Sensitivity estimation of conditional value at risk using randomized quasi-Monte Carlo

Abstract

Conditional value at risk (CVaR) is a popular measure for quantifying portfolio risk. Sensitivity analysis of CVaR is very useful in risk management and gradient-based optimization algorithms. In this paper, we study the infinitesimal perturbation analysis estimator for CVaR sensitivity using randomized quasi-Monte Carlo (RQMC) simulation. We first prove that the RQMC-based estimator is strongly consistent under very mild conditions. Under some technical conditions, RQMC that uses -dimensional points in CVaR sensitivity estimation yields a mean error rate of for arbitrarily small . The numerical results show that the RQMC method performs better than the Monte Carlo method for all cases. The gain of plain RQMC deteriorates as the dimension increases, as predicted by the established theoretical error rate.

Keywords: Value at risk; Conditional value at risk; Sensitivity; Quasi-Monte Carlo

1 Introduction

In the financial industry, value at risk (VaR) and conditional VaR (CVaR) are two important tools for quantifying and managing portfolio risk. From the view of statistics, VaR is a quantile of a portfolio’s loss (or profit) over a holding period. On the other hand, CVaR is the average of tail losses while VaR only serves as a threshold of large loss. Therefore, CVaR may provide incentives for risk managers to take into account tail risks beyond VaR. Suppose that the loss is a random function of some parameters. The VaR and CVaR of the loss are therefore functions of the parameters. The partial derivatives of these function are called the sensitivities of VaR and CVaR (Hong, 2009; Hong and Liu, 2009; Fu et al., 2009; Jiang and Fu, 2015). These sensitivities are useful in risk management and gradient-based optimization algorithms. Moreover, Asimit et al. (2019) pointed out that sensitivity analysis and capital allocation problems both boil down to similar mathematical formulations. The Euler allocation rule of the total regulatory capital set via CVaR is a special case of CVaR sensitivities. In this paper, we focus on sensitivity analysis of CVaR using simulation.

Sensitivity estimation has been studied extensively in financial engineering. It includes the sensitivities of option prices, which are known as Greeks (see Broadie and Glasserman, 1996). Additionally, Hong et al. (2014) considered the problem of estimating the sensitivities of portfolio credit risk. There are several widely used approaches in the simulation literature. The finite difference (FD) method is the simplest one, but it suffers from the trade-off between the bias and variance of the estimator (see Fox and Glynn, 1989). The infinitesimal perturbation analysis (IPA) takes the pathwise derivatives of the performance function in the estimation, which is also known as the pathwise method (see Glasserman, 2004). From another perspective, the performance function is viewed as a parameter-free function of some random variables whose joint distribution depends on the parameter. The likelihood ratio (LR) method takes the derivatives of the joint density in the estimation. Both IPA and LR methods enjoy the usual Monte Carlo variance rate , which is faster than the FD method. Unlike LR, IPA needs stronger conditions that rule out discontinuous functions. However, the IPA estimator usually has a smaller variance than the LR estimator when they are both applicable (Cui et al., 2019). Recently, Peng et al. (2018) proposed a generalized LR method that extends IPA and LR to handle discontinuous functions.

Related work on sensitivity analysis of CVaR includes Scaillet (2004) and Hong and Liu (2009). Particularly, Hong and Liu (2009) proposed an IPA type CVaR sensitivity estimator. Under certain conditions, the IPA method is applicable because the performance function of CVaR is a hockey stick function. In addition, Hong and Liu (2009) established a central limit theorem for the proposed estimator. It should be noted that the IPA estimator of CVaR sensitivity is biased since it is a sample average of dependent observations that includes the VaR estimator, differently from the IPA estimators developed in Greeks estimation. In this paper, we analyze the IPA estimator proposed by Hong and Liu (2009) in the framework of randomized quasi-Monte Carlo (RQMC). RQMC is a randomized version of quasi-Monte Carlo (QMC). The (R)QMC method which has the potential to accelerate the convergence becomes an alternative method in simulation. It is widely used in financial engineering, such as option pricing and Greeks estimation (see, e.g., Joy et al., 1996; Wang and Tan, 2013; Xie et al., 2019). Recently, He and Wang (2020) established a deterministic error bound for the QMC-based quantile estimator. They also showed that under certain conditions the RQMC-based CVaR estimator has a root mean squared error (RMSE) of for arbitrarily small , where is the dimension of RQMC points used in the simulation. To the best of our knowledge, very few works are concerned with sensitivity estimation of CVaR in (R)QMC. The results in He and Wang (2020) cannot be extended to sensitivity estimation. Particularly, the strong consistency for the VaR and CVaR estimators is remain unclear when using RQMC.

There are two major difficulties in analyzing the RQMC-based CVaR sensitivity estimator. The first difficulty is that the estimator is an estimated function at an estimated VaR rather than the usual sample average. As a result, the numerical analysis in (R)QMC quadrature cannot be applied directly. The second difficulty is due to the discontinuity and singularity of the performance function of CVaR sensitivity. For this case, the well-known Koksma-Hlawka inequality for assessing QMC error is useless (Niederreiter, 1992). In this paper, we first establish the strong consistency for the RQMC-based estimator by making use of the recent work of Owen and Rudolf (2020). As a by-product, the strong consistency for the VaR and CVaR estimators is also proved under very mild conditions. We then study the convergence rates of the estimator. Under some technical conditions, we find that the RQMC-based estimator yields a mean error rate of for arbitrarily small . The technical conditions are verified for portfolio loss of geometric Brownian motions driven models or when the loss is a quadratic form of normally distributed variables. Our contribution is two-fold.

-

•

We give a rigorous error analysis of CVaR sensitivity estimation when using RQMC. It is sometimes straightforward to replace Monte Carlo with RQMC for practical problems in finance. Such a simple replacement often leads to an improvement as frequently observed in the numerical results. Theoretical analysis is expected to better understand the performance of RQMC.

-

•

As a by-product of the error analysis, we find that the efficiency of CVaR sensitivity estimation depends on the RQMC integration of two specific discontinuous integrands. This paves the way to improve the RQMC accuracy in CVaR sensitivity estimation. If some strategies are applied to improve the RQMC integration of the two integrands, one would expect a better performance of CVaR sensitivity estimation. In the (R)QMC literature, there are some promising strategies to handle discontinuities in numerical integration, such as dimension reduction techniques and smoothing methods (Wang and Tan, 2013; Zhang and Wang, 2019).

The remainder of this paper is organized as follows. In Section 2, we present some background on VaR, CVaR and its sensitivity estimation. In Section 3, we focus on analyzing the RQMC-based CVaR sensitivity estimator. Some important (R)QMC preliminaries are first reviewed. Strong consistency and some stochastic bounds are then established. Section 4 gives some numerical examples, including portfolios of European options modeled to be driven by a geometric Brownian motion and a quadratic loss model arising from the delta-gamma approximation of portfolio value change. Section 5 concludes this paper. A technical lemma and its proof are deferred to the Appendix.

2 Background and Simulation-based Estimation

Let be the random loss and be the cumulative distribution function (CDF) of . For any , we define, respectively, the -VaR and the -CVaR of as

where . The -VaR is the lower -quantile of the distribution of . If has a density in a neighborhood of , then . From this point of view, CVaR is the expected shortfall or the tail conditional expectation.

Suppose that are observations of . Monte Carlo sampling renders independent and identically distributed (iid) observations. In the QMC sampling, the observations are deterministic, but with better uniformness. In the RQMC framework, the observations are dependent random variables retaining the better uniformness (see Section 3.1 for the details). In either case, based on the observations, one can estimate the CDF by the so-called empirical CDF

| (2.1) |

It is natural to estimate the -VaR and the -CVaR by

| (2.2) | ||||

| (2.3) |

respectively. The crucial step is to estimate the CDF via (2.1). We expect that a better estimate of the CDF leads to an improved estimate of the quantile. Recently, Kaplan et al. (2019) compared two approaches for quantile estimation via RQMC.

Suppose that the random loss can be modeled as a function , where is the parameter of interest with range . To emphasize the dependence on the parameter , the -VaR and the -CVaR of are rewritten as and , respectively. In this paper, we are interested in the sensitivity estimation of CVaR with respect to , i.e., . Let . To obtain an IPA estimator of the CVaR sensitivity, we need the following technical assumptions.

Assumption 2.1.

There exists a random variable with such that

for all , and exists with probability 1 (w.p.1) for all .

Assumption 2.2.

The VaR function is differentiable for any .

Assumption 2.3.

For any , .

Under Assumptions 2.1–2.3, Hong and Liu (2009) showed that by interchanging the expectation and differentiation,

To simplify the notation, we let and denote and , respectively. Suppose that we are able to obtain observations of , denoted by . Hong and Liu (2009) proposed an IPA estimate of given by

| (2.4) |

where is obtained by (2.2). The IPA estimator is a sample average of dependent variables that involve the VaR estimator . As a result, the CVaR sensitivity estimator (2.4) is biased. Hong and Liu (2009) proved an asymptotic bias of in the Monte Carlo setting.

The random loss is often expressed as a function of random variables, say, for . The random variables are called the risk factors or scenarios. In this paper, we assume that the closed forms of and are available so that one can generate the sample . If the random loss is modeled as a conditional expectation which is not given analytically, one may resort to nested simulation. This is beyond the scope of this paper. Interested readers are referred to Gordy and Juneja (2010); Broadie et al. (2011).

3 RQMC-based Estimation of CVaR Sensitivity

The incorporation of QMC or RQMC in estimating the CVaR sensitivity is straightforward provided that the mechanism of sampling the random loss via standard uniform distributed variables is specified. In what follows, we suppose that can be expressed as

| (3.1) |

where is a given measurable function, and . The model (3.1) was also studied in VaR estimation with Latin hypercube sampling (Avramidis and Wilson, 1998; Dong and Nakayama, 2017). It is allowed that has singularities along the boundary of the unit cube. That is why we do not consider the closed set or the half closed set . As we can see from the numerical examples in Section 4, the random loss is unbounded with singularities along the boundary of the unit cube. Let . Instead of generating an iid sample in the Monte Carlo framework, we now generate the sample

via RQMC points in . It then follows by substituting the sample in (2.1) and (2.4) to obtain the associated CVaR sensitivity estimator. There are various QMC points designed with high uniformness in the literature, which are known as low discrepancy points. A better performance of RQMC can be therefore expected. The price for switching from Monte Carlo to (R)QMC is to specify the model as the form (3.1).

3.1 QMC and RQMC theory

In this subsection, we review the philosophy of the QMC world and some important QMC integration error analysis in the literature. Let’s start by estimating an integral over the unit cube

The QMC quadrature rule takes the average

| (3.2) |

where are carefully chosen points in . The well-known Koksma-Hlawka inequality gives a deterministic error bound for the quadrature rule (3.2),

| (3.3) |

where , is the variation of in the sense of Hardy and Krause, and is the star-discrepancy of points in ; see Niederreiter (1992) for details. There are many ways to construct low discrepancy point sets such that . By (3.3), the QMC error is of for integrands with bounded variation in the sense of Hardy and Krause (BVHK). However, if the integrand is discontinuous or unbounded, the variation is usually unbounded (Owen, 2005). For this case, the Koksma-Hlawka inequality is useless. In this paper, we restrict our attention to -nets in base for which the sample size has the form . Our results also work for -sequences without that restriction on . For , the space consists of all measurable function on for which .

Definition 3.1.

An elementary interval in base is a subset of of the form

where , with for .

Definition 3.2.

Let and be nonnegative integers with . A finite sequence is a -net in base if every elementary interval in base of volume contains exactly points of the sequence.

Definition 3.3.

Let be a nonnegative integer. An infinite sequence is a -sequence in base if for all and the finite sequence is a -net in base .

For deterministic QMC, it is important to obtain an estimate of the quadrature error . But the upper bound in (3.3) is very hard to compute, and it is restricted to functions of finite variation. Instead, one can randomize the points and treat the random version of the quadrature in (3.2) as an RQMC quadrature rule. That is why we focus on using RQMC. Usually, the randomized points are uniformly distributed over , and the low discrepancy property of the points is preserved under the randomization (see L’Ecuyer and Lemieux (2005) and Chapter 13 of the monograph Dick and Pillichshammer (2010) for a survey of various RQMC methods). In this paper, we focus on the use of scrambling technique proposed by Owen (1995) to randomize -nets.

Owen (1995) applied a scrambling scheme on the nets that retains the net property. Let . We may write the components of in their base expansion where for all . The scrambled version of is a sequence with written as where are defined in terms of random permutations of the . The permutation applied to depends on the values of for . Specifically, , and in general

| (3.4) |

Each permutation is uniformly distributed over the permutations of , and the permutations are mutually independent. There are some good properties of scrambled digital nets or sequences, which can be found in Owen (1995, 1997a).

-

•

A scrambeled -net and scrambled -sequence are -net and -sequence w.p.1, respectively.

-

•

For any point in , the scrambling version of the point is uniformly distributed over . This implies that the estimate (3.2) is unbiased if using the scrambling method to randomize the QMC points.

-

•

If in (3.2) are points of a scrambled -net, then for any squared integrable integrand , . This suggests that the RQMC-based estimate is asymptotically faster than Monte Carlo estimates for a large class of integrands.

The results on scrambled nets are highly dependent on the smoothness properties of the integrand. If the integrand is sufficiently smooth, the scrambled net variance is improved to ; see Owen (1997b, 2008) for details. On the other hand, if the integrand is discontinuous, the scrambled net variance turns out to be for arbitrarily small (He and Wang, 2015; He, 2018). We next encapsulate their results as a proposition that will be used in the following error analysis.

Proposition 3.4.

Let , where and . Suppose that given by (3.2) is an RQMC quadrature rule using a scrambled -net in base with . Assume that the boundary of the set admits a -dimensional Minkowski content , defined by

| (3.5) |

where is the -dimensional Lebesgue measure, and denotes the outer parallel body of at distance .

-

•

If is constant, then .

-

•

If is of BVHK, then for arbitrarily small .

-

•

If satisfies the boundary growth condition with arbitrarily small rates (see Definition 3.12), then for arbitrarily small .

Proof.

The use of in the convergence orders is to hide the logarithmic factor. As commented in He and Wang (2015), is the surface area of the set in the terminology of geometry. If is a convex set in , then its boundary has a -dimensional Minkowski content. In this case, since the surface area of a convex set in is bounded by that of the unit cube, which is . More generally, Ambrosio et al. (2008) found that if has a Lipschitz boundary, then admits a ()-dimensional Minkowski content.

It should be noted that the true value is usually unknown. The CVaR sensitivity estimate (2.4) is not the usual quadrature rule of the form (3.2). But if we replace the VaR estimate with the true value in (2.4), it turns out to be a quadrature rule for the discontinuous function . From this point of view, the results in Proposition 3.4 can be used to study the error rate of the CVaR sensitivity estimate. The challenge is how to bound the gap due to the replacement. This is the topic of Section 3.3.

3.2 Strong Consistency

Hong and Liu (2009) established the strong consistency for the Monte Carlo sensitivity estimator. Their proof relies heavily on the strong law of large numbers (SLLN) for an iid sample. Recently, Owen and Rudolf (2020) proved the SLLN for scrambled digital net integration for integrands in for any . Together with this fundamental result, the strong consistency of an RQMC-based CVaR sensitivity estimate can be easily proved following the steps in the proof of (Hong and Liu, 2009, Theorem 4.1). Define

| (3.6) |

where and .

In He and Wang (2020), the consistency was proved for the VaR estimator based on deterministic QMC, but not for its randomized counterpart. We are ready to show the strong consistency of the RQMC-based estimators. We need the following assumption, which is the minimal requirement for establishing the strong consistency of the Monte Carlo quantile estimator (Serfling, 1980, p. 75).

Assumption 3.5.

For any , is the unique solution of .

Theorem 3.6.

If Assumption 3.5 holds and the VaR estimator is based on a scrambled -net in base with , then

Proof.

By the SLLN established in (Owen and Rudolf, 2020, Theorem 5), for all ,

The following steps are in lines with the proof of the strong consistency of the Monte Carlo estimate (Serfling, 1980, p. 75). By Assumption 3.5, we have for any . Since and w.p.1. We thus have

By (2.2), we have . Therefore,

implying w.p.1. ∎

Theorem 3.7.

Proof.

Since , . By the SLLN established in Owen and Rudolf (2020),

By the triangle inequality and Theorem 3.6, we have

as w.p.1. Together with (2.3), we find that w.p.1 as .

Note that given by (3.6) is the quadrature rule with

and . Since for some , by the SLLN again,

as w.p.1. It suffices to prove that w.p.1.

Let , where . Since for , using the SLLN again,

By the Hölder inequality, we have

| (3.7) |

where we use the fact that the function never change the sign when varying .

3.3 Stochastic bounds

Assumption 3.8.

For any , defined over is a continuous random variable whenever components of are fixed and the remaining one is uniformly distributed over an open interval in .

Lemma 3.9.

Proof.

Let be the order statistics of in increasing order. By the definition of , we have , where denotes the smallest integer no less than . Notice that

Therefore,

Let . It then follows

If the loss is a continuous random variable, w.p.1 for iid observations . This is because for all . Things become complicated for RQMC sampling since the observations are dependent. Under Assumption 3.8, Lemma 6.1 shows that there are at most of with equal value when using a scrambled -net w.p.1. This implies that w.p.1, completing the proof. ∎

Note that Sobol’ sequences are -sequences in base with depending on . For this case, the constant in (3.8) can be reduced to although the value of may be much larger than ; see Remark 6.2 for a discussion.

Remark 3.10.

Assumption 3.8 is stronger than Assumption 2.3. To verify Assumption 3.8, it turns out to look at a function of one-dimensional variable for any , denoted by . Good smoothness of does not necessarily render a continuous random variable. For example, for , and otherwise. It is not difficult to see that , but whenever . For this case, is not a continuous random variable. This is due to the absence of strict monotonicity. If the function is strictly monotonic over and , then is a continuous random variable with density

| (3.9) |

for in the support of . This result can be easily extended to the situation in which is piecewise strictly monotonic. Suppose that and has countable solutions on . It is clear that is strictly monotonic on an open interval determined by any two successive solutions, in which has a density of the form (3.9). The overall density is piecewise. As a result, is a continuous random variable.

Theorem 3.11 (Bounded case).

Proof.

Notice that because . Similarly, thanks to , giving .

Theorem 3.11 requires the boundedness of , which may not hold in practice. If is unbounded, the inequality (3.11) does not hold. To get rid of this, we use a truncated version of so that the inequality (3.11) can be applied. We first introduce the so-called boundary growth condition for controlling the function around the boundaries of the unit cube. Let . For a set , denotes the mixed partial derivative of taken once with respect to components with indices in .

Definition 3.12.

A function defined on is said to satisfy the boundary growth condition if

| (3.13) |

holds for all , some rates , some and all .

The boundary growth condition is the second growth condition described in Owen (2006). We use a region

to avoid the singularities for small . We now define an extension of from to such that for . One can extend the function to the whole unit cube with some good properties as in Owen (2006). That is,

| (3.14) |

where , denotes the point with for and for . Taking , serves as an approximation of , which is of BVHK (Owen, 2006) and therefore bounded.

Theorem 3.13 (Unbounded case).

Suppose that Assumptions 2.1–2.2 and 3.8 are satisfied. The estimator given by (2.4) is based on a scrambled -net in base with . Let . If satisfies the boundary growth condition (3.13) with arbitrarily small rates and admits -dimensional Minkowski content defined by (3.5), then

for arbitrarily small .

Proof.

We let from now on and work on the extension defined by (3.14), where is to be determined. Let . By the triangle inequality and using (3.11) by replacing with , with probability one,

Taking the expectation, we have

| (3.15) |

where we use the fact that each due to scrambling.

If satisfies the boundary growth condition with rates , Propositions 3.2 and 3.3 in He (2018) show that for any , there exists such that

Note that by the first part of Proposition 3.4. Taking , it then follows from (3.15) that

Since and are arbitrarily small positive numbers, we conclude for arbitrarily small . By the last part of Proposition 3.4, we have . As a result,

∎

Remark 3.14.

From the proofs of Theorems 3.11 and 3.13, the error of the CVaR sensitivity estimator is bounded by the numerical integration errors of the two discontinuous functions: and . We therefore cannot expect a better RQMC error rate than those for RQMC integration with discontinuous integrands. From this point of view, sensitivity estimation of CVaR is rather challenging for RQMC due to the discontinuities and singularities involved in the two functions. To improve the RQMC efficiency, one should pay more attention to handle the two discontinuous functions.

4 Numerical study

In this section, we examine three cases of CVaR sensitivity estimation. In our numerical experiments on RQMC, we use randomized Sobol’ points by the linear scrambling of Matoušek (1998), which has been carried out in the generator scramble in MATLAB.

4.1 Single Asset

Consider a portfolio of a single European put option that was studied in Broadie et al. (2011) for testing their adaptive nested simulation. The underlying asset follows a geometric Brownian motion with an initial price of . The drift of this process under the real-world distribution is . The annualized volatility is . The risk-free rate is . The strike of the put option is , and the maturity is years (i.e., three months). The risk horizon is years (i.e., one week).

Denote by the underlying asset price at the risk horizon . This price in the real-world is generated according to

| (4.1) |

where is the CDF of the standard normal distribution, , and hence . Using the Black–Scholes formula (Hull, 2015), the value of the put option at time is

| (4.2) |

where , and

The portfolio value loss can be expressed explicitly as a function of , say, . Here is the parameter of interest, such as , , , etc. For this example, the nested simulation is unnecessary. We now write the initial value as a function of , denoted by . The derivative of with respect to (denoted by ) is known as Greeks (see Hull, 2015, Chapter 15). From (4.2), the portfolio value at time can be viewed as a function of the random factor and possibly the parameter , denoted by . By the chain rule, we have

| (4.3) |

where we use the fact that the delta of the option at time is

Assumption 2.1 can be easily verified by taking as a small neighborhood of the parameter being estimated.

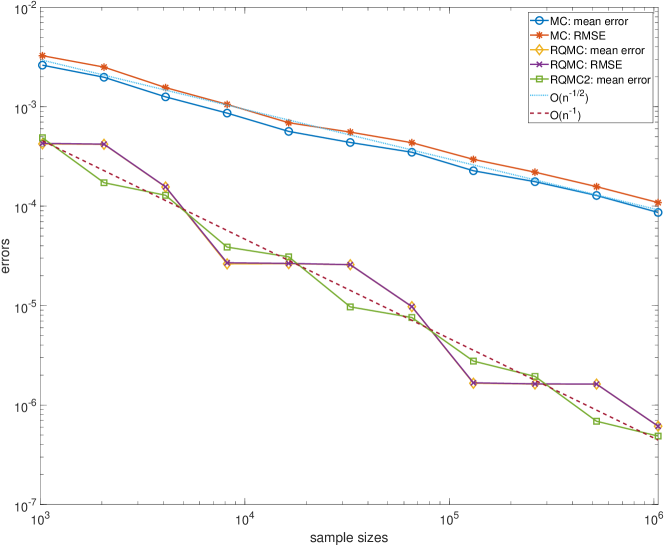

Case 1. Consider . It is easy to see that and , and hence , which is unbounded. As we will see later, all the assumptions in Theorem 3.13 are satisfied. The CVaR sensitivity estimate based on RQMC can therefore enjoy a mean error of for arbitrarily small .

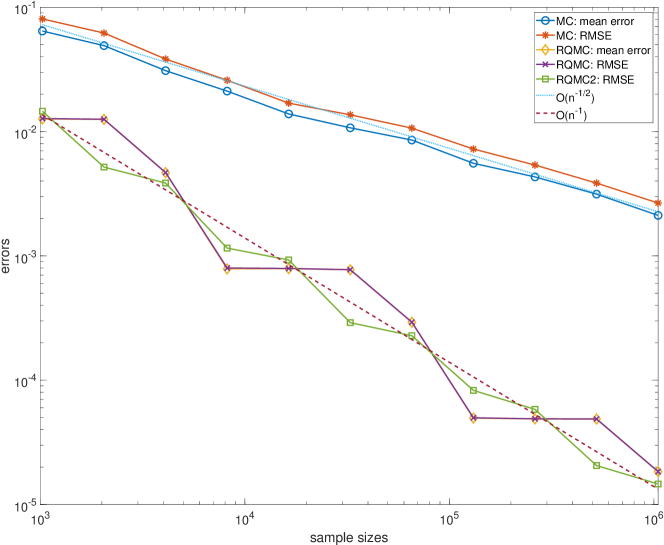

Case 2. Consider . It is easy to see that and . The later is known as the rho of the option at time . So , which is bounded. Notice that

where is the density of the standard normal distribution. Since for some constant , goes to infinity as or when . It is common that the risk horizon is very small relative to the maturity . So for this case, is unbounded, leading to unbounded variation of in the sense of Hardy and Krause. Therefore, the faster rate (3.10) in Theorem 3.11 cannot be applied. Recall that the mean error can be bounded by the root mean squared error. Theorem 3.11 directly yields that the mean error is . This is rather conservative because the problem is only one-dimensional. On the other hand, by applying Theorem 3.13 which allows unbounded , a mean error of can be achieved.

We now verify the assumptions in Theorem 3.13 for various cases of including the two cases above. It is not difficult to see that , implying the loss is strictly increasing in . So , where is the unique solution to . The closed-form for -VaR is thus available, i.e., . It is obvious that Assumptions 2.2 and 2.3 and 3.8 are satisfied. Note that , whose boundary admits Minkowski content Ambrosio et al. (2008). It remains to show that satisfies the boundary growth condition (3.13) with an arbitrarily small growth rate. That is, for arbitrarily small ,

To this end, we first introduce some useful upper bounds that were also used in He (2018, 2019). Note that

| (4.4) |

as (see Patel and Read, 1996, Chapter 3.9). For any fixed and arbitrarily small ,

| (4.5) |

Since , by (4.1) and (4.5), we find that

| (4.6) |

for any fixed . Using (4.4) again, for arbitrarily small ,

| (4.7) |

Note that for a constant , and can be expressed as the form for some constants . Overall, can be expressed as a function of , i.e.,

| (4.8) |

Using , , and (4.6), we find that . By (4.8), we have

By the chain rule, we have

By using (4.6) and (4.7), and thanks to the boundedness of , The boundary growth condition is thus verified.

To compare the performances of Monte Carlo and RQMC based sensitivity estimators, we need to know the theoretical value of the CVaR sensitivity. Although the VaR has a closed form, it is difficult to compute the sensitivity of CVaR analytically. To get an accurate estimate as the benchmark, we use the RQMC-based estimate (2.4) by replacing with the theoretical value of VaR with 100 replications, each using a large sample size . We denote this method as RQMC2, and compare it with the crude estimate (2.4) for sample sizes . In our numerical experiments, we take . For Case 1, the benchmark is . For Case 2, the benchmark is . In Figures 1 and 2, we compare both the mean errors and RMSEs for Monte Carlo and RQMC. We observe that the mean error and RMSE for RQMC overlap considerably with a decay rate of nearly . RQMC yields a much better error rate of convergence compared to that of Monte Carlo. RQMC2 is actually an RQMC quadrature for the discontinuous function . The mean error of RQMC2 is very close to , as predicted by Proposition 3.4. Comparing RQMC and RQMC2, we find that the performance of the sensitivity estimator (2.4) is similar to that of the quadrature rule for the discontinuous function . Both share an error rate of nearly . Although RQMC2 is an unbiased estimate of , it needs to know the true value of which is impossible for most cases. Without the unbiasedness, the usual estimate (2.4) seems to be comparable to the unbiased one.

The analysis for a call option is similar. In this case, the option price at time is

| (4.9) |

and the derivative becomes

| (4.10) |

The numerical results are not reported in this paper for saving space.

4.2 Multiple Assets

In this subsection, we consider a portfolio of assets . The underlying asset prices follow a geometric Brownian motion. At time , the asset prices are

| (4.11) |

where is a -dimensional Brownian motion with correlation matrix , is the drift under the real-world distribution for the th asset, and is the associated volatility. It is clear that . Let be a decomposition of satisfying . Then can be simulated via

| (4.12) |

where and . By doing so, is a function of or .

Suppose that the portfolio is composed of European options, where the th option is written on the th asset with a maturity and a strike , . Denote the price of the th option at time by , which can be obtained via the Black–Scholes formula (4.2) or (4.9). The portfolio value loss at time is

where is the loss of the th option. The derivative is then

where can be obtained by (4.3) or (4.10) depending on the type of the option.

If components of are fixed and the remaining one , is a function of or . As a function of , by (4.2) and (4.9), its derivative can be expressed as a linear combination of terms like or , where are some constants. So the equation has a finite number of roots for . Since is infinitely times differentiable with respect to , is piecewise strictly monotonic with respect to (or equivalently ), verifying Assumption 2.3 (see Remark 3.10 for greater details).

We next focus on the growth condition required in Theorem 3.13. The remaining conditions in Theorem 3.13 can be easily verified. Since is a linear combination of , it suffices to verify the growth condition for . Without loss of generality, assume that the th option is a put option on the first asset, i.e., . By (4.11) and (4.12), we have

where are the entries of the matrix . From (4.3) and (4.10), we find that can be expressed as a function of , say . For any , is a linear combination of terms with the form , where , for any , and . Note that

for arbitrarily small . Taking the derivative of (4.8) times with respect to , we can see that is bounded by a linear combination of terms for constants and . This is due to the fact that is bounded for any nonnegative integer . Similar to (4.6), for any , and arbitrarily small ,

The growth condition for is thus satisfied with arbitrarily small rates . The RQMC-based CVaR sensitivity estimate yields a mean error rate of as confirmed by Theorem 3.13.

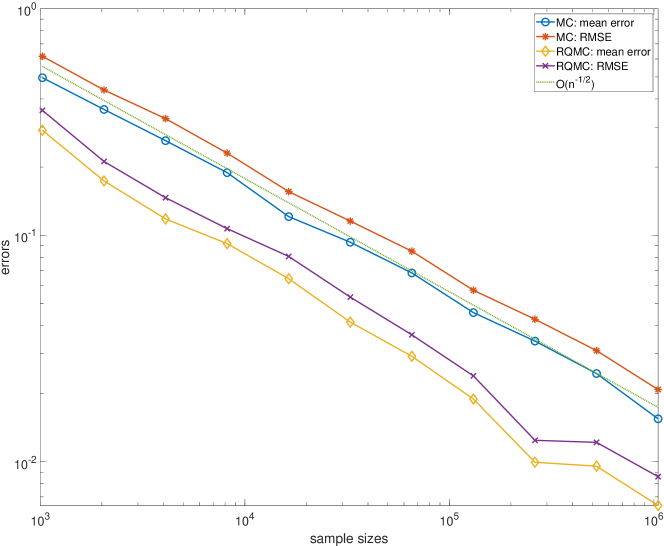

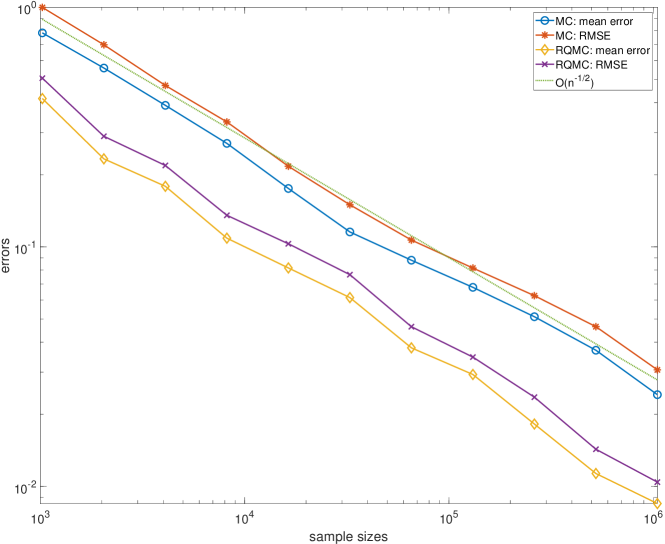

In the numerical study, we consider the following simple test portfolios:

-

•

Portfolio A. One call and one put options on independent underlying assets. Each option has a maturity of and a strike of . Each asset has an initial value of and a volatility of . The real-world interest rates are , and the risk-free interest rate is .

-

•

Portfolio B. Same as Portfolio A, but with each pair of underlying assets having correlation , i.e., for any .

The risk horizon we choose is again years, and we consider . For Portfolio A with independent assets, we take the matrix in (4.12). For Portfolio B with correlated assets, we take the principal components construction (Glasserman, 2004) for obtaining , that is where are the eigenvalues of the correlation matrix and are the corresponding eigenvectors of unit length. To get an accurate estimate as the benchmark, we run the RQMC method with 100 replications, each using a large sample size . Figures 3 and 4 show the convergence results of Monte Carlo and RQMC for the two portfolios, respectively. It is clear that RQMC performs better than Monte Carlo. The mean error rate of RQMC diminishes compared to the case of a single option. As predicted by the theoretical rate , RQMC suffers from the curse of dimensionality although the rate is asymptotically better than the Monte Carlo rate .

Sensitivity estimation of CVaR is more challenging for RQMC due to both discontinuity and high dimensionality. To overcome the impact of high dimensionality, some dimension reduction strategies are proposed in the literature (Wang and Tan, 2013; Weng et al., 2016). It is widely believed that RQMC can be very effective if the effective dimensions of the function is low (Caflisch et al., 1997). The decomposition of the correlation matrix is not unique, and it has an impact on the effective dimensions of the two important functions and . It therefore leaves room for choosing a proper matrix in (4.12) to reduce the effective dimensions. On the other hand, to overcome the impact of discontinuity, one may resort to some smoothing methods, such as conditioning (Zhang and Wang, 2019). RQMC enjoys a faster rate of convergence if the integrand is sufficiently smooth. He (2019) showed that RQMC together with conditioning achieves a mean error of for option pricing problems. We leave these strategies of improving RQMC efficiency for future research.

4.3 Delta-Gamma Approximation

Consider a portfolio of many assets (such as stocks, options) that depend on risk factors. Let denote the changes in the risk factors in a given time period . Hong and Liu (2009) studied a quadratic model

| (4.13) |

where , and are known. Assume that is positive definite, and with mean and covariance (also positive definite). The simple model (4.13) is actually the delta-gamma approximation of the loss studied in Section 4.2. Glasserman et al. (2000) used the approximation to guide the selection of effective variance reduction techniques in estimating VaR.

The mean and covariance are estimated from historical data. We are interested in estimating CVaR sensitive to the parameter for some . Let be a decomposition of the covariance. We may write

where and . It then gives

If components of are fixed, is a quadratic function of the remaining component, which is piecewise strictly monotonic. Assumption 2.3 is therefore verified. The derivative is then

where denotes the th row of the matrix and similarly for . It then follows by (4.5) and (4.7) that the growth condition for is satisfied with arbitrarily small rates. The RQMC-based CVaR sensitivity estimate yields a mean error rate of as confirmed by Theorem 3.13. The quadratic model (4.13) is much simpler than the model in Section 4.2. We do not report the numerical results here.

5 Conclusion

In this paper we found convergence rates of RQMC for CVaR sensitivity estimation. The theoretical results show that RQMC yields an asymptotically faster error rate than Monte Carlo, but the rate deteriorates as the dimension increases. It is important to note that the results we proved are the worst-case error rates. A good performance can be expected from RQMC in high dimensions if dimension reduction methods and smoothing methods are well utilized. We hope that the established theoretical results could be helpful for guiding a good way to improve plain RQMC.

Acknowledgments

This work was supported by the National Science Foundation of China (No. 12071154) and the Fundamental Research Funds for the Central Universities (No. 2019MS106).

6 Appendix

Lemma 6.1.

Let , where is a scrambled -net in base with . If Assumption 3.8 is satisfied, there are at most of the observations with equal value w.p.1.

Proof.

Suppose that are obtained by scrambling as described in (3.4). Assume that with unequal components on the th coordinate, i.e., . We write and in the -adic expansion, where . Let . For all , , but . Denote and as random permutations of and , respectively. According to the scrambling procedure (3.4), for all , and are independent because different permutations are applied. Recall that all permutations are independent. This implies that conditional on for all , and independently. This uniformity property can be proved as in the proof of (Owen, 1995, Proposition 2), which showed each . By Assumption 3.8, conditional on all with and for (denote these information as ), and are independent continuous random variables, implying . By the law of total expectation, we have

By the definition of -net, there are at most points of with equal value. For any two distinct points, the associated random observations of are different w.p.1. Consequently, there are at most of the observations with equal value w.p.1. ∎

Remark 6.2.

The constant may be conservative for some cases of . For example, a Sobol’ sequence is a -sequence in base . The value of depends on and is larger than 0 for moderately large ; see Dick and Niederreiter (2008) for detailed discussion. Direction numbers for generating Sobol’ sequences that satisfy the so-called Property A in up to 1111 dimensions have been given in Joe and Kuo (2008). Property A was introduced by Sobol (1976). If the unit cube is divided by the planes into equally-sized subcubes, then a sequence of points in satisfies Property A if, after dividing the sequence into consecutive blocks of points, each one of the points in any block belongs to a different subcube. This property guarantees that all the points are distinct. For this case, from the proof of Lemma 6.1, the constant can be replaced by .

References

- Ambrosio et al. (2008) L. Ambrosio, A. Colesanti, and E. Villa. Outer Minkowski content for some classes of closed sets. Mathematische Annalen, 342(4):727–748, 2008.

- Asimit et al. (2019) V. Asimit, L. Peng, R. Wang, and A. Yu. An efficient approach to quantile capital allocation and sensitivity analysis. Mathematical Finance, pages 1–26, 2019.

- Avramidis and Wilson (1998) A. N. Avramidis and J. R. Wilson. Correlation-induction techniques for estimating quantiles in simulation experiments. Operations Research, 46(4):574–591, 1998.

- Broadie and Glasserman (1996) M. Broadie and P. Glasserman. Estimating security price derivatives using simulation. Management science, 42(2):269–285, 1996.

- Broadie et al. (2011) M. Broadie, Y. Du, and C. C. Moallemi. Efficient risk estimation via nested sequential simulation. Management Science, 57(6):1172–1194, 2011.

- Caflisch et al. (1997) R. E. Caflisch, W. J. Morokoff, and A. B. Owen. Valuation of mortgage backed securities using Brownian bridges to reduce effective dimension. Journal of Computational Finance, 1(1):27–46, 1997.

- Cui et al. (2019) Z. Cui, M. C. Fu, J. Hu, Y. Liu, Y. Peng, and L. Zhu. On the variance of single-run unbiased stochastic derivative estimators. INFORMS Journal on Computing, 32(2):390–407, 2019.

- Dick and Niederreiter (2008) J. Dick and H. Niederreiter. On the exact t-value of Niederreiter and Sobol’ sequences. Journal of Complexity, 24(5-6):572–581, 2008.

- Dick and Pillichshammer (2010) J. Dick and F. Pillichshammer. Digital Nets and Sequences: Discrepancy Theory and Quasi–Monte Carlo Integration. Cambridge University Press, 2010.

- Dong and Nakayama (2017) H. Dong and M. K. Nakayama. Quantile estimation with latin hypercube sampling. Operations Research, 65(6):1678–1695, 2017.

- Fox and Glynn (1989) B. L. Fox and P. W. Glynn. Replication schemes for limiting expectations. Probability in the Engineering and Informational Sciences, 3:299–318, 1989.

- Fu et al. (2009) M. C. Fu, L. J. Hong, and J.-Q. Hu. Conditional Monte Carlo estimation of quantile sensitivities. Management Science, 55(12):2019–2027, 2009.

- Glasserman (2004) P. Glasserman. Monte Carlo Methods in Financial Engineering. Springer, 2004.

- Glasserman et al. (2000) P. Glasserman, P. Heidelberger, and P. Shahabuddin. Variance reduction techniques for estimating value-at-risk. Management Science, 46(10):1349–1364, 2000.

- Gordy and Juneja (2010) M. B. Gordy and S. Juneja. Nested simulation in portfolio risk measurement. Management Science, 56(10):1833–1848, 2010.

- He (2018) Z. He. Quasi-Monte Carlo for discontinuous integrands with singularities along the boundary of the unit cube. Mathematics of Computation, 87(314):2857–2870, 2018.

- He (2019) Z. He. On the error rate of conditional quasi–Monte Carlo for discontinuous functions. SIAM Journal on Numerical Analysis, 57(2):854–874, 2019.

- He and Wang (2015) Z. He and X. Wang. On the convergence rate of randomized quasi–Monte Carlo for discontinuous functions. SIAM Journal on Numerical Analysis, 53(5):2488–2503, 2015.

- He and Wang (2020) Z. He and X. Wang. Convergence analysis of quasi-Monte Carlo sampling for quantile and expected shortfall. Mathematics of Computation, 2020. Appeared online.

- Hong (2009) L. J. Hong. Estimating quantile sensitivities. Operations research, 57(1):118–130, 2009.

- Hong and Liu (2009) L. J. Hong and G. Liu. Simulating sensitivities of conditional value at risk. Management Science, 55(2):281–293, 2009.

- Hong et al. (2014) L. J. Hong, S. Juneja, and J. Luo. Estimating sensitivities of portfolio credit risk using Monte Carlo. INFORMS Journal on Computing, 26(4):848–865, 2014.

- Hull (2015) J. C. Hull. Options, Futures, and Other Derivatives. Pearson, 2015.

- Jiang and Fu (2015) G. Jiang and M. C. Fu. Technical note–On estimating quantile sensitivities via infinitesimal perturbation analysis. Operations Research, 63(2):435–441, 2015.

- Joe and Kuo (2008) S. Joe and F. Y. Kuo. Constructing Sobol sequences with better two-dimensional projections. SIAM Journal on Scientific Computing, 30(5):2635–2654, 2008.

- Joy et al. (1996) C. Joy, P. P. Boyle, and K. S. Tan. Quasi-Monte Carlo methods in numerical finance. Management Science, 42(6):926–938, 1996.

- Kaplan et al. (2019) Z. Kaplan, Y. Li, M. Nakayama, and B. Tuffin. Randomized quasi-Monte Carlo for quantile estimation. In Proceedings of the 2019 Winter Simulation Conference, pages 1–14, 2019.

- L’Ecuyer and Lemieux (2005) P. L’Ecuyer and C. Lemieux. Recent advances in randomized quasi-Monte Carlo methods. In M. Dror, P. L’Ecuyer, and F. Szidarovszky, editors, Modeling Uncertainty: An Examination of Stochastic Theory, Methods, and Applications, pages 419–474. Kluwer Academic Publishers, 2005.

- Matoušek (1998) J. Matoušek. On the -discrepancy for anchored boxes. Journal of Complexity, 14(4):527–556, 1998.

- Niederreiter (1992) H. Niederreiter. Random Number Generation and Quasi-Monte Carlo Methods. SIAM, Philadelphia, 1992.

- Owen (1995) A. B. Owen. Randomly permuted -nets and -sequences. In H. Niederreiter and P. J.-S. Shiue, editors, Monte Carlo and Quasi-Monte Carlo Methods in Scientific Computing, pages 299–317. Springer, 1995.

- Owen (1997a) A. B. Owen. Monte Carlo variance of scrambled net quadrature. SIAM Journal Numerical Analysis, 34(5):1884–1910, 1997a.

- Owen (1997b) A. B. Owen. Scrambled net variance for integrals of smooth functions. The Annals of Statistics, 25(4):1541–1562, 1997b.

- Owen (2005) A. B. Owen. Multidimensional variation for quasi-Monte Carlo. In J. Fan and G. Li, editors, International Conference on Statistics in honour of Professor Kai-Tai Fang’s 65th birthday, pages 49–74, 2005.

- Owen (2006) A. B. Owen. Halton sequences avoid the origin. SIAM Review, 48(3):487–503, 2006.

- Owen (2008) A. B. Owen. Local antithetic sampling with scrambled nets. The Annals of Statistics, 36(5):2319–2343, 2008.

- Owen and Rudolf (2020) A. B. Owen and D. Rudolf. A strong law of large numbers for scrambled net integration. arXiv preprint arXiv:2002.07859, 2020.

- Patel and Read (1996) J. K. Patel and C. B. Read. Handbook of the Normal Distribution, volume 150. Marcel Dekker, New York, 1996.

- Peng et al. (2018) Y. Peng, M. C. Fu, J.-Q. Hu, and B. Heidergott. A new unbiased stochastic derivative estimator for discontinuous sample performances with structural parameters. Operations Research, 66(2):487–499, 2018.

- Scaillet (2004) O. Scaillet. Nonparametric estimation and sensitivity analysis of expected shortfall. Mathematical Finance, 14(1):115–129, 2004.

- Serfling (1980) R. J. Serfling. Approximation theorems of mathematical statistics. Wiley, New York, 1980.

- Sobol (1976) I. M. Sobol. Uniformly distributed sequences with an additional uniform property. USSR Computational Mathematics and Mathematical Physics, 16(5):236–242, 1976.

- Wang and Tan (2013) X. Wang and K. S. Tan. Pricing and hedging with discontinuous functions: Quasi–monte carlo methods and dimension reduction. Management Science, 59(2):376–389, 2013.

- Weng et al. (2016) C. Weng, X. Wang, and Z. He. An auto-realignment method in quasi-Monte Carlo for pricing financial derivatives with jump structures. European Journal of Operational Research, 254(1):304–311, 2016.

- Xie et al. (2019) F. Xie, Z. He, and X. Wang. An importance sampling-based smoothing approach for quasi-Monte Carlo simulation of discrete barrier options. European Journal of Operational Research, 274(2):759–772, 2019.

- Zhang and Wang (2019) C. Zhang and X. Wang. Quasi-Monte Carlo-based conditional pathwise method for option greeks. Quantitative Finance, pages 1–19, 2019.