Value adjustments and dynamic hedging of reinsurance counterparty risk

Abstract.

Reinsurance counterparty credit risk (RCCR) is the risk of a loss arising from the fact that a reinsurance company is unable to fulfill her contractual obligations towards the ceding insurer. RCCR is an important risk category for insurance companies which, so far, has been addressed mostly via qualitative approaches. In this paper we therefore study value adjustments and dynamic hedging for RCCR. We propose a novel model that accounts for contagion effects between the default of the reinsurer and the price of the reinsurance contract. We characterize the value adjustment in a reinsurance contract via a partial integro-differential equation (PIDE) and derive the hedging strategies using a quadratic method. The paper closes with a simulation study which shows that dynamic hedging strategies have the potential to significantly reduce RCCR.

Keywords: Reinsurance, Counterparty Risk, Credit Value Adjustment, Quadratic Hedging

1. Introduction

General insurers frequently cede parts of their insurance risk to reinsurance companies in order to protect themselves from intolerably large losses in their insurance portfolio. This gives rise to a new type of risk, so-called reinsurance counterparty credit risk or RCCR. This is the risk of a loss for the ceding company caused by the fact that the reinsurer fails to honor her obligations from a reinsurance contract, for instance because the reinsurer defaults prior to maturity of the contract. Given the increased visibility of default risk in the reinsurance industry in the aftermath of the financial crisis, RCCR has become a highly relevant risk category, mainly because reinsurance recoveries represent large assets on insurance companies balance sheets. Its importance is also underlined in Solvency II regulatory directives. Nonetheless, the techniques for managing RCCR used in practice are mostly of a qualitative nature. Typically, ceding companies have minimum requirements on the credit quality of approved reinsurance companies, they set limits for the exposure to individual counterparties, and they sometimes require reinsurers to post some collateral; see for instance Bodoff [6]. The existing quantitative approaches for the management of RCCR are based on simple one-period models. This is in stark contrast to the banking world where sophisticated stochastic models are used in counterparty risk management to determine value adjustments for derivative transactions (so-called XVAs) and to find dynamic hedging and collateralization strategies, see for instance Gregory [20] or Brigo et al. [7] for an overview.

In this paper we explore the potential of dynamic risk management techniques for reinsurance counterparty risk. Our objective is twofold: we discuss the computation of value adjustments to account for reinsurance default when pricing a contract, and we analyse dynamic hedging strategies in view of reducing the risk exposure. In fact, counterparty risk towards a major reinsurance company is a low-frequency, high-severity event so that bearing this risk is not attractive for the ceding company.

We consider a setting that is tailored to the analysis of RCCR. We model the aggregate claim amount process underlying the reinsurance contract under consideration by a doubly stochastic compound Poisson process. To capture the effect that “reinsurance companies are most likely to default in times of market stress, that is exactly when cedants are most reliant upon their reinsurance covers” (Flower et al. [16]), we introduce several sources of dependence between the aggregate claim amount and the default process of the reinsurance company. There is positive correlation between the claim arrival intensity and the default intensity of the reinsurer; moreover, exhibits a contagious jump at the default time of the reinsurer. In line with the concept of market consistent valuation we define the credit value adjustment (CVA) for a reinsurance contract as the expected discounted value of the replacement cost for the contract incurred by the insurer at the default time . Using mathematical results from the companion paper Colaneri and Frey [11], we characterize the CVA as classical solution of an partial integro-differential equation. Next we address the hedging of RCCR by dynamic trading in a credit default swap (CDS) on the reinsurance company. Here we resort to a quadratic hedging approach (Schweizer [25]), since perfect replication is not possible. To determine the hedging strategy we make use of an orthogonal decomposition of the CVA into a hedgeable and a non-hedgeable part, based on the Galtchouk-Kunita-Watanabe decomposition of the associated discounted gains process. The paper closes with a simulation study. We analyse the impact of model parameters on the size of the CVA and we compare the performance of various hedging strategies. Our numerical experiments show that dynamic CDS hedging strategies significantly reduce reinsurance counterparty risk, both compared to a static hedging strategy (a strategy where the CDS position is not adjusted) and to the case where the insurance company does not hedge at all. More generally, the results suggest that dynamic risk-mitigation techniques can be very useful tools in the management of reinsurance counterparty risk.

We continue with a discussion of the existing literature. The quantitative literature on RCCR is relatively scarce. Interesting contributions from practitioners include Shaw [26] or Flower et al. [16] who propose a static model to assess the distribution of the RCCR loss, which can be used for reserving and economic capital purposes. They employ corporate bonds and CDSs to estimate reinsurance default rates and model correlation between defaults by reinsurers’ asset return correlations. Another example is offered by Kravych and Shevchenko [21] who study the problem of optimising the weight of different reinsurance companies in a given reinsurance program in order to minimize the expected loss due to RCCR. Also the solvency capital requirement for RCCR under the Solvency II standard formula is computed from a simple one-period credit risk model, see for instance CEIOPS [10]. On the academic side, Bernard and Ludkovski [2] and Cai et al. [8] study how the possibility of a default of the reinsurer affects the form of optimal reinsurance contracts. An excellent overview of counterparty risk management in banking is given in Gregory [20] or Brigo et al. [7]. Other recent contributions are, for instance Crépey [12, 13], Bo and Ceci [5]. Quadratic hedging criteria such as mean variance hedging and risk minimization have been applied in the insurance framework mainly for hedging life insurance contracts (e.g. unit linked contracts). Some recent references are, for instance Møller [23], Dahl and Møller [14], Vandaele and Vanmaele [27], Biagini et al. [3], Ceci et al. [9]

The rest of the paper is organized as follows. In Section 2 we introduce and develop the modelling framework and discuss the different forms of interaction between the insurance and the reinsurance companies that are captured by our setting. A rigorous construction of the model dynamics is provided in Section 2.2. In Section 3 we discuss the price of the reinsurance contract and the value adjustment to account for the reinsurer default. The hedging problem is studied in Section 4, and Section 5 contains the results from the numerical analysis. Some longer computations are relegated to the Appendix.

2. The model

2.1. The Setup

We work on a measurable space with a complete and right continuous filtration . We assume that on this space there are two equivalent probability measures: the physical measure and a risk neutral measure which is used for the valuation of financial and actuarial contracts. Using a risk-neutral measure for pricing purposes is in line with the principle of market consistency valuation, which is frequently used in the insurance framework and which represents one of the core elements of the Solvency II regulatory regime.

We consider a setup with two companies: an insurance company, labelled , and a reinsurer , who enter into a reinsurance contract with a given maturity (typically one year). To model the losses in the insurance portfolio underlying this contract we consider a sequence of claim arrival times and a sequence of claim sizes. Precisely, the are -stopping times such that a.s. and are a.s. strictly positive -measurable random variables. We define the counting process by , for every . Then the process given by

| (2.1) |

describes the aggregate claim amount underlying the reinsurance contract. It will be convenient to work with the integer-valued random measure on associated with the marked point process , that is

| (2.2) |

where is the Dirac measure at point . This allows for the following equivalent expression of

In our setting the reinsurance company may default and we denote by the -stopping time representing its default time; the default indicator process is given by

| (2.3) |

If , the reinsurer will not be able to fulfill his obligations which creates reinsurance counterparty credit risk (RCCR).

Next we specify the model for the loss process and the default indicator . In our analysis we are mostly concerned with valuation issues so we work under the risk-neutral measure ; to simplify the exposition we therefore introduce directly the dynamics of and . We assume that the point process modeling the claim arrivals has the -intensity for a nonnegative -adapted cádlág process (called in the sequel loss intensity), that is is a -martingale. We assume that claim sizes are independent random variables with identical distribution , and also independent of . Therefore the -predictable compensator of the measure is given by 111By definition of -predictable compensator, for every nonnegative, -predictable random function with , for every , the process is a -martingale.. We assume that the default indicator process admits a stochastic intensity (in the sequel called the default intensity of ), which is a nonnegative -adapted cádlág process such that the process

| (2.4) |

is a -martingale. Finally we describe the dynamics of the default and the claim arrival intensity. We assume that there is a standard two-dimensional -Brownian motion and that the processes and are of the form , , , where and are intensity-factor processes that satisfy the following system of SDEs

| (2.5) | ||||

| (2.6) |

for some and measurable functions , . We assume that the functions and and are continuous and increasing. A detailed construction of this model is given in Section 2.2. Modelling and as functions of the intensity factors and is mathematically convenient, see Remark 2.4 below.

We assume that the indemnity payment of the reinsurance contract is of the form for some bounded, increasing and Lipschitz continuous function . This covers typical forms of reinsurance (see, e.g. Albrecher et al. [1]). For examples, for a stop loss reinsurance contract with priority or lower attachment point and upper limit one takes (with ). Another example is offered by the excess-of-loss (XL) contract with retention level and upper limit . The payoff of this contract is given by

This can be written in the form if we set and .

We denote by the risk-free interest rate which is taken constant for simplicity. In line with market consistent valuation we define the market value of the reinsurance contract by

| (2.7) |

The quantity is the theoretical (counterparty-risk free) value of the reinsurance contract at time . Due to the fact that the reinsurer R may default, the transaction price (the price at which I and R are actually entering into the contract) needs to be adjusted. This is done via the credit value adjustment introduced in Section 3.

Remark 2.1 (Market consistent valuation).

The use of market consistent valuation does not mean that and are risk-neutral. In our context a risk premium can be built into the model by choosing the claim arrival intensity to be larger under than under ; by distorting the claim size distribution, making large claims more likely under than under ; and finally by assuming that the risk-neutral default intensity is larger than the -default intensity.

Remark 2.2 (Dependence and pricing contagion).

Our setting accounts for various forms of dependence between the default intensity of the reinsurer and the dynamics of the aggregate claim amount. First, there is correlation between Brownian motions, modelled by the parameter . In practice one would take , so that in a scenario where the insurance company experiences many losses (high claim arrival intensity ), the economic outlook for the reinsurance company gets less favourable (high default intensity ). This reflects the fact that “often there are strong correlations between reinsurance default and the loss experience of the ceded portfolio” (Flower et al. [16]). Second, there is pricing contagion. For , the risk-neutral claim arrival intensity jumps upward at , which translates into an upward jump of the market value of the reinsurance contract at , since claim arrival frequency becomes larger. This models the fact that the default of will reduce the supply for reinsurance, so that the market price of reinsurance goes up. We emphasize that this is a pure pricing phenomenon: we do not claim that the default of has an effect on the claim arrival intensity under the real-world measure. Note that each of these two forms of dependence between and imply that . In the financial literature on counterparty risk this inequality is known as wrong-way risk.

We now introduce a set of assumptions that give sufficient conditions for existence and uniqueness for the solutions of certain partial integro-differential equations that arise in the computation of the value adjustment and of the hedging strategy. Define the instantaneous covariance matrix of as

Assumption 2.3.

-

(A1)

The functions and are Lipschitz;

-

(A2)

There exists such that for every we have

(2.8) -

(A3)

The functions are Lipschitz continuous and bounded.

-

(A4)

The claim-size distribution has finite second moment.

Remark 2.4.

Instead of modelling the loss and default intensities as functions of the stochastic factors and , one might model directly the processes and . However, in this case it would be problematic to verify Assumption (A2), since intensities are forced to be nonnegative and therefore ellipticity of does not hold.

2.2. Model construction

The goal of this section is to provide a step-by-step construction of the model introduced in Section 2. Moreover, we establish certain mathematical properties that are needed for the characterization of the credit value adjustment. We start by fixing a filtered probability space . Let be a two-dimensional Brownian motion with components , let be a standard Poisson process independent of , and be a sequence of independent random variables with identical distribution , and that are also independent of and . Define the process with . This is a compound Poisson process with intensity equal to one and jump size distribution . Let the process be the unique solution of the SDE

| (2.9) |

We assume that there exists a -measurable random variable with unit exponential law, independent of and and we define as

| (2.10) |

By construction the random time is doubly stochastic with respect to the filtration with hazard rate , that is we have for every

| (2.11) |

see, e.g. Bielecki and Rutkowski [4, Section 8.2.1] or McNeil et al. [22, Section 10.5] for details. We define , , and we introduce the process as the unique solution to the SDE

| (2.12) |

To construct the aggregate claims process we use a time change argument. Define the process by for every and let . It is easy to see that is a doubly stochastic point process with intensity (see, e.g. Grandell [19]) and that the loss process is given by . Finally we define the filtration by

| (2.13) |

completed with -null sets, where is the natural filtration of the process . Notice that the random variables are -measurable, with being the sequence of jump times of . Moreover, is a stopping time with respect to the filtration . We also have that in equation (2.4) is -martingale. This is a consequence of the fact that is a martingale with respect to the filtration and, due to independence between and , this is also a martingale with respect to filtration . Now, since for every , then we have that the martingale property for holds for the filtration .

The contagion-free market.

In the remaining part of this section we introduce the contagion-free setting which will be used in the computations of the credit value adjustment and of the hedging strategies. Let be the unique solution to the SDE

| (2.14) |

It is easy to see that has the same dynamics as the “original” factor except for the jump at . We define for every , where , then is a doubly stochastic point process with intensity . We can use these processes to construct as follows,

| (2.15) |

Notice that before default, the triples and coincide, that is the processes and are indistinguishable.

We let . The following result holds.

Lemma 2.5.

The random time is doubly stochastic with respect to the background filtration .

Proof.

By the construction of we have for every . Now we observe that is adapted to and so is . Moreover we have that

which implies that ∎

3. Credit Value Adjustment

To resume the problem, we consider a reinsurance contract between and with maturity and payoff for a nonnegative and increasing function . For technical reasons we assume that is bounded and Lipschitz continuous; this assumption holds for the examples considered in Section 2.1. Moreover, the counterparty-risk free market value of this contract is given by

We assume that the premium for the contract has been paid at so that has no financial obligation towards . If defaults before the maturity date , the insurance company needs to renew her protection, that is she needs to buy a new reinsurance contract at the post-default market value . We assume that receives a recovery payment of size where is the loss given default of . Hence suffers a loss of size . We denote by the payment stream arising from the counterparty-risk loss. We have that

| (3.1) |

Note that under wrong-way risk, i.e. with , the loss of at is higher than its unconditional value. This is an important issue in the management of RCCR. For instance, in the Solvency II regulation it is stated that “As the failure of the counterparty is more likely when the potential loss is high, the LGD [in our case the loss caused by the default of ] should be determined for the case of a stressed situation,” see CEIOPS [10]. It is a strong point of our approach that wrong-way risk is generated endogenously by the model. In contrast, in the standard formula of Solvency II ad-hoc adjustments are necessary to account for wrong-way risk.

We define the credit value adjustment (CVA) for the reinsurance contract as the market consistent value of the future credit loss, that is

| (3.2) |

The amount can be viewed as a risk reserve that the insurance company has to set aside at time to cover for losses due to reinsurance counterparty risk. Alternatively, can be viewed as the pricing adjustment to account for RCCR at time , that is on the market consistent value of the cash-flow that is actually received by is equal to . This follows from the following lemma.

Lemma 3.1.

For one has

Proof.

Define the stopping time . Since is a -martingale and , we get from the optional sampling theorem that

| (3.3) |

Notice that on the set and therefore using equation (3.3) we get

so that the lemma follows from iterated conditional expectations (as ). ∎

Now we return to the interpretation of the . Fix . On the cash flow actually received by is given by The expected discounted value of this cash-flow equals

which is equal to , as the terms in the middle cancel by Lemma 3.1.

Next we want to represent the value of the CVA as classic solution of a partial integro-differential equation (PIDE). This allows for an alternative characterization of the adjusted price in addition to the stochastic representation given in equation (3.2), and it is essential for the computation of the hedging strategy in Section 4. As a first step we analyze the term that appears in the definition of the credit loss. Note that the shifted process has the same dynamics as ; hence it is a two-dimensional Markov process with generator

| (3.4) | ||||

| (3.5) |

This suggests that can be described as the solution of a backward equation involving the generator . The next proposition shows that this is in fact correct.

Proposition 3.2.

Under Assumption 2.3, there exists a unique bounded classical solution (i.e. continuous, in and in ) of the following backward PIDE

| (3.6) |

with terminal condition . Moreover, it holds for that

Proof.

The process is a two-dimensional Markov process with pure jump component and generator given in (3.4). The existence of a classical solution to the backward equation (3.6) follows from Colaneri and Frey [11]. Moreover, it holds that

The strong Markov property thus gives that on ,

where in the last equality we used that , and . ∎

Note that the regularity properties of the function ( in , in but only continuous in ) are due to the fact that is a pure jump process and therefore the smoothing effect coming from the diffusion does not apply in the direction. In the statement of Proposition 3.2 we refer for brevity to Assumption 2.3. However, Proposition 3.2 does not involve the process and therefore some of the conditions in the list (A1)–(A4) are unnecessary.

Proposition 3.3.

Under Assumptions 2.3 the value of the is given by

| (3.7) |

where is a classical solution (i.e. continuous, in and in ) of the following backward PIDE

| (3.8) |

for all with terminal condition . The operator (the generator of the three-dimensional Markov process ) is given by

| (3.9) | ||||

| (3.10) |

where is always evaluated at .

Proof.

The is a so-called payment-at-default claim (see for instance McNeil et al. [22, Section 10.5]). Proposition 3.2 allows to express its payoff at in terms of contagion free quantities. Then we get that

| (3.11) |

In equation (3.11) we can replace with since these sigma fields coincide up to time . Then we get from Lemma 2.5 and McNeil et al. [22, Theorem 10.19] that

| (3.12) |

Note that the process is Markovian with respect to the filtration with generator as in (3.10). It follows that there is a function such that

| (3.13) |

Then, by applying [11, Theorem 1] we get that is a classical solution of the backward PIDE (3.8). Finally note that on the event , and also , , which implies (3.7). ∎

Example 3.4.

In the numerical analysis we consider a special case of our setting. There the loss intensity is constant except for an upward jump at time that models price contagion. In this case we may identify the intensity and the intensity-factor process (i.e. is the identity function) and assume that

| (3.14) |

for constants and . Here the parameter models the percentage change in the loss intensity at . We now calculate the credit value adjustment for this situation. Under (3.14) the process is a compound Poisson process with intensity , jump-size distribution and generator

| (3.15) |

For given , define the function as the solution of the backward integral equation

| (3.16) |

with terminal condition . Then, the post default value of the reinsurance contract is given by222Of course other actuarial techniques such as Panjer recursion could be used as well to compute .

With this we get that credit value adjustment satisfies , where the function is the solution of the backward PIDE

| (3.17) |

for every with terminal condition , and where for a generic continuous function which is in , the operator is given by

| (3.18) |

Note that in this example the variable corresponding to loss intensity drops out of the equation (3.17) and therefore (A2) in Assumption 2.3 can be replaced by the simpler condition

-

(A2’)

There is some such that .

4. Hedging of Reinsurance Counterparty Credit Risk

In this section we investigate how the insurance company can reduce the losses arising from the default of the reinsurer by a dynamically adjusted position in a credit default swap (CDS) on . A CDS is a natural hedging instrument for credit risk since it makes a payment at , that is exactly when the counterparty risk loss arises. Moreover, there is a reasonably liquid market for CDSs on major reinsurane companies. Another option for managing counterparty risk would be a dynamically adjusted collateralization strategy as in Frey and Rösler [17]; however, one of the advantages of hedging with CDS contracts is that a strategy can be implemented unilaterally by . In our setting there are several sources of randomness that do not correspond to traded assets, such as the loss process or the loss intensity , and therefore perfect hedging is not possible. To deal with the ensuing market incompleteness we resort to a quadratic hedging method. Precisely we will consider self financing strategies and minimize the quadratic hedging error at the maturity date.

To proceed with a formal analysis of the hedging problem we need to discuss the dynamics of a self-financing CDS trading strategy. This issue is taken up next.

4.1. Dynamics of a CDS trading strategy

We consider a CDS contract on with fixed running spread premium and with default payment given by the deterministic loss given default of . To simplify the exposition we assume that the premium payments are made continuously. The cashflow stream associated to the CDS (from the viewpoint of ) is therefore given by

| (4.1) |

where the first term refers to the payment at default and the second term is the premium payment. Note that (4.1) describes the cash-flows of a CDS contract with notional equal to one; holding units of this contract is the same as holding one CDS contract with notional .

The present value of the future payments of the CDS is given by

| (4.2) |

Similarly as in Section 3, we characterize the process in terms of the classical solution of a backward partial differential equation (PDE).

Proposition 4.1.

Under Assumptions 2.3 the process is given by

where is a classical solution (i.e. in and in ) of the following backward PDE

| (4.3) |

with terminal condition . Here the operator is the generator of , that is

| (4.4) |

Proof.

Since in (2.4) is a - martingale we have that

| (4.5) |

Using Fubini’s theorem, Lemma 2.5 and McNeil et al. [22, Theorem 10.19] we get that the right hand side of (4.5) is equal to

| (4.6) |

By Markovianity of the process with respect to filtration , there exists a function such that conditional expectation in (4.6) is equal to . Denote by the generator of given by (4.4). Then it is easily seen that under Assumption 2.3, is the classical solution of (4.3), see, e.g. Oksendal [24, Theorem 8.2.1]. ∎

Finally we define the discounted gains process of the CDS (the past cashflows and the present value of the future cashflows, both discounted back to time zero) by

| (4.7) |

Note that for every and therefore is a square integrable -martingale. Consider now a self-financing trading strategy , where is the notional of the CDS position at time and where is the cash position at time . Then the value of this strategy at time equals , and the strategy is selffinancing if the discounted value satisfies

4.2. Quadratic hedging

Next we formalize the quadratic criterion that is used to determine the optimal hedging strategy. We call a self-financing trading strategy admissible if is -adapted and is -predictable and satisfies the integrability condition

| (4.8) |

Here denotes the predictable quadratic variation of the martingale (the predictable compensator of the pathwise quadratic variation of ). Condition (4.8) ensures that the discounted value process is a right continuous and square integrable martingale. The hedging problem amounts to finding a self-financing admissible strategy with initial value and CDS position that minimizes the quadratic hedging error

| (4.9) |

Such a strategy will be called -mean-variance minimizing.

Remark 4.2.

We continue with a few comments on the hedging criterion.

1) Minimizing the quadratic hedging error with respect to the risk-neutral measure , instead of the historical measure , has a couple of advantages. First, the ensuing CDS position is time-consistent: the CDS strategy that minimizes the conditional quadratic hedging error

over the period is the restriction of to the interval . This is in general not true for a -mean-variance minimizing strategy. Moreover, since the default and loss intensities under are typically higher than the corresponding -intensities (see Remark 2.1), more mass is put in expectation (4.9) on states where the counterparty-risk loss is large and the -mean-variance minimizing strategy will track the credit loss more closely in those states than a -mean-variance-minimizing strategy; this adds an additional layer of prudence to our approach. Finally a -mean-variance-minimizing strategy is comparatively easy to determine and the solution has a clear economic interpretation.

2) As an alternative to -mean-variance minimization one might consider risk minimization under as hedging criterion. The investment in the risky asset (the CDS in our setting) is the same for both approaches; the only difference is that in the mean-variance-hedging approach a self financing strategy is followed until time where the hedging error takes the form of a lump sum adjustment. In the risk minimization approach on the other hand the portfolio value is adjusted continuously at any . Note however that mean-variance hedging and risk minimization lead to different strategies if one works under the historical measure. For an in-depth discussion of these issues we refer to Schweizer [25].

To determine the -mean-variance minimizing strategy we first introduce the discounted gain process associated with the credit loss. This process is given by

| (4.10) |

where we recall that CL is the payment stream arising from the counterparty-risk loss defined in equation (3.1), and is easily seen to be a square integrable -martingale. Since the discounted gain process of the CDS in equation (4.7) is a -martingale, it is well known that the -mean-variance optimal strategy can be determined with the help of the Galtchouk-Kunita-Watanabe decomposition of with respect to . This result ensures the existence of a predictable process satisfying (4.8) and of a martingale null at time zero, which is strongly orthogonal to (that is the product of the two martingales is also a martingale or, equivalently, the predictable quadratic covariation vanishes) such that

| (4.11) |

Then the strategy with CDS position and initial value is -mean-variance minimizing. A detailed proof of this result can be found in Schweizer [25]. Intuitively, decomposition (4.11) permits to decompose the payment stream into its attainable part given by , and an unattainable part corresponding to non-hedgeable risk.

Identifying entails taking the predictable covariation with respect to on both sides of equation (4.11). Using orthogonality between and , we get that

where denotes the predictable quadratic covariation between martingales and . This implies that can be identified as predictable version of the Radon Nikodym density . Computing this density is the key point in the proof of the following theorem where we determine the -mean-variance minimizing strategy.

Theorem 4.3.

The -mean-variance minimizing strategy is characterized by the initial value and by the CDS position , for every , where

| (4.12) | ||||

| (4.13) | ||||

| (4.14) | ||||

| and | ||||

| (4.15) | ||||

Proof.

By definition which gives the initial value of the strategy. In order to determine note that in our setting the processes and are absolutely continuous with respect to Lebesgue measure. This implies that -a.s.

To derive the processes and we compute the pathwise quadratic (co)variations , respectively , and we use that , respectively , is the predictable compensator of these processes. We recall that is the compensated martingale given in equation (2.4) and denote by the compensated jump measure . From the PIDE characterization of the CVA in Proposition 3.3 and the Itô formula, see Appendix A for the detailed computations, we get that the martingale in (4.10) is explicitly given by

| (4.16) | ||||

| (4.17) | ||||

| (4.18) | ||||

| (4.19) |

In a similar way we obtain the martingale decomposition of the process . It holds that for every ,

| (4.20) | ||||

| (4.21) |

Then the quadratic covariation of the two martingales and and for the quadratic variation of is

| (4.22) | ||||

| (4.23) | ||||

| (4.24) | ||||

| (4.25) |

The predictable quadratic variation is then obtained by computing predictable compensators, which leads to (4.12) and (4.15) and implies the result.

∎

4.2.1. Special cases and interpretation.

In order to understand the form of it is instructive to consider first the limiting case where and where and for every . In that setting we can consider both and as parameters and get that

We clearly see that the CDS strategy generates a payment at the default time of size , that is the strategy provides a perfect hedge against the counterparty-risk loss at (pure hedging of jump risk). Note however, that the strategy is not self-financing, as the CDS position needs to be adjusted according to the random evolution of the aggregate claim amount .

For the strategy balances the hedging of jump risk and the hedging against fluctuations in the default intensity factor (hedging of spread risk). The optimal mean-variance strategy in the setting of Example 3.4 can be obtained by letting . Using the special notation for this case we obtain that

| (4.26) | ||||

| (4.27) |

If , and are all strictly positive, then an additional cross term appears in (4.12). It is intuitively clear that both partial derivatives are positive333A higher loss intensity makes a large credit loss more likely, thereby increasing the CVA, and a higher default intensity increases the value of the future CDS payments., so that the CDS position is increased by this term. This is due to the fact that some of the risk caused by fluctuations in the non-traded loss intensity factor can be hedged by increasing the position in the correlated CDS contract.

5. Numerical Experiments

In this section we present results from numerical experiments that complement the theoretical analysis. In Section 5.1 we focus on the relative importance of dependence and pricing contagion for wrong way risk; in Section 5.2 we study -mean-variance-minimizing strategies and we compare their performance to that of a static strategy.

Throughout our analysis we consider the following setup. We identify processes the and , that is we assume that and are the identity functions. The default intensity follows a CIR process with the dynamics

| (5.1) |

this allows for an explicit formula for the price of the CDS, see, e.g. Duffie et al. [15]. For the loss intensity we consider a jump diffusion of the form

| (5.2) |

If we take we recover the case of Example 3.4 where the loss intensity has a jump at default and is otherwise constant. Finally, we assume that claim sizes are Gamma distributed. We consider a reinsurance contract of stop loss type with payoff , capped at , we set the interest rate to and the loss-given-default of R and of the CDS to .

Next we briefly discuss the methods used in the numerical analysis. The main task is to calculate the CVA in (3.7). Using the equivalent formulation in (3.12) we see that this amounts to evaluating the expectation

| (5.3) |

We evaluate this term using Monte Carlo simulation. In general this is a nested Monte Carlo problem, as one needs also to compute the default free value of the reinsurance contract , for every . For the case where , follows a compound Poisson process and we may use Panjer recursion. For the general case, we mostly use a regression-based approach to reduce the computational cost (see, Glasserman [18, Chapter 8.6]). The computation of the mean-variance minimizing hedging strategies involves computing derivatives of the functions and . These are computed via a Monte Carlo approach, following Glasserman [18, Chapter 7.2].

5.1. CVA and wrong-way risk

In this section we analyse the impact of the pricing contagion and the correlation between the loss and the default intensities on the CVA by varying the parameters and . We assume that and that claim sizes are Gamma(1,1) distributed.

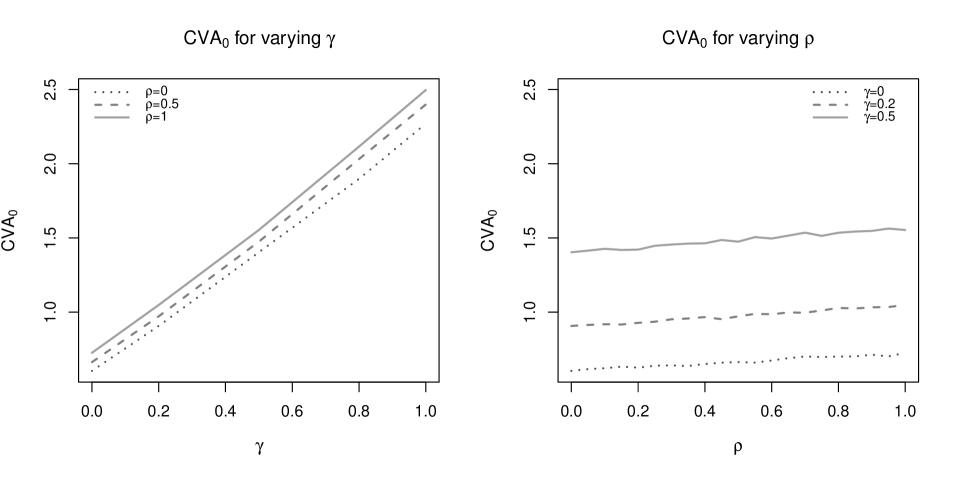

In Figure 1 we display the CVA at time for different values of (left panel) and for different correlation levels (right panel). In these plots we fixed . We see that increases in both and , which is in line with the observation in Remark 2.2. The effect of price contagion (i.e. variation in ) is quite pronounced and dominates the effect of dependence between intensities (i.e. variation in ), and we conclude that it is very important to incorporate price contagion into the analysis of RCCR.

|

5.2. Performance of hedging strategies

We now compute the hedging strategies corresponding to different parameter choices and we compare their performance to that of a static strategy. Precisely we consider the three cases described in Table 1 below. Case 1 and Case 2 correspond to a loss intensity that stays constant with a single jump at time , where it increases by . The parameters of the claims size distribution and the loss intensity are chosen in such a way that the expected contagion-free loss is the same (). However in Case 1 the insurance company experiences small but frequent losses whereas in Case 2 there are infrequent but large losses. Intuitively we therefore expect hedging to be more difficult in the second case.

| Case 1: | 100 | 0.2 | 0 | 0 | 0 | 1 | 1 |

|---|---|---|---|---|---|---|---|

| Case 2: | 10 | 0.2 | 0 | 0 | 0 | 10 | 1 |

| Case 3: | 100 | 0 | 1 | 0.2 | 0.2 | 1 | 1 |

In addition to the dynamic -mean-variance minimizing strategies from Theorem 4.3 we considered two simpler strategies. First we considered a static CDS hedging strategy where the value of the CVA at is invested in the CDS and where the position is not adjusted over time (in mathematical terms and . Moreover we considered a strategy labelled unhedged CVA, where the amount is invested in the bank account and where one does not invest in the CDS at all ( and ). In order to measure the performance of a hedging strategy we consider the value of the hedged CVA position, which is given by

| (5.4) |

In the sequel we refer to the process in (5.4) as the tracking error. Note that a positive value of corresponds to a loss for the insurance company. In our experiments we assume that the hedging portfolio is re-balanced approximately every two weeks. More frequent re-balancing is not practically feasible for insurance companies as the total claim amount is hard to evaluate.

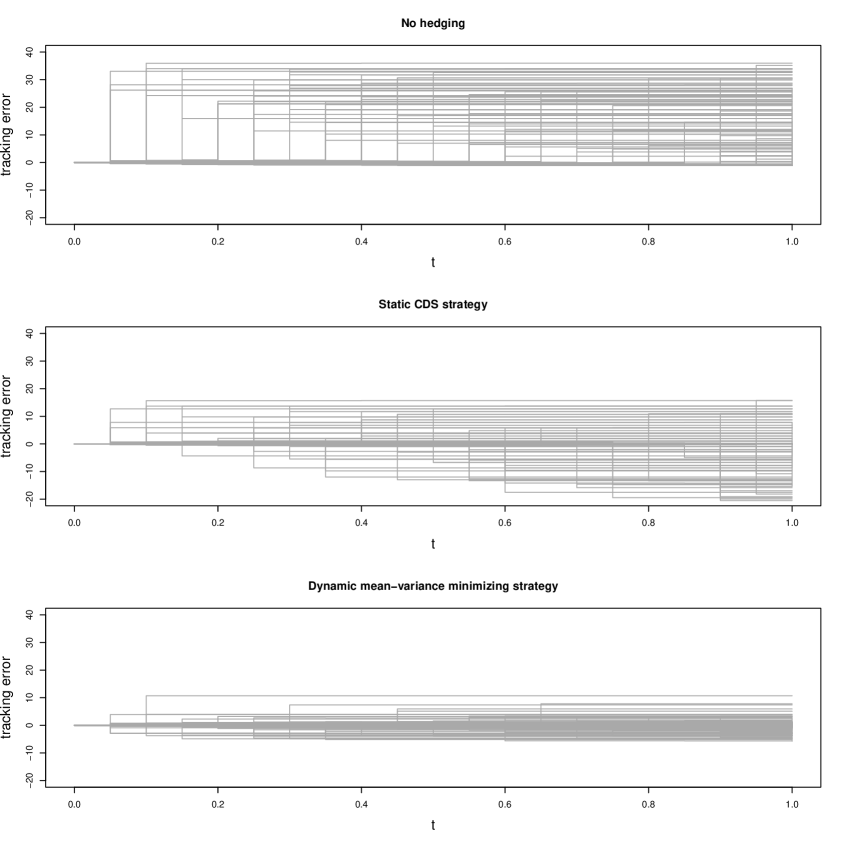

In Figure 2 we use the parameter set corresponding to Case 1. The plot displays 2000 trajectories of the tracking error, first for (unhedged CVA), second for the static CDS strategy and third for the dynamic -mean-variance minimizing strategy from Theorem 4.3.

|

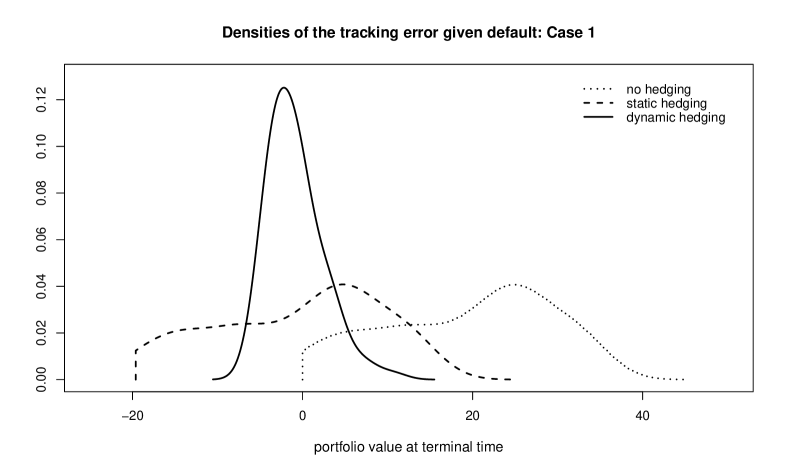

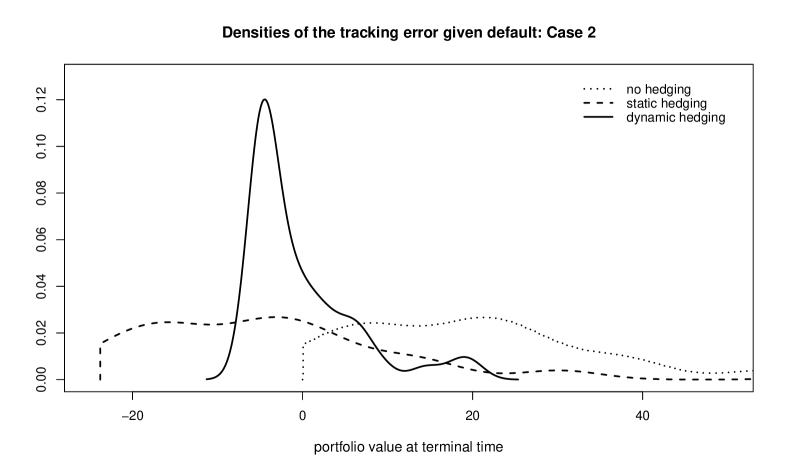

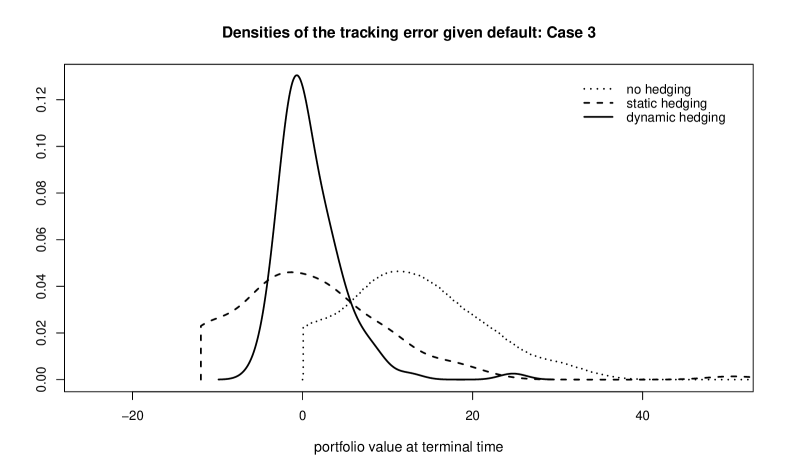

From Figure 2 it is evident that for all three strategies the tracking error jumps at , but the form of the jumps is very different. In the unhedged-CVA case the jump is always upwards and the size of the jump is equal to the replacement cost for the reinsurance contract. In this case a default of R is relatively expensive: the maximum loss that the insurance company incurs is around EUR , which is roughly three times the initial value of the reinsurance contract. In the middle panel we give the tracking error for the static CDS hedging strategy. We observe either a loss (under-hedging) or a profit (over-hedging). The maximum loss (and profit) is around EUR which implies that static hedging is an improvement over the unhedged CVA , but the tracking error still shows a high variability. The dynamic mean-variance minimizing strategy on the other hand significantly reduces the variability of the tracking error as it is clearly displayed in the lower panel. We conclude that this strategy out-performs the other hedging approaches by a large margin. The difference in the performance of the hedging strategies is illustrated further in Figure 3 where we plot the density of the tracking error conditional on . For a good hedging strategy the density of the tracking error should be concentrated around zero with a small mass in the tails. This is the case for the mean-variance minimizing strategy. The densities for the two other strategies have much larger mass in the tails. The shape of these densities is identical, but that corresponding to the static CDS strategy is shifted to the left, which results in a lower value of . The value of the -norm of for all three strategies is given in Table 2.

| Strategy | |

|---|---|

| No hedging | 22.65 |

| Static CDS hedging | 4.54 |

| Dynamic mean-variance minimizing | 0.62 |

|

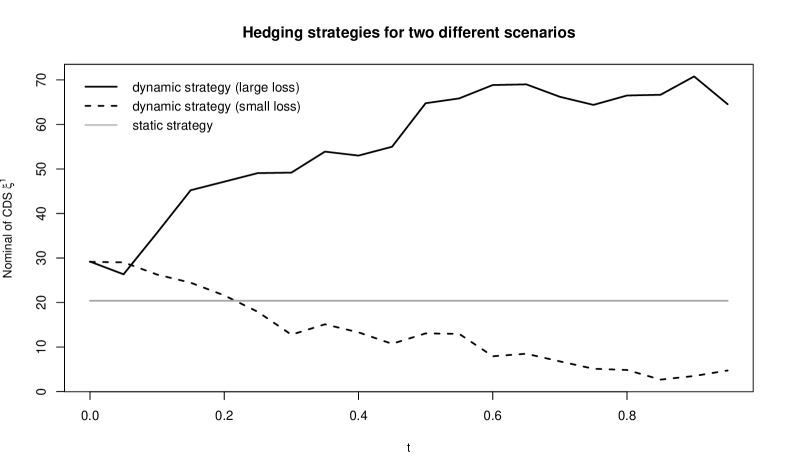

In order to explain the superior performance of the dynamic strategy we plot in Figure 4 two trajectories of the optimal strategy. The solid line corresponds to a trajectory of the claim amount process with a large loss, the dashed line to a trajectory with small loss. We compare these strategies to the static hedging strategy which is constant over time (grey line). We see that the optimal hedge ratio is quite sensitive with respect to the evolution of the underlying loss process.

|

In Case 2 we consider the situation where claims arrive less frequently but have on average a higher size. In this case hedging is more difficult, but the mean-variance minimizing strategy still outperforms the other approaches, as is clearly seen from Figure 5. Moreover, for the mean-variance minimizing strategy the -norm of the tracking error is considerably smaller than for the other strategies, see Table 3 for details. In Case 3 we consider the situation where the loss and the default intensities are correlated but there is no pricing contagion (), that is the loss intensity does not jump at time . Here the wrong way risk arises from correlation only. Figure 6 confirms the relative performance of the strategies for this case as well. In the general model with price contagion and correlation the qualitative results on the behaviour of the tracking error are similar to the ones described so far; we omit the details.

Summarizing, our results show that dynamic CDS trading strategies have the potential to significantly reduce reinsurance counterparty risk, both compared to a static hedging strategy and to the case where the insurance company does not hedge at all.

| Strategy | |

|---|---|

| No hedging | 39.78 |

| Static CDS hedging | 17.82 |

| Dynamic mean-variance minimizing | 2.17 |

|

|

Acknowledgements

The authors are grateful for useful comments from Hansjörg Albrecher. Support by the Vienna Science and Technology Fund (WWTF) through project MA14-031 is gratefully acknowledged. The work of K. Colaneri was partially supported by INdAM GNAMPA through the project UFMBAZ-2018/000349. A part of this article was written while K. Colaneri was affiliated with the School of Mathematics, University of Leeds, LS2 9JT, Leeds, UK. The work of the first and the second author was partially supported by INdAM-GNAMPA through projects UFMBAZ- 2017/0000327 and UFMBAZ-2019/000436.

Appendix A The martingales and

In the sequel we provide detailed computations for the dynamics of the martingale . We start with the martingale . For every we have that

so that

| (A.1) | ||||

| (A.2) |

Recall that by Proposition 3.3, is a smooth solutions of the PIDE (3.8), therefore it has the necessary regularity to apply the Itô formula. This gives

| (A.3) | ||||

| (A.4) | ||||

| (A.5) | ||||

| (A.6) | ||||

| (A.7) | ||||

| (A.8) |

Now using the fact that solves equation (3.8) we get that satisfies equation (4.16). Similar computations can be performed for the martingale , we omit the details.

References

- Albrecher et al. [2017] H. Albrecher, J. Beirlant, and J. Teugels. Reinsurance: Actuarial and Statistical Aspects. Wiley, 2017.

- Bernard and Ludkovski [2012] C. Bernard and M. Ludkovski. Impact of counterparty risk on the reinsurance market. North American Actuarial Journal, 16(1):87–111, 2012.

- Biagini et al. [2017] F. Biagini, C. Botero, and I. Schreiber. Risk-minimization for life insurance liabilities with dependent mortality risk. Mathematical Finance, 27(2):505–533, 2017.

- Bielecki and Rutkowski [2004] T. Bielecki and M. Rutkowski. Credit Risk: Modeling, Valuation and Hedging. Springer Science & Business Media, 2004.

- Bo and Ceci [2019] L. Bo and C. Ceci. Locally risk-minimizing hedging of counterparty risk for portfolio of credit derivatives. Applied Mathematics & Optimization, pages 1–52, 2019.

- Bodoff [2013] N. Bodoff. Reinsurance credit risk: A market-consistent paradigm for quantifying the cost of risk. Variance Advancing the Science of Risk, Casualty Actuarial Society, 7(1):11–28, 2013.

- Brigo et al. [2013] D. Brigo, M. Morini, and A. Pallavicini. Counterparty credit risk, collateral and funding: with pricing cases for all asset classes, volume 478. John Wiley & Sons, 2013.

- Cai et al. [2014] J. Cai, C. Lemieux, and F. Liu. Optimal reinsurance with regulatory initial capital and default risk. Insurance: Mathematics and Economics, 57:13–24, 2014.

- Ceci et al. [2017] C. Ceci, K. Colaneri, and A. Cretarola. Unit-linked life insurance policies: optimal hedging in partially observable market models. Insurance: Mathematics and Economics, 76:149–163, 2017.

- [10] CEIOPS. CEIOPS’ advice for Level 2 implementing measures on Solvency II: SCR Standard Formula, Article 109(1c), Correlations- Counterparty default risk module. Technical report, Committee of European Insurance and Occupational Pensions Supervisors, October 2009. CEIOPS-DOC-23/09.

- Colaneri and Frey [2019] K. Colaneri and R. Frey. Classical solutions of the backward PIDE for a Markov point process with characteristics modulated by a jump diffusion. Preprint ArXiv, https://arxiv.org/pdf/1903.07492.pdf, 2019.

- Crépey [2015a] S. Crépey. Bilateral counterparty risk under funding constraints—part i: Pricing. Mathematical Finance, 25(1):1–22, 2015a.

- Crépey [2015b] S. Crépey. Bilateral counterparty risk under funding constraints—part ii: Cva. Mathematical Finance, 25(1):23–50, 2015b.

- Dahl and Møller [2006] M. Dahl and T. Møller. Valuation and hedging of life insurance liabilities with systematic mortality risk. Insurance: mathematics and economics, 39(2):193–217, 2006.

- Duffie et al. [2000] D. Duffie, J. Pan, and K. Singleton. Transform analysis and asset pricing for affine jump-diffusions. Econometrica, 68(6):1343–1376, 2000.

- Flower et al. [2007] M. Flower, M. Afify, I. Cook, V. Gosrani, G. James, P. Koulovasilopoulos, J. Lincoln, D. Maneval, and J. Robinson. Reinsurance counterparty credit risks: Practical suggestions for pricing, reserving and capital modelling. GIRO working paper, Institute and Faculty of Actuaries, 2007.

- Frey and Rösler [2014] R. Frey and L. Rösler. Contagion effects and collateralized credit value adjustments for credit default swaps. International Journal of Theoretical and Applied Finance, 17(07):1450044, 2014.

- Glasserman [2003] P. Glasserman. Monte Carlo methods in financial engineering. Springer, 2003.

- Grandell [2012] J. Grandell. Aspects of risk theory. Springer Science & Business Media, 2012.

- Gregory [2012] J. Gregory. Counterparty credit risk and credit value adjustment: A continuing challenge for global financial markets. John Wiley & Sons, 2012.

- Kravych and Shevchenko [2011] Y. Kravych and P. Shevchenko. Managing exposure to reinsurance credit risk. pages 1–17, 2011.

- McNeil et al. [2015] A. McNeil, R. Frey, and P. Embrechts. Quantitative Risk Management: Concepts, Techniques and Tools - revised edition. Princeton University Press, 2015.

- Møller [2001] T. Møller. Risk-minimizing hedging strategies for insurance payment processes. Finance and Stochastics, 5(4):419–446, 2001.

- Oksendal [2013] B. Oksendal. Stochastic differential equations: an introduction with applications. Springer Science & Business Media, 2013.

- Schweizer [2001] M. Schweizer. A guided tour through quadratic hedging approaches. In E. Jouini, J. Cvitanic, and M. Musiela, editors, Option Pricing, Interest Rates and Risk Management, pages 538–574. Cambridge University Press, 2001.

- Shaw [2007] R.A. Shaw. The modelling of reinsurance credit risk. GIRO working paper, Institute and Faculty of Actuaries, 2007.

- Vandaele and Vanmaele [2008] N. Vandaele and M. Vanmaele. A locally risk-minimizing hedging strategy for unit-linked life insurance contracts in a lévy process financial market. Insurance: Mathematics and Economics, 42(3):1128–1137, 2008.