Learning Linear Non-Gaussian Causal Models in the Presence of Latent Variables

Abstract

We consider the problem of learning causal models from observational data generated by linear non-Gaussian acyclic causal models with latent variables. Without considering the effect of latent variables, one usually infers wrong causal relationships among the observed variables. Under faithfulness assumption, we propose a method to check whether there exists a causal path between any two observed variables. From this information, we can obtain the causal order among them. The next question is then whether or not the causal effects can be uniquely identified as well. It can be shown that causal effects among observed variables cannot be identified uniquely even under the assumptions of faithfulness and non-Gaussianity of exogenous noises. However, we will propose an efficient method to identify the set of all possible causal effects that are compatible with the observational data. Furthermore, we present some structural conditions on the causal graph under which we can learn causal effects among observed variables uniquely. We also provide necessary and sufficient graphical conditions for unique identification of the number of variables in the system. Experiments on synthetic data and real-world data show the effectiveness of our proposed algorithm on learning causal models.

Keywords: Causal Discovery, Structural Equation Models, Non-Gaussianity, Latent Variables, Independent Component Analysis.

1 Introduction

One of the primary goals in empirical sciences is to discover casual relationships among a set of variables of interest in various natural and social phenomena. Such causal relationships can be recovered by conducting controlled experiments. However, performing controlled experiments is often expensive or even impossible due to technical or ethical reasons. Thus, it is vital to develop statistical methods for recovering causal relationships from non-experimental data.

Probabilistic graphical models are commonly used to represent causal relations. Alternatively, Structural Equation Models (SEM) which further specify mathematical equations among the variables can be used to represent probabilistic causal influences. Linear SEMs are a special class of SEMs where each variable is a linear combination of its direct causes and an exogenous noise. Under the causal sufficiency assumption, by utilizing conventional causal structure learning algorithms such as PC (Spirtes et al., 2000) and IC (Pearl, 2009), we can identify a class of models that are equivalent in the sense that they represent the same set of conditional independence assertions obtained from data. If we have background knowledge about the data-generating mechanism, we may further narrow down the possible models that are compatible with the observed data (Peters et al., 2016; Ghassami et al., 2018; Salehkaleybar et al., 2018; Zhang et al., 2017; Peters and Bühlmann, 2013; Zhang and Hyvärinen, 2009; Hoyer et al., 2009; Janzing et al., 2012). For instance, Shimizu et al. (2006) proposed a linear non-Gaussian acyclic model (LiNGAM) discovery algorithm that can identify causal structure uniquely by assuming non-Gaussian distributions for the exogenous noises in the linear SEM model. However, LiNGAM algorithm and its regression-based variant (DirectLiNGAM) (Shimizu et al., 2011) rely on the causal sufficiency assumption, i.e., no unobserved common causes exist for any pair of variables that are under consideration in the model.

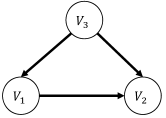

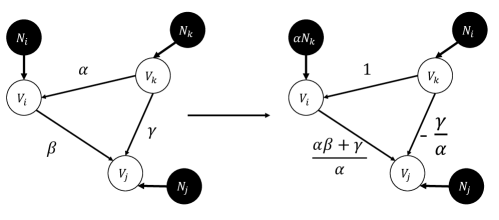

In the presence of latent variables, Hoyer et al. (2008) showed that linear SEM can be converted to a canonical form where each latent variable has at least two children and no parents. Such latent variables are commonly called “latent confounders”. Furthermore, they proposed a solution which casts the problem of identifying causal effects among observed variables into an overcomplete-ICA problem and returns multiple causal structures that are observationally equivalent. The time complexity of searching such structures can be as high as where and are the number of observed and total variables in the system, respectively. Entner and Hoyer (2010) proposed a method that identifies a partial causal structure among the observed variables by recovering all the unconfounded sets111A set of variables is called unconfounded if there is no variable outside the set which is confounder of some variables in the set. In Figure 1, variable is a confouder of variables and but it is not observable. Thus, the set of variables and is not unconfounded. and then learning the causal effects for each pair of variables in the set. However, their method may return an empty unconfounded set if latent confounders are the cause of most of observed variables in the system such as the simple example of Figure 1. Chen and Chan (2013) showed that a causal order and causal effects among observed variables can be identified if the latent confounders have Gaussian distribution and exogenous noises of observed variables are simultaneously super-Gaussian or sub-Gaussian.

In (Tashiro et al., 2014), the ideas in DirectLiNGAM was extended to the case where latent confounders exist in the system. The proposed solution first tries to find a root variable (a variable with no parents). Then, the effect of such variable is removed by regressing it out. This procedure continues until any variable and its residual becomes dependent. Subsequently, a similar iterative procedure is used to find a sink variable and remove its effect from other variables. However, this solution may not recover causal order in some causal graphs such as the one in Figure 1.222In Figure 1, the root variable () is latent and the regressor of sink variable and the residual are not independent without considering the latent variable in the set of regressors. Thus, no root or sink variable can be identified in the system.. Shimizu and Bollen (2014) proposed a Bayesian approach for estimating the causal direction between two observed variables when the sum of non-Gaussian independent latent confounders has a multivariate -distribution. They compute log-marginal likelihoods to infer causal directions.

Rather surprisingly, although the causal structure is in general not fully identifiable in the presence of latent variables, we will show that the causal order among the observed variables is still identifiable under the faithfulness assumption. In order to obtain a causal order, we first check whether there exists a causal path between any two observed variables. Subsequently, from this information, we obtain a causal order among them. Having established a causal order, we aim to figure out whether the causal effects are uniquely identifiable from observational data. We show by an example that causal effects among observed variables is not uniquely identifiable even if the faithfulness assumption holds true and the exogenous noises are non-Gaussian. We propose a method to identify the set of all possible causal effects efficiently in time that are compatible with the observational data. Furthermore, we present some structural conditions on the causal graph under which causal effects among the observed variables can be identified uniquely. We also provide necessary and sufficient graphical conditions under which the number of latent variables is uniquely identifiable.

The rest of this paper is organized as follows. In Section 2, we define the problem of identifying causal orders and causal effects in linear causal systems with latent variables. In Section 3, we propose our approach to learn the causal order among the observed variables and provide necessary and sufficient graphical conditions under which the number of latent variables is uniquely identifiable. In Section 4, we present a method to find the set of all possible causal effects which are consistent with the observational data and give conditions under which causal effects are uniquely identifiable. We conduct experiments to evaluate the performance of proposed solutions in Section 5 and conclude in Section 6.

2 Problem Definition

2.1 Notations

In a directed graph with the vertex set and the edge set , we denote a directed edge from to by . A directed path in is a sequence of vertices of where there is a directed edge from to for any . We define the set of variables as the intermediate variables on the path . We use notation to show that there exists a directed path from to . If there is a directed path from to , is ancestor of and that is a descendant of . More formally, and . Each variable is an ancestor and a descendant of itself.

We denote vectors and matrices by boldface letters. The vectors and represent -th row and column of matrix , respectively. The entry of matrix is denoted by . For matrix and matrix , the notation denotes the horizontal concatenation. For matrix and matrix , the notation shows the vertical concatenation.

2.2 System Model

Consider a linear SEM among a set of variables :

| (1) |

where the vectors and denote the random variables in and their corresponding exogenous noises, respectively. The entry of matrix shows the strength of direct causal effect of variable on variable . We assume that the causal relations among random variables can be represented by a directed acyclic graph (DAG). Thus, the variables in can be arranged in a causal order, such that no latter variable causes any earlier variable. We denote such a causal order on the variables by in which shows the position of variable in the causal order. The matrix can be converted to a strictly lower triangular matrix by permuting its rows and columns simultaneously based on the causal order.

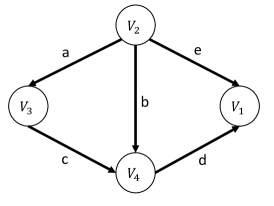

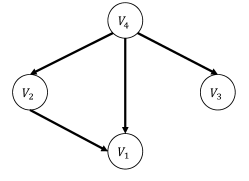

Example 1

Consider the following linear SEM with four random variables :

where and are some constants (see Figure 2). A causal order in this SEM model would be: . Hence, the matrix is strictly lower triangular where is a permutation matrix associated with defined by the following non-zero entries: .

We split random variables in into an observed vector and a latent vector where and are the number of observed and latent variables, respectively. Without loss of generality, we assume that first entries of are observable, i.e. and . Therefore,

| (2) |

where and are the vectors of exogenous noises of and , respectively. Furthermore, we have: .

The causal order among all variables , induces a causal order among the observed variables as follows: For any two observed variables , , if . Similarly, induces a causal order among latent variables. We denote this causal order by . It can be easily shown that and can be converted to strictly lower triangular matrices by permuting rows and columns simultaneously based on causal orders and , respectively.

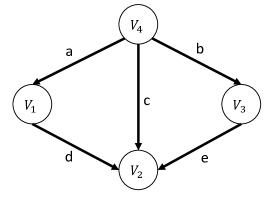

Example 2

In Example 1, suppose that only variables and are observable. Then, the causal order among observed variables would be: and . Thus, is a strictly lower triangular matrix where . For the latent variables, and .

In the remainder of this section, we briefly describe LiNGAM algorithm, which is capable of recovering the matrix uniquely if all variables in the model are observable and exogenous noises are non-Gaussian (Shimizu et al., 2006). The vector in Equation (1) can be written as a linear combination of exogenous noises as follows:

| (3) |

where . The above equation fits into the standard linear Independent Component Analysis (ICA) framework, where independent non-Gaussian components are all variables in . By utilizing statistical techniques in ICA (Hyvärinen et al., 2004), matrix can be identified up to scaling and permutations of its columns. More specifically, the independent components of ICA as well as the estimated matrix are not uniquely determined because permuting and rescaling them does not change their mutual independence. So without knowledge of the ordering and scaling of the noise terms, the following general ICA model for holds:

| (4) |

where contains independent components and these components (resp. the columns of ) are a permuted and rescaled version of those in (resp. the columns of ). In what follows, we use for the matrix while is the mixing matrix for the ICA model, as given in (4). Hence can be written as:

where is a permutation matrix and is a diagonal scaling matrix. Yet the corresponding causal model, represented by , can be uniquely identified because of its acyclicity constraint. In particular, the inverse of can be converted uniquely to a lower triangular matrix having all-ones on its diagonal by some scaling and permutation of the rows.

3 Identifying Causal Orders among Observed Variables

Since the graph with adjacency matrix is acyclic, there exists an integer such that . Thus, we can rewrite in the following form:

| (5) |

It can be seen that there exists a casual path of length from the exogenous noise of variable to variable if entry of matrix is nonzero. We define as the total causal effect of variable on variable .

Assumption 1

(Faithfulness assumption) The total causal effect from variable to is nonzero if there is a causal path from to . Thus, we have: if .

In the following lemma, we list two consequences of the faithfulness assumption that are immediate from the definition.

Lemma 1

Under the faithfulness assumptions, for any two observed variables and , , the following holds:

(i) Suppose that . If for some , then .

(ii) If there is no causal path between and , then and .

Based on Equation (2), we can write in terms of and as follows

| (6) |

where . Let , , and . Thus, where . This equation fits into a linear over-complete ICA where the exogenous noises are non-Gaussian and the number of observed variables is less than the number of variables in the system. The following proposition asserts when the columns of matrix are still identifiable up to some permutations and scaling.

Definition 2

(Reducibility of a matrix) A matrix is reducible if two of its columns are linearly dependent.

Proposition 3

((Eriksson and Koivunen, 2004), Theorem 3) In the linear over-completer ICA problem, the columns of mixing matrix can be identified up to some scaling and permutation if it is not reducible.

Lemma 4

The columns of corresponding to any two observed variables are linearly independent.

Proof

Consider any two observed variables and . We know that and are non-zero. Furthermore, is a sub-matrix of . Hence, based on Lemma 1 (), if there is no causal path between and , we have: and . Thus, and are not linearly dependent. Furthermore, if one of the variable is the ancestor of the another one, let say , according to Lemma 1 (), while . Thus, and are also not linearly dependent in this case and the proof is complete.

Although columns of corresponding to the observed variables are pairwise linearly independent, a column corresponding to a latent variable might be linearly dependent on a column corresponding to an observed or latent variable (see Example 3). In that case, we can remove the column and from matrix and vector , respectively and replace by where is a constant such that . We can continue this process until all the remaining columns are pairwise linearly independent. Let and be the resulting mixing matrix and exogenous noise vector, respectively. According to Lemma 4, all the columns of corresponding to observed variables are in . We utilize the matrix to recover a causal order among the observed variables.

Since the matrix is not reducible, its column can be identified up to some scaling and permutation according to Proposition 3. Let be the recovered matrix containing columns of . Consider any two observed variables and , i.e., . We extract two rows of corresponding to variables and . Let be the number of columns in whose first entries are zero but second entries are nonzero. Similarly, let be the number of columns that their first entries are nonzero but their second entries are zero. The following lemma asserts that the existence of a causal path between and can be checked from and (or equivalently, ).

Lemma 5

Under the faithfulness assumption, the existence of a causal path between any two observed variable can be inferred from matrix .

Proof. First, we show that if , then and . We know that the matrix can be converted to by some permutation and scaling of its columns. Moreover, contains some of the columns of including all the columns corresponding to the observed variables. Thus, from Lemma 1, we know that if for any , then . Moreover, we have: and . Hence, we can conclude that: and .

If and , then . By contradiction, suppose that there is no causal path between and or . The second case () does not happen due to what we just proved. Furthermore, from Lemma 1, we know that , . Therefore, which is in contradiction with our assumption. Hence, we can conclude that and if and only if .

We can construct an auxiliary directed graph whose vertices are the observed variables and a directed edge exists from to if (which we can infer from and ). Any causal order over the auxiliary graph is a correct causal order among the observed variables .

Example 3

Consider the causal graph in Figure 3. Suppose that variables and are latent. The matrix would be:

We can remove the third column from and update the vector to . Thus, the matrix is equal to:

which is not reducible. Without loss of generality, assume that the recovered matrix is equal to . Therefore, and . Hence, we can infer that there is a causal path from to .

Recovering the Number of Variables in the System

According to Proposition 3, the number of variables in the system can be recovered if and only if the matrix is not reducible. Furthermore, Equation (6) implies that matrix is not reducible if and only if the columns of the following matrix are not linearly independent: . In the rest of this section, we will present equivalent necessary and sufficient graphical conditions under which the number of variables in the systems can be uniquely identified. But before that, we present a simple example where is reducible and give a graphical interpretation of it.

Example 4

Consider a linear SEM with three variables and where , , and . Thus, the corresponding causal graph would be: . Suppose that is the only latent variable. Hence, , , and which is linearly dependent on the first column of . In fact, latent variable can be absorbed in variable by changing the exogenous noise of from to . Thus, the number of variables in this model cannot be identified uniquely in this model.

Definition 6

(Absorbing) Variable is said to be absorbed in variable if the exogenous noise of is set to zero , and the exogenous noise of is replaced by . We define absorbing a variable in by setting its exogenous noise to zero.

Definition 7

(Absorbablity) Let be the joint distribution of the observed variables after absorbing in . We say is absorbable in if .

The following theorem characterizes the graphical conditions where a latent variable is absorbable. The proof of theorem is given in Appendix A.

Theorem 8

(a) A latent variable is absorbable in if and only if it has no observable descendant.

(b) A latent variable is absorbable in variable (observed or latent), if and only if all paths from to its observable

descendants go through .

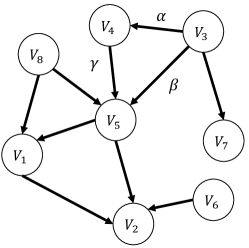

Example 5

Consider a linear SEM with corresponding causal graph in Figure 4 where and are the only observed variables. satisfies condition (a) and its exogenous noise can be set to zero. Furthermore, and satisfy condition (b) with respect to and they can be absorbed in by setting the exogenous noise of to . Finally, satisfies condition (b) and it can be absorbed in . Note that and cannot be absorbed in or .

Definition 9

We say a causal graph is minimal if none of its variables are absorbable.

Based on above definition, a causal graph is minimal if none of the latent variables satisfy the conditions in Theorem 8. We borrowed the terminology of minimal causal graphs from Pearl (1988) for polytree causal structures. In (Pearl, 1988), a casual graph is called minimal if it has no redundant latent variables in the sense that the joint distribution without latent variables remains a connected tree. Later, Etesami et al. (2016) showed that in minimal latent directed information polytrees, each node has at least two children. The following lemma asserts that the same argument holds true for the non-absorbable latent variables in our setting. The proof of lemma is given in Appendix B.

Lemma 10

A latent variable is non-absorbable if it has at least two non-absorbable children.

Next theorem gives necessary and sufficient graphical conditions for non-reduciblity of the matrix . The proof of theorem is given in Appendix C.

Theorem 11

The matrix is not reducible almost surely if and only if the corresponding causal graph is minimal.

Corollary 12

Under faithfulness assumption and non-Gaussianity of exogenous noises, the number of variables in the system is identifiable almost surely if the corresponding graph is minimal.

4 Identifying Total Causal Effects among Observed Variables

In this section, first, we will show by an example that total causal effects among observed variables cannot be identified uniquely under the faithfulness assumption and non-Gaussianity of exogenous noises333This example has also been studied in (Hoyer et al., 2008).. However, we can obtain all the possible solutions. Furthermore, under some additional assumptions on linear SEM, we show that one can uniquely identify total causal effects among observed variables.

4.1 Example of non-Uniqueness of Total Causal Effects

Consider causal graph in Figure 5 where and are observed variables and is latent variable. The direct causal effects from to , from to , and from to are , , and , respectively. We can write and based on the exogenous noises of their ancestors as follows:

| (7) | ||||

Now, we construct a second causal graph depicted in Figure 5 where the exogenous noises of variables and are changed to and , respectively. Furthermore, we set the direct causal effects from to , from to , and from to to , , and , respectively. It can be seen that equations in (7) do not change while the direct causal effect from to becomes in the second causal graph. Thus, we cannot identify causal effect from to merely by observational data from and . In Appendix D, we extend this example to the case where there might be multiple latent variables on the path from to and , and from to .

The above example shows that causal effects may not be identified even by assuming non-Gaussianity of exogenous noises if we have some latent variables in the system. In the following, we first show that the set of all possible total causal effects can be identified. Afterwards, we will present a set of structural conditions under which we can uniquely identify total causal effects among observed variables.

4.2 Identifying the Set of All Possible Total Causal Effects

Since the subgraph corresponding to is a DAG, there exists an integer such that . Hence, we can rewrite matrix given in (6) as follows

| (8) |

Lemma 13

Matrix in (6) can be converted to a strictly lower triangular matrix by permuting columns and rows simultaneously based on the causal order .

Proof.

Let be the permutation matrix corresponding the causal order . We want to show that is strictly lower triangular. It suffices to prove is strictly lower triangular for any . Suppose that there exists a nonzero entry, , in where . Then, there should be a directed path from observed variable to of length through latent variables in the causal graph where is the index of an observed variable whose order is in the causal order . This means variable should come before variable in any causal order. But this violates the causal order .

Previously, we showed that existence of a causal path between any two observed variables and can be determined by performing over-complete ICA. Let be the set of all observed descendants of , i.e., . We will utilize ’s to enumerate all possible total causal effects among the observed variables.

Remark 14

From Lemma 4, we have: for any .

As we discussed in Section 3, under non-Gaussianity of exogenous noises, the columns of can be determined up to some scalings and permutations by solving an overcomplete ICA problem. Let be the number of columns of . Furthermore, without loss of generality, assume that variables are the latent variables in the system whose corresponding columns remain in .

Theorem 15

Let , for any . Under faithfulness assumption and non-Gaussianity of exogenous noises, the number of all possible ’s that can generate the same distribution for according to (2), is equal to .

Proof. According to Proposition 3, under non-Gaussianity of exogenous noises, the columns of can be determined up to some scalings and permutations by solving an overcomplete ICA problem. Furthermore, for the column corresponding to the noise , , we have possible candidates with the same set of indicies of non-zero entries where all of them are pairwise linearly independent. Let be a matrix by selecting one of the candidates for each column corresponding to noise , . Thus, we have possible matrices444Please note that diagonal entries of should be equal to one. Otherwise we can normalize each column to its on-diagonal entry.. Now, for each , we just need to show that there exists an assignment for , , , and such that they satisfy (6) and and can be converted to strictly lower triangular matrices with some simultaneous permutations of columns and rows.

Let and . Assume that consists of the remaining columns which are not in . We also add columns corresponding to latent absorbed variables to . Now, we set and to and , respectively. By these assignments, the proposed matrix satisfies in (6). Thus, we just need to show that can be converted to a strictly lower triangular matrix by some permutations. To do so, first note that from Lemma 13, we know that matrix can be converted to a strictly lower triangular matrix by a permutation matrix . Furthermore, based on this property of matrix , we have: . Thus, we can write:

Since the matrix is a lower triangular matrix for any , can be converted to a lower triangular matrix by permutation matrix . Furthermore, the set of nonzero entries of is the same as the one of . Thus, is also a lower triangular matrix where all diagonal elements of it are equal to one. Hence, we can write in the form of where is a strictly lower triangular matrix. Therefore, we have:

| (9) |

where the last term shows that can be converted to a strictly lower triangular matrix and the proof is complete.

Comparing our results with (Hoyer et al., 2008), we can obtain all sets ’s and determine which columns can be selected as corresponding columns of observed variables in and then enumerate all the possible total causal effects while the proposed algorithm in (Hoyer et al., 2008) requires to search a space of different possible choices. Moreover, we can identify a causal order uniquely with the same time complexity by utilizing the method proposed in Section 3.

4.3 Unique Identification of Causal Effects under Structural Conditions

Based on Theorem 15, in this part, we propose a method to identify total causal effects uniquely under some structural conditions.

Assumption 2

Assume that for any observed variables and any latent variable , we have: .

Assumption 2 is a very natural condition that one expects to hold for unique identifiability of causal effects. This is because if Assumption 2 fails, then based on Theorem 15, there are multiple sets of total causal effects that are compatible with the observed data.

Theorem 16

Proof.

Let matrix be the output of over-complete ICA problem whose columns are the columns in matrix . We define as the the set of indices of nonzero entries of column , i.e. . We know that if corresponds to the observed variable . Moreover, under Assumption 2, any observed variable and any variable (observed or latent) have different sets and . Thus, each set is just equal to one of ’s, let say . The column normalized to shows the total causal effects from variable to other observed variables.

The description of the proposed solution in Theorem 16 is given in Algorithm 1. It is noteworthy to mention that the example in Section 4.1 (given in Figure 5) violates the conditions in Theorem 16 since we have . We have shown for this example that the causal effect from to cannot be identified uniquely.

5 Experiments

In this section, we first evaluate the performance of the proposed method in recovering causal orders from synthetic data, generated according to the causal graph in Figure 1. Our experiments show that the proposed method returns a correct causal order while, as we have discussed in Introduction section, the previous methods (Entner and Hoyer, 2010; Shimizu et al., 2011) cannot identify the causal order. We also consider another causal graph which satisfies Assumption 2 and demonstrate that the proposed method can return the correct causal effects. Next, we evaluate the performance of the proposed method for different number of variables in the system. Afterwards, for real data, we consider the daily closing prices of four world stock indicies and check the existence of causal paths between any two indicies. The results are compatible with common beliefs in economy.

5.1 Synthetic data

First, for the causal graph in Figure 1, we generated 1000 samples of observed variables and where nonzero entries of matrix is equal to . We utilized Reconstruction ICA (RICA) algorithm (Le et al., 2011) to solve the over-complete ICA problem as follows: Let be a matrix containing observational data where is -th sample of variable and is the number of samples. First, the sample covariance matrix of is eigen-decomposed, i.e., where is the orthogonal matrix, is a diagonal matrix, and is the sample mean vector. Then, the observed data is pre-whitened as follows: . The RICA algorithm tries to find matrix that is the minimizer of the following objective function:

where parameter controls the cost of penalty term. We estimated the matrix by where is the optimal solution of the above optimization problem.

In order to estimate the number of columns of , we held out 250 of samples for model selection. More specifically, we solved the over-complete ICA problem for different number of columns, evaluated the fitness of each model by computing the objective function of RICA over the hold-out set, and selected the model with minimum cost. In order to check whether an entry is equal to zero, we used the bootstrapping method (Efron and Tibshirani, 1994), which generates bootstrap samples by sampling with replacement from training data. For each bootstrap sample, we executed RICA algorithm to obtain an estimation of . Since in each estimation, columns are in arbitrary permutation, we need to match similar columns in estimations of . To do so, in each estimation, we divided all entries of a column by the entry with the maximum absolute value in that column. Then, we picked each column from the estimated mixing matrix, computed its distance from each column of another estimated mixing matrix, and matched to the one with a minimum distance. Afterwards, we used t-test with confidence level of to check whether an entry is equal to zero from the bootstrap samples. An estimation of from a bootstrap sample is given as follows:

Moreover, experimental results showed the correct support of , i.e., can be recovered with merely bootstrap samples. Thus, there is a causal path from to . Furthermore, for the causal graph in which is only the latent variable, we repeated the same procedure explained above. An estimation of from one of the bootstrap samples is given as follows:

From experiments, the estimated support of from bootstrap samples would be: . Thus, we can conclude that there is no causal path between and . Next, we considered the causal graph in Figure 6 where is the only latent variable. The direct causal effects of all directed edges are equal to . An estimation of from one of the bootstrap samples is given as follows:

Thus, we can imply that there is only a causal path from to . We can also estimate total causal effects between observed variables since this causal graph satisfies Assumption 2. The output of Algorithm 1 would be:

which is close to the true causal effects.

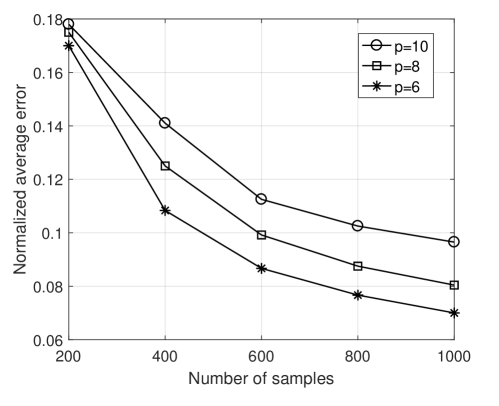

We generated 1000 DAGs of size by first selecting a causal order among variables randomly and then connecting each pair of variables with probability . We generated data from a linear SEM where nonzero entries of matrix is equal to , and the exogenous noises have a uniform distribution. In each generated DAG, we selected variables randomly as latent variables. We checked whether there is a causal path between any two observed variables by a similar procedure described for the previous examples. We define normalized error as the number of pairs such as that there exists a causal path from to in the true causal graph but we output that there is no causal path between them (or vice versa) to the total pairs, i.e., . In Figure 7, the average normalized error of the result given by our approach is depicted versus the number of samples. As can be seen, the average normalized error is fairly low for large enough samples. Furthermore, we have better performance for the cases with smaller number of variables in the system.

5.2 Real data

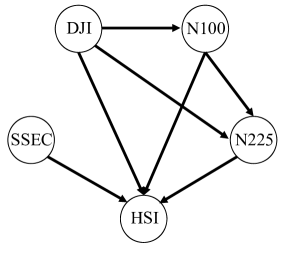

We considered the daily closing prices of the following world stock indicies from to , obtained from Yahoo financial database: Dow Jones Industrial Average (DJI) in USA, Nikkei 225 (N225) in Japan, Euronext 100 (N100) in Europe, Hang Seng Index (HSI) in Hong Kong, and the Shanghai Stock Exchange Composite Index (SSEC) in China.

Let be the closing price of -th index on day . We define the corresponding return by . We considered the returns of indicies as an observational data and applied the proposed method in Section 3 in order to check the existence of a causal path between any two indicies. Figure 8 depicts the causal relationships among the indicies. In this figure, there is a directed edge from index to index if we find a causal path from to . As can be seen, there are causal paths from DJI to HSI, N225, and N100 which is commonly known to be true in the stock market (Hyvärinen et al., 2010). Furthermore, HSI is influenced by all other indicies and SSEC only affects HSI which these findings are compatible with the previous results in (Hyvärinen et al., 2010).

6 Conclusions

We considered the problem of learning causal models from observational data in linear non-Gaussian acyclic models with latent variables. Under the faithfulness assumption, we proposed a method to check whether there exists a causal path between any two observed variables. Moreover, we gave necessary and sufficient graphical conditions to uniquely identify the number of variables in the system. From the information about existence of a directed path, we obtain a causal order among the observed variables. Next, we considered the problem of estimating total causal effects. We showed by an example that causal effects among observed variables cannot be identified uniquely even under the faithfulness assumption and non-Gaussianity of exogenous noises. However, we can identify all possible set of total causal effects that are compatible with the observational data efficiently in time. Furthermore, we presented structural conditions under which we can learn total causal effects among observed variables uniquely. Experiments on synthetic data and real-world data showed the effectiveness of our proposed algorithms on learning causal models.

Appendix A. Proof of Theorem 8

“if” part:

We say a directed path is latent if all the variables on the path except the endpoint are latent. The “if” parts of conditions in Theorem 8 can be rewritten as follows:

(a) Latent variable , , is absorbable in if it has no observable descendant.

(b1) Latent variable , , is absorbable in observed variable , , if is the only observed variable influenced by through some latent paths.

(b2) Latent variable , , is absorbable in latent variable , , if all latent paths from to observed variables go through .

It is easy to show that conditions (b1) and (b2) are equivalent to “if” part of condition (b) in Theorem 8.

From (6), we know that where entry of matrix is the total causal effect of latent variable to the observed variable . This entry would be zero if no directed path exists from latent variable to observed variable . Now, we prove the correctness of above conditions:

(a) If a latent variable has no observable descendant, then the -th column of is all zeros. Hence, there would be no changes in by setting to zero. Therefore, there would be no change in .

(b1) Since latent variable only influences one observed variable through latent paths, has only one non-zero entry and therefore linearly dependent on one of columns of identity matrix, let say -th column. Moreover, the total causal effect from to , i.e., is equal to since there is no causal path from to that goes through an observed variable other than . Thus, we replace by and set to zero and there would be no change in .

(b2) Consider any observed variable , . If all latent paths of go though , then since all the paths from to are latent. Thus, we can change to and set to zero and there would be no change in .

“only if” part:

Now, we probe that the conditions (a), (b1), and (b2) are the only absorbable case. It can be easily shown that an observed variable cannot be absorbed into any other observed or latent variables. Thus, it is just needed to consider the following cases:

-

•

Absorbing a latent variable in an observed variable: Suppose that a latent variable can be absorbed in an observed variable . Furthermore, assume that also influences other observed variable through latent path(s). That is, there exist some paths that start from and end in without traversing, . Let be the causal strength of such paths. Then, . To absorb in , should be zero which would contradict the faithfulness assumption.

-

•

Absorbing a latent variable in another latent variable: Suppose that a latent variable can be absorbed in another latent variable but for some observed variable , all latent paths from do not go through . Let be the causal strength of such paths. Then, . To absorb in , should be zero which contradicts the faithfulness assumption.

Appendix B. Proof of Lemma 10

Suppose that a latent variable has at least two non-absorbable children such as and . We need to consider three cases:

-

•

If both of and are observed variables, then is not absorbable according to Theorem 8.

-

•

Suppose that and are latent variables. Each of them must reach at least two observed variables through latent paths (due to condition (b) in Theorem 8). Thus, also reaches those observed variables through latent paths. Furthermore, all of latent paths starting from does not go through only one latent variables. Hence, none of the conditions in Theorem 8 are not satisfied and is not absorbable.

-

•

One of or , let say variable , is observed. must reach an observed variable other than through some latent paths. Otherwise, it is absorbable. Therefore, is not absorbable since it does not satisfy any conditions in Theorem 8.

Appendix C. Proof of Theorem 11

If is not minimal, then it can be easily seen that is also reducible. Now, suppose that is minimal. We want to show that is also not reducible almost surely. By contradiction, suppose that is reducible. Then two columns of must be linearly dependent. Now, two cases should be considered:

-

•

One column of , let say -th column, and one column of are linearly dependent. Hence, all the latent paths starting from latent variable influences only one observed variable (Condition (b) in Theorem 8). Thus, is not minimal which is a contradiction.

-

•

Two columns of , let say are linearly dependent. If the corresponding columns have only one non-zero entry, then both of them can be absorbed in an observed variable (Condition (b) in Theorem 8). Thus, is not minimal. Now, suppose that these columns have more than one nonzero entry each, let say entries and . Without loss of generality, suppose that is the ancestor of . Let be the maximum length of latent paths starting from latent variable . By induction on , we will show that -th columns of are linearly dependent with measure zero. The case of is trivial. Suppose that for , the statement holds true. We will prove it for . Let latent variable be a child of and assume some paths from do not go through . We know that:

(10) Furthermore,

(11) for some values . Moreover, for some . Plugging (11) into (10), we have:

The above equation holds with measure zero if which is true with measure one from the induction hypothesis.

Appendix D. An Example of non-Identifiability of Total Causal Effects

Let be a causal path of length from variable to variable . We define the weight of path , denoted by , as the product of direct causal strengths of edges on the path:

| (12) |

Suppose that be the set of all causal paths from variable to variable . It can be shown that the total causal effect from to can be computed by the following equation:

| (13) |

Now, consider a causal graph in Figure 5 where and are observed variables and is latent variable. There exist causal paths from to and , and from to with the following properties:

-

•

Let be the causal paths from variable to variable where is not on any of these paths. We assume that .

-

•

All intermediate variables in , and are latent.

We can write and based on the exogenous noises of their ancestors as follows:

| (14) | ||||

where , , and .

Now, we construct a causal graph depicted in Figure 5 where the exogenous noises of variables and are changed to and , respectively. Furthermore, we pick three paths , , where:

By our first property on the paths, we can find two paths and such that . We also change the matrix to matrix where all the entries of are the same as except three entries , , and . We will adjust these three entries such that the total causal effects from to , from to , and from to become 1, , and , respectively. Moreover, these adjustments should not change the dependencies of observed variables and to the exogenous noises of their ancestors given in Equation (14). It can be shown that we can change the three mentioned causal effects to our desired values by the following adjustments:

Now, consider any latent variable which is on one of the paths in , , or . Changes in those mentioned three edges cannot affect the total causal effect from to or since the edges , , and are not a part of any paths from to or . Thus, equations in (14) do not change while the total causal effect from to becomes in the second causal graph. It is noteworthy to mention that changes in the equations of latent variables are not important since we are not observing these variables.

References

- Chen and Chan (2013) Zhitang Chen and Laiwan Chan. Causality in linear nongaussian acyclic models in the presence of latent gaussian confounders. Neural Computation, 25(6):1605–1641, 2013.

- Efron and Tibshirani (1994) Bradley Efron and Robert J Tibshirani. An introduction to the bootstrap. CRC press, 1994.

- Entner and Hoyer (2010) Doris Entner and Patrik O Hoyer. Discovering unconfounded causal relationships using linear non-gaussian models. In JSAI International Symposium on Artificial Intelligence, pages 181–195. Springer, 2010.

- Eriksson and Koivunen (2004) Jan Eriksson and Visa Koivunen. Identifiability, separability, and uniqueness of linear ica models. IEEE signal processing letters, 11(7):601–604, 2004.

- Etesami et al. (2016) Jalal Etesami, Negar Kiyavash, and Todd Coleman. Learning minimal latent directed information polytrees. Neural computation, 28(9):1723–1768, 2016.

- Ghassami et al. (2018) AmirEmad Ghassami, Saber Salehkaleybar, Negar Kiyavash, and Elias Bareinboim. Budgeted experiment design for causal structure learning. In International Conference on Machine Learning, pages 1724–1733, 2018.

- Hoyer et al. (2008) Patrik O Hoyer, Shohei Shimizu, Antti J Kerminen, and Markus Palviainen. Estimation of causal effects using linear non-gaussian causal models with hidden variables. International Journal of Approximate Reasoning, 49(2):362–378, 2008.

- Hoyer et al. (2009) Patrik O Hoyer, Dominik Janzing, Joris M Mooij, Jonas Peters, and Bernhard Schölkopf. Nonlinear causal discovery with additive noise models. In Advances in neural information processing systems, pages 689–696, 2009.

- Hyvärinen et al. (2004) Aapo Hyvärinen, Juha Karhunen, and Erkki Oja. Independent component analysis, volume 46. John Wiley & Sons, 2004.

- Hyvärinen et al. (2010) Aapo Hyvärinen, Kun Zhang, Shohei Shimizu, and Patrik O Hoyer. Estimation of a structural vector autoregression model using non-gaussianity. Journal of Machine Learning Research, 11(May):1709–1731, 2010.

- Janzing et al. (2012) Dominik Janzing, Joris Mooij, Kun Zhang, Jan Lemeire, Jakob Zscheischler, Povilas Daniušis, Bastian Steudel, and Bernhard Schölkopf. Information-geometric approach to inferring causal directions. Artificial Intelligence, 182:1–31, 2012.

- Le et al. (2011) Quoc V Le, Alexandre Karpenko, Jiquan Ngiam, and Andrew Y Ng. Ica with reconstruction cost for efficient overcomplete feature learning. In Advances in neural information processing systems, pages 1017–1025, 2011.

- Pearl (1988) Judea Pearl. Probabilistic Reasoning in Intelligent Systems: Networks of Plausible Inference. Morgan Kaufmann, 1988.

- Pearl (2009) Judea Pearl. Causality. Cambridge university press, 2009.

- Peters and Bühlmann (2013) Jonas Peters and Peter Bühlmann. Identifiability of gaussian structural equation models with equal error variances. Biometrika, 101(1):219–228, 2013.

- Peters et al. (2016) Jonas Peters, Peter Bühlmann, and Nicolai Meinshausen. Causal inference by using invariant prediction: identification and confidence intervals. Journal of the Royal Statistical Society: Series B (Statistical Methodology), 78(5):947–1012, 2016.

- Salehkaleybar et al. (2018) Saber Salehkaleybar, Jalal Etesami, Negar Kiyavash, and Kun Zhang. Learning vector autoregressive models with latent processes. In International Conference on Machine Learning, pages 4000–4007, 2018.

- Shimizu and Bollen (2014) Shohei Shimizu and Kenneth Bollen. Bayesian estimation of causal direction in acyclic structural equation models with individual-specific confounder variables and non-gaussian distributions. The Journal of Machine Learning Research, 15(1):2629–2652, 2014.

- Shimizu et al. (2006) Shohei Shimizu, Patrik O Hoyer, Aapo Hyvärinen, and Antti Kerminen. A linear non-gaussian acyclic model for causal discovery. Journal of Machine Learning Research, 7(Oct):2003–2030, 2006.

- Shimizu et al. (2011) Shohei Shimizu, Takanori Inazumi, Yasuhiro Sogawa, Aapo Hyvärinen, Yoshinobu Kawahara, Takashi Washio, Patrik O Hoyer, and Kenneth Bollen. Directlingam: A direct method for learning a linear non-gaussian structural equation model. Journal of Machine Learning Research, 12(Apr):1225–1248, 2011.

- Spirtes et al. (2000) Peter Spirtes, Clark N Glymour, Richard Scheines, David Heckerman, Christopher Meek, Gregory Cooper, and Thomas Richardson. Causation, prediction, and search. MIT press, 2000.

- Tashiro et al. (2014) Tatsuya Tashiro, Shohei Shimizu, Aapo Hyvärinen, and Takashi Washio. Parcelingam: a causal ordering method robust against latent confounders. Neural computation, 26(1):57–83, 2014.

- Zhang and Hyvärinen (2009) Kun Zhang and Aapo Hyvärinen. On the identifiability of the post-nonlinear causal model. In Proceedings of the twenty-fifth conference on uncertainty in artificial intelligence, pages 647–655. AUAI Press, 2009.

- Zhang et al. (2017) Kun Zhang, Biwei Huang, Jiji Zhang, Clark Glymour, and Bernhard Schölkopf. Causal discovery in the presence of distribution shift: Skeleton estimation and orientation determination. In Proc. International Joint Conference on Artificial Intelligence (IJCAI 2017), 2017.