AlphaStock: A Buying-Winners-and-Selling-Losers Investment Strategy using Interpretable Deep Reinforcement Attention Networks

Abstract.

Recent years have witnessed the successful marriage of finance innovations and AI techniques in various finance applications including quantitative trading (QT). Despite great research efforts devoted to leveraging deep learning (DL) methods for building better QT strategies, existing studies still face serious challenges especially from the side of finance, such as the balance of risk and return, the resistance to extreme loss, and the interpretability of strategies, which limit the application of DL-based strategies in real-life financial markets. In this work, we propose AlphaStock, a novel reinforcement learning (RL) based investment strategy enhanced by interpretable deep attention networks, to address the above challenges. Our main contributions are summarized as follows: ) We integrate deep attention networks with a Sharpe ratio-oriented reinforcement learning framework to achieve a risk-return balanced investment strategy; ) We suggest modeling interrelationships among assets to avoid selection bias and develop a cross-asset attention mechanism; ) To our best knowledge, this work is among the first to offer an interpretable investment strategy using deep reinforcement learning models. The experiments on long-periodic U.S. and Chinese markets demonstrate the effectiveness and robustness of AlphaStock over diverse market states. It turns out that AlphaStock tends to select the stocks as winners with high long-term growth, low volatility, high intrinsic value, and being undervalued recently.

ACM Reference Format:

Jingyuan Wang, Yang Zhang, Ke Tang, Junjie Wu, Zhang Xiong. 2019. AlphaStock: A Buying-Winners-and-Selling-Losers Investment Strategy using Interpretable Deep Reinforcement Attention Networks In The 25th ACM SIGKDD Conference on Knowledge Discovery Data Mining (KDD ’19), August 4–8, 2019, Anchorage, AK, USA. ACM, NY, NY, USA, 9 pages.

https://doi.org/10.1145/3292500.3330647

1. Introduction

Given the ability in handling large scales of transactions and offering rational decision-makings, quantitative trading (QT) strategies have long been adopted in financial institutions and hedge funds and have achieved spectacular successes.Traditional QT strategies are usually based on specific financial logics. For instance, the momentum phenomenon found by Jegadeesh and Titman in the stock market (Jegadeesh and Titman, 1993) was used to build momentum strategies. The mean reversion (Poterba and Summers, 1988) proposed by Poterba and Summers believes that asset price tends to move to the average over time, so the bias of asset prices to their means could be used to select investment targets. The multi-factor strategy (Fama and French, 1996) uses factor-based asset valuations to select assets. Most of these traditional QT strategies, though equipped with solid financial theories, can only leverage some specific characteristic of financial markets, and therefore might be vulnerable to complex markets with diverse states.

In recent years, deep learning (DL) emerges as an effective way to extract multi-aspect characteristics from complex financial signals. Many supervised deep neural networks are proposed in the literature to predict asset prices using various factors, such as frequency of prices (Hu and Qi, 2017), economic news (Hu et al., 2018), social media (Xu and Cohen, 2018), and financial events (Ding et al., 2015, 2016). Deep neural networks are also adopted in reinforcement learning (RL) frameworks to enhance traditional shallow investment strategies (Jin and El-Saawy, 2016; Deng et al., 2017; Ding et al., 2018). Despite the rich studies above, applying DL to real-life financial markets still faces several challenges:

Challenge 1: Balancing return and risk. Most existing supervised deep learning models in finance focus on price prediction without risk awareness, which is not in line with fundamental investment principles and may lead to suboptimal performance (Fischer, 2018). While some RL-based strategies (Fischer, 2018; Moody et al., 1998) have considered this problem, how to adopt state-of-the-art DL approaches into risk-return-balanced RL frameworks, is yet not well studied.

Challenge 2: Modeling interrelationships among assets. Many financial tools in the market can be used to derive risk-aware profits from the interrelationship among assets, such as hedging, arbitrage, and the BWSL strategy used in this work. However, existing DL/RL-based investment strategies paid little attention to this important information.

Challenge 3: Interpreting investment strategies. There is a longstanding voice arguing that DL-based systems are “unexplainable black boxes” and therefore cannot be used in crucial applications like medicine, investment and military (Guidotti et al., 2018). RL-based strategies with deep structures make it even worse. How to extract interpretable rules from DL-enabled strategies remains an open problem.

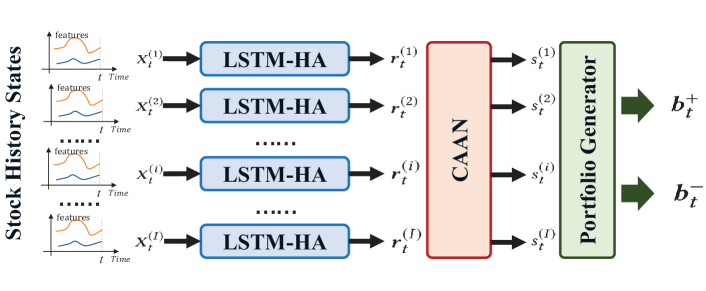

In this paper, we propose AlphaStock, a novel reinforcement learning based strategy using deep attention networks, to overcome the above challenges. AlphaStock is essentially a buying winners and selling losers (BWSL) strategy for stock assets. It consists of three components. The first is a Long Short-Term Memory with History state Attention (LSTM-HA) network, which is used to extract asset representations from multiple time series. The second component is a Cross-Asset Attention Network (CAAN), which can fully model the interrelationships among assets as well as the asset price rising prior. The third is a portfolio generator, which gives the investment proportion of each asset according to the output winner scores of the attention networks. We use a RL framework to optimize our model towards a return-risk-balanced objective, i.e., maximizing the Sharpe Ratio. In this way, the merit of representation learning via deep attention models and the merit of risk-return balance via Sharpe ratio targeted reinforcement learning are integrated naturally. Moreover, to gain interpretability for AlphaStock, we propose a sensitivity analysis method to unveil how our model selects an asset to invest according to its multi-aspect features.

Extensive experiments on long-periodic U.S. stock markets demonstrate that our AlphaStock strategy outperforms some state-of-the-art competitors in terms of a variety of evaluation measures. In particular, AlphaStock shows excellent adaptability to diverse market states (enabled by RL and Sharpe ratio) and exceptional ability for extreme loss control (enabled by CAAN). Extended experiments on Chinese stock markets further confirm the superiority of AlphaStock and its robustness. Interestingly, the interpretation analysis results reveal that AlphaStock selects assets by following a principle as “selecting the stocks as winners with high long-term growth, low volatility, high intrinsic value, and being undervalued recently”.

2. Preliminaries

In this section, we first introduce the financial concepts used throughout this paper, and then formally define our problem.

2.1. Basic Financial Concepts

Definition 1 (Holding Period).

A holding period is a minimum time unit to invest an asset. We divide the time axis as sequential holding periods with fixed length, such as one day or one month. We call the starting time of the -th holding period as the time .

Definition 2 (Sequential Investment).

A sequential investment is a sequence of holding periods. For the -th holding period, a strategy uses original capital to invest in assets at time , and gets profits (could be negative) at time . The capitals plus profits of the -th holding period are used as the original capitals of the -th holding period.

Definition 3 (Asset Price).

The price of an asset is defined as a time series , where denotes the price of asset at time .

In this work, we use a stock as an asset to describe our model, which could be extended to other types of assets by taking asset specificities and transaction rules into consideration.

Definition 4 (Long Position).

The long position is the trading operation that buys an asset at time first and then sells it at . The profit of a long position during the period from to for asset is , where is the buying volume of asset .

In the long position, traders expect an asset will rise in price, so they buy the asset first and wait for the price rise to earn profits.

Definition 5 (Short Position).

A short position is the trading operation that sells an asset at first and then buys it back at . The profit of a short position during the period from to for asset is , where is the selling volume of asset .

Short position is a reverse operation of the long position. Traders’ expectation in short position is that the price will drop, so they sell at a price higher than the price at which they buy it back later. In the stock market, a short position trader borrows stocks from a broker and sells them at . At , the trader buys the sold stocks back and returns them to the broker.

Definition 6 (Portfolio).

Given an asset pool with assets, a portfolio is defined as a vector , where is the proportion of the investment on asset , with .

Assume we have a collection of portfolios . The investment on portfolio is , with when taking a long position on , and when taking a short position. We then have the following important definition.

Definition 7 (Zero-investment Portfolio).

A zero-investment portfolio is a collection of portfolios that has a net total investment of zero when the portfolios are assembled. That is, for a zero-investment portfolio containing portfolios, the total investment .

For instance, an investor may borrow $1,000 worth of stocks in one set of companies and sell them as a short position, and then use the proceeds of short selling to purchase $1,000 stocks in another set of companies as a long position. The assemble of the long and short positions is a zero-investment portfolio. Note that while the name is “zero-investment”, there still exists a budget constraint to limit the overall worth of stocks that can be borrowed from the broker. Also, we ignore real-world transaction costs for simplicity.

2.2. The BWSL Strategy

In this paper, we adopt the buy-winners-and-sell-losers (BWSL) strategy for stock trading (Jegadeesh and Titman, 1993), the key of which is to buy the assets with high price rising rate (winners) and sell those with low price rising rate (losers). We execute the BWSL strategy as a zero-investment portfolio consisting of two portfolios: a long portfolio for buying winners and a short portfolio for selling losers. Given a sequential investment with periods, we denote the short portfolio for the -th period as and the long portfolio as , .

At time , given a budget constraint , we borrow the “loser” stocks from brokers according to the investment proportion in . The volume of stock that we can borrow is

| (1) |

where is the proportion of stock in . Next, we sell the “loser” stocks we borrowed and get the money . After that, we use to buy the “winner” stocks according to the long portfolio . The volume of stock that we can buy at time is

| (2) |

The money we used to buy winner stocks is the proceeds of short selling, so the net investment on the portfolio is zero.

At the end of the -th holding period, we sell stocks in the long portfolio. The money we can get is the proceeds of selling stocks using new prices at for all stocks, i.e.,

| (3) |

Next, we buy the stocks in the short portfolio back and return them to the broker. The money we spend on buying the short stocks is

| (4) |

The ensemble profit earned by the long and short portfolios is . Let denote the price rising rate of stock in the -th holding period. Then, the rate of return of the ensemble portfolio is calculated as

| (5) |

Insight I. As shown in Eq. (5), a positive profit, i.e., , means the average price rising rate of stocks in the long portfolio is higher than that in the short portfolio, i.e.,

| (6) |

A profitable BWSL strategy must ensure the stocks in the portfolio have a higher average price rising rate than the stocks in . That is to say, even the prices of all stocks in the market are falling, as long as we can ensure the price falling of stocks in is slower than that in , we can still get profits. On the contrary, even the prices of all stocks are rising, if the rising of stocks in is faster than that in , our strategy still lose money. This characteristic implies that the absolute price rising or falling of stocks is not the main concern of our strategy; rather, the relative price relations among stocks are much more important. As a consequence, we must design a mechanism to describe the interrelationships of stock prices in our model for the BWSL strategy.

2.3. Optimization Objective

In order to ensure that our strategy considers both return and risk of an investment, we adopt the Sharpe ratio, a risk-adjusted return developed by the Nobel laureate William F. Sharpe (Sharpe, 1994) in 1994, to measure the performance of our strategy.

Definition 8 (Sharpe Ratio).

The Sharpe ratio is the average return in excess of the risk-free return per unit of volatility. Given a sequential investment that contains holding periods, its Sharpe ratio is calculated as

| (7) |

where is the average rate of return per period for the investment, is the volatility that is used to measure risk of the investment, is a risk-free return rate, such as the return rate of bank.

Given a sequential investment with holding periods, is calculated as

| (8) |

where is a transaction cost in the -th period. The volatility in Eq. (7) is defined as

| (9) |

where is the average of .

For a -period investment, the optimization objective of our strategy is to generate the long and short portfolio sequences and that can maximize the Sharpe ratio of the investment as

| (10) |

Insight II. The Sharpe ratio evaluates the performance of a strategy from both profit and risk perspectives. This profit-risk balance characteristic requires our model not only focuses on maximizing return rate for each period, but also considers the long-term volatility of across all periods in an investment. In other words, designing a far-sighted steady investment strategy is more valuable than a short-sighted strategy with short-term high profits.

3. The AlphaStock Model

In this section, we propose a reinforcement learning (RL) based model called AlphaStock to implement a BWSL strategy with the Sharpe ratio defined in Eq. (7) as the optimization objective. As shown in Fig. 1, AlphaStock contains three components. The first component is a LSTM with History state Attention network (LSTM-HA). For each stock , we use the LSTM-HA model to extract a stock representation from its history states . The second component is a Cross-Asset Attention Network (CAAN) to describe interrelationships among the stocks. The CAAN takes as input the representations () of all stocks, and estimates a winner score for every stock. The is a score to indicate the degree of stock belonging to a winner. The third component is a portfolio generator, which calculates the investment proportions in and according to the scores () of all stocks. We use reinforcement learning to end-to-end optimize the three components as a whole, where the Sharpe ratio of a sequential investment is maximized through a far-sighted way.

3.1. Raw Stock Features

The stock features used in our model contains two categories. The first category is the trading features, which describes the trading information of a stock. At time , the trading features include:

Price Rising Rate (PR): The price rising rate of a stock during the last holding period. It is defined as for stock .

Fine-grained Volatility (VOL): A holding period can be further divided into many sub-periods. We set one month as a holding period in our experiment, thus a sub-period can be a trading day. VOL is defined as the standard deviation of the prices of all sub-periods from to .

Trade Volume (TV): The total quantity of stocks traded from to . It reflects the market activity of a stock.

The second category is the company features, which describe the financial condition of the company that issues a stock. At time , the company features include:

Market Capitalization (MC): For stock , it is defined as the product of the price and the outstanding shares of the stock.

Price-earnings Ratio (PE): It is the ratio of the market capitalization of a company to its annual earnings.

Book-to-market Ratio (BM): It is the ratio of the book value of a company to its market value.

Dividend (Div): It is the reward from company’s earnings to stock holders during the -th holding period.

Since the values of these features are not in the same scale, we standardize them into Z-scores.

3.2. Stock Representations Extraction

The performance of a stock has close relations with its history states. In the AlphaStock model, we propose a Long Short-Term Memory with History state Attention (LSTM-HA) model to learn the representation of a stock from its history features.

The sequential representation. In the LSTM-HA network, we use the vector to denote the history state of a stock at time , which consists of the stock features given in Section 3.1. We name the last historical holding periods at time , i.e., the period from time to time , as a look-back window of . The history states of a stock in the look-back window are denoted as a sequence 111We also use to denote the matrix , the two definitions are interchangeable., where . Our model uses a Long Short-Term Memory (LSTM) network (Hochreiter and Schmidhuber, 1997) to recursively encode into a vector as

| (11) |

where is the hidden state encoded by LSTM at step . The at the last step is used as a representation of the stock. It contains the sequential dependence among elements in .

The history state attention. The can fully exploit the sequential dependence of elements in , but the global and long-range dependence among are not effectively modeled. Therefore, we adopt a history state attention to enhance using all middle hidden states . Specifically, following the standard attention (Sutskever et al., 2014), the history state attention enhanced representation, denoted as , is calculated as

| (12) |

where is an attention function defined as

| (13) | |||||

Here, , and are the parameters to learn.

For the -th stock at time , the history state attention enhanced representation is denoted as . It contains both the sequential and global dependences of stock ’s history states from time to time . In our model, the representation vectors for all stocks are extracted by the same LSTM-HA network. The parameters , , and those of the LSTM network in Eq. (11) are shared by all stocks. In this way, the representations extracted by LSTM-HA are relatively stable and general for all stocks rather than for a particular one.

Remark. A major advantage of LSTM-HA is that it can learn both the sequential and global dependences from stock history states. Compared with the existing studies that only use a recurrent neural network to extract the sequential dependence in history states (Moody et al., 1998; Deng et al., 2017) or directly stack history states as an input vector of MLP (Jin and El-Saawy, 2016) to learn the global dependence, our model describes stock histories more comprehensively. It is worth mentioning that LSTM-HA is also an open framework. The representations learned from other types of information sources, such as news, events and social media (Hu et al., 2018; Ding et al., 2015; Xu and Cohen, 2018), could also be concatenated or attended with .

3.3. Winners and Losers Selection

In the traditional RL-based strategy models, the investment portfolio is often directly generated from the stock representations through a softmax normalization (Jin and El-Saawy, 2016; Deng et al., 2017; Ding et al., 2018). The drawback of this type of methods is that it does not fully exploit the interrelationships among stocks, which however is very important for the BWSL strategy as analyzed in Insight I of Section 2.2. In light of this, we propose a Cross-Asset Attention Network (CAAN) to describe the interrelationships among stocks.

The basic CAAN model. The CAAN model adopts the self-attention mechanism proposed by Ref. (Vaswani et al., 2017) to model the interrelationships among stocks. Specifically, given the stock representation (we omit time without loss of generality), we calculate a query vector , a key vector and a value vector for stock as

| (14) |

where , and are the parameters to learn. The interrelationship of stock to stock is modeled as using the of the stock to query the key of stock , i.e.,

| (15) |

where is a re-scale parameter setting following Ref. (Vaswani et al., 2017). Then, we use the normalized interrelationships as weights to sum the values of other stocks into an attenuation score:

| (16) |

where the self-attention function is a softmax normalized interrelationships of , i.e.,

| (17) |

We use a fully connected layer to transform the attention vector into a winner score as

| (18) |

where and are the connection weights and the bias to learn. The winner score indicates the degree of stock being a winner in the -th holding period. A stock with a higher score is more likely to be a winner.

Incorporating price rising rank prior. In the basic CAAN, the interrelationships modeled by Eq. (15) are directly learned from data. In fact, we could use priori knowledge to help our model to learn the stock interrelationships. We use to denote the rank of price rising rate of stock in the last holding period (from to ). Inspired by the method for modeling positional information from the NLP field, we use the relative positions of stocks in the coordinate axis of as a priori knowledge of the stock interrelationships. Specifically, given two stocks and , we calculate their discrete relative distance in the coordinate axis of as

| (19) |

where is a preset quantization coefficient. We use a lookup matrix to represent each discretized value of . Using the as the index, the corresponding column vector is an embedding vector of the relative distance .

For a pair of stocks and , we calculate a priori relation coefficient using as

| (20) |

where is a learnable parameter. The relationship between and estimated by Eq. (15) is rewritten as

| (21) |

In this way, the relative positions of stocks in price rising rate rank are introduced as a weight to enhance or weaken the attention coefficient. The stocks have similar history price rising rates will have a stronger interrelationship in the attention and then have similar winner scores.

3.4. Portfolios Generator

Given the winner scores of stocks, our AlphaStock model generally buys the stocks with high winner scores and sells those with low winner scores. Specifically, we first sort the stocks in descending order by their winner scores and obtain the sequence number for each stock . Let denote the preset size of portfolio and . If , stock will enter the portfolio , with the investment proportion calculated as

| (22) |

If , stock will enter with a proportion

| (23) |

The rest stocks are unselected for the lack of clear buy/sell signals. For simplicity, we can use one vector to record all the information of the two portfolios. That is, we form the vector of length , with if , or if , or 0 otherwise, . In what follows, we use and interchangeably as the return of our AlphaStock model for clarity.

3.5. Optimization via Reinforcement Learning

We frame the AlphaStock strategy into a RL game with discrete agent actions to optimize the model parameters, where a -period investment is modeled as a state-action-reward trajectory of a RL agent, i.e., . The is the history market state observed at , which is expressed as . The is an -dimensional binary vector, of which the element when the agent invests stock at , and otherwise222In the RL game, the actions of an agent are discrete states with the probability indicating whether to invest stock . In the real investment, we allocate capitals to stocks according the continuous proportion . This approximation is for the sake of problem solving.. According to , the agent has a probability to invest stock , which is determined by AlphaStock as

| (24) |

where is part of AlphaStock that generates , denotes the model parameters, and is to ensure . Let denote the Sharpe ratio of , then is the contribution of to , with .

For all possible , the average reward of the RL agent is

| (25) |

where is the probability of generating from . Then, the objective of the RL model optimization is to find the optimal parameters .

We use the gradient ascent approach to iteratively optimize at round as , where is a learning rate. Given a training dataset that contains trajectories , can be approximately calculated as (Sutton and Barto, 2018)

| (26) | ||||

The gradient , which is calculated by the Back Propagation algorithm.

In order to ensure the proposed model can beat the market, we introduce the threshold method (Sutton and Barto, 2018) into our reinforcement learning. Then the gradient in Eq. (26) is rewritten as

| (27) |

where the threshold is set as the Sharpe ratio of the overall market. In this way, the gradient ascent only encourages the parameters that can outperform the market.

4. Model Interpretation

In the AlphaStock model, the LSTM-HA and CAAN networks cast the raw stock features as winner scores. The final investment portfolios are directly generated from the winner scores. A natural follow-up question is: what kind of stocks would be selected as winners by AlphaStock? To answer this question, we propose a sensitivity analysis method (Adebayo et al., 2018; Wang et al., 2018, 2016) to interpret how the history features of a stock influence its winner score in our model.

We use to express the function of history features of a stock to its winner score . In our model, is a combined network of LSTM-HA and CAAN. We use to denote an element of which is the value of one feature (defined in Section 3.1) at a particular time period of the look-back window, e.g., the price rising rate of a stock at the time of three months ago.

Given the history state of a stock, the influence of to its winner score , i.e., the sensitivity of to , is expressed as

| (28) |

where denotes the elements of except .

For all possible stock states in a market, the average influence of the stock state feature to the winner score is

| (29) |

where is the probability density function of , and is an integral over all possible value of . According to the Large Number Law, given a dataset that contains history states of stocks in holding periods, the is approximated as

| (30) |

where is the history state of the -th stock at the -th holding period, and denotes the history states of other stocks that are concurrent with the history state of -th stock.

We use to measure the overall influence of a stock feature to the winner score. A positive value of indicates that our model tends to take a stock as a winner when is large, and vice versa. For example, in the experiment to follow, we obtain for the fine-grained volatility feature, which means that our model trends to select low volatility stocks as winners.

5. Experiment

In this section, we empirically evaluate our AlphaStock model by the data in the U.S. markets. The data in the Chinese stock markets are also used for robustness check.

5.1. Data and Experimental Setup

The data of U.S. stock market used in our experiments are obtained from Wharton Research Data Services (WRDS) 333https://wrds-web.wharton.upenn.edu/wrds/. The time range of the data is from Jan. 1970 to Dec. 2016. This long time range covers several well-known market events, such as the dot-com bubble from 1995 to 2000 and the subprime mortgage crisis from 2007 to 2009, which enables the evaluation over diverse market states. The stocks are from four markets: NYSE, NYSE American, NASDAQ, and NYSE Arca. The number of valid stocks is more than 1000 per year. We use the data from Jan. 1970 to Jan. 1990 as the training and validation set, and the rest as the test set.

In the experiment, the holding period is set to one month, and the number of holding periods in an investment is set to 12, i.e., the Sharpe ratio reward is calculated every 12 months for RL. The look-back window size is set to 12, i.e., we look back on the 12-month history states of stocks. The size of the portfolios is set as 1/4 of number of all stocks.

5.2. Baseline Methods

AlphaStock is compared with a number of baselines including:

Market: the uniform Buy-And-Hold strategy (Huang et al., 2016);

Cross Sectional Momentum (CSM) (Jegadeesh and Titman, 2002) and Time Series Momentum (TSM) (Moskowitz et al., 2012): two classic momentum strategies;

Robust Median Reversion (RMR): a newly reported reversion strategy (Huang et al., 2016);

Fuzzy Deep Direct Reinforcement (FDDR): a newly reported RL-based BWSL strategy (Deng et al., 2017);

AlphaStock-NC (AS-NC): the AlphaStock model without the CAAN, where the outputs of LSTM-HA are directly used as the inputs of the portfolio generator.

AlphaStock-NP (AS-NP): the AlphaStock model without price rising rank prior, where we use the basic CAAN in our model.

The baselines TSM/CSM/RMR represent the traditional financial strategies. TSM and CSM are based on the momentum logic and RMR is based on the reversion logic. FDDR represents the state-of-the-art RL-based BWSL strategy. AS-NC and AS-NP are used as a contrast to verify the effectiveness of the CAAN and price rising rank prior. The Market is used to indicate states of the market.

5.3. Evaluation Measures

The most standard evaluation measure for investment strategies is Cumulative Wealth, which is defined as

| (31) |

where is the rate of return defined in Eq. (5) and the transaction cost is set to 0.1% in our experiments according to Ref. (Deng et al., 2017).

The preferences of different investors are varied. Therefore, we also use some other evaluation measures including:

1) Annualized Percentage Rate (APR) is an annualized average of return rate. It is defined as , where is the number of holding periods in a year.

2) Annualized Volatility (AVOL) is an annualized average of volatility. It is defined as and is used to measure the average risk of a strategy during an unit time period.

3) Annualized Sharpe Ratio (ASR) is the risk-adjusted annualized return based on APR and AVOL. The formalized definition of ASR is .

4) Maximum DrawDown (MDD) is the maximum loss from a peak to a trough of a portfolio, before a new peak is attained. It is the other way to measure the investment risk. The formalized definition of MDD is

| (32) |

5) Calmar Ratio (CR) is the risk-adjusted APR based on Maximum DrawDown. It is calculated as .

6) Downside Deviation Ratio (DDR) measures the downside risk of a strategy as the average of returns when it falls below a minimum acceptable return (MAR). It is the risk-adjusted APR based on Downside Deviation. The formalized definition of DDR is given as

| (33) |

In our experiment, the MAR is set to zero.

5.4. Performance in U.S. Markets

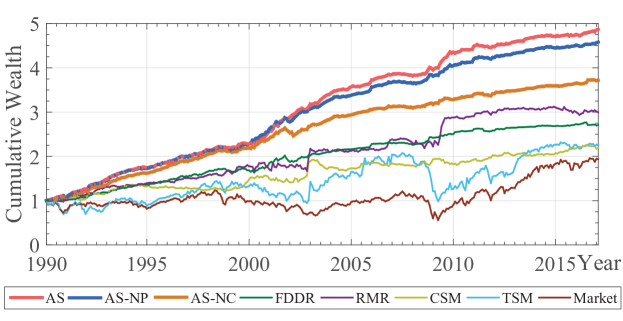

Fig. 2 is a cumulative wealth comparison of AlphaStock and the baselines. In general, the performance of AlphaStock (AS) is much better than other baselines, which verifies the effectiveness of our model. Some interesting observations are highlighted as follows:

1) The performance of AlphaStock is better than AlphaStock-NP and the performance of AlphaStock-NP is better than AlphaStock-NC, which indicates that the stock rank priors and interrelationships modeled by CAAN are very helpful for the BWSL strategy.

2) The FDDR is also a kind of deep RL investment strategy, which extracts the fuzzy representations of stocks using a recurrent deep neural network. In our experiment, the performance of AlphaStock-NC is better than FDDR, indicating the advantage of our LSTM-HA network in the stock representation learning.

3) The TSM strategy performs well in the bull market but very poorly in the bear market (the financial crisis in 2003 and 2008), while the RMR has an opposite performance. This implies the traditional financial strategies can only adapt to a certain type of market state without an effective forward-looking mechanism. This defect is greatly addressed by the RL strategies, including AlphaStock and FDDR, which perform much stably across different market states.

| APR | AVOL | ASR | MDD | CR | DDR | |

| Market | 0.042 | 0.174 | 0.239 | 0.569 | 0.073 | 0.337 |

| TSM | 0.047 | 0.223 | 0.210 | 0.523 | 0.090 | 0.318 |

| CSM | 0.044 | 0.096 | 0.456 | 0.126 | 0.350 | 0.453 |

| RMR | 0.074 | 0.134 | 0.551 | 0.098 | 1.249 | 0.757 |

| FDDR | 0.063 | 0.056 | 1.141 | 0.070 | 0.900 | 2.028 |

| AS-NC | 0.101 | 0.052 | 1.929 | 0.068 | 1.492 | 1.685 |

| AS-NP | 0.133 | 0.065 | 2.054 | 0.033 | 3.990 | 4.618 |

| AS | 0.143 | 0.067 | 2.132 | 0.027 | 5.296 | 6.397 |

The performances evaluated by other measures are listed in Table 1. For the measures underlined (AVOL, MDD), the lower value indicates the better performance, while the situation is opposite for the other measures. As shown in Table 1, the performances of AlphaStock, AlphaStock-NP and AlphaStock-NC are better than other baselines with all measures, confirming the effectiveness and robustness of our strategy. The performances of AlphaStock, AlphaStock-NP and AlphaStock-NC are close in terms of ASR, which might be due to all of these models are optimized for maximizing the Sharpe ratio. The profits of AlphaStock and AlphaStock-NP measured by APR are higher than that of AlphaStock-NC, at the cost of a little bit higher volatility.

More interestingly, the performance of AlphaStock measured by MDD, CR and DDR is much better than that of AlphaStock-NP. The similar results could be observed by comparing MDD, CR and DDR of AlphaStock-NP and AlphaStock-NC. The three measures are used to indicate the extreme loss in an investment, i.e., the maximum draw down and the returns below the minimum acceptable threshold. The results suggest that the extreme loss control ability of the three models are AlphaStock AlphaStock-NP AlphaStock-NC, which highlights the contribution of the CAAN component and the price rising rank prior. Indeed, CAAN with price rising rank priors fully exploits the ranking relationship among stocks. This mechanism can protect our strategy from the error of “buying losers and selling winners”, and therefore can greatly avoid extreme losses in investments. In summary, AlphaStock is a very competitive strategy for investors with different types of preferences.

5.5. Performance in Chinese Markets

In order to further testify the robustness of our model, we run the back-test experiments of our model and baselines over the Chinese stock markets, which contains two exchanges: Shanghai Stock Exchange (SSE) and Shenzhen Stock Exchange (SZSE). The data are obtained from the WIND databese444http://www.wind.com.cn/en/Default.html. The stocks are the RMB priced ordinary shares (A-share) and the total number of stocks used for experiment is 1,131. The time range of our data is from Jun. 2005 to Dec. 2018, with the period from Jun. 2005 – Dec. 2011 used as the training/validation set and the rest as the test set. Since the Chinese markets cannot short sell, so we only use the portfolio in the experiment.

The experimental results are given in Table 2. From the table we can see that the performances of AlphaStock, AlphaStock-NP and AlphaStock-NC are better than that of other baselines again. This verifies the effectiveness of our model over the Chinese markets. By further comparing Table 2 with Table 1, it turns out that the risk of our model measured by AVOL and MDD in the Chinese markets is higher than that in the U.S. markets. This might be attributable to the market faultiness of emerging countries like China, with more speculative capital but less effective governance. The lack of short sell mechanism also contributes to the imbalance of market forces. The AVOL and MDD of the Market and other baselines in the Chinese markets are also higher than that in the U.S. markets. Compared with these baselines, the risk control ability of our model is still competitive. To sum up, the experimental results in Table 2 indicate the robustness of our model over emerging markets.

| APR | AVOL | ASR | MDD | CR | DDR | |

| Market | 0.037 | 0.260 | 0.141 | 0.595 | 0.062 | 0.135 |

| TSM | 0.078 | 0.420 | 0.186 | 0.533 | 0.147 | 0.225 |

| CSM | 0.023 | 0.392 | 0.058 | 0.633 | 0.036 | 0.064 |

| RMR | 0.079 | 0.279 | 0.282 | 0.423 | 0.186 | 0.289 |

| FDDR | 0.084 | 0.152 | 0.553 | 0.231 | 0.365 | 0.801 |

| AS-NC | 0.104 | 0.113 | 0.916 | 0.163 | 0.648 | 1.103 |

| AS-NP | 0.122 | 0.105 | 1.163 | 0.136 | 0.895 | 1.547 |

| AS | 0.125 | 0.103 | 1.220 | 0.135 | 0.296 | 1.704 |

5.6. Investment Strategies Interpretation

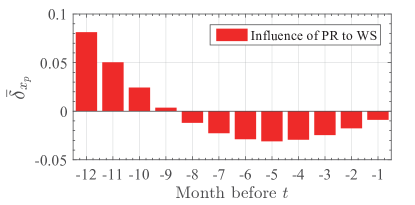

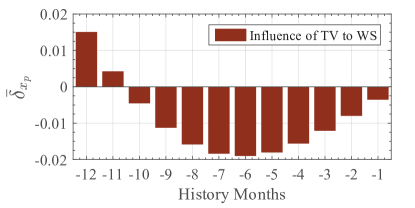

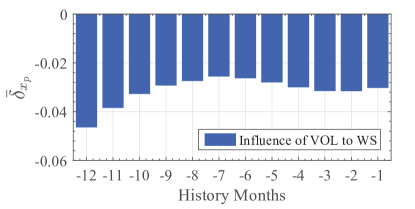

Here, we try to interpret the underlying investment strategies of AlphaStock, which is crucial for practitioners to better understanding this model. To this end, we use in Eq. (30) to measure the influence of the stock features defined in Section 3.1 to AlphaStock’s winner selection. Figures 3(a)-3(b) plot the influences from the trading features. The vertical axis denotes the influence strengths indicated by , and the horizontal axis denotes how many months before the trading time. For example, the bar indexed by “-12” of the horizontal axis in Fig. 3(a) denotes the influence of stock price rising rate (PR) at the time of twelve months ago.

As shown in Fig. 3(a), the influence of history price rising rate is heterogeneous along the time axis. The PR in long-term months, i.e., 9 to 11 months ahead, has positive influence to winner scores, but for the short-term months, i.e., 1 to 8 months ahead, the influence becomes negative. This result indicates that our model tends to buy the stocks with long-term rapid price increase (valid excellence) or with short-term rapid price retracement (over undervalued). This implies that AlphaStock behaviors like a long-term momentum but short-term reversion mixed strategy. Moreover, since price rising is usually accompanied by frequent stock trading, Fig. 3(b) shows that the of trading volumes (TV) has a similar tendency with the price rising rate (PR). Finally, as shown in Fig. 3(c), the volatilities (VOL) have negative influence to winner scores for all history months. It means that our model trends to select low volatility stocks as winners, which indeed explains why AlphaStock can adapt to diverse market states.

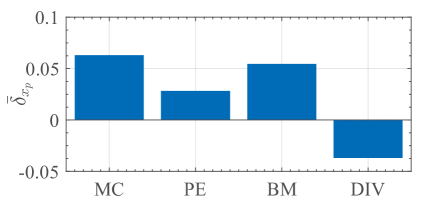

Fig. 3(d) further exhibits the average influences of different company features to the winner score, i.e., the averaged on all history months. It turns out that Market Capitalization (MC), Price-earnings Ratio (PE), and Book-to-market Ratio (BM) have positive influences. The three features are important company valuation factors for a listed company, which indicates that AlphaStock tends to select companies with sound fundamental values. In contrast, dividends mean a part of company values are returned to shareholders and could reduce the intrinsic value of a stock. That is why the influence of Dividends (DIV) is negative in our model.

To sum up, while AlphaStock is an AI-enabled investment strategy, the interpretation analysis proposed in Section 4 can help to extract investment logics from AlphaStock. Specifically, AlphaStock suggests selecting the stocks as winners with high long-term growth, low volatility, high intrinsic value, and being undervalued recently.

6. Related Works

Our work is related to the following research directions.

Financial Investment Strategy: Classic financial investment strategy includes Momentum, Mean Reversion, and Multi-factors. In the first work of BWSL (Jegadeesh and Titman, 1993), Jegadeesh and Titman found “momentum” could be used to select winners and losers. The momentum strategy buys assets that have had high returns over a past period as winners, and sells those that have had poor returns over the same period. Classic momentum strategies include the Cross Sectional Momentum (CSM) (Jegadeesh and Titman, 2002) and the Time Series Momentum (TSM) (Moskowitz et al., 2012). The mean reversion strategy (Poterba and Summers, 1988) considers asset prices always return to their mean over a past period, so it buys assets with a price under their historical mean and sells above the historical mean. The multi-factor model (Fama and French, 1996) uses factors to compute a valuation for each asset and buys/sells those assets with price under/above their valuations. Most of these financial investment strategies can only exploit a certain factor of financial markets and thus might fail in complex market environments.

Deep Learning in Finance: In recent years, deep learning approaches begin to be applied in the financial areas. In the literature, L. Zhang et al. proposed to exploit frequency information to predict stock prices (Hu and Qi, 2017). News and social media were used in price prediction in Refs. (Hu et al., 2018; Xu and Cohen, 2018). Information about events and corporation relationships were used to predict stock prices in Ref. (Ding et al., 2015; Chen et al., 2018). Most of these works focus on price prediction rather than end-to-end investment portfolio generation like us.

Reinforcement Learning in Finance: The RL approaches used in investment strategies fall in two categories: the value-based and the policy-based (Fischer, 2018). The value-based approaches learn a critic to describe the expected outcomes of markets to trading actions. Typical value-based approaches in investment strategies include Q-learning (Neuneier, 1995) and deep Q-learning (Jin and El-Saawy, 2016). A defect of value-based approaches is the market environment is too complex to be approximated by a critic. Therefore, policy-based approaches are considered as more suitable to financial markets (Fischer, 2018). The AlphaStock model also belongs to this category. A classic policy-based RL algorithm in investment strategy is the Recurrent Reinforcement Learning (RRL) (Moody et al., 1998). The FDDR (Deng et al., 2017) model extends the RRL framework using deep neural networks. In the Investor-Imitator model (Ding et al., 2018), a policy-based deep RL framework was proposed to imitate the behaviors of different types of investors. Compared with RRL and its deep learning extensions, which focus on exploiting sequential dependence in financial signals, our AlphaStock model pays more attention to the interrelationships among assets. Moreover, deep RL approaches are often hard to deployed in real-life applications for unexplainable deep network structures. The interpretation tools offered by our model can solve this problem.

7. Conclusions

In this paper, we proposed a RL-based deep attention network to design a BWSL strategy called AlphaStock. We also designed a sensitivity analysis method to interpret the investment logics of our model. Compared with existing RL-based investment strategies, AlphaStock fully exploits the interrelationship among stocks, and opens a door for solving the “black box” problem of using deep learning models in financial markets. The back-testing and simulation experiments over U.S. and Chinese stock markets showed that AlphaStock performed much better than other competing strategies. Interestingly, AlphaStock suggests buying stocks with high long-term growth, low volatility, high intrinsic value, and being undervalued recently.

Acknowledgments

J. Wang’s work was partially supported by the National Natural Science Foundation of China (NSFC) (61572059, 61202426), the Science and Technology Project of Beijing (Z181100003518001), and the CETC Union Fund (6141B08080401). Y. Zhang’s work was partially supported by the National Key Research and Development Program of China under Grant (2017YFC0820405) and the Fundamental Research Funds for the Central Universities. K. Tang’s work was partially supported the National Social Sciences Foundation of China (No.14BJL028). J. Wu’s work was partially supported by NSFC (71725002, 71531001, U1636210).

References

- (1)

- Adebayo et al. (2018) Julius Adebayo, Justin Gilmer, Michael Muelly, Ian Goodfellow, Moritz Hardt, and Been Kim. 2018. Sanity checks for saliency maps. In NIPS’18. 9525–9536.

- Chen et al. (2018) Yingmei Chen, Zhongyu Wei, and Xuanjing Huang. 2018. Incorporating Corporation Relationship via Graph Convolutional Neural Networks for Stock Price Prediction. In CIKM’18. ACM, 1655–1658.

- Deng et al. (2017) Yue Deng, Feng Bao, Youyong Kong, Zhiquan Ren, and Qionghai Dai. 2017. Deep direct reinforcement learning for financial signal representation and trading. IEEE TNNLS 28, 3 (2017), 653–664.

- Ding et al. (2015) Xiao Ding, Yue Zhang, Ting Liu, and Junwen Duan. 2015. Deep learning for event-driven stock prediction.. In IJCAI’15. 2327–2333.

- Ding et al. (2016) Xiao Ding, Yue Zhang, Ting Liu, and Junwen Duan. 2016. Knowledge-driven event embedding for stock prediction. In COLING’16. 2133–2142.

- Ding et al. (2018) Yi Ding, Weiqing Liu, Jiang Bian, Daoqiang Zhang, and Tie-Yan Liu. 2018. Investor-Imitator: A Framework for Trading Knowledge Extraction. In KDD’18. ACM, 1310–1319.

- Fama and French (1996) Eugene F Fama and Kenneth R French. 1996. Multifactor explanations of asset pricing anomalies. J. Finance 51, 1 (1996), 55–84.

- Fischer (2018) Thomas G Fischer. 2018. Reinforcement learning in financial markets-a survey. Technical Report. FAU Discussion Papers in Economics.

- Guidotti et al. (2018) Riccardo Guidotti, Anna Monreale, Salvatore Ruggieri, Franco Turini, Fosca Giannotti, and Dino Pedreschi. 2018. A survey of methods for explaining black box models. ACM Computing Surveys (CSUR) 51, 5 (2018), 93.

- Hochreiter and Schmidhuber (1997) Sepp Hochreiter and Jurgen Schmidhuber. 1997. Long Short-Term Memory. Neural Computation 9, 8 (1997), 1735–1780.

- Hu and Qi (2017) Hao Hu and Guo-Jun Qi. 2017. State-Frequency Memory Recurrent Neural Networks. In ICML’17. 1568–1577.

- Hu et al. (2018) Ziniu Hu, Weiqing Liu, Jiang Bian, Xuanzhe Liu, and Tie-Yan Liu. 2018. Listening to chaotic whispers: A deep learning framework for news-oriented stock trend prediction. In WSDM’18. ACM, 261–269.

- Huang et al. (2016) Dingjiang Huang, Junlong Zhou, Bin Li, Steven CH Hoi, and Shuigeng Zhou. 2016. Robust median reversion strategy for online portfolio selection. IEEE TKDE 28, 9 (2016), 2480–2493.

- Jegadeesh and Titman (1993) Narasimhan Jegadeesh and Sheridan Titman. 1993. Returns to buying winners and selling losers: Implications for stock market efficiency. J. Finance 48, 1 (1993), 65–91.

- Jegadeesh and Titman (2002) Narasimhan Jegadeesh and Sheridan Titman. 2002. Cross-sectional and time-series determinants of momentum returns. RFS 15, 1 (2002), 143–157.

- Jin and El-Saawy (2016) Olivier Jin and Hamza El-Saawy. 2016. Portfolio Management using Reinforcement Learning. Technical Report. Stanford University.

- Moody et al. (1998) John Moody, Lizhong Wu, Yuansong Liao, and Matthew Saffell. 1998. Performance functions and reinforcement learning for trading systems and portfolios. Journal of Forecasting 17, 5-6 (1998), 441–470.

- Moskowitz et al. (2012) Tobias J Moskowitz, Yao Hua Ooi, and Lasse Heje Pedersen. 2012. Time series momentum. J. Financial Economics 104, 2 (2012), 228–250.

- Neuneier (1995) Ralph Neuneier. 1995. Optimal Asset Allocation using Adaptive Dynamic Programming. In NIPS’95.

- Poterba and Summers (1988) James M Poterba and Lawrence H Summers. 1988. Mean reversion in stock prices: Evidence and implications. J. Financial Economics 22, 1 (1988), 27–59.

- Sharpe (1994) William F Sharpe. 1994. The sharpe ratio. JPM 21, 1 (1994), 49–58.

- Sutskever et al. (2014) Ilya Sutskever, Oriol Vinyals, and Quoc V Le. 2014. Sequence to Sequence Learning with Neural Networks. NIPS’14 (2014), 3104–3112.

- Sutton and Barto (2018) Richard S Sutton and Andrew G Barto. 2018. Reinforcement learning: An introduction. MIT press.

- Vaswani et al. (2017) Ashish Vaswani, Noam Shazeer, Niki Parmar, Jakob Uszkoreit, Llion Jones, Aidan N Gomez, Łukasz Kaiser, and Illia Polosukhin. 2017. Attention is all you need. In NIPS’17. 5998–6008.

- Wang et al. (2016) Jingyuan Wang, Qian Gu, Junjie Wu, Guannan Liu, and Zhang Xiong. 2016. Traffic speed prediction and congestion source exploration: A deep learning method. In ICDM’16. IEEE, 499–508.

- Wang et al. (2018) Jingyuan Wang, Ze Wang, Jianfeng Li, and Junjie Wu. 2018. Multilevel wavelet decomposition network for interpretable time series analysis. In KDD’18. ACM, 2437–2446.

- Xu and Cohen (2018) Yumo Xu and Shay B Cohen. 2018. Stock movement prediction from tweets and historical prices. In ACL’18, Vol. 1. 1970–1979.