Time between the maximum and the minimum of a stochastic process

Abstract

We present an exact solution for the probability density function of the time-difference between the minimum and the maximum of a one-dimensional Brownian motion of duration . We then generalise our results to a Brownian bridge, i.e. a periodic Brownian motion of period . We demonstrate that these results can be directly applied to study the position-difference between the minimal and the maximal height of a fluctuating -dimensional Kardar-Parisi-Zhang interface on a substrate of size , in its stationary state. We show that the Brownian motion result is universal and, asymptotically, holds for any discrete-time random walk with a finite jump variance. We also compute this distribution numerically for Lévy flights and find that it differs from the Brownian motion result.

The properties of extremes of a stochastic process/time series of a given duration are of fundamental importance in describing a plethora of natural phenomena Gumbel ; katz02 ; katz05 ; Krug07 ; NK11 . For example, this time series may represent the amplitude of earthquakes in a specific seismic region, the amount of yearly rainfall in a given area, the temperature records in a given weather station, etc. The study of extremes in such natural time series have gained particular relevance in the recent context of global warming in climate science RP06 ; RC2011 ; Christ13 ; WHK14 ; MBK19 . Extremal properties also play an important role for stochastic processes that are outside the realm of natural phenomena. For example, in finance, a natural time series is the price of a stock for a given period BP2000 ; yor01 ; embrechts13 ; Challet17 . Knowing the maximum or the minimum value of a stock during a fixed period is obviously important, but an equally important question is when does the maximum (minimum) value of the stock occurs within this period . Let and denote these times (see e.g. Fig. 1). For a generic stochastic process, computing the statistics of and is a fundamental and challenging problem. The simplest and the most ubiquitous stochastic process is the one-dimensional Brownian motion (BM) of a given duration , for which the probability distribution function (PDF) of can be computed exactly levy40 ; feller50 ; SA53 ; morters10

| (1) |

The cumulative distribution is known as the celebrated arcsine law of Lévy levy40 . By the symmetry of the BM, the distribution of is also described by the same arcsine law (1). In the past decades, the statistics of has been studied for a variety of stochastic processes, going beyond BM. Examples include BM with drift majumdar08 ; drift , constrained BM randon-furling07 ; randon-furling08 ; schehr10 (such as the Brownian bridge and the Brownian excursion, see also schehr10 ; PLDM03 for real space renormalization group method), Bessel processes schehr10 , Lévy flights SA53 ; majumdar10 , random acceleration process rosso10 , fractional BM delorme16 ; tridib18 , run-and-tumble particles anupam_rtp , etc. The statistics of has also been studied in multi-particle systems, such as independent BM’s comtet10 as well as for vicious walkers rambeau11 . Moreover, the arcsine law and its generalisations have been applied in a variety of situations such as in disordered systems MRZ10 , stochastic thermodynamics barato18 , finance dale80 ; baz04 and sports clauset15 .

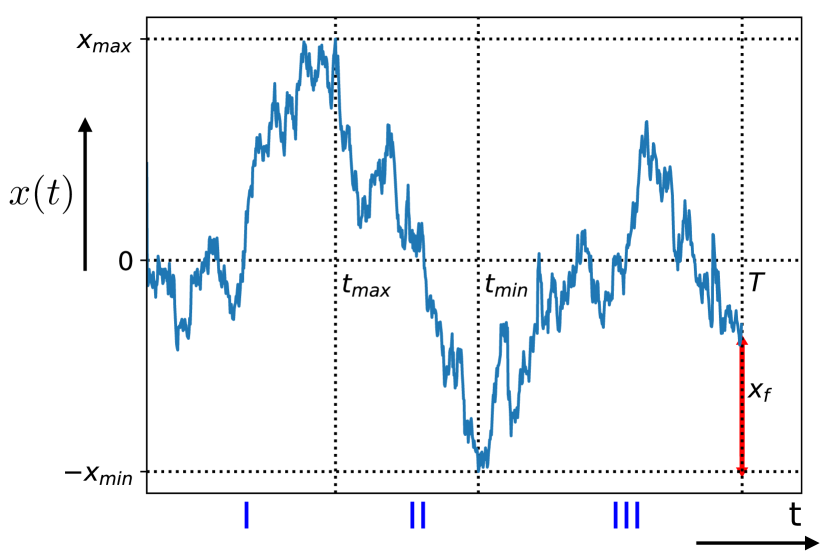

While the marginal distributions of and are given by the same arcsine law in Eq. (1) for a BM due its symmetry, one expects that and are strongly correlated. For example, if the maximum occurs at a certain time, it is unlikely that the minimum occurs immediately after or before. These anti-correlations are encoded in the joint distribution which does not factorise into two separate arcsine laws. These anti-correlations also play an important role for determining the statistics of another naturally important observable, namely the time-difference between and : . In the context of finance where the price of a stock is modelled by the exponential of a BM, represents the time-difference between the occurrences of the minimum and the maximum of the stock price. For instance, if as in Fig. 1, an agent would typically sell her/his stock when the price is the highest and then wait an interval before re-buying the stock, because the stock is the cheapest at time . Hence a natural question is: how long should one wait between the buying and the selling of the stock? In other words, one would like to know the PDF of the time difference . To calculate this PDF, we need to know the joint distribution . Computing this joint distribution and the PDF for a stochastic process is thus a fundamentally important problem.

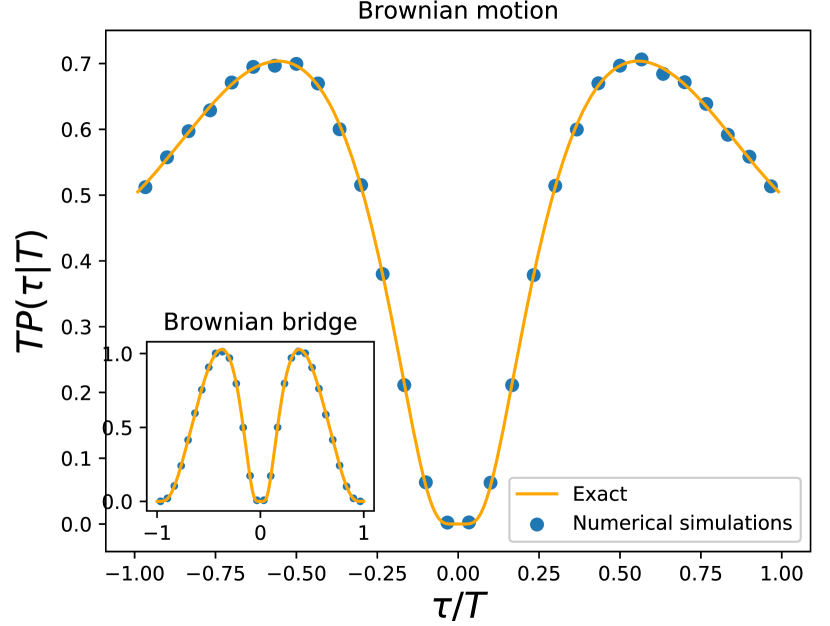

In this Letter, by using a path-integral method, we compute exactly the joint distribution for a BM of a given duration . This joint distribution does not depend on the initial position . Hence, without loss of generality, we set . We also generalise our results to the case of a Brownian bridge (BB), which is a periodic BM of period . Using these results, we first compute exactly the covariance function that quantifies the anti-correlation between and . We find for a BM ( being the Riemann zeta function) while for a BB. From this joint distribution, we also compute exactly the PDF for the BM as well as for the BB. We show that for a BM of duration , starting at some fixed position, has a scaling form for all and : where the scaling function with is given by

| (2) |

Clearly is symmetric around , but is non-monotonic as a function of (see Fig. 2 where we also compare it with numerical simulations, finding excellent agreement). This function has asymptotic behaviors

| (3) |

For a BB, we get

| (4) |

which is again symmetric around (see the inset of Fig. 2) and has the asymptotic behaviors

| (5) |

Next, we demonstrate that these scaling functions are universal in the sense of Central Limit Theorem. Indeed, consider a time series of steps generated by the positions of a random walker evolving via the Markov rule

| (6) |

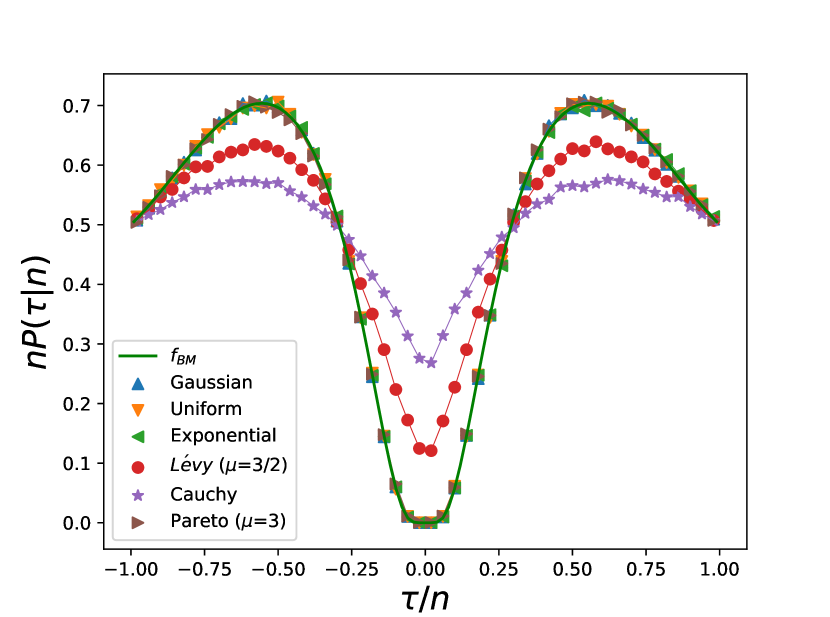

starting from , where ’s are independent and identically distributed random jump variables, each drawn from a symmetric and continuous PDF . For all such jump distributions with a finite variance , we expect that, for large , the corresponding PDF of the time difference would converge to the same scaling function as the BM. Similar result holds for the BB as well. We confirm this universality by an exact computation for and numerically for other distributions with finite (see Fig. 3). In contrast, for Lévy flights is divergent since has a heavy tail for large , with index . In this case, the PDF of is characterised by a different scaling function parameterised by that we compute numerically. Finally, we show how our results can be applied to study similar observables for heights in the stationary state of a Kardar-Parisi-Zhang (KPZ) or Edwards-Wilkinson (EW) interfaces in one-dimension on a finite substrate of size .

Brownian motion. We start with a BM over the time interval , starting at as in Fig. 1. Let and denote the magnitude of the maximum and the minimum in . Our strategy is to first compute the joint distribution of these four random variables and then integrate out and to obtain the joint PDF . We note that while the actual values and do depend on the starting position , their locations and are independent of , since it corresponds to a global shift in the position but not in time. The joint distribution of and can be computed by integrating out and (see e.g. KMS13 ; MSS16 ). Without any loss of generality, we will assume that (the case can be analysed in the same way). The grand joint PDF can be computed by decomposing the time interval into three segments: (I) , (II) and (III) . In the first segment (I), the trajectory starts at at time , arrives at at time and stays inside the space interval during (see Fig. 1). In the second segment (II), the trajectory starts at at time and arrives at at time and stays inside the box . Finally, in the third segment (III), the trajectory starts at at time and stays inside the box during . Clearly the trajectory stays inside the box because, by definition, it can neither exceed its maximum value , nor can it go below its minimum . Let us also denote by .

To enforce the trajectory to stay inside the box, one needs to impose absorbing boundary condition at both and . However, for a continuous time Brownian motion, it is well known that one can not simultaneously impose absorbing boundary condition and also require the trajectory to arrive exactly at the absorbing boundary at a certain time. One way to get around this problem is to introduce a cut-off such that the actual values of the maximum and the minimum are respectively and , see Fig. 1 in the Supp. Mat. (SM) supmat . One then computes the probability of the trajectory for a fixed and eventually takes the limit . We use the Markov property of the process to express the total probability of the trajectory as the product of the probabilities of the three individual time segments. These probabilities can be expressed in terms of a basic building block or Green’s function defined as follows. Let denote the probability density for a BM, starting at at , to arrive at at time while staying inside the box during . Note that . This Green’s function can be computed by solving the Fokker-Planck equation, , with absorbing boundary conditions at both and Redner ; Risken

| (7) |

We first shift the origin in Fig. 1 to . The probability of the trajectory in the three segments is then proportional respectively to (I) , (II) and (III) , where, in the last segment, we integrate over the final position of the trajectory inside the box (see Fig. 1). Hence is given, up to an overall normalization factor, by the product of three individual pieces. Using the Green’s function in Eq. (7), one can compute explicitly this grand PDF and finally integrate over and to obtain the joint PDF [see SM supmat for details]. From the latter, we compute the covariance of and explicitly, as given above. Also, by integrating the joint PDF over and with fixed, we compute explicitly the PDF and find that it has the scaling form given in Eq. (2) supmat .

Discrete time random walks and Lévy flights. It is natural to ask whether the PDF of the continuous-time BM derived above holds for discrete-time random walks/Lévy flights defined in Eq. (6). For such a discrete-time walk, let () denote the time at which the maximum (minimum) is reached. Remarkably, Sparre Andersen showed that the marginal distribution [equivalently ] is completely universal for all , i.e. is the same for any symmetric jump PDF SA53 – thus it is identical both for random walks with finite jump variance and Lévy flights. In particular, for large , converges to the arcsine law in Eq. (1), with replaced by and replaced by . Does this universality hold also for the PDF of the time difference ? To investigate this question, we computed exactly for the special of a double exponential jump PDF . The details are left in the SM supmat and here we just outline the main results. We find that, for large , converges to the scaling form where satisfies the integral equation

| (8) |

Remarkably, this integral equation can be solved and we show that obtained for the continuous-time BM in Eq. (2). This representation of in Eq. (8) turns out to be useful to compute the moments of explicitly (see supmat ). We would indeed expect this Brownian scaling form to hold for any jump densities with a finite variance , due to the Central Limit Theorem. We have verified numerically this universality for other jump distributions with a finite variance (see Fig. 3). However, for heavy tailed distributions, such as for Lévy flights with index , we numerically find that, while for large , , the scaling function depends on (see Fig. 3), except at the endpoints where it seems that independently of . The result for is thus less universal compared to the marginal distributions of and given by the arcsine laws (1).

Brownian bridge. We now turn to the statistics of and for a BB where the initial and the final positions are identical. The motivation for studying the BB comes from the fact that this will be directly applicable to study KPZ/EW interfaces with periodic boundary conditions in space (see below). For the BB, it is well known feller50 that , i.e., uniform over . The same result holds for as well. However, we find that the PDF of their difference takes the scaling form for all , where the scaling function is nontrivial as in Eq. (4). To derive this result, we follow the same path decomposition method as in the case of the BM, except in the third segment where we need to impose that the final position of the trajectory is . Thus, while in the time segments (I) and (II) the probabilities are exactly the same for the BM and the BB, in segment (III) we have simply for the BB (after the shift of the origin to ). Taking the product of the three segments, and following the same calculations as in the BM case (see supmat ), we obtain the result for in Eq. (4). As shown in the SM supmat , this result can also alternatively derived by exploiting a mapping, known as Vervaat’s construction vervaat79 , between the BB and the Brownian excursion (the latter being just a BB constrained to stay positive on ). We have also verified these calculations by simulating a BB using an algorithm proposed in Ref. majumdar15 finding excellent agreement (see Fig. 2).

Fluctuating interfaces. Our results can be applied directly to -dimensional KPZ/EW interfaces. Consider a one-dimensional interface growing on a finite substrate of length , with denoting the height of the interface at position and time , with review_kpz1 ; review_kpz2 ; spohn_houches . We study both free and periodic boundary conditions (FBC and PBC respectively). In the former case, the height at the endpoints and are free, while in the latter case . The height field evolves by the KPZ equation kpz86

| (9) |

where and is a Gaussian white noise with zero mean and correlator . The zero-mode, i.e. the spatially averaged height , typically grows with time. Hence, the PDF of does not reach a stationary state, even for a finite system. However, the distribution of the relative heights does reach a stationary state at long times for finite . For the simpler case of the EW edwads82 interface ( in Eq. (9)), the joint PDF of the stationary relative height , in the case of the FBC, is given by majumdar04 ; comtet05 ; schehr06

| (10) |

Here is a normalization constant and the delta-function enforces the zero area constraint , which follows from the definition of the relative height. Incidentally, this result for the FBC holds also for the KPZ equation with , but only in the large limit. Thus locally, the stationary height field , for , is a BM in space, with playing the role of time. For the PBC an additional factor is present in Eq. (10) (see Refs. majumdar04 ; comtet05 ; schehr06 ) and moreover it holds for any finite and arbitrary supmat . The PDF of the maximal relative height was computed exactly for both boundary conditions majumdar04 ; comtet05 . These distributions are nontrivial due to the presence of the global constraint of zero area under the BM/BB. Under the correspondance , and , the stationary interface maps onto a BM (for FBC) and to a BB (for PBC) of duration , with an important difference however: the corresponding BM and BB have a zero-area constraint. While this constraint affects the PDF of the maximal (minimal) height, it is clear that the position at which the maximal (respectively minimal) height occurs is not affected due to this global shift by the zero mode. Hence, the distributions of the positions of maximal and minimal height for the stationary KPZ/EW interface is identical to that of and for the BM (for FBC) and of the BB (for PBC). Hence the PDF of given in Eqs. (2) and (4) also gives the PDF of the position-difference between the minimal and maximal heights in the stationary KPZ/EW interface. We have verified this analytical prediction for the KPZ/EW interfaces by solving Eq. (9) numerically, finding excellent agreement (see Figs. 4 and 5 in supmat ).

We have presented an exactly solvable example for the distribution of the time difference between the occurrences of the maximum and the minimum of a stochastic process of a given duration . Our results show that, even for BM or BB, this distribution is highly non-trivial. We have also shown how the same distribution shows up for KPZ/EW interfaces in (1+1) dimensions in their stationary state. Computing this non-trivial distribution for other stochastic processes, such as Lévy flights, remains a challenging open problem.

References

- (1) E. J. Gumbel, Statistics of Extremes (Dover, New York, 1958).

- (2) R. W. Katz, M. B. Parlange, P. Naveau, Adv. Water Resour. 25, 1287 (2002).

- (3) R. W. Katz, G. S. Brush, M. B. Parlange, Ecology 86, 1124 (2005).

- (4) J. Krug, J. Stat. Mech. P07001 (2007).

- (5) J. Neidhart, J. Krug, Phys. Rev. Lett. 107, 178102 (2011).

- (6) S. Redner, and M. R. Petersen, Phys. Rev. E 74, 061114 (2006).

- (7) S. Rahmstorf, D. Coumou, P. Natl Acad. Sci. USA 108, 17905 (2011).

- (8) B. Christiansen, J. Clim. 26, 7863 (2013).

- (9) G. Wergen, A. Hense, and J. Krug, Clim. Dyn. 42, 1275 (2014).

- (10) S. N. Majumdar, P. von Bomhard, J. Krug, Phys. Rev. Lett. 122, 158702 (2019).

- (11) J.-P. Bouchaud, M. Potters, Theory of financial risks. From Statistical Physics to Risk Management, Cambridge University Press, Cambridge (2000).

- (12) M. Yor, Exponential functionals of Brownian motion and related processes, Springer Science Business Media (2001).

- (13) P. Embrechts, C. Klüppelberg, T. Mikosch, Modelling extremal events: for insurance and finance (Vol. 33), Springer Science Business Media (2013).

- (14) D. Challet, Appl. Math. Fin. 24, 1 (2017).

- (15) P. Lévy, Sur certains processus stochastiques homogénes, Compos. Math. 7, 283 (1940).

- (16) W. Feller, Introduction to Probability Theory and Its Applications, John Wiley Sons, New York (1950).

- (17) E. Sparre Andersen, On the fluctuations of sums of random variables, Math. Scand. 1, 263 (1954).

- (18) P. Mörters, Y. Peres, Brownian motion, Vol. 30, Cambridge University Press, (2010).

- (19) E. Buffet, J. Appl. Math. Stoch. Anal. 16, 201 (2003).

- (20) S. N. Majumdar, J.-P. Bouchaud, Quant. Fin. 8, 753 (2008).

- (21) J. Randon-Furling, S. N. Majumdar, J. Stat. Mech. P10008 (2007).

- (22) S. N. Majumdar, J. Randon-Furling, M. J. Kearney, M. Yor, J. Phys. A: Math. Theor. 41, 365005 (2008).

- (23) G. Schehr, P. Le Doussal, J. Stat. Mech. P01009 (2010).

- (24) P. Le Doussal, C. Monthus, Physica A, 317, 140 (2003).

- (25) S. N. Majumdar, Physica A 389, 4299 (2010).

- (26) S. N. Majumdar, A. Rosso, A. Zoia, J. Phys. A 43, 115001 (2010).

- (27) M. Delorme, K. J. Wiese, Phys. Rev. E 94, 052105 (2016).

- (28) T. Sadhu, M. Delorme, K. J. Wiese, Phys. Rev. Lett. 120, 040603 (2018).

- (29) P. Singh, A. Kundu, J. Stat. Mech. P083205 (2019).

- (30) S.N. Majumdar, A. Comtet, J. Randon-Furling, J. Stat. Phys. 138, 955 (2010).

- (31) J. Rambeau, G. Schehr, Phys. Rev. E 83, 061146 (2011).

- (32) S. N. Majumdar, A. Rosso, A. Zoia, Phys. Rev. Lett. 104, 020602 (2010).

- (33) A. C. Barato, É. Roldàn, I. A. Martínez, S. Pigolotti, Phys. Rev. Lett. 121, 090601 (2018).

- (34) C. Dale, R. Workman, Financ. Anal. J. 36, 71 (1980).

- (35) J. Baz, G. Chacko, Financial derivatives: Pricing, applications, and mathematics, Cambridge University Press, (2004).

- (36) A. Clauset, M. Kogan, S. Redner, Phys. Rev. E 91, 062815 (2015).

- (37) A. Kundu, S. N. Majumdar, G. Schehr, Phys. Rev. Lett. 110, 220602 (2013).

- (38) S. N. Majumdar, S. Sabhapandit, G. Schehr, Phys. Rev. E 94, 062131 (2016).

- (39) H. Risken, The Fokker-Planck Equation, Springer, Berlin, Heidelberg (1996).

- (40) S. Redner, A guide to first-passage processes, Cambridge University Press (2001).

- (41) F. Mori, S. N. Majumdar, G. Schehr, see Supplemental Material, which includes Refs. majumdar07 ; ivanov ; mounaix ; mushk_book ; lam_shin ; lam_shin2 .

- (42) S. N. Majumdar, Brownian functionals in physics and computer science, in The Legacy Of Albert Einstein: A Collection of Essays in Celebration of the Year of Physics, 93 (2007).

- (43) V. V. Ivanov, Astron. Astrophys. 286, 328 (1994).

- (44) S. N. Majumdar, P. Mounaix, G. Schehr, J. Stat. Mech. P09013 (2014).

- (45) N. I. Muskhelishvili, Singular integral equations, boundary problems of function theory and their application to mathematical physics, Melbourne: Dept. of Supply and Development, Aeronautical Research Laboratories (1949).

- (46) C.-H. Lam, F. G. Shin, Phys. Rev. E 57, 6506 (1998).

- (47) C.-H. Lam, F. G. Shin, Phys. Rev. E 58, 5592 (1998)

- (48) W. Vervaat, Ann. Probab., 143 (1979).

- (49) S. N. Majumdar, H. Orland, J. Stat. Mech., P06039 (2015).

- (50) T. Halpin-Healy, Y. C. Zhang, Phys. Rep. 254, 215 (1995).

- (51) J. Krug, Adv. Phys. 46, 139 (1997).

- (52) H. Spohn, in Stochastic processes and random matrices, 177 (2017).

- (53) M. Kardar, G. Parisi, Y.-C. Zhang, Phys. Rev. Lett. 56, 889 (1986).

- (54) S. F. Edwards, D.R. Wilkinson, P. Roy. Soc. Lond. A Mat. 381, 17 (1982).

- (55) S. N. Majumdar, A. Comtet, Phys. Rev. Lett. 92, 225501 (2004).

- (56) S. N. Majumdar, A. Comtet, J. Stat. Phys. 119, 777 (2005).

- (57) G. Schehr, S. N. Majumdar, Phys. Rev. E 73, 056103 (2006).