On Polyhedral and Second-Order Cone Decompositions of Semidefinite Optimization Problems

Abstract

We study a cutting-plane method for semidefinite optimization problems, and supply a proof of the method’s convergence, under a boundedness assumption. By relating the method’s rate of convergence to an initial outer approximation’s diameter, we argue the method performs well when initialized with a second-order cone approximation, instead of a linear approximation. We invoke the method to provide bound gaps of - for sparse PCA problems with s of covariates, and solve nuclear norm problems over matrices.

keywords:

Semidefinite optimization , Cutting plane , Nuclear norm , Sparse PCA.1 Introduction

We study decomposition schemes for semidefinite optimization problems (SDOs) of the form:

| (1) | ||||

| s.t. |

Problem (1) is tractable from a traditional complexity theory perspective, because we can solve it

to -optimality in polynomial time

via interior point methods (IPMs); see Ramana [18] for a complete characterization of the complexity of SDOs. However, it is notoriously difficult to solve in practice, because IPMs memory requirements scale at a demanding rate. Indeed, state-of-the-art SDO solvers such as MOSEK cannot solve constrained instances of Problem (1) with variables on a standard laptop, and it is optimization folklore that there is a gap between SDOs theoretical and practical tractability.

Motivated by the demanding memory requirements of IPMs, a stream of literature studies inexact methods for SDOs, which replace the semidefinite constraint with weaker yet less computationally demanding constraints. This approach was first investigated by Kim and Kojima [12], who observed that relaxing a positive semidefinite constraint to the weaker constraint that all minors of a matrix are positive semidefinite yields a second-order cone (SOC)-representable outer approximation of the positive semidefinite (PSD) cone.

In a related line of work, Krishnan and Mitchell [14] propose applying Kelley [11]’s cutting plane method to generate an improving sequence of outer approximations of the positive semidefinite cone. Their approach converges whenever the feasible region is bounded, albeit exponentially slowly in the worst-case. Unfortunately, in [14]’s implementation, Kelley’s method performs poorly in practice and often provides weaker bounds than those obtained by enforcing SOC-representable minor constraints, as found empirically in [21, 1].

From a traditional complexity theory perspective, the slow rate of convergence of Kelley [11]’s method is unsurprising. Indeed, SDOs cannot be approximated arbitrarily well using polynomially-sized linear optimization problems (LOs) [5, Proposition 3], and therefore any LO-based cutting-plane method for SDOs converges exponentially slowly in the worst-case. However, there are numerous examples of cutting-plane methods with slow worst-case rates of convergence which nonetheless successfully solve large-scale problems in practice [see 6, 9, 4, and references therein]. Moreover, optimizers widely believe that there is a gap between the observed and worst-case performance of cutting-plane methods [see 16, Section 5.2]. Therefore, a slow worst-case rate of convergence does not preclude Kelley’s method from performing well in practice.

1.1 Our Contributions

In this paper, we provide a different perspective on Kelley’s method than the traditional complexity theory perspective. By bounding the number of iterations required to obtain an -feasible solution to Problem (1), we establish that the method’s worst-case performance depends explicitly on the diameter of an initial outer approximation of the problem, and argue that this dependence also appears in practice.

By examining this worst-case bound, we diagnose why existing implementations of Kelley [11]’s method do not scale well in practice. Namely, they are initialized with LO-representable outer approximations of the PSD cone, which do not capture its inherent nonlinearity. Indeed, as we establish in Section 2, the diameter of an LO-representable approximation grows linearly with , and therefore the rate of convergence of Kelley’s method (under this initial approximation) depends upon . After observing that Kelley’s method performs poorly in both theory and practice with an LO-representable initial approximation, we propose initializing Kelley’s method with a SOC-representable approximation. We establish that (a) the diameter of this approximation grows at the slower rate of , and (b) initializing a cutting-plane method with a SOC approximation performs better in both theory and practice.

Finally, we apply Kelley’s method to two problems from the machine learning literature: sparse principal component analysis (PCA) and nuclear norm minimization. For sparse PCA, we demonstrate that initializing Kelley’s method with an SOC-representable feasible region provides bounds which are comparable with the SDO-representable bound of d’Aspremont et al. [7], and successfully supplies near-exact bounds for problems with s of covariates. For nuclear norm minimization problems, we reformulate the nuclear norm in terms of its dual norm, and invoke this reformulation to derive a new class of cutting-planes. Moreover, we demonstrate that combining Kelley’s method with this class of cuts scales better than IPMs for nuclear norm minimization problems.

1.2 Structure

The rest of this paper is laid out as follows:

- •

- •

-

•

In Section 4, we present numerical results demonstrating that the outer-approximation method is competitive with state-of-the-art methods for both sparse principal component analysis and nuclear norm minimization problems.

1.3 Notation

We let nonbold face characters such as denote scalars, lowercase bold faced characters such as denote vectors, uppercase bold faced characters such as denote matrices, and calligraphic uppercase characters such as denote sets. We assume that matrices are symmetric, unless stated otherwise. We let denote the set of running indices . We let denote a vector of all ’s, denote a vector of all ’s, and denote the identity matrix, with dimension implied by the context. We let denote the positive semidefinite cone.

We also use an assortment of matrix operators. We let denote the spectral norm of a matrix, denote the Euclidean inner product between two matrices, denote the Frobenius norm of a matrix, and denote the singular value norm of a matrix; see Horn and Johnson [10] for a general theory of matrix operators.

Finally, we let denote the diameter of a set , i.e.,

where is the (Frobenius) norm for vectors (matrices).

2 Two Outer Approximations of the PSD cone

In this section, we introduce two outer approximations of the positive semidefinite cone, bound the diameters of the approximations, and propose two classes of separating hyperplanes which iteratively refine the approximations.

2.1 A Linear Outer Approximation

The following problem is a valid relaxation of Problem (1), which is LO-representable [see 17, Table 1]:

| (2) | |||||

| s.t. | |||||

In Section 3, we will iteratively improve the quality of outer approximations of SDOs, such as Problem (2), by adding cutting planes, and prove that any limit point of this procedure solves Problem (1). As Section 3’s proof of convergence relies on a compactness argument, which in turn rests on the boundedness of the initial feasible region, we now prove that imposing the constraint in Problem (2) ensures that all feasible solutions are contained within a convex, compact set.

Proposition 1.

Proof.

The boundedness of the set follows because:

Therefore, Problem (2)’s feasible region is a polytope (i.e., a bounded polyhedron) and the result holds. ∎

A corollary of Proposition 1 is that , because . Consequently, the set of feasible solutions to Problem (2) has a diameter of .

Unfortunately, while Problem (2) is a very tractable outer approximation, various authors [21, 1] have observed that it poorly approximates Problem (1) in practice. Motivated by these observations, we now argue that Problem (2) should not be used as an initial outer-approximation for a cutting-plane method, because it is dominated by an equally tractable yet much tighter nonlinear approximation. To this end, we now bound the degree to which solutions to Problem (2) violate the constraint , in terms of , and demonstrate that (2) offers poor constraint violation guarantees, since the worst-case value of grows in magnitude with :

Proposition 2.

Let be a feasible solution to Problem (2) such that is held constant. Then,

Proof.

Proposition 2 demonstrates that even if the optimal choice of is bounded in trace norm by a constant, the quality of Problem (2)’s approximation degrades with . This result explains why various authors [21, 13, 1] have found that Problem (2) poorly approximates Problem (1) in a high-dimensional setting.

We now present a SOC-representable outer approximation of Problem (1), and establish that it enjoys more attractive worst-case guarantees than a linear outer approximation.

2.2 A Second-Order Cone Outer Approximation

The following problem is a valid relaxation of Problem (1), which is SOC representable [see 12]:

| (3) | |||||

| s.t. | |||||

We now relate the diameter of Problem (3)’s feasible region to a trace constraint:

Proposition 3.

Proof.

The minor constraints in Problem (3) are equivalent to requiring that . Therefore, this result follows directly from the observation that:

We now bound the degree to which solutions to Problem (3) violate the constraint , and establish that Problem (3) enjoys better constraint violation guarantees than Problem (2):

Proposition 4.

Let be a feasible solution to Problem (3) such that . Then

Proof.

The result follows from observing that , and invoking the eigenvalue-trace bound. The bound is tight in the absence of additional problem structure [22, Theorem 2.1].∎

Observe that Proposition 4’s bound holds upon relaxing to , as the later constraint is equivalent to writing for some , and Proposition 4’s bound is minimized over by setting .

Two important instances of Proposition 4’s bound arise in correlation matrices where and spectraplex matrices where . In these cases:

respectively. Indeed, imposing the constraint in Problem (3) provides a dimension-independent violation bound, while imposing the same constraint in Problem (2) yields a bound of the order .

The worst-case value of is times smaller in Problem (3) than Problem (2). Therefore, we have established that Problem (3) is a tighter approximation than Problem (2). As optimizers widely believe that LOs and SOCPs are equally tractable in the age of modern IPMs, we will use Problem (3) as an initial approximation when developing a cutting-plane method in Section 3, and not consider Problem (2) for the rest of the paper.

2.3 Two Classes of Separating Hyperplanes

We now present two classes of separating hyperplanes which allow us to improve the outer approximations presented in Problems (2)-(3). Our first class of separating hyperplanes rests on an almost tautological result, namely:

Proposition 5.

The following two constraints are equivalent:

Proof.

The result follows from the self-duality of . ∎

For a given , Proposition 5 yields an extreme ray in time via the power method, see [10]; namely

Moreover, either verifies membership of if , or provides a separating hyperplane such that and for any feasible . We refer to this class of cuts as “trailing eigenvalue cuts”.

The next class of separating hyperplanes is derived from a reformulation of the PSD cone which is, to our knowledge, new:

Proposition 6.

The following two constraints are equivalent:

Proof.

The first constraint is equivalent to requiring that

because if and only if . Moreover, all eigenvalues are non-negative if and only if the singular values are such that , since for any symmetric matrix ; see [10, 2.6.P15]. Thus, the result follows from the duality of the spectral and nuclear norms. ∎

The following proposition demonstrates that an extreme ray of Proposition 6’s reformulation of the PSD cone is given via a singular value decomposition (SVD):

Proposition 7.

Let be a symmetric matrix. Then, an optimal solution to the problem

is given by setting , where is a singular value decomposition of .

Proof.

Let denote the eigenvalues of , and denote the singular values of . Then, the result follows from observing that , by Hölder’s inequality:

because the spectral norm is dual to the nuclear norm, and Hölder’s inequality is tight when , because and therefore .∎

Observe that either verifies membership of if , or provides a separating hyperplane such that and . We refer to this class of separating hyperplanes as “nuclear norm cuts”.

Pros and Cons of The Two Separation Oracles

In this section, we restated a well-known separation oracle for the PSD cone, and derived a new separation oracle. Conceptually, both oracles are similar, as they both rest upon semi-infinite reformulations of the positive semidefinite cone. However, they admit practical differences. For a matrix with negative eigenvalues, the trailing eigenvalue oracle provides orthogonal separating hyperplanes, while the nuclear norm oracle only provides one hyperplane. Moreover, as observed by Permenter and Parrilo [17], trailing-eigenvalue cuts can be aggregated into a single nonlinear cut, which ensures that is positive semidefinite on the subspace spanned by all trailing eigenvectors, by imposing a semidefinite constraint [17].

In spite of the aggregate power of trailing-eigenvalue cuts, nuclear norm cuts may sometimes be preferable. Indeed, while imposing trailing-eigenvalue cuts sometimes causes the multiplicity of ’s smallest eigenvalue to increase [21], nuclear norm cuts penalize the absolute sum of all eigenvalues, rather than the worst-case eigenvalue, and therefore do not have this defect. Moreover, as we show in Section 4.2, nuclear norm cuts minimize the nuclear norm of a matrix in the problem’s original space, while trailing eigenvalue cuts can only be applied to nuclear norm minimization after reformulating the problem in a higher-dimensional space, which is inefficient. We summarize the advantages and disadvantages of both cuts in Table 1.

| Cut | Characteristics |

|---|---|

| Trailing EV | () Each cut generated in time |

| () Multiple cuts per iterate | |

| () Cuts can be aggregated | |

| () Aggregating cuts is expensive | |

| () Models nuclear norm in extended space | |

| Nuclear Norm | () Penalizes trailing eigenvalue clustering |

| () Models nuclear norm in original space | |

| () Each cut generated in time |

3 An Efficient Algorithmic Approach

In this section, we present an efficient numerical approach to solve Problem (1). Our approach is an outer-approximation strategy, which takes a tractable SOC-representable approximation of the original problem, and iteratively improves the approximation by adding cutting planes.

3.1 A Cutting-Plane Method

The previous section presents tractable outer-approximations of Problem (1) and demonstrates that these approximations can be iteratively improved by adding cutting planes. Consequently, a valid numerical strategy for solving Problem (1) is the cutting-plane method, which was originally proposed by Kelley [11] under an assumption that the problem’s feasible region is polyhedral. The cutting-plane method replaces the constraint with infinitely many linear constraints of the form , which must hold for each in some convex set . Specifically,

| (4) |

for trailing eigenvalue cuts and

| (5) |

for nuclear-norm cuts. After performing this reformulation, the cutting-plane method iteratively minimizes over outer-approximations of Problem (1), which are given by imposing finitely many constraints of the form

These approximations are iteratively improved by (a) minimizing over them to obtain optimal but infeasible iterates , and (b) refining them by adding a constraint corresponding to a most violated at , , where

This numerical strategy yields a sequence of optimal but infeasible iterates, until some iterate is -feasible, i.e.,

at which point the method terminates with an optimal and -feasible solution. We present this strategy in Algorithm 1.

| s.t. | |||

We now prove that Algorithm 1 converges. Proofs of convergence for cutting-plane methods rely on compactness arguments, which can be established by bounding Problem (3)’s feasible region. To supply a proof of convergence, we require:

Assumption 1.

All feasible solutions to Problem (1) are contained within a convex set , such that .

Assumption 1 is often satisfied naturally. For instance, the trace of is constrained in SDO relaxations of binary quadratic and sparse principal component analysis problems. Alternatively, Assumption 1 can be satisfied by imposing the big-M constraint for a large positive number .

Our proof of convergence also rests on the requirement that the functions are Lipschitz continuous, i.e., there exists a Lipschitz constant such that for any feasible in Problem (3) and any separating hyperplane ,

This holds for both cuts outlined previously, by combining the Cauchy-Schwarz inequality with norm equivalence. Indeed,

for trailing eigenvalue cuts and

for nuclear norm cuts. We now state our main result:

Theorem 1.

Suppose that Assumption 1 holds and the separation oracle in Algorithm 1 is exact. Let be a feasible solution returned by the -th iterate of Algorithm 1, where

is the Lipschitz constant and is the aforementioned trace bound. Then, is an optimal and -feasible solution to Problem (1). Moreover, any limit point of solves (1).

Remark 1.

Note that the sequence of iterates need not converge to a single solution . For instance, there could be multiple optimal solutions and multiple subsequences of which each converge towards different minimizers. However, if Problem (1) admits a unique optimal solution and Assumption 1 holds then converges to the unique optimal .

Remark 2.

An alternative to Assumption 1 is to regularize the objective with a strongly convex term for some . This term ensures the boundedness of a cutting-plane method’s iterates without Assumption 1, by making the objective function coercive. Moreover, it guarantees that Algorithm 1 converges to the unique optimal , because the regularized problem admits a unique optimal solution [see 3, Proposition 1.1.2].

Proofs of convergence of general cutting-plane methods have been supplied by a number of authors since the work of Kelley [11]; see for instance [3, Section 7.5.3], [16, Section 5.2]. To keep this paper self-contained, and make explicit Theorem 1’s dependence upon Assumption 1, we now supply a proof of convergence; essentially due to [16]:

Proof.

Suppose that at some iteration , Algorithm 1 has not converged. Then, we have that , but , which implies that

where the second inequality follows by Lipschitz continuity. Rearranging the above inequality implies , i.e., Algorithm 1 never visits any ball of radius twice. Moreover, by iteration , Algorithm 1 has visited non-overlapping balls with combined volume

and these balls must be centered at feasible points, i.e., contained within a ball of radius which has volume

That is, if Algorithm 1 has not converged at iteration , we have:

which implies that we converge to an -optimal solution within iterations, for any . ∎

We note that Theorem 1’s bound depends explicitly on Assumption 1’s trace bound. Therefore, Algorithm 1 is particularly well-suited to problems with a constraint on . Moreover, the above bound illustrates why a SOC-representable initial feasible region will outperform an LO-representable initial feasible region in practice: a worst-case rate of convergence which depends on , rather than , often translates to numerically superior performance in practice.

4 Numerical Results

In this section, we apply Algorithm 1 to large-scale sparse principal component analysis and nuclear norm minimization problems, using trailing eigenvalue (resp. nuclear norm) cuts for sparse PCA (resp. nuclear norm minimization). All experiments were implemented in Julia

using MOSEK and JuMP.jl [8], and performed on one Intel Xeon E- v4 GHz CPU, using GB RAM and six CPU cores with two threads each ( threads total).

4.1 Sparse Principal Component Analysis

Given high-dimensional data and its normalized centered covariance matrix , a common task is to compress , by projecting onto a small number of principal components. This task is known as principal component analysis (PCA), and is achieved by performing singular value decomposition to obtain , and projecting onto the leading eigenvectors via .

PCA is sometimes criticized for producing uninterpretable features, because each new feature is a linear combination of all original features. This is often unacceptable because:

-

•

In medical applications, downstream decisions taken via PCA must be interpretable.

-

•

In financial applications such as investing across index funds, each non-zero entry in each PC incurs a cost.

One approach to obtain interpretable principal components is to stipulate that they are sparse, i.e., have at most non-zero entries. This approach leads to the following problem [see 7]:

| (6) |

Unfortunately, this problem cannot be solved to certifiable optimality when [see 2, for a certifiably optimal approach].

Motivated by the observation that SDO relaxations provide near-exact upper bounds on in practice, d’Aspremont et al. [7] proposed the relaxation:

| (7) |

Unfortunately, modern IPMs cannot solve Problem (7) for , because all known reformulations of the constraint require linear inequality constraints. Therefore, we apply Algorithm 1 (with trailing eigenvalue cuts) to this problem, and compare the bounds obtained via Algorithm 1 to the best feasible solution obtained by the method of Berk and Bertsimas [2] (with a time limit of seconds). We also compare our bounds with the exact SDO bound given in Problem (7), wherever it can be computed by MOSEK within our GB peak memory budget.

For completeness, we now describe the datasets which we benchmark our approach on. Note that the first three datasets are distributed via the UCI Machine Learning Repository [15].

-

•

The Pitprops dataset: a covariance matrix derived from observations of features.

-

•

The normalized communities dataset: a correlation matrix derived from observations of features, after eliminating categorical variables.

-

•

The normalized Arrhythmia dataset: a correlation matrix derived from observations of features, after eliminating categorical variables.

-

•

Wilshire : a correlation matrix derived from observations of changes in daily stock prices from January to December , obtained via Yahoo! Finance using the R package quantmod [see 20], after eliminating stocks which were not traded in all days considered.

As optimizing over SOC constraints is too expensive when , we adopt a more tractable initial approximation for the Wilshire dataset. Namely, we aggregate the SOC constraints into constraints, by (a) observing that

since , and (b) introducing the auxiliary variables to model a relaxation of the sparsity constraint . This yields the following SOC relaxation, which is weaker than Problem (3)’s relaxation, but has , rather than , SOC/linear inequality constraints:

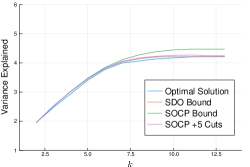

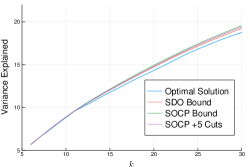

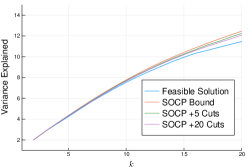

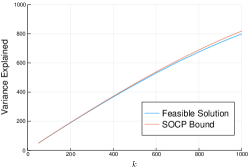

We now present our experimental results. Table 2 depicts the time required for Algorithm 1 to generate a bound with or cuts, and the time required for MOSEK to solve the SDO relaxation when ; Table 3 depicts the magnitude of the bound gaps for the different bounds when ; Figure 1 depicts the quality of the SOC and SDO bounds, for varying , against the optimal solution obtained by the algorithm of [2] (for ) or the best solution obtained after seconds (for ). We do not generate cuts for the Wilshire dataset, as the SOC bound is sufficiently tight here.

| Problem | Approach runtime (s) | |||

|---|---|---|---|---|

| SOC | SOC cuts | SOC cuts | SDO | |

| pitprops | ||||

| norm communities | ||||

| norm arrythmia | n/a | |||

| norm wilshire | n/a | n/a | n/a | |

| Problem | Bound gap () | |||

|---|---|---|---|---|

| SOC | SOC cuts | SOC cuts | SDO | |

| pitprops | ||||

| norm communities | ||||

| norm arrythmia | n/a | |||

| norm wilshire | n/a | n/a | n/a | |

Our main findings from this set of experiments are as follows:

- •

-

•

For sparse PCA problems where , Problem (3)’s outer approximation provides an accurate upper bound in a tractable fashion. Moreover, for larger problems where , aggregating the SOCP constraints yields a looser yet still tractable bound. This is because Problem (7) contains the constraint , which, as established in Proposition 4, provides tight constraint violation guarantees.

4.2 Nuclear Norm Minimization

Given an incomplete set of observations of a low-rank matrix , a central problem in machine learning is to recover the entire matrix, by solving:

| (8) |

Unfortunately, all known algorithms for solving Problem (8) to certifiable optimality require exponential time in both theory and practice [19]. Consequently, various authors including [19] have proposed instead solving Problem (8)’s convex relaxation:

| (9) |

By exploiting Schur complements, Recht et al. [19] have established that Problem (9) is SDO-representable. Unfortunately, their reformulation is intractable for even medium-sized problems, as it rests upon lifting the nuclear norm objective to a higher dimensional space. An alternative approach is to apply Algorithm 1 with nuclear norm cuts, i.e., exploit Proposition 6’s semi-infinite reformulation of the nuclear norm objective, and iteratively solve a sequence of SOCPs of the form:

where we impose the SOC-representable Frobenius norm constraint, because it is valid by the relation [see 10]. Moreover, Proposition 7 proves that at each iteration a most-violated in the semi-infinite constraint is given by taking an SVD of and setting .

When we performed our numerical experiments, rather than solving Problem (9), we applied Algorithm 1 to the following problem (taking in our experiments).

| (10) | ||||

| s.t. |

Solving this problem as a surrogate for Problem (9) serves a dual purpose: (a) it ensures that Problem (9) has a unique solution, which prevents degeneracy and discourages stalling behaviour, and (b) it ensures that converges to Problem (10)’s unique solution; see Remark 2.

We now compare the time required for our approach to obtain a solution within of optimality, to the time required for MOSEK to solve a semidefinite reformulation of the problem, where we generate a rank matrix from two factors with i.i.d. entries, and randomly sample half the entries from the matrix, i.e., let . As MOSEK does not allow SOC constraints and quadratic objective terms to be mixed, we model the Frobenius norm term by invoking the equivalence

Figure 2 depicts the runtime requirement for both approaches (averaged over instances), and demonstrates that Algorithm 1 outperforms IPMs when (i.e., there are constraints).

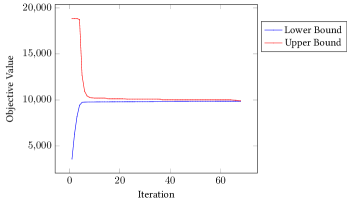

Our approach also generates solutions to Problem (10) for larger problem sizes. Figure 3 depicts the convergence profile of our approach for an instance (generated in the same manner as the previous experiment) where ; convergence was attained after seconds. The convergence profile is typical: we obtain a near-exact lower bound within iterations, and require many more iterations to identify the optimal solution.

Our main set of findings from this experiment are as follows:

-

•

Although IPMs scale better than outer-approximation methods from a traditional complexity theory perspective, in practice Kelley’s cutting-plane method solves nuclear norm minimization problems faster. This is because (a) Kelley’s method solves nuclear norm minimization problems in their original space, while an SDO reformulation lifts the problem via Schur complements, and (b) while the traditional complexity theory accurately describes the performance of IPMs, it is too conservative with respect to cutting-plane methods.

-

•

The bottleneck in applying Algorithm 1 to larger-scale matrix completion problems is the SVD step, which scales at a rate of . Therefore, one future direction is to replace the SVD step with an inexact oracle, which performs matrix sketching to yield valid inexact cuts in time.

Acknowledgements

We are grateful to Peter Cohen for editorial comments.

References

- Ahmadi and Majumdar [2019] A. A. Ahmadi and A. Majumdar. Dsos and sdsos optimization: more tractable alternatives to sum of squares and semidefinite optimization. SIAM Journal on Applied Algebra and Geometry, 3(2):193–230, 2019.

- Berk and Bertsimas [2019] L. Berk and D. Bertsimas. Certifiably optimal sparse principal component analysis. Mathematical Programming Computation, pages 1–40, 2019.

- Bertsekas [1999] D. P. Bertsekas. Nonlinear programming. Athena Scientific, 1999.

- Bertsimas et al. [2019] D. Bertsimas, R. Cory-Wright, and J. Pauphilet. A unified approach to mixed-integer optimization: Nonlinear formulations and scalable algorithms. arXiv:1907.02109, 2019.

- Braun et al. [2015] G. Braun, S. Fiorini, S. Pokutta, and D. Steurer. Approximation limits of linear programs (beyond hierarchies). Mathematics of Operations Research, 40(3):756–772, 2015.

- Dantzig et al. [1954] G. Dantzig, R. Fulkerson, and S. Johnson. Solution of a large-scale traveling-salesman problem. Journal of the operations research society of America, 2(4):393–410, 1954.

- d’Aspremont et al. [2005] A. d’Aspremont, L. El Ghaoui, M. Jordan, and G. Lanckriet. A direct formulation for sparse pca using semidefinite programming. In NIPS, pages 41–48, 2005.

- Dunning et al. [2017] I. Dunning, J. Huchette, and M. Lubin. Jump: A modeling language for mathematical optimization. SIAM Review, 59(2):295–320, 2017.

- Fischetti et al. [2016] M. Fischetti, I. Ljubić, and M. Sinnl. Redesigning benders decomposition for large-scale facility location. Management Science, 63(7):2146–2162, 2016.

- Horn and Johnson [1990] R. A. Horn and C. R. Johnson. Matrix analysis. 1990.

- Kelley [1960] J. E. Kelley, Jr. The cutting-plane method for solving convex programs. Journal of the society for Industrial and Applied Mathematics, 8(4):703–712, 1960.

- Kim and Kojima [2001] S. Kim and M. Kojima. Second order cone programming relaxation of nonconvex quadratic optimization problems. Optimization methods and software, 15(3-4):201–224, 2001.

- Kocuk et al. [2016] B. Kocuk, S. S. Dey, and X. A. Sun. Strong socp relaxations for the optimal power flow problem. Operations Research, 64(6):1177–1196, 2016.

- Krishnan and Mitchell [2006] K. Krishnan and J. E. Mitchell. A unifying framework for several cutting plane methods for semidefinite programming. Optimization Methods and Software, 21(1):57–74, 2006.

- Lichman [2013] M. Lichman. Uci machine learning repository. https://archive.ics.uci.edu/ml/datasets.html, 2013.

- Mutapcic and Boyd [2009] A. Mutapcic and S. Boyd. Cutting-set methods for robust convex optimization with pessimizing oracles. Optimization Methods & Software, 24(3):381–406, 2009.

- Permenter and Parrilo [2018] F. Permenter and P. Parrilo. Partial facial reduction: simplified, equivalent sdps via approximations of the psd cone. Mathematical Programming, 171:1–54, 2018.

- Ramana [1997] M. V. Ramana. An exact duality theory for semidefinite programming and its complexity implications. Mathematical Programming, 77(1):129–162, 1997.

- Recht et al. [2010] B. Recht, M. Fazel, and P. Parrilo. Guaranteed minimum-rank solutions of linear matrix equations via nuclear norm minimization. SIAM Review, 52(3):471–501, 2010.

- Ryan [2008] J. A. Ryan. quantmod: Quantitative financial modelling framework. R package, 2008.

- Sivaramakrishnan [2002] K. K. Sivaramakrishnan. Linear programming approaches to semidefinite programming problems. PhD thesis, RPI, 2002.

- Wolkowicz and Styan [1980] H. Wolkowicz and G. Styan. Bounds for eigenvalues using traces. Linear algebra and its applications, 29:471–506, 1980.