fminipagem O #2 #2

Mechanics of good trade execution in the framework of linear temporary market impact

Abstract. We define the concept of good trade execution and we construct explicit adapted good trade execution strategies in the framework of linear temporary market impact. Good trade execution strategies are dynamic, in the sense that they react to the actual realisation of the traded asset price path over the trading period; this is paramount in volatile regimes, where price trajectories can considerably deviate from their expected value. Remarkably however, the implementation of our strategies does not require the full specification of an SDE evolution for the traded asset price, making them robust across different models. Moreover, rather than minimising the expected trading cost, good trade execution strategies minimise trading costs in a pathwise sense, a point of view not yet considered in the literature. The mathematical apparatus for such a pathwise minimisation hinges on certain random Young differential equations that correspond to the Euler-Lagrange equations of the classical Calculus of Variations. These Young differential equations characterise our good trade execution strategies in terms of an initial value problem that allows for easy implementations.

1 Introduction

Executions of large trades can affect the price of the traded asset, a phenomenon known as market impact. The price is affected in the direction unfavourable to the trade: while selling, the market impact decreases the price; while buying, the market impact increases the price. Therefore, a trader who wishes to minimise her trading costs has to split her order into a sequence of smaller sub-orders which are executed over a finite time horizon. How to optimally split a large order is a question that naturally arises.

Academically, the literature discussing such an optimal split was initiated by the seminal papers by Almgren and Chriss, (2001) and by Bertsimas and Lo, (1998). Both papers deal with the trading process of one large market participant who would like to buy or sell a large amount of shares or contracts during a specified duration. The optimisation problem is formulated as a trade-off between two pressures. On the one hand, market impact demands to trade slowly in order to minimise the unfavourable impact that the execution itself has on the price. On the other hand, traders have an incentive to trade rapidly, because they do not want to carry the risk of adverse price movements away from their decision price. Such a trade-off between market impact and market risk is usually translated into a stochastic control problem where the trader’s strategy (i.e. the control) is the trading speed. The class of admissible strategies defines the set over which the risk-cost functional is optimised.

In the design of mathematical models for optimal trade execution we identify two phases. The first phase is the description of trading costs. This refers to the choice of a function that depends on time, asset price, quantity to execute and trading speed, and models the instantaneous cost of trading. The overall cost during the time window is then expressed as the time integral

where the path is the evolution of the asset price during the trading period. The letter stands for quantity of the asset and the trajectory , , is referred to as inventory trajectory. Its time derivative is the rate of execution and it represents the control variable that a trader modulates while executing the trade.

The minimisation of the trading cost faces the challenge that the price path is not known at the beginning of the trading period. Hence, in order to gain some predictive power, a stochastic model for the evolution of the asset price is introduced. This is the second phase in the design of mathematical models for trade execution. Concretely, it means that a stochastic process is introduced and the actual price trajectory is thought of as a realisation of this stochastic process. Then, the mathematical optimisation focuses on the expected trading cost

| (1.1) |

Notice that this entails a considerable degree of model dependency, in that the optimisation is based on the distributional assumptions on the price process.

Two alternatives exist for the minimisations of the expected trading cost in equation (1.1). These alternatives are static minimisation (giving rise to static trading strategies) and dynamic minimisation (giving rise to dynamic trading strategies).

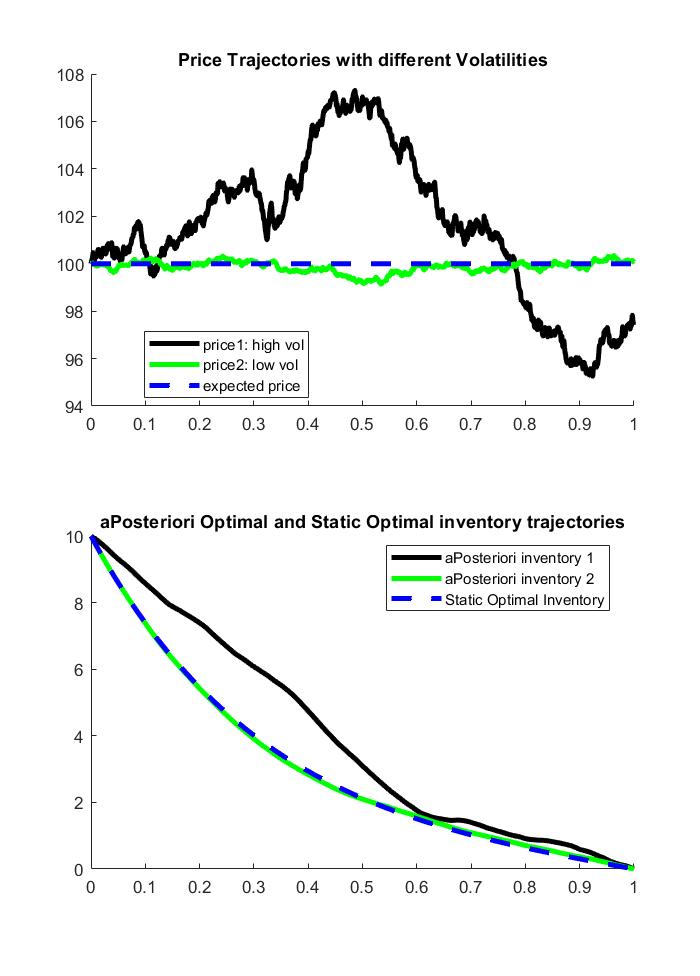

Static strategies are completely decided at the beginning of the trading period; they are based only on the information available at the initial time of the trade. Mathematically, this is formulated by considering as a deterministic path. In this case it is often observed that, by interchanging expectation and time integral in equation (1.1), the actual realisation of the price process disappears from the formulae, replaced by its expected trajectory. When the expected price path is the only feature of the price process that enters the formulae (as in Almgren and Chriss, (2001)), the static strategy does not take into account the volatility of asset prices, whose role however is paramount in financial markets. A visual representation of the relevance of volatility in the context of trade execution is provided by Figure 1.

In Figure 1 Almgren and Chriss’s framework is adopted. The price process is a standard one-dimensional Brownian motion and two price paths are considered, one with low volatility and the other with high volatility. Notwithstanding the remarkable difference between the two, they have the same expected path (dashed blue line in the first quadrant) and, as a consequence, the static liquidation strategy is the same for both price paths (dashed blue line in the second quadrant). The simplicity of the model is such that it compromises on the possibility to distinguish rather different market regimes. This is made clear by comparing the static optimal solution with the a-posteriori one.

The a-posteriori solution is the minimiser of the cost functional given the actual price trajectory . This is not implementable in real trading because it is anticipative, in that it assumes that the entire price trajectory is known at the beginning of the trading period. However, since it is independent of the choice of the price process, the a-posteriori solution constitutes a useful term of comparison for the stochastic model. In the example of Figure 1, we observe how different the two a-posteriori solutions corresponding to the two market regimes are. In the case of low volatility, the a-posteriori solution is close to the static one, because the price path does not depart significantly from its expected trajectory. Instead, in the case of high volatility, the a-posteriori solution deviates from the static one: the inventory trajectory is considerably steeper where the price is above its expected value, and it is almost flat when the price is below its expected value.

In order to take into account more features of the price process (such as its volatility), the literature on optimal trade execution has utilised the mathematical techniques of stochastic optimal control. This has produced the second alternative the minimisation of the expected cost in equation (1.1), and dynamic trading strategies proliferated since Bertsimas and Lo, (1998) (in discrete time) and Gatheral and Schied, (2011) (in continuous time). An excellent presentation of the techniques of stochastic optimal control applied to trade execution is contained in the textbook by Cartea et al., (2015).

Dynamic trading strategies take fully into account the distributional features of the price process because they are obtained via the Hamilton-Jacobi-Bellman equation, in which the generator of the diffusion that models the price enters.222In the case of linear temporary market impact and quadratic inventory cost, a recent work by Belak et al., (2018) actually discusses techniques that can be more generally applied to the case of general semimartingales. In this case there is no HJB equation; instead the authors rely on forward-backward stochastic differential equations. In Section 2, we will review this general solution. Furthermore, dynamic strategies are random when seen from the initial time, in that they depend on the information that is revealed to the trader during the trading period. Mathematically, this means that dynamic strategies are stochastic processes adapted to the relevant market information filtration. Since deterministic strategies are in particular adapted stochastic processes, the class of static strategies is a subset of the class of dynamic strategies. Therefore, the minimisation over the class of dynamic strategies is expected to improve the result obtained when minimising over the smaller class of static strategies.

This however is not always confirmed in the models. Indeed, despite the mathematical sophistication, cases exist in which optimal trading strategies, although sought among dynamic ones, are in fact static. One of such cases is for example the “Liquidation without penalties only temporary impact” in (Cartea et al., 2015, Section 6.3), an other is the “Optimal acquisition with terminal penalty and temporary impact” in (Cartea et al., 2015, Section 6.4). This reduction to static optimal solutions clashes with the intuition for which trading strategies should take into account actual realisations of price paths, as the a-posteriori solutions in Figure 1 suggest.

A second drawback of applying the technique of HJB equation to the problem of optimal trade execution is the heavy model dependence. Optimality of the trading strategies holds under the assumption that the price follows some specified dynamics, and this invests of considerable importance the second phase in the design of mathematical models.

In this paper, we propose a new alternative for the minimisation of trading costs. This new alternative considers the pathwise optimisation of the cost functional without taking expectation. We observe that the reason for the anticipativeness of a-posteriori solutions is the imposition of the constraint that the liquidation terminates exactly at the (arbitrarily fixed) trading horizon. Relaxing this constraint enables to produce adapted pathwise solutions that display two remarkable features. On the one hand, they avoid the degeneracy to static trajectories even in the cases where the techniques of HJB equation do not produce genuinely dynamic strategies; on the other hand, their model dependence is moderate and confined to the expected trajectory of the price path, as was the case for static strategies, rather than to the full law of the price process.

Our trading strategies give rise to inventory trajectories that are obtained in closed-form formulae. Moreover, we can characterise these trajectories as solutions to certain random Young differential equations, inspired by the second-order Euler-Lagrange equations in the classical Calculus of Variations. Such a characterisation allows to implement the inventory trajectories via an easily-simulated initial value problem.

The rest of the paper is organised as follows. Section 2 describes in detail the mathematical framework in which the problem of optimal trade execution is formulated. Our descriptions examines in particular two aspects of the mathematical models. The first aspect (Section 2.1) is the reduction to static optimal inventories that happens in the context of stochastic optimal control of the expected quantity in equation (1.1). Proposition 2.2 examines such a reduction, listing its causes. This is novel in the literature and answers the questions raised in Brigo and Di Graziano, (2014), Brigo and Piat, (2018) and Bellani et al., (2018) about the comparison between static and dynamic solutions to the problem of optimal trade execution. The second aspect is the unbiasedness of liquidation errors (Section 2.2).

Section 3 presents the concept of good trade execution. Section 3.1 specialises good trade executions in the case of linear temporary market impact and quadratic inventory cost. In particular, Section 3.1.1 derives a closed-form formula for good trade executions, and Section 3.1.2 characterises it in terms of a Cauchy problem with random Young differential equations. Uniqueness of the good trade execution follows from this characterisation.

Section 3.2 presents good trade executions with risk criteria other than the quadratic inventory cost. More precisely, Section 3.2.1 considers a time-dependent variant of the quadratic inventory cost, whereas Section 3.2.2 presents good trade executions when the risk criterion is inspired by the value-at-risk adopted in Gatheral and Schied, (2011).

2 Framework

We adopt the perspective of liquidation; the case of acquisition is mutatis mutandis the same. Let denote initial inventory, and let be the liquidation target. The letter stands for quantity of the asset and the trajectory , , shall be referred to as inventory trajectory. Its time derivative is the rate of execution and it represents the control variable that a trader modulates while executing the trade. Without yet referring to any probabilistic structure, let us introduce the space of such inventory trajectories:

The subscript “pw” stands for “pathwise” and emphasises the non-probabilistic perspective.

Definition 2.1.

Let be a probability space, and let be a stochastic process defined on it. We say that is a price process if: 1. for all the second moment of is finite; 2. the maps and are in ; 3. there exists some such that all the paths of are of finite -variation, i.e. for all in ,

Notice that the paths of the price process are not necessarily assumed to be continuous.

Given a price process , we let be the minimal -completed right-continuous filtration generated by . It is always assumed that is trivial.

If the price process is a semimartingale, we additionally introduce the following terminology. We say that the semimartingale is a totally square integrable special semimartingale if the following two conditions hold:

-

1.

the semimartingale is a special semimartingale, i.e. it admits a canonical decomposition

where is a predictable bounded variation process, is a local martingale, and ;

-

2.

the following integrability holds:

where denotes the quadratic variation of the local martingale , and denotes the -variation of the path on the time interval .333Recall that the 2-variation of a path is defined as where the supremum is taken over all the partitions of the interval .

Execution rates are progressively measurable square-integrable processes; more precisely, we define the space of execution rates as

| (2.1) |

Notice that the measurability depends on the filtration of the price process.

Admissible inventory trajectories are first integrals of execution rates with initial value . More precisely, we define the space of admissible inventory trajectories as

| (2.2) |

Among admissible inventory trajectories we distinguish those that are fuel-constrained, namely such that their terminal value is . Thus, a fuel-constrained admissible inventory trajectory is an -adapted process with absolutely continuous paths, with deterministic initial value , terminal value , and such that its derivative is in . More precisely, we define the space of fuel-constrained admissible inventory trajectories as

Notice that every realisation of a generic in is a path in , namely for all in and all in it holds

In the space of fuel-constrained inventory trajectories we isolate the subspace of static trajectories, given by

These are the execution strategies whose entire trajectories are -measurable, namely deterministic. We say that the admissible inventory trajectories not in are non-static (or dynamic): therefore, the admissible inventory trajectory is non-static if is in .

It is convenient to extend the definitions of the spaces of inventory trajectories to the case where the initial time is not zero. The symbols , , and will denote the straightforward generalisations of the definitions above to the case where the initial time is in and the trajectories are pinned to the value at time .

With the notation introduced so far, we now formulate the classical stochastic optimisation problem associated with optimal trade execution.

Let denote the state variable, which keeps track of the fundamental price and of the inventory . The dynamics of is controlled by an execution rate in . In order to emphasise this dependence, we can write , where is the control in the space of execution rates. With this notation, we express the objective function of the classical stochastic optimisation problem as

| (2.3) |

where is in , and where is a Lagrangian that describes risk-adjusted execution-impacted costs from trade. The stochastic optimisation problem for fuel-constrained inventory trajectories is therefore written as

| (2.4) |

An important aspect in the definition of the Lagrangian in equation (2.3) is the description of how the trade execution impacts the price, i.e. the market impact. In this work we focus on the so-called temporary market impact.

Let denote the price process at time . We say that the liquidator exerts a temporary market impact on if for some function in the execution price of her order at time is

where is the liquidator’s inventory trajectory, and denotes its time derivative at time . A well-known example of temporary market impact is given by , for some coefficient of market impact. In this case, the execution cost is a linear function of the rate of execution ; since in a liquidation is decreasing, the steepest the inventory trajectory is at time , the smaller the execution price is at time . The classical formulation in Almgren and Chriss, (2001) utilises this linear temporary market impact.

In the following two paragraphs 2.1 and 2.2, we introduce the concepts of reduction to static optimal strategies and the concept of liquidation error. We show that, in the context of linear temporary market impact with quadratic inventory cost, fuel-constrained optimal liquidation strategies are bound to be static, and non-fuel constrained optimal liquidation strategies commit biased errors of liquidation. This motivates the search for a formulation of the problem of optimal execution that is alternative to the classical one of equation (2.4). A possible alternative will then be presented in Section 3; under this alternative, optimal liquidation strategies will be non-static, and – despite being non-fuel constrained – they will have unbiased liquidation errors.

2.1 Reduction to static optimal strategies

In a temporary market impact model, trade revenues gained in the infinitesimal time are . When the temporary market impact is linear, this becomes

where revenues decompose in a first summand where the price process appears, and a second summand that does not comprise the price process. Clearly, such a decomposition holds in more general situations than the one of linear market impact. If this decomposition holds for the whole Lagrangian and if the bounded variation component of the price process is deterministic, then we observe the reduction of optimal dynamic solutions to optimal static ones. This happens in some cases studied in the literature (see (Cartea et al., 2015, Sections 6.3 and 6.4)), where the optimal inventory trajectory, although sought dynamic, is eventually found to be static. It means that the optimiser of (2.4) is in the space of static inventory trajectories. The following proposition explains this phenomenon, pointing out those aspects of the model that cause the reduction to static trade executions.

Proposition 2.2 (“Reduction to static optimal trade executions”).

Assume that

| (2.5) |

for some Caratheodory function444See Definition A.2 in Appendix A for the definition of Caratheodory function. The function in the statement of Proposition 2.2 is assumed to be a Caratheodory function with the choices: 1. the open interval as the subset of in Definition A.2; 2. the two-dimensional variable as the variable in Definition A.2. that does not depend on . Assume that there exist an integrable function on and a constant such that

Let the price process be a totally square integrable continuous canonical semimartingale with canonical decomposition

| (2.6) |

Assume that is -measurable, namely that the drift of the price process is deterministic. Then, for all it holds

Proof.

We give first the proof in the case where in the canonical decomposition of is a martingale.

Let be in . Let be the state variable and let be the two dimensional path . Let in be the function . Notice that

is a centred martingale. Hence,

It holds

where the infimum on the right hand side is taken in a pathwise sense for each realisation of the price . In fact, the integrand does not depend on such a realisation (i.e. it does not depend on in ) because is non-random. Therefore, any minimising sequence for the infimum inside the expectation is actually independent of and we have

This yields the stated equality in the case where is a martingale. If instead is only a local martingale, a standard localisation argument concludes the proof. ∎

Remark 2.3.

The classical optimal trade execution proposed by Almgren and Chriss, (2001) was originally formulated with optimality claimed over the set of static inventory trajectories and under the assumption that the price process is an arithmetic Brownian motion. However, it is easy to show that the same solution of the static optimisation is obtained if the Brownian motion is replaced by any square-integrable martingale. In this sense, the static optimal solution of Almgren and Chriss is robust. In view of Proposition 2.2, this robustness actually extends to the case where the liquidation strategy is regarded as the optimiser over the class of fuel-constrained inventory trajectories.

Remark 2.4.

A simple case where the optimal trading strategy is non-static is discussed by Gatheral and Schied, (2011). This means that the optimal inventory trajectory obtained from the stochastic control problem is in the space . In view of Proposition 2.2, we understand the dynamism of their solution by noticing the following. The risk measure adopted by those authors (see (Gatheral and Schied, 2011, Section 2.1)) is the value-at-risk of the position , and this has the consequence of disrupting the assumption that the Lagrangian can be decomposed as in equation (2.5). Indeed, Gatheral and Schied consider the optimisation

| (2.7) |

where the price process is the exponential martingale of , where denotes the standard one-dimensional Brownian motion, and where and are positive coefficients. Equation (2.7) is (Gatheral and Schied, 2011, Equation (2.7)). Alternatively, it can be noticed that the same minimisation as in equation (2.7) is produced by choosing and . Indeed, the expected cost

| (2.8) |

differs from the expected cost in equation (2.7) (where the price process is the exponential martingale) only by a constant. With the modelling choices in equation (2.8), the Lagrangian does not incorporate any risk criterion and thus it satisfies the assumptions of Proposition 2.2, but the price process has a position dependent drift coefficient, violating the assumption that in equation (2.6) is deterministic.

Remark 2.5.

In view of Proposition 2.2, we understand why incorporating signals (i.e. short-term price predictors) in the framework of optimal trade execution leads to dynamic optimal strategies (see Cartea and Jaimungal, (2016) and Lehalle and Neuman, (2019)). Indeed, signals are incorporated by modelling the price evolution as

where is a Markov process that represents the signal. The stochasticity of disrupts the assumption on the drift in Proposition 2.2.

Corollary 2.6.

Assume the setting of Proposition 2.2. Assume that the price process is modelled as the diffusion

| (2.9) |

for some measurable Lipschitz coefficients and . Assume that the drift coefficient is a deterministic function of time only. Assume that

-

1.

for all the map is strictly convex;

-

2.

there exist exponents and coefficients , such that

for all , and .

Then, the infimum in equation (2.4) is attained for some optimal deterministic in , where denotes the Sobolev space of absolutely continuous function such that their -th power and the -th power of their derivative are integrable on the time interval .

Remark 2.7.

The assumptions on in Corollary 2.6 are satisfied in particular by the classical choice

| (2.10) |

where is a coefficient of temporary market impact and is a coefficient of risk aversion (or of inventory cost). Therefore, Corollary 2.6 explains why in (Cartea et al., 2015, Section 6.3) the optimal solution is sought dynamic and eventually found to be static. This also says that, although in Almgren and Chriss, (2001) the optimal trade execution was sought only over the class for tractability, this was in fact without loss of generality (Remark 2.3).

2.2 Errors of liquidation

The space of fuel-constrained admissible inventory trajectories has been isolated from the space of first integrals of execution rates. An inventory trajectory in is said to commit a liquidation error, because with positive probability . Liquidation errors are common among dynamic solutions to optimal trade execution problems. This is because the mathematical techniques used for dynamic solutions are not well-suited to simultaneously impose the two constraints and . Clearly, the constraint has the priority and hence the constraint is relaxed. The usual relaxation entails to introduce a terminal penalisation for the outstanding inventory at final time. Hence, if is the Lagrangian describing risk-adjusted cost of trade, it is custom to relax the minimisation in equation (2.4) and consider instead the problem

| (2.11) |

where is a coefficient of penalisation for outstanding terminal inventory. Notice that the minimisation is performed over the broad class of first integrals of execution rates. Notice also that the objective function in equation (2.11) can be expressed in the general form discussed so far because

where .

We isolate liquidation errors whose expected value is null from those that on average either finish the liquidation before the time horizon (negative liquidation error) or after it (positive liquidation error).

Definition 2.8.

We say that the admissible inventory trajectory in has an unbiased liquidation error if . We say that has a biased liquidation error if instead .

By extension we say that a liquidation strategy is unbiased if its inventory trajectory has unbiased liquidation error, and we say that it is biased if it is not unbiased.

The next proposition shows that the classical optimisation problem corresponding to linear temporary market impact with quadratic inventory cost produces in general optimal liquidation strategies with biased liquidation error. In other words, if the optimal inventory trajectory in this framework happens to have unbiased liquidation error, this unbiasedness is not robust with respect to the values of the model parameters , and : independently changing these values will disrupt the expected value of the inventory at , turning it into a biased termination.

The solution to the optimisation problem is derived from Belak et al., (2018). Notice that the statement is general with respect to the distributional assumption of the price process, which is only assumed to be a totally square integrable semimartingale.

Proposition 2.9.

Let the price process be a totally square integrable special semimartingale. Consider the minimisation problem

| (2.12) |

where the Lagrangian is . Let be the minimiser for (2.12), and let . Then, is included in a manifold of dimension .

Proof.

Let be the ratio between the coefficient of risk aversion and the coefficient of linear temporary market impact. Let be the ratio between the coefficient of penalisation of outstanding inventory at time and the coefficient of linear temporary market impact. Define the functions and as follows:

| (2.13) |

Let be the following conditional expectation at time :

| (2.14) |

where is the price process with canonical decomposition . Then, (Belak et al., 2018, Theorem 3.1) proves that the optimal inventory trajectory that solves the minimisation problem in equation (2.12) is

| (2.15) |

This minimiser produces unbiased liquidation errors only if

Consider and as functions of . Let be defined as

Then, is a regular value of and . ∎

Remark 2.10.

Remark 2.11.

When the price process is a martingale, the optimal inventory trajectory of equation (2.15) is such that the terminal value is

In this case then, the optimal inventory trajectory will always finish with a positive inventory left to liquidate after the initially fixed time horizon of the liquidation.

Remark 2.12.

A liquidation strategy that is unbiased for any choice of and is obtained from equation (2.15) only in the limit as , which yields the fuel-constrained solution

where . This says that the inventory trajectory in equation (2.15) has unbiased liquidation error only in the degenerate case of deterministic terminal inventory.

3 Good trade executions

Let be a price process as defined in Definition 2.1. Let the class of inventory rates and the class of admissible inventory trajectories be as defined in equations (2.1) and (2.2) respectively.

From the class of admissible inventory trajectories we isolate the class of unbiased admissible inventory trajectories. An unbiased admissible inventory trajectory is defined as an -adapted process with absolutely continuous paths, with deterministic initial value , expected terminal value , and such that its derivative is in . More precisely, we define the space of unbiased admissible inventory trajectories as

The constraint relaxes the fuel constraint used in the definition of . Recall that, without loss of generality, the liquidation target is set equal to ; nonetheless, we do not suppress it from our equations because this makes the formulae easier to interpret (see Remarks 3.13 and 3.15).

We consider the following minimisation problem over the class of unbiased admissible inventory trajectories:

| (3.1) |

where is a space-differentiable Caratheodory function.555See Definitions A.2 and A.3. We use the symbol to denote the map , for in .

Assumption 3.1.

Let be the Lagrangian in the minimisation problem (3.1). It is assumed that is a space-differentiable Caratheodory function, and that the function is such that: 1. is in the Sobolev space for all compact subsets of ; 2. for almost every in , only if ; 3. the functions and are non-negative and square-integrable over .

Assumption 3.1 is used to associate the Lagrangian in equation (3.1) with a weight function on the Sobolev space and with a weight function on .

Definition 3.2.

Let be a space-differentiable Caratheodory function. Let satisfy Assumption 3.1. Let be in . Then, the pathwise -weight of is defined by the equation

| (3.2) |

where

Remark 3.3.

Let be a space-differentiable Caratheodory function, and define . Assume that satisfies points 1. and 2. in Assumption 3.1. Assume that is non-negative and square-integrable. If for all and all , then we drop the requirement that is non-negative and square-integrable and we understand equation (3.2) with the convention that .

Definition 3.4.

Let be as in Definition 3.2. Let be in . Then, the -weight of is defined by the following equation

| (3.3) |

where is the random variable , where are the paths of and, for every in , is the pathwise -weight of .

Every square-integrable random variable with identifies a subclass of trajectories in with specified terminal (random) variable. More precisely, for every in with we define

The class with is the class of inventory trajectories that commit no liquidation error, namely .

Definition 3.5 (“Optimal execution of terminal variable ”).

Let be in with . We say that in is the optimal execution of terminal variable if minimises over , namely if and for all it holds

with probability one.

For every we trivially have that . We can define a “tubular” neighbourhood of by looking at those trajectories in such that the -norm of the difference between terminal values is controlled by the -weight of the difference . More precisely, for in and we set

| (3.4) |

This captures the idea of not being too far from the terminal value given that the trajectory has kept close to in the time window .

Also, we define a pathwise analogous to the tubular neighbourhood of equation (3.4). Given a non-negative in we define

| (3.5) |

where is the absolute value of the difference between the values of and of at time , and is the pathwise -weight of the difference .

Remark 3.6.

Notice that both and depend on the Lagrangian . Nonetheless, we omit this dependence from the notation, and the symbols for these tubular neighbourhoods do not carry reference to .

Definition 3.7 (“Good trade execution”).

We say that in is a -good trade execution for the minimisation in equation (3.1) if there exist and such that

-

1.

for all in it holds

-

2.

for all in it holds

with probability one.

When we emphasise the path of a good trade execution, we use interchangeably the term good inventory trajectory.

Remark 3.8.

3.1 Quadratic inventory cost

In this section (Section 3.1), we consider the following Lagrangian :

| (3.6) |

where is a coefficient of market impact, and is a coefficient of risk aversion. For future reference, we set . Notice that in fact does not depend on . We study the problem in (3.1) with as in equation (3.6).

Remark 3.9.

The Lagrangian in equation (3.6) represents risk-adjusted revenues from trade where the market impact is temporary and linear, and the risk criterion is quadratic inventory cost. This aligns to common modelling choices such as those in Lehalle and Neuman, (2019) and in Belak et al., (2018). However, our relaxation of the fuel constraint entails that the inventory is sought in : we do not modify the objective function as is instead common in the studies of optimal dynamic liquidation strategies, where the terms of terminal asset position and of terminal inventory cost are usually added to the function that describes revenues from trade (see beginning of Section 2.2).

Remark 3.10.

The Lagrangian in equation (3.6) is the same as the Lagrangian in equation (2.10). However, the optimisation in equation (3.1) is pathwise and hence it differs from the classical optimisation of expected risk-adjusted revenues used in equation (2.4). For this reason, the martingale cancellation exploited in the proof of Proposition 2.2 is not applicable to the present case: we will be able to produce a non-static solution also in the case where the price process has deterministic drift (in particular, where the price process is a martingale).

Lemma 3.11.

Proof.

As for the requirements in Assumption 3.1, we only notice that the case is covered in Remark 3.3. As for the second part of the claim, we apply Lemma A.1 from Appendix A to see that the pathwise -weight is a seminorm. The fact that the -weight is a seminorm follows from the fact that the pathwise -weight is a seminorm. Finally, guarantees that if . ∎

We denote the pathwise seminorm induced by the pathwise -weight by . More precisely, we set

| (3.7) |

for in . Moreover, we denote the seminorm on induced by the -weight by .

3.1.1 Closed-form formula

Proposition 3.12.

Let be as in equation (3.6). Let be the ratio of the coefficients of risk aversion and of market impact, namely . Let be the function , and let be the constant

For , define

| (3.8) |

Then, is a -good trade execution. The constant is explicitly given by the formula

the random variable is explicitly given by the formula

Remark 3.13.

The structure of the solution in equation (3.8) is threefold: a time-dependent convex combination between initial inventory and liquidation target appears on the first line; a dynamic response to the actual price trajectory appears on the second line; an adjustment for the terminal constraint appears on the third line.

Proof of Proposition 3.12.

Let be as in equation (3.8). The fact that is in is apparent. Let and notice that is absolutely continuous with derivative

| (3.9) |

Let be in . We write for the difference , and we observe that and . Then, we have

The second integral on the right hand side is . Using integration-by-parts we see that in fact , because of equation (3.9). Therefore, the difference is non-negative if

This gives .

Secondly, consider the expected difference . We can estimate

because . Moreover,

Therefore, the expected difference is non-negative if

This gives the constant in the statement and concludes the proof. ∎

Remark 3.14.

We remark that the good inventory trajectory of equation (3.8) is written without assuming a particular SDE dynamics for the price evolution. In particular, Proposition 3.12 applies to the case in which the price process is modelled as a fractional Brownian motion, or as the sum of a possibly discontinuous semimartingale and a fractional Brownian motion. Moreover, the good inventory trajectory is robust, in the sense that it retains its optimality when one price process is replaced by another price process with for all .

Remark 3.15.

Given as in equation (3.8), we can compute

and estimate

We therefore remark the following two facts. First, the smaller is, the more precise the good execution of Proposition 3.12 is. Second, the square of the coefficient of linear market impact is inversely proportional to the standard deviation of , and thus the precision with which the good execution of equation (3.8) gets to its liquidation target increases when the strategy itself can exert more influence on the execution price.

Remark 3.16.

Unbiased admissible inventory trajectories have been defined as absolutely continuous stochastic processes on such that . This has meant that the constant in equation (3.8) has been chosen to minimise . We can give two alternatives to this minimisation:

-

1.

Choose in such a way to minimise

for some . The symbol stands for the mean . This yields

where . Notice that this tends to the former choice when .

-

2.

Choose in such a way to minimise

for some . This yields

with as above.

Notice however that the alternative choices for the constant make the corresponding inventory trajectory fall out of the set .

3.1.2 Characterisation via Euler-Lagrange equation

The differential equation in (3.9) is the linchpin on which the derivation of the good inventory trajectory is based. This equation is the Euler-Lagrange equation associated with the functional . Equation (3.9) is a random ordinary differential equation, where differentiation is possible because the price process is cancelled out in the sum . Such a cancellation allows to circumvent the need of an integration with respect to the price process. However this integration is possible; Appendix A presents the theory of the Euler-Lagrange equation in the presence of a (rough) price path. The motivation for this theory comes from the fact that equation (3.9) can be rewritten as

| (3.10) |

We interpret the system in equation (3.10) as a random Young differential equation. This equation is useful in simulations because it avoids the computation of the integrals in equation (3.8) and the evaluation of hyperbolic functions. Moreover, since we use Young integration to integrate with respect to the price process , the system in equation (3.10) has a pathwise meaning and thus it also makes sense in the practical implementation of the trading strategy, where the price process is replaced by the single price path observed during the liquidation.

In this paragraph, we apply the theory of Appendix A in order to characterise the good trade execution of Proposition 3.12 in terms of an initial value problem for the dynamics in (3.10).

We start by noticing that the Lagrangian in equation (3.6) satisfies Assumption A.4 in Appendix A. Equation (3.10) is equation (A.12) with given by (3.6). Moreover, by casting Definition A.11 to the case of equation (3.10), we have:

Definition 3.17.

Let be in . We say that solves equation (3.10) if for all in , all in and all the following holds:

| (3.11) |

We remark that Definition 3.17 is pathwise: a scenario in could be fixed and the definition would still make sense. The integral on the left hand side of equation (3.11) is well defined because for all in the path is in . Similarly, the first integral on the right hand side has a pathwise meaning and it is well defined because is in for all in . Thirdly, the integral on the right hand side of equation (3.11) is the Young integral introduced in Lemma A.10.

Lemma 3.18.

Let and be two solutions to equation (3.10). If , then there exist constants and such that

if , then there exist constants and such that

In particular, in both cases the difference between and is deterministic.

Proof.

Let be arbitrary in . By Definition 3.17 we have that

Let . Subtract one line from the other and obtain that the function

is constantly null. The first two summands are differentiable in and hence the third summand is differentiable too. Since is arbitrary, is differentiable in . Differentiating , we obtain

Hence , proving the lemma. ∎

Lemma 3.19.

Proof.

Let and be two solutions to equation (3.10) satisfying the constraints in (3.12). Assume . Then, by Lemma 3.18 it must be

for constants and . Therefore

Solving for and we find .

The case is analogous. ∎

Having established uniqueness of the solution to equation (3.10) with constraint (3.12), we link equation (3.10) to the good trade execution of Proposition 3.12. This link is established as an application of Lemma A.12 from Appendix A.

Lemma 3.20.

We are finally in the position to prove the main result of this paragraph.

Proposition 3.21 (“Characterisation of good trade execution via Euler-Lagrange equation”).

Remark 3.22.

Proposition 3.12 gives a characterisation of the good trade execution in terms of an initial value problem that is easily simulated. This is the practical relevance of the characterisation. We will rely on the initial value problem (3.10) with initial conditions (3.13) in our numerical experiments in Section 4.

Proof.

First we examine the following two implications.

- 1.

-

2.

A solution to equation (3.10) is a good trade execution. Assume that solves the Euler-Lagrange equation in (3.10). Then, by Lemma 3.20 we have that is absolutely continuous in for all in and its time derivative is . Hence, for all in and all in we have

where . The first summand on the right hand side is null and thus . This shows that is a -good trade execution.

In view of these two implications and of Lemma 3.19, it only remains to show that the initialisations in equation (3.13) are equivalent to the constraints in (3.12).

Consider an equation of the form

where the unknown is in , the matrix is in and and are two-dimensional real vectors. Equation (3.10) is of this form with the choice and

Assume first that is differentiable. Then, if we set we have that solves the ordinary differential equation

| (3.14) |

where . This ordinary differential equation has a two-dimensional space of solutions; hence we can exploit these two degrees of freedom to adjust for the constraints and .

Define the function as

Define the function as

The general solution to equation (3.14) is

The constraints and impose the choices

where

Hence, the constraints and are translated into the initialisation in the statement.

The case where the map is not differentiable is handled via a standard approximation argument. ∎

3.2 Alternative risk criteria

We present two alternatives to the risk criterion used in Section 3.1. This means that we modify the third summand in the Lagrangian of equation (3.6), and we study the minimisation problem with such a modified Lagrangian. The first alternative (Section 3.2.1) preserves the same structure but increases the weight of the coefficient of risk aversion linearly in time. The second alternative (Section 3.2.2) is instead inspired by the value-at-risk for geometric Brownian motion used in Gatheral and Schied, (2011).

3.2.1 Linearly time-dependent coefficient of risk aversion

The third summand in the Lagrangian of equation (3.6) accounts for the risk aversion. So far this term has been taken constant in the time variable . We now propose a linear -dependence, with higher risk aversion for closer to the liquidation horizon . More precisely, we consider the Lagrangian

| (3.15) |

where is a coefficient of market impact and is a coefficient of risk aversion. For future reference, we set . We study the minimisation problem in (3.1) with as in equation (3.15).

Lemma 3.23.

We denote the pathwise seminorm induced by the pathwise -weight by . More precisely, we set

| (3.16) |

for in . Moreover, we denote the seminorm on induced by the -weight by .

We proceed with statements analogous to those in Sections 3.1.1 and 3.1.2, namely: in Proposition 3.24 we give a closed-form formula for a good trade execution in the case of the Lagrangian of (3.15); then, in Proposition 3.25 we show that in fact such a good trade execution is unique, and we characterise it as the solution of a random Young differential equation. All the arguments are straightforward adaptations from those presented above, and thus we omit the proofs.

Proposition 3.24.

Let the Lagrangian be as in equation (3.15). Let and be the first and the second Airy’s functions, namely the two independent solutions to the second order linear ordinary differential equation . Define the functions , , as follows

where the innermost integral in the definition of is the Young integral introduced in Appendix A. Define the constants and as follows

For , define

| (3.17) |

Then, is a -good trade execution, where

where the symbol denotes the time derivative of the product function .

The Lagrangian in equation (3.15) satisfies Assumption A.4 from Appendix A. Equation (A.12) in the present case reads

| (3.18) |

We show that the good trade execution in Proposition 3.24 is characterised as the unique solution to the random Young differential equation (3.18).

Proposition 3.25.

The good trade execution of Proposition 3.24 is characterised as the unique solution to the random Young differential equation (3.18) with initialisation

where and are as in Proposition 3.24, and

In particular, the good trade execution in Proposition 3.24 is the only good trade execution for the minimisation (3.1) with the Lagrangian as in equation (3.15).

3.2.2 VaR-inspired risk criterion

Gatheral and Schied, (2011) model the fundamental price as a geometric Brownian motion and they adopt the value-at-risk as measure of risk aversion. This means penalising instantaneous revenues from trade by subtracting a term proportional to at every time . Inspired by their modelling choices, we now consider the Lagrangian

| (3.19) |

where is a coefficient of market impact and is a coefficient of risk aversion. Notice that in fact does not depend on . We study the minimisation problem in (3.1) with as in equation (3.19).

Lemma 3.26.

Proof.

We denote the pathwise seminorm induced by the pathwise -weight by . More precisely, we set

| (3.20) |

for in . Moreover, we denote the seminorm on induced by the -weight by .

We proceed with statements analogous to those in Sections 3.1.1 and 3.1.2, namely: in Proposition 3.27 we give a closed-form formula for a good trade execution in the case of the Lagrangian in equation (3.19); then, in Proposition 3.30 we show that such a good trade execution is unique, and we characterise it as the solution of a random Young differential equation. All the arguments are straightforward adaptations from those presented above, and thus we omit the proofs.

Proposition 3.27.

Let be as in equation (3.19). Let be the constant

For , define

| (3.21) |

Then, is a -good trade execution. The random variable is explicitly given by the formula

and the constant is explicitly given by the formula .

Remark 3.28.

The good trade execution in equation (3.21) has the same structure of the one in equation (3.8), namely: a time-dependent convex combination of and (first line), a dynamic response to the realisation of the price path (second line), and an adjustment for the constraint (third line). Moreover, notice that

so that the good trade execution in equation (3.21) and the good trade execution in equation (3.8) agree when the risk aversion vanishes, i.e. in the limit as .

Remark 3.29.

The Lagrangian in equation (3.19) satisfies Assumption A.4 from Appendix A. With this , equation (A.12) reads

| (3.22) |

where . We now characterise the good trade execution in Proposition 3.27 as the unique solution to the random Young differential equation (3.22). Observe that equation (3.22) is solved by direct integration and this simplifies several calculations compared to the cases of Sections 3.1.2 and 3.2.1.

Proposition 3.30.

The good trade execution of Proposition 3.27 is characterised as the unique solution to the random Young differential equation (3.22) with initialisation

In particular, the good trade execution in Proposition 3.27 is the only good trade execution for the minimisation (3.1) with is as in equation (3.19).

4 Applications

In this section we given two applications of the trading schedule proposed in Proposition 3.12.

Because of the reliance on the expected trajectory of the fundamental price, the use case of our framework is one where such an expected trajectory can serve as a reliable forecast for the price. This means that an implicit mean-reversion is assumed, and we will be choosing our price processes accordingly.

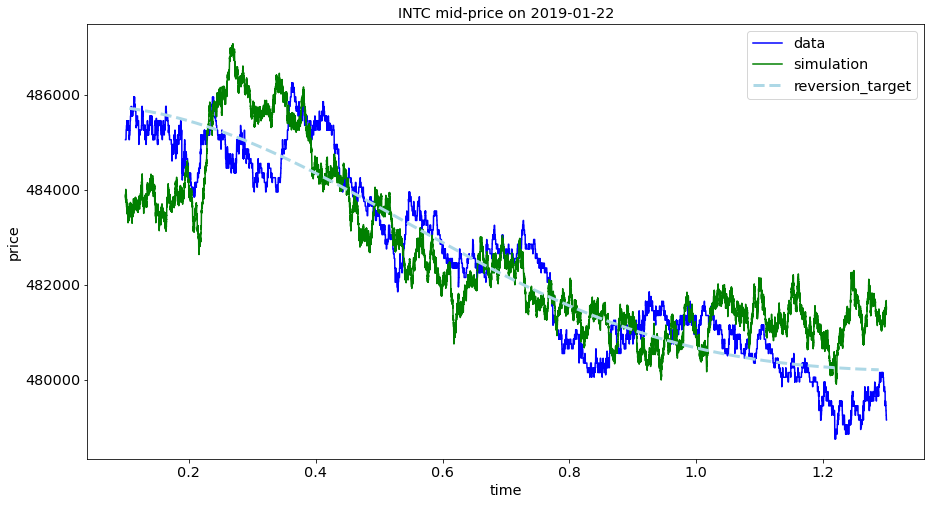

4.1 INTC shares: high-frequency mean-reverting jump diffusion

We consider the liquidation of a large portfolio of shares; the whole liquidation happens during intraday trading hours and on a single limit order book. We model the fundamental price on the mid-price of the order book, according to the following high-frequency mean-reverting jump-diffusion model:

| (4.1) |

where is -measurable, continuous and of finite variation, is the Ornstein-Uhlenbeck process , and is a compound Poisson process independent from and with i.i.d marks symmetrically distributed around zero. Therefore, the expected price trajectory is , and it represents the reversion target. The liquidator acts adopting this as her price forecast during the execution.

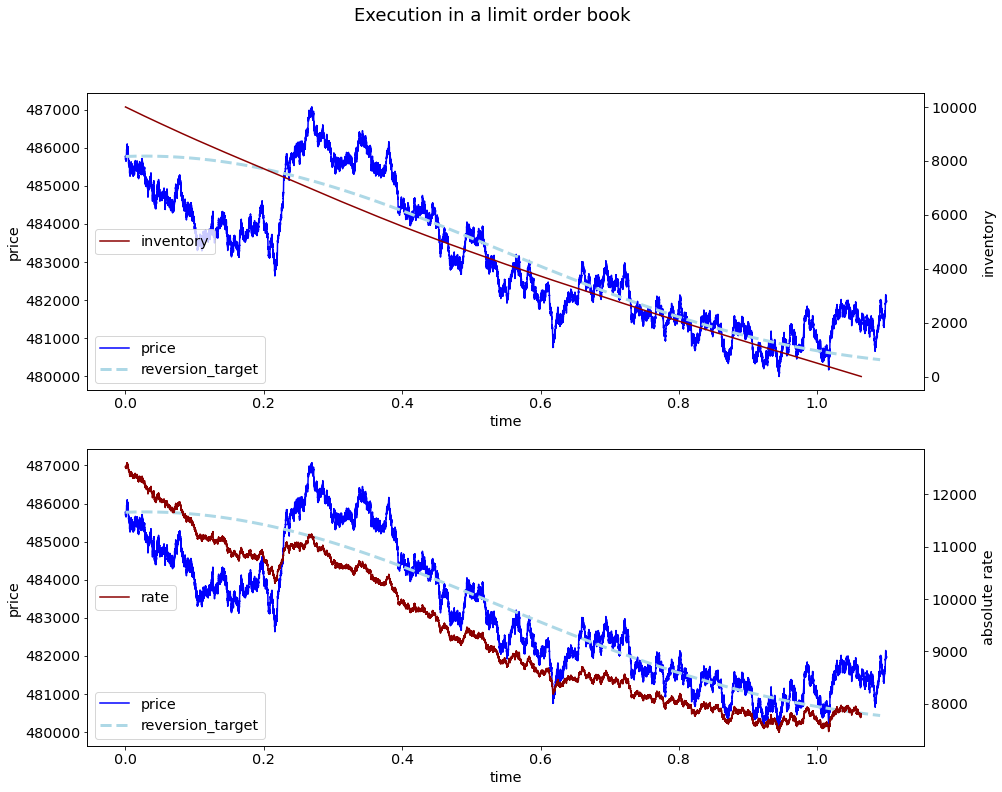

As an example, we calibrate our model to the high-frequency NASDAQ order book data available for the trading of INTC on 22 January 2019. The dataset is provided by LOBSTER (https://lobsterdata.com/). The calibration procedure is straightforward: we first extrapolate the mean-reversion target from the raw data, we then estimate the Ornstein-Uhlenbeck factor from the difference between the log-price and the logarithm of the mean-reversion target, and we finally calibrate the point process on the data points that are displaced beyond standard deviations from the expected value. In the interest of conciseness, we omit the details of this calibration procedure. The so-calibrated price process is displayed in the upper quadrant of Figure 2, together with the original data stream.

The lower quadrant in Figure 2 reports the inventory trajectory and its rate of execution computed as a solution to the Cauchy problem of equation (3.10) with initialisation (3.13). We remark two aspects observable from the picture. The first aspect is that the liquidation terminates after the initially decided horizon for the liquidation. This is because the realisation of the price path dwells for most of the time window of the liquidation below its expected value. Consequently, the liquidator decreases the rate of liquidation, in order to prevent her own price impact from exacerbating her trading cost even further. The trade-off between a limited exposure to market volatility and a parsimonious rate is resolved in favour of the latter. The second aspect is the reaction to the price jump that happens around . The jump is upward and hence favourable to the liquidation. Consequently, the liquidator reacts by increasing the rate of execution to exploit this.

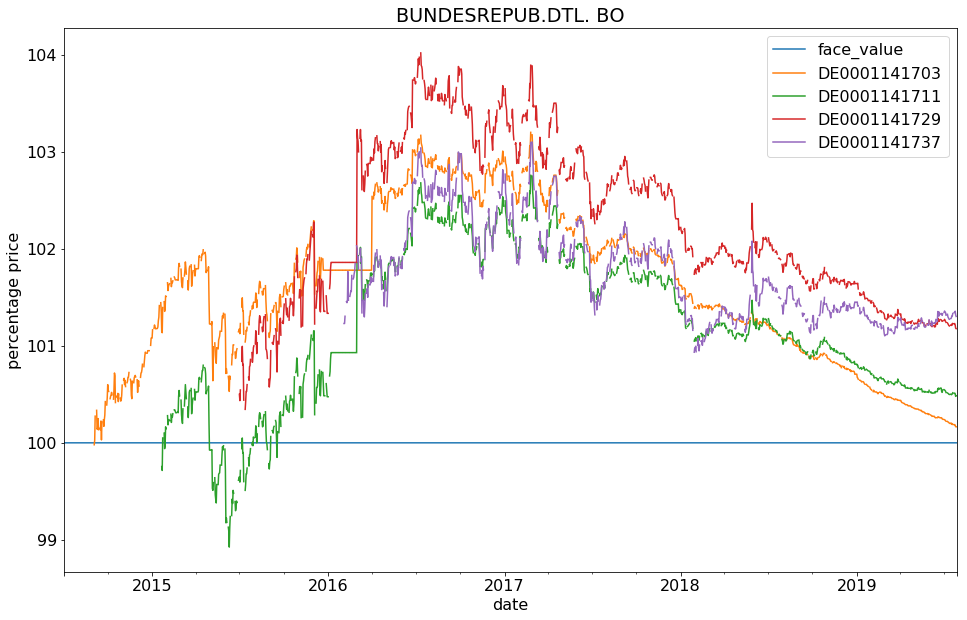

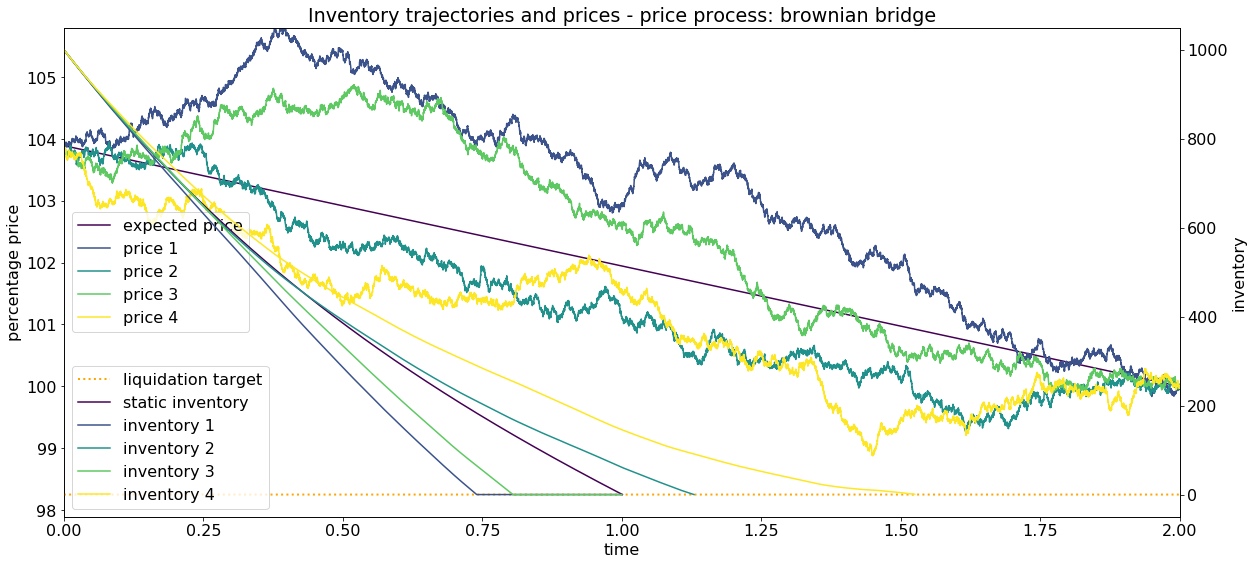

4.2 5Y government bonds: Brownian bridge

As a second application, we consider an entirely different time scale from the one of intraday INTC stock price, and in fact different from the time scale at which models of trade executions are usually applied. In this sense, the application is at the boundary between trade execution and dynamic portfolio management.

We consider the sale of 5Y government bonds motivated by market conditions whereby bond yields are negative. Historically, this was observed in 2016 for German bunds and such a phenomenon reappeared in March 2019. Four examples are reported in the upper quadrant of Figure 3, where we show the prices of 5Y German bunds with maturities October 2019, April 2020, October 2020, and April 2021.

The reason for negative yields was twofold. On the one hand, central banks launched programmes to stimulate the economy by cutting interest rates and by injecting liquidity via the so-called quantitative easing. On the other hand, in volatile economic regimes risk-adversed investors tend to move their capital to safe investments such as government bonds (a phenomenon known as flight-to-quality), and this exerted upward pressure on bond prices.

We consider an investor who wishes to unwind a long position on a negative yielding bond before incurring into the sure loss at the bond’s maturity. The sale is done gradually in time, on the one hand because the investor does not want to suddenly loose all the liquidity associated with the bonds, and on the other hand because the investor is mindful of the market impact that an abrupt sale would incur into.

In the upper quadrant of Figure 3 we observe that, after the period of overprice and as the maturity approaches, the trajectories converge on a downward slope towards the face value, which pins the trajectories at maturity. We base our modelling choices on this observation and, in line with a tradition that dates back to the Seventies (Boyce, (1970)), we adopt a Brownian bridge as the price process. More precisely, the price process is modelled as

| (4.2) |

where is the face value of the bond, is a standard one-dimensional Brownian motion, and is the volatility coefficient. In this model for the price process, the expected price path is the line segment from the decision price at time to the face value at maturity.

The second quadrant in Figure 3 shows good trade executions in this setting. The inventory trajectories are simulated following the dynamics in equation (3.10) with initialisation (3.13).

The way in which the good trade executions react to market scenarios is indicative of the dynamic adjustment of inventory trajectories during the liquidation. In particular, in scenarios #1 and #3 the liquidation is faster than the static solution; in this way it exploits favourable market conditions. Notice that this is advantageous especially in scenario #3, where a faster liquidation means that the liquidator concentrates her sale before the price plunges below its expected trend. On the contrary, in scenario #4, the good inventory trajectory is less steep than the static solution, because unfavourable market conditions recommend to parsimoniously impact the price.

5 Conclusions

In this paper, we examined the mathematical models of optimal trade execution with respect to two properties: non-static trajectories and unbiased liquidation errors. Non-static trajectories are those that react to the actual realisation of the price path during the execution, rather than being based only on assumed distributional properties of this price. Secondly, a liquidation error is said to be unbiased if its expectation is zero, entailing that the expected value of the terminal inventory coincides with the execution target.

We introduced our proposal for execution strategies, which enjoy both properties. In particular, in order to have non-static solutions even when the fundamental price is modelled as a martingale, we considered the minimisation of trading costs from a pathwise perspective, rather than the minimisation of expected trading costs.

We considered three risk criteria. The first criterion is the classical quadratic inventory cost; the second is a time-dependent modification of the first; the third was inspired by the value-at-risk employed in Gatheral and Schied, (2011). For all of them, we derived explicit closed-form formulae of our inventory trajectories. Furthermore, we characterised them through initial value problems that allow to easily implement our strategies in practice. We demonstrated this through two applications, one on the liquidation of INTC shares, the other on the liquidation of German bunds.

Acknowledgements

We are grateful to Eyal Neuman for discussion and suggestions that helped us improve the paper. We would also like to thank two anonymous referees for their comments and recommendations.

|

|

| initial inventory : 10000.0 price process : see equation (4.1) liquidation target : 0.0 coef market impact : 1.35 time horizon of liquidation : 1.0 coef risk aversion : 1.15 initial price : 485777 |

|

| bond name ISIN borrower issue date maturity cpn red.yield BUNDESREPUB.DTL.BO 2015 ZERO 17/04/20 DE0001141711 BCKKE 2015-01-23 2020-04-17 0.00 -0.6459 BUNDESREPUB.DTL.BO 2015 1/4% 16/10/20 DE0001141729 BCKKE 2015-07-03 2020-10-16 0.25 -0.6955 BUNDESREPUB.DTL.BO 2014 1/4% 11/10/19 DE0001141703 BCKKE 2014-09-05 2019-10-11 0.25 -0.4781 BUNDESREPUB.DTL.BO 2016 ZERO 09/01/21 DE0001141737 BCKKE 2016-02-05 2021-04-09 0.00 -0.7484 |

|

| initial inventory : 1000.0 price process : see equation (4.2) liquidation target : 0.0 volatility : 1.1642 time horizon of liquidation : 1.0 coef market impact : 0.05855 initial price : 103.893 coef risk aversion : 0.07341 |

References

- Almgren and Chriss, (2001) Almgren, R. and Chriss, N. (2001). Optimal execution of portfolio transactions. Journal of Risk, 3:5–40.

- Belak et al., (2018) Belak, C., Muhle-Karbe, J., and Ou, K. (2018). Liquidation in target zone models. Market Microstructure and Liquidity, 04(03n04):1950010.

- Bellani et al., (2018) Bellani, C., Brigo, D., Done, A., and Neuman, E. (2018). Static vs adaptive strategies for optimal execution with signals. International Journal of Financial Engineering (to appear).

- Bertsimas and Lo, (1998) Bertsimas, D. and Lo, A. W. (1998). Optimal control of execution costs. Journal of Financial Markets, 1(1):1–50.

- Boyce, (1970) Boyce, W. M. (1970). Stopping rules for selling bonds. The Bell Journal of Economics and Management Science, 1(1):27–53.

- Brigo and Di Graziano, (2014) Brigo, D. and Di Graziano, G. (2014). Optimal trade execution under displaced diffusions dynamics across different risk criteria. Journal of Financial Engineering, 1(2):1450018.

- Brigo and Piat, (2018) Brigo, D. and Piat, C. (2018). Static vs adapted optimal execution strategies in two benchmark trading models.

- Cartea et al., (2017) Cartea, A., Donnelly, R., and Jaimungal, S. (2017). Algorithmic trading with model uncertainty. SIAM J. Financial Math., 8(1):635–671.

- Cartea and Jaimungal, (2016) Cartea, A. and Jaimungal, S. (2016). Incorporating order-flow into optimal execution. Math. Financ. Econ., 10(3):339–364.

- Cartea et al., (2015) Cartea, A., Jaimungal, S., and Penalva, J. (2015). Algorithmic and high-frequency trading. Cambridge University Press, Cambridge, United Kingdom.

- (11) Casgrain, P. and Jaimungal, S. (2019a). Algorithmic trading in competitive markets with mean field games. SIAM News, 52(2):1–2.

- (12) Casgrain, P. and Jaimungal, S. (2019b). Trading algorithms with learning in latent alpha models. Math. Finance, 29(3):735–772.

- Cordoni and Persio, (2020) Cordoni, F. and Persio, L. D. (2020). A maximum principle for a stochastic control problem with multiple random terminal times. Mathematics in engineering, 2(3):557–583.

- Dacorogna, (2008) Dacorogna, B. (2008). Direct methods in the calculus of variations, volume 78 of Applied Mathematical Sciences. Springer, New York, second edition.

- Denny and Suchanek, (1986) Denny, J. and Suchanek, G. L. (1986). On the use of semimartingales and stochastic integrals to model continuous trading. Journal of Mathematical Economics, 15(3):255–266.

- Gatheral and Schied, (2011) Gatheral, J. and Schied, A. (2011). Optimal Trade Execution Under Geometric Brownian Motion In The Almgren And Chriss Framework. International Journal of Theoretical and Applied Finance (IJTAF), 14(03):353–368.

- Huang et al., (2019) Huang, X., Jaimungal, S., and Nourian, M. (2019). Mean-field game strategies for optimal execution. Appl. Math. Finance, 26(2):153–185.

- Kentia and Kühn, (2018) Kentia, K. and Kühn, C. (2018). Nash equilibria for game contingent claims with utility-based hedging. SIAM Journal on Control and Optimization, 56(6):3948–3972.

- Lehalle and Neuman, (2019) Lehalle, C.-A. and Neuman, E. (2019). Incorporating signals into optimal trading. Finance and Stochastics, 23(2):275–311.

- Mitchell and Chen, (2020) Mitchell, D. and Chen, J. (2020). Market or limit orders? Quantitative Finance, 20(3):447–461.

- Roux and Zastawniak, (2018) Roux, A. and Zastawniak, T. (2018). Game options with gradual exercise and cancellation under proportional transaction costs. Stochastics, 90(8):1190–1220.

- Xu and Zhou, (2013) Xu, Z. Q. and Zhou, X. Y. (2013). Optimal stopping under probability distortion. The Annals of Applied Probability, 23(1):251–282.

Appendix A Euler-Lagrange equations with price paths

All the statements in this appendix are pathwise, hence we leave probability out of the picture. In particular, the symbol will denote a (possibly discontinuous) single path of finite -variation, for some . We consider the following functions spaces. The space is the space of smooth functions with compact support in the open interval . The Sobolev space is the space of absolutely continuous functions on the closed interval such that and its derivative are square integrable over . The Sobolev space is endowed with the norm

The space is defined as the closure of in .

Lemma A.1.

Let and be non-negative bounded measurable functions defined on . Then,

is a seminorm on .

Proof.

Notice that for in we can write , where is the norm associated with the measure , and is the norm associated with the measure . Therefore, the triangle inequality is proved by the following chain of inequalities:

where on the first line we used Minkowski inequality in and , and on the second line we applied Minkowski inequality in . ∎

Definition A.2 (“Caratheodory function”).

Let be an open set in . The function is called Caratheodory function if: 1. for almost every in , the map is continuous; 2. for every in , the function is Lebesgue-measurable.

Definition A.3.

Let be an open subset of . Let be a Caratheodory function. We say that is space-differentiable if for all in the map is in .

In this appendix we consider Lagrangians for which the following assumption holds.

Assumption A.4.

Let be a Caratheodory function. It is assumed that

| (A.1) |

where is a space-differentiable Caratheodory function on such that there exist a function in and a constant such that

| (A.2) |

for all in and all , , in .

The space variables are alternatively labelled as . Hence, we interpret as the placeholder for the variable denoting the fundamental price, we interpret as the placeholder for the variable denoting the inventory, and we interpret as the placeholder for the variable denoting the rate of execution. In the following, we adopt these letters for the space variables; hence, in particular denotes the derivative of with respect to the variable , and denotes the derivative of with respect to the variable .

Remark A.5.

When does not depend on , the decomposition in equation (A.1) has the form of the decomposition in equation (2.5). However, we do not restrict to that case in this appendix. In particular, our treatment encompasses the case of the functional used in Gatheral and Schied, (2011), which we discuss in Section 3.2.2.

Let be a path on and assume that is of finite -variation for some . Let be a Caratheodory function satisfying Assumption A.4. Let be the functional

| (A.3) |

Let be in and consider the affine space

We study the minimisation problem

| (A.4) |

Proposition A.6 (“Weak form of Euler-Lagrange equation”).

Proof.

As an application of the sufficient condition for optimality established in Proposition A.6, we derive the optimal static inventory trajectory in the case of linear temporary market impact and quadratic inventory cost.

Corollary A.7.

Proof.

Equation (A.5) is the weak form of the Euler-Lagrange equation. In the next paragraph, we introduce the pathwise integration with respect to the path . This will allow to move from the condition in equation (A.5) to the stronger formulation of the Euler-Lagrange equation.

Young integration and integration-by-parts formula

Let be the closed time interval from time zero to the time horizon . We consider partitions of . A partition is simultaneously considered as the finite collection of points and as the finite collection of adjacent subintervals. Given a partition of and a time instant in , we adopt the following notational convention:

| (A.7) |

The mesh-size of the partition is defined as

Let be a function on . If and are in , we let denote the increment of from to . The resulting two-parameter function is additive, in that for all it holds . For more general two-parameter functions defined on we can relax the additivity and consider the following property.

Definition A.8.

Let be a function on . We say that is super-additive if for all it holds

Lemma A.9.

Let be a super-additive function on such that it is null and uniformly continuous on the diagonal, i.e. and

| (A.8) |

Let be a super-additive function on . Let and be exponents such that . Then,

where the limit is taken along arbitrary sequences of partitions of with mesh-size tending to zero.

Proof.

Let be such that . Then,

On the second line we have applied Hölder inequality and on the third line we have used super-additivity. We conclude by recalling the uniform continuity of equation (A.8). ∎

Lemma A.10.

Let be an absolutely continuous path on the closed interval . Let be a path on of finite -variation for some . Then, for all the limit

exists and is the same along any sequence of partitions of . Such a limit defines the Young integral

Moreover, the following integration-by-parts formula holds

where the second integral on the left hand side is the Stieltjes integral of against .

Proof.

Let be an arbitrary partition of . For all in we have

| (A.9) |

Consider first the right hand side of equation (A.9). Consider the first two summands on the right hand side of equation (A.9). If we sum over in we have the telescopic sum

and this does not depend on the partition of . The third summand on the right hand side of equation (A.9) can be bound as follows:

Hence, by Lemma A.9, we have

Here, we have applied Lemma A.9 with , , , and . Therefore, if we apply the operator to the right hand side of equation (A.9), we obtain

Consider now the left hand side of equation (A.9). The limit

is the Stieltjes integral and thus converges and is the same along any sequence of partitions with vanishing meshsize. Therefore, if we apply the operator to both side of equation (A.9) we must have that the limit in equation (A.10) exists and is equal to

This concludes the proof of the lemma. ∎

Strong form of Euler-Lagrange equation

Relying on the Young integral introduced in the previous paragraph, we now formulate the strong form of the Euler-Lagrange equation associated with the minimisation problem in equation (A.4).

Definition A.11.

Let be a constant. Let be a path on and assume that is of finite -variation for some . Let be a Caratheodory function on such that

for some integrable function in and some constant . We say that the function in solves the equation

| (A.10) |

if for all in and all it holds

| (A.11) |

where the last integral on the right hand side is the Young integral introduced in Lemma A.10.

Lemma A.12.

Proof.

Proposition A.13 (“Strong form of Euler-Lagrange equation”).

Let be a path on and assume that is of finite -variation for some . Consider a Lagrangian satisfying Assumption A.4. Assume that the space-differentiable Caratheodory function is in and such that

for some non-zero constant in and some function in .666This assumption on the form of the partial derivative is satisfied in all three examples that we consider in the paper, namely by the Lagrangians in equations (3.6), (3.15) and (3.19). Assume that is a minimiser for (A.4). Then, solves the Euler-Lagrange equation

| (A.12) |

in the sense of Definition A.11.