\ul

Predicting Consumer Default:

A Deep Learning Approach††thanks: We are grateful to Dokyun Lee, Sera Linardi, Yildiray Yildirim, Albert Zelevev and seminar participants at the Financial Conduct Authority, the University of Pittsburgh, the European Central Bank, Baruch College and Goethe University for useful comments and suggestions. This research was supported by the National Science Foundation under Grant No. SES 1824321. This research was also supported in part by the University of Pittsburgh Center for Research Computing through the resources provided. Correspondence to: stefania.albanesi@gmail.com.

We develop a model to predict consumer default based on deep learning. We show that the model consistently outperforms standard credit scoring models, even though it uses the same data. Our model is interpretable and is able to provide a score to a larger class of borrowers relative to standard credit scoring models while accurately tracking variations in systemic risk. We argue that these properties can provide valuable insights for the design of policies targeted at reducing consumer default and alleviating its burden on borrowers and lenders, as well as macroprudential regulation.

JEL Codes: C45; D14; E27; E44; G21; G24.

Keywords: Consumer default; credit scores; deep learning; macroprudential policy.

1 Introduction

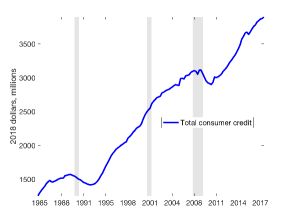

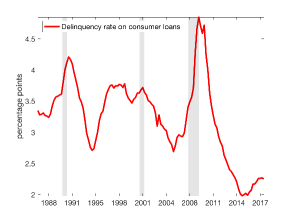

The dramatic growth in household borrowing since the early 1980s has increased the macroeconomic impact of consumer default. Figure 1 displays total consumer credit balances in millions of 2018 USD and the delinquency rate on consumer loans starting in 1985. The delinquency rate mostly fluctuates between 3 and 4%, except at the height of the Great Recession when it reached a peak of over 5%, and in its aftermath when it dropped to a low of 2%. With the rise in consumer debt, variations in the delinquency rate have an ever larger impact on household and financial firm balances sheets. Understanding the determinants of consumer default and predicting its variation over time and across types of consumers can not only improve the allocation of credit, but also lead to important insights for the design of policies aimed at preventing consumer default or alleviating its effects on borrowers and lenders. They are also critical for macroprudential policies, as they can assist with the assessment of the impact of consumer credit on the fragility of the financial system.

This paper proposes a novel approach to predicting consumer default based on deep learning. We rely on deep learning as this methodology is specifically designed for prediction in environments with high dimensional data and complicated non-linear patterns of interaction among factors affecting the outcome of interest, for which standard regression approaches perform poorly. Our methodology uses the same information as standard credit scoring models, which are one of the most important factors in the allocation of consumer credit. We show that our model improves the accuracy of default predictions while increasing transparency and accountability. It is also able to track variations in systemic risk, and is able to identify the most important factors driving defaults and how they change over time. Finally, we show that adopting our model can accrue substantial savings to borrowers and lenders.

Credit scores constitute one of the most important factors in the allocation of consumer credit in the United States. They are proprietary measures designed to rank borrowers based on their probability of future default. Specifically, they target the probability of a 90 days past due delinquency in the next 24 months.111The most commonly known is the FICO score, developed by the FICO corporation and launched in 1989. The three credit reporting companies or CRCs, Equifax, Experian and TransUnion have also partnered to produce VantageScore, an alternative score, which was launched in 2006. Credit scoring models are updated regularly. More information on credit scores is reported in Section 6.1 and Appendix D. Despite their ubiquitous use in the financial industry, there is very little information on credit scores, and emerging evidence suggests that as currently formulated credit scores have severe limitations. For example, \citeNNew_Narrative_NBER show that during the 2007-2009 housing crisis there was a marked rise in mortgage delinquencies and foreclosures among high credit score borrowers, suggesting that credit scoring models at the time did not accurately reflect the probability of default for these borrowers. Additionally, it is well known that credit scores and indiscriminately low for young borrowers, and a substantial fraction of borrowers are unscored, which prevents them from accessing conventional forms of consumer credit.

The Fair Credit Reporting Act, a legislation passed in 1970, and the Equal Opportunity in Credit Access Act of 1984 regulate credit scores and in particular determine which information can be included and must be excluded in credit scoring models. Such models can incorporate information in a borrower’s credit report, except age and location. These restrictions are intended to prevent discrimination by age and factors related to location, such as race.222Credit scoring models are also restricted by law from using information on race, color, gender, religion, marital status, salary, occupation, title, employer, employment history, nationality. The law also mandates that entities that provide credit scores make public the four most important factors affecting scores. In marketing information, these are reported to be payment history, which is stated to explain about 35% of variation in credit scores, followed by amounts owed, length of credit history, new credit and credit mix, explaining 30%, 15%, 10% and 10% of the variation in credit scores respectively. Other than this, there is very little public information on credit scoring models, though several services are now available that allow consumers to simulate how various scenarios, such as paying off balances or taking out new loans, will affect their scores.

The purpose of our analysis is to propose a model to predict consumer default that uses the same data as conventional credit scoring models, improves on their performance, benefiting both lenders and borrowers, and provides more transparency and accountability. To do so, we resort to deep learning, a type of machine learning ideally suited to high dimensional data, such as that available in consumer credit reports.333For excellent reviews of how machine learning can be applied in economics, see \citeNmullainathan2017machine and \citeNathey2019machine. Our model uses inputs as features, such as debt balances and number of trades, delinquency information, and attributes related to the length of a borrower’s credit history, to produce an individualized estimate that can be interpreted as a probability of default. We target the same default outcome as conventional credit scoring models, namely a 90+ days delinquency in the subsequent 8 quarters. For most of the analysis, we train the model on data for one quarter and test it on data 8 quarters ahead, in keeping with the default outcome we are considering, so that our predictions are truly out of sample. We present a variety of performance metrics suggesting that our model has very strong predictive ability. Accuracy, that is percent of observations correctly classified, is above 86% for all periods in our sample, and the AUC-Score, a commonly used metric in machine learning, is always above 92%.

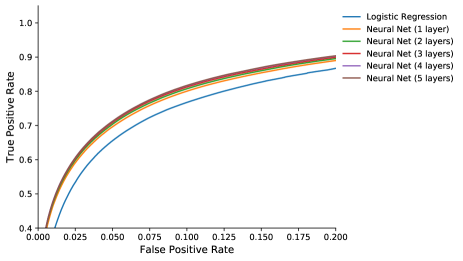

To better assess the validity of our approach, we compare our deep learning model to logistic regression and a number of other machine learning models. Deep learning models feature multiple hidden layers, designed to capture multi-dimensional feature interactions. By contrast, logistic regression can be interpreted as a neural network without any hidden layers. Our results suggest that deep learning is necessary to capture the complexity associated with default behavior, since all deep models perform substantially better than logistic regression. The importance of feature interaction reflects the complexity associated with default behavior. Additionally, our optimized model combines a deep neural network and gradient boosting and outperforms other machine learning models, such as random forests and decision trees, as well as deep neural networks and gradient boosting in isolation. However, all approaches show much stronger performance than logistic regression, suggesting that the main advantage is the adoption of a deep framework.

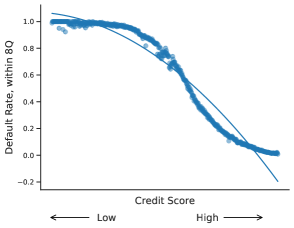

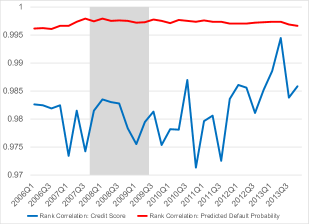

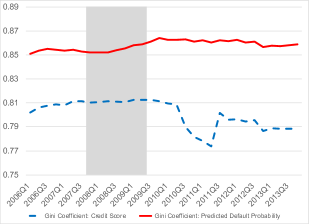

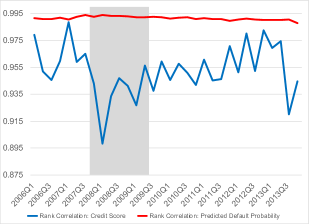

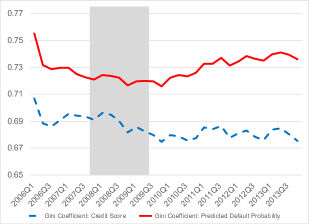

We also compare the performance of our model to a conventional credit score. By construction, credit scores only provide an ordinal ranking of consumers based on their default risk, and are not associated to a specific default probability. Yet, it is still possible to compare performance by assessing whether borrowers fall in different points of the distribution with the credit score compared to our model predictions. We find that our model performs significantly better than conventional credit scores. The rank correlation between realized default rates and the credit score is about 98%, where it is close to 1 for our model. Additionally, the Gini coefficient for the credit score, a measure of the ability to differentiate borrowers based on their credit score is approximately 81% and drops during the 2007-2009 crisis, while the Gini coefficient for our model is approximately 86% and stable over time. Perhaps most importantly, the credit score generates large disparities between the implied predicted probability of default and the realized default rate for large groups of customers, particularly at the low end of the credit score distribution. As an illustration, among Subprime borrowers, 17% display default behavior which is consistent with Near Prime borrowers and 15% display default behavior consistent with Deep Subprime. The default rates for Deep Subprime, Subprime and Near Prime borrowers are respectively 95%, 79% and 44%, so this misclassification is large, and it would imply large losses for lenders and borrowers in terms of missed revenues or higher interest rates. By contrast, the discrepancy between predicted and realized default rates for our model is never more than 4 percentage points for categories with at least a percent share of default risk.

Another advantage of our approach when compared to conventional credit scoring models is that we can generate a predicted probability of default for a much larger class of borrowers. Borrowers may be unscored because they do not have sufficient information in their credit report or because the information is stale, and approximately 8% of borrowers fall into this category.444See \citeNCFPB_2016_unscored. For more information, see Section 6.1.1. The absence of a credit score implies that these borrowers do not qualify for most types of credit and is very consequential. Our model can generate a predicted probability of default for all borrowers with a non-empty credit record. We achieve this in part by not including lags in our specification, which implies that only current information in a borrower’s credit report is used. This is not costly from a performance standpoint as many attributes used as inputs in the model are temporal in nature and capture lagged behavior, such as ”worst status on all trades in the last 6 months.”

We also examine the ability of our model to capture the evolution of aggregate default risk. Since our data set is nationally representative and we can score all borrowers with a non-empty credit record, the average predicted probability of default in the population based on our model corresponds to an estimate of aggregate default risk. We find that our model tracks the behavior of aggregate default rates remarkably well. It is able to capture the sharp rise in aggregate default rates in the run up and during the 2007-2009 crisis and also captures the inversion point and the subsequent drastic reduction in this variable. With the growth in consumer credit, household balance sheets have become very important for macroeconomic performance. Having an accurate assessment of the financial fragility of the household sector, as captured by the predicted probability of default on consumer credit has become crucially important and can aid in macro prudential regulation, as well as for designing fiscal and monetary policy responses to adverse aggregate economic shocks. This is another advantage of our model compared to credit scores, since the latter only provides an ordinal ranking of consumers with respect to their probability of default. Our model can provide such a ranking but in addition also provides an individual prediction of the default rate which can be aggregated into a systemic measure of default risk for the household sector.

As a final application, we compute the value to borrowers and lenders of using our model. For consumers, the comparison is made relative to the credit score. Specifically, we compute the credit card interest rate savings of being classified according to our model relative to the credit score. Being placed in a higher default risk category substantially increases the interest rates charged on credit cards at origination and increasingly so as more time lapses since origination, whereas being placed in a lower risk category reduces interest rate costs. We choose credit cards as they are a very popular form of unsecured debt, with 73% of consumers holding at least one credit or bank card. In percentage of credit cards balances, average net interest rate expense savings are approximately 5% for low credit score borrowers. These values constitute lower bounds as they do not include the higher fees and more stringent restrictions associated with credit cards targeted to low credit score borrowers and the increased borrowing limits available to higher credit score borrowers. For lenders, we calculated the value added by using our model in comparison to not having a prediction of default risk or having a prediction based on logistic regression. We use logistic regression for this exercise as it is understood to be the main methodology for conventional credit scoring models. Over a loan with a three year amortization period, we find that the gains relative to no forecast are in the order of 75% with a 15% interest rate, while the gains for relative to a model based on logistic regression are approximately 5%. These results suggest that both borrowers and lenders would experience substantial gains from switching to our model.

Our analysis contributes to the literature on consumer default in a variety of ways. We are the first to develop a prediction model of consumer default using credit bureau data that complies with all of the restrictions mandated by U.S. legislation in this area, and we do so using a large and temporally extended panel of data. This enables us to evaluate model performance in a setting that is closer to the one prevailing in the industry and to train and test our model in a variety of different macroeconomic conditions. Previous contributions either focus on particular types of default or use transaction data that is not admissible in conventional credit scoring models. The closest contributions to our work are \citeNkhandani, \citeNbutaru and \citeNsirignano. \citeNkhandani apply a decision tree approach to forecast credit card delinquencies with data for 2005-2009. They estimate cost savings of cutting credit lines based on their forecasts and calculate implied time series patterns of estimated delinquency rates. \citeNbutaru apply machine learning techniques to combined consumer trade line, credit bureau, and macroeconomic variables for 2009-2013 to predict delinquency. They find substantial heterogeneity in risk factors, sensitivities, and predictability of delinquency across lenders, implying that no single model applies to all institutions in their data. \citeNsirignano examine over 120 million mortgages between 1995 to 2014 to develop prediction models of multiple states, such as probabilities of prepayment, foreclosure and various types of delinquency. They use loan level and zip code level aggregate information, and provide a review of the literature using machine learning and deep learning in financial economics. \citeNkvamme2018 predict mortgage default using use convolutional neural networks and emphasize the advantages of deep learning, but they do not evaluate their models out of sample the way we do. Finally, \citeNlessmann reviews the recent literature on credit scoring, which is based on substantially smaller datasets than the one we have access to, and recommends random forests as a possible benchmark. However, we find that our hybrid model as well as our model components, a deep neural network and gradient boosted trees, improves substantially over random forests, possibly owing to recent methodological advances in deep learning, including the use of dropout, the introduction of new activation functions and the ability to train larger models.

Our model is interpretable, which implies that we are able to assess the most important factors associated with default behavior and how they vary over time. This information is important for lenders, and can be used to comply with legislation that requires lenders and credit score providers to notify borrowers of the most important factors affecting their credit score. Additionally, it can be used to formulate economic models of consumer default. The literature on consumer default555 Some notable contributions include \citeNchatterjee2007quantitative, \citeNlivshits2007consumer, and \citeNathreya2012quantitative. suggests that the determinants of default are related to preferences, such as impatience which increases the propensity to borrow, or adverse expenditure of income shocks. Based on these theories, it is then possible to construct theoretical models of credit scoring, of which \citeNchatterjee2016theory is a leading example. We find that the number of trades and the balance on outstanding loans are the most important factors associated with an increase in the probability of default, in addition to outstanding delinquencies and length of the credit history. This information can be used to improve models of consumer default risk and enhance their ability to be used for policy analysis and design.

We also identify and quantify a variety of limitations of conventional credit scoring models, particularly their tendency to misclassify borrowers by default risk, especially for relatively risky borrowers. This implies that our default predictions could help improve the allocation of credit in a way that benefits both lenders, in the form of lower losses, and borrowers, in the form of lower interest rates. Our results also speak to the perils associated with using conventional credit scores outside on the consumer credit sphere. As it is well known, credit scores are used to screen job applicants, in insurance applications, and a variety of additional settings. Economic theory would suggest that this is helpful, as long as credit score provide information which is correlated with characteristics that are of interest for the party using the score (\citeNCorbae_Glover_2018). However, as we show, conventional credit scores misclassify borrowers by a very large degree based on their default risk, which implies that they may not be accurate and may not include appropriate information or use adequate methodologies. The broadening use of credit scores would amplify the impact of these limitations.

The paper is structured as follows. Section 2 describes our data. Section 3 discusses the patterns of consumer default that motivate our adoption of deep learning. Section 4 describes our prediction problem and our model. Section 5 provides a comprehensive performance assessment of our model, compares it to other approaches, and uses a variety of interpretability techniques to understand which factors are strongly associated with default behavior. Section 6 compares our model to conventional credit scores, illustrates its performance in predicting and quantifying aggregate default risk and calculates the value added of adopting our model over alternatives for lenders and borrowers.

2 Data

We use anonymized credit file data from the Experian credit bureau. The data is quarterly, it starts in 2004Q1 and ends in 2015Q4. The data comprises over 200 variables for an anonymized panel of 1 million households. The panel is nationally representative, constructed from a random draw for the universe of borrowers with an Experian credit report. The attributes available comprise information on credit cards, bank cards, other revolving credit, auto loans, installment loans, business loans, first and second mortgages, home equity lines of credit, student loans and collections. There is information on the number of trades for each type of loan, the outstanding balance and available credit, the monthly payment, and whether any of the accounts are delinquent, specifically 30, 60, 90, 180 days past due, derogatory or charged off. All balances are adjusted for joint accounts to avoid double counting. Additionally, we have the number of hard inquiries by type of product, and public record items, such as bankruptcy by chapter, foreclosure and liens and court judgments. For each quarter in the sample, we also have each borrowers’s credit score. The data also includes an estimate of individual and household labor income based on IRS data. Because this is data drawn from credit reports, we do not know gender, marital status or any other demographic characteristic, though we do know a borrower’s address at the zip code level. We also do not have any information on asset holdings.

Table 1 reports basic demographic information on our sample, including age, household income, credit score and incidence of default, which here is defined as the fraction of households who report a 90 or more days past due delinquency on any trade. This will be our baseline definition of default, as this is the outcome targeted by credit scoring models. Approximately 34% of consumers display such a delinquency.

| Feature | Mean | Std. Dev. | Min | 25% | 50% | 75% | Max |

|---|---|---|---|---|---|---|---|

| Age | 45.8 | 16.3 | 18 | 32.2 | 45.1 | 57.8 | 83 |

| Household Income | 77.1 | 55.0 | 15 | 42 | 64 | 90 | 325 |

| Credit Score | 678.4 | 111.0 | 300 | 588 | 692 | 780 | 839 |

| Default within 8Q | 0.339 | 0.473 | 0 | 0 | 0 | 1 | 1 |

Credit score corresponds to Vantage Score 3. Household income is in USD thousands, trimmed at the 99th percentile. Source: Authors’ calculations based on Experian Data.

3 Patterns in Consumer Default

We now illustrate the complexity of the relation between the various factors that are considered important drivers of consumer default. Our point of departure are standard credit scoring models. While these models are proprietary, the Fair Credit Reporting Act of 1970 and the Equal Opportunity in Credit Access Act of 1984 mandate that the 4 most important factors determining the credit scores be disclosed, together with their importance in determining variation in credit scores. These include credit utilization and number of hard inquiries, which are supposed to capture a consumer’s demand for credit, the variety of debt products, which capture the consumer’s experience in managing credit, and the number and severity of delinquencies. Each of these factors is stated to account for 10-35% of the variation in credit scores. The length of the credit history is also seen as a proxy on a consumer’s experience in managing credit, and this is reported as accounting for 15% of the variation in credit scores.666For an overview of the information available to borrowers about the determinants for their credit score, see https://www.myfico.com/resources/credit-education/whats-in-your-credit-score. The models used to determine credit scores as a function of these attributes are not disclosed, but they are widely believed to be based on linear and logistic regression as well as score cards. Additionally, available credit scoring algorithms typically do not score all borrowers.

Subsequently, we illustrate the properties of consumer default that suggest deep learning might be a good candidate for developing a prediction model. Specifically, we show that default is a relatively rare but very persistent outcome, there are substantial non-linearities in the relation between default and plausible covariates, as well as high order interactions between covariates and default outcomes.

3.1 Default Transitions

The default outcome we consider is a 90+ days delinquency, which occurs if the borrower has missed scheduled payments on any product for 90 days or more.777For instance, if no payment has been made by the last day of the month within the past three months and the payment was due on the first day of the month three months ago. For credit cards, this occurs if the borrower does not make at least their minimum payment. This is the default outcome targeted by the most widely used credit scoring models, which rank consumers based on their probability of becoming 90+ days delinquent in the subsequent 8 quarters. We refer to borrowers who are either current or up to 60 days delinquent on their payments as current.

The transition matrix from current to 90+ days past due in the subsequent 8 quarters is given in Table 2. Clearly, the two states are both highly persistent, with a 77% of current customers remaining current in the next 8 quarters, and 93% of customers in default remaining in that state over the same time period. The probability of transition from current to default is 23%, while the probability of curing a delinquency with a transition from default to current is only 7%. These results suggest that default is a particularly persistent state, and predicting a transition into default is very valuable form the lender’s perspective, since they are unlikely to be able to recuperate their losses. But it is also quite difficult, as the current state is also very persistent.

| Current/Next 8Q | No default | Default |

|---|---|---|

| No default | 0.776 | 0.224 |

| Default | 0.073 | 0.927 |

Quarterly frequency of transition from current to default. Current corresponds to 0-89 day past due on any trade, Default corresponds to 90+ day past due on any trade in the subsequent 8 quarters. Source: Authors’ calculations based on Experian Data.

3.2 Non-linearities

Our model includes a relatively large list of features, which is presented in Table 19. The summary statistics for these features are reported in Table 20 in the Appendix. As is demonstrated in the table, there is a wide dispersion in the distribution of these variables. For example, the average balance on credit card trades is approximately $4,500, but the standard deviation, at $9,800, is more than twice as large. Similarly, average total debt balances are approximately $77,000, while the standard deviation is $170,000 and the 75th percentile $95,000, suggesting a high upper tail dispersion of this variable. The other features display similar patterns.

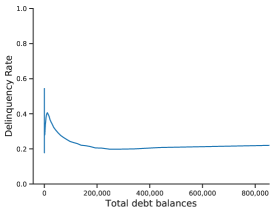

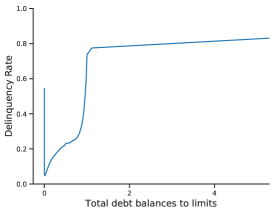

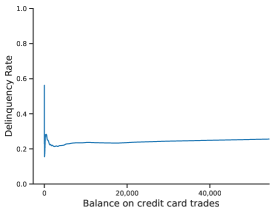

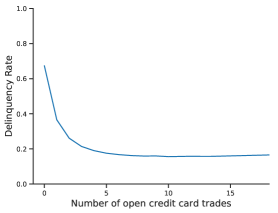

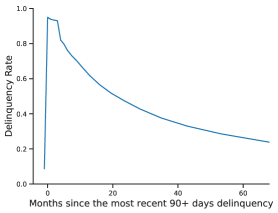

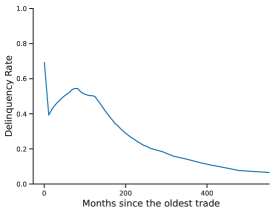

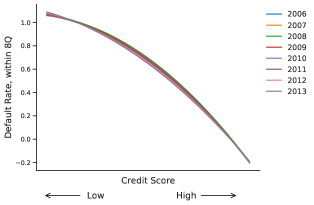

The features are used to predict the probability of default. We now illustrate the highly non-linear relation between the features and the incidence of default. Figure 2 shows how the default rate, defined as the fraction of borrowers with a 90+ day past due delinquency in the subsequent 8 quarters, varies with total debt balances, credit utilization, the credit limit on credit cards, the number of open credit card trades, the number of months since the most recent 90+ day past due delinquency and the months since the oldest trade was opened. The figures show that while the relation between the features and the incidence of default is mostly monotone, it is highly nonlinear, with vary little variation in the incidence of default for most intermediate values of the variable and much higher or lower values at the extremes of the range of each covariate. The variables in the figure are just illustrative, a similar pattern holds for most plausible features.

Delinquency rate is the fraction with 90+ days past due trades in subsequent 8 quarters. In panel (e) and (f), -1 implies no past delinquency. Source: Authors’ calculations based on Experian Data.

3.3 High Order Interactions

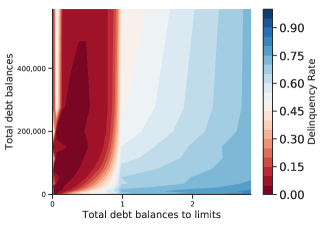

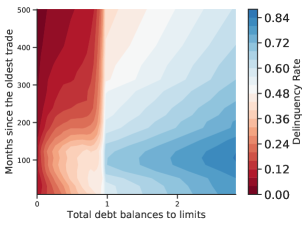

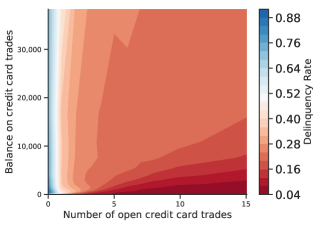

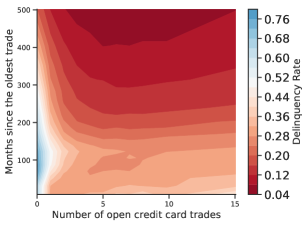

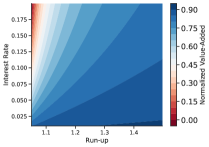

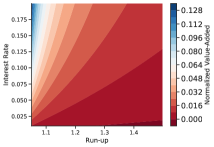

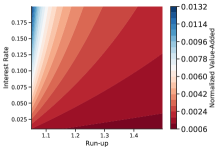

Multidimensional interactions are another feature of the relation between default and plausible covariates, that is default behavior is simultaneously related with multiple variables. To see this, Figure 3 presents contour plots of the relation between the incidence of default and couples of covariates. The covariates reported here are chosen since they are important driving factors in default decisions, based on our model, as discussed in Section 5.2. Panels (a) and (b) explore the joint variation in the incidence of default with total debt balances, credit utilization (total debt balances to limits), and credit history. Blue values correspond to high delinquency rates while red values to low delinquency rates. As can be seen from both panels, higher credit utilization corresponds to higher delinquency rate, but for given credit utilization, an increase in total debt balances first decreases then increases the delinquency rate, where the switch in sign depends on the utilization rate. For given utilization rates, a longer credit history first increases then decreases the delinquency rate, provided the utilization rate is smaller than 1.888Utilization rates above 1 can arise for a delinquent borrower if fees and other penalty add to their balances for given credit limits. Panels (c) and (d) explore the relation between default and credit card borrowing. Default rates decline with the number of credit cards, though for a given number of credit card trades, they mostly increase with credit card balances. This relation, however varies with the level of both variables. An increase in the length of credit history is typically associated with lower default rates, however, if the number of open credit cards is low, this relation is non-monotone. The variables reported in the figures are illustrative of a general pattern in the joint relation between couples of covariates and default rates.

Relationship between 90+ days past due delinquency rate and pairs of covariates. Source: Authors’ calculations based on Experian Data.

This pattern of multidimensional non-linear interactions across covariates is fairly difficult to model using standard econometric approaches. For this reason, we propose a deep learning approach to be explained below.

4 Model

Predicting consumer default maps well into a supervised learning framework, which is one of the most widely used techniques in the machine learning literature. In supervised learning, a learner takes in pairs of input/output data. The input data, which is typically a vector, represent pre-identified attributes, also known as features, that are used to determine the output value. Depending on the learning algorithm, the input data can contain continuous and/or discrete values with or without missing data. The supervised learning problem is referred to as a ”regression problem” when the output is continuous, and as a ”classification problem” when the output is discrete. Once the learner is presented with input/output data, its task is to find a function that maps the input vectors to the output values. A brute force way of solving this task is to memorize all previous values of input/output pairs. Though this perfectly maps the input data to the output values in the training data set, it is unlikely to succeed in forecasting the output values if (1) the input values are different from the ones in the training data set or (2) when the training data set contains noise. Consequently, the goal of supervised learning is to find a function that generalizes beyond the training set, so that it correctly forecasts out-of-sample outcomes. Adopting this machine-learning methodology, we build a model that predicts defaults for individual consumers. We define default as a 90+ days delinquency on any debt in the subsequent 8 quarters, which is the outcome targeted by conventional credit scoring models. Our model outputs a continuous variable between 0 and 1 that can be interpreted under certain conditions as an estimate of the probability of default for a particular borrower at a given point in time, given input variables from their credit reports.

We start by formalizing our prediction problem. We adopt a discrete-time formulation for periods 0,1,…,T, each corresponding to a quarter. We let the variable prescribe the state at time for individual with denoting the set of states. We define if a consumer is 90+ days past due on any trade and otherwise. Consumers will transition between these two states over their lifetime.

Our target outcome is 90+ days past due in the subsequent 8 quarters, defined as:

| (1) |

We allow the dynamics of the state process to be influenced by a vector of explanatory variables , which includes the state . In our empirical implementation, represents the features in Table 19. We fix a probability space and an information filtration . Then, we specify a probability transition function satisfying

| (2) |

where is a parameter to be estimated. Equation 2 gives the marginal conditional probability for the transition of individual ’s debt from its state at time to state at time given the explanatory variables .999The state encompasses realizations of the state between time and . Let denote the standard softmax function:

| (3) |

where . The vector output of the function is a probability distribution on .

The marginal probability defined in equation 2 is the theoretical counterpart of the empirical transition matrix reported in Table 2. We propose to model the transition function with a hybrid deep neural network/gradient boosting model, which combines the predictions of a deep neural network and an extreme gradient boosting model. We explain each of the component models and their properties and the rationale for combining them below.

4.1 Deep Neural Network

One component of our model is based on deep learning, in the class used by \citeNsirignano. We restrict attention to feed-forward neural networks, composed of an input layer, which corresponds to the data, one or more interacting hidden layers that non-linearly transform the data, and an output layer that aggregates the hidden layers into a prediction. Layers of the networks consist of neurons with each layer connected by synapses that transmit signals among neurons of subsequent layers. A neural network is in essence a sequence of nonlinear relationships. Each layer in the network takes the output from the previous layer and applies a linear transformation followed by an element-wise non-linear transformation.

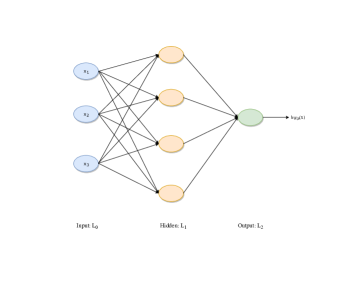

Figure 4 illustrates an example of a two layer neural network. This neural network has 3 input units (denoted ), 4 hidden units, and 1 output unit. Let denote the number of layers in this network (). We label layer as , where layer is the input layer, and layer is the output layer. The layers between the input () and the output layer () are called hidden layers. Given this notation, there are hidden layers, 1 in this specific example. A neural network without any hidden layers () is a logistic regression model.

There are two ways to increase the complexity a neural network: (1) increase the number of hidden layers and (2) increase the number of units in a given layer. Lower tier layers in the neural network learn simpler patterns, from which higher tier layers learn to produce more complex patterns. Given a sufficient number of neurons, neural networks can approximate continuous functions on compact sets arbitrarily well (see \citeNhornik1989 and \citeNhornik1991). This includes approximating interactions (i.e., the product and division of features). There are two main advantages of adding more layers over increasing the number of units to existing layers; (1) later layers build on early layers to learn features of greater complexity and (2) deep neural networks– those with three or more hidden layers– need exponentially fewer neurons than shallow networks (\citeNbengiolecun and \citeNmontufar).

In the neural network represented in Figure 4, the parameters to be estimated are , where denotes the weight associated with the connection between unit in layer and unit in layer , and is the bias associated with unit in layer . Thus, in this example . This implies that there are a total of 21 = (3+1)*4+5 parameters (four parameters to reach each neuron and five weights to aggregate the neurons into a single output). In general, the number of weight parameters in each hidden layer is , plus for the output layer, where denotes the number of neurons in each layer ,…, .

Let denote the activation (e.g., output value) of unit in layer . Fix and , our neural network defines a hypothesis that outputs a real number between 0 and 1.101010This is a property of the sigmoid activation function. Let denote the activation function that applies to vectors in an element-wise fashion. The computation this neural network represents, often referred to as forward propagation, can be written as:

There are many choices to make when structuring a neural network, including the number of hidden layers, the number of neurons in each layer, and the activation functions. We built a number of network architectures having up to fifteen hidden layers.111111The number of layers and the number of neurons in each layer, along with other hyperparameters of the model, are chosen by Tree-structured Parzen Estimator (TPE) approach. See Appendix C for more details. All architectures are fully connected so each unit receives an input from all units in the previous layer.

Neural networks tend to be low-bias, high-variance models, which imparts them a tendency to over-fit the data. We apply dropout to each of the layers to avoid over-fitting (see \citeNsrivastava). During training, neurons are randomly dropped (along with their connections) from the neural network with probability (referred to as the dropout rate), which prevents complex co-adaptations on training data.

We apply the same activation function (rectified linear unit or RELU) at all nodes, which is obtained via hyperparameter optimization,121212There are many potential choices for the nonlinear activation function, including the sigmoid, relu, and tanh. and defined as:

| (4) |

Let denote the number of neurons in each layer ,…, . Define the output of neuron in layer as . Then, define the vector of outputs (including the bias term ) for this layer as . For the input layer, define . Formally, the recursive output of the layer of the neural network is:

| (5) |

with final output:

| (6) |

The parameter specifying the neural network is:

| (7) |

4.2 Decision Tree Models

The second component of our model is Extreme Gradient Boosting, which builds on decision tree models. Tree-based models split the data several times based on certain cutoff values in the explanatory variables.131313Splitting means that different subsets of the dataset are created, where each observation belongs to one subset. For a review on decision trees, see \citeNkhandani. A number of such models have become quite prevalent in the literature, most notably random forests (see \citeNbreiman and \citeNbutaru) and Classification and Regression Trees, known as CART. We briefly review CART and then explain gradient boosting.

4.2.1 CART

There are a number of different decision tree-based algorithms. As an illustration of the approach, we describe Classification and Regression Trees or CART. CART models an outcome for an instance as follows:

| (8) |

where each observation belongs to exactly one subset . The identity function returns 1 if is in and 0 otherwise. If falls into , the predicted outcome is , where is the mean of all training observations in .

The estimation procedure takes a feature and computes the cut-off point that minimizes the Gini index of the class distribution of , which makes the two resulting subsets as different as possible. Once this is done for each feature, the algorithm uses the best feature to split the data into two subsets. The algorithm is then repeated until a stopping criterium is reached.

Tree-based models have a number of advantages that make them popular in applications. They are invariant to monotonic feature transformations and can handle categorical and continuous data in the same model. Like deep neural networks, they are well suited to capturing interactions between variables in the data. Specifically, a tree of depth can capture interactions. The interpretation is straightforward, and provides immediate counterfactuals: ”If feature had been bigger / smaller than the split point, the prediction would have been instead of .” However, these models also have a number of limitations. They are poor at handling linear relationships, since tree algorithms rely on splitting the data using step functions, an intrinsically non-linear transformation. Trees also tend to be unstable, so that small changes in the training dataset might generate a different tree. They are also prone to overfitting to the training data. For more information on tree-based models see \citeNmolnar.

4.2.2 eXtreme Gradient Boosting (XGBoost)

Gradient Boosted Trees (GBT) are an ensemble learning method that corrects for tree-based models’ tendency to overfit to training data by recursively combining the forecasts of many over-simplified trees. Though shallow trees are ”weak learners” on their own with little predictive power, the theory behind boosting proposes that a collection of weak learners, as an ensemble, creates a single strong learner with improved stability over a single complex tree.

At each step m, , of gradient boosting, an estimator, , is computed on the residuals from the previous models predictions. A critical part of gradient boosting method is regularization by shrinkage as proposed by \citeNfriedman. This consists in modifying the update rule as follows:

| (9) |

where represents a weak learner of fixed depth, is the step length and is the learning rate or shrinkage factor.

XGBoost is a fast implementation of Gradient Boosting, which has the advantages of fast speed and high accuracy. For classification, XGBoost combines the principles of decision trees and logistic regression, so that the output of our XGBoost model is a number between 0 and 1. For the remainder of the paper we refer to XGBoost as GBT.141414For more on XGBoost, see \citeNchen2018hybrid and \citeNren2017novel.

4.3 Hybrid DNN-GBT Model

We examined two techniques to create a hybrid DNN-GBT ensemble model. Ensemble models combine multiple learning algorithms to generate superior predictive performance than could be obtained from any of the constituent learning algorithms alone. The first method combines the two models by replacing the final layer of the neural network with a gradient boosted trees model. Examples of this approach are \citeNchen2018hybrid and \citeNren2017novel. The second, uses both models separately and then averages out the final predicted probabilities of the two models. We found the latter to perform better on our dataset. This method is similar to \citeNkvamme2018, who combined a convolutional neural network with a random forest by averaging. Thus, our methodology relies on combining the output of the deep neural network with the output of a gradient boosted trees model. This is achieved in two steps:

-

1.

For each observation, run DNN and GBT separately and obtain predicted probabilities for each of the models;

-

2.

Take the arithmetic mean of the predicted probabilities.151515We have investigated alternative weighting schemes, and the results are reported in Table 18.

5 Implementation

Table 19 lists the features from the credit report data we use as inputs in the model. These covariates are chosen based on economic theory (see for example \citeNchatterjee2007quantitative) as well as based on information from currently used credit scoring models. They include information on balances and credit limits for different types of consumer debt, severity and number of delinquencies, credit utilization by type of product, public record items such as bankruptcy filings by chapter and foreclosure, collection items, and length of the credit history. In order to be consistent with the restrictions of the Fair Credit Reporting Act on 1970 and the Equal Opportunity in Credit Access Act of 1984 we do not include information on age or zip code, and we do not include any information on income, to be consistent with current credit scoring models. Table 19 lists the full set of features used in our machine learning models.

It is important to note that we do not use any lagged features. This is because many of the features have a temporal dimension, for example ”worst present status on any traded in the last 6 months.” Importantly, excluding lags enables us to provide a default prediction to any borrower with a non-empty credit record, which implies that we can score virtually all consumers.

5.1 Classifier Performance

In this section, we describe the performance of our hybrid model under various training and testing windows. First, we evaluate our model on the pooled sample (2004Q1-2013Q4), where we apply a random 60%-20%-20% split to our training, validation, and testing sets. Then, to account for look-ahead bias, we train and test our models based on 8 quarter windows that were observable at the time of forecast. In particular, we require our training and testing sets to be separated by 8 quarters to avoid overlap. For instance, the second out-of-sample model was calibrated using input data from 2004Q2, from which the parameter estimates were applied to the input data in 2006Q2 to generate forecasts of delinquencies over the 8 quarter window from 2006Q3-2008Q2. This gives us a total of 32+1 calibration and testing periods reported in Table 3. The percentage of 90+ days past due accounts within 8 quarters varies from 32.5% to 35.9%.

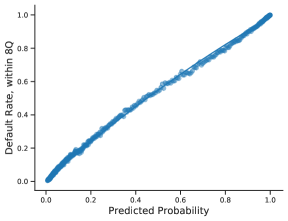

The hybrid model outputs a continuous variable that, under certain circumstances, can be interpreted as an estimate of the probability of an account becoming 90+ days delinquent during the subsequent 8 quarters. One measure of the model’s success is its ability to differentiate between accounts that did become delinquent and those that did not; if these two groups have the same forecasts, the model provides no value. Table 3 presents the average forecast for accounts that did and did not fall into the 90+ days delinquency category over the 32+1 evaluation periods. For instance, during the testing period for 2010Q4, the model’s average prediction among the 35.44% of accounts that became 90+ days delinquent was 73.17%, while the average prediction among the 64.56% of accounts that did not was 16.03%. We should highlight that these are truly out-of-sample predictions, since the model is calibrated using input data from 2008Q4. This shows the forecasting power of our model in distinguishing between accounts that will and will not become delinquent within 8 quarters. Furthermore, this forecasting power seems to be stable over the 32+1 calibration and evaluation periods, partly driven by the frequent re-calibration of the model that captures some of the changing dynamics of consumer behavior.

| Training Window | Testing Window | Data | Predicted | Delinquents | Non-Delinquents |

|---|---|---|---|---|---|

| 2004Q1-2013Q4 | 2004Q1-2013Q4 | 0.3396 | 0.3354 | 0.7516 | 0.1213 |

| 2004Q1 | 2006Q1 | 0.3248 | 0.2919 | 0.6508 | 0.1192 |

| 2004Q2 | 2006Q2 | 0.3274 | 0.3042 | 0.6732 | 0.1246 |

| 2004Q3 | 2006Q3 | 0.3306 | 0.3102 | 0.6838 | 0.1256 |

| 2004Q4 | 2006Q4 | 0.3347 | 0.3128 | 0.6843 | 0.1260 |

| 2005Q1 | 2007Q1 | 0.3410 | 0.3160 | 0.6851 | 0.1251 |

| 2005Q2 | 2007Q2 | 0.3444 | 0.3196 | 0.6861 | 0.1271 |

| 2005Q3 | 2007Q3 | 0.3469 | 0.3201 | 0.6847 | 0.1265 |

| 2005Q4 | 2007Q4 | 0.3505 | 0.3307 | 0.6972 | 0.1329 |

| 2006Q1 | 2008Q1 | 0.3535 | 0.3370 | 0.7090 | 0.1335 |

| 2006Q2 | 2008Q2 | 0.3545 | 0.3340 | 0.6982 | 0.1341 |

| 2006Q3 | 2008Q3 | 0.3558 | 0.3338 | 0.7019 | 0.1305 |

| 2006Q4 | 2008Q4 | 0.3587 | 0.3429 | 0.7121 | 0.1364 |

| 2007Q1 | 2009Q1 | 0.3588 | 0.3483 | 0.7223 | 0.1391 |

| 2007Q2 | 2009Q2 | 0.3580 | 0.3507 | 0.7259 | 0.1415 |

| 2007Q3 | 2009Q3 | 0.3573 | 0.3525 | 0.7279 | 0.1437 |

| 2007Q4 | 2009Q4 | 0.3589 | 0.3540 | 0.7277 | 0.1448 |

| 2008Q1 | 2010Q1 | 0.3589 | 0.3612 | 0.7359 | 0.1514 |

| 2008Q2 | 2010Q2 | 0.3568 | 0.3630 | 0.7366 | 0.1558 |

| 2008Q3 | 2010Q3 | 0.3559 | 0.3635 | 0.7365 | 0.1574 |

| 2008Q4 | 2010Q4 | 0.3544 | 0.3628 | 0.7317 | 0.1603 |

| 2009Q1 | 2011Q1 | 0.3541 | 0.3577 | 0.7282 | 0.1545 |

| 2009Q2 | 2011Q2 | 0.3511 | 0.3591 | 0.7265 | 0.1603 |

| 2009Q3 | 2011Q3 | 0.3500 | 0.3555 | 0.7248 | 0.1566 |

| 2009Q4 | 2011Q4 | 0.3484 | 0.3538 | 0.7242 | 0.1558 |

| 2010Q1 | 2012Q1 | 0.3467 | 0.3559 | 0.7331 | 0.1557 |

| 2010Q2 | 2012Q2 | 0.3434 | 0.3498 | 0.7264 | 0.1528 |

| 2010Q3 | 2012Q3 | 0.3396 | 0.3498 | 0.7295 | 0.1546 |

| 2010Q4 | 2012Q4 | 0.3358 | 0.3488 | 0.7326 | 0.1547 |

| 2011Q1 | 2013Q1 | 0.3341 | 0.3481 | 0.7350 | 0.1540 |

| 2011Q2 | 2013Q2 | 0.3317 | 0.3440 | 0.7305 | 0.1522 |

| 2011Q3 | 2013Q3 | 0.3298 | 0.3440 | 0.7342 | 0.1520 |

| 2011Q4 | 2013Q4 | 0.3275 | 0.3400 | 0.7299 | 0.1501 |

Performance metrics for our model of default risk over 32+1 testing windows. For each testing window, the model is calibrated on data over the period specified in the training window, and predictions are based on the data available as of the data in the training window. For example, the fourth row reports the performance of the model calibrated using input data available in 2004Q3, and applied to 2006Q3 data to generate forecasts of delinquencies for within 8 quarter delinquencies. Average model forecasts over all customers, and customers that (ex-post) did and did not become 90+ days delinquent over the testing window are also reported. Source: Authors’ calculations based on Experian Data.

We also look at accounts that are current as of the forecast date but become 90+ days delinquent within the subsequent 8 quarters. In particular, we contrast the model’s average prediction among individuals who were current on their accounts but became 90+ days delinquent with the average prediction among customers who were current and did not become delinquent. Given the difficulty of predicting default among individuals that currently show no sign of delinquency, we anticipate the model’s performance to be less impressive than the values reported in Table 3. Nonetheless, the values reported in Table 4 indicate that the model is able to distinguish between these two populations. For instance, using input data from 2008Q4, the average model prediction for individuals who were current on their debts and became 90+ days delinquent is 45.13%, contrasted with 12.48% for those who did not. As in Table 3, the model’s ability to distinguish between these two classes is consistent across the 32+1 evaluation periods listed in Table 4.

| Training Window | Testing Window | Data | Predicted | Delinquent | Non-delinquent |

|---|---|---|---|---|---|

| 2004Q1-2013Q4 | 2004Q1-2013Q4 | 0.1676 | 0.1616 | 0.5253 | 0.088 |

| 2004Q1 | 2006Q1 | 0.1844 | 0.1540 | 0.4232 | 0.0931 |

| 2004Q2 | 2006Q2 | 0.1702 | 0.1467 | 0.3970 | 0.0954 |

| 2004Q3 | 2006Q3 | 0.1695 | 0.1467 | 0.3974 | 0.0956 |

| 2004Q4 | 2006Q4 | 0.1727 | 0.1473 | 0.3995 | 0.0947 |

| 2005Q1 | 2007Q1 | 0.1805 | 0.1515 | 0.4012 | 0.0964 |

| 2005Q2 | 2007Q2 | 0.1813 | 0.1521 | 0.3948 | 0.0983 |

| 2005Q3 | 2007Q3 | 0.1831 | 0.1502 | 0.3873 | 0.0971 |

| 2005Q4 | 2007Q4 | 0.1847 | 0.1567 | 0.4031 | 0.1008 |

| 2006Q1 | 2008Q1 | 0.1890 | 0.1628 | 0.4177 | 0.1033 |

| 2006Q2 | 2008Q2 | 0.1896 | 0.1619 | 0.4077 | 0.1044 |

| 2006Q3 | 2008Q3 | 0.1872 | 0.1558 | 0.3979 | 0.1000 |

| 2006Q4 | 2008Q4 | 0.1817 | 0.1588 | 0.4043 | 0.1043 |

| 2007Q1 | 2009Q1 | 0.1781 | 0.1618 | 0.4167 | 0.1066 |

| 2007Q2 | 2009Q2 | 0.1752 | 0.1638 | 0.4223 | 0.1089 |

| 2007Q3 | 2009Q3 | 0.1713 | 0.1660 | 0.4290 | 0.1116 |

| 2007Q4 | 2009Q4 | 0.1661 | 0.1627 | 0.4170 | 0.1120 |

| 2008Q1 | 2010Q1 | 0.1683 | 0.1717 | 0.4396 | 0.1175 |

| 2008Q2 | 2010Q2 | 0.1668 | 0.1772 | 0.4519 | 0.1221 |

| 2008Q3 | 2010Q3 | 0.1661 | 0.1793 | 0.4580 | 0.1238 |

| 2008Q4 | 2010Q4 | 0.1644 | 0.1785 | 0.4513 | 0.1248 |

| 2009Q1 | 2011Q1 | 0.1674 | 0.1764 | 0.4529 | 0.1208 |

| 2009Q2 | 2011Q2 | 0.1668 | 0.1805 | 0.4593 | 0.1247 |

| 2009Q3 | 2011Q3 | 0.1669 | 0.1769 | 0.4555 | 0.1211 |

| 2009Q4 | 2011Q4 | 0.1597 | 0.1716 | 0.4431 | 0.1200 |

| 2010Q1 | 2012Q1 | 0.1604 | 0.1725 | 0.4500 | 0.1195 |

| 2010Q2 | 2012Q2 | 0.1622 | 0.1694 | 0.4478 | 0.1155 |

| 2010Q3 | 2012Q3 | 0.1598 | 0.1678 | 0.4450 | 0.1151 |

| 2010Q4 | 2012Q4 | 0.1575 | 0.1667 | 0.4459 | 0.1145 |

| 2011Q1 | 2013Q1 | 0.1606 | 0.1708 | 0.4601 | 0.1154 |

| 2011Q2 | 2013Q2 | 0.1603 | 0.1695 | 0.4579 | 0.1144 |

| 2011Q3 | 2013Q3 | 0.1578 | 0.1660 | 0.4525 | 0.1123 |

| 2011Q4 | 2013Q4 | 0.1548 | 0.1622 | 0.4442 | 0.1106 |

Performance metrics for our model of default risk over 32+1 testing windows for customers who are current as of the forecast date but become 90+ days delinquent in the following 8 quarters. For each testing window, the model is calibrated on data over the period specified in the training window columns, and predictions are based on the data available as of the data in the training window. For example, the fourth row reports the performance of the model calibrated using input data available in 2004Q3, and applied to 2006Q3 data to generate forecasts of delinquencies for within 8 quarter delinquencies. Average model forecasts over all current customers, and all current customers that did and did not become 90+ days delinquent over the testing window are also reported. Source: Authors’ calculations based on Experian Data.

Under certain conditions, the forecasts generated by our model can be converted to binary decisions by comparing the forecast to a specified threshold and classifying accounts with scores exceeding that threshold as high-risk. Setting the threshold level comes with a trade-off. A low level threshold leads to many accounts being classified as high risk, and even though this approach may accurately capture customers who are actually high-risk and about to default on their payments, it can also give rise to many low-risk accounts incorrectly classified as high-risk. By contrast, a high threshold can result in too many high-risk accounts being classified as low-risk.

This type of trade-off is inherent in any classification problem, and involves trading off Type-I (false positives) and Type-II (false negatives) errors in a classical hypothesis testing context. In the credit risk management context, a cost/benefit analysis can be formulated contrasting false positives to false negatives to make this trade-off explicit, and applying the threshold that will optimize an objective function in which costs and benefits associated with false positives and false negatives are inputs.

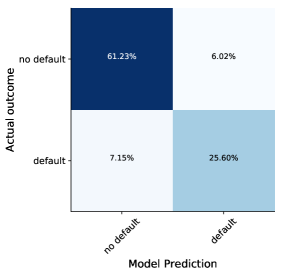

A commonly used performance metric in the machine learning and statistics literature is a contingency table, often referred to as the confusion matrix, that describes the statistical behavior of any classification algorithm. In our application, the two rows correspond to ex post realizations of the two types of accounts in our sample, no default and default. We define no default accounts as those who do not become 90+ days delinquent during the forecast period, and default accounts as those who do. The two columns correspond to ex ante classifications of the accounts into these categories. If a predictive model is applied to a set of accounts, each account falls into one of the four cells in the confusion matrix, thus the performance of the model can be assessed by the relative frequencies of the entries. In the Neymann-Pearson hypothesis-testing framework, the lower-left entry is defined as Type-I error and the upper right as Type-II error, while the objective of the researcher is to minimize Type-II error (i.e., maximize ”power”) subject to a fixed level of Type-I error (i.e., ”size”).

As an illustration, Figure 5 Panel (a) shows the confusion matrix for our hybrid DNN-GBT model calibrated using 2011Q4 data and evaluated on 2013Q4 data and a threshold of 50%. This means that accounts with estimated delinquency probabilities greater than 50% are classified as default and 50% or below as no default. For this quarter, the model classified 61.23% + 7.15% = 68.38% of the accounts as no default, of which 61.23% did indeed not default and 7.15% actually defaulted, that is, they were 90+ days delinquent in the subsequent 8 quarters. By the same token, of the 6.02% + 25.60% = 31.62% borrowers who defaulted, the model accurately classified 25.60%. Thus, the model’s accuracy, defined as the percent of instances correctly classified, is the sum of the entries on the diagonal of the confusion matrix, that is, 61.23 % + 25.60% = 86.83%.

We can compute three additional performance metrics from the entries of the confusion matrix, which we describe heuristically here and define formally in the appendix. Precision measures the model’s accuracy in instances that are classified as default. Recall refers to the number of accounts that defaulted as identified by the model divided by the actual number of defaulting accounts. Finally, the F-measure is simply the harmonic mean of precision and recall. In an ideal scenario, we would have very high precision and recall.

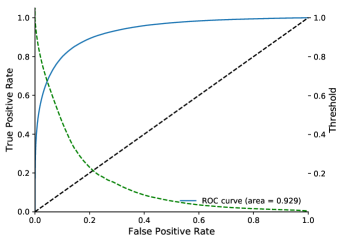

We can track the trade-off between true and false positives by varying the classification threshold of our model, and this trade-off is plotted in Figure 5 Panel (b). The blue line, called the Receiver Operating Characteristic (ROC) curve, is the pairwise plot of true and false positive rates for different classification thresholds (green line), and as the threshold decreases, the figure shows that the true positive rate increases, but so does the false positive rate. The ROC curve illustrates the non-linear nature of the trade-offs, implying that increase in true positive rates is not always proportionate with the increase in false positive rates. The optimal threshold then considers the cost of false positives with respect to the gain of true positives. If these are equal, the optimal threshold will correspond to the tangent point of the ROC curve with the 45 degree line.

The last performance metric we consider is the area under the ROC curve, known as AUC score, which is a widely used measure in the machine-learning literature for comparing models. It can be interpreted as the probability of the classifier assigning a higher probability of being in default to an account that is actually in default. The ROC area of our model ranges from 0.9239 to 0.9305, demonstrating that our machine-learning classifiers have strong predictive power in separating the two classes.

| Training Window | Testing Window | AUC score | Precision | Recall | F-measure | Accuracy | Loss |

|---|---|---|---|---|---|---|---|

| 2004Q1-2013Q4 | 2004Q1-2013Q4 | 0.9527 | 0.8662 | 0.8061 | 0.8351 | 0.8918 | 0.2609 |

| 2004Q1 | 2006Q1 | 0.9244 | 0.8551 | 0.6988 | 0.7691 | 0.8637 | 0.3236 |

| 2004Q2 | 2006Q2 | 0.9254 | 0.8488 | 0.7178 | 0.7779 | 0.8657 | 0.3181 |

| 2004Q3 | 2006Q3 | 0.9262 | 0.8494 | 0.7253 | 0.7824 | 0.8667 | 0.3164 |

| 2004Q4 | 2006Q4 | 0.9251 | 0.8499 | 0.7255 | 0.7828 | 0.8653 | 0.3203 |

| 2005Q1 | 2007Q1 | 0.9257 | 0.8583 | 0.7209 | 0.7836 | 0.8642 | 0.3211 |

| 2005Q2 | 2007Q2 | 0.9256 | 0.8595 | 0.7220 | 0.7848 | 0.8636 | 0.3221 |

| 2005Q3 | 2007Q3 | 0.9249 | 0.8624 | 0.7169 | 0.7829 | 0.8621 | 0.3254 |

| 2005Q4 | 2007Q4 | 0.9239 | 0.8558 | 0.7278 | 0.7866 | 0.8616 | 0.3273 |

| 2006Q1 | 2008Q1 | 0.9252 | 0.8522 | 0.7371 | 0.7905 | 0.8619 | 0.3263 |

| 2006Q2 | 2008Q2 | 0.9247 | 0.8570 | 0.7286 | 0.7876 | 0.8607 | 0.3272 |

| 2006Q3 | 2008Q3 | 0.9255 | 0.8604 | 0.7270 | 0.7881 | 0.8609 | 0.3265 |

| 2006Q4 | 2008Q4 | 0.9261 | 0.8564 | 0.7386 | 0.7931 | 0.8618 | 0.3248 |

| 2007Q1 | 2009Q1 | 0.9279 | 0.8528 | 0.7489 | 0.7975 | 0.8635 | 0.3207 |

| 2007Q2 | 2009Q2 | 0.9281 | 0.8487 | 0.7569 | 0.8002 | 0.8647 | 0.3195 |

| 2007Q3 | 2009Q3 | 0.9289 | 0.8467 | 0.7617 | 0.8020 | 0.8656 | 0.3170 |

| 2007Q4 | 2009Q4 | 0.9305 | 0.8524 | 0.7640 | 0.8058 | 0.8678 | 0.3129 |

| 2008Q1 | 2010Q1 | 0.9302 | 0.8401 | 0.7802 | 0.8091 | 0.8678 | 0.3141 |

| 2008Q2 | 2010Q2 | 0.9299 | 0.8345 | 0.7845 | 0.8087 | 0.8676 | 0.3147 |

| 2008Q3 | 2010Q3 | 0.9297 | 0.8326 | 0.7859 | 0.8086 | 0.8676 | 0.3145 |

| 2008Q4 | 2010Q4 | 0.9295 | 0.8339 | 0.7818 | 0.8070 | 0.8675 | 0.3158 |

| 2009Q1 | 2011Q1 | 0.9302 | 0.8406 | 0.7773 | 0.8077 | 0.8689 | 0.3135 |

| 2009Q2 | 2011Q2 | 0.9289 | 0.8332 | 0.7790 | 0.8051 | 0.8676 | 0.3163 |

| 2009Q3 | 2011Q3 | 0.9294 | 0.8397 | 0.7719 | 0.8043 | 0.8686 | 0.3142 |

| 2009Q4 | 2011Q4 | 0.9296 | 0.8365 | 0.7736 | 0.8038 | 0.8684 | 0.3135 |

| 2010Q1 | 2012Q1 | 0.9301 | 0.8313 | 0.7802 | 0.8049 | 0.8689 | 0.3120 |

| 2010Q2 | 2012Q2 | 0.9290 | 0.8312 | 0.7724 | 0.8008 | 0.8680 | 0.3136 |

| 2010Q3 | 2012Q3 | 0.9288 | 0.8275 | 0.7735 | 0.7996 | 0.8683 | 0.3123 |

| 2010Q4 | 2012Q4 | 0.9280 | 0.8177 | 0.7775 | 0.7971 | 0.8671 | 0.3146 |

| 2011Q1 | 2013Q1 | 0.9288 | 0.8143 | 0.7815 | 0.7976 | 0.8674 | 0.3123 |

| 2011Q2 | 2013Q2 | 0.9284 | 0.8139 | 0.7787 | 0.7959 | 0.8675 | 0.3120 |

| 2011Q3 | 2013Q3 | 0.9288 | 0.8097 | 0.7820 | 0.7956 | 0.8675 | 0.3109 |

| 2011Q4 | 2013Q4 | 0.9292 | 0.8095 | 0.7817 | 0.7954 | 0.8683 | 0.3085 |

Performance metrics for our model of default risk. The model calibrations are specified by the training and testing windows. The results of classifications versus actual outcomes over the following 8Q are used to calculate these performance metrics for 90+ days delinquencies within 8Q. Source: Authors’ calculations based on Experian Data.

Table 5 reports the performance metrics widely used in the machine-learning literature for each of the 32+1 models discussed. Our models exhibit strong predictive power across the various performance metrics. For instance, the 85.70% precision implies that when our classifier predicts that someone is going to default, there is an 85.70% chance this person will actually default; while the 72.86% recall means that we accurately identified 72.86% of all the defaulters. Our approach of using only one quarter of data to train the model is rather restrictive. Using more quarters usually increases model performance, so since most credit scoring applications will use a training data that exceeds one quarter, performance metrics are likely to improve relative to what we report in our exercise.

| Training Window | Testing Window | AUC score | Precision | Recall | F-measure | Accuracy | Loss |

|---|---|---|---|---|---|---|---|

| 2004Q1-2013Q4 | 2004Q1-2013Q4 | 0.9263 | 0.7974 | 0.5465 | 0.6485 | 0.9007 | 0.2423 |

| 2004Q1 | 2006Q1 | 0.8774 | 0.7744 | 0.3960 | 0.5240 | 0.8673 | 0.3174 |

| 2004Q2 | 2006Q2 | 0.8657 | 0.7288 | 0.3567 | 0.4790 | 0.8680 | 0.3156 |

| 2004Q3 | 2006Q3 | 0.8642 | 0.7232 | 0.3564 | 0.4775 | 0.8678 | 0.3168 |

| 2004Q4 | 2006Q4 | 0.8642 | 0.7256 | 0.3643 | 0.4851 | 0.8664 | 0.3206 |

| 2005Q1 | 2007Q1 | 0.8642 | 0.7394 | 0.3611 | 0.4853 | 0.8617 | 0.3289 |

| 2005Q2 | 2007Q2 | 0.8616 | 0.7331 | 0.3499 | 0.4737 | 0.8590 | 0.3329 |

| 2005Q3 | 2007Q3 | 0.8606 | 0.7439 | 0.3349 | 0.4618 | 0.8571 | 0.3370 |

| 2005Q4 | 2007Q4 | 0.8601 | 0.7270 | 0.3585 | 0.4802 | 0.8566 | 0.3380 |

| 2006Q1 | 2008Q1 | 0.8621 | 0.7207 | 0.3787 | 0.4965 | 0.8548 | 0.3403 |

| 2006Q2 | 2008Q2 | 0.8614 | 0.7264 | 0.3628 | 0.4839 | 0.8532 | 0.3414 |

| 2006Q3 | 2008Q3 | 0.8606 | 0.7280 | 0.3479 | 0.4708 | 0.8536 | 0.3420 |

| 2006Q4 | 2008Q4 | 0.8577 | 0.7115 | 0.3522 | 0.4712 | 0.8564 | 0.3366 |

| 2007Q1 | 2009Q1 | 0.8602 | 0.7050 | 0.3714 | 0.4865 | 0.8604 | 0.3286 |

| 2007Q2 | 2009Q2 | 0.8596 | 0.6920 | 0.3833 | 0.4934 | 0.8621 | 0.3256 |

| 2007Q3 | 2009Q3 | 0.8597 | 0.6826 | 0.3922 | 0.4981 | 0.8646 | 0.3208 |

| 2007Q4 | 2009Q4 | 0.8578 | 0.6859 | 0.3736 | 0.4838 | 0.8675 | 0.3163 |

| 2008Q1 | 2010Q1 | 0.8609 | 0.6794 | 0.4175 | 0.5172 | 0.8688 | 0.3151 |

| 2008Q2 | 2010Q2 | 0.8617 | 0.6662 | 0.4364 | 0.5273 | 0.8695 | 0.3135 |

| 2008Q3 | 2010Q3 | 0.8620 | 0.6595 | 0.4483 | 0.5338 | 0.8699 | 0.3126 |

| 2008Q4 | 2010Q4 | 0.8638 | 0.6710 | 0.4376 | 0.5298 | 0.8723 | 0.3092 |

| 2009Q1 | 2011Q1 | 0.8665 | 0.6871 | 0.4381 | 0.5351 | 0.8725 | 0.3086 |

| 2009Q2 | 2011Q2 | 0.8671 | 0.6784 | 0.4517 | 0.5424 | 0.8728 | 0.3085 |

| 2009Q3 | 2011Q3 | 0.8685 | 0.6899 | 0.4377 | 0.5356 | 0.8733 | 0.3068 |

| 2009Q4 | 2011Q4 | 0.8658 | 0.6802 | 0.4223 | 0.5211 | 0.8760 | 0.3025 |

| 2010Q1 | 2012Q1 | 0.8669 | 0.6723 | 0.4332 | 0.5269 | 0.8752 | 0.3024 |

| 2010Q2 | 2012Q2 | 0.8690 | 0.6894 | 0.4241 | 0.5252 | 0.8756 | 0.3018 |

| 2010Q3 | 2012Q3 | 0.8683 | 0.6861 | 0.4200 | 0.5211 | 0.8766 | 0.3001 |

| 2010Q4 | 2012Q4 | 0.8672 | 0.6784 | 0.4187 | 0.5178 | 0.8772 | 0.2988 |

| 2011Q1 | 2013Q1 | 0.8700 | 0.6734 | 0.4462 | 0.5367 | 0.8763 | 0.2996 |

| 2011Q2 | 2013Q2 | 0.8705 | 0.6746 | 0.4452 | 0.5364 | 0.8767 | 0.2985 |

| 2011Q3 | 2013Q3 | 0.8695 | 0.6721 | 0.4374 | 0.5299 | 0.8775 | 0.2970 |

| 2011Q4 | 2013Q4 | 0.8679 | 0.6668 | 0.4343 | 0.5260 | 0.8789 | 0.2951 |

Performance metrics for our model of default risk for the current population. Borrowers who are current do not have any delinquencies. The model calibrations are specified by the training and testing windows. The results of classifications versus actual outcomes over the following 8Q are used to calculate these performance metrics for 90+ days delinquencies within 8Q. Source: Authors’ calculations based on Experian Data.

Table 6 reports the same performance metrics for the population of borrowers who are current, that is, they do not have any delinquencies in the quarter they are assessed. As previously noted, this is a smaller population with a lower probability of default. Performance metrics drop marginally relative to those for the model applied to the population of all borrowers but they are still very strong. For example, the AUC score drops from 92-93% to 86-88%, accuracy mostly remain in the same range and the loss increases by 1-2 percentage points.

5.2 Model Interpretation

We use our hybrid DNN-GBT model to uncover associations between the explanatory variables and default behavior. Since we do not identify causal relationships, our goal is simply to find covariates that have an important impact on default outcomes. Our findings can be used to better understand default behavior, further refine model specification and possibly aid in the formulation of theoretical models of consumer default. For this exercise, we mainly use the pooled model, which uses all available data. This allows us to assess factors that are critical in default behavior throughout the sample period with the best performing model. We also consider time variation in the factors influencing the default decision in subsets of our sample.

5.2.1 Explanatory Power of Variables

We start by examining the explanatory power of each of our features. We follow an approach similar to \citeNsirignano, which amounts to a perturbation analysis on the pooled sample using our hybrid model. First, we draw a random sample of 100,000 observations from the testing sample. Then, for each variable, we re-shuffle the feature, keeping the distribution intact and the model’s loss function is evaluated with the changed covariate. We repeat this step 10 times, and report the average of the loss and accuracy. Then, the variable is replaced to its original values, and a perturbation test is performed on a new variable. Perturbing the variable of course reduces the accuracy of the model, and the test loss becomes larger. If a particular variable has strong explanatory power, the test loss will significantly increase. The test loss for the complete model when no variables are perturbed is the Baseline value. Features that have large explanatory power, and whose information is not contained in the other remaining variables will increase the loss significantly if they are altered. Table 7 reports the results. Features relating to credit history, debt balances, and the number and credit available on revolving trades dominate the list. Specifically, months since the most recent 90+ days delinquency and months since the oldest trade was opened each increase the loss by 13%, the number of open credit card trades and credit amount on revolving trades increase the loss by 11%, while the balance on first mortgage trades and monthly payment on first mortgages increase the loss by 10%. These results suggest that revolving debt, length of credit history and temporal proximity to a delinquency are all important factors in default behavior. Based on publicly available information, length of the credit history is also an important determinant of standard credit scoring models, though payment history rather than balances or number of trades is understood as the most critical. This approach to assessing the importance of different features for the predicted probability of default has two major shortcomings. First, when features are highly correlated, the interpretation of feature importance can be biased by unrealistic data instances. To illustrate this problem, consider two highly correlated features. As we perturb one of the features, we create instances that are unlikely or even impossible. For example, mortgage balances are highly correlated with and lower than total debt balances, yet this perturbation approach could create instances in which total debt balances are smaller than mortgage balances. Since many of the features are strongly correlated, care must be taken with interpretation of feature importance. We list the highly correlated features in Appendix C. An additional concern with this perturbation approach is that the distribution of some features are highly skewed, which implies that the probability of their value being different than where the mass of their distribution is concentrated is quite low. Moreover, skewness varies substantially across features, therefore the informativeness of the perturbation may differ across variables. In the next section, we examine a more robust approach that is less susceptible to these limitations.

| Feature | Accuracy | Loss |

|---|---|---|

| Months since the oldest trade was opened | 0.8762 | 0.2941 |

| Months since the most recent 90 or more days delinquency | 0.8782 | 0.2936 |

| Open credit card trades | 0.8793 | 0.2895 |

| Credit amount on revolving trades | 0.8806 | 0.2876 |

| Balance on first mortgage trades | 0.8741 | 0.2876 |

| Monthly payment on open first mortgage trades | 0.8727 | 0.2866 |

| Open bankcard revolving, and charge trades | 0.8804 | 0.2865 |

| Total credit amount on open trades | 0.8803 | 0.2851 |

| Total debt balances | 0.8814 | 0.2844 |

| Monthly payment on all debt | 0.8797 | 0.2840 |

| Credit amount on open credit card trades | 0.8819 | 0.2812 |

| Worst ever status on any trades in the last 24 months | 0.8852 | 0.2784 |

| Months since the most recently opened first mortgage | 0.8835 | 0.2780 |

| Balance on collections | 0.8818 | 0.2779 |

| Monthly payment on credit card trades | 0.8831 | 0.2776 |

| Balance on bankcard revolving and charge trades | 0.8843 | 0.2769 |

| Balance on credit card trades | 0.8839 | 0.2769 |

| Credit amount on open mortgage trades | 0.8846 | 0.2765 |

| Monthly payment on open auto loan trades | 0.8837 | 0.2758 |

| Months since the most recent 30-180 days delinquency | 0.8849 | 0.2756 |

| Worst present status on any trades | 0.8856 | 0.2751 |

| Months since the most recently opened credit card trade | 0.8850 | 0.2746 |

| Credit amount on unsatisfied derogatory trades | 0.8825 | 0.2743 |

| Balance on revolving trades | 0.8848 | 0.2743 |

| Months since the most recently opened auto loan trade | 0.8848 | 0.2736 |

| Credit amount on open installment trades | 0.8846 | 0.2731 |

| Credit amount paid down on open first mortgage trades | 0.8870 | 0.2721 |

| ⋮ | ⋮ | ⋮ |

| Mortgage inquiries made inthe last 3 months | 0.8913 | 0.2605 |

| First mortgage trades opened in the last 6 months | 0.8914 | 0.2605 |

| Bankcard revolving and charge inquiries made in the last 3 months | 0.8914 | 0.2604 |

| Auto loan or lease inquiries made in the last 3 months | 0.8912 | 0.2603 |

| Balance on open bankcard revolving, and charge trades with credit line suspended | 0.8914 | 0.2603 |

| Baseline | 0.8914 | 0.2603 |

This table reports a perturbation analysis on the pooled sample using our hybrid model. For each variable, we re-shuffle the feature, keeping the distribution intact in the test dataset and the model’s loss function is evaluated on the test dataset with the changed covariate. We repeat this step 10 times, and report the average of the loss and accuracy. Then, the variable is replaced to its original values, and a perturbation test is performed on a new variable. Perturbing the variable of course reduces the accuracy of the model, and the test loss becomes larger. If a particular variable has strong explanatory power, the test loss will significantly increase. The test loss for the complete model when no variables are perturbed is the Baseline value.

5.2.2 Economic Significance of Variables

We now turn to analyzing the economic significance of our features for default behavior. We adopt SHapley Additive exPlanations (SHAP), a unified framework for interpreting predictions, to explain the output of our hybrid deep learning model (for a detailed description of the approach see \citeNSHAP). SHAP uses a game theoretical concept to assign each feature a local importance value for a given prediction. Though Shapley values are local by design, they can be combined into global explanations by averaging the absolute Shapley values featurewise. Then, we can compare features based on their absolute average Shapley values, with higher values implying higher feature importance. Similarly to permutation feature importance, SHAP is a feature importance measure. The main difference between the two is that while permutation feature importance is based on the decrease in model performance, SHAP is based on the magnitude of feature attributions.

We first compute the Shapley values for the Deep Neural Network model and the Gradient Boosted Trees model separately, then simply average them for each individual and for each feature.161616We implement Deep SHAP, a high-speed approximation algorithm for SHAP values in deep learning models to compute the Shapley values for our 5 hidden layer neural network. For GBT, we implement TreeExplainer, a high-speed exact algorithm for tree ensemble methods. Because our dataset is fairly large with many features, we pass a random sample of 100 observations, referred to as background observations, to compute the expected value for both models. We use a random sample of 100,000 observations for explaining the model. By the Shapley efficient property, the SHAP values for an observation sum up to the difference between the predicted value of that observation and the expected value, computed using the background dataset:

| (10) |

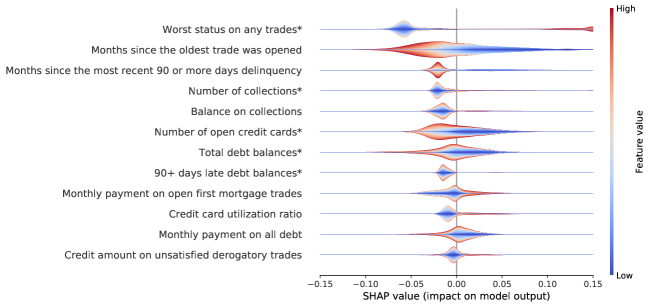

where f is the model prediction, M is the number of features, and is the feature attribution for feature j (i.e., the Shapley values). Thus, we can interpret the Shapley value as the contribution of a feature value to the difference between the model’s prediction and the mean prediction, given the current set of feature values. As an illustration, a SHAP value of 0.1 implies that the feature’s value for that particular instance contributed to an increase of 0.1 to the predicted probability compared to the mean prediction. Features that are highly correlated can decrease the importance of the associated feature by splitting the importance between both features. We account for the effect of feature correlation on interpretability by grouping features with a correlation larger than 0.7, and summing the SHAP values within each groups. We denote these groups with an asterisk for the rest of the analysis and report the composition of feature groups in Table 21 in the appendix.

Figure 6 sorts features by the sum of absolute SHAP value magnitudes, and plots the distribution of the impact each feature has on the model output for the twelve most important features or groups of correlated features. The color represents the feature value (red: high, blue: low), whereas the position on the horizontal axis denotes the contribution of the feature. The charts plot the distribution of SHAP values for individual instances in the 100,000 testing sample. The most important feature in terms of SHAP value magnitude is the worst status on any trades. High values of this variable tend to increase predicted default risk, whereas low values tend to decrease it, though the distribution of instances is dispersed. Features capturing credit history, such as length of credit history and recent delinquencies, also have high SHAP values, specifically, high values of these variables lower predicted default risk, with a much more dispersed distribution. Additionally, credit card utilization, credit amount on derogatory trades and outstanding collections are typically associated with an increase in predicted default probability. Higher total debt balances are also associated with a lower than expected predicted default risk, reiterating the notion that the borrowers with the most credit are also associated with lower predicted probability of default, which suggests that credit allocation decisions are made to minimize default probabilities. As in the perturbation exercise, we find that number of trades and balances seem to have the strongest association with variation in the predicted probability of default, whereas credit inquiries do not play a sizable role.