Bias-Variance Games††thanks: This work was initiated during the Special Quarter on Data Science and Online Markets held in the spring of 2018 at Northwestern University when the fifth author was supported as a McCormick Advisory Council Visiting Associate Professor. The first, second, and fourth authors gratefully acknowledge the support of National Science Foundation award number 1718670. The first, third, and fourth authors gratefully acknowledge the support of National Science Foundation award number 1618502.

Abstract

Firms engaged in electronic commerce increasingly rely on predictive analytics via machine-learning algorithms to drive a wide array of managerial decisions. The tuning of many standard machine learning algorithms can be understood as trading off bias (i.e., accuracy) with variance (i.e., precision) in the algorithm’s predictions. The goal of this paper is to understand how competition between firms affects their strategic choice of such algorithms. To this end, we model the interaction of two firms choosing learning algorithms as a game and analyze its equilibria. Absent competition, players care only about the magnitude of predictive error and not its source. In contrast, our main result is that with competition, players prefer to incur error due to variance rather than due to bias, even at the cost of higher total error. In addition, we show that competition can have counterintuitive implications—for example, reducing the error incurred by a firm’s algorithm can be harmful to that firm—but we provide conditions under which such phenomena do not occur. In addition to our theoretical analysis, we also validate our insights by applying our metrics to several publicly available datasets.

1 Introduction

Firms that engage in electronic commerce increasingly rely on predictive analytics to drive a wide array of managerial decisions, ranging from product recommendations to customer targeting and pricing. Given data, perhaps from past consumer behavior, a firm facing a potential customer will use predictive models or learning algorithms (henceforth algorithms) to anticipate the customer’s future behavior and preferences, allowing the firm to better tailor its recommendation, targeting, and pricing decisions. In general, the success of such predictive analyses depends on the effectiveness of the algorithms used. Research on such algorithms has proliferated, and their capabilities have advanced incredibly over the past couple of decades.

The point of departure for this paper is the observation that, in many applications, firms that utilize predictive analytics do so in a competitive environment, and so the efficacy of a firm’s analytics depends not only on its own expertise and technology but also on that of its competitors. In this paper we address the question of how the competitive nature of the interaction affects a firm’s choice of algorithms. For example, while a particular algorithm may be best for a monopolistic firm targeting a customer, it may be suboptimal in a competitive environment. Furthermore, the optimal choice of algorithm in the competitive environment may depend on the competitors’ choices of algorithms.

For a concrete example, consider the increasingly popular box subscription companies that mail personalized monthly boxes of fashion, food, or other products to subscribers. The appeal of these companies lies in their high level of personalization, often achieved by machine learning algorithms (Sinha et al.,, 2016). Stitch Fix, for example, uses such algorithms to predict each subscriber’s fashion taste and sends a box matching this taste (Gaudin,, 2016). The better the fit, the more satisfied the subscriber, leading to greater customer acquisition and retention. Of course, Stitch Fix competes with other companies, such as Trunk Club, that also personalize their boxes using learning algorithms. Ultimately, the profitability of such a company will depend not only on how well it manages to predict a customer’s fashion taste, but also on the predictions of its competitors.

For a more general example, consider the so-called “Long Tail” marketplaces, which are characterized by huge numbers of goods that individually have low demand but that collectively make up substantial market share. One of the key drivers of Long Tail markets is the ability of firms to connect supply and demand, typically through machine learning algorithms that predict consumers’ tastes and match them to products (Anderson,, 2006). Often, many firms compete in the same Long Tail market, and in this case their success depends not only on their own ability to match goods to consumers, but also on the predictive ability of their competitors.

One useful way of analyzing algorithms’ predictive ability is by examining the different sources of error they incur. There are two general types of errors: a lack of accuracy—called bias—in which the predictions are not, on average, equal to the true value; and a lack of precision—called variance—in which the predictions are not clustered tightly around their average. The total error of an algorithm can be decomposed into these two kinds of error.

In practice, there are various ways to control the bias and variance of an algorithm. For example, one could allow the algorithm to consider more complex functions to map data onto predictions, such as deeper decision trees or regressions with higher degree functions, which result in lower bias but higher variance. Alternatively, a technique called regularization—intuitively, penalizing predictions that are less smooth—is often used to decrease variance at the expense of higher bias. Finally, increasing the amount of training data decreases variance. Algorithms that predict well are ones that control the tradeoff between bias and variance so as to minimize the total error, regardless of its source.

In this paper we aim to understand how competition affects the optimal way to trade off bias and variance. We show that, holding total error fixed, absent competition there is no preference for variance versus bias. In contrast, in competitive environments it is better to reduce bias at the expense of variance, even when this leads to higher total error. This result holds up under several natural theoretical models of predictive error and in an empirical study. Consequently, training an algorithm in isolation to minimize error does not lead to optimal parameter settings for algorithms in competitive environments. An implication of these results is that, in competitive environments, there is an added benefit to algorithms that consider more complex functions and an added cost to regularization.

Overview of model and results.

In this paper we model the interaction of two firms as a game, and analyze the game’s equilibria. Players’ actions are learning algorithms, functions that map feature vectors to predicted labels. Players’ payoffs depend both on the error of their chosen algorithm’s prediction—specifically, the squared distance between the true label and the algorithm’s predicted label—and on whether or not their algorithm’s prediction is better than that of their opponent. We view the game as consisting of three stages: First, in the ex ante stage, each player chooses an algorithm. Second, in the interim stage, a feature vector is realized, and each player’s chosen algorithm yields a distribution over predictions for this particular feature vector. Finally, in the ex post stage, predictions and payoffs are realized. Although players act only in the ex ante stage, most of our analysis focuses on understanding players’ preferences in the interim stage.

For the analysis of the interim stage, we suppose that the feature vector is fixed. We abstract away from the details of specific algorithms, and instead model an algorithm as a probability distribution over prediction errors. Thus, players’ actions correspond to probability distributions, and players’ action spaces—the sets of possible actions they can choose—correspond to families of probability distributions that range over biases and variances. A canonical example is the set of normal distributions with different means and standard deviations.

Our main theoretical result considers a two-player game where each player’s action space consists of normal distributions with the same total mean squared error—namely, they have the same total error but different biases and variances. Absent competition, a player would be indifferent among all these distributions. In contrast, we prove that, in the competitive scenario, each player would prefer error distributions with lower bias (and therefore higher variance), and that this holds regardless of the actual prediction made by the opponent. In game theoretic terms, minimal-bias is an ex post dominant strategy. This strong result persists in games with more than two players. It also implies that the unique Nash equilibrium of the game is the one in which each player chooses the distribution with minimal bias.

We then extend our analysis, and show that the preference for lower bias persists when the total error is not fixed. In particular, we consider a case where, absent competition, players are not indifferent between the various available combinations of bias and variance, but rather where there is some most-preferred distribution with nonzero bias that has minimal total error. Here we show that, under competition, players strictly prefer a distribution with lower bias than this most-preferred distribution, even though it has higher total error.

We supplement these theoretical results with numerical analyses that demonstrate the robustness of the theoretical findings. First, we numerically test the robustness of our insight on the strategic preference for reduced bias with non-normal families of distributions, such as Laplace, logistic, and uniform. Our insight persists for many of the variations, but, notably, it fails for uniform distributions. Second, we investigate the dependence of the results on the form of players’ payoff functions. In particular, we study variations in the benefit from winning relative to the cost of prediction errors. We find by numerical calculation that the ex post preference for lower bias fails to extend. However, we also find that minimal-bias remains a dominant strategy—that is, players prefer lower bias (and higher variance) for every choice of probability distribution by the opponent (although not for every realization of this distribution).

After establishing players’ preferences for lower bias in the interim stage, we next turn to the analysis of the ex ante stage. In this stage each player chooses an algorithm that, for each possible feature vector, will yield a distribution over total error with some bias and some variance. This general setting is substantially more complicated, as each potential algorithm may imply a different total error, bias, and variance for each feature vector. Nonetheless, we show that, under some assumptions, our insight on the preference for lower bias persists. We also theoretically, numerically, and empirically verify the assumptions necessary for this result, focusing on the particular learning algorithm of ridge regression—a variant of linear regression that allows for flexibility to control the bias-variance tradeoff using a regularization parameter.

Finally, we conduct an empirical study of our bias-variance game for a family of learning algorithms on benchmark datasets. In this study, players utilize a particular learning algorithm to make predictions, given a particular dataset.111We use the California housing prices data from the 1990 Census, a data set first utilized by Pace and Barry, (1997) and included in the Python Scikit-learn library. We also use data on wine quality, designed and utilized by Cortez et al., (2009). Specifically, the players use a ridge regression algorithm. When there is only one player we show that the optimal choice of regularization parameter—the parameter that controls the bias-variance tradeoff—is large, but when there are two players, payoffs increase as the parameter is lowered. In other words, in the latter scenario there is a preference for lower bias and higher variance. Thus, the algorithmic optimizations of the non-competitive and competitive settings are qualitatively distinct and result in quite different preferences with respect to the tradeoff between bias and variance.

To give some context for the theoretical results, we provide a few additional observations about algorithms in competitive situations. Counterintuitively, we show that there are families of distributions and opponent choices for which a player prefers a distribution with higher bias (respectively, higher variance) even while holding variance (respectively, bias) fixed. Nonetheless, we also show that higher bias (with variance fixed) is not beneficial for natural families of distributions, such as normal and Laplace. Moreover, for normal distributions, our main theoretical result (described above) strengthens this conclusion on the harmfulness of higher bias by showing that decreasing bias is beneficial even at the expense of increased variance (holding the total error fixed). The above counterintuitive observation—the possibility that increasing bias can be beneficial—highlights the obstacles that our main theoretical analysis must overcome.

Related literature.

The analysis of strategic interactions that involve machine learning algorithms is a newly burgeoning area of study in both economics and computer science. For example, Eliaz and Spiegler, (2019) study the interaction of a rational agent and a learning algorithm, and consider the question of whether the agent has an incentive to truthfully report her information to the algorithm. Liang, (2019) and Olea et al., (2019) study scenarios in which there are multiple algorithms that compete with one another. Liang, (2019) considers games of incomplete information in which the players have data and use algorithms to derive their beliefs. Olea et al., (2019) study a game between agents competing to predict a common variable, and where agents obtain the same data but differ in the algorithms they utilize for prediction. In all these papers, the algorithms under consideration are fixed exogenously. Our paper, in contrast, focuses on the strategic choice of algorithms in competitive environments.

On the computer science side, our study is related to the “dueling algorithms” framework of Immorlica et al., (2011). Within this framework, Ben-Porat and Tennenholtz, (2019), building on Ben-Porat and Tennenholtz, (2017), study the problem of multiple learners selecting a hypothesis, i.e., a function mapping the features to a prediction, from the same hypothesis class on the same data set. They work within the PAC-learning framework of Valiant, (1984), and consider equilibria in the game where, for each point in the dataset, a payoff of one is split evenly between all players whose predictions are within a given error tolerance. A key point of difference between this setup and ours is that they consider competition between specific algorithms, such as linear regressors, and study the questions of whether equilibria exist and can be learned. On the other hand, we study the general tradeoff between bias and variance in the equilibrium choice of algorithms.

Organization.

Section 2 introduces the general framework and describes the ex ante and interim stages, the one- and two-player games that we study, and some basic properties. Section 3 considers the one-player intuition that reducing bias or reducing variance is always beneficial, when everything else is held fixed, in the two-player game. Counterintuitively, there are two-player scenarios where a player would want to increase bias or variance. On the other hand, for normally-distributed errors, reducing bias to zero is beneficial. Section 4 contains our main analysis of the two-player interim game. For normally-distributed error, we show that there is an ex post preference for lowering bias at the expense of variance, we argue that the natural ridge regression algorithm indeed has normally-distributed error, and we present simulation results for other distributions of error and a variety of utility functions. In Section 5 we then turn to the ex ante game, where we show that the insight on the preference for variance over bias persists. In Section 6 we consider an empirical version of the game played on a standard benchmark data sets with ridge regression, and show that qualitative conclusions of our theoretical analysis continue to hold. Finally, Section 7 concludes with some discussion.

2 Model and Preliminaries

We begin in Section 2.1 with a brief overview of the general framework for statistical decision theory, including a formalization of the ex ante and interim stages. This is followed by a description of the model for the interim stage game in Section 2.2. Since most of our analysis is about this stage, we defer the formalization of the ex ante stage game to Section 5.

2.1 The General Framework

We begin by sketching a general framework of statistical decision theory, which is our point of departure. For more details and references see Friedman et al., (2001).

There is a prior distribution over pairs , where each is a feature vector and each is a label. A typical example is that is linear plus unbiased noise, namely

where the are independent random variables with and , and where is a -dimensional vectors of fixed but unknown parameters.

A learning algorithm takes training data as input, and produces an estimator as output. Given a new point , the estimator predicts that the corresponding value of is .

Define the loss of a learning algorithm at feature vector as

Note that the loss is random—it depends on both the randomness in and the randomness inherent in .

The risk function of a learning algorithm at is

where the expectation is taken over both the randomness in that produced and the randomness in (but note that is fixed).

A well-known result is that when the loss is defined as above (squared-loss), then the risk can be decomposed into bias and variance:

where is the bias of the estimator at , the second term is the variance of the estimator (computed with respect to the randomness of ) at , and the third term is the irreducible error.

Ideally, we would like our learning algorithm to have minimal risk for all ’s. However, this is generally not possible. Instead, one way of identifying a good algorithm is to find one that minimizes the Bayes risk

which is the expected value of the risk with respect to the distribution over feature vectors .

Now, in practice we may not know the distribution over ’s, and in this case a common approach is to consider the empirical risk

of an estimator. Minimizing the empirical risk is not helpful, since one could always choose for which when , and otherwise. Common ways to get around this problem are (i) to limit the class of functions from which is chosen, and (ii) to find an estimator that minimizes the regularized empirical risk

Here, is the regularization parameter and is some penalty function. For example, in ridge regression, which we will use as a running example throughout the paper, the goal is to find a linear estimator for which is minimal.

In regularized empirical risk minimization, there are various ways to choose the regularization parameter . The goal is to choose so that the Bayes risk of the resulting estimator is minimal. Typically, modifying affects the bias and variance of an estimator. For example, in ridge regression, increasing decreases the variance and increases the bias of the chosen estimator. At the optimal , the tradeoff between the bias and variance of the chosen estimator is such that its Bayes risk is minimal.222In practice, finding such a is often done using cross-validation (see, e.g., Friedman et al.,, 2001).

The standard framework can be viewed as consisting of three stages: (i) in the ex ante stage, the estimator is chosen; (ii) in the interim stage, the feature vector and its label are realized (although the latter remains unknown); and (iii) in the ex post stage, the estimate is produced.

2.2 The Interim Game

In most of our analysis we will examine the interim stage, and so we will assume that and are fixed (and the latter unknown). Any choice of algorithm implies a distribution over predictions about the value of , and so a distribution over the error in prediction, . In our analysis here we will abstract away from the particular algorithm, and will only be concerned with the algorithm’s error in prediction.

We will focus on a standard measure of error, namely, mean squared error. Thus, if the predictive error of an algorithm is a number , then the squared error is . The best algorithm is one with predictive error of 0.

This paper is concerned with players’ choices of algorithms. In our abstraction for the interim game we will thus let each player choose a distribution over errors, each representing the distribution over the error in predicting by some algorithm. (Looking ahead, when we describe the ex ante game in Section 5, players will actually be choosing regularization parameters of certain algorithms, which indirectly imply various distributions over error.) We will suppose that players choose from a class of distributions, as follows. Fix a random variable with mean 0 and standard deviation 1. A common choice for will be normal, a choice we motivate in Section 4.3, but we can also consider uniform, triangle, Laplace, and other distributions. Players will then choose a distribution from a class made up of shifts and spreads of . A typical example will be the class

the set of distributions whose squared-bias plus variance is at least 1 (which means their total squared error is at least 1). Each element of this class yields a different distribution over predictive error, and represents a different algorithm whose error has the corresponding distribution.

Some discussion of this modeling assumption is warranted. The class of distributions represents the error distributions of all algorithms available to a player. In particular, this precludes the possibility that a player chooses an algorithm, observes the realized prediction, and then uses some alteration of that prediction. For a concrete example of what this implies, consider the distribution with bias and variance , and observe that above. Then our assumption precludes the possibility that the player takes the realization of and subtracts 1 from it, yielding a perfect estimator.

To understand why this assumption is reasonable in our context, recall that the choice of algorithms is actually made in the ex ante stage, before a specific is realized. In the context of regularized empirical risk minimization, the optimal estimator minimizes the Bayes risk, but this does not imply that it minimizes the risk for every realized . Making modifications to , such as subtracting 1 from it, may lower the risk for certain ’s, but in expectation will be harmful since is already optimal.

In our model, the algorithm chosen in the ex ante stage will yield different error distributions for different ’s. And while for some ’s it may be beneficial to take the realization of the algorithm and subtract 1 from it, for other ’s this same modification will be harmful. Furthermore, as will be formalized in Section 5, eventually the algorithm will be chosen so as to maximize utility, in expectation over all ’s. And if subtracting 1 from a particular algorithm’s realization is beneficial, then this algorithm does not maximize utility.

2.2.1 One player

As a benchmark, consider a setting in which there is only one player, and suppose that she chooses an error distribution . On realization (that is, a prediction with predictive error ), let the player’s utility be : a benefit of 1 minus her squared error. This utility function captures the idea that the player obtains positive utility from making a perfect prediction (the benefit of 1), but that this utility decreases with the squared error (the loss of ). In the box subscription company example from the introduction, the benefit represents future profits from a particular customer, whereas the loss accounts for the lack of customer retention in case of inaccurate taste predictions. Note that the total utility could be negative; in the example this would represent a firm’s failure to recoup the costs of an initial loss leader or promotion. We focus on this utility function for our theoretical analysis, but in Section 4.4 we argue that our results are robust to other specifications of the utility function, and in particular to ones where the chance of a negative payoff is negligible.

Given the utility function , a player’s expected utility from is . The following is a simple observation:

Claim 2.1.

If , where is a random variable with mean 0 and variance 1, then .

Proof.

is a random variable with variance and expected value . Since , it follows that . Thus, . ∎

This observation implies three corollaries, formalized below. First, for fixed bias, the player prefers minimal variance. Similarly, for fixed variance, the player prefers minimal bias. Finally, the player is indifferent between distributions that have the same bias squared plus variance. Although these corollaries are straightforward, in Section 3 we will show that, without further assumptions, none of them hold in the competitive setting.

Corollary 2.2.

For any , if , then the player prefers to .

Corollary 2.3.

For any , if , then the player prefers to .

Corollary 2.4.

If , , and , then the player is indifferent between and .

Individual rationality.

An additional definition that will be useful is that of individual rationality. Intuitively, a distribution is individually rational if a player derives non-negative utility from choosing it. Formally:

Definition 2.1.

A distribution satisfies individual rationality (IR) if .

A simple observation that follows from 2.1 is that is IR if and only if .

2.2.2 Two players

Recall that our goal is to analyze the effect of competition on firms’ choices of learning algorithms. As described in the introduction, we will model this as a game, and we call this game the Bias-Variance Game. In this game, each of two players simultaneously chooses an error distribution. Prediction errors are realized, and the player with lower prediction error, say , obtains utility , just like the one-player case. The player with higher prediction error obtains utility 0.

This specification of utilities, as well as variants that we discuss in Section 4.4, capture the main competitive force we wish to analyze: the desire of a player both to minimize error (this is the term), and to obtain lower error than her competitor (this is the benefit of 1 from winning).

In our notation, when discussing player , we will denote by the identity of the other player. A formal description of the game follows:

Definition 2.2 (The Bias-Variance Game).

Given two classes of distributions, and , the two player bias-variance game proceeds as follows:

-

1.

Each player simultaneously chooses a distribution from .

-

2.

Each is realized as some .

-

3.

Each player obtains utility . That is, the player wins and obtains utility ; the other player, , loses and obtains utility .

In our theoretical analysis we will primarily consider bias-variance games where is a family of distributions in which the error of every is normalized to . In our numerical analysis in Section 4.4 we relax this restriction.

Individual rationality.

As in the one-player benchmark, we will be interested in player choices that are individually rational. A straightforward result is that individual rationality of the one-player setting implies individual rationality of the two-player setting, as the following proposition demonstrates:

Proposition 2.5.

Bias-variance games with distributions satisfying are individually rational: namely, expected payoffs in the game are non-negative.

Proof.

In the one-player setting player ’s expected payoff with realization is which satisfies individual rationality. Consider the two-player game where the other player has realization . When the other player’s realization is , the payoff of player is non-negative for all : for player wins and has non-negative payoff and for then player loses and has payoff 0. When the other player’s realization is , then player ’s distribution of payoffs in the two player game dominates his distribution of payoffs in the one-player setting (when player loses, instead of a negative payoff her payoff is zero). As the latter setting had non-negative expectation, so does the former. ∎

Solution concepts.

When there is a single player, the concept of optimality is straightforward. When there are more players, however, different actions may be better depending on the actions of other players. “Solutions” to games thus consist of finding strategies of players that satisfy different notions of equilibrium. For our main theoretical result on the preference of variance over bias we will utilize a very strong notion, namely that of ex post dominant strategies. A strategy is ex post dominant for player if it yields that player the highest utility regardless of the realized prediction of the opponent.

Definition 2.3.

A strategy is ex post dominant for player if for all and all realizations of player it holds that .

For our numerical and empirical results we will consider two weaker notions. The first, dominant strategies, requires that a strategy be optimal against any strategy of the opponent, but not necessarily against any realization of that strategy:

Definition 2.4.

A strategy is dominant for player if for all and all it holds that . If the inequality is strict for all , then is strictly dominant.

The second, pure Nash equilibrium, does not require that a strategy be optimal against any strategy of the opponent, but only against that player’s own Nash equilibrium strategy:

Definition 2.5.

A strategy profile is a pure Nash equilibrium if for each player and strategy it holds that .

Observe that if is ex post dominant, then it is also dominant. Furthermore, if and are dominant for players and , respectively, then is a pure Nash equilibrium. Finally, if and are strictly dominant then is the unique Nash equilibrium.

3 Reducing Bias or Variance, All Else Fixed

We begin our analysis by describing some counterintuitive implications of competition. In particular, we show that the simple corollaries from the one-player benchmark in Section 2.2.1 no longer hold, and that reducing bias (resp., variance) holding variance (resp., bias) fixed can be harmful.

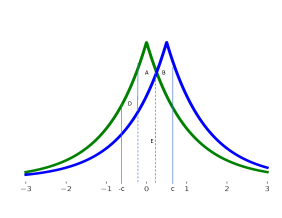

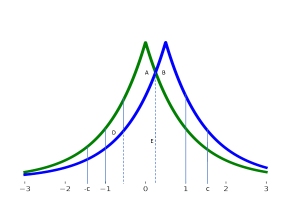

Example 3.1 (Reducing variance can be harmful; see Figure 1(a)).

Suppose player 2 plays the distribution , where is some small number, and player 1 plays the distribution . Player 1’s strategy is monotone and satisfies IR, and she obtains positive expected utility: Given that she wins, she is likely within of 0, and she wins with positive probability. However, if player 1 decreases her variance to 0, she will obtain utility close to 0, since she will hardly ever win (for small enough ).

Example 3.2 (Reducing bias can be harmful; see Figure 1(b)).

Player 2 plays the uniform distribution on the interval . For small enough this satisfies IR. Player 1 plays the uniform distribution on the interval . Again, for small enough this satisfies IR. Now consider a deviation by Player 1 to the interval , a deviation that reduces bias. This is harmful: Before the deviation, she never won when her realization was in . After the deviation, however, the only difference is the additional possibility of winning when her realization is in . But such victories are harmful, as they consist only of negative utilities.

Unlike Example 3.1, Example 3.2 is somewhat unnatural for our application to machine learning algorithms, in that the error distributions used are uniform. In Section 4.3 we argue that we should expect the distribution of the predictions of learning algorithms to be normal. Is there an example in which reducing bias is harmful, but where the class of distributions is more natural? The following two theorems state that there is not. The first considers a class of distributions that are single-peaked, monotone, and with convex tails,333A distribution is defined to have convex tails if its probability density function is convex and decreasing away from the mean. and the second considers normal distributions.

Theorem 3.1.

Let be monotonically increasing, convex on , and symmetric around 0. Let be IR (so as to satisfy ) and . Then for any realization of player .

The proof of this theorem and of Theorem 3.2, below, are given in Appendix A.

Note that the assumption that is IR is necessary. To see this, consider an that is not IR, for example one in which and . Suppose also that the opponent’s realization is . Observe that, in this case, is close to 0, since the probability that wins is small. However, decreasing to 0 leads to an for which : player nearly always wins, in which case her utility will be close to .

The assumption that is single-peaked (which follows from monotonicity and symmetry) is also necessary. To see this, consider a with two peaks, for example some infinitesimal perturbation of a Bernoulli distribution. The peaks are at and so that . Now, consider the case in which , and suppose . Then player wins whenever the realization is close to the lower peak, which happens with probability , and obtains utility close to 1 conditional on winning. Hence, . However, under the utility conditional on winning is close to 0, since the realized values will be near the peaks and .

One drawback of Theorem 3.1 is that it does not apply to normal distributions, since such distributions are not convex on . However, as we are particularly interested in normal distributions, we have a version of the theorem that applies specifically to them:

Theorem 3.2.

Let be normal; let and satisfy ; and let . Then for any realization of player .

4 Tradeoff Between Bias and Variance

Thus far, we have argued that simple observations that hold in the one-player case fail to extend to the competitive setting, and that reducing bias or variance may actually be harmful (holding all else fixed). We now turn to our main analysis, which considers the tradeoff between bias and variance: if there is only one player, she is indifferent between the two sources of error as long as their sum (or rather, the sum of bias squared and variance) is fixed. In this section, we show that in a competitive setting players are no longer indifferent, and, furthermore, that there is a clear preference for error incurred by variance over error incurred by bias.

We proceed as follows. In Section 4.1 we state our main result about the tradeoff between bias and variance in a two-player bias-variance game. We assume that , which ensures the individual rationality constraint is satisfied.444In fact, this assumption implies that the IR constraint binds in the one-player setting—that is, for all . This assumption is necessary for our analysis, but in Section 4.4 we show numerically that it is not necessary for our main result to hold. We fix the random variable to be normal, and show that for arbitrary realizations of the opponent player , reducing bias while increasing variance to is always strictly beneficial for player . That is, the minimal-bias strategy is ex post dominant. This result implies that the profile in which both players choose their minimal-bias strategy is the unique Nash equilibrium of the game. We also argue that our result extends to more than two players and to asymmetric strategy classes.

Next, in Section 4.2, we show that our insight on the preference for lower bias persists also when the total error is not constant across available error distributions. In particular, we suppose that for some convex function , and so there is some optimal distribution with minimal error. We show that, in the competitive setting, on the margin it is beneficial for players to choose a distribution with lower bias than this optimal distribution.

We then turn to the various assumptions in the analysis—namely, the normality assumption and the form of the utility functions. In Section 4.3, we motivate the focus on normal distributions by arguing formally that they are a natural distribution for error in machine learning contexts. Then, in Section 4.4, we consider distributions other than normal, as well as variations on the players’ utility functions. We perform numerical analyses on these variations, and demonstrate that our insight on the preference for lower bias is robust.

4.1 Preference for Lower Bias in Normal Distribution

In Theorem 3.2 we showed that reducing bias in normal distributions is beneficial if the variance is fixed. Here we give a “stronger” result: that as long as the total error is fixed, reducing bias (which increases variance) is beneficial. This is the main result of the paper.

Theorem 4.1.

Let be normal with mean 0 and variance 1, and let and , where . If then for any realization of player .

The proof of Theorem 4.1, given in Appendix B, is essentially a straightforward (albeit long and somewhat involved) calculation. The main idea is to consider the expected utility of a player as a function of her chosen bias and some realization of the opponent’s strategy. We calculate the derivative of this expected utility with respect to the bias, and show that it is negative. Thus, increasing bias (and so decreasing variance) leads to lower expected utility.

An immediate corollary of Theorem 4.1 is that the minimal-bias strategy is ex post strictly dominant.555For strictness we ignore the 0-measure event , for which all strategies are payoff equivalent.

Corollary 4.2.

Let be an exogenous lower bound on the choice of . Let be normal with mean 0 and variance 1. The minimal-bias strategy with mean and variance is ex post strictly dominant within the strategy class .

Many players and asymmetric strategies

Because no-bias is ex post dominant—and so player prefers minimal-bias for any realization of the opponent’s error—the result of Corollary 4.2 immediately extends to more than two players. Consider the bias-variance game with any number of players, and in which a player’s payoff is if her realization is lower than all others’ realizations, and 0 otherwise. Then, within the same strategy class as in Corollary 4.2, minimal-bias is an ex post dominant strategy. To see this, observe that player ’s utility can be maximized with the opponents’ errors summarized by ex post error . If agent has lower error then wins, otherwise loses. Because Corollary 4.2 implies that no-bias is dominant regardless of the other’s realization, it is, in particular, optimal given realization .

Another immediate implication of the result that minimal bias is optimal for player regardless of the realization of player ’s strategy is that ’s strategy class could be different from ’s—for example, it could include normal distributions with a different bias-variance tradeoff, or even distributions other than normal.

4.2 Non-Constant Bias-Variance Tradeoff

Our main result, Theorem 4.1, states that, when the tradeoff between bias and variance is fixed (specifically, when ) players strictly prefer a distribution with lower bias. In this section we show that the insight on the preference for lower bias persists also when the tradeoff is not fixed, and that in this case players prefer to lower bias on the margin.

To this end, consider the class of normal distributions with , where is strictly convex and differentiable. Also, suppose that , let , and suppose . Strict convexity of implies that, in the single-player game, the unique optimal choice of distribution from this class is the one in which the bias squared is . As with the case of constant bias-variance tradeoff, however, this is no longer the optimal choice under competition:

Theorem 4.3.

Let be normal with mean 0 and variance 1, and for every let with . Then for every realization of player .

Proof.

Let , where , and define . Then for any bias and tradeoff ,

| (1) |

Evaluated at the point , we thus have

The first equality follows since . The second equality holds since has minimum at and so . Finally, the inequality follows from Theorem 4.1. ∎

4.3 Motivation for Normal Distribution

One of the main assumptions we make in our analysis above is that the error of players’ algorithms is normally distributed. This assumption is natural in the context of machine learning algorithms, and many commonly-used econometric and machine learning procedures with tuning parameters determining the bias-variance tradeoff have been demonstrated to produce predictions with asymptotically normal error distributions; some examples can be found in Chen and White, (1999), Ormoneit and Sen, (2002), Hable, (2012), and Wager and Athey, (2018). To formally describe these results we need a definition:

Definition 4.1.

Let be an infinite sequence of random variables. The sequence is asymptotically normal with asymptotic bias and asymptotic variance if converges with in distribution to , the normal distribution with bias and variance .666Rearranging, we see that as the sequence converges so resembles . Asymptotic normality is a consequence of the Central Limit Theorem where the variance converges at a rate of (the standard deviation converges at a rate of ); thus, is the variance normalized by which converges to a constant.

Parameter estimates obtained from the ridge regression—which we employ for our empirical results in Section 6—are known to be asymptotically normal, with corresponding to the size of the training sample (e.g., Hoerl and Kennard,, 1970; Brown and Zidek,, 1980). In this section we provide some formal definitions and statements to describe these results.

Ridge regression is linear regression with a quadratic regularizer. Features lie in a dimensional space and hypotheses are given by weights as the linear weighted sums of the features, i.e., . The hypothesis selected by the ridge regression on the set of training points is , where the weights minimize the following quantity, the regularized empirical risk function with the quadratic regularizer and regularization parameter :

| (2) |

The regularization parameter is responsible for the bias-variance tradeoff in the prediction. The presence of the regularizer reduces the dependence of the vector of predicted weights on individual observations, making the corresponding predictions more “stable” as the regularization parameter increases. At the same time, the increase in makes the prediction less data-dependent and, therefore, more biased. In other words, while increasing increases the bias of prediction, it decreases the variance. This last statement is formalized in Proposition C.3 in Appendix C.2.

In the “classic” ridge regression model of Hoerl and Kennard, (1970) for a fixed regularization parameter asymptotic bias of the estimator remains finite while its variance decreases at rate as the sample size A possible approach to maintain a meaningful bias-variance tradeoff is to re-scale the regularization parameter to set it in which case the “new” regularization parameter is This is the approach that was pursued in Brown and Zidek, (1980) and the follow-up literature. In the recent literature on ridge regression with high-dimensional regressors, including Karoui, (2013), Dobriban and Wager, (2018), Hastie et al., (2019) Tsigler and Bartlett, (2020), and Wu and Xu, (2020), nonzero asymptotic bias and variance arise in the regime with the dimension of the feature vector growing with the size of the sample

4.4 Numerical Results for Other Distributions and Payoffs

In this section we illustrate the robustness of Theorem 4.1. Specifically, in the proof of Theorem 4.1, there are three assumptions that enable a clean closed form for ex post utility, and thus simplify our argument: (a) the the error distributions are normal; (b) the utility function is ; and (c) . The fact that both the benefit from winning and the total error are 1 simplifies the proof of Theorem 4.1.

In this section we vary the distributions, utility function, and tradeoff, and numerically evaluate the players’ utilities. The subsequent calculations suggest that our insight on the preference of variance over bias holds generally in many cases beyond our theoretical assumptions (a), (b) and (c).

Other distributions.

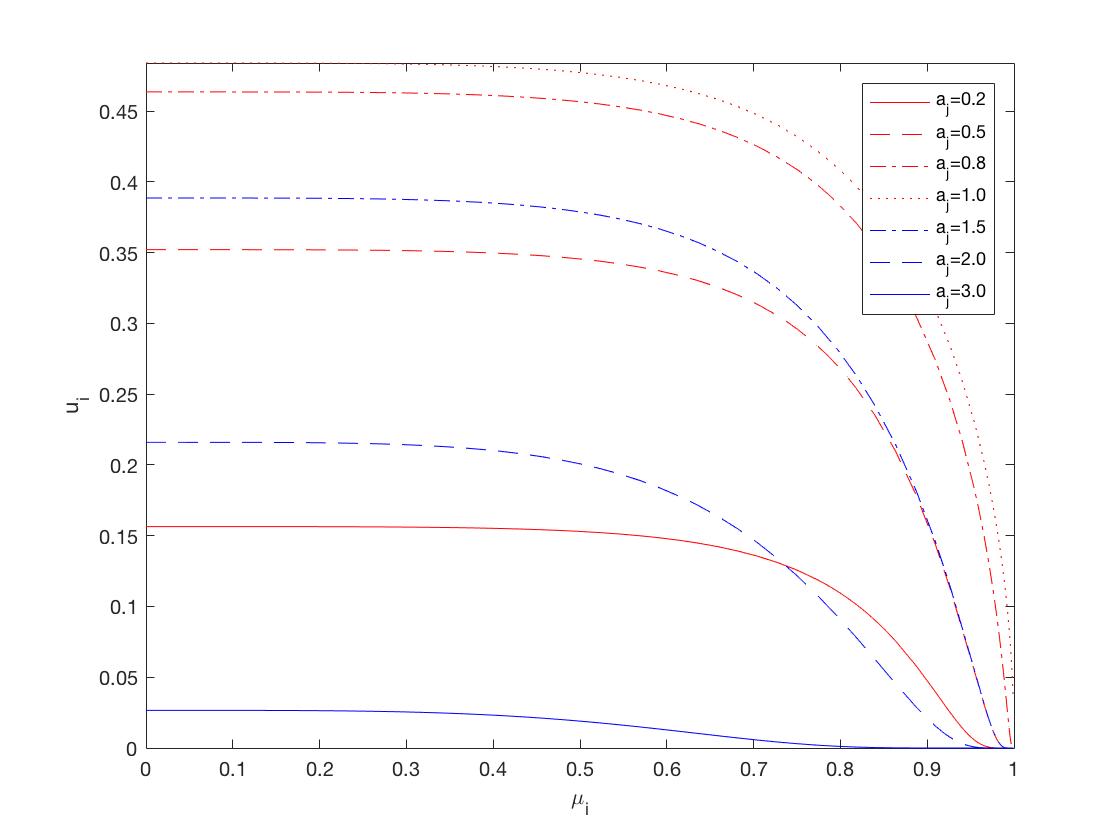

We first numerically calculate the ex post utility curves against arbitrary realizations from the opponent player, as well as the expected utility curves against arbitrary strategies of the opponent, on various distributions. As shown in LABEL:thm:lower-bias_normal_undertradeoff, with the normal distribution, the ex post utility curve is always decreasing, for all opponents’ realizations. Numerical evaluations with the Laplace distribution indicate that its ex post utility curve is also decreasing for all opponents’ realizations; see Figure 2, where we plot the ex post utility curves holding realization fixed for both normal and Laplace distributions. The -axis of each figure is player ’s bias , and the -axis is the ex post utility . Another interesting observation from this numerical result is that with normal distributions, the ex post utility is almost flat for —i.e., while is a dominant strategy, picking any is a “pretty good” strategy.

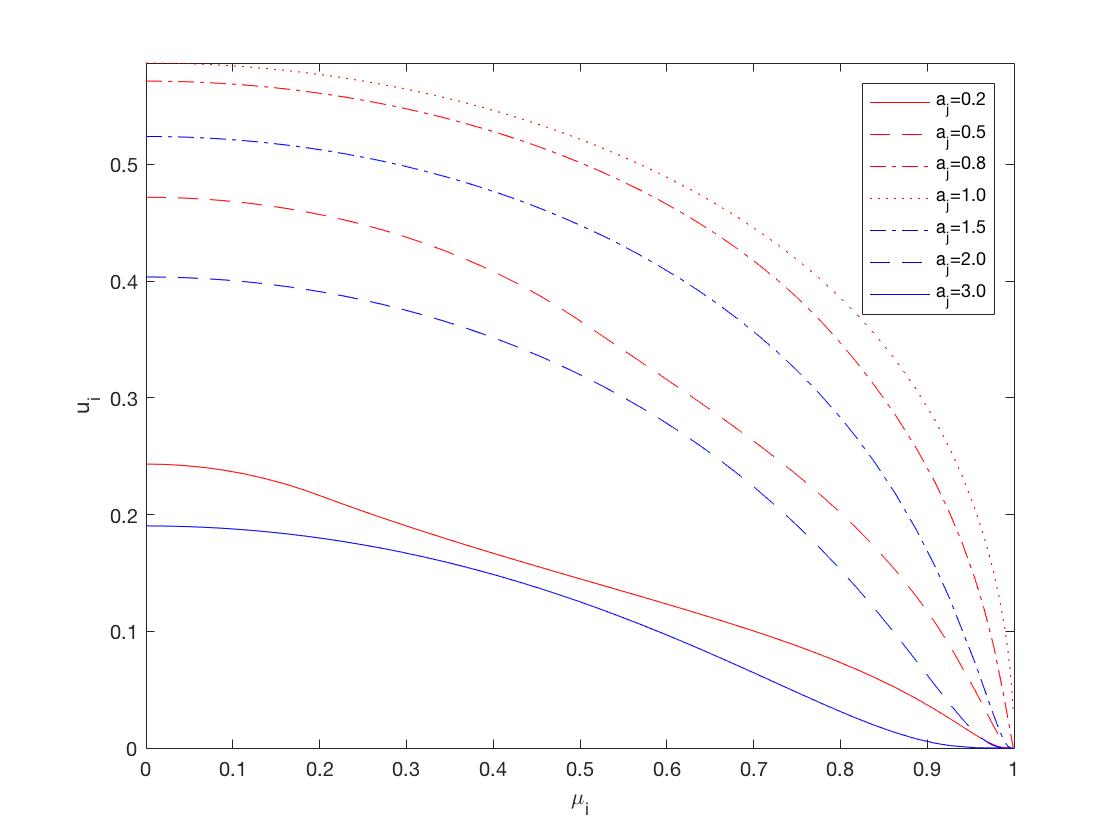

For the logistic distribution, the ex post utility curve is no longer decreasing; however, the expected utility curve is decreasing against arbitrary strategies of the opponent. Thus, the no-bias distribution is a dominant (although not ex post dominant) strategy.

Finally, for uniform distributions, monotonicity does not hold on either the ex post utility curve or the expected utility curve. In fact, there exists a pure Nash equilibrium with non-zero bias. See Figure 3 for utility plots under logistic and uniform distributions.

These plots and calculations indicate that the preference for variance over bias is robust—and holds for Laplace and logistic distributions—but not universal—as demonstrated by the uniform distribution

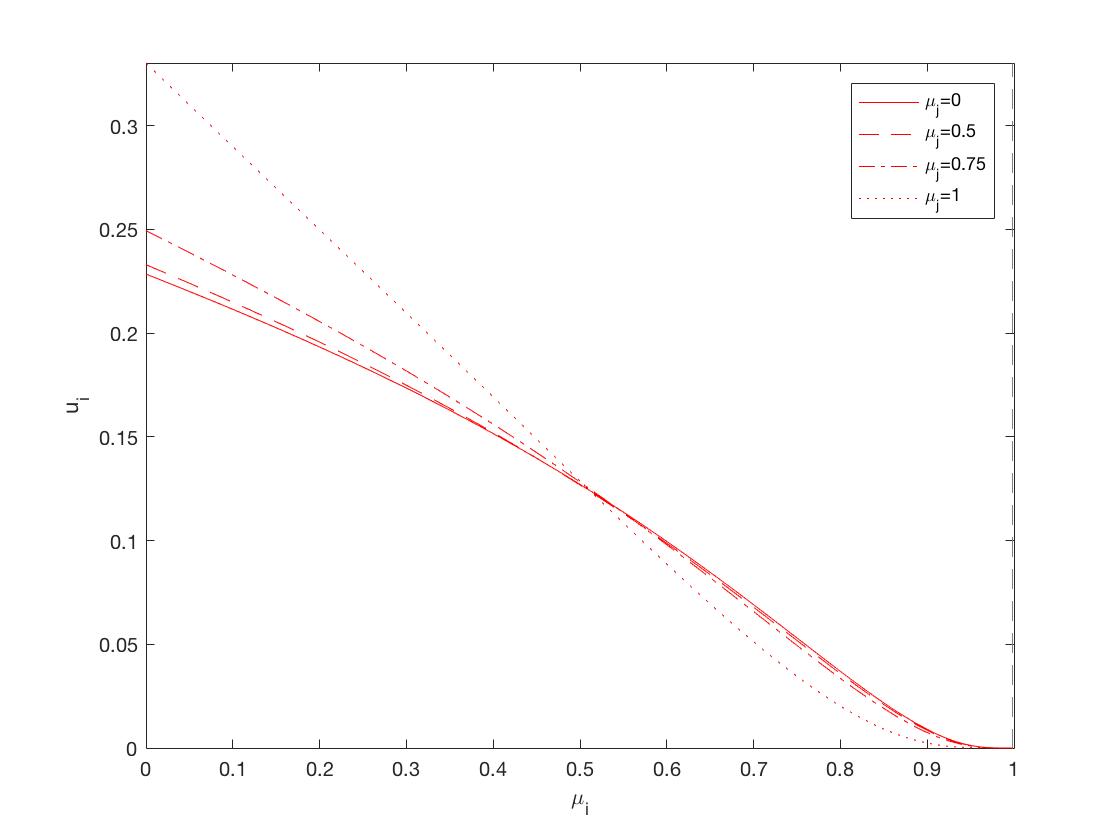

Other utility functions.

Another assumption that is important for our theoretical analysis is the form of the utility function. More generally, suppose players’ utility functions for arbitrary reward , with normal distribution . Observe that for very large , the resulting game is close to a constant-sum game, as the error terms are nearly irrelevant, and that the probability of negative payoffs is negligible.

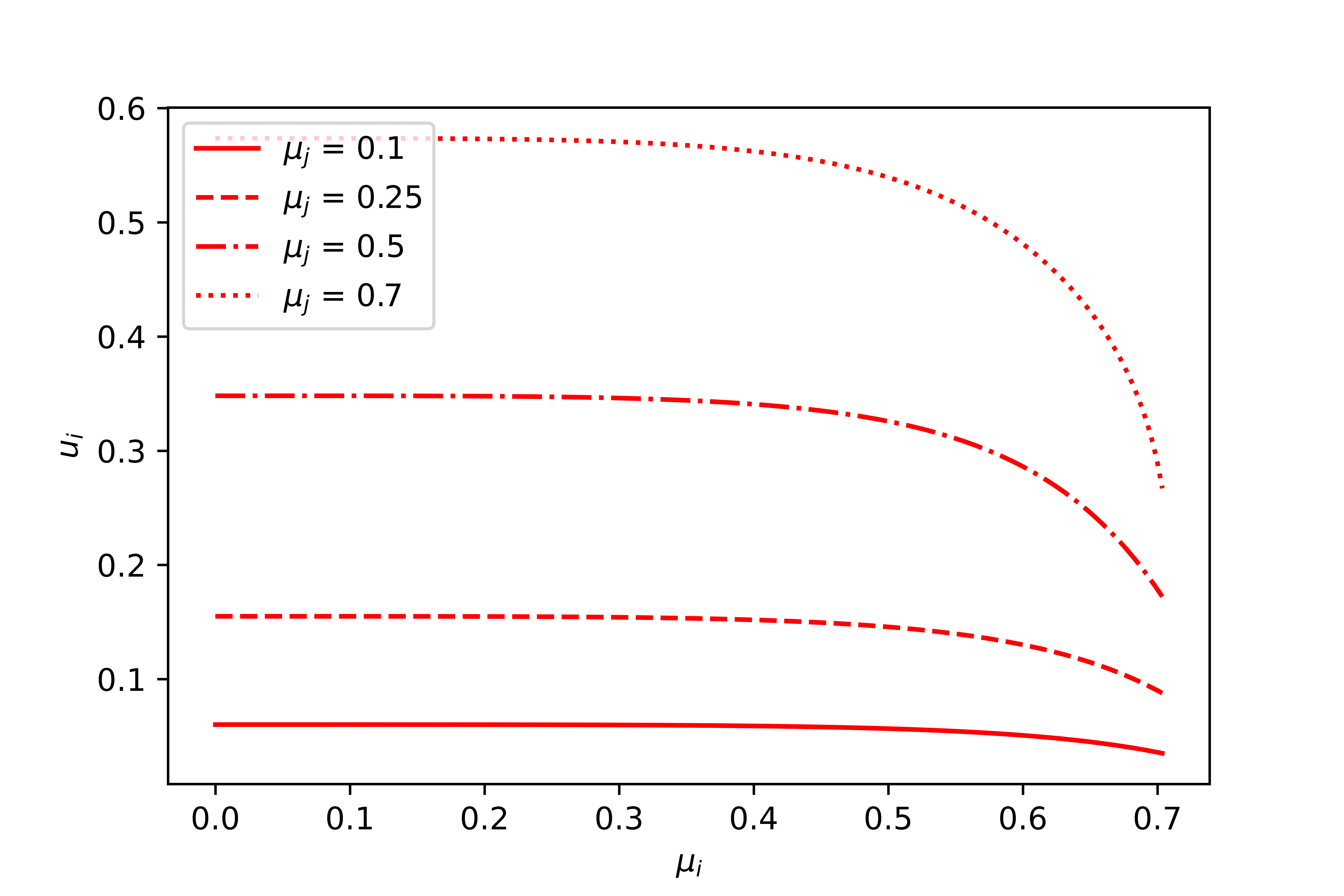

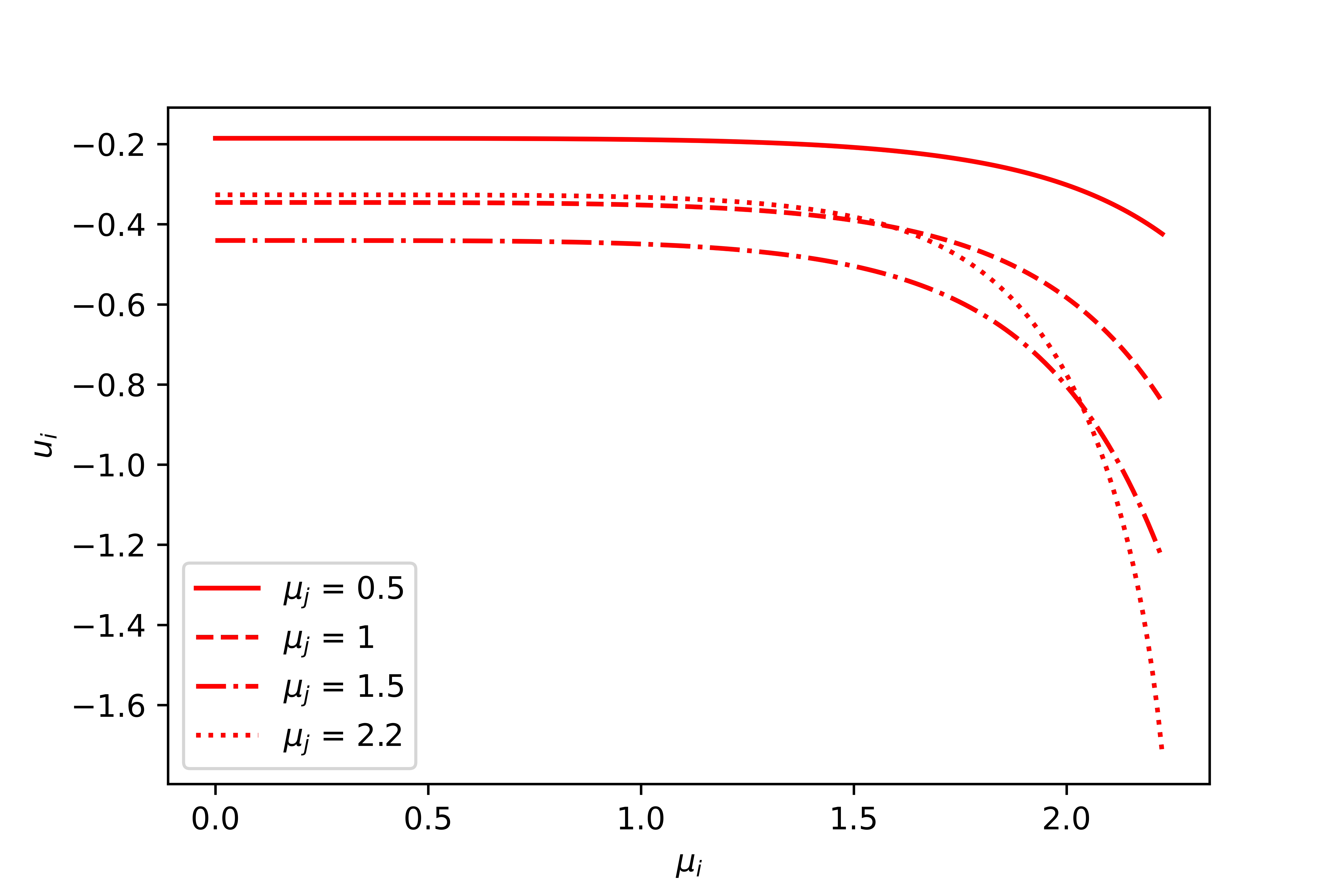

Our main theoretical result considered the case , but for general reward , in which the individual rationality constraint either does not bind or is violated, the monotonicity of ex post utility may not hold. However, numerical calculations demonstrate that the expected utility curve is still decreasing against arbitrary strategies of the opponent, and so no-bias remains a dominant strategy—see Figure 4.

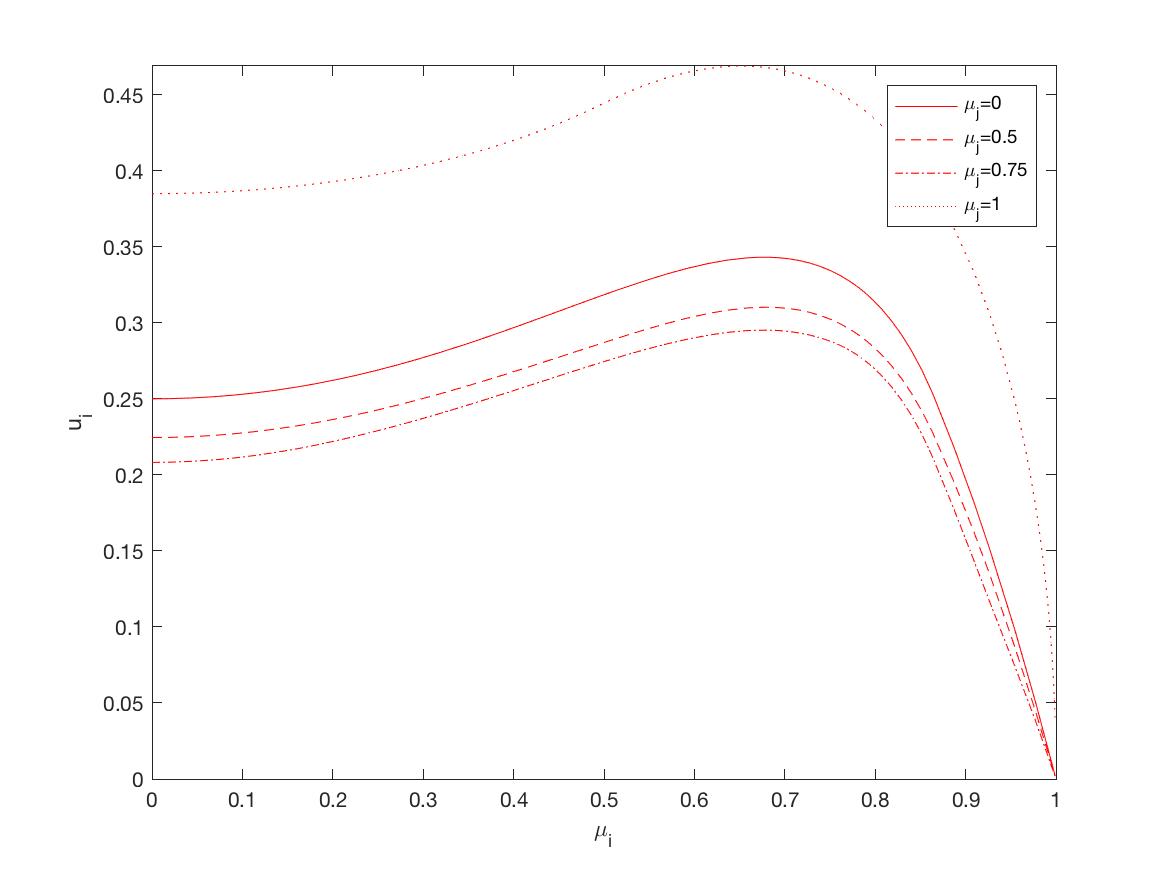

Other tradeoffs.

Finally, our theoretical analysis focused on the assumption that , but more generally one might suppose that the tradeoff (for both players) is different. Similarly to what we observe when we vary the reward in the utility function, the ex post monotonicity of utility may not hold when . However, numerical calculations demonstrate that the expected utility curve is still decreasing against arbitrary strategies of the opponent, and so no-bias remains a dominant strategy—see Figure 5.

5 The Ex Ante Game

Having established players’ preferences for lower bias in the interim stage, we now turn to analyze the ex ante stage. In our analysis thus far we assumed that is fixed, and were concerned with the effects of different algorithms’ estimates of . We now take a step back to the ex ante stage of the general framework, where the choice of algorithm is made prior to observing the realized feature vector .

Fix a learning problem as described in Section 2.1: a function and a distribution over pairs. For simplicity, we will suppose the there is a fixed class of available estimators indexed by a regularization parameter, namely . That is, when players choose algorithms, their decision consists of choosing a parameter , thus yielding the estimator . The ex ante game is then the following:

-

1.

Each player obtains an independent dataset and chooses a regularization parameter .

-

2.

A pair is chosen according to .

-

3.

Utilities are realized:

if , and

otherwise.777In the 0-measure event that predictions are identical, suppose ties are broken uniformly at random.

Let be the regularization parameter for which the Bayes risk is minimal, namely . In particular, for this choice of , the sum of squared-bias and variance under , in expectation over , is minimal.

Denote . For each , this optimal estimator yields a particular (and possibly different) bias and variance . Let be the bias-variance tradeoff at yielded by . It is straightforward to see that, in the one-player game where the utility is one minus the squared-error, this choice of , and so of , maximizes expected utility. Once again, we will show that under competition players can profitably deviate by lowering and choosing an estimator with lower bias (and higher total error).

Our result, Theorem 5.1 below, relies on five assumptions that are sufficient to guarantee the preference for lower bias. Before stating the theorem we list the assumptions and their theoretical, numerical, and empirical justifications.

- A1

- A2

-

A3

Lowering simultaneously decreases for every . Formally,

for every . We note that this assumption is provably true in the specific case where each is a ridge regression with regularization parameter —see Proposition C.3.

-

A4

For each , let be the sum of squared-bias and variance at and :

Then is strictly convex and differentiable.

-

A5

Let denote an independent normal random variable with mean and variance such that . Then at the optimal , the random variables

where the randomness is over and the normal distributions, are (weakly) negatively correlated. We note that a sufficient condition for this assumption to hold is that for every , the minimal risk is achieved at . In particular, we prove that this is true for ridge regression with one-dimensional feature vectors—see Proposition C.2. In addition, in Appendix E we validate assumption A5 empirically in the same datasets and games from Section 6.

We now state and prove our main theorem for this section. Let be the optimal regularization parameter and the resulting estimator. Then when player chooses , player can profitably deviate by choosing with . Formally:

Theorem 5.1.

Suppose assumptions A1-A5 hold. Then

Theorem 5.1 states that, when both players choose to minimize the Bayes risk, then each player can profitably deviate by choosing a lower . Thus, the action profile in which both players choose is not a Nash equilibrium. Under a stronger version of assumption A2, we can show that lowering below is strictly beneficial for player for every choice of player . In particular, this holds under assumption A2’:

-

A2’

The result of Theorem 4.1 holds also when the tradeoff between squared-bias and variance is different for the two players: For any and , if each player chooses a distribution from the class then lower bias is a dominant strategy.

6 Empirical Results

In this section we test our insight on the preference of variance over bias in real datasets.

Data description

We consider two widely-used benchmark datasets, chosen mostly for convenience and because they are standard datasets often used to test new ideas in machine learning. We implement a similar regression problem (discussed below) separately for the two datasets.

The first dataset is the California housing prices data from the 1990 Census, a dataset first utilized by Pace and Barry, (1997) and included in the Python Scikit-learn library. It includes 20640 observations on 9 features, such as number of rooms, median income, etc. From this data we set up a regression problem of predicting the order of magnitude of the median house prices (i.e., its logarithm) from the other features. For features where orders of magnitude may be more relevant than absolute magnitude, we include both the feature and its logarithm.

The second dataset is the wine quality data designed by Cortez et al., (2009). It records 12 features for 6497 observations, where 11 features are physicochemical properties and the last feature is the quality of wine. The dataset is partitioned into two sub-datasets – one for red wine with 1599 observations and one for white wine with 4898 observations. We set up the regression problems of predicting the quality of wine from the other physicochemical properties for the two sub-datasets separately.

Experiment setup

We analyze a game between two players, each of whom gets roughly half the data and employs a ridge regression in order to predict median housing prices in the California housing prices data (resp. qualities of wine in the wine quality data). In both datasets, various features tend to be highly correlated, which makes the design matrix (covariance matrix of the feature vector) nearly non-invertible. This, in turn, makes the estimated feature weights in the linear regression unstable, largely varying from sample to sample. A common tool used to stabilize the estimated feature weights is linear regression with regularization, namely, ridge regression. Running a ridge regression involves setting a regularization parameter , where is the standard ordinary least squares (OLS) regression, and increasing leads to a model with greater bias but lower variance of the resulting predictions. Thus, we will let the players play the game for various values of . Further discussion of ridge regression is given in Section 4.3.

The design of the game is as follows:

-

1.

The dataset is uniformly partitioned with 10% as the test set and 90% as the training set. Each player uniformly draws 50% of the training set as her own training set.

-

2.

Players choose regularization parameters and , respectively, and perform ridge regression on their own training sets.

-

3.

The expected payoffs of players are given by the bias-variance game (Definition 2.2 and the description in Section 5) evaluated on the test set. On each point in the test set, the player whose prediction is closest to the true label wins and obtains payoff of one minus the squared error of the prediction; the other player’s payoff is zero. Each player’s payoff in the game is the average payoff over the points in the test set.

Experiment results

We used Monte Carlo simulations to approximate expected utilities of the players. We repeat steps 1-3 above by independently drawing training and validation samples 100 times for the California housing prices data (resp. 10000 times for the wine quality data) and computing payoffs that result from a given pair of choices of regularization parameters . We contrast the optimal choice of regularization parameter in the single-player setting with the two-player game.

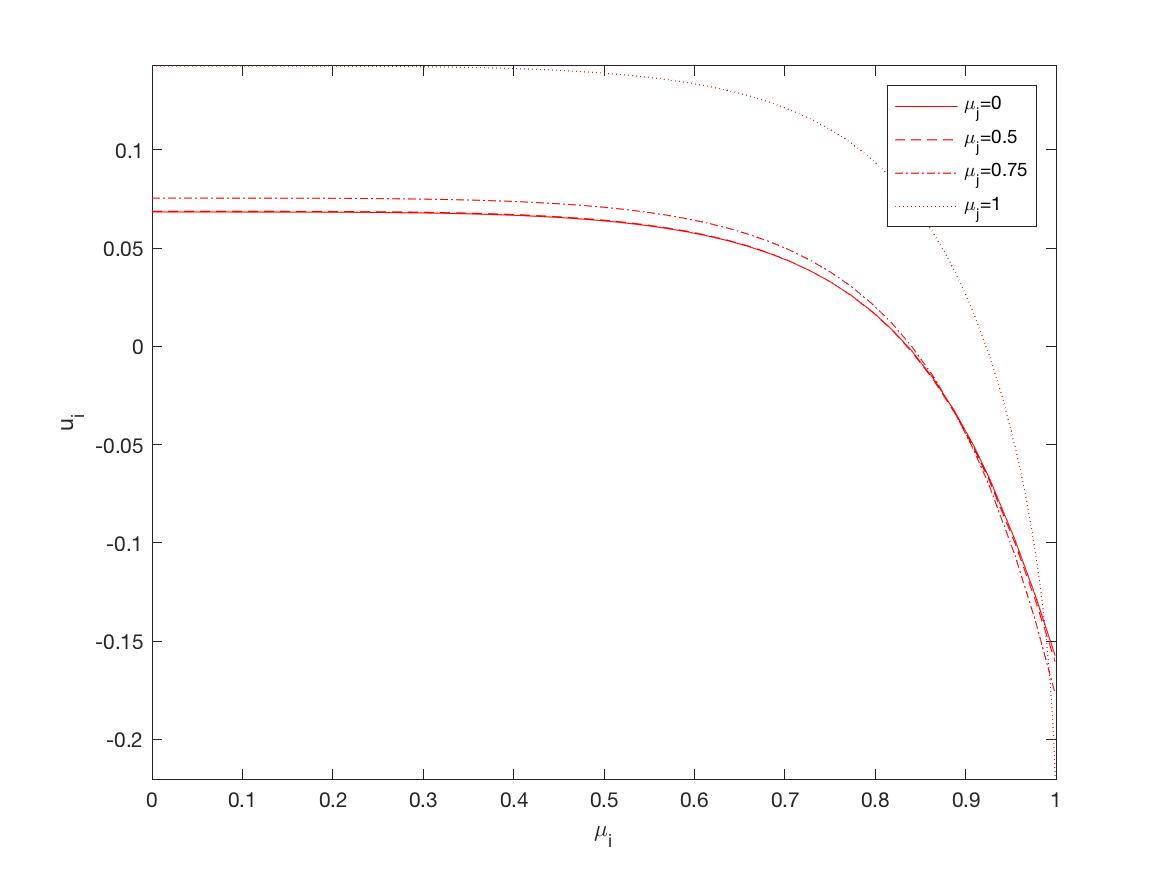

For the California housing prices data, Player 1’s utility in the single-player setting is depicted in Figure 6(a) as a function of the player’s regularization parameter, ranging from to . The optimal parameter choice is . In Figure 6(b), Player 1’s utility in the two-player game is plotted as a function of for fixed values of Player 2’s regularization parameter . For all choices of , Player 1’s utility is optimized by selecting .

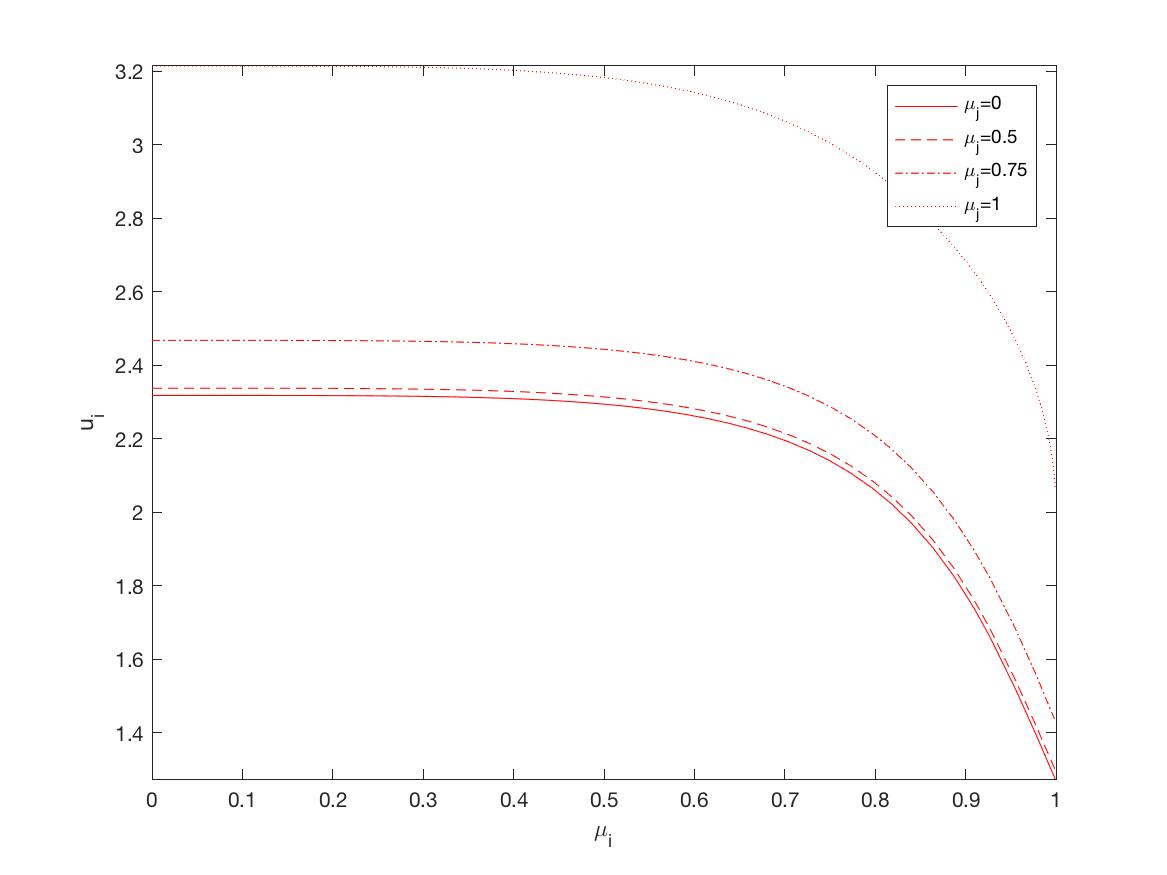

For the red wine quality data, Player 1’s utility in the single-player setting is depicted in Figure 7(a) as a function of the player’s regularization parameter, ranging from to . The optimal parameter choice is . In Figure 7(b), Player 1’s utility in the two-player game is plotted as a function of for fixed values of Player 2’s regularization parameter . For all choices of , Player 1’s utility is optimized by selecting .888 Similar results hold for the white wine quality data. In particular, Player 1’s utility is optimized by selecting in the two-player game.

The conclusions of our theoretical study are corroborated by this empirical ridge regression game. Specifically, the optimal single-player regularization parameter in a ridge regression is generally non-zero, while, as long as the benefit of winning is sufficiently large, the two-player best response is to lower the regularization parameter to zero. In Appendix E, we also demonstrate that two of the assumptions used in Theorem 5.1 for the ex ante game hold in our empirical ridge regression game. We view these results as affirming the validity of our insight on the preference of variance over bias in competitive settings beyond our theoretical and numerical analyses.

7 Conclusions

In this paper we studied competing machine learning algorithms by abstracting the problem to a distribution-selection game in which bias and variance can be traded off. While outcomes of real learning algorithms can be complex, our bias-variance game is amenable to theoretical analysis, and we formally prove that for normal distributions reducing bias at the expense of variance is a best response. Thus, there is a clear preference for lower bias, even at the expense of higher total error.

In addition to our theoretical analyses, we verified the robustness of our insight on the preference for lower bias numerically under several variations of the game. We also considered the empirical game on a benchmark data set using ridge regression, where the same qualitative conclusions from our theoretical analysis were demonstrated.

Many aspects of machine learning problems change significantly in competitive environments. For example, in a different context but a similar vein, Mansour et al., (2018) consider the classical bandit model of online learning and study the effect competition between the algorithms on the exploration vs. exploitation tradeoff. These authors show that the presence of competition may lead to the strategic choice of algorithms that do not explore as much as they would absent competition, and may thus be worse learners. More generally, we believe that there are many more unresolved issues in the intersection of machine learning and competition, and suggest this general area as a fruitful and important one for future study.

References

- Anderson, (2006) Anderson, C. (2006). The long tail: Why the future of business is selling less of more. Hachette Books.

- Ben-Porat and Tennenholtz, (2017) Ben-Porat, O. and Tennenholtz, M. (2017). Best response regression. In Advances in Neural Information Processing Systems, pages 1499–1508.

- Ben-Porat and Tennenholtz, (2019) Ben-Porat, O. and Tennenholtz, M. (2019). Regression equilibrium. In Proceedings of the 2019 ACM Conference on Economics and Computation, pages 173–191.

- Brown and Zidek, (1980) Brown, P. J. and Zidek, J. V. (1980). Adaptive multivariate ridge regression. The Annals of Statistics, 8(1):64–74.

- Chen and White, (1999) Chen, X. and White, H. (1999). Improved rates and asymptotic normality for nonparametric neural network estimators. IEEE Transactions on Information Theory, 45(2):682–691.

- Cortez et al., (2009) Cortez, P., Cerdeira, A., Almeida, F., Matos, T., and Reis, J. (2009). Modeling wine preferences by data mining from physicochemical properties. Decision support systems, 47(4):547–553.

- Dobriban and Wager, (2018) Dobriban, E. and Wager, S. (2018). High-dimensional asymptotics of prediction: Ridge regression and classification. The Annals of Statistics, 46(1):247–279.

- Eliaz and Spiegler, (2019) Eliaz, K. and Spiegler, R. (2019). The model selection curse. American Economic Review: Insights, 1(2):127–40.

- Friedman et al., (2001) Friedman, J., Hastie, T., Tibshirani, R., et al. (2001). The Elements of Statistical Learning, volume 1. Springer Series in Statistics, New York.

- Gaudin, (2016) Gaudin, S. (2016). At Stitch Fix, data scientists and A.I. become personal stylists. https://www.idginsiderpro.com/article/3067264/at-stitch-fix-data-scientists-and-ai-become-personal-stylists.html. Accessed 2019-12-11.

- Hable, (2012) Hable, R. (2012). Asymptotic normality of support vector machine variants and other regularized kernel methods. Journal of Multivariate Analysis, 106:92–117.

- Hastie et al., (2019) Hastie, T., Montanari, A., Rosset, S., and Tibshirani, R. J. (2019). Surprises in high-dimensional ridgeless least squares interpolation. arXiv preprint arXiv:1903.08560.

- Hoerl and Kennard, (1970) Hoerl, A. E. and Kennard, R. W. (1970). Ridge regression: applications to nonorthogonal problems. Technometrics, 12(1):69–82.

- Immorlica et al., (2011) Immorlica, N., Kalai, A. T., Lucier, B., Moitra, A., Postlewaite, A., and Tennenholtz, M. (2011). Dueling algorithms. In Proceedings of the forty-third annual ACM symposium on Theory of computing, pages 215–224. ACM.

- Karoui, (2013) Karoui, N. E. (2013). Asymptotic behavior of unregularized and ridge-regularized high-dimensional robust regression estimators: rigorous results. arXiv preprint arXiv:1311.2445.

- Liang, (2019) Liang, A. (2019). Games of incomplete information played by statisticians. arXiv preprint arXiv:1910.07018.

- Mansour et al., (2018) Mansour, Y., Slivkins, A., and Wu, Z. S. (2018). Competing bandits: Learning under competition. In 9th Innovations in Theoretical Computer Science Conference (ITCS 2018). Schloss Dagstuhl-Leibniz-Zentrum fuer Informatik.

- Olea et al., (2019) Olea, J. L. M., Ortoleva, P., Pai, M. M., and Prat, A. (2019). Competing models. arXiv preprint arXiv:1907.03809.

- Ormoneit and Sen, (2002) Ormoneit, D. and Sen, Ś. (2002). Kernel-based reinforcement learning. Machine learning, 49(2-3):161–178.

- Pace and Barry, (1997) Pace, R. K. and Barry, R. (1997). Sparse spatial autoregressions. Statistics & Probability Letters, 33(3):291–297.

- Sinha et al., (2016) Sinha, J. I., Foscht, T., and Fung, T. T. (2016). How data analytics and AI are driving the subscription e-commerce phenomenon. MIT Sloan Management Review.

- Tsigler and Bartlett, (2020) Tsigler, A. and Bartlett, P. L. (2020). Benign overfitting in ridge regression. arXiv preprint arXiv:2009.14286.

- Valiant, (1984) Valiant, L. G. (1984). A theory of the learnable. Communications of the ACM, 27(11):1134–1142.

- Wager and Athey, (2018) Wager, S. and Athey, S. (2018). Estimation and inference of heterogeneous treatment effects using random forests. Journal of the American Statistical Association, 113(523):1228–1242.

- Wu and Xu, (2020) Wu, D. and Xu, J. (2020). On the optimal weighted l2 regularization in overparameterized linear regression. Advances in Neural Information Processing Systems, 33:10112–10123.

Appendix

Appendix A Proofs from Section 3

Theorem 3.1.

Let be monotone increasing, convex on , and symmetric around 0. Let be IR (so as to satisfy ) and . Then for any realization of player .

Proof.

The proof consists of several cases.

-

1)

: Since , it must be the case that . Thus, for any realization in which player gets non-zero utility, his utility is nonnegative under both and .

Consider first the distribution . Observe that, by monotonicity, for each point , the pdf at under is higher than under . Since all such realizations lead to positive utility, .

Next, consider the comparison between and . On the interval the distribution is an inversion of with higher probability closer to the origin, and so on this sub-interval leads to higher utility. On the interval the pdf of dominates that of , and so also here leads to higher utility. Thus, , and so .

-

2a)

: Consider Figure 8(a), in which is the green pdf and is the blue pdf. Area E (from to , and below both curves) leads to the same utility for both distributions. Area A (under ) leads to higher utility than area B (under ). And finally, area D (under ) leads to strictly positive utility. Thus, overall, .

(a) Case 2a

(b) Case 2b Figure 8: Case 2 of Theorem 2.1. -

2b)

: Consider Figure 8(b), in which is the green pdf and is the blue pdf. Area E (from to , and below both curves) leads to the same utility for both distributions. Area A (under ) leads to higher utility than area B (under ). Area D (under ) leads to strictly positive utility.

It remains to show that the losses under due to realizations in are smaller than the losses on the same intervals due to . To this end, we will consider points , and show that the sum of the pdfs of at and is larger than the sum of the pdfs of at those same points. Let be the pdf of . Then the sum of the pdfs of at points and is . The sum of the pdfs of at the points and and is . By convexity, , completing the claim.

∎

Theorem 3.2.

Let be normal; let and satisfy ; and let . Then for any realization of player .

Proof.

The proof is nearly identical to that of Theorem 3.1, except for case 2b: the upper tail of the normal distribution is convex only from onward. So this case must be handled differently.

However, to complete the proof, we actually only need that the pdf of be convex from the point and higher. Since it holds that , and so is convex on whenever , completing the proof. ∎

Appendix B Proof of Theorem 4.1

Theorem 4.1.

Let be normal with mean 0 and variance 1, and let and , where . If then for any realization of player .

Proof.

Since players are symmetric, we drop all subscripts in the discussion below. We compute the expected utility of player when he plays action against the realization of player . Without loss of generality, we assume . First we characterize the closed form of for all ; then we argue that , where ; and finally we show that for all , which completes the proof.

We first focus on . Observe that

| We can now evaluate | ||||

| where is the CDF of , i.e., the standard normal distribution. Now, | ||||

| Because of the constraint that , we can eliminate some terms: | ||||

| Next we consider for . Note that in this case, agent ’s realization is 1 deterministically, which implies that her utility conditioning on winning is zero. Her utility conditioning on losing is also zero by definition. Thus, for . To see that , note that and . Thus, | ||||

| and | ||||

Invoking the Squeeze Theorem yields . Finally, taking the derivative of with respect to for yields

To prove Theorem 4.1, it is sufficient to show that this derivative is strictly negative for all and . This condition is expressed as

| (3) | ||||

The remaining part of the proof, showing that inequality (3) holds, follows from a long and algebraic calculation that we formalize as Lemma B.1. ∎

We now show that the derivative of the ex post utility with respect to against realization of the opponent is strictly negative for all and .

Lemma B.1.

Inequality (3) holds for all and .

Notice that there may be two regimes: (a) the player always gains positive payoff, i.e., ; (b) the player sometimes suffers non-positive payoff, i.e., . We break Lemma B.1 into these two regimes and show them separately.

Lemma B.2.

Inequality (3) holds for all and .

Proof.

We start with inequality (3), copied here:

The proof is a two-case analysis, working backwards from inequality (3) to show that it holds from lemma domain and case assumptions in both cases. Some steps are exact algebraic manipulations (“if and only if” or ) and some steps are weakly restrictions to stronger requirements (“is implied by” or ). We use the arrows for visual simplicity to indicate the type of each step. Each step includes an explanation. Consider the following two cases based on the sign of .

| Case 1: . To start, multiplying both sides of equation (3) by , we get inequality | ||||

| Now it is clear that we can drop the term because we have from . So we get | ||||

| Replacing the exponential functions with their respective Taylor series, we get | ||||

| Pulling out the first two terms of the series, we get | ||||

| Separate the previous line into two inequalities described by Condition 1a and Condition 1b; if both are true then the combined inequality is true. | ||||

| Condition 1a: | ||||

| Multiplying through by , we get | ||||

| Splitting out the terms in the first bracket and canceling , we get | ||||

| Further canceling additive constants from both sides, we get | ||||

| Dividing out and grouping all terms on one side, we get | ||||

| Condition 1b: | ||||

| Dropping the terms – by the left-hand side sum terms dominating for every – we get | ||||

| Noting and canceling a factor of , we get | ||||

| Case 2: . | ||||

| Note that we have because the lemma’s domain has and . Starting anew for Case 2 from inequality (3), replacing the exponential functions with their respective Taylor Series, we get inequality | ||||

| Pulling out the first two terms of the series, we get | ||||

| Separate the previous line into two inequalities described by Condition 2a and Condition 2b; if both are true then the combined inequality is true. | ||||

| Condition 2a: | ||||

| Multiplying through by , we get | ||||

| Splitting out the terms in the first bracket and canceling the resulting (additively) matching terms, we get | ||||

| Further canceling additively and then moving the factor of , we get | ||||

| Combining like-terms on each side and dividing through by , we get | ||||

| Dividing by and re-organizing, we get | ||||

| Condition 2b: | ||||

| To prove that the inequality of the previous line holds, it is sufficient to show that the next inequality holds for pairs of consecutive terms within its sums ; for each fixed, even , we require: | ||||

| Factoring out common terms within the bracket of the Taylor series terms, we get | ||||

| Multiplying through by , we get | ||||

| Expanding within the second brackets, we get | ||||

| Dropping the terms because they correspond exactly to an inequality already shown to hold in the sequence of steps to prove Condition 2a, we get | ||||

| Dropping the multiplicative constant and then the additive constant, both of which are non-negative, we get | ||||

| This last inequality holds because both sides are non-positive and the left-hand-side has weakly smaller magnitude.∎ | ||||

Lemma B.3.

Inequality (3) holds for all and .

Proof.

Let be the left-hand-side in inequality (3), i.e.,

Next we show the following inequalities: for all and ,

(i) ;

(ii) ;

(iii) ;

and for all and ,

(iv) .

Combining (i)–(iv) proves the lemma.

Proof of (i).

By definition, plugging in , is

Now consider the Taylor series expansion of and in . We analyze the first term and the remaining terms separately.

The first term of the Taylor series expansion in is

for all .

The k-th even terms and (k+1)-th odd terms of the Taylor series expansion, for , in are

for all .

Proof of (ii).

By definition,

| Plugging in yields | ||||

Now consider the Taylor series expansion of and in . We analyze the first term and the remaining terms separately.

The first term of Taylor series expansion in is

for all .

The k-th even terms and (k+1)-th odd terms of the Taylor series expansion, for , in are

for all .

Proof of (iii).

By definition,

| Plugging in yields | ||||

Note that and we show is non-decreasing in below. To see this, consider the partial derivative of with respect to , it is

Multiplying by , we get

| (5) | ||||

Now consider the Taylor series expansion of and in (LABEL:eq:(iii)). We analyze the first two terms and the remaining terms separately.

The first and second terms of the Taylor series expansion in (LABEL:eq:(iii)). It is

for all .

The k-th term of the Taylor series expansion, for , in (LABEL:eq:(iii)). It is

| (6) | ||||

Multiplying by ,

Note that and for all . Thus, to show (LABEL:eq:(iii)_2) is non-negative for all , it is sufficient to argue

which is true for all .

Proof of (iv).

By definition,

Now consider the Taylor series expansion of and in . We analyze the first two terms and the remaining terms separately.

The first and second terms of the Taylor series expansion of are

which is true for all and .

The k-th term of the Taylor series expansion, for , of . It is

| (7) | ||||

Multiplying by ,

Notice that and for all and . Thus, to show (LABEL:eq:(iv)) is non-negative for all and , it is sufficient to argue

which is true for all and . ∎

Appendix C Bias and Variance in Ridge Regression

C.1 One-Dimensional Case

Suppose that features of training points are single-dimensional with labels

where are normally distributed with mean zero and variance

In this model, when running ridge regression, the regularization parameter that minimizes the regularized risk is independent of :

Proposition C.1.

The that minimizes the regularized risk minimizes the sum of variance and squared-bias for every feature .

Proof.

When a ridge regression with regularization parameter is used to estimate from the training set of points, the corresponding estimator is

The prediction for label of the new example with feature and label produced from the ridge regression is

The error of this prediction is

The expectation of this error is

which represents the bias. The magnitude of the bias depends on the value of the feature vector and the (unknown) parameter .

The term

has expectation equal to zero. Its variance is

For any given , the squared error of is thus the squared-bias plus the variance, namely

Observe that the for which this is minimized is independent of . ∎

An implication of Proposition C.1 is that, in this setting, assumption A5 from Section 5 holds. As in Section 4.2, let us suppose that the value of the bias-variance tradeoff is continuous and differentiable, and that this holds for every . Recall that is the sum of squared-bias and variance at and , namely

Assumption A4 from Section 5 states that the expectation of , taken over the randomness of , is convex and differentiable. For the following proposition, let us assume that these properties hold for every , and not just in expectation:

-

A4’

is strictly convex and differentiable for every .

Proposition C.2.

Under assumption A4’, assumption A5 holds.

Proof.

Assumption A5 states that

are weakly negatively correlated. We will show that in the one-dimensional ridge regression setup of this section, the two random variables are, in fact, uncorrelated.

By Proposition C.1, the that minimizes the regularized risk minimizes the sum of variance and squared-bias for every feature . By assumption A4’, this implies that, for every fixed ,

Thus, the random variable , with distribution over , is constant and equal to 0. It is thus uncorrelated with the second random variable from assumption A5. ∎

C.2 Multidimensional Case

Suppose that feature vector is -dimensional and

where are independent across examples and and

We show that, when running ridge regression in this model, an increase in the regularizer increases the bias and decreases the variance on the prediction of any :

Proposition C.3.

In ridge regression, for every vector , the bias is increasing in and the variance is decreasing in .

Proof.

Let be the design matrix containing the feature vectors of examples in the training data, and . Then the estimator of the ridge regression can be written as

This representation shows the decomposition of the bias and variance term of the estimator. Denote

and

Then the prediction for the new example is

The mean squared error is

We note that the first element of the mean squared error is a quadratic form. It determines the dependence of the mean squared error on To find the minimum, note that

Finally

Taking the derivative with respect to we obtain a positive semidefinite matrix, meaning that bias is always increasing in The variance term is then

The derivative of this matrix with respect to is

which is a negative semidefinite matrix and so the variance always increases in ∎

Appendix D Proof of Theorem 5.1

Proof.

By assumption A1,

a normal distribution with squared-bias and total error . Denote by the total error of when the feature vector is and the squared-bias is . Then, as in Equation (1), for each fixed we can write

where . Thus,

By assumption A3,

and by assumption A2,

By assumption A5,

Finally, since minimizes the Bayes risk, assumption A4 implies that

Putting these together implies the claimed inequality. ∎

Appendix E Empirical Demonstration of Assumptions

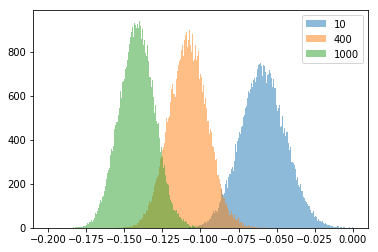

In this section we empirically demonstrate that two of the assumptions used in Theorem 5.1 for the ex ante game hold when the game played on the California housing prices data and the wine quality data from Section 6.

First, we demonstrate that assumption A1 on the normality of prediction error holds. For the California housing prices data, Figure 9 plots the distribution, over random choices of the training data, of the error in prediction on a particular point in the test data for three values of regularization parameter . Notice that the distributions appear roughly normal, and that the predictions of the lower value have higher variance and lower bias.999Similar observations holds for the wine quality data.