High-dimensional vector autoregressive time series modeling via tensor decomposition

Abstract

The classical vector autoregressive model is a fundamental tool for multivariate time series analysis. However, it involves too many parameters when the number of time series and lag order are even moderately large. This paper proposes to rearrange the transition matrices of the model into a tensor form such that the parameter space can be restricted along three directions simultaneously via tensor decomposition. In contrast, the reduced-rank regression method can restrict the parameter space in only one direction. Besides achieving substantial dimension reduction, the proposed model is interpretable from the factor modeling perspective. Moreover, to handle high-dimensional time series, this paper considers imposing sparsity on factor matrices to improve the model interpretability and estimation efficiency, which leads to a sparsity-inducing estimator. For the low-dimensional case, we derive asymptotic properties of the proposed least squares estimator and introduce an alternating least squares algorithm. For the high-dimensional case, we establish non-asymptotic properties of the sparsity-inducing estimator and propose an ADMM algorithm for regularized estimation. Simulation experiments and a real data example demonstrate the advantages of the proposed approach over various existing methods.

Keywords: Factor model; High-dimensional time series; Reduced-rank regression; Tucker decomposition; Variable selection.

1 Introduction

High-dimensional time series is one of the most common types of “big data” and can be found in many areas including meteorology, genomics, finance and economics (Hallin and Lippi,, 2013). The classical vector autoregressive (VAR) model is fundamental to multivariate time series modeling and has recently been applied to the high-dimensional case under certain structural assumptions, e.g., the banded structure (Guo et al.,, 2016), network structure (Zhu et al.,, 2017), and linear restrictions (Zheng and Cheng,, 2020). Consider the VAR model of the form (Lütkepohl,, 2005; Tsay,, 2010):

| (1) |

where is the observed time series with , are independent and identically distributed () innovations with , and , s are transition matrices of unknown parameters, and is the sample size. It can be difficult to perform the estimation even when the dimensions and are moderately large (De Mol et al.,, 2008; Carriero et al.,, 2011; Koop,, 2013).

On the other hand, compared with model (1), the vector autoregressive moving average (VARMA) model usually performs better in practice since it can provide a more flexible autocorrelation structure (Athanasopoulos and Vahid,, 2008; Chan et al.,, 2016). However, the VARMA model may have a serious identification problem (Chan et al.,, 2016; Wilms et al.,, 2017; Dias and Kapetanios,, 2018), and its estimation is often unstable since the corresponding objective function involves a high-order polynomial. As a result, it is common in practice to employ a VAR model to approximate VARMA processes, and the order may be very large in order to provide a better fit for the data (Ravenna,, 2007). For example, to guarantee the approximation accuracy, we need to assume that and as for univariate and multivariate cases (Said and Dickey,, 1984; Li et al.,, 2014). This makes the number of parameters in model (1), , much larger.

Therefore, to make inference on the VAR model for high-dimensional time series, it is necessary to restrict the parameter space of model (1) to a reasonable number of degrees of freedom. A direct method is to assume that the transition matrices s are sparse and apply sparsity-inducing regularized estimation, e.g., the -regularization (Lasso or Dantzig selector) for VAR models (Kock and Callot,, 2015; Davis et al.,, 2016; Basu and Michailidis,, 2015; Han et al.,, 2015; Wu and Wu,, 2016). However, unlike the traditional linear regression, time series data have non-negligible temporal and cross-sectional dependencies, which will seriously affect the accuracy of the regularized estimation. Moreover, as explained in Remark 1 in Section 2, the stationarity of the VAR model essentially entails that the average magnitude of parameters is bounded by . This makes the variable selection much more challenging and hence limits the popularity of sparsity-inducing regularized estimation for time series data.

Another important approach to reducing the dimensionality of model (1) arises naturally from the reduced-rank regression (Yuan et al.,, 2007; Negahban and Wainwright,, 2011; Chen et al.,, 2013; Raskutti et al.,, 2019; Basu et al.,, 2019). The VAR model in (1) can be rewritten as

| (2) |

where , and is assumed to have a low rank (Velu et al.,, 1986; Velu and Reinsel,, 2013). Based on the reduced-rank VAR model in (2), Carriero et al., (2011) considered a Bayesian method to predict large macroeconomic data, and both the number of variables and the sample size diverge to infinity. However, unlike the reduced-rank regression, we may have alternative ways to define the low-rankness of parameter matrices s with . Specifically, the rank of is the dimension of the column space of s. Denote and , where is the vectorization of . The ranks of and are then the dimensions of the row space and vectorized matrix space of s, respectively. The three dimensions are different in general, and the corresponding low-rank structures have different physical interpretations; see Section 2 for details. Similarly to model (2) above, Reinsel, (1983) proposed an autoregressive index model, where the low-rank assumption was imposed on . Moreover, the transition matrices s may have a low-rank structure along different lags, i.e. may be low-rank. In fact, the VARMA model can be treated as a parsimonious formulation for VAR models, since it restricts the degrees of freedom on transition matrices over different lags (Tsay,, 2010).

It is noteworthy that imposing the low-rank assumption on any one of , and leads to a different physical interpretation as it amounts to reducing the dimensionality along one of the three different directions. This inspires us to rearrange the transition matrices s into a tensor. Interestingly, the corresponding mode-1, -2 and -3 matricizations of the tensor happen to be , and , respectively; see Kolda and Bader, (2009) and Section 2. By adopting the standard Tucker decomposition for the transition tensor, different low-rank structures can be assumed simultaneously along the three directions, and hence the parameter space of the VAR model can be efficiently restricted. We call the resulting model the multilinear low-rank VAR model, since the Tucker ranks are also called multilinear ranks.

In the literature, low-rank structures of high-dimensional time series are commonly explored through factor models (Stock and Watson,, 2005; Bai and Ng,, 2008; Stock and Watson,, 2011; Bai and Wang,, 2016). Similarly, as a means of low-rank discovery for VAR processes, the proposed model is naturally interpretable from the factor modeling perspective. As we will discuss in Section 2.2, by imposing the low-rankness along three directions, the proposed model can extract different dynamic factors across response variables, predictor variables, and predictor time lags. Indeed, the proposed model can be written as a static factor model (SFM) (Bai and Wang,, 2016) yet endowed with additional low-rank structures for more substantial dimension reduction. However, in contrast to factor models which are mainly used for interpretation, it is worth noting that the proposed model can be used for forecasting. On the other hand, the dynamic factor model (DFM) in the literature can be constructed by combining the SFM with a certain dynamic structure for the latent factors (Stock and Watson,, 2011). Compared to the DFM with VAR latent factors (Amengual and Watson,, 2007), the proposed model may be more flexible in the sense that it can extract different sets of dynamic factors from the response and the lagged predictors s, whereas the DFM restricts them to be identical. In addition, the proposed model can capture the possible low-rank structure across the time lags.

Another important contribution of this paper is to introduce a sparse decomposition for the transition tensor to further increase the estimation efficiency for much higher-dimensional time series data. In the literature, sparsity-inducing regularization has been widely considered in reduced-rank regression to improve interpretability and efficiency. For example, Chen and Huang, (2012) and Bunea et al., (2012) considered row-wise sparsity in singular value decomposition, where zero rows imply irrelevance of the corresponding predictors to the responses; Lian et al., (2015) proposed to directly restrict the rank of the coefficient matrix with entry-wise sparsity, which however does not lead to a sparse decomposition; Chen et al., (2012) obtained a sparse singular value decomposition of the coefficient matrix by slightly relaxing the strict orthogonality; and Uematsu et al., (2019) achieved the sparsity and strict orthogonality simultaneously. Note that as in Uematsu et al., (2019), our estimation method is able to keep the strict orthogonality of the factor matrices in the tensor decomposition.

Our work is also related to the fast-growing literature on tensor regression; see, e.g., Zhou et al., (2013), Li et al., (2018), Li and Zhang, (2017), Sun and Li, (2017) and Raskutti et al., (2019). Whereas most of the existing work focuses on tensor-valued predictors or responses, we employ tensor decomposition as a novel approach to the dimensionality reduction of vector-valued time series models. To summarize, the proposed methods have the following attractive features:

-

(a)

The proposed model substantially reduces the dimension along three directions of the transition tensor, allowing each direction to have a different low-rank structure. This results in interpretable physical structures and interesting connections with factor models in the literature, and allows us to handle much higher dimensional data than the reduced-rank VAR model in (2).

-

(b)

Through the sparsity assumption on the three factor matrices, the proposed high-dimensional method further improves the model interpretability and estimation efficiency by selecting important variables for each response, predictor or temporal factor. The corresponding estimation can be accomplished by an ADMM algorithm which effectively untangles the -regularization and orthogonality constraints.

The rest of the paper is organized as follows. Section 2 introduces the proposed model and discusses its connections with factor models. Section 3 presents asymptotic properties of the least squares estimator in low dimensions and an alternating least squares algorithm. For the high-dimensional case, the sparse higher-order reduced-rank estimation is proposed in Section 4, taking into account both the orthogonality and sparsity. Its non-asymptotic properties are established, and an ADMM algorithm is developed. A consistent rank selection method is proposed in Section 5. Simulation experiments and real data analysis are presented in Sections 6 and 7, respectively. A short discussion is given in Section 7. All technical proofs are given in the Appendix.

2 Multilinear low-rank vector autoregression

2.1 Tensor decomposition

Tensors, also known as multidimensional arrays, are natural higher-order extensions of matrices. A multidimensional array is called a th-order tensor, and the order of a tensor is known as the dimension, way or mode; we refer readers to Kolda and Bader, (2009) for a detailed review on tensor notations and operations. This paper will focus on third-order tensors.

Throughout the paper, we denote vectors by small boldface letters , , matrices by capital letters , , and tensors by Euler script capital letters , . For a vector , denote by and its and norms, respectively. For a matrix , denote by , , , , , , and its Frobenius norm, vectorized norm (i.e. ), “norm”, spectral norm, nuclear norm, vectorization, transpose and the -th largest singular value, respectively. For two symmetric matrices and , we write if is positive semidefinite. Furthermore, for a tensor , let and be its Frobenius norm and “norm”, respectively.

For a tensor , its mode-1 matricization is defined as the -by- matrix whose -th entry is , for and , and contains all mode-1 fibers . The mode-2 and mode-3 matricizations can be defined similarly. The matricization of tensors helps to link the concepts and properties of matrices to those of tensors. The mode-1 multiplication of a tensor and a matrix is defined as

| (3) |

Multiplications and can be defined similarly.

Unlike matrices, there is no universal definition of the rank for tensors. In this paper, we consider the multilinear ranks of a tensor , where

| (4) |

and and are the ranks of and , respectively. Note that , and are analogous to the row rank and column rank of a matrix, but these three ranks are not necessarily equal. The multilinear ranks are also known as Tucker ranks, as they are closely related to the Tucker decomposition.

2.2 Multilinear low-rank vector autoregression

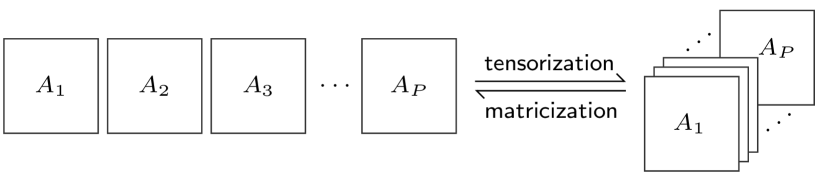

For the VAR model in (1), we can rearrange its transition matrices into a tensor ; see Figure 1 for an illustration. Denote by the mode- matricization of , where . It can be verified that , and , which correspond to the column, row and vectorized matrix spaces of s, respectively.

If the transition tensor has multilinear low ranks , i.e. for , then there exists a Tucker decomposition, or , where is the core tensor, and , and are factor matrices. As a result, model (1) can be written as

| (5) |

where . For simplicity, we call model (5) the multilinear low-rank VAR model.

In addition, since , where is the Kronecker product, model (5) also has the following equivalent forms

| (6) |

where .

Assumption 1.

All roots of the matrix polynomial , , are outside the unit circle, where is the set of complex numbers.

Assumption 1 is the sufficient and necessary condition for the existence of a unique strictly stationary solution to model (1). When , Assumption 1 is equivalent to , where denotes the spectral radius of .

Remark 1.

To gain insight into the effect of the stationarity condition on the entries of , we may consider the following result regarding random matrices. Suppose that the entries of are with mean zero and variance , that is, they are equally important. Then, by Bai, (1997), in probability as . In other words, when , a larger will shrink the entries of towards zero.

Note that the Tucker decomposition in (5) is not unique since for any nonsingular matrices , and . Hence, we consider a special Tucker decomposition: the higher-order singular value decomposition (HOSVD); see De Lathauwer et al., (2000). Specifically, we let be a tall matrix consisting of the top left singular vectors of for each , where are the multilinear ranks of the tensor . Let the core tensor . Then has the following all-orthogonal property: for each , the rows of are pairwise orthogonal.

Remark 2.

Since is orthonormal, it follows from (6) that

| (7) |

The above representation reveals an interesting dynamic factor based interpretation for the proposed model. Specifically, represents response factors across the variables of , where is the th response factor, for . Thus, if the th entry of is zero, i.e., , then is irrelevant to . In other words, can be interpreted as the loadings of the response factors.

On the right side of (7), the predictor has the bilinear form . On the one hand, represents predictor factors across the variables (rows) of the predictor matrix , where is the th predictor factor, for , with for . Hence, if , then is irrelevant to . On the other hand, represents temporal factors across the time lags (columns) of the predictor matrix , where is the th temporal factor, for . As a result, implies that the -th lagged predictor is irrelevant to . Therefore, and can be interpreted as the loadings of the predictor and temporal factors, respectively.

For simplicity, we call , and the response, predictor and temporal ranks, respectively. Similar formulations can be found in matrix variate regressions (e.g., Zhao and Leng,, 2014; Ding and Cook,, 2018). The response, predictor and temporal factors interpretations of (7) reveal that the proposed model is related to factor modeling, one of the most widely used techniques for high-dimensional time series. We will explore the similarities and differences between them in the next subsection.

2.3 Connections with factor modeling for time series

In the literature, low-rank structures of high-dimensional time series are commonly explored through factor models (Stock and Watson,, 2005; Bai and Ng,, 2008; Stock and Watson,, 2011; Bai and Wang,, 2016). The multilinear low-rank assumption of in the proposed model fulfills a similar purpose as it extracts dynamic factors along three dimensions, as shown in our discussion about (7). Meanwhile, the proposed model can be used directly for forecasting, which is another attractive feature compared to factor models. In the following, we take a closer look at the factor structures of the proposed model and both static and dynamic factor models in the literature, and discuss some interesting connections between them.

The static factor model (SFM) is commonly written as

| (8) |

where is the observed time series, are latent factors with , is the factor loading matrix, and is the random error. The usual normalization restrictions require that and that is a full-rank diagonal matrix, where ; see Bai and Wang, (2016).

We can show that the proposed model in (6) has an SFM representation. Specifically, as shown in Section E of the Appendix, there exist and such that

| (9) |

for , where and the resulting satisfy the aforementioned normalization restrictions, and is the normalized version of . Let denote the column space of a matrix, and it can be verified that .

Remark 3.

Consider generated by the proposed model. A useful by-product of representation (9) is that the low-dimensional subspace can actually be estimated by , where is the estimator of obtained by fitting an SFM with . Moreover, let be the orthonormalization of . Then , and their orthogonal projectors are identical, namely . Thus, the estimation error of can be measured by the commonly-used subspace distance , where ; see Vu and Lei, (2013).

On the other hand, the dynamic factor model (DFM) can be defined by combining model (8) with a certain dynamic structure, e.g., the VAR, for the latent factor process (Amengual and Watson,, 2007). To fix ideas, suppose that evolves as the VAR(1),

| (10) |

where is the transition matrix, and is the random error. Let and . Then, the conjunction of (8) and (10) can also be written as

| (11) |

where is diagonal, is orthonormal, and . Interestingly, (11) resembles the VAR with measurement error, where is the observed outcome of the true VAR(1) process subject to measurement error . Note that the naive estimation ignoring the measurement error of the autoregressive process will result in asymptotic biases; see, e.g., Staudenmayer and Buonaccorsi, (2005).

However, if , we may gain more insights by comparing the DFM in (11) to the proposed model of lag order one. Note that when the latter reduces to the reduced-rank VAR,

with and being orthonormal and , while the DFM model in (11) with has the form of

Hence, we may argue that the proposed model is more flexible than the DFM in (11), as the former can accommodate different low-dimensional patterns for the response and predictors s, whereas the latter requires the subspaces of and s to be identical. It is also worth noting that when , another advantage of the proposed model is that it can capture the possible low-rank structure across time lags of the predictors; see (7) in the previous subsection. Lastly, we note that the proposed model may be extended along the line of the factor augmented VAR models (FAVAR) (Bernanke et al.,, 2005) by incorporating known low-dimensional factors.

Remark 4.

In contrast to the proposed model, the classical factor model in the general form of (8) is not specific to VAR models, since it allows for general latent factors. However, the general factor model in (8) cannot be directly used for forecasting unless an additional dynamic structure is imposed on the latent factor process, e.g., (10). As discussed above, if the multilinear low-rank assumption holds, the proposed model can be more favorable than the DFM.

3 Low-dimensional time series modeling

3.1 Multilinear low-rank least squares estimation

For the multilinear low-rank VAR model in (5) with ranks , the multilinear low-rank (MLR) least squares estimator can be defined as

| (12) |

where

| (13) |

We will derive asymptotic properties of when both and are fixed and the true multilinear ranks are known. Note that the minimization in (12) is unconstrained, so the Tucker decomposition of is not unique.

Let be the true value of the vectorized HOSVD components and be the corresponding estimator. Let be a function of . Let , with ,

and . Denote

| (14) |

where is an permutation matrix such that with .

Theorem 1.

The proof of Theorem 1 relies on the technique for deriving asymptotic distributions of overparameterized models in Shapiro, (1986). It does not require that and s are identifiable, nor does it require imposing identification constraints on the estimation in (12).

However, if we are further interested in estimating the true components and s in the HOSVD of , the identifiability of these components, i.e., the uniqueness of the HOSVD, will be required. This is guaranteed by the following assumption.

Assumption 2.

For each , (i) the singular values of are distinct, and (ii) the first element in each column of is positive.

In Assumption 2, Condition (i) avoids indeterminacy of the factor loading vectors and holds generally in practice. Condition (ii) rules out sign switches in and is commonly used in low-rank matrix models (Li et al.,, 2016).

Accordingly, based on the unconstrained estimator , we can define each uniquely as the top left singular vectors of such that the first element in each column of is positive, and set . As a result, the estimators and s are consistent and asymptotically normal.

Corollary 1.

The next corollary shows that the proposed estimator is asymptotically more efficient than the ordinary least squares (OLS) estimator

for the full VAR model in (1) and the reduced-rank regression (RRR) estimator

for the reduced-rank VAR model in (2), where is the rank of . Denote by and the transition tensors formed by and , respectively.

Corollary 2.

Under the conditions of Theorem 1, and in distribution as . Moreover, it holds that .

3.2 Alternating least squares algorithm

Let be the -field generated by and recall that . The objective function in (12) is a nonlinear function of , , and . However, from model (5), we have

| (16) |

which implies that the objective function in (12) is linear with respect to any of , , and when the other three are fixed.

Given the multilinear ranks , we can employ Algorithm 1 to find . Note that this is an alternating least squares algorithm where each step has a closed-form solution. In practice, the multilinear ranks need to be selected consistently, and we relegate the details to Section 5. The following proposition gives the convergence property of Algorithm 1.

Proposition 1.

Suppose that the stationary points of the objective function in (12) are isolated, up to an arbitrary nonsingular linear transformation. Then converges to a stationary point as , where . Moreover, let be a strict local minimum of the objective function. Then will be attracted to if the initial value is sufficiently close to .

Initialize:

HOSVD: with multilinear ranks

repeat

until convergence

Finalize: top left singular vectors of with positive first elements,

Remark 5.

If the sample size is sufficiently large, by Corollary 2, can be used as the initial value of Algorithm 1. For smaller sample sizes, or the nuclear norm estimator to be discussed in Section 5 can be employed instead. Moreover, Algorithm 1 does not guarantee convergence to the global solution defined in (12). As a result, in practice, we recommend a random initialization method with , where is a preliminary estimate, say, or , and is a random perturbation whose entries are drawn independently from . Many randomized initial values can be tried, and the solution which yields the smallest value for the objective function will be adopted.

Remark 6.

Algorithm 1 corresponds to the unconstrained estimation in (12). Thus, we do not need the orthogonality constraints of and s. The unidentifiability of the Tucker decomposition does not affect the convergence of the algorithm, since Proposition 1 does not require that the convergent sequence is unique. Moreover, note that the final estimates and s in Algorithm 1 are obtained from the unconstrained estimate of , which is consistent with the definitions of and s in Corollary 1. Similar alternating algorithms without imposing identification constraints can be found in the literature of tensor decomposition; see, e.g. Zhou et al., (2013) and Li et al., (2018).

4 High-dimensional time series modeling

4.1 Sparse higher-order reduced-rank VAR

As discussed in Section 2.2, the proposed model can effectively capture the dynamic information along three dimensions by response, predictor and temporal factors, with and representing the the corresponding factor loadings. However, when the dimensions and/or are very large, the fitted loading matrices often contain many small values, indicating relatively insignificant contribution of certain variables or lags to the factors. For example, if the th entry of is very small, then may be irrelevant to the th response factor, with and ; see also the discussion below (7) for similar interpretations regarding and .

To improve the interpretability, we may shrink the small values in the factor loading matrices to zero by imposing sparsity assumptions on s. This allows us to substantially reduce the number of unknown parameters while performing data-driven variable selection for each factor, and hence the estimation efficiency is also improved; see Chen et al., (2012) and Uematsu et al., (2019).

Specifically, we introduce the following -penalized Sparse Higher-Order Reduced-Rank (SHORR) estimator:

| (17) |

subject to

| (18) |

where is defined as in (13), and . Unlike the unconstrained estimation in (12), the orthogonality constraints in (18) are necessary; otherwise, the sparsity patterns of cannot be identified. As in Section 3, we will derive the statistical properties of the proposed estimator under the true multilinear ranks , while a consistent rank selection procedure will be discussed in Section 5.

Remark 7.

The proposed SHORR estimation method is different from the row-sparse reduced-rank regression that has been studied extensively in the literature (Chen and Huang,, 2012; Bunea et al.,, 2012). We avoid imposing the row-sparsity because (1) it would restrict the flexibility and interpretability of the VAR model, and (2) with a row-sparse response factor matrix , those unselected time series cannot be predicted at all. Thus, we consider the general sparsity structure for s rather than the row-sparsity.

Remark 8.

Alternatively, one might consider penalizing each individually, e.g. with the penalty term . Unfortunately, the three tuning parameters will bring about much higher computational costs and significant theoretical difficulties. To circumvent this problem, the SHORR estimator induces sparsity for , and jointly since . Implementation of this joint penalty is convenient through the alternating algorithm to be introduced in Section 4.3. Similar ideas of joint penalization can be found in the literature, e.g., the joint Lasso penalty in Zhao and Leng, (2014) and the joint penalty for left and right singular vectors for sparse SVD in Chen et al., (2012). Moreover, when is relatively small, we might wish to impose sparsity on and only, and then can be replaced by .

4.2 Theoretical properties of the SHORR estimator

To derive the non-asymptotic estimation and prediction error bounds of the SHORR estimator, we make the following assumptions.

Assumption 3.

(Gaussian error) The errors are Gaussian random vectors with mean zero and positive definite covariance matrix .

Assumption 4.

(Sparsity) Each column of the factor matrices has at most nonzero entries, for .

Assumption 5.

(Restricted parameter space) The parameter space for and with is , where with and , and is a uniform lower threshold for elements of s.

Assumption 6.

(Relative spectral gap) The nonzero singular values of satisfy that for and , where is a positive constant.

Assumption 3 enables us to apply the concentration inequalities for VAR models in Basu and Michailidis, (2015). The Gaussian condition may be relaxed to sub-Gaussianity by techniques in Zheng and Raskutti, (2019). Assumption 4 states the sparsity of each factor matrix. Assumption 5 imposes an upper bound on the core tensor , which is not a stringent assumption since large singular values in could cause nonstationarity of the VAR process. The lower threshold for the s is essential to restrict the estimation error to a subspace such that the restricted eigenvalue condition (Bickel et al.,, 2009) can be established. Note that may shrink to zero as the dimension increases, so this condition is not too stringent. Assumption 6 guarantees that the singular values of each are well separated. This rules out unidentifiability and allows us to derive the upper bound for the perturbation errors in Lemma 1 in Section D of the Appendix.

Assumption 1 guarantees that the eigenvalues of the Hermitian matrix over the unit circle are all positive, where denotes the conjugate transpose of . Following Basu and Michailidis, (2015), let

where and denote the minimum and maximum eigenvalues of a matrix, respectively. It holds that

| (19) |

and

| (20) |

Theorem 2.

Suppose that Assumptions 1 and 3-6 hold, and are known. If and , then

| (21) |

and

| (22) |

with probability at least , where are absolute constants, , , with , and .

Theorem 2 gives the non-asymptotic error upper bounds under high-dimensional scaling. When the multilinear ranks and lower threshold are fixed, (21) shows that is a consistent estimator if . In this setting, the estimation and prediction error bounds in (21) and (22) become and , respectively.

Remark 9.

Basu and Michailidis, (2015) considers estimation of stationary Gaussian VAR() models with sparse transition matrices such that . For the Lasso estimator , it was shown that and with high probability, which are consistent with the regular error bounds for the Lasso as corresponds to the number of parameters (e.g., Wang et al.,, 2015). In contrast, we assume that admits an HOSVD with sparse factor matrices , but itself is not necessarily sparse. When each is row-sparse with nonzero rows, for , it can be checked that is a sparse tensor with sparsity level . In this case, the SHORR estimator has the same error bounds as the Lasso estimator. However, in the general case, even when has a sparse HOSVD, may not be highly sparse, i.e., is larger than , so may be more efficient than .

4.3 ADMM algorithm

There are two major challenges in developing an efficient algorithm for the SHORR estimator. First, the core tensor is subject to the all-orthogonal constraint in (18) which cannot be handled in a straightforward way. Second, the -regularization in (17) and the orthogonality constraints in (18) are imposed jointly on s. The former is nonsmooth while the latter is nonconvex. To deal with these challenges, we adopt the alternating direction method of multipliers (ADMM) algorithm (Boyd et al.,, 2011) to update s and alternatingly; see Algorithm 2.

Firstly, to tackle the all-orthogonal constraint of , our idea is to separate it into three orthogonality constraints on the matricizations for . This is to say that can be decomposed as , where is a diagonal matrix, and , , and are orthonormal matrices with . Then, the augmented Lagrangian corresponding to the objective function in (17) can be written as

where , are the tensor-valued dual variables, and is the set of regularization parameters. This leads us to Algorithm 2. Note that all-orthogonal constraint of has been transferred to the matrices s in line 10, so no constraint is needed for updating in line 7 of Algorithm 2.

Secondly, we consider the update of s. Since in (13) is a least squares loss function with respect to each , the -update steps in lines 4-6 of Algorithm 2 are -regularized least squares problems subject to an orthogonality constraint, which can be written in the general form:

| (23) |

Since the -regularization and the orthogonality constraint for are difficult to handle jointly, we adopt an ADMM subroutine to separate them into two steps. Specifically, we introduce the dummy variable as a surrogate for and write problem (23) into the equivalent form as follows:

| (24) |

Then the corresponding augmented Lagrangian formulation is

| (25) |

where is the dual variable, and is a regularization parameter. The ADMM subroutine for (25) is presented in Algorithm 3. This yields solutions to the -update subproblems in Algorithm 2.

Note that the -update step in Algorithm 3 and the -update step in line 10 of Algorithm 2 are least squares problems with an orthogonality constraint. Hence, they can be solved efficiently by the splitting orthogonality constraint (SOC) method (Lai and Osher,, 2014). The -update step in Algorithm 3 is an -regularized minimization, which can be solved by the explicit soft-thresholding. The - and -update steps in lines 7 and 9 of Algorithm 2 are simple least squares problems.

For general nonconvex problems, it is well known that ADMM algorithms need not converge, and even if they do, they need not converge to an optimal solution. A comprehensive algorithmic convergence analysis for Algorithm 2 is challenging due to both the nested ADMM subroutine, Algorithm 3, and its interplay with the outer loop of Algorithm 2.

Wang et al., 2019b gives a rigorous convergence analysis of multi-block ADMMs for nonconvex nonsmooth optimization with linear equality constraints. Their theory would be applicable to Algorithm 3 if the -update step in line 3 were exact. The extension to the inexact -update step would require a sophisticated analysis of the optimization error of the SOC method. We do not delve into the development of the convergence theory further in this paper. Nonetheless, similarly to the analysis in Uematsu et al., (2019), under some high-level assumptions on , we can still obtain the following convergence result for Algorithm 2.

Proposition 2.

Remark 10.

The initial value for Algorithm 2 can be set to the nuclear norm (NN) estimator for low-rank VAR models (Negahban and Wainwright,, 2011), and it holds ; see also Section 5. Consequently, if one searches the SHORR estimator within a neighborhood of of radius , then all iterates will satisfy . Additionally, Theorem 2 implies , where is the global solution. A similar convex relaxation based initialization approach is used by Uematsu et al., (2019) for a nonconvex optimization problem with jointly imposed sparsity and orthogonality constraints. Moreover, since Algorithm 2 and Proposition 2 do not guarantee the convergence to a global solution, similarly to the random initialization method in Remark 5, in practice we can try many randomized initial values , where the entries of the perturbation are drawn independently from such that , and then select the final solution as the one with the smallest value for the objective function.

Remark 11.

The above algorithms are presented under known multilinear ranks and a fixed tuning parameter . In practice, to save computational costs, we recommend a two-step procedure: first select the ranks by the method to be introduced in Section 5, and then fixing these rank, select the tuning parameter by a fine grid search with information criterion such as the BIC or its high-dimensional extensions. Although the degrees of freedom in a sparse and orthogonal matrix are unclear, the total number of nonzero elements in , , and could be used as proxies.

5 Rank Selection

The theoretical results we derived for MLR and SHORR estimators hinge on correct multilinear ranks. This section introduces a procedure for consistent rank selection.

Suppose that is a consistent initial estimator of . We propose the following ridge-type ratio estimator (Xia et al.,, 2015) to estimate the multilinear ranks,

for , where , , and is a parameter that needs to be well chosen; see the assumption below. Here we allow , and the multilinear ranks to diverge with . For , denote

Assumption 7.

The parameter is chosen such that (i) and (ii) .

Remark 12.

In Assumption 7, Condition (i) states that the estimation error is dominated by , while Condition (ii) requires that grows much slower than s. Roughly speaking, Condition (ii) may be violated if the smallest nonzero singular value of is too small, or if there is a big drop from to , for some and . In either case, it will be more difficult for the ridge-type ratio to select the rank correctly. Note that if all the nonzero singular values are bounded above and away from zero, then Condition (ii) simply becomes .

Similar to the minimal signal assumption for variable selection consistency of sparsity-inducing estimators, Assumption 7 is essential to the rank selection consistency:

For the initial estimator, in this paper we use the nuclear norm (NN) estimator for low-rank VAR models defined as

Note that the estimation error rate derived in Negahban and Wainwright, (2011) for VAR(1) models can be readily extended to VAR() cases, which yields ; see also Remark 10. Then, the rank selection consistency in Theorem 3 would hold for a relatively large range of . In practice, we recommend using , which is shown to perform satisfactorily in the first simulation experiment of Section 6.

6 Simulation experiments

6.1 Rank selection consistency

As the rank selection method proposed in Section 5 will be used throughout all the following simulations and real data analysis in the next section, we first conduct an experiment to evaluate its consistency.

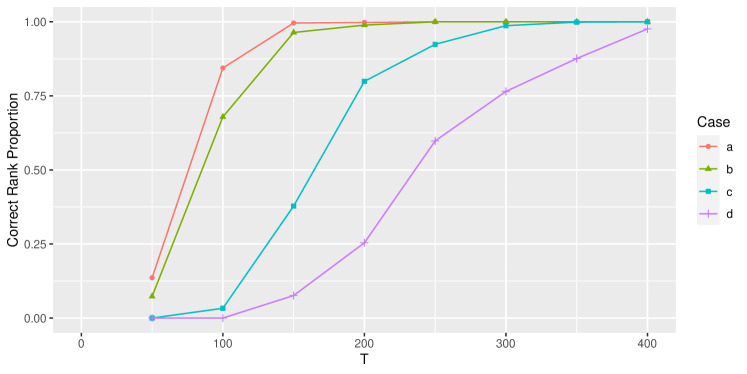

The data are generated from the proposed model in (5) with dimensions , multilinear ranks , and . To examine how the singular values of s impact the rank selection performance, we let be a diagonal cube with superdiagonal elements (case a), (case b), (case c), or (case d). As a result, the three nonzero singular values of every are exactly and . We generate the orthonormal factor matrices s as the first left singular vectors of Gaussian random matrices while ensuring that the stationarity condition in Assumption 1 holds. The parameter for the proposed ridge-type ratio estimator is set to . Figure 2 presents the proportion of correct rank selection, i.e., the event , across different sample sizes based on 1000 replications for each setting. First, it can be seen that the proportion increases as increases and reaches almost one when for all cases. Second, as noted in Remark 12, the rank selection may be more difficult if the smallest nonzero singular value is too small, or if there is a big gap between any two consecutive nonzero singular values. Thus, the better performance of cases a and b may be due to their larger compared to the other two cases. Moreover, it can be seen that cases a and c outperform cases b and d, respectively, which may be explained by the equality of the singular values and in the former cases.

6.2 Performance of MLR and SHORR estimators

We conduct two experiments to verify the theoretical properties of the proposed MLR and SHORR estimators.

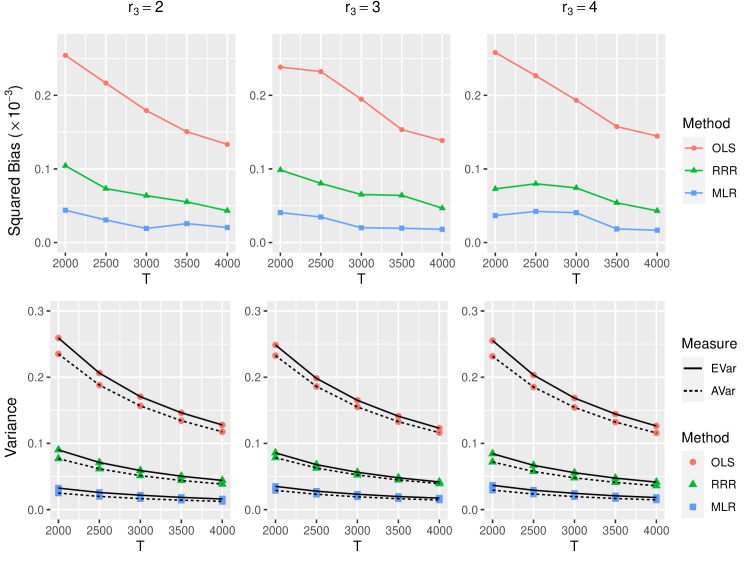

We first verify the asymptotic results in Section 3 for the proposed MLR estimator in comparison with the other two low-dimensional estimators, and . The data are generated from model (5) with , , , and or 4. We generate by scaling a randomly generated tensor with independent standard normal entries such that , and generate s by the same method as in the previous experiment. There are 1000 replications for each setting. Throughout this and all following experiments, the multilinear ranks are selected by the method in Section 5. For each estimator, i.e., or , we calculate the average bias across all elements of and all replications. The square of this average bias is plotted against in the upper panels of Figure 3. We also calculate the empirical and asymptotic variances for each element of according to Theorem 1 and Corollary 2. The averages of these empirical and asymptotic variances over all elements of and all replications, denoted by EVar and AVar, respectively, are plotted against in the lower panels of Figure 3. It can be seen that has much smaller squared bias, EVar and AVar than and . In addition, the EVar generally matches the corresponding AVar well, with their difference getting smaller as increases, although the EVar tends to overestimate the variances for all cases due to the large relative to the sample size. In sum, the asymptotic theory of the proposed MLR estimator in Section 3 is confirmed by this experiment.

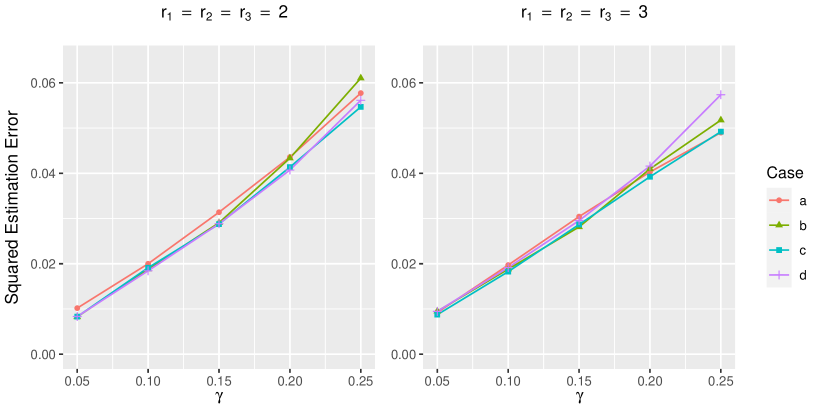

The goal of the next experiment is to verify the non-asymptotic error bound of the proposed SHORR estimator. We consider two settings of the multilinear ranks, and , and the following four cases of for model (5). For case a, we set and . Then, cases b-d are defined by changing one of the settings in case a while keeping all others fixed. Specifically, we set in case b, in case c, and in case d. The core tensor is generated in the same way as in the previous experiment, and the sparse orthonormal factor matrices s are generated randomly by the method given in Section F of the Appendix. The regularization parameter is selected by the BIC. By Theorem 2, fixing the multilinear ranks, it holds , where . Thus, we denote and set the sample size such that , 0.1, 0.15, 0.2, and 0.25. The mean squared error , averaged over 500 replications, is plotted against in Figure 4. It is shown that the mean squared error generally increases linearly in , and the four lines in each plot almost coincide. These findings support the error bound in Theorem 2.

6.3 Comparison with existing estimation methods

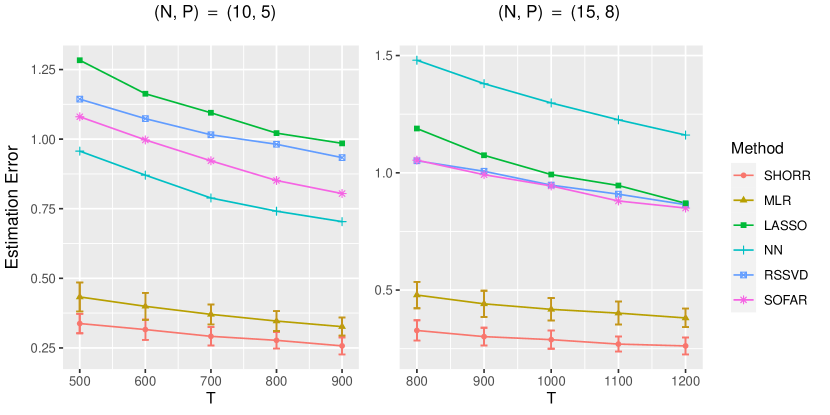

In the following experiment, we compare the performance of the proposed MLR and SHORR estimators with those of four existing ones for low-rank and/or sparse VAR models, including (i) Lasso (Tibshirani,, 1996; Basu and Michailidis,, 2015); (ii) nuclear norm (Negahban and Wainwright,, 2011, NN); (iii) regression with a sparse SVD (Chen et al.,, 2012, RSSVD); and (iv) sparse and orthogonal factor regression (Uematsu et al.,, 2019, SOFAR).

The data are generated from model (5) with (case a) or (case b). For both cases, we let , and . For case a, and s are generated by the same methods as in the previous subsection, and in case b, zeros rows are added below the s in case a. In both cases, entry-wisely . Hence, it is not sparse in case a, but is sparse in case b due to the zero rows of s. Figure 5 plots the estimation error averaged over 500 replications against and for the smaller and larger cases, respectively. The error bars representing one standard deviation are also displayed for the proposed estimators, and suppressed for the others for clearer presentation.

Under both smaller and larger , Figure 5 shows that both and significantly outperform the other estimators which either consider the low-rankness along only one direction or ignore it completely. Moreover, consistently outperforms as the former exploits the sparsity of s in addition to the low-rankness along three dimensions. It is also interesting to note the different performances of and in Figure 5. Since only exploits entry-wise sparsity of , it has the worst performance when is not sparse, as shown in the left panel. In contrast, only takes into account the low-rankness, so it performs best among the four existing estimators when is not sparse, and yet becomes the worst when is sparse as is the case for the right panel. This suggests that higher efficiency can be achieved by incorporating both the low-rankness and sparsity, which is the key advantage of the proposed .

6.4 Comparison with factor models

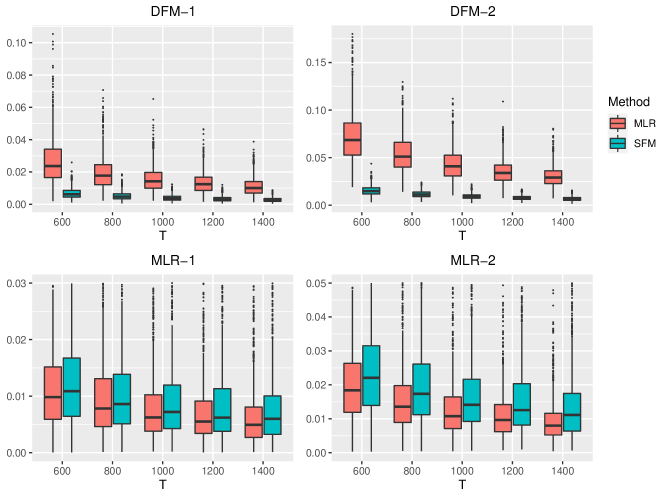

The final experiment aims to compare the proposed model to the static and dynamic factor models, namely SFM and DFM, discussed in Section 2.3. Note that the SFM cannot be directly used for forecasting since it does not impose an explicit model on the latent factors. However, for data generated by both the proposed model and the DFM, the SFM can be used to estimate the low-dimensional subspace where the conditional mean lies; see Remark 3.

We consider four data generating processes for with dimension . Two of them are generated by DFMs with :

-

•

DFM-1: The DFM with , specified jointly by the SFM and the autoregressive latent factor , where is a randomly generated vector with unit Euclidean norm, , and .

-

•

DFM-2: The DFM with , specified jointly by the SFM and the VAR(1) process for the latent factors , where is a randomly generated orthonormal matrix, , and .

The other two are generated by the proposed model with and :

-

•

MLR-1: The proposed multilinear low-rank VAR model in (5) with . The core tensor and factor matrices s are generated in the same way as the first experiment in Section 6.2.

-

•

MLR-2: Same as MLR-1 except for .

We first compare the performance of the proposed model and the SFM in terms of the estimation accuracy of the conditional mean subspace. The estimation of the SFM is conducted by the principal component method in Bai and Wang, (2016). The subspace estimation error can be measured by for DFM-1 and DFM-2, and for MLR-1 and MLR-2, where is the normalized version of for the fitted SFM. The results based on 1000 replications are displayed in Figure 6. It can be seen from the upper panels of the figure that the conditional mean subspaces for DFM-1 and DFM-2 can be consistently estimated by fitting the corresponding SFMs. However, as discussed in Section 2.3, for data generated by the DFM, fitting the proposed model will lead to model misspecification. This may explain why the subspace estimation error for the MLR method is much larger and seems to persist for large in the upper panels of Figure 6. On the other hand, when the data generating process is MLR-1 or MLR-2, the lower panels of Figure 6 show that both methods can estimate the subspace consistently, although the MLR method is more efficient. This agrees with our observation that the proposed model admits an SFM representation.

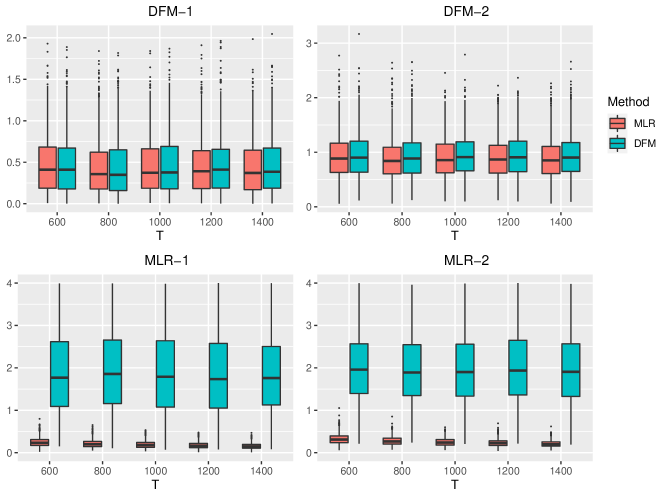

We next compare the performance of the proposed model and the DFM through the prediction error of the conditional mean . The DFM is estimated by a two-step approach, where we first obtain the estimated factors by fitting an SFM, and then fit a (vector) autoregressive model to . Figure 7 displays the prediction error based on 1000 replications. Remarkably, as shown in the upper panels, even if the data are generated from the DFM-1 or DFM-2, the proposed model exhibits competitive forecasting performance despite the model misspecfication. On the other hand, as shown in the lower panels, when the data are generated from MLR-1 or MLR-2, the forecasting performance of the fitted DFM is rather poor. As discussed in Section 2.3, the proposed model can accommodate different low-dimensional patterns for the response and predictors s, whereas the DFM requires the subspaces of and s to be identical. When the DGP is the proposed model with distinct and , the DFM will forecast based on . However, the true conditional expectation of is dependent on , and the latter could be different from, or even orthogonal to, . Consequently, when the response’s low-dimensional subspace is applied to the predictors, the DFM may have no predictive power at all. This explains why forecasting based on the DFM leads to considerable prediction errors. The robust forecasting performance of the proposed model reflects that its low-dimensional structure can be much more flexible than that of the DFM.

7 Real data analysis

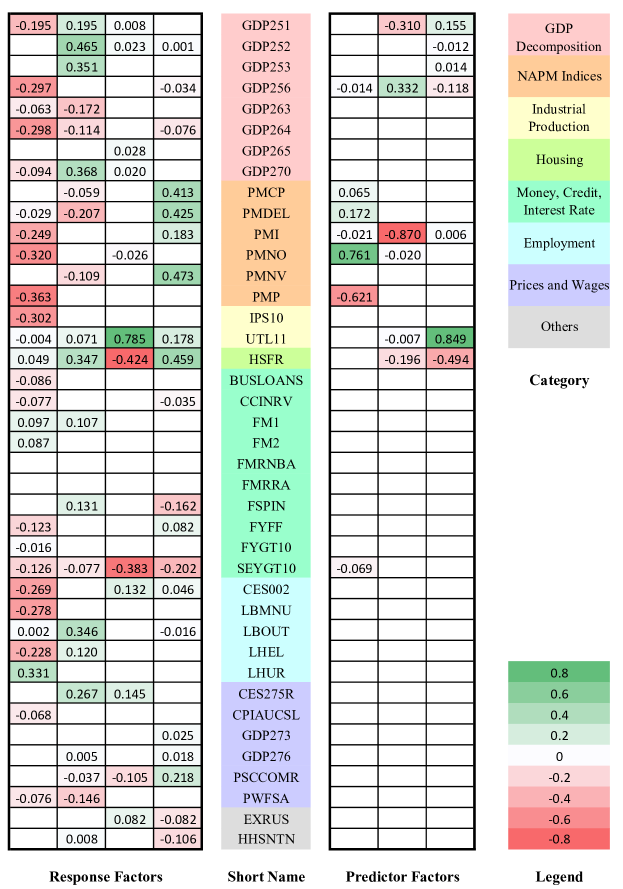

This section applies the proposed estimation methods to jointly model 40 quarterly macroeconomic sequences of the United States from 1959 to 2007, with 194 observed values for each variable (Koop,, 2013). All series are seasonally adjusted except for financial variables, transformed to stationarity, and standardized to zero mean and unit variance. These variables capture many aspects of the economy, and can be classified into eight categories: (i) GDP and its decomposition, (ii) National Association of Purchasing Managers (NAPM) indices, (iii) industrial production, (iv) housing, (v) money, credit and interest rate, (vi) employment, (vii) prices and wages, and (viii) others. The VAR model has been widely applied to fit these series in empirical econometric studies for structural analysis and forecasting; see Stock and Watson, (2009) and Koop, (2013). Table 2 gives more details about these macroeconomic variables.

We first apply the SHORR estimation to the entire data set, with the lag order fixed at for the fitted VAR model as suggested by Koop, (2013). Since the number of variables is much larger than the lag order , we do not perform variable selection for the factor matrix related to lags; that is, we replace with in the penalty term. The multilinear ranks are selected by the ridge-type ratio estimator, which results in , and the tuning parameter is selected by BIC.

The penalty yields sparse estimated factor matrices and , and the estimated coefficients are presented in Figure 8. The factor loading provides insights into the dynamic relationship among the 40 macroeconomic variables. The four response factors, denoted by for , contain nearly all of the variables and encapsulate different aspects of the economy: is mostly related to investments, imports, industrial production and employments; includes personal consumption, housing starts, and labor productivity; includes manufacturing, housing starts, and treasury bill yield rates; and includes NAPM indices, housing starts, and price index. Each response factor covers multiple categories of macroeconomic indices, and no clear group structure can be observed. However, it is noteworthy that only twelve variables are selected by the three predictor factors, and the sparse formulations of the predictor factors mainly consist of variables from the first four categories, including real GDP, private investment, NAPM indices, manufacturing and housing starts. The above result leads to an interesting interpretation: the activeness of production and investment serves as the driving force of the whole economy and usually precedes changes in other economic aspects such as the price indices, financial indices, and labor markets.

We next evaluate the forecasting performance of and in comparison with the competing estimators considered in Section 6. The following rolling forecasting procedure is adopted: first, use the historical data with the end point rolling from Q4-2000 to Q3-2007 to fit the models; and then, conduct one-step-ahead forecasts based on the fitted models. The selected ranks and tuning parameters for are preserved from the analysis of the entire data set, i.e. , and the selected ranks for MLR and RRR estimation are also fixed accordingly.

The and norms of the forecast errors for various methods are displayed in Table 1. It can be seen that the proposed MLR and SHORR estimators have much smaller forecast errors than competing ones, including the DFM with and the regularized and unregularized estimation methods for the VAR model. This can be explained by the capability of the proposed estimators to substantially reduce the dimensionality along three directions simultaneously. The SHORR estimator performs best among all estimators as it enforces sparsity of the factor matrices and hence prevents overfitting most effectively.

8 Conclusion and discussion

For a large VAR() model, its reduced-rank structure can be defined in three different ways. The novelty of the proposed approach lies in its ability to jointly enforce three different reduced-rank structures. This is made possible by rearranging the transition matrices of the VAR model into a tensor such that the Tucker decomposition can be conducted. As a result, the parameter space is restricted effectively along three directions, and the capability of the classical VAR model for modeling large-scale time series is substantially expanded.

Moreover, for the high-dimensional setup, this paper further proposes a sparsity-inducing estimator to improve the model interpretability and estimation efficiency. An ADMM algorithm is developed to tackle the computational challenges due to the all-orthogonal constraints on as well as the jointly imposed -regularization and orthogonality constraints on s. It is worth noting that this paper has a different focus than most work on tensor regression: here we employ the tensor technique as a novel approach to the dimension reduction problem in classical VAR time series modeling.

This paper may be extended in three possible directions. Firstly, the proposed estimators do not take into account the possible correlation structure among components of , which will reduce the estimation efficiency. Let be an estimator of . As in Davis et al., (2016), we may alternatively consider the generalized least squares loss rather than . However, the difficulty would be to find a good estimator . Secondly, the tensor technique potentially can be applied to many variants of the VAR model, e.g., those with a nonlinear dynamic structure such as the threshold VAR model (Tsay,, 1998) and the varying coefficient VAR model (Lütkepohl,, 2005). For instance, consider the time-varying coefficient VAR model with lag one, . Similarly, the coefficient matrices can be rearranged into a tensor with . If has multilinear low ranks , then the number of parameters will be . Moreover, a fourth-order tensor can be used to handle the case of lag order . Lastly, the proposed model can be generalized to a tensor autoregressive model for matrix-valued or tensor-valued time series; see Wang et al., 2019a for a related work.

Acknowledgements

We are grateful to the joint editor, the associate editor and three anonymous referees for their valuable comments which led to substantial improvement of this paper. Lian and Li are co-corresponding authors and contributed to the paper equally. This research was partially supported by GRF grants 11300519 and 17305319 from the Hong Kong Research Grant Council and a Key Program grant 72033002 from National Natural Science Foundation of China.

References

- Amengual and Watson, (2007) Amengual, D. and Watson, M. W. (2007). Consistent estimation of the number of dynamic factors in large N and T panel. Journal of Business & Economic Statistics, 25:91–96.

- Athanasopoulos and Vahid, (2008) Athanasopoulos, G. and Vahid, F. (2008). VARMA versus VAR for macroeconomic forecasting. Journal of Business & Economic Statistics, 26:237–252.

- Bai and Ng, (2008) Bai, J. and Ng, S. (2008). Large dimensional factor analysis. Foundations and Trends® in Econometrics, 3:89–163.

- Bai and Wang, (2016) Bai, J. and Wang, P. (2016). Econometric analysis of large factor models. Annual Review of Economics, 8:53–80.

- Bai, (1997) Bai, Z. D. (1997). Circular law. The Annals of Probability, 25:494–529.

- Basu et al., (2019) Basu, S., Li, X., and Michailidis, G. (2019). Low rank and structured modeling of high-dimensional vector autoregressions. IEEE Transactions on Signal Processing, 67:1207–1222.

- Basu and Michailidis, (2015) Basu, S. and Michailidis, G. (2015). Regularized estimation in sparse high-dimensional time series models. The Annals of Statistics, 43:1535–1567.

- Bernanke et al., (2005) Bernanke, B. S., Boivin, J., and Eliasz, P. (2005). Measuring the effects of monetary policy: A factor-augmented vector autoregressive (FAVAR) approach. Quarterly Journal of Economics, 120:387–422.

- Bickel et al., (2009) Bickel, P. J., Ritov, Y., and Tsybakov, A. B. (2009). Simultaneous analysis of lasso and dantzig selector. The Annals of Statistics, 37:1705–1732.

- Boyd et al., (2011) Boyd, S., Parikh, N., Chu, E., Peleato, B., and Eckstein, J. (2011). Distributed optimization and statistical learning via the alternating direction method of multipliers. Foundations and Trends in Machine learning, 3:1–122.

- Bunea et al., (2012) Bunea, F., She, Y., and Wegkamp, M. H. (2012). Joint variable and rank selection for parsimonious estimation of high-dimensional matrices. The Annals of Statistics, 40:2359–2388.

- Carriero et al., (2011) Carriero, A., Kapetanios, G., and Marcellino, M. (2011). Forecasting large datasets with bayesian reduced rank multivariate models. Journal of Applied Econometrics, 26:735–761.

- Chan et al., (2016) Chan, J. C. C., Eisenstat, E., and Koop, G. (2016). Large bayesian VARMAs. Journal of Econometrics, 192:374–390.

- Chen et al., (2012) Chen, K., Chan, K.-S., and Stenseth, N. C. (2012). Reduced rank stochastic regression with a sparse singular value decomposition. Journal of the Royal Statistical Society: Series B, 74:203–221.

- Chen et al., (2013) Chen, K., Dong, H., and Chan, K.-S. (2013). Reduced rank regression via adaptive nuclear norm penalization. Biometrika, 100:901–920.

- Chen and Huang, (2012) Chen, L. and Huang, J. Z. (2012). Sparse reduced-rank regression for simultaneous dimension reduction and variable selection. Journal of the American Statistical Association, 107:1533–1545.

- Davis et al., (2016) Davis, R. A., Zang, P., and Zheng, T. (2016). Sparse vector autoregressive modeling. Journal of Computational and Graphical Statistics, 25:1077–1096.

- De Lathauwer et al., (2000) De Lathauwer, L., De Moor, B., and Vandewalle, J. (2000). A multilinear singular value decomposition. SIAM Journal on Matrix Analysis and Applications, 21:1253–1278.

- De Mol et al., (2008) De Mol, C., Giannone, D., and Reichlin, L. (2008). Forecasting using a large number of predictors: Is bayesian shrinkage a valid alternative to principal components? Journal of Econometrics, 146:318–328.

- Dias and Kapetanios, (2018) Dias, G. F. and Kapetanios, G. (2018). Estimation and forecasting in vector autoregressive moving average models for rich datasets. Journal of Econometrics, 202:75–91.

- Ding and Cook, (2018) Ding, S. and Cook, R. D. (2018). Matrix variate regressions and envelope models. Journal of the Royal Statistical Society, Series B, 80:387–408.

- Guo et al., (2016) Guo, S., Wang, Y., and Yao, Q. (2016). High-dimensional and banded vector autoregressions. Biometrika, 103:889–903.

- Hallin and Lippi, (2013) Hallin, M. and Lippi, M. (2013). Factor models in high-dimensional time series: A time-domain approach. Stochastic Processes and their Applications, 123:2678–2695.

- Han et al., (2015) Han, F., Lu, H., and Liu, H. (2015). A direct estimation of high dimensional stationary vector autoregressions. The Journal of Machine Learning Research, 16:3115–3150.

- Izenman, (1975) Izenman, A. J. (1975). Reduced-rank regression for the multivariate linear model. Journal of Multivariate Analysis, 5:248–264.

- Kock and Callot, (2015) Kock, A. B. and Callot, L. (2015). Oracle inequalities for hgh dimensional vector autoregressions. Journal of Econometrics, 186:325–344.

- Kolda and Bader, (2009) Kolda, T. G. and Bader, B. W. (2009). Tensor decompositions and applications. SIAM Review, 51:455–500.

- Koop, (2013) Koop, G. M. (2013). Forecasting with medium and large bayesian vars. Journal of Applied Econometrics, 28:177–203.

- Lai and Osher, (2014) Lai, R. and Osher, S. (2014). A splitting method for orthogonality constrained problems. Journal of Scientific Computing, 58:431–449.

- Lange, (2010) Lange, K. (2010). Numerical analysis for statisticians. Springer Science & Business Media.

- Li et al., (2014) Li, G., Leng, C., and Tsai, C.-L. (2014). A hybrid bootstrap approach to unit root tests. Journal of Time Series Analysis, 35:299–321.

- Li et al., (2016) Li, G., Yang, D., Nobel, A. B., and Shen, H. (2016). Supervised singular value decomposition and its asymptotic properties. Journal of Multivariate Analysis, 146:7–17.

- Li and Zhang, (2017) Li, L. and Zhang, X. (2017). Parsimonious tensor response regression. Journal of the American Statistical Association, 112:1131–1146.

- Li et al., (2018) Li, X., Xu, D., Zhou, H., and Li, L. (2018). Tucker tensor regression and neuroimaging analysis. Statistics in Biosciences, 10:520–545.

- Lian et al., (2015) Lian, H., Feng, S., and Zhao, K. (2015). Parametric and semiparametric reduced-rank regression with flexible sparsity. Journal of Multivariate Analysis, 136:163–174.

- Lütkepohl, (2005) Lütkepohl, H. (2005). New Introduction to Multiple Time Series Analysis. Springer, Berlin.

- Mirsky, (1960) Mirsky, L. (1960). Symmetric gauge functions and unitarily invariant norms. The Quarterly Journal of Mathematics, 11:50–59.

- Negahban and Wainwright, (2011) Negahban, S. and Wainwright, M. J. (2011). Estimation of (near) low-rank matrices with noise and high-dimensional scaling. The Annals of Statistics, 39:1069–1097.

- Raskutti et al., (2019) Raskutti, G., Yuan, M., and Chen, H. (2019). Convex regularization for high-dimensional multi-response tensor regression. The Annals of Statistics, 47:1554–1584.

- Ravenna, (2007) Ravenna, F. (2007). Vector autoregressions and reduced form representations of dsge models. Journal of Monetary Economics, 54:2048–2064.

- Reinsel, (1983) Reinsel, G. (1983). Some results on multivariate autoregressive index models. Biometrika, 70:145–156.

- Said and Dickey, (1984) Said, E. S. and Dickey, D. A. (1984). Testing for unit roots in autoregressive-moving average models of unknown order. Biometrika, 71:599–607.

- Shapiro, (1986) Shapiro, A. (1986). Asymptotic theory of overparameterized structural models. Journal of the American Statistical Association, 81:142–149.

- Staudenmayer and Buonaccorsi, (2005) Staudenmayer, J. and Buonaccorsi, J. P. (2005). Measurement error in linear autoregressive models. Journal of the American Statistical Association, 100:841–852.

- Stock and Watson, (2005) Stock, J. H. and Watson, M. W. (2005). Implications of dynamic factor models for VAR analysis. National Bureau of Economic Research Working Paper No. 11467.

- Stock and Watson, (2009) Stock, J. H. and Watson, M. W. (2009). Forecasting in dynamic factor models subject to structural instability. In The Methodology and Practice of Econometrics: A Festschrift in Honour of David F. Hendry. Oxford University Press.

- Stock and Watson, (2011) Stock, J. H. and Watson, M. W. (2011). Dynamic factor models. In Clements, M. P. and Hendry, D. F., editors, Oxford Handbook of Economic Forecasting. Oxford University Press.

- Sun and Li, (2017) Sun, W. W. and Li, L. (2017). Store: sparse tensor response regression and neuroimaging analysis. The Journal of Machine Learning Research, 18:4908–4944.

- Tibshirani, (1996) Tibshirani, R. (1996). Regression shrinkage and selection via the lasso. Journal of the Royal Statistical Society. Series B, 58:267–288.

- Tsay, (1998) Tsay, R. S. (1998). Testing and modeling multivariate threshold models. Journal of the American Statistical Association, 93:1188–1202.

- Tsay, (2010) Tsay, R. S. (2010). Analysis of Financial Time Series. John Wiley & Sons, 3rd edition.

- Tsay, (2013) Tsay, R. S. (2013). Multivariate time series analysis: with R and financial applications. John Wiley & Sons.

- Tucker, (1966) Tucker, L. R. (1966). Some mathematical notes on three-mode factor analysis. Psychometrika, 31:279–311.

- Uematsu et al., (2019) Uematsu, Y., Fan, Y., Chen, K., Lv, J., and Lin, W. (2019). Sofar: large-scale association network learning. IEEE Transactions on Information Theory, 65:4924–4939.

- Velu and Reinsel, (2013) Velu, R. P. and Reinsel, G. C. (2013). Multivariate reduced-rank regression: theory and applications, volume 136. Springer Science & Business Media.

- Velu et al., (1986) Velu, R. P., Reinsel, G. C., and Wichern, D. W. (1986). Reduced rank models for multiple time series. Biometrika, 73:105–118.

- Vu and Lei, (2013) Vu, V. Q. and Lei, J. (2013). Minimax sparse principal subspace estimation in high dimensions. The Annals of Statistics, 41:2905–2947.

- (58) Wang, D., Liu, X., and Chen, R. (2019a). Factor models for matrix-valued high-dimensional time series. Journal of Econometrics, 208:231–248.

- (59) Wang, Y., Yin, W., and Zeng, J. (2019b). Global convergence of ADMM in nonconvex nonsmooth optimization. Journal of Scientific Computing, 78:29–63.

- Wang et al., (2015) Wang, Z., Gu, Q., Ning, Y., and Liu, H. (2015). High dimensional EM algorithm: Statistical optimization and asymptotic normality. In Advances in neural information processing systems, pages 2521–2529.

- Wilms et al., (2017) Wilms, I., Basu, S., Bien, J., and Matteson, D. S. (2017). Sparse identification and estimation of large-scale vector autoregressive moving averages. arXiv preprint arXiv:1707.09208.

- Wu and Wu, (2016) Wu, W.-B. and Wu, Y. N. (2016). Performance bounds for parameter estimates of high-dimensional linear models with correlated errors. Electronic Journal of Statistics, 10:352–379.

- Xia et al., (2015) Xia, Q., Xu, W., and Zhu, L. (2015). Consistently determining the number of factors in multivariate volatility modelling. Statistica Sinica, 25:1025–1044.

- Yu et al., (2014) Yu, Y., Wang, T., and Samworth, R. J. (2014). A useful variant of the Davis-Kahan theorem for statisticians. Biometrika, 102:315–323.

- Yuan et al., (2007) Yuan, M., Ekici, A., Lu, Z., and Monteiro, R. (2007). Dimension reduction and coefficient estimation in multivariate linear regression. Journal of the Royal Statistical Society: Series B, 69:329–346.

- Zhang, (2019) Zhang, A. (2019). Cross: Efficient low-rank tensor completion. The Annals of Statistics, 47:936–964.

- Zhao and Leng, (2014) Zhao, J. and Leng, C. (2014). Structure LASSO for regression with matrix covariates. Statistica Sinica, 24:799–814.

- Zheng and Raskutti, (2019) Zheng, L. and Raskutti, G. (2019). Testing for high-dimensional network parameters in auto-regressive models. Electronic Journal of Statistics, 13:4977–5043.

- Zheng and Cheng, (2020) Zheng, Y. and Cheng, G. (2020). Finite time analysis of vector autoregressive models under linear restrictions. Biometrika. To appear.

- Zhou et al., (2013) Zhou, H., Li, L., and Zhu, H. (2013). Tensor regression with applications in neuroimaging data analysis. Journal of the American Statistical Association, 108:540–552.

- Zhu et al., (2017) Zhu, X., Pan, R., Li, G., Liu, Y., and Wang, H. (2017). Network vector autoregression. The Annals of Statistics, 45:1096–1123.

| Unregularized methods | Regularized methods | |||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| Criterion | OLS | RRR | DFM | MLR | SHORR | LASSO | NN | RSSVD | SOFAR | |

| norm | 20.16 | 13.31 | 6.36 | 5.81 | 6.72 | 8.16 | 6.33 | 6.28 | ||

| norm | 8.32 | 4.55 | 2.85 | 2.56 | 3.06 | 3.36 | 3.02 | 3.02 | ||

| Short name | C | T | Description | Short name | C | T | Description |

|---|---|---|---|---|---|---|---|

| GDP251 | 1 | 5 | Real GDP, quantity index (2000=100) | FM2 | 5 | 6 | Money stock: M2 (bil$) |

| GDP252 | 1 | 5 | Real personal cons exp, quantity index | FMRNBA | 5 | 3 | Depository inst reserves: nonborrowed (mil$) |

| GDP253 | 1 | 5 | Real personal cons exp: durable goods | FMRRA | 5 | 6 | Depository inst reserves: total (mil$) |

| GDP256 | 1 | 5 | Real gross private domestic investment | FSPIN | 5 | 5 | S&P’s common stock price index: industrials |

| GDP263 | 1 | 5 | Real exports | FYFF | 5 | 2 | Interest rate: federal funds (% per annum) |

| GDP264 | 1 | 5 | Real imports | FYGT10 | 5 | 2 | Interest rate: US treasury const. mat., 10-yr |

| GDP265 | 1 | 5 | Real govt cons expenditures & gross investment | SEYGT10 | 5 | 1 | Spread btwn 10-yr and 3-mth T-bill rates |

| GDP270 | 1 | 5 | Real final sales to domestic purchasers | CES002 | 6 | 5 | Employees, nonfarm: total private |

| PMCP | 2 | 1 | NAPM commodity price index (%) | LBMNU | 6 | 5 | Hrs of all persons: nonfarm business sector |

| PMDEL | 2 | 1 | NAPM vendor deliveries index (%) | LBOUT | 6 | 5 | Output per hr: all persons, business sec |

| PMI | 2 | 1 | Purchasing managers’ index | LHEL | 6 | 2 | Index of help-wanted ads in newspapers |

| PMNO | 2 | 1 | NAPM new orders index (%) | LHUR | 6 | 2 | Unemp. rate: All workers, 16 and over (%) |

| PMNV | 2 | 1 | NAPM inventories index (%) | CES275R | 7 | 5 | Real avg hrly earnings, non-farm prod. workers |

| PMP | 2 | 1 | NAPM production index (%) | CPIAUCSL | 7 | 6 | CPI all items |

| IPS10 | 3 | 5 | Industrial production index: total | GDP273 | 7 | 6 | Personal consumption exp.: price index |

| UTL11 | 3 | 1 | Capacity utilization: manufacturing (SIC) | GDP276 | 7 | 6 | Housing price index |

| HSFR | 4 | 4 | Housing starts: Total (thousands) | PSCCOMR | 7 | 5 | Real spot market price index: all commodities |

| BUSLOANS | 5 | 6 | Comm. and industrial loans at all comm. Banks | PWFSA | 7 | 6 | Producer price index: finished goods |

| CCINRV | 5 | 6 | Consumer credit outstanding: nonrevolving | EXRUS | 8 | 5 | US effective exchange rate: index number |

| FM1 | 5 | 6 | Money stock: M1 (bil$) | HHSNTN | 8 | 2 | Univ of Mich index of consumer expectations |

Appendix A Proofs of Theorems 1-3

Proof of Theorem 1.

The proof generally follows from Proposition 4.1 in Shapiro, (1986) for overparameterized models. The VAR() model can be written as the linear regression problem

| (26) |

Let denote the component parameters in the Tucker decomposition forms, let denote the true parameter , and let denote the vectorized OLS estimates without constraint. With Assumption 1, according to classical asymptotic theory for stationary VAR model (Tsay,, 2013), as ,

| (27) |

Consider the discrepancy function for any ,

| (28) |

Obviously, is a nonnegative and twice continuously differentiable function, and equals to zero if and only if .

In order to calculate the Jacobian matrix , we define the tensor matricization transformation operator which is an matrix and satisfies that for any tensor . In fact, is a full-rank matrix indicating the corresponding position in of ’s each entry in , and can be regarded as the natural extension of the permutation matrix for matrix transpose. Also note that only depends on the value of and , and since we consider fixed and in this part, we simplify it to .

Therefore,

| (29) |

and the Jacobian matrix of is

| (30) |

Then, by Proposition 4.1 in Shapiro, (1986), we know that the minimizer of , namely the MLR estimator, has the asymptotic normality,

| (31) |

and , where is the projection matrix, is the Fisher information matrix of as goes to infinity, is the Jacobian matrix of with respect to the overparameterized model parameters , is the asymptotic covariance matrix for and denotes the Moore-Penrose inverse. Since in the VAR() model, we have . ∎

Proof of Theorem 2.

The proof of Theorem 2 consists of two parts.

-

•

The first part shows the estimation error bounds given the deterministic realization of the time series process, assuming that the deviation bound condition and restricted eigenvalue condition hold.

-

•

The second step is the stochastic analysis in which we show that these two regulatory conditions are satisfied with high probability converging to 1.

Based on the linear regression form (26), we can rewrite as

| (32) |

Denote , and . By the optimality of the SHORR estimator,

| (33) |

Note that , so we can decompose into two parts,

| (34) |

and bound these two parts separately. We denote the event that these two inner products are bounded by and as ,

| (35) |

Denote by the nonzero index set of , and by is the complement of . By the sparsity of each in Assumption 4, . In the following proof, we use the abused notation. For any matrix and any vector norm , we denote and .

On the event , if we multiply 2 to both sides of (33) we can have

| (36) |

On the left-hand side, by triangle inequality,

| (37) |

whereas on the right-hand side, . So we have

| (38) |

Next, we assume that there is a lower bound for . Thus, we define the event , where . On the event ,

| (39) |

By the perturbation bound for HOSVD in Lemma 1, we have

| (40) |

where , and

| (41) |

Therefore, we have

| (42) |

where .

If we denote , we can obtain the estimation error bound and in-sample prediction error bound

| (43) |

which conclude the deterministic analysis.

In the second part, we show that the events and occur with high probability. In the high-dimensional regression literature, the conditions in and are known as deviation bound condition and restricted eigenvalue condition. We defer the proof of both conditions to Lemma 2 and 3, where we show that and hold simultaneously with probability at least , given that the sample size . ∎

Proof of Theorem 3.

By definition, for any tensor , where and ,

| (44) |

In other words, the Frobenius norm of the error tensor is equivalent to the norm of the singular values of any matricization. By Mirsky’s singular value inequality (Mirsky,, 1960),

| (45) |

Obviously, the error bound is smaller than the error bound, so it follows the same upper bound,

| (46) |

Note that . For , since and , is the dominating term in . For , since and , is the dominating term.

Hence, for as ,

| (47) |

For ,

| (48) |

For ,

| (49) |

∎

Appendix B Proofs of Corollaries 1 and 2

Proof of Corollary 1.

Here we prove the asymptotic normality for , since the proofs for the and are similar. In this part, we simplify to . Note that and are the eigenvectors of and respectively. By Theorem 1, . Note that

| (50) |

so we have

| (51) |

Therefore, is asymptotically normally distributed.

By the matrix perturbation expansion (Izenman,, 1975; Velu and Reinsel,, 2013),

| (52) |

Therefore, is also asymptotically normally distributed.

For , by the definition of HOSVD,

| (53) |

So we have

| (54) |

Therefore, is also normally distributed with mean zero, as . For simplicity, we omit the covariance of each component, but they can be easily calculated by the above formula. ∎

Proof of Corollary 2.

The -consistency and asymptotic normality of has been studied in the proof of Theorem 1, with .

As discussed previously, where is a projection matrix. Note that , where is the projection matrix onto the orthogonal compliment of . Then, it is clear that .

For the RRR estimator, the components in the SVD, , can be denoted as . Therefore, the gradient matrix of the RRR is . Since in Tucker decomposition is exactly the same as the left singular vectors in the SVD of , we can view the Tucker decomposition as a further decomposition of the matrix . Therefore, . By similar arguments in the proof of Theorem 1, we can obtain that the RRR estimator has the asymptotic covariance and it is smaller than or equal to since . ∎

Appendix C Proofs of Propositions 1 and 2

Proof of Proposition 1.

Proof of global convergence hinges on standard arguments for block relaxation algorithm (Lange,, 2010). Note that although the objective function is nonconvex, the subproblem of each updating step is well-defined, differentiable and convex. Since the algorithm decreases the objective function monotonically, the convergence is guaranteed and any convergent point is a stationary point. With a slight abuse of notation, denote the objective function of by , and then global convergence is guaranteed under the following conditions: (i) is coercive; (ii) the stationary points of are isolated; (iii) the algorithm mapping is continuous; (iv) is a fixed point of the algorithm if and only if it is a stationary point of ; (v) with equality if and only if is a fixed point of the algorithm.

Condition (i) is guaranteed by the compactness of the set . Condition (ii) is assumed. Condition (iii) follows from the implicit function theorem since the algorithmic map is a composition of four differentiable and convex maps. A fixed point satisfies that and ; therefore the fixed point of the mapping , i.e., condition (iv) is satisfied. Finally, each step monotonically decreases , so they give a strict decrease if and only if they actually change the corresponding components. Hence, condition (v) is satisfied.

Proof of local convergence hinges on the Ostrowski’s theorem, which states that the sequence is locally attracted to if the spectral radius of the differential of the algorithmic map . The condition can be shown to be true based on the local convergence of block relaxation algorithm by Lange, (2010), and we omit the detailed proof here. ∎

Proof of Proposition 2.

The proof of this proposition follows the same lines as that of Theorem 3 in Uematsu et al., (2019). In this analysis, we fix parameters and Lagrangian multipliers , and consider the objective function . By the nature of the ADMM algorithm applied to , the resulting sequence is non-increasing. Clearly, the value of the function is bounded from below. Hence, the sequence converges.

Note that the subspace of matrices with the orthonormal constraint is a Stiefel manifold which is compact and smooth. Moreover, on the Stiefel manifold, the objective function is strongly convex with respect to any one of the blocks and , for , when all the other blocks are fixed.