as in Assumption 3.2. This is because there is no other way to convey the control outcome information from the no intervention units to the intervention units. On the other hand, the structure itself is more than necessary to identify the principal stratification effects when the groups are randomized. I do not assume that such a common latent rank exists across potential outcomes rather that latent rank variable exists for each potential outcome and is a definition as opposed to an assumption. Such a variable exists whether is finitely supported or continuous. In fact, we can always construct such a conditional latent variable . Let, , for the right-continuous conditional cumulative distribution function. Moreover,

where and , resulting in a quantile function that generates the random variable (see Rüschendorf’s (2009) Proposition 2.1 for the presence of such a latent variable).

For the identification, I impose two restrictions on the relationship between the proxy variable and the control outcome . First, I need to determine the complete latent ranking of , , over the entire support of . To achieve the requirement, I assume has a strictly increasing and continuous distribution function.

Assumption 3.3.

is the support of , and for every , is strictly increasing and continuous.

This assumption is required to point identify the parameter of interest. Although a partial identification is possible with a finitely supported proxy variable , this is beyond the scope of this study, as my primary focus is point identification.

Second, I assume that the latent rankings of and are similarly associated with (endogenous) treatment given . The latent rankings of the same correlation with D is an example of when following rank similarity restriction holds.

Assumption 3.4.

is the latent ranking of and is the latent ranking of , as defined in Definition 3.1.

for each , where is the support of conditional on .

Remark 2.

The distributions of and may differ arbitrarily, and and may be finitely supported for point identification. In Appendix C.6, I demonstrate that a binary may satisfy both Assumption 3.3 and 3.4 with a continuous proxy .

The repeated measure of in the baseline, namely , is not always available. The discreteness of further motivates the use of a nonrepeated because DiD may predict outside the allowable range. A that solely determines given is a good proxy because the latent rank of equals that of , which can be identically distributed with the latent rank of . As another example of a structure to determine a good proxy, an underlying unobserved determinant , in addition to identical shocks () called slippages, can determine both and (Heckman et al., 1997). In both cases, conditioning on affecting and may eliminate multidimensional relations that may violate Assumption 3.4. Appendix C.4 displays the conditions sufficient for Assumption 3.4 using structural models with illustrations for the microcredit example (Example C.1).

Note that the rank similarity restriction is on the reduced-form latent ranks. Structural modeling on the latent ranks helps us in justifying the restriction, but the model is not necessary. Randomization helps us in proceeding with reduced-form latent ranks because are common across treatment and control groups.

In addition, I assume the following restriction for the support of the covariates :

Assumption 3.5.

is the support of conditional that , and is the support of conditional that . Assume that .

Remark 3.

This assumption imposes a restriction on the population supports, and for the purpose of identification, one can justify Assumption 3.5 with RCT data.

3.2 Identification result

Given the above restrictions, I present the main result. The target parameter is the distribution , its quantile, and the mean computed from the distribution.

Theorem 3.2.

Proof.

See Appendix B. ∎

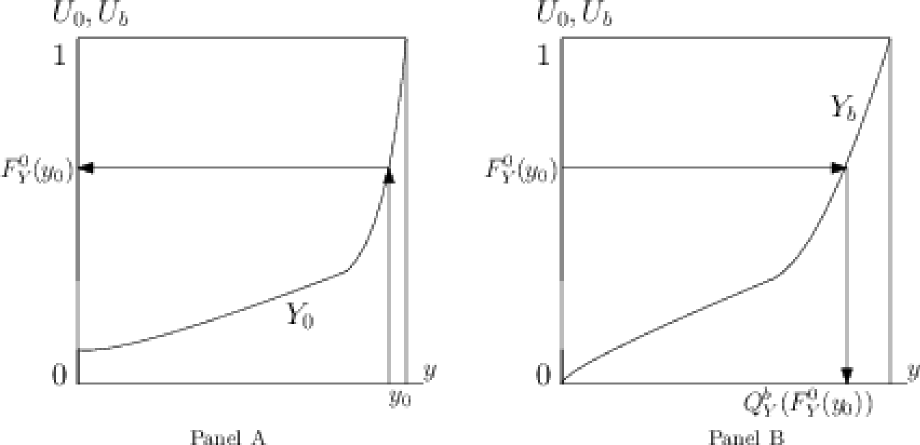

Figure 1 summarizes the concept underlying the formula. For simplicity, we can consider the case without the covariates W. As Panel A in Figure 1 describes, the events and are equivalent almost surely for every in the support of , . Although may have a positive mass in the support of , it does not hamper this step because we only need to evaluate in the support of . Rank similarity equates the events of and , with a conditional expectation of . As Panel B in Figure 1 shows, we may find the quantile of in the support of the random variable . Such a quantile can be found for every from the continuity of . Therefore, for every value of the latent rank , we can indicate its quantile in terms of . Then the events and have the same probability conditional on . Thus, I equate the conditional expectation of with that of .

While standard CiC approaches (Athey and Imbens, 2006; Huber et al., 2020) include a support condition for the latent rank variable, this condition is not presented in this study because I do not impose a structural function with a common latent rank variable across the functions. I define the latent ranks from the potential outcome as uniform random variables on , and impose a direct pairwise relation in unobserved ranking variables and . This direct relation is a distinction from the control function approaches (e.g., Imbens and Newey, 2009; D’Haultfoeuille and Février, 2015; Torgovitsky, 2015; Ishihara, 2020)

3.3 ATT identification with homogeneity restriction

With the rank similarity binding the control outcome and proxy variable, I present the ITTTA and ITTNA identification process without, for example, imposing restrictions on and . Although the ITTTA and ITTNA have important scientific and policy implications, I may be able to separate the ATT from the ITTTA if the following homogeneity assumption holds.

The above assumption indicates that the direct effect has the same mean for the treated and nontreated. This homogeneity assumption is related to the exclusion restriction, , and is substantially weaker. One can consider the exclusion restriction as a special case, as the homogeneous direct effect is 0. With the homogeneity, the ATT, , is simply the difference between the ITTTA and ITTNA, . This homogeneity restriction may be justified when the assignment effect is universal across units. For example, if the assignment causes an equilibrium effect on the local prices of essentials, then the homogeneity assumption may hold. By contrast, if the assignment causes a spillover effect that affects the treated and nontreated differently, then the assumption is implausible. Although this restriction is strong, I have two justifications for the above quantity. First, it is challenging to separate the ATT from the ITTTA unless scalar unobservable restrictions are imposed on both and . Second, the above quantity may still operate as a back-of-the-envelope calculation of the magnitude of the ATT. For example, as the spillover of microcredit access may represent a transfer from the treated to the nontreated, the direct effect for the treated may be lower than that of the nontreated. In that case, the ATT value may be underestimated with the back-of-envelope calculation (see Section 5 for its application to the microcredit experiment and Section 6 for the complexities of this concept for two-sided cases).

4 Estimation

As demonstrated in Section 3 and Appendix C.4, it is desirable to condition the distributions on pretreatment covariates to justify the conditional rank similarity. Dimensionality becomes a serious issue when we nonparametrically estimate conditional distribution functions for each subsample , with W containing continuous variables. Melly and Santangelo (2015) extended Athey and Imbens’ (2006) estimator to incorporate covariates into a semiparametric quantile regression model. However, semiparametric quantile regressions remain flexible only when they involve a smooth conditional density (see Chernozhukov et al. 2013). As my identification analysis now accepts as a binary or discrete random variable, the quantile regression approach may be undesirable. Therefore, I consider a distribution regression-based approach and incorporate Davezies et al.’s (2018) recent development of cluster-robust inferences for the empirical process. Finally, cluster dependency is inevitable in my leading examples and my inference strategy closely follows that of Chernozhukov et al. (2013).

I begin with a random sample of observations. Consider an estimation of the semiparametric conditional distribution functions. To estimate the parameter of interest, I first estimate the following distribution functions:

Hereafter, is a transformed vector of the original pretreatment covariates, such as polynomials or B-splines, and is the set of indexes for the subgroups, such as or . Following Foresi and Peracchi (1995) and Chernozhukov et al. (2013), I estimate the conditional distribution functions for conditional on a subgroup out of and as

for some known link function . I estimate as

for each where is the support of conditional on the subgroup and is a dimension of . For the main application in Section 5, I use the logit link function. Appendix D.2 shows the robustness to other link function choices such as probit link and complementary log-log link.

As an alternative, quantile function of for may be estimated directly. Following the quantile regression estimator of KoenkerBassett78,

where

Once these estimators are obtained, the conditional counterfactual distribution is

where

in which is the support of conditional on and is a corresponding percentile. Therefore, the unconditional distribution can be obtained by

where . The mean effect of interest is obtained as follows

and the quantile difference is obtained by inverting the distribution functions

For the random sample of clusters, rather than individual observations, I estimate

with

for each , where is the number of clusters and represents the size of each cluster . The difference appears in the bootstrap procedure and a few modifications under the assumptions of the data-generating process. In Appendices A.1 and A.2, I show that the proposed estimators are uniformly asymptotically normal. As a result, (clustered) exchangeable bootstrap inferences are shown to be valid for generating uniform confidence intervals (see also Appendices E.1 and E.2 for this estimator’s finite sample properties).

5 Application

5.1 Microcredit experiment in Morocco: background

Crépon et al. (2015) conducted a one-sided noncompliance experiment in the rural areas of Morocco, choosing target areas where the participant villagers had not experienced microcredit services before the experiment. This location choice was a novel feature of the study, and the authors estimated the relative effects of new access and no access, rather than the effect of expanding microcredit. Here, as introduced in Section 3, denotes the binary assignment (i.e., access to microcredit services) and D is the binary treatment of taking up microcredit. By construction, people in control villages, , automatically have . The administrative observation of the take-up decision validates the successful implementation of this procedure. Overall, the take-up rate is relatively low. As reported in column (1) of Table 2 in Crépon et al. (2015), only % of the treated units in the sample took a loan from the microcredit company. This number reduces to % with non-zero business outputs in the baseline survey.

For the present analysis, the most important feature is that Crépon et al. (2015) conducted a detailed baseline survey before the experimental intervention. The dataset comprised the production output market values before and after the experiment. Although this baseline survey feature is common in field experiments, only a few studies allow the application of my strategy, as they do not report take-up behaviors in the baseline sample. Based on the aforementioned information, denotes the baseline sales value output and indicates the endline sales value output.

In the experiment, a local microfinance institution called Al Amana entered randomly selected villages. After Al Amana opened new branches at the beginning of the study, the authors conducted a baseline survey containing all the outcome measures of interest as the terminal outcome measures. Upon completing the baseline survey, a randomization process separated villages into pairs with similar observed characteristics; one of each pair was randomly assigned as the treatment village and the other as the control village. Al Amana agents visited the treatment villages and promoted participation in microcredit, while the control villages had no access. At the time of intervention, all the newly opened branches offered fully functional services. For the control group, we can confirm that this one-sided noncompliance feature, in the administrative report of the proportion of Al Amana clients, is zero. The main sample in Crépon et al. (2015) is only a subsample (not the entire sample) of units that had a high borrowing probability. Although the study collected baseline survey observations for households, from villages, they also added the endline observations, totaling observations, as their analysis did not necessarily require a baseline survey structure. I use their extended sample in column (1) of Tables 1 and 3 to replicate their original estimates, but I limit the sample to the baseline survey units in the remainder of the study.

| (1) | (2) | (3) | (4) | |

| Model | OLS | OLS | OLS | OLS |

| Outcome | level output | log output | ||

| Assignment () | ||||

| () | () | () | () | |

| Self-employed in baseline | Y | Y | Y | |

| Strata dummies | Y | Y | Y | |

| Obs | ||||

| control mean | ||||

NOTE: Standard errors reported in parenthesis are clustered in village levels. *, ** and *** indicate statistical significance of 10%, 5%, 1% sizes respectively. Units in levels are Moroccan Dirham, 1MAD USD. Self-employed indicates that the estimates are for the subgroup of business owners at the baseline.

Table 1 shows the ITT estimates using regression analysis to control for the covariates, including number of household members, number of adults, the household head’s age, indicator variables for animal husbandry, other nonagricultural activities, outstanding loans over the past 12 months, household spouses as the survey respondents, and other household members acting as the survey respondents. These linear regression analyses are also conditioned for strata dummies (paired villages) except for column (4).

As column (1) shows, there is a positive and significant effect of microcredit access on production output sales. As my method requires a continuous , I restrict the study sample to individuals who had positive sales values in the baseline survey. As emphasized earlier, and do not need to be continuous. Conditional on , some observations with represent exit behaviors during the study period, and the mass at does not hamper the analysis.

This sample selection may change the interpretation of the effect but does not generate any bias. Columns (2) and (3) show the same estimates, except for self-employed individuals at the baseline. This procedure reduces the original sample size to approximately half. Column (2) shows the effect on the output level and column (3) shows the effect on the output log. As the output values contain zeroes, I apply the inverse hyperbolic sine transformation, , instead of the natural log. Therefore, the estimates interpret the approximated semi-elasticities for small effects. Overall, we need to convert the estimates using the hyperbolic sine formula to interpret the large coefficients, whereas the standard exponential approximation works well for this application to evaluate large means (for a detailed discussion, see Bellemare and Wichman, 2019). Both effects are positive and precisely measured, and the remainder of the arguments are all based on the log output, as the revenue distribution is heavily right skewed with a few outliers. It appears that the issue of outliers in the output values does not matter extraordinarily. Appendix D.3 presents additional results using the output level with or without trimming the extreme output values, which are consistent with the log output findings in the main analysis.

5.2 Original use of the baseline survey

Crépon et al. (2015) report the baseline survey for a similar purpose to mine. The purpose is to assess the heterogeneity in the ITT of the access to microcredit by subgroups with particular take-up decision. In particular, our shared concern is the possibility of the direct effect of microcredit access for those who do not take up credit.

As I quoted earlier in example LABEL:ex.micro.quote, there are many reasons why the access to microcredit might have a direct effect even though people do not take up credit. For example, the promotion of the credit company might encourage small business owners to continue their business. Because of the new access, the owners expect to have additional credit available in the future even though they are not borrowing right now. The nature of the village level assignment also generates equilibrium effects and peer effects. The expanded credit use in the treatment village would alter the interest rates of informal lending and product prices within the village as equilibrium realizations. Furthermore, nonborrowing people might receive transfers from relatives and friends who succeed in their business due to borrowing, while these people might also need to cover the payment for the debt of failing relatives.

The idea of the original study is to estimate the propensity to borrow from microcredit using covariates from a baseline survey. In other words, the parameter

is identified, where . With this parameter, one might test the following hypotheses

and

Table 2 shows the results in the original article based on a regression analysis. The results suggest that the units with top 30% of the propensity score have a more substantial and significant effect, while the units with bottom 30% have a small and insignificant effect.

| Outcome: | output | output | log output |

|---|---|---|---|

| (1) | (2) | (3) | |

| High 30% | 15773.7*** | 13647.2** | 0.4736** |

| (4153.6) | (6095.3) | (0.1985) | |

| Low 30% | 646.6 | 1818.3 | 0.2739 |

| (2701.1) | (4088.1) | (0.1900) | |

| Sample selection | |||

| Self-employed | Yes | Yes | |

| control mean | 30,450 | 33,554 | 8.7079 |

| Obs | 4,934 | 2,453 | 2,453 |

Note: Standard errors reported in parenthesis are clustered in village levels. *, ** and *** indicate statistical significance of 10%, 5%, 1% sizes respecively. Self-employed indicates that the estimates are for the subgroup of business owners at the baseline.

However, testing or do not necessarily relate the primary interest of whether the direct effect exists and invalidate the use of IV estimator. First, the event of the low propensity score might be different from the event of no take-up under treatment . The subgroup of nonborrowers might be sorted on unobservables by , but the propensity score based strategy allows sorting only on observables . Second, as we see in the discussion of the identification section, a small violation to the exclusion restriction might result in a large magnitude of the bias in the ATT when the take-up probability is low. Therefore, a small violation to the null , which is not detectable, might generate a huge bias in the ATT.

Table 3 shows the original and additional IV estimates that are valid only if the direct effect for the treated is zero. Under the conventional assumption, the estimated ATT may overestimate the effect for the treated, implying that policymakers may be overly encouraged to promote microcredit services. Thus, I compare my preferred estimate for the ITTTA with these two-stage least squares (2SLS) ATT/ITTTA estimates. The 2SLS estimates in columns (2) and (3) include paired village dummies, following Crépon et al.’s (2015) original specification. For my later estimates, I do not include these paired village dummies to prevent the incidental parameters problem for nonlinear estimators. Nevertheless, the 2SLS estimate with dummies in column (4) has a similar magnitude to the estimate without dummies in column (3), indicating that strata dummies improve their precision.

| (1) | (2) | (3) | (4) | |

| Model | 2SLS | 2SLS | 2SLS | 2SLS |

| Outcome | level output | log output | ||

| Treatment () | ||||

| () | () | () | () | |

| Self-employed in baseline | Y | Y | Y | |

| Strata dummies | Y | Y | Y | |

| Obs | ||||

| control mean | ||||

NOTE: Standard errors reported in parenthesis are clustered in village levels. *, ** and *** indicate statistical significance of 10%, 5%, 1% sizes respecively. Self-employed indicates that the estimates are for the subgroup of business owners at the baseline. 2SLS stands for the two-stage least squares method.

5.3 ITTTA and ITTNA estimations

With the baseline outcome as the proxy for the control outcome , I can directly identify the counterfactual distribution of conditional on the endogenous subgroup for each (see Section 3 for details of this procedure).

Outcomes and are the production output sales values stemming from small business activities. Based on the random assignment of credit access and the fact that microcredit was not available during the baseline period or for control villages, these two outcomes, and , should be similar, except for the random shocks occurring over the study’s two-year period. Appendix C.4 offers detailed arguments to justify the rank similarity based on the so-called slippages argument (Heckman et al. 1997). In this study, although the rank similarity assumption does not have any testable restrictions per se, I conducted a diagnostic test supporting the rank similarity assumption in this application (see Appendix D.4 for results and other details).

Table 16 shows the estimates of the subgroup effects unconditional on achieved by integrating out. Column (1) represents the ITTNA, the direct effect for the nontreated with assignment . Column (2) addresses the ITTTA, as the combined effect of taking up treatment , with takers gaining access to assignment . In column (3), I offer a back-of-the-envelope calculation of the treatment’s net effect, or the ATT, as discussed in Section 3.3.

| (1) | (2) | (3) | |

| Model | RS | RS | RS |

| Parameter | ITTNA | ITTTA | ITTTA - ITTNA |

| Outcome | log output | ||

| Assignment () | |||

| by subgroups of () | () | () | () |

| Self-employed in basline | Y | Y | Y |

| Obs | |||

NOTE: Standard errors reported in parenthesis are generated from 300 bootstrap draws clustered in village levels for (1)-(3). *,**,*** indicates statistical significance of 10%,5% and 1% sizes respectively. Logit link is used for (1) and (2). RS stands for the rank similarity estimator proposed in this paper.

As shown in column (2), the ITTTA is strongly positive and significant, but its magnitude is less than % of the 2SLS estimate, which should have been similar to the ITTTA if the direct effect for the treated was zero. A cautionary note when interpreting the difference between the two point estimates for the treated is that it is not statistically significant. As the p-value of the test for this difference is , it is not possible to conclude that the proposed estimate implies that the 2SLS estimator is biased. Indeed, this insignificance appears in column (1), as the ITTNA, representing the estimated direct effect for the nontreated, is insignificant. If the direct effects are homogeneous, then the magnitude and insignificance of the ITTNA may correspond to the magnitude and insignificance of the difference between the ITTTA and IV. By combining the ITTTA and ITTNA signs and magnitudes, may still have a positive direct but imprecisely estimated effect. Nevertheless, we cannot distinguish imprecisely estimated small effect against no effect.

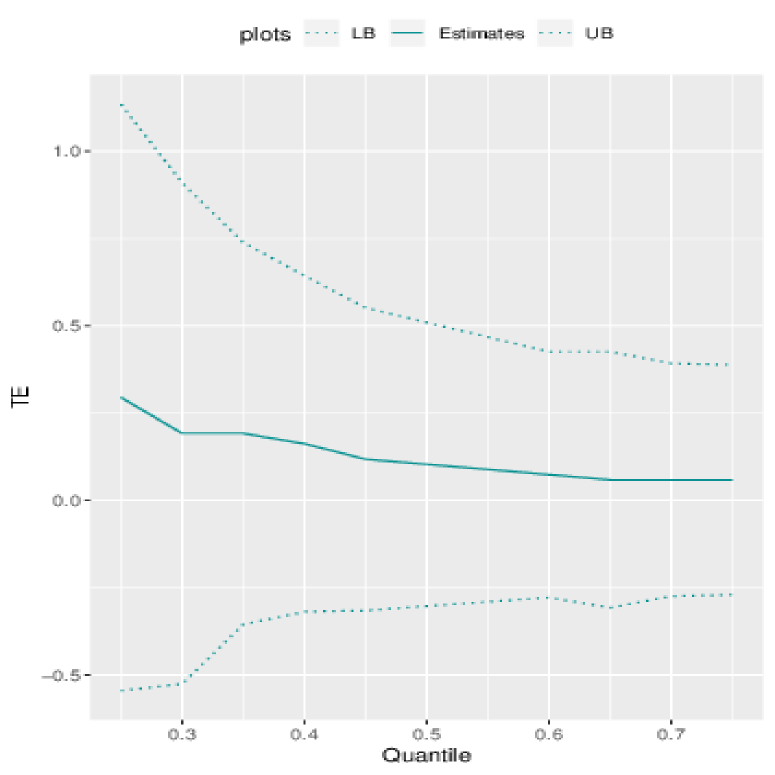

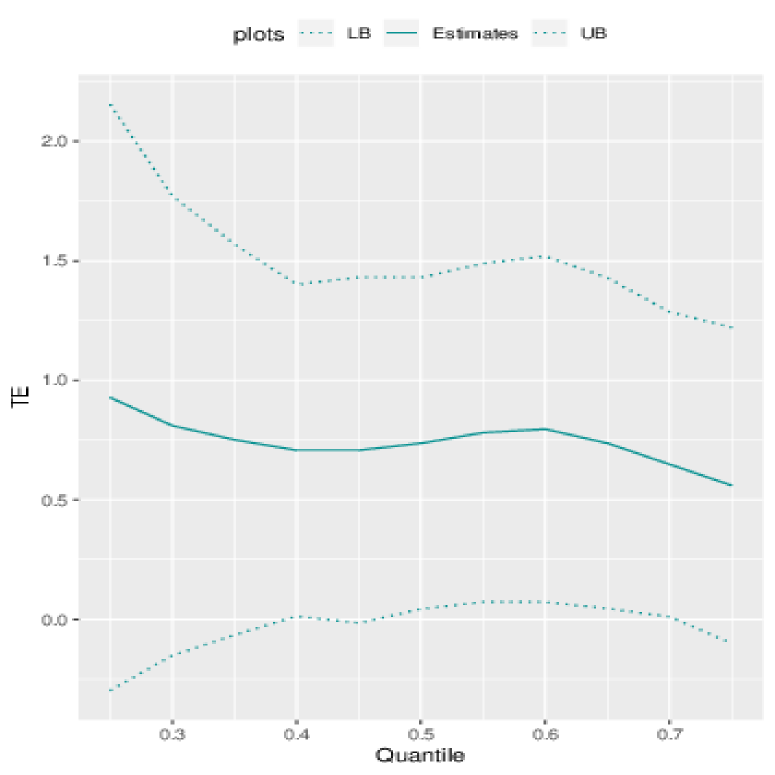

Column (3)’s ATT back-of-the-envelope calculation suggests a sufficiently large effect from the treatment itself. Although the validity of this estimate depends on the homogeneity of the direct effect, the direct effect may be smaller for the treated than the nontreated, as discussed in Section 3.3. Therefore, it is assuring to see the positive and marginally significant effect confirming the ATT’s positivity. In Appendix D.1, I display the quantile differences of the direct effects for the nontreated, , (Figure 1) and the quantile difference of the combined effects for the treated, , (Figure 2), along with uniform % confidence intervals. The results indicate the relatively monotonous effects over the range of quantile values for the combined effect of the treated. Specifically, the quantile differences are conditional on those who had businesses at the baseline. Therefore, this result does not contradict previous findings that business revenue effects appear in the upper tail of the distributions (Angelucci et al., 2015).

Although Table 16 findings may alter policymakers’ decisions, I must clarify two limitations of this analysis. First, the focus of this study was limited to the subsample of business owners before the experiment. Second, the conventional IV estimate and my preferred estimate differ, but not statistically. Therefore, my empirical results should be considered as additional evidence for policymakers. I encourage future researchers to collect a detailed baseline survey to evaluate the intervention of interest and further understand the nature of the treatment effect through the ITTTA and ITTNA.

6 Two-sided noncompliance

Thus far, I have focused on one-sided noncompliance cases because two-sided noncompliance designs are complicated by the dynamic nature of taking up the treatment. This complication further distinguishes my analysis from the previous literature, including Huber et al. (2020), by selecting plausible kinds of latent rank restrictions separately for each design. In two-sided noncompliance cases, the practical complication involves justifications for the rank similarity assumption for which the rationale is that the underlying latent rank of the control outcome and proxy variable would be similar conditional on the endogenous subgroups of and . In one-sided noncompliance cases, the similarity of and is a natural concept because both variables are determined when neither nor is available. For two-sided noncompliance designs, is no longer a purely comparable outcome with . As the control units may have taken up treatment without assignment , represents the outcomes nontreated and treated under . Below, I articulate my argument for two-sided noncompliance designs in two cases.

If and denote the potential choice under assignment , then . A two-sided noncompliance experiment is a design generated from for both . The observed outcome takes the following form:

| (3) |

where represents the outcome with assignment and treatment .

The main parameters stay the same as the ITTTA and ITTNA. Under the monotonicity of almost surely, they have similar interpretations. The ITTTA is a principal stratification effect of for the union of basic principal stratum . The ITTTA is also the sum of the effect from the intended channel for the complier, , and the assignment’s direct effect for the treated holding the same treatment status in the control, . Therefore, verifying the ITTTA can still determine whether has an impact, at least for those who comply with intention . The ITTNA is the same direct effect by monotonicity. Nevertheless, the identification rationale may differ.

6.1 Treatment available before the randomized assignment

Consider a two-sided noncompliance experiment where treatment may be available before the assignment of . If the same treatment had been available in a previous period, but assignment encouraged taking up , then the rank similarity strategy for one-sided noncompliance cases may still work out. Nevertheless, the justification for Assumption 3.4 should be based on and , instead of . The key notion is the stability of taking up treatment within the units without the assignment. While was available in the baseline, no factors should affect take-up behavior in the control group . Therefore, the distribution should not change in the control group over time. If is the treatment in the baseline and and are the baseline proxies with and without , then . With these notations, I propose the following modified rank similarity assumption.

Assumption 6.1.

This modified rank similarity imposes that the latent rankings do not change in and for those who maintained the same treatment status without assignment , and who would behave similarly in . With this modified rank similarity, the ITTTA and ITTNA are identified when the compliance rates are stable over time without the assignment (see de Chaisemartin and D’Haultfoeuille 2017, Assumption 2).

Corollary 6.1.

6.2 Two-sided noncompliance, but not before the experiment

Next, I consider treatment introduced after assignment . In this case, it is difficult to justify the rank similarity in an analogous manner. While now contains the outcome of taking up treatment , cannot have this component in the baseline. Thus, I consider a modification to the rank similarity to deal with this difficulty. The weakened rank similarity assumption imposes a restriction only for the nontreated, solely restricting on the latent ranks of and given and .

Assumption 6.2.

Given this weaker restriction, I show the ITTNA identification process, but not for the ITTTA.

Theorem 6.2.

Proof.

See Appendix B. ∎

The ITTTA may still be identified from the total law of expectation using the ITT estimate. In other words, . Nevertheless, it is limited in its precision when it must be divided by the small probability of if the take-up rate is low. In addition, the ITTNA can be the only parameter of interest in some two-sided noncompliance designs. In Appendix C.4, I provide an example of the selective attrition problem, which is illustrated with van den Berg and Vikström (2014), to show the usefulness of Theorem 6.2 on its own.

Corollary 6.3.

Consider the differential attrition model as specified above. Suppose assumptions 3.1, 3.2, and 3.5 hold and, assumption 3.3 holds for a baseline variable conditional on . Let be the latent ranking of conditional on .

Suppose further that assumption 6.2 with , and the monotonicity in the form of almost surely holds. Then

so that we have identification of

Proof.

The proof immediately follows as a special case of theorem 6.2 by flipping the order of the monotonicity from to , and focused on the case of which implies almost surely. ∎

Remark 4.

The same approach may not work if the differential attrition works in the other way, namely . Nevertheless, if we may assume the rank similarity in and conditional on , then the same argument works to identify

6.3 Identifying other parameters

The limited identifiability in Theorem 6.2 derives from the restriction’s weakness, which is typical of a two-sided noncompliance design. Further, the proposed rank similarity approach itself cannot identify the other parameters studied in Huber et al. (2020), such as the net (indirect) effects of for the compliers or other principal strata. The critical difference lies in their restrictions on the model. As with other CiC models, Huber et al. (2020) assumed that the potential outcomes share a common latent rank variable across . Given that the same single unobserved scalar governs all the outcomes with and without assignment within a strong model, the restrictions on the common latent variable allow them to identify all the mediation parameters. Huber et al. (2020) successfully found the mechanical latent rank conditions needed for each mediating effect, but the rationales for each latent rank restriction is not provided. Specifically, for operations involving the treated outcomes , it is challenging to justify the associated latent rank restrictions. Further, it is difficult to weaken Huber et al. (2020) restrictions because the latent rank restrictions are not separated from the model.

In this study, I do not impose such a model, but the potential outcome structure. With only the potential outcome structures, I explicitly declare which latent rank restrictions could be plausible under what kinds of designs, thereby offering a conservative approach to identifying the key principal stratification parameters. Nevertheless, I consider the net effects of treatment , which is the ATT, with a homogeneity assumption rather than the latent rank restrictions for or , as shown in Section 3.3. A similar procedure is possible in two-sided noncompliance designs. In Appendix C.2, I describe the identification process of the following net effect of for the complier, similar to the local average treatment effect (LATE):

| (4) |

under a homogeneity assumption, , that is stronger than that discussed in Section 3.3. The formula follows because when almost surely. As in Section 3.3, the above net effect may still work as a back-of-the-envelope calculation when the homogeneity assumption is violated. (see Appendix F for the empirical application of two-sided noncompliance and homogeneity assumption justifications).

7 Conclusions

This study presents a method that does not require any additional instruments, treatment exogeneity, or specific experimental designs to identify treatment effect heterogeneity across endogenous decisions in randomized experiments. In contrast to the existing literature, I used a variable from a baseline survey to proxy for the control outcomes. I then offered a procedure to directly identify the ITTs conditional on endogenous strata using proxy variables from the baseline survey. My chosen method produced three distinct novelties. First, exploiting the baseline survey—a typical feature of experimental studies—the relatively conservative natural experimental approach in RCTs offers fewer parameters, which are identified through substantially fewer model structures and weaker restrictions, than in the recent work of Huber et al. (2020). Second, I only required the continuous variable to act as a proxy variable, not as the outcome of interest. Unlike in standard CiC models, I expanded the considerations of the proxy variable, not necessarily representing a repeated outcome measure, and this flexibility allowed for identification with discrete outcomes. This feature is critical, as the exact repeated outcome measure may not be available in a baseline survey. Therefore, this method allows us to apply a CiC strategy to nonrepeatable binary outcome measures, such as survival events and degree attainment. As the DiD strategy is not available without identically comparable repeated outcomes, this feature has added value to the CiC strategies themselves. Third, I proposed estimators that have several desirable properties, including flexible covariates, outcome specifications, and clustered sampling robustness.

Under the exclusion restriction requiring that the assignment’s direct effect be 0, the ITT conditional on the treated, which I termed the ITTTA, must equal the ATT. In the microcredit application, I found that the conventional IV estimate for the ITTTA/ATT is 2.2 times larger than that of my preferred estimate, while the estimates are not statistically different. As the estimates are not distinguishable due to large standard errors, my empirical result does not offer a conclusive statement on the validity of the conventional estimate. In addition, my comparison may not be fair because the focus of my procedure was limited to a subsample of business owners. Nevertheless, this study highlights the importance of directly identifying treatment effect heterogeneity. Overall, I provide an option for applied researchers to further understand treatment effects and accordingly offer better policy guidelines.

By allowing nonrepeated measures within CiC strategies, additional research questions arise for the identification of treatment effects. For example, the need for a continuous proxy is a major limitation of the proposed procedure, emerging as the limited interpretability of the results in this study. Overall, continuous baseline variables are not always available. Thus, identification without a continuous proxy is an important future research topic. The estimation procedure followed a specific semiparametric distribution regression to tackle the possible high dimensionality. However, the proposed procedure may have resulted in a small sample problem when many discrete covariates were present. Testing rank similarity restrictions is also an important future research direction. In Appendix D.4, I implemented a version of Dong and Shen’ (2018) means test for rank similarity through baseline covariates. Although the diagnostic test is successful, more sophisticated rank similarity tests that require additional data and restrictions are desirable in this context. In particular, for one-sided noncompliance experiments, the endogenous taking up of a treatment will not be observed in a control group and this produces tougher challenges for testing rank similarity. Overall, undertaking these identification and estimation issues remains an important topic for future research.

Supplementary Material

- Supplementary Appendix:

-

Asymptotic statement for the proposed estimators (the Appendix A), proofs for the statements in the main text (the Appendix B), additional discussions (the Appendix C), additional figures and tables (the Appendix D), Monte Carlo simulations for the estimators (the Appendix E) , and an additional empirical application with a two-sided noncompliance experiment (the Appendix F). (.pdf file)

- Data and Codes:

-

R-package (ptse) and replication codes for results in Section 4, Appendix D and F, and Datasets for applications, downloaded from ICPSR websites (https://doi.org/10.3886/E116333V1) for Crépon et al. (2015) and

(https://doi.org/10.3886/E116375V1) for Gertler et al. (2012). (.zip file)

Acknowledgement

I thank Edward Vytlacil, Yuichi Kitamura, Yusuke Narita, Mitsuru Igami, and Joseph Altonji for their guidance and support. I have benefited from comments particularly from Sukjin Han, Hiro Kasahara, Donhyuk Kim, Jinwook Kim, Yoshiaki Omori, Jeff Qiu, Pedro Sant’Anna, Kensuke Teshima, and seminars participants at Yale, 2018 Kyoto Summer Workshop, Workshop on Advances in Econometrics 2019, Osaka School of International Public Policy, Hitotsubashi Institute of Economic Research, Kyoto Institute of Economic Research, Auburn University, Kansas State University, and Yokohama National University. All errors are my own. This paper was a dissertation chapter and previously circulated as a job market paper titled “Identification and inference of post-treatment subgroup effects.” This work is supported by Research Grants for Young Researchers, Hitotsubashi University.

Supplementary Appendix

Appendix A Asymptotics for the proposed estimators

A.1 For random sample of individual observations.

I first assume the data generating process satisfies the following restrictions:

Assumption A.1 (DGP).

The sample is an iid draw from the probability law over the support . Let be a support of conditional on , and let and be supports of and conditional on and for each .

Assume the following

-

1.

and are compact subsets of for each .

-

2.

If is absolutely continuous with respect to the Lebesgue measure, then suppose the conditional density is uniformly bounded and uniformly continuous in .

-

3.

and are uniformly bounded, and uniformly continuous in and for each .

-

4.

for each , and .

I also assume that the conditional distribution functions have the following semiparametric forms

Assumption A.2 (Distribution Regression).

Suppose we have

for some link function for all . For this specification, assume that the minimal eigenvalue of

is bounded away from zero uniformly over , where is the derivative of . Assume also that the analogous restriction holds for

and

for each .

Assume further that .

This is a standard regularity condition for distribution regression models (Chernozhukov et al., 2013).

Under these assumptions, these conditional distribution functions weakly converge jointly. Let

for every .

Lemma A.1.

Proof of Lemma A.1.

Step 1: Weak convergences of Z-functions

For the proof of Lemma A.1, we would like to introduce approximate Z-map notations.

For every , let be -vector of population moment equations such that the true parameter solves the moment condition . Let be an empirical analogue. Let an estimator satisfies

where is a numerical tolerance parameter with .

Let be an approximate Z-map which assigns one of its -approximate zeros to each element so that

For each , let

and for each . Also let , and be -vector valued functions with each q-th coordinate being , and .

In Lemma A.2 below, it is shown that the union of classes of functions

is -Donsker with a square-integrable envelope function. Let and for each , then the Donskerness implies

in where for each are -Brownian bridges.

Step 2: Applying Functional Delta method through the stacking rule

From the first order conditions, for each and , and for each for every .

Following the argument of Chernozhukov et al. (2013), the three kinds of approximate Z-maps are Hadamard differentiable for each case, and from the stacking rule as in Lemma B.2 of Chernozhukov et al. (2013), we have

in by the functional delta method.

Step 3: Applying another Hadamard differentiable map to conclude the statement

Finally, consider the mapping such that

for every . From the Hadamard differentiability of at tangentially to with the derivative map . From the stacking rule, applying the mapping for each process, the statement of the lemma holds. ∎

Lemma A.2.

Under the assumptions of Lemma A.1, the class of functions

is -Donsker with a square-integrable envelope.

Proof.

From Theorem 19.14 in van der Vaart (1998), a suitable measurable class of measurable functions is -Donsker if the uniform entropy integral with respect to an envelope function

is finite and the envelope function satisfies .

Consider classes of functions

which are VC classes of functions. Note that the target class of functions is the union of

for each and

for each . These are Lipschitz transformation of VC-class of functions and finite set of functions and where the Lipschitz coefficients bounded by . Therefore, from Example 19.19 of van der Vaart (1998), the constructed class of functions has the finite uniform entropy integral relative to the envelope function , which is square-integrable from the assumption. Suitable measurability is granted as it is a pointwise measurable class of functions. Thus, the class of functions is Donsker. ∎

Lemma A.3.

Proof.

As in Step 2 in the proofs of Theorem 5.1 and 5.2 in Chernozhukov et al. (2013), and are uniformly bounded “parametric” family (Example 19.7 in van der Vaart (1998)) indexed by for each respectively. From the assumption that the density function is uniformly bounded,

for some constant for every . The compactness of implies the uniform -covering numbers to be bounded by independent of so that the Pollard’s entropy condition is met. Therefore, the class of is suitably measurable as well. As indicator functions of all rectangles in form a VC class, we can construct that contains union of all the families and and the indicators of all the rectangles in that satisfies DKP condition.

∎

Given the weak convergence of the distribution regressions, the conditional estimator

is in the form of following map: for distribution functions ,

where is the quantile function from . In a parallel argument to Melly and Santangelo (2015) based on quantile regressions, the above map is Hadamard differentiable from the Hadamard-differentiability of the quantile function (Lemma 21.4 (ii), van der Vaart, 1998) and the chain rule of the Hadamard-differentiable maps (Lemma 20.9, van der Vaart, 1998).

Lemma A.4.

Let and be uniformly continuous and differentiable distribution functions with uniformly bounded densities and . Let be also a distribution function. Suppose has a support as a bounded subset of real line, and for every .

Then the map is Hadamard differentiable at tangentially to a set of functions with the derivative map

For the proof of the Hadamard derivative expression, I show the following lemma.

Lemma A.5.

Suppose is a uniformly continuous and differentiable distribution function with uniformly bounded density function with its support where . Let for all .

Let be a distribution function over a support , then is Hadamard differentiable at tangentially to a set of function with the derivative map

Proof.

From the assumption, we have

Let uniformly in as , and let and . Then uniformly in as by the assumption.

Thus, we have

so that we have

whereas the RHS has a limit

by the uniform differentiability of .

∎

Proof of Lemma A.4.

First, let so that . From the lemma A.5 and the lemma 21.4 (ii) from van der Vaart (1998), is Hadamard differentiable at tangentially to the set of functions with the derivative map

Therefore, from the Chain rule of the Hadamard differentiability (Lemma 20.9, van der Vaart, 1998), the map is Hadamard differentiable with the derivative map shown in the lemma. ∎

Next, let

where for where is a class of suitably measurable functions 222Suitably measurability or -measurability can be verified by showing the class is pointwise measurable. A class of measurable functions is pointwise measurable if there is a countable subset such that for every there is a sequence such that for every . For example, the class is pointwise measurable. This is because we can take which is countable, and for arbitrary which characterise the arbitrary function , and the sequence of functions such that converges to . Therefore, the relevant class used here is shown to be pointwise measurable. including

and all the indicators of the rectangles in .

From the derivative expression in the lemma A.4 and the joint weak convergence of the empirical processes, the counterfactual conditional distribution weakly converges.

Theorem A.6.

Proof.

From Lemma A.3, we can choose satisfying the requirement defined earlier so that satisfies the DKP condition (Chernozhukov et al., 2013, Appendix A.). Then assumptions of Lemma E.4 in Chernozhukov et al. (2013) is satisfied to conclude the first statement.

For the second statement, note that

Therefore, the functional delta method and the Hadamard differentiability of the transformation implies the above process weakly converges to the process shown in the statement. ∎

The unconditional counterfactual distribution is attained by applying Lemma D.1 from Chernozhukov et al. (2013) showing the Hadamard differentiability of the counterfactual operator

Theorem A.7.

Proof.

Note that

and

Also we have,

From the Slutzky lemma (Theorem 18.10 (v) in van der Vaart, 1998), Functional delta method, and the Hadamard differentiability of the operator (Chernozhukov et al., 2013, Lemma D.1), we have

where

Therefore, continuous mapping theorem (Theorem 18.11 in van der Vaart, 1998) implies the statement. ∎

Proof.

Immediate from the Hadamard-differentiability of the quantile function (Lemma 21.4 (ii), van der Vaart, 1998). ∎

Proof.

Let be the mapping . Let as and let . Then it is Hadamard differentiable at tangentially to a set of functions such that

Since

the statement holds. ∎

Given the asymptotic normality, I propose an inference based on a bootstrap procedure. Suppose the bootstrap draws are exchangeable.

Assumption A.3 (Exchangeable bootstrap).

Let is an exchangeable, non-negative random vector independent of the data such that for some ,

where , and is an outer probability measure with respect to .333For an arbitrary maps on a metric space and a bounded function ,

Let be the bootstrapped version of the estimators using

and let

where .

Corollary A.10.

A.2 For clustered samples

Now consider the asymptotic property of the clustered version of estimator. First, I assume the following data generating process:

Assumption A.4 (Cluster DGP).

Let denote clusters, and an index denote individual ’s observation in a cluster .

Suppose the following restrictions:

-

1.

is exchangeable, namely, for any permutation of ,

and clusters are independent across .

-

2.

and .

-

3.

is supported for and has a finite support .

-

4.

the same support and density conditions as in Assumption A.1.

-

5.

where

for each , and .

Furthermore, I modify the moment condition as follows:

Assumption A.5 (Distribution Regression and Cluster Moment Condition).

Suppose we have

for some link function for all . For this specification, assume that the minimal eigenvalue of

is bounded away from zero uniformly over , where is the derivative of . Assume also that the analogous restriction holds for

and

for each . Assume further that .

Remark 5.

The additional assumption of is replacing the square integrability of the envelope function for a class of Z-maps as the first order conditions of the semiparameteric distribution regressions.

From the linearity of the expectation operator, it is sufficient to have the cluster size finite as well as the previous moment condition for every .

Let

and

where

and

for each .

Corollary A.11.

Under assumptions for Theorem 3.2, and, Assumptions A.4 and A.5, we have

in , where for every are tight zero-mean Gaussian processes with each covariance function of the form

where

for each and , and we have

in for suitably measurable specified earlier where is a tight zero-mean Gaussian process with the covariance kernel

Proof.