Optimal Investment with Correlated Stochastic Volatility Factors 111Data sharing is not applicable to this article as no new data were created or analyzed in this study.

Maxim Bichuch

Department of Mathematics, SUNY at Buffalo, 244 Mathematics Building

Buffalo, NY 14260, USA, email: mbichuch@buffalo.edu. Work is partially supported by NSF grant DMS-1736414. Research is partially supported by the Acheson J. Duncan Fund for the Advancement of Research in Statistics.Jean-Pierre Fouque

Department of Statistics and Applied Probability,

South Hall 5504,

University of California

Santa Barbara, CA 93106

fouque@pstat.ucsb.edu. Work supported by NSF grant DMS-1814091.

Abstract

The problem of portfolio allocation in the context of stocks evolving in random environments, that is with volatility and returns depending on random factors, has attracted a lot of attention. The problem of maximizing a power utility at a terminal time with only one random factor can be linearized thanks to a classical distortion transformation. In the present paper, we address the situation with several factors using a perturbation technique around the case where these factors are perfectly correlated reducing the problem to the case with a single factor. Our proposed approximation requires to solve numerically two linear equations in lower dimension instead of a fully non-linear HJB equation. A rigorous accuracy result is derived by constructing sub- and super- solutions so that their difference is at the desired order of accuracy. We illustrate our result with a particular model for which we have explicit formulas for the approximation. In order to keep the notations as explicit as possible, we treat the case with one stock and two factors and we describe an extension to the case with two stocks and two factors.

The portfolio optimization problem was first introduced and studied in the continuous-time framework in [18, 19], which provided explicit solutions on how to trade stocks and/or how to consume so as to maximize one’s utility, with risky assets following the Black-Scholes-Merton model (that is, geometric Brownian motions with constant returns and constant volatilities), and when the utility function is of specific types (for instance, Constant Relative Risk Aversion (CRRA)).

Stochastic volatility models have been widely studied over the last thirty years in the context of option pricing and the presence of several factors driving volatility has been well documented (see for instance [10], [13] and references therein). In general settings, the models are intractable and often asymptotic solutions are sought, see e.g. [21], [11], [12], [6].

In a general setting, [17] showed existence and uniqueness of an optimal strategy using the duality approach.

As an alternative approach, in a Markovian setting, the portfolio optimization problem with factors driving returns and volatility can be solved directly by describing it as a solution to an HJB equation with terminal condition given by the utility function.

Example of the latter approach in a portfolio optimization problem with multiscale factor models for risky assets include [14], where return and volatility are driven by fast and slow factors.

Specifically, the authors heuristically derived the asymptotic approximation to the value function and the optimal strategy

for general utility functions. This analysis is complemented in [7] and in [8] in a non-Markovian context. The multiscale feature is essential to be able to consider multiple factors, because each factor requires a unique time scale.

The analysis simplifies considerably in the case of a single factor and power utilities thanks to a distortion transformation which linearizes the problem (see [22], [14], [8]).

Our aim in this paper is to solve a problem with multiple factors of the same time scale. We do so by considering the case with multi factors and power utility as a perturbation problem around the case where the factors are perfectly correlated which reduces the problem to solving linear problems. Additionally, we find a “nearly-optimal” strategy, among all admissible strategies, without limiting them to strategies that asymptotically a-priori converge to the zeroth order strategy. The “nearly-optimal” strategy, if followed, produces an expected utility of the terminal wealth matching the value function at both zeroth and first order asymptotic expansion.

The main idea of this paper is to first calculate a heuristic asymptotic expansion in the correlation parameter. Then, based on this expansion, we derive a verification result for the HJB equation, which in turn, allows us to bound the value function from above and below similar to the method used e.g. in [2] and [3]. This procedure also produces a “nearly-optimal” strategy, and shows that the expected utility of the terminal wealth associated with this strategy is also within the same bounds as the value function.

The rest of the paper is structured in the following way. In Section 2, we study in details the case of investments in one stock and a risk-free account where the returns and volatility of the stock are driven by two factors. Our asymtotics around the case of perfect correlation between these two factors reveals a simple correction to the value function, which takes into account an imperfect correlation as well as a simple strategy which generates the corrected value function.

A proof of this accuracy is given in Section 3.

In Section 4, we extend the model studied in [4] which admits explicit formulas and enables us to illustrate the accuracy of our approximation.

Finally, to demonstrate that our approach generalizes to the case with multi assets, we consider in Section 5.1 two assets driven by two factors nearly fully correlated. We also extend the model of [4] in that case and we discuss the difference with the models considered in [1].

2 Models with one Stock and two Factors

We consider a model with a stock price driven by two correlated stochastic volatility factors:

(1)

(2)

The three Brownian motions and are defined on a filtered probability space

We assume that the two Brownian motions are correlated according to , and that they are correlated to the Brownian motion according to with constant coefficients such that and

(3)

Throughout the paper, we work under standing classical hypotheses on the coefficients of the system (1)-(2) ensuring existence and uniqueness of a strong solution.

We assume also that the market contains a bond, that carries zero interest rate for convenience. Let be the number of shares of stock held at time . Thus, the evolution of the wealth process following the self-financing strategy is given by:

(4)

and the value function of the optimal investment problem with terminal time and utility is the following:

(5)

where denotes the conditional expectation , and the supremum is taken over all admissible Markovian strategies such that stays nonnegative for all given , and satisfy the integrability condition

(6)

In this paper we consider the case with utility functions being of power type:

(7)

Define the differential operators

(8)

(9)

The value function satisfies:

(10)

(11)

A related problem with power utility of consumption and several factors is studied in [15] where it is proved that the associated HJB equation admits a classical solution.

Maximizating over gives:

(12)

where denotes a derivative with respect to

Substituting (12) into (10), it follows that

(13)

where the Sharpe ratio is defined by

We proceed in the next section to solve the problem when the two factors are perfectly correlated. It turns out that this solution follows [7]. We then compute the first order perturbation adjustment, around the perfectly correlated case. In Section 3, using these zero and first order perturbations, we construct sub- and super-solutions to the original PDE (13), and rigorously show the error of the constructed approximation.

2.1 Transformation of the Non-linear HJB Equation

We perform a distortion transformation of the HJB equation (13) for the value function , as follows. Fix and consider

(14)

Then, thanks to the power utility scaling, must satisfy:

(15)

(16)

(17)

where

we denote

(18)

We have one degree of freedom, namely , and

in order to cancel the non-linear terms, one must have

(19)

which can be achieved only if and , that is when the two factors and are perfectly correlated.

So we digress a little to review that case.

2.2 Fully Correlated Factors

We start by recalling the result from [14] as applied to our case. More specifically, in the case of fully correlated factors we are able to easily adapt the computations there as follows.

Let us temporarily assume that , then, condition (3) forces us to also assume that , with .

We consider the “distortion transformation” used in [22] and [14]:

(20)

where the superscript indicates that this function will be the zeroth order in the asymptotics presented in the following section.

The function satisfies

and is given by (9) with .

Note that in this case, we may assume that , and we get a Feynman–Kac type formula:

(27)

where is defined so that

(28)

is a standard Brownian motion under it.

2.3 Asymptotics Around the Fully Correlated Case

We now go back to the general correlation structure (3) and the non-linear HJB equation (15). Our goal is to expand around the fully correlated case when , and , presented in the previous section.

Accordingly, we now assume that have the following form:

(29)

where and

is a small parameter, , small enough to ensure a proper covariance structure satisfying (3). Indeed, (3) then becomes:

(30)

for , small enough.

Consider the ansatz

(31)

where the exponent is given by (23): .

Plugging this ansatz in the HJB equation (13) and canceling terms of zero order in gives that the function satisfies (24) and, therefore, is given by (27).

Cancelling the terms of order one in , we deduce that the function must satisfy:

We now consider a zeroth order approximation to given in (12), by substituting the zeroth order approximation for from (31), namely, , and by using the zeroth order approximation from (29). We obtain

(37)

Note that , and therefore once we show the appropriate integrability conditions in Corollary 2, it will follows that is an admissible strategy.

Next, we consider the value

(38)

obtained by following the strategy in (4). It satisfies the linear equation:

(39)

(40)

Consistent with the previous distortion transformation (14) letting

(41)

it follows that solves:

(42)

(43)

(44)

A classical regular expansion argument for PDEs (as in [14][Section 6.3.2] for instance) shows that

(45)

where the function and are exactly those obtained in the previous section in (24) and (32) respectively. Therefore, up to the first order in , is identical to expanded heuristically in (31). Once we prove in Section 3 that the expansion (31) for is accurate, we will also be able to conclude that

the strategy given by (37) generates up to order the value given by (5) or (10).

3 Proof of Accuracy

We now go back to the general case as in Section 2. The goal is to make rigorous the previous heuristic results. In other words, we prove that the expansion in (31) is correct. Moreover, as explained at the end of Section 2.3, we justify that the zeroth order strategy from (37) indeed, achieves the maximum value up to order .

Recall the original HJB equation (13) for the value function , the distortion transformation (14) and the resulting non-linear HJB equation for (15).

Note that we still assume that is given by (23), however, (15) the equation for remains fully nonlinear. The distortion transformation (14) will be key to build sub- and super-solutions for (13), but first, we need some smoothness properties for the functions and . In this section we will commonly use the notation that a function is bounded away from zero, which we define as is such that .

3.1 Smoothness of and

We have the following:

Lemma 1.

Assume that are bounded, twice differentiable with bounded derivatives, and that ,

are bounded away from zero.

Then, and , the solutions of (24) and (32) respectively, exist and they are unique and bounded. Moreover, their derivatives up to order two are bounded. Additionally, and are also given by their Feynman–Kac representations (27) and (36) respectively.

Proof.

We show the proof for , whereas the proof for is similar.

First, note that under our coefficient assumptions, the operator appearing in (26) is (degenerate) elliptic. Then, existence and uniqueness of the classical solution of (24) follows from [20][Theorem 6].

Therefore, it is easily seen that all the assumptions of Feynman–Kac formula in [16][Theorem 5.7.6]

hold. Thus, from (27),

it follows that is bounded.

Since is a classical solution to (24), it is differentiable, and we can consider , its derivative with respect to .

By differentiating (24), we obtain the system of PDEs:

(46)

(47)

(48)

(49)

Note that here, as per our convention, denotes the partial derivative of with respect to Denoting by the vector and by the vector, the system of equations (48) can be rewritten:

(50)

where is the identity matrix, is a potential matrix, and the last term being a source term.

Therefore, the assumptions of [16][Theorem 5.7.6] again hold, and is given by the Feynman-Kac formula,

Under our coefficient assumptions, this shows that and are bounded. Differentiating the system (48) with respect to , one obtains equations for the second order derivatives and their boundedness is derived by using again a Feynman–Kac representation and our coefficient assumptions. Here, we omit these straightforward lengthy details as well as the calculation details for given by (32) and its derivatives. Finally, we similarly conclude that the Feynman–Kac representation (36) of holds.

∎

Corollary 2.

Under the assumptions of Lemma 1, the strategy given in (37) is admissible.

Proof.

Under our assumptions from (27) , we have that is bounded away from zero. Moreover, from Lemma 1, we have that are bounded. Therefore it follows that is also bounded.

Thus from the definition of in (37), it follows that given by (4) is a generalized geometric Brownian motion, and thus is positive. Additionally, satisfies the admissibility constraint (6).

∎

3.2 Building Sub- and Super-Solutions

The goal is now to obtain bounds for the value function , solution to the HJB equation (13), and to justify the approximation (31).

Consider and given as solutions to (24) and (32) respectively and under the assumptions of Lemma 1. Using those and the distortion transformation (14), define

(51)

where is a constant to be determined later independently of , and where is given by (23). Here, we assume to start with and the case will be treated in Section 3.2.4.

Observe that from the boundary conditions of and , we have

Note also that from the Feynman–Kac formula (27), the function is bounded, positive, and bounded away from zero. On the other hand, the function is bounded, and, therefore, for small enough, , and consequently, is well defined.

3.2.1 Strategy of the proof of accuracy

Recall the HJB equation (10) and its two operators and defined in (8) and (9) respectively.

From it, we define the operator

(52)

where .

We will show that there exists such that for small enough we have

(53)

where the strategy is given by (37) and the strategy is any admissible strategy.

By Itô’s formula and a justification of the martingale property which will be given later, we then conclude that

(54)

(55)

(56)

(57)

(58)

(59)

(60)

and, by taking a supremum over :

(61)

In other words, is a submartingale along and

is a supermartingale along any admissible . In turn,

(56) and (61) show that is a sub-solution and is a super-solution. Using again the definition (14) of , we deduce that our proposed approximation is accurate at the order :

(62)

uniformly in .

This is formalized in the following:

Theorem 3.

In addition to the coefficient assumptions in Lemma 1, we assume that

is bounded and bounded away from zero, and . Then, there exits a constant such that, for small enough, the functions defined in (51) are super- and sub-solutions, and the accuracy of approximation (62) holds. Moreover, the strategy given by (37), is “nearly-optimal”, in other words, if followed, then the expected utility of the terminal wealth will differ from the value function by , i.e.

(63)

uniformly in .

Proof.

The proof follows the argument presented at the begining of Section 3.2.1 and will mainly consists in deriving

the key inequalities (53).

Recall that , and that the strategy is given by (37).

3.2.2 Super-solution, computation of

By direct computation, we get:

(64)

(65)

(66)

where the quantities are given by

(67)

(68)

(69)

(70)

(71)

(72)

(73)

(74)

(75)

(76)

(77)

From the equations (24) and (32) satisfied by and respectively, the terms of order one and of order in (66) cancel.

For , we have and consequently . Therefore, from the boundedness of , one can choose independently of such that the term in in (66) is positive. Finally, since the and terms are all bounded, it follows that for small enough the estimate (53) for follows.

Note that for deriving (56) from this estimate, one needs to check that the martingale parts are true martingales. This can be seen by writing these quantities explicitly and using again the boundedness of the derivatives of and and the admissibility of . We omit the details.

3.2.3 Sub-solution, computation of

Using the fact that , a similar calculation with any admissible strategy reveals:

Using the boundedness of , and the fact that one can choose independently of such that the term in in (83) is negative,

and the other terms are absorbed for small enough.

We conclude that the inequality (53) for holds. The martingale terms in

(60) are handled as before, before taking the supremum in the admissible .

The rest of the proof follows the same lines as in the case .

4 An Example with Explicit Formula

In our approach, the solution of non-linear HJB equation (10) is approximated by where and are the solutions of the linear equations (24) and (32) respectively. The advantage is that these two equations are linear and also are of lower dimension being independent of . In this section, we provide an example with explicit formulas for the approximation which we use as benchmark in a numerical illustration presented in Section 4.1.

We consider the following model

(95)

(96)

with and where recall that Assume also that and , and , where is a compact. Note the singularity when . When and the Brownian motions are perfectly correlated this does not happen since in that case , as and the boundary is absorbing.

Therefore, it is not surprising that when small enough we should still be able to ignore the possibility of crossing the boundary with high probability.

Consider the case, , the other case is similar.

Next, observe that satisfies

(97)

where is a one-dimensional Brownian motion, defined by , where in turn the Brownian motions are defined similar to (28) as

Compare with the following two diffusions

(98)

(99)

We have that are both CIR processes, and under our assumptions they both satisfy the Feller condition and therefore a.s.. Additionally, they also sandwich , i.e. . Therefore, a.s., and all the absolute values of inside the square roots above, can be removed and written simply as

Next, note that a CIR model has a good rate function [5] and therefore, for small enough,

for all on a set with probability at least

Therefore, the same is also true for there.

Next, we have that

(100)

where is another one-dimensional Brownian motion.

Recall that . Using the fact that , we have that on , then, for small enough, we can further assume that on a set with probability at least the process on the entire

Indeed, observe that on , where we have that

Note that

is a Brownian motion on , where and is its inverse. Let and recall that

Therefore using the fact that , on

it can be then calculated that for small enough,

On , we can get rid all the absolute values in (95)-(96).

Thus, as opposed to finding the true PDE solution in (15) we will instead proceed to find the solution to the approximate PDE

(101)

(102)

(103)

(104)

More specifically, consider the problem

(105)

Here we need to tweak the definition of admissibility and additionally require that in order for strategy to be admissible. Below we will show that is admissible.

Then

for , we have that

(106)

Therefore

(107)

The modified problem (105) leads to the HJB equation (102) with the boundary conditions (104) with standard transformation. Therefore, we proceed to solve (102), (104). By the above discussion, we can also ignore the boundary conditions. Performing the asymptotic expansion leads to the same equations (24) and (32).

Therefore, for convenience, we will drop the tilde, and still call the -approximations to by and the zero order associated strategy .

Therefore, (24), the equation satisfied by becomes:

(108)

(109)

(110)

We use the standard ansatz Then

(111)

(112)

(113)

Letting then

(114)

(115)

The solution is given by and

, where are assumed to be two distinct real roots of the quadratic The latter is achieved, for example, if

We note that is an admissible strategy. Let From the fact that

we conclude that

is bounded by . Since we get that

(121)

(122)

A technical, but simple calculation via affine ansatz solution then shows that for small enough, such that

we have that

is finite. Similar calculation can be done with other term involving by utilizing the fact that

where

(123)

We want to highlight, that this is really the strategy , i.e. the “nearly-optimal” strategy associated with the zero order expansion of , but since the difference between and is small, this strategy will also achieve the desired accuracy level of Additionally, while it is possible to repeat this entire calculation in the other two cases, when and , and find the solution and the zero order strategy, this is not necessary in order to find a “nearly-optimal” strategy. We start with , and then choose small enough, such that . While the process will leave the set with strictly positive probability, since this probability is very small, as explained above, this can be ignored. In other words, we can employ the strategy , and it will still be “nearly-optimal”, as implied by (107).

Moreover, in the case we can also find the term.

Indeed, the PDE satisfied by is

(124)

(125)

(126)

where

(127)

(128)

From the Feynman–Kac representation (36) for , we have that

(129)

(130)

where we have used that evolves as a CIR process under , the Brownian motion given by (28):

and has the p.d.f.

(131)

(132)

where is the modified Bessel function of the first kind of order .

We note, that this calculation can also be done for the other two cases and .

Remark 2.

The model used in this example is based on square-root processes and does not satisfy the assumptions of Theorem 3. Extending the accuracy result to that case requires another stopping argument at the first time one of the two processes or exit the interval

for some small parameter . The stopped model satisfies the assumption but doesn’t anymore allow for explicit formulas for the functions and . A careful argument is needed to pass to the limit uniformly in . This was done, for instance, for another nonlinear perturbation problem in [9] in the context of stochastic volatility uncertainty. It is quite technical and beyond the scope of this paper.

4.1 Numerical Illustration

We illustrate our finding in the previous Section 4 numerically.

We use the parameters:

(133)

(134)

The graphs are all drawn as functions of at the point In this case it is easily seen that the Feller condition for the diffusions in (99) is satisfied.

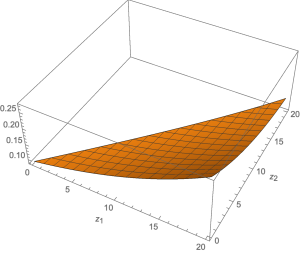

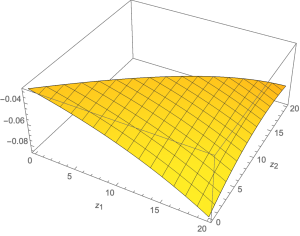

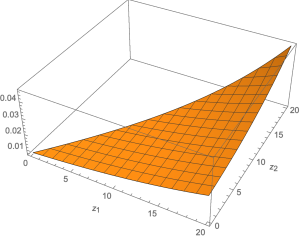

Figure 1 illustrates: – the difference between the numerical solution of , and its approximation (top left);

– the difference between the numerical solution of , and the numerical solution of the non-linear HJB equation using the strategy from (120) (top right);

and – the difference between and its approximation (bottom).

First, note that we expect from Theorem 3 and the approximation (107) that these errors are of order , and respectively. Next, it can be computed that for . Since we approximately have that Therefore, we observe as expected that is positive. Finally, since , and , it follows that , which is again consistent with the sign observed in Figure 1. We want to emphasize that as expected this graph shows that if the simple zero order approximating strategy is used the difference in utility is of order , and thus as expected this is a ”nearly-optimal” strategy.

Figure 1: Top left: graph of – the difference between the numerical solution , and its approximation .

Top right: the graph of – the difference between the numerical solution of , and the numerical solution of the HJB equation but using the strategy .

Bottom: the graph of – the difference between the numerical solution , and its approximation

All graphs are done as a function of at the point

5 Extension to Models with Multi Assets

We now show how to extend our results to a model with multi-assets, and multi-factors. Consider a model with multiple assets governed by

(135)

(136)

where we use the vector notation and the

correlation structure between the Brownian motions is given by:

with parameters ensuring a proper correlation structure (in particular and symmetries , ).

Assuming that the wealth is fully invested in the stocks in a self-financed way, then the wealth process is given by:

(137)

where is the amount invested in asset at time .

The value function of the optimal investment problem with terminal time and utility is:

(138)

We define the following operators:

(139)

(140)

The value function then satisfies:

(141)

(142)

Our asymptotics will be around the case where the Brownian motions are fully correlated. In order to model this regime, we define:

(143)

with and , and

is a small parameter, , small enough to ensure a proper covariance structure.

Remark 3.

The model that we are perturbing corresponding to in (143), cannot be of eigenvalue equality (EVE) type as considered in [1] unless , that is models with a single factor. Indeed, the matrix with , admits zero as eigenvalue as soon as and therefore, cannot satisfy the EVE condition unless in the uncorrelated case .

In order to keep the formulas as explicit as possible, we present the case with two assets and two factors.

5.1 Model with Two Assets

We continue illustrate the calculation of the expansions in an example with two assets and two driving factors. Therefore the model will now be governed by (135)–(136) with .

Maximization over in (141) gives:

(144)

where denotes a derivative with respect to , and to ensure that the two stocks are not fully correlated.

Substituting (144) into (141), it follows that

(145)

(146)

(147)

where

For , we again perform a distortion transformation (14) of the HJB equation (145) for the value function . Similar to (15), must satisfy:

(148)

(149)

(150)

(151)

5.1.1 Fully Correlated Case

Analogous to Section 2.3, we temporarily assume that the two stochastic volatility factors are fully correlated:

, , and

We consider the ansatz

(152)

Let Then, it follows that satisfies

(153)

(154)

(155)

Choosing

linearizes the equation to get:

(156)

(157)

where

(158)

We have the Feynman–Kac representation:

(159)

where is defined so that

is standard Brownian motion under it, and we denoted

(160)

5.1.2 Asymptotics

In the general case, we will assume a correlation structure of the form (143):

(161)

with and

is a small parameter, , small enough to ensure a proper covariance structure. As was done previously in the case with one stock and a risk-free asset, we will now expand the general case, around the known case of , and calculate the asymptotic expansion similar to (31).

(162)

Note that the expansion has the same number of arguments as before, as there are still two factors, though the functions will be different.

Expanding the correlation coefficients as in (161) and the value function as in (162),

we see that satisfies an equation similar to (32):

(163)

where denote the gradient and the Hessian of and

(164)

(165)

(166)

We now consider , the first order approximation to given in (144), by substituting the first order approximation for from (31), namely,

Therefore,

(167)

We next use in the supremum of (141) together with the expansions (161), (162) and evaluate the equation, to get that:

(168)

(169)

(170)

(171)

where the last equality is obtained by cancelling the first two terms using the equations (156) and (163) satisfied by and respectively.

To summarize, this formal computation shows that the strategy given by (167) generates the value given by (141) up to order .

5.1.3 Explicit Formulas

We again consider a specific choice of a model, similar to the example in Section 4.

Namely, we change (95) and (96) to account for two stocks to be:

(172)

(173)

with in (135) and (136).

Similar to Section 4, we have that outside of a set with small probability is bounded as , and Therefore similar to (102), let

be a solution to the approximating PDE:

(174)

(175)

(176)

(177)

(178)

(179)

Then as before (107) holds. Therefore we solve for our approximations , , similarly to Section 4.

Namely, is the solution to PDE:

(180)

(181)

(182)

which is the same as (108), only with ,

and therefore can be solved the same way as in Section 4.

Moreover, analogously to (120) from (167) we have that

(183)

The same is true regarding in case , then it is the solution of the PDE

The problem of portfolio optimization with power utilities when returns and volatilities are driven by a single factor can be linearized by using a classical distortion transformation. In this paper we proposed to treat this same problem in the presence of several factors. Our approach is to consider a perturbation around the case where the factors are fully correlated which can be linearized and amenable to simpler equations. We identify the leading order term for the value function corresponding to a Merton’s portfolio and we characterize the first order correction as the solution to a linear equation. An example with explicit solutions is given to illustrate the quality of the approximation. Under a set of reasonable assumptions, we rigorously establish an accuracy result for this regular perturbation problem by using the construction of sub- and super-solutions to the fully nonlinear HJB equation characterizing the value function. In turn, we deduce that the leading order approximation of the optimal strategy generates the value function up to the first order of accuracy.

Acknowledgement

The authors would like to thank Ruimeng Hu for her comments on an earlier version of the paper. The authors are also grateful to the two referees whose comments and suggestions helped a lot in improving the paper.

References

[1]

L. Avanesyan, M. Shkolnikov, and R. Sircar.

Construction of forward performance processes in stochastic factor

models and an extension of widder’s theorem.

arXiv:1805.04535v1, 2018.

[2]

M. Bichuch.

Asymptotic analysis for optimal investment in finite time with

transaction costs.

SIAM Journal on Financial Mathematics, 3(1):433–458, 2012.

[3]

M. Bichuch and R. Sircar.

Optimal investment with transaction costs and stochastic volatility

part ii: Finite horizon.

SIAM Journal on Control and Optimization, 57(1):437–467, 2019.

[4]

G. Chacko and L. M. Viceira.

Dynamic consumption and portfolio choice with stochastic volatility

in incomplete markets.

Review of Financial Studies, 18(4):1369–1402, 2005.

[5]

Alberto Chiarini and Markus Fischer.

On large deviations for small noise itô processes.

Advances in Applied Probability, 46(4):1126–1147, 2014.

[6]

J. Feng, M. Forde, and J.-P. Fouque.

Short-maturity asymptotics for a fast mean-reverting heston

stochastic volatility model.

SIAM Journal on Financial Mathematics, 1(1):126–141, 2010.

[7]

J.-P. Fouque and R. Hu.

Asymptotic optimal strategy for portfolio optimization in a slowly

varying stochastic environment.

SIAM Journal on Control and Optimization, 5(3), 2017.

[8]

J.-P. Fouque and R. Hu.

Optimal portfolio under fractional stochastic environment.

Mathematical Finance, 29(3), 2019.

[9]

J.-P. Fouque and N. Ning.

Uncertain volatility models with stochastic bounds.

SIAM Journal on Financial Mathematics, 9(4):1175–1207, 2018.

[10]

J.-P. Fouque, G. Papanicolaou, and R. Sircar.

Derivatives in financial markets with stochastic volatility.

Cambridge University Press, 2000.

[11]

J.-P. Fouque, G. Papanicolaou, and R. Sircar.

Mean-reverting stochastic volatility.

International Journal of theoretical and applied finance,

3(01):101–142, 2000.

[12]

J.-P. Fouque, G. Papanicolaou, R. Sircar, and K. Solna.

Multiscale stochastic volatility asymptotics.

Multiscale Modeling & Simulation, 2(1):22–42, 2003.

[13]

J.-P. Fouque, G. Papanicolaou, R. Sircar, and K. Solna.

Multiscale Stochatic Volatility for Equity, Interest-Rate and

Credit Derivatives.

Cambridge University Press, 2011.

[14]

J.-P. Fouque, R. Sircar, and T. Zariphopoulou.

Portfolio optimization & stochastic volatility asymptotics.

Mathematical Finance, 2016.

[15]

H. Hata, H. Nagai, and S.-J Sheu.

An optimal consumption problem for general factors models.

SIAM Journal on Control and Optimization, 56(5):3149–3183,

2018.

[16]

I. Karatzas and S. Shreve.

Brownian motion.

In Brownian Motion and Stochastic Calculus, pages 47–127.

Springer, 1998.

[17]

D. Kramkov and W. Schachermayer.

Necessary and sufficient conditions in the problem of optimal

investment in incomplete markets.

The Annals of Applied Probability, 13(4):1504–1516, 2003.

[18]

R. C. Merton.

Lifetime portfolio selection under uncertainty: The continuous-time

case.

Review of Economics and statistics, 51:247–257, 1969.

[19]

R. C. Merton.

Optimum consumption and portfolio rules in a continuous-time model.

Journal of economic theory, 3(4):373–413, 1971.

[20]

O. Oleinik.

On the smoothness of solutions of degenerating elliptic and parabolic

equations.

In Doklady Akademii Nauk, volume 163, pages 577–580. Russian

Academy of Sciences, 1965.

[21]

R. Sircar and G. Papanicolaou.

Stochastic volatility, smile & asymptotics.

Applied Mathematical Finance, 6:107–145, 1999.

[22]

T. Zariphopoulou.

Optimal investment and consumption models with non-linear stock

dynamics.

Mathematical Methods of Operations Research, 50(2):271–296,

1999.