Myopic robust index tracking with Bregman divergence

Abstract

Index tracking is a popular form of asset management. Typically, a quadratic function is used to define the tracking error of a portfolio and the look back approach is applied to solve the index tracking problem. We argue that a forward looking approach is more suitable, whereby the tracking error is expressed as an expectation of a function of the difference between the returns of the index and of the portfolio. We also assume that there is a model uncertainty in the distribution of the assets, hence a robust version of the optimization problem needs to be adopted. We use Bregman divergence in describing the deviation between the nominal and actual (true) distribution of the components of the index. In this scenario, we derive the optimal robust index tracking portfolio in a semi-analytical form as a solution of a system of nonlinear equations. Several numerical results are presented that allow us to compare the performance of this robust portfolio with the optimal non-robust portfolio. We show that, especially during market downturns, the robust portfolio can be very advantageous.

keywords:

Index tracking; Robust index tracking; Bregman divergence; Kullback-Leibler divergenceG11; D81

1 Introduction.

A popular form of passive asset management is the so-called index tracking (see discussions, for example, in Andriosopoulos and Nomikos (2014); Beasley et al. (2003); Gaivoronski et al. (2005)). Essentially, it means that the fund

manager (or the investor) tries to replicate the performance of an index either through its value or its return (see Strub and Baumann (2018) and the references therein).

In a frictionless and liquid market, a full replication portfolio (i.e. by holding exactly the same composition as the index) obviously yields the best

tracking performance. This has already been discussed in many past studies, e.g., Beasley et al. (2003); Strub and Baumann (2018). However, if transaction costs are

considered or some of the components of the index are illiquid (see Maginn et al. (2007)), then a full replication portfolio does not necessarily deliver the best performance.

This is due to the fact that a full replication portfolio will involve high transaction costs and because buying and selling illiquid assets will be difficult. Thus, to replicate the index, the fund manager may

choose a tracking portfolio with only a subset of representative assets (see Strub and Baumann (2018); de Paulo et al. (2010); Guastaroba and Speranza (2012) among others). It is worth noting that, in

general, the assets in the tracking portfolio do not have to be the components of the index as long as they exhibit good similarity with the index (see for

example, Andriosopoulos and Nomikos (2014)).

To satisfactorily solve the index tracking problem or the related enhanced tracking problem (which tracks the index as well as outperforms it), predominantly the look back approach has

been used in the literature, see e.g., Strub and Baumann (2018); Guastaroba et al. (2016); Chiam et al. (2013); Montfort et al. (2008); Beasley et al. (2003). This approach relies on the assumption that a portfolio that has tracked

the index well in the past will also demonstrate good tracking performance in the future. The past realizations of

the return (or value) of the index and the return (or value) of the tracking portfolio are collected and the tracking error is defined as a function of the

difference between the index and the tracking portfolio. A quadratic function is often used to define such a tracking error.

The above approach may lead to poor performance if the future differs vastly from the past. Another way to solve the index tracking problem is by adopting the forward looking approach. This is based on defining the tracking error as the expectation of a function of the difference between the return of the index and the

return of the tracking portfolio (see for example, de Paulo et al. (2010); Meade and Salkin (1990)). The expectation is calculated by using the joint distribution of the index

and of the tracking portfolio. A reliable estimation of the joint distribution is required in order to guarantee a good performance of this approach. If uncertainty in the

distribution of the assets is present, a robust version of the approach needs to be taken.

From the onset of the paper, we should point out that index tracking has not received the attention it deserves until recently, but the situation has since changed dramatically. Many aspects of index tracking attract the attention of the research community.

An interesting recent research is directed towards the attempt to unify the two tasks, selecting the “optimal subset” and determining the “best” weights in a single step. This approach is attractive especially if an index contains a large number of stocks while one is interested to have a (very) small number of stocks in the portfolio (Benidis et al. (2018)). In other words, the goal in this case is to select a sparse index tracking portfolio. While we are also interested in developing such types of approaches, they are based on different optimization techniques (e.g., sparse non-convex optimization Benidis et al. (2018), mixed-integer programming Canakgoz and Beasley (2008), Filippi et al. (2016)), and we are not discussing these approaches in our paper.

It may be possible to use quite sophisticated statistical multivariate models and numerical approximation techniques to better mimic the underlying joint distribution of the stock returns and the index returns, and our theory allows for such models to be used as a nominal distribution in index tracking. However, our point of view in this paper is that even then a robustness approach is worth using as it has the potential to safeguard against deviations from the nominal model.

The paper Gnägi and Strub (2020) gives a review of recent approaches and examines critically the gaps in the literature on enhanced index-tracking problem. It also proposes novel matheuristics (combining metaheuristics with mathematical programming) numerical algorithms to solve index-tracking problems with very large indices (e.g., with more than 9000 constituents). Among the many constraints they consider, is also the achievement of a given target excess return in the future. Because future outcomes are uncertain, they end up requiring a minimum expected excess return which may not deliver the target in an out-of-sample period. The paper does not deal with the robustness-type penalties that are of main interest in our paper.

As mentioned, the most recent literature focuses on the look back approach and a great effort has been made to model transaction costs and other sophisticated

restrictions on the tracking portfolio such as choosing which components of the index to include. The aim of this paper is,

however, to develop a robust version of index tracking. As far as the authors are aware, this has not been

done in the past. When done,the concern has mainly been about robustness with respect to parameter uncertainty rather than robustness about distributional uncertainty (Fabozzi (2007)). One possible exception is Lejeune (2012) where a minimax game theoretic interpretation of the robust forward looking approach is discussed. However, in Lejeune (2012),

only parameter uncertainty is considered, that is, the authors assume that the excess returns are imperfectly known but belong to a class of distributions characterized by an ellipsoidal distributional set. In contrast, we consider the uncertainty in the joint distribution of the index and the tracking portfolio, and find the

optimal way to track the index under the worst case distribution. Our approach could be compared to the recently popular distributional robustness methodology. A survey of this methodology, with a focus on actuarial applications, can be found in Blanchet et al. (2019). To the best of our knowledge, we have not seen application of this methodology to the index tracking problem.

The model uncertainty in our paper is measured through a special form of Bregman divergence (see Bregman (1967)). The notion of Bregman divergence is quite general. It has been used as a means to measure the pairwise dissimilarity between matrices (Penev and Prvan (2016)), between vectors (Banerjee et al. (2005)), and also between functions (Goh and Dey (2014), Penev and Naito (2018)). In the latter case, the authors in Goh and Dey (2014) call it a functional Bregman divergence. Precise definition is given in Section 3.

The classical Kullback-Leibler (KL) divergence also belongs to the class of Bregman divergences. It can be used as a benchmark. However, KL divergence is not appropriate to handle heavy tailed distributions which are commonly observed in financial asset returns (Dey and Juneja (2010), Poczos and Schneider (2011)). Hence we choose another family of Bregman divergences whereby the convex function in the divergence’s definition in Section 3 has a stronger polynomial growth than the one that is used in the case of KL. Yet we are using a family of Bregman divergences that is parameterized by one positive parameter

only and is such that allows us to recover the KL divergence in a limit when

.

In such a way we can study the effect of stronger robustification achieved when

runs away from the zero value. As we point out in detail in Remark 3.3, this goal is indeed achieved by our choice of the function in the specification of the Bregman divergence.

Our first contribution is the derivation of a semi-closed form of the worst case distribution

for

the chosen Bregman divergence.

The second contribution is the derivation of the optimal index tracking portfolio in a semi-analytical form. The derivation of such a robust index tracking portfolio was the main goal of our work. Thirdly, we investigate the performance of our proposed robust tracking portfolio

in a short numerical study aiming to demonstrate the robustness effect. Our next contribution is related to extending our approach to deal with a variety

of loss functions that are suitable to measure the quality of an index tracking portfolio. Finally, we also include a real data example in order to illustrate the

out-of-sample performance of our method.

The structure of this paper is outlined below. In Section 2, we formulate the index tracking problem, and present the look back approach and the forward looking

approach through a simple example. In Section 3, we formulate the robust index tracking problem and derive the robust index tracking portfolio. In Section 4, we extend our model to tackle enhanced index tracking. In Section 5 we present our numerical study. Section 6 concludes and outlines avenues for further research.

2 Myopic Index Tracking

In this section, we formulate the index tracking problem and compare the look back approach and the forward looking approach through a simple example.

Consider an index that consists of risky assets. A fund manager is interested in constructing a tracking portfolio that contains risky assets

that may not necessarily belong to the index.

The aim is to replicate the return of the index over a fixed investment period.

In particular, since the return of the index is available for analysis after each investment period, we focus on a short term one-period (called “myopic”) index tracking.

Within this period, we denote by the random vector of returns of the

risky assets included in the portfolio. Hence , denotes the return of the th individual asset over the intended investment period. The return of the index over this investment period is denoted as . We then define , and .

Throughout the paper, we assume that all random quantities are defined on a complete probability space () with the sample space , the -algebra , and the probability measure , where the -algebra .

In addition, we assume that short selling is permitted.

At the beginning of the investment period, the fund manager re-balances the portfolio with a control , where , , denotes the proportional allocation of the wealth of the investor into the th asset. Let be the set of admissible strategies such that

Two approaches exist to track an index. The look back approach finds the optimal portfolio based on the historical data. Let and , denote the return of the risky assets and the return of the index, respectively, on the th day before today. Define , and . Under this approach, the optimal control can be obtained by solving

| (1) |

The joint distribution of the index and of the tracking portfolio is taken to be the empirical distribution.

In contrast, the forward looking approach finds the optimal portfolio by solving

| (2) |

Under this approach, the actual distribution can be assumed to be essentially arbitrary.

It is easy to see that the forward looking approach relies on the future estimation of the actual distribution. If the empirical distribution delivers a good estimate of the future, then the look back approach is equivalent to the forward looking approach. However, this is not the case if another assumption is made about the actual distribution. Thus, unless the empirical distribution represents a reliable estimate, the two approaches yield different outcomes in general. In addition, even though the empirical distribution may represent a good estimate of the future, there is always an uncertainty in the estimation of the actual distribution. It is obvious that the “look back” is just a specific way to perform “forward looking” by using an empirical distribution of risk factors.

3 Myopic Robust Index Tracking

To model the uncertainty associated with the estimation of the actual distribution, we use the Bregman divergence.

3.1 The Bregman Divergence

The following definition of a Bregman divergence is taken from Penev and Naito (2018).

Definition 1.

Given a strictly convex function , where is a convex set, the local Bregman divergence between two points and is defined as

The above definition can also be applied point wise for positive density functions , defined on a common domain. The point wise application means that in this case means a simple derivative and we interpret locally, for a fixed

Using this localized divergence measure at the point we then define the global (or also called functional) Bregman divergence between the densities and

| (3) |

where is some non-negative weight function.

In the definition of the Bregman divergence, any strictly convex function could be chosen. A specific choice has been suggested in the paper Penev and Naito (2018), which we also take on board here. We take the strictly convex function to be

Then, for two densities and of the -dimensional argument it is easy to see that

It is worth noting that our special form of Bregman divergence is closely related to the so-called Tsallis divergence and -divergence (see for example Cichocki and Amari (2010); Poczos and Schneider (2011)).

-divergence is closely related to the special case of our Bregman divergence. It differs by a re-parameterization on which both divergences are defined.

It is quite a laborious task to discuss and compare the many different types of divergences that exist in the literature. Such a comparison is done in the monograph Amari (2016) and in Dey and Juneja (2010). The reader can also consult p. 187 in Amari & Cichocki (2010) where our current use of Bregman divergence is discussed under the name “-divergence”. It contains both Kullback-Leibler and Itakura-Saito divergences and

has found earlier applications in classical robustness and in machine learning. Similar comparisons are also done on p. 9 of Dey and Juneja (2010) which demonstrates that the polynomial divergence of which our chosen Bregman divergence is based, is a strictly monotone increasing function of the Rényi entropy. Hence minimizing the one or the other delivers essentially the same result.

In this paper, we prefer to work with the Bregman divergence in its functional form (3) when describing an ambiguity set around certain nominal probability distribution. Earlier approaches have described ambiguity sets using support and moment information or structural properties such as symmetry, unimodality, etc. We suggest that in the setting of index tracking, the uncertainty around the nominal model is difficult to specify accurately enough and for this reason considering a “full” functional-type neighbourhood is more suitable to start with. It is remarkable that the objective function for the robust index tracking problem in this functional setting is tractable and allows us to derive the optimal robust portfolio in a semi-analytical form as a solution of a system of nonlinear equations.

Since our purpose is to robustify the inference, it is essential for us to use the Bregman divergence (in particular, in its specific form of - divergence). In Mihoko & Eguchi (2002) the -divergence is used (which is essentially the same as the density power divergence of Basu et al. (1998)) and it is explicitly demonstrated that using the global -divergence leads to parameter estimators that are robust in the classical sense i.e., their influence function is bounded.

Now, by choosing the following weight function

we have constructed the following functional Bregman divergence:

| (4) | |||||

where

From now on, we will always denote the nominal distribution’s density by . Expectations in this paper are always supposed to be taken with respect to the nominal distribution . Then there will be a one-to-one correspondence between the pair and the pair where

Hence by slight abuse of notation, we will shorten the notation by replacing with

Remark 1.

We comment on our choice of the weight function in the definition of the functional Bregman divergence. Its usefulness goes much beyond the obvious fact that it leads to a simple expression for In Vemuri et al. (2011) it is argued that re-scaling at each the usual Bregman divergence can bring about intrinsic robustification. The way the Bregman divergence is re-scaled in Vemuri et al. (2011) leads to the so-called Total Bregman Divergence, which is too computationally heavy to be implemented in our case of functional Bregman divergence. However, the main idea of using a re-scaling that is inversely dependent on the derivative of the function can be applied also in our case and suggests the above choice of Our numerical experiments support this choice.

Remark 2.

One essential advantage of the special form of the Bregman divergence we use is that by just one parameter ( we can control the deviation from the well-known Kullback-Leibler (KL) divergence The latter is obtained as a limiting case when Indeed, as , we see that

This limit result then yields

The value of parameterizes a whole class of Bregman divergences and dictates the extent to which the robust method differs from the non-robust method (in Basu et al. (1998) it is called an algorithmic parameter). By varying the value of we can achieve a compromise between robustness and efficiency, as is standard in robust statistic setting. Larger values of correspond to a stronger emphasis on robustness. These would be useful when there is a belief that the divergence between the nominal distribution and the actual distribution of the returns might be large.

In a special case where both the nominal distribution and the actual distribution are multivariate normal, the above Bregman divergence can be calculated in a closed form.

Example [Multivariate Normal]. Suppose that the nominal distribution is a -dimensional multivariate normal distribution and an actual distribution is another -dimensional multivariate normal distribution Then, the Bregman divergence as defined above can be calculated in closed form as:

| (5) | |||||

provided is positive definite, where

If , the above formula simplifies to

| (6) |

It is worth noting that if we set in (6) we get

i.e., one half of the squared Mahalanobis distance between the multivariate normal distributions and

3.2 Robust Index Tracking

To perform index tracking in a robust way, we need to consider perturbations of the nominal distribution of the index. These perturbed distributions can be contained inside a ball of certain radius around the nominal distribution. To this end, let us construct a Bregman divergence ball. Suppose that , the so-called nominal distribution, is the joint density of the assets in the index, and is the density of a perturbation of , we denote by the set of all functions representable in the form where is a density. A Bregman divergence ball around of radius around is defined as

| (7) |

We stress again that all moments throughout this paper are defined with respect to the nominal distribution. Then the robust version of the control problem (2) is defined as

| (8) |

where

In the next section, we will derive a semi-analytical form of the optimal portfolio under the constructed Bregman divergence.

3.3 Robust Optimal Portfolio under Bregman Divergence

The robust optimal index tracking portfolio can be obtained by applying the following result.

Theorem 3.1.

For a fixed, small enough if there exist , and such that

where

then is an optimal index tracking portfolio.

Proof.

Using the definition of we see that (8) becomes

| (9) |

To solve the inner optimization problem, we first write down the Lagrangian. For a fixed and a , the Lagrangian is

where

Differentiating inside the expectation and setting the result equal to zero yields:

| (10) |

Solving this equation, we obtain

| (11) |

provided that .

Next, we verify that this is indeed an optimal solution. The proof follows similarly to (Glasserman and Xu, 2014, proposition 2.3) and (Dey and Juneja, 2010, theorem 2). The idea is to show that along any feasible direction the value of the Lagrangian can not be optimized any further.

Choose an arbitrary For , define , then we have

If we consider as a function of , and define

it is then easy to calculate

This implies then

since satisfies (10). In addition, we know that is convex in its first argument, thus is convex in which implies

is an optimal solution. Because is arbitrary, we can not improve the value of the objective along any feasible direction from . This concludes

that is an optimal solution.

Next, we notice that the set

is not empty. By Theorem 2.1. in Ben-Tal et al. (1988), strong duality holds. This implies (see for example, pp. 242–243 in Boyd and Vandenberghe (2004)) that the optimal solution and its corresponding satisfies the following system:

We denote the solution of this system as . Thus, we obtain

| (12) |

where is the solution of . With an appropriate choice of (small) , we can always achieve that in (12) is well-defined and positive. Indeed, for the limiting case (corresponding to the KL divergence) we have

and the solution clearly being positive.

As in Proposition 2.3 of Glasserman and Xu (2014) we can argue that by continuity we can find a set such that will stay positive for any

Using (12), we end up with the optimization problem

| (13) |

In Appendix 7.2 we demonstrate that the solution to this optimization problem satisfies the system of equations in the statement of Theorem 3.1.

∎

As mentioned in Remark 2, as , the chosen Bregman divergence converges to the Kullback-Leibler (KL) divergence. Indeed, as , the system in Theorem 3.1 also converges to the corresponding system of the KL divergence. This is summarized in the following result.

Remark 3.

We have assumed existence of in Theorem 3.1 and this is exploited in the resulting presentation of It is clear, however, that the case should safely be excluded. Indeed if was zero then the restriction about

belonging to the ball of radius around is ignored. Then

implies to minimize where is a negative random variable, under the only restriction that This is equivalent to ask to minimize

where stands for calculating the expected value under the “arbitrary”

actual distribution. This problem does not have a solution since for any specified such that we can find another such that as long as puts higher mass at the negative values of with a large magnitude.

It is also important to note that for the chosen in Theorem 3.1 the solution of the equation system for and is also required to satisfy the condition Finding precise conditions which must satisfy under a general nominal distribution seems to be very difficult. However, we can state that numerically, in all examples that we have tried, we have observed that if certain is found which “works”, then all values also work, i.e., for them, respective and satisfying the system of equations exist with the inequality

being satisfied.

Corollary 3.2.

Suppose that there exist , and such that

where

then is an optimal index tracking portfolio.

The proof of the Corollary is obtained by taking a limit as in Theorem 3.1.

Remark 4.

The main part of the numerical procedure of our method is the implementation of the solution of the nonlinear equation system from Theorem 3.1. We used MATLAB and applied the interior-point method for solving box-constrained nonlinear systems. Initial guesses for the solution were necessary to be chosen for the portfolio’s weights, and for the parameters and Uniform initial weights turned out to be working fine all the time. The initial weights for the remaining parameters required more careful choosing and experimentation. The ones that worked fine for our numerical experiments were and

4 Modified myopic robust index tracking

The discussion in Section 3.3 can be extended to cover a specific form of modified myopic robust index tracking problem. In the previous section we measured the quality of the index tracking by using the quadratic loss function since this is the typical choice in the portfolio tracking literature. This choice equally penalizes the performance of the portfolio whenever it deviates by the same magnitude irrespectively of whether the deviation is above or below the value of the index.

The main focus in de Paulo et al. (2010) is on formulating an optimization problem that represents a balancing of the trade-off between tracking error and excess return.

A different goal may be of interest in a robust setting. Typically, in the latter setting, the goal is to safeguard against worst-case scenarios and the solution obtained reflects this goal. Hence it is expected to give superior performance, especially in a downturn market. If for various reasons the investor still remains in the market during a downturn (for example, expecting that this downturn would be relatively short-lived, or because of limited liquidity), one would not be willing to penalize if the portfolio outperforms the index in such cases.

Obviously, a more reasonable choice to replace the loss to be used in such a situation would be based, for example, on a smooth approximation of the function

Other choices also make sense, for example Direct utilization of these types of functions makes a lot of sense since we do not really want to penalize when the portfolio happens to outperform the index.

However, there is a technical difficulty to overcome if we want to include such type of losses in our approach. It is related to the fact that the functions and are not smooth at the origin. If we would like to utilize the steps as in Theorem 3.1 and show that the Hessian is negative semi-definite, we need a convex twice differentiable loss function to replace Also, from a technical prospective, the gradient of should be possible to calculate, preferably in a closed form. We suggest the function with a suitably chosen small as approximation for For approximation of the expression from the literature (see e.g., Chen and Mangasarian (1995)) can be used and is known as “the neural networks smooth plus function”. Using these, the function in Theorem 3.1 can be replaced by or by respectively. The corresponding gradient of is to be replaced by the gradient of or and these are easily calculated by using the chain rule and the derivatives of one-dimensional argument for and Both derivatives of or w.r.t. the components of deliver smooth approximating functions. We prefer the first approximation since its second mixed derivatives appear to be varying more smoothly around the origin for small values of Elementary calculation of the integral gives the following approximations for the function :

| (14) |

Here denotes the cumulative distribution function of the univariate standard normal distribution, denotes the density and the function is defined as Having in mind the relationship (14) simplifies further to the explicit expression

| (15) |

Differentiating (14) delivers the resulting approximations for the derivatives of :

| (16) |

Of course, the approximations for the derivatives of are:

5 Numerical Analysis

In this section, we perform various numerical comparisons to illustrate the usefulness of our model. It is worth noting that there is some difference between the general theory (in particular, the statements in Section 3) and the way to illustrate the theory via examples. We stress that, as seen in Section 3, the main theoretical statement in Theorem 3.1 on the basis of which our numerical procedure is implemented, does not explicitly require calculation of the least favourable distribution in the Bregman ball; all that is needed is the radius of the ball. If we wanted to illustrate the full effect of the robustification theory on a particular example, we should ideally be able to calculate the least favourable distribution and simulate from it. Determining the least favourable distribution is very difficult even if the nominal distribution was multivariate normal. On the other hand, we know that the least favourable distribution is on the surface of the ball (since the Lagrange multiplier is not equal to zero). Hence, just for the purpose of generating illustrative examples, we have chosen a distribution that has the maximal allowed divergence from the nominal and is possible to deal with (e.g., in Example 5.1, we choose it to be multivariate normal with the same covariance matrix as the nominal but with a re-scaled mean). Of course, this distribution is not necessarily the least favourable though it is on the maximal allowable distance from the nominal distribution. This approach allows us to simulate our toy examples. We follow traditional approaches in the robustness literature where a contaminated neighbourhood is typically a neighbourhood of the multivariate normal distribution, e.g., Huber and Ronchetti (2009). For this reason, we choose our testing of the statements of Theorem 3.1 to involve perturbations of multivariate normal and of multivariate t. We are aware of the fact that these simulations represent a simplistic indicative study of the effect of the general statement of Theorem 3.1. A more comprehensive numerical work would be required to test our procedure by examining Bregman neighbourhoods of other nominal distributions of interest in finance. As this paper is more on the methodological side, such numerical work is beyond the scope of the presented research. We hope that the reader will still be able to get some insight about the usefulness of our approach by examining the presented numerical examples.

One more point to make is that the least favourable distribution corresponds to a pessimistic scenario that may not be the one that would actually happen hence our examples, by not directly simulating from it, hopefully still give useful insight in the performance of the robust procedure.

5.1 Performance Comparison via simulation: Index Tracking

We first compare the performance of the robust and the non-robust portfolio in the context of index tracking. Suppose that we have an index which is made up of five assets according to the following weight vector:

| (22) |

The expected return and the covariance matrix of these five assets are given by

| (33) |

We will use the first four assets to track this hypothetical index. The following example is used to demonstrate the comparison.

Example [Multivariate Normal (MVN)].

Suppose that the nominal distribution is a -dimensional multivariate normal distribution and an actual distribution is an -dimensional multivariate normal distribution which is on a Bregman divergence from the nominal. Fix , we assume and take , which results in for some .

We simulate returns from the nominal distribution to calculate the robust portfolio. The same number of simulations is used to draw samples from the actual distribution to make a comparison between the robust and non-robust portfolios. Several measures are used to accomplish the comparison. The first measure is the number of times (in percentage) that the robust case outperforms the non-robust case. We call this measure the Beating Time (BT). The larger the BT, the more times the robust portfolio outperforms the non-robust one. The out-performance is in the sense of a lower tracking error, where the tracking error (TE) is defined as

Here is a control (either robust or non-robust) applied to the tracking portfolio, denotes the return of the assets in the tracking portfolio, and denotes the return of the index. The second measure we apply to both controls is the expected tracking error (ETE). Obviously, the smaller the expected tracking error, the better the portfolio (on average). We also compare the performance of the robust and non-robust portfolios with the index, and introduce a measure called the expected excess of index (EEI), where the excess of index (EI) is defined as

Thus, a negative EI indicates the portfolio is beaten by the index. The EEI is the average of EI over the number of simulations performed.

| BT | ETE | EEI | |||||

|---|---|---|---|---|---|---|---|

| robust | non-robust | difference | robust | non-robust | difference | ||

| () | () | ||||||

| 0.1 () | 50.51 | 3.1055 | 3.1055 | 0.0000 | 24.8692 | 24.8728 | -0.0036 |

| 0.2 () | 51.67 | 3.2016 | 3.2017 | -0.0001 | 39.7446 | 39.7556 | -0.0110 |

| 0.5 () | 53.99 | 3.5174 | 3.5180 | -0.0006 | 68.8326 | 68.8753 | -0.0427 |

| 0.8 () | 55.25 | 3.8417 | 3.8431 | -0.0014 | 89.3307 | 89.4115 | -0.0808 |

| 1.0 () | 55.91 | 4.0573 | 4.0594 | -0.0021 | 100.6753 | 100.7832 | -0.1079 |

| 2.0 () | 58.25 | 5.1028 | 5.1099 | -0.0071 | 143.4931 | 143.7447 | -0.2516 |

| 5.0 () | 61.51 | 7.8510 | 7.8812 | -0.0302 | 219.2462 | 219.9450 | -0.6988 |

| BT | ETE | EEI | |||||

|---|---|---|---|---|---|---|---|

| robust | non-robust | difference | robust | non-robust | difference | ||

| () | () | ||||||

| 0.1 () | 52.10 | 3.2702 | 3.2702 | 0.0000 | -47.5911 | -47.5978 | 0.0067 |

| 0.2 () | 54.20 | 3.4338 | 3.4340 | -0.0002 | -62.4633 | -62.4805 | 0.0172 |

| 0.5 () | 56.89 | 3.8817 | 3.8827 | -0.0010 | -91.5435 | -91.6003 | 0.0568 |

| 0.8 () | 58.00 | 4.2989 | 4.3011 | -0.0022 | -112.0351 | -112.1365 | 0.1014 |

| 1.0 () | 58.56 | 4.5659 | 4.5691 | -0.0032 | -123.3760 | -123.5082 | 0.1322 |

| 2.0 () | 60.64 | 5.8053 | 5.8149 | -0.0096 | -166.1784 | -166.4697 | 0.2913 |

| 5.0 () | 63.36 | 8.8956 | 8.9325 | -0.0369 | -242.6700 | -241.8988 | 0.7712 |

In this example, both the nominal and the actual distribution are MVN. From (6), it is easy to see that the Bregman divergence between these two distributions is given by

This then implies

which allows us to get the relevant .

It can be seen that in both Table 1 and Table 2, the robust portfolio

outperforms the non-robust one when BT or ETE is used as a comparison measure. In contrast, when EEI is used, if there is a loss made, i.e., the portfolio underperforms the index, the robust portfolio safeguards and performs better. This leads to a positive difference in

the last column of Table 2. When there is a profit made, the opposite happens and a negative difference

is recognized as shown in Table 1.

Recall that the parameter controls the amount of robustness applied: the smaller the , the less robustness effect. This belief is confirmed from the results obtained in Table 3 and Table 4 when is taken to be 0.05. Attention should be directed at comparing the pairs: Table 3 with Table 1, and Table 4 with Table 2, respectively. It becomes apparent that, when the ball radius is small (hence no need of significant robustification), the performance is about the same no matter whether or was used. However, when is increased to, say, 2 or 5, more robustification is required and using the higher value of proves to bring a higher percentage of BT.

| BT | ETE | EEI | |||||

|---|---|---|---|---|---|---|---|

| robust | non-robust | difference | robust | non-robust | difference | ||

| () | () | ||||||

| 0.1 () | 50.63 | 3.1101 | 3.1101 | 0.0000 | 25.7668 | 25.7716 | -0.0048 |

| 0.2 () | 51.36 | 3.2124 | 3.2125 | -0.0001 | 41.0720 | 41.0879 | -0.0159 |

| 0.5 () | 52.38 | 3.5506 | 3.5515 | -0.0009 | 71.1951 | 71.2628 | -0.0677 |

| 0.8 () | 53.09 | 3.9019 | 3.9043 | -0.0024 | 92.6362 | 92.7703 | -0.1341 |

| 1.0 () | 53.53 | 4.1379 | 4.1416 | -0.0037 | 104.5987 | 104.7813 | -0.1826 |

| 2.0 () | 55.27 | 5.3099 | 5.3228 | -0.0129 | 150.5243 | 150.9677 | -0.4434 |

| 5.0 () | 58.17 | 8.6066 | 8.6615 | -0.0549 | 235.8081 | 237.0205 | -1.2124 |

| BT | ETE | EEI | |||||

|---|---|---|---|---|---|---|---|

| robust | non-robust | difference | robust | non-robust | difference | ||

| () | () | ||||||

| 0.1 () | 52.52 | 3.2788 | 3.2789 | -0.0001 | -48.4876 | -48.4966 | 0.0090 |

| 0.2 () | 53.38 | 3.4506 | 3.4509 | -0.0003 | -63.7882 | -63.8128 | 0.0246 |

| 0.5 () | 54.05 | 3.9254 | 3.9270 | -0.0016 | -93.8985 | -93.9878 | 0.0893 |

| 0.8 () | 54.70 | 4.3738 | 4.3776 | -0.0038 | -115.3283 | -115.4953 | 0.1670 |

| 1.0 () | 55.10 | 4.6639 | 4.6695 | -0.0056 | -127.2841 | -127.5062 | 0.2221 |

| 2.0 () | 56.78 | 6.0434 | 6.0606 | -0.0172 | -173.1823 | -173.6927 | 0.5104 |

| 5.0 () | 59.40 | 9.7240 | 9.7904 | -0.0664 | -258.4161 | -259.7455 | 1.3294 |

5.2 Performance Comparison via simulation during market downturn

In this section, we illustrate the effect of using the loss function from Section 4 on two examples: the first example involves the multivariate normal as a nominal distribution and the second example deals with multivariate as a nominal distribution.

Example [Nominal multivariate normal].

Given that all components of the chosen mean vector of the multivariate normal are positive, the single scalar multiplication with a value of represents a market downturn scenario. As is related to the radius a larger value of pushes further in the negative territory. The number of simulations used to calculate the robust portfolio and to assess the performance was kept at as a sufficient stabilization of the results was already appearing at this number of simulations.

We applied the smoothed loss function from Section 4 with and We varied the radius through the range as before and registered the percentage of cases in which the Bregman-based portfolio outperformed the non-robust one. (The non-robust portfolio was defined as minimizing the same loss but without considering a neighbourhood around the nominal distribution).

As expected, the percentage of cases in which the robust portfolio was not worse than the non-robust one was quite large. The results are presented in Table 5.

Similar results to the ones presented in Table 5 can be obtained when was used as a smoothed loss function. The results clearly outline the significant benefits of using the robust portfolio in a market downturn scenario. Of course, this is to be expected by the nature of the optimization problem that is solved in the robust setting. We note that in Table 5 the cases where both portfolios deliver a zero value for the loss have been counted towards the percentage BT (since these cases are considered as “not worse” for the robust portfolio). One may suggest that it might be fairer to exclude theses cases from the comparison (i.e., to consider in what proportion of cases the robust portfolio delivered a truly better outcome). It would be expected that this proportion would be smaller but still high enough. Indeed this expectation is confirmed by the results that are presented in Table 6.

| BT | ETE | |||

|---|---|---|---|---|

| robust | non-robust | difference | ||

| () | ||||

| 0.1 () | 81.24 | 58.5587 | 58.9210 | -0.3623 |

| 0.2 () | 84.06 | 52.3295 | 52.9541 | -0.62464 |

| 0.5 () | 88.65 | 41.2324 | 42.3339 | -1.1015 |

| 0.8 () | 91.46 | 34.5631 | 36.0577 | -1.4946 |

| 1.0 () | 92.72 | 31.1530 | 32.8128 | -1.6598 |

| 2.0 () | 96.28 | 20.3921 | 22.4897 | -2.0976 |

| 5.0 () | 99.11 | 8.36022 | 10.5283 | -2.1681 |

| BT | ETE | |||

|---|---|---|---|---|

| robust | non-robust | difference | ||

| () | ||||

| 0.1 () | 58.34 | 58.5587 | 58.9210 | -0.3623 |

| 0.2 () | 62.00 | 52.3295 | 52.9541 | -0.6246 |

| 0.5 () | 68.65 | 41.2324 | 42.3339 | -1.1015 |

| 0.8 () | 72.98 | 34.5631 | 36.0577 | -1.4946 |

| 1.0 () | 75.20 | 31.1530 | 32.8128 | -1.6598 |

| 2.0 () | 82.69 | 20.3921 | 22.4897 | -2.0976 |

| 5.0 () | 91.66 | 8.36022 | 10.5283 | -2.1681 |

Example [Multivariate t (MVT)].

Suppose now that the nominal distribution is a -dimensional multivariate t distribution and an actual distribution is taken to be an

-dimensional multivariate t distribution

such that ,

for some .

First, we note that a multivariate distribution has a density (see for example, (Nadarajah and Kotz, 2008, p99)):

| (34) |

We remind the reader that the matrix in (34) is not the covariance matrix of the multivariate distribution, but the covariance matrix is defined for every and can be expressed as

We again applied the smoothed loss function from Section 4 with and We present results below for the case of 10 degrees of freedom but we experimented with many other values for the degrees of freedom and the results follow the same pattern. We varied the values of through the range and calculated the resulting radius numerically. The portfolio weights generally stabilized with fewer than the 1,000,000 simulations we performed. As before, we registered the percentage of cases in which the Bregman-based portfolio was not worse than the non-robust portfolio with respect to the loss . (The non-robust portfolio was defined as minimizing the same loss but without considering a neighbourhood around the nominal distribution.)

The results are summarized in Table 7 and similar results can be obtained when is used as a smooth loss function.

As before, an additional table is provided for the market downturn scenario, where we exclude “zero” loss results where the robust and non-robust strategies performed equally. As shown in Table 8, the proportion BT was again in favor of the robust portfolio.

The results of this section clearly outline the significant benefits of using the robust tracking portfolio in a market downturn scenario also for the case where the nominal distribution is heavy-tailed (such as the multivariate with 10 degrees of freedom). When the radius is zero and the robust and non-robust strategies coincide, hence, up to a negligible numerical effect, the percentage was about in Table 7 and about in Table 8. As starts getting smaller, the advantage of the robust approach starts popping up and is increasing monotonically when the magnitude of increases.

| k, | BT | ETE | ||

|---|---|---|---|---|

| robust | non-robust | difference | ||

| () | ||||

| 74.0965 | 72.9088 | 72.9100 | -0.0012 | |

| 75.6374 | 67.4686 | 67.5311 | -0.0625 | |

| 77.1499 | 62.0974 | 62.4280 | -0.3306 | |

| 78.5679 | 56.8677 | 57.5992 | -0.7315 | |

| 80.1557 | 51.8374 | 53.0417 | -1.2043 | |

| 81.8112 | 47.0439 | 48.7512 | -1.7073 | |

| 83.5051 | 42.5242 | 44.7248 | -2.2006 | |

| 88.1117 | 30.7946 | 34.1600 | -3.3655 | |

| k, | BT | ETE | ||

|---|---|---|---|---|

| robust | non-robust | difference | ||

| () | ||||

| 50.77 | 72.9088 | 72.9100 | -0.0012 | |

| 51.55 | 67.4686 | 67.5311 | -0.0625 | |

| 52.66 | 62.0974 | 62.4280 | -0.3306 | |

| 53.50 | 56.8677 | 57.5992 | -0.7315 | |

| 54.53 | 51.8374 | 53.0417 | -1.2043 | |

| 55.68 | 47.0439 | 48.7512 | -1.7073 | |

| 56.93 | 42.5242 | 44.7248 | -2.2006 | |

| 60.72 | 30.7946 | 34.1600 | -3.3655 | |

5.3 Real data example

The simulation method offers the right vehicle to examine the merits of our methodology. This is because only via simulations (where we know the nominal, the actual model and the true radius of contamination) we can sense the effects of our methodology. However, an indirect way to investigate these effects would be to investigate the out-of-sample performance on some real data.

We are not aware of another method in the literature for robust index tracking (in the sense we used it here as robustness

to deviations from a nominal model), with which to compare. Hence we illustrate the performance of our method on data from the Hang Seng index (Hong Kong).

This index contains 31 stocks. The paper Beasley et al. (2003) contains many data sets that have been refereed to since then in other papers. In particular, Guastaroba and Speranza (2012), too, uses these data sets. The description of the data sets and a way to access it can be found on page 60 of Guastaroba and Speranza (2012).

We are following the same design as done in Guastaroba and Speranza (2012), and apply the same experimental setting as described in Table 1 in their paper. For each stock, 291 consecutive weekly prices are provided. From these, the first 104 weekly prices are chosen as in-sample observations, i.e. the initial time period is The the next weeks are set to be the out-of-sample (or validation) period.

Based on the testing data, we used the MATLAB procedure stepwiseglm to extract 12 stocks to include in our portfolio. This procedure creates a linear regression model

using the stepwise regression approach by adding or removing predictors from the set of 31 stocks to model the response (i.e., the index value in our case).

Admittedly, this may not be the best way to choose stocks to be included in the index tracking portfolio but it is a reasonable way of doing it and, as discussed in the introduction, we are unable to discuss rigorously the problem of selecting the “optimal subset” selection in this paper. As a result of applying the MATLAB procedure, we obtained stocks with indices

which we included in our portfolio.

The Table 9 below gives the estimated correlations matrix of the returns of the chosen 12 stocks (columns 1 to 12) and the return of the index (column 13), rounded by two decimal places.

| 1 | 0.60 | 0.66 | 0.69 | 0.64 | 0.76 | 0.83 | 0.61 | 0.31 | 0.70 | 0.56 | 0.69 | 0.82 |

| 0.60 | 1 | 0.63 | 0.64 | 0.51 | 0.65 | 0.67 | 0.67 | 0.32 | 0.59 | 0.47 | 0.57 | 0.77 |

| 0.66 | 0.63 | 1 | 0.80 | 0.67 | 0.74 | 0.73 | 0.69 | 0.35 | 0.67 | 0.67 | 0.76 | 0.86 |

| 0.69 | 0.64 | 0.80 | 1 | 0.70 | 0.81 | 0.75 | 0.73 | 0.33 | 0.73 | 0.68 | 0.78 | 0.89 |

| 0.64 | 0.51 | 0.67 | 0.70 | 1 | 0.71 | 0.65 | 0.64 | 0.37 | 0.64 | 0.69 | 0.64 | 0.82 |

| 0.76 | 0.65 | 0.74 | 0.81 | 0.71 | 1 | 0.72 | 0.70 | 0.27 | 0.77 | 0.64 | 0.74 | 0.88 |

| 0.83 | 0.67 | 0.73 | 0.75 | 0.65 | 0.72 | 1 | 0.66 | 0.27 | 0.71 | 0.60 | 0.78 | 0.87 |

| 0.61 | 0.67 | 0.69 | 0.73 | 0.64 | 0.70 | 0.66 | 1 | 0.35 | 0.69 | 0.58 | 0.69 | 0.84 |

| 0.31 | 0.32 | 0.35 | 0.33 | 0.37 | 0.27 | 0.27 | 0.35 | 1 | 0.33 | 0.33 | 0.28 | 0.41 |

| 0.70 | 0.59 | 0.67 | 0.73 | 0.64 | 0.77 | 0.71 | 0.69 | 0.33 | 1 | 0.54 | 0.73 | 0.83 |

| 0.56 | 0.47 | 0.67 | 0.68 | 0.69 | 0.64 | 0.60 | 0.58 | 0.33 | 0.54 | 1 | 0.62 | 0.76 |

| 0.69 | 0.57 | 0.76 | 0.78 | 0.64 | 0.74 | 0.78 | 0.69 | 0.28 | 0.73 | 0.62 | 1 | 0.86 |

| 0.82 | 0.77 | 0.86 | 0.89 | 0.82 | 0.88 | 0.87 | 0.84 | 0.41 | 0.83 | 0.76 | 0.86 | 1 |

The correlation matrix is clearly non-diagonal. It has one outstanding large eigenvalue (8.93689), with the smallest eigenvalue being 0.0051 and the remaining ones are all larger than 0.0051 but smaller than one.

Replacing expected values by empirical averages in the main Theorem 3.1, we are able to find the optimal weighting for our stock selection:

(rounded up to the fourth decimal). The values for the other parameters were: These wights should be compared to the optimal non-robust weights:

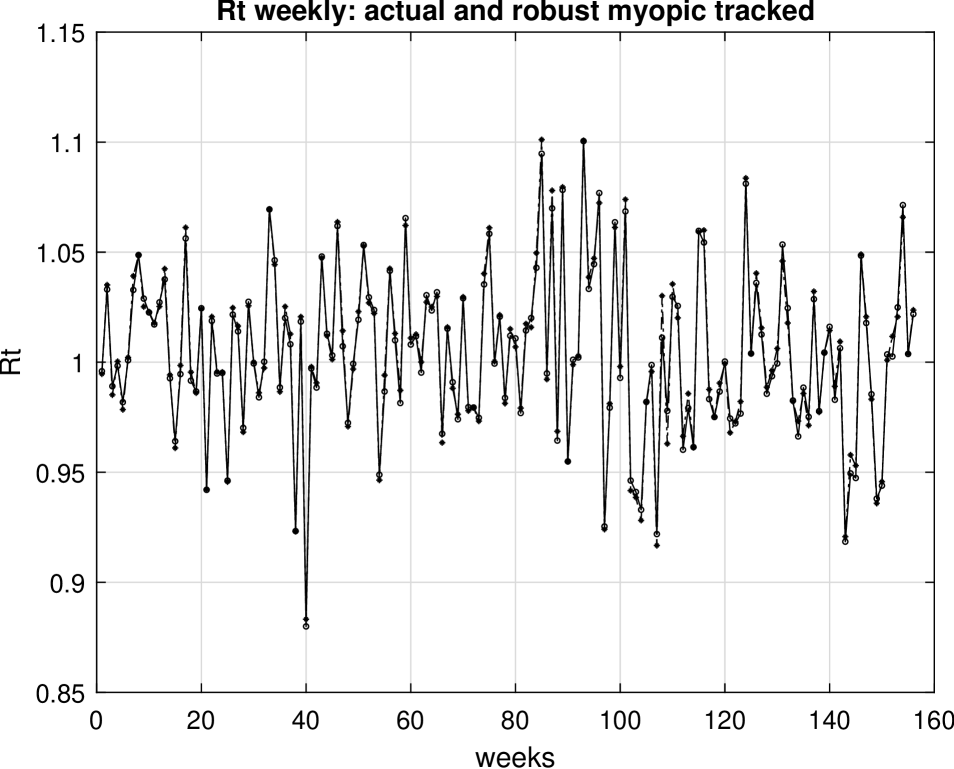

Following the spirit of myopic index tracking, we then applied a moving window of size 104 when working on the remaining out-of-sample 52 data points. Each time, a new data point was added the earliest one was deleted when re-calculating the weights in the next time point. That is, at each time point after the sliding window contained the last 104 time points when re-calculating the weights. The predicted weights form time point were used to update the portfolio weights to be applied at time point We applied the non-robust approach, too, and compared the outcomes of the two procedures. The ETE values for the robust and non-robust approach were almost identical on the testing data set: for robust versus for the non-robust but the robust approach outperformed the non-robust in the out-of-sample performance ( for robust versus for non-robust). The important quantity of interest, BT, was also in favour of the robust approach again in the out-of-sample performance (27 out of 52) when the quadratic loss was used. This increased to 42 out of 52, i.e., , when the of Equation 15, with was used. These outcomes are in line with the heuristic of the methodology and with the simulations results of Sections 5.1 and 5.2. Figure 1 illustrates the accuracy of the approximation of the vector via across all 156 time points. It is perhaps not surprising that we obtain such an excellent index tracking performance as the proportion of chosen stocks (12 out of 31) is relatively high, and in the same setting as in Guastaroba and Speranza (2012), two years of in-sample training and a subsequent 12 months of out-of-sample testing has been applied.

6 Discussion

Various extensions of the suggested approach are of interest and are left for further research. As is to be expected, the robustness effect depends on more than one factor. The value of the “radius of contamination” , and the

model distribution, all have an effect on performance and a thorough investigation of their interplay needs to be addressed in the future. Obviously, the value of the chosen radius of the divergence ball is strongly related to the amount of contamination around the nominal model. This information, especially in realistic financial portfolios, is difficult to access. However our simulations lead us to believe that even with a slightly miss-specified value of one can still enjoy the improvement delivered by the robust procedure.

Another adjustment parameter is the value in the definition of the divergence. As pointed by Basu et al. (1998), there is no universal way of selecting it. It becomes apparent that the choices of and must be inter-related. In simplistic situations, recommendations in this paper about the choice of are given as a way of compromise by fixing an acceptable level of efficiency loss for gaining robustness, but a thorough study of the issue is lacking. This represents an avenue for future research.

Another important question is how to measure the quality of the index tracking. We have focused on the quadratic loss function since this is the typical choice in the portfolio tracking literature. This choice equally penalizes the performance of the portfolio whenever it deviates by the same magnitude irrespectively of whether the deviation is above of below the value of the index. A more reasonable choice of loss can be based on the functions and discussed in Section 4. Using such type of loss functions delivers a better performance in a clear downturn market scenario as shown in Section 5. However, in alternative mixed scenarios, and since there is often no clear separation between market upturn and market downturn in reality, using this loss may be disadvantageous for the investor as it may reduce their average gains. Further research in this direction will also be beneficial. A thorough comparison with the approach from Roll (1992) is on our agenda.

Finally, the numerical examples in this paper illustrated effects when the actual distribution is on a maximal allowable distance from the nominal. This is not necessarily the least-favorable distribution: the least favorable distribution will never be known in practice and in the theoretical discussion we can only get it in the semi-closed form (11) as a part of an implicit solution of an equation system. Despite this, the actual distributions we used for numerical illustrations still give a good proxy of the expected effect. Of course, in our theoretical derivations, we did not need the explicit form of the least-favorable distribution and the derivations in Section 3.3 remain universally valid. The mean vector and the covariance matrix used in our simulations were selected to be close to the daily returns in the Australian share market. For daily returns, assuming multivariate normality is often appropriate. However, when the returns are collected from a longer time horizon or when the nominal distribution itself is different from the multidimensional normal, the benefits of the robust portfolio in the case of quadratic loss may be more or less spectacular depending on how heavy-tailed the nominal distribution turns out to be. In this case, explicit formulae for the divergence, such as, for example, (5), would rarely be available. This does not prevent our methodology from working- the required expected values under the nominal distribution in the main Theorem 3.1 are to be replaced with their empirical counterparts. More numerical work could demonstrate the advantages of the methodology in such heavy-tailed cases.

As mentioned in the introduction, we do not discuss the approaches to sparse index tracking portfolio selection in this paper. The combined requirement for sparsity and robustness in index tracking leads to interesting and challenging optimization problems that are left as a future research avenue.

7 Appendix

7.1 Justification of (5) and (6)

7.2 Justification of the solution to the outer optimization problem

We notice that

We write the Lagrangian of the outer optimization problem.

The first order condition can then be obtained:

| (35) |

To check that the solution of the above equation is optimal, we calculate the Hessian. For , we see that

Since ,

it is easy to see that the Hessian is negative semi-definite. As a consequence, we have verified that the solution of (7.2) is optimal, and we will denote it as . This finishes the proof of Theorem 3.1.

Funding

This work was supported by the Australian Research Council’s Discovery Project funding scheme (Project DP160103489).

References

- Amari (2016) Amari,Shun-ichi, 2016. Information Geometry and Its Applications. Springer, Japan.

- Amari & Cichocki (2010) Amari, S. & Cichotski, A. (2010). Information geometry of divergence functions. Bulletin of the Polish academy of scinces. Tehcnical sciences, 58 (1), 183–195.

- Andriosopoulos and Nomikos (2014) Andriosopoulos, K. & Nomikos, N. (2014). Performance replication of the Spot Energy index with optimal equity portfolio selection: Evidence from the UK, US and Brazilian markets. European Journal of Operational Research 234 (2), 571–582.

- Banerjee et al. (2005) Banerjee, A.& Merugu, S. & Dhillon, I. & Ghosh, J. (2005). Clustering with Bregman Divergences. Journal of Machine Learning Research 6, 1705–1749.

- Basu et al. (1998) Basu, A., & Harris, N., & Hjort, N., & Jones, M.C. (1998). Robust and efficient estimation by minimizeing a denisty power divergence. Biometrika 85 , 549–559.

- Beasley et al. (2003) Beasley J. E., A. & Meade, N. & Chang T.J. (2003). An evolutionary heuristic for the index tracking problem. European Journal of Operational Research 148 (3), 621–643.

- Benidis et al. (2018) Benidis, K., & Feng, Y., & Palomar, D. (2018) Sparse Portfolios for High-Dimensional Financial Index Tracking. IEEE Transactions on Signal Processing 66 (1), 155-170.

- Ben-Tal et al. (1988) Ben-Tal, A. & Teboulle, M. & Charnes A. (1988). The role of duality in optimization problems involving entropy functionals with applications to information theory. Journal of Optimization Theory and Applications 58 (2), 209–223.

- Blanchet et al. (2019) Blanchet, J., Lam, H., Tang, Q. and Yuan, Z. (2019). Robust actuarial risk analysis. North American Actuarial Journal 23 (1), 33-63.

- Boyd and Vandenberghe (2004) Boyd, S. & Vandenberghe, L. (2004). Convex Optimization. (Seventh printing with corrections 2009) Cambridge University Press

- Bregman (1967) Bregman, L. M. (1967). The relaxation method of finding the common points of convex sets and its application to the solution of problems in convex programming. USSR Computational Mathematics and Mathematical Physics 7 (3), 200–217.

- Canakgoz and Beasley (2008) Canakgoz, N. A.& Beasley, J. E. (2009). Mixed-integer programming approaches for index tracking and enhanced indexation. European Journal of Operational Research 196 (1), 384–399.

- Chen and Mangasarian (1995) Chen, C. and Mangasarian, O. (1995). Smoothing methods for convex inequalities and linear complementarity problems. Mathematical Programming 71, 51–69.

- Chiam et al. (2013) Chiam S. C., A. & Tan, K.C. & Mamun A.A. (2013). Dynamic index tracking via multi-objective evolutionary algorithm. Applied Soft Computing 13 (7), 3392–3408.

- Cichocki and Amari (2010) Cichocki, A. & Amari, S. (2018). Families of Alpha- Beta- and Gamma- Divergences: Flexible and Robust Measures and Similarities. Entropy 12, 1532–1568.

- Dey and Juneja (2010) Dey, S. & Juneja, S. (2010). Entropy approach to incorporate fat tailed constraints in financial models. SSRN electronic journal. https://papers.ssrn.com/sol3/papers.cfm?abstract_id=1647048, Tata Institute of Fundamental Research Mumbai, India (last download 27 11 2017).

- de Paulo et al. (2010) de Paulo, W. L. & de Oliveira, E. M. & Vosta, O. L. do V. (2016). Enhanced index tracking optimal portfolio selection. Finance Research Letter 16, 92–102.

- Dose and Cincotti (2005) Dose, C. & Cincotti, S. (2005). Clustering of financial time series with application to index and enhanced index tracking portfolio. Physica A: Statistical Mechanics and its Applications 355 (1), 145–151.

- Fabozzi (2007) Fabozzi, F. J. (2007). Robust portfolio optimization and management. Wiley, New Jersey.

- Filippi et al. (2016) Filippi, C. & Guastaroba, G. & Speranza, M. (2016). A heuristic framework for the bi-objective enhanced index tracking problem. Omega 65, 122–137.

- Gaivoronski et al. (2005) Gaivoronski, A. A. & Krylov, A. & Wijst, N. van der (2005). Optimal portfolio selection and dynamic benchmark tracking. European Journal of Operational Research 163 (1), 115–131.

- Glasserman and Xu (2014) Glasserman, P. & Xu, X. B. (2014). Robust risk measurement and model risk. Quantitative Finance 14 (1), 29–58.

- Gnägi and Strub (2020) Gnägi,M. & Strub, O. (2020). Tracking and outperforming large stock-market indices. Omega, 90, 101999.

- Goh and Dey (2014) Goh, G. & Dey, D. (2014). Bayesian model diagnostics using functional Bregman divergence. Journal of Multivariate Analysis 124, 371–383.

- Guastaroba et al. (2016) Guastaroba, G. & Mansini, R. & Ogryczak W. & Speranza, M.G. (2016). Linear programming models based on Omega ratio for the enhanced index tracking problem. European Journal of Operational Research 251 (3), 938–956.

- Guastaroba and Speranza (2012) Guastaroba, G. & Speranza, M.G. (2012). Kernel Search: An application to the index tracking problem. European Journal of Operational Research 217 (1), 54–68.

- Huber and Ronchetti (2009) Huber, P.& Ronchetti, E. (2009). Robust Statistics, 2nd Edition. Wiley, New York.

- Lejeune (2012) Lejeune, M. A. (2012). Game theoretical approach for reliable enhanced indexation. Decision Analysis 9 (2), 146–155.

- Maginn et al. (2007) Maginn, J. L. & Tuttle, D. L. & McLeavey, D. W. & Pinto, J. E. (2007). Managing Investment Portfolios. (3rd Edition) John Wiley & Sons, Inc.

- Meade and Salkin (1990) Meade, N. & Salkin, G. R.(1990). Developing and Maintaining an Equity Index Fund. The Journal of Operational Research Society 41 (7), 599–607.

- Mihoko & Eguchi (2002) Mihoko, M. & Eguchi, S. (2002). Robust Blind Source Separation by Beta Divergence. Neural Computation, 14, 8, 1859–1886.

- Montfort et al. (2008) Montfort, K. V. & Visser, E. & Draat, L. F. V.(2008). Index Tracking by Means of Optimized Sampling. The Journal of Portfolio Management Winter 34 (2), 143–152.

- Nadarajah and Kotz (2008) Nadarajah, S. & Kotz, S. (2008). Estimation Methods for the Multivariate t Distribution. Acta Applicandae Mathematicae 102 (1), 99–118.

- Penev and Naito (2018) Penev, S. & Naito, K. (2018). Locally robust methods and near-parametric asymptotics. Journal of Multivariate Analysis, 167, 395–417

- Penev and Prvan (2016) Penev, S. & Prvan, T. (2016). Robust estimation in structural equation models using Bregman and other divergences with t-centre approach to estimate the covariance matrix. ANZIAM Journal, 56, (Proceedings CTAC2014), C339-C354.

- Poczos and Schneider (2011) Poczos B., A. & Schneider, J. (2011). On the estimation of -divergences. Journal of Maching Learning Research: Workshops and Conferences 15, 609–617.

- Roll (1992) Roll, R. (1992). A mean/variance analysis of tracking error. The Journal of Portfolio Management 18, 13–22.

- Strub and Baumann (2018) Strub, O. & Baumann, P. (2018). Optimal construction and rebalancing of index-tracking portfolios. European Journal of Operational Research 264 (1), 370–387.

- Vemuri et al. (2011) Vemuri, B. & Liu, M. & Amari, S-I. & Nielsen, F. (2011). Total Bregman Divergence and Its Applications to DTI Analysis. IEEE Transactions on Medical Imaging, 30, 475-483.