Optimal life-cycle consumption and investment decisions under age-dependent risk preferences111Preprint

Abstract

In this article we solve the problem of maximizing the expected utility of future consumption and terminal wealth to determine the optimal pension or life-cycle fund strategy for a cohort of pension fund investors. The setup is strongly related to a DC pension plan where additionally (individual) consumption is taken into account. The consumption rate is subject to a time-varying minimum level and terminal wealth is subject to a terminal floor. Moreover, the preference between consumption and terminal wealth as well as the intertemporal coefficient of risk aversion are time-varying and therefore depend on the age of the considered pension cohort. The optimal consumption and investment policies are calculated in the case of a Black-Scholes financial market framework and hyperbolic absolute risk aversion (HARA) utility functions. We generalize Ye (2008) (2008 American Control Conference, 356-362) by adding an age-dependent coefficient of risk aversion and extend Steffensen (2011) (Journal of Economic Dynamics and Control, 35(5), 659-667), Hentschel (2016) (Doctoral dissertation, Ulm University) and Aase (2017) (Stochastics, 89(1), 115-141) by considering consumption in combination with terminal wealth and allowing for consumption and terminal wealth floors via an application of HARA utility functions. A case study on fitting several models to realistic, time-dependent life-cycle consumption and relative investment profiles shows that only our extended model with time-varying preference parameters provides sufficient flexibility for an adequate fit. This is of particular interest to life-cycle products for (private) pension investments or pension insurance in general.

keywords:

Pension investments , optimal life-cycle consumption and investment , age-dependent risk aversion , HARA utility function , martingale methodJEL:

G11 , G22 , C61 , D141 Introduction

A suitable management of pensions needs to consider earnings/contributions and investment, but should also account for the required consumption during the accumulation and/or decumulation phase. For this sake, in this paper we consider the finite horizon portfolio problem of maximizing expected utility of future consumption and terminal wealth to determine the optimal pension or life-cycle fund strategy for a cohort of pension fund investors. The setup is strongly related to a DC pension plan where additionally (individual) consumption is taken into account. Within this framework, Lakner and Nygren (2006) describe the trade-off the investor faces as a compromise between ‘living well’ (consumption) and ‘becoming rich’ (terminal wealth). Classical consumption-investment problems consider constant risk aversion in the intertemporal utility functions for consumption besides a personal discount rate or impatience factor, see Merton (1969) or Merton (1971). Within classical models (where constant relative risk aversion (CRRA) utilities are applied), optimal portfolio policies turn out to be constant over the life-cycle, meaning time and wealth independent. According to Aase (2017) this is ‘against empirical evidence, and against the typical recommendations of portfolio managers’. Furthermore, Aase (2017) and Yang et al. (2014) argue that the tendency of stocks to outperform bonds over long horizons in the past is one of the reasons why people at a younger age are advised to allocate a higher proportion of wealth to equities compared to older people. Evidence for changing risk aversion over the life-cycle is reported in the literature, although there is no broad agreement on its behavior: Morin and Suarez (1983), Bakshi and Chen (1994), Palsson (1996), Bellante and Green (2004), Al-Ajmi (2008), Ho (2009), Yao et al. (2011) and Albert and Duffy (2012) observe increasing risk aversion by age, Bellante and Saba (1986) and Wang and Hanna (1997) find risk aversion decreasing by age and Riley and Chow (1992) detect different behavior between the pre- and post-retirement phase. Age-depending risk preferences can economically be motivated by the observed behavior of people to stepwise reduce their investment risk the closer to retirement. This behavior is reflected in many life-cycle fund allocation policies, see for instance Gebler and Matterson (2010) or Erickson and Cunniff (2015). An important economic reasoning behind is that the older the person, the less time to retirement entrance is left and therefore the less likely it is for her to overcome a potential market crash, strongly connected to the fear of having an insufficient wealth left for retirement. Moreover, it is reasonable that the closer to retirement time, the more satisfaction is connected with savings, i.e. with a lower consumption surplus, which yields a higher initial wealth for the decumulation phase. Based on these economic reasons, it is meaningful to consider age-varying preference parameters (dependent on the age of the pension cohort or the individual investor) in form of a coefficient of risk aversion, later called , and a weighting factor, later referred to as , that governs the relative importance of consumption at different points in time. The latter has no impact on risk aversion but can control for the varying preference between consumption and terminal wealth over time. In an analysis of the optimal controls in Section 4 we show that our proposed model can explain and describe people’s observed behavior of reducing relative risky investments by time while simultaneously targeting a certain function for the consumption rate on average. In opposite, we find that the previously described existing models are not able to capture this behavior. Therefore, particulary Section 4 shows that it is economically important to have separate functions or parameters for risk aversion and preference of consumption over terminal wealth, and .

In addition, consumption and wealth floors are introduced which have an economic meaning as minimum required levels of consumption and wealth. This motivates the development of a dynamic life-cycle model with time-varying risk preferences such as coefficient of risk aversion and consumption and wealth floors which can capture age-depending consumption and investment behavior of investors.

Related literature to this topic consider stochastic income and unemployment risks, see Bodie et al. (1992), Koo (1998), Munk (2000), Viceira (2001), Huang and Milevsky (2008), Jang et al. (2013), Bensoussan et al. (2016), Wang et al. (2016) or Chen et al. (2018). Setups where the investor faces uncertain lifetime, mortality and optimal life insurance are considered in Yaari (1965), Pliska and Ye (2007), Menoncin and Regis (2017), Zou and Cadenillas (2014), Kronborg and Steffensen (2015), Shen and Wei (2016), Duarte et al. (2014), Huang et al. (2012), Kronborg and Steffensen (2015), Shen and Wei (2016) and Ye (2008); optimal consumption and investment under insurer default risk is studied by Jang et al. (2019). Kraft and Munk (2011), Kraft et al. (2018), Andréasson et al. (2017), Cuoco and Liu (2000) and Damgaard et al. (2003) analyze optimal housing as a durable good. Constraints in the optimization problem are considered in Cuoco (1997), Elie and Touzi (2008) and Grandits (2015). Moreover, Akian et al. (1996), Altarovici et al. (2017) and Dai et al. (2009) analyze the portfolio problem under transaction costs. The application of HARA utility functions in a life-cycle context can be found in Huang and Milevsky (2008), Ye (2008), Chang and Rong (2014), Chang and Chang (2017) and Wang et al. (2017). Moreover, Back et al. (2019) study a life-cycle consumption problem for HARA utility with time-independent, increasing risk aversion and examine the relation between age and portfolio risk by using Monte Carlo analysis. Tang et al. (2018) study an optimal consumption-investment problem under CRRA utility function with age-independent risk aversion, but examine the impact of hyperbolic discounting, where the rate of time preference is a function of time. We generalize this approach by considering general or , respectively, and by introducing age-varying risk aversion.

In this paper we apply HARA utility functions on both the consumption and terminal wealth and consider time-varying preferences: an age-depending preference between consumption and terminal wealth and an age-depending coefficient of risk aversion in the intertemporal consumption utility. For simplicity, income is treated as a deterministic process. Furthermore, we do not model mortality and consider a fixed time horizon that corresponds to a retirement age, thus we assume the agent to survive up to the age of retirement. A positive, fixed floor in the terminal utility ensures a minimum liquid asset wealth level at the age of retirement, which is meaningful as the retiree needs wealth to live from and could possibly afford housing from this wealth. In addition, a positive, time-varying floor in the consumption utility guarantees a minimum (time-dependent) consumption rate. This is essential during the accumulation phase as for instance living expenses, rental payments when home is rented or mortgage payments and maintenance costs when home is bought and financed by debt or only maintenance costs when the agent already fully owns a house (e.g. inherited) need to be covered. Therefore, the economic demand for both a positive minimum level of consumption and terminal wealth can be motivated.

Most related to our work are Ye (2008), Steffensen (2011), Hentschel (2016) and Aase (2017). The difference of our approach to these papers is as follows. Ye (2008) considers income, mortality and HARA utilities for both consumption and terminal wealth under a constant coefficient of risk aversion, i.e. constant , but where the age-dependent preference between consumption and wealth is incorporated. We generalize the results by introducing a time-dependent coefficient of risk aversion . Steffensen (2011) provides a first insight into the optimal policy when the utility parameters of the intertemporal utility, which is of a CRRA type, are time-varying; thus and are captured. But the model disregards terminal wealth, consumption floor and labor income. In a similar fashion, Hentschel (2016) studies the consumption problem for CRRA utility with habit formation and considers and . Similar to Steffensen (2011), neither terminal wealth nor consumption floor nor income are included in their model. Finally, Aase (2017) uses the martingale method (that allows to reformulate the optimal stochastic control problem to a simpler maximization problem with constraint) to determine optimal consumption and investment under mortality and a CRRA utility with age-depending risk aversion . But the model does not consider terminal wealth, consumption floor, income or time-varying preference .

The main contributions and innovations of this paper can be summarized as follows: we consider all the ‘ingredients’ of the models in the above mentioned papers (, , terminal wealth, floors for consumption and terminal wealth via HARA utilities, income process) that leads to a novel, very flexible and more realistic dynamic life-cycle model framework. We extend or generalize Ye (2008) by adding an age-dependent coefficient of risk aversion and Steffensen (2011), Hentschel (2016) and Aase (2017) by considering terminal wealth and allowing for consumption and terminal wealth floors via an application of HARA utility functions. The corresponding consumption-investment problem is solved analytically and interpretation is provided. In a case study, where we fit realistic predetermined target policies for consumption and relative allocation to several models, we realize that only our proposed and most general model is sufficiently flexible to describe human preferences on consumption and investment in a suitable fashion. This implies that modeling the agent’s preferences in an age-depending fashion is inevitable.

To solve the respective portfolio problem, we follow a separation approach similar to the ones developed by Karatzas and Shreve (1998) and Lakner and Nygren (2006). It divides the original consumption-terminal wealth optimization problem into two sub-problems, the corresponding consumption problem and the terminal wealth problem. These separate problems are to be solved individually. Due to time-dependent preference parameters we apply the martingale method in line with Aase (2017) to solve the individual problems in closed form. Afterwards, we show how the individual solutions have to be glued together in order to obtain the general solution to the original consumption-terminal wealth problem.

The remainder of this paper is organized as follows. Section 2 introduces the financial market and the portfolio problem of interest, Section 3 shows the separation approach and the solution to the problem. A fit of the analytic strategy to suitable consumption and investment curves is conducted in Section 4, followed by an investigation of the optimal controls and corresponding wealth process. Section 5 concludes. A summarizes all proofs of the claimed statements: the proofs for Section 3.1 on the consumption problem can be found in A.1, the proofs related to Section 3.2 on the terminal wealth problem in A.2, and for the proofs associated with Section 3.3 on merging both individual solutions, see A.3.

2 The financial market model and consumption-investment problem

We consider a frictionless financial market which consists of continuously traded assets, one risk-free asset and risky assets. Let represent the fixed and finite investment horizon. Uncertainty in the continuous-time financial market is modeled by a complete, filtered probability space , where is the sample space, the real-world probability measure, is the natural filtration generated by , , augmented by all the null sets, and , , , is a standard -dimensional Brownian motion. The price of the risk-free asset at time is denoted by and is subject to the equation

| (1) |

with constant risk-free interest rate . The remaining assets in the market are risky assets with price , , at time subject to the stochastic differential equations

| (2) |

with constant drift , , and constant volatility vector . The volatility matrix is defined by , the covariance matrix of the log-returns is which is assumed to be strongly positive definite, i.e. there exists such that -a.s. it holds , . Furthermore, let denote the market price of risk. In this case of Black-Scholes market dynamics, according to Karatzas and Shreve (1998), there exists a unique risk-neutral probability measure defined by and the market is complete (that allows to value payment streams under the measure as expected discounted values, meaning that the cost of a portfolio replicating the contract is given by its expected discounted value under ). The corresponding pricing kernel or state price deflator, denoted by , is defined as

| (3) |

and can be used for the valuation of payment streams under the real-world probability measure. Its dynamics are subject to the stochastic differential equation

We consider -progressively measurable trading strategies , , such that -a.s. it holds and . represents the number of individual shares of asset held by the investor at time . The corresponding relative portfolio process is denoted by with risky relative investment and risk-free relative investment , where denotes the fraction of wealth allocated to asset at time . It is to satisfy , -a.s.. Moreover, let denote a non-negative, progressively measurable, real-valued stochastic consumption rate process with , -a.s., and a non-negative, deterministic income-rate process with . Those technical conditions are assumed to get a solution for the subsequently formulated stochastic problem. The dynamics of the investor’s wealth process under the strategy to initial wealth , including liquid assets, consumption and income, is then given by

| (4) |

The relative investment in the risk-free asset is . We consider the objective of maximizing expected utility of future terminal wealth and consumption, starting at time and ending at . Hence the objective function to be maximized is

| (5) |

where denotes the initial endowment of the investor. All expectations in this paper are with respect to the real-world measure . The general portfolio optimization problem with initial wealth to be solved is then given by

| (6) |

subject to (4). is the value function of the problem. denotes the set of admissible strategies such that , -a.s., , and which admit a unique solution to (4) while satisfying the integrability condition . The so-called budget constraint reads

| (7) |

It describes the requirement that today’s value of future consumption and terminal wealth, less income, must not exceed the initial endowment. It can be shown that for the optimal to Problem (6), Equation (7) holds with equality. We consider a preference utility model given by the utility functions

| (8) | ||||

for , continuous, , , , , , deterministic, and with . is a continuously differentiable and strictly concave terminal utility function, denotes a continuous (intertemporal consumption) utility function which is continuously differentiable and strictly concave in the second argument. This utility model accounts for several desired aspects: minimum liquid asset wealth level at the age of retirement , minimum consumption rate and time-varying preference of consumption over terminal wealth in terms of . Moreover, the coefficient of risk aversion in the consumption utility is now a continuous function in time.

Remark 1

Notice that the associated Arrow-Pratt measure of absolute risk aversion, developed by Pratt (1964) and Arrow (1970), admits the following hyperbolic representation

For this reason, we use the notation of an increasing as a synonym for a decreasing coefficient of risk aversion and vice versa. Further note that does not appear in . Therefore we have two input functions and where has no influence on risk aversion, but determines it; hence a very flexible model.

Since we have and by definition of the utility functions in (8), we restrict

| (9) |

on the initial endowment in (7). It is useful to define

| (10) |

can be interpreted as the time value of all future minimal liabilities less income. equals the sum of the time wealth necessarily required to meet all the future minimum living expenses and expenditures , during the remaining time and the time value of the minimum desired terminal wealth level ; future salary income is subtracted as it reduces the time value of the minimum required capital.

3 Solution: Separation technique

In the sequel we follow the separation technique approach by Karatzas and Shreve (1998) and Lakner and Nygren (2006) for solving the consumption-terminal wealth problem as defined by (6). We split the problem into two sub-problems: the consumption-only and terminal wealth-only problem. Both individual problems are separately solved via the martingale method, similar to the approach by Aase (2017). The individual problem solutions are optimally merged at the end. For this sake, let us consider the two individual problems first.

3.1 The consumption problem

The consumption-only problem is

| (11) | ||||

subject to the budget constraint

| (12) |

denotes the set of admissible strategies such that , -a.s., , and which admit a unique solution to (4) while satisfying .

Steffensen (2011) provides a proof for CRRA utility functions by solving the associated Hamilton-Jacobi-Bellman (HJB) equation. We follow the approach by Aase (2017), likewise for a HARA utility function. We extend the findings of Aase (2017) by introducing a time-varying, deterministic consumption floor , a time-varying preference function of consumption over terminal wealth and an income-rate process .

In order to guarantee the consumption rate floor, note , let us assume the following lower boundary for which equals the integral over the discounted consumption floor rate minus income rate over the whole horizon of interest:

| (13) | ||||

Notice that is possible since a sufficiently large positive income stream can be high enough to finance consumption. Using the martingale method we solve the problem as summarized by the theorem below.

Theorem 2

We remind the reader that all proofs can be found in A. It is clear that , a.s.. We now aim to interpret the optimal investment strategy as proportional portfolio insurance (PPI) strategy. The first strategy family corresponds to a constant multiple, the latter one is more general and also covers proportional strategies with time-varying or even state-dependent multiples. Zieling et al. (2014) evaluate the performance of such strategies. Theorem 2 shows that the optimal investment strategy generally is a PPI strategy with time-varying floor at time , equal to the time value of the accumulated outstanding future consumption floor minus income. Notice that can firstly be determined at time , since the value depends on the stochastic which is not known before time . Hence, is time- and also state-dependent and thus the optimal PPI strategy itself is time- and state-dependent through its PPI multiple. The PPI multiple in summary is time-varying, state-dependent and depends on all future coefficients of risk aversion via .

Furthermore, holds by the assumption in (13). In addition, converges to when approaches . Thus, a.s., which additionally follows directly from the formula for in Theorem 2. This further implies that is an admissible pair, i.e. . The next remark provides the solution under time-independent risk aversion.

Remark 3

When , then

which is a conventional CPPI strategy with constant multiple. Moreover, if , i.e. the minimum consumption is eating up the whole income, then

which is a constant mix strategy and represents the standard, well-known result for CRRA utility with constant risk aversion parameter.

Some comments on the initial capital and the sign of the risky investments come next. As already pointed out, a start with a negative initial capital to Problem (11) is possible and might be reasonable in a sense that accumulated income over the life-cycle is expected to exceed total consumption. Hence, there is no need to require positive capital to this problem. For this reason, can happen and might be reasonable, too.

Theorem 2 tells that the optimal relative investment strategy is given by

where a.s.. Let for , which for instance is the case when there is only one risky asset () because then since was assumed. Then

Even if the first part of the remark argues that is a meaningful case, the conclusion under sounds odd at a first glance. But when looking at the optimal exposure to risky asset , one finds that

which, under , is positive no matter if or . Therefore, the amount of money invested in the risky assets is always positive. The opposite inequalities and conclusions for and apply if . In summary, the sign of the optimal exposure to the single risky assets is determined by

Thus, is possible although it might be .

Finally, let for all . When , the optimal exposure to the risk-free asset is negative because

This in turn implies that in case of , the investor takes leverage by borrowing from the risk-free account to achieve her investment goals. Leverage at this point can make sense as future income provides some security; note that immediately implies that the time value of accumulated future income exceeds the expected value of consumption.

Some more properties of can be found analytically as follows. The first and second derivative of , , with respect to wealth are

Let for , then

-

1.

.

-

2.

either and or and .

This implies that at time :

-

1.

is increasing in if and only if , and decreasing in otherwise.

-

2.

is concave in if and only if

-

(a)

either and

-

(b)

or and ,

and convex in otherwise.

-

(a)

The opposite inequalities and conclusions for and its derivatives apply if .

The optimal controls in Theorem 2 determine the value function and the value for as follows.

Theorem 4

The optimal value function to Problem (11) is strictly increasing and concave in . Its value and first and second derivative with respect to the initial budget are given by

3.2 The terminal wealth problem

The terminal wealth-only problem is

| (16) | ||||

subject to the budget constraint

| (17) |

denotes the set of admissible strategies such that , -a.s., , and which admit a unique solution to (4) for .

In order to guarantee the terminal wealth floor, note , let us assume the following lower bound for which equals the discounted terminal floor:

| (18) |

Applying the martingale approach leads to the solution to the terminal wealth problem according to the upcoming theorem.

Theorem 5

Theorem 5 shows that the optimal fraction of wealth allocated to the risky assets follows a CPPI strategy with floor at time , with constant multiple. Moreover, by the assumption in (18). In addition, converges to when approaches . Thus, it follows a.s., which additionally yields that is an admissible pair, i.e. . The characteristics a.s. also directly follows from the formula for in Theorem 5. The next remark shows that the optimal proportion allocated to the risky assets is constant over time if one disregards the floor .

Remark 6

When , then

which is a constant mix strategy and equals the standard result for CRRA utility with constant risk aversion parameter, where the optimal fraction of wealth allocated to the single risky assets does not depend on time or wealth.

In what follows we analyze some characteristics of the optimal strategy . The first and second derivative of , , with respect to wealth are

Let for . Then and , where the inequalities hold strictly when . Hence, increases and is concave in the wealth . Otherwise, if for , then decreases and is convex in the wealth . For the optimal exposure to the risky assets it therefore holds

Thus, either it is and or and .

The optimal controls in Theorem 5 determine the value function and the value for .

3.3 Optimal merging of the individual solutions

Let denote the optimal controls to Problem (11) with optimal wealth process to the initial wealth and the optimal controls to Problem (16) with optimal wealth process to the initial wealth . Then merging the two solutions to solve Problem (6) is based on the following theorem.

Theorem 8

The connection between the value functions is

Notice that , hence (9) ensures that is claimed. When discounted future income exceeds consumption over the considered period, i.e. when the initial budget to the consumption problem is negative (), then and a higher amount of money is invested according to the terminal wealth problem at initial time as the initial endowment of the investor.

Theorem 8 shows that an optimal allocation to consumption and terminal wealth at together with the solution to the two separate problems equals the solution to the original optimization problem. The optimal initial budgets are denoted by and . The next lemma provides a condition for and .

Lemma 9

The optimal solves

| (19) |

and is subject to . The optimal is then given by .

Within our specified setup, we can address the condition in Lemma 9 in more detail, the result is provided next.

Lemma 10

The optimal to (19) exists uniquely and satisfies the boundary condition . is the solution to the equation

| (20) |

with

| (21) |

The optimal is given by .

Moreover, the optimal Lagrange multiplier is given by

For general and , as the unique solution to Equation (20) can for instance be determined numerically. Denote by with the optimal allocation of the initial wealth according to Lemma 10 in what follows and denote and . We use the individual solutions to the two separate Problems (11) and (16) and merge both solutions optimally according to Lemma 10 to obtain the solution to the original Problem (6).

Theorem 11

It follows immediately that , a.s.. Theorem 11 furthermore proves that the general optimal relative investment strategy can be written as a mixture of a PPI and a CPPI strategy, but is not necessarily of a PPI or even CPPI type itself. The PPI comes from the consumption-only problem, see Theorem 2, the CPPI arises as the solution to the terminal wealth-only problem, see Theorem 5. The way which of the two strategies dominates the overall optimal investment policy is initially determined by the wealth distribution through and and later through and . The special case where the coefficient of risk aversion from consumption equals the one from terminal wealth at any time is covered by the next remark.

Remark 12

Assume constant. Then the optimal controls turn into

with

where

The optimal investment strategy now is a traditional CPPI strategy with floor and constant multiple vector . The optimal consumption rate is the sum of the consumption floor and the time-varying proportion of the cushion at time . The fraction between the risky exposure (vector) and consumption is time-varying and it holds

| (22) |

Optimal consumption as well as, under , optimal risky exposure linearly increase in the cushion . Hence, the higher the surplus , the more is invested risky and the more is consumed. The formula (22) shows that, under , an increase in the cushion leads to a stronger increase in the risky exposure than in consumption . Therefore, for a larger surplus , also the relative increase in the risky exposure is larger than the relative increase in consumption, thus investing money in stocks is preferred to consuming.

The associated optimal wealth process is given as a function of the pricing kernel

This special case result coincides with the findings by Ye (2008), who used the HJB approach, extended by additionally providing the optimal wealth process .

We aim to interpret the optimal for time-varying and particularly to point out the difference to constant in Remark 12. Writing where follows the wealth process of a standard CPPI strategy with floor at time to the initial endowment and constant multiplier vector , we obtain the following representation of the optimal investment decision

| (23) |

which can be implemented easily; is defined in (10). Formula (23) shows that the optimal relative allocation can be written as a PPI strategy in with floor plus a PPI strategy in with floor . Alternatively, write , where is the replicating wealth process of a PPI strategy with floor to the initial wealth and now time- and state-varying multiplier vector and, in contrast to , a non-zero consumption rate process. Then can be reformulated as

| (24) | ||||

This formula shows that the optimal relative investment is the sum of a conventional CPPI strategy on with floor and a PPI strategy on with floor .

Recall from Remark 12 that for constant follows a traditional CPPI strategy to the floor . The formula for in (24) shows that the optimal strategy for time-varying consists of two parts:

-

1.

The first part coincides with and is a traditional CPPI strategy in to the floor .

-

2.

The second, additional part is a time- and state-varying term which can be either positive, negative or zero; hence it can reduce or increase risky investments or can leave it unmodified in comparison with .

It is the second part which leads to a deviation in compared to . For this sake, we analyze this second piece in what follows. Note that by Theorem 2 it holds a.s..

-

1.

If , for instance this is reasonable for and an income rate that outweighs or exceeds consumption, then it follows

This implies for at time :

-

(a)

:

-

(b)

:

-

(c)

:

-

(a)

-

2.

If , for instance this is reasonable for and a high demand for consumption in the past, then it follows

This in turn implies for at time :

-

(a)

:

-

(b)

:

-

(c)

:

-

(a)

In particular, consider the situation and let hold for risky asset . Under , the optimal relative investment in stock , which is , is reduced compared to the relative investment decision under . Since can be interpreted as higher risk aversion for consumption than terminal wealth, this is meaningful.

In the situation the interpretation seems counterintuitive at first glance. But when looking at risky exposures rather than risky relative investments, analogue conclusions hold. The same approach shall be used when considering .

Furthermore, it is worth to mention that approaches when approaches , which can be observed in (23); the argument is the following: When falls towards , then automatically approaches and converges towards simultaneously, since , and , a.s. which was already shown in Sections 3.1 and 3.2. We moreover proved that in this case and approach . By Theorem 11 it follows that also must converge to . Therefore, as is assumed, it follows that a.s., which can additionally be seen in the respective formula in Theorem 11, and the optimal decision rules provide portfolio insurance over the whole life-cycle. is called the minimum asset wealth level, it holds .

The optimal exposure to the risky assets equals the sum of the optimal risky exposures of the two sub-problems

and by the findings in Sections 3.1 and 3.2 it holds

For the ease of exposition we so far assumed that the income process is deterministic. The following remark shows the solution for a stochastic income process.

Remark 13 (Stochastic income process)

Let be a non-negative, stochastic income-rate process with , -a.s.. The stated results are still valid after replacing integrals of the form by the more general conditional expectation by the Bayes formula for arbitrary , in particular in the definition of and . If is supposed to be independent to , i.e. independent to the market stochastics, then the conditional expectation can be reduced to . For the lower bounds of and , (9) and (13) need to be replaced by

where denotes the minimal level of income; is meaningful due to unemployment benefits paid by the government.

4 Analysis of optimal controls and wealth process: A case study

This section targets to calibrate the life-cycle model to realistic time-dependent structures for consumption and investment observed in practice and outline the difference between our presented solution with age-depending and functions and the models with either only or time-varying or none. Hence, we not only estimate , and for our model, but additionally provide the respective estimates when or , or both, are assumed to be constants. A comparison of the fit of the different models allows for making a statement on the accuracy of the models in describing the agent’s behavior. For notational convenience we call the three benchmark models as follows:

-

1.

: constant, time-varying

-

2.

: time-varying, constant

-

3.

: and constant

The subscript thus indicates whether or are age-varying. Therefore, our model is denoted by . As already indicated in Section 1, is (partially) covered by Steffensen (2011), Hentschel (2016) and Aase (2017), and are covered by Ye (2008).

In the later Subsection 4.3, we additionally analyze the impact of the floors and , where our model is compared to the same model but with CRRA utility functions, i.e. and . The CRRA model is denoted by and is (partially) considered by Steffensen (2011), Hentschel (2016) and Aase (2017).

4.1 Assumptions

We assume an exemplary agent with average income, liabilities etc. A similar case study can be carried out for a pension cohort, but for simplicity and data availability we consider an individual client. In detail, we make the following (simplifying) assumptions:

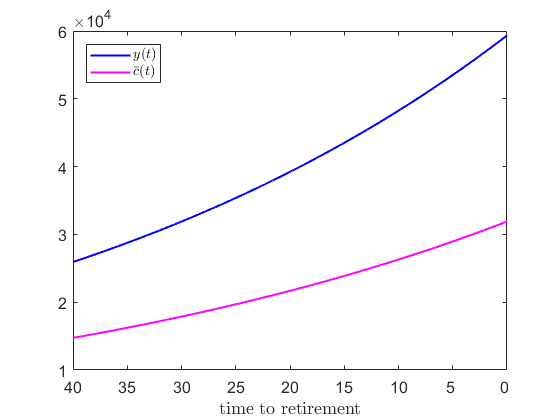

Let the market consist of one risk-free and one risky asset () with parameters , , and ; these values correspond approximately to the EURONIA Overnight Rate and the performance of the DAX 30 Performance Index as an equity index over the year period from 17 October 2007 to 17 October 2018. The risky asset can coincide with, but is not restricted to a pure equity portfolio. In general it can be any arbitrary given portfolio which consists of risky assets. The price process of the risky asset is assumed to be with initial price . Furthermore, let years be the time to retirement, years the current age of the investor and years the age of retirement. For the net salary function it is assumed with EUR and . This corresponds to a net annual starting salary approximately equal to the average for a graduate in Germany in 2017 (cf. online portals Absolventa GmbH (2018) or StepStone (2017)), with an annual increase equal to the average for a household’s net salary in Germany over years 2011 to 2016 according to Statistisches Bundesamt (2018). Net income accumulated over the first year is and income accumulated within the year from time to is .

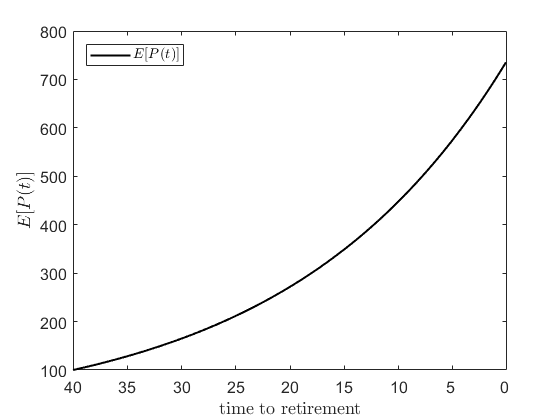

For the agent’s utility functions, let (cf. Ye (2008)) and . Let the terminal wealth floor be EUR which is motivated by the following argument: According to Statistisches Bundesamt (2017), Deutsche Aktuarvereinigung e.V.(2017) (DAV) or Wirtschaftskammer Österreich (2016) a lifetime around years can be expected for a currently year old person in Germany. Thus survival of years are expected after retirement at the age of . We assume that the agent secures the income inflow during retirement to be of the last wage paid from year to (replacement ratio of ), which is EUR. Assume that every year, half of this amount is covered by a separate pension account or plan, e.g. provided by the government. In addition, the agent wants to secure against longevity risk, hence considers years instead of years for the remaining lifetime after the age of retirement. Thus, as value at time is chosen to be . Finally, the function for the net consumption floor is supposed to take the form with EUR and . This corresponds to a starting value equal to approximately of the average household consumption in Germany in 2016 as starting point, with an annual increase equal to the increase in average household consumption in Germany over years 2011 to 2016 (published by Statistisches Bundesamt (2018)). Minimum consumption expenses incurred within the first year is , within year to is . The assumed income and consumption floor rates are visualized in Figure 1.

4.2 Fitting / Calibration under exponential preferences and discussion

In what follows we calibrate the remaining utility parameters , and to suitable curves for consumption and relative allocation. The targeted curves for parameter fitting are summarized by Table 1. The consumption rate is calibrated with respect to the hump-shaped type observed by Carroll (1997), Gourinchas and Parker (2002), Jensen and Steffensen (2015) and Tang et al. (2018). The relative risky investment is calibrated towards the rule of thumb; a similar structure is frequently applied by financial advisors and asset management companies for life-cycle funds (see Malkiel (1990), Bodie and Crane (1997), Shiller (2005), Minderhoud et al. (2011), Gebler and Matterson (2010), Shafir (2013)). Following this popular rule, the client at age years starts with a equity investment, linearly decreases it by her age such that she ends with a investment in equities at the age of retirement with years. We would like to mention that in particular relative risky investment curves or products provided by asset management companies are to be understood deterministic, i.e. wealth- / state-independent. Therefore, we calibrate the remaining unknown parameters with respect to the expected values for consumption and risky relative investment. In more detail, we fit the expected value for consumption, which is , to the given consumption curve. For we apply the following estimate: we estimate the risky exposure without any bias and then replace by its unbiased expectation to obtain the estimate for . By doing this we replace by and fit the latter expression to the given linear relative investment curve. For further readings on deterministic investment strategies we refer to Christiansen and Steffensen (2013) and Christiansen and Steffensen (2018). In summary, we have unbiased estimates for the expected values of optimal consumption, risky exposure and wealth process, and a modified estimate for the expectation of the optimal relative risky investment.

| in EUR, | in EUR, |

| rule (total stock ratio) | thus EUR ( of average household consumption in Germany in 2016, cf. Statistisches Bundesamt (2018), as starting consumption rate), turning point at (age ) with a maximum targeted consumption of EUR. |

Let and take the form of an exponential function, i.e. and . Moreover, let EUR. The estimation is carried out via the Matlab function lsqcurvefit which solves nonlinear curve-fitting (data-fitting) problems in a least-squares sense and minimizes the sum of the squared relative distances. The underlying time points for target consumption and allocation are set weekly on an equidistant grid which yields points in the time interval with .

Table 2 gives an overview of the estimated utility parameters and provides the sum of squared relative errors as a quality criterion. The errors show that considering age-depending functions and simultaneously in model leads to a comparatively huge improvement in accuracy of the fit compared to any of the three benchmark models: model sum of squared relative distances is only of the respective sum for model which provides the second best fit in terms of sum of squared relative residuals.

| Sum of squared relative distances | ||||

|---|---|---|---|---|

| , | , | |||

| , | , | |||

| , | , | |||

| , | , |

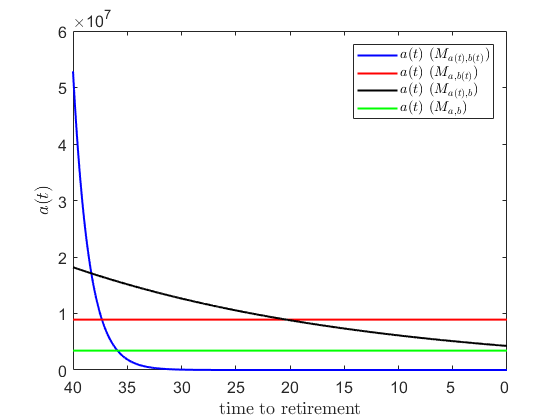

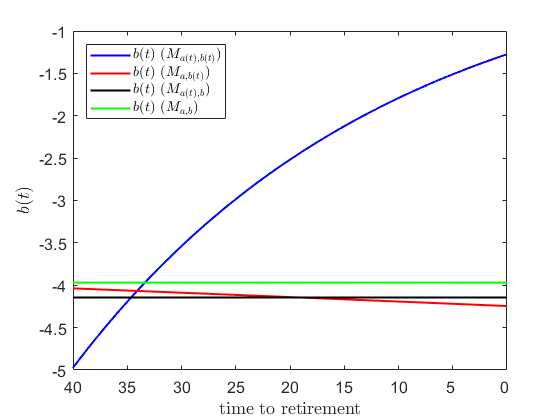

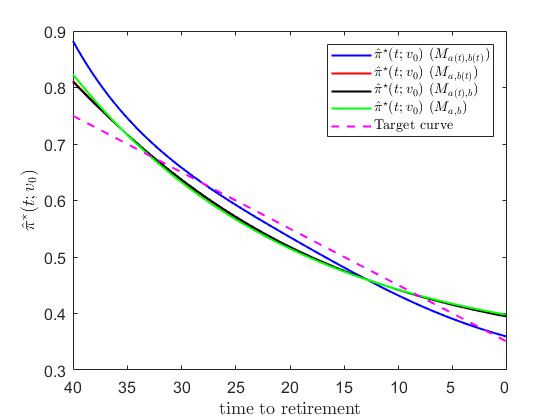

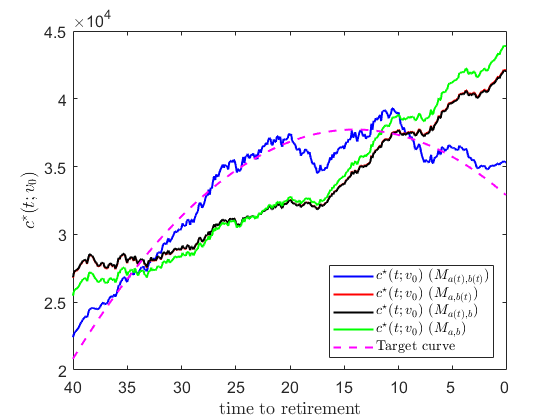

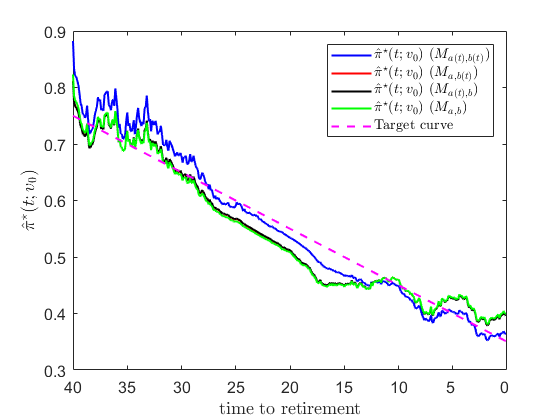

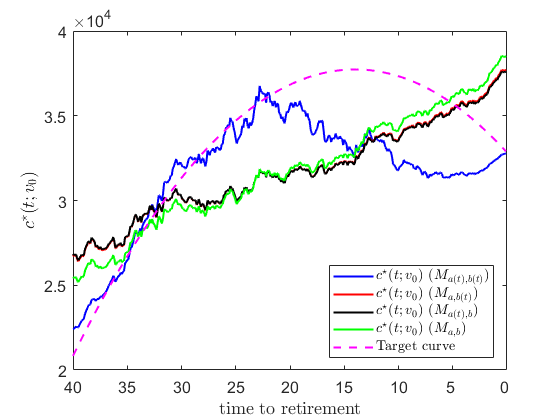

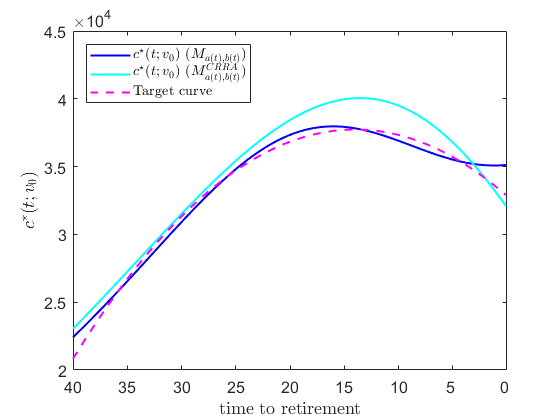

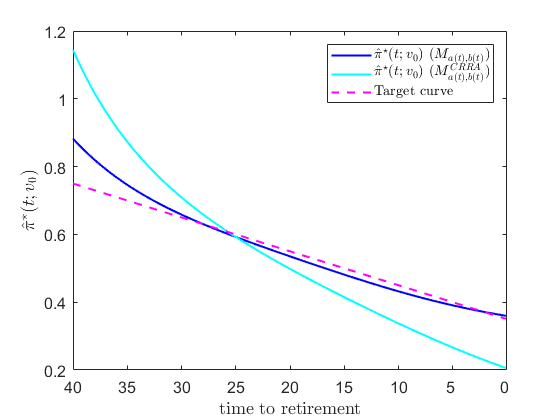

Figure 2 visualizes the fitted parameters and preference functions , , . The table and figure show that the estimated coefficient of risk aversion for our model is more negative, which means a higher risk aversion, compared to the three benchmark models , , . Furthermore, is decreasing both within model and . In contrast, increases in model over time whereas it decreases in the comparison model . in models , , stay very close over the whole life-cycle whereas in starts more negative and ends less negative. In summary, this means that in model the risk aversion decreases through increasing , but preference of the investor between consumption and terminal wealth is shifted more and more to terminal wealth through decreasing .

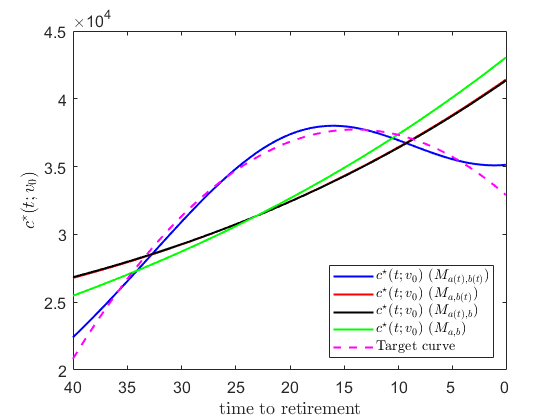

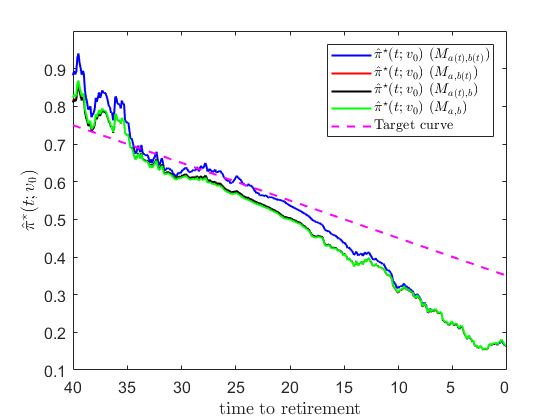

Figure 3 illustrates the expected optimal consumption rate and relative risky investment for the fitted parameters in comparison with the given target policies or average profile. In addition to Table 2 the figure illustrates that, under exponential preferences and , only the most flexible model provides an accurate and precise fit for both consumption rate and risky relative allocation. We realize that the benchmark models , , apparently do not provide enough flexibility to simultaneously describe the predetermined consumption and relative allocation curves. Whereas the fits for the relative investment look acceptable, all three benchmark models fail in explaining the targeted consumption rate . We further notice that and for the models and are very similar (red and black lines in the respective figures).

In summary, Table 2 and Figure 3 demonstrate that model is the only one among our considered models which provides enough flexibility to model a hump-shaped consumption decision curve besides a linear risky allocation curve. All three benchmark models, which disregard time-dependency of or or both, do not lead to a satisfactory fit. In addition, fitting optimal consumption of the four models to the given consumption curve, while ignoring relative investments, shows the same picture. The result is that the sum of the squared distances associated with model is only of the respective sum associated with the second best model . This supports our findings and conclusion that time-varying preference parameters are indeed needed to model the given time-dependent hump-shaped consumption and linear risky allocation in an accurate way.

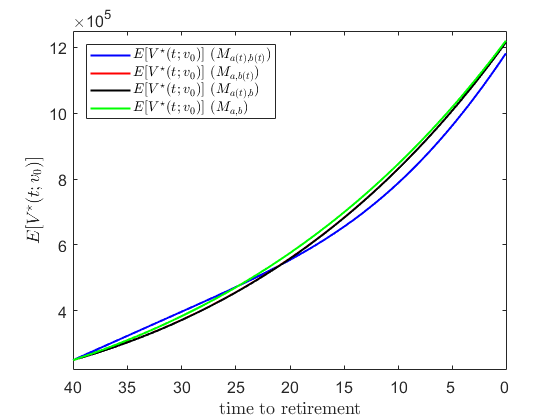

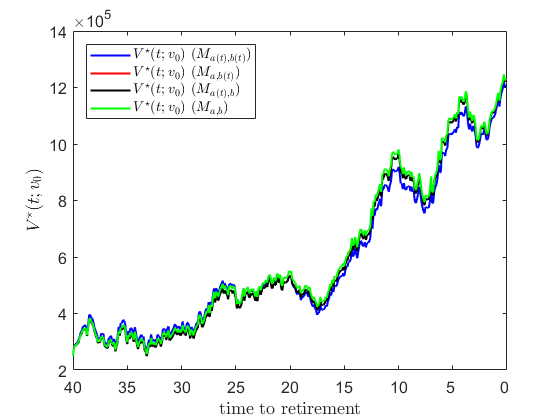

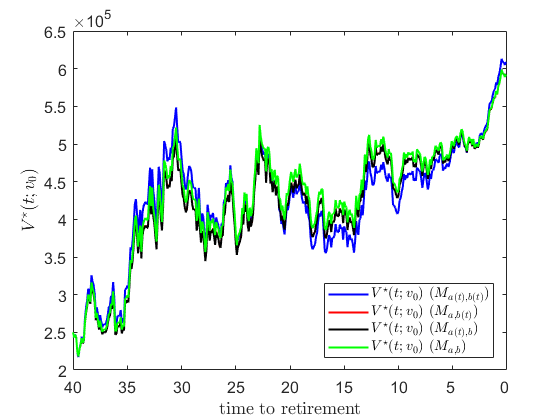

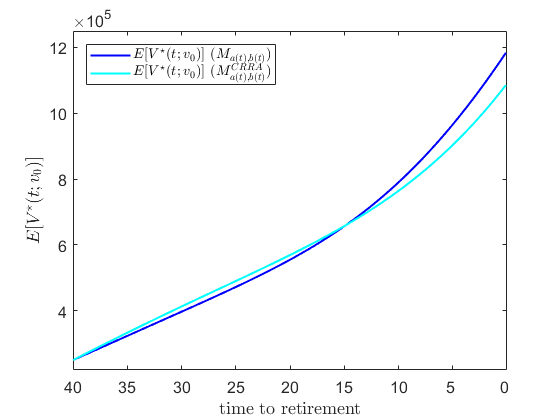

In addition to the parameter estimation for the expected path, we provide the figures for optimal consumption, risky relative portfolio and wealth process of all four models under two representative scenarios: a mostly upward (see Figure 4) and a mostly downward (see Figure 5) moving path for the underlying stock. The corresponding expected paths for the consumption rate, the relative risky investment and the wealth process can be found in Figure 3.

In the increasing stock price case optimal consumption and risky relative allocation for model stay very close to the targeted curve since the corresponding wealth stays close to its expected path and shows some reverting behavior. For a stronger increasing underlying price process, consumption exceeds the given consumption curve for the expected path. When the stock price decreases, then optimal consumption and risky allocation for model fall below the target curves after approximately to years. In particular higher consumption can no longer be afforded due to a poorly performing equity market. This goes hand in hand with a reduction on the relative risky allocation.

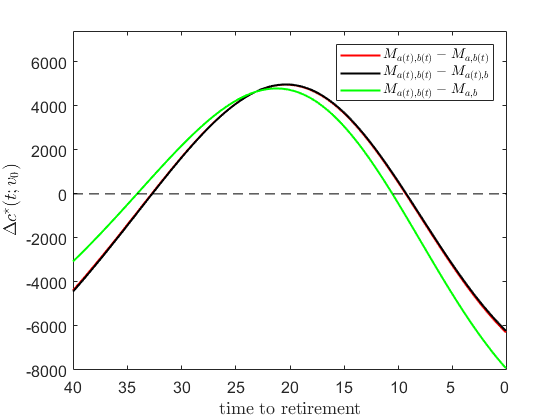

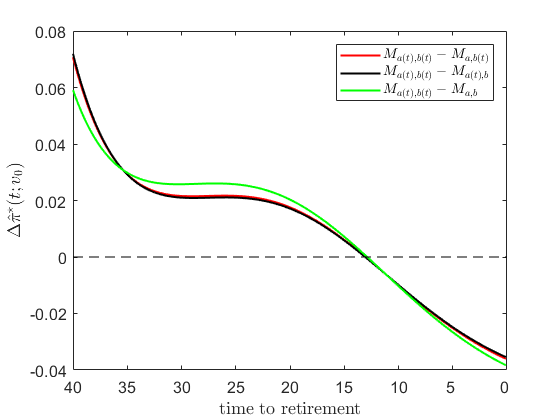

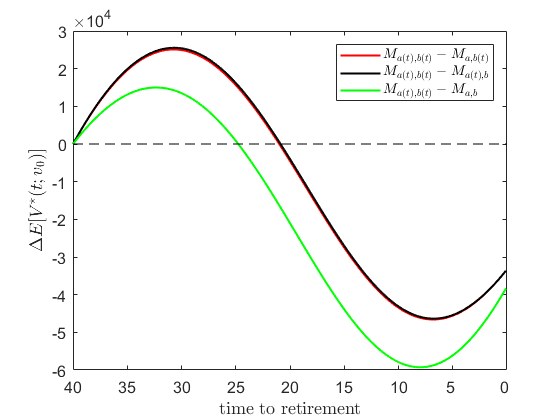

At first glance, it seems that there is a big difference in optimal consumption between our model and the three benchmark models , and while optimal risky investments and wealth paths for all four models remain in a quite narrow area, although deviation of risky investments from its target curve can be high. This is due to different scales for wealth and consumption. Figure 6 visualizes the differences, denoted by , in the fitted consumption and relative risky investment and the corresponding wealth process for the three benchmark models to our model within the expected path situation. It can be observed that relative risky allocation of model exceeds the ones associated with the three benchmark models in the first half of the considered period of years by up to eight percentage points, and falls below in the second half. Moreover, the difference looks monotone decreasing in age. Furthermore, the wealth process which corresponds to model outperforms the three benchmark models in the first half, but provides a lower wealth in the second half due to a higher consumption rate from approx. year to , with a certain recovery in the wealth close to retirement.

The two exemplary scenarios and the expected development situation which was used for fitting show that the benchmark models , and overestimate the given consumption curve in early and older years (close to and ) and underestimate it in between. For our model , the optimal consumption rate stays very close to its target curve until consumption cannot be afforded anymore because of a low wealth as result of a strong market decline. We conclude that especially within phases of poor stock performance, both and can deviate a lot from their given curves.

4.3 Comparison with CRRA

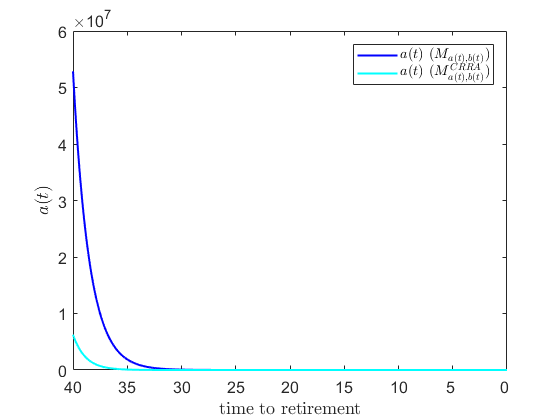

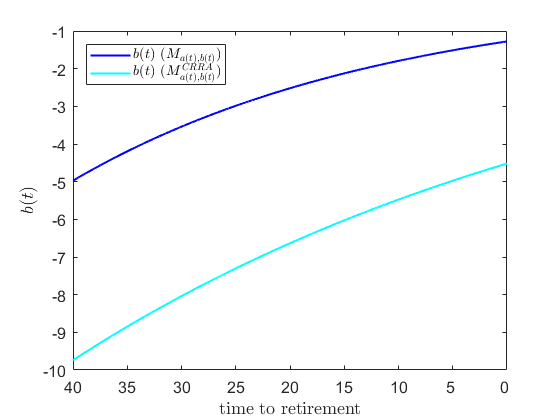

We conclude the case study section by exploring the impact of minimum consumption and wealth floors on calibration and optimal controls. For this sake, we fit the model to the very same parameters and target curves as before, but now enforce and . This CRRA model is referred to as . Table 3 provides the estimated parameters and the sum of the squared relative residuals. In terms of this sum, it is clear that model provides a more adequate fit than model , its sum is only of the sum which corresponds to . Going even further, all three benchmark models , and from the previous subsection, which all consider minimum levels for consumption and wealth, provide a more precise fit than in view of the sum of squared relative residuals. This shows that the introduction of floors for consumption and wealth in the model is essential.

| Sum of squared relative distances | ||||

|---|---|---|---|---|

| , | , | |||

| , | , |

Figure 7 visualizes the estimated input functions, Figure 8 provides the graphics about the fitted consumption and relative risky portfolio process with the expected wealth and stock price path. Besides a larger sum of the squared relative distances for model , especially the fitted risky investments in Figure 8 show that zero floors for consumption and wealth ( and ) leads to an imprecise calibration and a large deviation from its given target curve due to a drop in model flexibility. Table 3 suggests that this drop in flexibility is attempted to be compensated by a higher risk aversion in terms of more negative estimated values for and , see also Figure 7.

5 Conclusion

This paper studies the optimal quantitative and dynamic consumption and investment strategies under age-dependent risk preferences (coefficient of risk aversion and preference between consumption and terminal wealth ). The findings demonstrate that strategies applied for life-cycle pension funds or pension insurance could significantly be improved by taking age-dependent risk preferences into account. For this reason, the paper combines the elements terminal wealth with a minimum level and consumption under time-varying risk preferences and minimum level into a dynamic life-cycle consumption-investment model. A sound economic understanding of the model parts is provided. In Section 3 the corresponding portfolio optimization problem is solved analytically with a separation approach which allows to solve the consumption and the terminal wealth part of the original consumption-investment problem separately. The formulas show that age-depending risk preferences in combination with terminal wealth considerations and minimum levels for consumption and wealth have a significant impact on the optimal controls.

Section 4 investigates the optimal controls and provides a comparison with already existing and solved benchmark models. The analysis is divided into two parts. In the first part the risk preferences are calibrated towards given realistic curves for consumption and investment. The result emphasizes that only our proposed flexible model, in comparison with the other considered benchmark models, provides an adequate fit of the agent’s behavior. We draw the conclusion that time-varying preferences (risk aversion and preference between consumption and terminal wealth ) are necessary to provide a sufficient degree of flexibility to accurately fit the two control variables consumption and investment: Our proposed model turns out to be able to explain the given investor consumption and investment decisions, but the benchmark models fail. The very same result is obtained when time-dependent preference functions are considered, but the consumption and wealth floors are omitted. The second part focuses on the behavior analysis of the optimal consumption, investment and wealth under a positive and negative market environment.

Future research on this topic could deal with generalizations of the dynamic life-cycle model. For instance, investment constraints could be included to make the whole setup more applicable as budgets in practice are commonly exposed to constraints on allocation or risk. Furthermore, since unemployment risk and uncertain future income are essential for individuals, those risks and impacts on the optimal controls and wealth process could be further explored. Finally, including mortality and a life insurance product into the model could help people in determining their optimal individual life insurance investment embedded in a more realistic, flexible framework.

Acknowledgements

Pavel V. Shevchenko acknowledges the support of Australian Research Council’s Discovery Projects funding scheme (project number DP160103489).

References

- Aase (2017) Knut K. Aase. The investment horizon problem: a possible resolution. Stochastics, 89(1):115–141, 2017.

- Absolventa GmbH (2018) Absolventa GmbH. Einstiegsgehalt von Berufseinsteigern 2018, 2018. URL https://www.absolventa.de/karriereguide/arbeitsentgelt/einstiegsgehalt.

- Akian et al. (1996) Marianne Akian, Jose Luis Menaldi, and Agnes Sulem. On an Investment-Consumption Model with Transaction Costs. SIAM Journal on Control and Optimization, 34(1):329–364, 1996.

- Al-Ajmi (2008) Jasmin Al-Ajmi. Risk Tolerance of Individual Investors in an Emerging Market. International Research Journal of Finance and Economics, 17:15–26, 2008.

- Albert and Duffy (2012) Steven M. Albert and John Duffy. Differences in Risk Aversion between Young and Older Adults. Neuroscience and Neuroeconomics, 2012(1):3–9, 2012.

- Altarovici et al. (2017) Albert Altarovici, Max Reppen, and H. Mete Soner. Optimal consumption and investment with fixed and proportional transaction costs. SIAM Journal on Control and Optimization, 55(3):1673–1710, 2017.

- Andréasson et al. (2017) Johan G. Andréasson, Pavel V. Shevchenko, and Alex Novikov. Optimal consumption, investment and housing with means-tested public pension in retirement. Insurance: Mathematics and Economics, 75:32–47, 2017.

- Arrow (1970) Kenneth J. Arrow. Essays in the Theory of Risk-Bearing. North-Holland Publising Company, Amsterdam, 1970.

- Back et al. (2019) Kerry Back, Ruomeng Liu, and Alberto Teguia. Increasing risk aversion and life-cycle investing. Mathematics and Financial Economics, 13(2):287–302, 2019.

- Bakshi and Chen (1994) Gurdip S. Bakshi and Zhiwu Chen. Baby Boom, Population Aging, and Capital Markets. The Journal of Business, 67(2):165–202, 1994.

- Bellante and Green (2004) Don Bellante and Carole A. Green. Relative risk aversion among the elderly. Review of Financial Economics, 13(3):269–281, 2004.

- Bellante and Saba (1986) Don Bellante and Richard P. Saba. Human capital and life-cycle effects on risk aversion. The Journal of Financial Research, 9(1):41–51, 1986.

- Bensoussan et al. (2016) Alain Bensoussan, Bong-Gyu Jang, and Seyoung Park. Unemployment Risks and Optimal Retirement in an Incomplete Market. Operations Research, 64(4):1015–1032, 2016.

- Bodie and Crane (1997) Zvi Bodie and Dwight B. Crane. Personal Investing: Advice, Theory, and Evidence. Financial Analysts Journal, 53(6):13–23, 1997.

- Bodie et al. (1992) Zvi Bodie, Robert C. Merton, and William F. Samuelson. Labor supply flexibility and portfolio choice in a life cycle model. Journal of Economic Dynamics & Control, 16:427–449, 1992.

- Carroll (1997) Christopher D. Carroll. Buffer-stock saving and the life cycle / permanent income hypothesis. The Quarterly Journal of Economics, 112:1–55, 1997.

- Chang and Chang (2017) Hao Chang and Kai Chang. Optimal consumption-investment strategy under the Vasicek model: HARA utility and Legendre transform. Insurance: Mathematics and Economics, 72:215–227, 2017.

- Chang and Rong (2014) Hao Chang and Xi-min Rong. Legendre Transform-Dual Solution for a Class of Investment and Consumption Problems with HARA Utility. Mathematical Problems in Engineering, 2014:1–7, 2014.

- Chen et al. (2018) An Chen, Felix Hentschel, and Xian Xu. Optimal retirement time under habit persistence: what makes individuals retire early? Scandinavian Actuarial Journal, 3:225–249, 2018.

- Christiansen and Steffensen (2013) Marcus C. Christiansen and Mogens Steffensen. Deterministic mean-variance-optimal consumption and investment. Stochastics, 85(4):620–636, 2013.

- Christiansen and Steffensen (2018) Marcus C. Christiansen and Mogens Steffensen. Around the Life-Cycle: Deterministic Consumption-Investment Strategies. North American Actuarial Journal, 22(3):491–507, 2018.

- Cuoco (1997) Domenico Cuoco. Optimal Consumption and Equilibrium Prices with Portfolio Constraints and Stochastic Income. Journal of Economic Theory, 72:33–73, 1997.

- Cuoco and Liu (2000) Domenico Cuoco and Hong Liu. Optimal consumption of a divisible durable good. Journal of Economic Dynamics & Control, 24:561–613, 2000.

- Dai et al. (2009) Min Dai, Lishang Jiang, Peifan Li, and Fahuai Yi. Finite Horizon Optimal Investment and Consumption with Transaction Costs. SIAM Journal on Control and Optimization, 48(2):1134–1154, 2009.

- Damgaard et al. (2003) Anders Damgaard, Brian Fuglsbjerg, and Claus Munk. Optimal consumption and investment strategies with a perishable and an indivisible durable consumption good. Journal of Economic Dynamics & Control, 28:209–253, 2003.

- Deutsche Aktuarvereinigung e.V.(2017) (DAV) Deutsche Aktuarvereinigung (DAV) e.V. Sterbetafeln: Der statistische Blick auf die Lebenserwartung, 2017. URL https://aktuar.de/fachartikelaktuaraktuell/AA38_Sterbetafeln.pdf#search=lebenserwartung.

- Duarte et al. (2014) I. Duarte, D. Pinheiro, A. A. Pinto, and S. R. Pliska. Optimal life insurance purchase, consumption and investment on a financial market with multi-dimensional diffusive terms. Optimization, 63(11):1737–1760, 2014.

- Elie and Touzi (2008) Romuald Elie and Nizar Touzi. Optimal lifetime consumption and investment under a drawdown constraint. Finance and Stochastics, 12:299–330, 2008.

- Erickson and Cunniff (2015) Hans Erickson and John Cunniff. TIAA-CREF Asset Management: Lifecycle 2060 Fund. Technical report, Teachers Insurance and Annuity Association of America-College Retirement Equities Fund (TIAA-CREF), 730 Third Avenue, New York, NY 10017, 2015.

- Gebler and Matterson (2010) Jeff Gebler and Wade Matterson. Life Cycle Investing for the Post-retirement Segment. Technical report, Milliman, North Sydney NSW 2060, Australia, August 2010. Milliman Research Report.

- Gourinchas and Parker (2002) Pierre-Olivier Gourinchas and Jonathan A. Parker. Consumption over the life cycle. Econometrica, 70(1):47–89, 2002.

- Grandits (2015) Peter Grandits. An optimal consumption problem in finite time with a constraint on the ruin probability. Finance and Stochastics, 19:791–847, 2015.

- Hentschel (2016) Felix Hentschel. Planning for individual retirement: optimal consumption, investment and retirement timing under different preferences and habit persistence. PhD thesis, Ulm University, 2016.

- Ho (2009) H. Ho. An experimental study of risk aversion in decision-making under uncertainty. International Advances in Economic Research, 15:369–377, 2009.

- Huang and Milevsky (2008) Huaxiong Huang and Moshe A. Milevsky. Portfolio choice and mortality-contingent claims: The general HARA case. Journal of Banking & Finance, 32:2444–2452, 2008.

- Huang et al. (2012) Huaxiong Huang, Moshe A. Milevsky, and Thomas S. Salisbury. Optimal retirement consumption with a stochastic force of mortality. Insurance: Mathematics and Economics, 51:282–291, 2012.

- Jang et al. (2013) Bong-Gyu Jang, Seyoung Park, and Yuna Rhee. Optimal retirement with unemployment risks. Journal of Banking & Finance, 37:3585–3604, 2013.

- Jang et al. (2019) Bong-Gyu Jang, Hyeng Keun Koo, and Seyoung Park. Optimal consumption and investment with insurer default risk. Insurance: Mathematics and Economics, 88:44–56, 2019.

- Jensen and Steffensen (2015) Ninna Reitzel Jensen and Mogens Steffensen. Personal finance and life insurance under separation of risk aversion and elasticity of substitution. Insurance: Mathematics and Economics, 62:28–41, 2015.

- Karatzas and Shreve (1998) Ioannis Karatzas and Steven E. Shreve. Methods of Mathematical Finance. Springer, New York, 1998.

- Koo (1998) Hyeng Keun Koo. Consumption and Portfolio Selection with Labor Income: A Continuous Time Approach. Mathematical Finance, 8(1):49–65, 1998.

- Kraft and Munk (2011) Holger Kraft and Claus Munk. Optimal Housing, Consumption, and Investment Decisions over the Life Cycle. Management Science, 57(6):1025–1041, 2011.

- Kraft et al. (2018) Holger Kraft, Claus Munk, and Sebastian Wagner. Housing Habits and Their Implications for Life-Cycle Consumption and Investment. Review of Finance, 22(5):1737–1762, 2018.

- Kronborg and Steffensen (2015) Morten Tolver Kronborg and Mogens Steffensen. Optimal consumption, investment and life insurance with surrender option guarantee. Scandinavian Actuarial Journal, 1:59–87, 2015.

- Lakner and Nygren (2006) Peter Lakner and Lan Ma Nygren. Portfolio Optimization With Downside Constraints. Mathematical Finance, 16(2):283–299, 2006.

- Malkiel (1990) Burton G. Malkiel. A Random Walk Down Wall Street. W. W. Norton & Co., New York, 1990.

- Menoncin and Regis (2017) Francesco Menoncin and Luca Regis. Longevity-linked assets and pre-retirement consumption/portfolio decisions. Insurance: Mathematics and Economics, 76:75–86, 2017.

- Merton (1969) Robert C. Merton. Lifetime Portfolio Selection under Uncertainty: The Continuous-Time Case. The Review of Economics and Statistics, 51(3):247–257, 1969.

- Merton (1971) Robert C. Merton. Optimum Consumption and Portfolio Rules in a Continuous-Time Model. Journal of Economic Theory, 3(4):373–413, 1971.

- Minderhoud et al. (2011) Ingmar Minderhoud, Roderick Molenaar, and Eduard Ponds. The Impact of Human Capital on Life-Cycle Portfolio Choice: Evidence for the Netherlands. Network for Studies on Pensions, Aging and Retirement (Netspar), 2011.

- Morin and Suarez (1983) Roger-A. Morin and A. Fernandez Suarez. Risk Aversion Revisited. The Journal of Finance, 38(4):1201–1216, 1983.

- Munk (2000) Claus Munk. Optimal consumption/investment policies with undiversifiable income risk and liquidity constraints. Journal of Economic Dynamics & Control, 24:1315–1343, 2000.

- Palsson (1996) Anne-Marie Palsson. Does the degree of relative risk aversion vary with household characteristics? Journal of Economic Psychology, 17:771–787, 1996.

- Pliska and Ye (2007) Stanley R. Pliska and Jinchun Ye. Optimal life insurance purchase and consumption/investment under uncertain lifetime. Journal of Banking & Finance, 31:1307–1319, 2007.

- Pratt (1964) John Winsor Pratt. Risk Aversion in the Small and in the Large. Econometrica, 32(1/2):122–136, 1964.

- Riley and Chow (1992) William B. Riley and K. Victor Chow. Asset Allocation and Individual Risk Aversion. Financial Analysts Journal, 48(6):32–37, 1992.

- Shafir (2013) Eldar Shafir. The Behavioral Foundations of Public Policy. Princeton University Press, Princeton, New Jersey, 2013.

- Shen and Wei (2016) Yang Shen and Jiaqin Wei. Optimal investment-consumption-insurance with random parameters. Scandinavian Actuarial Journal, 1:37–62, 2016.

- Shiller (2005) Robert J. Shiller. Life-Cycle Portfolios as Government Policy. The Economists’ Voice, 2(1), 2005. Article 14.

- Statistisches Bundesamt (2017) Statistisches Bundesamt. Statistisches Jahrbuch. Technical report, Statistisches Bundesamt (Destatis), Wiesbaden, Germany, October 2017. Kapitel 2: Bevölkerung, Familien, Lebensformen.

- Statistisches Bundesamt (2018) Statistisches Bundesamt. Laufende Wirtschaftsrechnungen: Einkommen, Einnahmen und Ausgaben privater Haushalte. Technical report, Statistisches Bundesamt (Destatis), Wiesbaden, Germany, February 2018. Wirtschaftsrechnungen, Fachserie 15 Reihe 1.

- Steffensen (2011) Mogens Steffensen. Optimal consumption and investment under time-varying relative risk aversion. Journal of Economic Dynamics & Control, 35(5):659–667, 2011.

- StepStone (2017) StepStone. Der StepStone Gehaltsreport 2017 für Absolventen, 2017. URL https://www.stepstone.de/Ueber-StepStone/knowledge/gehaltsreport-fur-absolventen-2017/.

- Tang et al. (2018) Siqi Tang, Sachi Purcal, and Jinhui Zhang. Life Insurance and Annuity Demand under Hyperbolic Discounting. Risks, 6(2), 2018. 43.

- Viceira (2001) Luis M. Viceira. Optimal Portfolio Choice for Long-Horizon Investors with Nontradable Labor Income. The Journal of Finance, 56(2):433–470, 2001.

- Wang et al. (2016) Chong Wang, Neng Wang, and Jinqiang Yang. Optimal consumption and savings with stochastic income and recursive utility. Journal of Economic Theory, 165:292–331, 2016.

- Wang et al. (2017) Chunfeng Wang, Hao Chang, and Zhenming Fang. Optimal Consumption and Portfolio Decision with Heston’s SV Model Under HARA Utility Criterion. Journal of Systems Science and Information, 5(1):21–33, 2017.

- Wang and Hanna (1997) Hui Wang and Sherman Hanna. Does Risk Tolerance Decrease With Age? Financial Counceling and Planning, 8(2):27–31, 1997.

- Wirtschaftskammer Österreich (2016) Wirtschaftskammer Österreich. WKO Statistik: Lebenserwartung, 2016. URL https://www.wko.at/service/zahlen-daten-fakten/bevoelkerungsdaten.html.

- Yaari (1965) Menahem E. Yaari. Uncertain Lifetime, Life Insurance, and the Theory of the Consumer. The Review of Economic Studies, 32(2):137–150, 1965.

- Yang et al. (2014) Honglin Yang, Penglan Fang, Hong Wan, and Yong Zha. Inter-Temporal Optimal Asset Allocation and Time-Varying Risk Aversion. Applied Mathematics & Information Sciences, 8(6):2729–2737, 2014.

- Yao et al. (2011) R. Yao, D. L. Sharpe, and F. Wang. Decomposing the Age Effect on Risk Tolerance. Journal of Socio-Economics, 40(6):879–887, 2011.

- Ye (2008) Jinchun Ye. Optimal Life Insurance, Consumption and Portfolio: A Dynamic Programming Approach. 2008 American Control Conference, pages 356–362, 2008.

- Zieling et al. (2014) Daniel Zieling, Antje Mahayni, and Sven Balder. Performance evaluation of optimized portfolio insurance strategies. Journal of Banking & Finance, 43:212–225, 2014.

- Zou and Cadenillas (2014) Bin Zou and Abel Cadenillas. Explicit solutions of optimal consumption, investment and insurance problems with regime switching. Insurance: Mathematics and Economics, 58:159–167, 2014.

Appendix A Proofs

A.1 The consumption problem

Proof 1 (Proof of Theorem 2)

The Lagrangian of the Problem (11) subject to (12) is

By the structure of the utility function, the optimal fulfills and thus the first order conditions involve existence of a Lagrange multiplier such that the optimal maximizes and such that complementary slackness holds true. Hence it can be shown that the Karush-Kuhn-Tucker conditions besides the first derivative condition are satisfied.

Following Aase (2017), let denote the directional derivative of in the feasible direction . The directional derivative of a function in the direction is generally defined by

If is differentiable at this results in

In our case, for the inner function it holds

By the dominated convergence theorem, which allows interchanging expectation and differentiation, the first order condition gives

for all feasible . In order to fulfill this condition for any , the optimal consumption rate process must be

| (25) |

Since strictly increases in , the budget constraint (12) for the optimal solution in (11) turns to equality, i.e.

When plugging in (25) and by Fubini, the budget condition turns into

Here we used that is a log-normal random variable and so is . For any , the above equality determines uniquely, since the integral in which appears strictly decreases in and has the limits and as approaches and . It follows immediately that the condition in (13) is inevitable. The optimal wealth process which arises by applying is

can be written as where is independent of and is -measurable. Therefore it follows

for any , where we used that and thus are log-normally distributed. Define the function by

then the optimal wealth process is given by

| (26) |

with defined in (13). The dynamics can be calculated as

Notice that by Itô’s formula,

Moreover, it holds

With this we obtain

Define

In summary, the dynamics of the optimal wealth process is then given by

| (27) |

with drift

By (25) it follows

Hence

In order to determine the optimal investment strategy to Problem (11) we compare the optimal wealth dynamics in (4) and (27):

Matching the diffusion terms yields the equality

which simultaneously matches the drift terms. By the first mean value theorem for integrals111For two integrable functions and on the interval , where is continuous and does not change sign on , there exists such that it furthermore follows that there exists such that

This determines the optimal investment strategy to be

| (28) |

A.2 The terminal wealth problem

Proof 3 (Proof of Theorem 5)

The Lagrangian of the Problem (16) subject to (17) is

First of all, it is clear that . By the structure of the utility function, the optimal fulfills and thus the first order conditions involve existence of a Lagrange multiplier such that the optimal maximizes and such that complementary slackness holds true. Hence it can be shown that the Karush-Kuhn-Tucker conditions besides the first derivative condition are satisfied. By the dominated convergence theorem, the first order condition with respect to the directional derivative gives

which has to be satisfied for all suitable ; hence the optimal terminal wealth has to fulfill

| (30) |

Since strictly increases in , complementary slackness implies equality for the budget constraint

Using (30) and Fubini this gives

Solving for yields

| (31) |

where in (18) is required. Plugging this back into (30), the optimal terminal wealth is

| (32) |

The optimal wealth process replicates and is uniquely given by

This finally gives

| (33) |

with defined in (18). Recall that

It follows by Itô

Then the optimal wealth dynamics can be calculated as

Comparing the diffusion term with the one from (4) for implies

| (34) |

which automatically matches the drifts iff .

A.3 Optimal merging of the individual solutions

Proof 5 (Proof of Theorem 8)

-

1.

:

-

2.

:

Let denote the optimal controls which maximize with optimal wealth process to the initial wealth . Define

Then, and

Hence

Proof 6 (Proof of Lemma 9)

In accordance with Theorem 8 and by expressing , the candidate for the optimal is the one that satisfies the first order derivative condition on the budget

such that , with ; thus . Theorems 4 and 7 tell that and are strictly concave functions in respectively . Therefore, it follows

This implies that the candidates and are the solution when the constraint applies.

Proof 7 (Proof of Lemma 10)

In accordance with Theorems 4 and 7 we have

By equating and we obtain

Inserting in Equation (14), the optimal is the solution to

where the continuous function is defined by

It remains to verify and uniqueness of . For this sake, define the function by

is the root of the function , i.e. , if it holds . is continuous in , the exponent within the first integral is positive. Furthermore, due to claimed in (9) and , we have for the limits

Note, for general and . Additionally, is strictly monotone increasing in since

We conclude that there exists a unique root such that . Therefore, we conclude that the optimal and exist and are unique. is the solution to Equation (20). The optimal Lagrange multiplier is then given by

Proof 8 (Proof of Theorem 11)

Starting with we compare the dynamics of both sides of the equation:

| (35) |

Equation (4) for , and , with for , provides

Comparing the diffusion terms in (35) gives

Inserting this back and comparing the drift terms finally leads to

Notice that the pair is admissible, i.e. because and which implies

Using the solutions in Theorems 2 and 5 we derive the following for the utility setup in (8):

for all , with

Furthermore, solves (15):

Proof 9 (Proof of Remark 12)

The formula for the optimal investment strategy is straightforward from Theorem 11 as and for any . The optimal can be determined by Lemma 10 as the solution to Equation (20):

where

Therefore,

is the optimal budget to the consumption problem, is the optimal budget to the terminal wealth problem. Furthermore, by Lemma 10 one knows

This enables us to calculate to be

with defined in (10), and thus using Theorem 11:

With, again from Theorem 11,

because , it follows

Finally, the optimal consumption rate process can then be determined from Theorem 11 as

By defining

we obtain

With the definition of , the optimal wealth process finally can be written as