AN EXTENDED SPECULATION GAME FOR THE RECOVERY OF HURST EXPONENT OF FINANCIAL TIME SERIES

Abstract

The speculation game is an agent-based toy model to investigate the dynamics of the financial market. Our model has achieved the reproduction of 10 of the well-known stylized facts for financial time series. However, there is also a divergence from the behavior of real market. The market price of the model tends to be anti-persistent to the initial price, resulting in the quite small value of Hurst exponent of price change. To overcome this problem, we extend the speculation game by introducing a perturbative part to the price change with the consideration of other effects besides pure speculative behaviors.

keywords:

Cognitive agent-based model; Round-trip trading; Financial stylized facts.1 Introduction

The financial time series of asset returns have several qualitative properties collectively called stylized facts. For example, one of the well known stylized facts is called heavy tails, which describes that the probability distribution of price returns has fatter tails than those of Gaussian distribution [1],[2]. Cont summarized 11 currently well known stylized facts including heavy tails [3]. They are quite nontrivial features which can be observed in different markets and instruments.

To investigate the emerging mechanism of stylized facts, we build a novel simple agent-based model named Speculation Game [4], which has two distinct features comparing with preceding agent-based market models. First, it takes account of round-trip trades by extending the decision-making structure of Minority Game [5]. Second, a mutual projection between players’ realistic and cognitive worlds is implemented explicitly. As a result of these novelties, Speculation Game succeeds in reproducing 10 out of the 11 well known stylized facts (see Table 1).

| Stylized fact | Reproducibility |

| Volatility clustering | |

| Intermittency | |

| Heavy tails | |

| Absence of autocorrelation in returns | |

| Slow decay of autocorrelation in volatilities | |

| Volume/volatility correlation | |

| Aggregational Gaussianity | |

| Conditional heavy tails | |

| Asymmetry in time scales | |

| Leverage effect | |

| Gain/loss asymmetry | |

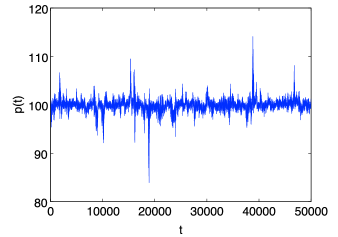

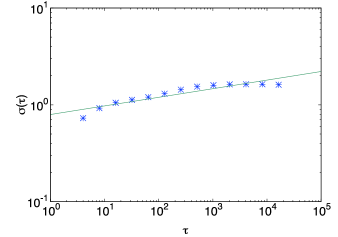

However, there is still a divergence from the behavior of real market. The market price of Speculation Game tends to stick around the initial price as Fig. 2 displays (the parameters are fixed as , , , , in this study), which causes an anti-persistent price change with very small Hurst exponents. As a power exponent of regression line of standard deviation (or several other forms) on time scale , Hurst exponent describes the long-term trend in the price time series. Standard deviations of price changes on different time scales can be calculated as follows,

| (1) |

When , a price time series is a random walk. When , it shows a persistent trend while it has a mean-reverting feature when . Hurst exponent in Speculation Game is found as , which indicates its price time series has a too strong mean-reverting characteristic. Note that the fitting of regression is also not very good as in Fig. 2.

Objective of this study is to overcome the price sticking problem and recover Hurst exponent to the normal level like ones in the real financial markets. Particularly, some perturbation is added to price change as the consideration of other effects besides pure speculative behaviors.

2 Speculation Game and its Extension

Speculation Game is a repeated game in which players in a gamified market, with an initial market wealth and randomly given strategies, compete with each other to increase wealth through round-trip trades. The game proceeds with updates alternating between players’ realistic and cognitive worlds.

At discrete time , player using her best strategy () takes an action from the set: buy (), sell (), or hold (idle) (). When she sum it’s an order with strategy , the quantity of order is decided both with her market wealth and the board lot amount , the latter of which describes the ease of placing orders with multiple quantities, as follows,

| (2) |

where stands for a flooring operator. Note that the closing quantity of a round-trip trade is required to be equal to the opening one . Also, the player’s initial market wealth is decided with a uniformly distributed random number to enable her to order one unit at least

| (3) |

If as a result of round-trip trade, the player will be forced to leave the market and substituted by a new player.

Following the order imbalance equation defined by Cont and Bouchaud [6], the market price change is calculated as follows by letting the initial market price as ,

| (4) |

Then, the quantized price movement (the last digit in the history ) is decided by the magnitude correlation between and the cognitive threshold , the latter of which can be explained as a threshold value for the players to recognize a big price move:

| (5) |

To find an action of the best strategy , the player with memory at first takes the reference of the last digits of history . Next, she looks up strategy to obtain a recommended action corresponding to the historical pattern (see Table 2). However, when the recommendation is the same as the opening order , the player will hold the position.

| History | Recommended action | ||||||

|---|---|---|---|---|---|---|---|

| ⋮ | ⋮ | ||||||

To determine the best strategy , all strategies are evaluated through virtual round-trip trades in the background similarly. Hence, performance of the strategies are assessed in the cognitive world, in terms of the accumulated strategy gains () calculated with cognitive price corresponding to the rough information of in . Letting , is updated as

| (6) |

The gain of strategy in a round-trip trade reads as

| (7) |

Thus, the accumulated strategy gain is calculated by:

| (8) |

Whenever the accumulated gain of the strategy in use is updated, all will be reviewed to renew the strategy with the best performance. If the best strategy happens to be one of the unused strategies with a virtual trade ongoing, the virtual position will be closed immediately before the player switches the strategy at the next time step. Note that the evaluating system is developed by considering that the investing strategies should be evaluated through by round-trip trades, as Katahira and Akiyama pointed out [7].

Since the self-financing assumption is not required in Speculation Game, when a round-trip trade is closed in the realistic world, the player’s market wealth is updated with an investment adjustment , which is the conversion of strategy gain in the cognitive world with taken into consideration,

| (9) |

where can be an arbitrary function. In the game, is used for the simplicity.

As an extension to the original model, a random perturbation is further added to as

| (10) |

where the first term of Eq. (10) could be considered as the effect given by the pure speculative players while the second one as other effects by other types of traders such as long term value traders, hedgers, and so on. Due to this extension, never takes zero so that become a quaternary time series instead of a quinary one.

3 Result and Discussion

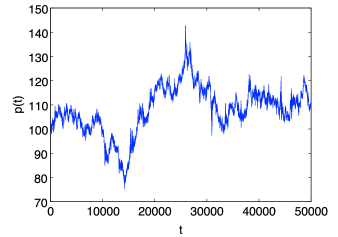

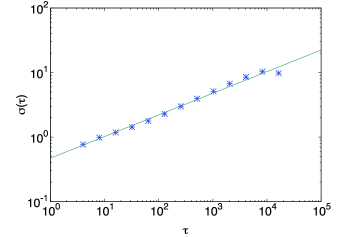

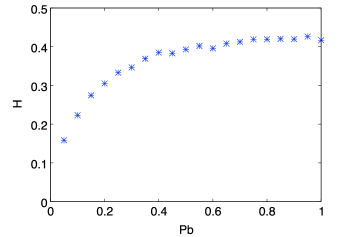

By adding the random perturbation, the dynamics of market price in Speculation Game becomes more realistic. As Fig. 4 displays, can escape from the initial price range and shows long-term fluctuating structures when . Accordingly, Hurst exponent also increases to the normal level () as with a better fitting () as the regression line shown in Fig. 4. It can also be inferred from these results that the long-term fluctuations and trends originated from those non-speculative behaviors.

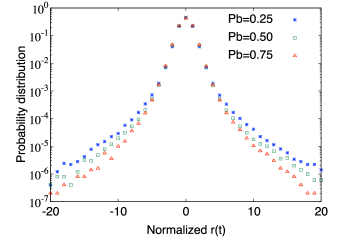

On the other hand, the further increment of perturbation would weaken the stylized properties as well. For instance, the probability distributions of price returns have less heavier tails as more perturbation is added, which is displayed in Fig. 6. Since the similar propensity is confirmed for many of other reproduced stylized features in Speculation Game, speculative behaviors can be considered as the main source for the emergence of stylized facts. Note that adding moderate price perturbation () is favorable in the viewpoint of efficiency to enhance Hurst exponent because excess contribute less to the increment of as Fig. 6 shows. Also, it is reasonable that the perturbation can not make because of pure random walk nature.

4 Conclusion and Future Work

To conclude, adding moderate perturbation to can solve the price sticking problem and recover Hurst exponent for our Speculation Game. Simulation results also indicate that the non-speculative behaviors generate the long-term fluctuations and trends while speculative ones contribute to the emergence of well-known financial stylized facts.

For future research, decision-making structures for fundamentalists and news traders need to be developed for the generation of a long-term trend. Adding perturbation is the simplest way to include the effects brought by those non-pure speculative behaviors, though these effects should be further verified in a more concrete way as well.

Acknowledgments

This work was supported by JSPS KAKENHI grant number JP17J09156.

References

- [1] Mantegna, R. N., & Stanley, H. E. (2000). An introduction to econophysics: correlation and complexity in finance. Cambridge, UK: Cambridge University.

- [2] Gopikrishnan, P., Plerou, V., Liu, Y., Amaral, L. N., Gabaix, X., & Stanley, H. E. (2000). Scaling and correlation in financial time series. Physica A: Statistical Mechanics and its Applications, 287(3), 362-373.

- [3] Cont, R. (2001). Empirical properties of asset returns: stylized facts and statistical issues. QUANTITATIVE FINANCE, 1, 223-236.

- [4] Katahira, K., Chen, Y., Hashimoto, G., & Okuda, H. (2019). Development of an agent-based speculation game for higher reproducibility of financial stylized facts. Physica A: Statistical Mechanics and its Applications, 524, 503-518.

- [5] Challet, D., & Zhang, Y. C. (1997). Emergence of cooperation and organization in an evolutionary game. Physica A: Statistical Mechanics and its Applications, 246(407), 18.

- [6] Cont, R., & Bouchaud, J. P. (2000). Herd behavior and aggregate fluctuations in financial markets. Macroeconomic dynamics, 4(02), 170-196.

- [7] Katahira, K., & Akiyama, E. (2017) Minority Game in a Heterogeneous Population with Periodic Participations. Journal of Information Processing Society of Japan 58(1), 269-277 [published in Japanese].