Long Range Dependence for Stable Random Processes

Abstract

We investigate long and short memory in -stable moving averages and max-stable processes with -Fréchet marginal distributions. As these processes are heavy-tailed, we rely on the notion of long range dependence suggested by Kulik and Spodarev (2019) based on the covariance of excursions. Sufficient conditions for the long and short range dependence of -stable moving averages are proven in terms of integrability of the corresponding kernel functions. For max-stable processes, the extremal coefficient function is used to state a necessary and sufficient condition for long range dependence.

AMS Subj. Class.: 60G10, 60G52, 60G70.

1 | Introduction

The occurrence of long memory in time series has been known for a long time starting from the work of Hurst (1951). Since then, this phenomenon has been observed and studied in applications in various fields including biophysical data (Burnecki (2012)), network traffics (Pilipauskaitė and Surgailis (2016)), neuroscience (Botcharova et al. (2014)), and geosciences (Montillet and Yu (2015)), etc. A typical example in financial applications (see e.g. Cheung and Lai (1995) and Panas (2001)) is a stationary solution of a autoregressive moving average FARIMA() process with stable innovations. In light of the variety of applications, a wide range of statistical models and methods for long range dependent processes has been developed, see, for instance, Avram and Taqqu (1986), Kasahara et al. (1988), Kokoszka and Taqqu (1996) for classical ones, and Magdziarz and Weron (2007) Beran et al. (2012), Jach et al. (2012), Koul and Surgailis (2018) for more recent developments. For a broader overview, we recommend the books of Doukhan et al. (2003), Beran et al. (2013), and Samorodnitsky (2016). These instruments rely on the explicit definition of long range dependence (LRD, for short) of a stationary time series or, more generally, a stationary stochastic process . Here and throughout this paper, stationarity is understood in the sense that all finite-dimensional distributions of are invariant under translations. There are many definitions of LRD in the literature depending on the class of processes to which belongs. For instance, if has a finite variance the following definition is classical, cf. (Samorodnitsky, 2016, P. 194-195):

Definition 1.1

A stationary stochastic process on some domain with is called long range dependent if

where , , is its covariance function. For processes in discrete time, the integral above should be changed to a sum.

Also, is antipersistent if , , and short range dependent, otherwise.

Alternative definitions of long memory rely e.g. on the unboundedness of the spectral density of at zero, growth comparisons of partial sums, phase transition in limit theorems for sums or maxima, etc., cf. Heyde and Yang (1997); Dehling and Philipp (2002); Samorodnitsky (2004); Lavancier (2006); Giraitis et al. (2012); Beran et al. (2013); Paulauskas (2016); Samorodnitsky (2016); Jach et al. (2012).

Many of these approaches fail for heavy-tailed stochastic processes whose variance does not exist. Such processes occur, for instance, in modelling of network data, in finance and in insurance (see e.g. Kokoszka and Mikosch (1997) who call the FARIMA() process with -stable innovations long range dependent if or Embrechts et al. (1997); Resnick (2007)). In order to allow for the analysis of long memory behaviour in a broader setting, Kulik and Spodarev (2019) propose to consider the covariance of indicator functions of excursions and introduce

Definition 1.2

A real-valued stationary stochastic process where is an unbounded subset of is short range dependent (SRD) if

| (1) |

for any finite measure on . Otherwise, i.e. if there exists a finite measure such that the integral in inequality is infinite, is long range dependent. For stochastic processes in discrete time, the integral should be replaced by the summation .

One major advantage of this definition is that the above covariance exists in any case due to the boundedness of the indicators. Furthermore, the definition turns out to be useful as it offers the applicability of limit theorems for certain functionals of the process of interest.

In practice, however, the computation of the multiple integral in (1) might prove to be tricky. Therefore, we restrict ourselves here to the wide class of positively associated stochastic processes, including the class of infinitely divisible moving average processes with nonnegative kernels (Bulinski and Shashkin, 2007, Chapter 1, Theorem 3.27). This will allow us to eliminate the absolute value in (1).

To introduce the notion of positive association, we need the class of real-valued bounded coordinate-wise nondecreasing Borel functions on , . For a real-valued stochastic process and a set , we denote .

Definition 1.3

A real-valued stochastic process is positively associated if for any disjoint finite subsets and all functions and .

By setting and for , and for , we have and . Consequently, for a positively associated stochastic process , it holds , i.e. the absolute value in (1) can be omitted.

In this paper, we consider two important subclasses of positively associated stationary processes that satisfy certain stability properties. More precisely, we study -stable moving averages and max–stable processes with -Fréchet marginals. As these processes are heavy-tailed, the classical definition of LRD (1.1) does not apply. Instead, we check 1.2.

With regard to this endeavor, we first establish a general framework to compute the double integral by inverting the univariate characteristic function of and the bivariate characteristic function of . Thus, our 2.4 yields

where is the Fourier transform of measure .

Integrating this relation with respect to will establish short or long range dependence according to 1.2. Subsequently, we will apply this result to get the LRD of symmetric -stable (SS) moving averages which are defined as follows.

Definition 1.4 (Samorodnitsky and Taqqu (1994))

Let be a measurable function with , . Then, a SS moving average process with parameter and kernel function is a stochastic process defined by

| (2) |

where is a SS random measure with Lebesgue control measure.

Here and throughout the paper, we use the notation , , to imply that .

Regarding the SRD/LRD of the process given in (2), our main result relies on the notion of –spectral covariance , , where , . The –spectral covariance was first introduced by Paulauskas (1976) and its properties were studied in Damarackas and Paulauskas (2014) and Damarackas and Paulauskas (2017). In Paulauskas (2016), it was discussed how the integrability of can be used for the definition of the memory property. Here, we establish by 3.4 that is short range dependent if or, equivalently, . Also, 3.5 establishes long range dependence if where is the minimum of and . These results hold also for -stable linear time series if integrals are replaced by sums.

To put our results into context, one may refer to other research and discussion on memory properties of stable processes such as Rachev and Samorodnitsky (2002), Maejima and Yamamoto (2003), Samorodnitsky (2004). Also, we demonstrate how our findings are meaningful in practice by detecting LRD in a real world data set consisting of daily log-returns based on the opening price of the Intel corporation share.

Analogously to -stable processes, which have become popular as limits of rescaled sums of stochastic processes, max-stable processes have become a widely used concept in extreme value analysis occurring as limiting models for maxima. Thus, they have found applications in various areas such as meteorology (Coles, 1993; Buishand et al., 2008; Davison and Gholamrezaee, 2012; Oesting et al., 2017, see e.g.), hydrology Asadi et al. (2015) and finance (Zhang and Smith, 2010). Max-stable processes are defined as follows.

Definition 1.5

A real-valued stochastic process is called a max-stable process if, for all , there exist functions and such that

where the processes , , are independent copies of , and means equality in distribution. If the index set is finite, is also called a max-stable vector.

It follows from the univariate extreme value theory that the marginal distributions of a max-stable process are either degenerate or follow a Fréchet, Gumbel or Weibull law. While covariances always exist in the Gumbel and Weibull case and, thus, the classical notion of long-range dependence applies, we will consider the case when is a stationary max-stable process with -Fréchet marginal distributions, i.e. for all and some and all . Here, covariances do not exist if .

In combination with Definition 1.2, a well-established dependence measure for max–stable stochastic processes allows for an easily tractable condition for short and long memory, respectively. More specifically, we use the pairwise extremal coefficient defined via the relation , which holds for all , to show that a stationary max-stable process with -Fréchet marginal distributions is long range dependent if and only if (cf. 4.3).

To summarize, our paper is structured as follows: Section 2 establishes the framework to invert the bivariate characteristic functions. In Section 3, we make use of this framework to find conditions for long range dependence of symmetric -stable moving averages and linear time series, while, in Section 4, we investigate long range dependence of a stationary max-stable process with -Fréchet marginals. Finally, we model the daily log-returns of an Intel corporation share by a SS moving average and show that is LRD in Section 5. For the sake of legibility, some of the proofs have been left out of the main part of this paper. They can be found in the Appendix.

2 | From Characteristic Function to Covariance of Indicators

In this section, we express the covariance of indicators of excursions of random variables above some levels through their uni- and bivariate characteristic functions. Notice that for random variables and it holds that

| (3) |

Theorem 2.1

Suppose and are identically distributed random variables with marginal characteristic function and joint characteristic function . Then, for a finite measure with its Fourier transform denoted by it holds that

| (4) |

Proof: Let and be independent copies of and . Then

| (5) |

If we denote the difference of the two indicators by , then by (Schilling, 2017, Theorem 19.12)111We thank René Schilling for his idea which simplifies our original proof. we get that the last equality in (5) simplifies to

| (6) |

where . By A.1 one can interchange the expectation and the integrals in equation (6) and computes

| (7) |

which is independent of . Thus, equation (6) simplifies to

The second identity in (4) follows from splitting the integrals into the positive and negative half-lines and substituting afterwards. ∎

Corollary 2.2

Proof.

Equality (8) follows immediately from and being real-valued as characteristic functions of a symmetric random variable and random vector, respectively.

Equality (9) follows from for any . ∎

If the stationary real-valued stochastic process is positively associated, we can apply 2.1 and, in the symmetric case, 2.2 to and to check the long range dependence of .

To do so, let in integral (1). However, the resulting expressions in (4), (8) or (9) might prove difficult to integrate w.r.t. over the whole real line. Thus, it is worth noting that the following lemma allows us to restrict integration to unbounded subsets over which it might be easier to integrate.

Lemma 2.3

Let denote the Lebesgue measure on and let be an arbitrary subset with . Then, a process is SRD or LRD iff is SRD or LRD, respectively.

Now we give the main result of this section showing the use of characteristic functions to check the short or long range dependence of .

Theorem 2.4

Suppose we have a stationary real-valued, positively associated stochastic process with absolutely continuous marginal distributions. Denote the univariate characteristic function of by and the bivariate characteristic function of by . Furthermore, let be an arbitrary subset with .

-

(a)

Then, is short range dependent if

(10) for any finite measure with Fourier transform .

-

(b)

Additionally, if is symmetric for all , then condition (10) rewrites as

(11)

Otherwise, i.e. if there exists a finite measure such that the integral in (10) is infinite, is long range dependent.

3 | Long Range Dependence of –stable Moving Averages

In this section, we investigate the LRD of SS moving averages in continuous and discrete time.

By 1.4, a symmetric -stable moving average with kernel function , , is defined by , , where is a symmetric -stable random measure.

Remark 3.1

-

(a)

Note that the SS moving average process is stationary, is absolutely continuous and, by Property 3.2.1 from Samorodnitsky and Taqqu (1994), the random vector is symmetric for every .

-

(b)

By Bulinski and Shashkin (2007), Theorems 1.3.5 and 1.3.27, is positively associated if the kernel function is nonnegative.

-

(c)

To exclude the trivial case for all we always assume that the Lebesgue measure of the set is positive.

By Samorodnitsky and Taqqu (1994), Proposition 3.4.2., the characteristic function of , , is given by

| (12) |

Moreover, the bivariate characteristic function of is given by

| (13) |

Before we get to our main result, we need to introduce the -spectral covariance of a stable vector as defined by (Damarackas and Paulauskas, 2017, equation (11)). Let be the unit circle. Recall that a random vector is symmetric -stable with parameter if there exists a finite measure on , the so-called spectral measure, such that the characteristic function of is given by

where is the standard inner product on .

Definition 3.2

Suppose is an -stable random vector with spectral measure , then the -spectral covariance of and is given by

| (14) |

Let us calculate the -spectral covariance of , , where is a SS moving average.

Lemma 3.3

Suppose with is a SS moving average process. Then, the -spectral covariance of , , is given by

| (15) |

Proof: Denote and , Proposition 3.4.3 in Samorodnitsky and Taqqu (1994) and the the symmetry of yields that is SS with spectral measure defined for all Borel sets by

where

Hereby is an absolutely continuous measure w.r.t. the Lebesgue measure with density . With we get

Thus,

∎

Now, a sufficient condition for the short range dependence of can be formulated in terms of or, equivalently, in terms of the kernel function .

Theorem 3.4

Let be a SS moving average process with parameter , nonnegative kernel function and -spectral covariance given in (15). is SRD if

| (16) |

or, equivalently, .

Proof: Without loss of generality, assume is a probability measure. Now, apply 2.4 to for some and choose It follows from the integrability of that as . Thus, there exists a constant such that for all where . Hence, it holds that and

Obviously, the right-hand side of the equality in (11) is bounded by

| (17) |

By inequalities (32) and (33) in Lemma A.3 we get

Next, show that condition (16) holds true iff . By Fubini’s theorem we get

∎

Naturally, one may also ask for sufficient conditions for the long range dependence of . Such a condition is given by

Theorem 3.5

Let be a SS moving average process with parameter and nonnegative kernel function . Then, is long range dependent if

| (18) |

Proof: Given in the appendix. ∎

Additionally, if the kernel function is eventually monotonic, then we can simplify condition (18) as follows.

Corollary 3.6

Let be a SS moving average process with parameter and nonnegative kernel function which is eventually monotonic, i.e. there is a number such that is monotonically decreasing on or monotonically increasing on . Then, is long range dependent if

| (19) |

Additionally, if is symmetric, the two sufficient conditions (19) are equivalent.

Proof.

Suppose is monotonically decreasing on and compute the integral (18). Thus, we have

The claim follows from the fact that . The case of monotonically increasing on some interval follows analogously.

∎

Now let us give an example of a kernel function whose corresponding SS moving average is long range dependent if .

Example 3.7

Suppose we have a SS moving average process with parameter and nonnegative kernel function as where and . Obviously, and where for some . Notice that

if or, equivalently, . Analogously to the proof of 3.6, this implies that fulfills equation (18) if . Thus, is long range dependent if by 3.5 and is short range dependent if by Theorem 3.4.

Remark 3.8

On one hand, this example was given to illustrate that the conditions (19) in 3.6 are useful when the kernel function itself is not eventually monotonic but rather asymptotically equivalent to such a function. On the other hand, this example motivates our conjecture that a SS moving average is long range dependent iff . However, the conjecture’s proof is still to be found.

Similar results as above can be obtained for symmetric -stable linear time series .

Definition 3.9 (Hosoya (1978))

Let be a sequence of i.i.d. SS random variables with characteristic function , , , . Let be a sequence of numbers such that . The stochastic process defined by

| (20) |

is called a linear SS time series.

Notice that can be written as a continuous time SS moving average with parameter and kernel function sampled at time instants . Thus, is positively associated if the coefficients are nonnegative for all . Moreover, the function simplifies to , .

Remark 3.10

Theorems 3.4 and 3.5 as well as 3.6 apply to linear processes with the obvious substitute of for . Indeed, let be a stationary SS time series with parameter and nonnegative coefficients . If

| (21) |

then is short range dependent. If

| (22) |

then is long range dependent. Additionally, if the coefficients are for some monotonically increasing for all or monotonically decreasing for all , then is long range dependent if or , respectively.

4 | Long Range Dependence of Max-stable Processes

In this section, we demonstrate that it is possible to use already existing dependence properties to check 1.2 instead of inverting characteristic functions as in the previous sections.

Any max-stable process is positively associated, see for instance Proposition 5.29 in Resnick (2013). Its dependence properties are typically summarized by its pairwise extremal coefficients defined via

cf. Schlather and Tawn (2003). By a series expansion of the logarithm, it can be seen that . Thus, , where corresponds to the case of (asymptotic) independence between and while means full dependence. Even though the joint distribution of is not uniquely determined by , this characteristic turns out to be a useful tool for the identification of dependence properties. For instance, Stoev (2008), Kabluchko and Schlather (2010) and Dombry and Kabluchko (2017) provide necessary and sufficient conditions for ergodicity and mixing of a max-stable process in terms of its pairwise extremal coefficients.

Here, we focus on the property of long-range dependence given by 1.2. We obtain bounds for , , , by making use of the following lemma.

Lemma 4.1

Let be a bivariate max-stable random vector with -Fréchet margins, , and extremal coefficient . Then, we have

for all .

Proof.

It is well-known that the cumulative distribution function of a bivariate max-stable random vector with -Fréchet margins is of the form

where is a bivariate random vector with cf. Chapter 5 in Resnick (2013), for instance. This so-called spectral vector is closely connected to the extremal coefficient via the relation . Thus, we obtain

| (23) |

Distinguishing between the two cases and , it can be seen that the right-hand side of equation (23) can be bounded from above by

where we used the fact that . This gives the lower bound stated in the lemma. Analogously, we obtain

which gives the corresponding upper bound. ∎

Remark 4.2

Using Equation 3, Lemma 4.1 yields the following bounds for :

for and if due to the -Fréchet margins. Consequently, one obtains for the integral in (1) that

| (24) |

From the lower and the upper bound in (24), we directly obtain a necessary and sufficient condition for long range dependence. Interestingly, unlike in case of -stable processes, the criterion does not depend on .

Theorem 4.3

Let be a stationary max-stable process with -Fréchet marginal distributions, , and pairwise extremal coefficients . Then, is long range dependent if and only if

| (25) |

.

Proof.

Example 4.4

Here, we consider two popular examples of max-stable processes, namely the extremal Gaussian process and the Brown–Resnick process.

-

1.

The extremal Gaussian process (Schlather, 2002) is a max-stable process with -Fréchet marginal distributions and finite-dimensional distributions of the form

where is a centered stationary Gaussian process on . The extremal coefficients of the extremal Gaussian process are given by

where denotes the correlation function of the underlying Gaussian process . Provided that for all , we have that , and, consequently,

that is, the process is long range dependent by 4.3.

-

2.

The Brown–Resnick process (Kabluchko et al., 2009) is a max-stable process with -Fréchet marginal distributions and finite-dimensional distributions of the form

where is a centered Gaussian process with stationary increments on . The extremal coefficients of the Brown–Resnick process can be expressed in terms of the variogram , , of the underlying Gaussian process via the relation

where denotes the standard normal distribution function.

Now assume that there exists some constant such that for being sufficiently large. From Mill’s ratio as with being the standard normal density function, it follows that

is integrable. Thus, by 4.3, the Brown–Resnick process is SRD if

which is true, for instance, for any fractional Brownian motion .

If, in contrast, the variogram of the underlying Gaussian process is bounded as in the case of a stationary process, we obtain that . Thus, analogously to the case of the extremal Gaussian process, the Brown-Resnick process can be shown to be LRD.

Note that these conditions also appear in the literature when analyzing the existence of a mixed moving maxima (M3) representation of a Brown-Resnick process: In Kabluchko et al. (2009), it is shown that a M3 representation exists if . In case of a bounded variogram, however, the resulting Brown-Resnick is not even mixing. As sufficient and necessary conditions for the existence of a M3 representation are stated in terms of the asymptotic behavior of the sample paths of the underlying Gaussian process rather than in terms of its variogram (cf. Wang and Stoev, 2010; Dombry and Kabluchko, 2017, for instance), to the best of our knowledge, there is no general treatment of the gap between these two cases. Similarly, for SRD/LRD, a detailed analysis of further cases is beyond the scope of this paper.

Remark 4.5

In this section, using known dependency properties allows to avoid complex calculation such that no restrictions on the index set are required. In particular, all the results are also valid for max-stable random fields, i.e. the case that .

5 | Application to Data

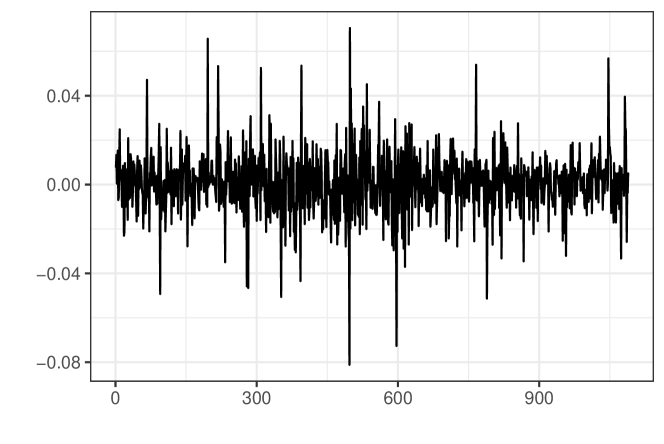

In this section, we want to motivate our theoretical results by showing their applicability to real world data. To do so, let us consider the daily log-returns of the Intel corporation share from Mar 03, 2013 to Aug 21, 2017 depicted in Figure 1.

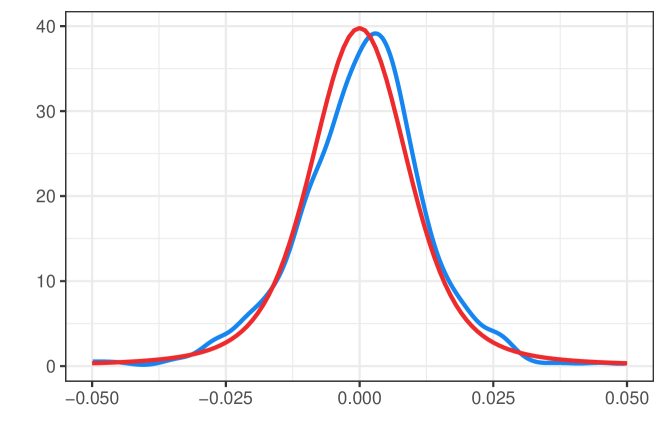

Preliminary analysis has shown that the marginal distribution of these log-returns fits reasonably well to that of a symmetric -stable distribution with estimated index of stability and scale parameter as depicted in Figure 2. For simplicity, here we use the simple and consistent estimation procedure proposed by McCulloch (1986).

Further, we model this time series using a linear SS process , with , as described in 3.9. By 3.10, we can apply our previous continuous-time results from Section 3 by considering a continuous-time SS moving average with a piecewise constant kernel function and interpreting the time series as sampled at time instances .

To do so, we estimate a continuous-time kernel function by a non-parametric approach and check the conditions in Theorems 3.4 and 3.5. By 3.7, it suffices to check the condition , if the estimated kernel function exhibits power decaying tails.

However, to the best of our knowledge, there is no universally applicable non-parametric approach for kernel estimation in our setting. For instance, the procedure proposed by Kampf et al. (2020) estimates the kernel of a SS moving average under certain conditions posed on the underlying kernel function . However, the authors of this particular paper conclude that under their assumptions, must be bounded and for all where which, in particular, implies that . Consequently, 3.4 implies that this kernel estimation procedure is applicable in our setting only if is SRD.

Therefore, let us choose a simple parametric minimal contrast method based on the codifference

of and as defined in (Samorodnitsky and Taqqu, 1994, Definition 2.10.1). Here describes the covariation norm of a SS random variable given by (Samorodnitsky and Taqqu, 1994, Definition 2.8.1).

We assume that the kernel function of is causal, i.e., supported on the positive half-line, and parametrized like

where . By 3.7, the process is well-defined iff and long range dependent iff .

By (Samorodnitsky and Taqqu, 1994, Example 3.6.2) we have that and . By simple calculations, we get that for all

Note here that despite the process being defined on the whole real line, we are only interested in sample time points for our data analysis. Consequently, the codifference of and writes

| (26) |

By (Samorodnitsky and Taqqu, 1994, Prop. 2.8.2) it holds that and for all where and are the scale parameters of and , respectively. We compare the theoretical quantity (26) to

where and are estimators of and , respectively. Again, we use the approach proposed by McCulloch (1986) to estimate . When estimating , we do the same based on computed observations , , where denotes the length of the original sample.

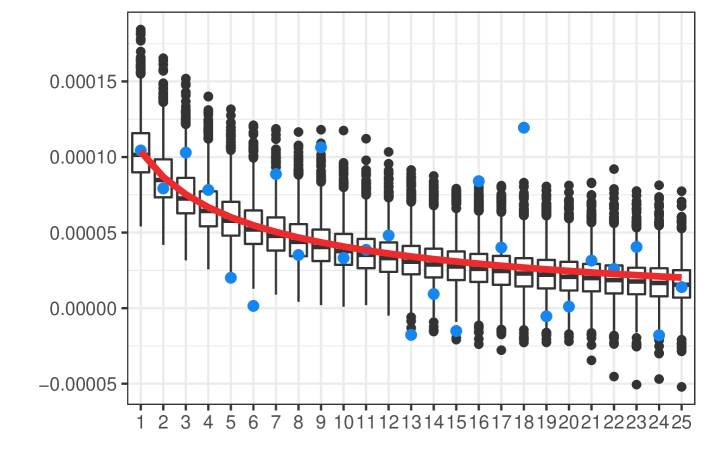

Now, let us estimate the parameters and by minimizing the -distance of and based on the first 25 time instances. We choose this value based on the computation costs of a higher threshold and on the fact that this value has proven useful in simulation studies as part of the preliminary analysis. Using our procedure, we estimate and . To validate our estimation, we ran a parametric bootstrap and simulated 1000 SS time series with kernel parameters and to get a grasp on the variance of in our chosen model. The results of our parametric bootstrap are depicted in Figure 3. It shows that despite some discrepancies with regard to the empirically computed , which is to be expected in real data, our model exhibits a reasonable fit for the data set.

Notice that, due to the empirical estimation of the scale parameters and , it happens that for some , which is impossible for the theoretical codifference . This, however, does not substantially affect the quality of the fit of to . By the same parametric bootstrap we find the standard deviations of for and for . It holds that which implies by 3.7 that the log-returns of Intel Corporation are long range dependent.

Data Availability Statement

The data used in this paper was provided by a free data sample from

https://www.quandl.com/data/EOD/INTC.

References

- Asadi et al. (2015) P. Asadi, A. C. Davison, and S. Engelke. Extremes on river networks. Ann. Appl. Stat, 9(4):2023–2050, 2015.

- Avram and Taqqu (1986) F. Avram and M. S. Taqqu. Weak convergence of moving averages with infinite variance. In Dependence in probability and statistics (Oberwolfach, 1985), volume 11 of Progr. Probab. Statist., pages 399–415. Birkhäuser Boston, Boston, MA, 1986.

- Beran et al. (2012) J. Beran, B. Das, and D. Schell. On robust tail index estimation for linear long-memory processes. J. Time Series Anal., 33(3):406–423, 2012.

- Beran et al. (2013) J. Beran, Y. Feng, S. Ghosh, and R. Kulik. Long memory processes. Probabilistic Properties and Statistical Methods. Springer, 2013.

- Botcharova et al. (2014) M. Botcharova, S. F. Farmer, and L. Berthouze. Markers of criticality in phase synchronization. Front. Syst. Neurosci., 8:176, 2014.

- Buishand et al. (2008) T. Buishand, L. De Haan, C. Zhou, et al. On spatial extremes: with application to a rainfall problem. Ann. Appl. Stat, 2(2):624–642, 2008.

- Bulinski and Shashkin (2007) A. Bulinski and A. Shashkin. Limit Theorems for Associated Random Fields and Related Systems. World Scientific Publishing Co. Pte. Ltd., 2007.

- Burnecki (2012) K. Burnecki. Farima processes with application to biophysical data. J. Stat. Mech. Theory Exp, 2012(05):P05015, 2012.

- Cheung and Lai (1995) Y.-W. Cheung and K. S. Lai. A search for long memory in international stock market returns. J. Int. Money Finance, 14(4):597–615, 1995.

- Coles (1993) S. G. Coles. Regional modelling of extreme storms via max-stable processes. J. R. Stat. Soc. Ser. B. Stat. Methodol., 55(4):797–816, 1993.

- Damarackas and Paulauskas (2014) J. Damarackas and V. Paulauskas. Properties of spectral covariance for linear processes with infinite variance. Lith. Math. J., 54(3):252–276, 2014.

- Damarackas and Paulauskas (2017) J. Damarackas and V. Paulauskas. Spectral covariance and limit theorems for random fields with infinite variance. J. Multivariate Anal., 153:156–175, 2017.

- Davison and Gholamrezaee (2012) A. C. Davison and M. M. Gholamrezaee. Geostatistics of extremes. P. Roy. Soc. A-Math. Phy., 468(2138):581–608, 2012.

- Dehling and Philipp (2002) H. Dehling and W. Philipp. Empirical process techniques for dependent data. In Empirical process techniques for dependent data, pages 3–113. Birkhäuser Boston, Boston, MA, 2002.

- Dombry and Kabluchko (2017) C. Dombry and Z. Kabluchko. Ergodic decompositions of stationary max-stable processes in terms of their spectral functions. Stochastic Process. Appl., 127(6):1763–1784, 2017.

- Doukhan et al. (2003) P. Doukhan, G. Oppenheim, and M. S. Taqqu, editors. Theory and applications of long-range dependence. Birkhäuser Boston, Inc., Boston, MA, 2003.

- Embrechts et al. (1997) P. Embrechts, C. Klüppelberg, and T. Mikosch. Modelling Extremal Events for Insurance and Finance. Springer-Verlag, Berlin Heidelberg, 1997.

- Giraitis et al. (2012) L. Giraitis, H. L. Koul, and D. Surgailis. Large sample inference for long memory processes. Imperial College Press, London, 2012.

- Heyde and Yang (1997) C. C. Heyde and Y. Yang. On defining long-range dependence. J. Appl. Probab., 34(4):939–944, 1997.

- Hosoya (1978) Y. Hosoya. Discrete-time stable processes and their certain properties. Ann. Probab., 6(1):94–105, 02 1978.

- Hurst (1951) H. E. Hurst. Long-term storage capacity of reservoirs. Trans. Amer. Soc. Civil Eng., 116:770–799, 1951.

- Jach et al. (2012) A. Jach, T. McElroy, and D. N. Politis. Subsampling inference for the mean of heavy-tailed long-memory time series. J. Time Series Anal., 33(1):96–111, 2012.

- Kabluchko and Schlather (2010) Z. Kabluchko and M. Schlather. Ergodic properties of max-infinitely divisible processes. Stochastic Process. Appl., 120(3):281–295, 2010.

- Kabluchko et al. (2009) Z. Kabluchko, M. Schlather, and L. de Haan. Stationary max-stable fields associated to negative definite functions. Ann. Probab., 37(5):2042–2065, 2009.

- Kampf et al. (2020) J. Kampf, G. Shevchenko, and E. Spodarev. Nonparametric estimation of the kernel function of symmetric stable moving average random functions. Ann. Inst. Statist. Math., to appear, 2020. doi: 10.1007/510463-020-00751-6.

- Kasahara et al. (1988) Y. Kasahara, M. Maejima, and W. Vervaat. Log-fractional stable processes. Stochastic Process. Appl., 30(2):329–339, 1988.

- Kokoszka and Mikosch (1997) P. Kokoszka and T. Mikosch. The integrated periodogram for long-memory processes with finite or infinite variance. Stochastic Process. Appl., 66(1):55–78, 1997.

- Kokoszka and Taqqu (1996) P. S. Kokoszka and M. S. Taqqu. Parameter estimation for infinite variance fractional ARIMA. Ann. Statist., 24(5):1880–1913, 1996.

- Koul and Surgailis (2018) H. L. Koul and D. Surgailis. Asymptotic distributions of some scale estimators in nonlinear models with long memory errors having infinite variance. J. Time Series Anal., 39(3):273–298, 2018.

- Kulik and Spodarev (2019) R. Kulik and E. Spodarev. Long range dependence of heavy tailed random functions. arXiv e-prints, page arXiv:1706.00742v3, 2019.

- Lavancier (2006) F. Lavancier. Long memory random fields. In Dependence in probability and statistics, volume 187 of Lecture Notes in Statist., pages 195–220. Springer, New York, 2006.

- Maejima and Yamamoto (2003) M. Maejima and K. Yamamoto. Long-memory stable Ornstein-Uhlenbeck processes. Electron. J. Probab., 8(19):1–18, 2003.

- Magdziarz and Weron (2007) M. Magdziarz and A. Weron. Fractional Langevin equation with -stable noise. A link to fractional ARIMA time series. Studia Math., 181(1):47–60, 2007.

- McCulloch (1986) J. H. McCulloch. Simple consistent estimators of stable distribution parameters. Commun. Stat-Simul C, 15(4):1109–1136, 1986.

- Montillet and Yu (2015) J.-P. Montillet and K. Yu. Modeling geodetic processes with Levy -stable distribution and FARIMA. Math. Geosci., 47(6):627–646, 2015.

- Oesting et al. (2017) M. Oesting, M. Schlather, and P. Friederichs. Statistical post-processing of forecasts for extremes using bivariate Brown–Resnick processes with an application to wind gusts. Extremes, 20(2):309–332, 2017.

- Panas (2001) E. Panas. Estimating fractal dimension using stable distributions and exploring long memory through arfima models in athens stock exchange. Appl Financ Econ, 11(4):395–402, 2001.

- Paulauskas (2016) V. Paulauskas. Some remarks on definitions of memory for stationary random processes and fields. Lith. Math. J., 56(2):229–250, 2016.

- Paulauskas (1976) V. J. Paulauskas. Some remarks on multivariate stable distributions. J. Multivariate Anal., 6(3):356–368, 1976.

- Pilipauskaitė and Surgailis (2016) V. Pilipauskaitė and D. Surgailis. Anisotropic scaling of the random grain model with application to network traffic. J. Appl. Probab., 53(3):857–879, 2016.

- Rachev and Samorodnitsky (2002) S. T. Rachev and G. Samorodnitsky. Erratum to: “Long strange segments in a long-range-dependent moving average” [Stochastic Process. Appl. 93 (2001), no. 1, 119–148;]. Stochastic Process. Appl., 101(1):161, 2002.

- Reed and Simon (1981) M. Reed and B. Simon. Methods of Modern Mathematical Physics, Volume 1, Functional Analysis. Academic Press, 1981.

- Resnick (2007) S. I. Resnick. Heavy-Tail Phenomena: Probabilistic and Statistical Modeling. Springer, New York, 2007.

- Resnick (2013) S. I. Resnick. Extreme Values, Regular Variation and Point Processes. Springer, 2013.

- Samorodnitsky (2004) G. Samorodnitsky. Extreme value theory, ergodic theory and the boundary between short memory and long memory for stationary stable processes. Ann. Probab., 32(2):1438–1468, 2004.

- Samorodnitsky (2016) G. Samorodnitsky. Stochastic processes and long range dependence. Springer Series in Operations Research and Financial Engineering. Springer, Cham, 2016.

- Samorodnitsky and Taqqu (1994) G. Samorodnitsky and M. S. Taqqu. Stable non-Gaussian random processes. Stochastic Modeling. Chapman & Hall, New York, 1994. Stochastic models with infinite variance.

- Schilling (2017) R. L. Schilling. Measures, Integrals and Martingales. Cambridge University Press, second edition, 2017.

- Schlather (2002) M. Schlather. Models for stationary max-stable random fields. Extremes, 5(1):33–44, 2002.

- Schlather and Tawn (2003) M. Schlather and J. A. Tawn. A dependence measure for multivariate and spatial extreme values: Properties and inference. Biometrika, 90(1):139–156, 2003.

- Stoev (2008) S. A. Stoev. On the ergodicity and mixing of max-stable processes. Stochastic Process. Appl., 118(9):1679–1705, 2008.

- Strokorb and Schlather (2015) K. Strokorb and M. Schlather. An exceptional max-stable process fully parameterized by its extremal coefficients. Bernoulli, 21(1):276–302, 2015.

- Wang and Stoev (2010) Y. Wang and S. Stoev. On the structure and representations of max-stable processes. Adv. Appl. Probab., 42(3):855–877, 2010.

- Zhang and Smith (2010) Z. Zhang and R. L. Smith. On the estimation and application of max-stable processes. J. Statist. Plann. Inference, 140(5):1135–1153, 2010.

Appendix A Appendix

Lemma A.1

Suppose and are identically distributed random variables with marginal characteristic function and joint characteristic function . Also, let and be independent copies of and , respectively. Then, for a Fourier transform of a finite measure denoted by it holds that

where , and

Proof.

Let us define for and denote

where we have used (Schilling, 2017, Theorem 19.12) in the last equality and is the inverse Fourier transform of . It can be computed by tedious, yet simple calculations as

| (27) |

Computing one of these factors gives us

for some finite constant which is independent of , and . This constant exists because the function is bounded. Thus, for all by equality (27) and . Therefore, we can apply the dominated convergence theorem and . ∎

Lemma A.2

-

(a)

Suppose and . Then it holds that

-

(b)

Suppose and , then .

-

(c)

Let then

(28) where

Proof.

- (a)

-

(b)

Suppose , then

The claim follows analogously if .

-

(c)

For simplicity, consider the case After the change of variable, the integral in (28) rewrites

(31)

∎

Lemma A.3

Proof.

First, compute for the absolute value of the difference of characteristic functions in for any :

| (34) |

where we have used A.2(a) in the last inequality.

Similarly, we compute for the case as

| (35) |

where, again, we have used A.2(a) in the last inequality. Using the same arguments, we get for the case that

| (36) |

Now, plugging the estimates (34),(35) and (36) into and we get

| (37) |

We estimate the integral in (37) from above via the density of a bivariate normal law. Thus,

| (38) |

where we denoted

| (39) |

in the last equality. Now, we have a substitution

so that

Then, relation (38) rewrites

Now, show that is only infinite on a null set. More specifically, we show that if and only if . Recall that the Cauchy-Schwarz inequality (cf. Reed and Simon (1981), Theorem S.3.) states that

where equality holds if and only if there exists such that . In this case, relation yields . Note that due to being nonnegative, we can rewrite the condition as or ; hence, is a -periodic function with on a set of positive Lebesgue measure which contradicts because in that case as . Consequently, if and only if .

∎

Proof of 3.5: Let us choose where is the Dirac measure concentrated at zero. Obviously this measure is finite and by 2.2 we get for :

| (40) |

We denote and . Then, by for all we estimate

| (41) |

Thus, we obtain a lower bound for the right hand side of (41):

Note that for any Thus, for

Consequently, it holds

Now, by Fubini’s theorem and A.2 (c), this is greater or equal to

Thus, for we have that

Consequently, by 1.2 and Fubini’s theorem, is long range dependent if