The Optimal Deterrence of Crime:

A Focus on the Time Preference of DWI Offenders

Abstract

We develop a general model for finding the optimal penal strategy based on the behavioral traits of the offenders. We focus on how the discount rate (level of time discounting) affects criminal propensity on the individual level, and how the aggregation of these effects influences criminal activities on the population level. The effects are aggregated based on the distribution of discount rate among the population. We study this distribution empirically through a survey with 207 participants, and we show that it follows zero-inflated exponential distribution. We quantify the effectiveness of the penal strategy as its net utility for the population, and show how this quantity can be maximized. When we apply the maximization procedure on the offense of impaired driving (DWI), we discover that the effectiveness of DWI deterrence depends critically on the amount of fine and prison condition.

Yuqing Wang1 and Yan Ru Pei2∗

1. Department of Sociology, University of Macau

Avenida da Universidade, Taipa, Macau, China

email: yuqing.wang@connect.um.edu.mo

2. Department of Physics, University of California

San Diego, 9500 Gilman Drive, La Jolla, California 92093-0319, USA

email: yrpei@ucsd.edu

* corresponding author

Declaration of interest: none

Keywords: General Deterrence, Rational Choice Theory, Social Welfare Function, Economic Optimization, Time Preference, Impaired Driving

JEL Classification: C12, C25, C61, C83, I31, K14, K42

1 Introduction

It is commonly accepted that crimes are detrimental to the general well-being of a society, so it is socially favorable to reduce the level of criminal activities through the implementation of certain legal practices (Dostoyevsky, 2017). In some modern theories of crime, this argument is formalized using an economic model, which attempts to characterize a criminal offense by the social disutility it generates for the population (Becker, 1968). The net disutility is evaluated as the difference of the benefit it generates for the offender and the cost it incurs for the victim. And by taking the sum of the disutilities of all criminal offenses, we obtain the total disutility of criminal activities in the population. Therefore, through reducing the level of criminal activities, the total disutility is effectively decreased, thus achieving a more socially favorable state (Ehrlich, 1996) for the population.

It is important to predict the effectiveness of the legal practices before they are implemented. To do so accurately, it is necessary to first predict the level of criminal activities in a population. This is done through an understanding of the underlying mechanism behind how the level of criminal activities is influenced by certain legal practices. This understanding can be achieved by applying the concept of deterrence in penology, which states that the threat of punishment prevents a person from committing a crime (Jervis, 1979). We can formalize this concept under the framework of rational choice theory (Von Neumann et al., 2007) by focusing on the net utility of crime for the offender. The net utility is simply the difference of the utility that the crime rewards the offender and the expected disutility that the potential punishment incurs. Therefore, by increasing the threat of punishment, the expected disutility of punishment will be greater, and the offender will be less inclined to commit the crime. If the threat of punishment increases to the point where the net utility becomes negative for the offender, then the offender will decide against committing the crime (in accordance with rational choice theory), and a successful deterrence is achieved. To quantify the “threat of punishment” as a disutility, we denote the specific implementation of the legal practices as a penal strategy, which we specify with factors such as the severity, certainty, and celerity of the punishment (Jervis, 1979).

A penal strategy generates social benefits as the reduction of criminal activities; however, it also generates social costs as a direct result of its implementation (Greenberg, 1990). These costs generally increase with the threat of punishment that the strategy imposes. For example, increasing the certainty of punishment implies using more police resources for criminal detection, and increasing the severity of punishment implies using more prison resources to enforce a longer term of imprisonment. Besides the implementation cost, the punishment itself is also a disutility for the offender, which appears as the opportunity cost, stigma, and any dissatisfaction that is associated with the punishment (Menninger, 1968). It is crucial that this disutility is included as a cost of the penal strategy, as the utility function of the offender is also part of the utility function of the society (Arrow, 1950). The optimal penal strategy should aim to maximize the difference of the all benefits and costs it generates.

The social benefit of the penal strategy is associated with the nonoccurrence of crimes while the social cost is associated with the occurrence (and the ensuing punishment) of crimes. To evaluate the benefits and costs, it is necessary to predict the number of criminal offenses under the penal strategy. Before we make this prediction on the population level, we first study the occurrence of a criminal offense under the penal strategy on the individual level. To begin with, we assume that whether a crime occurs or not depends on various traits of the offender and victim (Tittle et al., 2003), which we can denote as the parameterization of their utility functions, or utility parameters. Individuals with different utility parameters evaluate the net utility of the crime differently, resulting in the difference in their decisions of whether to commit the crime or not. For example, offenders with different perceptions of risk may evaluate the disutility of the threat of punishment differently, and those who perceive the disutility to be greater are less likely to commit the crime. Therefore, it is possible to make an a priori categorization of an individual as a potential offender or non-offender based on how he/she evaluates the net utility of crime using his/her utility parameters. We then extend this analysis to the population level by studying how these parameters are distributed among the population. We first evaluate the net utility of crime for every individual under the penal strategy in effect, and record the number of times that the net utilities evaluate to a negative value. This number is then equal to the predicted number of criminal offenses in the population, which we can use to compute the benefits and costs associated with the penal strategy. The difference of benefits and costs is the net utility of the penal strategy for the population, and the goal is to find the optimal penal strategy that maximizes this net benefit.

As an example, we focus on the time preference of an individual as his/her major behavioral trait, and study how this trait influences his/her criminal propensity towards committing the offense of impaired driving (DWI). In this work, an individual’s time preference is described using the hyperbolic time discounting model (Thaler, 1981), under which the level of time preference can be quantified as the rate at which the discounting function decays, or discount rate. In short, a person with a larger discount rate will assign a higher value to present rewards relative to future rewards, so he/she is more likely going to commit a crime as the relative value of the immediate reward from the crime is greater with respect to the potential future punishment (Nagin and Pogarsky, 2004). The discount rate then serves as a strong predictor of whether an individual will become a DWI offender, and by knowing how the discount rate is distributed among a population, we can accurately predict the number of DWI incidents under a penal strategy. The goal of this paper is then to empirically measure this distribution, evaluate explicitly the net social benefit that a penal strategy generates based on this distribution, and find the penal strategy that maximizes this net social benefit.

We first briefly present the structure of the paper. In section 2, we describe the time preference and risk perception of an individual in terms of hyperbolic time discounting (Thaler, 1981) and probability weighing function (Tversky and Fox, 1995), and discuss how these two traits generate variations in individual criminal propensities. In section 3, we use a graph theoretical (West et al., 1996) approach to model the criminal activities in a population as a directed graph, with an arrow denoting a criminal offense pointing from the offender to the victim. Given a penal strategy, the graph is partitioned into two subgraphs, one consisting of the offenders and one consisting of the non-offenders111This is technically not the case as we are partitioning the edges instead of the nodes. However, in section 4, we show that the two partitioning schemes are equivalent in the context of DWI.. The social welfare function (Arrow, 1950) is constructed as the sum over the graph connections. In section 4, we derive an explicit expression for the social welfare function based on several simplifying assumptions in the context of DWI. In section 5, we find the optimal penal strategy by maximizing the social welfare function, and show that abrupt changes in the optimum can be realized by varying the amount of fine and prison conditions. In section 6, we estimate empirically how the discount rate (denoting the level of time preference) and probability weighing factor (denoting the level of risk aversion) are distributed among the population by conducting a survey for 207 participants; in addition, we show that the two behavioral traits are distributed independently. In section 7, we discuss several possible extensions to our model which can be made to account for a wider range of behavioral traits and more complex criminal patterns.

2 Preliminaries

The main goal of this paper is to find the optimal penal strategy. However, at this point, this is an ill-defined goal as we have not yet defined exactly what constitutes a penal strategy (or what we are trying to optimize over) and exactly what this penal strategy should aim to maximize (or what we are trying to find the optimum of). To formally define the optimization problem, we first have to introduce the necessary concepts in penology and economy. We first provide a brief overview of the concept of deterrence in criminology (Jervis, 1979), and introduce the object of penal strategy which quantifies the “level” of deterrence. We then briefly discuss the concepts of hyperbolic time discounting (Thaler, 1981) and prospect theory (Tversky and Fox, 1995) in the context of deterrence. Finally, we illustrate how a person’s behavioral traits can be specified by the parameters of his/her utility function (Von Neumann et al., 2007), and we use a person’s discount rate as an illustrative example.

2.1 Penal Strategy

Deterrence theory states that the threat of punishment prevents people from committing crimes. In its traditional formulation, a penal strategy is specified by three main factors - the severity, certainty, and celerity of punishment. and the celerity of punishment (Jervis, 1979). It is generally believed that the strength of each factor is correlated with the level of criminal activities in a population, and there has been a fair share of studies justifying these correlations (Antunes and Hunt, 1973; Yu, 1994), both theoretical and empirical. Interestingly, the results seem to disagree wildly on the prominence of these correlations (Mendes, 2004; Gray and Martin, 1969), with some going as far as to questioning the signs of the correlations (Sherman, 1993).

In this work, we define an object named penal strategy which factors into a person’s utility function in the form of the expected level of punishment. Whenever an individual decides to commit a crime, he/she absorbs this disutility subconsciously into his/her utility function to evaluate whether committing crime is “worth it” or not (see section 3.2). Under a particular class of crime, a penal strategy can be specified by a vector of parameters . As an example, for the crime of DWI, a penal strategy can be specified with five parameters, . Given this strategy, the offender is apprehended with probability (certainty of punishment), and he/she has the choice of being punished with a fine or be imprisoned for a duration of (severity of punishment), with the delay in punishment being (celerity of punishment).

The parameter is an abstract quantity describing the rate at which disutility is incurred onto an individual during imprisonment (see section 2.2), and can be roughly interpreted as how “unpleasant” the imprisonment condition is (Friedman, 1999). One may be tempted to lump this quantity together with and define simply as the total disutility incurred on the individual during imprisonment, thus effectively quantifying the “severity” of punishment. Even ignoring the effect of hyperbolic time discount (see section 2.2), this coarse characterization of “severity” makes sense only if the goal to focus on how severity affects the personal utility function of the offender. If we take into account the cost of social utility in actually implementing this strategy, is substantially different from in the sense that increasing (making the condition more unpleasant) incurs little cost while increasing (increasing the term of imprisonment) incurs a cost that scales roughly proportional to (see section 4.3). This seems to suggest that making the imprisonment condition more unpleasant is a more economically efficient strategy than increasing the term of imprisonment, which is true only to a certain extent, as we shall discuss in section 5222It has been suggested that prisons should be made as unpleasant as possible since making the prison more unpleasant (increasing ) costs essentially nothing (Friedman, 1999) while at the same time being able to decrease the level of criminal activity. However, this strategy is justified only if the well-being of the criminal is ignored as a factor for the social welfare function, then in this case the optimal strategy would trivially be a strategy that is infinitely unpleasant (e.g. execution). A more in-depth and practical study of the effect of on the total social benefit is presented in section 5.3.

The discrepancy between the offender’s personal utility function and the victim’s utility function (even in the absence of the convolution of behavioral traits such as time discounting and risk preference) is the source of non-triviality for finding the optimal penal strategy (see section 2.4). In fact, one can observe a rather nice duality between this discrepancy in the utility functions to the characterization of specific and general deterrence333There is a nice overview of these two modes of deterrence in the paper (Stafford and Warr, 1993).. Specific deterrence focuses on the effect of punishment targeting the offender after the crime has been committed. A strategy based on the principle of specific deterrence would then focus on the utility function of the offender, and the optimal penal strategy under this framework would be a strategy that incurs the minimal amount of disutility on the offender (while at the same time being sufficient enough to deter future offenses). On the other hand, general deterrence focuses on the effect of the threat of punishment on preventing any crimes from occurring in the first place. A strategy based on the principle of general deterrence would then focus on the utility functions of the victims and non-offenders, and the optimal penal strategy under this framework would be a strategy threatening a large amount of disutility on the offender. In an ideal world, this means that crime would occur very infrequently, which decreases the social cost of enforcing any punishment and increases the social benefit of the victims (see 4.3 for a formal discussion).

It is then natural to let the function of which we try to find the maximum be the social welfare function (Arrow, 1950) which includes the sum of the utilities of all members in the population - the offenders, victims, and non-offenders. Under this definition of the optimization problem, the distinction between specific deterrence and general deterrence is non-existence from an utilitarian standpoint. As maximizing this function guarantees that the penal strategy is optimal in both frameworks of deterrence. The optimal penal strategy should then accomplishes three goals which all contribute to the maximization of the social welfare function, thus achieving an utilitarian optimum. The first goal is to maximize the total number of members that can be deterred from committing the crime in the first place; the second goal is to minimize the cost of implementing the strategy itself; and the third goal is to minimize the disutility incurred on the offender during the punishment. Note that this optimum, in general, does not correspond to the judicial optimum, where the level of punishment matches exactly with the degree of crime (Hamilton and Rytina, 1980), and the correlation between the two optima is an interesting point of research that we leave open for our future work.

2.2 Hyperbolic Time Discounting

Hyperbolic time discounting is a time-inconsistent model that accounts for the phenomenon that a delayed reward is generally less appealing to a human than an immediate reward, even though the reward is the same (Thaler, 1981). There has been studies on how hyperbolic time discounting affects the behaviors of the offenders, and how it affects their perception of deterrence (Nagin and Pogarsky, 2001; Loughran et al., 2012). However, the works are mostly empirically, and to our knowledge, there has been no work on how the phenomenon of hyperbolic time discounting can be actually used to inform an optimal penal strategy.

Formally, we can define a particular reward to be , and the utility gain of receiving that reward delayed by to be . We can then express as follow

where is the utility gain of receiving the reward immediately. We see that is a monotonously decreasing function with respect to , with governing the rate of decrease. For the rest of the paper, we refer to as the discount rate444Technically speaking, this is an abuse of notation as the discount rate is only well-defined for the model of exponential time discounting, because the relative decay rate is constant for an exponential function but not for a hyperbolic function. Therefore, we use the terminology “discount rate” purely for the sake of denoting the parameter in this context., which is a parameter that fully specifies the discounting function. The utility of a delayed reward can be easily generalized for modeling the disutility of a delayed punishment, where we simply interpret as the disutility of a punishment, , delayed by time .

A more interesting application of the discounting function would be to evaluate the disutility of a continuous punishment, such as imprisonment, by integrating the discounting function with respect to time. To be more specific, we consider a continuous punishment where the disutility per unit of time is . If the punishment is enforced continuously in the time window on an offender whose discount rate is , then the total disutility that the individual receives is

Alternatively, we can denote as the time duration from the current time to the start of the punishment, and as the length of the punishment. This allows us to write

| (1) |

In the context of imprisonment, we can interpret as the disutility that the individual receives per unit time during imprisonment, including the opportunity cost of not working and the discomfort of the jail/prison environment. We denote as the harshness of the imprisonment condition. We can interpret as the term of imprisonment and as the time between getting caught to the punishment being enforced. In the language of deterrence theory, the pair quantifies the “severity” of punishment, and quantifies the “celerity” of punishment.

We can easily check the asymptotic behavior of in the following two limits

For a person with a discount rate of , the perceived disutility is simply the total disutiltiy of imprisonment in the absence of time discounting. As the discount rate increases, the magnitude of decreases monotonously, meaning that the threat of imprisonment is less effective for an individual with a higher discount rate. In the limit of large , the disutility begins to scale inversely with the , and approaches zero for .

Suppose we are implementing a strategy with the hope of incurring a disutility of for the offender, then there the two parameters have to follow some constraint. To find this constraint, we set the expression in equation 1 equal to

| (2) |

Note that scales linearly with , with the slope being , which scales exponentially with . This means that when a punishment is delayed, the length of the punishment has to increase accordingly in order to “compensate” for the disutility decay. For an individual with a higher discount rate , the disutility decay as a result of the delay will be more prominent, so the length of punishment has to be increased by a greater amount to incur the desired disutility for the individual. In some sense, for an offender with a large discount rate , the factor of “celerity” is more important than “severity”. This discussion is formalized in appendix 55.

2.3 Probability Weighing Function

Having discussed the concept of hyperbolic time discounting and relating it to two of the three factors of deterrence - severity and celerity of punishment, we move on to the third factor of deterrence - certainty of punishment, which we should refer to more formally as probability of apprehension. This factor can be modeled under the economic framework of prospect theory (Tversky and Fox, 1995). Simply put, prospect theory states that for an event with some known probability of occurring, the probability perceived by a human is different from the actual probability. Therefore, when an individual is presented with an uncertain reward, the expected utility gain that he/she perceives is not the actual expected utility, as exemplified by Allais paradox (Allais, 1953).

Consider a simple lottery presented to an individual. The lottery returns reward with probability , and returns reward with probability , then the expected utility gain that the lottery returns is

This is, however, not the utility gain that the individual perceives. In fact, the perceived expected utility is given by

where is commonly termed the probability weighting function, a function that attempts to model how human evaluates the utility of uncertain events. The probability weighting function can be expressed as

| (3) |

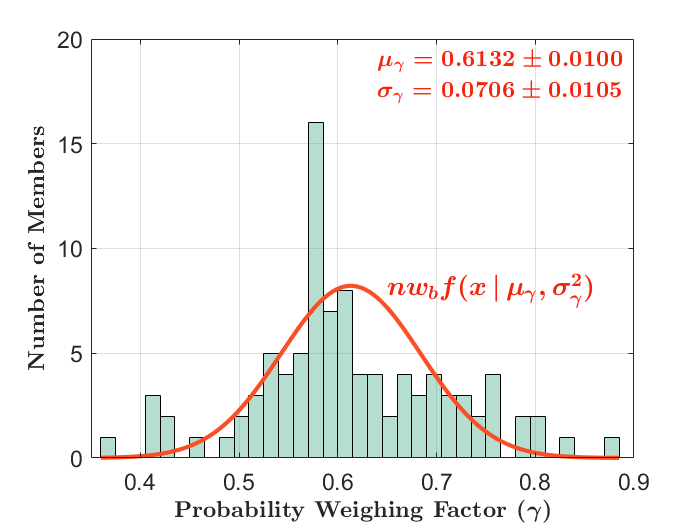

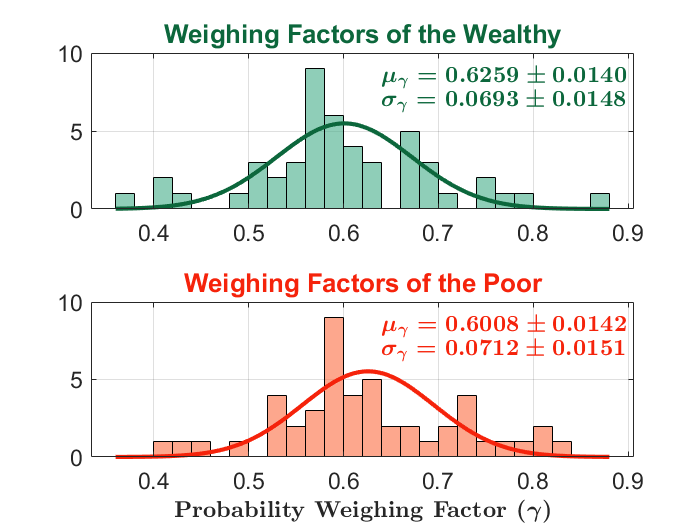

which is an inverse S shaped function with its level of curvature governed by the parameter , which we term the probability weighing factor. The probability weighing factor appears to be different across different people and across different classes of rewards/punishments, but empirical estimates of its value generally fall within the range (Andreoni et al., 2010). In section 6.2, we empirically estimate the mean of among our survey sample to be in the context of weighing the risk of committing DWI. Note that other forms of do exist (Gonzalez and Wu, 1999) which contains more than one parameters, but for this work, we focus on the form as appeared in equation 3.

It can be easily checked that the function satisfies the regularity condition of and . This is required as impossible events should be perceived as impossible, and certain events should be perceived as certain. In addition to the regularity conditions, is constructed such that there is another solution to for . We can denote this solution as , then it can be shown that (see appendix A)

This corresponds to the phenomenon that humans tend to overweight low-probability events and underweight high-probability events.

Therefore, under a particular deterrent strategy with the probability of apprehension being , the offender will perceive that probability as being . This discrepancy has to be taken into account when evaluating the probability of apprehension for the optimal penal strategy (see section 5.4). To see this clearly, consider a punishment incurring a disutility of on the offender, then the offender will perceive the expected disutility to be , instead of . For , the former is greater than the latter, meaning that the individual will over-evaluating the threat of punishment. The same argument goes for , where the individual will under-evaluate the threat of punishment. From a very cursory cost-benefit analysis, this suggests that a deterrent strategy with a low probability of apprehension is more economically efficient. To see this, assume that the cost of apprehension is , which scales linearly with the probability of apprehension. We then compute the perceived disutility per unit of cost to be

which is a monotonously decreasing function for sufficiently small (see appendix A). In fact, this ratio tends to infinity when , which suggests a deterrence strategy with zero probability of apprehension.

This is obviously not right, and the reason why this simple analysis breaks down is because we failed to consider the full utility function of the offenders, which includes the utility gain returned from the crime itself (see section 3.2). For now, equation 2.3 offers a nice intuitive insight as to why it may be preferable to use a deterrent strategy with low probability of apprehension, though it should be interpreted as a serious attempt for studying the cost-benefit ratio with respect to parameter .

2.4 Utility Function

There have been many studies investigating the correlations between criminal activity and obvious predictors such as wealth (Barnett, 1979), level of education (Lochner and Moretti, 2004), and social environment (Wiatrowski et al., 1981). Recently, there has been an emergence of studies offering behavioral analyses of the motivation behind criminal activity, which attempt to differentiate multiple facets of the behavioral traits including time-inconsistent behaviors (Sloan et al., 2014), risk averting/loving behaviors (Mungan and Klick, 2015), and behaviors induced by underlying psychological factors (van Winden and Ash, 2012). All these studies can be viewed as endeavors towards understanding the question of why certain individuals choose to commit crime under a particular deterrent strategy, while others do not. From an economic standpoint, the answer to this question is because the utility function of every individual is parameterized differently (see section 3.2). In this work, we focus on mainly two important parameters , wealth and discount rate. We believe that these two parameters are strong indicators of criminal behaviors (see section 4.2), and the distribution of the two parameters can be accurately measured within a population (see section 6.1 and 6.2).

An important side note to mention here is that it is, in fact, possible for to fully specify the behavioral traits of the population under two possible scenarios. The first scenario is when the pair forms a complete basis for describing all possible utility functions (Chajewska and Koller, 2000), meaning that all other behavioral traits can be uniquely specified by the values of . For example, it may be the fact the “recklessness” of an individual (Arnett, 1992) is simply an expression of wealth and discount rate555Note that the direction of causality may go the other way, meaning that it may just as well be that the discount rate is just an expression of recklessness.. An interpretation of this would be that if a person has a high discount rate, then he/she may be more “reckless” in the sense that he/she will be prone to seek immediate rewards at the sacrifice of future well-being. This is generally an unrealistic scenario, as it is rather ridiculous to assume that the complexities of human behavior can be described by merely two parameters.

The second, more realistic scenario is to relax the assumption that has to fully specify the behavioral traits of every member in the population, but we instead only require it to describe the average behavioral traits of the population. Therefore, if other behavioral traits are distributed among the population independently with respect to , then the general behavior of the population can be effectively predicted by “on average”. As an example, in section 6.2, we show empirically that the probability weighing factor , describing the risk preference of an individual, is in fact distributed independently with respect to . In the end, if we wish to find the optimal penal strategy, we are only interested in how the criminal behaviors across the entire population will respond to a particular deterrent strategy (see section 4.2), so it is only required that we know how the behavioral traits are distributed among the population (see section 4.4), meaning that it is unnecessary to predict the response of every single member.

2.4.1 Utility Function of the Offender

We first begin by assuming that all individuals are rational agents666The question of whether the assumption that all individuals are rational agents is valid or not is somewhat meaningless in a mathematical sense, as all “irrational” behavior of an individual can be explained, or made “rational” essentially, by a particular parameterization of the utility function such as his/her discount rate, probability weighing, underlying psychological factors, etc.. According to rational choice theory, whenever an individual is faced with a decision among multiple choices, the individual will select the one returning the highest utility gain (or lowest utility loss) for him/herself. This theory also applies to the decision process of a potential offender who weighs the expected return of the crime to decide whether to commit the crime or not. In short, the individual will only choose to commit the crime if the perceived expected utility gain is greater than zero. We can denote as the vector of parameters defining the utility function of the individual (which we simply refer to as utility parameters from here on), and denote as the current penal strategy. We let the utility gain returned from the crime be , and the perceived expected disutility of the possible punishment be . The individual will be deterred from committing the crime if the net utility gain of the crime is negative, or

Note that the utility parameters are different for every individual, so given a particular deterrent strategy , the above inequality is satisfied for certain values of but violated for others. Therefore, equation 2.4.1 (at equality) can be interpreted as a partition that separates the population into offenders and non-offenders (see section 4.2 for a detailed discussion for this partition).

As a simple example, we consider the case where the parameter is fully specified by the discount rate . Imagine a scenario where two individuals, Alice and Bob, are given the opportunity to commit a crime with a guaranteed reward returning some fixed utility gain . Alice has a small discount rate , and Bob has a large discount rate . If the crime is committed, there is some fixed change of being apprehended with the punishment being a 24 hour imprisonment starting next week. According to equation 1, we see that (as ), which means that Alice perceives the disutility of the punishment to be greater than what Bob perceives. Assuming that Alice is deterred from committing the crime, then

meaning that Bob won’t necessarily be deterred as well. Intuitively, what this means is that a punishment delayed by a week for Bob may not present sufficient level of threat for Bob than it does for Alice, so the deterrent strategy is not an effective strategy for Bob.

2.4.2 Utility Function of the Victim

A very crucial assumption here is that the offender is selfish in the sense that he/she seeks only to maximize his/her utility function and disregards the utility loss for the victim. If we denote the disutility of the victim as a result of the crime to be (where is the utility parameter for the victim), then we define total utility function to be the sum of the utility functions of both parties of the crime (the offender plus the victim)

where and are the utility parameters for the offender and victim respectively. Note that the offender will act to maximize only but not . Therefore, a naive deterrent strategy would be to set the expected disutility of punishment for the offender to be exactly equal to the disutility of the victim as a result of the crime, or , which translates to the problem of solving for . Under this deterrent strategy, the offender implicitly evaluates the disutility incurred on the victim, and would act indirectly to increase the total utility function777Note that under this model, a crime is justified as long as the net change in is positive after the offense. A commonly invoked example is when a poor offender steals from a rich victim, forcing a more efficient distribution of wealth, as the marginal utility of a dollar for the offender is greater than that of the victim..

This is a rather elegant solution, but it fails in mainly two respects. First, the solution to the equation depends on the parameters and . In other words, a different deterrent strategy has to be implemented for each offender-victim pair, which is neither practical nor fair, as it implies using some behavioral traits of the offender (which may be poorly measured) as a discriminant for enforcing a particular punishment. Second, even under the assumption that this strategy is possible and the total utility function between every offender-victim pair is maximized, the implementation of this strategy may be very costly, with its cost outweighing the net increase in . A general extension of this analysis is presented in section 3.2, with the analysis being performed under a general social welfare function which encapsulates the total utility functions of all the offender-victim pairs as well as the cost of implementing the penal strategy itself.

3 General Model of Deterrence

At this point, it should be very clear that the problem of finding an optimal strategy is not a trivial task, as it requires a simultaneous maximization the total utility function of each offender-victim pair and minimization of the cost of implementing the strategy. As briefly discussed in section 2.1, the problem can be defined as finding a strategy that maximizes the social welfare function, which we define to be the sum of the total utility of every member in a population. Note that the absolute social welfare function is very difficult to define and measure (Fleurbaey, 2009), so we focus only on the relative change in the social welfare function connected to the particular crime we are studying888This includes any victim’s loss associated with the crime, the cost that went into deterring this crime, and the disutility resulting from the punishment of the offenders of this crime., which we refer to as the relative social welfare function. In this paper, the crime we are focusing on is the offense of driving under influence, or DWI or short, then the goal is to find a penal strategy (see section 2.1) such that it maximizes the relative social welfare function of the crime of DWI.

3.1 Review of Old Model

The notion of formulating the problem of finding an optimal deterrent strategy in terms of maximizing the social welfare function is not novel. A systematic formulation has been developed by Gary Becker in his seminal paper which employs economic methods to determine the optimal probability and severity of punishment (Becker, 1968). However, there are multiple problems that the original model failed to address, and we here point out the three major ones.

First, the model assumes that the cost of enforcing the punishment scales proportionally with the disutility of the punishment that the offender perceives. This is generally not the case. For example, if we double the term of imprisonment, the cost of enforcing the imprisonment may be doubled, but the disutility for the offender may not be due to the presence of hyperbolic time discounting (see equation 1). Second, the model assumes that the punishment is either a fine or imprisonment, and the offender does not have a choice between the two. This assumption is rather problematic as it suggests the ideal strategy being a fine of a very large sum of money, which would ideally deter all offenders while costing very little (as the collection cost of fines is assumed to be small). In reality, a large amount of fine is rather meaningless for individuals of low income, as they would not be able to afford it anyway. A more realistic model will be to offer the offender the option to choose between a fine, imprisonment, and other forms of punishments. Lastly, the model accounts for the fact that an increase in the probability of apprehension and severity of punishment will reduce the number of offenses. However, it does not offer a formulation that allows for estimating exactly how many offenses would be deterred. Therefore, the optimization problem formulated only exists on a theoretical level, and a closed form solution containing variables that can actually be measured in a population does not exist.

3.2 Overview of New Model

In our model, we characterize the behavioral traits of each member with the utility parameters (see section 2.4), and we attempt to describe the criminal propensity of a population by the distribution of among a population (see section 4.4), which allows us to predict the response of the population to a particular penal strategy. To be more specific, our model is based on the assumption that a strategy will partition the population into offenders and non-offenders (see section 4.2), and the social welfare function can be explicitly evaluated over this partition, so the problem is converted in some sense to the optimal partitioning of the population into offenders and non-offenders. In addition, the model also assumes that the offender has the freedom to choose between multiple punishments, and for each possible punishment, both the social cost of enforcement and the disutility incurred on the offender is carefully considered (see section 4.3).

We first present a rigorous mathematical formulation of the relative social welfare function that can be constructed with respect to any class of crimes. The idea is to assume every ordered pair of two members within a population to be a possible pair of offender and victim. And under a specific deterrent strategy, we can divide all the pairings into two main groups. The first group consists of pairings on which a criminal offense won’t be realized due to successful deterrence, and this group generates social benefits from the crimes not occurring, which factor into the social welfare function as positive summation terms. The second group consists of pairings on which the deterrence fails and the occurrence of criminal offenses is possible, and this group generate social costs associated with the enforcement of punishments on the offenders, which factor into the social welfare function as negative summation terms. The model is general but often times quite difficult to study, but in most cases, simplifications can be made under reasonable assumptions justified under the crime of interest (see section 4.1).

3.3 Opportunities and Offenses

To begin with, we define a population to be a set (Enderton, 1977) whose elements are members making up the population. We define to be the counting measure operator (Halmos, 2013) which returns the cardinality of a finite set, and we denote the size of the population to be . For every member , we can fully characterize the member with its utility parameters .

We define a particular class of crime to be . Given a crime , and some time window , a directed graph (West et al., 1996) whose vertices are is generated, with the arrows representing a potential offender-victim pair. More specifically, the arrow represents an opportunity for crime with being the offender and being the victim. We can model the arrival of opportunities at each edge to be an independent Poisson process (Durrett, 2019) with rate , with the direction of the arrow being random. Therefore, the expected number of opportunities presented to every member in the time window is approximately 999Since the arrival of opportunities at each edge is a Poisson process with rate , the formation of an arrow pointing from to some other vertex is also a Poisson process with rate . Therefore, the formation of an arrow pointing from to any of all other vertices is a sum of independent Poisson processes, with the expected value being for large ..

We denote a punishment to be , which is defined by the form101010The form of the punishment can be a simple fine, imprisonment, community service, etc., the celerity, and the severity of the punishment. We define the set of all possible punishments be . In addition, we define the probability of apprehension to be . We can then express the penal strategy as , which is an -tuple. Under this strategy, the offender will be apprehended with probability of and given choices of punishment as specified by . The set of all deterrent strategies is then given by the Cartesian product 111111There are overlapping elements in the set , as the penal strategy is not affected by the ordering of . This means that there are elements in the set corresponding to the same strategy..

3.4 Deterrence

Note that when opportunity arrives for an offeder , the offender won’t necessarily take the opportunity. The opportunity will only be realized and converted into an offense if the net utility gain from committing the crime is positive for the potential offender under the deterrent strategy . We can then write the condition for deterrence as

| (4) |

where denotes the utility that the offender expects to gain from the crime , which is dependent on both and (the traits of the offender and the victim). is the probability weighing function of the offender parameterized by . denotes the total disutility that the offender expects to be incurred on him/her after apprehension, where denotes the disutility of punishment for the offender 121212Note that is only present in the utility function of the offender if he/she is actually aware of the deterrent strategy. See section 4.2.1 for a detailed discussion of the case where the offender is uninformed.; and denotes any disutility of being apprehended not directly resulting from the punishment (such as the stigma associated with being apprehended). For the rest of the paper, we refer to simply as stigma (Decker et al., 2015). Note that the individual will always choose the punishment incurring the least disutility, hence the function.

On the other hand, we can write the net gain/loss in the social welfare function as a result of the offense to be

where denotes the disutility incurred on the victim from the offense. Note that the utility that the offender gains from the crime131313It is assumed that the utility that the offender actually gains from the crime is equal to the utility that he/she expects to gain when evaluating his/her utility function before deciding to commit the crime is taken into account as part of the social welfare function (since the social welfare function must include the utility function of the offender as well). This means the increase in the social welfare function as a result of a crime not occurring is simply the inverse of , or

| (5) |

3.5 Costs of Punishment

To model the social cost of implementing the deterrent strategy, we consider two separate costs. The first cost is associated with the apprehension probability, which we can model as a fixed cost that depends only on the apprehension probability, , which we refer to as the detection cost. And the second cost is associated with enforcing the punishment on the offender, which depends on the form of punishment and also the two parties involved, . For the sake of simplicity, we do not consider any reformation effects as a result of the punishment (see section 4.1 for cases where this is approximately true). In other words, we assume that the offender’s utility parameters will not be modified through deterrence, so there is no social benefit associated with the decrease in likelihood of recidivism (Maltz, 1984). To study the social cost associated with the punishment more closely, we consider the punishments of fine and imprisonment as examples. For the sake of simplicity, we assume that the social cost of punishment depends only on the utility parameters of the offender.

3.5.1 Costs of Fine

We first consider the example of a simple fine, where the only cost associated with this punishment is the collection cost141414We are making the general assumption that the transfer of wealth from the offender to the collector is a simple transfer of utility within the population, so it does not result in any utility gain/loss in the social welfare function. This means that we are ignoring the effect of any inefficient distribution of wealth (Coleman, 1979) that may result from this trasnfer, and the only cost associated with this transfer is the cost of forcing this transfer itself. and the disutility is due to the offender’s stigma associated with apprehension. We can then write the total social cost of using a fine as punishment as

| (6) |

where denotes the punishment of a fine, and denotes the collection cost assumed to be independent of the fine amount. We denote to be the enforcement cost corresponding to the cost of enforcing the punishment onto the offender. is a prefactor translating the offender’s stigma into the disutility incurred on the society. To see the reasoning behind this prefactor and why it is greater than one, we can assume that the offender is a productive worker, and this stigma prevents the offender from being fully productive in the future151515This is due to the offender not being able to find a suitable job due to his/her criminal records.. We set the loss in the social utility (due to the deviation of the offender’s output from his/her full capability) as , then we see that this value must be greater than the loss for the offender in his/her potential compensation for his/her work, 161616This is because in a realistic economic model, the worker is only compensated with a fraction of his output value, with the rest of the value being absorbed by the consumer and the company.. We can denote as the opportunity cost of the punishment, corresponding to the value (unrelated to the crime) that the offender is otherwise able to create if he/she were not apprehended.

3.5.2 Costs of Imprisonment

We then consider the social cost of imprisonment. Note that besides the cost of having the stigma associated with apprehension, we also have to consider social costs such as the opportunity cost of keeping the offender in prison (instead of letting him/her work) for a time period of , and also the social benefit of the offender not being able to commit any more crime for the duration of his/her term of imprisonment. We can then write the total social cost of using imprisonment as punishment as

| (7) |

where denotes the punishment of imprisonment, and is the enforcement cost which can be assumed to be a function of (the delay in punishment) and (the length of imprisonment), with an explicit expression of this cost given in equation 19. In addition to the opportunity cost incurred after the period of punishment, can be interpreted as the opportunity cost incurred during the punishment as a reuslt of the offender not working for a time duration and plus any “discomfort” he perceives from the unpleasant imprisonment environment171717If we assume the presence of time discounting, then the social disutility as a result of imprisoning the offender ( in equation 7) will be substantially different than the disutility that the offender perceives ( in equation 4). To be more specific, the in equation 7 will not be time discounted as it represents actual social disutility, while the in equation 4 will be time discounted as it represents the offender’s perception of punishment. This discrepancy is very important if we were to use the discount rate as a parameter of when partitioning the population and evaluating the social cost of imprisonment (see sections 4.2 and 4.3).. The reasoning for the prefactor is similar to the discussion in the previous paragraph. And the last term denotes the social benefit of the criminal opportunities not being realized as a crime for a time period of .

3.6 Population Partition

We first define the following set of all ordered pairs , which corresponds to all possible offender-victim pairs. We may partition this set into multiple subsets given a deterrent strategy . We denote the first subset as , which satisfies the following condition

In other words, when an opportunity is formed from to , the offense will not be realized as the net utility gain for the offender is negative. The complement of this subset denotes the set of pairs on which offenses will be realized, and it can be further partitioned into disjoint subsets, with being the number of punishment options. For every , the subset satisfies the following condition

In other words, whenever an opportunity is formed from to , an offense will be realized as the net utility gain for the offender is positive. Furthermore, when caught, the offender will choose as punishment.

3.7 Social Welfare Function

We are now finally in the position to construct the social welfare function particular to the crime . We first zero the social welfare function to the welfare level corresponding to the scenario where every criminal opportunity has been realized, and no deterrent strategy has been implemented, then the problem of maximizing the expected social welfare function with respect to all possible deterrent strategies is given by (where the subscript is assumed)

| (8) |

Note that enters implicitly in the expression through the partitioning of the set and the cost associated with the punishment of offenders .

In this form, the model is complete. However, this formulation is not useful in any practical sense due to two reasons. First, in order for the optimization problem to be defined, we have to specify the distribution of in the population , otherwise there would be no way to “count” the number of members in each of the partitions of . The second problem is that the optimization problem is not computationally feasible. If we analyze the time complexity (Papadimitriou, 2003) of performing this optimization brute force, the algorithm has to check all possible deterrent strategies, with the number of operations scaling exponentially with 181818This is assuming some sort of discretization of the set of all possible deterrent strategies . Furthermore, given a penal strategy, the partitioning of requires operations191919This is because all edges have be to be checked, and the number of edges for a complete graph of vertices is .. Therefore, the time complexity of a brute force algorithm would be , which presents a major computational challenge.

4 A DWI Case Study

As discussed in section 3.7, the general form of the optimization problem as appeared in equation 8 is intractable from a computational standpoint. However, if we assume that the optimization problem is performed in the context of a specific crime, many simplifying assumptions can usually be made. In this section, we focus on the crime of DWI as an illustrative case study.

4.1 Simplifying Assumptions

If we let the crime be the class of DWI crimes, then there are several assumptions we can make to simplify the optimization problem as given in equation 8, to the point where an analytic approach is possible. There are two things to note. First, these assumptions are not strictly necessary for the main results of the paper to hold. Second, alternative simplifications can also be made depending on the crime of interest. We here make assumptions that are justified particular to the crime of DWI.

We first state the seven assumptions that we make, followed by a detailed discussion of the justification of these assumptions

-

•

Assumption One: Every member can be fully characterized by his/her level of wealth and discount rate.

-

•

Assumption Two: The utility function of every member is static.

-

•

Assumption Three: The probability weighing factor is constant for the population.

-

•

Assumption Four: The utility gain from an offense for the offender is dependent on his/her level of wealth, and the utility loss from an offense for the victim is fixed in expected value.

-

•

Assumption Five: The penal strategy is static and non-discriminatory is expected value.

-

•

Assumption Six: The opportunity cost of imprisonment, , scales proportionally with the offender’s level of wealth. In addition, the opportunity cost incurred during the punishment, , scales proportionally with the term of imprisonment .

-

•

Assumption Seven: The stigma associated with apprehension is independent of the form of punishment.

Assumption one means that can be fully specified with two parameters, where denotes the level of wealth and denotes the discount rate. We believe that these two parameters describe well the criminal behaviors of a population (see section 2.2), and can be easily measured within a population (see section 6). For an individual, the level of wealth correlates strongly with the utility gain from committing DWI (to be discussed shortly) and the opportunity cost of imprisonment (see section 3.5). The discount rate governs how fast the disutility of punishment decays with its delay (see section 2.2). In some sense, this pair of parameters allows us to determine the “level” of deterrence that the member perceives from a penal strategy, allowing us to predict his/her response when given a criminal opportunity. Furthermore, the disutility incurred on the member as a result of the punishment can also be easily evaluated from the two parameters.

Assumption two means that the utility function of the individual does not evolve in time, or at least in the time window in which the penal strategy is in effect. In the context of DWI, this means that as long as the punishment of multiple offenses is equal to the first offense, the offender won’t be less inclined to commit DWI even after an accident or apprehension. In other words, recidivism is possible for the offender. Even if we were to relax this assumption and allow the utility function of an offender to be modified after an accident or apprehension, if we assume that the probability of accident or apprehension is sufficiently small or the time interval between two consecutive DWI offenses is at the same order as the penal strategy time window202020If the probability of accident or apprehension is small, then we are only mismodeling a small fraction of the population whose utility functions are modified after the incident. Similarly, if the rate of DWI offenses is small, then we can assume that the rate of change in the utility function is also small, allowing us to make the static assumption (Kołsos, 1970) in the time frame where the penal strategy is implemented., then the change in the utility function will only account for a second order correction to the partitioning of the population, which we can ignore.

Assumption three states that the probability weighing factor is the same for every individual. Although this is not necessarily a realistic assumption (as seen in section 6.2), it is crucial for the simplification of the optimization problem as the function is related to in a highly nonlinear fashion (see equation 3).

Assumption four is a reasonable assumption in the context of drunk driving. Whenever an individual decides to commit DWI, in the majority of cases, it is usually motivated by the fact that the alternative of not committing DWI will result in some disutility scaling positively with his/her level of wealth212121A typical example would be when a person decides to drive home from a bar after drinking, the corresponding alternative would be to call a taxi and pick up his/her vehicle the next day, and the time spent doing so will result in the decrease of total productivity correlated positively with his/her current level of wealth (Jacobs, 1989). Furthermore, it can be assumed that probability and severity of the damages resulting from the DWI act is independent of . To begin with, the purpose of performing DWI (unlike other crimes such as burglary) is not for the forceful transfer of wealth from the victim to the offender, so there is no reason to assume that the expected disutility incurred on the victim will depend on the utility parameters of either party222222The involvement in a car accident is generally unintentional, with the probability and severity of damage correlated with the ability of the driver to operate the vehicle under influence, which can be reasonably assumed to be independent of . The damage can be set fixed in expected value, which is simply the expected damage of the car accident weighted by the probability.. This allows us to set the expected loss to the victim to some fixed amount.

Assumption five means that the probability of apprehension and punishment choices are the same for every offender regardless of his/her . However, DWI incidents may result in varying level of damages, ranging from minor damages such as running into a pole to serious damages such as killing a pedestrian. The punishment obviously has to be discriminatory towards the level of damages to be in accordance with criminal justice, meaning that offenders whose DWI act resulted in severe damages should be punished more severely. Nevertheless, as discussed in the last paragraph, the expected damage is fixed for every , so we can also make the assumption that the expected punishment will also be the same every . This implies that the enforcement cost of the punishment should be constant in expected value.

Assumption six states that the total loss in the value of the offender’s labor output (as a result of imprisonment) scales proportionally with his/her level of wealth. This is a fair assumption as a member’s level of wealth should act as a strong indicator of his/her rate of productivity. And since the total value of output is simply the rate of productivity multiplied by the time period, it can also be assumed that the opportunity cost incurred during the imprisonment period scales proportionally with the term of imprisonment.

Assumption seven implies that the negative effects of having a DWI record itself is the same regardless of punishment options that the offender chooses. This makes sense because the severity of the crime itself should be the only substantial characterization of the criminal background of the offender, and the form of punishment (or even the severity of punishment) should play little role in affecting the future prospect of the offender.

Under these assumptions, equations 4 and 5 simplify to

| (9) |

respectively, noting that the functions are independent of , or the victim’s utility parameters. And this allows for considerable simplification for the social welfare function in equation 8.

For further simplification, we can assume that a fine and imprisonment are the two only punishment options , or and . The the social welfare function can be reduced to

| (10) |

where the domain of optimization and the subscript is assumed. To understand this reduction, First, we first realize that neither the summands nor the partitions depend on (the victim) anymore, so the summation over is factored out to give us a prefactor of

Since the partition depends only the offender , we can define the partition over the vertices instead of the pairs 232323The partitioning is defined through the first equation in 9, which is only dependent on .. We then denote the three subsets as 242424 corresponds to non-offenders. corresponds to offenders choosing a fine over imprisonment. corresponds to offenders choosing imprisonment over a fine., with the number of subsets being as there are only two choices of punishments (fine or imprisonment). Recall that this optimization problem is over five parameters (see section 2.1), which is still somewhat computationally expensive. We show in the following sections how we can reparameterize the penal strategy to better specify the partitioning of the population (section 4.2), and how certain assumptions can be assumed to reduce the optimization to its asymptotic form (section 5.2).

4.2 Population Partition

There are several factors that enter the mindset of a potential offender performing DWI. The first is simply the utility gain from the crime itself, which we can assume to scale proportionally with his/her level of wealth (see 4.1)

where is denoted as the scaling factor. Recall that the probability of apprehension is , which the offender evaluates to , and the offender has the choice between a fine or imprisonment. For a fine, we can denote the disutility to be , and for imprisonment, we can write its disutility magnitude as (see equation 1)

| (11) |

where the expression is scaled with . Recall that is the length of imprisonment, and is the time of the delay in punishment.

If we model the stigma as , then the member will be deterred from committing a DWI offense if the following is satisfied (see equation 4)

| (12) |

where we’ve applied the assumption that the incurred stigma is independent of the form of punishment (hence why the min function is only over and ). The above inequality can be expressed equivalently as

| (13) |

If we denote

| (14) |

then the first condition can be written as . And since is a monotonously increasing function with respect to , there must be only one solution to the second condition in equation 13 at equality, which we can denote as 252525Note that no analytic expression of exists at is the solution to a transcendental equation.. Then similarly, we are allowed to write the second condition as .

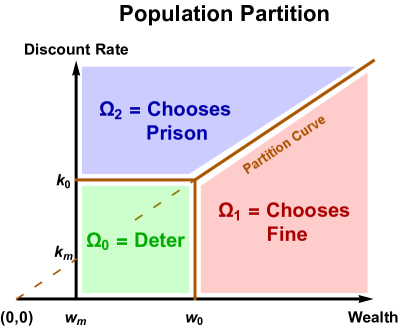

We then see that in order for an individual to be deterred, its level wealth must be below and its discount rate must be below . We then say that the penal strategy is targeting a wealth level of and a discount rate of . This defines the first subset of population (see section 3.2), which we term the non-offenders. We can interpret the subset as consisting members whose level of wealth is sufficiently low to be deterred by a fine of amount , while simultaneously having a sufficiently small discount rate to be deterred by an imprisonment length of (delayed by ). Note that given a strategy targeting , the amount of fine is specified by

And given a strategy targeting , the pair must be related as follow

| (15) |

where the is defined as follow

| (16) |

An important side note to mention is that in a realistic population sample, there should always be some positive infimum to the set of wealth levels which we can denote as , or

This assumption is necessary to account for some minimal wage standard of the society, and to make it mathematically possible to model the wealth distribution as a Pareto distribution (Arnold, 2014), for which there must be a positive lower bound to the domain of the distribution (see section 4.4). We then consider a possible strategy where the targeted wealth level is smaller than the minimum wealth level, or . In this case, every member would be an offender (or the non-offender subset, , would be empty), as the disutility of the fine is too small to deter a member of even the lowest level of wealth. For the sake of optimization, we don’t have to consider this strategy as this strategy only incurs enforcement cost, but does not return any social benefit as none of the members are deterred by the strategy.

The offenders are members in the population for which the penal strategy fails, and the set of offenders can be denoted as the complement of the set of non-offender, or . The set of offenders can be further partitioned into two subsets depending on whether the offender chooses a fine or imprisonment after being apprehended. The partition can be expressed as a curve on the coordinate system on which the members are indifferent towards the two punishment options. This is done by simply taking the two arguments of the function in equation 12 to be equal, which gives us

| (17) |

The above equation defines a curve in the coordinate system dividing the population into two regions. On one side of the curve, the population prefers a fine over imprisonment; we denote this subset as . On the other side of the curve, the population prefers imprisonment over a fine; we denote this subset as . We call this curve the partition curve. See figure 1 for a visual representation of the partition. Note that the offenders choosing a fine over imprisonment have a relatively low discount rate and high level of wealth, and the offenders choosing imprisonment over a fine have a relatively high discount rate and low level of wealth.

In most cases, we can approximate the partition curve as a straight line

| (18) |

noting that this expression does not depend explicitly on . See appendix B for a discussion on how the approximation is carried out. The partitioning scheme is then completely defined by the pair (see figure 1), which provides a huge simplification from the original 5 degrees of freedom of the penal strategy . From equation 15, we see that given and , can be uniquely specified, so the deterrent strategy can be alternatively parameterized as . The purpose of using as parameters is to reduce the complexity of the optimization problem by allowing the boundaries of the partitions to be easily described by the two parameters (see section 4.4).

4.2.1 Uninformed Members

The majority of the analysis performed in this section can be easily extended to model the population that is uninformed of the law (Kaplow, 1990). If a member is uninformed, then he/she is unaware of the deterrent strategy, thus the total disutility will be absent from his/her utility function, which gives us

We can make the simplifying assumption that (meaning that the utility gain from the crime is always greater than the stigma associated with apprehension), then the utility function is strictly positive. Therefore, the uninformed member will always choose to commit the crime given the opportunity.

This means that the uninformed members won’t contribute to the subset , since all of them are assumed to be offenders. However, when apprehended, an uninformed member would be given the same choices of punishments (as an informed member would be), so the partitioning between and still applies to the uninformed population exactly as it would for the informed population.

4.3 Social Welfare Function

Recall from section 3.2 that given a particular strategy , the social welfare function can be written as the social benefit gained from the deterred crimes under the strategy minus the detection cost and social cost of punishment (which is further broken down into enforcement cost and opportunity cost).

We first focus on the social benefit of deterred crimes. Whenever an individual commits an offense, a loss is usually incurred on the society. Using equation 9, we expressed the expected utility gain/loss of the society after an offense to be

where is the increase in utility of the offender, is the expected disutility incurred on the victim (assumed constant). If we zero the utility function to be when all criminal opportunities are realized and no penal strategy is in effect (see section 3.2), then the utility gain/loss of the society after an offense being deterred is simply the inverse of , or

We now consider the costs associated with implementing the strategy. We first look at the detection cost, which we can assume to scale proportionally with the probability of detection

where is the scaling factor262626A more realistic cost model for the probability of apprehension would be (Note that this expression diverges for , corresponding to the fact that certain apprehension is not possible in reality.) The derivation of this cost model is based on the fact that the failure of apprehension should decay exponentially with the number of “checkpoints”, which should scale proportionally with the cost. However, for , this can be approximated with ..

Lastly, we consider the social costs of the punishments. From equation 6, we see that the social cost of using a fine as punishment can be written as

where is the fixed collection cost and is the opportunity cost. Similarly, from equation 7, we write the social cost of using imprisonment as punishment as

where is the opportunity cost of imprisonment, and is the social benefit of the offender not being able to commit crimes for a time duration of . For the enforcement cost of imprisonment, we require that

which implies that the cost increases with duration of imprisonment and decreases with the length of delay272727The reason why we assume that the enforcement cost decreases with the length of delay is an empirical assumption. Consider a scenario where the punishment of imprisonment is enforced with a delay rather than being immediate, then the party enforcing the punishment will have sufficient time to better allocate the resources necessary for the enforcement, so that the enforcement will be performed in a more economically efficient fashion. In addition, there should also be the legal cost associated with sentencing the offender, and we can assume that the cost to increase with the rate at which the legal process is carried out.. A possible cost model of that satisfies the two conditions above can be written as

| (19) |

where is some fixed cost of enforcing the punishment that does not depend on or . can be interpreted as the “celerity” cost of the punishment that scales inversely with . The choice of using as the “celerity” cost is for analytic convenience and is not entirely realistic, though the exact choice of the celerity cost model does not alter the major results of this work282828In this work, we are only interested in the asymptotic scaling behavior of the social costs of imprisonment (see appendix C) with respect to , which should be at least exponential regardless of celerity cost model we use (as long as ). To see this, simply consider a cost model without celerity cost, or , which should give us the best scaling with respect to (as it does not incur any additional cost to decrease the delay in punishment). We simply set , then from equation 15, we see that scales exponentially with , which implies that must also scale exponentially. Therefore, for any celerity cost model satisfying , the social costs of imprisonment must scale at least exponentially with as well.. And is the “severity” cost which scales proportionally with the duration of imprisonment .

Putting everything together, we see that the total social costs associated with each punishment option (fine and imprisonment) can be written as

| (20) |

where is associated with the punishment of a fine, and is associated with the punishment of imprisonment. Therefore, equation 10 can be expressed explicitly as

| (21) |

where we’ve denoted . Note that the prefactor is ignored and simply absorbed into the constant 292929This gives us , which can be interpreted as the cost of apprehension per unit probability, per unit time, per unit population, per unit criminal activity.. At this point, we have accomplished two major task. The bounds of the summation indices (or the population partition in the space) are uniquely specified by (see 4.2), and the summands are expressed in terms of (with and constrained as equation 15). However, to perform the summation, we still have to know exactly how is distributed among each subset . In other words, we have to define the measure over which the summation is performed (Halmos, 2013). This is done in the immediately following section, by assuming a distribution of over the population.

4.4 Modeling the Distribution of Traits

The optimization can be made simpler if we approximate the counting measure as a probability measure scaled by the total population , where accounts for the uninformed population303030It is assumed that the distribution of over the informed and uninformed population will be the same.. In other words, the number of members with traits can be approximated as

where can be interpreted as the “density” of population with traits . If we further assume that and are distributed independently (with an empirical justification presented in section 6.3), then can be factorized as

We can model the distribution of wealth, , as a Pareto distribution (Arnold, 2014) with the domain being , where is the minimum wealth level of the population

| (22) |

In addition, we can model the distribution of discount rate, , as a zero-inflated313131Note that the use of the term “zero-inflated” is not technically valid, as the model is a continuous distribution instead of a discrete one. The term is rather used to denote the fact a large probability measure is concentrated at . exponential distribution (Lambert, 1992)

| (23) |

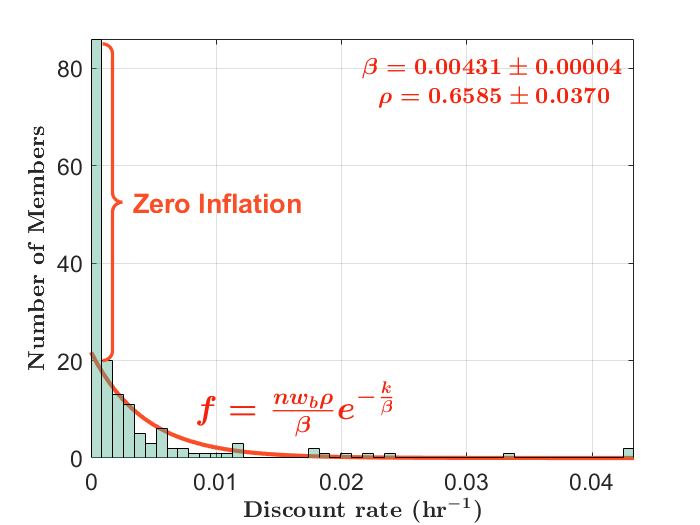

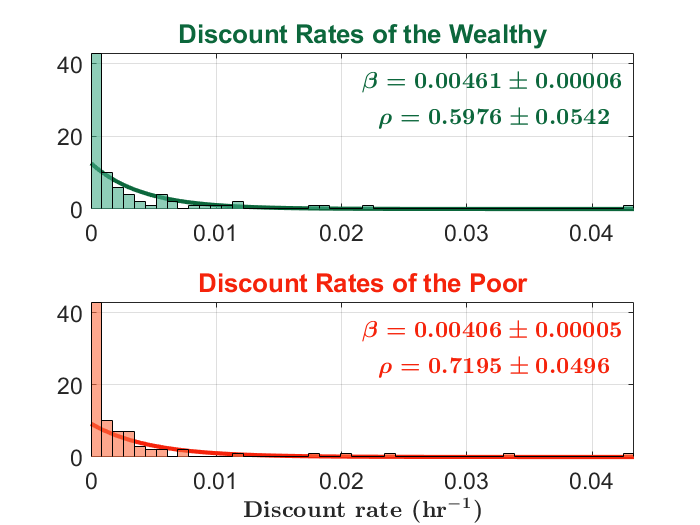

where is the Dirac Delta function323232The Dirac Delta function is a function that evaluates to zero everywhere except at , at which it is undefined. However, the Dirac Delta function has a well-defined integral which evaluates to one, or . Alternatively, can be interpreted as a distribution that generates a probability measure that is completely localized at . The use of is for the convenience of modeling the high concentration of probability measure at . Its use is not strictly necessary. In fact, any distribution that generates a high concentration of probability measure close to would suffice (Arfken and Weber, 1999), which accounts for the phenomenon that the majority of the population is expected to have a discount rate close to zero (meaning that most people are “rational” in time). The parameter is the fraction of population with non-zero discount rate, and is the mean discount rate among that population. The form of this distribution is justified with empirical measurements in a sample population of size 207 in section 6.1, where it is shown that the discount rates of the sample is well fitted by this distribution, and the estimators for from the sample are given.

Having now modeled the distribution of , we now give the explicit form of the social welfare function in integration form. For the sake of convenience, we first denote the following ratios

| (24) |

Under the assumption that , or equivalently , the social welfare function can be approximated as follow

| (25) |

where again, we are ignoring the prefactor of by absorbing it into the constant (see section 4.3) and the expression for the social costs of imprisonment, is given in equation 20. A visual representation of the bounds of the integrals is given in figure 1. Note that at this point, the optimization problem is completely well defined over the parameters , and the following section will be devoted to solving this optimization through a combination of the techniques of further reparameterization and asymptotic analysis.

5 Solving the Full Optimization Problem

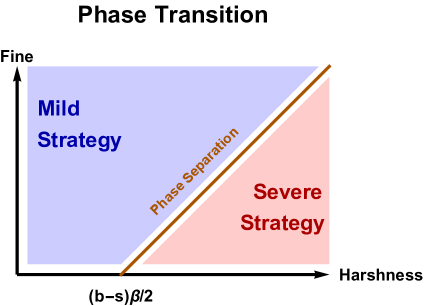

In this section, we perform an explicit optimization on the social welfare function. Even though the tools used for performing the optimization contains certain mathematical technicalities, there is a central concept that can be readily understood on an intuitive level. In short, we show that the pair (the fine amount and the harshness of imprisonment condition) is able to together induce an interesting phase transition on the optimal penal strategy. Section 5.1 provide an informal discussion of the concept of phase transition which originates from statistical physics (Mézard et al., 1987). In short, we show that when is above a certain threshold (or when the imprisonment condition is sufficiently harsh) and is below a certain threshold (or when the amount of fine is sufficiently small), then the social welfare function favors a penal strategy with a very severe term of imprisonment; otherwise, a severe term of imprisonment is not favored.

5.1 Phase Transition

The term phase transition (Mézard et al., 1987) is mainly used in physics to commonly describe the transition between different states of matter such as from solid to liquid (melting) or from liquid to gas (boiling). We here make no attempt to formally define the concept of phase transition as it is not completely relevant to our main points of discussion. In fact, we use the term phase transition very loosely in the context of penology to describe the phenomenon where when certain penal parameters cross a threshold, the space of realizable333333A realizable penal strategy means one that can be implemented without an excessively large amount of social cost penal strategies experiences a sudden change. This is analogous to the natural phenomenon where as a thermodynamic parameter (such as temperature) crosses a threshold (Prigogine et al., 1961), the state of the matter changes discontinuously (such as water boiling at 100 degrees). Here, our “thermodynamic parameter” are , and when it crosses a certain threshold, the value at the optimal penal strategy rises abruptly to an extremely high value, corresponding to the phenomenon where a severe strategy suddenly becomes favorable.

5.2 Reparameterization of the Social Welfare Function

Note that in section 4.4, we assumed that the factorization of the pdf of is possible, or . This means that the integrals over (see equation 25) can also be factorized as separate integrals over and , which allows for considerable simplification. If we denote the integral corresponding to subset as (meaning that the social welfare function can be written as ), then we find the following closed form expressions for the three integrals (where the denotations in equation 24 are applied)

where the following denotations are made

Note that denotes an exponential integral and denotes the upper Gamma function with their respective integrals (an asymptotic approximation) given by

The integrals can then be further reduced by applying these asymptotic approximations