Abstract.

This paper extends the core results of discrete time infinite horizon dynamic programming to the case of state-dependent discounting. We obtain a condition on the discount factor process under which all of the standard optimality results can be recovered. We also show that the condition cannot be significantly weakened. Our framework is general enough to handle complications such as recursive preferences and unbounded rewards. Economic and financial applications are discussed.

Keywords: Dynamic programming; optimality; state-dependent discounting

JEL Classification: C61, C62

Dynamic Programming with State-Dependent Discounting111We

thank Damien Eldridge, Simon Grant, Timo Henckel, Fedor Iskhakov,

Ruitian Lang, Andrzej Nowak, Ronald Stauber, the editor and two referees

for many helpful comments

and suggestions. The first author gratefully acknowledges financial

support from ARC grant FT160100423. The second author is supported by an

Australian Government Research Training Program (RTP) Scholarship.

Email: john.stachurski@anu.edu.au,

junnan.zhang@anu.edu.au

John Stachurskia and Junnan Zhangb

a, b Research School of Economics, Australian National University

1. Introduction

Researchers in economics and finance routinely adopt settings where the subjective discount rate used by agents in their models varies with the state. For example, Albuquerque et al. (2016) study an asset pricing model in which the discount rate is perturbed by an AR(1) process. They show that the resulting demand shocks help explain the equity premium puzzle. Mehra and Sah (2002) find that small fluctuations in agents’ discount factors can have large effects on equity price volatility. Schorfheide et al. (2018) and Gomez-Cram and Yaron (2020) likewise embed state-dependent discount factors into Epstein–Zin preferences to generate realistic asset prices and returns.

State-dependent and time-varying discount rates are also common in studies of savings, income and wealth. An early example is Krusell and Smith (1998). In related work, Krusell et al. (2009) model the discount process as a three state Markov chain and show how discount factor dispersion helps their heterogeneous agent model match the wealth distribution. Fagereng et al. (2019) use time-varying discount rates and portfolio adjustment frictions to explain the positive correlation between savings rates and wealth observed in Norwegian panel data. Hubmer, Krusell, and Smith (2020) model discount dynamics using a discretized AR(1) process.

State-dependent discounting is also found in analysis of fiscal and monetary policy. For example, Eggertsson and Woodford (2003) study monetary policy in the presence of zero lower bound restrictions with dynamic time preference shocks. Woodford (2011) considers the government expenditure multiplier in a similar environment. Eggertsson (2011) and Christiano, Eichenbaum, and Rebelo (2011) study the effect of fiscal policies at the zero lower bound on interest rates, while Nakata and Tanaka (2020) analyze the term structure of interest rates at the zero lower bound when agents have recursive preferences. In all of these models, state-dependent variation in discount rates plays a significant role.222See also Correia et al. (2013), Hills and Nakata (2018), Hills et al. (2019) and Williamson (2019).

In addition, state-dependent discounting is often used in studies of macroeconomic volatility. For example, Primiceri et al. (2006) argue that shocks to agents’ rates of intertemporal substitution are a key source of macroeconomic fluctuations. Justiniano and Primiceri (2008) study the shifts in the volatility of macroeconomic variables in the US and find that a large portion of consumption volatility can be attributable to the variance in discount factors. Additional research in a similar vein can be found in Justiniano et al. (2010), Justiniano et al. (2011), Christiano et al. (2014), Saijo (2017), and Bhandari et al. (2013).

The standard theory of dynamic programming over infinite horizons (see, e.g., Blackwell (1965), Stokey et al. (1989), or Bertsekas (2017)) does not accommodate state-dependent discounting. Instead, it assumes either zero discounting (and considers long-run average optimality) or a constant and positive discount rate, which corresponds to a discount factor strictly less than one. This implies that, in the canonical setting, the Bellman operator satisfies the conditions of Banach’s contraction mapping theorem, which in turn provides the foundations for the standard optimality theory.

We reconsider the standard theory when the constant discount factor is replaced by a discount process , so that time payoff is discounted to present value as rather than . Here is the initial condition of an exogenous Markov state process that drives evolution of the discount factor. We replace the traditional condition with a weaker “eventual discounting” condition: existence of a such that . For a finite irreducible state process, this is equivalent to existence of a such that , where is the unconditional expectation.

We show that, when eventual discounting holds, (i) the value function satisfies the Bellman equation, (ii) an optimal policy exists, (iii) Bellman’s principle of optimality holds, and (iv) value function iteration and Howard policy iteration (Howard, 1960) are both convergent. When is constant at , eventual discounting holds at , so these results capture the standard theory as a special case.

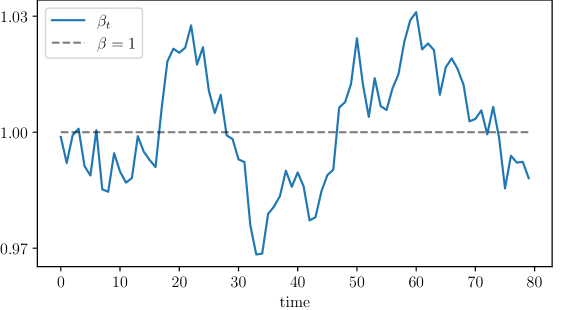

Our conditions do not rule out with positive probability. One example of why this matters is provided by the New Keynesian literature, where the discount factor is often allowed to temporarily attain or exceed unity, so that the zero lower bound on the nominal interest rates binds. For example, Christiano et al. (2011) admit a shock where in their study of the government spending multiplier. Similarly, Hills et al. (2019) analyze tail risk associated with the effective lower bound on the policy rate in a model where the discount process is a constant multiple of a discretized AR(1) process that regularly generates value of exceeding unity. Figure 1 illustrates by showing a simulated time path of using their parameters.333The specification is based around an AR(1) process and detailed in Example 4.3 below. Other studies using an AR(1) specification for the discount process or its logarithm include Nakata (2016), Hubmer et al. (2020), Albuquerque et al. (2016) and Schorfheide et al. (2018).

We discuss the eventual discounting condition at length in the paper, giving several equivalent conditions. One of these involves a bound on the spectral radius of a discounting operator. This connects our work to a strand of literature in finance that study the long-term factorization of stochastic discount factors using eigenfunctions of valuation operators (see, e.g., Hansen and Scheinkman (2009), Hansen and Scheinkman (2012), and Qin and Linetsky (2017)). Drawing on these ideas, Borovička and Stachurski (2020) and Christensen (2020) connect the spectral radius of valuation operators with existence and uniqueness of recursively defined utilities. However, neither of these papers provides results on optimality or dynamic programming.

To handle unbounded rewards, we extend two approaches that have been developed previously for the case of constant discounting. The first one treats homogeneous programs in the spirit of Alvarez and Stokey (1998) and Stokey et al. (1989, Section 9.3). The second uses a local contraction method pioneered in Rincón-Zapatero and Rodríguez-Palmero (2003) and further developed by Martins-da Rocha and Vailakis (2010) and Matkowski and Nowak (2011). In each case, we show how the eventual discounting condition can be adapted to handle these extensions.

In addition, we study dynamic programming with Epstein-Zin utilities, where rewards are unbounded above and the Bellman operator is not a contraction in the short or long run under standard metrics. To solve the problem we extend earlier work by Marinacci and Montrucchio (2010), Bloise and Vailakis (2018), and Becker and Rincón-Zapatero (2018), which exploits the monotonicity and concavity of the aggregator, to allow for state-dependent discounting. We show that, in the case of Epstein–Zin utility, the eventual discounting condition must be adapted to compensate for the role played by intertemporal elasticity of substitution.

Other papers have analyzed dynamic programming problems where discount rates can vary. For example, Karni and Zilcha (2000) study the saving behavior of agents with random discount factors in a steady-state competitive equilibrium. Cao (2020) proves the existence of sequential and recursive competitive equilibria in incomplete markets with aggregate shocks in which agents also have state-dependent discount factors. In the mathematical literature, various issues in dynamic programming with state-dependent discounting have been studied; see, for example, Jasso-Fuentes et al. (2020) and the references therein.444Jasso-Fuentes et al. (2020) also allow the discount process to be endogenous, a case not covered in our framework. In economic applications, this often comes in the form of Uzawa type preferences (Uzawa, 1968) that are common in open economy models where discount factors are dependent on consumption. See Uribe and Schmitt-Grohé (2017) for a review. However, these models can be treated using traditional dynamic programming techniques, since the discount factors are assumed to be strictly less than one in the literature. However, these papers assume that the discount process in the dynamic program is bounded above by one or by some constant less than one.555Schäl (1975) admits state-dependent discounting in discrete time under weaker conditions, but he directly assumes that expected discounted rewards are finite under any Markov policy. This restricts all primitives in the dynamic program simultaneously and makes the condition impractical for applications. This is too strict for many applications, as discussed above.

Our work is related to Toda (2019), who investigates an income fluctuation problem in which the agent has CRRA utility. He obtains a necessary and sufficient condition for the existence of a solution to the optimal saving problem with state-dependent discount factors. Ma et al. (2020) relax the CRRA restriction by constructing optimality results via a consumption policy operator. Their results are specialized to optimal savings with additively separable rewards and do not apply to problems that involve discrete choices, endogenous labor supply, durable goods, or other common features. In contrast, the theory below is developed in a general dynamic programming setting, where the state spaces are arbitrary metric spaces.

In addition, the consumption policy operator, around which the theory in Toda (2019) and Ma et al. (2020) is constructed, is defined from the Euler equation, which characterizes the solution in their setting. However, many recent applications of state dependent discounting use recursive preferences (see, e.g., Albuquerque et al. (2016), Basu and Bundick (2017), Schorfheide et al. (2018), Nakata and Tanaka (2020), or de Groot et al. (2020)), implying that the Euler equation contains the value function and the consumption policy operator methods break down. Our theory extends to recursive preferences and illuminates the role of elasticity of intertemporal substitution on eventual discounting.

2. A Dynamic Program

In what follows, for any metric space , the symbols , and denote the (Borel) measurable, bounded measurable and bounded continuous functions from to respectively. Unless otherwise stated, the last two spaces are endowed with the supremum norm and this norm is represented by . In expressions with products below, we adopt the convention that whenever .

2.1. Framework

The state of the world consists of a pair , where and represent endogenous and exogenous variables. These variables take values in separable metric spaces and respectively. The agent responds to by choosing future state from , where is the feasible correspondence. Let be the graph of , defined by

| (1) |

Similar to Bertsekas (2013), we combine the remaining elements of the dynamic programming problem into a single continuation aggregator , with the understanding that is the maximal value that can be obtained from the present time under the continuation value function , given current state and next period state . The aggregator maps each in into and is assumed to satisfy, for all and all ,

| (2) |

This basic monotonicity condition is satisfied in all applications of interest. Bellman’s equation takes the form

| (3) |

For fixed and , a dynamic program consists of a feasible correspondence and a continuation aggregator .

2.2. Feasibility and Optimality

Let be a dynamic program and let be the set of feasible policies, defined as all Borel measurable maps from to such that for each in . Given such , let be the policy operator on given by

| (4) |

Define the Bellman operator on by

| (5) |

Given in and in , we can interpret as the lifetime payoff of an agent who starts at state , follows policy for periods and uses to evaluate the terminal state. The -value function for an infinite-horizon problem is defined here as

| (6) |

The definition requires that this limit exists and is independent of . Below we impose conditions such that this is always the case.

We define the value function corresponding to our dynamic program by

| (7) |

at each in . A policy is called optimal if it attains the supremum in (7) at each in . We say that Bellman’s principle of optimality holds when

2.3. Assumptions

A dynamic program will be called regular if

-

(a)

is continuous, nonempty, and compact valued and

-

(b)

the function is bounded and measurable on for all , and also continuous when .

Most standard cases from the literature are regular, including all dynamic programs with a finite state space.666The continuity and compactness conditions are automatically satisfied when and are finite and endowed with the discrete topology. Further discussion of regularity is provided in Section 3.

Let for some and Markov process on with transition kernel .777That is, for all and in the Borel subsets of . Let represent expectation given . We call eventually discounting if for some , where

Example 2.1.

If there exists a constant such that for all , then . Eventual discounting holds if and only if .

Example 2.2.

If is iid, then where . Hence eventual discounting holds if and only if . In particular, higher moments have no influence on eventual discounting unless there is persistence.

Section 4 provides an extended discussion of eventual discounting for more sophisticated state processes.

Assumption 2.1 (Eventual Contractivity).

There is a nonnegative function in and a Feller transition kernel on such that is eventually discounting and

| (8) |

for all and .888Here we implicitly assume that the discount factor is known to the agent at the beginning of each period. Our results hold for alternative timing with slight modifications to (8). See Section 6.1.

The Feller property means that either is discrete or the law of motion is continuous.999More precisely, we assume that, for any , the function is continuous. This holds automatically when is countable (under the discrete topology). It also holds if is generated by a continuous law of motion, in the sense that for some continuous function and iid sequence . These two cases cover all the applications we consider. Further discussion can be found in Lemma 12.14 of Stokey et al. (1989).

2.4. Optimality Results

In the statement of the next theorem, a map from a metric space into itself is called eventually contracting if there exists an in such that the -th iterate is a contraction mapping.101010More precisely, a self-map on metric space is called eventually contracting if there exists an in and a such that for all in .

Theorem 2.1.

Let be a dynamic program. If is regular and Assumption 2.1 holds, then the following statements are true:

-

(a)

is eventually contracting on and is eventually contracting on .

-

(b)

For each feasible policy , the lifetime value is a well defined element of .

-

(c)

The value function is finite, continuous, and the only fixed point of in .

-

(d)

At least one optimal policy exists.

-

(e)

Bellman’s principle of optimality holds.

In addition, value function and Howard policy iteration converge:

-

(f)

for all and

-

(g)

when and for all .

This theorem extends the core results of dynamic programming theory to the case of state-dependent discounting. In particular, the value function satisfies the Bellman equation, an optimal policy exists, and Bellman’s principle of optimality is valid. Value iteration and policy iteration both lead to the value function, so that we have both existence of an optimal policy and means to compute it. The proof of Theorem 2.1 can be found in the appendix.

Relative to the results that can be obtained under standard contraction conditions (see, e.g., Bertsekas (2013)), the only significant weakening of the main findings is that and are eventually contracting, rather than always contracting in one step. Such an outcome cannot be avoided when values of the discount factor greater than one are admitted.

The eventual discounting condition is, in many cases, not just sufficient but also necessary for the dynamic program to be well defined and the optimality results to hold. Appendix A.6 provides additional discussion.

2.5. Blackwell’s Condition

Blackwell’s sufficient condition for a contraction has a natural analogue in the case of state-dependent discounting. As shown in Proposition A.4, if the Bellman operator satisfies

for all where is eventually discounting, then is eventually contracting on . As a consequence, has a unique fixed point in that is globally attracting under iteration of . This extends Blackwell’s original result,111111The original result states that if an operator is monotone and there exists a such that for all , then is a contraction (see, e.g., Stokey et al., 1989, Theorem 3.3). with the caveat that might not itself be a contraction. Again, this cannot be avoided when is allowed to take values greater than one.121212In fact, when is an eventual contraction on a Banach space, one can construct a complete metric on the same space under which is a contraction. See, for example, Krasnosel’skii et al. (1972). Our terminology on contractions in this section refers specifically to the supremum norm.

2.6. Monotonicity, Concavity and Differentiability

Next we show that standard results on monotonicity, concavity, and differentiability of the value function (cf, e.g., Stokey et al. (1989)) are preserved under state-dependent discounting without additional assumptions on the discount factor process. We assume that is a convex subset of in the discussion below and denote the set of functions in that are increasing and concave in .

Assumption 2.2.

For all and , (i) is increasing for all , (ii) is strictly concave, (iii) for all , and (iv) the set is convex.

Assumption 2.3.

The map is continuously differentiable on for all , , and .

The following theorem shows that the value function is increasing, strictly concave, and continuously differentiable in under standard assumptions.131313If is additively separable, sufficiency of the Euler equations and transversality conditions can also be established, analogous to Section 9.5 of Stokey et al. (1989).

Theorem 2.2.

Additional comments on these assumptions and results can be found in the applications.

3. Additively Separable Problems

In this section we study state-dependent discounting in settings where preferences are additively separable and rewards are bounded. (Extensions to unbounded rewards and recursive preferences are deferred to Sections 5 and 6.)

3.1. An Additively Separable Problem

Consider the dynamic program in Section 9.2 of Stokey et al. (1989) with the addition of state-dependent discounting. The objective is to maximize

| (9) |

As in Stokey et al. (1989), is assumed to be bounded and continuous on , while is a continuous, nonempty, and compact-valued. We set where is continuous, bounded and nonnegative, while is Markov with Feller kernel .

We connect this dynamic program to our framework by setting with

| (10) |

for all . The monotonicity condition (2) is clearly satisfied. The function is bounded and Borel measurable on because and have these properties, and continuous when is continuous by the Feller property (see footnote 9). Hence is regular.

If is eventually discounting then Assumption 2.1 holds, since (10) yields

and an application of the triangle inequality gives (8).

To connect this application with the definition of optimality given in Section 2.2, fix and . The policy operator from (4) can be expressed as

| (11) |

where is generated by , the initial condition is , and conditions on . If we take , iterate forward times and apply the law of iterated expectations, we obtain

| (12) |

Recall from (6) that, to obtain the value of the policy , we take the limit of (12) in . Eventual discounting implies that the second term vanishes as .141414This term is dominated by . Hence it suffices to prove that as . Eventual discounting implies that for some , and, as shown in Proposition 4.1 below, this in turn gives . But then , as was to be shown. In the limit we obtain as the value in (9) under the policy . Maximizing over in yields the optimal policy.

The Bellman operator corresponding to is the map on defined by

| (13) |

Since the conditions of Theorem 2.1 are satisfied, the unique fixed point of in is , the value function of . Bellman’s principle of optimality applies and an optimal policy can be computed by either value function iteration or Howard’s policy iteration algorithm. Monotonicity, concavity and differentiability of can be obtained by imposing the same conditions that Stokey et al. (1989) impose on and and then applying Theorem 2.2.

3.2. Application to a Savings Problem

The dynamic program associated with the household problem in Hubmer et al. (2020) can be placed with the framework provided in the previous section. The continuation aggregator takes the form

| (14) |

where is current assets, is a vector of exogenous shocks taking values in , is the gross rate of return on asset holdings (which depends on both exogenous shocks and current asset holdings) and is labor income net of income tax and capital gains tax, as well as a lump sum transfer. The utility function is

| (15) |

Next period assets are constrained to lie in

| (16) |

This problem is not regular because is not bounded, since is unbounded below. However, in solving this dynamic program, Hubmer et al. (2020) reduce both the asset space and the exogenous shock space to a finite grid. The aggregator is then bounded and the continuity parts of the regularity condition are automatically satisfied (under the discrete topology). Hence, to show that all of the conclusions of Theorem 2.1 apply, we need only verify that eventual discounting holds. This issue is discussed for the parameterization in Hubmer et al. (2020) in Section 4 below.

4. The Discount Condition

In this section we discuss tests for the eventual discounting condition and develop intuition regarding its value.

4.1. Connection to Spectral Radii

Given and as in Assumption 2.1, let be the discount operator defined by

| (17) |

The next proposition shows that we can test Assumption 2.1 by computing the spectral radius of the operator .151515As usual, the spectral radius of a bounded linear operator from a Banach space to itself is given by , where is the operator norm. This limit always exists and is equal to . If is finite dimensional, it equals the maximal modulus of the eigenvalues of . See, for example, Bühler and Salamon (2018), Theorem 1.5.5. In stating it, we set where is a -valued Markov process generated by .

Proposition 4.1.

The spectral radius of satisfies . Moreover, is eventually discounting if and only if .

The expression for in Proposition 4.1 is obtained through a local spectral radius condition for positive linear operators. It provides both a simple representation of the spectral radius of and a link to eventual discounting. For example, it is immediate from that when . This, in turn, implies that is eventually discounting. The converse implication is more subtle and involves the Markov property. Details are in the appendix.

4.2. Finite Exogenous State

Testing eventual discounting is simple when is finite. In this case, can be represented as a Markov matrix of values , giving the one-step probability of transitioning from to , and can be represented as the matrix

| (18) |

Here and is the number of elements in . The spectral radius is equal to the dominant eigenvalue of , which is real and nonnegative by the Perron–Frobenius Theorem. In view of Proposition 4.1, eventual discounting holds if and only if this eigenvalue is strictly less than unity.

Example 4.1.

Christiano et al. (2011) consider the case with . The process stays at with probability and shifts permanently to with probability . Thus, by (18),

The eigenvalues are and , so is the maximum of these values. Since , eventual discounting holds if and only if . The condition is violated if the state is too large or too persistent. Christiano et al. (2011) set and consider , so eventual discounting is satisfied.

4.3. Stationary Spectral Radius

The expression obtained for in Proposition 4.1 is a geometric mean, and hence is determined by the asymptotic behavior of the discount process. When is irreducible, it seems likely that these asymptotics will be independent of the initial condition . This suggests that the conditional expectation and supremum in the definition of can be replaced by the unconditional expectation for the stationary process. The next proposition confirms this intuition.

Proposition 4.2.

If is finite and the exogenous state process is irreducible, then satisfies the stationary representation

| (19) |

Our analysis below shows that this stationary representation is also highly accurate even when is infinite, provided that is irreducible and sufficiently mean reverting for dependence on initial conditions to die out. This is helpful because the stationary representation of sometimes admits analytical solutions that facilitate benchmark calculations and enhance intuition.161616While finiteness of the state space can be weakened, as discussed above, irreducibility is essential. To see this, consider the application in Christiano et al. (2011), where the unique stationary distribution puts all mass on the low state and irreducibility fails. With all mass on the low state we have for all , and hence , which differs from .

4.4. Autoregressive Specifications

Some studies adopt discount processes that are autoregressive in levels or logs (e.g., Hubmer et al., 2020; Hills et al., 2019; Nakata, 2016) and then discretize them prior to computation. Such specifications always fit the dynamic programming framework adopted above after discretization.171717Recall that is assumed to be bounded and continuous in Assumption 2.1. Both conditions hold after discretization. (Continuity holds automatically under the discrete topology.) The only remaining issue is whether or not eventual discounting holds. For common reference, all examples use the state process

| (20) |

4.4.1. AR(1) in Levels

We first give examples where is a multiple of . After following the discretization procedure used by the authors, we calculate the spectral radius of the matrix (18).

Example 4.2.

Hubmer et al. (2020) take the AR(1) specification where follows (20) with , and and discretize the process onto a grid of 15 states via Tauchen’s method. This gives , so eventual discounting holds. This is as expected, since the mean is substantially less than one and low volatility suggests that the impact of stochastic variation is minor.

Example 4.3.

In Hills et al. (2019), the discount process is where obeys (20). They consider several parameterizations, the most empirically motivated of which is , , and . Under this parameterization regularly exceeds one, as observed in the simulated process shown in Figure 1. Nonetheless, after following their discretization procedure and computing the spectral radius of , we find , so eventual discounting holds.

Example 4.4.

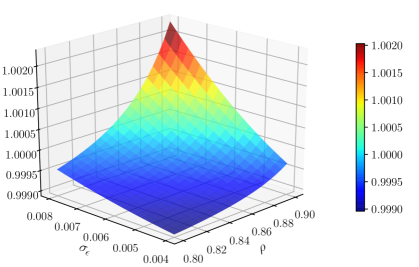

To illustrate how the stochastic properties of affect the size of , we take the parameterization in Example 4.3 as a benchmark and vary the persistence term and the volatility . Other parameters are held constant. Figure 2 plots the resulting values of . The figure shows that higher volatility and higher persistence both increase , leading to a failure of eventual discounting when . Note also that there is a positive interaction between persistence and volatility, with the effect of each parameter enhanced by the other.

Some further insight can be gained by considering the expected two period discount factor when and is as given in (20). Under the stationary distribution, which governs asymptotic outcomes, this evaluates to

| (21) |

The value in (21) depends on the sign of . Positive correlation combined with positive volatility in the state process leads to a value greater than the stationary mean. This is because, under positive correlation, positive deviations from the mean tend to occur consecutively and reinforce each other.

4.4.2. AR(1) in Logs

Next we set where obeys the AR(1) specification (20). This specification is arguably more natural than the direct AR(1) approach discussed above due to positivity. While the state space is not finite, irreducibility of leads us to conjecture that an approximate version of Proposition 4.2 holds, so that the stationary geometric mean for the original process will be close to when the latter is calculated using an appropriately discretized version of the process. As shown in Appendix A.5, for the original process we have

| (22) |

Numerical experiments show that the expression on the right hand side of (22) provides a good approximation of even when the discretization is relatively coarse, and an almost perfect approximation when the discretization is fine. Table 1 illustrates by comparing given by (22) and under two different levels of discretization, for a range of parameter values.181818 is the number of grid points. We use the Rouwenhorst’s method for discretization, which has strong asymptotic properties in terms of approximating the distributions of Gaussian AR(1) processes (Kopecky and Suen, 2010). We fix because it has no effect on the errors.

| Parameters | N=10 | N=200 | |||

|---|---|---|---|---|---|

| Error | Error | ||||

| 0.956 | 0.956 | 2.5e-05 | 0.956 | 1.1e-06 | |

| 0.970 | 0.970 | 3.9e-04 | 0.970 | 1.8e-05 | |

| 0.959 | 0.959 | 7.6e-05 | 0.959 | 3.5e-06 | |

| 0.981 | 0.980 | 1.2e-03 | 0.981 | 5.8e-05 | |

| 0.965 | 0.964 | 3.2e-04 | 0.965 | 1.5e-05 | |

| 1.006 | 1.001 | 4.7e-03 | 1.005 | 2.5e-04 | |

Given this tight relationship between and , we can use (22) to examine how the parameters of the state process affect eventual discounting. Consistent with our previous findings, the expression in (22) indicates that is increasing in all of the three parameters (although the effect is now exponential). Higher persistence and higher volatility reinforce each other. The impact of is nonlinear and large in the neighborhood of unity.

5. Unbounded Rewards

In this section we show that the optimality results presented above extend to a range of unbounded reward settings after suitable modifications. We consider the additively separable aggregator

| (23) |

The continuation value function is in , which is the set of all candidate value functions and varies across applications. As before, and is a Feller transition kernel. The feasible correspondence is assumed to be continuous, nonempty, and compact valued. The reward function is continuous but not necessarily bounded. The Euclidean norm is represented by .

5.1. Homogeneous Functions

We begin by extending the core results of Alvarez and Stokey (1998) to the case of state-dependent discounting. We consider reward functions that are homogeneous of degree and feasible correspondences that are homogeneous of degree one.191919Recall that a real-valued defined on a convex cone of is homogeneous of degree if for all and .

Assumption 5.1.

is a convex cone in and when and . For each , is homogeneous of degree , and there exists a such that

Assumption 5.1 follows Alvarez and Stokey (1998). The next assumption generalizes their growth restriction to problems with state-dependent discounting.

Assumption 5.2.

There exists an in such that when . In addition, for generated by ,

| (24) |

The function is a state-dependent upper bound on the growth rate of the state variable. Comparing to the eventual discounting condition in Section 2.3, the extra term in (24) reflects the need to take into account the growth restriction when the reward function is homogeneous and unbounded above. If both and are constant, then (24) reduces to the condition used in Alvarez and Stokey (1998).

In household problems where the state is asset holdings, the gross asset return bounds the growth rate of the state. The condition in (24) implies that the shocks to the discount factor and asset return have a similar effect on eventual discounting, but their relative importance depends on the degree of homogeneity of the reward function.

Let be the space of continuous functions on that are homogeneous of degree in and bounded in the norm defined by

| (25) |

Then is a Banach space (Stokey et al., 1989). To make the problem well defined, we let so the -value function is given by .

Proposition 5.1.

Example 5.1.

Consider the household saving problem in Toda (2019) where the exogenous state is Markovian on with stochastic kernel . The asset return and discount function are bounded continuous functions of . The utility function is with . The budget constraint is where is the beginning-of-period wealth and is consumption. The Bellman equation is

If we use the constraint to eliminate in the Bellman equation and let , then Assumption 5.1 is satisfied with and . By Proposition 4.1, Assumption 5.2 holds if with defined by

where we let the upper bound function . This is a direct extension of the results in Toda (2019) to the case of infinite . In particular, the condition reduces to the condition in Proposition 1 of Toda (2019) whenever is finite.

5.2. Local Contractions

Next we adopt a local contraction approach to dynamic programs with state dependent discounting and unbounded rewards, extending methods first developed in Rincón-Zapatero and Rodríguez-Palmero (2003). As in the previous section, the aggregator has the form of (23).

Let be all continuous functions on . Let be compact and write where is a sequence of strictly increasing and compact subsets of . Let

Let and be an unbounded sequence of increasing positive real numbers. Let be all such that

The pair forms a Banach space (Matkowski and Nowak, 2011).

Assumption 5.3.

for all , all , and all , and is eventually discounting in the sense of Section 2.3.

Proposition 5.2.

Under Assumption 5.3, the lifetime value is well defined and finite on for any , there exists a sequence such that the value function is the unique fixed point of on , for all , there exists an optimal policy, and the principle of optimality holds.

Example 5.2.

Consider a stochastic optimal growth model with state dependent discounting, total production and continuous utility . The feasible correspondence is . Let and let be compact. Suppose , and . Let be an increasing sequence of compact sets covering such that for all .202020For example, set for all , where is some large constant. Assumption 5.3 holds and Proposition 5.2 can be applied if is eventual discounting.

6. Further Extensions

We study two further extensions. Section 6.1 studies an alternative discount specification to the framework in Section 2. Section 6.2 extends our main results to Epstein-Zin preferences with unbounded rewards.

6.1. Alternative Discount Specifications

Discounting methods that differ from the preceding framework can also be analyzed. To illustrate, we consider the shocks to long-run discount factors found in Primiceri et al. (2006), Justiniano et al. (2010), Leeper et al. (2010), and Christiano et al. (2014). Their maximization problems are analogous to the additively separable problem in Section 3.1, with the difference that is replaced by for some constant . While the discount factor can be expressed as after setting and , notice that is not observable until . Hence inequality (8) cannot be used, since it assumes that is visible at .

To handle such cases, one option is to replace inequality (8) with

| (26) |

Inequality (26) integrates over , supposing that its realization is not observed at the time that is chosen. We prove in the appendix that Theorem 2.1 extends to this case: the theorem is valid under eventual discounting when (26) replaces (8).

The set up of Primiceri et al. (2006) and other authors mentioned above satisfies (26) after redefining the aggregator and the exogenous state variable.212121To be specific, let the exogenous state variable be . The aggregator then becomes , where , , and is the transition kernel on induced by . The only question, then, is whether or not eventual discounting holds. The following proposition shows that, in many cases, the answer depends only on the value of in . Stochastic components are irrelevant.

Proposition 6.1.

If for all and is positive and bounded, then eventual discounting holds if and only if .

The intuition behind Proposition 6.1 is that the spectral radius equals the asymptotic growth rate of the discount factor process. If and is positive and bounded, the asymptotic growth rate is equal to .

6.2. Epstein-Zin Preferences

Next we extend the preceding results on dynamic programming under state-dependent discounting to settings where lifetime utility is governed by Epstein–Zin preferences. Lifetime utility of an agent satisfies

| (27) |

where is the relative risk aversion and is the elasticity of intertemporal substitution. The agent maximizes lifetime utility by choosing consumption subject to . Here is asset holding of the agent at the beginning of time and is returns. We focus on the empirically relevant case of and , as in, say, Bansal and Yaron (2004), Albuquerque et al. (2016), or Schorfheide et al. (2018). This is the most challenging setting because the usual contraction argument fails and the utility function is unbounded above.

6.2.1. Discounting Continuation Values

Let , assume that and are functions of the exogenous state, and define the aggregator by

| (28) |

where , , and are asset holding, exogenous state, and consumption, respectively, satisfying .

Assumption 6.1.

The functions and are nonnegative elements of . In addition, for generated by , we have

| (29) |

Assumption 6.1 is an eventual discounting condition for the Epstein–Zin case. It is modified to take into account both the underlying growth rate, as in Assumption 5.2, and also the role of elasticity of intertemporal substitution. (Intuition and numerical applications are provided below.)

Let be all such that is finite. We show in Appendix A.4.2 that there exists an upper bound function such that is a self map on the order interval with the pointwise partial order. Then we show that is well defined on the order interval and is a fixed point of . In addition, if satisfies an interiority condition, the fixed point is unique. See Proposition A.6.

Let be the space of functions in that are homogeneous of degree one in . Our main result for this section is as follows.

Proposition 6.2.

If Assumption 6.1 holds, then is a well defined element of and equal to the value function. There exists an optimal policy that is homogeneous of degree one in and the principle of optimality holds.

Notice that Proposition 6.2 contains no analogue of the eventual contraction condition in Assumption 2.1. This is because, as mentioned above, and are not contraction mappings under conventional metrics. Instead, the proof uses monotonicity and a form of concavity inherent in Epstein–Zin preferences, combined with fixed point results due to Marinacci and Montrucchio (2010).

6.2.2. Alternative Preference Shocks

While (27) parallels the definitions in, say, Epstein and Zin (1989), Nakata and Tanaka (2020) and de Groot et al. (2020), other studies introduce preference shocks to current consumption (Albuquerque et al., 2016; Schorfheide et al., 2018). In this setting, lifetime utility satisfies

| (30) |

where is a fixed constant and is a preference shock.222222Some authors also place an additional term before . This is inconsequential to our optimality results since we can simply redefine to include . As we now show, the preceding analysis can be brought to bear on this case as well.

Using homogeneity and dividing both sides of (30) by yields

| (31) |

where . If is measurable with respect to the time- information set, then (31) becomes

| (32) |

where . This is the same as the original Koopmans equation in (27) with .232323The equivalence between and is demonstrated in de Groot et al. (2020) using the Euler equation in an expected utility setting. Optimality results from the previous section can now be applied.

6.2.3. Interpretation

Condition (29) is the key restriction required for Proposition 6.2 and elasticity of intertemporal substitution plays a role. To illustrate the implications of the condition we consider the study of Albuquerque et al. (2016), who adopt the specification in (30) with satisfying . In view of the discussion in Section 6.2.2, we can study optimality by applying the eventual discounting condition (29) to the transformed representation (32). By a result analogous to Proposition 4.1, condition (29) is equivalent to with defined by

| (33) |

One way to obtain insight on the value is to use the stationary approximation , where . The advantage of the stationary approximation is that, if we specialize to , then we obtain the analytical expression

| (34) |

(See Appendix A.5 for details.) Analogous to the findings in Section 4.4.2 (cf. Table 1), this stationary representation closely approximates for a discretized version with moderately fine grid.

The expression in (34) sheds light on the role that elasticity of intertemporal substitution plays in eventual discounting. The impact of in (34) is not monotone because the mean term is typically negative, while the volatility term is positive. Nonetheless, we can understand the impact of by the relative weight placed on the mean and volatility terms: enters (34) directly for the mean and is squared on the volatility term. Hence, as rises and falls, the relative importance of in determining increases. Conversely, as , the volatility term increasingly dominates.

Intuitively, if is large, then the agent is more willing to shift consumption across time, so the volatility in the discount factor plays a lesser role. Conversely, when is small, consumption cannot shift as freely to compensate for fluctuations in the discount factor. Hence volatility in the discount factor has a large impact on lifetime utility.

6.2.4. Numerical Analysis

In the applications discussed in Section 4.2, discount dynamics are driven by Gaussian AR(1) processes, where standard discretization methods are available and eventual discounting is easy to test. In some recent studies, however, discounting is driven by a Markov process and additional innovations, as in Albuquerque et al. (2016), or stochastic volatility, as in Basu and Bundick (2017). For such cases, one can either use a more sophisticated discretization procedure (see, e.g., Farmer and Toda (2017)) or use Monte Carlo.

To illustrate the Monte Carlo method, we return to the model in Albuquerque et al. (2016) studied above, where the eventual discounting condition is (29), or equivalently, with defined in (33). An analytical expression was obtained in (34) for the case when is constant, but in Albuquerque et al. (2016) this is not the case. Nonetheless, by the strong law of large numbers, we can approximate each by generating independent simulated paths of and calculating

| (35) |

Using the parameters in Albuquerque et al. (2016), we find that increases with and exceeds one when is large, as shown in Table 2.242424We treat the baseline model in Albuquerque et al. (2016), where and . There are three exogenous states: preference shock , log consumption growth , and log price consumption ratio . The discount factor is with , , , and . The logarithm of returns satisfies where and with and . The remaining parameters can be solved as detailed in their Internet Appendix, giving , and . We run a large number of simulations () for each experiment to ensure that is close to . The last row lists the standard error for each estimate by calculating the standard deviation of 1000 simulated with replaced by an approximating normal distribution for computational efficiency. This is in line with the analytical expression given by (34), which yields if we fix . Hence eventual discounting fails under their parameterization.252525We have not shown the eventual discounting condition to be necessary in the Epstein–Zin case, so the optimization problem in Albuquerque et al. (2016) might still be well defined. The quantitative exercise in Albuquerque et al. (2016) does not shed light on this issue because they do not solve the agent’s optimization problem directly. Instead, they assume that a solution exists and use it to derive asset pricing moments.

| Length of Paths | ||||

|---|---|---|---|---|

| Estimate of | 1.00355 | 1.00698 | 1.01220 | 1.01321 |

| Standard Error | (0.00004) | (0.00008) | (0.00045) | (0.00054) |

6.2.5. The Role of Elasticity of Intertemporal Substitution

In a New Keynesian model with preference similar to (30) studied by Basu and Bundick (2017), de Groot et al. (2018) show that the responses to discount factor shocks explode when the elasticity of intertemporal substitution approaches one, and that this issue disappears if is constant. This matches (34). If the volatility term is not zero, then becomes arbitrarily large as approaches one. Hence it appears that the large responses found in de Groot et al. (2018) are the result of an ill-defined household problem that fails the eventual discounting condition. If , then (34) becomes . Letting approach one will push down instead so the issue disappears.

In de Groot et al. (2018), the asymptote in the responses is attributed to the distributional weights on current and future utility not summing to one. They propose an alternative setting where current utility is weighted by and future utility is weighted by with . We show in the appendix that the eventual discounting condition for this specification is the same as Assumption 6.1. Since is assumed to be strictly less than one in de Groot et al. (2018), we let for some and assume fixed returns. Then (34) implies that . The previous discussion shows that, in this case, eventual discounting holds when approaches one. This provides an alternative explanation of why the model does not produce an asymptote in responses to discount factor shocks.

7. Conclusion

We introduce a weak discounting condition and show that, under this condition, standard infinite horizon dynamic programs with state-dependent discount rates are well defined and well behaved. The value function satisfies the Bellman equation, an optimal policy exists, Bellman’s principle of optimality is valid, value function iteration converges and so does Howard’s policy iteration algorithm. The method can be applied to a broad range of dynamic programming problems, including those with discrete choices, continuous choices and recursive preferences.

We connect eventual discounting to a spectral radius condition and provided guidelines on how to calculate the spectral radius for a range of discount specifications. We show that the condition is more likely to fail when the discount process has higher mean, persistence, or volatility. For models with Epstein–Zin preferences and state-dependent discount factors, the condition also depends on the elasticity of intertemporal substitution.

One natural open question is: how do our results translate into continuous time? It would also be valuable to understand how the results change if discounting depends on endogenous states and actions. Finally, more research is needed on how close to necessary the eventual discounting conditions are for recursive preference models, and especially those involving long run risks, since these models generate realistic asset price processes by driving their parameterizations close to the boundary between stability and instability. These questions are left to future research.

Appendix A Remaining Proofs

In what follows, we consider the dynamic program described in Section 2.1.

A.1. Proofs for Section 2

A.1.1. Proof of Theorem 2.1

For each , let be defined on by (4). Let be defined on by (5). We prove part (a) through two lemmas.

Lemma A.1.

If , then is eventually contracting on .

Proof.

Fix and . The map is Borel measurable on by the regularity conditions and measurability of . It is bounded by the assumption that is bounded. Hence is a self-map on . To see that it is eventually contracting, fix in and observe that, by Assumption 2.1,

for any . We can write this expression as

| (36) |

where is the operator defined by

Since , is a self-map on . Since is order preserving, we can iterate on (36) to obtain for all .

Let be a Markov process generated by and started at , let , and let be the controlled Markov process generated by with . We then have and, iterating on this equation,

| (37) |

Since , taking the supremum yields . It now follows from the eventual discounting property that is a contraction for some . Hence is eventually contracting. ∎

Lemma A.2.

The operator is eventually contracting on .

Proof.

Fix . The map is continuous on by regularity and Berge’s Maximum Theorem (Aliprantis and Border, 2006, Theorem 17.31). It is bounded by boundedness of . Hence is a self-map on . To see that it is eventually contracting, fix in and observe that, by Assumption 2.1,

for any . We can write this expression as

| (38) |

where is the operator on defined by

It follows from regularity and the Feller property (see footnote 9) that is continuous. Since , it follows from the maximum theorem that is a self-map on . Since is order preserving, we can iterate on (38) to obtain for all .

Now set , let be a Markov process generated by with initial condition and let . We then have and hence

More generally, for arbitrary , we have . Since , taking the supremum gives for all . It follows from eventual discounting that is a contraction for some and hence is eventually contracting. ∎

Corollary A.3.

If , the -value function is the unique fixed point of in and for all . The Bellman operator has a unique fixed point in and for all .

Proof.

Next we show that given by Corollary A.3 is the value function. First note that by definition. Iterating on both sides and using (2), we have . Taking to infinity, it follows from Corollary A.3 that . Taking the supremum over gives .

For the other direction, regularity and the measurable maximum theorem (Aliprantis and Border, 2006, Theorem 18.19) ensure that there exists a such that . Then we have . Because and has a unique fixed point in by Corollary A.3, . By the definition of , we have . Therefore, and is the optimal policy. This proves (c) and (d).

A.1.2. Blackwell’s Condition

Proposition A.4 (Blackwell’s Condition).

Let be a regular dynamic program. If there exists a nonnegative function and a Feller transition kernel on such that is eventually discounting and the Bellman operator satisfies

| (39) |

for all , , and , then is eventually contracting on .

Proof of Proposition A.4.

For any , we have

for all , where is lower semicontinuous (Aliprantis and Border, 2006, Lemma 17.29) and thus . Inequality (39) implies that

It then follows from (2) that

Exchanging the roles of and , we have

Iterating on the above inequality, it follows from a similar argument to the proof of Lemma A.2 that . Since is a self map on , it follows from eventual discounting that is eventually contracting. ∎

A.1.3. Monotonicity, Concavity, and Differentiability

Proof of Theorem 2.2.

Since is a closed subset of , it suffices to show that maps to functions in that are strictly concave in . For monotonicity, pick any and . Then for any ,

where the first inequality holds because and the second inequality holds because is increasing in by Assumption 2.2. For concavity, pick any satisfying and and define . Then, for any and ,

where the first inequality holds because is strictly concave and the second inequality holds because by Assumption 2.2. The strict concavity of and the maximum theorem imply that is single-valued and continuous.

A.2. Proofs for Section 4

Proof of Proposition 4.1.

Since , defined in (17) is a bounded linear operator. It follows from Theorem 1.5.5 of Bühler and Salamon (2018) that always exists and is bounded above by .

Let on . For each and , an inductive argument gives

| (40) |

Thus, eventual discounting can be written as for some . Applying Theorem 9.1 of Krasnosel’skii et al. (1972), since (i) is a positive linear operator on , (ii) the positive cone in this set is solid and normal under the pointwise partial order262626A cone is solid if it has an interior point; it is normal if implies that . The cone of nonnegative functions in is both solid and normal., and (iii) lies interior to the positive cone in , we have

| (41) |

where the second equality is due to (40), nonnegativity of and the definition of the supremum norm. This confirms the first claim in Proposition 4.1. It also follows immediately that implies eventual discounting.

To see that the converse is true, suppose there exists an such that . Then any can be expressed uniquely as for some with . For sufficiently large , it follows from the Markov property that

The right hand side is dominated by , where . If , then , and this term approaches . Hence , as was to be shown. ∎

Proof of Proposition 4.2.

The proof of Proposition 4.1 uses the fact that holds when is a positive (i.e., order preserving) linear operator on a Banach lattice with solid positive cone, denotes the spectral radius of a linear operator mapping this Banach lattice to itself, and is interior to the positive cone (Krasnosel’skii et al., 1972, Theorem 9.1). If is finite and is irreducible with stationary distribution , we can take to be all and set . Under this norm, is interior to the positive cone of because, by irreducibility, for all . Applying the above expression for the spectral radius to , as well as the result in (40), we obtain

| (42) |

where the last equality uses the law of iterated expectations and the definition of in Proposition 4.2.

It remains only to show that , where the latter is defined, as before, using the supremum norm (see, e.g., (41)). In other words, we need to show that

| (43) |

On finite dimensional normed linear spaces, any two norms are equivalent (see, e.g., Bühler and Salamon (2018), Theorem 1.2.5), so we can take positive constants and with on . The equality in (43) easily follows and the proof is now complete. ∎

A.3. Proofs for Section 5

A.3.1. Homogeneous Functions

Let the operators and be as defined in (4) and (5), respectively, with aggregator given by (23). The definition of is given in Section 5.1.

Proof of Proposition 5.1.

We first show that is eventually contracting on . Since Assumption 5.1 holds, the Feller property implies that maps to itself. Note that for any , we have . It follows from Assumption 5.2 that for any ,

An inductive argument gives that

where the norm is defined in (25). Therefore, we have

By Assumption 5.2, is eventually contracting on . Hence, has a unique fixed point on and for any .

Since is not necessarily in , we cannot apply the same argument to . Hence, we prove the remaining results directly. We first show that is well defined. It follows from Assumptions 5.1 and 5.2 that

where . It follows from Proposition 4.1 and the Cauchy root test that the series converges absolutely and hence is finite and well defined.

Next we show that . Since , we have for any ,

It follows from induction that

| (44) |

where is given by . Since , we have . Taking to infinity in (44), the last term goes to 0 and thus for all . By the measurable maximum theorem, we can find such that . A similar argument shows that achieves the maximum. Therefore, is the value function and is the optimal policy.

Because is homogeneous of degree , we have for any ,

It follows that , that is, the optimal policy is homogeneous of degree one. ∎

A.3.2. Local Contractions

Recall that the operators and are as defined in (4) and (5), respectively, with aggregator given by (23).

Proof of Proposition 5.2.

Define if and . Since is continuous and every is compact, for all . For any initial state , we can find such that . It follows from Assumption 5.3 that for all .

Choose any increasing and unbounded such that . Since is Feller, is continuous on every for , where the space is defined in Section 5.2. It follows from Remark 1(a) of Matkowski and Nowak (2011) that .

Since for all , we have on

An inductive argument gives

Taking the supremum, we have . Since is eventually discounting, is a 0-local contraction for some .272727We say an operator is a 0-local contraction if there exists a such that for all and all . Then it follows from Proposition 1 of Matkowski and Nowak (2011) that has a unique fixed point in . It can be proved in the same way that is also a 0-local contraction and hence is well defined and finite for any initial state. Since we can find such that by the measurable maximum theorem, the optimality results follow from a similar argument to the proofs of Theorem 2.1. ∎

A.4. Proofs for Section 6

A.4.1. Alternative Discount Specifications

Here we sketch the proof of Theorem 2.1 for the alternative timing when the aggregator satisfies (26). Let be a Markov process generated by starting at and let . A similar argument to the proof of Lemma A.1 yields , where represents expectation conditional on . Taking the supremum gives . Similar result holds for the Bellman operator . Therefore, both and are eventually contracting if for some . The rest of the proof remains the same.

Proof of Proposition 6.1.

Recall that the primitives are redefined as in footnote 21. Then the aggregator satisfies

Based on the discussion above, the eventual discounting condition remains the same. It then follows from Proposition 4.1 that eventual discounting holds if and only if and

where represents conditional expectation under . Since is induced by and , we can write . Then we have , where and are positive constants such that for all . Taking gives , so eventual discounting holds if and only if . ∎

A.4.2. Epstein-Zin Preferences

For ease of notation, we replace with in what follows. The definition of and are given in Section 6.2. Let the operators and be as defined in (4) and (5), respectively, with aggregator given by (28). Let and be defined in the same way except that is replaced by

| (45) |

which is a special case of when . We first prove a useful lemma.

Lemma A.5.

and for all .

Proof.

Since , by Jensen’s inequality, we have

for all and . It follows that

That can be shown in a similar way. ∎

A central result of this section is the following proposition, which guarantees that the -value function is well defined and a fixed point of .

Proposition A.6.

Under Assumption 6.1, there exists a function given by

| (46) |

such that and is a self map on . The -value function is well defined and is the least fixed point of on . Furthermore, if satisfies that for all , then is the unique fixed point of on and for all .

We first give two lemmas that are crucial to the proof of Proposition A.6. The first lemma shows that can indeed act as an upper bound function.

Lemma A.7.

and for all .

Proof.

Let where

By Proposition 4.1 and Assumption 6.1, we have

where is as defined in (33). It follows from the root test that is well defined and bounded on . Hence, and it satisfies . Therefore, .

Next, we use the operator defined above to show that . Since is increasing in , by the Monotone Convergence Theorem, we have . Write . Since , it follows that

Since , by the Minkowski inequality, we have

Note that the following equation holds

by the Markov property. It follows that

Taking to infinity, we have . By Lemma A.5, . ∎

Lemma A.8.

for all and .

Proof.

Evidently is measurable given . To see that is bounded, we have

where the first inequality follows from Lemma A.5 and the second inequality follows from the fact that and for all . Dividing both sides by yields (assuming )

Since and are bounded, . ∎

Proof of Proposition A.6.

It is apparent that . It follows from Lemma A.7, Lemma A.8, and the monotonicity of that is a self map on . Let be a countable chain282828A set is called a chain if for every , either or . on . Then both and are measurable and bounded in norm by . So is a countably chain complete partially ordered set. For any increasing , it follows from the Monotone Convergence Theorem that . Hence, is monotonically sup-preserving. Then, by the Tarski-Kantrovich Theorem,292929See, for example, Becker and Rincón-Zapatero (2018) for a version of the theorem and related definitions. is the least fixed point of on .

If satisfies that for all , then there exists an such that . Since , and are comparable. Uniqueness and convergence then follow from Theorems 10 and 11 in Marinacci and Montrucchio (2010). ∎

Recall from Section 6.2 that is all functions in that are homogeneous of degree one in . The following lemma is useful in the proof of Proposition 6.2.

Lemma A.9.

For any , and there exists a homogeneous in that satisfies and for all .

Proof.

Pick and we can write for some bounded measurable . Then (28) becomes

| (47) |

Since is continuous and is measurable, by the measurable maximum theorem, is measurable and there exists a such that . Since in (47), a similar argument to the proof of Lemma A.8 shows that is bounded in .

In fact, is the solution of the single variable optimization problem maximizing over where

It has closed-form solution . Therefore, is homogeneous in and thus is also homogeneous in . It follows that . Since is bounded, . ∎

Proof of Proposition 6.2.

By Lemma A.9, there exists a such that . It follows from Lemma A.7 that and hence . Then the monotonicity of implies that for all . By Lemma A.9 and the monotonicity of , is an increasing sequence on bounded above by . Therefore, the pointwise limit is well defined and is also in .

To see that is the value function, pick any . Since is an increasing sequence converging to , . Taking to infinity, it follows from Proposition A.6 that . Next we show that can be achieved by a feasible policy. Since , the monotonicity of implies that . Taking to infinity yields . By Lemma A.9, there exists a homogeneous that satisfies the interiority condition and . Then we have and hence by the monotonicity of . Taking to infinity, it follows from Proposition A.6 that . Since for all , . ∎

A.5. Analytical Expression for the Geometric Mean

A.6. Necessity

In many settings, the eventual discounting condition cannot be weakened without violating finite lifetime values. Here we briefly illustrate this point, using the connection to spectral radii provided in Proposition 4.1.

Consider a standard dynamic program with lifetime rewards given constant and reward flow . In this setting, cannot be relaxed without imposing specific conditions on rewards. For example, if there are constants such that the process satisfies for all , then we clearly have303030The equivalence in (50) is easy to see because, by the Monotone Convergence Theorem, we have and, moreover, .

| (50) |

Eventual discounting has the same distinction once we replace the constant with a process under standard regularity conditions. For example, if is compact and for some and -Markov process , then

| (51) |

To see this, suppose first that . Since , we have

By Cauchy’s root convergence criterion, the sum will be finite whenever . This holds when by Proposition 4.1.

References

- Albuquerque et al. (2016) Albuquerque, R., M. Eichenbaum, V. X. Luo, and S. Rebelo (2016): “Valuation risk and asset pricing,” The Journal of Finance, 71, 2861–2904.

- Aliprantis and Border (2006) Aliprantis, C. D. and K. C. Border (2006): Infinite Dimensional Analysis: A Hitchhiker’s Guide, Springer.

- Alvarez and Stokey (1998) Alvarez, F. and N. L. Stokey (1998): “Dynamic programming with homogeneous functions,” Journal of Economic Theory, 82, 167–189.

- Bansal and Yaron (2004) Bansal, R. and A. Yaron (2004): “Risks for the long run: A potential resolution of asset pricing puzzles,” The Journal of Finance, 59, 1481–1509.

- Basu and Bundick (2017) Basu, S. and B. Bundick (2017): “Uncertainty shocks in a model of effective demand,” Econometrica, 85, 937–958.

- Becker and Rincón-Zapatero (2018) Becker, R. A. and J. P. Rincón-Zapatero (2018): “Recursive Utility and Thompson Aggregators I: Constructive Existence Theory for the Koopmans Equation,” Tech. rep., CAEPR WORKING PAPER SERIES 2018-006.

- Benveniste and Scheinkman (1979) Benveniste, L. M. and J. A. Scheinkman (1979): “On the differentiability of the value function in dynamic models of economics,” Econometrica: Journal of the Econometric Society, 727–732.

- Bertsekas (2013) Bertsekas, D. P. (2013): Abstract dynamic programming, Athena Scientific Belmont, MA.

- Bertsekas (2017) ——— (2017): Dynamic programming and optimal control, vol. 2, Athena Scientific.

- Bhandari et al. (2013) Bhandari, A., D. Evans, M. Golosov, and T. J. Sargent (2013): “Taxes, debts, and redistributions with aggregate shocks,” Tech. rep., National Bureau of Economic Research.

- Blackwell (1965) Blackwell, D. (1965): “Discounted dynamic programming,” The Annals of Mathematical Statistics, 36, 226–235.

- Bloise and Vailakis (2018) Bloise, G. and Y. Vailakis (2018): “Convex dynamic programming with (bounded) recursive utility,” Journal of Economic Theory, 173, 118–141.

- Borovička and Stachurski (2020) Borovička, J. and J. Stachurski (2020): “Necessary and sufficient conditions for existence and uniqueness of recursive utilities,” The Journal of Finance.

- Bühler and Salamon (2018) Bühler, T. and D. Salamon (2018): Functional Analysis, The American Mathematical Society.

- Cao (2020) Cao, D. (2020): “Recursive equilibrium in Krusell and Smith (1998),” Journal of Economic Theory, 186, 104978.

- Cheney (2013) Cheney, W. (2013): Analysis for applied mathematics, vol. 208, Springer Science & Business Media.

- Christensen (2020) Christensen, T. M. (2020): “Existence and uniqueness of recursive utilities without boundedness,” Tech. rep., arXiv preprint arXiv:2008.00963.

- Christiano et al. (2011) Christiano, L., M. Eichenbaum, and S. Rebelo (2011): “When is the government spending multiplier large?” Journal of Political Economy, 119, 78–121.

- Christiano et al. (2014) Christiano, L. J., R. Motto, and M. Rostagno (2014): “Risk shocks,” American Economic Review, 104, 27–65.

- Correia et al. (2013) Correia, I., E. Farhi, J. P. Nicolini, and P. Teles (2013): “Unconventional fiscal policy at the zero bound,” American Economic Review, 103, 1172–1211.

- de Groot et al. (2020) de Groot, O., A. W. Richter, and N. Throckmorton (2020): “Valuation Risk Revalued,” Tech. rep., CEPR Discussion Paper No. DP14588.

- de Groot et al. (2018) de Groot, O., A. W. Richter, and N. A. Throckmorton (2018): “Uncertainty shocks in a model of effective demand: Comment,” Econometrica, 86, 1513–1526.

- Du (2006) Du, Y. (2006): Order structure and topological methods in nonlinear partial differential equations: Vol. 1: Maximum principles and applications, vol. 2, World Scientific.

- Eggertsson (2011) Eggertsson, G. B. (2011): “What fiscal policy is effective at zero interest rates?” NBER Macroeconomics Annual, 25, 59–112.

- Eggertsson and Woodford (2003) Eggertsson, G. B. and M. Woodford (2003): “Zero bound on interest rates and optimal monetary policy,” Brookings papers on economic activity, 2003, 139–211.

- Epstein and Zin (1989) Epstein, L. G. and S. E. Zin (1989): “Substitution, Risk Aversion, and the Temporal Behavior of Consumption and Asset Returns: A Theoretical Framework,” Econometrica, 57, 937–969.

- Fagereng et al. (2019) Fagereng, A., M. B. Holm, B. Moll, and G. Natvik (2019): “Saving Behavior Across the Wealth Distribution: The Importance of Capital Gains,” Tech. rep., Princeton.

- Farmer and Toda (2017) Farmer, L. E. and A. A. Toda (2017): “Discretizing nonlinear, non-Gaussian Markov processes with exact conditional moments,” Quantitative Economics, 8, 651–683.

- Gomez-Cram and Yaron (2020) Gomez-Cram, R. and A. Yaron (2020): “How Important Are Inflation Expectations for the Nominal Yield Curve?” The Review of Financial Studies.

- Hansen and Scheinkman (2009) Hansen, L. P. and J. A. Scheinkman (2009): “Long-term risk: An operator approach,” Econometrica, 77, 177–234.

- Hansen and Scheinkman (2012) ——— (2012): “Recursive utility in a Markov environment with stochastic growth,” Proceedings of the National Academy of Sciences, 109, 11967–11972.

- Hills and Nakata (2018) Hills, T. S. and T. Nakata (2018): “Fiscal multipliers at the zero lower bound: the role of policy inertia,” Journal of Money, Credit and Banking, 50, 155–172.

- Hills et al. (2019) Hills, T. S., T. Nakata, and S. Schmidt (2019): “Effective lower bound risk,” European Economic Review, 120, 103321.

- Howard (1960) Howard, R. A. (1960): Dynamic programming and Markov processes, John Wiley.

- Hubmer et al. (2020) Hubmer, J., P. Krusell, and A. A. Smith (2020): “Sources of US wealth inequality: Past, present, and future,” NBER Macroeconomics Annual 2020, volume 35.

- Jasso-Fuentes et al. (2020) Jasso-Fuentes, H., J.-L. Menaldi, and T. Prieto-Rumeau (2020): “Discrete-time control with non-constant discount factor,” Mathematical Methods of Operations Research, 1–23.

- Justiniano and Primiceri (2008) Justiniano, A. and G. E. Primiceri (2008): “The time-varying volatility of macroeconomic fluctuations,” American Economic Review, 98, 604–41.

- Justiniano et al. (2010) Justiniano, A., G. E. Primiceri, and A. Tambalotti (2010): “Investment shocks and business cycles,” Journal of Monetary Economics, 57, 132–145.

- Justiniano et al. (2011) ——— (2011): “Investment shocks and the relative price of investment,” Review of Economic Dynamics, 14, 102–121.

- Karni and Zilcha (2000) Karni, E. and I. Zilcha (2000): “Saving behavior in stationary equilibrium with random discounting,” Economic Theory, 15, 551–564.

- Kopecky and Suen (2010) Kopecky, K. A. and R. M. Suen (2010): “Finite state Markov-chain approximations to highly persistent processes,” Review of Economic Dynamics, 13, 701–714.

- Krasnosel’skii et al. (1972) Krasnosel’skii, M. A., G. M. Vainikko, P. P. Zabreiko, Y. B. Rutitskii, and V. Y. Stetsenko (1972): Approximate Solution of Operator Equations, Springer Netherlands.

- Krusell et al. (2009) Krusell, P., T. Mukoyama, A. Şahin, and A. A. Smith (2009): “Revisiting the welfare effects of eliminating business cycles,” Review of Economic Dynamics, 12, 393–404.

- Krusell and Smith (1998) Krusell, P. and A. A. Smith (1998): “Income and wealth heterogeneity in the macroeconomy,” Journal of Political Economy, 106, 867–896.

- Leeper et al. (2010) Leeper, E. M., T. B. Walker, and S.-C. S. Yang (2010): “Government investment and fiscal stimulus,” Journal of Monetary Economics, 57, 1000–1012.

- Ma et al. (2020) Ma, Q., J. Stachurski, and A. A. Toda (2020): “The income fluctuation problem and the evolution of wealth,” Journal of Economic Theory, 187, 105003.

- Marinacci and Montrucchio (2010) Marinacci, M. and L. Montrucchio (2010): “Unique solutions for stochastic recursive utilities,” Journal of Economic Theory, 145, 1776–1804.

- Martins-da Rocha and Vailakis (2010) Martins-da Rocha, V. F. and Y. Vailakis (2010): “Existence and uniqueness of a fixed point for local contractions,” Econometrica, 78, 1127–1141.

- Matkowski and Nowak (2011) Matkowski, J. and A. S. Nowak (2011): “On discounted dynamic programming with unbounded returns,” Economic Theory, 46, 455–474.

- Mehra and Sah (2002) Mehra, R. and R. Sah (2002): “Mood fluctuations, projection bias, and volatility of equity prices,” Journal of Economic Dynamics and Control, 26, 869–887.

- Nakata (2016) Nakata, T. (2016): “Optimal fiscal and monetary policy with occasionally binding zero bound constraints,” Journal of Economic Dynamics and Control, 73, 220–240.

- Nakata and Tanaka (2020) Nakata, T. and H. Tanaka (2020): “Equilibrium Yield Curves and the Interest Rate Lower Bound,” CARF F-Series CARF-F-482, Center for Advanced Research in Finance, Faculty of Economics, The University of Tokyo.

- Primiceri et al. (2006) Primiceri, G. E., E. Schaumburg, and A. Tambalotti (2006): “Intertemporal disturbances,” Tech. rep., National Bureau of Economic Research.

- Qin and Linetsky (2017) Qin, L. and V. Linetsky (2017): “Long-term risk: A martingale approach,” Econometrica, 85, 299–312.

- Rincón-Zapatero and Rodríguez-Palmero (2003) Rincón-Zapatero, J. P. and C. Rodríguez-Palmero (2003): “Existence and uniqueness of solutions to the Bellman equation in the unbounded case,” Econometrica, 71, 1519–1555.

- Saijo (2017) Saijo, H. (2017): “The uncertainty multiplier and business cycles,” Journal of Economic Dynamics and Control, 78, 1–25.

- Schäl (1975) Schäl, M. (1975): “Conditions for optimality in dynamic programming and for the limit of n-stage optimal policies to be optimal,” Probability Theory and Related Fields, 32, 179–196.

- Schorfheide et al. (2018) Schorfheide, F., D. Song, and A. Yaron (2018): “Identifying Long-Run Risks: A Bayesian Mixed-Frequency Approach,” Econometrica, 86, 617–654.

- Stokey et al. (1989) Stokey, N. L., R. E. Lucas, and E. C. Prescott (1989): Recursive methods in economic dynamics, Harvard University Press.

- Toda (2019) Toda, A. A. (2019): “Wealth distribution with random discount factors,” Journal of Monetary Economics, 104, 101–113.

- Uribe and Schmitt-Grohé (2017) Uribe, M. and S. Schmitt-Grohé (2017): Open economy macroeconomics, Princeton University Press.

- Uzawa (1968) Uzawa, H. (1968): “Time preference, the consumption function, and optimum asset holdings,” Value, capital and growth: papers in honor of Sir John Hicks. The University of Edinburgh Press, Edinburgh, 485–504.

- Williamson (2019) Williamson, S. D. (2019): “Low real interest rates and the zero lower bound,” Review of Economic Dynamics, 31, 36–62.

- Woodford (2011) Woodford, M. (2011): “Simple Analytics of the Government Expenditure Multiplier,” American Economic Journal: Macroeconomics, 3, 1–35.