Active preference learning based on radial basis functions

Email: alberto.bemporad@imtlucca.it

⋆Dalle Molle Institute for Artificial Intelligence - USI/SUPSI, Manno, Switzerland

Email: dario.piga@supsi.ch

)

Abstract

This paper proposes a method for solving optimization problems in which the decision-maker cannot evaluate the objective function, but rather can only express a preference such as “this is better than that” between two candidate decision vectors. The algorithm described in this paper aims at reaching the global optimizer by iteratively proposing the decision maker a new comparison to make, based on actively learning a surrogate of the latent (unknown and perhaps unquantifiable) objective function from past sampled decision vectors and pairwise preferences. The surrogate is fit by means of radial basis functions, under the constraint of satisfying, if possible, the preferences expressed by the decision maker on existing samples. The surrogate is used to propose a new sample of the decision vector for comparison with the current best candidate based on two possible criteria: minimize a combination of the surrogate and an inverse weighting distance function to balance between exploitation of the surrogate and exploration of the decision space, or maximize a function related to the probability that the new candidate will be preferred. Compared to active preference learning based on Bayesian optimization, we show that our approach is superior in that, within the same number of comparisons, it approaches the global optimum more closely and is computationally lighter. MATLAB and a Python implementations of the algorithms described in the paper are available at http://cse.lab.imtlucca.it/~bemporad/idwgopt.

Keywords: Active preference learning, preference-based optimization, global optimization, derivative-free algorithms, black-box optimization, surrogate models, multi-objective optimization, inverse distance weighting, Bayesian optimization.

1 Introduction

Taking an optimal decision is the process of selecting the value of certain variables that produces “best” results. When using mathematical programming to solve this problem, “best” means that the taken decision minimizes a certain cost function, or equivalently maximizes a certain utility function. However, in many problems an objective function is not quantifiable, either because it is of qualitative nature or because it involves several goals. Moreover, sometimes the “goodness” of a certain combination of decision variables can only be assessed by a human decision maker.

This situation arises in many practical cases. When calibrating the parameters of a deep neural network whose goal is to generate a synthetic painting or artificial music, artistic “beauty” is hardly captured by a numerical function, and a human decision-maker is required to assess whether a certain combination of parameters produces “beautiful” results. For example, the authors of [4] propose a tool to help digital artists to calibrate the parameters of an image generator so that the synthetic image “resembles” a given one. Another example is in industrial automation when a calibrating the tuning knobs of a control system: based on engineering insight and rules of thumb, the task is usually carried out manually by trying a series of combinations until the calibrator is satisfied by the observed closed-loop performance. Another frequent situation in which it is hard to formulate an objective function is in multi-objective optimization [7]. Here, selecting a-priori the correct weighted sum of the objectives to minimize in order to choose an optimal decision vector can be very difficult, and is often a human operator that needs to assess whether a certain Pareto optimal solution is better than another one, based on his or her (sometimes unquantifiable) feelings.

It is well known in neuroscience that humans are better at choosing between two options (“this is better than that”) than among multiple ones [5, 6]. In consumer psychology, the “choice overload” effect shows that a human, when presented an abundance of options, has more difficulty to make a decision than if only a few options are given. On the other hand, having a large number of possibilities to choose from creates very positive feelings in the decision maker [6]. In economics, the difficulty of rational behavior in choosing the best option was also recognized in [29], due to the complexity of the decision problem exceeding the cognitive resources of the decision maker. Indeed, choosing the best option implies ranking choices by absolute values and therefore quantifying a clear objective function to optimize, a process that might be difficult due to the complexity and fuzziness of many criteria that are involved. For the above reasons, the importance of focusing on discrete choices in psychology dates back at least to the 1920’s [31].

Looking for an optimal value of the decision variables that is “best”, in that the human operator always prefers it compared to all other tested combinations, may involve a lot of trial and error. For example, in parameter calibration the operator has to try many combinations before being satisfied with the winner one. The goal of active preference learning is to drive the trials by automatically proposing decision vectors to the operator for testing, so to converge to the best choice possibly within the least number of experiments.

In the derivative-free black-box global optimization literature there exist some methods for minimizing an objective function that can be used also for preference-based learning. Since, given two decision vectors , , we can say that is not “preferred” to if , finding a global optimizer can be reinterpreted as the problem of looking for the vector such that it is preferred to any other vector . Therefore, optimization methods that only observe the outcome of the comparison (and not the values , not even the difference ) can be used for preference-based optimization. For example particle swarm optimization (PSO) algorithms [18, 32] drive the evolution of particles only based on the outcome of comparisons between function values and could be used in principle for preference-based optimization. However, although very effective in solving many complex global optimization problems, PSO is not conceived for keeping the number of evaluated preferences small, as it relies on randomness (of changing magnitude) in moving the particles, and would be therefore especially inadequate in solving problems where a human decision maker is involved in the loop to express preferences.

Different methods were proposed in the global optimization literature for finding a global minimum of functions that are expensive to evaluate [25]. Some of the most successful ones rely on computing a simpler-to-evaluate surrogate of the objective function and use it to drive the search of new candidate optimizers to sample [15]. The surrogate is refined iteratively as new values of the actual objective function are collected at those points. Rather than minimizing the surrogate, which may easily lead to miss the global optimum of the actual objective function, an acquisition function is minimized instead to generate new candidates. The latter function consists of a combination of the surrogate and of an extra term that promotes exploring areas of the decision space that have not been yet sampled.

Bayesian Optimization (BO) is a very popular method exploiting surrogates to globally optimize functions that are expensive to evaluate. In BO, the surrogate of the underlying objective function is modeled as a Gaussian process (GP), so that model uncertainty can be characterized using probability theory and used to drive the search [21]. BO is used in several methods such as Kriging [22], in Design and Analysis of Computer Experiments (DACE) [26], in the Efficient Global Optimization (EGO) algorithm [17], and is nowadays heavily used in machine learning for hyper-parameter tuning [3].

Bayesian optimization has been proposed also for minimizing (unknown) black-box functions based only on preferences [4, 10, 1]. The surrogate function describing the observed set of preferences is described in terms of a GP, using a probit model to describe the observed pairwise preferences [8] and the Laplace approximation of the posterior distribution of the latent function to minimize. The GP provides a probabilistic prediction of the preference that is used to define an acquisition function (like expected improvement) which is maximized in order to select the next query point. The acquisition function used in Bayesian preference automatically balances exploration (selecting queries with high uncertainty on the preference) and exploitation (selecting queries which are expected to lead to improvements in the objective function).

In this paper we propose a new approach to active preference learning optimization that models the surrogate by using general radial basis functions (RBFs) rather than a GP, and inverse distance weighting (IDW) functions for exploration of the space of decision variables. A related approach was recently proposed by one of the authors in [2] for global optimization of known, but difficult to evaluate, functions. Here, we use instead RBFs to construct a surrogate function that only needs to satisfy, if possible, the preferences already expressed by the decision maker at sampled points. The training dataset of the surrogate function is actively augmented in an incremental way by the proposed algorithm according to two alternative criteria. The first criterion, similarly to [2], is based on a trade off between minimizing the surrogate and maximizing the distance from existing samples using IDW functions. At each iteration, the RBF weights are computed by solving a linear or quadratic programming problem aiming at satisfying the available training set of pairwise preferences. The second alternative criterion is based on quantifying the probability of getting an improvement based on a maximum-likelihood interpretation of the RBF weight selection problem, which allows quantifying the probability of getting an improvement based on the surrogate function. Based on one of the above criteria, the proposed algorithm constructs an acquisition function that is very cheap to evaluate and is minimized to generate a new sample and to query a new preference.

Compared to preferential Bayesian optimization, the proposed approach is computationally lighter, due to the fact that computing the surrogate simply requires solving a convex quadratic or linear programming problem. Instead, in PBO, one has to first compute the Laplace approximation of the posterior distribution of the preference function, which requires to calculate (via a Newton-Raphson numerical optimization algorithm) the mode of the posterior distribution. Then, a system of linear equations, with size equal to the number of observations, has to be solved. Moreover, the IDW term used by our approach to promote exploration does not depend on the surrogate, which guarantees that the space of optimization variables is well explored even if the surrogate poorly approximates the underlying preference function. Finally, the performance of our method in approaching the optimizer within the allocated number of preference queries is similar and sometimes better than preferential Bayesian optimization, as we will show in a set of benchmarks used in global optimization and in solving a multi-objective optimization problem.

The paper is organized as follows. In Section 2 we formulate the preference-based optimization problem we want to solve. Section 3 proposes the way to construct the surrogate function using linear or quadratic programming and Section 4 the acquisition functions that are used for generating new samples. The active preference learning algorithm is stated in Section 5 and its possible application to solve multi-objective optimization problems in Section 6. Section 7 presents numerical results obtained in applying the preference learning algorithm for solving a set of benchmark global optimization problems, a multi-objective optimization problem, and for optimal tuning of a cost-sensitive neural network classifier for object recognition from images. Finally, some conclusions are drawn in Section 8.

A MATLAB and a Python implementation of the proposed approach is available for download at http://cse.lab.imtlucca.it/~bemporad/idwgopt.

2 Problem statement

Let be the space of decision variables. Given two possible decision vectors , consider the preference function defined as

| (1) |

where for all it holds , , and the transitive property

| (2) |

The objective of this paper is to solve the following constrained global optimization problem:

| (3) |

that is to find the vector of decision variables that is “better” (or “no worse”) than any other vector according to the preference function .

Vectors in (3) define lower and upper bounds on the decision vector, and imposes further constraints on , such as

| (4) |

where , and when (no inequality constraint is enforced). We assume that the condition is easy to evaluate, for example in case of linear inequality constraints we have , , , . When formulating (3) we have excluded equality constraints , as they can be eliminated by reducing the number of optimization variables.

The problem of minimizing an objective function under constraints,

| (5) |

can be written as in (3) by defining

| (6) |

In this paper we assume that we do not have a way to evaluate the objective function . The only assumption we make is that for each given pair of decision vectors , , only the value is observed. The rationale of our problem formulation is that often one encounters practical decision problems in which a function is impossible to quantify, but anyway it is possible to express a preference, for example by a human operator, for any given presented pair . The goal of the active preference learning algorithm proposed in this paper is to suggest iteratively a sequence of samples to test and compare such that approaches as grows.

In what follows we implicitly assume that a function actually exists but is completely unknown, and attempt to synthesize a surrogate function of such that its associated preference function defined as in (6) coincides with on the finite set of sampled pairs of decision vectors.

3 Surrogate function

Assume that we have generated samples of the decision vector, with such that , , , and have evaluated a preference vector

| (7) |

where is the number of expressed preferences, , , , .

In order to find a surrogate function such that

| (8) |

where is defined from as in (6), we consider a surrogate function defined as the following radial basis function (RBF) interpolant [11, 23]

| (9) |

In (9) function is the Euclidean distance

| (10) |

is a scalar parameter, is a RBF, and are coefficients that we determine as explained below. Examples of RBFs are (inverse quadratic), (Gaussian), (thin plate spline), see more examples in [11, 2].

In accordance with (8), we impose the following preference conditions

| (11) |

where is a given tolerance and are slack variables, , .

Accordingly, the coefficient vector is obtained by solving the following convex optimization problem

| (12) |

where are positive weights, for example , . The scalar is a regularization parameter. When problem (12) is a quadratic programming (QP) problem that, since for all , admits a unique solution. If problem (12) becomes a linear program (LP), whose solution may not be unique.

Note that the use of slack variables in (12) allows one to relax the constraints imposed by the specified preference vector . Constraint infeasibility might be due to an inappropriate selection of the RBF and/or to outliers in the acquired components of vector . The latter condition may easily happen when preferences are expressed by a human decision maker in an inconsistent way.

For a given set of samples, setting up (12) requires computing the symmetric matrix whose -entry is

| (13) |

with for the inverse quadratic and Gaussian RBF, while for the thin plate spline RBF . Note that if a new sample is collected, updating matrix only requires computing for all .

An example of surrogate function constructed based on preferences generated as in (6) by the following scalar function [2]

| (14) |

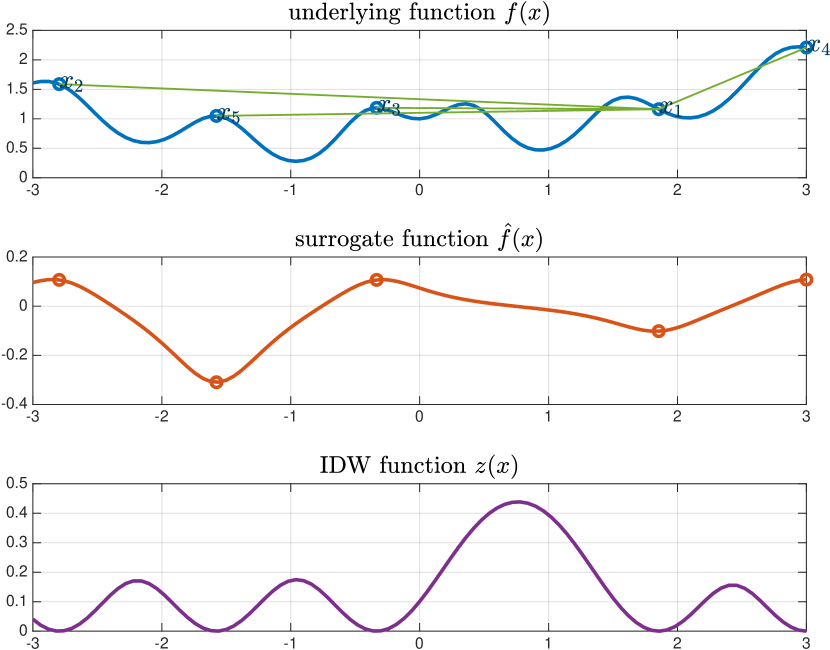

is depicted in Figure 1. The surrogate is generated from samples by solving the LP (12) () with matrix generated by the inverse quadratic RBF with and .

3.1 Self-calibration of RBF

Computing the surrogate requires to choose the hyper-parameter defining the shape of the RBF (Eq. (9)). This parameter can be tuned through -fold cross-validation [30], by splitting the available pairwise comparisons into (nearly equally sized) disjoint subsets. To this end, let us define the index sets , , such that , , for all , . For a given and for all , the preferences indexed by the set are used to fit the surrogate function by solving (12), while the performance of in predicting comparisons indexed by is quantified in terms of number of correctly classified preferences , where if or otherwise, and is the preference function induced by as in (6). Since the hyper-parameter is scalar, a fine grid search can be used to find the value of maximizing .

Since in active preference learning the number of observed pairwise preferences is usually small, we use , , namely -fold cross validation or leave-one-out, to better exploit the available comparisons.

Let be the best vector of decision variables in the finite set , that is

| (15) |

Since in active preference learning one is mostly interested in correctly predicting the preference w.r.t. the best optimal point , the solution of problem (12) and the corresponding score are not computed for all indexes such that , that is the preferences involving are only used for training and not for testing.

The -fold cross-validation procedure for self-calibration requires to formulate and solve problem (12) times ( times in case of leave-one-out cross validation, or less when comparisons involving are only used for training). In order to reduce computations, self-calibration can be executed only at a subset of iterations.

4 Acquisition function

Let be the best vector of decision variables defined in (15). Consider the following procedure: () generate a new sample by pure minimization of the surrogate function defined in (9),

with obtained by solving the LP (12), () evaluate , () update , and () iterate over . Such a procedure may easily miss the global minimum of (3), a phenomenon that is well known in global optimization based on surrogate functions: purely minimizing the surrogate function may lead to converge to a point that is not the global minimum of the original function [15, 2]. Therefore, the exploitation of the surrogate function is not enough to look for a new sample , but also an exploration objective must be taken into account to probe other areas of the feasible space.

In the next paragraphs we propose two different acquisition functions that can be used to define the new sample to compare the current best sample to.

4.1 Acquisition based on inverse distance weighting

Following the approach suggested in [2], we construct an exploration function using ideas from inverse distance weighting (IDW). Consider the IDW exploration function defined by

| (16) |

where is defined by [28]

| (17) |

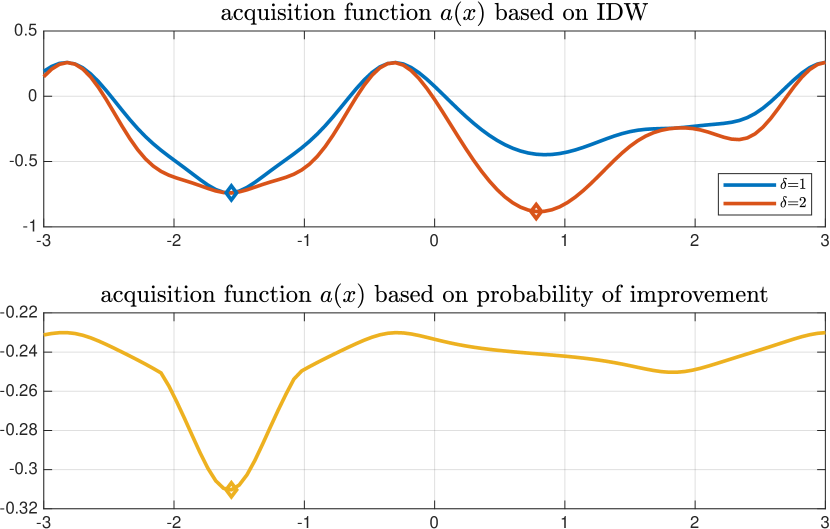

Clearly for all , and in . The arc tangent function in (16) avoids that gets excessively large far away from all sampled points. Figure 1 shows the IDW exploration function obtained from (16) for the example generated from (14).

Given an exploration parameter , the acquisition function is defined as

| (18) |

where

is the range of the surrogate function on the samples in . By setting

| (19a) | |||

| we get , , and therefore | |||

| (19b) | |||

Clearly if at least one comparison . The scaling factor is used to simplify the choice of the exploration parameter .

The following lemma immediately derives from [2, Lemma 2]:

Lemma 1

Function is differentiable everywhere on .

As we will detail below, given a set of samples and a vector of preferences defined by (7), the next sample is defined by solving the global optimization problem

| (20) |

Problem (20) can be solved very efficiently using various global optimization techniques, either derivative-free [25] or, if and is also differentiable, derivative-based. In case some components of vector are restricted to be integer, (20) can be solved by mixed-integer programming.

4.2 Acquisition based on maximum likelihood of improvement

We show how the surrogate function derived by solving problem (12) can be seen as a maximum likelihood estimate of an appropriate probabilistic model. The analyses described in the following are inspired by the probabilistic interpretation of support vector machines described in [9].

Let and let be the -dimensional vector obtained by collecting the terms , with , .

Let us rewrite the QP problem (12) without the slack variables as

| (21) |

where

| (22a) | ||||

| (22b) | ||||

| (22c) | ||||

are piecewise linear convex functions of , for all .

Theorem 1

For a given hyper-parameter , let be the minimizer of problem (21) and let . Then vector is the minimizer of the following problem

| (23) |

Proof See Appendix.

In order to avoid heavy notation, we restrict the coefficients in (12) such that they are equal when the preference is the same, that is where are given positive weights.

Let us now focus on problem (23) and consider the joint p.d.f.

| (24) |

defined for and , and parametrized by , a strictly positive scalar , and a generic unit vector .

The distribution (24) is composed by three terms. The first term is a normalization constant. We will show next that does not depend on when we restrict . The second term depends on all the parameters and it is related to the objective function minimized in (23). The last term ensures integrability of and that the normalization constant does not depend on , as discussed next. A possible choice for is .

The normalization constant is given by

| (25) |

where for the term is the integral defined as

| (26) |

The following Theorem shows that does not depend on , and so is also independent of .

Theorem 2

Let in (24) be . For any ,

| (27) |

Proof See Appendix.

Because of Theorem 2, since now on, when

we restrict , we will drop the dependence on of and simply write .

Let us assume that the samples of the training sequence are i.i.d. and generated from the joint distribution defined in (24). The negative log of the probability of the dataset given is

| (28) |

Thus, for fixed values of and , by Theorem 1 the minimizer of

is . In other words, for any fixed , the solution of the QP problem (12) can be reinterpreted as times the maximizer of the joint likelihood with respect to , , when .

It is interesting to note that the marginal p.d.f. derived from the probabilistic model (24) is equal to

| (29) |

and therefore the corresponding preference posterior probability is

| (30) |

where .

The preference posterior probability given (30) can be used now to explore the vector space , as we describe next.

Let be the vector obtained by solving (12) with samples and preferences. Let us treat again as a free sample to optimize and consider (30) also for the new generic th comparison

A criterion to choose is to maximize the preference posterior probability of obtaining a “better” sample compared to the current “best” sample given by (30), or equivalently of getting . This can be achieved by the following acquisition function

| (31) |

4.3 Scaling

Different components of may have different upper and lower bounds , . Rather than using weighted distances as in stochastic process model approaches such as Kriging methods [26, 17], we simply rescale the variables in optimization problem (3) to range in . As described in [2], we first tighten the given range by computing the bounding box of the set and replacing with . The bounding box is obtained by solving the following optimization problems

| (32) |

where is the th column of the identity matrix, . Note that Problem (32) is a linear programming (LP) problem in case of linear inequality constraints . Then, we operate with new scaled variables , , and replace the original preference learning problem (3) with

| (33) |

where the scaling mapping is defined as

| (34) |

where clearly , , and is the set

| (35) |

When is the polyhedron , (35) corresponds to defining the new polyhedron

| (36) |

where

| (37) |

and is the diagonal matrix whose diagonal elements are the components of .

Note that in case the preference function is related to an underlying function as in (6), applying scaling is equivalent to formulate the following scaled preference function

| (38) |

5 Preference learning algorithm

Algorithm 1 summarizes the proposed approach to solve the optimization problem (3) by preferences using RBF interpolants (9) and the acquisition functions defined in Section 4.

Input: Upper and lower bounds , constraint set ; number of initial samples, number of maximum number of function evaluations; ; ; ; self-calibration index set .

Output: Global optimizer .

In Step 0. Latin Hypercube Sampling (LHS) [24] is used to generate the initial set of samples. The generated samples may not satisfy the constraint . We distinguish between two cases:

-

)

the comparison can be done even if and/or ;

-

)

can only be evaluated if .

In the first case, the initial comparisons are still useful to define the surrogate function. In the second case, a possible approach is to generate a number of samples larger than and discard the samples . An approach for performing this is suggested in [2, Algorithm 2].

Step 0.(0..1)0..1.4 requires solving a global optimization problem. In this paper we use Particle Swarm Optimization (PSO) [18, 32] to solve problem (20). Alternative global optimization methods such as DIRECT [16] or others methods [12, 25] could be used to solve (20). Note that penalty functions can be used to take inequality constraints (4) into account, for example by replacing (20) with

| (39) |

where in (39).

Algorithm 1 consists of two phases: initialization and active learning. During initialization, sample is simply retrieved from the initial set . Instead, in the active learning phase, sample is obtained in Steps 0.(0..1)0..1.1–0.(0..1)0..1.4 by solving the optimization problem (20). Note that the construction of the acquisition function is rather heuristic, therefore finding global solutions of very high accuracy of (20) is not required.

When using the acquisition function (18), the exploration parameter promotes sampling the space in in areas that have not been explored yet. While setting makes Algorithm 1 exploring the entire feasible region regardless of the results of the comparisons, setting can make Algorithm 1 rely only on the surrogate function and miss the global optimizer. Note that using the acquisition function (31) does not require specifying the hyper-parameter . On the other hand, the presence of the IDW function in the acquisition allows promoting an exploration which is independent of the surrogate, and therefore might be a useful tuning knob to have. Clearly, the acquisition function (31) can be also augmented by the term as in (18) to recover such exploration flexibility.

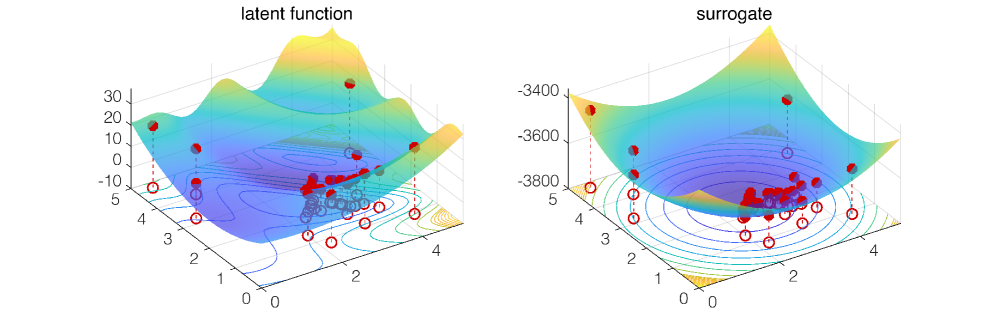

Figure 1 (upper plot) shows the samples generated by Algorithm 1 when applied to minimize the function (14) in , by setting , , , , generated by the inverse quadratic RBF with , and .

5.1 Computational complexity

Algorithm 1 solves quadratic or linear programs (12) with growing size, namely with variables, a number of linear inequality constraints with depending on the outcome of the preferences, and equality constraints. Moreover, it solves global optimization problems (20) in the -dimensional space, whose complexity depends on the used global optimizer. The computation of matrix requires overall RBF values , , . The leave-one-out cross validation executed at Step 0.(0..1)0..1.1 for recalibrating requires to formulate and solve problem (12) at most times. On top of the above analysis, one has to take account the cost of evaluating the preferences , .

6 Application to multi-objective optimization

The active preference learning methods introduced in the previous sections can be effectively used to solve multi-objective optimization problems of the form

| (40d) | |||||

| (40e) | |||||

where is the optimization vector, , , are the objective functions, , and is the function defining the constraints on (including possible box and linear constraints). In general Problem (40) admits infinitely many Pareto optimal solutions, leaving the selection of one of them a matter of preference.

Pareto optimal solutions can be expressed by scalarizing problem (40) into the following standard optimization problem

| (41a) | |||||

| (41b) | |||||

where are nonnegative scalar weights, and . Let us model the preference between Pareto optimal solution through the preference function

| (42) |

where . The optimal selection of a Pareto optimal solution can be therefore expressed as a preference optimization problem of the form (3), with , , .

Without loss of generality, we can set and eliminate , so to solve a preference optimization problem with variables under the constraints , . In Section 7.3 we will illustrate the effectiveness of the active preference learning algorithms introduced earlier in solving the multi-objective optimization problem (40) under the preference function (42).

7 Numerical results

In this section we test the active preference learning approach described in the previous sections on different optimization problems, only based on preference queries.

Computations are performed on an Intel i7-8550 CPU @1.8GHz machine in MATLAB R2019a. Both Algorithm 1 and the Bayesian active preference learning algorithm are run in interpreted code. Problem (20) (or (39), in case of constraints) is solved by the PSO solver [33]. For judging the quality of the solution obtained by active preference learning, the best between the solution obtained by running the optimization algorithm DIRECT [16] through the NLopt interface [14] and by running the PSO solver [33] was used as the reference global optimum. The Latin hypercube sampling function lhsdesign of the Statistics and Machine Learning Toolbox of MATLAB is used to generate initial samples.

7.1 Illustrative example

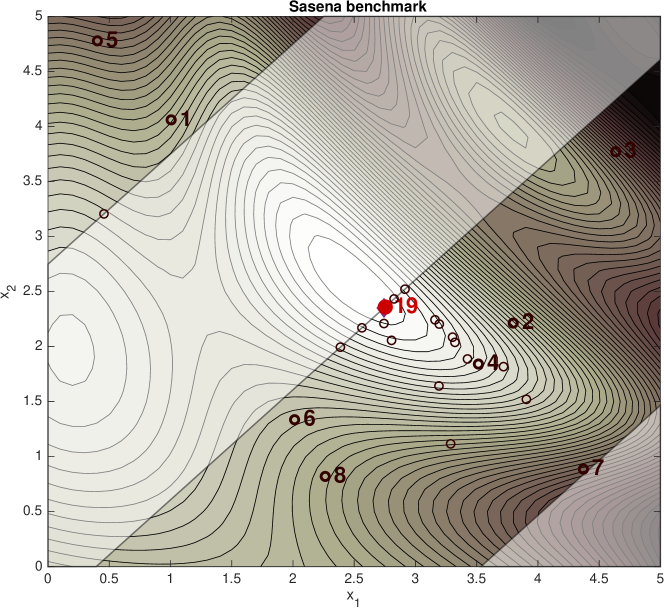

We first illustrate the behavior of Algorithm 1 when solving the following constrained benchmark global optimization problem proposed by Sasena et al. [27]:

| (43) |

The minimizer of problem (43) is with optimal cost . Algorithm 1 is run with initial parameter and inverse quadratic RBF to fit the surrogate function, using the acquisition criterion (18) with , , feasible initial samples, . Self-calibration is executed at steps indexed by over a grid of values , , .

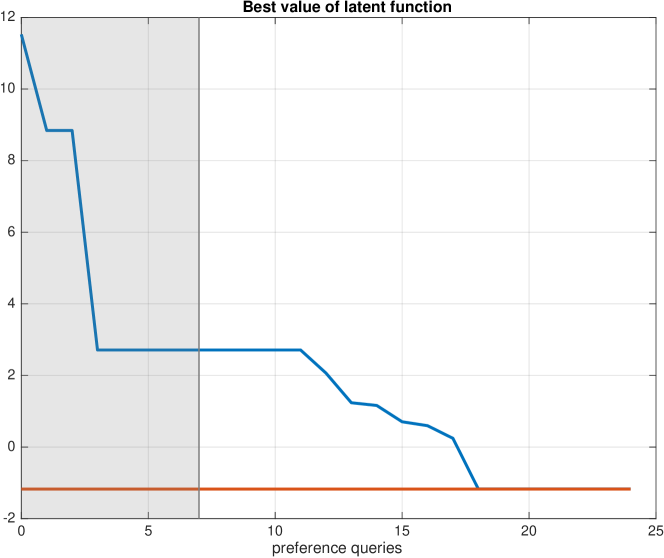

Figures 3 shows the samples generated by a run of Algorithm 1, Figure 4 the best (unmeasured) value of the latent function as a function of the number of preference queries, Figure 5 the shapes of and of the surrogate function . It is apparent that while achieves the goal of driving the algorithm towards the global minimum, its shape is quite different from , as it has been constructed only to honor the preference constraints (11) at sampled values. Therefore, given a new pair of samples , that are located far away from the collected samples , the surrogate function may not be useful in predicting the outcome of the comparison .

It is apparent that can be arbitrarily scaled and shifted without changing the outcome of preferences. While the arbitrariness in scaling is taken into account by the term in (18), it would be immediate to modify problem (12) to include the equality constraint

| (44) |

so that by construction is zero at the current best sample .

7.2 Benchmark global optimization problems

We test the proposed global optimization algorithm on standard benchmark global optimization problems. Problems brochu-2d, brochu-4d, brochu-6d were proposed in [4] and are defined as follows:

with , where the minus sign is introduced as we minimize the latent function, while in [4] it is maximized. For the definition of the remaining benchmark functions and associated bounds on variables the reader is referred to [2, 13].

In all tests, the inverse quadratic RBF with initial parameter is used in Algorithm 1, with in (18), initial feasible samples generated by Latin Hypercube Sampling as described in [2, Algorithm 2], and . Self-calibration is executed at steps indexed by over a grid of values , , , with the same set used to solve problem (43).

For comparison, the benchmark problems are also solved by the Bayesian active preference learning algorithm described in [4], which is based on a Gaussian Process (GP) approximation of the posterior distribution of the latent preference function . The posterior GP is computed by considering a zero-mean Gaussian process prior, where the prior covariance between the values of the latent function at the two different inputs and is defined by the squared exponential kernel

| (45) |

where and are positive hyper-parameters. The likelihood describing the observed preferences is constructed by considering the following probability description of the preference :

| (48) |

where is the cumulative distribution of the standard Normal distribution, and is the standard deviation of a zero-mean Gaussian noise which is introduced as a contamination term on the latent function in order to allow some tolerance on the preference relations (see [8] for details). The preference relation is treated as two independent observations with preferences and . The hyper-parameters and , as well as the noise standard deviation , are computed by maximizing the probability of the evidence [8, Section 2.2]. For a fair comparison with the RBF-based algorithm in this paper, these hyper-parameters are re-computed at the steps indexed by . Furthermore, the same number of initial feasible samples is generated using Latin hypercube sampling [24].

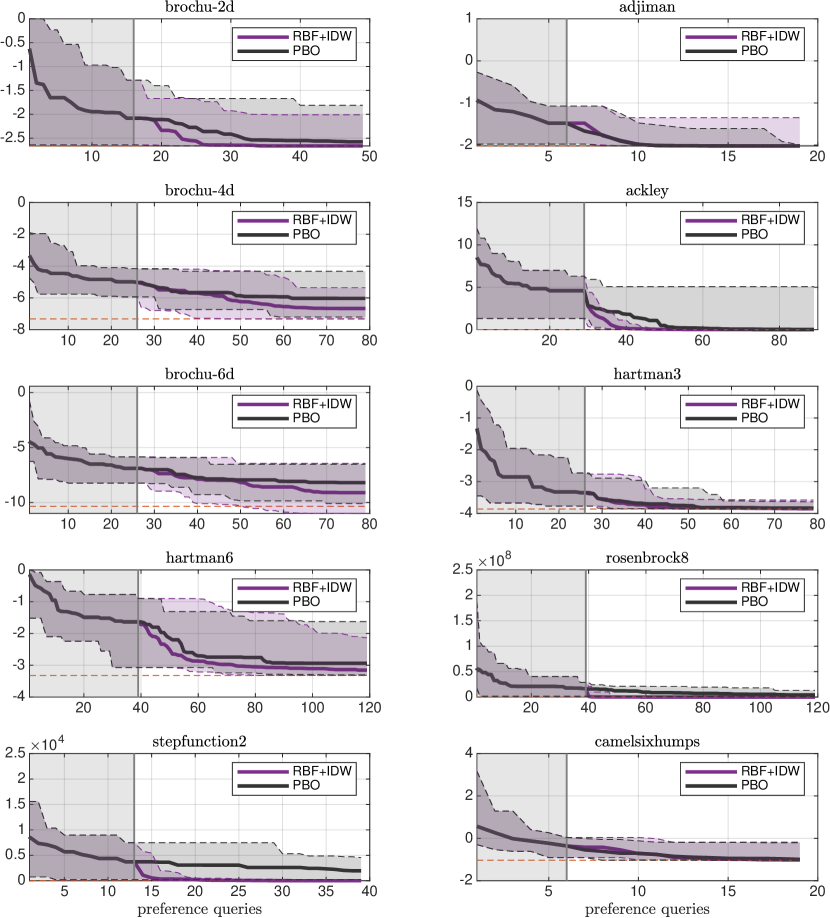

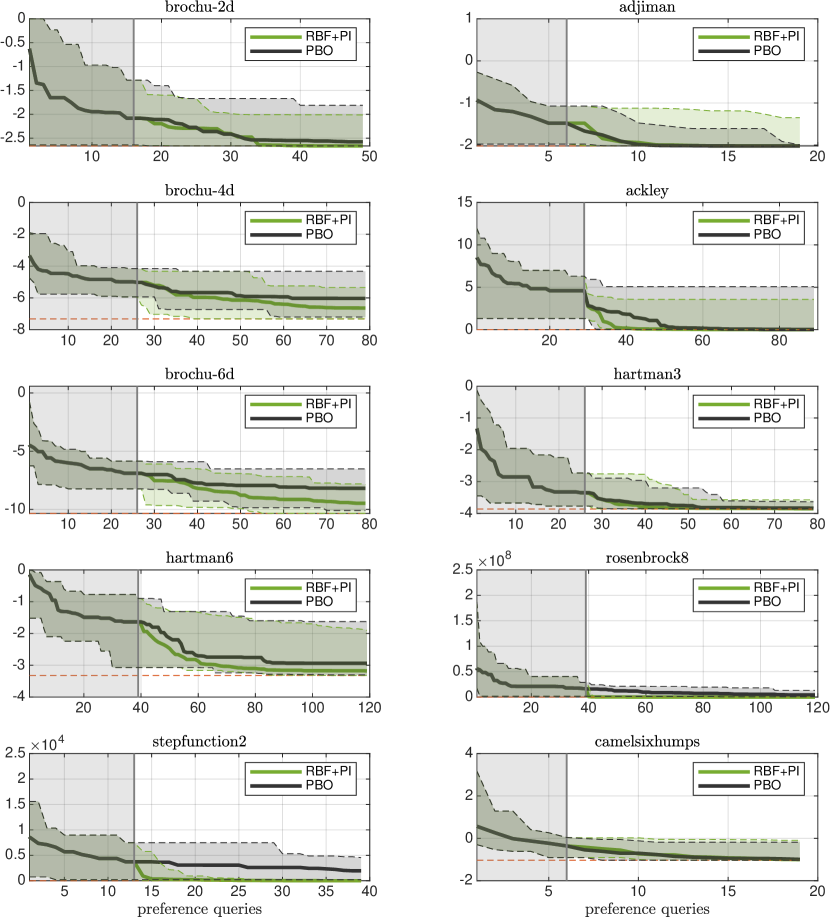

Algorithm 1 is executed using both the acquisition function (18) (RBF+IDW) and (31) (RBF+PI), and results compared against those obtained by Bayesian active preference learning (PBO), using the expected improvement as an acquisition function [4, Sec. 2.3]. Results are plotted in Figures 6 and 7, where the median performance and the band defined by the best- and worst-case instances over runs is reported as a function of the number of queried preferences. The vertical line represents the last query at which active preference learning begins. The average CPU time spent on solving each benchmark problem is reported in Table 1.

It is apparent that, compared to PBO, the RBF+IDW and RBF+PI algorithms perform better in approaching the minimum of the latent function and are computationally lighter. The RBF+IDW and RBF+PI algorithms have instead similar performance and computational load. Around 40 to 80% of the CPU time is spent in self-calibrating as described in Section 3.1.

| problem | RBF+IDW | RBF+PI | PBO | |

|---|---|---|---|---|

| brochu-2d | 2 | 5.9 | 6.0 | 18.5 |

| adjiman | 2 | 1.2 | 1.2 | 13.3 |

| brochu-4d | 4 | 21.1 | 21.4 | 30.7 |

| ackley | 2 | 30.8 | 30.9 | 51.2 |

| brochu-6d | 6 | 20.3 | 22.5 | 32.3 |

| hartman3 | 3 | 19.7 | 20.4 | 27.2 |

| hartman6 | 6 | 57.6 | 61.5 | 60.6 |

| rosenbrock8 | 8 | 68.1 | 70.1 | 306.4 |

| stepfunction2 | 4 | 4.2 | 4.3 | 45.2 |

| camelsixhumps | 2 | 1.2 | 1.2 | 14.6 |

7.3 Multi-objective optimization by preferences

We consider the following multi-objective optimization problem

| (49d) | |||||

| (49e) | |||||

Let assume that the preference is expressed by a decision maker in terms of “similarity” of the achieved optimal objectives, that is a Pareto optimal solution is “better” than another one if the objectives are closer to each other. In our numerical tests we therefore mimic the decision maker by defining a synthetic preference function as in (6) via the following latent function

| (50) |

As we have three objectives, we only optimize over and set , under the constraints , .

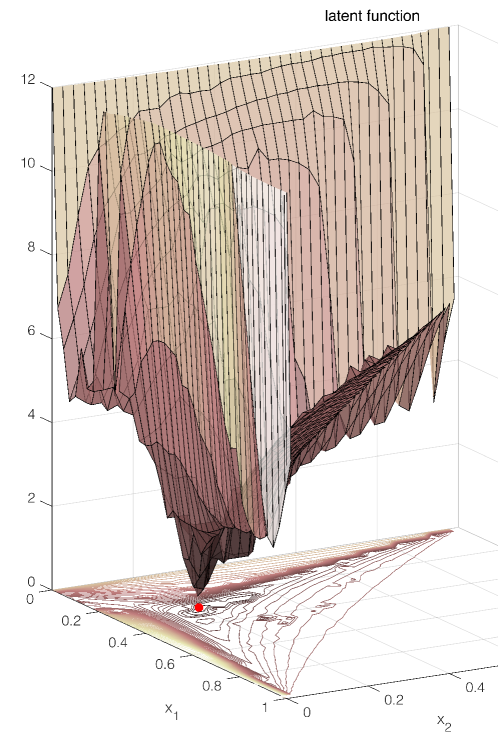

Figure 8 shows the results obtained by running times Algorithm 1 with , , and the same other settings as in the benchmarks examples described in Section 7.2. The optimal scalarization coefficients returned by the algorithm are , and , that lead to . The latent function (50) optimized by the algorithm is plotted in Figure 9. Note that the optimal multi-objective achieved by setting , corresponding to the intuitive assignment of equal scalarization coefficients, leads to the much worse result .

7.4 Choosing optimal cost-sensitive classifiers via preferences

We apply now the active preference learning algorithm to solve the problem of choosing optimal classifiers for object recognition from images when different costs are associated to different types of misclassification errors.

A four-class convolutional neural network (CNN) classifier with 3 hidden layers and a soft-max output layer is trained using 20000 samples, which consist of all and only the images of the CIFAR-10 dataset [20] labelled as: automobile, deer, frog, ship, that are referred in the following as classes , , , , respectively. The network is trained in 150 epochs using the Adam algorithm [19] and batches of size 2000, achieving an accuracy of 81% over a validation dataset of 4000 samples.

We assume that a decision maker associates different costs to misclassified objects and the predicted class of an image is computed as

| (51) |

where is the network’s confidence (namely, the output of the softmax layer) that the image is in class , and are nonnegative weights to be tuned in order to take into account the preferences of the decision maker. As for the multi-objective optimization example of Section 7.3, without loss of generality we set and the constraints , , thus eliminating the variable .

In our numerical tests we mimic the preferences expressed by the decision maker by defining the synthetic preference function as in (6), where the (unknown) latent function is defined as

| (52) |

In (52), the term is the number of samples in the validation set of actual class that are predicted as class according to the decision rule (51), while is the cost of misclassifying a sample of actual class as class . The considered costs are reported in Table 2, which describes the behaviour of the decision maker in associating a higher cost in misclassifying automobile and ship rather than misclassifying deer and frog. In (52), is a random variable uniformly distributed between and and it is introduced to represent a possible inconsistency in the preferences made by the user.

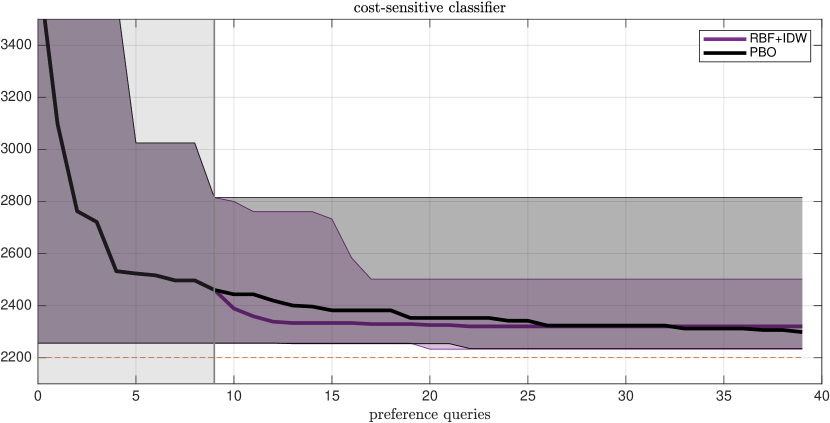

Figure 10 shows the results obtained by running times Algorithm 1 with , , , and the same other settings as in the benchmarks examples described in Section 7.2, and by running preference-based Bayesian optimization. The optimal weights returned by the algorithm after evaluating samples are , , and , that lead to a noise-free cost in (52) equal to (against 2585 obtained for unweighted costs, namely, for ). As expected, higher weights are associated to automobile and ship (class and , respectively). For judging the quality of the computed solution, the minimum of the noise-free cost is computed by PSO and used as the reference global optimum.

| predicted class | |||||

|---|---|---|---|---|---|

| actual class | 0 | 10 | 10 | 3 | |

| 4 | 0 | 2 | 4 | ||

| 4 | 2 | 0 | 4 | ||

| 3 | 10 | 10 | 0 | ||

8 Conclusions

In this paper we have proposed an algorithm for choosing the vector of decision variables that is best in accordance with pairwise comparisons with all possible other values. Based on the outcome of an incremental number of comparisons between given samples of the decision vector, the main idea is to attempt learning a latent cost function, using radial basis function interpolation, that, when compared at such samples, provides the same preference outcomes. The algorithm actively learns such a surrogate function by proposing iteratively a new sample to compare based on a trade-off between minimizing the surrogate and visiting areas of the decision space that have not yet been explored. Through several numerical tests, we have shown that the algorithm performs better than active preference learning based on Bayesian optimization, in that it approaches the optimal decision vector with less computations.

The approach can be extended in several directions. First, rather than only comparing the new sample with the current best , one could ask for expressing preferences also with one or more of the other existing samples . Second, the codomain of the comparison function could be extended to say where means “ is much better/worse than ”, and then extend (11) to include a much larger separation than whenever the corresponding preference . Third, often one can qualitatively assess whether a given sample is “very good”, “good”, “neutral”, “bad”, or “very bad”, and take this additional information into account when learning the surrogate function, for example by including additional constraints that force the surrogate function to lie in on all “very bad” samples, in on all “bad” samples, …, in on all “very good” ones, and choosing an appropriate value of . Furthermore, while a certain tolerance to errors in assessing preferences is built-in in the algorithm thanks to the use of slack variables in (11), the approach could be extended to better take evaluation errors into account in the overall formulation and solution method.

Finally, we remark that one should be careful in using the learned surrogate function to extrapolate preferences on arbitrary new pairs of decision vectors, as the learning process is tailored to detecting the optimizer rather than globally approximating the unknown latent function and, moreover, the chosen RBFs may not be adequate to reproduce the shape of the unknown latent function.

Acknowledgement

The authors thank Luca Cecchetti for pointing out the literature references in psychology and neuroscience cited in the introduction of this paper.

References

- [1] M. Abdolshah, A. Shilton, S. Rana, S. Gupta, and S. Venkatesh. Multi-objective bayesian optimisation with preferences over objectives. arXiv preprint arXiv:1902.04228, 2019.

- [2] A. Bemporad. Global optimization via inverse distance weighting. 2019. Submitted for publication. Also available on arXiv at https://arxiv.org/pdf/1906.06498.pdf. Code available at http://cse.lab.imtlucca.it/~bemporad/idwgopt.

- [3] E. Brochu, V.M. Cora, and N. De Freitas. A tutorial on Bayesian optimization of expensive cost functions, with application to active user modeling and hierarchical reinforcement learning. arXiv preprint arXiv:1012.2599, 2010.

- [4] E. Brochu, N. de Freitas, and A. Ghosh. Active preference learning with discrete choice data. In Advances in neural information processing systems, pages 409–416, 2008.

- [5] B.K.H Chau, N. Kolling, L.T. Hunt, M.E. Walton, and M.F.S. Rushworth. A neural mechanism underlying failure of optimal choice with multiple alternatives. Nature neuroscience, 17(3):463, 2014.

- [6] A. Chernev, U. Böckenholt, and J. Goodman. Choice overload: A conceptual review and meta-analysis. Journal of Consumer Psychology, 25(2):333–358, 2015.

- [7] A. Chinchuluun and P.M. Pardalos. A survey of recent developments in multiobjective optimization. Annals of Operations Research, 154(1):29–50, 2007.

- [8] W. Chu and Z. Ghahramani. Preference learning with gaussian processes. In Proceedings of the 22nd international conference on Machine learning, pages 137–144. ACM, 2005.

- [9] V. Franc, A. Zien, and B. Schölkopf. Support vector machines as probabilistic models. In Proc. of the 28th International Conference on Machine Learning, pages 665–672, Bellevue, WA, USA, 2011.

- [10] J. González, Z. Dai, A. Damianou, and N. D. Lawrence. Preferential bayesian optimization. In Proceedings of the 34th International Conference on Machine Learning, pages 1282–1291, 2017.

- [11] H.-M. Gutmann. A radial basis function method for global optimization. Journal of Global Optimization, 19:201–2227, 2001.

- [12] W. Huyer and A. Neumaier. Global optimization by multilevel coordinate search. Journal of Global Optimization, 14(4):331–355, 1999.

- [13] M. Jamil and X.-S. Yang. A literature survey of benchmark functions for global optimisation problems. Int. J. Mathematical Modelling and Numerical Optimisation, 4(2):150–194, 2013. https://arxiv.org/pdf/1308.4008.pdf.

- [14] S.G. Johnson. The NLopt nonlinear-optimization package. http://github.com/stevengj/nlopt.

- [15] D.R. Jones. A taxonomy of global optimization methods based on response surfaces. Journal of Global Optimization, 21(4):345–383, 2001.

- [16] D.R. Jones. DIRECT global optimization algorithm. Encyclopedia of Optimization, pages 725–735, 2009.

- [17] D.R. Jones, M. Schonlau, and W.J. Matthias. Efficient global optimization of expensive black-box functions. Journal of Global Optimization, 13(4):455–492, 1998.

- [18] J. Kennedy. Particle swarm optimization. Encyclopedia of Machine Learning, pages 760–766, 2010.

- [19] D. P. Kingma and J. L. Ba. Adam: a method for stochastic optimization. In Proc. International Conference on Learning Representation, San Diego, CA, USA, May 7-9 2015.

- [20] A. Krizhevsky, V. Nair, and G. Hinton. CIFAR-10 (canadian institute for advanced research).

- [21] H.J. Kushner. A new method of locating the maximum point of an arbitrary multipeak curve in the presence of noise. Journal of Basic Engineering, 86(1):97–106, 1964.

- [22] G. Matheron. Principles of geostatistics. Economic geology, 58(8):1246–1266, 1963.

- [23] D.B. McDonald, W.J. Grantham, W.L. Tabor, and M.J. Murphy. Global and local optimization using radial basis function response surface models. Applied Mathematical Modelling, 31(10):2095–2110, 2007.

- [24] M.D. McKay, R.J. Beckman, and W.J. Conover. Comparison of three methods for selecting values of input variables in the analysis of output from a computer code. Technometrics, 21(2):239–245, 1979.

- [25] L.M. Rios and N.V. Sahinidis. Derivative-free optimization: a review of algorithms and comparison of software implementations. Journal of Global Optimization, 56(3):1247–1293, 2013.

- [26] J. Sacks, W.J. Welch, T.J. Mitchell, and H.P. Wynn. Design and analysis of computer experiments. Statistical Science, pages 409–423, 1989.

- [27] M.J. Sasena, P. Papalambros, and P. Goovaerts. Exploration of metamodeling sampling criteria for constrained global optimization. Engineering optimization, 34(3):263–278, 2002.

- [28] D. Shepard. A two-dimensional interpolation function for irregularly-spaced data. In Proc. ACM National Conference, pages 517–524. New York, 1968.

- [29] H.A. Simon. A behavioral model of rational choice. The quarterly journal of economics, 69(1):99–118, 1955.

- [30] M. Stone. Cross-validatory choice and assessment of statistical predictions. Journal of the Royal Statistical Society: Series B (Methodological), 36(2):111–133, 1974.

- [31] L.L. Thurstone. A law of comparative judgment. Psychological review, 34(4):273, 1927.

- [32] A.I.F. Vaz and L.N. Vicente. A particle swarm pattern search method for bound constrained global optimization. Journal of Global Optimization, 39(2):197–219, 2007.

- [33] A.I.F. Vaz and L.N. Vicente. PSwarm: A hybrid solver for linearly constrained global derivative-free optimization. Optimization Methods and Software, 24:669–685, 2009. http://www.norg.uminho.pt/aivaz/pswarm/.

Appendix

Proof of Theorem 1

Proof of Theorem 2

Let be arbitrary unit vectors. Then, there exists an orthogonal (rotation) matrix with determinant such that . Let be a vector value function defined as . Note that the the Jacobian matrix of is , and thus its determinant is equal to .