On Rank Estimators in Increasing Dimensions

Abstract

The family of rank estimators, including Han’s maximum rank correlation (Han,, 1987) as a notable example, has been widely exploited in studying regression problems. For these estimators, although the linear index is introduced for alleviating the impact of dimensionality, the effect of large dimension on inference is rarely studied. This paper fills this gap via studying the statistical properties of a larger family of M-estimators, whose objective functions are formulated as U-processes and may be discontinuous in increasing dimension set-up where the number of parameters, , in the model is allowed to increase with the sample size, . First, we find that often in estimation, as , rate of convergence is obtainable. Second, we establish Bahadur-type bounds and study the validity of normal approximation, which we find often requires a much stronger scaling requirement than . Third, we state conditions under which the numerical derivative estimator of asymptotic covariance matrix is consistent, and show that the step size in implementing the covariance estimator has to be adjusted with respect to . All theoretical results are further backed up by simulation studies.

Keywords: Bahadur-type bounds, degenerate U-processes, maximal inequalities, uniform bounds.

JEL Codes: C55, C14.

1 Introduction

1.1 The General Set-up, Motivation, and Main Results

Let denote a random sample of size from the probability measure . Let be a class of real-valued, possibly asymmetric and discontinuous, functions on . This paper studies the following M-estimator with an objective function of a U-process structure,

| (1.1) |

Let

This paper aims to establish asymptotic properties of as an estimator of in situations with large or increasing dimensions and (with respect to the sample size ), to which existing results do not apply.

Members of (1.1) include the following notable examples proposed and studied in the current literature in fixed dimension, i.e., and for all : (1) Han’s maximum rank correlation (MRC) estimator for the generalized regression model (Han,, 1987); (2) Cavanagh and Sherman’s rank estimator for the same model as Han’s (Cavanagh and Sherman,, 1998); (3) Khan and Tamer’s rank estimator for the semiparametric censored duration model (Khan and Tamer,, 2007); and (4) Abrevaya and Shin’s rank estimator for the generalized partially linear index model (Abrevaya and Shin,, 2011). One common feature of these models is the presence of a linear index of the form , where represents covariates of dimension which is typically large in many economic applications. The linear index structure is introduced to alleviate the “curse of dimensionality” associated with fully nonparametric models. Although motivated by possibly large dimension , properties of in these examples have only been established for fixed when approaches infinity (i.e., does not change with ). Instead, this paper models the large case by allowing to go to infinity as , denoted as , facilitating an explicit characterization of the effect of dimensionality on inference in these models.

More broadly, for the general set-up (1.1), we allow both and to go to infinity as and establish the following properties of : (i) consistency; (ii) rate of convergence; (iii) normal approximation; and (iv) accuracy of normal approximation. The last property is also referred to as the “Bahadur-Kiefer representation” or simply the “Bahadur-type bound” (Bahadur,, 1966; Kiefer,, 1967; He and Shao,, 1996), and is the major focus of this paper. Specifically, in Theorems 2.2, 2.3, and 2.4, under different scaling requirements for , , and , where characterizes the function complexity of , we prove consistency, efficient rate of convergence, and derive Bahadur-type bounds for the general M-estimator of the form (1.1). To facilitate inference, we construct consistent estimators of the asymptotic covariance matrix of similar to the numerical derivative estimators in Pakes and Pollard, (1989), Sherman, (1993), and Khan and Tamer, (2007). The increasing dimension set-up in this paper reveals that for consistent variance-covariance matrix estimation, the step size in computing the numerical derivative should depend not only on the sample size but also the dimensions and .

To provide further insight on the role of the dimension , we apply our general results, Bahadur-type bounds especially, to the aforementioned rank estimators (1)-(4). Note that for these estimators . Corollaries 3.1–3.4 provide sufficient conditions to guarantee consistency, efficient rate of convergence, and asymptotic normality (ASN) of the rank correlation estimators in increasing dimension. They demonstrate that, compared to competing alternatives such as simple linear regression, in terms of estimation, rank estimators are very appealing, maintaining the minimax optimal rates (Yu,, 1997), while enjoying an additional robustness property to outliers and modeling assumptions. With regard to normal approximation, on the other hand, a much stronger scaling requirement might be needed, and a lower accuracy in normal approximation is anticipated. This observation also echoes a common belief in robust statistics that stronger scaling requirement than is needed for normal approximation validity (Jurečková et al.,, 2012).

All the theoretical results are further backed up by simulation studies. In particular, using Han’s MRC estimator introduced below, we have demonstrated that for a given sample size, the accuracy of the normal approximation deteriorates quickly as the number of parameters increases, indicating that our theoretical bound is difficult to improve further. Also, our simulation results suggest that for variance estimation, the step size needs to be adjusted with respect to . Practically, our results indicate that although the linear index was introduced to alleviate the curse of dimensionality, one must be cautious in conducting inference using rank estimators when there are many covariates.

1.2 The Generalized Regression Model and Han’s MRC

Han’s MRC in Example (1) is the first rank correlation estimator proposed to estimate the parameter in the generalized regression model:

| (1.2) |

where , is a strictly increasing function of each of its arguments, and is a non-degenerate monotone increasing function of its argument. Important members of the generalized regression model in (1.2) include many widely known and extensively used econometrics models in diverse areas in empirical microeconomics such as the binary choice models, the ordered discrete response models, transformation models with unknown transformation functions, the censored regression models, and proportional and additive hazard models under the independence assumption and monotonicity constraints.

Han, (1987) proposed estimating in (1.2) with

| (1.3) |

For model identification, following Sherman, (1993), we assume the first component of is equal to 1, and express as . We consider estimating by , the subvector of excluding its first component. We will use the generalized regression model (1.2) and Han’s MRC to illustrate our notation, assumptions, and main results in Section 2. We defer a rigorous analysis of Han’s estimator including verification of assumptions to Section 3 which also presents results for the other three rank correlation estimators.

Empirically, consider estimating the individual demand curve for a durable good such as a refrigerator. Let be whether the individual buys a refrigerator and be the vector of characteristics of the individual and the refrigerator included in the model. There are many potential candidates for the components of such as personal income, marital status, the number of children, space of the kitchen, food habits; size of the refrigerator, temperature controls, lighting, shelves, dairy compartment, chiller, door styles. Assuming a single index form with , this binary choice model falls into our framework with (1.2). Our increasing dimension set-up allows more characteristics to be included in as the sample size increases and our results show that even with the single index form, estimation and inference are possible if increases very mildly with but otherwise are very challenging.

1.3 A Brief Review of Related Works and Technical Challenge

In contrast with the fixed dimension setting, where the model is assumed unchanged as goes to infinity, the increasing dimension triangular array setting (Portnoy,, 1984; Fan et al.,, 2015; Chernozhukov et al.,, 2015, 2017) makes our analysis different from and more challenging than most existing ones (cf. Theorem 3.2.16 and Example 3.2.22 in van der Vaart and Wellner, (1996), or the main theorem in He and Shao, (1996)). Technically, this paper builds on and contributes to two distinct literatures: the literature on estimation and inference in increasing dimension where existing works exclude discontinuous loss functions and the literature on rank estimation where existing works focus exclusively on finite dimensions. As a technical contribution, we establish a maximal inequality, yielding a uniform bound for degenerate U-processes in increasing dimensions which not only allows us to extend existing results on rank estimation in finite dimension to increasing dimensions but also establish Bahadur-type bounds. Besides the crucial role played by our new maximal inequality for degenerate U-processes in this paper, it should prove to be an indispensible tool in nonparametric and semiparametric econometrics in increasing dimensions where many estimators and test statistics are closely related to U-processes.

Since Huber’s seminal paper (Huber,, 1973), there has been a long history in statistics on evaluating the impact of parameter dimension on inference. Huber himself raised questions on the scaling limits of for assuring M-estimation consistency and asymptotic normality in his 1973 paper (Huber,, 1973). For addressing them, Portnoy, (1984), Portnoy, (1985), Mammen, (1989), and Mammen, (1993) studied the linear regression model using smooth M-estimators such as the ordinary least squares. Their results revealed that, in response to Huber’s question, for the simple linear regression model, asymptotic normality is usually attainable even when is large. In contrast, Portnoy, (1988) studied maximum likelihood estimators of generalized linear models, and proved that, for guaranteeing the validity of normal approximation, the requirement is in general unrelaxable. Different from the analysis in large setting, the techniques in Portnoy, (1988) are applicable to more general cases. For example, focusing on the general likelihood problem with a differentiable likelihood function, Spokoiny, 2012a has provided a finite-sample analysis of normal approximation accuracy. Related results have also been developed in He and Shao, (2000). As a direct consequence, a set of regularity conditions could be derived for constructing Bahadur-type bounds, guaranteeing ASN provided some scaling requirements hold.

Extending existing works allowing for increasing parameter dimension, this paper studies asymptotic properties of in (1.1), allowing both and to go to infinity as . The potential discontinuity and U-process structure of the objective function prevent results or the proof strategy in the current literature on increasing parameter dimension from being directly applicable. On the other hand, for (1.1), the increasing dimension set-up in this paper poses technical challenges to the proof strategy adopted for fixed and exclusively studied in the current literature. To see this, recall that the main argument used in the current literature to establish asymptotic properties for estimators of the form (1.1) for fixed and follows Sherman (Sherman,, 1993, 1994), which relies on the Hoeffding decomposition, a uniform bound for degenerate U-processes, and the classical M-estimation framework tracing back to Huber’s seminal paper, Huber, (1967). Specifically, for the statistic in (1.1), Hoeffding, (1948) derived the following well-known expansion now known as the Hoeffding decomposition:

| (1.4) |

where

| (1.5) | ||||

Hoeffding, (1948) further showed that for fixed and ,

| (1.6) |

where the remainder term , formulated as a degenerate U-statistic, is asymptotically negligible in large samples. As a result, is asymptotically equivalent to defined below:

| (1.7) |

Sherman (Sherman,, 1993, 1994) was the first to notice that, by (1.4) and the negligibility of , the U-statistic formulation has intrinsically helped smooth the loss function in (1.1) from to , and hence renders an asymptotically normal estimator , even though the original loss function may not be differentiable.

For increasing dimensions and , the Hoeffding decomposition of takes the same form as in the case of fixed and . However existing maximal inequalities or uniform bounds for degenerate U-processes for finite dimensions crucial to Sherman (Sherman,, 1993, 1994) and the classical M-estimation theory for finite dimensions are inapplicable. In response to the first challenge, this paper develops a maximal inequality, yielding a uniform bound for degenerate U-processes in increasing dimensions, which allows us to show that under regularity conditions, is asymptotically equivalent to . Due to the smoothness of , we are able to build on and improve arguments used in the proofs of Spokoiny, 2012a on M-estimators with differentiable objective functions in increasing dimensions to establish asymptotic properties of .

1.4 Notation

For a set , denote its binary Cartesian product as . For a probability measure , denote its product measure as . For , the -norm of a vector is denoted by . The -induced matrix operator norm of a matrix is denoted by . One example is the spectral norm , which represents the maximal singular value of . In the sequel, when no confusion is possible, we will omit the subscript in the -norm of or when . The minimum and maximum eigenvalues of a real symmetric matrix are denoted by and respectively. Let denote the identity matrix. Let denote the unit-sphere of under . For a twice differentiable real-valued function , let denote the vector of partial derivatives and denote the Hessian matrix of . Let denote an open ball of radius centered at , and let denote a closed ball of center and radius . For two real numbers and , we define and . We use to denote convergence in probability with respect to , and to denote convergence in distribution. For any two real sequences and , we write if there exists an absolute positive constant such that for any large enough . We write if both and hold. We write if for any absolute positive constant , we have for any large enough . We write and if and hold stochastically. We let be generic absolute positive constants, whose values will vary at different locations.

1.5 Paper Organization

The rest of this paper is organized as follows. In Section 2, we introduce general methods for handling M-estimators of the particular format. In particular, Section 2.1 gives a new U-process bound in increasing dimensions, and Section 2.2 studies M-estimators of the form (1.1), whose loss functions are possibly discontinuous. Section 3 applies the results in Section 2 to the four motivating rank estimators. Section 4 offers detailed finite-sample studies, illustrating the impact of dimension on coverage probability and tuning parameter selection in the asymptotic covariance estimation. Concluding remarks and possible extensions are put in the end of the main text. All proofs are relegated to an appendix.

2 Asymptotic Theory for the M-estimator

Recall that is a random sample from , rendering an empirical measure . Let be a VC-subgraph class of real-valued functions, with denoting the -dimension of (see Section 2.6.2 in van der Vaart and Wellner, (1996) for explicit definitions of VC-subgraph and VC-dimension of a VC-subgraph class). In addition, we assume the function class to be uniformly bounded by an absolute constant. The family of bounded VC-subgraph classes includes, as subfamilies, those rank estimators proposed in Han, (1987), Cavanagh and Sherman, (1998), Khan and Tamer, (2007), and Abrevaya and Shin, (2011), and suffices for our purpose.

Without loss of generality, we assume that

| (2.1) |

which can always be arranged by working with throughout.

The derivation of asymptotic properties of can be understood in two steps. First we show the asymptotic equivalence of and by proving negligibility of and then establish asymptotic properties of . Essential to the first step is an increasing dimension analogue of maximal inequalities for degenerate U-processes in finite dimensions. Because of increasing dimensions, we need to calculate an exact order of the decaying rate of in a local neighborhood of , the proof of which requires a substantial amount of modifications to the decoupling arguments in Nolan and Pollard, (1987). For the second step, we exploit Spokoiny’s bracketing device technique (cf. Corollary 2.2 in Spokoiny, 2012b ) on M-estimators with differentiable objective functions.

2.1 A Maximal Inequality for Degenerate U-processes

For fixed dimensions, Sherman (Sherman,, 1993, 1994) proved a maximal inequality for degenerate U-processes and used it to show that, when is -Donsker (Dudley,, 1999), uniformly over a small neighborhood surrounding ,

| (2.2) |

which, combined with the fact that is usually a smooth function by integration, is sufficient to guarantee that the stochastic differentiability condition (cf. Theorem 3.2.16 in van der Vaart and Wellner, (1996)) holds. This suffices for establishing ASN in fixed dimension. However, when we allow the dimension to increase with the sample size, (2.2) is no longer correct.

To account for the effect of increasing dimension, we establish a new maximal inequality for degenerate U-processes in increasing dimensions. Theorem 2.1 below works out an exact order of the rate of convergence of as shrinks to the true point at different rates . It is formulated as two maximal inequalities, corresponding to the Glivenko-Cantalli and Donsker properties, for a degenerate U-process.

Theorem 2.1.

Suppose that is uniformly bounded by an absolute constant, of VC-dimension , and is defined as in (1.3). Further recall that we have assumed satisfies (2.1). If , then the following two claims hold.

-

(i)

Let and be two sequences of nonnegative real numbers converging to zero. If

then there exists a sequence of nonnegative real numbers (only depending on ) converging to zero such that

-

(ii)

Let be a sequence of nonnegative real numbers converging to zero, and be a sequence of nonnegative real numbers (only depending on ) converging to zero. Denote . Suppose

We then have

(2.3) holds for all sufficiently large .

For deriving Theorem 2.1, one might consider employing the decoupling techniques as introduced in the proofs of the Main Corollary in Sherman, (1994), or Theorem 5.3.7 in de la Pena and Giné, (2012). However, since the considered U-process depends on an increasing number of covariates, the constants in the moment inequalities therein (e.g., in Sherman, (1994)) are no longer finite and are difficult to characterize in increasing dimensions. Instead, we resort to Nolan and Pollard’s original treatment of degenerate U-processes.

Specifically, denoting

a modification to Theorem 6 in Nolan and Pollard, (1987) will give us

| (2.4) |

Here for any , and have been introduced in (1.3), and and are two functions generated from . We have thus explicitly transformed the analysis of a degenerate U-process to that of a moment bound, and two empirical processes. Lastly, the bounds on the two empirical processes could be derived using, for example, Theorem 9.3 in Kosorok, (2007).

2.2 Main Results

We are now ready to state the main results in this section. For analyzing the statistical properties of the general M-estimator , three targets are in order: (i) consistency; (ii) rate of convergence; and (iii) Bahadur-type bounds. Of note, our analysis is under the increasing dimension triangular array setting where the true data generating process is allowed to change with the sample size .

We first establish consistency. This is via the following two assumptions.

Assumption 1.

For each specified , is a compact subset of , and there exists an absolute constant such that and for any positive absolute constant , there exists another absolute constant depending on such that

| (2.5) |

Assumption 2.

is a continuous function at any , and is almost everywhere continuous at .

Assumption 1 is the standard identifiability condition. Since as a function of is also to change with , it is regulated by a constant to eliminate the non-identifiable cases in large . Assumption 2 enforces certain level of smoothness on and . Both are regular, and in particular, verifiable for all the considered examples of rank estimators using explicit expressions for and for these estimators. For example, for Han’s MRC, Assumption 1 can be established using Taylor expansion applied to with

With Assumptions 1 and 2, we immediately obtain the following theorem, establishing consistency for the studied M-estimator .

It is of interest to point out that consistency is established solely based on an requirement of (which also intrinsically depends on ), since the uniform consistency of to can be determined solely by the relation between and . For the four examples of rank correlation estimators (1)-(4), so consistency is ensured under Assumptions 1 and 2 as long as the number of parameters increases at a slower rate than the sample size .

For establishing rates of convergence and Bahadur-type bounds, on the other hand, more assumptions are needed. For each in and for each , define

Here corresponds to in (1.6), and is the key for establishing ASN of in (1.7). The following assumption regulates .

Assumption 3.

For each , the following conditions hold.

-

(i)

For each in , all mixed second partial derivatives of with respect to exist on .

-

(ii)

There exist two positive absolute constants such that , where .

-

(iii)

There exists a positive constant for some absolute constant , such that for any , where .

-

(iv)

Assume , where and are two positive absolute constants.

-

(v)

There exist absolute constants and such that, for any , the following holds:

Assumption 3 is the key assumption in order to establish Bahadur-type bounds for , and is posed for the M-estimation problem (1.6) of loss function corresponding to the function . In the following we discuss more about this assumption. In detail, Assumptions 3(i), (ii), and (iv) are regularity conditions to make sure that the studied problem is well posited, a condition corresponding to the local strong convexity condition in the high dimensional statistics literature (cf. Section 2.4 in Negahban et al., (2012)), and are verifiable for different methods. Consider, for example, Han’s MRC estimator introduced in Section 1.2 for which :

where

Assumptions 3(i), (ii), and (iv) then are immediately ensured by Theorem 4 and subsequent discussions in Sherman, (1993). Assumption 3(iii) requires that is sufficiently smooth in , for example, has continuous and bounded mixed partial derivatives up to three. Assumption 3(v) requires the existence of exponential moments of the errors. They correspond to the “local identifiability condition”: Assumption (), and the “exponential moment condition”, Assumption (), in Spokoiny, 2012a and Spokoiny, (2013) separately. These conditions are often implied by subgaussian designs. Particularly, in Theorem 3.1 in Section 3.1, we will verify Assumptions 3(iii) and (v) for , i.e., Han’s MRC under primitive conditions.

With the above assumptions, statistical properties of could then be established as follows.

For the four examples of rank correlation estimators, so Theorem 2.3 leads to the minimax optimal rate under the condition: . However, Theorem 2.4 below implies that much stronger requirements on are needed to establish Bahadur-type bounds, see Corollaries 3.1-3.4 for details.

Theorem 2.4.

Remark 2.5.

In the analysis, and characterize the behavior of the smoothed estimator and the degenerate U-process separately. On the other hand, throughout the above three theorems, the dimension of data points, , is not present. Instead, the impact of on estimation and inference has been characterized by and , both of which are usually of an order equal to or even greater than . It is also noteworthy to point out that our analysis does allow an arbitrary subset of to be fixed, and the theory will directly proceed. In particular, when are all invariant with regard to , we derived the conventional Bahadur representation for the studied class of M-estimators under the low-dimensional setting, which is a stronger result than asymptotic normality.

We conclude this section with a brief discussion on consistent estimation of the asymptotic covariance matrix in Theorem 2.4. For this, we are focused on the covariance estimator of a numerical derivative form, used in Pakes and Pollard, (1989), Sherman, (1993), and Khan and Tamer, (2007).

First, for each in and for each in , define

Then, we define the numerical derivative of as follows:

where denotes a sequence of real numbers converging to zero, and denotes the unit vector in with the th component equal to one. Finally, we define the estimator of the matrix as with

To estimate the matrix , we define the following function:

Then, we define the estimator of the matrix as with

Let , and let denote the VC-dimension of . The following theorem establishes the consistency of the covariance estimator.

The increasing dimension set-up reveals that for consistent variance-covariance matrix estimation, the step size in computing the numerical derivative should depend not only on the sample size but also on the dimensions and .

3 Asymptotic Properties of Rank Estimators

This section studies the four examples introduced in Introduction. In the sequel, the data points are understood to be independent and identically drawn from the considered model. Of note, throughout the following four examples, when the studied model is fixed, our result renders the conventional Bahadur representation for the corresponding estimator in fixed dimensions (see, for example, Subbotin, (2008) for such a bound in fixed dimensions). Hence, we recover the asymptotic-normality-type theory in the corresponding paper, but under a stronger moment condition in order to take the impact of increasing dimension into consideration. In addition, it is worthwhile to point out that, for all studied methods, the dimension of the data points and the VC dimensions and of the studied function classes are all of the same order as , the number of parameters to be estimated. Accordingly, in the following, we can use to solely characterize the impact of dimension on inference.

3.1 Han’s Maximum Rank Correlation Estimator

This section studies the generalized regression model (1.2) and Han’s MRC estimator, as have been introduced in Section 1.2. Let be a subset of . For any , let , where . For any vector , we define

Write with

Thus, Han’s MRC estimator of , , can be expressed as

To conduct inference on based on , we further define

Then, we define the estimator of the matrix as and the estimator of the matrix as , where

Let , where denotes the last components in . Assume the following assumption holds

Assumption 4.

Assume

Assumption 5.

For some absolute constant , .

Assumption 6.

Let denote the conditional density function of given . Assume for any in the support of , where is an absolute constant.

We then have the following corollary.

Corollary 3.1.

We have

In the following, we discuss more on the assumptions posed for Han’s MRC estimator. Since the estimator takes pairwise differences as input, without loss of generality, the design is assumed to be zero-mean. First, Assumption 1 can be established using Assumptions 3(ii), (iii), and Taylor expansion. Secondly, the conditions in Assumptions 2 and 3(i) are regular and can be satisfied. Then, Theorem 4 and subsequent discussions in Sherman, (1993) ensure Assumptions 3(ii) and (iv) hold. Lastly, we deal with Assumptions 3(iii) and (v), which indeed deserve more discussion. In the following, we give sufficient conditions for guaranteeing Assumptions 3(iii) and (v) hold.

More notation is needed. Let denote the conditional density function of given and . Let denote the marginal density function of . Let

We assume the following conditions on the design as well as the noisy hold.

Condition 1.

Suppose is multivariate subgaussian, i.e., there exists an absolute constant such that , where .

Condition 2.

(i) Suppose that has uniformly bounded derivatives up to order three, i.e., there exists an absolute constant such that for any and in the support of and , respectively; (ii) for any and ; (iii) Universally over the support of and any , for some positive absolute constants , where represents the probability measure of given .

Condition 3.

Suppose that is bounded, i.e., there exists an absolute constant such that for any and in the support of and , respectively.

We then have the following theorem, which states that the above conditions are sufficient ones to ensure Assumptions 3(iii) and (v) hold.

3.2 Cavanagh and Sherman’s Rank Estimator

In contrast to Han’s original proposal, Cavanagh and Sherman, (1998) proposed estimating in (1.2) using

where

and one candidate function for is

Here and are two absolute constants, and hence is a trimming function for balancing the statistical efficiency and robustness to outliers. Let , and we aim to estimate .

We define the estimator and other parameters similarly as in Section 1.2 and Section 3.1, with their explicit definitions relegated to the appendix Section A.2.1. Then we have the following corollary.

Corollary 3.2.

We have

- (i)

-

(ii)

Suppose that Assumption 7 holds. If , then

- (iii)

-

(iv)

Under conditions in (iii), if we further have and , then

In particular, we could choose , which will render a consistent covariance estimator under the same scaling condition as (iii).

3.3 Khan and Tamer’s Rank Estimator for Duration Models

Consider Khan and Tamer’s setting (Khan and Tamer,, 2007), where the data are subject to censoring and the variable is no longer always observed. Use to denote the random censoring variable, which can be arbitrarily correlated with . Let be a binary variable indicating whether is uncensored or not. Let denote a scalar random variable with for uncensored observations, and otherwise. Consider the following right censored transformation model (Khan and Tamer,, 2007):

where is assumed to be strictly monotonic. The -dimensional vector is unknown and is to be estimated.

We define the estimator and other parameters similarly as in Section 1.2 and Section 3.1, with their explicit definitions relegated to the appendix Section A.2.2. Then we have the following corollary.

Corollary 3.3.

We have

- (i)

-

(ii)

Under Assumption 8, if , then

- (iii)

-

(iv)

Under conditions in (iii), if we further have and , then

In particular, we could choose , which will render a consistent covariance estimator under the same scaling condition as (iii).

3.4 Abrevaya and Shin’s Rank Estimator for Partially Linear Index Models

Consider Abrevaya and Shin’s partially linear index model (Abrevaya and Shin,, 2011):

where , , is a non-degenerate monotone function, is a smooth function, and is a random noisy independent of . Our primary interest is to estimate . For this, Abrevaya and Shin, (2011) proposed using , where

Here is a function facilitating pairwise comparison (Honoré and Powell,, 2005). It involves a kernel function and a bandwidth parameter . Let . Our aim is to estimate .

With the estimator and other parameters similarly defined as in Section 1.2 and Section 3.1 and put in the appendix Section A.2.3, we have the following corollary.

Corollary 3.4.

We have

- (i)

-

(ii)

Under Assumptions 9, if , then

- (iii)

-

(iv)

Under conditions in (iii), if we further have and , then

In particular, we could choose . This will render a consistent covariance estimator under the scaling condition , which, at various cases, will be the same as the scaling condition in (iii).

4 Simulation Results

This section presents results from a small simulation study to illustrate two main implications of our theory. First for each fixed , the normal approximation to the finite sample distribution of the studied rank correlation estimator will quickly become unreliable as grows, suggesting that our theoretical bound is difficult to be improved in a significant way. Secondly, in estimating the asymptotic covariance based on the covariance estimator of the numerical derivative form, as fixed, the tuning parameter that minimizes the Median Absolute Error (MAE) of the estimator will increase with the dimension , echoing our theoretical observation.

In the simulation study, we focus on Han’s MRC estimator of the form (1.3) and the following binary choice model:

where with , and representing the true regression coefficient. For each and , we simulate independent observations from the above model. Let be the normalized regression coefficient. We aim to estimate using Han’s estimator , which is implemented using the iterative marginal optimization algorithm proposed by Wang, (2007), with the initial point chosen to be the truth.

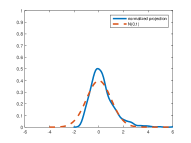

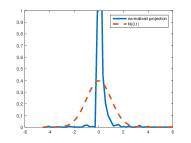

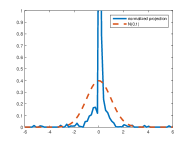

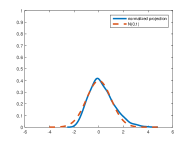

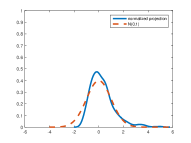

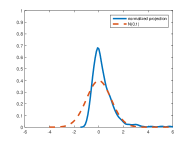

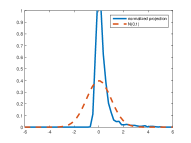

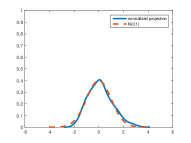

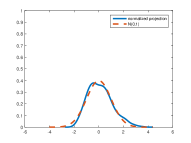

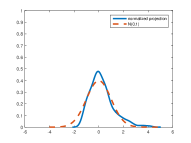

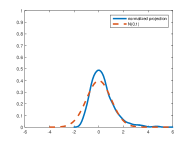

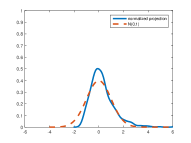

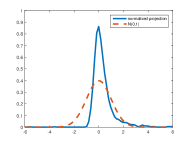

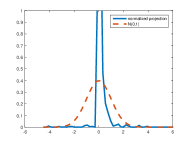

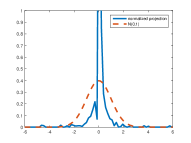

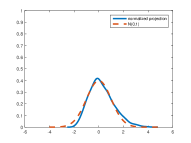

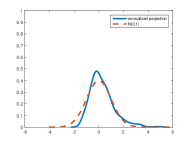

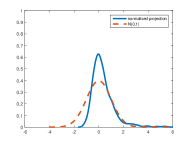

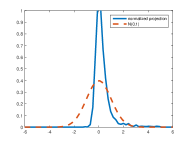

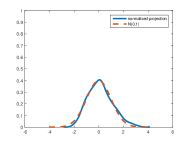

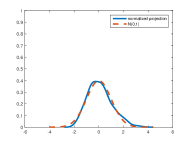

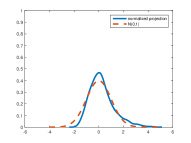

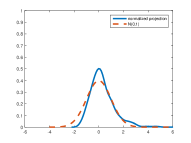

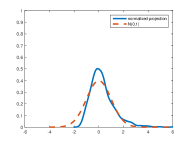

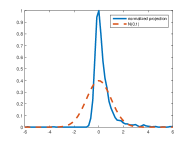

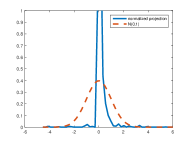

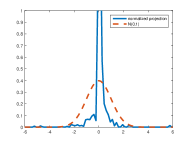

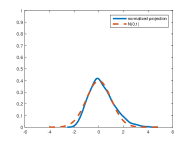

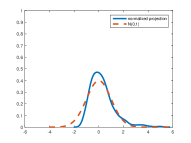

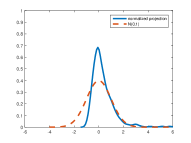

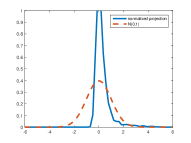

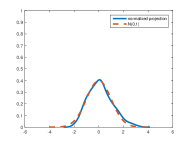

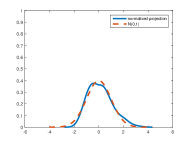

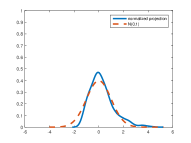

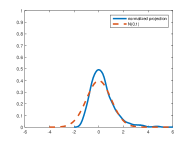

Based on 1,000 independent replications and using two-sided normal confidence interval, Tables 1-3 present the coverage probability as the nominal one varies from 0.5 to 0.95 for three projections of the same directions as , , and . For calculating the confidence intervals, we used the sample standard deviation of 1,000 replications. We further plot the kernel estimates of the density functions of the normalized three projected estimates against the density function of in Figures 1-3. The normalization is based on the true mean and the previous simulation-based standard deviation. In computing the kernel density estimates, we used normal kernel function and the bandwidth based on Silverman’s rule-of-thumb.

Both the tables and figures reveal the same overall pattern that, for each fixed , as increases, the coverage probability will deviate more from the nominal, and the kernel estimates of the density function of the normalized estimator itself will deviate more from the standard normal. As observed, the deviation from normal has become very severe even for very small . For example, for , we need to be approximately 400 for achieving satisfactory coverage probability. This supports the theoretical observations in Theorem 2.4 and Corollary 3.1(iii). We further conduct different types of normality tests (Kolmogorov-Smirnov, Lilliefors, Jarque-Bera, Anderson-Darling, Henze-Zirkler) on the derived projected estimates as well as the original multi-dimensional estimates. They all reject the null hypothesis of normality except when .

We then move on to study the estimation accuracy of the asymptotic covariance estimator discussed at the end of Section 2.2. For this, we focus on the same setup as previously conducted. Table 4 presents the MAE of the asymptotic covariance estimator for the projection direction . There, it could be observed that, for each fixed , the tuning parameter that attains the smallest MAE will in general become larger as increases, supporting our observation in Theorem 2.6 and Corollary 3.1(iv).

Concluding Remarks

This paper provided a first study of asymptotic properties of a general class of estimators defined as minimizers of possibly discontinuous objective functions of U-process structure allowing for the dimension of the parameter vector of interest to increase to infinity as the sample size increases to infinity. Members of this class include important rank correlation estimators as detailed throughout this paper. Technically we have established a maximal inequality for degenerate U-processes in increasing dimensions which has played a critical role in deriving our theoretical results. We have also applied our general theory to the four motivating rank correlation estimators. Using Han’s MRC estimator of the form (1.3), we have provided numerical support to our theoretical findings that for a given sample size, the accuracy of the normal approximation deteriorates quickly as the number of parameters increases and that for the variance estimation, the step size needs to be adjusted with respect to .

This paper is focused on the setting that the parameter of interest itself is of an increasing dimension and inference has to be drawn on it. On the contrary, a growing literature studies the case that the parameter to be inferred is of a fixed dimension, but allows for a dimension-increasing (but still less than ) nuisance in the model. Substantial developments have been made along this line. For example, Cattaneo et al., 2018a and Cattaneo et al., 2018b studied inferring the fixed-dimension linear component in a partially linear model, and Lei et al., (2018) established asymptotic normality of margins of linear and robust regression estimators in a simple linear model. Their set-up is fundamentally different from ours due to the difference of goals.111We note that our set-up is also fundamentally different from works on ”many moment asymptotics” in GMM models such as Han and Phillips, (2006), Newey and Windmeijer, (2009), and Caner, (2014), where the number of moment conditions increases but the number of parameters in such models is fixed as the sample size increases.

We end this section with a brief discussion on further extensions. An immediate extension is on studying “penalized” rank estimators in ultra high dimensional settings where the dimension could be even larger than the sample size. For this much more challenging setting, to the authors’ knowledge, most literature is still focused on simple structural statistical models (cf. Zhang and Zhang, (2014), Van de Geer et al., (2014), Lee et al., (2016), and Javanmard and Montanari, (2018) among many others). A notable exception is the post-selection inference framework proposed in Belloni et al., (2014) and Belloni et al., (2018), where a general set of regularization conditions has been posed for inference validity of Z-estimation. The authors believe that, combined with our local entropy analysis of the degenerate U-processes and the empirical process techniques developed by Talagrand and Spokoiny and specialized to rank estimators in this paper, the post-selection inference framework will prove useful in extending the current study to ultra high dimensional models. However, there are still many technical gaps, which we believe are fundamental and related to some key challenges in high dimensional probability in extending the scalar empirical processes to vector and matrix ones if no further smoothing (cf. Han et al., (2017)) is made. We will leave this for future research.

Acknowledgement

We thank Dr. Hansheng Wang for providing the code to implement the iterative marginal optimization algorithm, Mr. Shuo Jiang for helping conduct the simulations, and seminar/conference participants at Emory University, Peking University, and the 2019 Econometrics Workshop at Shanghai University of Finance and Economics for helpful comments. The research of Fang Han was supported in part by NSF grant DMS-1712536. We are also grateful to the Associate Editor and two anonymous referees for instructive comments that have greatly improved the paper.

Appendix A Appendix

A.1 Additional Notation

For a vector , we define . For two sequences of real numbers and , means that up to a multiplicative constant. We use the symbol to denote that and . In this appendix we drop the subscript in .

A.2 Notation and Assumptions in Section 3

Throughout this section, let , where denotes the last components in .

A.2.1 Notation and Assumptions in Section 3.2

The following definitions are similar to those in Section 1.2. We use to denote the expected value of , and . Let . We define

Write for and for . The estimator is defined as

To conduct inference on based on , we further define

Then, we define the estimator of the matrix as and the estimator of the matrix as , where

We then make the following assumptions.

A.2.2 Notation and Assumptions in Section 3.3

The following definitions are similar to those in Section 1.2. Let denote the expected value of , and . Let . We define

Write for and for . The estimator is defined as

To conduct inference on based on , we further define

Then, we define the estimator of the matrix as and the estimator of the matrix as , where

We then make the following assumptions.

A.2.3 Notation and Assumptions in Section 3.4

Let denote the density of . Let . We define

Write for . The estimator is defined as

Note that . This is different from the general set-up in Section 2.2. However, by Taylor expansion, we show that is negligible under the assumptions adopted in this section. Then, following the proof of the general method, we can similarly establish the consistency and asymptotic normality of .

To conduct inference on based on , we further define

Then, we define the estimator of the matrix as and the estimator of the matrix as , where

We make the following assumptions.

Assumption 9.

Assume

-

(i)

Assumption 1 holds for and ;

-

(ii)

The random variables and are independent.

-

(iii)

has an everywhere positive Lebesgue density, conditional on and .

-

(iv)

is continuously distributed on a compact subset of .

-

(v)

The kernel function satisfies: (1) is twice continuously differential with compact interval ; (2) is symmetric about 0 and integrates to 1; (3) for some integer , with and is bounded.

-

(vi)

The bandwidth is defined as for constants and .

-

(vii)

For any , the th derivative of with respect to is continuous and bounded for all .

-

(viii)

Assumption 3 holds for and .

Assumption 10.

Let denote the conditional density function of given . Assume for any and in the support of and , respectively, where is an absolute positive constant.

A.3 Proofs in Section 2

For each , define measures

and

To prove Theorems 2.1–2.4 in Section 2, we need several lemmas. For simplicity, we omit the parameter in each function in the lemmas. Let denote the envelope function of for which , for any . The covering number is defined as the smallest cardinality for a subclass of such that , for each .

A.3.1 Some Auxiliary Lemmas

Lemma A.1.

Suppose that is -uniformly bounded, then the class with envelope satisfies .

Proof.

Find functions such that

Then, with the appropriate ,

This implies that . ∎

Lemma A.2.

Suppose that is -uniformly bounded. Then , where .

Proof.

With a little abuse of notation, let be the Rademacher sequence, where is symmetric around 0. By the classic symmetrization theorem (cf. Theorem 8.8 in Kosorok,, 2007), we have

| (A.1) |

Next, we try to bound for fixed . To that end, consider the stochastic process . It is easy to verify that is sub-gaussian with parameter , where . Consequently, Dudley’s entropy integral, combined with the fact that , implies that

| (A.2) |

By Theorem 9.3 in Kosorok, (2007) and Lemma 20 in Nolan and Pollard, (1987), there exists a universal constant such that . Substituting this bound into (A.2), we find that there exist constants , only depending on but not on , such that

Combining this with (A.1) implies that . This completes the proof. ∎

Lemma A.3.

Suppose that is -degenerate and -uniformly bounded. Then .

Proof.

First, by the relationship between and : , we just need to show that is bounded. Apply Theorem 6 in Nolan and Pollard, (1987) to get

| (A.3) |

where is a universal constant, , , and . By Theorem 9.3 in Kosorok, (2007), we have , and thus for some constant depending on , where .

Since is -uniformly bounded, it holds that . Note also that is bounded when . We immediately have is bounded. Additionally, by the definition of , we see that . Combining all these points with (A.3) implies that there exists some constant depending on such that

for some large enough absolute constant . This completes the proof. ∎

Lemma A.4.

If for each , (i) , (ii) , (iii) , then almost surely.

The proof of this lemma follows along the same lines as the proof of Theorem 7 in Nolan and Pollard, (1987), though the condition (iii) in this lemma is different from there.

A.3.2 Proof of Theorem 2.1

Proof.

(i) It is equivalent to showing that there exists a sequence of nonnegative real numbers converging to zero such that

or

By Chebyshev’s inequality, it suffices to show that

We try to bound . Without loss of generality, assume is uniformly bounded by . Thus, for any , , i.e., the class of functions is 1-uniformly bounded. Similar to the proof of Lemma A.3, we apply Theorem 6 in Nolan and Pollard, (1987) here to get

| (A.4) | ||||

where is some constant. The second inequality holds because is concave in .

Note that and that is increasing in . Thus, from (A.4), we additionally have

| (A.5) | ||||

where the last inequality holds because is concave in . Now, we need only to consider .

By a decomposition of into a sum of its expected value, plus a smoothly parameterized, zero-mean empirical process, plus a degenerate -process of order two, we have

| (A.6) | ||||

where and .

By the condition in (i), it holds that . By Lemmas 16 and 20 in Nolan and Pollard, (1987), and Lemma A.1, we have . Then, following the proof of Lemma A.2, we have for some constant . Additionally, following the proof of Lemma A.3, we have for some constant .

Take . If and , then

because as . This completes proof of (i).

(ii) The proof is based on (A.4)–(A.6) in the proof of (i). First, by the condition in (ii), it holds that . Then, similar to the proof of (i), for some constant , and for some constant . Since and , there exists a constant depending on such that

holds for sufficiently large . Combining this with (A.5) implies that

for some constant . Finally, by the relationship between and , we conclude that

holds for sufficiently large . ∎

A.3.3 Proof of Theorem 2.2

Proof.

The proof is twofold. We first show the uniform convergence of , and then establish the consistency of .

Step 1. By Theorem 9.3 in Kosorok, (2007), we have for any and any finite measure . If , then all the three conditions in Lemma A.4 hold. Apply this lemma here to get that converges almost surely to uniformly in .

Step 2. Let , where . By Assumption 1, we see that is compact. By Assumption 2, is continuous. Combining these two pieces yields that exists. Again, by Assumption 1, we know that .

By Step 1, we can find a sufficiently large such that for all ,

holds almost surely. Combining this with the definition of yields that

This implies that , i.e., for all . Since this is true for any , we have

and hence also in probability. This completes the proof. ∎

A.3.4 Proof of Theorem 2.3

Proof.

The proof is conducted in four steps. Based on the Hoeffding decomposition of , we consider , and separately in the first three steps. We finally obtain the convergence rate of in the last step.

Step 1. Fixing , define

| (A.7) |

Additionally, expand about to get

| (A.8) |

where is a point on the line connecting and , and . Expand in about to get

for between and . By Assumption 3(ii) and (iii), we have

| (A.9) | ||||

Combining this with (A.7) and (A.8) yields

| (A.10) |

Step 2. Fixing in and in , define

With a little abuse of notation, we still use to denote some point between and below. Expand about to get

Note that . It then follows from the above equation and that

By Step 1, we have that

| (A.11) |

Next, we try to bound . Consider the vector process

According to Assumption 3(v), it holds, for any , , that

for any with . It then follows from Theorem A.3 in Spokoiny, (2013) that for any ,

where

Thus,

| (A.12) |

This, combined with (A.11), implies that

| (A.13) |

Step 3. By Assumption 2, is continuous at almost surely. Since is uniformly bounded, a dominated convergence argument implies that the same holds true for . In view of for all , it holds that . Thus, the boundedness of and the dominated convergence theorem establish

| (A.15) |

Equivalently, there exists a constant such that and as . By Theorem 2.1, there exists a sequence of nonnegative real numbers (depending on ) converging to zero as and , such that

| (A.16) |

holds for sufficiently large .

Step 4. The Hoeffding decomposition, combined with (A.10), (A.14), and (A.16) in the above three steps, implies that

| (A.17) | ||||

In view of , it holds that . This, combined with Assumption 3(iv), implies that there exists a constant depending on such that

holds for sufficiently large . Define the set

then holds for sufficiently large . The following analysis is on the set .

By Theorem 2.2, almost surely. Thus, for sufficiently large , . This implies that

In view of , it holds that

This, combined with Assumption 3(ii) and , implies that

| (A.18) |

where . By the definition of and , there exists a constant such that for sufficiently large . Combining this with (A.18) yields that

Solving the above equation establishes that

holds for sufficiently large , where is some constant depending only on , but not depending on . Thus,

holds for sufficiently large . This completes the proof. ∎

A.3.5 Proof of Theorem 2.4

Proof.

The proof is based on the proof of Theorem 2.3. We first define and . By Theorem 2.3, for any , there exists a constant such that

| (A.19) |

holds for sufficiently large . By the definition of , , it holds that for any , . This, combined with Assumption 3(ii) and (iv), implies that there exists a constant such that

| (A.20) |

holds for sufficiently large . Thus, by (A.19) and (A.20), there exists a constant depending on such that

| (A.21) |

holds for sufficiently large , where and .

Since is uniformly bounded and , Theorem 2.1(ii) implies that there exists a constant such that

| (A.24) |

holds for sufficiently large . This, together with (A.22) and (A.23), implies that

| (A.25) | ||||

In view of , and , it holds that

| (A.26) | ||||

for sufficiently large . Define the set

| (A.27) |

where

Then, . Additionally, . The following analysis is on the set .

By definition, . Apply the inequality in (A.27) twice, then multiply through by , consolidate terms, and use the fact that is negative definite to get that

| (A.28) |

Note that . This, combined with (A.28) and Assumption 3(ii), implies that

Recall the definition of and , we immediately have

Furthermore, if , then by Assumption 3(iv) and Slutsky’s Theorem, it hold that for any , . This completes the proof. ∎

A.3.6 Proof of Theorem 2.6

Proof.

Note that the function class is uniformly bounded by an absolute constant. We immediately have that is also uniformly bounded by an absolute constant. In addition, . It then follows from Lemma A.2 that

| (A.29) |

Since , we just need to consider

where

Expand about to get

| (A.30) |

where denotes some point between and . Note that . We can rewrite in the above equation as follows:

We discuss and separately. First, following the calculations in Step 2 of the proof of Theorem 2.3, we have

where . In view of , it then holds that

| (A.31) |

We now turn to consider . Following similar arguments as in Step 1 of the proof of Theorem 2.3, we have

Combining this with (A.31) and (A.30) implies that

| (A.32) |

Next, we consider . Expand about to get

| (A.33) |

where . Again using the equality , we have

| (A.34) |

By Assumption 3(ii) and (iii), we have

| (A.35) |

By Assumption 3(v), we know that is zero-mean subexponential. Thus, by the equivalent definitions of zero-mean subexponential variables, it holds that

| (A.36) |

is bounded. That is, . Put (A.33)–(A.36) together. We then have

This, combined with (A.32), implies that

Additionally, combining this with (A.29) implies that

Thus,

Similarly,

By assumption, , , and . It can then be easy to verify that

This, combined with Assumption 3(ii) and (iv), implies that , , and . Note that . Then, we have

Note also that

Apply the triangle inequality to the above equation to get that

This completes the proof. ∎

A.4 Proofs in Section 3

For the example in Section 1.2, we define , where is defined in the main text, and define . For the example in Section 3.2, we define and . For the example in Section 3.3, we define and . For the example in Section 3.4, we define and .

A.4.1 Some Additional Lemmas

Lemma A.5.

Suppose that Condition 1 in the main text holds. Then is multivariate subgaussion.

Proof.

Fix . Applying the triangle inequality yields that

In what follows, we discuss and separately. We first consider :

| (A.37) |

We then consider :

where the second and third inequalities hold because of the convexity of for . This, combined with (A.37) and Condition 1, implies that

which completes the proof. ∎

Next, we give the following lemma which establishes the upper bound for .

Proof.

Write . Substitute the equation for into and consolidate terms to get that

Fix . Expand about to get

where is between and . We wish to bound . To that end, we discuss separately for . With a little abuse of notation, we still use instead of below.

We first consider . By the property of exchangeability between integration and derivation with , we have

where

Similarly, we can write , and respectively as

where

and

Thus, we can rewrite as

To simplify the expression forms of the functions with , we introduce the following notations:

and

This, combined with that , allows us to rewrite as

Since the functions , are all bounded, we just need to bound and for .

We first consider and rewrite as follows:

where , and denotes the probability distribution of .

Let denote the unit vector in with the th component equal to one and let denote the th component of , where . By definition,

The term in brackets equals

Change variables from to , rearrange the terms in the fields of integration to get that

where denotes the distribution of . The inner integral equals

Integrate, then apply the moment condition in Assumption 5 to see that

Since and by Assumption 6, it then holds that

Thus,

Similarly,

Put all results together, and we have that

for some constant depending only on . Then

That is, . This completes the proof. ∎

The next three lemmas give the upper bound for , , and , respectively. Since the proofs of these lemmas are similar to the proof of Lemma A.6, we omit the proofs for simplicity.

A.4.2 Proof of Corollary 3.1

Proof.

Note that is uniformly bounded. To prove Corollary 3.1(i) and (ii), it suffices to show that the VC-dimension of is by Theorems 2.2 and 2.3.

To see this, define the following function:

and the following function class:

Note that is a -dimensional vector space of real-valued functions. By Lemma 18 in Pollard, (1984) and Lemma 2.4 in Pakes and Pollard, (1989), and are VC-classes of VC-dimensions for any . We further have, for any , , and ,

for . This, combined with Lemma 9.7 in Kosorok, (2007), implies that is a VC-class of VC-dimension . Then, apply Theorems 2.2 and 2.3 to complete the proof of Corollary 3.1(i) and (ii).

A.4.3 Proof of Corollary 3.2

Proof.

Similar to the proof of Corollary 3.1, it can be easy to show that the VC-dimensions of and are both of order . This, combined with that is uniformly bounded, proves Corollary 3.1(i) and (ii) by Theorems 2.2 and 2.3. Corollary 3.1(iii) follows from Lemma A.7 and Theorem 2.4. Corollary 3.1(iv) follows from Theorem 2.6. ∎

A.4.4 Proof of Corollary 3.3

Proof.

Similar to the proof of Corollary 3.1, one could show that the VC-dimension of and are both of order . Then, the proofs of Corollary 3.3 (i) and (ii) follow directly from the proof of Corollary 3.1. Finally, Lemma A.8, together with Theorem 2.4 imply Corollary 3.3(iii). Corollary 3.3(iv) follows from Theorem 2.6. ∎

A.4.5 Proof of Corollary 3.4

Proof.

(i) Similar to the proof of Theorem 2.2, the proof is twofold. We first show that converges in probability to uniformly in , and then establish the consistency of .

Step 1. Since is continuously differential with compact support by Assumption 9(vi), is bounded and is also a function of bounded variation. Thus, can be written as with appropriate bounded and monotone functions and . Let and denote the upper bounds of and respectively.

Let and . Then, . Similar to the proof of Corollary 3.1, it can be easy to verify that the VC-dimensions of and are both by considering the class of subgraphs of all functions in and separately. By Lemma 16 in Nolan and Pollard, (1987), the covering number of is bounded through . This, combined with Theorem 9.3 in Kosorok, (2007), Lemma A.2, A.4, and Hoeffding decomposition implies that

| (A.39) |

Next, we try to bound . Note that

| (A.40) | ||||

A th-order Tylor expansion of with respect to at 0 and Assumptions 9(vi)–(viii) imply that

| (A.41) |

This, combined with (A.39) and the triangular inequality, implies that

Thus, the uniform convergence of is shown.

Step 2. Following Step 2 in the proof of Theorem 2.2, it can be easy to show that . This completes proof of Corollary 3.4(i).

(ii) Similar to the proof of Theorem 2.3, the proof is conducted in four steps. We first define . Thus, . By a Hoeffding decomposition of , we have

where

and

The first three steps aim to establish bounds that are similar to (A.10), (A.14) and (A.16), respectively. The last step establishes the rate of convergence of .

Step 1. We first consider . By (A.39), there exists a constant such that

| (A.42) |

Fix . Similar to Step 1 in the proof of Theorem 2.3, we have

| (A.43) |

This, combined with (A.42), implies that

| (A.44) |

Step 2. Similar to (A.40), a change of variables and a th-order Tylor expansion imply that

for some constant . This, combined with (A.42), implies that

| (A.45) |

Following the proof of Theorem 2.3 in Step 2, we additionally have

where . Combining this with (A.45) implies that

| (A.46) | |||

Step 3. Following the proof of Theorem 2.1(i), one can get

where is a sequence of nonnegative real numbers converging to zero. Thus,

| (A.47) |

Step 4. By the Hoeffding decomposition of and the results in (A.44), (A.46) and (A.47), we have

| (A.48) | ||||

Then, following the proof of Theorem 2.3 in Step 4, we conclude that there exists a sufficiently large constant such that

| (A.49) |

holds for sufficiently large .

Since is uniformly bounded and by Lemma A.9, Theorem 2.1(ii) implies that there exists a constant such that

holds for sufficiently large . Thus,

| (A.50) |

In view of , it holds that as . This, combined with (A.51), implies that

| (A.51) |

Based on similar analyses at the beginning of this step, we conclude that, there exists a sufficiently large constant such that

holds for sufficiently large . This, combined with (A.49), implies that there exists a sufficiently large constant such that

This completes proof of (ii).

(iii) Similar to the proof of Theorem 2.4, we first define . Similarly, there exists a constant such that

| (A.52) |

holds for sufficiently large , where and .

Fix . Then following the proofs of Corollary 3.4(ii) in Step 1–2, we have

| (A.53) |

and

| (A.54) | ||||

Similar to (A.51), we have

| (A.55) |

This, together with (A.53) and (A.54), implies that

| (A.56) | ||||

The remaining proofs are straightforward and follow the proof of Theorem 2.4. In conclusion, if , we have

In addition, if , then for any ,

This completes the proof of (iii).

(iv) Note that . The proof is a little different from that in proving Theorem 2.6. To see this, define . Following the similar arguments in proof of (i), one can show that the VC-dimension of is of order . It then follows from Lemma A.2 that

Similar to the derivations in (A.40) and (A.41), we have

Then, following from the proof of Theorem 2.6, we get that

where . By assumption, , , and , one can show that

The remaining proof follows exactly from that in the proof of Theorem 2.6. ∎

A.5 Proof of Theorem 3.1

Proof.

We check Assumption 3(iii) and (v) separately under Conditions 1–3.

-

(iii)

The proof proceeds in two steps. We first calculate the third order mixed partial derivatives of . Then we establish the bound of for any .

Step 1. Fix and . Note that

where denotes the marginal distribution of and denotes the conditional density function of given , is a term that does not depend on , and

For simplicity, we consider only the first part of and denote

After some simple calculations, we have

where

Additionally, we have

where

According to Condition 2, we know that is uniformly upper bounded: for some absolute constant . We could then similarly define for the second part and write .

Step 2. For any , we consider . Expand about to get

Then,

By Condition 1, we know that there exists an absolute constant such that

Then, we can choose small enough such that . The first part of Assumption 3(iii) has been verified.

Next, we try to verify the second part of Assumption 3(iii). According to the results in Step 1, we expand about to get that

where depends only on the absolute constants and . Then, by the relationship between different matrix norms, we have that

Finally,

This completes the verification of Assumption 3(iii).

-

(v)

We first consider . Since is multivariate subgaussian by Condition 1, it holds that . According to calculations in the proof of Theorem 4 in Sherman, (1993), we have

For any , Lemma A.5 implies that under Conditions 3 and 1, and are both subgaussian with subgaussian norms and , respectively. Because the product of two subgaussian random variables is subexponential, is subexponential with a subexponential norm that depends only on and . By the definition of subexponential variables and , we have

(A.57) where and are constants depend on constants . This shows that Assumption 3(v) holds at .

Note that there are several equivalent definitions for a generic zero-mean subexponential variable . One of them is defined as follows: there is a constant such that is bounded for all . This definition implies that, for the subexponential variable , there is a constant such that is bounded for all . Because is a continuous function in , and in addition that the domain of this function is a compact set, it then holds

Thus, is subexponential for any . Similar to (A.57), we can establish the bound in Assumption 3(v).

This completes the proof. ∎

References

- Abrevaya and Shin, (2011) Abrevaya, J. and Shin, Y. (2011). Rank estimation of partially linear index models. The Econometrics Journal, 14(3):409–437.

- Bahadur, (1966) Bahadur, R. R. (1966). A note on quantiles in large samples. The Annals of Mathematical Statistics, 37(3):577–580.

- Belloni et al., (2018) Belloni, A., Chernozhukov, V., Chetverikov, D., and Wei, Y. (2018). Uniformly valid post-regularization confidence regions for many functional parameters in Z-estimation framework. The Annals of Statistics, 46(6B):3643–3675.

- Belloni et al., (2014) Belloni, A., Chernozhukov, V., and Kato, K. (2014). Uniform post-selection inference for least absolute deviation regression and other Z-estimation problems. Biometrika, 102(1):77–94.

- Caner, (2014) Caner, M. (2014). Near exogeneity and weak identification in generalized empirical likelihood estimators: Many moment asymptotics. Journal of Econometrics, 182(2):247–268.

- (6) Cattaneo, M. D., Jansson, M., and Newey, W. K. (2018a). Alternative asymptotics and the partially linear model with many regressors. Econometric Theory, 34:277–301.

- (7) Cattaneo, M. D., Jansson, M., and Newey, W. K. (2018b). Inference in linear regression models with many covariates and heteroskedasticity. Journal of the American Statistical Association, 113(523):1350–1361.

- Cavanagh and Sherman, (1998) Cavanagh, C. and Sherman, R. P. (1998). Rank estimators for monotonic index models. Journal of Econometrics, 84(2):351–381.

- Chernozhukov et al., (2017) Chernozhukov, V., Chetverikov, D., and Kato, K. (2017). Central limit theorems and bootstrap in high dimensions. The Annals of Probability, 45(4):2309–2352.

- Chernozhukov et al., (2015) Chernozhukov, V., Hansen, C., and Spindler, M. (2015). Valid post-selection and post-regularization inference: An elementary, general approach. Annual Review of Economics, 7:649–688.

- de la Pena and Giné, (2012) de la Pena, V. and Giné, E. (2012). Decoupling: From Dependence to Independence. New York: Springer.

- Dudley, (1999) Dudley, R. M. (1999). Uniform Central Limit Theorems. Cambridge University Press.

- Fan et al., (2015) Fan, J., Liao, Y., and Yao, J. (2015). Power enhancement in high-dimensional cross-sectional tests. Econometrica, 83(4):1497–1541.

- Han, (1987) Han, A. K. (1987). Non-parametric analysis of a generalized regression model: the maximum rank correlation estimator. Journal of Econometrics, 35(2-3):303–316.

- Han and Phillips, (2006) Han, C. and Phillips, P. C. (2006). GMM with many moment conditions. Econometrica, 74(1):147–192.

- Han et al., (2017) Han, F., Ji, H., Ji, Z., and Wang, H. (2017). A provable smoothing approach for high dimensional generalized regression with applications in genomics. Electronic Journal of Statistics, 11(2):4347–4403.

- He and Shao, (1996) He, X. and Shao, Q.-M. (1996). A general Bahadur representation of M-estimators and its application to linear regression with nonstochastic designs. The Annals of Statistics, 24(6):2608–2630.

- He and Shao, (2000) He, X. and Shao, Q.-M. (2000). On parameters of increasing dimensions. Journal of Multivariate Analysis, 73(1):120–135.

- Hoeffding, (1948) Hoeffding, W. (1948). A class of statistics with asymptotically normal distribution. The Annals of Mathematical Statistics, 19(3):293–325.

- Honoré and Powell, (2005) Honoré, B. E. and Powell, J. (2005). Pairwise difference estimators for nonlinear models. In Andrews, D.W.K., Stock, J.H. (Eds.) Identification and Inference in Econometric Models. Essays in Honor of Thomas Rothenberg, pages 520–553. Cambridge University Press.

- Huber, (1967) Huber, P. J. (1967). The behavior of maximum likelihood estimates under nonstandard conditions. In Proceedings of the Fifth Berkeley Symposium on Mathematical Statistics and Probability, pages 221–233. Berkeley, CA.

- Huber, (1973) Huber, P. J. (1973). Robust regression: Asymptotics, conjectures and Monte Carlo. The Annals of Statistics, 1(5):799–821.

- Javanmard and Montanari, (2018) Javanmard, A. and Montanari, A. (2018). De-biasing the lasso: Optimal sample size for Gaussian designs. The Annals of Statistics, 46(6A):2593–2622.

- Jurečková et al., (2012) Jurečková, J., Sen, P. K., and Picek, J. (2012). Methodology in Robust and Nonparametric Statistics. CRC Press.

- Khan and Tamer, (2007) Khan, S. and Tamer, E. (2007). Partial rank estimation of duration models with general forms of censoring. Journal of Econometrics, 136(1):251–280.

- Kiefer, (1967) Kiefer, J. (1967). On Bahadur’s representation of sample quantiles. The Annals of Mathematical Statistics, 38(5):1323–1342.

- Kosorok, (2007) Kosorok, M. R. (2007). Introduction to Empirical Processes and Semiparametric Inference. Springer.

- Lee et al., (2016) Lee, J. D., Sun, D. L., Sun, Y., and Taylor, J. E. (2016). Exact post-selection inference, with application to the lasso. The Annals of Statistics, 44(3):907–927.

- Lei et al., (2018) Lei, L., Bickel, P. J., and Karoui, N. E. (2018). Asymptotics for high dimensional regression m-estimates: Fixed design results. Probability Theory and Related Fields, 172(3-4):983—1079.

- Mammen, (1989) Mammen, E. (1989). Asymptotics with increasing dimension for robust regression with applications to the bootstrap. The Annals of Statistics, 17(1):382–400.

- Mammen, (1993) Mammen, E. (1993). Bootstrap and wild bootstrap for high dimensional linear models. The Annals of Statistics, 21(1):255–285.

- Negahban et al., (2012) Negahban, S. N., Ravikumar, P., Wainwright, M. J., and Yu, B. (2012). A unified framework for high-dimensional analysis of -estimators with decomposable regularizers. Statistical Science, 27(4):538–557.

- Newey and Windmeijer, (2009) Newey, W. K. and Windmeijer, F. (2009). Generalized method of moments with many weak moment conditions. Econometrica, 77(3):687–719.

- Nolan and Pollard, (1987) Nolan, D. and Pollard, D. (1987). U-processes: rates of convergence. The Annals of Statistics, 15(2):780–799.

- Pakes and Pollard, (1989) Pakes, A. and Pollard, D. (1989). Simulation and the asymptotics of optimization estimators. Econometrica, 57(5):1027–1057.

- Pollard, (1984) Pollard, D. (1984). Convergence of Stochastic Processes. Springer.

- Portnoy, (1984) Portnoy, S. (1984). Asymptotic behavior of M-estimators of regression parameters when is large. I. Consistency. The Annals of Statistics, 12(4):1298–1309.

- Portnoy, (1985) Portnoy, S. (1985). Asymptotic behavior of M estimators of regression parameters when is large; II. Normal approximation. The Annals of Statistics, 13(4):1403–1417.

- Portnoy, (1988) Portnoy, S. (1988). Asymptotic behavior of likelihood methods for exponential families when the number of parameters tends to infinity. The Annals of Statistics, 16(1):356–366.

- Sherman, (1993) Sherman, R. P. (1993). The limiting distribution of the maximum rank correlation estimator. Econometrica, 61(1):123–137.

- Sherman, (1994) Sherman, R. P. (1994). Maximal inequalities for degenerate U-processes with applications to optimization estimators. The Annals of Statistics, 22(1):439–459.

- (42) Spokoiny, V. (2012a). Parametric estimation. Finite sample theory. The Annals of Statistics, 40(6):2877–2909.

- (43) Spokoiny, V. (2012b). Supplement to “Parametric estimation. Finite sample theory”. The Annals of Statistics.

- Spokoiny, (2013) Spokoiny, V. (2013). Bernstein-von Mises Theorem for growing parameter dimension. arXiv preprint arXiv:1302.3430.

- Subbotin, (2008) Subbotin, V. Y. (2008). Essays on the Econometric Theory of Rank Regressions. PhD thesis, Northwestern University.

- Van de Geer et al., (2014) Van de Geer, S., Bühlmann, P., Ritov, Y., and Dezeure, R. (2014). On asymptotically optimal confidence regions and tests for high-dimensional models. The Annals of Statistics, 42(3):1166–1202.

- van der Vaart and Wellner, (1996) van der Vaart, A. and Wellner, J. (1996). Weak Convergence and Empirical Processes. Springer.

- Wang, (2007) Wang, H. (2007). A note on iterative marginal optimization: a simple algorithm for maximum rank correlation estimation. Computational Statistics and Data Analysis, 51(6):2803–2812.

- Yu, (1997) Yu, B. (1997). Assouad, Fano, and Le Cam. In Festschrift for Lucien Le Cam, 423–435. Springer, New York.

- Zhang and Zhang, (2014) Zhang, C.-H. and Zhang, S. S. (2014). Confidence intervals for low dimensional parameters in high dimensional linear models. Journal of the Royal Statistical Society: Series B, 76(1):217–242.

| nominal coverage probability | |||||||||||

| 0.5 | 0.55 | 0.6 | 0.65 | 0.7 | 0.75 | 0.8 | 0.85 | 0.9 | 0.95 | ||

| 100 | 1 | 0.606 | 0.644 | 0.692 | 0.731 | 0.781 | 0.822 | 0.860 | 0.890 | 0.914 | 0.932 |

| 2 | 0.806 | 0.829 | 0.844 | 0.862 | 0.881 | 0.895 | 0.907 | 0.920 | 0.930 | 0.948 | |

| 3 | 0.923 | 0.930 | 0.938 | 0.947 | 0.953 | 0.957 | 0.963 | 0.964 | 0.970 | 0.973 | |

| 4 | 0.877 | 0.892 | 0.905 | 0.920 | 0.926 | 0.939 | 0.945 | 0.948 | 0.956 | 0.964 | |

| 200 | 1 | 0.518 | 0.561 | 0.619 | 0.672 | 0.719 | 0.763 | 0.809 | 0.861 | 0.903 | 0.939 |

| 2 | 0.598 | 0.655 | 0.704 | 0.754 | 0.801 | 0.826 | 0.863 | 0.890 | 0.912 | 0.938 | |

| 3 | 0.702 | 0.746 | 0.788 | 0.820 | 0.846 | 0.874 | 0.893 | 0.911 | 0.930 | 0.953 | |

| 4 | 0.852 | 0.871 | 0.887 | 0.902 | 0.920 | 0.923 | 0.934 | 0.940 | 0.952 | 0.960 | |

| 400 | 1 | 0.502 | 0.552 | 0.588 | 0.648 | 0.699 | 0.749 | 0.797 | 0.857 | 0.900 | 0.946 |

| 2 | 0.500 | 0.555 | 0.604 | 0.663 | 0.724 | 0.766 | 0.819 | 0.858 | 0.905 | 0.945 | |

| 3 | 0.576 | 0.627 | 0.672 | 0.715 | 0.765 | 0.809 | 0.844 | 0.882 | 0.900 | 0.929 | |

| 4 | 0.613 | 0.672 | 0.711 | 0.737 | 0.782 | 0.833 | 0.870 | 0.890 | 0.920 | 0.944 | |

| nominal coverage probability | |||||||||||

| 0.5 | 0.55 | 0.6 | 0.65 | 0.7 | 0.75 | 0.8 | 0.85 | 0.9 | 0.95 | ||

| 100 | 1 | 0.606 | 0.644 | 0.692 | 0.731 | 0.781 | 0.822 | 0.860 | 0.890 | 0.914 | 0.932 |

| 2 | 0.790 | 0.820 | 0.839 | 0.858 | 0.875 | 0.890 | 0.905 | 0.914 | 0.929 | 0.945 | |

| 3 | 0.920 | 0.928 | 0.938 | 0.947 | 0.952 | 0.956 | 0.963 | 0.965 | 0.970 | 0.973 | |

| 4 | 0.876 | 0.890 | 0.903 | 0.918 | 0.926 | 0.939 | 0.944 | 0.949 | 0.956 | 0.965 | |

| 200 | 1 | 0.518 | 0.561 | 0.619 | 0.672 | 0.719 | 0.763 | 0.809 | 0.861 | 0.903 | 0.939 |

| 2 | 0.578 | 0.638 | 0.691 | 0.732 | 0.773 | 0.810 | 0.857 | 0.883 | 0.909 | 0.934 | |

| 3 | 0.699 | 0.735 | 0.770 | 0.801 | 0.831 | 0.869 | 0.889 | 0.912 | 0.929 | 0.947 | |

| 4 | 0.841 | 0.865 | 0.883 | 0.900 | 0.911 | 0.919 | 0.932 | 0.943 | 0.952 | 0.958 | |

| 400 | 1 | 0.502 | 0.552 | 0.588 | 0.648 | 0.699 | 0.749 | 0.797 | 0.857 | 0.900 | 0.946 |

| 2 | 0.519 | 0.573 | 0.623 | 0.661 | 0.701 | 0.754 | 0.810 | 0.861 | 0.901 | 0.947 | |

| 3 | 0.568 | 0.615 | 0.673 | 0.717 | 0.760 | 0.800 | 0.837 | 0.868 | 0.903 | 0.929 | |

| 4 | 0.592 | 0.637 | 0.675 | 0.732 | 0.774 | 0.817 | 0.856 | 0.881 | 0.911 | 0.937 | |

| nominal coverage probability | |||||||||||

| 0.5 | 0.55 | 0.6 | 0.65 | 0.7 | 0.75 | 0.8 | 0.85 | 0.9 | 0.95 | ||

| 100 | 1 | 0.606 | 0.644 | 0.692 | 0.731 | 0.781 | 0.822 | 0.860 | 0.890 | 0.914 | 0.932 |

| 2 | 0.804 | 0.828 | 0.846 | 0.861 | 0.880 | 0.897 | 0.907 | 0.921 | 0.931 | 0.948 | |

| 3 | 0.923 | 0.929 | 0.938 | 0.947 | 0.953 | 0.957 | 0.963 | 0.964 | 0.970 | 0.974 | |

| 4 | 0.877 | 0.892 | 0.904 | 0.920 | 0.926 | 0.939 | 0.945 | 0.948 | 0.956 | 0.964 | |

| 200 | 1 | 0.518 | 0.561 | 0.619 | 0.672 | 0.719 | 0.763 | 0.809 | 0.861 | 0.903 | 0.939 |

| 2 | 0.601 | 0.658 | 0.710 | 0.754 | 0.799 | 0.828 | 0.864 | 0.895 | 0.913 | 0.940 | |

| 3 | 0.712 | 0.749 | 0.787 | 0.820 | 0.843 | 0.874 | 0.893 | 0.913 | 0.930 | 0.954 | |

| 4 | 0.852 | 0.870 | 0.886 | 0.902 | 0.919 | 0.924 | 0.933 | 0.940 | 0.952 | 0.960 | |

| 400 | 1 | 0.502 | 0.552 | 0.588 | 0.648 | 0.699 | 0.749 | 0.797 | 0.857 | 0.900 | 0.946 |

| 2 | 0.502 | 0.547 | 0.602 | 0.661 | 0.720 | 0.771 | 0.813 | 0.861 | 0.908 | 0.944 | |

| 3 | 0.566 | 0.618 | 0.672 | 0.720 | 0.765 | 0.808 | 0.844 | 0.881 | 0.902 | 0.931 | |

| 4 | 0.617 | 0.663 | 0.708 | 0.738 | 0.789 | 0.835 | 0.871 | 0.892 | 0.920 | 0.946 | |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| 0.476 | 1.509 | 2.198 | 3.705 | 0.170 | 0.656 | 1.208 | 1.601 | 0.081 | 0.267 | 0.635 | 1.101 | |

| 0.468 | 1.555 | 2.197 | 3.786 | 0.160 | 0.663 | 1.269 | 1.695 | 0.073 | 0.275 | 0.671 | 1.144 | |

| 0.494 | 1.433 | 2.247 | 3.870 | 0.160 | 0.690 | 1.257 | 1.755 | 0.071 | 0.303 | 0.722 | 1.214 | |

| 0.521 | 1.402 | 2.473 | 3.802 | 0.175 | 0.755 | 1.334 | 1.774 | 0.081 | 0.339 | 0.764 | 1.261 | |

| 0.503 | 1.379 | 2.665 | 3.867 | 0.235 | 0.814 | 1.445 | 1.916 | 0.121 | 0.408 | 0.843 | 1.343 | |

| 0.657 | 1.464 | 2.962 | 4.762 | 0.329 | 0.874 | 1.452 | 2.161 | 0.201 | 0.475 | 0.869 | 1.379 | |