Storage or No Storage: Duopoly Competition Between Renewable Energy Suppliers in a Local Energy Market

Abstract

Renewable energy generations and energy storage are playing increasingly important roles in serving consumers in power systems. This paper studies the market competition between renewable energy suppliers with or without energy storage in a local energy market. The storage investment brings the benefits of stabilizing renewable energy suppliers’ outputs, but it also leads to substantial investment costs as well as some surprising changes in the market outcome. To study the equilibrium decisions of storage investment in the renewable energy suppliers’ competition, we model the interactions between suppliers and consumers using a three-stage game-theoretic model. In Stage I, at the beginning of the investment horizon (containing many days), suppliers decide whether to invest in storage. Once such decisions have been made (once), in the day-ahead market of each day, suppliers decide on their bidding prices and quantities in Stage II, based on which consumers decide the electricity quantity purchased from each supplier in Stage III. In the real-time market, a supplier is penalized if his actual generation falls short of his commitment. We characterize a price-quantity competition equilibrium of Stage II in the local energy market, and we further characterize a storage-investment equilibrium in Stage I incorporating electricity-selling revenue and storage cost. Counter-intuitively, we show that the uncertainty of renewable energy without storage investment can lead to higher supplier profits compared with the stable generations with storage investment due to the reduced market competition under random energy generation. Simulations further illustrate results due to the market competition. For example, a higher penalty for not meeting the commitment, a higher storage cost, or a lower consumer demand can sometimes increase a supplier’s profit. We also show that although storage investment can increase a supplier ’s profit, the first-mover supplier who invests in storage may benefit less than the free-rider competitor who chooses not to invest.

Index Terms:

Local energy market, Renewable generation, Energy storage, Market competition, Market equilibriumI Introduction

I-A Background and motivation

Renewable energy, as a clean and sustainable energy source, is playing an increasingly important role in power systems [2]. For example, from the year 2007 to 2017, the global installed capacity of solar panels has increased from 8 Gigawatts to 402 Gigawatts, and the wind power capacity has increased from 94 Gigawatts to 539 Gigawatts[2]. Compared with traditional larger-scale generators, renewable energy sources can be more spatially distributed across the power system, e.g., at the distribution level near residential consumers[2]. Due to the distributed nature of renewable energy generations, there has been growing interest in forming local energy markets for renewable energy suppliers and consumers to trade electricity at the distribution level [3]. Such local energy markets will allow consumers to purchase electricity from the least costly sources locally[4], and allow suppliers to compete in selling electricity directly to consumers (instead of dealing with the utility companies).

However, many types of renewable energy are inherently random, due to factors such as weather conditions that are difficult to predict and control. Under current multi-settlement energy market structures with day-ahead and real-time bidding rules (which are mostly designed for controllable generations)[5], renewable energy suppliers face a severe disadvantage in the competition by making forward commitment (in the day-ahead market) that they may not be able to deliver in real time. For example, suppliers are often subject to a penalty cost if their real-time delivery deviates from the commitment in the day-ahead market[6].

Energy storage has been considered as an important type of flexible resources for renewable energy suppliers to stabilize their outputs[7]. Investing in storage can potentially improve the renewable energy suppliers’ position in these energy markets. However, investing in storage incurs substantial investment costs. Furthermore, the return of storage investment depends on the outcome of the market, which in turn depends on how suppliers with or without storage compete for the demand. Therefore, it remains an open problem regarding whether competing renewable energy suppliers should invest in energy storage in the market competition and what economic benefits the storage can bring to the suppliers.

I-B Main results and contributions

In this paper, we formulate a three-stage game-theoretic model to study the market equilibrium for both storage investment as well as price and quantity bidding of competing renewable energy suppliers. In Stage I, at the beginning of the investment horizon, each supplier decides whether to invest in storage. We formulate a storage-investment game between two suppliers in Stage I, which is based on a bimatrix game to model suppliers’ storage-investment decisions for maximizing profits[8]. Given the storage-investment decisions in Stage I, competing suppliers decide the bidding price and bidding quantity in the (daily) local energy market in Stage II. We formulate a price-quantity competition game between suppliers using the Bertrand-Edgeworth model [9] (which models price competition with capacity constraints) in Stage II. Given suppliers’ bidding strategies, consumers decide the electricity quantity purchased from each supplier in Stage III. To the best of our knowledge, our work is the first to study the storage-investment equilibrium between competing renewable energy suppliers in the two-settlement energy market. This problem is quite nontrivial due to the penalty cost on the random generations of a general probability distribution.

By studying this three-stage model, we reveal a number of new and surprising insights that are against the prevailing wisdom in the literature on the renewable energy suppliers’ revenues in such a two-settlement market [6, 10] and on the economic benefits of storage supplementing in renewable energy sources [11, 12].

-

•

First, the uncertainty of the renewable generation can be favorable to suppliers. Note that the prevailing wisdom is that storage investment (especially when the storage cost is low) will improve suppliers’ revenue by stabilizing their outputs [11, 12]. In contrast, we find that the opposite may be true when considering market competition. Specifically, without storage, suppliers with random generations always have strictly positive revenues when facing any positive consumer demand. However, if both suppliers invest in storage and stabilize their renewable outputs, their revenues reduce to zero once the consumer demand is below a threshold, which is due to the increased market competition after storage investment.

-

•

Second, a higher penalty and a higher storage cost can also be favorable to the suppliers. Note that the common wisdom is that a higher penalty[10] and a higher storage cost[11] will decrease suppliers’ profit. However, when considering market competition, the opposite may be true. With a higher penalty for not meeting the commitment, renewable energy suppliers become more conservative in their bidding quantities, which can decrease market competition and increase their profits. Furthermore, a higher storage cost may change one supplier’s storage-investment decision, which can benefit the other supplier.

-

•

Third, the first-mover supplier who invests in energy storage can be at the disadvantage in terms of profit increase, which is contrary to the first-mover advantage gained by early investment of resources or new technologies [13]. We find that although investing in storage can increase one supplier’s profit, it may benefit himself less than his competitor (who does not invest in storage). This is because the later mover becomes a free rider, who may benefit from the changed price equilibrium in the energy market (due to the storage investment of the other supplier) but does not need to bear the investment cost.

In addition to these surprising and new insights, a key technical contribution of our work is the solution to the game-theoretic model for the price-quantity competition, which involves a general penalty cost due to random generations of a general probability distribution. Note that such a price-quantity competition with the Bertrand-Edgeworth model has been studied in literature under quite different conditions from ours. The works in [14, 15, 16] studied a general competition between suppliers with strictly convex production costs. They focused on the analysis of pure strategy equilibrium without characterizing the mixed strategy equilibrium. The study in [17] characterized both pure and mixed strategy equilibrium between suppliers with deterministic supply. However, this work considered zero cost related to the production (i.e., no production cost or possible penalty cost). In electricity markets, the works in [18] and [19] also used Bertrand-Edgeworth model to analyze the competition among renewable energy suppliers with random generations. However, both [18] and [19] considered the suppliers’ electricity-selling competition in a single-settlement energy market, and suppliers deliver random generations in real time. These studies did not consider day-ahead bidding strategies and any deviation penalty cost. In particular, the two-settlement markets with deviation penalty have been essential for ensuring the reliable operation of power systems. Our work is the first to consider the two-settlement energy market, characterizing both pure and mixed strategy equilibrium based on the Bertrand-Edgeworth model. Such a setting is nontrivial due to the penalty cost caused by the suppliers’ random production of a general probability distribution.

The remainder of the paper is organized as follows. First, we introduce the system model in Section II, as well as the three-stage game-theoretic formulation between suppliers and consumers in Section III. Then, we solve the three-stage problem through backward induction. We first characterize the consumers’ optimal purchase decision of Stage III in Section IV. Then, we characterize the price-quantity equilibrium of Stage II and the storage-investment equilibrium of Stage I in Sections V and VI, respectively. We propose a probability-based method to compute the storage capacity in Section VII. Furthermore, in Section IX, we extend some of the theoretical results and insights from the duopoly case to the oligopoly case. Finally, we present the simulation results in Section VIII and conclude this paper in Section X.

II System Model

We consider a local energy market at the distribution level as shown in Figure 1. Consumers can purchase energy from both the main grid and local renewable energy suppliers. To achieve a positive revenue, the renewable energy suppliers (simply called suppliers in the rest of the paper) need to set their prices no greater than the grid price, and they will compete for the market share. Furthermore, suppliers can choose to invest in energy storage to stabilize their renewable outputs and reduce the uncertainty in their delivery. Next, we will introduce the detailed models of timescales, suppliers and consumers, and characterize their interactions in the two-settlement local energy market.

II-A Timescale

We consider two timescales of decision-making. One is the investment horizon of days (e.g., corresponding to the total number of days for the storage investment horizon). Suppliers can decide (once) whether to invest in energy storage at the beginning of the investment horizon. The investment horizon is divided into many operational horizons (many days), and each corresponds to the daily operation of the energy market, consisting of many time slots (e.g., 24 hours of each day). In the day-ahead market on day , suppliers decide the electricity price and quantity to consumers for each hour of the next day . We will introduce the market structure in detail later in Section II.D.

II-B Suppliers

In Sections IV-VI, we focus on the duopoly case of two suppliers in our analysis. Later in Section IX, we further generalize to the oligopoly case with more than two suppliers. The reason for focusing on the duopoly case is twofold. First, our work focuses on a local energy market that is much smaller than a traditional wholesale energy market. The number of suppliers serving one local area is also expected to be limited [20], compared with thousands of suppliers in the wholesale energy market [21]. In such a small local energy market, a few large suppliers may dominate the market[22]. Second, we consider two suppliers for analytical tractability, which is without losing key insights and can effectively capture the impact of competition among suppliers considering the storage investment. For example, we show that in the duopoly case, the uncertainty of renewable generation can be beneficial to suppliers. Such an insight is still valid in the oligopoly case.

We denote as the set of two suppliers. For hour of day , the renewable output of supplier is denoted as a random variable , which is bounded in . We assume that the random generation has a continuous cumulative distribution function (CDF) with the probability density function (PDF) . The distribution of wind or solar power can be characterized using the historical data, which is known to the renewable energy suppliers.111In Section VIII of simulations, we use historical data to model the empirical CDF of renewable generations, which is explained in detail in Appendix.XIV. As renewables usually have extremely low marginal production costs compared with traditional generators, we assume zero marginal production costs for the suppliers[18] [19].

II-C Consumers

We consider the aggregate consumer population, and we denote the total consumer demand at hour of day as . Note that consumers in one local area usually face the same electricity price from the same utility. Thus, if the local market’s electricity price is lower than the grid price, all the consumers will first purchase electricity from local suppliers. From the perspective of suppliers, they only care about the total demand of consumers and how much electricity they can sell to consumers.

Furthermore, our work conforms to the current energy market practice that suppliers make decisions in the day-ahead market based on the predicted demand. Thus, for the demand , we consider it as a deterministic (predicted) demand in our model.222The day-ahead prediction of consumers’ aggregated demand can be fairly accurate[24]. We assume that the demand and supply mismatch due to the demand forecast error will be regulated by the operator in the real-time market. Since the electricity demand is usually inelastic [5], we also assume the following.

Assumption 1.

Consumers’ demand is perfectly inelastic in the electricity price.

Consumers must purchase their demand either from the main grid (at a fixed unit price ) or from the local renewable suppliers (with prices to be discussed later).333We do not consider demand response for the consumers.

II-D Two-settlement local energy market

We consider a two-settlement local energy market, which consists of a day-ahead market and a real-time market[5]. In such an energy market, suppliers have market power and can strategically decide their selling prices.444This price model is different from the usual practice of the wholesale energy market, where the market usually sets a uniform clearing price for all the suppliers through market clearing [5]. Consumers have the flexibility to choose suppliers by comparing prices [4]. We explain the two-settlement energy market in detail as follows.

-

•

In the day-ahead market on day (e.g., suppliers’ bids are cleared around 12:30pm of day , one day ahead of the delivery day [25]), supplier decides the bidding price and the bidding quantity for each future hour of the delivery day . Based on suppliers’ bidding strategies, consumers decide the electricity quantity purchased from supplier . Supplier will get the revenue of in the day-ahead market by committing the delivery quantity to consumers. Thus, the day-ahead market is cleared through matching supply and demand. Any excessive demand from the consumers will be satisfied through energy purchase from the main grid.

-

•

In the real-time market at each hour on the next day , if supplier ’s actual generation falls short of the committed quantity (i.e., ), he needs to pay the penalty in the real-time market, which is proportional to the shortfall with a unit penalty price . For the consumers, although suppliers may not deliver the committed electricity to them, the shortage part can be still satisfied by the system operator using reserve resources. The cost of reserve resources can be covered by the penalty cost on the suppliers.

Note that the suppliers and consumers make decisions only in the day-ahead market. No active decisions are made in the real-time market, but there may be penalty cost on the delivery shortage.

To facilitate the analysis, we further make several assumptions of this local energy market as follows. First, for the excessive amount of generations (i.e., ), we assume the following.

Assumption 2.

Suppliers can curtail any excessive renewable energy generation (beyond any specific given level).

Assumption 2 implies that we do not need to consider the possible penalty or reward on the excessive renewable generations in real time.555There are different policies to deal with the surplus feed-in energy of renewables. In some European countries, the energy markets give rewards to the surplus energy [26]. In the US, some markets deal with the surplus energy using the real-time imbalance price that can be either penalties or rewards [10].

Second, the local energy market is much smaller compared with the wholesale energy market. Thus, the suppliers are usually small and hence may focus on serving local consumers. It is less likely for them to trade in the wholesale energy market. This is summarized in the following assumption.

Assumption 3.

Suppliers only participate in the local energy market and serve local consumers. They do not participate in the wholesale energy market.

Third, for the bidding price and penalty price , we impose the following bounds.

Assumption 4.

Each supplier ’s bidding price has a cap that satisfies .

Assumption 5.

The penalty price satisfies .

Assumption 4 is without loss of generality, since no supplier will bid a price higher than ; otherwise, consumers will purchase from the main grid.666We avoid the case as it may bring ambiguity to the local energy market if the bidding price is equal to the main grid price , in which case it is not clear whether consumers purchase energy from the local energy market or from the main grid. Assumption 5 ensures that the penalty is high enough to discourage suppliers from bidding higher quantities beyond their capability. Note that price cap and the penalty are exogenous fixed parameters in our model. Next, we introduce how suppliers invest in the energy storage to stabilize their outputs.

II-E Storage investment

Each supplier decides whether to invest in storage at the beginning of the investment horizon. We denote supplier ’s storage-investment decision variable as , where means investing in storage and means not investing. If supplier invests in storage, we assume the following.

Assumption 6.

The with-storage supplier will utilize the storage to completely smooth out his power output at the mean value of renewable generations.

Thus, supplier with the renewable generation will charge and discharge his storage777There can be different ways to deal with the randomness of renewable generations, including the curtailment of renewable energy and the use of additional fossil generators to provide additional energy. It is interesting to combine energy storage with other mechanisms (such as renewable energy curtailment), which we will explore in the future work. to stabilize the power output at the mean value . The charge and discharge power is as follows.

| (1) |

where means charging the storage and means discharging the storage. Note that , which implies the long-term average power that the suppliers need to charge or discharge his storage is zero. Next, we introduce how to characterize the storage capacity and the storage cost.

First, based on the charge and discharge random variable , we propose a simple yet effective probability-based method to characterize the storage capacity using historical data of renewable generation . In particular, we set a probability threshold, and then aim to find a minimum storage capacity such that the energy level in the storage exceeds the capacity with a probability no greater than the probability threshold. We will explain this methodology in Section VII.

Second, we calculate the storage cost of suppliers over the investment horizon (scaled into one hour) as , where is the unit capacity cost over the investment horizon and is the scaling factor that scales the investment cost over years to one hour. The factor is calculated as follows. We first calculate the present value of an annuity (a series of equal annual cash flows) with the annual interest rate (e.g., ), and then we divide the annuity equally to each hour. This leads to the formulation of the factor as follows [27].

| (2) |

where is the number of years over the investment horizon (e.g., for Li-ion battery that can last for 15 years), and is the total hours in one year (e.g., ).

Therefore, given the parameter and as well as the probability distribution of random generation, the storage capacity and storage cost can be regarded as the fixed values for the supplier who invests in storage. Note that a higher storage capacity leads to a higher storage investment cost, which can further affect the storage-investment decisions in the suppliers’ competition. Next, in the Section III, we will introduce the three-stage model between suppliers and consumers in detail.

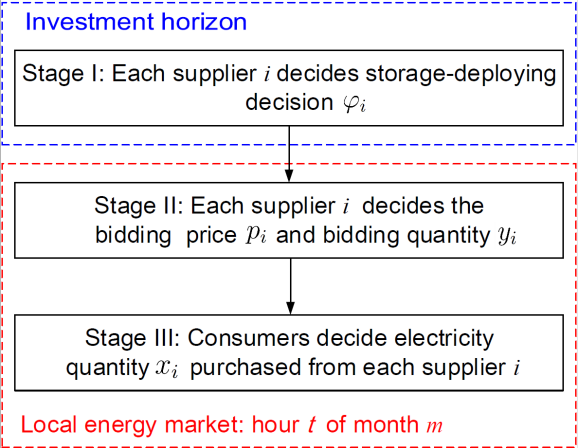

III Three-stage game-theoretic model

We build a three-stage model between suppliers and consumers. In Stage I, at the beginning of the investment horizon, each supplier decides whether to invest in storage. In the day-ahead energy market, for each hour of the next day, suppliers decide the bidding prices and quantities in Stage II, and consumers make the purchase decision in Stage III. Next, we first introduce the types of renewable-generation distributions for computing suppliers’ electricity-selling revenues over the investment horizon, and then we explain the three stages respectively in detail.

III-A Type of renewable-generation distributions

We cluster the distribution of renewable generation into several types. Note that suppliers’ revenues depend on the distribution of renewable generations. We use historical data of renewable energy to model the generation distribution. Specifically, for the renewable generations at hour of all the days over the investment horizon, we cluster the empirical distribution into types, e.g., for 12 months considering the seasonal effect. In this case, each type occurs with a probability considering 12 months.888There can be other types of clustering with unequal probabilities. We use the data of renewable energy of all days in month at hour to approximate the distribution of renewable generation at hour for all the days in this month . Then, to study the interactions between consumers and suppliers in the local energy market, we will assume that the renewable generation of day follows a random type (month) , uniformly chosen from . For notation convenience, we replace all the superscripts into .

III-B The three-stage model

We illustrate the three-stage model between suppliers and consumers in Figure 2.

-

•

Stage I: at the beginning of the investment horizon, each supplier decides the storage-investment decisions .

-

•

Stage II: in the day-ahead market, for each hour of the next day, each supplier decides his bidding price and bidding quantity based on suppliers’ storage-investment decisions, assuming that the renewable-generation distribution is of month .

-

•

Stage III: in the day-ahead market, for each hour of the next day, consumers decide the electricity quantity purchased from each supplier based on each supplier’s bidding price and quantity, assuming that the renewable-generation distribution is of month .

This three-stage problem is a dynamic game. The solution concept of a dynamic game is known as Subgame Perfect Equilibrium, which can be derived through backward induction[28]. Therefore, in the following, we will explain the three stages in detail in the order of Stage III, Stage II, and Stage I, respectively.

III-B1 Stage III

At hour of month , given the bidding price and bidding quantity of both suppliers in Stage II, consumers decide the electricity quantity purchased from supplier 1 and supplier 2, respectively. The objective of consumers is to maximize the cost saving of purchasing energy from local suppliers compared with purchasing from the main grid only. We denote such cost saving as follows:

| (3) |

Recall that we model the collective purchase decision of the entire consumer population together. Consumers must satisfy their demand either from the local energy market or from the main grid (at the fixed price ). The total cost of satisfying the entire demand by the main grid is fixed. Therefore, minimizing the total energy cost is equivalent to maximizing the cost savings in the local energy market. We present consumers’ optimal purchase problem as follows.

Stage III: Consumers’ Cost Saving Maximization Problem

| (4a) | ||||

| s.t. | (4b) | |||

| (4c) | ||||

Constraint (4b) states that the total purchased quantity is no greater than the demand . Constraints (4c) states that the quantity purchased from supplier is no greater than his bidding quantity . This problem is a linear programming and can be easily solved, which we show in Section IV. We denote the optimal solution to Problem (4) as a function of suppliers’ bidding prices and quantities , i.e., , where and .

III-B2 Stage II

Given the storage-investment decision in Stage I, both suppliers decide the bidding price and bidding quantity to maximize their revenues in Stage II. We denote supplier ’s electricity-selling revenue as , which consists of two parts: the commitment revenue from committing the delivery quantity in the day-ahead market, and the penalty cost in the real-time market. Supplier who invests in storage (i.e., ) will be penalized if the committed quantity is larger than his stable generation . Supplier who does not invest in storage (i.e., ) will be penalized if the commitment is larger than his actual random generation .

Note that the decisions of two suppliers are coupled with each other. If one supplier bids a lower quantity or a higher price, it is highly possible that consumers will purchase more electricity from the other supplier. We formulate a price-quantity competition game between suppliers given storage-investment decisions as follows.

Stage II: Price-quantity competition game

-

•

Players: supplier .

-

•

Strategies: bidding quantity and bidding price of each supplier .

-

•

Payoffs: supplier ’s revenue at hour of month is

(5) where we define

If both suppliers invest in storage (i.e., ), the equilibrium has been characterized in [17]. However, if there is at least one supplier who does not invest in storage (i.e., ), characterizing the equilibrium is quite non-trivial due to the penalty cost on the random generation of a general probability distribution. We will discuss how to characterize the equilibrium in detail in Section V. We denote the equilibrium revenue of supplier as .

III-B3 Stage I

At the beginning of the investment horizon, each supplier decides whether to invest in storage to maximize his expected profit. We denote supplier ’s expected profit as , which incorporates the expected revenue in the local energy market and the possible storage investment cost. As one supplier varies his storage-investment decisions, it leads to a different price-quantity subgame, which will affect both suppliers’ profits. Thus, suppliers’ storage-investment decisions are coupled and we formulate a storage-investment game between suppliers as follows.

Stage I: Storage-investment game

-

•

Players: supplier .

-

•

Strategies: whether investing in storage .

-

•

Payoffs: supplier ’s expected profit (scaled in one hour) is

(6)

This storage-investment game is a bimatrix game where each supplier has two strategies. Although the Nash equilibrium of bimatrix game can be easily solved numerically, the close-form equilibrium does not exist in all subgames of Stage II. It is challenging to analyze the storage-investment equilibrium with respect to the parameters, e.g., demand and storage cost, and we discuss it in detail in Section VI.

We solve this three-stage problem through backward induction. We first analyze the solution in Stage III given the bidding prices and bidding quantities in Stage II. Then, we incorporate the solution in Stage III to analyze the price and quantity equilibrium in Stage II, given (arbitrary) storage-investment decisions in Stage I. Finally, we incorporate the equilibrium of Stage II into Stage I to solve the storage-investment equilibrium. In the next three sections of Section IV, Section V, and Section VI, we will analyze the three stages in the order of Stage III, Stage II, and Stage I, respectively.

IV Solution of Stage III

In this section, we characterize consumers’ optimal purchase solution to Problem (4) in Stage III. We use subscript to denote supplier and we use to denote the other supplier. Note that in Stage III, the decisions are made independently for each hour of each day. For notation simplicity, we omit the superscript in the corresponding variables and parameters.

Given the bidding price and bidding quantity of suppliers, we characterize in Proposition 1 consumers’ optimal decision in Stage III. Recall that we assume that the bidding price in the local energy market is lower than the main grid price (i.e., ).

Proposition 1 (optimal purchase in Stage III).

-

•

If for some , then and

-

•

If , then the optimal purchase solution can be any element in the following set.

We assume that the demand will be allocated to the suppliers according to the condition either or . The condition or is selected based on maximizing the two suppliers’ total revenue.999If there is no difference between and , the demand will be allocated by either or with equal probabilities.

Proposition 1 shows that the consumers will first purchase the electricity from the supplier who sets a lower price. If there is remaining demand, then they will purchase from the other supplier. Furthermore, if consumers’ demand cannot be fully satisfied by the local suppliers, they will purchase the remaining demand from the main grid. We show the proof of Proposition 1 in Appendix.XV. Next we analyze the strategic bidding of suppliers in Stage II by incorporating consumers’ optimal purchase decisions .

V Equilibrium analysis of Stage II

In this section, we will characterize the bidding strategies of suppliers for the price-quantity competition subgame in Stage II, given the storage-investment decision in Stage I. Note that, depending on the storage-investment decisions in Stage I, there are three types of subgames: (i) the both-investing-storage () case, (ii) the mixed-investing-storage () case, where one invests in storage and one does not, and (iii) the neither-investing-storage () case. The competition-equilibrium characterization between suppliers is highly non-trivial, due to the general distribution of renewable generations and the penalty cost. In particular, the pure price equilibrium may not exist, which requires the characterization of the mixed price equilibrium. Next, we first show that each supplier’s equilibrium bidding quantity is actually a weakly dominant strategy that does not depend on the other supplier’s decision, based on which we further derive the suppliers’ bidding prices at the equilibrium for each subgame. Note that in Stage II, the decisions are made independently for each hour of each day. For notation simplicity, we omit the superscript in the corresponding variables and parameters.

V-A Weakly-dominant strategy for bidding quantity

We show that given the bidding price , each supplier has a weakly dominant strategy for the bidding quantity that does not depend on the other supplier’s quantity or price choice. This is rather surprising, and it will help reduce the two-dimensional bidding process (involving both quantity and price) into a one-dimensional bidding process (involving only price). Deriving the weakly dominant strategy is nontrivial due to the penalty cost on the renewable generation of a general probability distribution faced by the without-storage supplier.

We first define the weakly dominant strategy for the bidding quantity in Definition 1, which enables a supplier to obtain a revenue at least as high as any other bidding quantity , no matter what is the other supplier’s decision.

Definition 1 (weakly dominant strategy).

Given price and storage-investment decision , a bidding quantity is a weakly dominant strategy for supplier if

for any and .

We then characterize suppliers’ weakly dominant strategy for the bidding quantity in Theorem 1.

Theorem 1 (weakly dominant strategy for the bidding quantity).

The weakly dominant strategy is given by

| (7) |

where is the inverse function of the CDF of supplier ’s random generation.

Theorem 1 shows that a with-storage supplier (i.e., ) should bid the quantity at the stable production level (independent of price ) so that he can attract the most demand but do not face any penalty risk in the real-time market. For a without-storage supplier (i.e., ), however, he has to trade off between his bidding quantity and the penalty cost incurred by the random generation. His weakly dominant strategy depends on his own bidding price , but does not depend on the other supplier ’s bidding price or bidding quantity . Note that when price , the bidding quantity . Furthermore, the bidding quantity increases in price , which shows that the without-storage supplier should bid more quantities when he bids a higher price. When price , the bidding quantity satisfies (i.e., the maximum generation amount) since we assume .

V-B Equilibrium price-bidding strategy: pure equilibrium

We will further analyze the price equilibrium between suppliers based on the weakly dominant strategies for the bidding quantities in Theorem 1. We characterize the price equilibrium with respect to the demand that can affect the competition level between suppliers. For the and cases, we show that a pure price equilibrium exists when the demand is higher than a threshold (characterized in the later analysis). However, when the demand is lower than the threshold, there exists no pure price equilibrium due to the competition for the limited demand. For the case, the equilibrium structure is characterized by two thresholds of the demand (characterized in the later analysis). A pure price equilibrium will exist when the demand is higher than the larger threshold or lower than the other smaller threshold. However, when the demand is in the middle of the two thresholds, there exists no pure price equilibrium.

We first define the pure price equilibrium of suppliers in Definition 2, where no supplier can increase his revenue through unilateral price deviation.

Definition 2 (pure price equilibrium).

Given the storage-investment decision , a price vector is a pure price equilibrium if for both ,

| (8) |

for all , where is the weakly dominant strategies derived in Theorem 1.

Then, we show the existence of the pure price equilibrium in Proposition 2.

Proposition 2 (existence of the pure price equilibrium).

-

•

Subgames of type and type (i.e., when ):

-

–

If , there exists a pure price equilibrium , with equilibrium revenue , for any .

-

–

If , there is no pure price equilibrium.

-

–

-

•

Subgame of type ():

-

–

If , there exists a pure price equilibrium , with equilibrium revenue , for any .

-

–

If , there exists a pure price equilibrium , with equilibrium revenue , for any .

-

–

If , there is no pure price equilibrium.

-

–

We summarize the existence of pure price equilibrium and the weakly dominant strategy of bidding quantity in Table I.

| Subgame | Weakly dominant strategy of bidding quantity | Existence of pure price equilibrium | Non-existence of pure price equilibrium |

|---|---|---|---|

| , | (a) : , (b) : , | : no pure price equilibrium | |

| , | , | : , . | : no pure price equilibrium |

According to Proposition 2, for all the types of subgames, when the demand is higher than the summation of the suppliers’ maximum bidding quantities (i.e., ), both suppliers will bid the highest price . The reason is that both suppliers’ bidding quantities will be fully sold out in this case, and the highest price will give the highest revenue to each supplier. Basically there is no impact of market competition in this case. However, for the and subgames, if the demand is lower than the threshold , there exists no pure price equilibrium. In contrast, for the subgame, it is also possible that when the demand is smaller than a threshold (i.e., ), both suppliers have to bid zero price and get zero revenue. The intuition is that the competition level of the subgame is higher than that of the and subgames due to both suppliers’ stable outputs, which leads to zero bidding prices if the demand is low. The result of the subagame has been proved in [17]. We present the proofs of subgames of type and type in Appendix.XVI.

V-C Equilibrium price-bidding strategy: mixed equilibrium

When the demand is such a level that there is no pure price equilibrium as shown in Proposition 2, we characterize the mixed price equilibrium between suppliers.

First, we define the mixed price equilibrium under the weakly dominant strategy in Definition 3, where denotes a probability measure101010A probability measure is a real-valued function that assigns a probability to each event in a probability space. of the price over [17].

Definition 3 (mixed price equilibrium).

A vector of probability measures is a mixed price equilibrium if, for both ,

for any measure .

Definition 3 states that the expected revenue of supplier cannot be increased if he unilaterally deviates from the mixed equilibrium price strategy . Let denote the CDF of , i.e., . Let and denote the upper support and lower support of the mixed price equilibrium , respectively, i.e., and . To characterize the mixed price equilibrium, we need to fully characterize the CDF function (including and ) for each .

Then, we show that the mixed price equilibrium exists for each type of subgames and characterize some properties of the mixed price equilibrium in Lemma 1. Lemma 1 can be derived following the same method for the case in [17]. Later, we discuss how to compute the mixed price equilibrium of the , , and cases, respectively.

Lemma 1 (characterization of the mixed price equilibrium).

For any pair , when the demand falls in the range where no pure price equilibrium exists as shown in Proposition 2, the mixed price equilibrium exists and has properties as follows.

(i) Both suppliers have the same lower support and the same upper support:

| (9) |

(ii) The equilibrium electricity-selling revenues satisfy:

| (10) |

(iii) For any , is strictly increasing over , and has no atoms111111The atom at means that the left-limit of CDF at satisfies . over . Also, cannot have atoms at for both .

Lemma 1 shows that both suppliers’ mixed-price-equilibrium strategies have the same support and have continuous CDFs over . Based on Lemma 1, we next characterize the mixed price equilibrium for the subgames of each type , , and .

V-C1 subgame (i.e., )

As shown in Proposition 2, when the demand satisfies , there is no pure price equilibrium. We can characterize a close-form equilibrium revenue for each supplier at the mixed price equilibrium, which has been proved in [17]. Furthermore, under the mixed price equilibrium, both suppliers get strictly positive revenues, while they may get zero revenues under the pure price equilibrium as shown in Proposition 2. We show the close-form equilibrium revenue in Appendix.XI.

V-C2 subgame (i.e., )

In the subgame, a mixed price equilibrium arises when . However, we cannot characterize a close-form equilibrium revenue, as in the case due to the penalty cost on the general renewable generations for the without-storage supplier. Instead, we can first characterize the CDF of the mixed price equilibrium assuming the lower support in Theorem 2, and then show how to compute the lower support in Proposition 3. We present the proofs in Appendix.XVI.

Theorem 2 (: CDF of the mixed price equilibrium).

In the subgame (i.e., ), when , suppose that the common lower support of the mixed price equilibrium is known. Then, the suppliers’ mixed equilibrium price strategies are characterized by the following CDF :

-

•

If , we have

(11) -

•

If , we have

(12) for any .

As shown in Theorem 2, supplier ’s mixed strategy is coupled with the other supplier’s equilibrium revenue . Next, we will explain how to compute the lower support . Toward this end, in (11) and (12), we replace the equilibrium lower support by a variable , and replace by to emphasize that is a function of . Lemma 1 (iii) implies that there exists a solution to the equation for at least one of the suppliers. Furthermore, we can prove that decreases in , and hence the solution (in ) to is unique. Then, we can compute the lower support in Proposition 3.

Proposition 3 (: computing the lower support ).

Based on the solution such that , , we consider two cases and compute the lower support as follows.

-

1.

If has a solution for both suppliers, then the equilibrium lower support is .

-

2.

If has a solution for only one supplier , we have this unique solution as the equilibrium lower support .

Through Theorem 2 and Proposition 3, we can compute the lower support and suppliers’ equilibrium revenues. Although we cannot obtain a close-form equilibrium revenue, in Theorem 3, we can show that in the subgame, if two suppliers’ random generations have the same mean value, then the with-storage supplier’s equilibrium revenue is always strictly higher than that of the without-storage supplier.

Theorem 3 (: revenue comparison).

If , and , then for both pure and mixed price equilibrium. Particularly, if follows a uniform distribution over , we have

| (13) |

Theorem 3 shows the dominance of the with-storage supplier in the subgame, whose electricity-selling revenue can be much higher than that of the without-storage supplier. The intuition is that the random generation makes the without-storage supplier at the disadvantage in the market (due to the penalty cost). This suggests potential economic benefits of storage investment for the supplier.121212Note that Theorem 3 only compares the revenue of the two suppliers. When considering the storage investment cost in Stage I and comparing the suppliers’ profit, we will have some surprising results shown in Section VI and Section VIII. However, investing in storage does not always bring benefits. If both suppliers invest in storage, it may reduce both suppliers’ revenues compared with the case that at least one supplier does not invest in storage. We will discuss it later in Proposition 5.

V-C3 subgame (i.e., )

In the case, both suppliers do not invest in storage and face the penalty cost. When , for the mixed price equilibrium, we can neither obtain the close-form equilibrium revenue as in the case nor obtain the equilibrium strategy CDF as in Theorem 2 of the case. Note that in the and subgames, at least one supplier is not subject to the penalty cost, which makes it possible to characterize the equilibrium strategy CDF or even close-form equilibrium revenue. In this subgame, we will characterize a range of the lower support in Proposition 4.

Proposition 4 (: lower support).

In the subgame (i.e., ), when , the lower support of the mixed price equilibrium satisfies

| (14) |

The bidding quantity is the minimal bidding quantity of supplier when he uses the mixed price strategy. Proposition 4 shows that this minimal bidding quantity cannot be too lower or too higher for both suppliers.

Note that the mixed price equilibrium has a continuous CDF over shown in Lemma 1, but we cannot derive it in close form. To have a better understanding of the CDF, we discretize the price to approximate the original continuous price set, and compute the mixed equilibrium for the discrete price set. The details are shown in Appendix.XII.

V-D Strictly positive revenue in the and subgames

Analyzing the equilibrium revenues of the three types of subgames, we show in Proposition 5 that in the and subgames, both suppliers always get strictly positive revenues.

Proposition 5 (strictly positive revenue with randomness).

In the and subgames, each supplier always gets strictly positive revenue at (both pure and mixed) equilibrium, i.e., .

This result is counter-intuitive for the following reason. Recall that in the subgame, both suppliers can get zero revenue if the demand is below a threshold as shown in Proposition 2. The common wisdom is that when the generation is random, the revenues of suppliers tend to be low due to the penalty cost. In contrast, Proposition 5 shows that the suppliers’ revenues are always strictly positive when the generation is random. Thus, the randomness can in fact be beneficial. The underlying reason should be understood from the point of view of market competition. The randomness makes suppliers bid more conservatively in their bidding quantities, which leads to less-fierce market competition and thus increases their revenues.

VI Equilibrium analysis of Stage I

In Stage I, each supplier has two strategies: (i) investing in storage, i.e., , and (ii) not investing storage, i.e., , which leads to a bimatrix game. For this bimatrix game, we can analyze the equilibrium strategy by simply comparing the profits for each strategy pair of the two suppliers. Note that while the electricity-selling revenue is given in the results of Section V, the profit also depends on the storage cost. To calculate the storage investment cost, we also propose a probability-based method using real data to characterize the storage capacity for the with-storage supplier in Section VII.

Each supplier’s profit can be calculated by taking the expectation of the equilibrium revenue in the local energy market at each hour, and subtracting storage investment cost over the investment horizon (scaled into one hour). Note that suppliers’ storage-investment strategy pairs lead to four possible subgames: subgame (i.e. ), subgame (i.e., , including two cases: and ), and subgame (i.e. ). Taking the expectation of equilibrium revenue over all the hours in the investment horizon, we denote supplier ’s equilibrium revenue in the and subgames as and , respectively. For the subgame, we denote the with-storage and without-storage supplier ’s equilibrium revenue as and , respectively. For illustration, we list the profit table with all four strategy pairs in Table II.

| Supplier 2: invest | Supplier 2: not invest | |

|---|---|---|

| Supplier 1: invest | ||

| Supplier 1: not invest |

Next, we will first derive the conditions for each storage-investment strategy pair to be an equilibrium, respectively. Then, we analyze the equilibrium with respect to the parameters of storage cost and demand. Finally, we show that both suppliers can get strictly positive profits in this storage-investment game.

VI-A Conditions of pure storage-investment equilibrium

We will characterize the conditions on the storage cost and the subgame equilibrium revenue for each strategy pair to become an equilibrium, respectively.

First, we define the pure storage-investment equilibrium in Definition 4, which states that neither supplier has an incentive to deviate from his storage-investment decision at the equilibrium.

Definition 4 (pure storage-investment equilibrium).

A storage-investment vector is a pure storage-investment equilibrium if the profit satisfies for any , and any .

Based on Definition 4, we characterize the conditions on the storage cost and the subgame equilibrium revenue for the storage-investment pure equilibrium in Theorem 4, the proof of which is presented in Appendix.XVII.

Theorem 4 (conditions of pure storage-investment equilibrium).

-

•

case is an equilibrium if , for both .

-

•

case is an equilibrium (where and ) if and .

-

•

case is an equilibrium if , for both .

If satisfies none of the conditions above, there exists no pure storage-investment equilibrium.131313Note that if or , then the set or . This means that the condition or cannot be satisfied.

Theorem 4 shows that the storage-investment equilibrium depends on the comparison between the storage cost and the revenue difference between the cases and , or the cases and . Also, Theorem 4 implies that a lower storage cost will incentivize the supplier to invest in storage.

According to Theorem 4, given the storage cost and the expected equilibrium revenue of each subgame, we can characterize the pure equilibrium for nearly all values of . However, if storage cost satisfies none of the conditions in Theorem 4, there will be no pure price equilibrium. Note that when there is no pure storage-investment equilibrium, we can always characterize the mixed equilibrium as the game in Stage I is a finite game[28]. We show how to compute the mixed equilibrium in Appendix.XVII.

Since we cannot characterize close-form equilibrium revenues for the and subgames, it remains challenging to characterize the storage-investment equilibrium with respect to the system parameters, e.g., the storage cost and demand. In the next subsection, we will focus on deriving insights of the storage-investment equilibrium in some special and practically interesting cases.

VI-B Impact of storage cost and demand on storage-investment equilibrium

We analyze the impact of storage cost and demand on the storage-investment equilibrium and have the analytical results for the cases when: (i) the storage cost is sufficiently large; (ii) the demand is sufficiently large or small. We present all the proofs in Appendix.XVII.

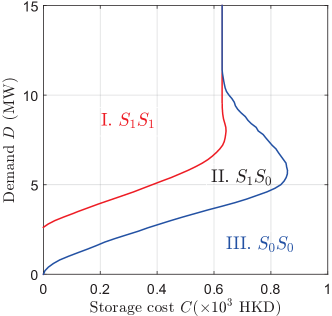

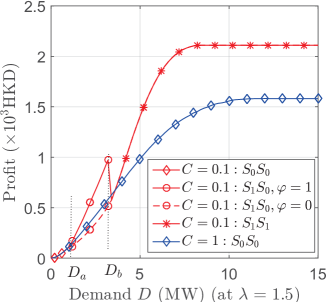

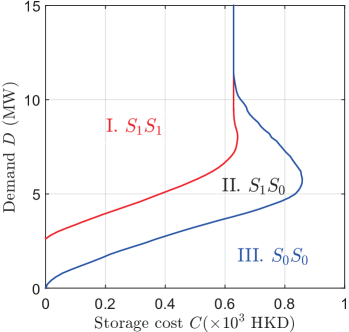

To better illustrate the storage-investment equilibrium, we show one simulation result of the equilibrium split (i.e., the storage-investment equilibrium with respect to parameters such as the demand and the storage cost) in Figure 3, and the details of the simulation setup are presented in Section VIII. In this simulation, for the illustration purpose, we consider the same demand for any hour of any month . We also consider two homogeneous suppliers (with the same storage cost, the same renewable energy capacity and the same renewable energy distribution) to reveal the impact on storage-investment decision.141414We can prove that a pure Nash equilibrium of storage investment always exists in this homogeneous case. However, for the heterogeneous case, we cannot theoretically prove that the pure Nash equilibrium always exists. In Appendix, we simulate an example with two heterogeneous suppliers (with different capacities of renewables) and show the storage-investment equilibrium in such a heterogeneous case. In Figure 3 (where the penalty price is Hong Kong dollars (HKD) per kWh), with respect to the demand and storage cost, the storage-investment equilibrium is divided into three regions: Region I of (the left side of the red curve), Region II of (between the red curve and the blue curve), and Region III of (the right side of the blue curve).

First, for the impact of the storage cost, a higher storage cost will discourage suppliers from investing in storage as implied in Theorem 4. We will further show that when the storage cost is higher than a threshold, no suppliers will invest in storage no matter what the demand or penalty. However, counter-intuitively, we also find that in the case of a zero storage cost, not both suppliers will invest in storage once the demand is lower than a certain threshold.

As shown in Figure 3, when the storage cost is larger than a threshold, i.e., HKD, the case will be the only equilibrium (independent of the demand ) and no suppliers invest in storage. We show this property in Proposition 6. The reason is that the benefit from investing in storage is bounded. When the storage cost is greater than a threshold corresponding to the bounded benefit, no suppliers will choose to invest in storage.

Proposition 6.

There exists a threshold such that if the storage cost satisfies for both , the case will be the unique pure storage-investment equilibrium.

However, as shown in Figure 3, when the demand is smaller than a certain threshold, i.e., MW, the case cannot be a pure equilibrium even when the storage cost . We show this property in Proposition 7. The reason is that when the demand is smaller than a certain threshold, in the case, both suppliers can only get zero revenues (as shown in Proposition 2) due to the competition. Thus, if the case is the storage-investment state where both suppliers invest in storage, one supplier can always deviate to not investing in storage, which can bring him a strictly positive profit as implied in Proposition 5.

Proposition 7.

If the demand satisfies for any and , the case cannot be the equilibrium.

Second, for the impact of demand, we already show that at a sufficiently low demand, the case cannot be the equilibrium in Proposition 7. We will further show that if the demand is higher than a certain threshold, each supplier has a dominant strategy of whether to invest in storage based on his storage cost, which does not depend on the other supplier’s decision. For example, at MW in Figure 3, for these two homogeneous suppliers, if the storage cost is higher than a threshold, i.e., HKD, each supplier will not invest in storage (i.e., ); otherwise, each supplier will invest (i.e., ). We show this property in Proposition 8. The reason is that if the demand is large enough, both suppliers can bid the highest price and sell out the maximum bidding quantity. Thus, there is no competition between suppliers, and they will make storage-investment decisions based on their own storage costs.

Proposition 8.

There exists and , such that when the demand satisfies for any and , supplier has the dominant strategy as follows.151515 We characterize the close-form threshold and in Appendix.XVII.

| (15) |

VI-C Strictly positive profits of suppliers

We show that in suppliers’ competition facing the cost of storage investment, both suppliers can get strictly positive profits.

Proposition 9 (strictly positive profit).

Both suppliers will get strictly positive profits at the storage-investment equilibrium.

This proposition also shows the benefit of the uncertainty of renewable generation, which is similar to Proposition 5. Recall that if both suppliers have stable outputs, they may get zero revenue (shown in Proposition 2) and thus get negative profit considering the storage cost. However, with the random generation, both suppliers will get strictly positive profits at the storage-investment equilibrium even facing the storage cost. We will explain it as follows. Note that in the case or the case, the without-storage supplier always gets a strictly positive revenue (shown in Proposition 5) with a zero storage cost. In the case or the case, if the with-storage supplier gets a non-positive profit, he can always deviate to not investing in storage. This deviation provides him a strictly positive profit, which implies that the supplier will always get strictly positive profit.

VII Characterization of storage capacity

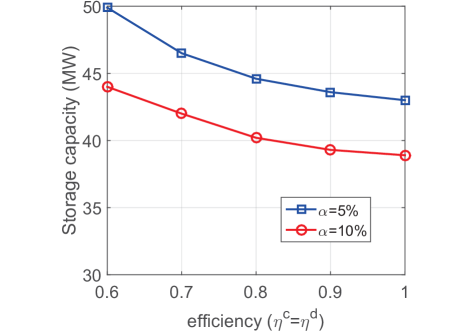

We propose a probability-based method using historical data of renewable generations to compute the storage capacity. Note that suppliers charge and discharge the storage to maintain his output at the mean value of the random renewable generations as shown in (1).161616It is interesting to size the variable storage capacity considering the possibility of not completely smoothing out the renewable output. However, it is quite challenging to characterize such an equilibrium storage capacity in closed-form, which we will study as future work. Therefore, the charge and discharge amounts are also random variables, and we characterize the storage capacity such that its energy level will not exceed the storage capacity with a targeted probability. In this part, we focus on the storage with 100% charge and discharge efficiency and no degradation cost. In Appendix.XIII, we show that a lower charge/discharge efficiency and the consideration of degradation cost will increase the total storage cost of a supplier, which further affects the storage-investment equilibrium.

To begin with, we set a probability target , and we aim to find a storage capacity such that the energy level in the storage exceeds the capacity with a probability no greater than . Specifically, the with-storage supplier will charge and discharge storage with value at hour of month as shown in (1). We assume that the initial energy level of storage is fixed for all the months and denote it as . Note that the energy level of storage is the sum of the charge and discharge over the time, and is constrained by the storage capacity. Starting from the initial energy level , the probability that energy level exceeds the minimum capacity (i.e., zero) and the maximum capacity (i.e., ) of the storage in a day of month is and , respectively. Considering all months , we aim to choose the storage capacity so that the following hold:

| (16) | |||

| (17) |

Then, we describe how to use historical data [29] to compute the storage capacity that satisfies the probability threshold as in (16) and (17). we will first characterize an upper bound for the probability that energy level exceeds the given storage capacity in terms of the random variable , and then we propose Algorithm 1 to compute the required storage capacity to satisfy (16) and (17).

First, given the underflow capacity and overflow capacity , we characterize an upper bound for and an upper bound for , respectively. We characterize these upper bounds based on Markov inequality [30], which is shown in Proposition 10.

Proposition 10 (Markov-inequality-based upper bound).

Given and , the Markov-inequality-based upper bounds are shown as follows.

-

•

For the upper bound :

(18) where .

-

•

For the upper bound :

(19) where .

Note that and are decreasing in and , respectively. Also, as , and as . These show that a larger capacity will decrease the probability that the charge/discharge exceeds the capacity. Also, for any probability threshold , we can always find a capacity, such that the probability that energy level exceeds the capacity is below .

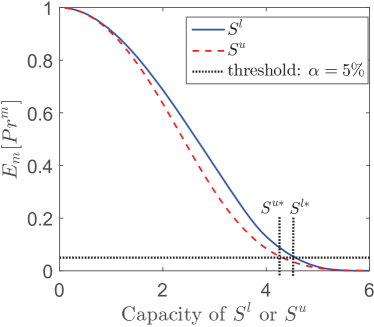

Second, we propose Algorithm 1 to characterize the storage capacity based on the historical data of (derived from the renewable generation data of ). We use the underflow capacity for supplier as an example for illustration, and the overflow capacity follows the same procedure. Specifically, for the underflow capacity , we search it in an increasing order from zero as in Step 4. Given , for each month , we calculate the exceeding probability according to (18) as in Steps 5-7. Note that based on the data samples of , is strictly convex in . Thus, for any , the value of can be efficiently computed using Newton’s method[31]. Further, we conduct an exhaustive search for to obtain . We calculate the expected exceeding probability over months as in Step 8. We obtain the minimal underflow capacity if the exceeding probability satisfies as in Step 9. Similarly, we can get the minimal overflow capacity . The required storage capacity is calculated as in Step 11.

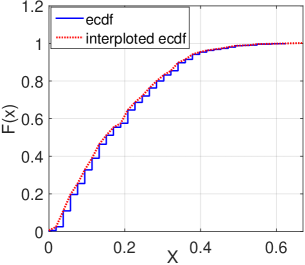

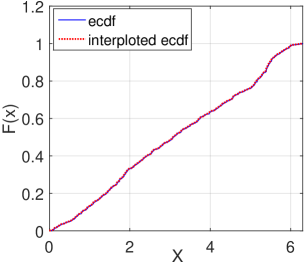

As an illustration, we calculate and show the underflow probability and overflow probability in the blue solid curve and red dashed curve respectively in Figure 4. The probability of (, respectively) decreases with respect to the capacity (, respectively). If the capacity (, respectively) is small and close to zero, the exceeding probability (, respectively) will approach one. However, when the capacity is large and close to a certain value (e.g., 6 in Figure 4), the corresponding exceeding probability will be close to zero. We choose the probability threshold and obtain the corresponding minimal capacity and as marked in Figure 4.

VIII Simulation

In simulations, in addition to some analytical properties of storage-investment equilibrium shown in Section VI, we will further investigate the impact of the penalty, storage cost, and demand on suppliers’ profits. We will show some counter-intuitive results due to the competition between suppliers. For example, a higher penalty, a higher storage cost, and a lower demand can even increase a supplier’s profit at the storage-investment equilibrium. Furthermore, the first supplier who invests in storage may benefit less than the competitor who does not invest in storage. We will illustrate the detailed results in the following.

VIII-A Simulation setup

In simulations, we consider two homogeneous suppliers (with the same renewable capacity, generation distribution, and storage cost) to show the storage-investment equilibrium. We also consider a fixed demand for all the hours and months for illustration. Next, we explain the empirical distribution of renewable generation as well as parameter configurations of the penalty price , demand , and storage cost .

VIII-A1 Empirical distribution of renewable generation

We use the historical data of solar energy generation in Hong Kong from the year 1993 to year 2012 [29] to approximate the continuous CDF of suppliers’ renewable generations. Specifically, we cluster the renewable generations at hour of all days into types (months) considering the seasonal effect. We use daily data (from the year 1993 to year 2012) of renewable energy in month at hour to approximate the distribution of renewable generation at hour of month . Based on the discrete data, we characterize a continuous empirical CDF to model the distribution of renewable power. We present the details of the characterization of empirical CDF in Appendix.XIV.

Furthermore, to check the reliability of the empirical distribution, we consider two sample data sets: one set consists of all the data samples from the year 1993 to 2012, and the other consists of the data samples from another specific year (e.g., 2013). We conduct Kolmogorov-Smirnov test [32] using the Matlab function kstest2 to test whether these two data sets are from the same continuous distribution [33]. The result shows that most of the hours of a month can pass the test. Also, our model is general for any continuous distribution of renewable generations. Interested readers can also use other data or other distributions of renewable energy to test the results.

VIII-A2 Parameters configuration

We explain the configuration of the parameters of the penalty price , demand , and storage cost , respectively. We set the parameters to reflect the real-world practice, and study the impact of the parameters on the market equilibrium.

-

•

The penalty : We choose the price cap HKD/kWh, since the electricity price for residential users in Hong Kong is around 1 HKD/kWh [34]. Note that a penalty price satisfies . In Figure 6(a), we will consider a wide range of the ratio to demonstrate the impact of the penalty. In Figures 6(b)(c)(d), we fix the penalty price HKD/kWh and focus on illustrating the impact of other parameters.

-

•

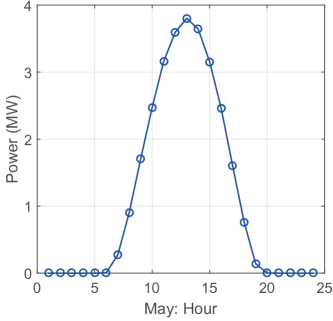

The demand : In Figure 6(d), we will discuss a wide range of demand from 0 MW to 15MW to show the impact of the demand. As a comparison, in Figure 5, we show the average renewable power across hours in May. In Figure 6(a) and (b), we fix the demand at MW to show the impact of other parameters ( and ). In Figure 6(c), we choose a larger demand MW and a smaller demand MW to show the impact of demand on the equilibrium profit.

-

•

The Storage cost : Recall that the storage investment cost is . There are different types of storage technologies with diverse capital costs and lifespans. For example, the pumped hydroelectric storage is usually cheap, and can last for 30 years with the capital cost HKD/kWh, while the Li-ion battery can last 15 years with the capital cost about HKD/kWh [35]. We choose the annual interest rate , and the storage capacity for the with-storage supplier is characterized as 43 MWh by Algorithm 1. We capture the impact of parameters and through the storage cost . According to the calculation of storage investment cost , we can calculate that the (hourly) investment cost of the pumped hydroelectric storage is HKD and the cost of the Li-ion battery is HKD. This shows that the storage cost can have a wide range.171717Note that we only consider the investment cost in the storage cost. In practice, there are also other costs that need to be included, such as maintenance cost. Then, in Figures 6(c), we will consider a wide range of storage costs from 0 to HKD. Although zero storage cost is not very practical, we use it to show a low storage cost and capture the entire range of the impact of the storage costs. In Figure 6(a)(b)(d), we choose lower storage costs ( and HKD) and higher storage costs ( and HKD) to show the different results under different storage costs.

VIII-B Simulation results

We will discuss the impact of penalty, storage cost, and demand on suppliers’ profits, and show some counter-intuitive results due to the competition between suppliers.

VIII-B1 The impact of penalty on suppliers’ profits

Although a higher penalty can increase the penalty cost on the without-storage supplier, surprisingly, we find that a higher penalty can also increase this supplier’s profit, due to the reduced market competition in the energy market.

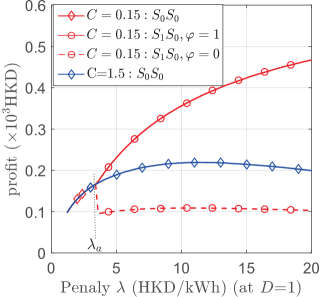

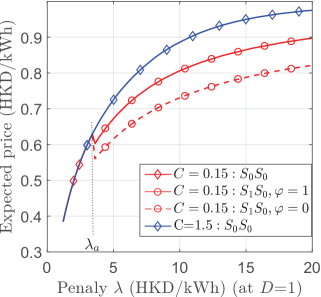

We show how suppliers’ profits and expected bidding prices at the storage-investment equilibrium change with the penalty (at demand MW) in Figure 6 and 6, respectively. Different colors represent different storage costs. The diamond marker shows that is the storage-investment equilibrium, and the circle marker shows that is the equilibrium. Also, when is the equilibrium, the solid lines and dashed lines distinguish the with-storage supplier and without-storage supplier, respectively.

First, we show that at the equilibrium where both suppliers do not invest in storage (i.e., ), a higher penalty can increase both suppliers’ profits. As shown in Figure 6, when the storage cost is high at HKD, both suppliers will not invest in storage for any value of the penalty from HKD/kWh to HKD/kWh (in blue curve with diamond marker). In this case, both suppliers’ profits can first increase (at HKD/kWh) and then decrease (at HKD/kWh) with (in blue curve). The intuition for the increase of profit at HKD/kWh is that a higher penalty decreases both suppliers’ bidding quantity if the bidding price remains the same. This reduces the market competition and enables both suppliers to bid a higher price in the local energy market as shown in Figure 6 (in blue curve). However, the increased penalty also increases the penalty cost on suppliers, so the suppliers’ profits will also decrease if the penalty is too high (at HKD/kWh).

Second, we show that at the equilibrium where one supplier invests in storage and one does not (i.e., ), a higher penalty can also increase both suppliers’ profits. We consider a low storage cost HKD as in red curves in Figure 6 and Figure 6. We see that if is low (at ), both suppliers will not invest in storage (i.e., ), and their profits increase with penalty shown in Figure 6 (at in red curve with diamond marker that overlaps with blue curve). As the penalty increases (at ), the equilibrium will change from to , since a higher penalty and a lower storage cost can enable a supplier to enjoy more benefits by investing in storage. We discuss the profit of the with-storage supplier and without-storage supplier respectively as follows.

-

•

For the with-storage supplier, as shown in Figure 6, when , his profit increases as penalty increases (in red solid curve), which can be much higher than the without-storage supplier (in red dashed curve). The reason is that in the case, the penalty cost makes the with-storage supplier dominate over the without-storage one. The with-storage supplier can bid higher prices than the without-storage supplier as shown in Figure 6 (in red solid curve and red dashed curve), and he also does not need to pay the penalty cost.

-

•

However, for the without-storage supplier, as shown in Figure 6, his profit also slightly increases as the penalty increases around HKD/kWh (in red dashed curve). The intuition is that a higher penalty gives the advantage to the with-storage supplier, which reduces the market competition and increases both suppliers’ bidding price as shown in Figure 6 (in red curves). Thus, it can also benefit the without-storage supplier. However, as shown in Figure 6, if the penalty further increases to HKD/kWh (in red dashed curve), the without-storage supplier’s profit will also decrease due to the increased penalty cost.

VIII-B2 The impact of storage cost on suppliers’ profits

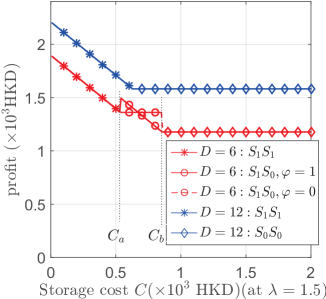

Intuitively, a higher storage cost will discourage a supplier from investing in storage, which generally decreases a supplier’s profit. However, we find that it may also increase a supplier’s profit if the other supplier changes his strategy due to the increased storage cost.

We show how suppliers’ profits at the storage-investment equilibrium change with the storage cost in Figure 6. Different colors represent different demands. The diamond marker, circle marker, and star marker correspond to different storage-investment equilibria of , , and , respectively. For the case, the solid lines and dashed lines distinguish the with-storage supplier and without-storage supplier, respectively.

As shown in Figure 6 (in both red curve and blue curve), generally the higher storage cost decreases suppliers’ profits. However, we show that the opposite may be true using the example of MW (in red curve). When the demand is at MW (in red curve), as the storage cost increases, the equilibrium changes from (when ), to (when ), and finally to (when ). When the equilibrium changes from to at the threshold , one with-storage supplier in the original case has a higher (upward jumping) profit, after the other supplier chooses not to invest in storage due to the high storage cost. This changes the equilibrium from to , which reduces the competition and gives more advantages to the with-storage supplier.

VIII-B3 The impact of demand on suppliers’ profits

Intuitively, a higher demand will increase a supplier’s profit. However, we show that a higher demand may also decrease a supplier’s profit if the other supplier changes his strategy due to the increased demand.

We show how suppliers’ profits at the storage-investment equilibrium change with the demand in Figure 6. Different colors represent different storage costs. The diamond marker, circle marker, and star marker correspond to different storage-investment equilibria of , , and , respectively. For the case, the solid lines and dashed lines distinguish the with-storage supplier and without-storage supplier respectively.

As shown in Figure 6 (in both red curve and blue curve), generally a higher demand increases a supplier’s profit. However, we show that the opposite may be true using the example of HKD (in red curve). When the storage cost is low at HKD (in red curve), as the demand increases, the equilibrium changes from (when ), to (when ), and finally to (when ). When the equilibrium changes from to at the threshold , the with-storage supplier in the original case has a smaller (downward jumping) profit, after the other supplier also chooses to invest in storage due to the high demand. This changes the equilibrium from to , which increases the market competition and weakens the advantage of the with-storage supplier in the original case. Furthermore, when the storage cost is high at HKD (in blue curve with diamond marker), both suppliers will not invest in storage independent of the demand.

VIII-B4 First-mover disadvantage and advantage

Intuitively, the first supplier who invests in storage can benefit more than the without-storage competitor. However, we find that if the storage cost is high, the first-mover supplier in investing storage can also benefit less than the free-rider competitor who does not invest in storage.

As shown in Figure 6 at MW (in red curve), the case is the equilibrium when the storage cost is in the range . If the storage cost is low at , the with-storage supplier’s profit is higher than the without-storage supplier’s profit. However, if the storage cost is high at , the with-storage supplier’s profit is lower than the without-storage supplier. This shows both advantage and disadvantage of the first-mover. Although in some situations investing storage will increase the supplier’s profit, he can get more profits if he waits for the other to invest first when the storage cost is high. However, if the storage cost is low, he should be the first to invest storage in order to get a higher profit.

IX Extensions: A more general oligopoly model

We build a more general oligopoly model and extend some of the theoretical results and insights from the duopoly case to the oligopoly case. Compared with the duopoly model, the only difference of the oligopoly model is that the number of suppliers can be more than two, i.e., . Following the analysis of the duopoly model, we also analyze the equilibrium in Stage II and Stage I in the oligopoly case and derive some insights. Specifically, in Stage II, we extend the theoretical results of the price-quantity competition equilibrium. In Stage I, we generalize analytical results of the impact of storage cost and demand on the storage-investment equilibrium. Furthermore, we show that some of the key insights from the duopoly case, e.g., the uncertainty of renewable generation can be beneficial to suppliers, still hold in the oligopoly case. Next, we will discuss the extensions of Stage II and Stage I in detail, respectively. We include all the proofs of the propositions in Appendix.XVIII.

IX-A Stage II Analysis

For Stage II, the weakly dominant strategy of bidding quantities still hold for the case of more than two suppliers. We generalize the conditions on the existence of the pure price equilibrium and show that the mixed price equilibrium also exists in the oligopoly case. Furthermore, we show that suppliers get positive revenues at the mixed price equilibrium. We show the extended analysis in detail as follows.

IX-A1 Weakly dominant strategy for bidding quantities

The weakly dominant strategies for bidding quantities still hold as in Theorem 1.

IX-A2 Existence of the pure price equilibrium

We derive the conditions for the existence of the pure price equilibrium among suppliers, and generalize Proposition 2. Specifically, we consider a general subgame in Stage II denoted as , where suppliers in the set invest in storage and suppliers in the set do not invest. Recall we denote the set of all the suppliers as , and we have . The case means that all the suppliers invest in storage, and the case means that no supplier invests in storage. We show the existence of the pure price equilibrium in Proposition 11.

Proposition 11 (existence of the pure price equilibrium in the oligopoly case).

Considering a subgame of storage investment among suppliers in Stage II, the existence of the pure price equilibrium depends on the demand as follows:

-

•

If , there exists a pure price equilibrium , with an equilibrium revenue for any and for any .

-

•

If for any , there exists a pure price equilibrium , with an equilibrium revenue , for any .

-

•

If there exists such that , there is no pure price equilibrium.

Similar to the duopoly case, the result of this proposition can be interpreted as follows. If the demand is higher than the threshold , all the suppliers can bid the price cap to sell the maximum quantities. If the demand is very low such that for any , the competition is fierce and all the suppliers bid zero price. However, if the demand is in the middle, there will be no pure price equilibrium.

Note that if the number of with-storage suppliers is no greater than one, i.e., , the condition that there exists such that cannot be satisfied. It means that there will be no pure equilibrium of for any demand .

IX-A3 Existence of the mixed price equilibrium

For the case in Proposition 11 that there exists no pure price equilibrium, we show that there exists a mixed price equilibrium. However, the characterization of mixed strategy is highly non-trivial for the oligopoly case and it is difficult to completely generalize Lemma 1. We generalize it partially as Proposition 12 to show the existence of the mixed price equilibrium and show that all the suppliers get positive revenues at the mixed price equilibrium.

Proposition 12 (mixed price equilibrium in the oligopoly case).

For any , when there is no pure price equilibrium, a mixed price equilibrium exists and the equilibrium electricity-selling revenues satisfies .