StateSpaceModels.jl: a Julia Package for Time-Series Analysis in a State-Space Framework

Abstract

StateSpaceModels.jl is an open-source Julia package for modeling, forecasting and simulating time series in a state-space framework. The package represents a straightforward tool that can be useful for a wide range of applications that deal with time series. In addition, it contains features that are not present in related commercial software, such as Monte Carlo simulation and the possibility of setting any user-defined linear model.

Keywords: State-space models, time-series analysis, Kalman filter, forecasting, Monte Carlo simulation.

1 Motivation

State-space modeling is a classical framework in control engineering that represents a system through the definition of input, state, and output variables [1]. Input variables are external entities that are inserted into the system and can serve as control inputs or noise. State variables represent unobserved components that evolve through time following a given state equation and also depending on the values of the input variables. Finally, output variables result from the realization of the state plus noise factors and represent the observable outcome of the system. In general, state-space models make use of the Kalman filter [2, 3] to obtain predictive estimates for the state.

Due to its comprehensive form and wide range of potential applications, state-space models found a niche in time-series modeling, forecasting, and simulation, representing a flexible framework for time-series analysis with time-varying parameters [4]. The ability to conveniently define the evolution of a time series allows the characterization of stochastic components, such as trend and seasonality, that are non-trivial to model in other frameworks.

There are several packages focused on state-space models for time-series analysis in other languages, such as KFAS in R [5] and Statsmodels in Python [6], as well as commercial software such as STAMP [7]. Among related Julia packages, we highlight:

The contributions brought by these packages notwithstanding, there are currently no state-space model packages aimed at time-series analysis in Julia. Furthermore, some have not been updated for a long time and are not functional in Julia 1.0. Thus, the main objectives of StateSpaceModels.jl [11] are:

-

1.

to fill this gap by implementing a general and intuitive framework in Julia for modeling, estimating, forecasting and simulating time series with state-space models;

-

2.

to provide an open-source package that is capable of performing the same functions as related commercial software such as STAMP and more;

-

3.

to develop a package for time-series analysis with state-space models that is fully implemented in Julia, contrary to related packages in other languages that depend on C or Fortran routines [5].

The remainder of this paper is organized as follows. In Section 2, the Gaussian state-space framework is introduced. In Section 3, the procedures for model specification are presented. Section 4 explains the filtering, estimation and smoothing processes. In Section 5, the forecasting and simulation procedures are presented. Section 6 contains examples of applications that illustrate the use of the package. Finally, conclusions and future work are provided in Section 7.

2 Gaussian state-space framework

For the sake of consistency and readability, we utilize in the package the same notation as [4]. Suppose we have a series of observations . In a state-space framework, it is assumed that the observations depend on a set of unobserved components denominated states, or simply the state, and denoted by . The state components often have physical interpretations, such as trend and seasonality in a time-series context or position and speed in a control setting.

The main idea behind state-space modeling is to define the evolution of the state and its relation with the observed variables. This is done through the following two equations, denoted the observation equation and the state equation, respectively:

| (1) | ||||

| (2) |

where is a vector of observations and is an unobserved vector representing the state at instant . Note that the behavior of the system over time is determined by as defined in Eq. (2), but cannot be directly observed, contrary to .

Matrices , , and are the ones that define how the observations relate to the state and how the state evolves over time, and are generally assumed to be known. The error terms and are supposed to be serially independent and independent of each other. Finally, and are the covariance matrices of the error terms. In this package, it is assumed that , , , and are not time-varying, as this is the case for the vast majority of practical applications. Conversely, is allowed to vary over time.

Next, for illustration purposes, we present an example model and show how it can be inserted into the state-space framework. Consider the following model, called the linear trend model:

| (3) | ||||

| (4) | ||||

| (5) |

where represents the trend component and the slope component. Note that the we can rewrite this model in the framework of Eq. (1)--(2) in the following manner:

| (6) | ||||

| (7) |

Similarly, more complex and sophisticated models can also be modeled in the state-space framework.

3 Model specification

Model specification is the step wherein the user defines the state-space model they want to consider. This is done through the creation of a StateSpaceModel structure that contains the observations as well as matrices , , and .

3.1 Predefined models

A set of predefined classical models is available, namely the local level model, the linear trend model, the basic structural model, and the structural model with exogenous variables. These models can be conveniently defined by calling a function and providing the observations . Note that all models automatically extend to the multivariate case.

3.1.1 Local level model

The local level model consists of a stochastic level component that is defined by a random walk:

| (8) | ||||

| (9) |

A local level StateSpaceModel can be created using:

where y is an observation vector in the univariate case or a matrix in column-wise fashion in the multivariate case, i.e., each column representing a variable and each line representing a time period.

3.1.2 Linear trend model

3.1.3 Structural model

The basic structural model consists of three stochastic components: trend, slope, and seasonality, defined in the following manner:

| (10) | ||||

| (11) | ||||

| (12) | ||||

| (13) |

In this model, there is a stochastic trend that contains a slope component, similarly to the linear trend model. Furthermore, a stochastic seasonal component is modeled so that its sum over the seasonality period is equal to zero except for a noise factor. A basic structural StateSpaceModel can be created using:

Additionally, a structural model can contain exogenous variables, also known as explanatory variables. Exogenous variables represent external factors that are correlated to the phenomenon in question and can, thus, be used to improve the estimation and forecasting by increasing the available information. This model is identical to (10)--(13) except for the observation equation, which has an additional exogenous factor:

| (14) |

A structural model with exogenous variables can be created with:

where X is a matrix containing the exogenous variables observations in column-wise fashion.

3.2 User-defined models

Apart from the well-known predefined models presented in Section 3.1, the package allows the input of any user-defined linear model through the definition of matrices , , and through the following constructor:

In the simpler case where is constant, the argument Z can be input as an Array{Float64, 2}. Conversely, if is time-varying, it must be input as an Array{Float64, 3} where the third dimension represents the time periods.

4 Filtering, estimation, and smoothing

Next, the model needs to be estimated. In this step, values for the covariance matrices and , initially assumed to be unknown, are obtained via maximum likelihood estimation [12]. In order to do that, the Kalman filter needs to be utilized. Additionally, a smoother is applied in order to obtain the so-called smoothed estimates for the state.

After specifying the model, the estimation step can be called with the function statespace:

In this step, the Kalman filtering, the maximum likelihood estimation of the fixed parameters, and the smoothing are conducted. The optional argument verbose, which defaults to 1, specifies the verbosity: 0 for no output, 1 for some progress information, and 2 for progress information as well as the optimization log.

An example of the estimation log with default verbosity can be seen below.

4.1 Filtering

The filtering step derives the predictive and filtered states as well as their covariance matrices at every time period via the Kalman filter. The predictive state and its variance are given by

| (15) | ||||

| (16) |

while the filtered state and its variance are given by

| (17) | ||||

| (18) |

where denotes the set of time periods .

Furthermore, the filter also computes the innovations, or prediction errors, as well as their covariance matrix at every time period:

| (19) | ||||

| (20) |

The package contains an implementation of the standard Kalman filter and the square-root Kalman filter [4]. The latter is a variant which utilizes Cholesky decomposition to ensure that the computed covariance matrices are positive semidefinite, thus avoiding numerical errors.

Additionally, in order to provide a flexible framework, we allow the utilization of any user-implemented variant of the Kalman filter through an abstract type called AbstractFilter:

The choice of the filter type must be done in the estimation step as follows:

If no filter_type is provided, the standard type KalmanFilter is utilized as a default option. Further information on Kalman filtering can be found in Chapter 4.3 of [4].

4.2 Estimation

The Kalman filter is responsible for deriving estimates for the predictive state and for its covariance matrix at each time period, but it is dependent on the values of the noise covariances and . Thus, these constant parameters need to be estimated via maximum likelihood [12]. The log-likelihood function is given by

| (21) |

which depends on the innovations and their covariance matrix at each time period. Therefore, at each optimization iteration, the Kalman filter needs to be executed.

The implemented optimization method RandomSeedsLBFGS generates random initial values for the parameters and then uses the L-BFGS algorithm [13] to maximize the log-likelihood function via the unconstrained optimization package Optim.jl [14].

Additionally, similar to the filtering step, users are able to define any desired optimization method through abstract type AbstractOptimizationMethod:

As with the filter type, the choice of optimization method must be done in the estimation step:

More advanced parameters, such as optimizer tolerances and the number of seeds, can be set within the RandomSeedsLBFGS constructor.

4.3 Smoothing

The smoothing step is conducted after estimation is complete. It consists in obtaining the so-called smoothed state and its covariance matrix at each time period, i.e.,

| (22) | ||||

| (23) |

Similar to the filtering step, the smoothing is conducted through an iterative process. The procedure is done backwards, starting from the final time period . The smoothed state estimates are useful for analyzing the behavior of the state components. Further information on state smoothing can be found on Chapter 4.4 of [4].

4.4 Missing observations

One interesting property of the Kalman filter and smoother is their ability to treat missing observations. Suppose we have a time series spanning time periods , but for some periods we have no observations available. This represents an obstacle for estimating a model in several frameworks. Nonetheless, the Kalman filter and smoother allow the derivation of minimum variance linear unbiased estimates for the missing observations so that a completion of the time series is possible. Conveniently, the only necessary modification in the filtering and smoothing equations is considering for the missing period.

In the package, this is implemented so that any NaN values in the observations are considered missing observations and automatically treated in the filtering and smoothing steps. In this way, the estimation is successfully conducted even when the time series of interest is incomplete.

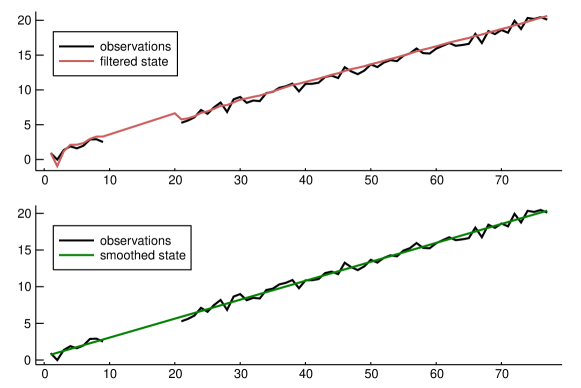

Consider the following simulated time series composed by a growing trend plus a Gaussian noise. Additionally, we remove observations 10 through 20 to treat them as missing:

The results of the estimation step are presented in Fig. 1. The predictive, filtered, and smoothed state estimates can be accessed in ss.filter.a, ss.filter.att, and ss.smoother.alpha, respectively. It is clear in Fig. 1 that the filter and smoother are able to effectively capture the growing linear trend of the series even in the period where observations are missing.

4.5 Estimation outputs

At the end of the filtering, estimation, and smoothing routine executed by the statespace function, a StateSpace structure is returned. It contains six fields:

-

•

model: the previously defined StateSpaceModel.

-

•

filter: a FilterOutput structure representing the result of the Kalman filter. It contains the predictive and filtered states as well as the innovations and their covariance matrices at each time period. Furthermore, there is a flag indicating if steady state was attained and the time period when it was attained.

-

•

smoother: a SmoothedState structure representing the result of the smoothing procedure. It contains the smoothed state as well as its covariance matrix at each time period.

-

•

covariance: a StateSpaceCovariance structure which contains the covariance matrices of the observation and state noises.

-

•

filter_type: the defined filter type.

-

•

optimization_method: the defined optimization method.

5 Forecasting and Simulation

Finally, after the model has been estimated, forecasting and Monte Carlo simulation can be conducted. In the case of forecasting, estimates for the future values of the time series are computed along with their probability distributions. Alternatively, it is possible to simulate an arbitrary number of future scenarios of the series, which is useful for a wide range of applications such as stochastic optimization.

The minimum mean square error forecasts for can be obtained by treating future values of as missing values. Forecasting is conducted with the function forecast, which receives a StateSpace structure coming from the estimation step and the number of time periods ahead to be forecast, and outputs the minimum square error forecasts and the predictive distributions of at each time period:

Alternatively, another powerful tool is the simulation of future scenarios, since these are used as input by several applications, such as certain stochastic optimization models. Performing Monte Carlo simulation in a time-series state-space framework involves sampling several scenarios for the observation and state errors utilizing the estimated variances and at each time period, and then computing the state-space recursions for each scenario.

Monte Carlo simulation can be conducted with the use of the function simulate, which receives a StateSpace structure coming from the estimation step, the number of time periods ahead , and the number of scenarios to be simulated, and outputs an matrix of scenarios for :

6 Applications

In this section, we present several practical applications which can be addressed via state-space modeling. We utilize StateSpaceModels.jl to tackle the presented problems and provide the results. Furthermore, for the sake of reproducibility, the code of some of the examples is in the folder examples in the StateSpaceModels.jl repository.

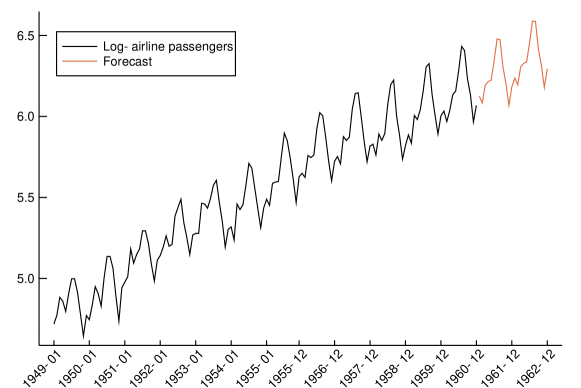

6.1 Airline passengers

As a first example, let us use the classical monthly airline passengers time series. In order to avoid multiplicative effects, we use the well-known approach of taking the log of the series. Fig. 2 shows the log-airline passengers time series. We can estimate a structural StateSpaceModel as follows.

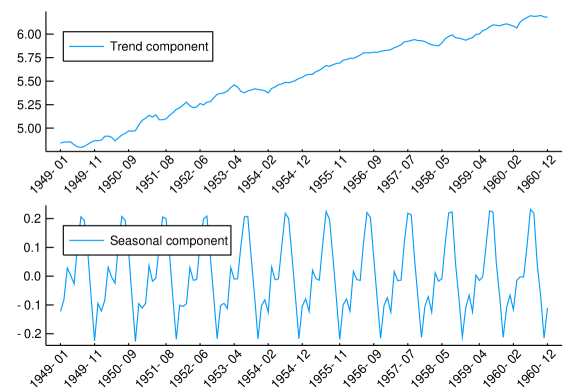

By estimating a structural model, we can analyzed the individual components of the series, such as trend and seasonality. These components are presented in Fig. 3 and represent dimensions 1 and 3 of the smoothed state, respectively.

We can also forecast the following two years of the time series by using the forecast function. The result is displayed in Fig. 2.

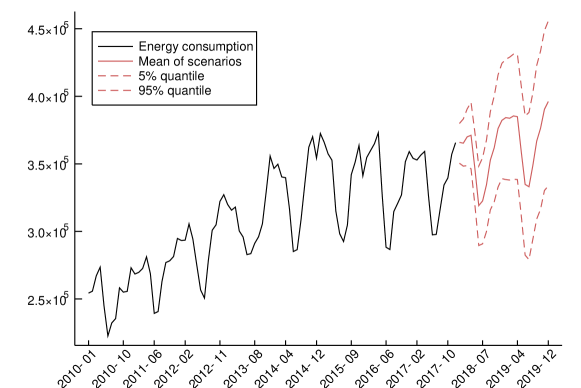

6.2 Electricity consumption

Another practical example is the study of monthly electricity consumption in a given area. In this example, we will use real data from a Brazilian distribution company. In addition, we will consider a temperature series, which is highly correlated to electricity consumption in Brazil, as an exogenous variable. A similar study using StateSpaceModels.jl was conducted in [15].

In this case, our objective is to simulate a large set of future scenarios that can be used as inputs in a stochastic optimization problem with the goal of obtaining the best contracting strategy for a distribution company. To this end, the function simulate will be used to perform Monte Carlo simulation. We will also use the square-root Kalman filter for this application.

The time series and the resulting simulation can be seen in Fig. 4. The future scenarios are graphically represented by their mean, which is identical to the forecast at each time period, as well as the 5% and 95% quantiles.

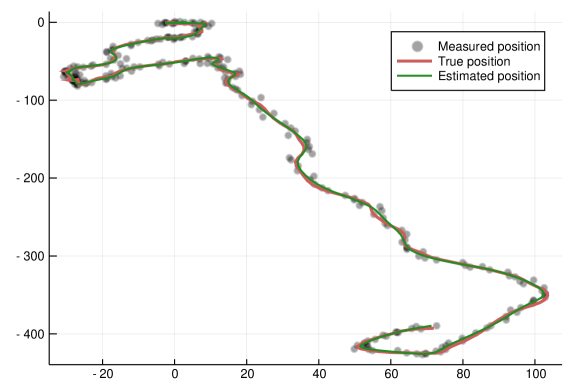

6.3 Vehicle tracking

Finally, in order to illustrate one application that does not fall into any of the predefined models, thus requiring a user-defined model, let us consider an example from control theory. More precisely, we are going to use StateSpaceModels.jl to track a vehicle from noisy sensor data. In this case, is a observation vector representing the corrupted measurements of the vehicle’s position on the two-dimensional plane in instant . Since sensors collect the observations with the presence of additive Gaussian noise, we need to filter the observation in order to obtain a better estimate of the vehicle’s position.

The position and speed in each dimension compose the state of the vehicle. Let us refer to as the position on the axis and to as the speed on the axis in instant . Additionally, let be the input drive force on the axis , which acts as state noise. For a single dimension, we can describe the vehicle dynamics as

| (24) | ||||

where is the time step and is a known damping effect on speed.

We can formulate the vehicle tracking problem in the StateSpaceModels.jl framework as:

In this example, we define the noise variances and , generate the noises and simulate a random vehicle trajectory using the state-space equations:

An illustration of the results can be seen in Fig. 5. It can be seen that the measurements are reasonably noisy when compared to the true position. Furthermore, the estimated positions, represented by the smoothed state, effectively estimate the true positions with small inaccuracies.

7 Conclusion

StateSpaceModels.jl is a flexible package for time-series modeling, forecasting, and simulating that is fully implemented in Julia. The package contains an implementation of the Kalman filter and smoother as well as their square-root variants. Additionally, users have the ability to use any implemented filter or optimization method. Missing observations in the form of NaN values are automatically treated in the filtering and smoothing steps.

Besides comprising several predefined classical models, it is also possible to define any linear model with the StateSpaceModel constructor. Forecasting and Monte Carlo simulation of future scenarios are also available. Finally, the package documentation contains a manual with straightforward examples that are simple to reproduce.

References

- [1] L. Zadeh and C. Desoer, Linear System Theory: The State Space Approach. Courier Dover Publications, 2008.

- [2] R. E. Kalman, ‘‘A new approach to linear filtering and prediction problems,’’ Journal of Basic Engineering, vol. 82, no. 1, pp. 35--45, 1960.

- [3] G. Welch, G. Bishop et al., ‘‘An introduction to the Kalman filter,’’ Department of Computer Science, University of North Carolina at Chapel Hill, Tech. Rep., 1995.

- [4] J. Durbin and S. J. Koopman, Time Series Analysis by State Space Methods. Oxford University Press, 2012.

- [5] J. Helske, ‘‘KFAS: Exponential family state space models in R,’’ Journal of Statistical Software, vol. 78, no. 10, pp. 1--39, 2017.

- [6] S. Seabold and J. Perktold, ‘‘Statsmodels: Econometric and statistical modeling with Python,’’ in 9th Python in Science Conference, 2010.

- [7] S. J. Koopman, A. C. Harvey, J. A. Doornik, and N. Shephard, ‘‘STAMP 6.0: Structural time series analyser, modeller and predictor,’’ London: Timberlake Consultants, 2000.

- [8] M. Schauer, ‘‘Kalman.jl,’’ [Online]. Available: https://github.com/mschauer/Kalman.jl

- [9] ‘‘StateSpace.jl,’’ [Online]. Available: https://github.com/ElOceanografo/StateSpace.jl

- [10] F. B. Carlson and M. Fält, ‘‘ControlSystems.jl: A Control Systems Toolbox for Julia,’’ 2016 [Online]. Available: https://github.com/JuliaControl/ControlSystems.jl

- [11] R. Saavedra, G. Bodin, and M. Souto, ‘‘StateSpaceModels.jl,’’ [Online]. Available: https://github.com/LAMPSPUC/StateSpaceModels.jl

- [12] G. Casella and R. L. Berger, Statistical Inference. Duxbury Pacific Grove, CA, 2002, vol. 2.

- [13] D. C. Liu and J. Nocedal, ‘‘On the limited memory BFGS method for large scale optimization,’’ Mathematical programming, vol. 45, no. 1-3, pp. 503--528, 1989.

- [14] P. K. Mogensen and A. N. Riseth, ‘‘Optim: A mathematical optimization package for Julia,’’ Journal of Open Source Software, vol. 3, no. 24, 2018.

- [15] R. Saavedra, G. Bodin et al., ‘‘Simulating low and high-frequency energy demand scenarios in a unified framework--Part I: Low-frequency simulation,’’ in Proceedings of the L Simpósio Brasileiro de Pesquisa Operacional, 2018.