Distribution-free consistent independence tests via center-outward ranks and signs

Abstract

This paper investigates the problem of testing independence of two random vectors of general dimensions. For this, we give for the first time a distribution-free consistent test. Our approach combines distance covariance with the center-outward ranks and signs developed in Hallin, (2017). In technical terms, the proposed test is consistent and distribution-free in the family of multivariate distributions with nonvanishing (Lebesgue) probability densities. Exploiting the (degenerate) U-statistic structure of the distance covariance and the combinatorial nature of Hallin’s center-outward ranks and signs, we are able to derive the limiting null distribution of our test statistic. The resulting asymptotic approximation is accurate already for moderate sample sizes and makes the test implementable without requiring permutation. The limiting distribution is derived via a more general result that gives a new type of combinatorial non-central limit theorem for double- and multiple-indexed permutation statistics.

Keywords: Combinatorial non-central limit theorem, degenerate U-statistics, distance covariance, center-outward ranks and signs, independence test.

1 Introduction

Let and be two real random vectors defined on the same (otherwise unspecified) probability space. This paper treats the problem of testing the null hypothesis

| (1.1) |

based on independent copies of . Testing independence is a fundamental statistical problem that has received much attention in literature.

For the simplest instance, the bivariate case with , Hoeffding, (1940), Hoeffding, (1948), Blum et al., (1961), Yanagimoto, (1970), Feuerverger, (1993), Bergsma and Dassios, (2014), among many others, have proposed tests that are consistent against all alternatives from slightly different but rather general classes of distributions. The tests are usually formulated using (univariate) ranks of the data, although recently more tests were proposed based on alternative summaries of the data, including (i) binning approaches based on a partition of the sample space (Heller et al., , 2013, 2016; Ma and Mao, , 2019; Zhang, , 2019), (ii) mutual information (Kraskov et al., , 2004; Kinney and Atwal, , 2014; Berrett and Samworth, , 2019), and (iii) the maximal information coefficient (Reshef et al., , 2011, 2016, 2018).

Testing independence of and consistently when one or both of the dimensions and are larger than one is substantially more challenging, as noted in Feuerverger, (1993, Sec. 7). Solutions have not been discovered until much more recently. Two tracks were pursued. First, Székely et al., (2007) generalized Feuerverger, ’s statistic to multivariate cases and proposed a new dependence measure termed “distance covariance”. It has been shown that under the existence of finite marginal first moments, the distance covariance is zero if and only if holds. For further extensions, Lyons, (2013) generalized distance covariance/correlation to general metric spaces, and Jakobsen, (2017) considered the corresponding test of independence in metric spaces.

The second track to characterize non-linear, non-monotone dependence is based on the maximal correlation introduced in Hirschfeld, (1935) and Gebelein, (1941), reformulated and examined by Rényi, 1959a ; Rényi, 1959b . Gretton et al., 2005c ; Gretton et al., 2005a ; Gretton et al., 2005b extended this idea to examine multivariate cases, resulting in the Hilbert-Schmidt independence criterion (HSIC), which is a consistent kernel-based measure of dependence in multivariate cases. Interestingly, Gretton et al., (2008) connected HSIC with a Gaussian kernel to the characteristic function-based statistic raised in Feuerverger, (1993), and Sejdinovic et al., (2013) pointed out the equivalence between distance covariance in general metric spaces and the kernel-based independence criterion.

A notable feature of both distance- and kernel-based statistics is that their null distributions depend on the distributions of and even in the large-sample limit. This dependence arises already for and is usually difficult to estimate. As a consequence, the tests are, unlike the rank tests of, e.g., Hoeffding, (1948) and Blum et al., (1961), no longer distribution-free and permutation analysis has to be conducted to implement them. To remedy this problem, Székely et al., (2007) proposed a nonparametric test based on distance correlation by applying a universal upper tail probability bound for all quadratic forms of centered Gaussian random variables that have their mean equal to one (Székely and Bakirov, , 2003). However, in practice this upper bound is usually too conservative for the approach to be a competitor to the computationally much more expensive permutation test (Székely and Rizzo, , 2009; Gretton et al., , 2008). This triggers the following question: For general , does there exist an asymptotically accurate consistent test of that is distribution-free and hence directly implementable?

Rank-based tests constitute a natural approach to answering the above question. Indeed, in contrast to Székely and Rizzo, (2009), Rémillard, (2009) claimed that the methods based on marginal ranks are effective and as powerful as original ones when the sample size is moderately large and this idea has been explored in depth in Lin, (2017). However, Bakirov et al., (2006) noted that the methods based on marginal ranks do not enjoy distribution-freeness except in dimension one, which is also recorded in, e.g., Theorem 2.3.2 in Lin, (2017). Using the idea of projection from Escanciano, (2006), Zhu et al., (2017) generalized Hoeffding’s (Hoeffding, , 1948) to multivariate cases, and Kim et al., (2018) proposed the analogues of Blum–Kiefer–Rosenblatt’s (Blum et al., , 1961) and Bergsma–Dassios–Yanagimoto’s (Yanagimoto, , 1970; Bergsma and Dassios, , 2014; Drton et al., , 2020). Weihs et al., (2018) proposed other multivariate extensions of Hoeffding’s , Blum–Kiefer–Rosenblatt’s , and Bergsma–Dassios–Yanagimoto’s , and did numerical studies comparing them to distance covariance applied to marginal ranks. Alternatively, Heller et al., (2013) developed a consistent multivariate test based on ranked distance covariance by transferring the original problem to testing independence of an aggregated contingency table. However, all the aforementioned tests are not distribution-free when or is larger than , and due to the difficulty of accounting for the dependence within and , permutation analysis is required for their implementation. On the other hand, Heller et al., (2012) and Heller and Heller, (2016) introduced distribution-free graph-based and rank-based tests. However, it is unclear if the former is consistent, and the latter requires choosing two arbitrary reference points. The latter test is almost surely consistent in the sense that the choice of reference points needs to avoid an (unknown) measure zero set.

This paper proposes a solution to the above question by combining Székely, Rizzo, and Bakirov’s distance covariance with a recently defined concept of multivariate ranks due to Hallin, (2017). Due to the lack of a canonical ordering on for , fundamental concepts related to distribution functions in dimension , such as ranks and quantiles, do not admit a simple extension for that maintains properties such as distribution-freeness. To overcome this limitation, several types of multivariate ranks have been introduced; see Hallin, (2017, Sec. 1.3) and, more recently, Ghosal and Sen, (2019) for a literature review. None of them, however, is distribution-free except for pseudo-Mahalanobis ranks (Hallin and Paindaveine, 2002b, ; Hallin and Paindaveine, 2002a, ), but these are restricted to the class of elliptically symmetric distributions (Fang et al., , 1990). Recently, Chernozhukov et al., (2017) introduced the concept of Monge–Kantorovich ranks and signs for all distributions with convex and compact supports, which is the first type of multivariate ranks that enjoys distribution-freeness for a rich class of distributions. Hallin, (2017) generalized this definition by refraining from moment assumptions and making the solution more explicit. He also adopted the new terminology center-outward ranks and signs. Hallin et al., (2020) further showed that center-outward ranks and signs are not only distribution-free, but also essentially maximal ancillary, which can be interpreted as “maximal distribution-free” in view of Basu, (1959). As shall be seen soon, the explicit nature of the solution is important as it allows for more delicate manipulations and ultimately allows us to form a test statistic of whose limiting null distribution can be determined. The limiting distribution furnishes an accurate approximation to the statistic’s null distribution already for moderate sample sizes and allows us to avoid computationally more involved permutation analysis.

In detail, our proposed test is based on applying distance covariance to center-outward ranks and signs. We show that the test is consistent and distribution-free over the class of multivariate distributions with nonvanishing (Lebesgue) probability densities; see Section 2 for the precise definition of this class. The consistency is a consequence of a result of Figalli, (2018). In light of the prior work of Székely et al., (2007), Hallin, (2017), and Figalli, (2018), our major new discovery is the form of the limiting null distribution of the test statistic, which is established with all parameters given explicitly. To this end, we study the weak convergence of U-statistics with a “degenerate” kernel and dependent (permutation) inputs, and derive a general combinatorial non-central limit theorem (non-CLT) for double- and multiple-indexed permutation statistics. This theorem is new and of independent interest beyond our particular application of asymptotic calibration of the size of the independence test under .

As we were completing this manuscript, we became aware of an independent work by Deb and Sen, (2019) who also proposed a rank-distance-covariance-based independence test. Their preprint was posted a few days before ours and presents, in particular, a result very similar to our Theorem 3.1. The derivations differ markedly, however. Deb and Sen, ’s proof uses techniques based on characteristic functions, whereas we develop a general combinatorial non-CLT theorem for double- and multiple-indexed permutation statistics that can be applied to the considered statistic as well as possible modifications. There are further differences in the precise setup of multivariate ranks: while we base ourselves directly on recent work by Hallin, (2017) and by Figalli, (2018), Deb and Sen, (2019) considered transports to the unit cube rather than the unit ball (see Definition 2.2 below) and present weakened assumptions in the definition of the ranks.

The rest of the paper is organized as follows. Section 2 introduces center-outward ranks and signs, and Section 3 specifies the proposed test. Section 4 gives the theoretical analysis, including the combinatorial non-CLT and a study of the proposed test. Computational aspects are discussed in Section 5, and numerical studies of the finite-sample behavior of our test and an analysis of stock market data are presented in Section 6. All proofs are relegated to a supplement.

Notation.

The sets of real and positive integer numbers are denoted and , respectively. For , we define . We write and for the multiset consisting of (possibly duplicate) elements . We use and to denote sequences. A permutation of a multiset is a sequence , where is a bijection from to itself. The family of all distinct permutations of a multiset is denoted . The Euclidean norm of is written . We write and for the identity matrix and all-ones matrix in , respectively. For a sequence of vectors , we use as a shorthand of . For a function , we define . The greatest integer less than or equal to is denoted . The symbol stands for the indicator function. Throughout, and refer to positive absolute constants whose values may differ in different parts of the paper. For any two real sequences and , we write if there exists such that for all large enough, and if for any , holds for all large enough. The symbols , , and stand for the open unit ball, closed unit ball, and unit sphere in , respectively. We use and to denote convergence in distribution and almost surely. For any random vector , we use to represent its probability measure.

2 Center-outward ranks and signs

In this section, we introduce necessary background on center-outward ranks and signs. As in Hallin, (2017), we will be focused on the family of absolutely continuous distributions on that have a nonvanishing (Lebesgue) probability density (Definition 2.1 below). In what follows it is understood that the dimension could be larger than 1 and that all considered probability measures are fixed, and not to be changed with the sample size in particular.

Definition 2.1.

Let be an absolutely continuous probability measure on with (Lebesgue) density . Such is said to be a nonvanishing probability measure/distribution if for all there exist constants such that for all . We write for the family of all nonvanishing probability measures/distributions on .

The considered generalization of ranks to higher dimensions rests on the following concept of a center-outward distribution function, whose existence and almost everywhere uniqueness within the family is guaranteed by the Main Theorem in McCann, (1995, p. 310).

Definition 2.2 (Definition 4.1 in Hallin, , 2017).

The center-outward distribution function of a probability measure is the almost everywhere unique function that (i) is the gradient of a convex function on , (ii) maps to the open unit ball , and (iii) pushes forward to , where is the product of the uniform measure on (for the radius) and the uniform measure on the unit sphere . To be explicit, property (iii) requires for any Borel set .

If and we further have , then the center-outward distribution function of coincides with the -optimal transport from to (Villani, , 2009, Theorem 9.4), i.e., it is the almost everywhere unique solution to the following optimization problem,

| (2.1) |

where denotes the push forward of under map . In other words, the optimization is done over all Borel-measurable maps from to pushing forward to . Assuming further that the Caffarelli’s regularity conditions including compactness of support (Chernozhukov et al., , 2017, Lemma 2.1) hold, coincides with the Monge–Kantorovich vector rank transformation proposed in Definition 2.1 in Chernozhukov et al., (2017). Lastly, it can be easily checked that when , reduces to , where is the usual cumulative distribution function.

In dimension , the distribution function determines the underlying probability distribution . A natural question is then whether similarly preserves all information about a distribution when . That this is indeed the case turns out to be highly nontrivial, and was not resolved until very recently. The following proposition shows that is a homeomorphism from to except for a compact set with Lebesgue measure zero, indicating that all the information about the probability measure can be captured using . This proposition will play a key role in our later justification of the consistency of our proposed test (Theorem 3.2).

Proposition 2.1 (Theorem 1.1 in Figalli, , 2018; Propositions 4.1, 4.2 in Hallin, , 2017).

Let , with center-outward distribution function . Then,

-

(i)

is a probability integral transformation of , that is, iff ;

-

(ii)

The set is compact and of Lebesgue measure zero. The restrictions of and to and are homeomorphisms between and . If , then the set is a singleton, and and are homeomorphisms between and .

We now move on to estimation of based on independent copies of . The considered estimator mimics the empirical version of the Monge–Kantorovich problem (2.1), and the key step is to “discretize” the unit ball to grid points. In the following we sketch Hallin’s approach to the construction of such a grid point set, with a focus on how to form the grid points when . To this end, let us first factorize into the following form, whose existence is clear:

| (2.2) |

Next, consider intersection points between

-

–

the hyperspheres centered at with radii , and

-

–

distinct unit vectors .

The unit vectors in are selected such that the uniform discrete distribution on this set converges weakly to the uniform distribution on . For , we can choose unit vectors such that the unit circle is divided into equal arcs. For , the requirement is satisfied almost surely when independently drawing unit vectors from the uniform distribution on . Moreover, it is not difficult to give a deterministic construction that serves our purpose; see Section B in the supplement.

Definition 2.3.

When , the augmented grid is the multiset consisting of copies of the origin whenever and the intersection points . When , letting , , and , the augmented grid is the multiset consisting of the origin whenever and the points .

Proposition 2.2.

As long as the uniform discrete distribution on converges weakly to the uniform distribution on , the uniform discrete distribution on the augmented grid , which assigns mass to the origin and mass to every other grid point, weakly converges to .

We are now ready to introduce Hallin’s estimator, , of . It is defined via the optimal coupling between the observed data points and the augmented grid .

Definition 2.4 (Definition 4.2 in Hallin, , 2017).

Let be data points in . Let be the collection of all bijective mappings between the multiset and the augmented grid . The empirical center-outward distribution function is defined as

| (2.3) |

the center-outward rank of is defined as , and the center-outward sign of is defined as if , and otherwise.

The following two propositions from Hallin, (2017) give the Glivenko–Cantelli strong consistency and distribution-freeness of the empirical center-outward distribution function. Both shall play key roles for the limiting null distribution and asymptotic consistency of the test statistic that will be proposed in Section 3.

Proposition 2.3 (Glivenko–Cantelli, Proposition 5.1 in Hallin, , 2017, Theorem 3.1 in del Barrio et al., , 2018).

Let with center-outward distribution function , and let be i.i.d. with distribution with empirical center-outward distribution function . Then

| (2.4) |

when and (2.2) holds.

Proposition 2.4 (Distribution-freeness, Proposition 6.1(ii) in Hallin, , 2017, Proposition 2.5(ii) in Hallin et al., , 2020).

Let be i.i.d. with distribution . Let be their empirical center-outward distribution function. Then for any decomposition of , the random vector is uniformly distributed over . The latter set is comprised of all permutations of the multiset ; recall the notation introduced at the end of Section 1.

3 A distribution-free test of independence

This section introduces the proposed distribution-free test of in (1.1) built on center-outward ranks and signs. The main new methodological idea is simple: We propose to plug the calculated center-outward ranks and signs, instead of the original data, into the consistent test statistics presented in the introduction (Section 1). The distribution theory for the proposed test statistic, however, is non-trivial and requires new technical developments, which shall be detailed in Section 4.

To illustrate our idea, we will focus on one particular consistent test statistic in the sequel, namely, the distance covariance of Székely et al., (2007). Other choices including HSIC and more recent proposals like the ball covariance proposed in Pan et al., (2020) shall be discussed in Section 4 following the presentation of our general combinatorial non-CLT.

We begin with details on the distance covariance that are necessary to convey the main idea. We first introduce a representation of the associated measure of dependence.

Definition 3.1 (Distance covariance measure of dependence, Székely et al., (2007)).

Let and be two random vectors with , and let be an independent copy of . The distance covariance of is defined as

| (3.1) |

which is finite and uses the kernel function

| (3.2) |

and its analogue . Here and are independent and both follow the distribution .

The finiteness of in (3.1) was proved by Lyons, (2013, Proposition 2.3). It can be shown that under the same conditions as in Definition 3.1,

where are independent copies of and

see also Bergsma and Dassios, (2014, Sec. 3.4). Accordingly, we have an unbiased estimator of the distance covariance between and as follows.

Definition 3.2 (Sample distance covariance, Székely and Rizzo, (2013)).

Let be independent copies of with , , . The sample distance covariance is defined as

| (3.3) |

where

| (3.4) | ||||

The following is a direct consequence of Lemma 1 in Yao et al., 2018b .

Proposition 3.1.

We are now ready to describe our distribution-free test of independence, which combines distance covariance with center-outward ranks and signs.

Definition 3.3 (The proposed distribution-free test statistic).

Let be independent copies of with and . Let and be the empirical center-outward distribution functions for and . We define the test statistic

| (3.5) |

By Proposition 2.4, the statistic is distribution-free under the independence hypothesis in (1.1). Hence, an exact critical value for rejection of can be approximated via Monte Carlo simulation. Numerically less demanding, one could instead adopt the critical value based on the limiting null distribution of derived from the following theorem.

Theorem 3.1 (Limiting null distribution).

Let be independent copies of with and , and and are independent. Then we have

| (3.6) |

as and (2.2) holds, where , , are the non-zero eigenvalues of the integral equation

| (3.7) |

in which and are defined as in (3.2), and are independent, and is a sequence of independent standard Gaussian random variables.

Remark 3.1.

In Section 4 we will prove Theorem 3.1 rigorously. Intuitively, it is helpful to first consider the following “oracle” test statistic :

where and denote the center-outward distribution functions of and , respectively. The infeasibility stems from the use of the (population) center-outward distribution functions. One can easily verify using the asymptotic theory of degenerate U-statistics that under the null

where and are defined as in Theorem 3.1. Somewhat surprising to us, the limiting null distribution of is exactly the same as that of .

Therefore, for any pre-specified significance level , our proposed test is hence

| (3.8) |

Consequently, by Theorem 3.1,

| (3.9) |

It should be highlighted that, thanks to distribution-freeness, given any fixed dimensions and , the asymptotically small term in (3.9) is independent of the underlying distributions, and converges to zero uniformly over all the underlying distributions with , , and independent of . The values of ’s, and hence also the critical value itself, are distribution-free and only depend on the dimensions and . The critical value may thus be calculated using numerical methods for each pair of and . Details will be described in Section 5.2. Table C.1 in the supplement further records the critical values at significance levels for with accuracy .

Due to (i) the near-homeomorphism property of the center-outward distribution function shown in Proposition 2.1; (ii) the strong Glivenko-Cantelli consistency of empirical center-outward distribution functions shown in Proposition 2.3; and (iii) the fact that the distance covariance measure of dependence is zero if and only if holds under finiteness of marginal first moments (Lyons, , 2013, Theorem 3.11), it holds that is asymptotically consistent and the corresponding test is consistent. This fact is summarized in the following theorem.

Theorem 3.2 (Consistency).

Let be independent copies of , where with center-outward distribution function , and with center-outward distribution function . We then have, as long as and (2.2) holds,

| (3.10) |

where with equality if and only if and are independent. In addition, under any fixed alternative , we obtain if and (2.2) holds, and thus

| (3.11) |

We conclude this section with one more remark that discusses an interesting connection between the proposed test and a famous dependence measure, Blum–Kiefer–Rosenblatt’s dependence measure (Blum et al., , 1961), when .

Remark 3.2.

In the univariate case (), the statistic is actually (up to a constant) a consistent estimator of Blum–Kiefer–Rosenblatt’s measure of dependence (Blum et al., , 1961). In detail, Theorem 3.2 has shown that . When and are both absolutely continuous, Bergsma, (2006, Lemma 10) showed that

where denotes the cumulative distribution function of . This implies that

The right-hand side is Blum–Kiefer–Rosenblatt’s and converges to it almost surely.

4 Theoretical analysis

This section provides the theoretical justification for the test in (3.8). By Proposition 2.4, both and are generated from uniform permutation measures. In view of Definition 3.3, it is hence clear that under the test statistic is a summation over the product space of two uniform permutation measures, which belongs to the family of permutation statistics.

The study of permutation statistics can be traced back at least to Wald and Wolfowitz, (1944), who proved an asymptotic normality result for single-indexed permutation statistics of the form . Here and are vectors that are possibly varying with , and is uniformly distributed on . Later, Noether, (1949), Hoeffding, (1951), Motoo, (1957), and Hájek, (1961), among many others, generalized Wald and Wolfowitz, ’s results in different ways, and Bolthausen, (1984) gave a sharp Berry–Esseen bound for such permutation statistics using Stein’s method.

Double-indexed permutation statistics, of the form with and as matrices possibly varying with , are more difficult to tackle. They were first investigated by Daniels, (1944), who gave sufficient conditions for asymptotic normality. Later, various weakened conditions were introduced in, e.g., Bloemena, (1964, Chap. 4.1), Jogdeo, (1968), Abe, (1969), Cliff and Ord, (1973, Chap. 2.4), Shapiro and Hubert, (1979), Barbour and Eagleson, (1986), Pham et al., (1989), and the Berry–Esseen bound was established in Zhao et al., (1997), Barbour and Chen, (2005), and Reinert and Röllin, (2009).

Despite this vast literature, there is a notable absence of results on permutation statistics which, as its degenerate U-statistics “cousins”, may weakly converge to a non-normal distribution. Our analysis of , however, hinges on such a combinatorial non-CLT. In the following, we present two general theorems that fill the gap.

Before stating the two theorems, we introduce some notions needed. For each , let be a random vector taking values in , a compact subset of . We consider triangular arrays , for , such that the random variables with uniform discrete distributions on the respective multisets , denoted by , weakly converge to as . We further introduce an independent copy of , denoted , and independent copies of the , denoted . Finally, for and , let be real-valued functions, the former of which may change with .

Our first theorem is then focused on double-indexed permutation-statistics of the form

| (4.1) |

where is uniformly distributed on .

Theorem 4.1.

Assume that for each , the functions , and satisfy the following conditions:

-

(i)

each is symmetric, i.e., for all ;

-

(ii)

the family , , is equicontinuous;

-

(iii)

each is non-negative definite, i.e.,

for all , , ;

-

(iv)

each has ;

-

(v)

each has ;

-

(vi)

as , the functions converge uniformly on to , with .

It then holds that

as , where , are i.i.d. standard Gaussian, and the , are eigenvalues of the Hilbert-Schmidt integral operator given by , i.e., for each the ’s solve the integral equations

for a system of orthonormal eigenfunctions .

Theorem 4.1 provides the essential component of our analysis for . However, is a permutation statistic that is not double- but quadruple-indexed. To cover this case, we have to extend Theorem 4.1 to multiple-indexed permutation statistics, the study of which is much more sparse (see, for example, Raic̆, (2015) for some recent progresses). Further notation is needed.

For all , let be a vector with , for . Let be a symmetric kernel of order , i.e., for all permutations and . For any integer , and any measure , we let

where are independent random vectors with distribution .

The next theorem treats a multiple-indexed permutation-statistic of order defined as

| (4.2) |

where is uniformly distributed on , and the triangular arrays are as introduced before the statement of Theorem 4.1.

Theorem 4.2.

With the aid of Theorem 4.2, we are now ready to prove Theorem 3.1, which presents the limiting null distribution of . In our context, , , , and is the kernel defined in (3.4). The multisets and are taken to be and , respectively. Accordingly, follows the uniform discrete distribution over , denoted by , and has a uniform discrete distribution over , denoted by . The functions , , , and can be chosen as , , , and , defined in the manner of (3.2), respectively.

We now verify properties (I)–(III). Write and . Notice that the kernel is symmetric and continuous on . We have

| and |

by Yao et al., 2018a (, Sec. 1.1). Moreover, the is symmetric, non-negative definite (Lyons, , 2013, p. 3291), and equicontinuous since

One can verify that , and converges uniformly to by combining the pointwise convergence using the Portmanteau Lemma (van der Vaart, , 1998, Lemma 2.2) and the equicontinuity of (Rudin, , 1976, Exercise 7.16). The similar results hold for and . Lastly, under , and are independent with margins uniformly distributed on and , respectively. Hence our statistic is distributed of the form (4.2).

In summary, Theorem 4.2 can be applied to the statistic and we have accordingly proven Theorem 3.1 rigorously. Furthermore, although our focus is on the combination of center-outward ranks and signs with the distance covariance statistic, the general form of our combinatorial non-CLTs (Theorems 4.1 and 4.2) also yields the limiting null distributions for test statistics based on plugging center-outward ranks and signs into HSIC-type or ball-covariance statistics (Gretton et al., 2005c, ; Gretton et al., 2005a, ; Gretton et al., 2005b, ; Pan et al., , 2020). We omit the details for these analogies.

5 Computational aspects

In this section, we describe the practical implementation of our test. To perform the proposed test, for any given , we fix a factorization such that

First, we need to compute and as defined in (2.3). This is an assignment problem and will be discussed in Section 5.1. After obtaining and , the test statistic in (3.5) can be computed using Equation (3.3) in Huo and Székely, (2016) in time. Second, we have to calculate the critical value defined in (3.8). This value can be estimated numerically, as detailed in Section 5.2. We have also provided the critical values at significance levels for with accuracy in Table C.1 in the supplement.

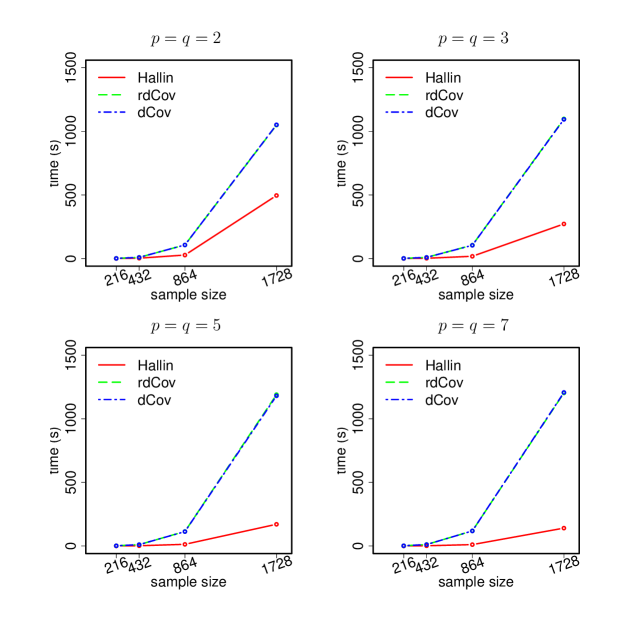

As shall be shown soon, the total computation complexity of our proposed test is in various cases. To contrast, to implement the distance covariance based test for instance, one has a time complexity , with representing the number of permutations. For many choices of , our test will have a clear computational advantage.

5.1 Assignment problems

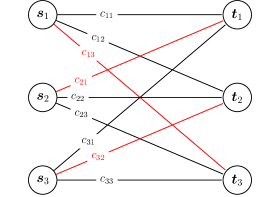

Problem (2.3) amounts to a linear sum assignment problem (LSAP), a fundamental problem in linear programming and combinatorial optimization. We define LSAP through graph theory. Consider a weighted (complete) bipartite graph with , , , where in Problem (2.3), and . The edge between and , denoted by , has a nonnegative weight , . We want to find an optimal matching, i.e., a subset of edges such that each vertex is an endpoint of exactly one edge in this subset with a minimum sum of weights of its edges; see Figure 5.1 for an illustration of , where edges in the optimal matching are marked in red.

We introduce some terms to state the theorem below. A perfect matching is a subset of edges such that each vertex is incident to exactly one edge. The total weight of a perfect matching is the sum of weights of the edges in this matching. A perfect matching is called -approximate for if its total weight is no larger than times the total weight of the optimal matching.

Theorem 5.1 (Gabow and Tarjan, (1989), Sharathkumar and Agarwal, (2012), Agarwal and Sharathkumar, (2014)).

Assume that points , have bounded integer coordinates, and that the squared distances are all bounded by some integer . Then there exists an algorithm to find the optimal matching in time. Furthermore,

-

(i)

if , there exists an exact algorithm for computing the optimal matching in time for any arbitrarily small constant ;

-

(ii)

if , there is an algorithm to compute a -approximate perfect matching in

time, where depending on is small.

In the supplement we will describe the algorithm developed by Gabow and Tarjan, (1989) under the basic settings. It is essentially the combination of the Hungarian method (Kuhn, , 1955, 1956; Munkres, , 1957) and the algorithm of Hopcroft and Karp, (1973). We will ignore the details of the faster exact algorithm for by Sharathkumar and Agarwal, (2012) and the approximate algorithm for by Agarwal and Sharathkumar, (2014); both algorithms improve the Gabow–Tarjan algorithm by exploiting the geometric structure of the weight matrix.

5.2 Eigenvalues and quadratic forms in normal variables

In Theorem 3.1, , are non-zero eigenvalues (counted with multiplicity) of the integral equation

Under the independence hypothesis , the eigenvalues , are given by all the products , where , and , are the non-zero eigenvalues of the integral equations

respectively (Nandy et al., , 2016, Lemma 4.2). The non-zero eigenvalues of integral equation with are given by

We are not aware of any closed form formulas for the eigenvalues when . However, in practice, the non-zero eigenvalues can be numerically estimated by the non-zero eigenvalues of the matrix

denoted by , where , , and , are points in the grid . Here are all negative (Lyons, , 2013, p. 3291). For , we take . We can obtain eigenvalues based on the grid similarly. Then we sort the positive products into a descendingly ordered sequence , and have the following theorem.

Theorem 5.2.

Let and be eigenvalues as defined in Theorem 3.1 and above, respectively. Let be a sequence of independent standard Gaussian random variables. Then it holds for any pre-specified significance level that

as and , where and are the quantiles of

respectively.

Consequently, we can approximate the quantile of quadratic form by estimating that of quadratic form for a sufficiently large . The latter is done by solving the inverse of the cumulative distribution function of quadratic form , which can be numerically evaluated using Farebrother, ’s (1984) algorithm or Imhof, ’s (1961) method.

6 Numerical studies

This section compares the performances of our tests using (i) the theoretical rejection threshold defined in (3.8) and computed using the approximation in Section 5.2, and (ii) a Monte Carlo simulation-based rejection threshold to the existing tests of independence that use (iii) distance covariance with marginal ranks (Lin, , 2017), and (iv) distance covariance (Székely and Rizzo, , 2013).

The test via distance covariance with marginal ranks proceeds as follows. Write for . Let be the rank of among for each . The marginal rank (vector) of is defined as . The marginal rank (vector) of is defined similarly. Then we run the permutation-based distance covariance test on the marginal ranks instead of the original data.

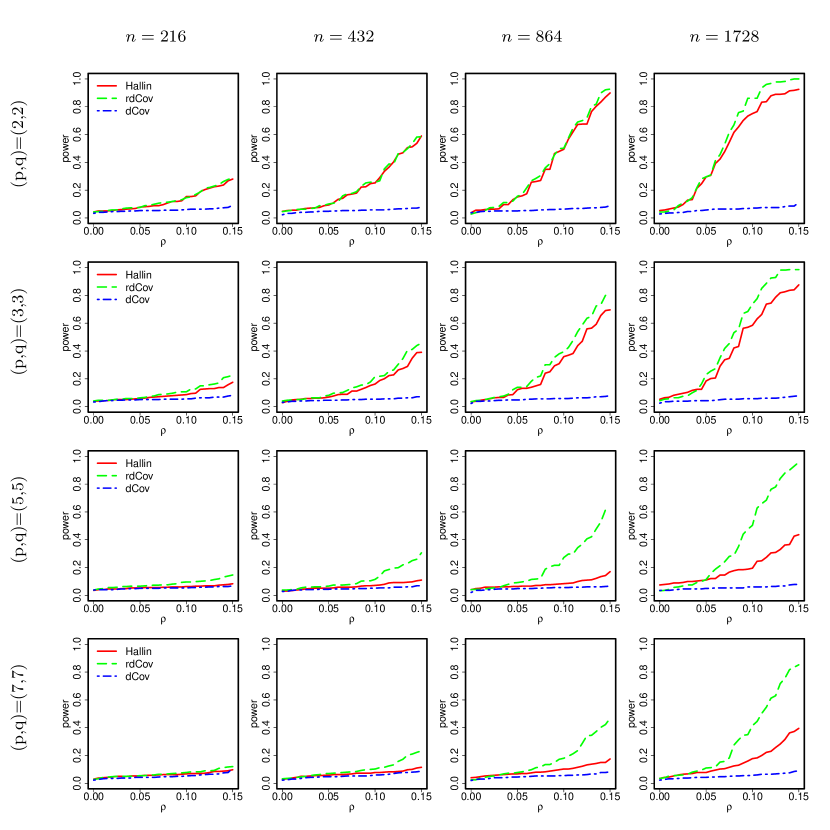

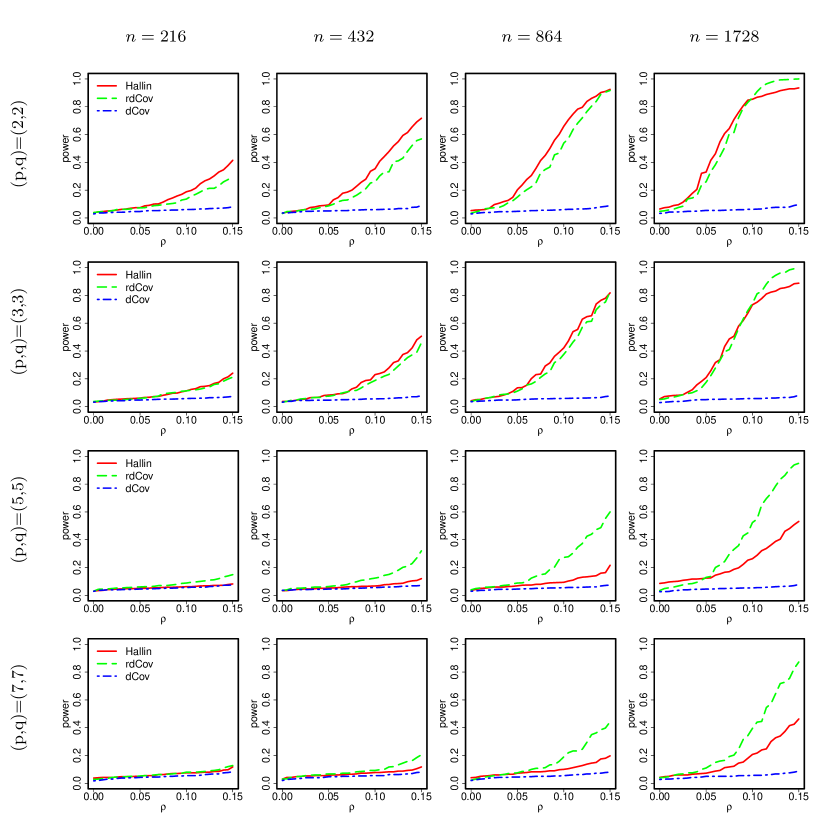

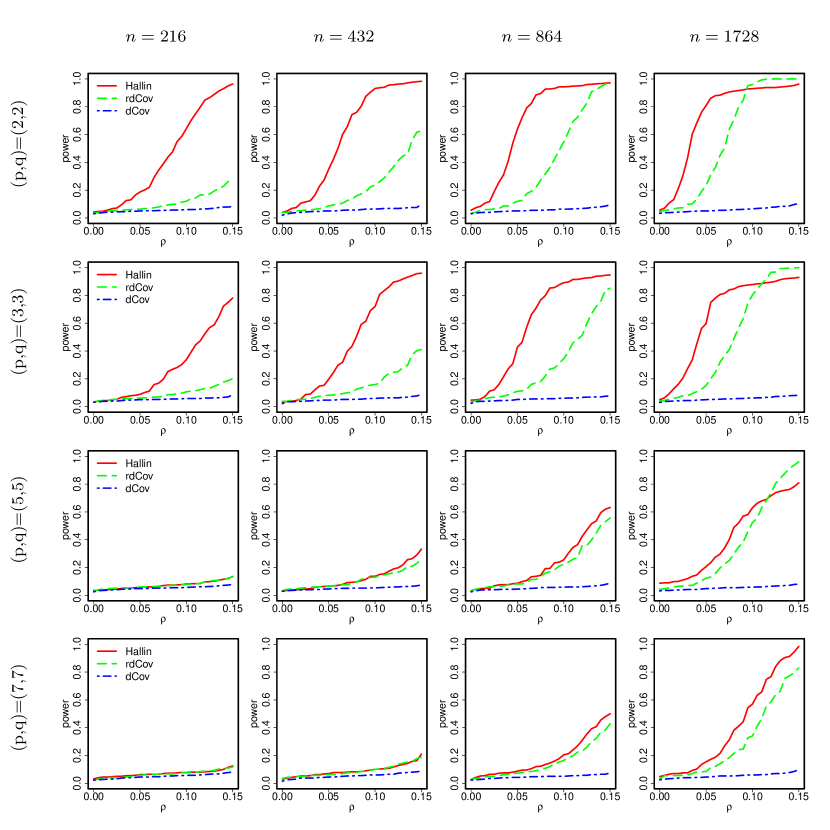

6.1 Simulation results

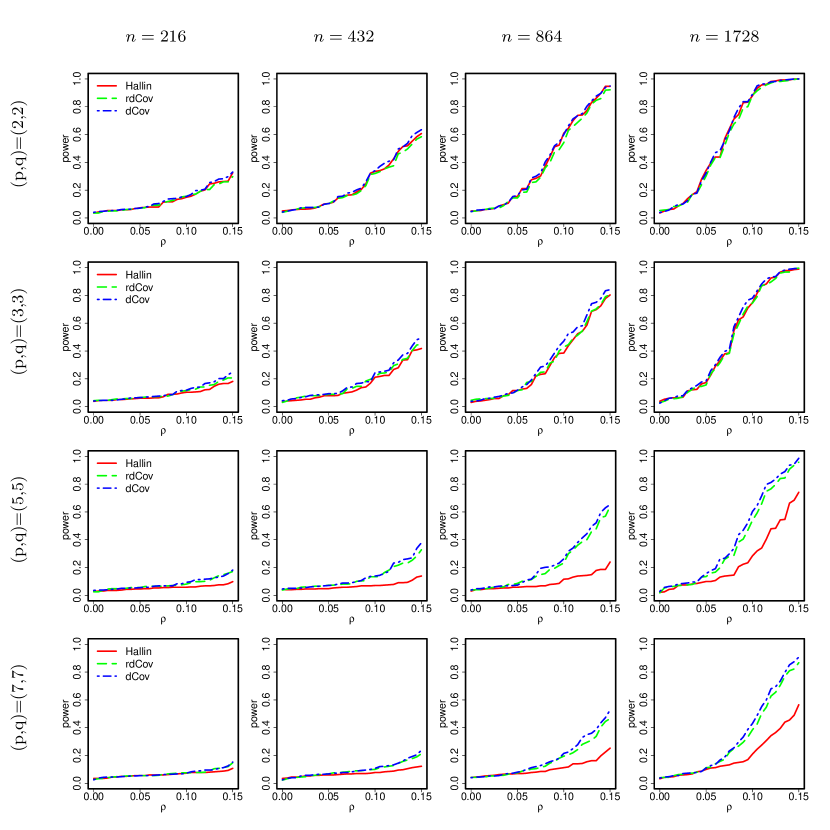

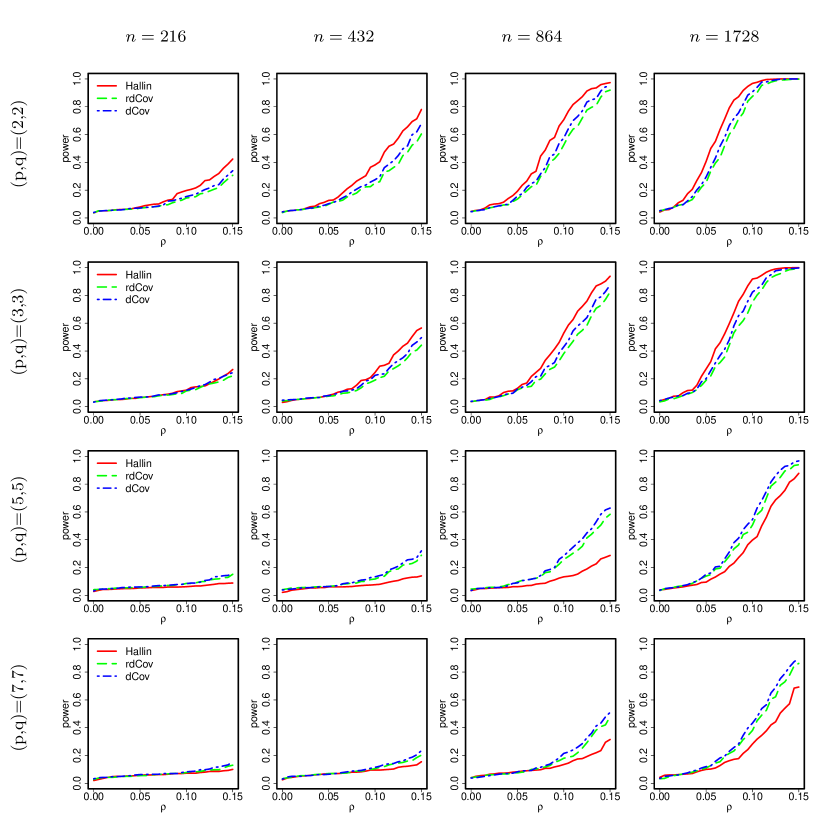

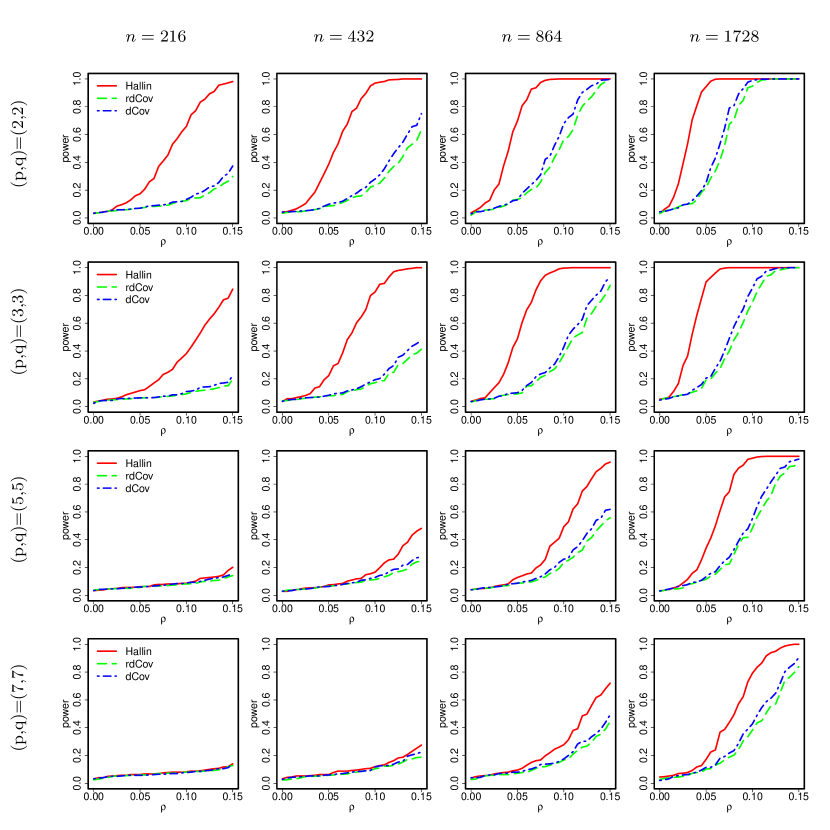

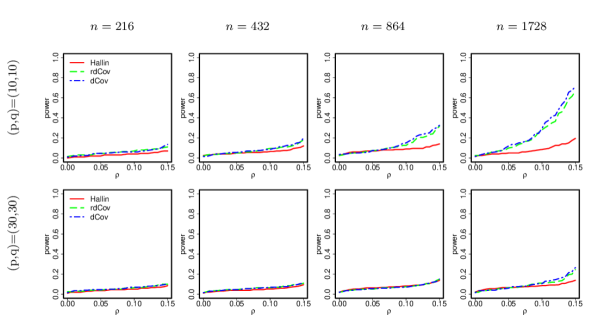

We first conduct Monte Carlo simulation experiments on the finite-sample performance of the proposed test from Section 3. We evaluate the empirical sizes and powers of the four competing tests stated above for both Gaussian and non-Gaussian distributions. The values reported below are based on simulations at the nominal significance level of , with sample size , dimensions , and correlation . More simulation studies on even higher dimensions of and 30 are presented in the supplement, Section C. For tests (iii) and (iv), we resample times in the permutation procedure.

Example 6.1.

The data are independently drawn from , which follows a multivariate normal distribution with mean zero and covariance matrix (where and is the -th standard basis vector in -dimensional space, i.e., all entries are zero except for the one at the -th position) with (a) ; (b) ; and (c) .

Example 6.2.

The data are independently drawn from , which is given by , and , , where stands for the quantile function for Student’s -distribution with degree of freedom (Cauchy distribution), and are generated as in Example 6.1.

| Hallin(t) | Hallin(s) | rdCov | dCov | ||

| 0.040 | 0.043 | 0.043 | 0.045 | ||

| 0.037 | 0.047 | 0.048 | 0.050 | ||

| 0.045 | 0.045 | 0.050 | 0.048 | ||

| 0.054 | 0.054 | 0.061 | 0.057 | ||

| 0.047 | 0.047 | 0.058 | 0.053 | ||

| 0.047 | 0.053 | 0.045 | 0.043 | ||

| 0.040 | 0.047 | 0.053 | 0.048 | ||

| 0.049 | 0.049 | 0.043 | 0.050 | ||

| 0.040 | 0.043 | 0.040 | 0.048 | ||

| 0.033 | 0.043 | 0.048 | 0.043 | ||

| 0.047 | 0.050 | 0.040 | 0.048 | ||

| 0.059 | 0.059 | 0.053 | 0.039 | ||

| 0.068 | 0.048 | 0.053 | 0.056 | ||

| 0.064 | 0.050 | 0.054 | 0.053 | ||

| 0.056 | 0.051 | 0.048 | 0.046 | ||

| 0.052 | 0.054 | 0.048 | 0.052 |

In these two examples, the independence hypothesis holds when . We first report the empirical sizes of all four considered tests, presented in Table 6.1. It can be observed that the proposed tests with either rejection threshold as well as their two competitors control the size effectively.

The empirical powers for Examples 6.1–6.2 are summarized in Figures 6.2–6.7. For the proposed test, we present results only for the theoretical rejection threshold as the results for the simulation-based threshold are similar and hence omitted.

Several facts are noteworthy. First, when the sample size is large and the dimension is relatively small, throughout all settings the performance of the proposed test is not much worse than the two competing ones. It should be highlighted that our method achieves this performance with smaller computational time, as shown in Figure 6.8 and also confirmed in our theoretical analysis of computational cost. Second, the proposed test beats the other two when the within-group correlation is high, i.e., as becomes larger from the setting (a) to (c), even when the dimension is high. Third, for heavy-tailed distributions, the tests via distance covariance with center-outward ranks and signs and marginal ranks perform better than the original distance covariance test. Lastly, compared to its competitors, the proposed test appears to be more sensitive to dimension. This is as expected.

6.2 Real stock market data analysis

We analyze the monthly log returns of daily closing prices for stocks that are constantly in the Standard & Poor 100 (S&P 100) index during the time period 2003 to 2012. The data are from Yahoo! Finance (finance.yahoo.com), and the stocks are classified into 10 sectors by Global Industry Classification Standard (GICS). Stock market data tend to be heavy-tailed with many outliers, and monthly log returns may reasonably be modeled as independent and identically distributed random variables. The time period we analyzed includes some well known turbulent stretches like the 2007-08 financial crisis, which, however, could be either explained using heavy-tailed (e.g., elliptical or stable) distribution models or captured as outliers.

In this section we limit our scope and focus on detecting between-group dependence between two sectors in S& P 100 that contain a rather small number of stocks: (1) Telecommunication, including stocks “AT&T Inc [T]” and “Verizon Communications [VZ]”; and (2) Materials, including stocks “Du Pont (E.I.) [DD]”, “Dow Chemical [DOW]”, “Freeport-McMoran Cp & Gld [FCX]”, and “Monsanto Co. [MON]”. We then consider detection of possible dependence between the Telecommunication sector and any two stocks in the Materials sector.

To this end, we apply the three considered tests to the monthly log returns of (T,VZ) coupled with either (DD,DOW), or (DD,FCX), or (DD,MON), or (DOW,FCX), or (DOW,MON), or (FCX,MON). The p-values for these three tests are reported in Table 6.2. There, one observes that using the proposed test yields uniformly the strongest evidence to conclude the existence of dependence between (T,VZ) and any two stocks in the Materials sector.

| (DD,DOW) | (DD,FCX) | (DD,MON) | (DOW,FCX) | (DOW,MON) | (FCX,MON) | ||

| Hallin | (T, VZ) | 0.001 | 0.005 | 0.002 | 0.004 | 0.001 | 0.065 |

| rdCov | (T, VZ) | 0.002 | 0.013 | 0.005 | 0.009 | 0.002 | 0.070 |

| dCov | (T, VZ) | 0.002 | 0.018 | 0.003 | 0.012 | 0.002 | 0.101 |

Acknowledgments

We thank the co-editor Hongyu Zhao, the anonymous associate editor, and two anonymous referees for their very detailed and constructive comments and suggestions, which have helped greatly to improve the quality of the paper.

Appendix A Proofs

Further concepts concerning U-statistics are needed. For any symmetric kernel , any integer , and any probability measure , we remind the definition of

and write

| (A.1) |

where are independent random variables with law and . We also have

| (A.2) |

for any (possibly dependent) random variables . This is the Hoeffding decomposition with respect to .

Additional notation.

Let denote . The cardinality of a set is written . For a multiset and , an -permutation of is a sequence , where is a bijection from to itself. For , let denote the family of all possible -permutations of set . For , let denote the positive part of . Let and denote the Hadamard product and dot product of two vectors , respectively. We use to denote convergence in probability. We use to represent the imaginary unit.

A.1 Proofs for Section 2 of the main paper

A.1.1 Proof of Proposition 2.2

Proof of Proposition 2.2.

We first prove the case and then generalize to . For simpler presentation, let denote the uniform measure (distribution) on the augmented grid , let denote the uniform measure on the points , and let denote the uniform measure on the points . Furthermore, let denote the uniform measure on , and let denote the uniform measure over the unit sphere .

If , then is the product measure of (for the radius) and (for the unit sphere). By assumption, weakly converges to as . Moreover, weakly converges to as by the following argument:

as . Combining these facts, and applying Theorem 2.8 in Billingsley, (1999) to the separable space , we deduce that , the product measure of and , weakly converges to as .

If , we compare the uniform measure on the augmented grid (denoted by ) and that on . For any -continuity set , we obtain

Therefore,

| (A.3) |

where the last step follows by noticing

as . We have proven in the case that weakly converges to and then . This, together with (A.3), proves that for any -continuity Borel set , and equivalently, weakly converges to as . ∎

A.2 Proofs for Section 3 of the main paper

A.2.1 Proof of Proposition 3.1

Proof.

The equivalence of these three versions of the sample distance covariance is well known; we include a proof for completeness but claim no originality here.

The sample distance covariance defined in Székely and Rizzo, (2013) and Székely and Rizzo, (2014) can be described as follows. First define

Similarly, we introduce the distances , and define the sums , and corresponding , in analogy to the quantities for the . Then the sample distance covariance from Definition 1 in Székely and Rizzo, (2013) is

| (A.4) |

and the sample distance covariance from Equation (3.2) in Székely and Rizzo, (2014) is

| (A.5) |

We first prove the equivalence between (A.4) and (A.5). Lemma 3.1 in Huo and Székely, (2016) gives that the right-hand side of (A.5) equals to

| (A.6) |

It remains to prove that the right-hand side of (A.4) equals to (A.6) as well, which can be established by straightforward calculation following the proof of Lemma 3.1 in Huo and Székely, (2016). First, one can verify the following equalities:

| (A.7) | ||||

| (A.8) | ||||

| (A.9) | ||||

| (A.10) | ||||

| (A.11) |

Next, we may simplify the right-hand side of (A.4). We have

where

| (A.12) | ||||

| (A.13) |

Furthermore, we have

| and |

Plugging all these equalities above into (A.12) and (A.13) completes the proof.

The equivalence between (A.5) and (3.3) is an immediate consequence of Lemma 1 in Yao et al., 2018b , which shows that (A.5) is equivalent to

| (A.14) |

where

By expanding the above summation, one obtains that (A.14) is equivalent to

| (A.15) |

where

Next, by expanding the summation again, we have (A.15) is equivalent to (3.3).

A.2.2 Proof of Theorem 3.1

Proof of Theorem 3.1.

This theorem is a corollary of Theorem 4.2, which we prove in Section A.3.2. In our context, , , , and is the kernel defined in (3.4). The multisets and are taken to be and , respectively. Accordingly, follows the uniform discrete distribution over , denoted by , and has a uniform discrete distribution over , denoted by . The functions , , , and can be chosen as , , , and , defined in the manner of (3.2), respectively. Recall that

| (A.17) |

with their analogues and . Here and are independent with law , and and are independent with law .

We verify the conditions in Theorem 4.2 as follows. Proposition 2.2 shows that and converge in distribution to and , respectively. We also have that (I) the kernel is symmetric and continuous on , and thus ; (II) ; (III)

Next we verify Assumptions (i)–(vi) for and . It can be easily seen that is symmetric (Assumption (i)), and has (Assumption (iv)) and (Assumption (v)) by Székely et al., (2007, Theorem 4(i)). Lyons, (2013, p. 3291) has proved that functions are non-negative definite (Assumption (iii)). We have is equicontinuous (Assumption (ii)) since

and moreover, It remains to prove that converges uniformly to (Assumption (vi)). Using the portmanteau Lemma (van der Vaart, , 1998, Lemma 2.2) and Proposition 2.2, we have for all ,

and thus converges pointwisely to . Then the uniform convergence follows from the equicontinuity of (Rudin, , 1976, Exercise 7.16). Assumptions (i)–(vi) can be similarly verified for and as well.

Lastly, using Proposition 2.4, and are uniformly distributed on and , respectively. In addition, under , and are independent. Hence our statistic is distributed as

where and are uniformly distributed on and independent, and thus the same as the form (4.2) by defining permutation for which subject to and for some . ∎

A.2.3 Proof of Theorem 3.2

Proof of Theorem 3.2.

We begin by proving the first claim (3.10). Let , , , denote , , , , respectively. Write , , and . The main idea here is to bound

Recall that

where

and Using the inequality

where could be duplicate, we deduce from (A.2.3) that

| (A.19) |

This implies

| (A.20) |

Applying Proposition 2.3 (Glivenko–Cantelli) to (A.20) yields that

| (A.21) |

This together with

the strong consistency of (Jakobsen, , 2017, Theorem 5.5), yields

Next we prove the second claim. It has been proved by Székely et al., (2007, Theorem 3(i)) that and equality holds if and only if and are independent. It remains to show that (a) the independence of and , is equivalent to (b) the independence of and . It is obvious that (b) implies (a). Then we prove (a) implies (b). For any Borel sets and , using Proposition 2.1(ii) and Definition 2.1, we deduce

and thus

| (A.22) |

We can similarly obtain

| (A.23) |

It follows that

A.3 Proofs for Section 4 of the main paper

A.3.1 Proof of Theorem 4.1

We first state the following properties of the limiting functions:

Lemma A.1.

The limiting functions , , satisfy:

- (i’)

-

is symmetric, i.e., for all ;

- (ii’)

-

is continuous;

- (iii’)

-

is non-negative definite;

- (iv’)

-

;

- (v’)

-

.

Proof of Lemmma A.1.

Given Assumption (vi), Properties (i’) and (iii’) readily follow from Assumptions (i) and (iii), respectively. Property (ii’) follows from Assumptions (ii) and (vi) by Theorem 7.12 in Rudin, (1976). Property (iv’) holds by noticing by Property (ii’) and the portmanteau lemma (van der Vaart, , 1998, Lemma 2.2), and

where the first step is by Assumption (iv), and the last step is due to Assumption (vi). For Property (v’), has been assumed in Property (vi), and since is compact and Property (ii’). ∎

Proof of Theorem 4.1.

The proof is divided into two steps. The first step consists of defining a “truncated” version of and finding the limiting distribution of . The second step is to bound the difference between and and then derive the limiting distribution of . To this end, we do some preliminary work. Using the Hilbert–Schmidt theorem (Simon, 2015a, , Theorem 3.2.1, Example 3.1.15), admits the following eigenfunction expansion by Assumptions (i) and (v),

where are all the non-zero eigenvalues of the integral equation

with by Assumption (iii), and orthonormal eigenfunctions are such that

| (A.24) |

Since the constant function is an eigenfunction associated with eigenvalue by Assumption (iv), using the orthogonality between and the constant function (Simon, 2015a, , Theorem 3.2.1) yields

| (A.25) |

We also define as all the non-zero eigenvalues of the integral equation with by Property (iii’), and orthonormal eigenfunctions are such that Denote , , and .

Step I. By Theorem 4.11.8 in Simon, 2015b , we may write

For each integer , we define the “truncated” permutation statistic

and derive the limiting distribution of as . Notice that can be written as

We separately study the two terms on the right-hand side of (A.3.1), starting from the first term. We first establish that, for any fixed , the random vector

has a mean of and a variance-covariance matrix of . We have for ,

| (A.26) |

where the last step uses (A.25). For and , it holds that

| (A.27) |

Moreover, we deduce from (A.27) and (A.26) that

| (A.28) |

where the penultimate step uses (A.24) and (A.25). Combining (A.26) and (A.28) confirms the claim that the mean and the variance-covariance matrix of are and , respectively.

This claim about allows us to use the multivariate Berry–Esséen theorem for permutation statistics (Bolthausen and Götze, , 1993, Theorem 1). Specifically, we present the version revised by Raic̆, (2015, p. 3). Define as a standard -dimensional Gaussian random vector with independent univariate standard Gaussian entries

and as the family of all measurable convex sets in . We obtain that for all , there exists a universal constant such that

| (A.29) |

where the last step is due to the facts that is fixed and that for each and any fixed , as we will show in Lemma A.2(b). Notice that for any , the set is a convex subset of . It follows that , and thus, by Slutsky’s theorem (van der Vaart, , 1998, Theorem 2.8). On the other hand, since

| (A.30) |

by Lemma A.2(a), we have where

We find using the generalized Slutsky’s theorem (as a consequence of Theorem 2.7 in van der Vaart, , 1998, p.10–11) that

| (A.31) |

recognizing the function for as continuous. This completes the analysis of the first term in (A.3.1).

We turn to the second term in (A.3.1). Denoting by , we have by Theorem 2 in Hoeffding, (1951),

| (A.32) | ||||

| (A.33) |

where the last step in (A.33) uses Lemma A.2(b). Therefore, we have

| (A.34) | ||||

| (A.35) |

where the first step in (A.35) applies Minkowski’s inequality (Billingsley, , 1995, p. 242) and the last step is based on (A.30) and (A.33). By DeGroot and Schervish, (2012, Exercise 4.3.5), it follows that

Here the second last step uses (A.34), and the last step is based on (A.30) and (A.35). Hence for the second term in (A.3.1), we have

| (A.37) |

Putting the two pieces (A.31) and (A.37) together, and using Slutsky’s theorem once again, we have

| (A.38) |

This completes Step I.

Step II. We will prove starting from (A.38). Following arguments of Serfling, (1980, Chap. 5.5.2), we first control . Letting

we have

Equations (2.2)–(2.3) in Barbour and Eagleson, (1986) give

| (A.39) | ||||

| (A.40) |

where for ,

To further bound (A.40), we apply the following inequalities for :

Using the inequalities we deduce that for all ,

| (A.41) |

Combining (A.39) and (A.41), we find that for ,

| (A.42) |

We next verify that can be made arbitrarily small for all large enough and all with possibly depending on . Fix any small . The first term in (A.42) is smaller than as long as is large enough, since

by Properties (i’)–(iii’) and Mercer’s theorem (Simon, 2015a, , Theorem 3.11.9(b)). In view of (A.30), the second term in (A.42) will be smaller than for each fixed and all , where may depend on . For the third term, combining the facts that by the portmanteau lemma (van der Vaart, , 1998, Lemma 2.2), and that

by Assumption (vi), we deduce for , that as . Recalling Assumptions (i)–(iii) and Properties (i’)–(iii’), it holds by Mercer’s theorem once again (Simon, 2015a, , Theorem 3.11.9(b)) that

which is smaller than for large enough. Adding these three terms together yields the result.

We are now ready to prove using Lévy’s continuity theorem (Billingsley, , 1995, Theorem 26.3). We have

| (A.43) |

In the last inequality, the first term arises from the bound , and the last term is due to Equation (4.3.10) in Koroljuk and Borovskich, (1994). Fix , and let arbitrarily small be given. We have proven that there exists such that for all and all , where may depend on , it holds that . We can find such that for all because by Property (v’). Taking , we can choose so that for all since (A.38) holds for . Then for all ,

and the proof of the theorem is complete. ∎

Lemma A.2.

For each and any fixed , we have (a) as ; (b) .

Proof of Lemma A.2.

We employ results in Atkinson, (1967). Consider the Banach space of all continuous functions on equipped with the sup norm . Define operators and on for each as

We first verify the three assumptions stated in Atkinson, (1967, Sect. 1):

- (1)

-

and are linear operators on Banach space into itself;

- (2)

-

for each ;

- (3)

-

is collectively compact, i.e., the set

has compact closure.

Note that Assumptions (2) and (3) together imply that the operator is compact (Anselone, , 1971, Chap. 1.4). Assumption (1) is obvious by Property (ii’) and Assumption (ii). We now verify Assumption (2). For each fixed and any fixed , the product yields a bounded and continuous function, and it follows from the portmanteau lemma (van der Vaart, , 1998, Lemma 2.2) that as . Since is continuous, we have . We also have

| (A.45) |

where the last step uses Assumption (vi); hence . Now, Assumption (2) holds by Theorem 7.9 and Exercise 7.16 in Rudin, (1976) and the fact that the family of functions is equicontinuous for each fixed , which can be shown via the following argument. Given any small , there exists such that implies by Assumption (ii) that for all , where , and thus implies

| (A.46) |

For Assumption (3), observe that the set is bounded and equicontinuous by (A.46), and thus has compact closure by the Arzelà–Ascoli theorem (Simon, 2015a, , Theorem 1.5.3).

To prove assertion (a) of the present lemma, we may apply Theorems 2 and 3 in Atkinson, (1967) to obtain that for any fixed , as .

The proof of (b) is separated into two parts. In the first part, we show that for each and any fixed , the are uniformly upper bounded for all sufficiently large . Applying Theorem 4 in Atkinson, (1967) yields that, for any small , there exists a sufficiently large such that for each , there exists a (not necessarily unique) eigenfunction with , , and

Invoking Properties (i’)–(iii’), Theorem 3.a.1 in König, (1986) guarantees that there exists an absolute constant such that for all , and therefore

This together with implies that

| (A.47) |

In order to prove that the are uniformly upper bounded for any fixed and all large enough, it suffices to control the right-hand side of (A.47). Consider an orthonormal basis associated with eigenvalue : , where is finite since

by Properties (i’)–(iii’) and Mercer’s theorem (Simon, 2015a, , Theorem 3.11.9(b)). Then can be represented by

First, notice that there exists such that for all ,

using the continuity of the eigenfunctions , which holds by Property (ii’) and Corollary 2 in Cucker and Smale, (2002, p. 34), together with the portmanteau lemma (van der Vaart, , 1998, Lemma 2.2). Then combining (A.3.1) and (A.3.1), it holds that for ,

| (A.49) |

This completes the first part by taking sufficiently small .

For the remaining part, we are to show that . Using Assumption (ii’), and once again, Corollary 2 in Cucker and Smale, (2002, p. 34), the eigenfunctions , , are seen to be continuous. The remaining fact thus holds because is compact and is finite. With this last step, the proof of the lemma is completed. ∎

A.3.2 Proof of Theorem 4.2

Proof of Theorem 4.2.

We consider the Hoeffding decomposition with respect to the product measure :

We have proven in Theorem 4.1 that

as . In order to prove that and have the same limiting distribution, we only need to show that for and apply Slutsky’s theorem (van der Vaart, , 1998, Theorem 2.8). To this end, it suffices to establish that for .

We start from the scenario and proceed in two steps, in which we show that (i) , and (ii) . By symmetry,

One readily verifies . To simplify notation, let

| (A.51) |

and adopt the convention that replacing an index of by a “” means averaging over this index. In particular,

| (A.52) |

and other averages are defined similarly. We obtain using the definition (A.51) that

| (A.53) | ||||||||

Step I. We show that . In view of (A.3.2), we have

Applying (A.53), direct calculation yields

| (A.54) |

where the implicit constant depends only on . This completes Step I.

Step II. We prove that . Notice that

where

We set

| (A.55) |

Combining (A.53) and (A.55), we deduce that

Here, can be decomposed as , where

Hence,

Using a straightforward calculation confirms that . First, for distinct, we have

where

| (A.56) | ||||

| (A.57) |

and other summands can be rewritten similarly. Moreover, we have in (A.56) that

and similar equations for all the other summands. In (A.57),

and similar equations for all the other summands. It follows that

Similar calculations for the cases when the pairs and have one, two, or three indices in common, give a total contribution of at most . Adding these together shows that . This together with (similar to Zhao et al., , 1997, p. 2212; Barbour and Chen, , 2005, Lemma 3.1) and (Hoeffding, , 1951, Theorem 2) implies that .

Taken together the two steps we carried out prove that . The proofs for , , are very similar and hence omitted. ∎

A.4 Proofs for Section 5 of the main paper

A.4.1 Proof of Theorem 5.1

Proof of Theorem 5.1.

Introducing the dummy variables with

the LSAP can be formulated as a linear program:

| subject to |

Then an edge is in the optimal matching if and only if the solution to the linear program has . The dual linear program is

| subject to |

The sufficient and necessary condition for an optimal solution to the LSAP is

We introduce a few more terms that are convenient for our description. A matching is a subset of edges whose vertices are disjoint. A matching is -feasible if the dual variables satisfy that

A -optimal matching is a -feasible perfect matching. An edge is called admissible with regard to a matching if . An admissible graph is the union of a matching and the set of all admissible edges. A vertex is called exposed if it is not incident to any edge in the current matching. An alternating path is one that starts with an exposed vertex and alternatingly traverses edges in the matching and not. An alternating tree is a rooted tree whose paths are alternating paths from its root. A labelled vertex is one that belongs to any alternating tree. An augmenting path is an alternating path between two exposed vertices.

For every , , let . It is equivalent to find the optimal matching for the weights and that for the weights . Let stand for the binary representation of , where . We initialize the weights and the dual variables , to zero and the matching to empty matching. The scaling algorithm proceeds in stages. At the -th stage, we go through match routines to find a -optimal matching, where the weight of edge has the binary representation (and thus is equal to or ), starting from dual variables , .

The match routine computes a -optimal matching in several phases, each of which consists of augmenting the matching and doing a Hungarian search. Let be the current matching initialized to empty matching. We will omit the superscript index when there is no confusion.

Step I. We first obtain a maximal set of vertex-disjoint augmenting paths in the admissible graph by performing a depth first search. The depth first search marks every vertex visited; initially no vertex is marked. We grow an augmenting path starting from an exposed vertex by searching all admissible edges and finding an edge where is not marked. If such exists, we mark , add edge to , and then (1) if is also exposed, add the augmenting path to , and start finding the next augmenting path; (2) if is matched to ( since has not been marked until this step), we mark , add edge to , and continue searching from . If there is no unmarked, we delete the last two edges in path and (1) restart searching if is not empty; (2) initialize a new path otherwise. We repeat these steps until we have gone through all exposed vertices in . Then for each path , we augment the matching by replacing edges in the even step with the ones in the odd steps, and decrease dual variables by for all to maintain -feasibility. If the new matching is perfect, the routine halts, otherwise we do a Hungarian search as below.

Step II. For each exposed vertex , we grow an alternating tree rooted at such that each vertex in that in this tree is reachable from the root via an alternating path consisting only of admissible edges. For a vertex in (resp. ) in an alternating tree, the path from the root is augmenting (resp. not augmenting). Let (resp. ) denote the set of vertices in (resp. ) that are labelled. At the beginning of Hungarian search, is defined as the set of the exposed vertices in and . Define

Depending on whether or , one of the following steps is taken:

Case 1. (find an augmenting path or add to alternating trees). Let for and be an admissible edge, where the existence is guaranteed by . If is exposed, an augmenting path has been found and the Hungarian search ends. If is matched to for some (notice that cannot be matched to since is not labelled currently), we add the edges and to all the alternating trees that involve , update and by adding vertices and respectively, and recompute .

Case 2. (update the dual solution). We decrease by for each , increase by for each , and recompute .

In summary, there are stages. At each stage, one routine consists of phases, and each phase runs in time. The overall running time is . ∎

A.4.2 Proof of Theorem 5.2

Proof of Theorem 5.2.

In order to prove as and , it suffices to show that

We only need to show the convergence of moment-generating functions:

| (A.58) |

as , for all and some , by arguments in Billingsley, (1995, p. 390). Notice that (A.58) is equivalent to

| (A.59) |

We have by Item (vi) in Lyons, (2018) that and

where , , and and are independent copies of and , respectively. This implies that the right-hand side of (A.59) converges to a nonzero real number for every where is some fixed small positive number (Rudin, , 1987, Theorem 15.5). This together with the fact that, for each fixed as by (A.30), concludes (A.59). ∎

Appendix B A particular construction of

Assuming , we give a particular construction of distinct unit vectors such that the uniform discrete distribution on this set converges weakly to the uniform distribution on . To this end, let us first factorize into the following form:

| (B.1) |

A factorization of satisfying (2.2) and (B.1) together will always exist. Indeed, letting , one possibility is to take , , (noticing ), and .

To construct deterministic points in the unit ball, we consider spherical coordinates. Let be a vector in Cartesian coordinates. Its spherical coordinates are defined implicitly as

| (B.2) |

where , , and . Notice that the inverse transform is unique, while the transform is not unique in some special cases: if , then are arbitrary; if , then are arbitrary. To avoid any ambiguity, we make the spherical coordinates unique by specifying that arbitrary coordinates are zero in these cases.

The following lemma constructs a set of points on the unit sphere such that the uniform discrete distribution on this set will weakly converge to the uniform distribution over .

Lemma B.1.

When , for each , let for , and define the function as

Let

| (B.4) |

Then the uniform discrete distribution on the set of points with spherical coordinates weakly converges to the uniform distribution over as .

The above construction might look mysterious at the first sight. Indeed, to construct an asymptotically uniform grid over , it is tempting to take a product of univariate uniform grids over all spherical coordinates. Unfortunately, points picked in this way can be shown to concentrate at the poles, and hence cannot serve the desired purpose. Instead, a more elaborate construction such as the one in Lemma B.1 is needed.

Proof of Lemma B.1.

We proceed in three steps. First, we give an alternative form of the uniform discrete distribution on the points with spherical coordinates . Next, we find this uniform distribution’s limiting distribution as . Lastly, we prove that this limiting distribution is uniformly distributed over the unit sphere .

First, let be random variables uniformly discrete distributed on the points for all such that are mutually independent. Notice that the uniform discrete distribution on the points with spherical coordinates is identical to the distribution given by random spherical coordinates , where

Second, we determine the limit of the distribution with random spherical coordinates (B) as . Let be independent random variables that are uniformly distributed on . We have for as by the following argument:

as . Accordingly, the limiting distribution of (B) is given by random spherical coordinates , where

due to the continuous mapping theorem (van der Vaart, , 1998, Theorem 2.3).

Lastly, we show that the distribution given by random spherical coordinates (B) is uniformly distributed over the unit sphere . The area element of , denoted by , can be written in terms of spherical coordinates as

where the first equality is by Blumenson, (1960) and the last equality uses the trigonometric power-reduction formulas (Beyer, , 1987, p. 388). Here is defined as (B.1). The transformation corresponding to (B) is

which is a bijection between and for (Beyer, , 1987, p. 381), and a bijection between and for . In view of (B), we have

This together with the fact that (B) ranges over for and ranges over for proves the distribution given by random spherical coordinates (B) is uniformly distributed over . ∎

To obtain a particular construction of , we expand the above approximation over the sphere to an approximating augmented grid for the ball.

Definition B.1.

Assuming , let for , and define for as in (B.4). With notation , the augmented grid is the multiset consisting of copies of the origin whenever and the points for that have spherical coordinates .

The following proposition is an immediate corollary of Lemma B.1.

Proposition B.1.

The uniform discrete distribution on the augmented grid , which assigns mass to the origin and mass to every other grid point, weakly converges to .

Appendix C Additional numerical results

C.1 Critical values

C.2 Additional simulation results

Example C.1.

The data are drawn from Example 6.1(b) with and .

Example C.2.

The data are drawn such that is generated from standard multivariate normal distribution, and for , with sample size , dimensions .

The values reported in Figure C.9 and Table C.4 are based on simulations at the nominal significance level of . Compared to Figure 6.3, Figure C.9 further confirms that, compared to its competitors, the proposed test appears to be more sensitive to dimension. Table C.4 further showed that, in the setup of Example C.2, the test via distance covariance with marginal ranks achieves the highest power, while the proposed test works well as long as even when .

| 0.490 | 0.320 | 0.249 | 0.211 | 0.187 | 0.172 | 0.156 | 0.146 | 0.139 | 0.130 | |

| 0.320 | 0.205 | 0.159 | 0.135 | 0.119 | 0.110 | 0.101 | 0.095 | 0.088 | 0.085 | |

| 0.249 | 0.159 | 0.124 | 0.105 | 0.093 | 0.086 | 0.079 | 0.073 | 0.069 | 0.066 | |

| 0.211 | 0.135 | 0.105 | 0.089 | 0.079 | 0.072 | 0.066 | 0.062 | 0.059 | 0.056 | |

| 0.187 | 0.119 | 0.093 | 0.079 | 0.070 | 0.064 | 0.059 | 0.055 | 0.052 | 0.049 | |

| 0.172 | 0.110 | 0.086 | 0.072 | 0.064 | 0.058 | 0.054 | 0.050 | 0.047 | 0.045 | |

| 0.156 | 0.101 | 0.079 | 0.066 | 0.059 | 0.054 | 0.049 | 0.047 | 0.044 | 0.042 | |

| 0.146 | 0.095 | 0.073 | 0.062 | 0.055 | 0.050 | 0.047 | 0.044 | 0.041 | 0.039 | |

| 0.139 | 0.088 | 0.069 | 0.059 | 0.052 | 0.047 | 0.044 | 0.041 | 0.039 | 0.037 | |

| 0.130 | 0.085 | 0.066 | 0.056 | 0.049 | 0.045 | 0.042 | 0.039 | 0.037 | 0.035 |

| 0.945 | 0.563 | 0.421 | 0.349 | 0.303 | 0.273 | 0.250 | 0.232 | 0.219 | 0.208 | |

| 0.563 | 0.338 | 0.255 | 0.213 | 0.186 | 0.168 | 0.156 | 0.144 | 0.136 | 0.130 | |

| 0.421 | 0.255 | 0.194 | 0.162 | 0.142 | 0.131 | 0.119 | 0.111 | 0.105 | 0.100 | |

| 0.349 | 0.213 | 0.162 | 0.136 | 0.119 | 0.107 | 0.100 | 0.092 | 0.088 | 0.082 | |

| 0.303 | 0.186 | 0.142 | 0.119 | 0.105 | 0.095 | 0.088 | 0.083 | 0.077 | 0.072 | |

| 0.273 | 0.168 | 0.131 | 0.107 | 0.095 | 0.088 | 0.079 | 0.073 | 0.071 | 0.066 | |

| 0.250 | 0.156 | 0.119 | 0.100 | 0.088 | 0.079 | 0.073 | 0.069 | 0.066 | 0.061 | |

| 0.232 | 0.144 | 0.111 | 0.092 | 0.083 | 0.073 | 0.069 | 0.064 | 0.060 | 0.059 | |

| 0.219 | 0.136 | 0.105 | 0.088 | 0.077 | 0.071 | 0.066 | 0.060 | 0.057 | 0.055 | |

| 0.208 | 0.130 | 0.100 | 0.082 | 0.072 | 0.066 | 0.061 | 0.059 | 0.055 | 0.052 |

| Hallin | rdCov | dCov | ||

| 1.000 | 1.000 | 1.000 | ||

| 1.000 | 1.000 | 1.000 | ||

| 1.000 | 1.000 | 1.000 | ||

| 1.000 | 1.000 | 1.000 | ||

| 0.777 | 0.997 | 0.981 | ||

| 1.000 | 1.000 | 1.000 | ||

| 1.000 | 1.000 | 1.000 | ||

| 1.000 | 1.000 | 1.000 | ||

| 0.238 | 0.811 | 0.693 | ||

| 0.888 | 1.000 | 1.000 | ||

| 1.000 | 1.000 | 1.000 | ||

| 1.000 | 1.000 | 1.000 | ||

| 0.144 | 0.612 | 0.436 | ||

| 0.496 | 0.973 | 0.950 | ||

| 0.998 | 1.000 | 1.000 | ||

| 1.000 | 1.000 | 1.000 |

References

- Abe, (1969) Abe, O. (1969). A central limit theorem for the number of edges in the random intersection of two graphs. Ann. Math. Statist., 40(1):144–151.

- Agarwal and Sharathkumar, (2014) Agarwal, P. K. and Sharathkumar, R. (2014). Approximation algorithms for bipartite matching with metric and geometric costs. In STOC’14—Proceedings of the 2014 ACM Symposium on Theory of Computing, pages 555–564. ACM, New York, NY.

- Anselone, (1971) Anselone, P. M. (1971). Collectively compact operator approximation theory and applications to integral equations. Prentice-Hall, Inc., Englewood Cliffs, NJ.

- Atkinson, (1967) Atkinson, K. E. (1967). The numerical solutions of the eigenvalue problem for compact integral operators. Trans. Amer. Math. Soc., 129:458–465.

- Bakirov et al., (2006) Bakirov, N. K., Rizzo, M. L., and Székely, G. J. (2006). A multivariate nonparametric test of independence. J. Multivariate Anal., 97(8):1742–1756.

- Barbour and Chen, (2005) Barbour, A. D. and Chen, L. H. Y. (2005). The permutation distribution of matrix correlation statistics. In Stein’s Method and Applications, volume 5 of Lect. Notes Ser. Inst. Math. Sci. Natl. Univ. Singap., pages 223–245. Singapore Univ. Press, Singapore.

- Barbour and Eagleson, (1986) Barbour, A. D. and Eagleson, G. K. (1986). Random association of symmetric arrays. Stochastic Anal. Appl., 4(3):239–281.

- Basu, (1959) Basu, D. (1959). The family of ancillary statistics. Sankhyā, 21(3/4):247–256.

- Bergsma, (2006) Bergsma, W. (2006). A new correlation coefficient, its orthogonal decomposition and associated tests of independence. Available at arXiv:math/0604627v1.

- Bergsma and Dassios, (2014) Bergsma, W. and Dassios, A. (2014). A consistent test of independence based on a sign covariance related to Kendall’s tau. Bernoulli, 20(2):1006–1028.

- Berrett and Samworth, (2019) Berrett, T. B. and Samworth, R. J. (2019). Nonparametric independence testing via mutual information. Biometrika, 106(3):547–566.

- Beyer, (1987) Beyer, W. H., editor (1987). CRC handbook of mathematical sciences (6th ed.). CRC Press, Boca Raton, FL.

- Billingsley, (1995) Billingsley, P. (1995). Probability and measure (3rd ed.). Wiley Series in Probability and Mathematical Statistics. John Wiley & Sons, Inc., New York, NY.

- Billingsley, (1999) Billingsley, P. (1999). Convergence of probability measures (2nd ed.). Wiley Series in Probability and Statistics. John Wiley & Sons, Inc., New York, NY.

- Bloemena, (1964) Bloemena, A. R. (1964). Sampling from a graph. W. R. van Zwet (Ed.). Mathematical Centre Tracts, No. 2. Mathematisch Centrum, Amsterdam, Netherlands.

- Blum et al., (1961) Blum, J. R., Kiefer, J., and Rosenblatt, M. (1961). Distribution free tests of independence based on the sample distribution function. Ann. Math. Statist., 32:485–498.

- Blumenson, (1960) Blumenson, L. E. (1960). Classroom Notes: A Derivation of -Dimensional Spherical Coordinates. Amer. Math. Monthly, 67(1):63–66.

- Bolthausen, (1984) Bolthausen, E. (1984). An estimate of the remainder in a combinatorial central limit theorem. Z. Wahrsch. Verw. Gebiete, 66(3):379–386.

- Bolthausen and Götze, (1993) Bolthausen, E. and Götze, F. (1993). The rate of convergence for multivariate sampling statistics. Ann. Statist., 21(4):1692–1710.

- Chernozhukov et al., (2017) Chernozhukov, V., Galichon, A., Hallin, M., and Henry, M. (2017). Monge-Kantorovich depth, quantiles, ranks and signs. Ann. Statist., 45(1):223–256.

- Cliff and Ord, (1973) Cliff, A. D. and Ord, J. K. (1973). Spatial autocorrelation. Monographs in spatial and environmental systems analysis, 5. Pion, London, England.

- Cucker and Smale, (2002) Cucker, F. and Smale, S. (2002). On the mathematical foundations of learning. Bull. Amer. Math. Soc. (N.S.), 39(1):1–49.

- Daniels, (1944) Daniels, H. E. (1944). The relation between measures of correlation in the universe of sample permutations. Biometrika, 33(2):129–135.

- Deb and Sen, (2019) Deb, N. and Sen, B. (2019). Multivariate rank-based distribution-free nonparametric testing using measure transportation. Available at arXiv:1909.08733.

- DeGroot and Schervish, (2012) DeGroot, M. H. and Schervish, M. J. (2012). Probability and statistics (4th ed.). Addison-Wesley, Boston, MA.

- del Barrio et al., (2018) del Barrio, E., Cuesta-Albertos, J. A., Hallin, M., and Matrán, C. (2018). Smooth cyclically monotone interpolation and empirical center-outward distribution functions. Available at arXiv:1806.01238v1.

- Drton et al., (2020) Drton, M., Han, F., and Shi, H. (2020+). High dimensional consistent independence testing with maxima of rank correlations. Ann. Statist. (in press).

- Escanciano, (2006) Escanciano, J. C. (2006). A consistent diagnostic test for regression models using projections. Econometric Theory, 22(6):1030–1051.

- Fang et al., (1990) Fang, K. T., Kotz, S., and Ng, K. W. (1990). Symmetric multivariate and related distributions, volume 36 of Monographs on Statistics and Applied Probability. Chapman and Hall, Ltd., London, England.

- Farebrother, (1984) Farebrother, R. W. (1984). Algorithm AS 204: The distribution of a positive linear combination of random variables. J. Roy. Statist. Soc. Ser. C, 33(3):332–339.

- Feuerverger, (1993) Feuerverger, A. (1993). A consistent test for bivariate dependence. Int. Stat. Rev., 61(3):419–433.

- Figalli, (2018) Figalli, A. (2018). On the continuity of center-outward distribution and quantile functions. Nonlinear Anal., 177(part B):413–421.

- Gabow and Tarjan, (1989) Gabow, H. N. and Tarjan, R. E. (1989). Faster scaling algorithms for network problems. SIAM J. Comput., 18(5):1013–1036.

- Gebelein, (1941) Gebelein, H. (1941). Das statistische Problem der Korrelation als Variations- und Eigenwertproblem und sein Zusammenhang mit der Ausgleichsrechnung. Z. Angew. Math. Mech., 21:364–379.