First-order sensitivity of the optimal value in a Markov decision model with respect to deviations in the transition probability function

Abstract

Markov decision models (MDM) used in practical applications are most often less complex than the underlying ‘true’ MDM. The reduction of model complexity is performed for several reasons. However, it is obviously of interest to know what kind of model reduction is reasonable (in regard to the optimal value) and what kind is not. In this article we propose a way how to address this question. We introduce a sort of derivative of the optimal value as a function of the transition probabilities, which can be used to measure the (first-order) sensitivity of the optimal value w.r.t. changes in the transition probabilities. ‘Differentiability’ is obtained for a fairly broad class of MDMs, and the ‘derivative’ is specified explicitly. Our theoretical findings are illustrated by means of optimization problems in inventory control and mathematical finance.

Keywords: Markov decision model; Model reduction; Transition probability function; Optimal value; Functional differentiability; Financial optimization

1 Introduction

Already in the 1990th, Müller [27] pointed out that the impact of the transition probabilities of a Markov decision process (MDP) on the optimal value of a corresponding Markov decision model (MDM) can not be ignored for practical issues. For instance, in most cases the transition probabilities are unknown and have to be estimated by statistical methods. Moreover in many applications the ‘true’ model is replaced by an approximate version of the ‘true’ model or by a variant which is simplified and thus less complex. The result is that in practical applications the optimal (strategy and thus the optimal) value is most often computed on the basis of transition probabilities that differ from the underlying true transition probabilities. Therefore the sensitivity of the optimal value w.r.t. deviations in the transition probabilities is obviously of interest.

Müller [27] showed that under some structural assumptions the optimal value in a discrete-time MDM depends continuously on the transition probabilities, and he established bounds for the approximation error. In the course of this the distance between transition probabilities was measured by means of some suitable probability metrics. Even earlier, Kolonko [20] obtained analogous bounds in a MDM in which the transition probabilities depend on a parameter. Here the distance between transition probabilities was measured by means of the distance between the respective parameters. Error bounds for the expected total reward of discrete-time Markov reward processes were also specified by van Dijk [40] and van Dijk and Puterman [41]. In the latter reference the authors also discussed the case of discrete-time Markov decision processes with countable state and action spaces.

In this article, we focus on the situation where the ‘true’ model is replaced by a less complex version (for a simple example, see Subsection 5.4.3 in the supplementary material). The reduction of model complexity in practical applications is common and performed for several reasons. Apart from computational aspects and the difficulty of considering all relevant factors, one major point is that statistical inference for certain transition probabilities can be costly in terms of both time and money. However, it is obviously of interest to know what kind of model reduction is reasonable and what kind is not. In the following we want to propose a way how to address the latter question.

Our original motivation comes from the field of optimal logistics transportation planning, where ongoing projects like SYNCHRO-NET [38] aim at stochastic decision models based on transition probabilities estimated from historical route information. Due to the lack of historical data for unlikely events, transition probabilities are often modeled in a simplified way. In fact, events with small probabilities are often ignored in the model. However, the impact of these events on the optimal value (here the minimal expected transportation costs) of the corresponding MDM may nevertheless be significant. The identification of unlikely but potentially cost sensitive events is therefore a major challenge. In logistics planning operations engineers have indeed become increasingly interested in comprehensibly quantifying the sensitivity of the optimal value w.r.t. the incorporation of unlikely events into the model. For background see, for instance, [15, 16]. The assessment of rare but risky events takes on greater importance also in other areas of applications; see, for instance, [21, 44] and references cited therein.

By an incorporation of an unlikely event into the model we mean, for instance, that under performance of an action at some time a previously impossible transition from one state to another state gets now assigned small but strictly positive probability . Mathematically this means that the transition probability is replaced by with , where is the Dirac measure at . More generally one could consider a change of the whole transition function (the family of all transition probabilities) to with small. For operations engineers it is here interesting to know how this change affects the optimal value, . If the effect is minor, then an incorporation can be seen as superfluous, at least from a pragmatic point of view. If on the other hand the effect is significant, then the engineer should consider the option to extend the model and to make an effort to get access to statistical data for the extended model.

At this point it is worth mentioning that a change of the transition function from to with small can also have a different interpretation than an incorporation of an (unlikely) new event. It could also be associated with an incorporation of an (unlikely) divergence from the normal transition rules. See Subsection 4.5 for an example.

In this article, we will introduce an approach for quantifying the effect of changing the transition function from to , with small, on the optimal value of the MDM. In view of , we feel that it is reasonable to quantify the effect by a sort of derivative of the value functional at evaluated at direction . To some extent the ‘derivative’ specifies the first-order sensitivity of w.r.t. a change of as above. Take into account that

| (1) |

To be able to compare the first-order sensitivity for (infinitely) many different , it is favourable to know that the approximation in (1) is uniform in for preferably large sets of transition functions. Moreover, it is not always possible to specify the relevant exactly. For that reason it would be also good to have robustness (i.e. some sort of continuity) of in . These two things induced us to focus on a variant of tangential -differentiability as introduced by Sebastião e Silva [36] and Averbukh and Smolyanov [1] (here is a family of sets of transition functions). In Section 3 we present a result on ‘-differentiability’ of for the family of all relatively compact sets of admissible transition functions and a reasonably broad class of MDMs, where we measure the distance between transition functions by means of metrics based on probability metrics as in [27].

The ‘derivative’ of the optimal value functional at quantifies the effect of a change from to , with small, assuming that after the change the strategy (tuple of the underlying decision rules) is chosen such that it optimizes the target value (e.g. expected total costs or rewards) in under the new transition function . On the other hand, practitioners are also interested in quantifying the impact of a change of when the optimal strategy (under ) is kept after the change. Such a quantification would somehow answers the question: How much different does a strategy derived in a simplified MDM perform in a more complex (more realistic) variant of the MDM? Since the ‘derivative’ of the functional under a fixed strategy turns out to be a building stone for the derivative of the optimal value functional at , our elaborations cover both situations anyway. For fixed strategy we obtain ‘-differentiability’ of even for the broader family of all bounded sets of admissible transition functions.

The ‘derivative’ which we propose to regard as a measure for the first-order sensitivity will formally be introduced in Definition 3.9. This definition is applicable to quite general finite time horizon MDMs and might look somewhat cumbersome at first glance. However, in the special case of a finite state space and finite action spaces, a situation one faces in many practical applications, the proposed ‘differentiability’ boils down to a rather intuitive concept. This will be explained in Section 5 of the supplementary material with a minimum of notation and terminology. In Section 5 of the supplementary material we will also reformulate a backward iteration scheme for the computation of the ‘derivative’ (which can be deduced from our main result, Theorem 3.14) in the discrete case, and we will discuss an example.

In Section 2 we formally introduce quite general MDMs in the fashion of the standard monographs [2, 12, 13, 30]. Since it is important to have an elaborate notation in order to formulate our main result, we are very precise in Section 2. As a result, this section is a little longer compared to the respective sections in other articles on MDMs. In Section 3 we carefully introduce our notion of ‘differentiability’ and state our main result concerning the computation of the ‘derivative’ of the value functional.

In Section 4 we will apply the results of Section 3 to assess the impact of one or more than one unlikely but substantial shock in the dynamics of an asset on the solution of a terminal wealth problem in a (simple) financial market model free of shocks. This example somehow motivates the general set-up chosen in Sections 2–3. All results of this article are proven in Sections 7–9 of the supplementary material. For the convenience of the reader we recall in Section 10 of the supplementary material a result on the existence of optimal strategies in general MDMs. Section 11 of the supplementary material contains an auxiliary topological result.

2 Formal definition of Markov decision model

Let be a non-empty set equipped with a -algebra , referred to as state space. Let be a fixed finite time horizon (or planning horizon) in discrete time. For each point of time and each state , let be a non-empty set. The elements of will be seen as the admissible actions (or controls) at time in state . For each , let

The elements of can be seen as the actions that may basically be selected at time whereas the elements of are the possible state-action combinations at time . For our subsequent analysis, we equip with a -algebra , and let be the trace of the product -algebra in . Recall that a map is said to be a probability kernel (or Markov kernel) from to if is a -measurable map for any , and for any . Here is the set of all probability measures on .

2.1 Markov decision process

In this subsection, we will give a formal definition of an -valued (discrete-time) Markov decision process (MDP) associated with a given initial state, a given transition function and a given strategy. By definition a (Markov decision) transition (probability) function is an -tuple

whose -th entry is a probability kernel from to . In this context will be referred to as one-step transition (probability) kernel at time (or from time to ) and the probability measure is referred to as one-step transition probability at time (or from time to ) given state and action . We denote by the set of all transition functions.

We will assume that the actions are performed by a so-called -stage strategy (or -stage policy). An (-stage) strategy is an -tuple

of decision rules at times , where a decision rule at time is an -measurable map satisfying for all . Note that a decision rule at time is (deterministic and) ‘Markovian’ since it only depends on the current state and is independent of previous states and actions. We denote by the set of all decision rules at time , and assume that is non-empty. Hence a strategy is an element of the set , and this set can be seen as the set of all strategies. Moreover, we fix for any some which can be seen as the set of all admissible decision rules at time . In particular, the set can be seen as the set of all admissible strategies.

For any transition function , strategy , and time point , we can derive from a probability kernel from to through

| (2) |

The probability measure can be seen as the one-step transition probability at time given state when the transitions and actions are governed by and , respectively.

Now, consider the measurable space

For any , , and define the probability measure

| (3) |

on , where should be seen as the initial state of the MDP to be constructed. The right-hand side of (3) is the usual product of the probability measure and the kernels ; for details see display (6) in Section 6 of the supplementary material. Moreover let be the identity on , i.e.

| (4) |

Note that, for any , , and , the map can be regarded as an -valued random variable on the probability space with distribution .

It follows from Lemma 6.1 in the supplementary material) that for any , , , and

-

(i)

,

-

(ii)

,

-

(iii)

,

-

(iv)

.

The formulation of (ii)–(iv) is somewhat sloppy, because in general a (regular version of the) factorized conditional distribution of given under (evaluated at a fixed set ) is only -a.s. unique. So assertion (iv) in fact means that the probability kernel provides a (regular version of the) factorized conditional distribution of given under , and analogously for (ii) and (iii). Note that the factorized conditional distribution in part (ii) is constant w.r.t. . Assertions (iii) and (iv) together imply that the temporal evolution of is Markovian. This justifies the following terminology.

Definition 2.1 (MDP)

Under law the random variable is called (discrete-time) Markov decision process (MDP) associated with initial state , transition function and strategy .

2.2 Markov decision model and value function

Maintain the notation and terminology introduced in Subsection 2.1. In this subsection, we will first define a (discrete-time) Markov decision model (MDM) and introduce subsequently the corresponding value function. The latter will be derived from a reward maximization problem. Fix , and let for each point of time

be a -measurable map, referred to as one-stage reward function. Here specifies the one-stage reward when action is taken at time in state . Let

be an -measurable map, referred to as terminal reward function. The value specifies the reward of being in state at terminal time .

Denote by the family of all sets , , , and set . Moreover let be defined as in (4) and recall Definition 2.1. Then we define our MDM as follows.

Definition 2.2 (MDM)

The quintuple is called (discrete-time) Markov decision model (MDM) associated with the family of action spaces , transition function , set of admissible strategies , and reward functions .

In the sequel we will always assume that a MDM satisfies the following Assumption (A). In Subsection 3.1 we will discuss some conditions on the MDM under which Assumption (A) holds. We will use to denote the expectation w.r.t. the factorized conditional distribution . For , we clearly have for every ; see Lemma 6.1 in the supplementary material. In what follows we use the convention that the sum over the empty set is zero.

Assumption (A): for any and .

Under Assumption (A) we may define in a MDM for any and a map through

| (5) |

As a factorized conditional expectation this map is -measurable (for any and ). Note that for the right-hand side of (5) does not depend on ; see Lemma 6.2 in the supplementary material. Therefore the map need not be equipped with an index .

The value specifies the expected total reward from time to of under when strategy is used and is in state at time . It is natural to ask for those strategies for which the expected total reward from time to is maximal for all initial states . This results in the following optimization problem:

| (6) |

If a solution to the optimization problem (6) (in the sense of Definition 2.4 ahead) exists, then the corresponding maximal expected total reward is given by the so-called value function (at time ).

Definition 2.3 (Value function)

For a MDM the value function at time is the map defined by

| (7) |

Note that the value function is well defined due to Assumption (A) but not necessarily -measurable. The measurability holds true, for example, if the sets are at most countable or if conditions (a)–(c) of Theorem 10.3 in the supplementary material) are satisfied; see also Remark 10.4(i) in the supplementary material.

Definition 2.4 (Optimal strategy)

In a MDM a strategy is called optimal w.r.t. if

| (8) |

In this case is called optimal value (function), and we denote by the set of all optimal strategies w.r.t. . Further, for any given , a strategy is called -optimal w.r.t. in a MDM if

| (9) |

and we denote by the set of all -optimal strategies w.r.t. .

Note that condition (8) requires that is an optimal strategy for all possible initial states . Though, in some situations it might be sufficient to ensure that is an optimal strategy only for some fixed initial state . For a brief discussion of the existence and computation of optimal strategies, see Section 10 of the supplementary material.

Remark 2.5

(i) In practice, the choice of an action can possibly be based on historical observations of states and actions. In particular one could relinquish the Markov property of the decision rules and allow them to depend also on previous states and actions. Then one might hope that the corresponding (deterministic) history-dependent strategies improve the optimal value of a MDM . However, it is known that the optimal value of a MDM can not be enhanced by considering history-dependent strategies; see, e.g., Theorem 18.4 in [13] or Theorem 4.5.1 in [30].

(ii) Instead of considering the reward maximization problem (6) one could as well be interested in minimizing expected total costs over the time horizon . In this case, one can maintain the previous notation and terminology when regarding the functions and as the one-stage costs and the terminal costs, respectively. The only thing one has to do is to replace “” by “” in the representation (7) of the value function. Accordingly, a strategy will be -optimal for a given if in condition (9) “” and “” are replaced by “” and “”.

3 ‘Differentiability’ in of the optimal value

In this section, we show that the value function of a MDM, regarded as a real-valued functional on a set of transition functions, is ‘differentiable’ in a certain sense. The notion of ‘differentiability’ we use for functionals that are defined on a set of admissible transition functions will be introduced in Subsection 3.4. The motivation of our notion of ‘differentiability’ was discussed subsequent to (1). Before defining ‘differentiability’ in a precise way, we will explain in Subsections 3.2–3.3 how we measure the distance between transition functions. In Subsections 3.5–3.6 we will specify the ‘Hadamard derivative’ of the value function. At first, however, we will discuss in Subsection 3.1 some conditions under which Assumption (A) holds true. Throughout this section, , , and are fixed.

3.1 Bounding functions

Recall from Section 2 that stands for the set of all transition functions, i.e. of all -tuples of probability kernels from to . Let be an -measurable map, referred to as gauge function, where . Denote by the set of all -measurable maps , and let be the set of all satisfying . The following definition is adapted from [2, 27, 43]. Conditions (a)–(c) of this definition are sufficient for the well-definiteness of (and ); see Lemma 3.2 ahead.

Definition 3.1 (Bounding function)

Let . A gauge function is called a bounding function for the family of MDMs if there exist finite constants such that the following conditions hold for any and .

-

(a)

for all .

-

(b)

for all .

-

(c)

for all .

If for some , then is called a bounding function for the MDM .

Note that the conditions in Definition 3.1 do not depend on the set . That is, the terminology bounding function is independent of the set of all (admissible) strategies. Also note that conditions (a) and (b) can be satisfied by unbounded reward functions.

The following lemma, whose proof can be found in Subsection 7.1 of the supplementary material, ensures that Assumption (A) is satisfied when the underlying MDM possesses a bounding function.

Lemma 3.2

Let . If the family of MDMs possesses a bounding function , then Assumption (A) is satisfied for any . Moreover, the expectation in Assumption (A) is even uniformly bounded w.r.t. , and is contained in for any , , and .

3.2 Metric on set of probability measures

In Subsection 3.4 we will work with a (semi-) metric (on a set of transition functions) to be defined in (11) below. As it is common in the theory of probability metrics (see, e.g., p. 10 ff in [31]), we allow the distance between two probability measures and the distance between two transition functions to be infinite. That is, we adapt the axioms of a (semi-) metric but we allow a (semi-) metric to take values in rather than only in .

Let be any gauge function, and denote by the set of all for which . Note that the integral exists and is finite for any and . For any fixed , the distance between two probability measures can be measured by

| (10) |

Note that (10) indeed defines a map which is symmetric and fulfills the triangle inequality, i.e. provides a semi-metric. If separates points in (i.e. if any two coincide when for all ), then is even a metric. It is sometimes called integral probability metric or probability metric with a -structure; see [28, 45]. In some situations the (semi-) metric (with fixed) can be represented by the right-hand side of (10) with replaced by a different subset of . Each such set is said to be a generator of . The largest generator of is called the maximal generator of and denoted by . That is, is defined to be the set of all for which for all .

We now give some examples for the distance . The metrics in the first four examples were already mentioned in [27, 28]. In the last three examples metricizes the -weak topology. The latter is defined to be the coarsest topology on for which all mappings , , are continuous. Here is the set of all continuous functions in . If specifically , then and the -weak topology is nothing but the classical weak topology. In Section 2 in [23] one can find characterizations of those subsets of on which the relative -weak topology coincides with the relative weak topology.

Example 3.3

Let and , where . Then equals the total variation metric . The set clearly separates points in . The maximal generator of is the set of all with ; see Theorem 5.4 in [28].

Example 3.4

For , let and , where . Then equals the Kolmogorov metric , where and refer to the distribution functions of and , respectively. The set clearly separates points in . The maximal generator of is the set of all with , where denotes the total variation of ; see Theorem 5.2 in [28].

Example 3.5

Assume that is a metric space and let . Let and , where with for and . Then is nothing but the bounded Lipschitz metric . The set separates points in ; see Lemma 9.3.2 in [8]. Moreover it is known (see, e.g., Theorem 11.3.3 in [8]) that if is separable then metricizes the weak topology on .

Example 3.6

Assume that is a metric space and let . For some fixed , let and , where with as in Example 3.5. Then is nothing but the Kantorovich metric . The set separates points in , because () does. It is known (see, e.g., Theorem 7.12 in [42]) that if is complete and separable then metricizes the -weak topology on .

Recall from [39] that for the -Wasserstein metric coincides with the Kantorovich metric. In this case the -weak topology is also referred to as -weak topology. Note that the -Wasserstein metric is a conventional metric for measuring the distance between probability distributions; see, for instance, [7, 18, 39] for the general concept and [4, 19, 22, 24] for recent applications.

Although the Kantorovich metric is a popular and well established metric, for the application in Section 4 we will need the following generalization from to .

Example 3.7

Assume that is a metric space and let . For some fixed and , let and , where with . The set separates points in (this follows with similar arguments as in the proof of Lemma 9.3.2 in [8]). Then provides a metric on which we denote by and refer to as Hölder- metric. Especially when dealing with risk averse utility functions (as, e.g., in Section 4) this metric can be beneficial. Lemma 11.1 in Section 11 of the supplementary material shows that if is complete and separable then metricizes the -weak topology on .

3.3 Metric on set of transition functions

Maintain the notation from Subsection 3.2. Let us denote by the set of all transition functions satisfying for all and . That is, consists of those transition functions with for all and . Hence, for the elements of all integrals of the shape , , , , exist and are finite. In particular, for two transition functions and from the distance is well defined for all and (recall that ). So we can define the distance between two transition functions and from by

| (11) |

for another gauge function . Note that (11) defines a semi-metric on which is even a metric if separates points in .

Maybe apart from the factor , the definition of in (11) is quite natural and in line with the definition of a distance introduced by Müller [27, p. 880]. In [27], Müller considers time-homogeneous MDMs, so that the transition kernels do not depend on . He fixed a state and took the supremum only over all admissible actions in state . That is, for any he defined the distance between and by . To obtain a reasonable distance between and it is however natural to take the supremum of the distance between and uniformly over and over .

3.4 Definition of ‘differentiability’

Let be any gauge function, and fix some being closed under mixtures (i.e. for any , ). The set will be equipped with the distance introduced in (11). In Definition 3.9 below we will introduce a reasonable notion of ‘differentiability’ for an arbitrary functional taking values in a normed vector space . It is related to the general functional analytic concept of (tangential) -differentiability introduced by Sebastião e Silva [36] and Averbukh and Smolyanov [1]; see also [9, 11, 37] for applications. However, is not a vector space. This implies that Definition 3.9 differs from the classical notion of (tangential) -differentiability. For that reason we will use inverted commas and write ‘-differentiability’ instead of -differentiability. Due to the missing vector space structure, we in particular need to allow the tangent space to depend on the point at which is differentiated. The role of the ‘tangent space’ will be played by the set

whose elements can be seen as signed transition functions. In Definition 3.9 we will employ the following terminology.

Definition 3.8

Let , be another gauge function, and fix . A map is said to be -continuous if the mapping from to is -continuous.

For the following definition it is important to note that lies in for any and .

Definition 3.9 (‘-differentiability’)

Let , be another gauge function, and fix . Moreover let be a system of subsets of . A map is said to be ‘-differentiable’ at w.r.t. if there exists an -continuous map such that

| (12) |

for every and every sequence with . In this case, is called ‘-derivative’ of at w.r.t. .

Note that in Definition 3.9 the derivative is not required to be linear (in fact the derivative is not even defined on a vector space). This is another point where Definition 3.9 differs from the functional analytic definition of (tangential) -differentiability. However, non-linear derivatives are common in the field of mathematical optimization; see, for instance, [32, 37].

Remark 3.10

(i) At least in the case , the ‘-derivative’ evaluated at , i.e. , can be seen as a measure for the first-order sensitivity of the functional w.r.t. a change of the argument from to , with small, for some given transition function .

(ii) The prefix ‘-’ in Definition 3.9 provides the following information. Since the convergence in (12) is required to be uniform in , the values of the first-order sensitivities , , can be compared with each other with clear conscience for any fixed . It is therefore favorable if the sets in are large. However, the larger the sets in , the stricter the condition of ‘-differentiability’.

(iii) The subset () and the gauge function tell us in a way how ‘robust’ the ‘-derivative’ is w.r.t. changes in : The smaller the set and the ‘steeper’ the gauge function , the less strict the metric (given by (11)), and therefore the more robust in . It is thus favorable if the set is small and the gauge function is ‘steep’. However, the smaller and the ‘steeper’ , the stricter the condition of ‘-differentiability’. More precisely, if and then ‘-differentiability’ w.r.t. implies ‘-differentiability’ w.r.t. . Also note that in general the choice of in Definition 3.9 is not influenced by the choice of the pair , and vice versa.

In the general framework of our main result (Theorem 3.14) we can not choose ‘steeper’ than the gauge function which plays the role of a bounding function there. Indeed, the proof of -continuity of the map in Theorem 3.14 does not work anymore if is replaced by for any gauge function ‘steeper’ than . And here it does not matter how exactly is chosen.

In the application in Section 4, the set should be contained in (for details see Remark 4.8). This set can be shown to be (relatively) compact w.r.t. for () but not for any ‘flatter’ gauge function . So, in this example, and certainly in many other examples, relatively compact subsets of w.r.t. should be contained in . It is thus often beneficial to know that the value functional is ‘differentiable’ in the sense of part (b) of the following Definition 3.11.

The terminology of Definition 3.11 is motivated by the functional analytic analogues. Bounded and relatively compact sets in the (semi-) metric space are understood in the conventional way. A set is said to be bounded (w.r.t. ) if there exist and such that for every . It is said to be relatively compact (w.r.t. ) if for every sequence there exists a subsequence of such that for some . The system of all bounded sets and the system of all relatively compact sets (w.r.t. ) are larger the ‘steeper’ the gauge function is.

Definition 3.11

In the setting of Definition 3.9 we refer to ‘-differentiability’ as

-

(a)

‘Gateaux–Lévy differentiability’ if .

-

(b)

‘Hadamard differentiability’ if .

-

(c)

‘Fréchet differentiability’ if .

Clearly, ‘Fréchet differentiability’ (of at w.r.t. ) implies ‘Hadamard differentiability’ which in turn implies ‘Gateaux–Lévy differentiability’, each with the same ‘derivative’.

The last sentence before Definition 3.11 and the second to last sentence in part (iii) of Remark 3.10 together imply that ‘Hadamard (resp. Fréchet) differentiability’ w.r.t. implies ‘Hadamard (resp. Fréchet) differentiability’ w.r.t. when .

The following lemma, whose proof can be found in Subsection 7.2 of the supplementary material, provides an equivalent characterization of ‘Hadamard differentiability’.

Lemma 3.12

Let , be another gauge function, be any map, and fix . Then the following two assertions hold.

(i) If is ‘Hadamard differentiable’ at w.r.t. with ‘Hadamard derivative’ , then we have for each triplet with and that

| (13) |

(ii) If there exists an -continuous map such that (13) holds for each triplet with and , then is ‘Hadamard differentiable’ at w.r.t. with ‘Hadamard derivative’ .

3.5 ‘Differentiability’ of the value functional

Recall that , , and are fixed, and let and be defined as in (5) and (7), respectively. Moreover let be any gauge function and fix some being closed under mixtures.

In view of Lemma 3.2 (with ), condition (a) of Theorem 3.14 below ensures that Assumption (A) is satisfied for any . Then for any , , and we may define under condition (a) of Theorem 3.14 functionals and by

| (14) |

respectively. Note that specifies the maximal value for the expected total reward in the MDM (given state at time ) when the underlying transition function is . By analogy with the name ‘value function’ we refer to as value functional given state at time . Part (ii) of Theorem 3.14 provides (under some assumptions) an ‘Hadamard derivative’ of the value functional in the sense of Definition 3.11.

Conditions (b) and (c) of Theorem 3.14 involve the so-called Minkowski (or gauge) functional (see, e.g., [33, p. 25]) defined by

| (15) |

where we use the convention , is any subset of , and we set . We note that Müller [27] also used the Minkowski functional to formulate his assumptions.

Example 3.13

For the sets (and the corresponding gauge functions ) from Examples 3.3–3.7 we have , , , , and , where as before and are used to denote the maximal generator of and , respectively. The latter three equations are trivial, for the former two equations see [27, p. 880].

Recall from Definition 2.4 that for given and the sets and consist of all -optimal strategies w.r.t. and of all optimal strategies w.r.t. , respectively. Generators of were introduced subsequent to (10).

Theorem 3.14 (‘Differentiability’ of and )

Let and be any generator of . Fix , and assume that the following three conditions hold.

-

(a)

is a bounding function for the MDM for any .

-

(b)

for any .

-

(c)

.

Then the following two assertions hold.

-

(i)

For any , , , the map defined by (14) is ‘Fréchet differentiable’ at w.r.t. with ‘Fréchet derivative’ given by

-

(ii)

For any and , the map defined by (14) is ‘Hadamard differentiable’ at w.r.t. with ‘Hadamard derivative’ given by

(17) If the set of optimal strategies is non-empty, then the ‘Hadamard derivative’ admits the representation

(18)

The proof of Theorem 3.14 can be found in Section 8 of the supplementary material. Note that the set shrinks as decreases. Therefore the right-hand side of (17) is well defined. The supremum in (18) ranges over all optimal strategies w.r.t. . If, for example, the MDM satisfies conditions (a)–(c) of Theorem 10.3 in the supplementary material, then by part (iii) of this theorem an optimal strategy can be found, i.e. is non-empty. The existence of an optimal strategy is also ensured if the sets are finite (a situation one often faces in applications). In the latter case the ‘Hadamard derivative’ can easily be determined by computing the finitely many values , , and taking their maximum. The discrete case will be discussed in more detail in Subsection 5.5 of the supplementary material.

If there exists a unique optimal strategy w.r.t. , then is nothing but the singleton , and in this case the ‘Hadamard derivative’ of the optimal value (functional) at coincides with .

Remark 3.15

(i) The ‘Fréchet differentiability’ in part (i) of Theorem 3.14 holds even uniformly in ; see Theorem 8.1 in the supplementary material for the precise meaning.

(ii) We do not know if it is possible to replace ‘Hadamard differentiability’ by ‘Fréchet differentiability’ in part (ii) of Theorem 3.14. The following arguments rather cast doubt on this possibility. The proof of part (ii) is based on the decomposition of the value functional in display (73) of the supplementary material and a suitable chain rule, where the decomposition (73) involves the sup-functional introduced in display (74) of the supplementary material. However, Corollary 1 in [6] (see also Proposition 4.6.5 in [35]) shows that in normed vector spaces sup-functionals are in general not Fréchet differentiable. This could be an indication that ‘Fréchet differentiable’ of the value functional indeed fails. We can not make a reliable statement in this regard.

(iii) Recall that ‘Hadamard (resp. Fréchet) differentiability’ w.r.t. implies ‘Hadamard (resp. Fréchet) differentiability’ w.r.t. for any gauge function . However, for any such ‘Hadamard (resp. Fréchet) differentiability’ w.r.t. is less meaningful than w.r.t. . Indeed, when using with instead of , the sets for whose elements the first-order sensitivities can be compared with each other with clear conscience are smaller and the ‘derivative’ is less robust.

(iv) In the case where we are interested in minimizing expected total costs in the MDM (see Remark 2.5(ii)), we obtain under the assumptions (and with the same arguments as in the proof of part (ii)) of Theorem 3.14 that the ‘Hadamard derivative’ of the corresponding value functional is given by (17) (resp. (18)) with “” replaced by “”.

Remark 3.16

(i) Condition (a) of Theorem 3.14 is in line with the existing literature. In fact, similar conditions as in Definition 3.1 (with ) have been imposed many times before; see, for instance, [2, Definition 2.4.1], [27, Definition 2.4], [30, p. 231 ff], and [43].

(ii) In some situations, condition (a) implies condition (b) in Theorem 3.14. This is the case, for instance, in the following four settings (the involved sets were introduced in Examples 3.3–3.7).

1) and .

2) and , as well as for

- , , are increasing,

- , , and are increasing.

3) and , as well as for

- ,

- and .

4) and , as well as for

- ,

- and for some and

. Recall that for .

The proof of (a)(b) relies in setting 1) on Lemma 3.2 (with ) and in settings 2)–4) on Lemma 3.2 (with ) along with Proposition 10.1 of the supplementary material. The conditions in setting 2) are similar to those in parts (ii)–(iv) of Theorem 2.4.14 in [2], and the conditions in settings 3) and 4) are motivated by the statements in [14, p. 11f].

(iii) In many situations, condition (c) of Theorem 3.14 holds trivially. This is the case, for instance, if and , or if and for some fixed and .

(iv) The conditions (b) and (c) of Theorem 3.14 can also be verified directly in some cases; see, for instance, the proof of Lemma 9.2 in Subsection 9.3.1 of the supplementary material.

In applications it is not necessarily easy to specify the set of all optimal strategies w.r.t. . While in most cases an optimal strategy can be found with little effort (one can use the Bellman equation; see part (i) of Theorem 10.3 in Section 10 of the supplementary material), it is typically more involved to specify all optimal strategies or to show that the optimal strategy is unique. The following remark may help in some situations; for an application see Subsection 4.4.

Remark 3.17

In some situations it turns out that for every the solution of the optimization problem (6) does not change if is replaced by a subset (being independent of ). Then in the definition (7) of the value function (at time ) the set can be replaced by the subset , and it follows (under the assumptions of Theorem 3.14) that in the representation (18) of the ‘Hadamard derivative’ of at the set can be replaced by the set of all optimal strategies w.r.t. from the subset . Of course, in this case it suffices to ensure that conditions (a)–(b) of Theorem 3.14 are satisfied for the subset instead of .

3.6 Two alternative representations of

In this subsection we present two alternative representations (see (19) and (20)) of the ‘Fréchet derivative’ in ((i)). The representation (19) will be beneficial for the proof of Theorem 3.14 (see Lemma 8.2 in Subsection 8.1 of the supplementary material) and the representation (20) will be used to derive the ‘Hadamard derivative’ of the optimal value of the terminal wealth problem in (28) below (see the proof of Theorem 4.6 in Subsection 9.3 of the supplementary material).

Remark 3.18 (Representation I)

By rearranging the sums in ((i)), we obtain under the assumptions of Theorem 3.14 that for every fixed the ‘Fréchet derivative’ of at can be represented as

| (19) | ||||

for every , , , and .

Remark 3.19 (Representation II)

For every fixed , and under the assumptions of Theorem 3.14, the ‘Fréchet derivative’ of at admits the representation

| (20) |

for every , , , and , where is the solution of the following backward iteration scheme

| (21) | ||||

Indeed, it is easily seen that coincides with the right-hand side of (19). Note that it can be verified iteratively by means of condition (a) of Theorem 3.14 and Lemma 3.2 (with ) that for every , , and . In particular, this implies that the integrals on the right-hand side of (21) exist and are finite. Also note that the iteration scheme (21) involves the family which itself can be seen as the solution of a backward iteration scheme:

see Proposition 10.1 of the supplementary material.

4 Application to a terminal wealth optimization problem in mathematical finance

In this section we will apply the theory of Sections 2–3 to a particular optimization problem in mathematical finance. At first, we introduce in Subsection 4.1 the basic financial market model and formulate subsequently the terminal wealth problem as a classical optimization problem in mathematical finance. The market model is in line with standard literature as [2, Chapter 4] or [10, Chapter 5]. To keep the presentation as clear as possible we restrict ourselves to a simple variant of the market model (only one risky asset). In Subsection 4.2 we will see that the market model can be embedded into the MDM of Section 2. It turns out that the existence (and computation) of an optimal (trading) strategy can be obtained by solving iteratively one-stage investment problems; see Subsection 4.3. In Subsection 4.4 we will specify the ‘Hadamard derivative’ of the optimal value functional of the terminal wealth problem, and Subsection 4.5 provides some numerical examples.

4.1 Basic financial market model, and the target

Consider an -period financial market consisting of one riskless bond and one risky asset . Further assume that the value of the bond evolves deterministically according to

for some fixed constants , and that the value of the asset evolves stochastically according to

for some independent -valued random variables on some probability space with distributions , respectively.

Throughout Section 4 we will assume that the financial market satisfies the following Assumption (FM), where is fixed and chosen as in (24) below. In Examples 4.4 and 4.5 we will discuss specific financial market models which satisfy Assumption (FM).

Assumption (FM): The following three assertions hold for any .

-

(a)

.

-

(b)

-a.s.

-

(c)

.

Note that for any the value (resp. ) corresponds to the relative price change (resp. ) of the bond (resp. asset) between time and . Let be the trivial -algebra, and set for any .

Now, an agent invests a given amount of capital in the bond and the asset according to some self-financing trading strategy. By trading strategy we mean an -adapted -valued stochastic process , where (resp. ) specifies the amount of capital that is invested in the bond (resp. asset) during the time interval . Here we require that both and are nonnegative for any , which means that taking loans and short sellings of the asset are excluded. The corresponding portfolio process associated with is given by

A trading strategy is said to be self-financing w.r.t. the initial capital if and for all . It is easily seen that for any self-financing trading strategy w.r.t. the corresponding portfolio process admits the representation

| (22) |

Note that corresponds to the amount of capital which is invested in the bond between time and . Also note that it can be verified easily by means of Remark 3.1.6 in [2] that under condition (c) of Assumption (FM) the financial market introduced above is free of arbitrage opportunities.

In view of (22), we may and do identify a self-financing trading strategy w.r.t. with an -adapted -valued stochastic process satisfying and for all . We restrict ourselves to Markovian self-financing trading strategies w.r.t. which means that only depends on and . To put it another way, we assume that for any there exists some Borel measurable map such that Then, in particular, is an -valued -Markov process whose one-step transition probability at time given state and strategy (resp. ) is given by with

| (23) |

The agent’s aim is to find a self-financing trading strategy (resp. ) w.r.t. for which her expected utility of the discounted terminal wealth is maximized. We assume that the agent is risk averse and that her attitude towards risk is set via the power utility function defined by

| (24) |

for some fixed (as in Assumption (FM)). The coefficient determines the degree of risk aversion of the agent: the smaller the coefficient , the greater her risk aversion. Hence the agent is interested in those self-financing trading strategies (resp. ) w.r.t. for which the expectation of under is maximized.

In the following subsections we will assume for notational simplicity that are fixed and that are a sort of model parameters. In this case the factor in in display (25) is superfluous; it indeed does not influence the maximization problem or any ‘derivative’ of the optimal value. On the other hand, if also the (Dirac-) distributions of would be allowed to be variable, then this factor could matter for the derivative of the optimal value w.r.t. changes in the (deterministic) dynamics of .

4.2 Embedding into MDM, and optimal trading strategies

The setting introduced in Subsection 4.1 can be embedded into the setting of Sections 2–3 as follows. Let be a priori fixed constants. Let and for any and . Then and Let . In particular, and the set of all decision rules at time consists of all those Borel measurable functions which satisfy for all (in particular is independent of ). For any , let the set of all admissible decision rules at time be equal to . Let as before .

Moreover let for any , and

| (25) |

Consider the gauge function defined by

| (26) |

Let be the set of all transition functions consisting of transition kernels of the shape

| (27) |

for some , where is the set of all satisfying , and the map is defined as in (23). In particular, (with defined as in Subsection 3.3), and it can be verified easily that given by (26) is a bounding function for the MDM for any (see Lemma 9.2(i) of the supplementary material). Note that plays the role of the portfolio process from Subsection 4.1. Also note that for some fixed , any self-financing trading strategy w.r.t. may be identified with some via .

Then, for every fixed and the terminal wealth problem introduced at the very end of Subsection 4.1 reads as

| (28) |

A strategy is called an optimal (self-financing) trading strategy w.r.t. (and ) if it solves the maximization problem (28).

Remark 4.1

In the setting of Subsection 4.1 we restrict ourselves to Markovian self-financing trading strategies w.r.t. which may be identified with some via . Of course, one could also assume that the decision rules of a trading strategy also depend on past actions and past values of the portfolio process . However, as already discussed in Remark 2.5(i), the corresponding history-dependent trading strategies do not lead to an improved optimal value for the terminal wealth problem (28).

4.3 Computation of optimal trading strategies

In this subsection we discuss the existence and computation of solutions to the terminal wealth problem (28), maintaining the notation of Subsection 4.2. We will adapt the arguments of Section 4.2 in [2]. As before are fixed constants.

Basically the existence of an optimal trading strategy for the terminal wealth problem (28) can be ensured with the help of a suitable analogue of Theorem 4.2.2 in [2]. In order to specify the optimal trading strategy explicitly one has to determine the local maximizers in the Bellman equation; see Theorem 10.3(i) in Section 10 of the supplementary material. However this is not necessarily easy. On the other hand, part (ii) of Theorem 4.3 ahead (a variant of Theorem 4.2.6 in [2]) shows that, for our particular choice of the utility function (recall (24)), the optimal investment in the asset at time has a rather simple form insofar as it depends linearly on the wealth. The respective coefficient can be obtained by solving the one-stage optimization problem in (29) ahead. That is, instead of finding the optimal amount of capital (possibly depending on the wealth) to be invested in the asset, it suffices to find the optimal fraction of the wealth (being independent of the wealth itself) to be invested in the asset.

For the formulation of the one-stage optimization problem note that every transition function is generated through (27) by some . For every , we use to denote any such set of ‘parameters’. Now, consider for any and the optimization problem

| (29) |

Note that lies in for any and , and that the integral on the left-hand side (exists and) is finite (this follows from displays (81)–(83) in Subsection 9.1 of the supplementary material) and should be seen as the expectation of under .

The following lemma, whose proof can be found in Subsection 9.1 of the supplementary material, shows in particular that

is the maximal value of the optimization problem (29).

Lemma 4.2

For any and , there exists a unique solution to the optimization problem (29).

Part (i) of the following Theorem 4.3 involves the value function introduced in (7). In the present setting this function has a comparatively simple form:

| (30) |

for any , , and .

Part (ii) involves the subset of which consists of all linear trading strategies, i.e. of all of the form for some , where

| (31) |

In part (i) and elsewhere we use the convention that the product over the empty set is .

Theorem 4.3 (Optimal trading strategy)

For any the following two assertions hold.

- (i)

-

(ii)

For any , let be the unique solution to the optimization problem (29) and define a decision rule at time through

(32) Then forms an optimal trading strategy w.r.t. . Moreover, there is no further optimal trading strategy w.r.t. which belongs to .

The proof of Theorem 4.3 can be found in Subsection 9.2 of the supplementary material. The second assertion of part (ii) of Theorem 4.3 will be beneficial for part (ii) of Theorem 4.6; for details see Remark 4.7. The following two Examples 4.4 and 4.5 illustrate part (ii) of Theorem 4.3.

Example 4.4 (Cox–Ross–Rubinstein model)

Let for some . Moreover let be any transition function defined as in (27) with for some , where and are some given constants (depending on ) satisfying . Then and conditions (a)–(c) of Assumption (FM) are clearly satisfied. In particular, the corresponding financial market is arbitrage-free and the optimization problem (29) simplifies to (up to the factor )

| (33) |

Lemma 4.2 ensures that (33) has a unique solution, , and it can be checked easily (see, e.g., [2, p. 86]) that this solution admits the representation

| (34) |

where and

Note that only fractions from the interval are admissible, and that the expression in the middle line in (34) lies in when . Thus, part (ii) of Theorem 4.3 shows that the strategy defined by (32) (with replaced by ) is optimal w.r.t. and unique among all .

In the following example the bond and the asset evolve according to the ordinary differential equation and the Itô stochastic differential equation

respectively, where and are constants and is a one-dimensional standard Brownian motion. We assume that the trading period is (without loss of generality) the unit interval and that the bond and the asset can be traded only at equidistant time points in , namely at , . Then, in particular, the relative price changes and are given by

and

respectively. In particular, and is distributed according to the log-normal distribution for any .

Example 4.5 (Black–Scholes–Merton model)

Let for , where . Moreover let be any transition function defined as in (27) with for , where and are some given constants (depending on ) satisfying . Then and it is easily seen that conditions (a)–(c) of Assumption (FM) hold. In particular, the corresponding financial market is arbitrage-free and the optimization problem (29) now reads as

| (35) |

where is the standard Lebesgue density of the log-normal distribution . Lemma 4.2 ensures that (35) has a unique solution, , and it is known (see, e.g., [26, 29]) that this solution is given by

| (36) |

where . Note that only fractions from the interval are admissible, and that the expression in the middle line in (36) is called Merton ratio and lies in when . Thus, part (ii) of Theorem 4.3 shows that the strategy defined by (32) (with replaced by ) is optimal w.r.t. and unique among all .

4.4 ‘Hadamard derivative’ of the optimal value functional

Maintain the notation and terminology introduced in Subsections 4.1–4.3. In this subsection we will specify the ‘Hadamard derivative’ of the optimal value functional of the terminal wealth problem (28) at (fixed) ; see part (ii) of Theorem 4.6. Recall that introduced in (24) is fixed and determines the degree of risk aversion of the agent.

By the choice of the gauge function (see (26)) we may choose (with introduced in Example 3.7) in the setting of Subsection 3.5. Note that coincides with the corresponding gauge function in Example 3.7 with . That is, in the end the metric (as defined in (11)) on is used to measure the distance between transition functions.

For the formulation of Theorem 4.6 recall from (14) the definition of the functionals and , where the maps and are given by (5) and (7), respectively. In the specific setting of Subsection 4.2 we know from (30) that

| (37) |

for any , , and .

Further recall that any induces a linear trading strategy through (31). Let be defined as on the left-hand side of (29) and set for any . Moreover, for any denote by the unique solution to the optimization problem (29) (Lemma 4.2 ensures the existence of a unique solution). Finally set .

Theorem 4.6 (‘Differentiability’ of and )

Remark 4.7

Basically Theorem 3.14 yields the first “” in (39) with replaced by . Since part (ii) of Theorem 4.3 ensures that for any there exists an optimal trading strategy which belongs to , we may replace for any in the representation (30) of the value function (or, equivalently, in the representation (37) of the value functional ) the set by (). Therefore one can use Theorem 3.14 to derive the first “” in (39). The second “” in (39) is ensured by the second assertion in part (ii) of Theorem 4.3. For details see the proof which is carried out in Subsection 9.3 of the supplementary material.

4.5 Numerical examples for the ‘Hadamard derivative’

In this subsection we quantify by means of the ‘Hadamard derivative’ (of the optimal value functional ) the effect of incorporating an unlikely but significant jump in the dynamics of an asset price on the optimal value of the corresponding terminal wealth problem (28). At the end of this subsection we will also study the effect of incorporating more than one jump.

We specifically focus on the setting of the discretized Black–Scholes–Merton model from Example 4.5 with (mainly) . That is, we let for , where . Moreover let correspond to for , where and are chosen such that . In fact we let specifically and . This set of parameters is often used in numerical examples in the field of mathematical finance; see, e.g., [25, p. 898]. For the initial state we choose . For the drift of the bond we will consider different values, all of them lying in . Moreover, we let (mainly) . Recall that determines the degree of risk aversion of the agent; a small corresponds to high risk aversion.

By a price jump at a fixed time we mean that the asset’s return is not anymore drawn from but is given by a deterministic value esstentially ‘away’ from . As appears from Table 1, in the case it seems to be reasonable to speak of a ‘jump’ at least if or . The probability under for a realized return smaller than (resp. larger than ) is smaller than . A realized return of (resp. ) is practically impossible; its probability under is smaller than (resp. ). That is, the choice or doubtlessly corresponds to a significant price jump.

If at a fixed time a formerly nearly impossible ‘jump’ can now occur with probability , then instead of one has . That is, instead of the transition function is now given by with generated through (27) by , , where

| (40) |

By part (ii) of Theorem 4.6 the ‘Hadamard derivative’ of the optimal value functional evaluated at can be written as

| (41) | |||||

with , where is given by (36). The involved factors are

| (42) | ||||

| (46) |

| (47) |

for , where ().

Note that is independent of , which can be seen from (40)–(47). That is, the effect of a jump is independent of the time at which the jump takes place. Also note that when . This is not surprising, because in this case the optimal fraction to be invested into the asset is equal to (see (36)) and the agent performs a complete investment in the bond at each trading time .

Remark 4.8

As mentioned before, the ‘Hadamard derivative’ evaluated at can be seen as the first-order sensitivity of the optimal value w.r.t. a change of to , with small. It is a natural wish to compare these values for different . In Subsection 9.4 of the supplementary material it is proven that the family is relatively compact w.r.t. (the proof does not work if is replaced by for any gauge function ‘flatter’ than ) for any fixed . As a consequence the approximation (1) with holds uniformly in , and therefore the values , , can be compared with each other with clear conscience.

By Remark 4.8 and (41) we are able to compare the effect of incorporating different ‘jumps’ in the dynamics of an asset price on the optimal value (functional) .

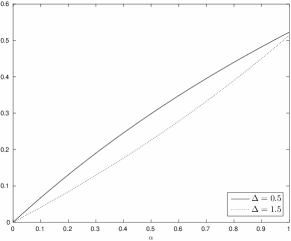

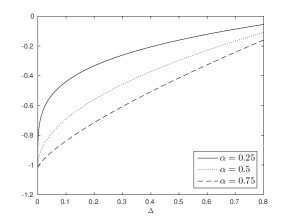

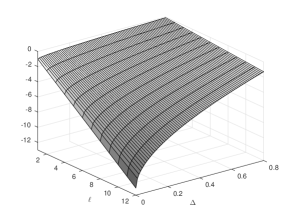

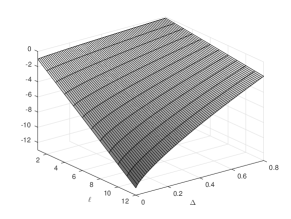

As appears from Figure 1 the negative effect of incorporating a ‘jump’ in the dynamics of an asset price is larger than the positive effect of incorporating a ‘jump’ for every choice of the agent’s degree of risk aversion. Figure 1 also shows the unsurprising effect that a high risk aversion (small value of ) leads to a negligible sensitivity.

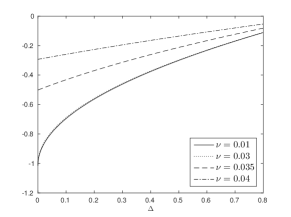

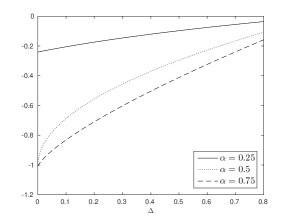

Next we compare the values of for trading horizons in dependence of the drift of the bond and the ‘jump’ . This choices of correspond respectively to a quarterly, monthly, and weekly time discretization. We will restrict ourselves to ‘jumps’ . On the one hand, this ensures that the ‘jumps’ are significant; see the discussion above. On the other hand, as just discerned from Figure 1, the effect of jumps ‘down’ are more significant than jumps ‘up’.

From Figure 2 one can see that for each trading time and any the (negative) effect of incorporating a ‘jump’ in the dynamics of an asset price is the smaller the smaller the spread between the drift of the asset and the drift of the bond. There is only a tiny (nearly invisible) difference between the ‘Hadamard derivative’ for the trading times . So the fineness of the discretization seems to play a minor part. Next we compare the values of for the drift of the bond in dependence of the risk aversion parameter and the ‘jump’ .

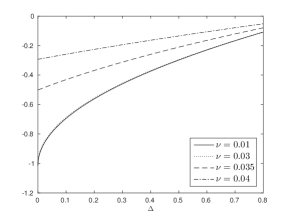

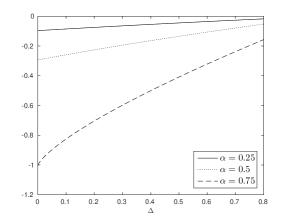

As appears from Figure 3, for any the (negative) effect of incorporating a ‘jump’ in the dynamics of an asset price is the smaller the higher the agent’s risk aversion, no matter what the drift of the bond looks like. Take into account that the extent of this effect is influenced via (41)–(47) by the optimal fraction to be invested into the asset which in turn depends on the risk aversion parameter (see (36)).

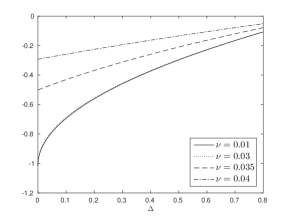

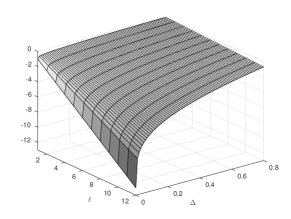

Finally, let us briefly touch on the case where more than one jump may appear. More precisely, instead of (with ) consider the transition function (with , , pairwise distinct) which is still generated by means of (40) but with the difference that at the different times the distribution is replaced by . Just as in the case , it turns out that it does not matter at which times exactly these jumps occur. Figure 4 shows the value of in dependence on and . It seems that for any fixed the first-order sensitivity increases approximately linearly in .

Supplementary material

The supplementary material illustrates the setting of Sections 2–3 in the case of finite state space and action spaces, and contains the proofs of the results from Sections 3–4. Moreover, supplemental definitions and results to Section 2 are given and the existence of optimal strategies in general MDMs is discussed. Finally, an supplemental topological result is shown.

References

- [1] Averbukh, V. I. and Smolyanov, O. G. (1967). The theory of differentiation in linear topological spaces. Russian Mathematical Surveys, 22, 201–258.

- [2] Bäuerle, N. and Rieder, U. (2011). Markov decision processes with applications to finance. Springer, Berlin.

- [3] Bauer, H. (2001). Measure and integration theory. de Gruyter, Berlin.

- [4] Bellini, F., Klar, B., Müller, A. and Rosazza Gianin, E. (2014). Generalized quantiles as risk measures. Insurance: Mathematics and Economics, 54, 41–48.

- [5] Bertsekas, D. P. (1995). Dynamic programming and optimal control. Vol. 1, Athena scientific, Belmont.

- [6] Cox Jr., S. H. and Nadler Jr., S. B. (1971). Supremum norm differentiability. Annales Societatis Mathematicae Polonae, 15, 127–131.

- [7] Dall’Aglio, G. (1956). Sugli estremi di momentidetle funzioni di ripartizione doppia. Annali Scuola Normale Superiore di Pisa, 10, 35–74.

- [8] Dudley, R. M. (2002). Real analysis and probability. Cambridge University Press, Cambridge.

- [9] Fernholz, L. T. (1983). Von Mises calculus for statistical functionals. Springer, Berlin.

- [10] Föllmer, H. and Schied, A. (2011). Stochastic finance. An introduction in discrete time. de Gruyter, Berlin.

- [11] Gill, R. D. (1989). Non- and semi-parametric maximum likelihood estimators and the von mises method - I. Scandinavian Journal of Statistics, 16, 97–128.

- [12] Hernández-Lerma, O. and Lasserre, J. B. (1996). Discrete-time Markov control processes: basic optimality criteria. Springer, Berlin.

- [13] Hinderer, K. (1970). Foundations of non-stationary dynamic programming with discrete time parameter. Lecture Notes in Economics and Mathematical Systems 33, Springer, Berlin.

- [14] Hinderer, K. (2005). Lipschitz continuity of value functions in Markovian decision processes. Mathematical Methods of Operations Research, 62, 3–22.

- [15] Holfeld, D. and Simroth, A. (2017). Learning from the past — risk profiler for intermodal route planning in SYNCHRO-NET. International Conference on Operations Research (OR2017), Berlin.

- [16] Holfeld, D., Simroth, A., Li, Y., Manerba, D. and Tadei, R. (2018). Risk analysis for synchro-modal freight transportation: the SYNCHRO-NET approach. Seventh International Workshop on Freight Transportation and Logistics (Odysseus 2018), Cagliari.

- [17] Kallenberg, O. (2002). Foundations of modern probability. Springer, Berlin.

- [18] Kantorovich, L. V. and Rubinstein, G. S. (1958). On a space of completely additive functions. Vestnik Leningrad University, 13, 52–59.

- [19] Kiesel, R., Rühlicke, R., Stahl, G. and Zheng, J. (2016). The Wasserstein metric and robustness in risk management. Risks, 4, 32.

- [20] Kolonko, M. (1983). Bounds for the regret loss in dynamic programming under adaptive control. Zeitschrift für Operations Research, 27, 17–37.

- [21] Komljenovic, D., Gaha, M., Abdul-Nour, G., Langheit, C. and Bourgeois, M. (2016). Risks of extreme and rare events in asset management. Safety Science, 88, 129–145.

- [22] Krätschmer, V., Schied, A. and Zähle, H. (2012). Qualitative and infinitesimal robustness of tail-dependent statistical functionals. Journal of Multivariate Analysis, 103, 35–47.

- [23] Krätschmer, V., Schied, A. and Zähle, H. (2017). Domains of weak continuity of statistical functionals with a view toward robust statistics. Journal of Multivariate Analysis, 158, 1–19.

- [24] Krätschmer, V. and Zähle, H. (2017). Statistical inference for expectile-based risk measures. Scandinavian Journal of Statistics, 44, 425–454.

- [25] Lemor, J. P., Gobet, E. and Warin, X. (2006). Rate of convergence of an empirical regression method for solving generalized backward stochastic differential equations. Bernoulli, 12, 889–916.

- [26] Merton, R. C. (1969). Lifetime portfolio selection under uncertainty: the continuous-time case. The review of Economics and Statistics, 51, 247–257.

- [27] Müller, A. (1997). How does the value function of a Markov decision process depend on the transition probabilities ? Mathematics of Operations Research, 22, 872–885.

- [28] Müller, A. (1997). Integral probability metrics and their generating classes of functions. Advances in Applied Probability, 29, 429–443.

- [29] Pham, H. (2009). Continuous-time stochastic control and optimization with financial applications. Springer, Berlin.

- [30] Puterman, M. L. (1994). Markov decision processes: discrete stochastic dynamic programming. Wiley, New York.

- [31] Rachev, S. T. (1991). Probability metrics and the stability of stochastic models. Wiley, New York.

- [32] Römisch, W. (2004). Delta method, infinite dimensional. Encyclopedia of Statistical Sciences, Wiley, New York.

- [33] Rudin, W. (1991). Functional Analysis. McGraw-Hill, New York.

- [34] Schäl, M. (1975). Conditions for optimality in dynamic programming and for the limit of -stage optimal policies to be optimal. Zeitschrift für Wahrscheinlichkeitstheorie und verwandte Gebiete, 32, 179–196.

- [35] Schirotzek, W. (2007). Nonsmooth analysis. Springer, Berlin.

- [36] Sebastião e Silva, J. (1956). Le calcul différentiel et intégral dans les espaces localement convexes, réels ou complexes, Nota I. Rendiconti, Atti della Accademia Nazionale dei Lincei, Serie VIII, Vol. VIII, 743–750.

- [37] Shapiro, A. (1990). On concepts of directional differentiability. Journal of Optimization Theory and Applications, 66, 477–487.

- [38] https://www.synchronet.eu/

- [39] Vallender, S. S. (1974). Calculation of the Wasserstein distance between probability distributions on the line. Theory of Probability and its Applications, 18, 784–786.

- [40] Van Dijk, N. M. (1988). Perturbation theory for unbounded Markov reward processes with applications to queueing. Advances in Applied Probability, 20, 99–111.

- [41] Van Dijk, N. M. and Puterman, M. L. (1988). Perturbation theory for Markov reward processes with applications to queueing systems. Advances in Applied Probability, 20, 79–98.

- [42] Villani, C. (2003). Topics in optimal transportation. American Mathematical Society, vol. 58.

- [43] Wessels, J. (1977). Markov programming by successive approximations with respect to weighted supremum norms. Journal of Mathematical Analysis and Applications, 58, 326–335.

- [44] Yang, M., Khan, F., Lye, L. and Amyotte, P. (2015). Risk assessment of rare events. Process Safety and Environmental Protection, 98, 102–108.

- [45] Zolotarev, V. M. (1983). Probability metrics. Theory of Probability and its Applications, 28, 278–302.

5 Supplement: The discrete case as an illustrating example

In Sections 2–3 we work in a rather general set-up. This implies that we cannot avoid dealing with ‘advanced’ objects. In the special case where the state space and the action spaces are finite the situation is different. In this case it is possible to present the basic definitions and the main result (Theorem 3.14) in a more comprehensible way. For the moment we assume that the reader is already familiar with the basic terminology of MDMs. Otherwise we advise the reader to first read Section 2. In Section 5.5 it will be discussed how the following elaborations fit to the general set-up of Sections 2–3.

5.1 Basic model components

Let be a finite state space, be a fixed finite time horizon, and be the finite set of possible actions that can be performed when the MDP is in state at time . For any , , and , the (one-step transition) probability measure on from which the state of the MDP at time is drawn, given that the MDP is in state and action is selected at time , can be identified with an element of . Here is the set of all vectors from whose entries are nonnegative and sum up to , and specifies the probability that the MDP will be in state at time , given it is in state and action is selected at time . In particular, if the initial state is fixed and refers to the corresponding index (i.e. ), the vector

| (48) |

in , with , can be identified with the transition probability function, i.e. with the ensemble of all transition probabilities. Here is the ‘clueing operator’ defined by . In fact is even an element of the following subset of :

| (49) |

If denotes the optimal value of the MDM based on transition probability function , then can be seen as a map from () to .

5.2 Definition of first-order sensitivity in the discrete case

It is tempting to consider the classical Fréchet (or total) derivative of at in order to obtain a tool for measuring the first-order sensitivity of the optimal value w.r.t. a change from to :

| (50) |

for any with , where is the closed ball in around with radius and . This approach is indeed expedient to some extent. However, one has to note that may lie outside ’s domain . To avoid this problem, we replace condition (50) by the following variant of (50):

| (51) |

for any with . Take into account that lies in for any and . Also note that, if is equipped with the max-norm, is contained in for any .

For classical Fréchet (or total) differentiability the derivative is required to be linear and continuous. On the one hand, for ‘Fréchet differentiability’ (see Definition 5.1) we will also require a sort of continuity, namely that the mapping from to is continuous, where is equipped with the relative topology of . On the other hand, the domain of is given by and thus not a linear space. Therefore linearity of is an indefinite property.

In view of (1), the quantity can be seen as a measure for the first-order sensitivity of the optimal value under transition probability function w.r.t. a change from to , with small. For this interpretation it is actually not necessary to require that is continuous or that the convergence in (51) holds uniformly in . One can indeed be content with the directional derivative, i.e. with the convergence in (51) for fixed . Nevertheless continuity and uniformity are natural wishes in this context, because they ensure stability of the first-order sensitivity w.r.t. small modifications of as well as comparability of the first-order sensitivity of (infinitely) many different . We refer to the discussion subsequent to (1).

Definition 5.1

A map is said to be ‘Fréchet differentiable’ at if there exists a map for which (51) (with replaced by respectively) holds and for which the mapping from to is continuous. In this case is called ‘Fréchet derivative’ of at .

5.3 Computation of first-order sensitivity in the discrete case

To specify the ‘Fréchet derivative’ of at we need some further notation. For any strategy , we use to denote the expected total reward (from time to ) when is the underlying transition probability function and the decisions are performed according to . In the finite setting there exists under at least one optimal strategy , i.e. a strategy with . We will write for the (finite) set of all optimal strategies w.r.t. . Then the results of Subsection 3.5 show that the ‘Fréchet derivative’ of at is given by

| (52) |

where refers to the ‘Fréchet derivative’ of at . The latter can be obtained from a suitable iteration scheme. According to Remark 3.19 we indeed have

(recall that is the initial state and that refers to a strategy) for

| (53) | ||||

, where the are given by the usual backward iteration scheme (see, e.g., Lemma 3.5 in [13] or p. 80 in [30]) for the computation of :

| (54) | ||||

. Here specifies the (one-stage) reward when making decision at time in state , and specifies the reward of being in state at terminal time . Also note that determines the action which is taken at time in state under strategy .

5.4 An example: stochastic inventory control

In this subsection we will consider an inventory control problem, which is a classical example in discrete dynamic optimization; see, e.g., [5, 12, 30] and references cited therein. At first, we introduce in Subsection 5.4.1 a (simple) inventory control model and formulate the corresponding inventory control problem. Thereafter, in Subsection 5.4.2, we will explain how the inventory control model can be embedded into the setting of Subsection 5.1. Finally, in Subsection 5.4.3 we will present some numerical examples for the ‘Fréchet derivative’ established in Subsection 5.3.

5.4.1 Basic inventory control model, and the target

Consider an -period inventory control system where a supplier of a single product seeks optimal inventory management to meet random commodity demand in such a way that a measure of profit over a time horizon of periods is maximized. For the formulation of the model, let be -valued independent random variables on some probability space , where can be seen as the random demand of the single product in the period between time and time . We denote by the counting density of (i.e. ) and assume that is known for any . Note that , where denotes the space of all real-valued sequences whose entries are nonnegative and sum up to . Let be the trivial -algebra, and set for any .

We suppose that within each period of time the available inventory level of the single product is restricted to units (for some fixed ) and that there is no backlogging of unsatisfied demand at the end of each period. The latter means that if at the end of a period the demand exceeds the current inventory, then the whole inventory is sold and the surplus demand gets lost.

Given an initial inventory level , the supplier intends to find optimal order quantities according to an order strategy to maximize some measure of profit. By order strategy we mean an ()-adapted -valued stochastic process , where specifies the amount of ordered units of the single product at the beginning of period . Here we suppose that the delivery of any order occurs instantaneously. Since excess demand is lost by assumption, the corresponding inventory (level) process associated with is given by

| (55) |

Note that corresponds to the amount of units of the single product sold in the period between time and time . Hence we refer to the process defined by

| (56) |

as sales process associated with .

In view of (55) and since the inventory capacity is restricted to units, we may and do identify any order strategy with an ()-adapted -valued stochastic process satisfying and for all . We restrict ourselves to Markovian order strategies which means that only depends on and . To put it another way, we suppose that for any there is some map such that . Hence, for given strategy (resp. ) the process is a -valued -Markov process whose one-step transition probability for the transition from state at time to state at time is given by with

| (57) |

The supplier’s aim is to find an order strategy (resp. ) for which the expected total profit is maximized. Here the profit can be seen as the difference between the sales revenue and the costs for ordering and holding the single product. For the sake of simplicity, we suppose that the sales revenue as well as the ordering and holding costs are known and linear in each period. Hence, we are interested in those order strategies (resp. ) for which the expectation of

is maximized, where and are for some fixed defined by

Note here that , and denote the sales revenue, the ordering costs, the fixed ordering costs, and the holding costs per unit of the single product, respectively.

5.4.2 Embedding into MDM, and optimal order strategies

The setting introduced in Subsection 5.4.1 can be embedded into the setting of Subsections 5.1 and 5.3 as follows. Let for the enumeration (with ) of given by with and (here is the ceiling function), .

Let with and for any and . For any , , and , let the component of the vector from (48) be given by

| (58) |

for some predetermined and for introduced in (57). In fact any element of is generated via (57)–(58) by some -tuple of counting densities on ; here should be seen as the counting densities of . The value in (58) should be seen as the probability of a transition from state to state in time between and (this transition probability is even independent of ).

For any and , set

| (59) | |||||

| (60) | |||||

| (61) |

By an (admissible) order strategy we understand an -tuple of maps satisfying

5.4.3 Numerical examples for the ‘Fréchet derivative’

Let us take up the numerical example at p. 41 in [30] where , , , , , and . We fix with , and denote by the unique element of generated by through (57)–(58). This choice of means that in each period the demand is , , or with probability , , and , respectively. Table 2 provides the (unique) optimal order strategy , and the second column of Table 3 displays the maximal expected total reward of the inventory control problem (62) for all possible initial inventory levels . Moreover, the last two columns in Table 3 display the ‘Fréchet derivative’ of at evaluated at direction and at direction (calculated with the iteration scheme (53)), again for all possible initial inventory levels . Here and are generated through (57)–(58) by and respectively, where and . As the optimal strategy is unique in our example, we even have .