Localizing Changes in High-Dimensional Vector Autoregressive Processes

Abstract

Autoregressive models capture stochastic processes in which past realizations determine the generative distribution of new data; they arise naturally in a variety of industrial, biomedical, and financial settings. A key challenge when working with such data is to determine when the underlying generative model has changed, as this can offer insights into distinct operating regimes of the underlying system. This paper describes a novel dynamic programming approach to localizing changes in high-dimensional autoregressive processes and associated error rates that improve upon the prior state of the art. When the model parameters are piecewise constant over time and the corresponding process is piecewise stable, the proposed dynamic programming algorithm consistently localizes change points even as the dimensionality, the sparsity of the coefficient matrices, the temporal spacing between two consecutive change points, and the magnitude of the difference of two consecutive coefficient matrices are allowed to vary with the sample size. Furthermore, the accuracy of initial, coarse change point localization estimates can be boosted via a computationally-efficient refinement algorithm that provably improves the localization error rate. Finally, a comprehensive simulation experiments and a real data analysis are provided to show the numerical superiority of our proposed methods.

Keywords: High dimensions; Vector autoregressive models; Dynamic programming; Change point detection.

1 Introduction

High-dimensional data are routinely collected in both traditional and emerging application areas. Time series data are by no means immune to this high dimensionality trend, and commonly arise in applications from econometrics (e.g. Bai and Perron, 1998; De Mol et al., 2008), finance (e.g. Chen and Gupta, 1997), genetics (e.g. Michailidis and d’Alché Buc, 2013), neuroimaging (e.g. Smith, 2012; Bolstad et al., 2011), predictive maintenance (e.g. Susto et al., 2014; Swanson, 2001; Yam et al., 2001), to name but a few.

Arguably, the most popular tool in modeling high-dimensional time series is the vector autoregressive (VAR) model (see e.g. Lütkepohl, 2005), where a -dimension time series is at a given time is prescribed as white noise perturbation a linear combinations of its past values; see Section 1.1 below for a definition. In its simplest form, a VAR(1) model implies that for and a given coefficient matrix . When is large relative to the number of observed samples in the time series, we refer to this as a high-dimensional VAR model. A large body of literature focuses estimation of parameters of these processes when the time series is stationary (as detailed in the related work section). In this paper, we consider non-stationary VAR models in which the linear coefficients are allowed to change as a function time in piece-wise constant manner. For a VAR(1) model, this implies that

where the entries of are piecewise-constant over time. The change point detection problem of interest is to estimate the times at which . This model is defined precisely in 1 below.

Despite the vast body of literature on different change point detection problems, the study on 1 is scarce (e.g. Safikhani and Shojaie, 2020) and popular change point detection methods focusing on mean or covariance changes do not perform well when the data corresponds to a non-stationary VAR model. This claim is supported by extensive numerical experiments in Section 5.1; for now, we present a teaser in Example 1.

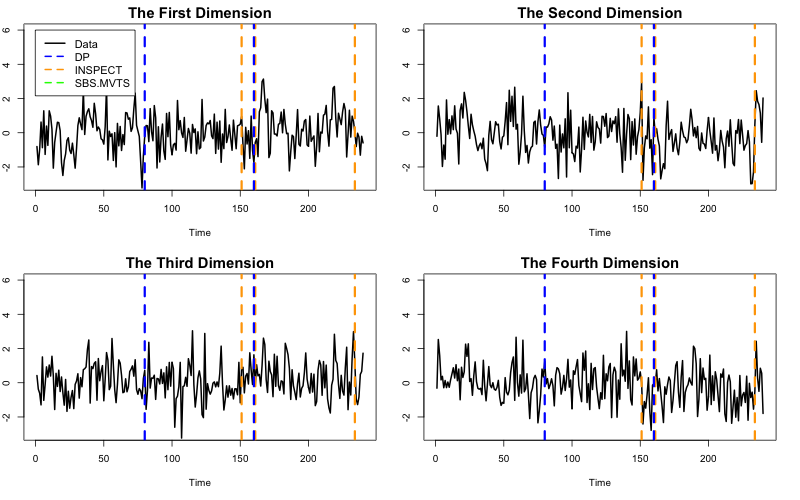

Example 1.

Let be generated from 1, with the number of samples , , lag and noise variance . The change points are and . The coefficient matrices are

where with odd coordinates being 0.1 and even coordinates being and is an all zero matrix.

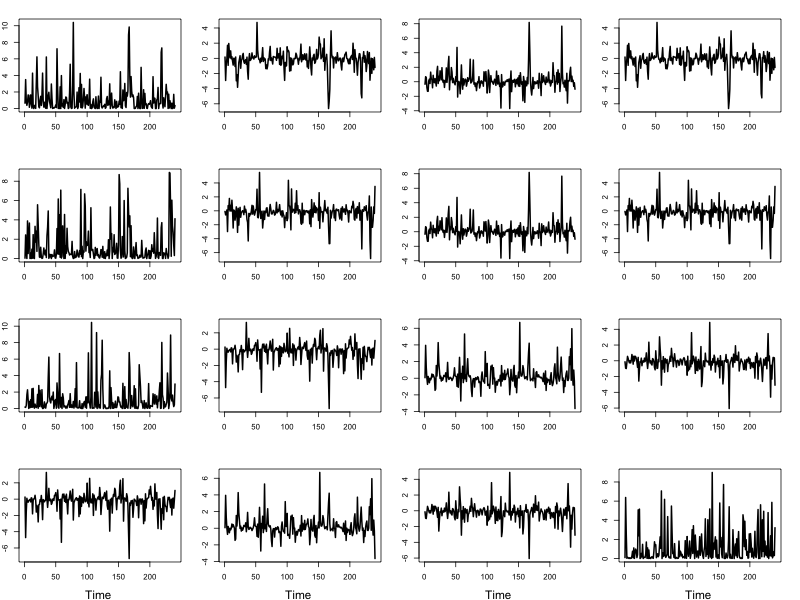

(A systematic study of Example 1 is provided in Section 5.1 scenario (ii).) Figures 1 and 2 show the first four coordinates of one realization of this process and the leading sub-matrices of their sample covariance matrices, respectively. As we can see from the black curves, the change points are not discernible from the raw data or the sample covariances. This phenomenon is further demonstrated in Figure 1 where two renowned competitors – “inspect” (Wang and Samworth, 2020) and “SBS-MVTS” (Baranowski and Fryzlewicz, 2019) – both fail here, but our proposed method penalized dynamic programming approach, indicated by DP and to be discussed in this paper, manages to identify the correct change points.

1.1 Problem formulation

We begin with a formal definition of a VAR process with lag :

Definition 1 (Vector autoregressive process with lag .).

The sequence is generated from a Gaussian vector autoregressive process with lag , , if there exists a collection of coefficient matrices such that

| (1) |

where and .

In addition, the time series is stable, if

| (2) |

In this paper, we study a specific type of non-stationary high-dimensional VAR model, which possesses piecewise-constant coefficient matrices, formally introduced in 1, which is built upon Definition 1.

Model 1 (Autoregressive model).

Let be a time series with random vectors in and let be an increasing sequence of change points. Let be the minimal spacing between consecutive change points, defined as

| (3) |

For any , set . We assume the following.

-

•

For each , , it holds that and are independent.

-

•

For each , is a subset of an infinite stable time series with coefficient matrices , with (see Definition 1).

-

•

For each , , satisfies the model

where if , and ’s are unobserved latent random vectors drawn from if .

Remark 1.

When defining a VAR() process, one implicitly assumes the lag- coefficient matrix is non-zero. In 1, we assume that each piece is taken from a stable VAR() process. In fact, what we only need is that is taken from a stable VAR() process and .

Given data sampled from 1, our main task is to develop computationally-efficient algorithms that can consistently estimate both the unknown number of change points and the change points , at which the coefficient matrices change. That is, we seek consistent estimators , such that, as the sample size grows unbounded, it holds with probability tending to 1 that

In the rest of the paper, we refer to as the localization error and as the localization rate.

1.2 Summary of main contributions

We now summarize the main contributions of this paper. First, we provide accurate change point estimators for 1 in high-dimensional settings where we allow model parameters, including the dimensionality of the data , the sparsity parameter , defined to be the number of non-zero entries of the coefficient matrices, the number of change points , the smallest distance between two consecutive change points , and the smallest difference between two consecutive different coefficient matrices (formally defined in 9 below), to change with the sample size . To the best of our knowledge, the theoretical results we provide in this paper are significantly sharper than any existing literature.

We note that these sharp bounds require several technical advances. Specifically, most existing change point detection methods assumes subsequent observations are independent, making key technical steps such as establishing restricted eigenvalue conditions easily verified. In contrast, our observations exhibit temporal dependence; no existing literature implies our results. Furthermore, we cannot directly leverage high-dimensional stationary VAR estimation bounds to obtain rates on change point detection. Analysis of our algorithm requires delicate treatment of small intervals between potential change points that allows us to prevent false discoveries and obtain sharp rates.

Second, we generalize the minimal partitioning problem (e.g. Friedrich et al., 2008) to suit the change point localizing problem in piecewise-stable high-dimensional vector autoregressive processes. The optimization problem can be solved using dynamic programming approaches in polynomial time. As we will further emphasize, this optimization tool is by no means new and has been mainly used to solve change point detection in univariate data sequences. In this paper, we have shown that for a much more sophisticated problem, this simple tool combined with the appropriate inputs computed by our method will still be able to produce consistent estimators.

Last, in the event that an initial estimator is at hand and satisfies mild conditions, we further devise an additional second step (Algorithm 2), to deliver a provably better localization error rate, even though our initial estimator’s output from the dynamic programming approach already provides the sharpest rates among the ones in the existing literature.

1.3 Related work

For the model described in Definition 1, if the dimensionality diverges as the sample size goes unbounded, then it is a high-dimensional VAR model, the recent literature on estimation of stationary high-dimensional VAR models is vast. Hsu et al. (2008), Haufe et al. (2010), Shojaie and Michailidis (2010), Basu and Michailidis (2015), Michailidis and d’Alché Buc (2013), Loh and Wainwright (2011), Wu and Wu (2016), Bolstad et al. (2011), Basu and Michailidis (2015), among many others, studied different aspects of the Lasso penalised VAR models; Han et al. (2015) utilized the Dantzig selector; Bickel and Gel (2011), Guo et al. (2016) and others resorted to banded autocovariance structures for time series modeling; the low rank conditions were exploited in Forni et al. (2005), Lam and Yao (2012), Chang et al. (2015), Chang et al. (2018), among many others; Xiao and Wu (2012), Chen et al. (2013) and Tank et al. (2015) focused on the properties of the covariance and precision matrices; various other inference related problems were also studied in Chang et al. (2017), Fiecas et al. (2018), Schneider-Luftman and Walden (2016), among many others.

The above list of references, far from being complete, is concerned with stationary time series. As for non-stationary high-dimensional time series data, Zhang et al. (2019) and Tu et al. (2017), among others, studied error-correction models; Wang et al. (2017) and Aue et al. (2009) examined the covariance change point detection problem; Cho and Fryzlewicz (2015),Cho (2016), Wang and Samworth (2018), Dette and Gösmann (2018), among many others, studied change point detection for high-dimensional time series with piecewise-constant mean; recently, Leonardi and Bühlmann (2016) examined the change point detection problem in regression setting and Safikhani and Shojaie (2020) proposed a fused-Lasso-based approach to estimate both the change points and the parameters of high-dimensional piecewise VAR models.

1.4 Notation

Throughout this paper, we adopt the following notation. For any set , denotes its cardinality. For any vector , let , , and be its -, -, - and entry-wise maximum norms, respectively; and let be the th coordinate of . For any square matrix , let and be the smallest and largest eigenvalues of matrix , respectively; for a non-empty , let be the sub matrix of consisting of the entries in coordinates . For any matrix , let be the operator norm of ; let , and , where is the vectorization of by stacking the columns of . In fact, corresponds to the Frobenius norm of . For any pair of integers with , we let and be the corresponding integer intervals.

2 Methods

In this section, we detail our approaches. In Section 2.1, we use a dynamic programming approach to solve the minimal partition problem (4), which involves a loss function based on Lasso estimators of the coefficient matrices (6) and which provides a sequence of change point estimators. In Section 2.2, we propose an optional post-processing algorithm, which requires an initial estimate as input. Such inputs can (but is not restricted to) be the estimator analyzed in Section 2.1. The core of the post-processing algorithm is to exploit a group Lasso estimation to provide refined change point estimators.

2.1 The minimal partitioning problem and dynamic programming approach

To achieve the goal of obtaining consistent change point estimators, we adopt a dynamic programming approach. In detail, let be an interval partition of into time intervals, i.e.

for some integers , where . For a positive tuning parameter , let

| (4) |

where is a loss function to be specified below, is the cardinality of and the minimization is taken over all possible interval partitions of .

The change point estimator induced by the solution to (4) is simply obtained by taking all the left endpoints of the intervals , except . The optimization problem (4) is known as the minimal partition problem and can be solved using dynamic programming with computational cost of order , where denotes the computational cost of solving with (see e.g. Algorithm 1 in Friedrich et al., 2008). Algorithms based on (4) are widely used in the change point detection literature. Friedrich et al. (2008), Killick et al. (2012), Rigaill (2010), Maidstone et al. (2017), Wang et al. (2018b), among others, studied dynamic programming approaches for change point analysis involving a univariate time series with piecewise-constant means. Leonardi and Bühlmann (2016) examined high-dimensional linear regression change point detection problems by using a version of dynamic programming approach.

We will tackle 1 in the framework of (4), by setting , where are two positive integers and

| (5) |

with

| (6) |

In the sequel, for simplicity we refer to the change point estimation pipeline based on (4), (5) and (6) as the dynamic programming (DP) approach. In the DP approach, the estimation is twofold. Firstly, we estimate the high-dimensional coefficient matrices adopting the Lasso procedure in (6), where the tuning parameter is used to obtain sparse estimates. Secondly, with the estimated coefficient matrices, we summon the minimal partitioning setup in (4) to obtain change point estimators, where the tuning parameter is deployed to penalize over-partitioning. More discussions on the choice of tuning parameters will be provided later in the sense of both theoretical guarantees and practical guidance.

Note that in (5) and (6), the summation over is taken only from to in order to guarantee that the loss function on each interval is solely depending on the information in that interval. For notational simplicity and with some abuse of the notation, in the proofs provided in the Appendices, we will just use instead of .

For completeness, we present the DP procedure in Algorithm 1.

2.2 Post processing through group Lasso

As shown in Section 3 below, the DP approach in Algorithm 1 delivers consistent change point estimators with localization error rate that are sharper than any other rates previously established in the literature. In fact, these rates can be further improved upon by deploying a more sophisticated procedure that refines the initial change point estimators via post-processing through group Lasso (PGL), step detailed in Algorithm 2.

| (7) |

The idea of the PGL algorithm is to refine a preliminary collection of change point estimators , which is taken in as inputs. The preliminary change point estimators produce a sequence of consecutive triplets , with and . The rest of the post processing works in each interval to refine the estimator , and thus can be scaled parallel.

In each interval, we first shrink it to a narrower one , in order to avoid false positive. The constants and are to some extent ad hoc, but works for a wide range of initial estimators, which are not necessarily consistent. We then conduct group Lasso procedure stated in (7) to refine . The improvement will be quantified in Section 3. Intuitively, the group Lasso penalty exploits the piecewise-constant property of the coefficient matrices and improves the estimation. It is worth mentioning that one may replace the Lasso penalty in (6) with the group Lasso penalty in the initial estimation stage and to improve the estimation from there, but due to the computational cost of the group Lasso estimation, we stick to the two-step strategy we introduce in this paper.

3 Consistency of the change point estimators

In this section, we provide the theoretical guarantees for the change point estimators arising from the DP approach and the PGL algorithm, based on data generated from 1.

3.1 Assumptions

We begin by formulating the assumptions we impose to derive consistency guarantees.

Assumption 1.

Consider 1. We assume the following.

-

a.

(Sparsity). The coefficient matrices satisfy the stability condition (2) and there exists a subset , , such that

In addition, suppose that

-

b.

(Spectral density conditions). For , , let be the population version of the lag- autocovariance function of and let be the corresponding spectral density function, defined as

Assume that

and

-

c.

(Signal-to-noise ratio). For any , there exists an absolute constant , dependent on and , such that

(8) where is the minimal spacing (see 3 above) and is the minimal jump size, defined as

(9) In addition, suppose that for some absolute constant .

1(a) and (b) are imposed to guarantee that the Lasso estimators in (6) exhibit good performance, while 1(c) can be interpreted as a signal-to-noise ratio condition for detecting and estimating the location of the change points. We further elaborate on these conditions next.

-

•

Sparsity. The set appearing in 1(a) is a superset of the union of all the nonzero entries of all the coefficient matrices. If, alternatively, the sparsity parameter is defined as , where and , for all , , then the signal-to-noise ratio in (8) and the localization error rate in Theorem 1 would change correspondingly, by replacing the sparsity level with .

-

•

Spectral Density. The spectral density condition in 1(b) is identical to Assumption 2.1 and the assumption in Proposition 3.1 in Basu and Michailidis (2015), which pertained to a stable VAR process without change points. As pointed out in Basu and Michailidis (2015), this holds for a large class of general linear processes, including stable ARMA processes.

-

•

Signal-to-noise ratio. We assume is upper bounded for stability, but we allow as , which is more challenging in terms of detecting the change points. Since , (8) also implies that

where . For convenience, we will assume without loss of generality that .

To facilitate the understanding of the signal-to-noise ratio condition, consider the case that , (8) becomes

which matches be the minimax optimal signal-to-noise ratio (up to constants and logarithmic terms) for the univariate mean change point detection problem (see e.g. Chan and Walther, 2013; Frick et al., 2014; Wang et al., 2018b).

1(c) can be expressed using a normalized jump size

which leads to the equivalent signal-to-noise ratio condition

Similar conditions are required in other change point detection problems, including high-dimensional mean change point detection (Wang and Samworth, 2018), high-dimensional covariance change point detection (Wang et al., 2017), sparse dynamic network change point detection (Wang et al., 2018a), high-dimensional regression change point detection (Wang et al., 2019), to name but a few. We remark that in these papers, which deploy variants of the wild binary segmentation procedure (Fryzlewicz, 2014), additional knowledge is needed in order to eliminate the dependence of the term in the signal-to-noise ratio condition. We refer the reader to Wang et al. (2018a) for more discussions regarding this point.

The constant is needed to guarantee consistency and can be set to zero if . We may instead replace it by a weaker condition of the form

where arbitrarily slow as . We stick with the signal-to-noise ratio condition (8) for simplicity.

3.2 The consistency of the dynamic programming approach

In our first result, whose proof is given in Appendix A, we demonstrate consistency of the dynamic programming approach introduced in Section 2, under the assumptions listed in Section 3.1.

Theorem 1.

Assume 1 and let be constant. Them, under 1, the change point estimators from the dynamic programming approach in Algorithm 1 with tuning parameters

| (10) |

are such that

where are absolute constants depending only on , and .

Remark 2.

We do not assume that Algorithm 1 admits a unique optimal solution . In fact the consistency result in Theorem 1 holds for any minimizer of DP.

Theorem 1 implies that with probability tending to 1 as grows,

where the second inequality follows from 1(c). Thus, the localization error rate converges to zero in probability, yielding consistency.

The tuning parameter affects the performance of the Lasso estimator, as elucidated in Lemma 12. The second tuning parameter prevents overfitting while searching the optimal partition as a solution to the problem (4). In particular, is determined by the squared -loss of the Lasso estimator and is of order .

We now compare the results in Theorem 1 with the guarantees established in Safikhani and Shojaie (2020).

-

•

In terms of the localization error rate, Safikhani and Shojaie (2020) proved consistency of their methods by assuming that the minimal magnitude of the structural changes is a sufficiently large constant independent of , while our dynamic programming approach is valid even when is allowed to decrease with the sample size . In addition, Safikhani and Shojaie (2020) achieve the localization error bound of order

where satisfies . Translating to our notation, their best localization error is at least

which is larger than our rate even in their setting where is a constant.

-

•

In terms of methodology, Safikhani and Shojaie (2020) adopted a two-stage procedure: first, a penalized least squares estimator with a total variation penalty is deployed to obtain an initial estimator of the change points; then an information-type criterion is applied to identify the significant estimators and to remove any false discoveries. The change point estimators in Safikhani and Shojaie (2020) are selected from fused Lasso estimators, which are sub-optimal for change point detection purposes, especially when the size of the structure change is small (see e.g. Lin et al., 2017). In addition, the theoretically-valid selection criterion proposed in Safikhani and Shojaie (2020) has a computational cost growing exponentially in , where is the number of change points estimated by the fused Lasso and in general one has that .

3.3 The improvement of the post processing through group Lasso

We now show that the PGL refinement procedure (Algorithm 2) applied to the estimators obtained wih Algorithm 1 delivers a smaller localization rate with no direct dependence on .

Theorem 2.

Assume the same conditions in Theorem 1. Let be any set of time points satisfying

| (11) |

Let be the change point estimators generated from Algorithm 2, with and the tuning parameter

as inputs. Then

where are absolute constants depending only on , and .

As we have already shown in Theorem 1, the estimators of the change points obtained of DP detailed in Algorithm 1 satisfy, with high probability, condition (11) and therefore can serve as qualified inputs to Algorithm 2. However, we would like to emphasize that Theorem 2 holds even when the inputs are a sequence of inconsistent initial estimators of the change points.

Compared to the localization errors given in Theorem 1, the estimators refined by the PGL algorithm provide a substantial improvement by reducing the localization rate by a factor of . We provide some intuitive explanations for the success of the PGL algorithm.

-

•

The intuition of the group Lasso penalty in (7) is as follows. Suppose that for simplicity . The use of the penalty term

implies that for any th entry, the group lasso solution is such that either the ’s’ and ’s are simultaneously or they are simultaneously nonzero. This penalty effectively conforms to 1(a), which requires that all the population coefficient matrices share the common support.

-

•

Even if the coefficient matrices do not share a common support, the group Lasso penalty (7) still works. Suppose again for simplicity that . In addition, let , have support and , have support . Then the common support of , is . Since , the localization rate in Theorem 2 will only be inflated by a constant factor. In fact, the numerical experiments in Section 5 also suggest that the PGL algorithm is robust even when the coefficient matrices do not share a common support.

-

•

The condition (11) is to ensure that there is one and only one true change point in every working interval used by the local refinement algorithm. The true change points can then be estimated separately using independent searches, in such a way that the final localization rate does not depend on the number of searches.

4 Sketch of the proofs

In this section we provide a high-level summary of the technical arguments we use to prove Theorem 1 Theorem 2. The complete proofs are given in the Appendices. The main arguments consists of three main three steps. Firstly, we will express a VAR process with arbitrary but fixed lag into an appropriate VAR(1) process (this is a standard reduction technique). Then we will lay down the key ingredients needed to prove Theorem 1 and, lastly, we will pinpoint the main task to prove Theorem 2.

Transforming VAR() processes to VAR(1) processes

For any general , a VAR() process can be rewritten as a VAR(1) process in the following way. Assuming 1, let

| (12) |

where, for , if , and is the unobserved random vector from drawn from , otherwise. In addition, let and

| (13) |

Then we can rewrite (1) as

| (14) |

which is now a VAR(1) process. We remark that the stability condition (2) is now equivalent to all the eigenvalues of as defined in (13) having a modulus strictly less than (e.g. Lütkepohl, 2005, Rule (7) in Section A.6 in). This further implies that (2) implies that .

The rest of the proof will be established based on this transformation, therefore, we assume .

Sketch of the Proof of Theorem 1

Proposition 3.

Under all the conditions in Theorem 1, the following holds with probability at least .

-

(i)

For each interval containing one and only one true change point , it holds that

-

(ii)

for each interval containing exactly two true change points, say , it holds that

-

(iii)

for any two consecutive intervals , the interval contains at least one true change point; and

-

(iv)

no interval contains strictly more than two true change points.

The four cases in Proposition 3 are proved in Lemmas 5, 6, 7 and 8, respectively, and Proposition 3 is proved consequently.

Proposition 4.

Under the same conditions of Theorem 1, if , then with probability at least , it holds that .

Proof of Theorem 1.

It follows from Proposition 3 that, . This combined with Proposition 4 completes the proof. ∎

The key insight for the DP approach is that, for an appropriate value of , the estimator in (6) based on any time interval is a “uniformly good enough” estimator, in the sense that it is sufficiently close to its population counterpart regardless of the choice of and even if contains multiple true change points. For instance, if contains three change points, then should not be a member in . This is guaranteed by the following arguments. Provided that is close enough to its population counterpart, under the signal-to-noise ration condition in 1(c), breaking this interval will return a smaller objective function value in (4).

In order to show that is a “good enough” estimator, we take advantage of the assumed sparsity of its population counterpart in Lemma 17. In particular, we show that is the unique solution to the equation

The above linear system implies that in general , as the covariance matrix changes if changes at the change points. However, we can quantify the size of support of on any generic interval as long as are sparse. With this at hand, we can further show that , which is what makes a “good enough” estimator for the purposes of change point localization.

The key ingredients of the proofs of both Propositions 3 and 4 are two types of deviation inequalities as follows.

-

•

Restricted eigenvalues. In the literature on high-dimensional regression problems, there are several versions of the restricted eigenvalue conditions (see, e.g. Bühlmann and van de Geer, 2011). In our analysis, such conditions amount to controlling the probability of the event

-

•

Deviations bounds. In addition, we need to control the deviations of the quantities of the form

for any interval .

Using well-established arguments to demonstrate the performance of the Lasso estimator, as detailed in e.g. Section 6.2 of Bühlmann and van de Geer (2011), the combination of restricted eigenvalues conditions and large probability bounds on the noise lead to oracle inequalities for the estimation and prediction errors in situations where there exists no change point and the data are independent. In the existing time series analysis literature, there are several versions of the aforementioned bounds for stationary VAR models (e.g. Basu and Michailidis, 2015). We have extended this line of arguments to the present, more challenging settings, to derive analogous oracle inequalities. See Appendix C for more details.

Sketch of the Proof of Theorem 2

The proof of Theorem 2 is based on an oracle inequality of the group Lasso estimator. Once it is established that for each interval used in Algorithm 2,

| (15) |

where and that there is one and only one change point in the interval for both the sequence and , then the final claim follows immediately that the refined localization error satisfies

The group Lasso penalty is deployed to prompt (15) and the designs of the algorithm guarantee the desirability of each working interval.

5 Numerical studies

In this section, we conduct a numerical study of the performance of the DP approach of Algorithm 1, of the PGL Algorithm 2 as well as some competing methods in a variety of different settings to support our theoretical findings. We will first provide numerical comparisons in the simulated data experiments then in a real data example. All the implementations of the numerical experiments can be found at https://github.com/darenwang/vardp.

We quantify the performance of the change point estimators relatively to the set of true change point using the absolute error and the scaled Hausdorff distance

where denotes the Hausdorff distance between two compacts sets in , given by

Note that if , then . For convenience we set .

As discussed in Section 1, algorithms targeting at high-dimensional VAR change point detection are scarce. In addition, we cannot provide any numerical comparisons with Safikhani and Shojaie (2020), because their algorithm is NP-hard in the worst-case scenario. To be more precise, their combinatorial algorithm scales exponentially in , which in general may be much bigger than . In all the numerical experiments, we compare our methods with the SBS-MVTS procedure proposed in Cho and Fryzlewicz (2015) and the INSPECT method proposed in Wang and Samworth (2018). The SBS-MVTS is designed to detect covariance changes in VAR processes, and the INSPECT detects mean change points in high-dimensional sub-Gaussian vectors. We follow the default setup of the tuning parameters for the competitors, specified in the R (R Core Team, 2017) packages wbs (Baranowski and Fryzlewicz, 2019) and InspectChangepoint (Wang and Samworth, 2020), respectively.

For the tuning parameters used in our approaches, throughout this section, let , and .

5.1 Simulations

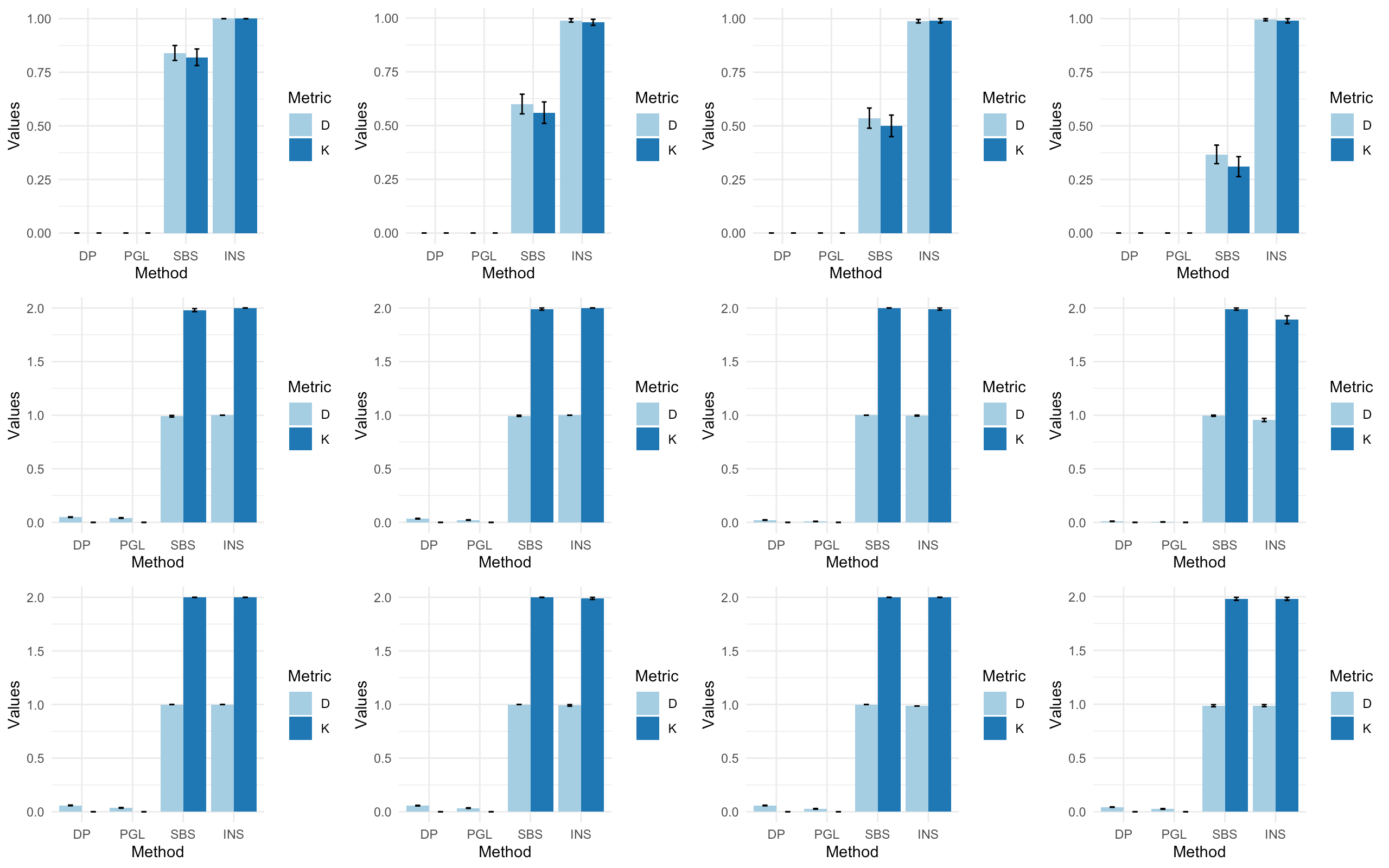

We generate data according to 1 in three settings, each consisting of multiple setups, and for each setup we carry out 100 simulations. These three settings are designed to have varying minimal spacing , minimal jump size and dimensionality , respectively and are as follows:

-

(i)

Varying . Let , , and . The only change point occurs at . The coefficient matrices are defined as

where the omitted entries that are zero.

-

(ii)

Varying . Let , , and . The change points occur at and . The coefficient matrices are

(16) where has odd coordinates equal 1 and even coordinates equal to , is an all zero matrix and .

-

(iii)

Varying . Let , , and . The change points occur at and . The coefficient matrices are

where with

and

| Setting | Metric | PDP | PGL | SBS-MVTS | INSPECT |

|---|---|---|---|---|---|

| (i) n=100 | 0.000 (0.000) | 0.000 (0.000) | 0.840 (0.348) | 1.000 (0.000) | |

| (i) n=120 | 0.000 (0.000) | 0.000 (0.000) | 0.600 (0.457) | 0.989 (0.081) | |

| (i) n=140 | 0.000 (0.000) | 0.000 (0.000) | 0.536 (0.470) | 0.988 (0.082) | |

| (i) n=160 | 0.000 (0.000) | 0.000 (0.000) | 0.367 (0.432) | 0.995 (0.051) | |

| (i) n=100 | 0.000 (0.000) | 0.000 (0.000) | 0.820 (0.386) | 1.000 (0.000) | |

| (i) n=120 | 0.000 (0.000) | 0.000 (0.000) | 0.560 (0.499) | 0.980 (0.141) | |

| (i) n=140 | 0.000 (0.000) | 0.000 (0.000) | 0.500 (0.502) | 0.990 (0.100) | |

| (i) n=160 | 0.000 (0.000) | 0.000 (0.000) | 0.310 (0.465) | 0.990 (0.100) | |

| (ii) | 0.049 (0.026) | 0.041 (0.030) | 0.990 (0.076) | 1.000 (0.000) | |

| (ii) | 0.035(0.027) | 0.022 (0.027) | 0.994 (0.059) | 1.000 (0.000) | |

| (ii) | 0.022 (0.024) | 0.009 (0.017) | 1.000 (0.000) | 0.996 (0.043) | |

| (ii) | 0.010 (0.018) | 0.004 (0.012) | 0.995 (0.054) | 0.955 (0.147) | |

| (ii) | 0.004 (0.013) | 0.002 (0.009) | 1.000 (0.000) | 0.831 (0.260) | |

| (ii) | 0.000 (0.000) | 0.000 (0.000) | 1.980 (0.140) | 2.000 (0.000) | |

| (ii) | 0.000 (0.000) | 0.000 (0.000) | 1.990 (0.100) | 2.000 (0.000) | |

| (ii) | 0.000 (0.000) | 0.000 (0.000) | 2.000 (0.000) | 1.999 (0.100) | |

| (ii) | 0.000 (0.000) | 0.000 (0.000) | 1.990 (0.100) | 1.890 (0.373) | |

| (ii) | 0.000 (0.000) | 0.000 (0.000) | 2.000 (0.000) | 1.650 (0.575) | |

| (iii) | 0.049 (0.034) | 0.026 (0.031) | 1.000 (0.000) | 1.000(0.000) | |

| (iii) | 0.059 (0.031) | 0.036 (0.032) | 1.000 (0.000) | 1.000 (0.000) | |

| (iii) | 0.057 (0.028) | 0.034 (0.029) | 1.000 (0.000) | 0.992(0.073) | |

| (iii) | 0.058 (0.028) | 0.027 (0.030) | 1.000 (0.000) | 1.000 (0.000) | |

| (iii) | 0.043 (0.024) | 0.026 (0.031) | 0.986 (0.097) | 0.987 (0.092) | |

| (iii) | 0.000 (0.000) | 0.000 (0.000) | 2.000 (0.000) | 2.000 (0.000) | |

| (iii) | 0.000 (0.000) | 0.000 (0.000) | 2.000 (0.000) | 2.000 (0.000) | |

| (iii) | 0.000 (0.000) | 0.000 (0.000) | 2.000 (0.000) | 1.990 (0.100) | |

| (iii) | 0.000 (0.000) | 0.000 (0.000) | 2.000 (0.000) | 2.000 (0.000) | |

| (iii) | 0.000 (0.000) | 0.000 (0.000) | 1.980 (0.141) | 1.980 (0.141) |

The numerical comparisons of all algorithms in terms of the absolute error and the scaled Hausdorff distance are reported in Table 1 and are also displayed in Figure 3. We can see that even though the dimension is moderate, neither SBS-MVTS nor INSPECT can consistently estimate the change points. In fact, both algorithms tend to infer that there is no change points in the time series, confirming the intuition discussed in Example 1.

In all of our approaches, we need to estimate the coefficient matrices, therefore the effective dimensions are , but not . The competitors SBS-MVTS and INSPECT, however, estimate the change points without estimating the coefficient matrices. This reduces the effective dimension to , which might be more efficient in terms of computation, but neither SBS-MVTS nor INSPECT can consistently estimate the change points in these settings.

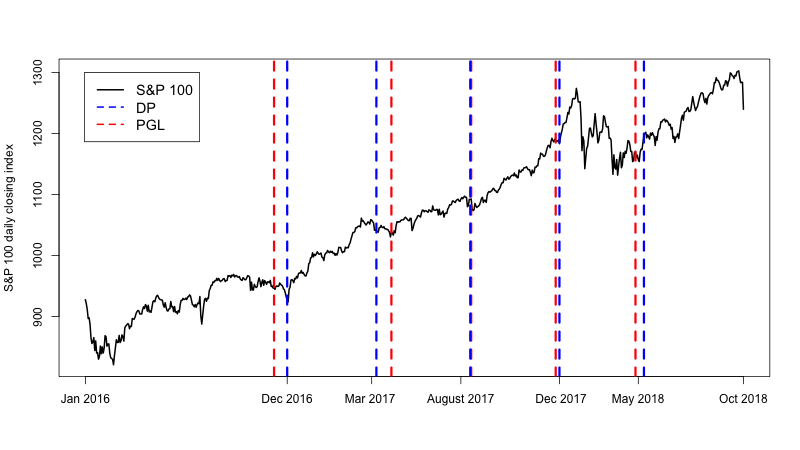

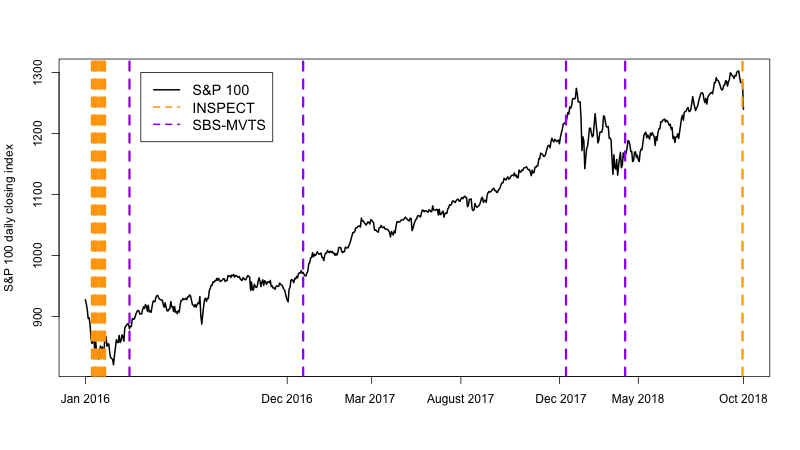

5.2 A real data example: S&P 100

We study the daily closing prices of the constituents of S&P 100 index from Jan 2016 to Oct 2018. The companies in the S&P 100 are selected for sector balance and represent about 51% of the market capitalization of the U.S. equity market. They tend to be the largest and most established firms in the U.S. stock market. Since the stock prices always exhibit upward trends, we therefore follow the standard procedure and de-trend the data by taking the first order difference. After removing missing values, our final dataset is a multivariate time series with and , where each dimension corresponds the daily stock price change of one firm during the aforementioned period.

In order to apply our algorithms, we rescale the data so that the average variance over all dimensions equals 1. We apply the DP and PGL algorithms to the data set and depict the detected change points in Figure 4a. Since the outputs of these two algorithms do not differ by much, we focus on the ones output by DP. The five estimated change points by DP are 3rd November 2016, 23rd March 2017, 15th August 2017, 29th December 2017 and 10th May 2018. There are some times, e.g. around Feb. 2018, where we see big changes in the S&P 100 index but none of the methods describes it as a change point. This is because our change point analysis is targeting changes in the interactions among companies, as captured by a VAR process, and not directly the mean price changes. Thus occasional large fluctuations in the data do not necessarily reflect the type of structural changes we seek to identify.

To argue that our methodology has lead to meaningful findings, we suggest a justification of each estimated change points. Four days after the first change point estimator, Trump won the presidential election. Eight days after the second change point estimator, President Trump signed two executive orders increasing tariffs. This is a key date in the U.S.-China trade war. The third change point estimator is associated with President Trump signing another executive order in March 2017, authorizing U.S. Trade Representatives to begin investigations into Chinese trade practices, with particular focus on intellectual property and advanced technology. The fourth change point estimator lines up with the best opening of the U.S. stock market in 31 years (e.g. Franck, 2018). The last change point estimator is associated with the White House announcement that it would impose a 25% tariff on $50 billion of Chinese goods with industrially significant technology at the end of May 2018. For comparison, we also show the change points found by SBS-MVTS and INSPECT in Figure 4b.

6 Conclusions

This paper considers change point localization in high-dimensional vector autoregressive process models. We have developed two procedures for change point localization that can be characterized as solutions to a common optimization framework and that can be efficiently implemented using a combination of dynamic programming and Lasso-type estimators. We have demonstrated that our methods yield the sharpest localization rates of autoregressive processes and match the best known rates for change point localization. We further conjecture that the localization rate of the PGL algorithm is minimax optimal. Both minimax rates and extensions of this framework beyond sparse models to other models of low-dimensional structure remain important open questions for future research.

References

- Aue et al. (2009) Aue, A., Hörmann, S., Horváth, L. and Reimherr, M. (2009). Break detection in the covariance structure of multivariate time series models. The Annals of Statistics, 37 4046–4087.

- Bai and Perron (1998) Bai, J. and Perron, P. (1998). Estimating and testing linear models with multiple structural changes. Econometrica 47–78.

- Baranowski and Fryzlewicz (2019) Baranowski, R. and Fryzlewicz, P. (2019). wbs: Wild binary segmentation for multiple change-point detection. R package version 1.4, URL https://cran.r-project.org/web/packages/wbs/index.html.

- Basu and Michailidis (2015) Basu, S. and Michailidis, G. (2015). Regularized estimation in sparse high-dimensional time series models. The Annals of Statistics, 43 1535–1567.

- Bickel and Gel (2011) Bickel, P. J. and Gel, Y. R. (2011). Banded regularization of autocovariance matrices in application to parameter estimation and forecasting of time series. Journal of the Royal Statistical Society: Series B (Statistical Methodology), 73 711–728.

- Bolstad et al. (2011) Bolstad, A., Van Veen, B. D. and Nowak, R. (2011). Causal network inference via group sparse regularization. IEEE transactions on signal processing, 59 2628–2641.

- Bühlmann and van de Geer (2011) Bühlmann, P. and van de Geer, S. (2011). Statistics for high-dimensional data: methods, theory and applications. Springer Science & Business Media.

- Chan and Walther (2013) Chan, H. P. and Walther, G. (2013). Detection with the scan and the average likelihood ratio. Statistica Sinica, 1 409–428.

- Chang et al. (2015) Chang, J., Guo, B. and Yao, Q. (2015). High dimensional stochastic regression with latent factors, endogeneity and nonlinearity. Journal of econometrics, 189 297–312.

- Chang et al. (2018) Chang, J., Guo, B. and Yao, Q. (2018). Principal component analysis for second-order stationary vector time series. The Annals of Statistics, 46 2094–2124.

- Chang et al. (2017) Chang, J., Yao, Q. and Zhou, W. (2017). Testing for high-dimensional white noise using maximum cross-correlations. Biometrika, 104 111–127.

- Chen and Gupta (1997) Chen, J. and Gupta, A. K. (1997). Testing and locating variance changepoints with application to stock prices. Journal of the American Statistical association, 92 739–747.

- Chen et al. (2013) Chen, X., Xu, M. and Wu, W. B. (2013). Covariance and precision matrix estimation for high-dimensional time series. The Annals of Statistics, 41 2994–3021.

- Cho (2016) Cho, H. (2016). Change-point detection in panel data via double cusum statistic. Electronic Journal of Statistics, 10 2000–2038.

- Cho and Fryzlewicz (2015) Cho, H. and Fryzlewicz, P. (2015). Multiple-change-point detection for high dimensional time series via sparsified binary segmentation. Journal of the Royal Statistical Society: Series B (Statistical Methodology), 77 475–507.

- De Mol et al. (2008) De Mol, C., Giannone, D. and Reichlin, L. (2008). Forecasting using a large number of predictors: Is bayesian shrinkage a valid alternative to principal components? Journal of Econometrics, 146 318–328.

- Dette and Gösmann (2018) Dette, H. and Gösmann, J. (2018). Relevant change points in high dimensional time series. Electronic Journal of Statistics, 12 2578–2636.

- Fiecas et al. (2018) Fiecas, M., Leng, C., Liu, W. and Yu, Y. (2018). Spectral analysis of high-dimensional time series. arXiv preprint arXiv:1810.11223.

- Forni et al. (2005) Forni, M., Hallin, M., Lippi, M. and Reichlin, L. (2005). The generalized dynamic factor model: one-sided estimation and forecasting. Journal of the American Statistical Association, 100 830–840.

- Franck (2018) Franck, T. (2018). The stock market is off to its best start in 31 years and that bodes well for the rest of 2018. The Consumer News and Business Channel. URL https://www.cnbc.com/2018/01/24/stock-market-off-to-best-start-in-31-years-bodes-well-for-2018.html.

- Frick et al. (2014) Frick, K., Munk, A. and Sieling, H. (2014). Multiscale change point inference. Journal of the Royal Statistical Society: Series B (Statistical Methodology), 76 495–580.

- Friedrich et al. (2008) Friedrich, F., Kempe, A., Liebscher, V. and Winkler, G. (2008). Complexity penalized m-estimation: Fast computation. Journal of Computational and Graphical Statistics, 17 201–204.

- Fryzlewicz (2014) Fryzlewicz, P. (2014). Wild binary segmentation for multiple change-point detection. The Annals of Statistics, 42 2243–2281.

- Guo et al. (2016) Guo, S., Wang, Y. and Yao, Q. (2016). High-dimensional and banded vector autoregressions. Biometrika asw046.

- Han et al. (2015) Han, F., Lu, H. and Liu, H. (2015). A direct estimation of high dimensional stationary vector autoregressions. The Journal of Machine Learning Research, 16 3115–3150.

- Haufe et al. (2010) Haufe, S., Müller, K.-R., Nolte, G. and Krämer, N. (2010). Sparse causal discovery in multivariate time series. In Causality: Objectives and Assessment. 97–106.

- Hsu et al. (2008) Hsu, N.-J., Hung, H.-L. and Chang, Y.-M. (2008). Subset selection for vector autoregressive processes using lasso. Computational Statistics & Data Analysis, 52 3645–3657.

- Killick et al. (2012) Killick, R., Fearnhead, P. and Eckley, I. A. (2012). Optimal detection of changepoints with a linear computational cost. Journal of the American Statistical Association, 107 1590–1598.

- Lam and Yao (2012) Lam, C. and Yao, Q. (2012). Factor modeling for high-dimensional time series: inference for the number of factors. The Annals of Statistics, 40 694–726.

- Leonardi and Bühlmann (2016) Leonardi, F. and Bühlmann, P. (2016). Computationally efficient change point detection for high-dimensional regression. arXiv preprint arXiv:1601.03704.

- Lin et al. (2017) Lin, K., Sharpnack, J. L., Rinaldo, A. and Tibshirani, R. J. (2017). A sharp error analysis for the fused lasso, with application to approximate changepoint screening. In Advances in Neural Information Processing Systems. 6884–6893.

- Loh and Wainwright (2011) Loh, P.-L. and Wainwright, M. J. (2011). High-dimensional regression with noisy and missing data: Provable guarantees with non-convexity. In Advances in Neural Information Processing Systems. 2726–2734.

- Lütkepohl (2005) Lütkepohl, H. (2005). New introduction to multiple time series analysis. Springer Science & Business Media.

- Maidstone et al. (2017) Maidstone, R., Hocking, T., Rigaill, G. and Fearnhead, P. (2017). On optimal multiple changepoint algorithms for large data. Statistics and Computing, 27 519–533.

- Michailidis and d’Alché Buc (2013) Michailidis, G. and d’Alché Buc, F. (2013). Autoregressive models for gene regulatory network inference: Sparsity, stability and causality issues. Mathematical biosciences, 246 326–334.

- R Core Team (2017) R Core Team (2017). R: A language and environment for statistical computing. URL https://www.R-project.org/.

- Rigaill (2010) Rigaill, G. (2010). Pruned dynamic programming for optimal multiple change-point detection. arXiv preprint arXiv:1004.0887.

- Safikhani and Shojaie (2020) Safikhani, A. and Shojaie, A. (2020). Joint structural break detection and parameter estimation in high-dimensional non-stationary var models. Journal of the American Statistical Association 1–26.

- Schneider-Luftman and Walden (2016) Schneider-Luftman, D. and Walden, A. T. (2016). Partial coherence estimation via spectral matrix shrinkage under quadratic loss. IEEE Transactions on Signal Processing, 64 5767–5777.

- Shojaie and Michailidis (2010) Shojaie, A. and Michailidis, G. (2010). Discovering graphical granger causality using the truncating lasso penalty. Bioinformatics, 26 i517–i523.

- Smith (2012) Smith, S. M. (2012). The future of FMRI connectivity. Neuroimage, 62 1257–1266.

- Susto et al. (2014) Susto, G. A., Schirru, A., Pampuri, S., McLoone, S. and Beghi, A. (2014). Machine learning for predictive maintenance: A multiple classifier approach. IEEE Transactions on Industrial Informatics, 11 812–820.

- Swanson (2001) Swanson, D. C. (2001). A general prognostic tracking algorithm for predictive maintenance. In 2001 IEEE Aerospace Conference Proceedings (Cat. No. 01TH8542), vol. 6. IEEE, 2971–2977.

- Tank et al. (2015) Tank, A., Foti, N. and Fox, E. (2015). Bayesian structure learning for stationary time series. arXiv preprint arXiv:1505.03131.

- Tu et al. (2017) Tu, Y., Yao, Q. and Zhang, R. (2017). Error-correction factor models for high-dimensional cointegrated time series.

- Wang et al. (2019) Wang, D., Lin, K. and Willett, R. (2019). Statistically and computationally efficient change point localization in regression settings. arXiv preprint arXiv:1906.11364.

- Wang et al. (2017) Wang, D., Yu, Y. and Rinaldo, A. (2017). Optimal covariance change point localization in high dimension. arXiv preprint arXiv:1712.09912.

- Wang et al. (2018a) Wang, D., Yu, Y. and Rinaldo, A. (2018a). Optimal change point detection and localization in sparse dynamic networks. arXiv preprint arXiv:1809.09602.

- Wang et al. (2018b) Wang, D., Yu, Y. and Rinaldo, A. (2018b). Univariate mean change point detection: Penalization, cusum and optimality. arXiv preprint arXiv:1810.09498.

- Wang and Samworth (2020) Wang, T. and Samworth, R. (2020). InspectChangepoint: High-Dimensional Changepoint Estimation via Sparse Projection. R package version 1.1, URL https://cran.r-project.org/web/packages/InspectChangepoint/index.html.

- Wang and Samworth (2018) Wang, T. and Samworth, R. J. (2018). High dimensional change point estimation via sparse projection. Journal of the Royal Statistical Society: Series B (Statistical Methodology), 80 57–83.

- Wu and Wu (2016) Wu, W.-B. and Wu, Y. N. (2016). Performance bounds for parameter estimates of high-dimensional linear models with correlated errors. Electronic Journal of Statistics, 10 352–379.

- Xiao and Wu (2012) Xiao, H. and Wu, W. B. (2012). Covariance matrix estimation for stationary time series. The Annals of Statistics, 40 466–493.

- Yam et al. (2001) Yam, R., Tse, P., Li, L. and Tu, P. (2001). Intelligent predictive decision support system for condition-based maintenance. The International Journal of Advanced Manufacturing Technology, 17 383–391.

- Zhang et al. (2019) Zhang, R., Robinson, P. and Yao, Q. (2019). Identifying cointegration by eigenanalysis. Journal of the American Statistical Association, 114 916–927.

Appendix

In the proofs, we do not track every single absolute constant. Except those which have specific meanings, used in the main text, all the others share a few pieces of notation, i.e. the constant are used in different places having different values.

Appendix A Proof of Theorem 1

As we mentioned in Section 4, for any positive integer , a VAR() process can be written as a VAR(1) process. Based on the transformation introduced in Section 4, in this section, we will first lay down the preparations, then prove Propositions 3 and 4 based on . All the technical lemmas are deferred to Appendix C.

We let be the solution to

| (17) |

Note that when contains no change points , . Let

Therefore by 1(a), . With a permutation if necessary, without loss of generality, we have that , which implies that each has the block structure

| (18) |

where . Denote

| (19) |

satisfying that and that if .

A.1 Proof of Proposition 3

Proof of Proposition 3.

The four cases in Proposition 3 are straightforward consequences of applying union bound arguments to Lemmas 5, 6, 7 and 8, respectively.

For illustration, we show how to apply the union bound argument to Lemma 5 and prove Case (i). Consider the collection of integer intervals

With the notation in Lemma 5, let be

By Lemma 5 and the fact that , it holds that

The proof is completed by noticing that (20) holds since is a minimizer of (4) and that all satisfies that , which follows from Corollary 20 and (10).

∎

Lemma 5 (Case (i)).

With all the conditions and notation in Proposition 3, assume that has one and only one true change point . Denote , and . If, in addition, it holds that

| (20) |

then with probability at least , it holds that with ,

| (21) |

Proof.

If , then (21) holds automatically. If and , then (21) also holds. In the rest of the proof, we assume that . To show (21), we prove by contradiction, assuming that

Due to (10) and the above, it holds that

| (22) |

Then (20) leads to

Denoting , , (23) leads to that

| (24) |

By Lemma 13(a), it holds that with at least probability

| (25) |

where the second inequality follows from Hölder’s inequality and the last inequality follows from Lemma 18 that with probability at least that

Therefore with probability at least

where the first inequality follows from Lemma 13(b), the third inequality follows from (22) and Lemma 18, and the last inequality follows from (22).

∎

Lemma 6 (Case (ii)).

With all the conditions and notation in Proposition 3, assume that containing exactly two change points and . Denote , , , and . If in addition it holds that

| (26) |

then

| (27) |

with probability at least .

Proof.

Since , due to 1, it holds that . In the rest of the proof, without loss of generality, we assume that . To show (27), we prove by contradiction, assuming that

| (28) |

Due to (10), we have that . Denote , . We then consider the following two cases.

Lemma 7 (Case (iii)).

With all the conditions and notation in Proposition 3, assume that there exists no true change point in . With probability at least , it holds that

Proof.

For any fixed , let and . By Corollary 20, it holds that with probability at least ,

where is the population counterpart of , replacing the coefficient matrix estimator with its population counterpart. Since , we have that with probability at least ,

Then, using a union bound argument, with probability at least , it holds that

∎

Lemma 8 (Case (iv)).

With all the conditions and notation in Proposition 3, assume that contains true change points , where . Then with probability at least , with an absolute constant ,

where , for any and .

Proof.

Since , we have that and . We prove by contradiction, assuming that

| (29) |

Note that for all . Let , . From Corollary 20, we have that with probability at least ,

| (30) |

where denotes the population counterpart of , by replacing the coefficient matrix estimator with its population counterpart. In the rest of the proof, without loss of generality, we assume that .

There are three cases: (1) , (2) and (3) . All these three cases can be shown using very similar arguments, and cases (2), (3) are both simpler than case (1), so in the sequel, we will only show case (1).

Suppose that . Then (30) gives

| (31) |

which implies that

| (32) |

By Lemma 13(a), and for all , it holds that with probability at least ,

| (33) |

where Lemma 18 and Hölder inequality are used in the third inequality. In addition, by Lemma 13(b), it holds that with probability at least ,

| (34) |

where the third inequality follows from Lemma 18 and the last follows from .

A.2 Proof of Proposition 4

Lemma 9.

Under the assumptions and notation in Proposition 4, suppose that there exists no true change point in the interval . For any interval , it holds that with probability at least ,

where is an absolute constant and is the population counterpart of by replacing the coefficient matrix estimator with its population counterpart.

Proof.

Let

Case 1. If , then and the claim holds automatically.

Case 2. If

then and by Lemma 13(b), we have with probability at least ,

| (35) |

where the last inequality follows from Lemma 18 and . We then have on the event in Lemma 13(a),

where the first inequality follows from (35), the second inequality follows from Lemma 13(a) and Lemma 18, the third follows from Hölder inequality and .

∎

Proof of Proposition 4.

Let be the population counterpart of by replacing the coefficient matrix estimator with its population counterpart. This proof is based on the events

and

In addition denote

where

Note that by Lemma 9 and Corollary 20 and union bounds

Let be such that for any . Denote

Given any collection , where , and , , let

| (36) |

For any collection of time points, when defining (36), the time points are sorted in an increasing order.

In addition, since

therefore is the minimal value of the objective function in (4).

Step 1. Let denote the change points induced by . If one can justify that

| (37) | ||||

| (38) | ||||

| (39) |

and that

| (40) |

then it must hold that , as otherwise if , then

Therefore due to the assumption that , it holds that

| (41) |

Note that (41) contradicts with the choice of .

Step 2.

Observe that (37) is implied by

| (42) |

which is immediate consequence of . Since are the change points induced by , (38) holds because is a minimizer.

Step 3. For every , let

Then (39) is an immediate consequence of the following inequality

| (43) |

Case 1. If , then

where is used in the last inequality.

case 2. If , then it suffices to show that

| (44) |

On , it holds that

| (45) |

In addition for each ,

where the inequality follows from . Therefore the above inequality implies that

| (46) |

Appendix B Proof of Theorem 2

Lemma 10.

Let be any linear subspace in and be a -net of , where is the unit ball in . For any , it holds that

where denotes the inner product in .

Proof.

Due to the definition of , it holds that for any , there exists a , such that . Therefore,

where the inequality follows from . Then we have

It follows from the same argument that

where satisfies . Combining the previous two equation displays yields

and the final claims holds. ∎

Lemma 11.

For data generated from 1, for any interval , it holds that for any , and ,

Proof.

Proof of Theorem 2.

For each and , let

Without loss of generality, we assume that . We proceed the proof discussing two cases.

Case (i). If

then the result holds.

Case (ii). Suppose

| (47) |

Since is bounded, .

Step 1. Let and therefore

it holds that

We first to prove that with probability at least ,

Due to (7), it holds that

| (48) |

which implies that

| (49) |

Note that

| (50) |

We then examine the cross term, with probability at least , which satisfies the following

| (51) |

where the first inequality follows from the inequality that and the second inequality follows from Lemma 11.

Now we are to explore the restricted eigenvalue inequality. Let

Due to (11) and Lemma 13 we have that with probability at least ,

| (53) |

Therefore, with probability at least ,

| (54) |

where the last inequality follows from Lemma 13(c), (47) and (53). In addition, note that for any , the square root of the second term of (54) can be bounded as

where the last inequality follows from generalized Hölder inequality in Lemma 14. Therefore, if , the previous display and (54) give

| (55) |

Then (52) and (55) together imply that

and therefore

Step 4. Denote and that . We have that

Therefore we have that

Therefore we have

Similarly, In addition we have

Therefore, it holds that

which implies that

This directly implies that

as desired. ∎

Appendix C Technical lemmas

In this section, we provide technical lemmas.

Lemma 12.

For 1, under 1, the following holds.

-

(a)

There exists an absolute constant , such that for any and any , it holds that

and

in particular, for any , it holds that

(56) -

(b)

Let be a -dimensional, centered, stationary process. Assume that for any , . The joint process satisfies 1(b). Let be the spectral density function of , and be the cross spectral density function of and , . There exists an absolute constant , such that for any and any , it holds that

Although there exists one difference between Lemma 12 and Proposition 2.4 in Basu and Michailidis (2015) that we have different spectral density distributions, while in Basu and Michailidis (2015), , the proof can be conducted in a similar way, only noticing that the largest eigenvalue should be taken as the largest over all different spectral density functions due to independence.

Proof.

The proof is an extension of Proposition 2.4 in Basu and Michailidis (2015) to the change point setting. As for (a), let and , where has the following block structure due to the independence,

where , . By the proof of proposition 2.4 in Basu and Michailidis (2015), . Note that

where . The rest follows the proof of Proposition 2.4 in Basu and Michailidis (2015).

As for (b), denote and . Observe that for , , the process has the spectral density function as follows, for ,

Therefore , and the rest follows from (a). ∎

Lemma 13.

For satisfying 1 and 1, we have the following.

-

(a)

For any interval and any , it holds that

where is a constant depending on , , , .

-

(b)

Let and be some constant depending on and . For any interval satisfying

(57) with probability at least , it holds that for any ,

(58) where are absolute positive constants depending on all the other constants.

-

(c)

Let . For any interval satisfying

(59) with probability at least , it holds that for any ,

(60) where are absolute constants.

Proof.

The claim (a) is a direct application of Lemma 12(b), by setting .

As for (b), let and . It is due to (56) that with probability at least , it holds that

| (61) |

The last inequality in (61) follows the proof of Lemmas 12 and 13 in the Supplementary Materials in Loh and Wainwright (2011), and the proof of Proposition 4.2 in Basu and Michailidis (2015), by taking

where the inequality holds due to (57), and by taking

Lemma 14 (Generalized Hölder inequality).

For any function , it holds that

Lemma 15.

Proof.

Lemma 16.

Under all the conditions in in Lemma 15, it holds with probability at least that

where is an absolute constant.

Proof.

Proof.

Due to (17), (18) and (19), for any realization of such VAR(1) process with transition matrix , the covariance of is of the form

where . Since is invertible, the matrix is unique and is of the same form as in (18). Since for all , by assumption it holds that

| (66) |

and

| (67) |

Combining (17), (66) and (67) leads to

∎

The difference between the lemma below and Lemma 15 is that Lemma 15 is concerned about the interval containing no true change points, but Lemma 18 deals with more general intervals.

Lemma 18.

Proof.

Due to 1, we have that and are independent, and that

Lemma 17 implies that , and that the support of is such that .

Let . From standard Lasso calculations, we have

| (68) |

Note that

As for , by Lemma 13(a), with probability at least ,

Consider the process , for any and , where with . Observe that

and

where and are used in the last inequality. It follows from Lemma 12(a) that with probability at least ,

therefore

Lemma 19.

Proof.

It follows from Lemma 18 that with probability at least ,

In addition,

where the second inequality is due to Lemma 13(a), (69) and (70); and the last inequality follows from Lemma 18.

∎

Corollary 20.

C.1 Additional lemmas for general

When extending from to general , the only nontrivial part is the counterpart of Lemma 18, which requires us to identify the population quantity of

| (71) |

when contains multiple change points, which is done in this subsection.

Lemma 21.

Suppose 1 holds with . Let be the covariance matrix of defined as

| (72) |

for each . With a permutation if needed, suppose that each , and , has the block structure

| (73) |

where . Let the matrix satisfy

| (74) |

Then the solution exists and is unique. It holds that

In addition, if we write

as the first rows of the matrix , where , then , , and consequently .

Proof.

It follows from (73), the covariance of is of the form

where for ,

for some ; for with ,

for some . Since

the matrix exits and is unique. The bounds on the operator norm of follows from the same argument used in (65). By matching coordinates, (74) is equivalent to

Let

where . It suffices to show that in the above block structure, only , which implies that . Since

by the uniqueness of , for any . Since the matrix

is the covariance matrix of , we have that

and that the matrix is invertible. We therefore complete the proof. ∎

Lemma 22.

Proof.

Step 1. For , let . Standard calculations lead to

| (78) |

Denote and . Let be defined as in (12). Note that only at . Observe that (78) gives

Step 2. As for term , by Lemma 13(a) and the assumption that , it holds that

Step 3. As for term , note that . Denote as the -th row of and thus . It holds that

Observe that and are independent if . Therefore with probability at least ,

where the last inequality follows from standard tail bounds for the sum of independent sub-exponential random variables together with the observations that for all . Therefore

where and are used in the last inequality.

Step 4. As for term , we have that

Using the same arguments as in Step 3, we have that

and . Due to the construction of , it holds that

Denote . Observe that

Consider the VAR process . Since

and that is a VAR(1) change point process, Lemma 13(a) gives

Therefore if , then with probability less than ,

So it holds that

Step 5. The previous calculations give

where . With the restricted eigenvalue condition in Lemma 13, standard Lasso calculations yields the desired results. ∎