Optimal Convergence Trading with Unobservable Pricing Errors

Abstract.

We study a dynamic portfolio optimization problem related to convergence trading, which is an investment strategy that exploits temporary mispricing by simultaneously buying relatively underpriced assets and selling short relatively overpriced ones with the expectation that their prices converge in the future. We build on the model of Liu and Timmermann [22] and extend it by incorporating unobservable Markov-modulated pricing errors into the price dynamics of two co-integrated assets. We characterize the optimal portfolio strategies in full and partial information settings both under the assumption of unrestricted and beta-neutral strategies. By using the innovations approach, we provide the filtering equation that is essential for solving the optimization problem under partial information. Finally, in order to illustrate the model capabilities, we provide an example with a two-state Markov chain.

Key words and phrases:

optimal control, convergence trade, regime-switching, partial information2010 Mathematics Subject Classification:

91G10, 91G801. Introduction

Convergence-type trading strategies have become one of the most popular trading strategies that are used to capitalize on market inefficiencies, or deviations from “equilibrium,” especially with the rapid developments in algorithmic and high-frequency trading. For a typical convergence trade, temporary mispricing is exploited by simultaneously buying relatively underpriced assets and selling short relatively overpriced assets in anticipation that at some future date their prices will have become closer. Thus one can profit by the extent of the convergence. A prime example of a convergence trade is a pairs trading strategy that involves a long position and a short position in a pair of similar stocks that have moved together historically and hence an investor can profit from the relative value trade arising from the cointegration between asset price dynamics involved in the trade. Other examples of convergence-type trading strategies can be given as risk arbitrage (known also as merger arbitrage) that speculates on successful completion of a merger of two companies or cash and carry trade that tries to benefit from pricing inefficiencies between spot market and futures market of the same underlying stock or commodity by simultaneously placing opposite bets on spot and futures markets.

In this work, we extend the convergence trade model given by Liu and Timmermann [22] that investigate the dynamic optimal portfolio allocation via expected utility maximization from terminal wealth, with two co-integrated assets with pricing errors and a market index. Liu and Timmermann [22] show that under recurring and non-recurring “arbitrage” opportunities, optimal portfolio allocations could deviate from conventional long-short delta-neutral strategies and it can be optimal to hold both risky assets long (or short) at the same time. We extend Liu and Timmermann [22] mainly in two directions. First, we assume that pricing errors related to the co-integrated assets are modulated by a continuous-time, finite-state Markov chain, which is taken to be unobservable and hence needs to be filtered out. Taking pricing errors (or “alphas” as commonly referred in finance literature) dependent on a hidden Markov chain captures certain salient features of convergence trade. Although most of the existing literature assumes that pricing errors are fully observable, in reality, those errors, albeit having a stochastic nature, cannot be known precisely or may depend on some unobservable state variables that change accordingly to certain factors in the economy or the market. By modeling those pricing errors depending on an unobservable regime-switching factor, we would like to build a more realistic representation for convergence trading. The second extension of our model is that we allow capital asset pricing model (CAPM) betas of two risky assets to be different. That enables us to show the optimal portfolio allocation for beta-neutral pairs trading, which is designed to keep the portfolio’s beta zero all the time and hence achieve market neutrality. It is a common market practice among pairs traders to have a beta-neutral portfolio to avoid market risk. Moreover, allowing different betas also enables us to account for “betting against beta” strategies that involve going short with high-beta stocks and going long with low-beta ones. Betting against beta type strategies are often associated with fluctuating low alpha Frazzini and Pedersen [14], which also justifies our choice of modeling pricing errors under regime switching and partial information.

There is a growing stream of literature about optimal convergence trading. Liu and Longstaff [21] has a partial equilibrium examination of convergence trading strategies, where the mispricing is modeled using a Brownian bridge. Jurek and Yang [17] incorporate an Ornstein–Uhlenbeck process to model the spread for non-myopic investors and solve the dynamic portfolio allocation for constant relative risk aversion and recursive Epstein–Zin utility function. By building on the results of Jurek and Yang [17], Liu and Timmermann [22] solve a similar problem by focusing both on recurring and non-recurring arbitrage opportunities in a continuous error-correction model with two co-integrated assets and a market index. Lei and Xu [20] extend Liu and Timmermann [22] by incorporating transaction costs. Inspired by the dynamic pairs trading model of Mudchanatongsuk et al. [23], Tourin and Yan [26] develop an optimal portfolio strategy to invest in two risky assets and the money market account, assuming that log-prices are co-integrated, and solve the optimal portfolio allocation problem for the exponential utility. Cartea and Jaimungal [9] extend Tourin and Yan [26] to allow the investor to trade in multiple co-integrated assets. Chiu and Wong [10] investigates the optimal dynamic trading of cointegrated assets using the classical mean-variance portfolio selection criterion. Angoshtari [3] studies the necessary and sufficient conditions for well-posedness and no-arbitrage for the model of Liu and Timmermann [22] by focusing on the concept of investor nirvana.

Considering similar problems under regime-switching and/or partial information in the literature, studies focusing on the dynamic portfolio choice problem are rather limited. Lee and Papanicolaou [19] solve the optimal pairs trading problem within a power utility setting, where the drift uncertainty is modeled by a continuous Gaussian mean-reverting process and necessitates Kalman filtering to extract the unobservable state process. Altay et al. [2] extend the pairs trading model of Mudchanatongsuk et al. [23] by incorporating regime switching under partial information and risk penalization. However, classical portfolio selection problems, which do not cover portfolios involving co-integrated assets, in a full or partial information and/or Markov regime-switching framework can be found, for example, in Zhou and Yin [28], Bäuerle and Rieder [6], and Sotomayor and Cadenillas [24] for the full information case with Markov regime switching or Bäuerle and Rieder [7], Björk et al. [8] and Frey et al. [15] for the partial information case.

In summary, we have the following key contributions. First, we compute the optimal unrestricted and beta-neutral strategies both in full and partial information settings for a log-utility trader by using dynamic programming. Second, we characterize the value function as the unique (classical) solution of the Hamilton–Jacobi–Bellman (HJB) equation, which is reduced to a system of ordinary differential equations (ODE) in the full information case, and given by a system of partial differential equations (PDE) in the partial information case. We also provide verification results for both cases. Third, to solve the convergence trade problem under partial information we compute the filtering equation by applying the innovations approach. Having the filter dynamics enables us to study the equivalent reduced problem where unobservable states of the Markov chain are replaced by their optional projection over the available filtration. Comparing optimal strategies under full and partial information, we obtain that the certainty equivalence principle holds, i.e., the optimal portfolio strategy in the latter case can be obtained by replacing the unobservable state variable with its filtered estimate. Finally, we analyze an example with a two-state Markov chain numerically and demonstrate certain features of our proposed model. In particular, we illustrate the dominance of unrestricted strategies over beta-neutral strategies. Moreover, we show that a trader who uses averaged data (in terms of parameters) is not performing better than the trader who uses a Markov modulated model in a full information setting. For the partial information case, our example suggests that there is a non-negative information premium, indicating that the fully informed trader has an advantage over the partially informed one.

The remainder of the paper is organized as follows. Section 2 introduces the model setting and the notation. In Section 3 we study the portfolio optimization problem in a full information setting with regime switching. In Section 4 we solve the utility maximization problem under partial information. In Section 5, we provide a numerical analysis of an example with a two-state Markov chain. We conclude with Section 6. In order to improve the flow of the paper we provide proofs of all results in the Appendix.

2. Model Setting and Notation

We study a modification of the continuous-time error-correction model of Liu and Timmermann [22] in a regime-switching setup under both full and partial information. Precisely we fix a probability space and a finite time horizon which coincides with the terminal time of an investment. We also introduce a complete and right-continuous filtration , representing the full information flow, and assume that all processes defined below are adapted to .

Let be a continuous-time finite-state Markov chain taking values in , for , where, without loss of generality, we assume that is the -th canonical vector in , for every . We denote by the infinitesimal generator of , with for every and , and let be its initial distribution.

Remark 2.1.

The finite-state nature of the Markov chain implies that for every , and every function we have where , for every .

We consider a market model where a trader can invest in a riskless asset with constant rate of return and three risky assets with price processes and , where the first one represents the market index and the other two are co-integrated assets. We assume that the price dynamics of market index is given by

| (2.1) |

where is the market risk premium, is the market volatility and is a standard Brownian motion. Moreover co-integrated asset prices are described by the following SDEs,

| (2.2) |

| (2.3) |

with and . Coefficients and are constant parameters and is a three-dimensional standard Brownian motion independent of .

We define the spread process by , for every . Here represents the mean-reverting component of pricing errors. We assume that -a.s. for every , so that becomes a stationary process with the dynamics

| (2.4) |

where

| (2.5) |

In (2.2) and (2.3), the infinitesimal expected returns are

and

respectively. It is evident from the form of infinitesimal returns that if is chosen to be identical to zero or is equal to , for every , asset price dynamics satisfy the CAPM relation, meaning that CAPM establishes the expected returns correctly and there is no mispricing in either asset. On the other hand, for example, if , the first asset has a higher expected return than it is justified by its exposure to market risk, and hence has a positive alpha, meaning it is undervalued. By choosing and dependent on the hidden Markov chain , we therefore, postulate that pricing errors (or alphas) depend on some common factor in the economy or the market that can not be directly observed by the trader. Also, as it is suggested by Liu and Timmermann [22], one can interpret those pricing errors as reflecting momentarily positive or negative liquidity shocks, which may vanish in liquid markets. For example, because of liquidity effects, stocks listed in S&P 500 have overstated betas Vijh [27], which in turn affects pricing errors. By assuming a regime-switching framework for pricing errors, we are also able to model such liquidity effects. This type of liquidity effects and related mispricing is actually very important for trades involving dual-listed companies (or so-called “Siamese twin” companies), which are incorporated in different countries and listed in different exchanges simultaneously while operating as a single entity. For such companies, since shares listed in different exchanges have same control rights and dividends are based on the same cash flow, most of the mispricing between two stocks is due to liquidity effects arising from stock exchanges that individual shares are traded in and hence prone to different regimes; see De Jong et al. [11] for more on stock price differentials of dual-listed companies. We should also remark that when we take and , the model becomes a regime-switching version of the original one suggested by Liu and Timmermann [22] that involves two assets with the same payoff trading at different prices.

3. Optimal Convergence Trade under Regime Switching

Let be the value of a portfolio , where quantities and denote fractions of the wealth invested at any time in the market index and in the co-integrated assets with prices and , respectively. Consequently the percentage of wealth invested in the riskless asset is . We introduce now the suitable set of strategies.

Definition 3.1.

A -admissible portfolio strategy is a self-financing, -predictable strategy such that

| (3.1) |

The set of -admissible strategies is denoted by .

For every , the dynamics of the convergence trading portfolio is given by

We consider a trader with logarithmic preferences and who aims to maximize the expected utility from terminal wealth at time in a market with regime switching. In this section, we assume that the trader may directly observe the state of the Markov chain Y that influences the dynamics of price processes and the spread. Formally, we address the following problem

| (3.2) |

where denotes the conditional expectation given , and . We define the value function corresponding to problem (3.2) as

| (3.3) |

Notice that for a given , is a controlled process. For the sake of notational simplicity from now on we suppress dependency and write instead of .

In Theorem 3.1, we address the optimization problem by applying dynamic programming. Our goal is to identify the optimal strategy as well as to characterize the value function as the unique solution of the corresponding HJB equation. This approach permits to examine the value function of the control problem in detail. One could alternatively derive the stochastic representation of the value function and characterize it up to the solution of a system of partial differential equations via Feynman–Kac type arguments for Markov-modulated diffusion processes; see, e.g., Baran et al. [5] and Escobar et al. [12].

In the sequel, we will use the following notation for the partial derivatives: for every function we write, for instance, . Also, by Remark 2.1 we have that and , for and .

Theorem 3.1.

Consider a trader endowed with a logarithmic utility function. Then the optimal portfolio strategy is

| (3.4) | |||||

| (3.5) | |||||

| (3.6) |

with and . The value function is of the form

| (3.7) |

where functions , and for solve the following system of ordinary differential equations

| (3.8) | |||

| (3.9) | |||

| (3.10) |

with terminal conditions , and for all , and where is given in (2.5) and

We provide the proof of the Theorem 3.1 in the Appendix.

Remark 3.2 (Discussion on the optimal trading strategy.).

The optimal trading strategy is Markov modulated and has a typical structure of a mean-variance portfolio weights. More specifically, numerator of each portfolio weight , , is associated with regime-switching parameters, and , related to the co-integration between and , or equivalently, to pricing errors. The denominator, on the other hand, is akin to the idiosyncratic risk components, , and . We should also emphasize that and do not depend on market parameters, , , and , since the market exposure of each asset is covered by investing in the market index. and can be seen as the relative idiosyncratic variation of (resp. ) with respect to (resp. ). The role of is actually to scale the contribution of pricing error and the independent idiosyncratic variance of in . Naturally, has the analogous interpretation. Note that when , meaning that there is no correlation between and , those contributions vanish and the optimal portfolio weights in each stock only depend on their own pricing errors and idiosyncratic risks. The structure of the market portfolio weight is similar to that in Liu and Timmermann [22] and given by the sum of Sharpe’s ratio of the market index and a linear combination of and , weighted by their corresponding betas. Finally as and are prone to different regimes so is , even if the market index dynamics is independent of the Markov chain.

3.1. Optimal Beta-Neutral Investment

To achieve market neutrality, traders may chose investment strategies so that the resulting portfolio has zero (CAPM) beta. The goal of this section is to characterize this type of trading strategies which are called beta-neutral. We should also remind the reader that this type of strategies can also be used for “betting against betas” type strategies in which high beta asset (short leg) is deleveraged so that its betas has been decreased to and the low beta asset (long leg) is leveraged so that its beta has become 1. We start with a formal definition.

Definition 3.3.

A -admissible beta-neutral portfolio strategy is -predictable self-financing strategy such that

and satisfying . We denote the set of -admissible beta-neutral strategies by .

In the next theorem we compute the optimal beta-neutral investment strategies and the corresponding value function. The proof of this result replicates that of Theorem 3.1 and it is therefore omitted.

Theorem 3.2.

Consider a trader with a logarithmic utility function. Then the optimal beta-neutral investment strategy is given by

| (3.11) | |||

| (3.12) | |||

| (3.13) |

The value function is of the form

| (3.14) |

where the functions , and for solve the following system of ordinary differential equations

| (3.15) | |||

| (3.16) | |||

| (3.17) |

with terminal conditions , and for all , and where and are as given in Theorem 3.1 and

Remark 3.4.

Notice that the ratio plays the role of in Theorem 3.1. In addition, setting in the current context corresponds to the so-called delta-neutral strategies. This is a class of investment strategies that satisfy . In other terms, this amounts to invest the same capital in each of the co-integrated stocks. In this setting the optimal delta-neutral strategy is given by

4. Optimal Convergence Trade under Partial Information

The goal of this section is to study the utility maximization problem related to convergence trade from the point of view of a partially informed investor. Therefore we now assume that the investor cannot directly observe the state of the Markov chain , and that her information comes from the observation of price processes and . Mathematically, the available information flow is given by filtration , where . Since the investor chooses how to allocate her wealth according to the available information, we will now consider the following set admissible strategy.

Definition 4.1.

An -admissible portfolio strategy is a self-financing and -predictable strategy that satisfies integrability condition (3.1), and is the set of all -admissible strategies.

In order to solve the optimization problem under partial information we first infer information about the state of the Markov chain from the observation process , using filtering techniques. The idea is to determine the conditional distribution of the unobservable state process , given the observed history. To this, for every functions we define the filter as the optional projection of the process on the available filtration, i.e.

Due to the nature of process , we get that

Therefore, solving the filtering problem amounts to compute conditional state probabilities,

for every . In the sequel we will use the notation to indicate the -dimensional process and where and for every . We will use the innovations approach to characterize processes for . Consider the following processes

and observe that the triplets and generate the same information flow. Then we define -Brownian motions and by

where and . Note that and are correlated Brownian motions with correlation coefficient and that there exists a -Brownian motion independent of such that . We now introduce the innovation process in the following way. Define

and denote by where, for and vector ; then we get that

for every . We will use also the matrix/vector form

where , ,

Remark 4.2.

The innovation process has two important features. First, is an -Brownian motion; see, for instance, Bain and Crisan [4, Proposition 2.30]. Second, by the independence between the Markov chain and the vector driving the observation we get that the filtration generated by and that generated by are the same; see Allinger and Mitter [1, Theorem 1]. Then we can apply Jacod and Shiryaev [16, Theorem III.4.34-(a)] and get that every -local martingale admits the following representation

| (4.1) |

for some -predictable 2-dimensional process such that

The filtering equation is computed in the next proposition. The proof of this result is given in Appendix.

Proposition 4.3.

For every , conditional state probabilities of the process satisfy the following system of SDEs

| (4.2) |

with , where for , is the 2-dimensional process with components

for every with and .

Having the dynamics of the filtered probabilities enables us to derive a semimartingale decomposition for the co-integrated asset price processes with respect to the information filtration. Precisely, we have that

| (4.3) | ||||

| (4.4) |

with and , and the market index price process which is not affected by the Markov chain, preserves its dynamics. This leads to the following for the spread and the wealth processes

| (4.5) |

| (4.6) |

respectively. Moreover, thanks to uniqueness of the solution of the filtering equation we can consider the -dimensional process as the state process and introduce the equivalent optimal control problem under full information, called the separated problem; see, e.g., Fleming and Pardoux [13]. The optimization problem we address now is

| (4.7) |

where denotes the conditional expectation given , and , where , with denoting the -dimensional simplex. Next, we resort to the HJB approach to solve problem (4.7). We define the value function by

| (4.8) |

In order to get explicit form for the value function up to the solution of a system of PDEs we restrict to the case where and . In this case coefficients and , for in equation (4.2) do not depend on and are given by

for every .

Theorem 4.1.

Suppose that and with and assume that the investor has logarithmic utility preferences. Then the optimal portfolio strategy is

| (4.9) | |||||

| (4.10) | |||||

| (4.11) |

The value function is of the form

| (4.12) |

where function solves the ordinary differential equation

| (4.13) |

with terminal condition and functions and solve the following system of partial differential equations

| (4.14) |

The proof of Theorem 4.1 is given in Appendix. We observe here that the function driving the quadratic term is independent of . Mathematically this is due to the fact that and are assumed to be constant and therefore the trader does not account for the effect of partial information on the quadratic level of the current spread. Optimal portfolio strategy under partial information shares similar properties of the full information one (see Remark 3.2), except that unobserved parameters are replaced by the filtered estimates. That is, the certainty equivalence principle holds for the optimization problem under partial information; see Kuwana [18] and Bäuerle and Rieder [6].

4.1. Optimal Beta-Neutral Investment under Partial Information

For comparison purposes we also investigate the structure of strategies leading to zero (CAPM) beta in the partial information setting. This means to consider investment strategies of the form outlined below.

Definition 4.4.

An -admissible beta-neutral investment strategy is an -predictable self-financing investment strategy such that

| (4.16) |

with . We denote by the set of all -admissible beta-neutral strategies.

The optimal beta-neutral investment strategy under restricted information and the corresponding value function are given in Theorem 4.2 below. The proof is similar to that of Theorem 4.1 and it is therefore omitted.

Theorem 4.2.

Assume that and with and consider a trader with a logarithmic utility function. Then, the optimal beta-neutral strategy under partial information is

The value function is of the form

where function solves the ordinary differential equation

with the terminal condition and functions and solve the following system of partial differential equations

with terminal conditions and and where and are the same of Theorem 3.1 and

Finally we again observe that for we recover delta-neutral strategies in partial information which are given by

5. Numerical Study with a 2-State Markov Chain

In this section, we consider a 2-state Markov chain , that is, . Here we resort to a numerical approach in order to get qualitative characteristics of optimal strategies and the value function both under full and partial information. In the sequel, we fix the values for the following parameters as , , , , , and .

5.1. Optimization problem under full information

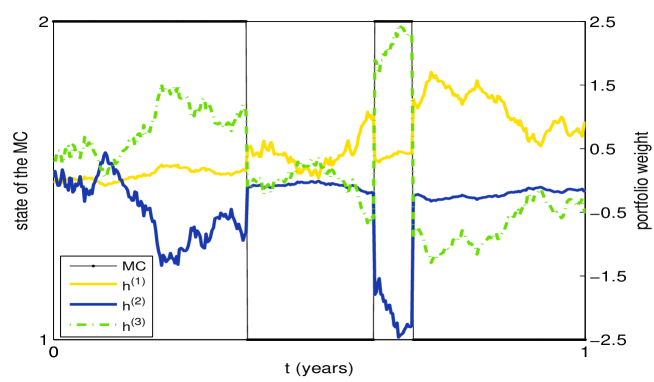

We first consider the full information setting where the trader is assumed to observe the state of the Markov chain. We begin with a simulation of a data set where we generate a Markov chain and the price processes, respectively. In Figure 1 we investigate the behavior of the optimal investment strategy for the simulated data. Clearly, we see that strategies depend on different regimes and present jumps at the jump times of the Markov chain. We also observe that the resulting optimal portfolio weights for the first and second assets change sign through time. In particular, we have long-long, long-short and short-short type optimal portfolios, which may indicate the flexibility of our modeling framework.

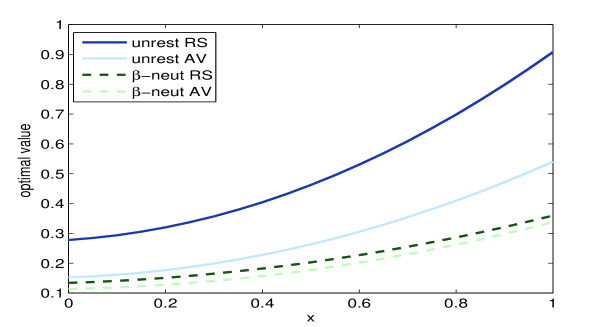

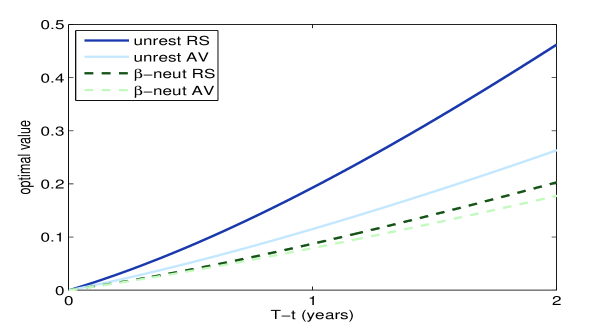

Next we investigate the properties of the value function. To this, we solve the system of ODEs in Theorem 3.1 numerically. Figure 2 summarizes our results. Let denote the stationary distribution of the Markov chain . We consider two traders, one of which ignores the Markov modulated nature of the underlying parameters and use the averaged data . The second trader, on the other hand, behaves optimally under our Markov modulated model. We set and , and compute . Then, we get and . In Figure 2 we plot , the value function obtained in the model assuming averaged data, and . We observe that , that is, averaged data does not suffice to obtain the optimal value for the convergence trade problem and hence on the average, the second trader performs better than the first one. We repeat this analysis for the case of beta-neutral trading and obtain same qualitative results.

In Figure 2 we also illustrate the dominance of the unrestricted strategies over the beta-neutral ones. This is quite natural since by restricting the set of admissible strategies, the trader could not realize all the benefits resulting from the co-integration between and . The gap between values depends on the choice of parameters and in particular it increases in initial spread () and time to maturity ().

5.2. Optimization problem under partial information

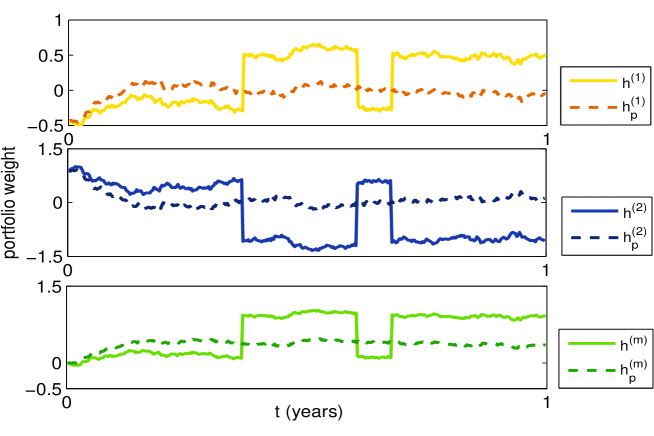

We now consider the partial information case. Since conditional state probabilities and satisfy for every , we can reduce the number of state variables for the optimization problem. In the following we denote by and . In Figure 3 we plot the optimal strategies followed by a fully informed investor who observes the state of the underlying Markov chain and the partially informed one who can only estimate the state of through observation of prices, for the simulated data. We observe that while the informed investor suddenly changes his behavior according to the change in the state of the Markov chain, portfolio weights for the partially informed investor are subject to the smoothing effect of filtering. The difference between portfolio allocation under full and partial information crucially depends on the amplitude of the noise.

Now we measure the advantage of the fully informed investor over the partially informed one. In order to do that, we consider the process defined by

where represents the value function corresponding to the full information setting and that corresponding to the partial information one. The process represents the loss of utility due to partial information (see, e.g., Lee and Papanicolaou [19] for the definition). By the form of value functions and Markov property of the pair we get that there exists a function such that , for every . In Figure 4 we plot the loss of utility in the 2-state Markov chain case. We observe that it is always grater than or equal to zero, meaning that information premium exists and it is always nonnegative. Moreover it is larger when conditional state probabilities are close to . This reflects the fact that more uncertainty about the state of the Markov chain leads to higher losses in utility.

6. Conclusion

In this paper, we have considered an extension to a regime-switching framework of the model proposed by Liu and Timmermann [22]. We have studied the optimization problem for a trader with logarithmic utility preferences under different levels of information. We have assumed that the mean-reverting component of pricing errors depends on a hidden Markov switching factor which may or may not be directly observed by the investor.

In the full information setting, that is when the state of the Markov chain is observable, we have computed the optimal strategy and characterized the value function as the unique (classical) solution of the HJB equation. In this framework, we can reduce the HJB to a system of ODEs. We have also discussed the structure of beta-neutral strategies, achieved by taking long and short positions in such a way that the impact of the overall market is minimized. In the partial information case, we have transformed the original problem into the so-called reduced (or separated) problem via filtering by replacing unobservable states of the Markov chain with their optional projections over the available filtration. Then we have addressed the resulting control problem by dynamic programming, and we have represented the value function in terms of the solution of a system of PDEs. Beta-neutral strategies are also obtained in the partial information framework. Finally, we have studied a numerical example with a two-state Markov chain. We have concluded that averaged data is not sufficient to obtain the optimal value in the full information case, and that there is always positive premium due to information superiority when we compare the optimal value under full and partial information.

Appendix: Proofs

Proof of Theorem 3.1.

Existence: We denote by the generator of the process , that is

for every function , i.e. bounded, differentiable with respect to and twice differentiable with respect to and , for every .

Suppose that the value function for every . Then it solves the HJB equation given by

| (A.1) |

for every , subject to the terminal condition , for all and . It follows from the form of the utility function that for all the value function can be rewritten as , for some function such that . Inserting the ansatz for the value function in equation (A.1) and taking first order conditions leads to

Second order conditions imply that portfolio weights given in (3.4)-(3.6) are candidates to be optimal strategies. Next, we insert the optimal portfolio weights in the HJB equation. This yields the following PDE:

| (A.2) |

We conjecture that . Substituting this ansatz in (A.2) results in a quadratic equation for . Setting the coefficients of the terms , and the independent term to zero yields that the functions , and solve the system of ODEs given in (3.8)-(3.10); see, e.g., Teschl [25, Theorem 3.9]).

Verification: In the sequel we verify martingale conditions that ensure that in (3.7) is indeed the value function. To this, let be a solution of the HJB equation (A.1) and and admissible control. By Itô’s formula we get

The last term in the expression above corresponds to the compensated integral with respect to the jump measure of , that is

where for every ,

is the jump measure of Markov chain with the compensator

and is the sequence of jump times of . Since satisfies equation (A.1) we get

The form of and integrability condition (3.1) ensure that integrals with respects to Brownian motions and the compensated jump measure are true -martingales. Then, taking expectations we get that

and the equality holds if is a maximizer of equation (A.1). ∎

Proof of Proposition 4.3.

In the following we use the notation , . Consider the semimartingale decomposition of given by

where is a -martingale. Now, projecting over leads to

where is an -martingale. Using the martingale representation in (4.1) we get

Let , for every . Computing the product and projecting on , we obtain

| (A.3) |

for every and for some -martingale . We now compute the product as

| (A.4) |

for every , where is an -martingale. Comparing the finite variation terms in (A.3) and (A.4), we get

for every . By taking , we obtain the result. Finally, since the drift and diffusion coefficients in (4.2) are continuous, bounded and locally Lipschitz, we get that is the unique strong solution of the system (4.2) . ∎

Proof of Theorem 4.1.

Existence: For notational ease we set and . Assume first that function is regular. Then it satisfies the following HJB equation

| (A.5) |

subject to the terminal condition , for all , and for every , where is given by

| (A.6) |

for every function , which is bounded, differentiable with respect to time and twice differentiable with respect to with bounded derivatives. By the form of the utility function we have that the value function has the form , for some function , such that for all . By inserting the first ansatz in equation (A.5) and considering the first order condition we get that the candidate for an optimal strategy is given by (4.9), (4.10),(4.11). Since is concave and increasing in , the second order condition implies that (4.9),(4.10) and (4.11) is the maximizer and the optimal portfolio strategy. Here, we choose of the form . Inserting this ansatz in equation (A.5) leads to the system of linear partial differential equations in (4.13), (4.14), (4.15).

Verification: To conclude that is the value function, we show a verification result. Let be a solution of (A.5) with the boundary condition . Let be an -admissible control, let the solution to equation (4.6). By applying Itô’s formula we get

By equation (A.5) we get

| (A.7) |

Note that stochastic integrals with respect to and are true martingales. This is a consequence of the fact that function solves the HJB equation, that is an -admissible strategy and that functions and their derivatives are bounded over the compact interval . Then taking the expectation on both sides of inequality (A.7) implies that . Moreover if is a maximizer of equation (A.5), then we obtain the equality . ∎

References

- Allinger and Mitter [1981] D. F. Allinger and S. K. Mitter. New results on the innovations problem for non-linear filtering. Stochastics: An International Journal of Probability and Stochastic Processes, 4(4):339–348, 1981.

- Altay et al. [2018] S. Altay, K. Colaneri, and Z. Eksi. Pairs trading under drift uncertainty and risk penalization. International Journal of Theoretical and Applied Finance, 21(07):1850046, 2018.

- Angoshtari [2016] B. Angoshtari. On the market-neutrality of optimal pairs-trading strategies. Available at SSRN: https://ssrn.com/abstract=2831836, 2016.

- Bain and Crisan [2009] A. Bain and D. Crisan. Fundamentals of Stochastic Filtering, volume 3. Springer, 2009.

- Baran et al. [2013] N. A. Baran, G. Yin, and C. Zhu. Feynman-kac formula for switching diffusions: connections of systems of partial differential equations and stochastic differential equations. Advances in Difference Equations, 2013(1):315, 2013.

- Bäuerle and Rieder [2004] N. Bäuerle and U. Rieder. Portfolio optimization with Markov-modulated stock prices and interest rates. Automatic Control, IEEE Transactions on, 49(3):442–447, 2004.

- Bäuerle and Rieder [2005] N. Bäuerle and U. Rieder. Portfolio optimization with unobservable Markov-modulated drift process. Journal of Applied Probability, 42(2):362–378, 2005.

- Björk et al. [2010] T. Björk, M. H. A. Davis, and C. Landén. Optimal investment under partial information. Mathematical Methods of Operations Research, 71(2):371–399, 2010.

- Cartea and Jaimungal [2016] Á. Cartea and S. Jaimungal. Algorithmic trading of co-integrated assets. International Journal of Theoretical and Applied Finance, 19(06):1650038, 2016.

- Chiu and Wong [2011] M. C. Chiu and H. Y. Wong. Mean–variance portfolio selection of cointegrated assets. Journal of Economic Dynamics and Control, 35(8):1369–1385, 2011.

- De Jong et al. [2009] A. De Jong, L. Rosenthal, and M. A. Van Dijk. The risk and return of arbitrage in dual-listed companies. Review of Finance, 13(3):495–520, 2009.

- Escobar et al. [2015] M. Escobar, D. Neykova, and R. Zagst. Portfolio optimization in affine models with markov switching. International Journal of Theoretical and Applied Finance, 18(05):1550030, 2015.

- Fleming and Pardoux [1982] W. Fleming and E. Pardoux. Optimal control for partially observed diffusions. SIAM Journal on Control and Optimization, 20(2):261–285, 1982.

- Frazzini and Pedersen [2014] A. Frazzini and L. H. Pedersen. Betting against beta. Journal of Financial Economics, 111(1):1–25, 2014.

- Frey et al. [2012] R. Frey, A. Gabih, and R. Wunderlich. Portfolio optimization under partial information with expert opinions. International Journal of Theoretical and Applied Finance, 15(01), 2012.

- Jacod and Shiryaev [1987] J. Jacod and A.N. Shiryaev. Limit Theorems for Stochastic Processes, volume 2003. Springer, 1987.

- Jurek and Yang [2007] J. W. Jurek and H. Yang. Dynamic portfolio selection in arbitrage. EFA 2006 Meetings Paper. Available at SSRN: https://ssrn.com/abstract=882536, 2007.

- Kuwana [1995] Y. Kuwana. Certainty equivalence and logarithmic utilities in consumption/investment problems. Mathematical Finance, 5(4):297–309, 1995.

- Lee and Papanicolaou [2016] S. Lee and A. Papanicolaou. Pairs trading of two assets with uncertainty in co-integration’s level of mean reversion. International Journal of Theoretical and Applied Finance, 19(08):1650054, 2016.

- Lei and Xu [2015] Y. Lei and J. Xu. Costly arbitrage through pairs trading. Journal of Economic Dynamics and Control, 56:1–19, 2015.

- Liu and Longstaff [2003] J. Liu and F. A. Longstaff. Losing money on arbitrage: Optimal dynamic portfolio choice in markets with arbitrage opportunities. The Review of Financial Studies, 17(3):611–641, 2003.

- Liu and Timmermann [2013] J. Liu and A. Timmermann. Optimal convergence trade strategies. The Review of Financial Studies, 26(4):1048–1086, 2013.

- Mudchanatongsuk et al. [2008] S. Mudchanatongsuk, J. A. Primbs, and W. Wong. Optimal pairs trading: A stochastic control approach. In 2008 American Control Conference, pages 1035–1039. IEEE, 2008.

- Sotomayor and Cadenillas [2009] L. R. Sotomayor and A. Cadenillas. Explicit solutions of consumption-investment problems in financial markets with regime switching. Mathematical Finance, 19(2):251–279, 2009.

- Teschl [2012] G. Teschl. Ordinary Differential Equations and Dynamical Systems, volume 140. American Mathematical Society, 2012.

- Tourin and Yan [2013] A. Tourin and R. Yan. Dynamic pairs trading using the stochastic control approach. Journal of Economic Dynamics and Control, 37(10):1972–1981, 2013.

- Vijh [1994] A. M. Vijh. S&p 500 trading strategies and stock betas. The Review of Financial Studies, 7(1):215–251, 1994.

- Zhou and Yin [2003] X. Y. Zhou and G. Yin. Markowitz’s mean-variance portfolio selection with regime switching: A continuous-time model. SIAM Journal on Control and Optimization, 42(4):1466–1482, 2003.