Abstract.

We show that competitive equilibria in a range of models related to production networks can be recovered as solutions to dynamic programs. Although these programs fail to be contractive, we prove that they are tractable. As an illustration, we treat Coase’s theory of the firm, equilibria in production chains with transaction costs, and equilibria in production networks with multiple partners. We then show how the same techniques extend to other equilibrium and decision problems, such as the distribution of management layers within firms and the spatial distribution of cities.

Keywords: Negative discounting; dynamic programming; production chains

JEL Classification: C61, D21, D90

Coase Meets Bellman: Dynamic Programming for

Production

Networks111We gratefully acknowledge valuable comments from our

editors and referees, as well as Pol

Antràs, Yongsung Chang, Davin Chor, Ryo Jinnai,

Young Sik Kim, Yuta Takahashi and Makoto Saito. We also acknowledge financial

support from Korea University (K1922081), BrainKorea21 Plus (K1327408 and T192201), JSPS Grant-in-Aid for

Scientific Research (20H05633 and 16H03598), Singapore Ministry of

Education Academic Research Fund R-122-000-140-112 and Australian

Research Council Award DP120100321. Email contacts:

tomookikuchi@waseda.jp,

nishimura@rieb.kobe-u.ac.jp,

john.stachurski@anu.edu.au, zhangjunnan1224@gmail.com

Tomoo Kikuchia, Kazuo Nishimurab,

John Stachurskic and Junnan Zhangd

††footnotetext:

a Graduate School of Asia-Pacific Studies, Waseda University;

b Research Institute of Economics and

Business Administration, Kobe University, and RIETI;

c Research School of Economics, Australian

National University;

d Center for Macroeconomic Research at School of

Economics, and Wang Yanan Institute for Studies in Economics, Xiamen

University

1. Introduction

Production networks have grown rapidly in size and complexity, in line with advances in communications, supply chain management and transportation technology (see, e.g., Coe and Yeung (2015)). These large and complex networks are sensitive to uncertainty, trade disputes, transaction costs and other frictions. Firms routinely shift production and task allocation across networks, in order to mitigate risk or exploit new opportunities (see, e.g., Farlow (2020)). There is an ongoing need to predict how equilibria in production networks adapt and respond to shocks, in order to understand their impact on domestic employment, industry concentration, productivity and tax revenue.

Dynamic programming provides one methodology for analyzing such equilibria. While dynamic programming is typically used to study dynamic models (see, e.g., Stokey and Lucas (1989)), it can also be applied to static models by reinterpreting the time parameter as an index over firms or other decision making entities, as seen in, for example, Garicano and Rossi-Hansberg (2006), Hsu et al. (2014), Tyazhelnikov (2019), and Antràs and De Gortari (2020). Our paper builds on this literature by providing a systematic way to apply the theory of dynamic programming to both production chains and production networks, as well as to a range of other static allocation problems involving firm management and economic geography.

This research agenda faces a technical hurdle: the dynamic programs most naturally mapped to the competitive allocation problems we wish to consider usually fail to be contractive. Contractivity fails because frictions such as the transaction costs or failure probabilities in the production chain models translate into negative discount rates in the corresponding dynamic program. In this paper, we circumvent the need for contractivity by drawing on dynamic programming methods originally developed to solve recursive preference problems.222See, for example, Epstein and Zin (1989), Bloise and Vailakis (2018) or Marinacci and Montrucchio (2019). In this sense, our work can be viewed as building connections between (a) the existing literature on dynamic programming for obtaining static competitive equilibria and (b) the modern theory of dynamic programming with recursive preferences.

The contributions of this paper fall into two parts. The first is providing a theory of dynamic programming in a loss-minimization setting where discount rates are negative. The second is applying this theory to a series of competitive equilibrium problems involving production chains, production networks and other related models. Through the application of this theory, we show how the dynamic programming tools can be used to obtain not only existence and uniqueness of equilibria, but also computational algorithms, results on comparative statics and insights into the underlying mechanisms.

Regarding application, we build on an analytical framework for analyzing allocation of tasks across firms first developed by Coase (1937). Subsequently, Kikuchi et al. (2018), Fally and Hillberry (2018) and Yu and Zhang (2019) developed Coasian models in which firms trade off coordination costs within the firm against transaction costs outside the firm. We show that competitive equilibria in these models can be recovered as solutions to dynamic programs and use the associated envelope condition to provide insight on some of the foundational conjectures of Coase (1937).

In the remainder of the paper, we then apply similar methods to study a range of additional applications, including settings where Coasian transaction costs are replaced by failures in production or costly transportation, as found, for example, in Levine (2012) and Costinot et al. (2013); models of knowledge organization and optimal management structures originally due to Garicano (2000); the analysis of central place theory in Hsu et al. (2014); and the configuration of general (nonsequential) production networks in the spirit of Baldwin and Venables (2013), Kikuchi et al. (2018), Yu and Zhang (2019) and Tyazhelnikov (2019).

The applications discussed above differ in many ways. There are different trade-offs that characterize each model, each of which leads to a particular endogenous structure. The negative discount dynamic programming theory developed here provides a unifying methodology and brings tools to bear on understanding the structure of the networks where firms, cities and managers coordinate production.

Regarding our technical contribution, the closest existing work in the economic literature is Bloise and Vailakis (2018), who treat noncontractive dynamic programming problems that arise from recursive utility. In addition to results on existence and uniqueness of fixed points of the Bellman operator, which parallel analogous results in Bloise and Vailakis (2018), we apply a fixed point result of Du (1989) to provide new results on monotonicity, convexity and differentiability of solutions, as well as a full set of optimality results linking Bellman’s equation to existence and characterization of optimal solutions.333This optimality theory is related to other studies of dynamic programming where the Bellman operator fails to be a contraction, such as Martins-da Rocha and Vailakis (2010) and Rincón-Zapatero and Rodríguez-Palmero (2003). Our methods differ because even the relatively weak local contraction conditions imposed in that line of research fail in our settings. The fixed point results in this paper are related to those found in Kamihigashi et al. (2015), but here we also prove uniqueness of the fixed point, as well as connections to optimality and shape and differentiability properties.

The remainder of this paper is structured as follows. In Section 2, we study a dynamic optimization problem under negative discounting and discuss its solution. In Section 3, we connect this discussion to Coase’s theory of the firm and elaborate on the relationship between our model and other related models. In Section 4 we show that our model can also be used to understand organization of knowledge within a firm. In Section 5 we extend our model to expand the scope of applications to more complex networks. Section 6 concludes. Most proofs are deferred to the appendix.

2. Negative Discount Dynamic Programming

In this section, we study a dynamic optimization problem in which an agent minimizes a flow of losses under negative discounting. While our main aim is to develop techniques for calculating equilibria in production networks, the topic of negative discount loss minimization does have some independent value.444 For example, Thaler (1981), Loewenstein and Prelec (1991) and Loewenstein and Sicherman (1991) document separate instances of such phenomena. Loewenstein and Sicherman (1991) found that the majority of surveyed workers reported a preference for increasing wage profiles over decreasing ones, even when it was pointed out that the latter could be used to construct a dominating consumption sequence. Loewenstein and Prelec (1991) obtained similar results, stating that “sequences of outcomes that decline in value are greatly disliked, indicating a negative rate of time preference” (Loewenstein and Prelec, 1991, p. 351).

Consider an agent who takes action in period with loss . We interpret as effort and as disutility. Her optimization problem is, for some ,

| (1) |

Throughout this section, we suppose that

| (2) |

The convexity in encourages the agent to defer some effort. Negative discounting () has the opposite effect. We call problem (1) under the assumptions in (2) a negative discount dynamic program.555The assumption cannot be weakened, since implies that the objective function is infinite. Conversely, with the assumption , minimal loss is always finite. Indeed, by choosing the feasible action path and for all , we get . Also, given our other assumptions, there is no need to consider the case because no solution exists. Because we are minimizing disutility, when any proposed solution can be strictly improved by shifting it one step into the future (set and for all ). Furthermore, if , and a solution exists, then the increments must converge to zero, and hence there exists a pair and with . Since is strictly convex, the objective can be reduced by redistributing a small amount from to . This contradicts optimality.

2.1. A Recursive View

We can express the problem recursively by introducing a state process that starts at and tracks the amount of tasks remaining. Set and . The Bellman equation for this problem is

| (3) |

The Bellman operator is

| (4) |

The Bellman operator is not a supremum norm contraction because .666For example, let and . Then while . One consequence is that, if we take an arbitrary continuous bounded function and iterate with , the sequence typically diverges. For example, if , then, , which diverges to . Nevertheless, we can show that is well behaved, with a unique fixed point, after we restrict its domain to a suitable candidate class . To this end, we set

Let be all continuous with . These upper and lower bounds have natural interpretations. Since completing all remaining tasks at once is in the choice set, its value is an upper bound of the minimized value. Regarding the lower bound , this is the value that could be obtained if (no discounting) and the agent, having no time constraint, subdivided without limit.

Proposition 2.1.

The Bellman operator has a unique fixed point in and as for all . Moreover,

-

1.

is strictly increasing, strictly convex, and continuously differentiable, and

-

2.

The policy is single-valued and satisfies

(5)

2.2. Equivalence

So far, we have solved the Bellman equation (3) and derived properties of its solutions. However, it is not clear whether the Bellman equation can characterize the solution to the dynamic optimization problem (1), since the constraint is not in the Bellman equation. We turn to this issue now.

Let

| (6) |

be the value function of the optimization problem (1). The next proposition shows that , the fixed point of , and that the policy correspondence solves (1). The proof can be found in Appendix A.3.

Proposition 2.2.

The sequence defined by , and is the unique solution to (1). Moreover, .

The envelope condition (5) now evaluates to

| (EN) |

for all , which links marginal value to marginal disutility at optimal action. Furthermore, (EN) implies that the sequence satisfies777To see this, note that solves . Since both and are convex, elementary arguments show that either or . It follows from (EN) that either or , which is equivalent to (EU).

| (EU) |

for all , which is akin to an Euler equation with a possibly binding constraint. In the applications below we use (EN) and (EU) to aid interpretation and provide economic intuition.

Equation (EU) implies that is a decreasing sequence. This agrees with our intuition, since future losses are given greater weight than current losses.

2.3. Additional Results

Instead of assuming as in (2), we can treat the case , which has hitherto been excluded:

Proposition 2.3.

Proposition 2.3 shows that the Euler equation (EU) becomes necessary and sufficient for optimality when . In fact, (EU) can be reduced to in this case, which helps derive analytical solutions for some of the applications.

As the above results suggest, the set of tasks will be completed in finite time if and only if . The proof is in the appendix.

3. Application: Production Chains

Now we turn to applications of our negative discount dynamic program motivated by production problems. We begin with linear production chains.

3.1. A Coasian Production Chain

In this section we consider a version of the Coasian models developed by Kikuchi et al. (2018), Fally and Hillberry (2018) and Yu and Zhang (2019). We show how competitive equilibrium in these models can be calculated using the dynamic programming theory from Section 2.

3.1.1. Set Up

Consider a market with many price-taking firms, each of which is either inactive or part of the production of a single good. To produce a unit of this good requires implementing a unit mass of tasks. The cost for any one firm of implementing an interval of length is denoted , where is increasing, strictly convex, continuously differentiable, and satisfies .888Unlike Kikuchi et al. (2018), we allow .

Firms face transaction costs, as a wedge between cost to the buyer and payment received by the seller.999This follows Kikuchi et al. (2018) and also studies such as Boehm and Oberfield (2020), where frictions in contract enforcement are treated as a variable wedge between effective cost to the buyer and payment to the supplier. Transaction costs fall on buyers, so that, for a transaction with face value , the seller receives and the buyer pays with .101010For example, might be the cost of writing a contract for a transaction with face value . This cost rises in because more expensive transactions merit more careful contracts.

Firms are indexed by integers . A feasible allocation of tasks across firms is a nonnegative sequence with . We identify firm with the most downstream firm, firm with the second most downstream firm, and so on. Let be the downstream boundary of firm , so that and for all . Then, profits of the th firm are

| (7) |

Here is a price function, with interpreted as the price of the good at processing stage .

Definition 3.1.

Given a price function and a feasible allocation , let be corresponding profits, as defined in (7). The pair is called an equilibrium for the production chain if

-

1.

,

-

2.

for any pair with , and

-

3.

for all .

Conditions 1–3 eliminate profits for active firms and prevent entry by inactive firms.

3.1.2. Solution by Dynamic Programming

An equilibrium of the production chain satisfies , which has the same form as the Bellman equation (3). Moreover, iterating on this relation yields the price of the final good

| (8) |

which is analogous to the total loss in (1). These facts lead us to a version of the negative discount dynamic program introduced in Section 2 where a (fictitious) agent seeks to minimize subject to . By construction, any feasible action path is also a feasible allocation of tasks in the production chain.

Since and , the assumptions in (2) are satisfied. Hence there exists a unique solution by Proposition 2.2. Let be the corresponding value function given by (6). The next proposition shows that the solution to this dynamic program is precisely the competitive equilibrium of the Coasian production chain.

Proposition 3.1.

If and for all , then is an equilibrium for the production chain.

For firm with downstream boundary , the envelope condition (EN) yields

| (9) |

Since is the optimal range of tasks implemented in-house by firm in equilibrium, this expresses Coase’s key idea: the size of the firm is determined as the scale that equalizes the marginal costs of in-house and market-based operations. The Euler equation (EU) also implies that is decreasing, so firm size increases with downstreamness. This generalizes a finding of Kikuchi et al. (2018).

3.1.3. An Example

Suppose that the range of tasks implemented by a given firm satisfies , where is capital and is labor. Given rental rate and wage rate , the cost function is subject to . Suppose further that, as in Lucas (1978), the production function has the form , where has constant returns to scale and is increasing and strictly concave (due to “span-of-control” costs). To generate a closed-form solution, we take and , with . The resulting cost function has the form , where is a positive constant.

By Proposition 3.1, the optimal action path for the fictitious agent corresponds to the equilibrium allocation of tasks across firms, and the value function is the equilibrium price function. Since , Proposition 2.3 applies and (EU) yields for all , where . From we obtain . Substituting this path into (6) gives the price function

| (10) |

As anticipated by the theory, is strictly increasing and strictly convex.

Intuitively, firm-level span-of-control costs cannot be eliminated in aggregate due to transaction costs, which force firms to maintain a certain size. This leads to strict convexity of prices. If firms have constant returns to management (), then the price function in (10) becomes linear.111111The above result on the size of firms is related to Antràs and De Gortari (2020), who prove it is optimal to locate relatively downstream stages of production in relatively central locations where trade costs are lower. Their result holds because trade costs have more pronounced effects in more downstream stages of production in their model. Similarly, in our model, transaction costs have more pronounced effects in more downstream states of production, due to (EU).

3.2. Specialization and Failure Probabilities

Production processes typically involve a series of complementary tasks. Mistakes in any one task can dramatically reduce the product’s value. Implications of such specialization and failure probabilities were studied in, among others, the O-ring theory of economic development by Kremer (1993) and the production chain models of Levine (2012) and Costinot et al. (2013). These papers show how equilibrium allocations can serve to mitigate the potentially exponential cost of failures in long production chains.121212For example, in Levine (2012), long chains involve a high degree of specialization and produce a large quantity of output but are also more prone to failure. However, chains in his model are long only if the failure rate is low thus mitigating the exponential impact that production failure of a single link has on output. Similarly, Costinot et al. (2013), in a global supply chain model where production of the final goods is sequential and subject to mistakes, show that countries with lower probabilities of making mistakes specialize in later stages of production. In this section, we show that these ideas are also amenable to analysis using the negative discount dynamic program from Section 2.

Consider, as before, a competitive market where producers implement a mass of tasks contained in . We drop the assumption of positive transaction costs and replace it with positive probability of defects.131313Defects can alternatively be understood as iceberg costs, where some percentage of goods are lost in transporting them from one producer to the next. Due to these defects, a producer who buys at stage and sells at must buy units of the partially completed good at to sell one unit of the processed good at . Larger then corresponds to a production process that is more prone to failure. Profits for such a firm facing price function are

This parallels the profit function (7) from the Coasian production chain model. If we adopt the Cobb–Douglass technology from Section 3.1.3, then the price of the final good is

| (11) |

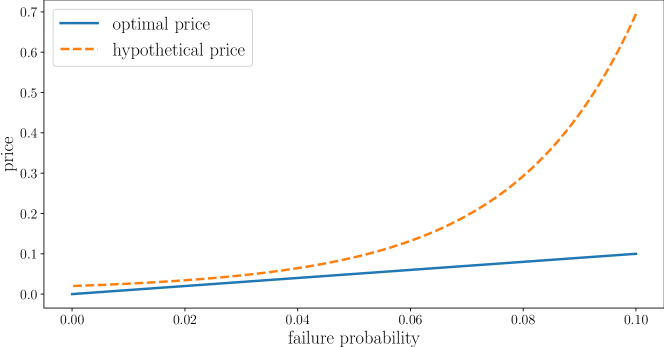

A rise in the failure probability leads to only a moderate increase in the final good price. This is because producers increase their range of internal production to mitigate any rise in cost associated with a higher production failure of upstream producers. As a result, there are fewer producers in production chains and the compounding effect of higher production failures is limited.

To clarify this point, let us compare this outcome with a hypothetical model where producers do not adjust their production according to failure probabilities. Suppose in particular that production chains are simply divided into equal tasks by producers. In this case, the final good price is

| (12) |

Now a small increase in increases the final good price exponentially. This is intuitive, as an increase in cost compounds over all producers involved in the production chain. See Figure 1 for a comparison of prices with and without producers adjusting for failure probabilities.141414In this example, we set , , and .

Thus, returning to the original model, we see that equilibrium prices induce producers to adjust to changes in failure probabilities, which optimally mitigates the potentially exponential impact of failures on the cost of the final good.

4. Application: Knowledge and Communication

Many firms are characterized by a pyramidal structure, in which employees form management layers with each layer smaller than the previous one. These features were modeled by Garicano (2000), where hierarchical organization of knowledge involves a trade-off between the cost of acquiring problem solving knowledge and the cost of communicating with others for help. In this section, we solve a version of Garicano’s model using the dynamic programming theory from Section 2.

Consider a firm where production requires solving a set of problems. Employees at management layer are assigned problems . They learn to solve at cost and pass on the remainder to the next management layer . This incurs additional communication costs that are proportional to the value of problems assigned to layer with coefficient .

Let be a (fictitious) price function that assigns value to problems. Profits of the th management layer are

where is the value of problems assigned to layer , is the cost of communicating and assigning unsolved problems to the next layer, and is the cost of learning to solve . Setting profits to zero and minimizing with respect to yields

This parallels the Bellman equation (3) of the negative discount dynamic program in Section 2.

Suppose that employees can learn to solve problems. In other words, for a given range of problems , the number of employees required to solve is . Assume that is strictly increasing, strictly concave, and continuously differentiable with , and that for some wage rate . Then the assumptions in (2) are satisfied if we let and . The Euler equation (EU) implies that the optimal sequence is decreasing, as is the number of employees in each layer as . This replicates Garicano’s result that the top management layer has the smallest number of employees and each layer below is larger than the one above.

The Euler equation (EU) adds additional insight: each layer of management acquires knowledge up to the point where the marginal cost of learning equals the marginal cost of communicating and assigning unsolved problems to the next layer. The envelope condition (EN) implies , which says that, in equilibrium, the marginal value of problems assigned to a management layer equals the marginal cost of learning to solve problems within the layer.151515This result is analogous to (9) for the production chain model and reminiscent of Coase’s theory of the firm in the context of knowledge organization within a firm.

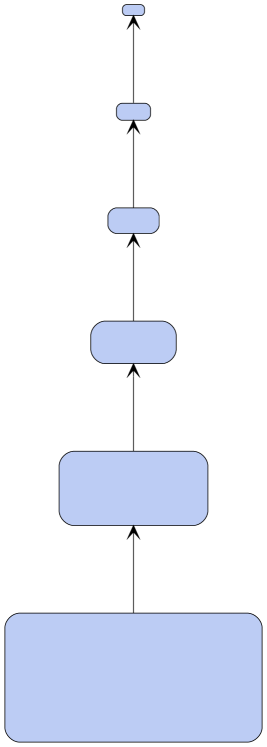

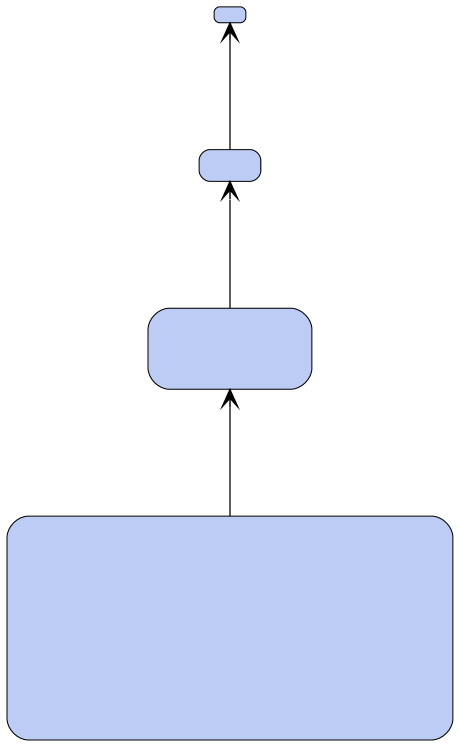

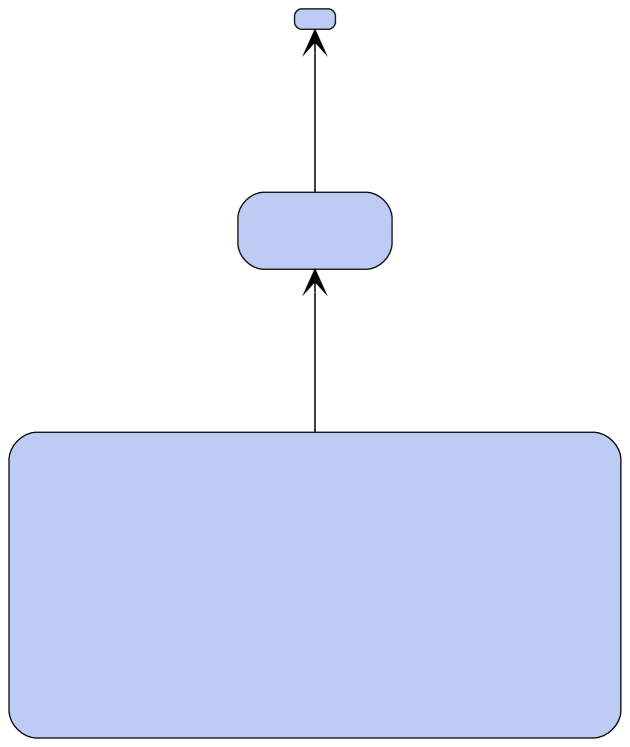

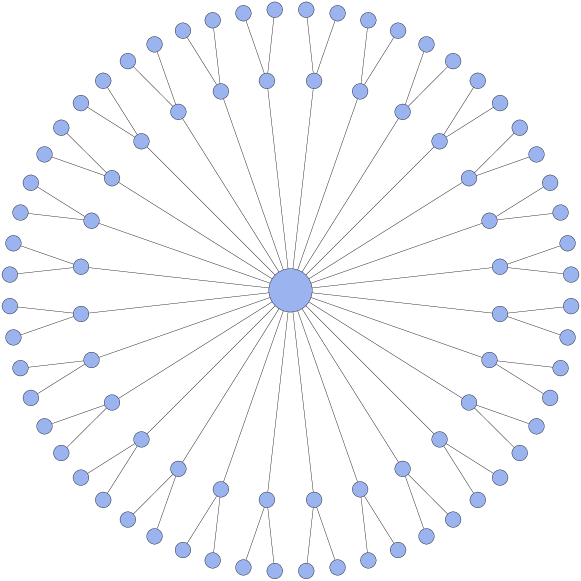

Figure 2 plots the optimal organizational structures of three firms given by the model above.161616We set and . Each node corresponds to one management layer, who asks the layer above for help, and its size is proportional to the number of employees in that layer. As shown in the graphs, each firm has a pyramidal structure and higher communication costs increase the relative knowledge acquisition of lower layers and reduce the number of layers.

5. Extension: Nonlinear Networks

In this section we treat more general network models that cannot be directly handled by the theory in Section 2. Unlike the linear chains discussed above, agents can interact with multiple partners. In Section 5.1, we study a problem from economic geography. In Section 5.2 we study chains with multiple upstream partners using a general dynamic programming theory developed in Appendix A.1.

5.1. Spatial Networks

The distribution of city sizes shows remarkable regularity, as described by the rank-size rule.171717See Gabaix and Ioannides (2004) and Gabaix (2009) for surveys. One early attempt to match the empirical city size distribution is found in the central place theory of Christaller (1933). Hsu (2012) and Hsu et al. (2014) formalize Christaller’s theory. In this section, we develop a model with similar insights by extending our earlier dynamic programming results.

Consider a government that opens competition for many developers to build cities to host a continuum of dwellers indexed by . Each developer can build a large city that hosts everyone or build a smaller city and pay other developers to build “satellite cities” that host the rest of the population. Further satellites can be built for existing cities until all dwellers are accommodated. This chain of city building starts with a single developer, who is assigned the whole population, and ends with a network of cities consisting of multiple layers.

Building satellite cities incurs extra costs that are charged as an ad valorem tax on the payments to the developers. We can think of the extra costs as costs of providing public goods that connect different cities such as roads, electricity, water, telecommunication, etc. Developers are paid according to a price , which is a function of the population assigned. The cost function of building a city is and the tax rate is . A developer assigned to host dwellers maximizes profits by solving

where is the payment to the developer, is the cost of building a city of population , is the number of satellite cities, and is the cost of assigning population to satellites. In equilibrium, a city network is formed where every dweller is accommodated and every developer makes zero profits. The equilibrium price function satisfies

| (13) |

To find the equilibrium price function, we first solve a negative discount dynamic program and then show that its value function is the solution to (13).

Consider a dynamic optimization problem with value function given by

| (14) |

The problem in (14) is a modified version of (1) that also features negative discounting and a convex loss function. In the context of our city network model, (14) describes a social planner who minimizes the total cost of hosting the whole population, where stands for the size of cities on layer .

In what follows we let with . To emulate the bifurcation process in Hsu (2012) and Hsu et al. (2014), we let . A similar argument to the proof of Proposition 2.3 gives the Euler equation

| (15) |

Using this equation, it can be shown with some algebra that for and the value function is . It is straightforward to verify that satisfies (13). Hence, the value function for the social planner is also the equilibrium price function under which all developers make zero profits.

The Euler equation (15) describes the emergence of optimal city hierarchy where each developer expands a city to accommodate more dwellers until the marginal cost of expanding equals the marginal cost of building and expanding satellite cities. An envelope condition similar to (EN) also holds: if a developer is assigned dwellers and delegate dwellers to satellite cities, the equilibrium is reached when . This shows that the marginal value that a city provides must be equal to the marginal cost of accommodating one more city dweller.

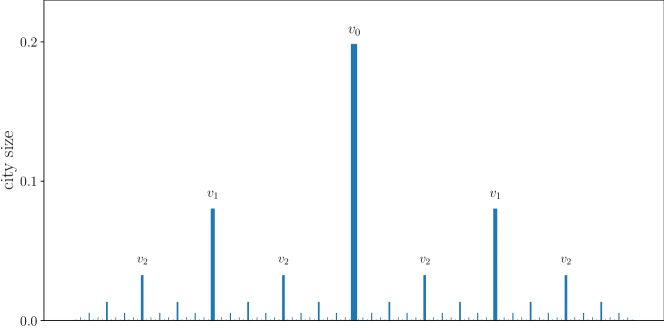

Figure 3 illustrates the optimal city hierarchy by placing cities according to Hsu (2012) and Hsu et al. (2014).181818We set and . It replicates the relative sizes of cities on different layers as in Hsu (2012) and Hsu et al. (2014). Moreover, since the number of cities doubles from one layer to the next, the rank of a city on layer is . Hence, the city size distribution generated by our model follows a power law similar to Hsu (2012). In fact, the rank and size of a city satisfy

where is a constant determined by . When approaches , the slope approaches one, which corresponds to the well-documented rank-size rule.

5.2. Snakes and Spiders

Modern production networks are characterized by processes that are both sequential and non-sequential. Baldwin and Venables (2013) refer to the sequential processes as “snakes” and the non-sequential processes as “spiders”, and analyze how the location of different parts of a production chain is determined by unbundling costs of production across borders. Here we study a model of production networks featuring both snakes and spiders.

As in Kikuchi et al. (2018) and Yu and Zhang (2019), we consider a generalization of the production chain model in Section 3.1, where each firm can also choose the number of suppliers. To account for costs of extending spiders, we assume that firms bear an additive assembly cost that is strictly increasing in the number of suppliers, with . Then for a firm at stage that subcontracts tasks of range to suppliers, the profits are

where is the price function. Having multiple suppliers leads to another trade-off: firms potentially benefit from subcontracting at a lower price but also have to pay additional assembly costs.

We index the layers in the production network by integers with layer 0 consisting only of the most downstream firm. Let be the downstream boundary of firms on layer , each producing and having suppliers. Then the boundary of firms on the next layer is given by . We call an equilibrium for the production network if (i) , (ii) for all and , and (iii) for all where

| (16) |

As in Section 3.1.2, we seek to find an equilibrium using dynamic programming methods. Let be the solution to the following Bellman equation

| (17) |

Let and where and are the minimizers under . Let be all continuous such that for all .

Proposition 5.1.

If and as , then (17) has a unique solution and is an equilibrium for the production network.

In Appendix A.5, we show that the unique solution can be computed by value function iteration. We then prove that induces an equilibrium allocation. Theorem A.2 can also be used to show the monotonicity of .

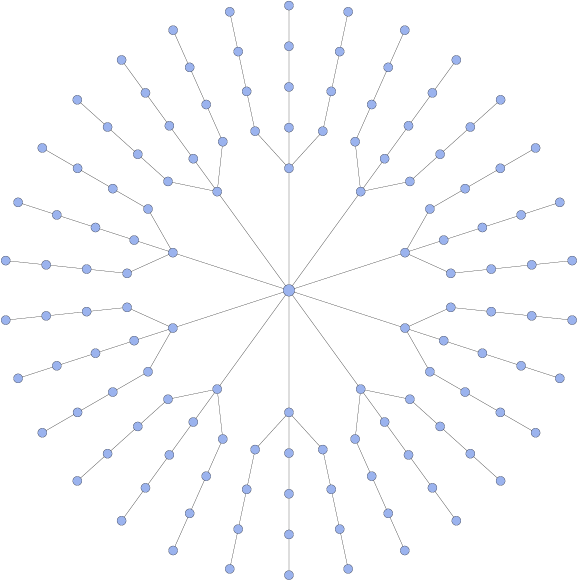

Figure 4 plots two production networks with different transaction costs, where each node corresponds to a firm in the network and the one in the center is the most downstream firm.191919We set and . The size of each node is proportional to the size of the firm, represented by the sum of assembly and transaction costs. Figure 4 shows that more downstream firms are larger and have more upstream suppliers. Comparing panels (A) and (B), we can see that lower transaction costs increase the number of firms involved in the production network, encouraging the expansion of snakes. This is in line with the model prediction of Baldwin and Venables (2013) that decreasing frictions leads to a finer fragmentation of the production.202020Tyazhelnikov’s (2019) model of international production chains shares some features with the model above. His model nests both snakes and spiders. Each firm makes optimal decision conditional on its production location at the next stage. If we interpret market transactions as offshoring, the multiple upstream supplier model becomes a model in which firms decide to produce parts of a production chain in any number of countries.

6. Conclusion

This paper shows how competitive equilibria in a range of production chain and network models can be recovered as solutions to dynamic programming problems. Equilibrium prices are identified with the value function of a dynamic program, while competitive allocations across firms are identified with choices under the optimal policy. Dynamic programming methods are brought to bear on both the theory of the firm and the structure of production networks, providing new insights, as well as new analytical and computational methods. In addition to production problems, we also consider related competitive problems from economic geography and firm management.

Apart from the model of snakes and spiders in Section 5.2, all of the problems faced by individual firms are convex. This assumption allowed us to obtain sharp results and useful characterizations. An important remaining task is to extend our results to a range of cases that feature non-convexities. This work is left for future research.

Appendix A Appendix

A.1. A General Dynamic Programming Framework

In this section, we provide a general dynamic programming framework suitable for analyzing equilibria in production networks.

A.1.1. Set Up

Given a metric space , let denote the set of functions from to and let be all continuous functions in . Given , we write if for all , and .

Let be a compact metric space. Let be a metric space and let be a nonempty, continuous, compact-valued correspondence from to . We understand as the set of available actions for an agent in state . Let be all feasible state-action pairs. Let be an aggregator, mapping into , with the interpretation that is lifetime loss associated with current state , current action and continuation value function . A pair with these properties is referred to as a dynamic program.

The Bellman operator associated with such a pair is the operator defined by

| (18) |

A fixed point of in is said to satisfy the Bellman equation.

A.1.2. Fixed Point Results

Fix a dynamic program and consider the following assumptions:

-

.

is continuous on when .

-

.

If with , then for all .

-

.

Given , and , we have

-

.

There is a in such that .

-

.

There is a in and an such that and .

Assumptions – impose some continuity, monotonicity and concavity. Assumptions – provide upper and lower bounds for the set of candidate value functions.

Although contractivity is not imposed, we can show that the Bellman operator (18) is well behaved under – after restricting its domain to a suitable class of candidate solutions. To this end, let

Theorem A.1.

Let be a dynamic program and let be the Bellman operator defined in (18). If satisfies –, then

-

1.

has a unique fixed point in .

-

2.

For each , there exists an and such that

(19) -

3.

is upper hemicontinuous on .

A.1.3. Shape and Smoothness Properties

We now give conditions under which the solution to the Bellman equation associated with a dynamic program possesses additional properties, including monotonicity, convexity and differentiability. In what follows, we assume that is convex in and is convex in . We let

-

1.

be all increasing functions in and

-

2.

be all convex functions in .

We assume that defined above contains at least one element of each set. The following assumption is needed for convexity and differentiability.

Assumption A.1.

In addition to –, the dynamic program satisfies the following conditions:

-

1.

If , then is strictly convex on .

-

2.

If and , then is differentiable on .

We can now state the following result.

Theorem A.2.

If is strictly increasing for all , then is strictly increasing. If Assumption A.1 holds, then is strictly convex, is single-valued, is differentiable on and

| (20) |

whenever .

A.1.4. The Principle of Optimality

If we consider the implications of the preceding dynamic programming theory, we have obtained existence of a unique solution to the Bellman equation and certain other properties, but we still lack a definition of optimal policies, and a set of results that connect optimality and solutions to the Bellman equation. This section fills these gaps.

Let be all such that for all . For each and , define the operator by

| (21) |

This can be understood as the lifetime loss of an agent following with continuation value . Let be the set of (nonstationary) policies, defined as all such that for all . For stationary policy , we simply refer it as . Let the -value function be defined as

| (22) |

where is the lower bound function in . Note that is always well defined. The agent’s problem is to minimize by choosing a policy in . The value function is defined by

| (23) |

and the optimal policy is such that . We impose the following assumption.

Assumption A.2.

In addition to –, the dynamic program satisfies the following conditions:

-

1.

If , and , then .

-

2.

There exists a such that, for all , and ,

(24)

Part 1 of Assumption A.2 is a weak continuity requirement on the aggregator with respect to the continuation value, similar to Assumption 4 in Bloise and Vailakis (2018). Part 2 of Assumption A.2 is analogous to the Blackwell’s condition, with the significant exception that in (24) is not restricted to be less than one.

Theorem A.3.

If Assumption A.2 holds, then and an optimal stationary policy exists. Moreover, a stationary policy is optimal if and only if .

A.2. Proofs for the General Theory

To prove Theorem A.1, we first give a fixed point theorem for monotone concave operators on a partially ordered Banach space due to Du (1989).212121The theory of monotone concave operators dates back to Krasnosel’skii (1964). Similar treatments include, for example, Guo and Lakshmikantham (1988), Guo et al. (2004), and Zhang (2013).

Theorem A.4 (Du, 1989).

Let be a normal cone on a real Banach space .222222A cone is said to be normal if there exists such that for all and . Suppose with and is an increasing concave operator. If for some and , then has a unique fixed point in . Furthermore, for any and , for some .

Proof of Theorem A.1.

By and Berge’s theorem of the maximum, is continuous. Hence maps to itself. It follows directly from that is isotone on , in the sense that implies . Conditions – and the isotonicity of imply that, when , we have . In particular, is an isotone self-map on .

The Bellman operator is also concave on , in the sense that

| (25) |

Indeed, fixing such and applying , we have

for all . Since, for any pair of real valued functions we have , it follows that (25) holds.

The preceding analysis shows that is an isotone concave self-map on . In addition, by and , we have and for some . Since is an order interval in the positive cone of the Banach space , and since that cone is normal and solid, the first two claims in Theorem A.1 are now confirmed via Theorem A.4. The final claim is due to Berge’s theorem of the maximum. ∎

Proof of Theorem A.2.

The first part of the theorem follows directly from the fact that is a closed subspace. The proof is omitted. To prove the strict convexity of , it suffices to show that is strictly convex for all since is a closed subspace of . Pick any with and any . Let . Pick any and let be such that . It follows that

where the first inequality holds because is strictly convex and the second inequality holds because is convex. Therefore, is strictly convex. Strict convexity of then implies that is single-valued.

We say that a dynamic programming problem has the monotone increasing property if for all and Assumption A.2 are satisfied. We state two useful lemmas from Bertsekas (2013).

Lemma A.5 (Proposition 4.3.14, Bertsekas (2013)).

Let the monotone increasing property hold and assume that the sets

are compact for all , , and greater than some integer . If satisfies , then . Furthermore, there exists an optimal stationary policy.

Lemma A.6 (Proposition 4.3.9, Bertsekas (2013)).

Under the monotone increasing property, a stationary policy is optimal if and only if .

Proof of Theorem A.3.

Theorem A.1 implies that . To prove , it suffices to show that the conditions of Lemma A.5 hold and .

It follows from that for all . Therefore, the monotone increasing property is satisfied. Since is a self-map on , to check the conditions of Lemma A.5, it suffices to prove that the set

is compact for any , , and . Since is continuous by , is a closed set. Since is compact-valued, is compact. It remains to show that . By and the monotone increasing property, we have for any , for all . Then by definition, for all . Taking the infimum gives . Lemma A.5 then implies that and there exists an optimal stationary policy. The principle of optimality follows directly from Lemma A.6. ∎

A.3. Proofs for Section 2

Let be the set of increasing convex functions in . Throughout the proofs, we regularly use the alternative expression for given by

| (26) |

Also, given , define

and

| (27) |

These functions are clearly well-defined, unique and single-valued. Let and . Let be the constant defined by

| (28) |

We begin with several lemmas. The proof of the first lemma is trivial and hence omitted.

Lemma A.7.

We have if and only if . If , then .

Lemma A.8.

If , then if and only if .

Proof.

First suppose that . Seeking a contradiction, suppose there exists a such that . Since we have and hence

Since , this implies that . Combining these inequalities gives , contradicting convexity of .

Now suppose that . We claim that , or, equivalently . To prove , observe that since we have , and hence

It follows that

Taking the limit gives . ∎

Proof of Proposition 2.1.

Let , and . Conditions – in Section A.1.2 obviously hold. Condition holds since . For condition , note that . Then if and if . For , so we can choose any . For ,

Since is increasing, we can choose any where . The first part of the proposition thus follows from Theorem A.1.

Consider the alternative expression for in (26). Since is strictly convex, is strictly convex for all . Hence, part 1 of Assumption A.1 holds. Evidently is strictly convex for all .

Next we show that is strictly increasing for all . Pick any and . For ease of notation, let for . If , then

where the first inequality holds since is available when is chosen and the second inequality holds since is strictly increasing. If , we first consider the case of . Then . For the case of , we have where . Since is not constant, implies that is strictly increasing. It follows that

Therefore, is a self-map on and is strictly increasing and strictly convex for all . Theorem A.2 then implies that is strictly increasing and strictly convex.

The next lemma further characterizes and .

Lemma A.9.

Let . If satisfy , then and . Moreover, if , then ; if , then .

Proof.

Pick any . Since and are convex, the maps and both satisfy the single crossing property. It follows from Theorem of Milgrom and Shannon (1994) that and are increasing.

For the last claim, since is increasing, Lemma A.8 implies that, if , then ; and if , then . ∎

The following lemma characterizes the solution to (1) and is useful when showing the equivalence between (1) and (3).

Lemma A.10.

If is a solution to (1), then is monotone decreasing and if and only if .

Proof.

The first claim is obvious, because if is a solution to (1) with , then, given that , swapping the values of these two points in the sequence will preserve the constraint while strictly decreasing total loss. Regarding the second claim, since is monotone decreasing, it suffices to check the case . To this end, suppose to the contrary that is a solution to (1) with and . Consider an alternative feasible sequence defined by , and for other . If we compare the values of these two sequences we get

The term inside the parenthesis converges to

where the first inequality follows from , and strict convexity of ; and the second inequality is by the definition of . We conclude that for sufficiently small, the difference is positive, contradicting optimality.

Finally we check the claim . Note that if then there is nothing to prove, so we can and do take . Seeking a contradiction, suppose instead that and . Consider an alternative feasible sequence defined by , and for other . In this case we have

The term inside the parentheses converges to

where the final equality is due to and Lemma A.7. Once again we conclude that for sufficiently small, the difference is positive, contradicting optimality. ∎

Proof of Proposition 2.2.

To show the equivalence between (1) and (3), we first show that (1) is equivalent to where is as defined in (22). Suppose that the optimal policy is and we let . Then we have

| (29) |

It is clear that is finite. Therefore, the optimal policy must satisfy , otherwise the last term in (29) would go to infinity. Let . We claim that solves (1). Suppose not and the solution to (1) is . Then by Lemma A.10, for all for some . Thus we can construct a policy that reproduces and gives a lower loss. This is a contradiction. Conversely, suppose that the solution to (1) is . Using the same argument, we can show that the policy that gives rise to is an optimal policy. Therefore, .

Next we show that using Theorem A.3. Both conditions in Assumption A.2 can be verified for . Part 1 of Assumption A.2 is trivial in this setting, since pointwise clearly implies at each . Part 2 also holds, since for any and , we have

Hence Theorem A.3 applies. It follows from Theorem A.3 that , there exists an stationary optimal policy, and the Bellman’s principle of optimality holds. Since satisfies , is a stationary optimal policy.

Proposition A.11.

For all and increasing convex , we have

Proposition A.11 implies uniform convergence in finite time. In particular, for we have everywhere on . Note that this bound is independent of the initial condition .

Proof of Proposition A.11.

It suffices to show that if , then on . We prove this by induction.

To see that on , pick any and recall from Lemma A.8 that if and , then . Applying this result to both and gives . Hence on as claimed.

Turning to the induction step, suppose now that on , and pick any . Let be arbitrary, let be the -greedy function, and let . By Lemma A.9, we have , and hence

In other words, given function , the optimal choice at is less than . Since this is true for both and , we have

Using the induction step we can now write

The last expression is just , and we have now shown that on . The proof is complete. ∎

Proof of Proposition 2.3.

Since , (EU) is equivalent to .

Sufficiency. Let and for . Let be any feasible sequence. Let and . It suffices to prove that

Since is convex, we have

Since , rearranging gives

Since , the summation is zero and . We have

Since and are feasible, and go to zero as . Hence .

Existence and Uniqueness. Since is feasible and satisfies for all , we have

where is well defined on because is increasing, strictly convex, and . Hence, is well defined on and is continuous and strictly increasing in . Since and , there exists a unique such that satisfying is feasible, for all , and is strictly decreasing. That is an optimal solution then follows from the sufficiency part. Since is strictly convex, the solution is unique.

Necessity. Since we have pinned down a unique solution of (1) which satisfies , the condition is also necessary. ∎

A.4. Proofs for Section 3

Proof of Proposition 3.1.

We must verify that satisfies Definition 3.1. We first consider the case of . By Propositions 2.1 and 2.2, the value function is a solution to the Bellman equation (3), and hence satisfies

| (30) |

and lies in the class of increasing, convex and continuous functions such that for all . In addition, with as the optimal state process (see Proposition 2.2), we have,

| (31) |

We need to show that 1–3 of Definition 3.1 hold when and for all . Part 1 is immediate because and all functions in must have this property, while Part 2 follows directly from (30). To see that Part 3 of Definition 3.1 also holds, let . By the definition of the state process, the sequence then corresponds to the downstream boundaries of a set of firms obeying task allocation . The profits of firm are . By (31) and , we have for all . Hence Part 3 of Definition 3.1 also holds, as was to be shown.

If , part 1 follows from the definition of the value function (6). By Proposition 2.3, for any with , there exists a unique optimal allocation such that , and . Since is a feasible allocation at stage with , part 2 follows from the definition of the value function. To see part 3, let and . By Proposition 2.3, we have . Since for all , it follows again from Proposition 2.3 that is an optimal allocation for stage . Therefore, for all . Hence, for all . ∎

A.5. Proofs for Section 5

Proof of Proposition 5.1.

To study this problem in the framework of Section A.1, we set , , , and

Since as , we can restrict to be so that is compact-valued. Under the conditions of Proposition 5.1, it can be shown that – hold with and (see Yu and Zhang (2019)). Then, Theorem A.1 implies that the Bellman equation (17) has a unique solution in , for all where

and and exist. We need only verify that given by , and is an equilibrium, the definition of which is given in Section 5.2.

References

- Antràs and De Gortari (2020) Antràs, P. and A. De Gortari (2020): “On the geography of global value chains,” Econometrica, 88, 1553–1598.

- Baldwin and Venables (2013) Baldwin, R. and A. J. Venables (2013): “Spiders and snakes: offshoring and agglomeration in the global economy,” Journal of International Economics, 90, 245–254.

- Benveniste and Scheinkman (1979) Benveniste, L. M. and J. A. Scheinkman (1979): “On the differentiability of the value function in dynamic models of economics,” Econometrica, 47, 727–732.

- Bertsekas (2013) Bertsekas, D. P. (2013): Abstract Dynamic Programming, Athena Scientific Belmont, MA.

- Bloise and Vailakis (2018) Bloise, G. and Y. Vailakis (2018): “Convex dynamic programming with (bounded) recursive utility,” Journal of Economic Theory, 173, 118–141.

- Boehm and Oberfield (2020) Boehm, J. and E. Oberfield (2020): “Misallocation in the market for inputs: enforcement and the organization of production,” The Quarterly Journal of Economics, 135, 2007–2058.

- Christaller (1933) Christaller, W. (1933): Central Places in Southern Germany, Translation into English by Carlisle W. Baskin in 1966, Englewood Cliffs, NJ: Prentice-Hall.

- Coase (1937) Coase, R. H. (1937): “The nature of the firm,” Economica, 4, 386–405.

- Coe and Yeung (2015) Coe, N. M. and H. W.-C. Yeung (2015): Global Production Networks: Theorizing Economic Development in an Interconnected World, Oxford University Press.

- Costinot et al. (2013) Costinot, A., J. Vogel, and S. Wang (2013): “An elementary theory of global supply chains,” The Review of Economic Studies, 80, 109–144.

- Du (1989) Du, Y. (1989): “Fixed points of a class of non-compact operators and applications,” Acta Mathematica Sinica, 32, 618–627.

- Epstein and Zin (1989) Epstein, L. and S. Zin (1989): “Substitution, risk aversion, and the temporal behavior of consumption and asset returns: a theoretical framework,” Econometrica, 57, 937–69.

- Fally and Hillberry (2018) Fally, T. and R. Hillberry (2018): “A Coasian model of international production chains,” Journal of International Economics, 114, 299–315.

- Farlow (2020) Farlow, A. (2020): “Beyond COVID-19: Supply Chain Resilience Holds Key to Recovery,” Tech. rep., Baker McKenzie.

- Gabaix (2009) Gabaix, X. (2009): “Power laws in economics and finance,” Annu. Rev. Econ., 1, 255–294.

- Gabaix and Ioannides (2004) Gabaix, X. and Y. M. Ioannides (2004): “The evolution of city size distributions,” in Handbook of Regional and Urban Economics, Elsevier, vol. 4, 2341–2378.

- Garicano (2000) Garicano, L. (2000): “Hierarchies and the organization of knowledge in production,” Journal of Political Economy, 108, 874–904.

- Garicano and Rossi-Hansberg (2006) Garicano, L. and E. Rossi-Hansberg (2006): “Organization and inequality in a knowledge economy,” The Quarterly Journal of Economics, 121, 1383–1435.

- Guo et al. (2004) Guo, D., Y. J. Cho, and J. Zhu (2004): Partial Ordering Methods in Nonlinear Problems, Nova Publishers.

- Guo and Lakshmikantham (1988) Guo, D. and V. Lakshmikantham (1988): Nonlinear Problems in Abstract Cones, Academic Press.

- Hsu (2012) Hsu, W.-T. (2012): “Central place theory and city size distribution,” The Economic Journal, 122, 903–932.

- Hsu et al. (2014) Hsu, W.-T., T. J. Holmes, and F. Morgan (2014): “Optimal city hierarchy: a dynamic programming approach to central place theory,” Journal of Economic Theory, 154, 245–273.

- Kamihigashi et al. (2015) Kamihigashi, T., K. Reffett, and M. Yao (2015): “An application of Kleene’s fixed point theorem to dynamic programming,” International Journal of Economic Theory, 11, 429–434.

- Kikuchi et al. (2018) Kikuchi, T., K. Nishimura, and J. Stachurski (2018): “Span of control, transaction costs, and the structure of production chains,” Theoretical Economics, 13, 729–760.

- Krasnosel’skii (1964) Krasnosel’skii (1964): Positive Solutions of Operator Equations, Noordhoff.

- Kremer (1993) Kremer, M. (1993): “The O-ring theory of economic development,” The Quarterly Journal of Economics, 108, 551–575.

- Levine (2012) Levine, D. K. (2012): “Production chains,” Review of Economic Dynamics, 15, 271–282.

- Loewenstein and Prelec (1991) Loewenstein, G. and D. Prelec (1991): “Negative time preference,” The American Economic Review, 81, 347–352.

- Loewenstein and Sicherman (1991) Loewenstein, G. and N. Sicherman (1991): “Do workers prefer increasing wage profiles?” Journal of Labor Economics, 9, 67–84.

- Lucas (1978) Lucas, R. E. (1978): “On the size distribution of business firms,” The Bell Journal of Economics, 508–523.

- Marinacci and Montrucchio (2019) Marinacci, M. and L. Montrucchio (2019): “Unique tarski fixed points,” Mathematics of Operations Research, 44, 1174–1191.

- Martins-da Rocha and Vailakis (2010) Martins-da Rocha, F. V. and Y. Vailakis (2010): “Existence and uniqueness of a fixed point for local contractions,” Econometrica, 78, 1127–1141.

- Milgrom and Shannon (1994) Milgrom, P. and C. Shannon (1994): “Monotone comparative statics,” Econometrica: Journal of the Econometric Society, 157–180.

- Rincón-Zapatero and Rodríguez-Palmero (2003) Rincón-Zapatero, J. P. and C. Rodríguez-Palmero (2003): “Existence and uniqueness of solutions to the Bellman equation in the unbounded case,” Econometrica, 71, 1519–1555.

- Stokey and Lucas (1989) Stokey, N. and R. E. Lucas (1989): Recursive Methods in Economic Dynamics (with EC Prescott), Harvard University Press.

- Thaler (1981) Thaler, R. (1981): “Some empirical evidence on dynamic inconsistency,” Economics Letters, 8, 201–207.

- Tyazhelnikov (2019) Tyazhelnikov, V. (2019): “Production Clustering and Offshoring,” Tech. rep., University of Sydney.

- Yu and Zhang (2019) Yu, M. and J. Zhang (2019): “Equilibrium in production chains with multiple upstream partners,” Journal of Mathematical Economics, 83, 1–10.

- Zhang (2013) Zhang, Z. (2013): Variational, Topological, and Partial Order Methods with Their Applications, vol. 29 of Developments in Mathematics, Springer Berlin Heidelberg.