Counterfactual Distribution Regression

for Structured Inference

Abstract

We consider problems in which a system receives external perturbations from time to time. For instance, the system can be a train network in which particular lines are repeatedly disrupted without warning, having an effect on passenger behavior. The goal is to predict changes in the behavior of the system at particular points of interest, such as passenger traffic around stations at the affected rails. We assume that the data available provides records of the system functioning at its “natural regime” (e.g., the train network without disruptions) and data on cases where perturbations took place. The inference problem is how information concerning perturbations, with particular covariates such as location and time, can be generalized to predict the effect of novel perturbations. We approach this problem from the point of view of a mapping from the counterfactual distribution of the system behavior without disruptions to the distribution of the disrupted system. A variant on distribution regression is developed for this setup.

1 Introduction

1.1 Contribution

Consider a complex system such as the London Underground, a large network of fast trains for the daily commute of passengers. Measures such as the number of passengers exiting at each station can be used to quantify the behavior of the system. Unplanned disruptions sometimes happen, which stop trains from running within particular segments of the network. A local disruption has effects elsewhere in the system, primarily in stations adjacent to the disrupted region. As discussed by Silva et al. (2015), there is enough structure in the system such that past disruptions can inform predictions of what will happen under a novel disruption that takes place at a previously unseen location.

We will call a perturbation, or shock, any kind of external event that directly changes a particular mechanism in the system. For instance, a signal failure in the Underground will stop trains from navigating through particular rails. Even though the local nature of the perturbation can be assumed to be known, with obvious immediate effects (e.g., no trains in particular lines), a perturbation will also have effects elsewhere in the system, which may need to be learned from data. For instance, passengers who cannot reach a particular destination may decide to leave at a different location. The number of passengers exiting a station may go up or down depending on the flow of passengers quitting earlier or not being able to reach it. Assuming access to a historical database of past disruptions and assumptions about invariances of particular components of the system, a model can estimate the effect of line closures on passenger behavior, a quantity of interest for policies that attempt to mitigate the effect of such perturbations (such as crowd management and compensation for excess demand by auxiliary services such as buses).

In this paper, we consider the general setting of building predictive models for the effects of perturbations on a system. We borrow concepts from causal inference, in particular counterfactual modeling, where given a model for the “natural regime” of the system, i.e., its usual dynamics, at the moment of a shock we generate a distribution over counterfactual outcomes, which is a probabilistic assessment of its possible trajectories had no shock taken place, given the history of the system up to that moment. We assume the existence of a mapping from the counterfactual distribution of a set of variables in the system to the “factual” distribution of target system variables, indexed by covariates describing the perturbation.

1.2 Setup

Consider a probability distribution , where is a given function space, describing the natural regime of an observed -dimensional random variable, i.e., . The distributions is defined over an undirected graph, , with a set of vertices such that , and where the edge set forms an adjacency matrix . Within the context of our working example, denotes whether stations and are physically adjacent in the London Underground, otherwise, with being the number of passengers exiting at station within a given time window.

The natural regime can be perturbed by external events. The goal is to predict changes induced by such external events on . Let be the perturbed distributions associated with such events. We assume the th perturbation to be fully characterized by set of features , where can be interpreted as the set of locations where the perturbation is applied to the network and belongs to an arbitrary feature space . In general, a perturbation may affect all via indirect effects that depend on the graph structure. In the simplest setting, for example, one can assume a perturbation applied to to have visible effects to all such that .

Given a dataset of observations from the natural regime

| (1) |

and a dataset of observations and features from different perturbed regimes

| (2) |

we describe a method where when a new perturbation applied to node , it predicts (marginals of) distribution describing the system measurements under the new perturbation . We define perturbations as applied to single nodes, thus allowing real-world events to generate multiple perturbation data points.

The core methodology is to cast as the output of a distribution regression model (Sutherland et al., 2012), a class of regression models where the covariates are the corresponding natural regime distribution , the perturbation features and the adjacency matrix . More explicitly, we seek a model , such that we can predict the exit counts distribution under a new unseen perturbation associated with features by letting

| (3) |

where is a “counterfactual” distribution, i.e., the distribution of system variables had no disruption taken place. Unlike standard regression models, is an unobservable structured covariate that is estimated from the data at hand. This data is independent of the data used in the estimation of (3), as they represent different regimes.

1.3 Relationship to Causal Modeling

Equation (3) is motivated by predictive causal modeling problems where given data from the observational regime of a system and from (possibly) a set of experiments, we infer the predictive distribution of the outcomes of a system under an intervention. These problems can be found in the machine learning literature (Spirtes et al., 2000; Pearl, 2000) and in some recent advances in the statistics literature such as Peters et al. (2016). In our approach, we do not directly target the estimation of causal effects, such as the difference in expected outcomes between two levels of treatment (Imbens and Rubin, 2015). Instead, given a disruption (which can be interpreted as type of natural experiment, Dunning, 2012), we predict what will happen to a system in a near future. The counterfactual state of the system, i.e., its probabilistic behaviour had no disruption taken place, plays an important role, but only as a useful covariate that can aid prediction.

The distribution of outcomes under an intervention can be inferred by combining observational data and data from the system under interventions. In the context of causal graphical model (Pearl, 2000; Spirtes et al., 2000), the operational definition of an intervention is the modification of one of the factors of the observational distribution function, which factorizes according to a directed causal graph. Assuming that the density function exists, the causal graph implies that the joint density function is given by the product of conditional density functions , where are the parents (direct causes) of in the graph (Pearl, 2000). An intervention on changes into some . Conditional densities can also be expressed in terms of equations , where are unobservable causes of . For example, an intervention on a random variable is said to be perfect if it replaces its natural regime equation, say , by the equation for some constant . This is to be contrasted with a soft intervention, which modifies the equation for while keeping a dependence on at least some of its direct causes. For example, a soft intervention on that weakens its response with respect to one of its direct causes can be modelled parametrically by a regime parameter , as in . A modelling choice is to assume that this parameter appears on interventions at other variables , as an example of sharing statistical strength between different interventions. See Spencer et al. (2015) for a recent example of this approach to modelling in applied biology, and early work by Cooper and Yoo (1999) and Tian and Pearl (2001) on causal inference by combining multiple interventions and natural experiments. In particular, parameters for the natural regime, such as , are also present in the modelling of the interventional regime. It is explicit here that the natural regime informs the interventional one.

Modeling the predictive distribution of soft interventions by first learning of a full causal graphical model requires assumptions about how such interventions interact with unobserved causes . In our example above, the contribution of was left unchanged. This type of modelling is particularly difficult if the different unobserved causes are confounded, possibly requiring strong assumptions about the parametric shape of such interventions. This is not necessary in our setup because we are not trying to estimate a full causal graphical model, which encodes the effect of perfect interventions and how unmeasured confounding takes place. Instead, our assumption is that perturbations come from a family of interventions where invariance (3) holds, while making no claims concerning the representation of perfect interventions and arbitrary causal effects. This assumption requires that we have access to a set of datasets collected under different perturbations, including the natural regime, so that predictions can be made on a new unseen perturbation that is different from the existing ones but which is assumed to fit within the postulated relationship.

In particular, our graph is not a causal graph in the sense of encoding the Causal Markov condition (Spirtes et al., 2000), but a symmetric graph of physical constraints as in the analysis of interference in social networks and spatial effects (see e.g. Aronow et al., 2017; Aronow and Samii, 2017). The graph is assumed as part of the data, as opposed to a quantity to be estimated. Physical-constraint graphs can be used to inform the learning of a causal graph as done by Novershtern et al. (2011), but here we are interested solely in predicting the effect of natural experiments coming from an unknown set of soft interventions. Equation (3) replaces the typical assumptions of invariances in causal graphical modelling with a more black-box approach for predictive modelling under regime changes. By using Equation (3), we assume that there is a common real-world meaning for the elements in this class of perturbations, such as each element is an unplanned partial line closure in the London Underground.

Traditional counterfactual models (Imbens and Rubin, 2015) postulate a joint distribution among potential outcomes. While in principle we could derive relationship (3) not only from an explicit model for soft interventions, but also from an explicit latent variable for the joint distribution of potential outcomes, this again requires strong assumptions, some of which are untestable since only one potential outcome is observable at a time. However, by exploiting the distribution of the counterfactuals as inputs to outcomes of interest, as opposed to using the latent values of the counterfactuals, we sidestep the computational complexity of modelling the distribution of the observed disrupted variables as the marginal of a possibly high-dimensional missing data model.

1.4 Relationship to Standard Distribution Regression

Our problem is formulated as a distribution regression problem whose theoretical and practical aspects have been largely addressed in the literature (Sutherland et al., 2012; Lampert, 2015; Szabó et al., 2016; Law et al., 2018). To the best of our knowledge, the definition of a perturbation map has not been considered in the past. The perturbation map can be interpreted as a distribution regression where both the regressor and the output are distributions, unlike the classical setting (Sutherland et al., 2012) where the input are sets of observations. The goal is to estimate a mapping between the input and output distributions.

2 Method

2.1 Distribution-to-distribution regression model

Let be a probability distribution defined over the product function space . A distribution-to-distribution regression model is a functional such that

| (4) |

where is the expectation of with respect to the joint distribution . For simplicity, we consider the case of a single input distribution. Handling multidimensional inputs is conceptually a direct extension.

2.2 Reproducing kernel Hilbert spaces

We follow the framework of casting distribution regression in terms of reproducible kernel Hilbert spaces (Muandet et al., 2017). A vector space with inner product is an Hilbert space if it is complete with respect to the norm defined by , for all .

Given an input space , a reproducing kernel Hilbert space (RKHS) over is an Hilbert space of functions that satisfy the additional smoothness condition

| (5) |

A RKHS is completely characterized by its reproducing kernel, a symmetric and positive-definite function that satisfies the reproducing property,

| (6) |

This implies , where is usually referred to as the canonical feature map .

2.3 RKHS embedding of distributions

The canonical feature map can be used to obtain an Hilbert space representation of any element of the input space . Let be a probability distribution defined over . Its Hibert space representation is then defined by

| (7) |

and it is called the RKHS mean embedding of . Under mild conditions on , is such that (Smola et al. (2007))

| (8) |

If is a characteristic kernel, the map is injective and

| (9) |

For example, both the Laplace and Gaussian kernels defined by and are characteristic on . More generally, a kernel is characteristic if it is translation invariant and its Fourier transform has support over the whole space (see Sriperumbudur et al. (2010) and also Fukumizu et al. (2004) for more details on the definition of the class of characteristic kernels.). For any distribution , an empirical estimation of is

| (10) |

It can be shown that is an unbiased estimate of (Sriperumbudur et al., 2012) and

| (11) |

2.4 Regression in the Hilbert space

Given a distribution-to-distribution regression model, , and a kernel function that is characteristic on , the RKHS regression model, , is a linear operator from the RKHS of to the RKHS of .

Definition 1 (Non-parametric model).

The non-parametric model is a linear operator implicitly defined by , where are realizations of .

Given a dataset of samples drawn from a set of input-output distributions

| (12) |

let (). Then the optimal RKHS regression model is

| (13) |

The empirical mean embeddings are obtained from (12) via (10). Note that, for finite , the operator acts non-trivially only on the -dimensional subspace spanned by the columns of , which is assumed to have full column rank.

Lemma 1 (Estimation of the non-parametric model).

2.5 Finite-dimensional parametrizations of

In some cases, as in the experiments shown in Section 3, one may prefer to choose a finite-dimensional parametrization of . Here, we give two examples where structural assumptions are made directly on the RKHS linear operator . The alternative approach where structural constraints are imposed directly on the distribution-to-distribution regression model, , is in general harder and will be considered in Section 2.6. Here, we assume for simplicity that all and belong to the same function space, i.e., where and and focus on two specific models: a one-parameter model, where the RKHS operator is defined by for all and and a mixture of mean embeddings, where the RKHS operator is defined by , for all , .

Definition 2 (One-parameter model).

The one-parameter model is a linear operator defined by

| (16) |

where the RKHS identity operator is defined by for any .

This is the simplest possible non-trivial linear operator in . Given the training sample, , a least-squares estimate of the free parameter is

| (17) |

where , for all and .

Lemma 2 (Estimation of the one-parameter model).

Definition 3 (Mixture of embeddings).

The mixture of embeddings model is a linear operator defined by

| (20) |

where ().

Given a meta-distribution we consider the dataset

| (21) |

the least-squares estimate of is

| (22) |

where the empirical mean embeddings are obtained from and we assume that is big enough for the matrix to be full rank.

Lemma 3 (Estimation of the mixture of embedding model).

Remark 1.

To simplify the notation we assume that an equal number of samples from and each (, is available.

Remark 2.

The mixture of embeddings model defined in Definition 3 is an example of regression model, and , which takes multiple inputs. This is the model class we have used in the application described in Section 3.1 and corresponds to a distribution-to-distribution regression model , i.e., , where the expectation is over the meta-distribution generating dataset defined in (2.5).

Remark 3.

Even for the simple RKHS linear operators defined in this section, it is not straightforward to obtain an explicit form of the corresponding distribution-to-distribution regression model, , which is defined implicitly by . Even when all have a density, it cannot be guaranteed that the outputs of such a model, , also have a density.

2.6 Direct parametrization of

A more intuitive way of defining a model class is to impose a structure directly on the distribution-to-distribution functional, . The drawback of this approach is the need to find the structure of the corresponding RKHS linear operator . This is in general a highly non-trivial task as the constraints on are expressed in equations involving expectations of the kernel function with respect to the input and output distributions. More concretely, given , the task is to find such that

| (25) |

A special case where a possible parametric version of can be obtained directly from the corresponding parametric version of is when is a mixture of distributions, i.e.,

| (26) |

In this case, we need to solve

| (27) |

where . A possible solution is a linear operator as defined below.

Definition 4 (Mixture of distributions model).

The mixture of distributions model is a linear operator , , defined by

| (28) |

where is the identity operator defined in Definition 2.

2.7 Sampling from the mean embedding

Samples from the mean embedding of a distribution are often obtained via herding, which requires to solve a non-convex optimization problem for each new sample. It is known that herding becomes expensive and unreliable in high dimensions. Here, we propose an alternative method that only requires solving a single simplex-constrained convex minimization.

Suppose we are given the empirical mean embedding, , of an unknown distribution, , but have no access to its samples. In the distribution-to-distribution settings described here, is the output of the RKHS regression model, i.e., , but what follows may apply to more general cases. The task is to reconstruct the unavailable samples of .

The strategy is to choose a basis for the target functions space and to approximate the target distribution with an approximating mixture of elements from such a basis. The resulting empirical mean embedding is then used to compute an estimate of the mixture’s coefficients by solving a regression problem in the RKHS of . This is possible because the parameters of the mixture of distributions and the corresponding mixture of embeddings can be chosen to be the same, as we have shown in Section 2.6. Finally, approximate samples from are obtained by sampling from the obtained approximating mixture.

Lemma 5 (Mean embedding sampling).

Let be a given empirical mean embedding and the unknown distribution associated with . Let be a suitable finite-dimensional basis of the functions space and assume it is possible to sample from all (). Then approximate samples from are the realizations of

| (32) |

where is defined in (29) and is the empirical embedding computed from the samples of ().

Lemma 6 (Consistency of the sampling scheme).

Let be a set of samples from (usually unavailable) and a dataset of samples from the approximating mixture defined in Lemma 5. Then

| (33) |

where , and is a measure of the distance between and .

3 Implementation and experiments

3.1 Spatial interference via distribution regression

The general scheme proposed in Section 2 can be straightforwardly adapted to tackle the causal interference task outlined in Section 1.2. Let be the adjacency matrix of a graph with nodes and an observed random variable defined on . The task is to model the distribution of under perturbations applied at given nodes of . For simplicity, perturbations are assumed to be fully characterized by their “centre node”, , but dependencies on extra features and possible extended “centre regions” can be included without major changes. We seek a distribution-to-distribution regression model, , whose input are the adjacency matrix of the graph, , the perturbation centre, , and the distribution of when no perturbations are active, . We also assume that and the target distribution belong to the same function space, . Because of the added dependence on the graph structure we call a spatial interference distribution-to-distribution model (see Section 1.2) The underlying assumption is the existence of a meta-distribution, such that and

| (34) |

where , , . The regression model is then a map from to . The task is to learn given the datasets , and , where ().

Step 1 (Preprocessing).

Reformulate the problem to frame it into the mixture of embeddings regression tasks described in Section 2.5. For each perturbation, we form a set of input distributions that depend on and the distribution features, i.e.,

| (35) |

Since we only need a dataset of samples from the input distributions, the functionals are not required to have an explicit form. Let be the distributions describing a set of random variables, , that depend deterministically on and the perturbation features. For example, we can let be defined by

| (36) |

where and is the length of the path connecting and on . While figuring out a functional form of is generally difficult, we can easily compute the corresponding empirical mean embeddings, , as in (10) given the realization datasets (, ) obtained deterministically from according to (36). The mean embedding of the observed output distributions to be used for training are computed as in (10) from .

Step 2 (RKHS inference).

Learn a model that relates the input embeddings, , to the outputs, . As mentioned in Remark 2 of Section 2.5, we choose a mixture of embeddings model (see Definition 3) with estimated parameter (22). Then use the trained model to compute the mean embedding of , which is the distribution associated with a new unseen perturbation centered in . To make the prediction, we first need to form the sample datasets corresponding to the input distributions, , associated with the centre of the new disruption, , and computed from as in (36). From such sample datasets we can compute the empirical embeddings of and let

| (37) |

Step 3 (Sampling from the model’s output).

In order to compute approximate samples from , define a basis for the function space of the target distribution, . A possible simple choice is to use the marginals of the input distributions

| (38) |

where the canonical basis vectors are defined by (), with being the Kronecker delta. The empirical embeddings of the function space basis are obtained from , which in turn are obtained from . More precisely, we compute the datasets defined by

and compute the corresponding (, ) as in (10). Then, define an approximating mixture (, ) of and estimate the corresponding mixture weights as described in Section 2.7. Approximated samples from are then the realizations of , where

| (39) |

3.2 Modelling perturbations in the London Underground

The predictive power of the distribution regression interference model outlined in Section 3.1 is tested on a real-world data consisting of observed exit counts from the London underground. We consider a graph with nodes corresponding to the stations in the whole London Underground (all 11 underground lines are included) and adjacency matrix defined by

| (42) |

The natural regime dataset, , consists of days of input-output records from late 2013

| (43) |

where () is the number of journey records for , the ‘observation’ time window, and the origin and destination journey , and and the corresponding starting and exit times. We have access to the features of observed disruptions

| (44) |

where is the disruption’s day, the disruption’s starting and ending times and (“region of interest”) the list of stations that are endpoints of some disrupted link.

For each day and each minute in a day, we compute the number of journeys completed between station and station

| (45) |

which can be interpreted as exchangeable samples of a natural regime random variable (for each disruption, we exclude the sample associated with the disruption day). For each disruption , we want to describe a random variable , associated with the number of exits in region of interest. Here we have access to a single realization, , of , which is defined by

| (46) |

where is defined in (45). We let the input variables associated with the -th output, , be the probability distributions, , associated with a set of random variables , where are deterministic function of . In particular, we choose and defined by

| (47) | ||||

where , , if is verified and zero otherwise, with being the distance between and computed on the graph associated with adjacency matrix , the adjacency matrix corresponding to disruption defined by

| (50) |

a threshold and for all . In terms of the new variables, the network interference problem presented in Section 1.2 is reformulated as a standard RKHS distribution-to-distribution regression of the type analyzed in Section 2

| (51) |

The estimation of the regression model and the approximate sampling from a predicted perturbed distribution are obtained as in Section 2 and 3.1. In particular, as the support of the output distributions depends on the features of the new disruption, , i.e., (), the following features-specific basis is constructed from a set of rescaled marginals of :

| (52) |

where , , , , , , and .

3.3 Empirical results

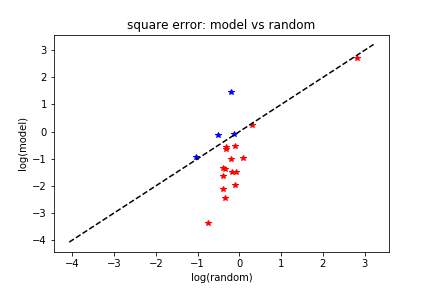

To test the London Underground model outlined in Section 3.2, we have created a reduced dataset of disruptions by selecting the disruptions with highest observable score

| (53) |

where , are the distributions describing the input random variables defined in (47) and the corresponding realizations sets obtained from the normal regime datasets defined in (43). The observable score for disruption depends on the difference between (, ), the number of people exiting at from paths that are feasible on the disruption day, i.e., for , and (, , and the number of people exiting at from paths that are infeasible on the disruption day. We refer to this score as ‘observable’ because it can be computed before measuring the effects of a disruption, given the disruption’s features and the natural regime datasets (43). The score is a proxy for the ‘unobservable’ severity score

| (54) |

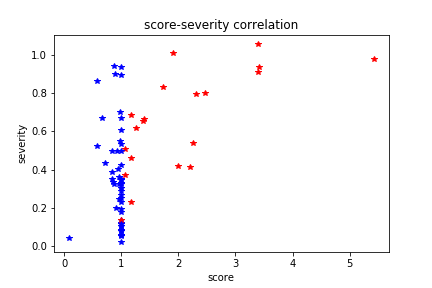

where , , defined in (43), . The severity score is unobservable because it is not available before observing the effects of a disruption. Figure 1 shows the approximate correlation between observable scores and true severity scores, with disruptions selected for the experiment marked in red.

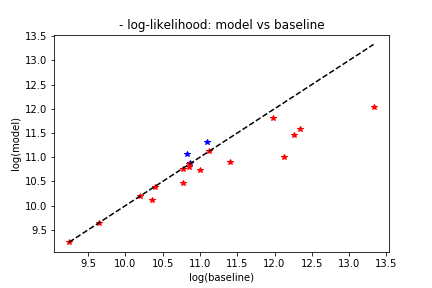

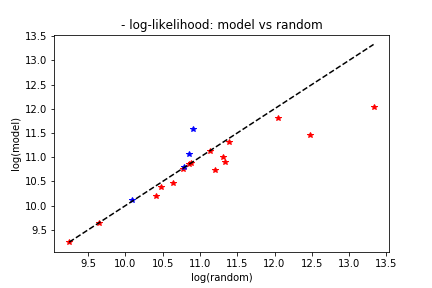

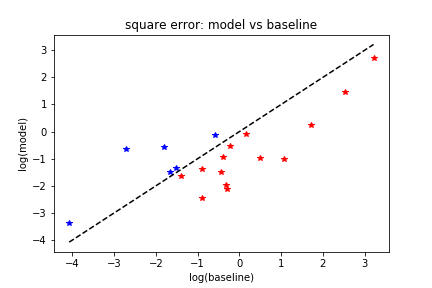

The model evaluation has been performed by splitting the dataset of selected disruptions in subsets and running training-evaluation instances. Each instance corresponds to a different test set, with the model trained on the remaining nine subsets. Thus, all averages and log-likelihood evaluations reported in Figures 2, 3, 4 and 5 are out-of-sample predictions, with models tested on disruptions that were not used for training. For computational efficiency, the value of the kernel parameter was obtained through cross-validation over the all sample and kept fixed over all training-testing instances. The usual procedure would be to fix by cross-validation on the training set of each training-testing instance. Figure 2 and 3 show the predictive performance of the proposed model against a baseline model and a set of random models. The baseline model is the empirical distribution obtained from the natural regime dataset. The random models are obtained by letting be a realization of in the definition of the approximating mixtures needed for sampling (with the same basis elements used for the proposed model). Figure 4 and 5 compare the shapes of station-specific densities associated with the proposed model and the baseline (densities associated with the random models are all similar and removed for visual reasons.). Predictions and log-likelihood evaluations are all (pseudo-)empirical estimations obtained by sampling from the models according to the sampling procedure described in Section 2.7. For the baseline model we used are the true natural regime’s samples. Let , where is the output of the proposed regression model with being the approximating mixture described in Section 3.1 and the estimated mixing weights vector (39), is the random model mentioned above with being the approximating mixture described in Section 3.1 and random weights and is the baseline model defined implicitly by , (, , , ). For each , all models output a multivariate distribution, , describing a vector-valued random variable . The station-specific marginal densities (, ) shown in Figure 4 and 5 are computed through the entry-wise density estimators

| (55) |

where is a set of realizations of () and is a smoothing parameter.

Acknowledgements

We thank Transport for London for kindly providing access to data. This work was supported by a ESPRC grant EP/N020723/1 to NC, RS and SMK. AG acknowledges funding from the Gatsby Charitable Foundation. RS received further support from the Alan Turing Institute, under the EPSRC grant EP/N510129/1.

Appendix

Proofs

Proof of Lemma 1:

Assume that the meta-distribution introduced in (4) can be represented by a unique RKHS linear operator such that

| (56) |

for any possible pair of input-output distributions . For simplicity, we assume that (14) holds exactly but misspecification terms can also be added with minor changes to the following. Assumption (14) implies directly

| (57) |

where the empirical mean embeddings are associated with the dataset defined in (12). The error terms obey

| (58) |

where . Equation (57) implies

| (59) |

For any , we define

| (60) |

which are the subspaces of spanned by the columns of . We prove the consistency of the estimator (13) as a map between and as follows

| (61) | |||||

| (62) | |||||

| (63) | |||||

| (64) | |||||

| (65) | |||||

| (66) |

where

| (67) |

This implies and hence the statement.

Proof of Lemma 2:

Assuming an exact model for all , implies

| (68) |

where obey

| (69) |

with (). This implies

| (70) |

and hence , where

| (71) |

Then

| (72) | |||||

| (73) | |||||

| (74) | |||||

| (75) |

Proof of Lemma 3:

When (20) holds exactly, it implies

| (76) |

with obeying

| (77) | |||||

| (78) | |||||

| (79) |

and . This implies

| (80) | |||||

| (81) | |||||

| (82) | |||||

| (83) | |||||

| (84) | |||||

| (85) |

Proof of Lemma 4:

Let the meta-distribution generating the realizations dataset be such that

| (86) |

for any . Equation (27) and Definition 4 imply that the meta-distribution is also such that

| (87) |

for any . This means that can be estimated by solving a RKHS linear least-squares problem analogous to the one defined in (22). Moreover, as belongs to a sub-class of the models defined in Definition 3, the consistency of (29) can be obtained directly from Lemma 3 by adding the extra constraint , with defined in (29). Since is a convex constraint, the solution, , of (29) is unique and, for any , obeys

| (88) |

where is the solution of the unconstrained problem (22) and the equality follows from Lemma 3.

Proof of Lemma 5:

Let be a given empirical mean embedding, the unknown distribution associated with and a suitable finite-dimensional basis of the functions space . Then can be approximated by a superposition of

| (89) |

where denotes the part of that is not captured by . From Section 2.6, this implies

| (90) |

where are the mean embeddings of and the mean embedding of the error term. Assume we can sample from the basis distributions and let

| (91) |

be the corresponding realizations datasets. Then we can compute the associated empirical mean embeddings as in (10) and obtain an estimate of the unknown mixture weights from

| (92) |

For small we have and samples from can be obtained as realizations of a random variable described by the obtained mixture

| (93) |

Proof of Lemma 6:

Let be the approximating mixture defined in Lemma 5. Let measure the discrepancy between the target distribution and the best possible approximating mixture (). Similarly, we can let be defined by

| (94) |

where and is such that the equality in (94) holds. We want to show that the difference between the empirical expectation of an arbitrary RKHS function, , with respect with the target distribution, , and the empirical expectation of obtained from the sampling procedure described by Lemma 5 tends to zero when , , , with and defined in Lemma 6. From the definitions in Lemma 6 we have

| (95) | |||||

| (96) | |||||

| (97) | |||||

| (98) | |||||

| (99) |

References

- Aronow and Samii [2017] Peter M Aronow and Cyrus Samii. Estimating spatial effects. Unpublished manuscript, 2017.

- Aronow et al. [2017] Peter M Aronow, Cyrus Samii, et al. Estimating average causal effects under general interference, with application to a social network experiment. The Annals of Applied Statistics, 11(4):1912–1947, 2017.

- Cooper and Yoo [1999] G. Cooper and C. Yoo. Causal discovery from a mixture of experimental and observational data. Proceedings of the 15th conference on Uncertainty in Artificial Intelligencem (UAI-1999), pages 116–125, 1999.

- Dunning [2012] T. Dunning. Natural Experiments in the Social Sciences: A Design-Based Approach. Cambridge University Press, 2012.

- Fukumizu et al. [2004] Kenji Fukumizu, Francis R Bach, and Michael I Jordan. Dimensionality reduction for supervised learning with reproducing kernel hilbert spaces. Journal of Machine Learning Research, 5(Jan):73–99, 2004.

- Imbens and Rubin [2015] G. Imbens and D. Rubin. Causal Inference for Statistics, Social, and Biomedical Sciences: An Introduction. Cambridge University Press, 2015.

- Lampert [2015] Christoph H Lampert. Predicting the future behavior of a time-varying probability distribution. In Proceedings of the IEEE Conference on Computer Vision and Pattern Recognition, pages 942–950, 2015.

- Law et al. [2018] Ho Chung Leon Law, D Sutherland, Dino Sejdinovic, and Seth Flaxman. Bayesian approaches to distribution regression. population, 2:3, 2018.

- Muandet et al. [2017] Krikamol Muandet, Kenji Fukumizu, Bharath Sriperumbudur, Bernhard Schölkopf, et al. Kernel mean embedding of distributions: A review and beyond. Foundations and Trends® in Machine Learning, 10(1-2):1–141, 2017.

- Novershtern et al. [2011] N. Novershtern, A. Regev, and N. Friedman. Physical module networks: an integrative approach for reconstructing transcription regulation. Bioinformatics, 27:177–185, 2011.

- Pearl [2000] J. Pearl. Causality: Models, Reasoning and Inference. Cambridge University Press, 2000.

- Peters et al. [2016] J. Peters, P. Buhlmann, and N. Meinshausen. Causal inference using invariant prediction: identification and confidence intervals (with discussion). Journal of the Royal Statistical Society: Series B, 78:947–1012, 2016.

- Silva et al. [2015] R. Silva, S. M. Kang, and E. M. Airoldi. Predicting traffic volumes and estimating the effects of shocks in massive transportation systems. Proceedings of the National Academy of Sciences, 112:5643–5648, 2015.

- Smola et al. [2007] Alex Smola, Arthur Gretton, Le Song, and Bernhard Schölkopf. A hilbert space embedding for distributions. In International Conference on Algorithmic Learning Theory, pages 13–31. Springer, 2007.

- Spencer et al. [2015] S. E. F. Spencer, S. M. Hill, and S. Mukherjee. Inferring network structure from interventional time-course experiments. Annals of Applied Statistics, 9:507–524, 2015.

- Spirtes et al. [2000] P. Spirtes, C. Glymour, and R. Scheines. Causation, Prediction and Search. Cambridge University Press, 2000.

- Sriperumbudur et al. [2010] Bharath K Sriperumbudur, Arthur Gretton, Kenji Fukumizu, Bernhard Schölkopf, and Gert RG Lanckriet. Hilbert space embeddings and metrics on probability measures. Journal of Machine Learning Research, 11(Apr):1517–1561, 2010.

- Sriperumbudur et al. [2012] Bharath K Sriperumbudur, Kenji Fukumizu, Arthur Gretton, Bernhard Schölkopf, Gert RG Lanckriet, et al. On the empirical estimation of integral probability metrics. Electronic Journal of Statistics, 6:1550–1599, 2012.

- Sutherland et al. [2012] Dougal J Sutherland, Liang Xiong, Barnabás Póczos, and Jeff Schneider. Kernels on sample sets via nonparametric divergence estimates. arXiv preprint arXiv:1202.0302, 2012.

- Szabó et al. [2016] Zoltán Szabó, Bharath Sriperumbudur, Barnabás Póczos, and Arthur Gretton. Learning theory for distribution regression. Journal of Machine Learning Research, 17(152):1–40, 2016.

- Tian and Pearl [2001] Jin Tian and Judea Pearl. Causal discovery from changes. In Proceedings of the Seventeenth conference on Uncertainty in artificial intelligence, pages 512–521. Morgan Kaufmann Publishers Inc., 2001.