lemmasection

Compact Autoregressive Network

Abstract

Autoregressive networks can achieve promising performance in many sequence modeling tasks with short-range dependence. However, when handling high-dimensional inputs and outputs, the huge amount of parameters in the network lead to expensive computational cost and low learning efficiency. The problem can be alleviated slightly by introducing one more narrow hidden layer to the network, but the sample size required to achieve a certain training error is still large. To address this challenge, we rearrange the weight matrices of a linear autoregressive network into a tensor form, and then make use of Tucker decomposition to represent low-rank structures. This leads to a novel compact autoregressive network, called Tucker AutoRegressive (TAR) net. Interestingly, the TAR net can be applied to sequences with long-range dependence since the dimension along the sequential order is reduced. Theoretical studies show that the TAR net improves the learning efficiency, and requires much fewer samples for model training. Experiments on synthetic and real-world datasets demonstrate the promising performance of the proposed compact network.

Keywords: artificial neural network, dimension reduction, sample complexity analysis, sequence modeling, tensor decomposition

1 Introduction

Sequence modeling has been used to address a broad range of applications including macroeconomic time series forecasting, financial asset management, speech recognition and machine translation. Recurrent neural networks (RNN) and their variants, such as Long-Short Term Memory (Hochreiter and Schmidhuber,, 1997) and Gated Recurrent Unit (Cho et al.,, 2014), are commonly used as the default architecture or even the synonym of sequence modeling by deep learning practitioners (Goodfellow et al.,, 2016). In the meanwhile, especially for high-dimensional time series, we may also consider the autoregressive modeling or multi-task learning,

| (1) |

where the output and each input are -dimensional, and the lag can be very large for accomodating sequential dependence. Some non-recurrent feed-forward networks with convolutional or other certain architectures have been proposed recently for sequence modeling, and are shown to have state-of-the-art accuracy. For example, some autoregressive networks, such as PixelCNN (Van den Oord et al., 2016b, ) and WaveNet (Van den Oord et al., 2016a, ) for image and audio sequence modeling, are compelling alternatives to the recurrent networks.

This paper aims at the autoregressive model (1) with a large number of sequences. This problem can be implemented by a fully connected network with inputs and outputs. The number of weights will be very large when the number of sequences is large, and it will be much larger if the data have long-range sequential dependence. This will lead to excessive computational burden and low learning efficiency. Recently, Du et al., (2018) showed that the sample complexity in training a convolutional neural network (CNN) is directly related to network complexity, which indicates that compact models are highly desirable when available samples have limited sizes.

To reduce the redundancy of parameters in neural networks, many low-rank based approaches have been investigated. One is to reparametrize the model, and then to modify the network architecture accordingly. Modification of architectures for model compression can be found from the early history of neural networks (Fontaine et al.,, 1997; Grézl et al.,, 2007). For example, a bottleneck layer with a smaller number of units can be imposed to constrain the amount of information traversing the network, and to force a compact representation of the original inputs in a multilayer perceptron (MLP) or an autoencoder (Hinton and Salakhutdinov,, 2006). The bottleneck architecture is equivalent to a fully connected network with a low-rank constraint on the weight matrix in a linear network.

Another approach is to directly constrain the rank of parameter matrices. For instance, Denil et al., (2013) demonstrated significant redundancy in large CNNs, and proposed a low-rank structure of weight matrices to reduce it. If we treat weights in a layer as a multi-dimensional tensor, tensor decomposition methods can then be employed to represent the low-rank structure, and hence compress the network. Among these works, Lebedev et al., (2014) applied the CP decomposition for the 4D kernel of a single convolution layer to speed up CNN, and Jaderberg et al., (2014) proposed to construct a low-rank basis of filters to exploit cross-channel or filter redundancy. Kim et al., (2016) utilized the Tucker decomposition to compress the whole network by decomposing convolution and fully connected layers. The tensor train format was employed in Novikov et al., (2015) to reduce the parameters in fully connected layers. Several tensor decomposition methods were also applied to compress RNNs (Tjandra et al.,, 2018; Ye et al.,, 2018; Pan et al.,, 2019). In spite of the empirical success of low-rank matrix and tensor approaches in the literature, theoretical studies for learning efficiency are still limited.

A fully connected autoregressive network for (1) will have weights, and it will reduce to for an MLP with one hidden layer and hidden units. The bottleneck architecture still has too many parameters and, more importantly, it does not attempt to explore the possible compact structure along the sequential order. We first simplify the autoregressive network into a touchable framework, by rearranging all weights into a tensor. We further apply Tucker decomposition to introduce a low-dimensional structure and translate it into a compact autoregressive network, called Tucker AutoRegressive (TAR) net. It is a special compact CNN with interpretable architecture. Different from the original autoregressive network, the TAR net is more suitable for sequences with long-range dependence since the dimension along the sequential order is reduced.

There are three main contributions in this paper:

1. We innovatively tensorize weight matrices to create an extra dimension to account for the sequential order and apply tensor decomposition to exploit the low-dimensional structure along all directions. Therefore, the resulting network can handle sequences with long-range dependence.

2. We provide theoretical guidance on the sample complexity of the proposed network. Our problem is more challenging than other supervised learning problems owing to the strong dependency in sequential samples and the multi-task learning nature. Moreover, our sample complexity analysis can be extended to other feed-forward networks.

3. The proposed compact autoregressive network can flexibly accommodate nonlinear mappings, and offer physical interpretations by extracting explainable latent features.

The rest of the paper is organized as follows. Section 2 proposes the linear autoregressive networks with low-rank structures and presents a sample complexity analysis for the low-rank networks. Section 3 introduces the Tucker autoregressive net by reformulating the single-layer network with low-rank structure to a compact multi-layer CNN form. Extensive experiments on synthetic and real datasets are presented in Section 4. Proofs of theorems and detailed information for the real dataset are provided in the Appendix.

2 Linear Autoregressive Network

This section demonstrates the methodology by considering a linear version of (1), and theoretically studies the sample complexity of the corresponding network.

2.1 Preliminaries and Background

2.1.1 Notation

We follow the notations in Kolda and Bader, (2009) to denote vectors by lowercase boldface letters, e.g. ; matrices by capital boldface letters, e.g. ; tensors of order 3 or higher by Euler script boldface letters, e.g. . For a generic th-order tensor , denote its elements by and unfolding of along the -mode by , where the columns of are the -mode vectors of , for . The vectorization operation is denoted by . The inner product of two tensors is defined as . The Frobenius norm of a tensor is defined as . The mode- multiplication of a tensor and a matrix is defined as

for , respectively. For a generic symmetric matrix , and represent its largest and smallest eigenvalues, respectively.

2.1.2 Tucker decomposition

The Tucker ranks of are defined as the matrix ranks of the unfoldings of along all modes, namely , . If the Tucker ranks of are , where , there exist a tensor and matrices , such that

| (2) |

which is known as Tucker decomposition (Tucker,, 1966), and denoted by . With the Tucker decomposition (2), the -mode matricization of can be written as

| (3) |

where denotes the Kronecker product for matrices.

2.2 Linear Autoregressive Network

Consider a linear autoregressive network,

where is the output, s are weight matrices, and is the bias vector. Let be the -dimensional inputs. We can rewrite it into a fully connected network,

| (4) |

for , where is the weight matrix. Note that denotes the effective sample size, which is the number of samples for training. In other words, the total length of the sequential data is .

To reduce the dimension of , a common strategy is to constrain the rank of to be , which is much smaller than . The low-rank weight matrix can be factorized as , where is a matrix and is a matrix, and the fully connected network can be transformed into

| (5) |

The matrix factorization reduces the number of parameters in from to . However, if both and are large, the weight matrix is still of large size.

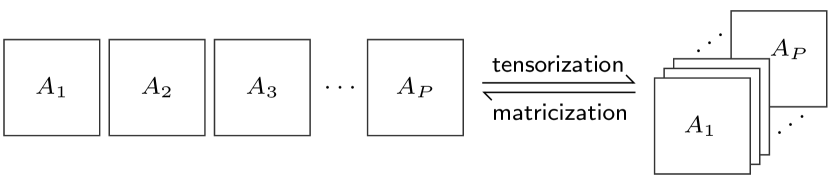

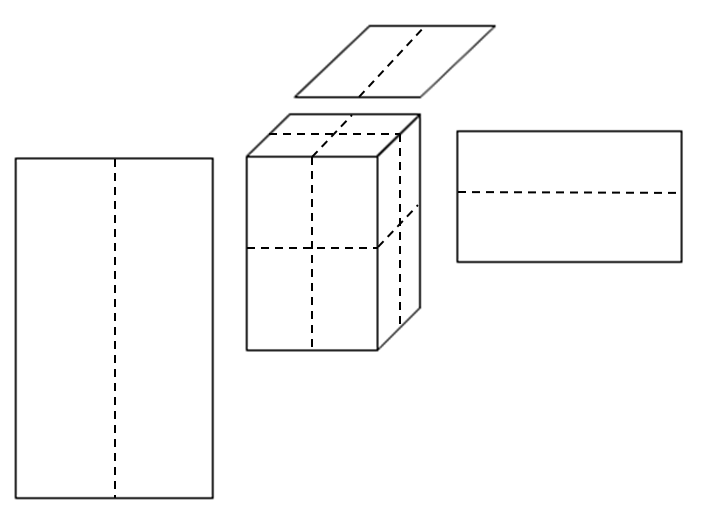

We alternatively rearrange the weight matrices s into a 3rd-order tensor such that ; see Figure 1 for the illustration. The Tucker decomposition can then be applied to reduce the dimension from three modes simultaneously. If the low-Tucker-rank structure is applied on with ranks , the network becomes

| (6) |

by Tucker decomposition . The Tucker decomposition further reduces the dimension from the other two modes of low-rank structure in (5), while the low-rankness of only considers the low-dimensional structure on the 1-mode of but ignores the possible compact structure on the other two modes.

We train the network based on the squared loss. For simplicity, each sequence is subtracted by its mean, so the bias vector can be disregarded. The weight matrix or tensor in (4), (5) and (6) can be trained, respectively, by minimizing the following ordinary least squares (OLS), low-rank (LR) and low-Tucker-rank (LTR) objective functions,

These three minimizers are called OLS, LR and LTR estimators of weights in the linear autoregressive network, respectively.

The matrix factorization or tensor Tucker decomposition is not unique. Conventionally, orthogonal constraints can be applied to these components to address the uniqueness issue. However, we do not impose any constraints on the components to simplify the optimization and mainly focus on the whole weight matrix or tensor instead of its decomposition.

2.3 Sample Complexity Analysis

The sample complexity of a neural network is defined as the training sample size requirement to obtain a certain training error with a high probability, and is a reasonable measure of learning efficiency. We conduct a sample complexity analysis for the three estimators, , and , under the high-dimensional setting by allowing both and to grow with the sample size at arbitrary rates.

We further assume that the sequence is generated from a linear autoregressive process with additive noises,

| (7) |

Denote by the true parameters in (7) and by the corresponding folded tensor. We assume that has Tucker ranks , and , and require the following conditions to hold.

Condition 1.

All roots of matrix polynomial are outside unit circle.

Condition 2.

The errors is a sequence of independent Gaussian random vectors with mean zero and positive definite covariance matrix , and is independent of the historical observations .

Condition 1 is sufficient and necessary for the strict stationarity of the linear autoregressive process. The Gaussian assumption in Condition 2 is very common in high-dimensional time series literature for technical convenience (Basu and Michailidis,, 2015).

Multiple sequence data may exhibit strong temporal and inter-sequence dependence. To analyze how dependence in the data affects the learning efficiency, we follow Basu and Michailidis, (2015) to use the spectral measure of dependence below.

Definition 1.

Define the matrix polynomial , where z is any point on the complex plane, and define its extreme eigenvalues as

where is the Hermitian transpose of .

By Condition 1, the extreme eigenvalues are bounded away from zero and infinity, . Based on the spectral measure of dependence, we can derive the non-asymptotic statistical convergence rates for the LR and LTR estimators. Note that denotes a generic positive constant, which is independent of dimension and sample size, and may represent different values even on the same line. For any positive number and , and denote that there exists such that and , respectively.

Theorem 1.

Suppose that Conditions 1-2 are satisfied, and the sample size . With probability at least ,

where is the dependence measure constant.

Theorem 2.

Suppose that Conditions 1-2 are satisfied, and the sample size . With probability at least ,

The proofs of Theorems 1 and 2 are provided in the supplemental material. The above two theorems present the non-asymptotic convergence upper bounds for LTR and LR estimators, respectively, with probability tending to one as the dimension and sample size grow to infinity. Both upper bounds take a general form of , where captures the effect from dependence across , and denotes the number of parameters in Tucker decomposition or matrix factorization. From Theorems 1 and 2, we then can establish the sample complexity for these two estimators accordingly.

Theorem 3.

For a training error , if the conditions of Theorem 1 hold, then the sample complexity is for the LTR estimator to achieve .

Moreover, if the conditions of Theorem 2 hold, then the sample complexity is for the LR estimator to achieve .

Remark 1.

The OLS estimator can be shown to have the convergence rate of , and its sample complexity is for a training error and .

The sample complexity for the linear autoregressive networks with different structures is proportional to the corresponding model complexity, i.e. sample complexity is . Compared with the OLS estimator, the LR and LTR estimators benefit from the compact low-dimensional structure and have smaller sample complexity. Among the three linear autoregressive networks, the LTR network has the most compact structure, and hence the smallest sample complexity.

Remark 2.

The sample complexity analysis of the autoregressive networks can be extended to the general feed-forward networks, and explains why the low-rank structure can enhance the learning efficiency and reduce the sample complexity.

3 Tucker Autoregressive Net

This section introduces a compact autoregressive network by formulating the linear autoregressive network with the low-Tucker-rank structure (6), and it has a compact multi-layer CNN architecture. We call it the Tucker AutoRegressive (TAR) net for simplicity.

3.1 Network Architecture

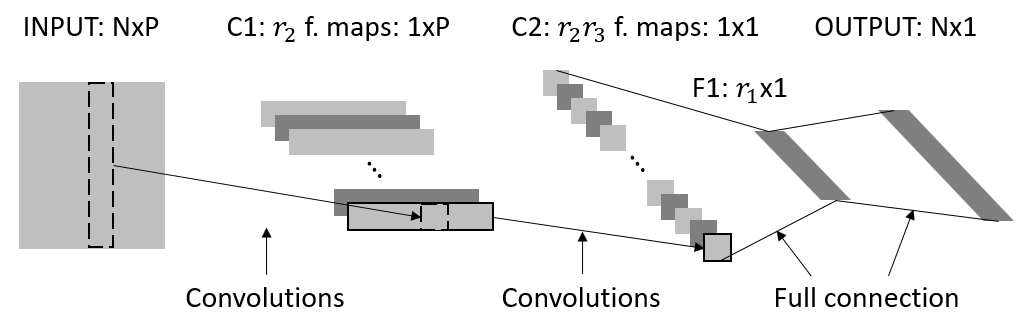

Rather than directly constraining the matrix rank or Tucker ranks of weights in the zero-hidden-layer network, we can modify the network architecture by adding convolutional layers and fully connected layers to exploit low-rank structure. By some algebra, the framework (6) can be rewritten into

where . A direct translation of the low-Tucker-rank structure leads to a multi-layer convolutional network architecture with two convolutional layers and two fully connected layers; see Figure 2 and Table 1.

| Symbol | Layer | Content and explanation | Dimensions | No. of parameters |

| INPUT | - | design matrix | - | |

| C1 | convolutions | feature maps | ||

| C2 | convolutions | feature maps | ||

| F1 | full connection | response factor loadings | ||

| OUTPUT | full connection | output prediction |

To be specific, each column in is a convolution and the first layer outputs feature maps. Similarly, represents the convolution with kernel size and channels. These two convolutional layers work as an encoder to extract the -dimensional representation of the input for predicting . Next, a full connection from predictor features to output features with weights is followed. Finally, a fully connected layer serves as a decoder to ouputs with weights .

The neural network architectures corresponding to the low-rank estimator and ordinary least squares estimator without low-dimensional structure are the one-hidden-layer MLP with a bottleneck layer of size and the zero-hidden-layer fully connected network, respectively.

The CNN representation in Figure 2 has a compact architecture with parameters, which is the same as that of the Tucker decomposition. Compared with the benchmark models, namely the one-hidden-layer MLP (MLP-1) and zero-hidden-layer MLP (MLP-0), the introduced low-Tucker-rank structure increases the depth of the network while reduces the total number of weights. When the Tucker ranks are small, the total number of parameters in our network is much smaller than those of the benchmark networks, which are and , respectively.

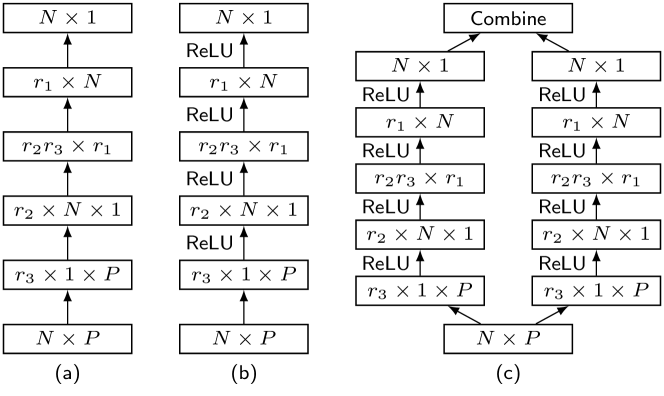

To capture the complicated and non-linear functional mapping between the prior inputs and future responses, non-linear activation functions, such as rectified linear unit (ReLU) or sigmoid function, can be added to each layer in the compact autoregressive network. Hence, the additional depth from transforming a low-Tucker-rank single layer to a multi-layer convolutional structure enables the network to better approximate the target function. The linear network without activation in the previous section can be called linear TAR net (LTAR).

3.2 Separable Convolutional Kernels

Separable convolutions have been extensively studied to replace or approximate large convolutional kernels by a series of smaller kernels. For example, this idea was explored in multiple iterations of the Inception blocks (Szegedy et al.,, 2015, 2016, 2017) to decompose a convolutional layer with a kernel into that with and kernels.

Tensor decomposition is an effective method to obtain separable kernels. In our TAR net, these two convolutional layers extract the information from inputs along the column-wise direction and row-wise direction separately. Compared with the low-rank matrix structure, the additional decomposition in the Tucker decomposition along the second and third modes in fact segregates the full-sized convolutional kernel into pairs of separable kernels.

3.3 Two-Lane Network

If no activation function is added, the first two row-wise and column-wise convolutional layers are exchangeable. However, exchanging these two layers with nonlinear activation functions can result in different nonlinear approximation and physical interpretation.

For the general case where we have no clear preference on the order of these two layers, we consider a two-lane network variant, called TAR-2 network, by introducing both structures into our model in parallel followed by an average pooling to enhance the flexibility; see Figure 3.

3.4 Implementation

3.4.1 Details

We implement our framework on PyTorch, and the Mean Squared Error (MSE) is the target loss function. The gradient descent method is employed for the optimization with learning rate and momentum being and , respectively. If the loss function drops by less than , the procedure is then deemed to have reached convergence.

3.4.2 Hyperparameter tuning

In the TAR net, the sequential dependence range and the Tucker ranks , and are prespecified hyperparameters. Since cross-validation cannot be applied to sequence modeling, we suggest tuning hyperparameters by grid search and rolling forecasting performance.

4 Experiments

This section first performs analysis on two synthetic datasets to verify the sample complexity established in Theorem 3 and to demonstrate the capability of TAR nets in nonlinear functional approximation. A US macroeconomic dataset Koop, (2013) is then analyzed by the TAR-2 and TAR nets, together with their linear counterparts. For the sake of comparison, some benchmark networks, including MLP-0, MLP-1, Recurrent Neural Network (RNN) and Long Short-Term Memory (LSTM), are also applied to the dataset.

4.1 Numerical Analysis for Sample Complexity

4.1.1 Settings

In TAR net or the low-Tucker-rank framework (6), the hyperparameters, and , are of significantly smaller magnitude than or , and are equally set to or . As sample complexity is of prime interest rather than the range of sequential dependence, we let equal to or . For each combination of , we consider and , and the sample size is chosen such that .

4.1.2 Data generation

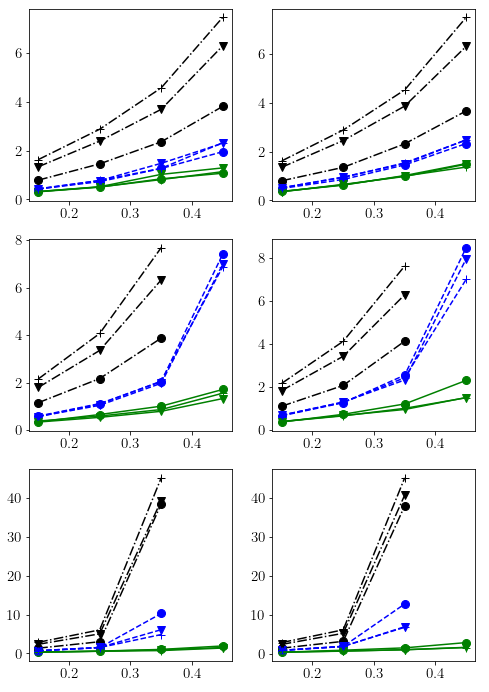

We first generate a core tensor with entries being independent standard normal random variables, and then rescale it such that the largest singular value of is . For each , the leading singular vectors of random standard Gaussian matrices are used to form . The weight tensor can thereby be reconstructed, and it is further rescaled to satisfy Condition 1. We generate sequences with identical . The first simulated data points at each sequence are discarded to alleviate the influence of the initial values. We apply the MLP-0, MLP-1 and LTAR to the synthetic dataset. The averaged estimation errors for the corresponding OLS, LR, and LTR estimators are presented in Figure 4.

4.1.3 Results

The -axis in Figure 4 represents the ratio of , and the -axis represents the averaged estimation error in Frobenius norm. Along each line, as is set to be fixed, we obtain different points by readjusting the sample size . Roughly speaking, regardless of the models and parameter settings, estimation error increases with varying rates as the sample size decreases. The rates for OLS rapidly become explosive, followed by LR, whereas LTR remains approximately linear, which is consistent with our findings at Theorem 3.

Further observation reveals that the increase in predominantly accelerates the rates for OLS and LR, but appears to have insignificant influence on the estimation error from LTR.

For the case with , instability of the estimation error manifests itself in LR under insufficient sample size, say when is as large as . This further provides the rationale for dimension reduction along sequential order. When , the solution is not unique for both OLS and LR, and consequently, these points are not shown in the figure.

4.2 Numerical Analysis for Nonlinear Approximation

4.2.1 Settings

The target of this experiment is to compare the expressiveness of LTAR, TAR and TAR-2 nets. The conjecture is that, regardless of the data generating process, TAR-2 and TAR nets under the same hyperparameter settings as the LTAR net would have an elevated ability to capture nonlinear features. We set , and have also tried several other combinations. Similar findings can be observed, and the results are hence omitted here.

4.2.2 Data generation

Two data generating processes are considered to create sequences with either strictly linear or highly nonlinear features in the embedding feature space. We refer to them as L-DGP and NL-DGP, respectively. L-DGP is achieved by randomly assigning weights to LTAR layers and producing a recursive sequence with a given initial input matrix. NL-DGP is attained through imposing a nonlinear functional transformation to the low-rank hidden layer of an MLP. In detail, we first transformed a matrix to a low-rank encoder. Then, we applied a nonlinear mapping to the encoder, before going through a fully connected layer to retrieve an output of size .

4.2.3 Implementation & Evaluation

In this experiment, we use L-DGP and NL-DGP to separately generate 200 data sequences which are fitted by TAR-2, TAR and LTAR nets. The sequence lengths are chosen to be either or . For each sequence, the last data point is retained as a single test point, whereas the rest are used in model training. We adopt three evaluation metrics, namely, the averaged norm between prediction and true value, the standard Root-Mean-Square Error (RMSE), and Mean Absolute Error (MAE). The results are given in Table 2.

4.2.4 Results

When the data generating process is linear (L-DGP), the LTAR net reasonably excels in comparison to the other two, obtaining the smallest -norm, RMSE and MAP. TAR-2 yields poorer results for a small sample size of due to possible overparametrization. However, its elevated expressiveness leads it to outperform TAR when .

For nonlinear data generating process (NL-DGP), as we expect, the TAR-2 and TAR nets with nonlinear structure outperform the LTAR net. In the meanwhile, as the exchangeability of latent features holds, the TAR-2 net seems to suffer from model redundancy and thereby performs worse than the TAR net.

4.3 US Macroeconomic Dataset

4.3.1 Dataset

We use the dataset provided in Koop, (2013) with US macroeconomic variables. They cover various aspects of financial and industrial activities, including consumption, production indices, stock market indicators and the interest rates. The data series are taken quarterly from 1959 to 2007 with a total of observed time points. In the preprocessing step, the series were transformed to be stationary before being standardized to have zero mean and unit variance; details see the supplemental material.

| DGP | Network | -norm | RMSE | MAP | |

| L-DGP | 100 | TAR-2 | 5.5060 | 1.1238 | 0.8865 |

| TAR | 5.4289 | 1.0998 | 0.8702 | ||

| LTAR | 5.1378 | 1.0388 | 0.8265 | ||

| 500 | TAR-2 | 5.1836 | 1.0493 | 0.8369 | |

| TAR | 5.2241 | 1.0585 | 0.8436 | ||

| LTAR | 4.9338 | 0.9972 | 0.7936 | ||

| NL-DGP | 100 | TAR-2 | 5.2731 | 1.0703 | 0.8579 |

| TAR | 5.2710 | 1.0712 | 0.8510 | ||

| LTAR | 5.3161 | 1.0738 | 0.8573 | ||

| 500 | TAR-2 | 5.0084 | 1.0111 | 0.8062 | |

| TAR | 5.0036 | 1.0110 | 0.8060 | ||

| LTAR | 5.0144 | 1.0126 | 0.8087 |

4.3.2 Models for comparison

For the sake of comparison, besides the proposed models, TAR-2, TAR and LTAR, we also consider four other commonly used networks in the literature with well-tuned hyperparameters. The first two are the previously mentioned MLP-0 and MLP-1. The remaining two are RNN and LSTM, which are two traditional sequence modeling frameworks. RNN implies an autoregressive moving average framework and can transmit extra useful information through the hidden layers. It is hence expected to outperform an autoregressive network. LSTM may be more susceptible to small sample size. As a result, RNN and LSTM with the optimal tuning hyperparameter serve as our benchmarks.

4.3.3 Implementation

Following the settings in Koop, (2013), we set . Consistently, the sequence length in both RNN and LSTM is fixed to be , and we consider only one hidden layer. The number of neurons in the hidden layer is treated as a tunable hyperparameter. To be on an equal footing with our model, the size of the hidden layer in MLP-1 is set to . We further set , and . The bias terms are added back to the TAR-2, TAR and LTAR nets for expansion of the model space.

The dataset is segregated into two subsets: the first 104 time points of each series are used as the training samples with an effective sample size of 100, whereas the rolling forecast procedure is applied to the rest 90 test samples. For each network, one-step-ahead forecasting is carried out in a recursive fashion. In other words, the trained network predicts one future step, and immediately includes the new observation for the prediction of the next step. The averaged -norm, RMSE and MAP are used as the evaluation criteria.

| Network | -norm | RMSE | MAE |

| MLP-0 | 11.126 | 1.8867 | 1.3804 |

| MLP-1 | 7.8444 | 1.3462 | 1.0183 |

| RNN | 5.5751 | 0.9217 | 0.7064 |

| LSTM | 5.8274 | 0.9816 | 0.7370 |

| LTAR | 5.5257 | 0.9292 | 0.6857 |

| TAR | 5.4675 | 0.9104 | 0.6828 |

| TAR-2 | 5.4287 | 0.8958 | 0.6758 |

4.3.4 Results

From Table 3, the proposed TAR-2 and TAR nets rank top two in terms of one-step-ahead rolling forecast performance, exceeding the fine-tuned RNN model with the size of the hidden layer equal to one. The two-lane network TAR-2 clearly outperforms the one-lane network TAR emphasizing its ability to capture non-exchangeable latent features. According to our experiments, the performance of both RNN and LSTM deteriorates as the dimension of the hidden layer increases, which indicates that overfitting is a serious issue for these two predominate sequence modeling techniques. Figure 5 plots the forecast values against the true values of the variables “SEYGT10” (the spread between 10-yrs and 3-mths treasury bill rates) for the TAR-2 net and the RNN model. It can be seen that TAR-2 shows strength in capturing the pattern of peaks and troughs, and hence resembles the truth more closely.

![[Uncaptioned image]](/html/1909.03830/assets/Real2.png)

5 Conclusion and Discussion

This paper rearranges the weights of an autoregressive network into a tensor, and then makes use of the Tucker decomposition to introduce a low-dimensional structure. A compact autoregressive network is hence proposed to handle the sequences with long-range dependence. Its sample complexity is also studied theoretically. The proposed network can achieve better prediction performance on a macroeconomic dataset than some state-of-the-art methods including RNN and LSTM.

For future research, this work can be improved in three directions. First, our sample complexity analysis is limited to linear models, and it is desirable to extend the analysis to networks with nonlinear activation functions. Secondly, the dilated convolution, proposed by WaveNet Van den Oord et al., 2016a , can reduce the convolutional kernel size along the sequential order, and hence can efficiently access the long-range historical inputs. This structure can be easily incorporated into our framework to further compress the network. Finally, a deeper autoregressive network can be constructed by adding more layers into the current network to enhance the expressiveness of nonlinearity.

Appendix A Technical Proofs of Theorems 1 and 2

A.1 Proofs of Theorems

We first prove the statistical convergence rate for and denote it as for simplicity. The main ideas of the proof come from Raskutti et al., (2019).

Denote , then by the optimality of the LTR estimator,

where denotes the tensor outer product.

Since the Tucker ranks of both and are , the Tucker ranks of are at most . Denote the set of tensor . Then, we have

Given the restricted strong convexity condition, namely , we can obtain an upper bound,

Since is a strictly-stationary VAR process, we can easily check that it is a -mixing process. Denote the unconditional covariance matrix of as . Let and be the corresponding matrix from . By spectral measure (Basu and Michailidis,, 2015, Proposition 2.3), the largest eigenvalue of is upper bounded, namely .

Therefore, conditioning on all ’s, we have

Denote and denote as the -th row of . Further, if we condition on , since is a sequence of iid random vectors with mean zero and covariance , for any ,

where is a random tensor with i.i.d. standard normal entries.

Since is a sequence of -mixing random variables with mean zero and unit variance, by Lemma 3, for each , there exists some constant and , such that

Taking a union bound, if , we have

Therefore, we have

For any fixed , it can be checked that . Hence, there exists a constant such that for any

Consider a -net for . Then, for any , there exists a such that . Note that the multilinear ranks of are at most . As shown in Figure 6, we can split the higher order singular value decomposition (HOSVD) of into 8 parts such that such that for and , and for any .

Note that

Since each , .

Since , by Cauchy inequality, . Hence, we have

In other words,

Therefore, we have

By Lemma 1, . We can take and , and then obtain that

Finally, by Lemma 2, the restricted convexity condition holds for , with probability at least , which concludes the proof of .

Similarly, we can obtain the error upper bound for by replacing the covering number of low-Tucker-rank tensors to that of low-rank matrices, and the covering number of low-rank matrices are investigated by Candes and Plan, (2011).

A.2 Three Lemmas Used in the Proofs of Theorems

Lemma 1.

(Covering number of low-multilinear-rank tensors) The -covering number of the set is

Proof.

The proof hinges on the covering number for the low-rank matrix studied by Candes and Plan, (2011).

Recall the HOSVD , where and each is an orthonormal matrix. We construct an -net for by covering the set of and all ’s. We take to be an -net for with . Next, let . To cover , it is beneficial to use the norm, defined as

where denotes the th column of . Let . One can easily check that , and thus an -net for obeying .

Denote and we have . It suffices to show that for any , there exists a such that

For any fixed , decompose it by HOSVD as . Then, there exist with , satisfying that and . This gives

Since each is an orthonormal matrix, the first term is . For the second term, by the all-orthogonal property of and the orthonormal property of and ,

Similarly, we can obtain the upper bound for the third and the last term, and thus show that .

∎

Lemma 2.

(Restricted strong convexity) Suppose that , with probability at least ,

where .

Proof.

Denote , , and . Note that

Thus, the objective is to show is lower bounded away from zero.

Since and by spectral measure, we have . Then, it suffices to show that does not deviate much from zero for any .

By Proposition 2.4 in Basu and Michailidis, (2015), for any single vector such that , any ,

Then, we can extend this deviation bound to the union bound on the set . By Lemma 1, for , we can construct a -net of cardinality at most and approximate the deviation on this net, which yields that for some ,

Then, we can set , and then we obtain that for ,

Therefore,

∎

The following Lemma is the concentration of -mixing subgaussian random variables in Wong et al., (2019).

Lemma 3.

Let consist of a sequence of mean-zero random variables with exponentially decaying -mixing coefficients, i.e. there exists some constant such that , . Let be such that . Choose a block length and let . We have, for any ,

Appendix B Real Dataset Information

The US macroeconomics dataset is provided by Koop, (2013). The dataset includes a list of 40 quarterly macroeconomic variables of the United States, from Q1-1959 to Q4-2007. All series are transformed to be stationary as in Table 1, standardized to have zero mean and unit variance, and seasonally adjusted except for financial variables. These forty macroeconomic variables capture many aspects of the economy (e.g. production, price, interest rate, consumption, labor, stock markets and exchange rates) and many empirical econometric literature have applied VAR model to these data for structural analysis and forecasting (Koop,, 2013).

| Short name | Code | Description | Short name | Code | Description |

| GDP251 | 5 | Real GDP, quantity index (2000=100) | SEYGT10 | 1 | Spread btwn 10-yr and 3-mth T-bill rates |

| CPIAUCSL | 6 | CPI all items | HHSNTN | 2 | Univ of Mich index of consumer expectations |

| FYFF | 2 | Interest rate: federal funds (% per annum) | PMI | 1 | Purchasing managers’ index |

| PSCCOMR | 5 | Real spot market price index: all commodities | PMDEL | 1 | NAPM vendor deliveries index (%) |

| FMRNBA | 3 | Depository inst reserves: nonborrowed (mil$) | PMCP | 1 | NAPM commodity price index (%) |

| FMRRA | 6 | Depository inst reserves: total (mil$) | GDP256 | 5 | Real gross private domestic investment |

| FM2 | 6 | Money stock: M2 (bil$) | LBOUT | 5 | Output per hr: all persons, business sec |

| GDP252 | 5 | Real Personal Cons. Exp., Quantity Index | PMNV | 1 | NAPM inventories index (%) |

| IPS10 | 5 | Industrial production index: total | GDP263 | 5 | Real exports |

| UTL11 | 1 | Capacity utilization: manufacturing (SIC) | GDP264 | 5 | Real imports |

| LHUR | 2 | Unemp. rate: All workers, 16 and over (%) | GDP 265 | 5 | Real govt cons expenditures & gross investment |

| HSFR | 4 | Housing starts: Total (thousands) | LBMNU | 5 | Hrs of all persons: nonfarm business sector |

| PWFSA | 6 | Producer price index: finished goods | PMNO | 1 | NAPM new orders index (%) |

| GDP273 | 6 | Personal Consumption Exp.: price index | CCINRV | 6 | Consumer credit outstanding: nonrevolving |

| CES275R | 5 | Real avg hrly earnings, non-farm prod. workers | BUSLOANS | 6 | Comm. and industrial loans at all comm. banks |

| FM1 | 6 | Money stock: M1 (bil$) | PMP | 1 | NAPM production index (%) |

| FSPIN | 5 | S&P’s common stock price index: industrials | GDP276_1 | 6 | Housing price index |

| FYGT10 | 2 | Interest rate: US treasury const. mat., 10-yr | GDP270 | 5 | Real final sales to domestic purchasers |

| EXRUS | 5 | US effective exchange rate: index number | GDP253 | 5 | Real personal cons expenditures: durable goods |

| CES002 | 5 | Employees, nonfarm: total private | LHEL | 2 | Index of help-wanted ads in newspapers |

References

- Basu and Michailidis, (2015) Basu, S. and Michailidis, G. (2015). Regularized estimation in sparse high-dimensional time series models. The Annals of Statistics, 43(4):1535–1567.

- Candes and Plan, (2011) Candes, E. J. and Plan, Y. (2011). Tight oracle inequalities for low-rank matrix recovery from a minimal number of noisy random measurements. IEEE Transactions on Information Theory, 57(4):2342–2359.

- Cho et al., (2014) Cho, K., Van Merriënboer, B., Gulcehre, C., Bahdanau, D., Bougares, F., Schwenk, H., and Bengio, Y. (2014). Learning phrase representations using rnn encoder-decoder for statistical machine translation. In Empirical Methods in Natural Language Processing.

- Denil et al., (2013) Denil, M., Shakibi, B., Dinh, L., De Freitas, N., et al. (2013). Predicting parameters in deep learning. In Advances in Neural Information Processing Systems, pages 2148–2156.

- Du et al., (2018) Du, S. S., Wang, Y., Zhai, X., Balakrishnan, S., Salakhutdinov, R. R., and Singh, A. (2018). How many samples are needed to estimate a convolutional neural network? In Advances in Neural Information Processing Systems, pages 373–383.

- Fontaine et al., (1997) Fontaine, V., Ris, C., and Boite, J.-M. (1997). Nonlinear discriminant analysis for improved speech recognition. In Fifth European Conference on Speech Communication and Technology.

- Goodfellow et al., (2016) Goodfellow, I., Bengio, Y., and Courville, A. (2016). Deep learning. MIT press.

- Grézl et al., (2007) Grézl, F., Karafiát, M., Kontár, S., and Cernocky, J. (2007). Probabilistic and bottle-neck features for lvcsr of meetings. In 2007 IEEE International Conference on Acoustics, Speech and Signal Processing-ICASSP’07, volume 4, pages IV–757. IEEE.

- Hinton and Salakhutdinov, (2006) Hinton, G. E. and Salakhutdinov, R. R. (2006). Reducing the dimensionality of data with neural networks. Science, 313(5786):504–507.

- Hochreiter and Schmidhuber, (1997) Hochreiter, S. and Schmidhuber, J. (1997). Long short-term memory. Neural Computation, 9(8):1735–1780.

- Jaderberg et al., (2014) Jaderberg, M., Vedaldi, A., and Zisserman, A. (2014). Speeding up convolutional neural networks with low rank expansions. In Proceedings of the British Machine Vision Conference. BMVA Press.

- Kim et al., (2016) Kim, Y.-D., Park, E., Yoo, S., Choi, T., Yang, L., and Shin, D. (2016). Compression of deep convolutional neural networks for fast and low power mobile applications. In International Conference on Learning Representations.

- Kolda and Bader, (2009) Kolda, T. G. and Bader, B. W. (2009). Tensor decompositions and applications. SIAM Review, 51(3):455–500.

- Koop, (2013) Koop, G. M. (2013). Forecasting with medium and large bayesian vars. Journal of Applied Econometrics, 28(2):177–203.

- Lebedev et al., (2014) Lebedev, V., Ganin, Y., Rakhuba, M., Oseledets, I., and Lempitsky, V. (2014). Speeding-up convolutional neural networks using fine-tuned cp-decomposition. arXiv preprint arXiv:1412.6553.

- Novikov et al., (2015) Novikov, A., Podoprikhin, D., Osokin, A., and Vetrov, D. P. (2015). Tensorizing neural networks. In Advances in Neural Information Processing Systems, pages 442–450.

- Pan et al., (2019) Pan, Y., Xu, J., Wang, M., Ye, J., Wang, F., Bai, K., and Xu, Z. (2019). Compressing recurrent neural networks with tensor ring for action recognition. In Proceedings of the AAAI Conference on Artificial Intelligence, volume 33, pages 4683–4690.

- Raskutti et al., (2019) Raskutti, G., Yuan, M., and Chen, H. (2019). Convex regularization for high-dimensional multi-response tensor regression. The Annals of Statistics, page to appear.

- Szegedy et al., (2017) Szegedy, C., Ioffe, S., Vanhoucke, V., and Alemi, A. A. (2017). Inception-v4, inception-resnet and the impact of residual connections on learning. In Thirty-First AAAI Conference on Artificial Intelligence.

- Szegedy et al., (2015) Szegedy, C., Liu, W., Jia, Y., Sermanet, P., Reed, S., Anguelov, D., Erhan, D., Vanhoucke, V., and Rabinovich, A. (2015). Going deeper with convolutions. In Proceedings of the IEEE Conference on Computer Vision and Pattern Recognition, pages 1–9.

- Szegedy et al., (2016) Szegedy, C., Vanhoucke, V., Ioffe, S., Shlens, J., and Wojna, Z. (2016). Rethinking the inception architecture for computer vision. In Proceedings of the IEEE Conference on Computer Vision and Pattern Recognition, pages 2818–2826.

- Tjandra et al., (2018) Tjandra, A., Sakti, S., and Nakamura, S. (2018). Tensor decomposition for compressing recurrent neural network. In 2018 International Joint Conference on Neural Networks, pages 1–8.

- Tucker, (1966) Tucker, L. R. (1966). Some mathematical notes on three-mode factor analysis. Psychometrika, 31(3):279–311.

- (24) Van den Oord, A., Dieleman, S., Zen, H., Simonyan, K., Vinyals, O., Graves, A., Kalchbrenner, N., Senior, A., and Kavukcuoglu, K. (2016a). Wavenet: A generative model for raw audio. arXiv preprint arXiv:1609.03499.

- (25) Van den Oord, A., Kalchbrenner, N., Espeholt, L., Vinyals, O., Graves, A., et al. (2016b). Conditional image generation with pixelcnn decoders. In Advances in Neural Information Processing Systems, pages 4790–4798.

- Wong et al., (2019) Wong, K. C., Li, Z., and Tewari, A. (2019). Lasso guarantees for -mixing heavy tailed time series. The Annals of Statistics, page to appear.

- Ye et al., (2018) Ye, J., Wang, L., Li, G., Chen, D., Zhe, S., Chu, X., and Xu, Z. (2018). Learning compact recurrent neural networks with block-term tensor decomposition. In Proceedings of the IEEE Conference on Computer Vision and Pattern Recognition, pages 9378–9387.