Variational Bayes on Manifolds

Abstract

Variational Bayes (VB) has become a widely-used tool

for Bayesian inference in statistics and machine learning. Nonetheless, the development of the existing VB

algorithms is so far generally restricted to

the case where the variational parameter space is Euclidean,

which hinders the potential broad application of VB methods.

This paper extends the scope of VB to

the case where the variational parameter space is a Riemannian manifold.

We develop an efficient manifold-based VB algorithm

that exploits both the geometric structure of the constraint parameter space

and the information geometry of the manifold of VB approximating probability distributions.

Our algorithm is provably convergent and achieves a convergence rate of order and for a non-convex evidence lower bound function and a strongly retraction-convex evidence lower bound function, respectively.

We develop in particular two manifold VB algorithms, Manifold Gaussian VB and Manifold Wishart VB, and demonstrate through numerical experiments that

the proposed algorithms are stable, less sensitive to initialization and compares favourably to existing VB methods.

Keywords. Marginal likelihood, variational Bayes, natural gradient, stochastic approximation, Riemannian manifold.

1 Introduction

Increasingly complicated models in modern statistics and machine learning have called for more efficient Bayesian estimation methods. Of the Bayesian tools, Variational Bayes (VB) (Waterhouse et al.,, 1996; Jordan et al.,, 1999) stands out as one of the most versatile alternatives to conventional Monte Carlo methods for statistical inference in complicated models. VB approximates the posterior probability distribution by a member from a family of tractable distributions indexed by variational parameters belonging to a parameter space . The best member is found by minimizing the Kullback-Leibler divergence from the candidate member to the posterior. VB methods have found their application in a wide range of problems including variational autoencoders (Kingma and Welling,, 2013), text analysis (Hoffman et al.,, 2013), Bayesian synthetic likelihood (Ong et al., 2018a, ), deep neural nets (Tran et al.,, 2019), to name but a few.

Most of the existing VB methods work with cases where the variational parameter space is (a subset of) the Euclidean space . This paper considers the VB problem where is a Riemannian manifold, which naturally arises in many modern applications. For example, in Gaussian VB where the VB approximating distribution is a multivariate Gaussian with mean and covariance , belongs to the product manifold where is an Euclidean manifold and is the manifold of symmetric and positive definite matrices. We develop manifold-based VB algorithms that cast Euclidean-based constrained VB problems as manifold-based unconstrained optimization problems under which the solution can be efficiently found by exploiting the geometric structure of the constraints. Optimization algorithms that work on manifolds often enjoy better numerical properties. See the monograph of Absil et al., (2009) for recent advances.

Many Euclidean-based VB methods employ (Euclidean) stochastic gradient decent (SGD) for solving the required optimization problem, and it is well-known that the natural gradient (Amari,, 1998) is of major importance in SGD. The natural gradient, a geometric object itself, takes into account the information geometry of the family of approximating distributions to help stabilize and speed up the updating procedure. For a comprehensive review and recent development of the natural gradient descent in Euclidean spaces, the reader is referred to Martens, (2020). Extending natural gradient decent for use in Riemannian stochastic gradient decent is a non-trivial task and of interest in many VB problems. This paper develops a mathematically formal framework for incorporating the natural gradient into manifold-based VB algorithms. The contributions of this paper are threefold:

-

•

We develop a doubly geometry-informed VB algorithm that exploits both the geometric structure of the manifold constraints of the variational parameter space, and the information geometry of the manifold of the approximating family, which leads to a highly efficient VB algorithm for Bayesian inference in complicated models.

-

•

The proposed manifold VB algorithm is provably convergent and achieves a convergence rate of order and , with and the number of iterations, for a non-convex lower bound function and a strongly retraction-convex lower bound function, respectively.

-

•

We develop in detail a Manifold Gaussian VB algorithm and a Manifold Wishart VB algorithm, both can be used as a general estimation method for Bayesian inference. The numerical experiments demonstrate that these manifold VB algorithms work efficiently, are more stable and less sensitive to initialization as compared to some existing VB algorithms in the literature. We would like to emphasize that making VB more stable and less initialization-sensitive is of major importance in the current VB literature. We also apply our VB method to estimating a financial time series model and demonstrate its high accuracy in comparison with a “gold standard” Sequential Monte Carlo method.

The paper is organized as follows. Section 2 reviews the VB method on Euclidean spaces and sets up notations. Section 3 develops the manifold-based VB algorithm and Section 4 studies its convergence properties. Section 5 presents the Manifold Gaussian VB and the Manifold Wishart VB algorithms, and their applications. Section 6 concludes. The technical proofs are presented in the Appendix.

2 VB algorithms on Euclidean spaces

This section gives a brief overview of VB methods where the variational parameter lies in (a subset of) a Euclidean space. It also gives the definition of the natural gradient, and the motivation for extending the Euclidean-based VB problem into manifolds.

Let be the data and the likelihood function based on a postulated model, with the set of model parameters to be estimated. Let be the prior. Bayesian inference requires computing expectations with respect to the posterior distribution whose density (with respect to some reference measure such as the Lebesgue measure) is

where , called the marginal likelihood. It is often difficult to compute such expectations, partly because the density itself is intractable as the normalizing constant is often unknown. For simple models, Bayesian inference is often performed using Markov Chain Monte Carlo (MCMC), which estimates expectations w.r.t. by sampling from it. For models where is high dimensional or has a complicated structure, MCMC methods in their current development are either not applicable or very time consuming. In the latter case, VB is often an attractive alternative to MCMC. VB approximates the posterior by a probability distribution with density , - the variational parameter space, belonging to some tractable family of distributions such as Gaussian. The best is found by minimizing the Kullback-Leibler (KL) divergence from to

It is easy to see that

thus minimizing KL is equivalent to maximizing the lower bound on

| (2.1) |

SGD techniques are often employed to solve this optimization problem. The VB approximating distribution with the optimized is then used for Bayesian inference. See Tran et al., (2021) for an accessible tutorial introduction to VB.

Let

be the set of VB approximating probability distributions parameterized by , and

| (2.2) |

be the Fisher information matrix w.r.t. . By the Taylor expansion, we have that

| (2.3) |

This shows that the local KL divergence around the point is characterized by the Fisher matrix . Formally, can be made into a Riemannian manifold with the Riemannian metric induced by the Fisher information matrix (Rao,, 1945; Amari,, 1998).

Assume that the objective function is smooth enough, then

The steepest ascent direction for maximizing among all the directions with a fixed length is

| (2.4) |

By the method of Lagrangian multipliers, this steepest ascent is

| (2.5) |

Amari, (1998) termed this the natural gradient and popularized it in machine learning. In the statistics literature, the steepest ascent in the form (2.5) has been used for a long time and is often known as Fisher’s scoring in the context of maximum likelihood estimation (see, e.g., Longford, (1987)). We adopt the term natural gradient in this paper. The efficiency of the natural gradient over the ordinary gradient has been well documented (Sato,, 2001; Hoffman et al.,, 2013; Tran et al.,, 2017). A remarkable property of the natural gradient is that is is invariant under parameterization (Martens,, 2020), i.e. it is coordinate-free and an intrinsic geometric object. This further motivates the use of natural gradient in optimization on manifolds.

Most of the VB methods and natural gradient descent are developed for cases where the variational parameter lies in an unconstrained Euclidean space. In many situations, however, belongs to a non-linear constrained space that forms a differential manifold. A popular example is Gaussian VB where the covariance matrix of size is subject to the symmetric and positive definite constraint. Ong et al., 2018b avoid the difficulty of dealing with this constraint by using a factor decomposition , where a full-rank matrix of size with , and a diagonal matrix. Such a decomposition is invariant under orthogonal transformations of , i.e.

for all with an orthogonal matrix, i.e. . That is, the variational parameter lies in a quotient manifold where each point in this manifold is an equivalence class

| (2.6) |

This manifold structure is not considered in Ong et al., 2018b . Zhou et al., (2020) take into account this manifold structure and report some improvement over the plain VB methods. Another example is Wishart VB where the VB distribution is an inverse-Wishart distribution . Here, the variational parameter lives in the manifold of the symmetric and positive definite matrices.

Related work

As we employ the SGD method for optimizing the lower bound , our paper is related to the recent development of SGD algorithms on Riemannian manifolds. Bonnabel, (2013) is one of the first to develop SGD where the cost function is defined on a Riemannian manifold. It is showed in his paper that under some suitable conditions the Reimannian SGD algorithm converges to a critical point of the cost function. In a recent paper, Kasai et al., (2019) propose an adaptive SGD on Riemannian manifolds, which uses different learning rates for different coordinates. Their method is proved to converge to a critical point of the cost function at a rate . For a recent discussion of generalization of Euclidean adaptive SGD algorithms, such as Adam and Adagrad, to Riemannian manifolds, see Bécigneul and Ganea, (2018). The monograph of Absil et al., (2009) provides an excellent account of recent development on optimization on matrix manifolds. Companion user-friendly software such as Manopt (Boumal et al.,, 2014) has been developed to assist fast growing research in Riemannian optimization.

The natural gradient has been widely used in the machine learning literature; see, e.g., Sato, (2001), Hoffman et al., (2013), Khan and Lin, (2017) and Martens, (2020). However, most of the existing work only consider cases where the variational parameter belongs to an Euclidean space. Zhou et al., (2020) is the only paper that we are aware of develops a VB method on manifolds. However, their paper only considers the Factor Gaussian VB for the particular quotient manifold in (2.6), and does not consider natural gradient. Our paper develops a general VB method for Riemannian manifolds that incorporates the natural gradient, and provides a careful convergence analysis.

3 VB on manifolds with the natural gradient

This section presents our proposed VB algorithm on manifolds. Recall that we are interested in a VB problem where the variational parameter lies in a Riemannian manifold , i.e. we wish to solve the following optimization problem

In order to incorporate the natural gradient into Riemannian SGD, we view the manifold as embedded in a Riemannian manifold , whose Riemannian metric is defined by the Fisher information matrix . Let be the tangent space to at . The inner product between two tangent vectors is defined as

| (3.1) |

For VB on manifolds without using the natural gradient, this inner product is the usual Euclidean metric, i.e. . The metric in (3.1) is often referred to as the Fisher-Rao metric. Let be a differentiable function defined on such that its restriction on is the lower bound . Similar to (2.4)-(2.5), it can be shown that the steepest ascent direction at for optimizing the objective function , i.e. the direction of

is the natural gradient

| (3.2) |

Here, denotes the directional derivative of at in the direction of , and is the usual Euclidean gradient vector of . We note that, for ,

We recall that the Riemannian gradient of a smooth function on a Riemannian manifold , embedded in and equipped with the Riemannian metric , is the unique vector in the tangent space at such that

The following lemma is important for the purpose of this paper. It shows that the natural gradient is a Riemannian gradient defined in the ambient manifold , which leads to a formal framework for associating the natural gradient to the Riemannian gradient of the lower bound defined in the manifold .

Lemma 3.1.

The natural gradient of the function on the Riemannian manifold with the Fisher-Rao metric (3.1) is the Riemannian gradient of . In particular, the natural gradient at belongs to the tangent space to at .

We now need to associate the Riemannian gradient to the Riemannian gradient of the lower bound defined in ; the latter is what we need for using Riemannian SGD to optimize . This is done in the two cases: is a submanifold (Section 3.1) and is a quotient manifold (Section 3.2).

3.1 Riemannian submanifolds

Suppose that is a submanifold of . In order to define the Riemannian gradient of the lower bound defined on the manifold , we need to equip with a Riemannian metric. In most cases, this metric is inherited from that of in a natural way. Since is a subspace of , the Riemannian metric of can be defined as

with viewed as vectors in . With this metric, we can define the orthogonal complement of in , i.e. . Write

where and denote the projections on and , respectively. Recall that , . Then, the Riemannian gradient of is the projection of on

| (3.3) |

This is because

In some cases, such as Gaussian VB in Section 5.1,

, then ,

i.e. the natural gradient is the Riemannian gradient of .

In some other cases, however, using the inherited metric might lead to a projection that is cumbersome to compute.

In such cases, one needs to use an alternative Riemannian metric on such that the projection is easy to compute.

Below we give an example in the case of Stiefel manifold, which is a popular manifold in many applications.

Stiefel manifolds. Suppose that is a Stiefel manifold defined as

| (3.4) |

where is the set of real matrices of size . We can think of as embedded in , , equipped with the Fisher-Rao metric

| (3.5) |

where denotes the vectorization operator, is the Fisher matrix defined in (2.2) with the variational distribution. The natural gradient of function at is

| (3.6) |

where is the inverse of vec, sending a -vector to the corresponding matrix in . It is easy to see that the tangent space of at is

If we equip with the Riemannian metric defined in (3.5), the projection on is cumbersome to compute. We therefore opt to use the usual Euclidean metric

The following lemma gives an expression for the Riemannian gradient of defined on the Stiefel manifold, and is useful for many applications involving Stiefel manifolds. Similar results to Lemma 3.2 can be found in the literature (see., e.g., (Edelman et al.,, 1998)), however, here we state and prove the results specifically for the case is the natural gradient.

Lemma 3.2.

Let be a function on the Stiefel manifold equipped with the usual Euclidean metric. The Riemannian gradient of at is

| (3.7) |

with given in (3.6), and .

3.2 Quotient manifolds

This section derives the Riemannian gradient of when is a quotient manifold induced from the ambient manifold . Suppose that is a Riemannian manifold with the Riemannian metric . Suppose that there is an equivalence relation on defined as

and thus . This is the case of Gaussian VB with the covariance matrix having a factor decomposition. Define the equivalence class

i.e., the class of all parameterizations that represent the same distribution. Let

and define the canonical projection

| (3.8) |

Then we can endow the quotient set with the topology induced from by the projection . This makes become a smooth manifold called the quotient manifold, see Absil et al., (2009). If we define , i.e. , then is the function defined on that we want to optimise. For optimisation on , one needs to be able to represent numerically tangent vectors at each . Geometrical objects in , such as points and tangent vectors, are vectors in the usual sense, so they can be numerically represented in computer for numerical computation. However, geometrical objects in the quotient manifold are abstract, much of reseach in quotient manifolds has been focused on how to represent these geometrical objects numerically. The key tool is the concept of horizontal lift; see, e.g. Absil et al., (2009); Kobayashi and Nomizu, (1969).

By the level set theorem (Tu,, 2011, Chapter 2), is an embedded submanifold in , hence, it admits a tangent space

called the vertical space, which is a linear subspace of . Let be the orthogonal complement of in , called the horizontal space, i.e. The orthogonality here is w.r.t. the metric defined on . For each tangent vector at , there exists an unique vector in the horizontal space such that (Kobayashi and Nomizu,, 1969, Prop. 1.2)

is called the horizontal lift of . Then, as ,

| (3.9) |

which shows that the directional derivative of in the direction of is characterised by the directional derivative of in the direction of the horizontal lift . Intuitively, for the optimization purposes, we can ignore the vertical space and just focus on the horizontal space, as the objective function doesn’t change along the vertical space. It’s worth noting that the property (3.9) does not depend on any particular choice in .

Let be the Riemannian gradient of at . We have that, for all

as doesn’t change along the vertical space, which shows that . Let be the tangent vector to at that has as its horizontal lift. Then, by equipping with the inner product inherited from ,

| (3.10) |

we have that is the Riemannian gradient of at . We note that (3.10) does not depend on the choice of . So, with the inherited inner product from , the usual Riemannian gradient of on is the horizontal lift of the Riemannian gradient of on . This remarkable property of quotient manifolds makes it convenient for numerical optimisation problems.

Remark 3.1.

Technically, in order for the inherited Riemannian metric on to be well-defined, it is often required in the literature that does not depend on . This condition is typically not satisfied when is equipped with the Fisher-Rao metric as considered in this paper. However, as we show above, the Riemannian gradient of is still well-defined without this requirement, as (3.10) holds for any .

3.3 Retraction

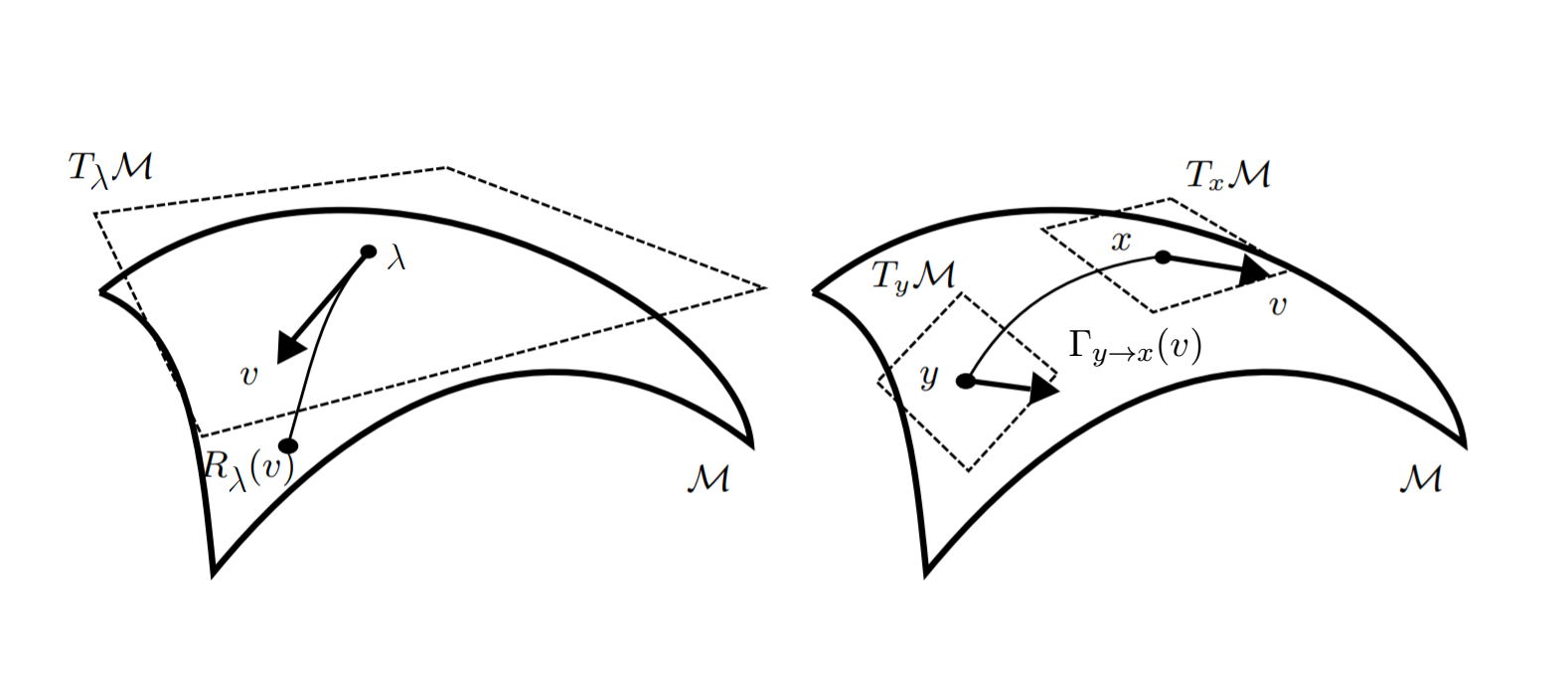

After deriving the Riemannian gradient, which is the steepest ascent direction of the lower bound function at the current point on the manifold, we need to derive the exponential map111In general, an exponential map at is defined locally near . In order to define exponential map on the entire tangent space, the manifold needs to be complete, see, e.g., Tu, (2011). , denoted by , that projects a point on the tangent space back to the manifold. Exponential map is a standard concept in differential geometry. Intuitively, exponential maps are mappings that, given a point on a manifold and a tangent vector at , generalize the concept “” in Euclidean spaces. is a point on the manifold that can be reached by leaving from and moving in the direction while remaining on the manifold. We refer to Absil et al., (2009) for a precise definition and examples. One major drawback of exponential maps is that their calculation is often cumbersome in practice. Retraction, the first order approximation of the exponential map, is often used instead. A retraction at has the important property that it preserves gradients, i.e. the curve satisfies for every . See (Absil et al.,, 2009, Chapter 4) for a formal definition of retraction and Manton, (2002) for an interpretation of retraction from a local optimization perspective. Also see Figure 1 (Left) for a visualization.

Closed-form formulae for retractions on common manifolds are available in the literature, see, for example, Absil et al., (2009). For instance, a popular retraction on the Stiefel manifold is

| (3.11) |

Here , where is the QR decomposition of , and is upper triangular. See Sato and Aihara, (2019) for an efficient computation of this retraction based on the Cholesky QR factorization. For quotient manifolds, a popular retraction is

is the horizontal lift of , and is the canonical projection in (3.8).

3.4 Momentum

The momentum method, which uses a moving average of the gradient vectors at the previous iterates to accelerate convergence and also help reduce noise in the estimated gradient, is widely used in Euclidean-based stochastic gradient optimization. Extending the momentum method to manifolds requires parallel translation, a tool in differential geometry for moving tangent vectors from one tangent space to another, while still preserving the length and angle (to some fixed direction) of the original tangent vectors. Similar to exponential map, a parallel translation is often approximated by a vector transport which is much easier to compute; see (Absil et al.,, 2009, Chapter 8) for a formal definition. See Figure 1 (Right) for a visualization. Let denote the vector transport of tangent vector to tangent space . A simple vector transport is the projection of on , i.e. . Roy and Harandi, (2017) is the first to use the momentum method in Riemannian SGD, but they do not provide any convergence analysis.

3.5 Manifold VB algorithm

The pseudo-code in Algorithm 1 summarizes our VB algorithm on manifolds. We use the “hat” notation in to emphasize that the natural gradient is obtained from a noisy and unbiased estimator of the Euclidean gradient as we often don’t have access to the exact .

That is, starting from an initial , the initial momentum gradient can be found by projecting the natural gradient estimate on . The relevant projections were described in Sections 3.1 and 3.2. At a step , from , we move on the tangent space along the direction to find the next iterate by retraction, . Then, we calculate the natural gradient estimate at , whose projection on gives the Riemannian gradient . Finally, the new momentum gradient is calculated from the vector transport of (to ) and .

4 Convergence analysis

To be consistent with the standard notation in the optimization literature, and with an abuse of notation, let us define the cost function as . That is, our optimization problem is

| (4.1) |

In this section, for notational simplicity, we will denote by the Riemannian gradient of the cost function , and by its unbiased estimator. Let be the iterates from Algorithm 1, and be the -field generated by . Because of the unbiasedness, we can write

with a martingale difference w.r.t. , i.e. . For the purpose of convergence analysis, we write our manifold VB algorithm as follows

| (4.2) |

The minus sign in results from the change in the notation above, and with the suitable choice of and we can recover Algorithm 1.

We next need some definitions.

Definition 4.1.

(Huang et al., 2015a, , Section 3.3) A neighborhood of is said to be totally retractive if there is such that for any , and is a diffeomorphism on , where is the ball of radius in centered at the origin .

Definition 4.2.

(Huang et al., 2015b, , Definition 3.1) For a function on a Riemannian manifold with retraction , define for , . The function f is retraction-convex with respect to the retraction in a set if for all , , is convex for all t which satisfy for all . Moreover, is strongly retraction-convex in if is strongly convex, that is for some positive constants .

Remark 4.1.

If is strongly convex with then

where If we assume that is strongly retraction-convex in and for any , there exists such that and the derivative is bounded, then the chain rule implies with As a result,

In Theorem 1, we show the convergence of (4.2) under suitable conditions imposed on the objective function . It is worth emphasizing that the convergence analysis in this section is done in a general setting for Riemannian SGD with momentum rather than restricting on the VB problem in the previous sections. It can therefore be applied to more general settings.

Theorem 1.

-

Assume that

-

•

There exists a totally retractive neighborhood of , , such that for any .

-

•

and are bounded such that almost surely for some constant .

-

•

is -Lipschitz with respect to retraction , that is, for , .

Consider the sequence obtained from (4.2) using . The following holds true:

| (4.3) |

Moreover, when the objective function is strongly retraction-convex, for , by choosing , there exists a constant such that

The proof can be found in the Appendix. We note that the first assumption in Theorem 1 is standard, see, for example Huang et al., 2015a . The condition is essential to make sure that stays bounded. That is, it does not diverge to infinity, which is the key property of the algorithm. While the Lipschitz property of guarantee that we can expand using Taylor expansion. The assumption related to the martingale difference is justified by the fact that the estimator is unbiased.

5 Applications

5.1 Manifold Gaussian VB

Gaussian VB (GVB) uses a multivariate Gaussian distribution for the VB approximation , . GVB has been extensively used in the literature, often with some simplifications imposed on ; e.g., is a diagonal matrix or has a factor structure . One of the reasons of imposing these simplifications is to deal with the symmetric and positive definiteness constraints on . We do not impose any simplifications on , and deal with these constraints by considering the VB optimization problem on the manifold of symmetric and positive definite matrices . We can think of as embedded in .

From (2.1), the gradient of lower bound is (Tran et al.,, 2021)

Here, we use the so-called score-function VB as in Tran et al., (2017), which does not require the gradient of the log-likelihood. We follow Tran et al., (2017) and use a control variate for the gradient of lower bound

| (5.1) |

where is a vector selected to minimize the variance of the gradient estimate

with the size of , which can be estimated by sampling from .

Mardia and Marshall, (1984) show that the Fisher information matrix for the multivariate Gaussian distribution is

where is an matrix with entries

One can derive that , with the Kronecker product. Therefore

| (5.2) |

which gives a convenient form for obtaining an approximate natural gradient. The natural gradient w.r.t. and is approximated as

| (5.3) | ||||

| (5.4) |

As , the projection in (3.3) is the identity, hence is the Riemannian gradient of lower bound w.r.t. . The Manifold GVB algorithm is outlined in Algorithm 2.

One of the most popular retractions used for the manifold of symmetric and positive definite matrices is (see the Manopt toolbox of Boumal et al., (2014))

| (5.5) |

and vector transport

| (5.6) |

The Matlab code implementing the Manifold GVB algorithm is made available online at https://github.com/VBayesLab.

Numerical experiments

We apply the Manifold GVB algorithm to fitting a logistic regression model using the German Credit dataset. This dataset, available on the UCI Machine Learning Repository https://archive.ics.uci.edu/ml/index.php, consists of observations on 1000 customers, each was already rated as being “good credit” (700 cases) or “bad credit” (300 cases). The covariates include credit history, education, employment status, etc. and lead to totally 25 predictors after using dummy variables to represent the categorical covariates.

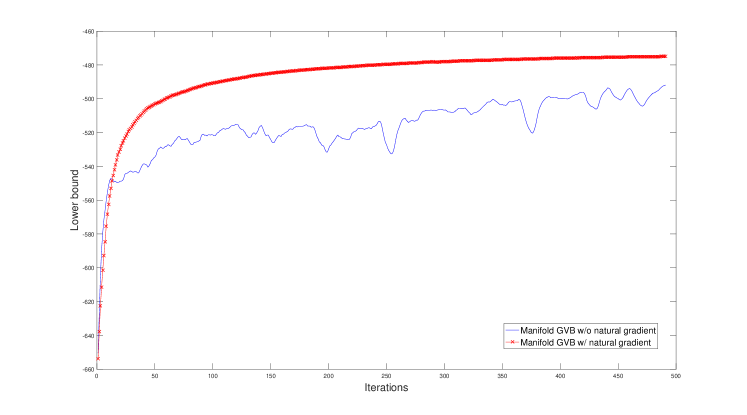

A naive GVB implementation is to only update when its updated value satisfies the symmetric and positive definiteness constraint. This naive implementation didn’t work at all in this example. To see the usefulness of incorporating the natural gradient into the Manifold GVB, we compare Algorithm 2 with a version without using the natural gradient. As shown in Figure 2, using the natural gradient leads to a much faster and more stable convergence. Also, the Manifold GVB without the natural gradient requires a large number of samples used in estimating the gradient (5.1) (we used ), compared to for the Manifold GVB with the natural gradient. The CPU running time for the Manifold GVB algorithms with and without the natural gradient is 43 and 280 seconds, respectively.

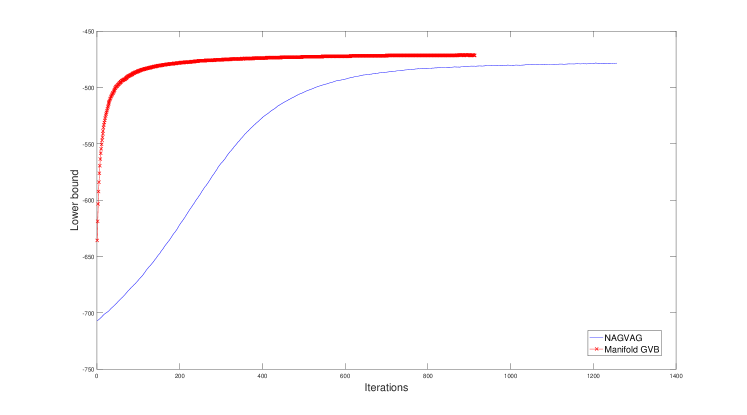

Tran et al., (2019) develop a Gaussian VB algorithm where is factorized as with a vector, and term their algorithm NAGVAC. Figure 3 plots the lower bound estimates of the Manifold GVB and NAGVAC. Manifold GVB stopped after 921 iterations and NAGVAC stopped after 1280 iterations, and their CPU running times are 19 seconds and 12 seconds, respectively. As shown, the Manifold GVB algorithm converges quicker than NAGVAC and obtains a larger lower bound. We note, however, that NAGVAC is less computational demanding than Manifold GVB in high-dimensional settings such as deep neural networks.

To assess the training stability of the Manifold GVB and NAGVAC algorithms, we use the same initialization and for both algorithms and run each for 20 different replications. The standard deviations of the estimates of (across the different runs, then averaged over the 25 coordinates) for NAGVAC and Manifold GVB are 0.03 and 0.01, respectively. This demonstrates that the Manifold GVB algorithm is more stable than NAGVAC. To assess their sensitivity to the initialization, in each algorithm, we now use a random initialization but fix the random seed in the updating stage. The standard deviations of the estimates of (across the different runs, then averaged over the 25 coordinates) for NAGVAC and Manifold GVB are 0.0074 and 0.0009, respectively. This demonstrates that the Manifold GVB algorithm is less sensitive to the initialization than NAGVAC.

Application to financial time series data

This section applies the MGVB method to analyze a financial stock return data set, and compares MGVB to Sequential Monte Carlo (SMC). We consider the GARCH model of Bollerslev, (1986) for modelling the underlying volatility dynamics in the Standard & Poor 500 stock indices observed from 4 Jan 1988 to 26 Feb 2007 (1000 observations). Let be the stock returns. We consider the following GARCH model

The parameters are , and , with the constraint to ensure the stationarity. To impose this constraint, we parameterize and as and with . We use an inverse Gamma prior IG for and an uniform prior for and . Finally, we use the following transformation

and work with the unconstrained parameters , but we will report the results in terms of the original parameters .

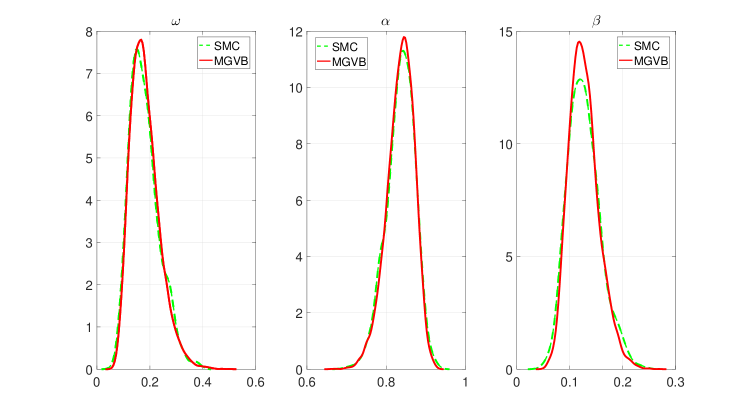

We compare the MGVB method to SMC. In this application with only three unknown parameters, SMC is applicable and can be considered as the “gold standard” as it produces an asymptotically exact approximation of the posterior . We implement the likelihood annealing SMC method of Tran et al., (2014), which is a robust SMC sampling technique that first draws samples from an easily-generated distribution and then moves these samples via annealing distributions towards the posterior distribution through weighting, resampling and Markov moving. We run SMC with 10,000 particles and the annealing distributions are adaptively designed such that the effective sample size is always at least 80%. Figure 4 plots the posterior estimates for the model parameters by SMC and MGVB, which shows that the MGVB estimates are almost identical to that of SMC. The CPU running time for MGVB and SMC is 10.4 and 380.5 seconds, respectively.

5.2 Manifold Wishart Variational Bayes

Suppose that we are interested in approximating the posterior distribution of a covariance matrix of size by an inverse-Wishart distribution . The density is

with

the multivariate gamma function. The gradient of w.r.t. and are

and

where . From this, it is straightforward to estimate the gradients of the lower bound and using the score-function method. It is often much more efficient to use

| (5.7) |

instead of , which is analogous to the use of the natural gradient in (5.4). The natural-gradient-like expression in (5.7) is often found very useful in practice; without it, it is difficult for the manifold Wishart VB algorithm that only uses the Euclidean to converge. As lies on the manifold of symmetric and positive definite matrices, the retraction and vector transport in (5.5) and (5.6) can be used. To update , it is recommended to use some adaptive learning method such as ADAM or AdaDelta, or an approximate natural gradient. If we set the correlation between and to be zero, then the natural gradient of the lower bound with respect to is approximated by

| (5.8) |

where .

A numerical example

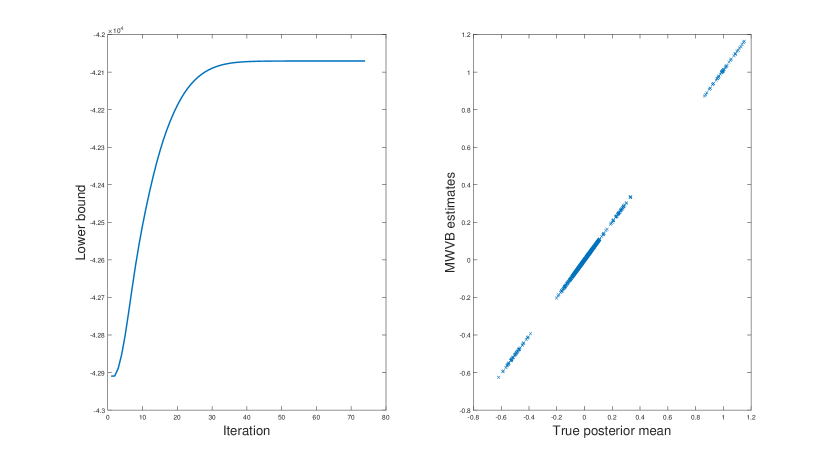

Data of size is generated from , where the elements of the true covariance matrix are . An inverse-Wishart() prior is used for with and . It is easy to see that the posterior distribution of is inverse-Wishart with the degree of freedom and scale matrix . We run the manifold Wishart VB algorithm with the inital value and , where is the sample covariance matrix of the .

In the first simulation, we consider and . The estimation result is summarized in Table 1. We consider the second simulation with and . The lower bound and a plot of the true posterior means of the v.s. their VB estimates are shown in Figure 5. These results show that the manifold Wishart VB algorithm appears to work effectively and efficiently in this example.

| True | VB | True | VB | True | VB | |||

|---|---|---|---|---|---|---|---|---|

| 0.89 (0.03) | 0.91 (0.04) | 0.39 (0.02) | 0.39 (0.02) | |||||

| 0.25 (0.02) | 0.26 (0.02) | 0.83 (0.03) | 0.84 (0.03) | |||||

| 0.29 (0.02) | 0.30 (0.02) | |||||||

| 0.93 (0.04) | 0.94 (0.04) | 0.35 (0.02) | 0.35 (0.02) | |||||

| 1.18 (0.06) | 1.19 (0.07) | 0.96 (0.04) | 0.97 (0.04) |

6 Conclusion

We proposed a manifold-based Variational Bayes algorithm that takes into account both information geometry and geometric structure of the constraint parameter space. The algorithm is provably convergent for the case when the objective function either non-convex or strongly retraction-convex. Our numerical experiments demonstrate that the proposed algorithm converges quickly, is stable and compares favourably to the existing VB methods. An interesting research direction is to develop a Manifold VB method for the Sylvester normalizing flows of Berg et al., (2018). We leave it as an interesting project for future research.

Acknowledgment

Tran would like to thank Prof. Pierre-Antoine Absil for useful discussions, and Nghia Nguyen for his help with the SMC implementation.

Appendix

Proof of Lemma 3.1.

Proof of Lemma 3.2.

Much of our proof is taken from Tagare, (2011). The idea of the proof is that we want to find a vector in that represents the action of the differential via the natural gradient . Let such that its columns together with the columns of form an orthonormal basis for . As is an orthogonal matrix, for any , there exists a such that . Write with the -matrix formed by the first rows of , the matrix formed by the last rows of . That is, any matrix can be written as

If , then implies that . So is a subset of the set

It’s easy to check that this set is also a subset of . We arrive at an alternative representation of the tangent space

| (6.2) |

We want to find a vector in that represents the action of the differential on , with characterized by ; i.e. find , such that

| (6.3) |

As the gradient , it can be written as . Based on the natural gradient ,

| (6.4) |

where we have used the fact that with , and that . We have that

| (6.5) |

Comparing (Proof of Lemma 3.2.) and (6.5) gives

As and ,

From (6.3), is the Riemannian gradient of . This completes the proof. ∎

Proof of Theorem 1.

(i) First, we consider the case is not assumed to be convex. Consider the update

| (6.6) | ||||

where , is a martingale difference. Since a.s, we have . This can be proved as follows. First for the rest of this proof, we use to denote vector/scalar with . Let be a parallel translation. From Lemma 6 Huang et al., 2015a , there exists a constant such that

| (6.7) |

which, together with implies

| (6.8) |

If we take norm of the second equation in (6.6), and using (6.8) we have

| (6.9) |

With and if are sufficiently small, using induction, we can show that . Indeed assuming , using (Proof of Theorem 1.), we have

Next, applying the Taylor expansion to the function and using the Lipschitz continuity of as well as the smoothness of in , there exists a constant such that

| (6.10) |

From (6.6), squaring both sides of the second equation we obtain

| (6.11) | ||||

where

From (6.8), with small enough so that , we have

Consider the second term without the constant in (6.11), we have

Recall that is an isometry, see, for example Absil et al., (2009). As a result we have

In view of the fundamental theorem of calculus (see (Huang et al., 2015a, , Lemma 8)), we have for some constant . Then, for , we have

| (6.12) | ||||

and

| (6.13) | ||||

For (II), since is a.s bounded by , we derive from (6.8) that

| (6.14) |

| (6.16) |

where . Next, using the second equation in (6.6) and (6.15), we have

| (6.17) | ||||

Multiplying (6.16), (6.17) with (to be chosen later) and respectively and then adding to (6.10) we have

| (6.18) | ||||

Note that,

(In the second inequality above, we have used the fact that with ). Plugging back to (6.18), we obtain

| (6.19) | ||||

Now select and let satisfy

taking the expectation of both sides of (6.19), we have

| (6.20) | ||||

Take the sum, we have

Then

Hence

If we choose , then

(ii) Now we assume that is strongly retraction convex with

| (6.21) |

for some (see Remark 4.1). Let when is small. Rewrite (6.17)

| (6.22) | ||||

Multiplying (6.16), (6.22) with (to be chosen later) and respectively and then adding to (6.10) we have

We deduce from (6.21) that

| (6.25) | ||||

On the other hand due to (6.12) we have

| (6.26) | ||||

Adding (6.24) and (Proof of Theorem 1.) and using (Proof of Theorem 1.) we have for

that

| (6.27) | ||||

Since is strongly retraction-convex, there exists such that . As a result, if then we have from Cauchy’s inequality that

Let and be such that

and

we have

As a result, recall the definition of , we have

where .

With , we have

When is large then

Thus for ,

we have

∎

References

- Absil et al., (2009) Absil, P.-A., Mahony, R., and Sepulchre, R. (2009). Optimization algorithms on matrix manifolds. Princeton University Press.

- Amari, (1998) Amari, S. (1998). Natural gradient works efficiently in learning. Neural computation, 10(2):251–276.

- Bécigneul and Ganea, (2018) Bécigneul, G. and Ganea, O.-E. (2018). Riemannian adaptive optimization methods. arXiv preprint arXiv:1810.00760.

- Berg et al., (2018) Berg, R. v. d., Hasenclever, L., Tomczak, J. M., and Welling, M. (2018). Sylvester normalizing flows for variational inference. arXiv preprint arXiv:1803.05649.

- Bollerslev, (1986) Bollerslev, T. (1986). Generalized autoregressive conditional heteroskedasticity. Journal of Econometrics, 31(3):307 – 327.

- Bonnabel, (2013) Bonnabel, S. (2013). Stochastic gradient descent on Riemannian manifolds. IEEE Transactions on Automatic Control, 58(9):2217–2229.

- Boumal et al., (2014) Boumal, N., Mishra, B., Absil, P.-A., and Sepulchre, R. (2014). Manopt, a Matlab toolbox for optimization on manifolds. Journal of Machine Learning Research, 15:1455–1459.

- Edelman et al., (1998) Edelman, A., Arias, T., and Smith, A. (1998). The geometry of algorithms with orthogonality constraints. SIAM J. Matrix Anal. Appl., 20(2):303–353.

- Hoffman et al., (2013) Hoffman, M. D., Blei, D. M., Wang, C., and Paisley, J. (2013). Stochastic variational inference. Journal of Machine Learning Research, 14:1303–1347.

- (10) Huang, W., Absil, P.-A., and Gallivan, K. A. (2015a). A Riemannian symmetric rank-one trust-region method. Mathematical Programming, 150(2):179–216.

- (11) Huang, W., Gallivan, K. A., and Absil, P.-A. (2015b). A Broyden class of quasi-Newton methods for Riemannian optimization. SIAM Journal on Optimization, 25(3):1660–1685.

- Jordan et al., (1999) Jordan, M. I., Ghahramani, Z., Jaakkola, T. S., and Saul, L. K. (1999). An introduction to variational methods for graphical models. Machine learning, 37(2):183–233.

- Kasai et al., (2019) Kasai, H., Jawanpuria, P., and Mishra, B. (2019). Adaptive stochastic gradient algorithms on riemannian manifolds. arXiv preprint arXiv:1902.01144.

- Khan and Lin, (2017) Khan, M. E. and Lin, W. (2017). Conjugate-computation variational inference: Converting variational inference in non-conjugate models to inferences in conjugate models. In Proceedings of the 20th International Conference on Artificial Intelligence and Statistics (AISTATS).

- Kingma and Welling, (2013) Kingma, D. P. and Welling, M. (2013). Auto-encoding variational bayes. arXiv preprint arXiv:1312.6114.

- Kobayashi and Nomizu, (1969) Kobayashi, S. and Nomizu, K. (1969). Foundations of Differential Geometry, Vols. 1 and 2. Wiley, New York.

- Longford, (1987) Longford, N. T. (1987). A fast scoring algorithm for maximum likelihood estimation in unbalanced mixed models with nested random effects. Biometrika, 74(4):817–827.

- Manton, (2002) Manton, J. H. (2002). Optimization algorithms exploiting unitary constraints. IEEE Transactions on Signal Processing, 50(3):635–650.

- Mardia and Marshall, (1984) Mardia, K. V. and Marshall, R. J. (1984). Maximum likelihood estimation of models for residual covariance in spatial regression. Biometrika, 71(1):135–146.

- Martens, (2020) Martens, J. (2020). New insights and perspectives on the natural gradient method. Journal of Machine Learning Research, 21(146):1–76.

- (21) Ong, V. M., Nott, D. J., Tran, M.-N., Sisson, S. A., and Drovandi, C. C. (2018a). Variational Bayes with synthetic likelihood. Statistics and Computing, 28(4):971–988.

- (22) Ong, V. M.-H., Nott, D. J., and Smith, M. S. (2018b). Gaussian variational approximation with factor covariance structure. Journal of Computational and Graphical Statistics, 27(3):465–478.

- Rao, (1945) Rao, C. R. (1945). Information and accuracy attainable in the estimation of statistical parameters. Bull. Calcutta. Math. Soc, 37:81–91.

- Roy and Harandi, (2017) Roy, S. K. and Harandi, M. (2017). Constrained stochastic gradient descent: The good practice. In In Proceedings of the International Conference on Digital Image Computing: Techniques and Applications (DICTA).

- Sato and Aihara, (2019) Sato, H. and Aihara, K. (2019). Cholesky QR-based retraction on the generalized Stiefel manifold. Computational Optimization and Applications, 72(2):293–308.

- Sato, (2001) Sato, M. (2001). Online model selection based on the variational bayes. Neural Computation, 13(7):1649–1681.

- Tagare, (2011) Tagare, H. D. (2011). Notes on optimization on Stiefel manifolds. http://noodle.med.yale.edu/ hdtag/notes/steifel_notes.pdf.

- Tran et al., (2019) Tran, M.-N., Nguyen, N., Nott, D., and Kohn, R. (2019). Bayesian deep net GLM and GLMM. Journal of Computational and Graphical Statistics.

- Tran et al., (2021) Tran, M.-N., Nguyen, T.-N., and Dao, V.-H. (2021). A practical tutorial on Variational Bayes. arXiv:2103.01327.

- Tran et al., (2017) Tran, M.-N., Nott, D. J., and Kohn, R. (2017). Variational Bayes with intractable likelihood. Journal of Computational and Graphical Statistics, 26(4):873–882.

- Tran et al., (2014) Tran, M.-N., Pitt, M. K., and Kohn, R. (2014). Annealed important sampling for models with latent variables. http://arxiv.org/abs/1402.6035.

- Tu, (2011) Tu, L. W. (2011). An introduction to manifolds. Springer New York.

- Waterhouse et al., (1996) Waterhouse, S., MacKay, D., and Robinson, T. (1996). Bayesian methods for mixtures of experts. In Touretzky, M. C. M. D. S. and Hasselmo, M. E., editors, Advances in Neural Information Processing Systems, pages 351–357. MIT Press.

- Zhou et al., (2020) Zhou, B., Gao, J., Tran, M.-N., and Gerlach, R. (2020). Manifold optimisation assisted Gaussian variational approximation. Journal of Computational and Graphical Statistics (to appear).