Proof.

. :

On the Existence of Simpler Machine Learning Models

It is almost always easier to find an accurate-but-complex model than an accurate-yet-simple model. Finding optimal, sparse, accurate models of various forms (linear models with integer coefficients, decision sets, rule lists, decision trees) is generally NP-hard. We often do not know whether the search for a simpler model will be worthwhile, and thus we do not go to the trouble of searching for one. In this work, we ask an important practical question: can accurate-yet-simple models be proven to exist, or shown likely to exist, before explicitly searching for them? We hypothesize that there is an important reason that simple-yet-accurate models often do exist. This hypothesis is that the size of the Rashomon set is often large, where the Rashomon set is the set of almost-equally-accurate models from a function class. If the Rashomon set is large, it contains numerous accurate models, and perhaps at least one of them is the simple model we desire. In this work, we formally present the Rashomon ratio as a new gauge of simplicity for a learning problem, depending on a function class and a data set. The Rashomon ratio is the ratio of the volume of the set of accurate models to the volume of the hypothesis space, and it is different from standard complexity measures from statistical learning theory. Insight from studying the Rashomon ratio provides an easy way to check whether a simpler model might exist for a problem before finding it, namely whether several different machine learning methods achieve similar performance on the data. In that sense, the Rashomon ratio is a powerful tool for understanding why and when an accurate-yet-simple model might exist. If, as we hypothesize in this work, many real-world data sets admit large Rashomon sets, the implications are vast: it means that simple or interpretable models may often be used for high-stakes decisions without losing accuracy.

1 Introduction

Following the principle of Occam’s Razor, one should use the simplest model that explains the data well. However, finding the simplest model, let alone any simple-yet-accurate model, is hard. As soon as simplicity constraints such as sparsity are introduced, the optimization problem for finding a simpler model typically becomes NP-hard. Thus, practitioners – who have no assurance of finding a simpler model that achieves the performance level of a black box – may not see a reason to attempt such potentially difficult optimization problems. Thus, sadly, what was once the holy grail of finding simpler models, has been, for the most part, abandoned in modern machine learning. In this work, we ask a question that is essential, and potentially game-changing, for this discussion: what if we knew, before attempting a computationally expensive search for a simpler-yet-accurate model, that one was likely to exist? Perhaps knowing this would allow us to justify the time and expense of searching for such a model. If it is true that many data sets have large enough Rashomon sets to admit simple models, then there are important implications for society – it means we may be able to use simpler or interpretable models for many high-stakes problems without losing accuracy.

Proving the existence of simpler models before aiming to find them differs from the current approach to machine learning in practice. We generally do not think about going from more complicated spaces to simpler ones; in fact, the reverse is true, where typical statistical learning theory and algorithms allowed us to maintain generalization when handling more complicated model classes (e.g., large margins for support vector machines with complex kernels or large margins for boosted trees) Cortes and Vapnik (1995); Schapire et al. (1998). We even build neural networks that are so complex that they can achieve zero training error, and try afterwards to determine why they generalize Belkin et al. (2019); Nakkiran et al. (2021). However, because simple models are essential for many high-stakes decisions (Rudin, 2019), perhaps we should return to the goal of aiming directly for simpler models. We will need new ideas in order to do this.

Decades of study about generalization in machine learning have provided many different mathematical theories. Many of them measure the complexity of classes of functions without considering the data (e.g., VC theory, Vapnik, 1995), or measure properties of specific algorithms (e.g., algorithmic stability, see Bousquet and Elisseeff, 2002). However, none of these theories seems to capture directly a phenomenon that occurs throughout practical machine learning. In particular, there are a vast number of data sets for which many standard machine learning algorithms perform similarly. In these cases, the machine learning models tend to generalize well. Furthermore, in these same cases, there is often a simpler model that performs similarly and also generalizes well.

We hypothesize that these three observations can all be explained by the same phenomenon: the “Rashomon effect,” which is the existence of many almost-equally-accurate models (Breiman et al., 2001). Firstly, following a key argument in our work, if there is a large Rashomon set of almost-equally-accurate models, a simple model may also be contained in it. Secondly, if the Rashomon set is large, many different machine learning algorithms may find different but approximately-equally-well-performing models inside it. An experimenter could then observe similar performance for different types of algorithms that produce very different functions. Thirdly, if the Rashomon set is large enough to contain simpler models, those models are guaranteed to generalize well. As we will show in Section 5.2, there are mathematical assumptions that allow us to prove existence of simpler models within the Rashomon set. If the assumptions are satisfied, a model from a simpler class is approximately as accurate as the most accurate model within the hypothesis space, which consequently leads to better generalization guarantees. The assumptions are based in approximation theory, which models how one class of functions can approximate another.

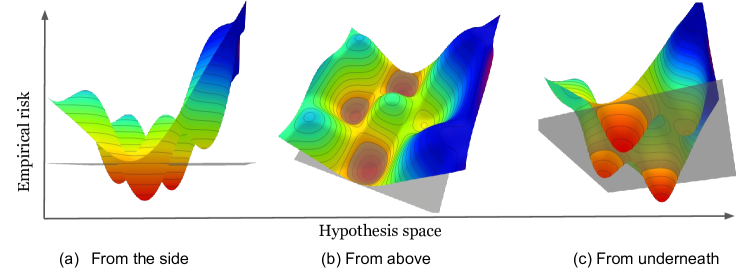

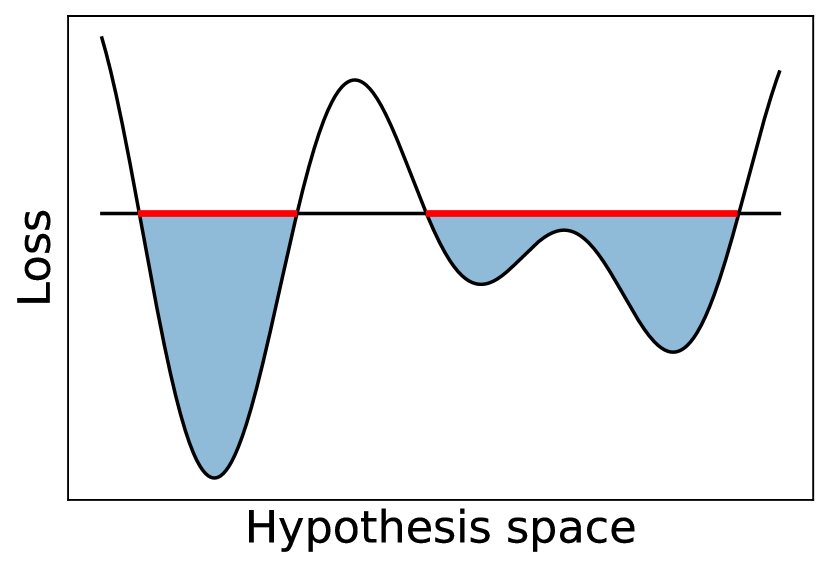

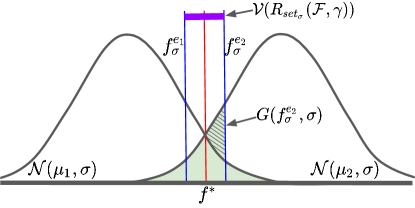

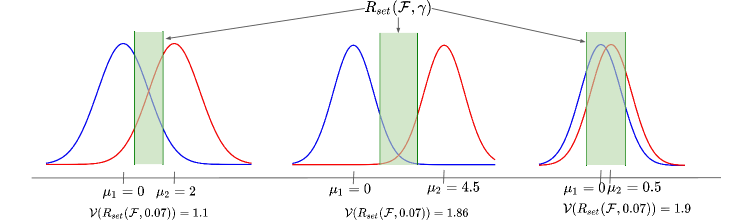

We quantify the magnitude of the Rashomon effect through the Rashomon ratio, which is the ratio of the Rashomon set’s volume to the volume of the hypothesis space. An illustration of the Rashomon set is shown in Figure 1; it does not need to be a connected or convex set. The Rashomon ratio can serve as a gauge of simplicity for a learning problem.111Such measures are typically called “complexity” measures, but the Rashomon ratio measures simplicity, not complexity. As a property of both a data set and a hypothesis space, it differs from the VC dimension (Vapnik and Chervonenkis, 1971) (because the Rashomon ratio is specific to a data set), it differs from algorithmic stability (see Rogers and Wagner, 1978; Kearns and Ron, 1999) (as the Rashomon ratio does not rely on robustness of an algorithm with respect to changes in the data), it differs from local Rademacher complexity (Bartlett et al., 2005) (as the Rashomon ratio does not measure the ability of the hypothesis space to handle random changes in targets and actually benefits from multiple similar models), and it differs from geometric margins (Vapnik, 1995) (as the maximum margin classifier can have a small minimum margin yet the Rashomon ratio can be large, and margins are measured with respect to one model, whereas the Rashomon ratio considers the existence of many). We provide theorems that show simple cases when the Rashomon ratio disagrees with these complexity measures in Section 3 and Appendix B. The Rashomon set is not just functions within a flat minimum; it could consist of functions from many non-flat local minima as illustrated in Figure 7 in Appendix A, and it applies to discrete hypothesis spaces where gradients, and thus “sharpness” (Dinh et al., 2017) do not exist. For linear regression, we derive a closed form solution for the volume of the Rashomon set in parameter space in Theorem 10 in Appendix B.1.

Our theory and empirical results have implications beyond cases where the size of the Rashomon set can be estimated in practice: they suggest computationally inexpensive ways to gauge whether the Rashomon set is large without directly measuring it. In particular, our results indicate that when many machine learning methods perform similarly on the same data set (without overfitting), it could be because the Rashomon set of the functions these algorithms consider is large. Thus, after running different machine learning methods and observing similar performance, our results indicate that it may be worthwhile to optimize directly for simpler models within the Rashomon set.

We summarize the contributions of this work as follows: (i) We define the Rashomon ratio as an important characteristic of the Rashomon set. (ii) We provide generalization bounds for models from the Rashomon set, and show that the size of the Rashomon set serves as a barometer for the existence of accurate-yet-simpler models that generalize well. These are different from standard learning theory bounds that consider the distance between the true and empirical risks for the same function. (iii) We provide several approaches for estimating the size of the Rashomon set. (iv) We show empirically that when a large Rashomon set occurs, most machine learning methods tend to perform similarly, and also in these cases, simple or sparse (yet accurate) models exist. (v) We demonstrate that the Rashomon ratio, as a gauge of simplicity of a machine learning problem, is different from other known complexity measures such as VC-dimension, algorithmic stability, geometric margin, and Rademacher complexity. (vi) We show that larger Rashomon sets might occur in the presence of label or feature noise.

2 Related Work

There are several bodies of relevant literature as discussed below.

Rashomon sets:

Rashomon sets have been used for various purposes (Breiman et al., 2001; Srebro et al., 2010; Fisher et al., 2019; Coker et al., 2021; Tulabandhula and Rudin, 2014b; Meinshausen and Bühlmann, 2010; Letham et al., 2016; Nevo and Ritov, 2017). For instance, Srebro et al. (2010) consider a loss-restricted class of close-to-optimal models, and with an assumption of H-smoothness of a loss function, they obtain a tighter excess risk bound through local Rademacher complexity (Bartlett et al., 2005). Our bounds do not work the same way and aim to prove a different type of result. Other works aim to search through the Rashomon set to find the most extreme models within it, rather than looking at the size of the Rashomon set, as we do in this work. Fisher et al. (2019) leverages the Rashomon set in order to understand the spectrum of variable importance and other statistics across the set of good models. Our work considers the existence of models from simpler classes rather than exploring the Rashomon set to find a range of variable importance or other statistics. The work of Tulabandhula and Rudin (2013, 2014a, 2014b) uses the Rashomon set to assist with decision making, by finding the range of downstream operational costs associated with the Rashomon set. Rashomon sets are related to p-hacking and robustness of estimation, because the Rashomon set is a set over which one might conduct a sensitivity analysis to choices made by an analyst (Coker et al., 2021). Large Rashomon sets can occur when the machine learning pipeline is underspecified. D’Amour et al. (2020) provides multiple examples of underspecification in computer vision, natural language processing, and healthcare domains; their work builds off of (an earlier version of) our work. Madras et al. (2019) proposed a post-hoc local-ensemble method that measures underspecification for a given test datum. Marx et al. (2020) studies conflicting predictions between models within the Rashomon set, while Coston et al. (2021) investigates predictive disparities for algorithmic fairness.

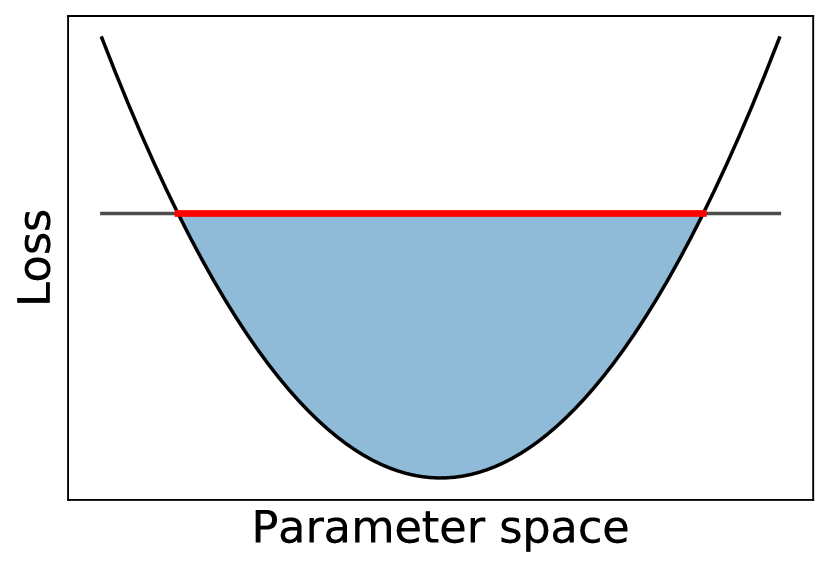

Flat minima or wide valleys:

The concept of flat minima (wide valleys) has been explored in the deep learning literature as a possible way to understand convergence properties of the complicated, non-convex loss functions that deep networks traverse during training (Hochreiter and Schmidhuber, 1997; Dinh et al., 2017; Keskar et al., 2016; Chaudhari et al., 2019). Based on a minimum-message-length argument (Wallace and Boulton, 1968), several works claim that flat loss functions lead to better generalization due to a robustness to noise around the minimum (Hochreiter and Schmidhuber, 1997; Keskar et al., 2016; Chaudhari et al., 2019). Following Hochreiter and Schmidhuber (1997), Dinh et al. (2017) define volume -flatness, which constitutes a special case of our Rashomon sets, as shown in Figure 7 in Appendix A. In particular, the Rashomon set is defined over the hypothesis (functional) space, while the volume -flatness is defined in a parameter space (though sometimes we use parameter space for ease of computation), and the Rashomon set is not necessarily a single connected component (although it might be in the case of a convex loss over a continuous domain), while volume -flatness pertains only to a connected set. This means that the Rashomon set can contain models from different local minima, or can be defined on discrete spaces, while volume -flatness is relevant only for continuous loss functions. Another way of quantifying flatness is -sharpness (Keskar et al., 2016; Dinh et al., 2017), which measures the change of the loss function inside a -ball in a parameter space. In the case of a connected Rashomon set, this loss difference corresponds to the Rashomon parameter .

Statistical learning theory:

Numerous works provide generalization bounds based on different complexity measures, and under different assumptions. Some discuss Rademacher (Srebro et al., 2010; Kakade et al., 2008) and Gaussian complexities (Kakade et al., 2008), PAC-Bayes theorems (Langford and Shawe-Taylor, 2002), covering numbers bounds (Zhou, 2002), and margin bounds (Vapnik and Chervonenkis, 1971; Schapire et al., 1998; Koltchinskii and Panchenko, 2002). In contrast, under assumptions elaborated in Section 5, the Rashomon ratio provides a certificate of the existence of a simpler model that generalizes. The use of approximating sets, as used extensively in this paper, is used throughout the literature on learning theory (Lecué, 2011; Lugosi and Wegkamp, 2004; Schapire et al., 1998; Mendelson, 2003). An example of this is the classical generalization bound for boosting and margins (Schapire et al., 1998), which uses combinations of several random draws of base classifiers to represent combinations of base classifiers. This is an instance of the so-called “Maurey’s lemma,” which provides an approximating set for linear model classes.

3 Rashomon Set Definitions and Notation

Consider a training set of data points , drawn i.i.d. from an unknown distribution on a bounded set , where and are an input and an output space respectively. Our hypothesis space is . We limit the hypothesis space to contain only models that vary within the bounded domain where the data reside. We will assume that the hypothesis space is bounded and that there is a prior distribution over functions in . To measure the quality of a prediction made by a hypothesis, we use a loss function . Specifically, for each given point and a hypothesis , the loss function is . For a given we will also overload notation by writing that takes explicitly as an argument: . We are interested in learning a model that minimizes the true risk which depends on unknown distribution and therefore is estimated with an empirical risk:

The empirical Rashomon set (or simply Rashomon set) is a subset of models of the hypothesis space that have training performance close to the best model in the class, according to a loss function (Breiman et al., 2001; Srebro et al., 2010; Fisher et al., 2019; Coker et al., 2021; Tulabandhula and Rudin, 2014b). More precisely:

Definition 1 (Rashomon set).

Given , a data set , a hypothesis space , and a loss function , the Rashomon set is the subspace of the hypothesis space defined as follows:

where is an empirical risk minimizer for the training data with respect to loss function :

If we want to specify the data set that is used to compute the Rashomon set, we indicate the data set in the subscript, as . Fisher et al. (2019)’s definition of Rashomon set is distinct from ours in that we typically use an empirical risk minimizer to define the Rashomon set instead of a prespecified reference model which is independent of the sample.

The hypothesis space can be a well-defined hypothesis space, such as the space of decision trees of depth or neural nets with hidden layers, or it can be a more general space (a meta-hypothesis space) that contains models from different hypothesis spaces (e.g., linear functions, polynomials up to degree , and piecewise constant functions).

We call the Rashomon parameter. Since hypothesis spaces can vary from one problem to another, we will often normalize the size of the Rashomom set via the Rashomon ratio which takes the Rashomon set as input and outputs a value between 0 and 1. Given a prior, , on the hypothesis space, the Rashomon ratio measures the fraction of the hypothesis space contained in the Rashomon set. Unless explicitly specified, is assumed to be uniform. For simplicity, we will denote the Rashomon ratio as . In general, the Rashomon ratio is . If the hypothesis space has a uniform prior, then the Rashomon ratio is the volume of the Rashomon set divided by the volume of the hypothesis space , where is the volume function. If the hypothesis space is discrete with a uniform prior, the Rashomon ratio can be computed as where . The Rashomon ratio represents the fraction of models that are good (the fraction of models that fit the data about equally well). A larger Rashomon ratio implies that more models perform about equally well. The data set is denoted in the subscript, as .

We consider true Rashomon sets that contain models with low true risk, relative to the optimal true risk value, with parameter :

where minimizes the true risk. denotes the Rashomon ratio for the true Rashomon set.

A large true Rashomon set, as it turns out, can be a certificate of the existence of a simpler model. Though, since we can never actually explore the true Rashomon set, we would never know whether it will be (or has been) useful for a particular problem. We explain this in Section 5, and spend most of our effort considering empirical Rashomon sets, which are easier to work with in practice.

When the hypothesis space has a parameterized representation (denote ), we assume that we can parameterize each model with a unique parameter vector of finite length and denote . In the next section, we discuss properties of the Rashomon ratio as a complexity measure.

4 Rashomon ratio as a simplicity measure

| Complexity measure | Property of | Depends on data | Considers set of good models |

|---|---|---|---|

| VC Dimension | hypothesis space | no | no |

| Algorithmic stability (Hypothesis stability Bousquet and Elisseeff (2002)) | algorithm, hypothesis space | no | no |

| Empirical algorithmic stability (Algorithmic hypothesis stability Bousquet and Elisseeff (2002)) | algorithm, hypothesis space | yes | no |

| Geometric margins | one function | yes | no |

| Empirical Local Rademacher Complexity (Bartlett et al., 2005) | hypothesis space | depends on features, not on labels | no |

| Rashomon ratio | hypothesis space | yes, but not always on labels (see Theorem 10) | yes |

The Rashomon ratio, as a property of a data set and a hypothesis space, serves as gauge of simplicity of the learning problem. If the Rashomon set is large, many different reasonable optimization procedures could lead to a model from the Rashomon set. Therefore, for large Rashomon sets, accurate models tend to be easier to find (since optimization procedures can find them). In other words, if the Rashomon ratio is large, the Rashomon set could contain many accurate and simple models, and the learning problem becomes simpler. On the other hand, smaller Rashomon ratios might imply a harder learning problem, especially in the case of few deep and narrow local minima.

The Rashomon ratio can give insight into the simplicity of a learning problem, though it was designed for a fundamentally different goal than well-known complexity measures from learning theory (see Table 1). While those complexity measures were designed to help us understand generalization, the Rashomon ratio (with additional assumptions) helps us understand whether simpler functions might exist with the same level of accuracy as complex functions. The Rashomon ratio depends on a loss function, the hypothesis space, and a data set, while the majority of other measures are either data-agnostic or focus on properties of a specific model in the space.

The Rashomon ratio is different from VC dimension.

The VC dimension (Vapnik and Chervonenkis, 1971) shows the expressive power of a hypothesis space for any data set including an extreme arrangement of data points and labels. On the contrary, the Rashomon set depends on an empirical risk minimizer that we compute directly for a specific data set, which may not be extreme.

The Rashomon ratio is different from algorithmic stability.

Algorithmic stability (Bousquet and Elisseeff, 2002) (see Definition 11) depends on a change to a data set, whereas Rashomon Ratio uses a fixed data set. As we will show in Theorem 10 in Appendix B.1, in the case of linear least squares regression, the Rashomon ratio depends on features () only, and does not depend on regression targets . In contrast, hypothesis stability depends heavily on . In fact, if we can control how we change the set of targets, hypothesis stability (a form of algorithmic stability) can be made to change by an arbitrarily large amount. This is formalized in Theorem 2 with proof in Appendix B.2.

Theorem 2 (Rashomon ratio is not algorithmic stability).

Consider a distribution over a discrete domain and a learning algorithm that minimizes the sum of squares loss : . for a linear hypothesis space . For any , there exist joint distributions and where for drawn i.i.d. from , drawn from over , and drawn from over , the expected Rashomon ratios are the same:

yet hypothesis stability constants are different by our arbitrarily chosen value of : where and denote data sets and , is the hypothesis stability coefficient of algorithm for distribution and is the hypothesis stability coefficient for distribution .

The Rashomon ratio is different from geometric margins.

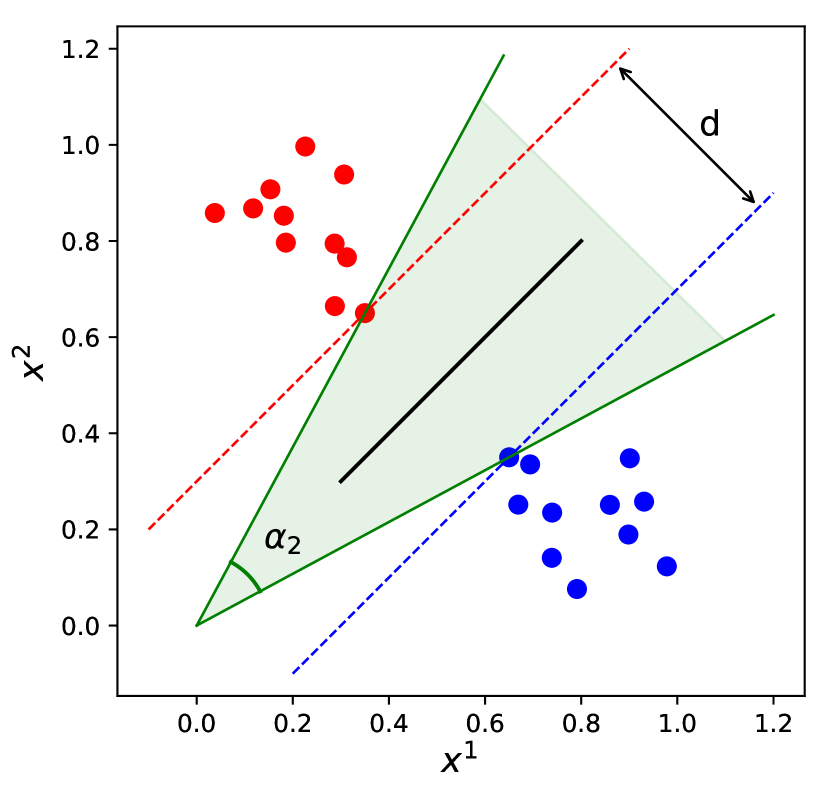

The margin (i.e., the minimum margin of the maximum margin classifier) (Schapire et al., 1998; Burges, 1998) depends on points closest to the decision boundary (support vectors), while the Rashomon set does not necessarily rely on the support vectors and may depend on the full data set. Theorem 3 shows this with proof in Appendix B.3.

Theorem 3 (Rashomon ratio is not the geometric margin).

For any fixed , there exists a fixed hypothesis space , a Rashomon parameter , and there exist two data sets and with the same empirical risk minimizer such that the geometric margin is the same for both data sets, yet the Rashomon ratios are different:

The Rashomon ratio is different from empirical local Rademacher complexity.

Empirical Rademacher complexity (Bartlett et al., 2005) (see Definitions 12) measures how well the hypothesis space can fit random assignments of the labels. The Rashomon ratio uses fixed labels. It measures the number of models that are close to optimal. In other words, the Rashomon set benefits from having multiple similar models, while Rademacher complexity treats them as equivalent. Please see Theorem 4 with definition and proof in Appendix B.4.

Theorem 4 (Rashomon ratio is not local Rademacher complexity).

For , there exist two data sets and , a hypothesis space , and a Rashomon parameter such that the local Rademacher complexities defined on the Rashomon sets for and are the same: yet the Rashomon ratios are different:

Now that we have established that the Rashomon ratio is not the same as other simplicity measures, we can now shift our focus to proving simplicity and generalization properties of models in the Rashomon set. This is critical to our thesis that simple-yet-accurate models exist.

5 Rashomon Set Models: Simplicity and Generalization

Consider two hypothesis (functional) spaces with different levels of complexity, where the lower-complexity space serves as a good approximating set (i.e., a good cover) for the higher-complexity space. The hypothesis spaces are called , for the simpler space, and , for the more complex space, where . Here, to determine the complexity of a hypothesis space, we use traditional notions of complexity (conversely, simplicity) such as covering numbers or VC dimension. For a useful example of a simple and a more complex space, consider to be the space of linear models with real-valued coefficients in a space of dimensions, and consider to be the space of scoring systems (Ustun and Rudin, 2016), which are sparse linear models, with at most nonzero integer coefficients, . Another example is if the more complex space consists of boosted decision trees, and consists of single trees. Generalization bounds would be tighter if we could use the lower complexity space , but as we are considering functions from , learning theory often has us include the complexity of in the bound. Given this setup, we have several questions to answer:

-

1.

What if the higher-complexity hypothesis space we chose were more complex than necessary for modeling the data? In that case, if we had instead used the simpler model class , would we still get a model that is (almost) as good as we could have obtained using the more complex class ? If so, perhaps we can leverage the complexity of the simpler model class for generalization bounds on our model rather than the more complex class . We answer this question in Section 5.1, where a property on the complex space that will help us is that the true Rashomon set of is large enough to admit a simpler model. We do not need to know what this model is and we may never discover it (we would likely discover a different model using data).

-

2.

Under what conditions on the complex and simpler model classes does the property we mentioned above (that the Rashomon set includes simpler models) hold? Does it hold often? As it turns out, under natural conditions on the function class and loss function, a large Rashomon set in the complex class does imply the existence of simple-yet-accurate models. We identify these conditions in Section 5.2, namely that the loss function is smooth, and that serves as a cover for . Thus, under these natural conditions that occur in practice, a large Rashomon set for a complex class of functions implies the existence of a simple-yet-accurate model.

The bounds we present in Section 5.1 do not serve the same purpose as standard statistical learning theoretic bounds, as they do not aim to bound generalization error for a single function (that is, the difference between training and test loss for a function). Rather, we are interested in bounding train loss of one function (a simpler function) with test loss of another (the optimal model in a more complex function class). Standard learning theory analysis handles the single function case nicely; we are concerned with other questions here.

5.1 The True Rashomon Set Can Be Very Helpful… But You Might Not Know When

As in classic Occam’s razor bounds, we start with finite hypothesis spaces. Consider finite hypothesis spaces and , where . Consider the first question discussed above: Given and , can we have a guarantee that a model we produce using a simpler function class on our data could be approximately as good as the test performance of the best model from ? In the following theorem, we will make a key assumption that allows us to do this: we assume that the Rashomon set of includes a member of the simpler class of functions, , even if we do not know which function it is. Later, in Section 5.2, we show conditions under which simple models from are proven to exist in the Rashomon set of , which depends on the size of ’s Rashomon set. Here, denotes the cardinality of the finite space . These bounds can be generalized to infinite hypothesis spaces with a simple extension to covering numbers, but they are designed for intuition, which works nicely with finite hypothesis spaces. Again, this is different from a regular learning theory bound as it does not consider generalization of just one function.

Theorem 5 (The advantage of a true Rashomon set).

Consider finite hypothesis spaces and , such that . Let the loss be bounded by , . Define an optimal function . Assume that the true Rashomon set includes a function from , so there exists a model such that . (Note that we do not know .) In that case, for any with probability at least with respect to the random draw of data:

| (1) |

where . (Unlike , we do know because we can calculate it.)

That is, we can bound the best empirical model from with the true risk of the best model within . Thus, if the Rashomon set is large enough to include a single model from , we can work with the simpler class in practice and achieve strong performance guarantees.

The main assumption in Theorem 5 is about the population, and does not rely on the sample. It relies only on the existence of one special function in the true Rashomon set. There are no smoothness assumptions on the loss function. If the main assumption of this theorem holds, then we gain the benefit of guarantees on from looking only at empirically. We cannot check whether the assumption holds since it involves the true risk, but practitioners can reap the benefits of it anyway: The possibility of a large Rashomon set may embolden the practitioner to minimize over , achieving test error close to the best of if the conditions of Theorem 5 are indeed satisfied.

To make the connection of this result to Rashomon sets more explicit, we will choose a specific relationship between and , specifically, will be a random sample of that is chosen prior to, and separately from, learning. This is an artificial example in that would never actually be chosen as a random sample from in reality. However, the random sampling assumption permits to be distributed fairly evenly within , which, arguably, could approximate the way some simpler spaces are embedded in more complex spaces.

If is a random sample of functions from , and if has a large true Rashomon set, then the true Rashomon set is likely to include at least one model from . In that case, Theorem 5 applies. This is formalized below.

Theorem 6 (Example of the advantage of a large true Rashomon set).

Consider finite hypothesis spaces and , such that and is uniformly drawn from without replacement. For loss bounded by , if the Rashomon ratio is at least

then for any , with probability at least with respect to the random draw of functions from to form and with respect to the random draw of data, the assumptions of Theorem 5 hold and thus the bound (1) holds.

Table 2 shows possible values of the lower bound on the Rashomon ratio, given and . For example, the first line of the table states that if at least a tiny fraction (0.0053%) of the complex function space consists of good models, and there exists at least 100,000 simple functions in , then the chance that we will find an accurate-but-simple model on our data set is over 99%.

The intuition for Theorem 6 holds beyond the case when is randomly sampled from , it holds whenever covers sufficiently well. This intuition is that as the true Rashomon ratio increases, it is more likely that the empirical risk minimum of will be close to the minimum of the true risk of .

| If then to get the bound (1) to hold with probability at least 99% |

| the Rashomon ratio should be . |

| If then to get the bound (1) to hold with probability at least 99% |

| the Rashomon ratio should be . |

| If then to get the bound (1) to hold with probability at least 99% |

| the Rashomon ratio should be . |

5.2 Proving the Existence of Simple-yet-Accurate Models with Good Generalization

Theorems 5 and 6 do not take advantage of the fact that we can investigate empirically, and more easily than we can investigate ; these theorems instead only discuss exploration of . Thus, the next analysis makes two improvements: (1) it studies empirical Rashomon sets instead of true Rashomon sets, (2) it substitutes the unrealistic random draw assumption for a realistic smoothness assumption. We now assume smoothness of the loss over the function space.

The field of Approximation Theory provides general conditions under which classes of functions can approximate each other. Given a target function from one class, we want to know whether a sequence of functions from another class can converge to the target. Table 3 in Appendix C.4 shows classes of functions that can be approximated by classes . For instance, piecewise constant functions, such as decision trees, can approximate smooth functions.

For a hypothesis space and some , define the -ball of functions centered at as A loss is said to be K-Lipschitz, , if for all and for all : The -norm can be defined, for example, as , where is a measure on . Define a -packing as a finite set such that , meaning that for all . The packing number is the largest -packing.

Theorem 7 below uses the approximating set argument from the previous subsection, but now requires the Rashomon set to be large enough to include balls of functions rather than using the random draw assumption. As long as the set of simpler functions is distributed well among the full hypothesis space, each ball contains at least one function from the simpler class.

Theorem 7 (Existence of multiple simpler models).

For -Lipschitz loss bounded by , consider hypothesis spaces and , . With probability greater than w.r.t. the random draw of training data, if for every model there exists such that , then there exists at least functions such that:

-

1.

They are from the simpler space: .

-

2.

for all , where is the Rademacher complexity of a hypothesis space . (This is from standard learning theory.)

From Theorem 7, we see that since larger Rashomon sets have larger packing numbers, they contain more simpler models with good generalization guarantees. Note that in Theorem 7, other complexity measures from learning theory could be used. We chose Rademacher complexity as it provides the tightest bound among standard complexity measures.

Theorem 7 has practical implications. If the Rashomon set is large, and the smoothness conditions are obeyed, Theorem 7 shows that many simple-yet-accurate models would exist, prior to actually finding them. Knowledge that simple models exist implies it will be worthwhile to actually solve the difficult optimization problem to find a simple model.

Thus, if the Rashomon set is large, we have a guarantee. But how will we know when is the Rashomon set large? This is what we answer in the next section.

6 Larger Rashomon Ratios Correlate with Similar Performance of Machine Learning Algorithms, and Good Generalization

We expect that in many real-world applications of machine learning, properties similar to the assumptions behind our theorems hold, i.e., that large enough Rashomon sets intersect simpler hypothesis spaces in ways that lead to or explain good performance. This conjecture is difficult to verify theoretically because it is not a mathematical conjecture about the structure of two specific function spaces, but a statement about many function spaces, and how they interact with commonly occurring data sets. Thus, we consider this question empirically.

Our experiments will demonstrate that, in the case where Rashomon sets are large, two conclusions follow that are consistent with our theoretical development. First, training performance in simpler hypothesis spaces is correlated with test performance in the more complex hypothesis spaces (Theorem 5), and second, that good training performance in a simpler space correlates with good generalization performance of other models in the more complex space . Most importantly, our experiments suggest an intriguing alternative to the often difficult computational problem of directly estimating the size of the Rashomon set, namely that similar performance across a range of algorithms with different hypothesis spaces is strongly correlated with a large Rashomon set.

Now we will describe our experimental setup for arriving at these conclusions.

6.1 Experimental Design

Data sets.

We used 38 machine learning classification data sets from the UCI Machine Learning Repository (Dua and Graff, 2019), among which 16 have categorical features and 22 have real-valued features. The majority of the data sets are binary classification data sets and we adapted the rest to binary classification (as shown in Table 4 in Appendix D) to make importance sampling easier (as discussed in Appendix E). The number of features varies from 3 to 784, with the majority of the data sets being in the 15–25 feature range. Appendix D contains a description of the data sets we considered.

Definition of complex hypothesis space.

For these experiments, we will consider to be the union () of the hypothesis spaces of five popular machine learning algorithms: logistic regression (LR), CART, random forests (RF), gradient boosted trees (GBT), and support vector machines with RBF kernels (SVM). CART, RF and GBT were regularized by varying the tree depth, the minimum number of samples required to split a node, the minimum number of samples required to create a leaf node, and the number of trees in the ensemble. SVMs were tuned by varying the regularization parameter and the kernel coefficient and LR by varying the regularization parameter. Appendix E discusses the effect of regularization on the model class. We chose algorithms that search hypothesis spaces of different complexity to ensure that these algorithms produce diverse models. The notion of as a union of hypothesis spaces may seem surprising at first, but it is consistent with how many machine learning practitioners approach problems by running a collection of machine learning techniques in parallel and comparing the results, creating a de facto union space. Our experiment has three steps, as follows.

Step 1: Run all machine learning algorithms.

We obtain training and generalization performance from all algorithms (logistic regression, CART, random forests, gradient boosted trees, and SVM with RBF kernels) on all data sets.

Step 2: Estimate the size of the Rashomon set.

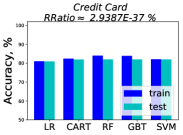

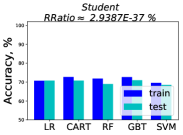

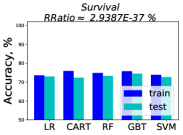

It is not possible to measure the Rashomon set of such a complex model space, so we will estimate its size by sampling from an approximating set, which is decision trees of bounded depth. Decision trees are easy to sample and can refine an input space arbitrarily finely as tree depth increases. With sufficient depth they can approximate many other types of hypothesis spaces, including those used by other machine learning methods. Thus, we will measure the size of the Rashomon set and Rashomon ratio in decision trees of depth seven as a surrogate for measuring these quantities in . The suitability of these trees for this role is an empirical observation about the data sets we have used; they may not be a suitable surrogate for some other data sets, e.g., imagery data. We measure the size of the empirical Rashomon ratio as a surrogate for the true Rashomon ratio when referring to Theorem 5. To estimate the Rashomon ratio of depth seven decision trees, we used importance sampling. The proposal distribution assigns the correct labels to the leaves of the tree based on the training data. Since the data are populated on a bounded domain, to grow a tree up to a depth fully, we make splits. For each data set and each depth, we average our results over ten folds for data sets with less than 200 points and over five folds for data sets with more than 200 points, and we sample 250,000 decision trees per fold. We choose the Rashomon parameter to be 5%, and, therefore, all the models in the Rashomon set have empirical risk not more than , where is the lowest achievable empirical risk across all algorithms we considered. We further discuss experimental setup in Appendix E.

Step 3: See if a large Rashomon Set in Step 2 correlates with performance differences in Step 1.

By construction, the hypothesis spaces of each of the machine learning algorithms we consider are embedded in . RF and GBT both enjoy extremely rich hypothesis spaces that are likely close in size to itself. LR and CART are less expressive than these others, so we will view LR and CART as simpler, type, hypothesis spaces. Our question to answer is whether a large Rashomon set measured in Step 2 correlates with the functions from (CART, LR) having performance as good as that of (GBT, RF, SVM) as our theory predicts it will.

6.2 Experimental Results

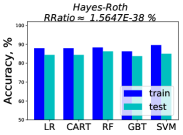

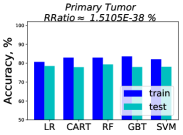

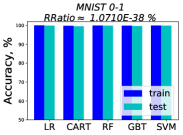

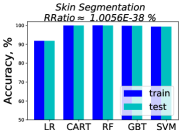

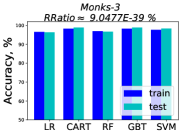

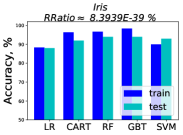

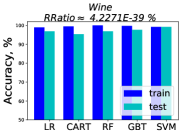

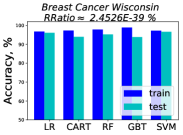

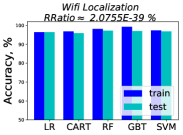

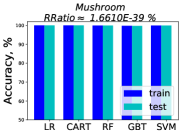

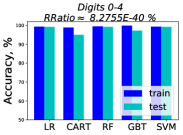

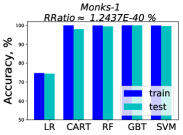

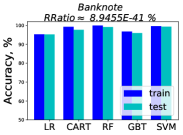

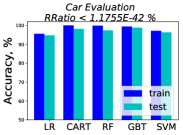

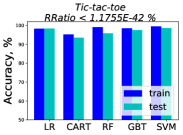

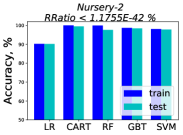

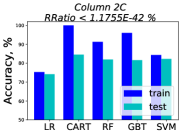

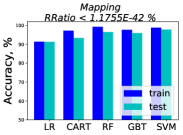

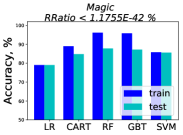

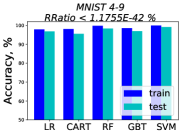

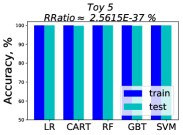

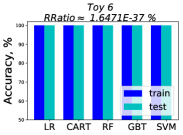

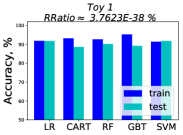

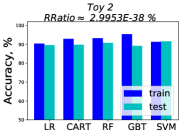

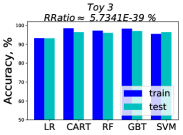

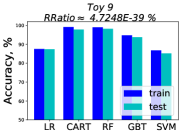

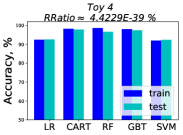

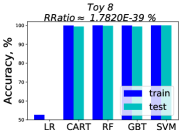

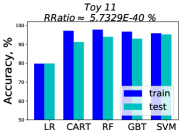

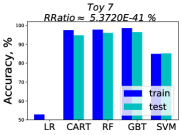

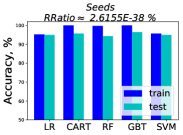

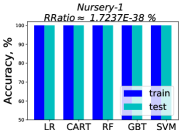

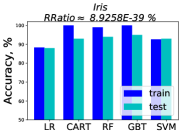

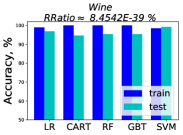

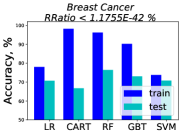

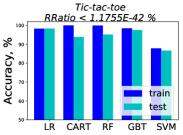

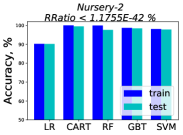

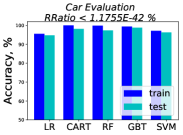

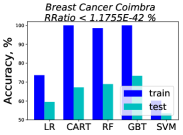

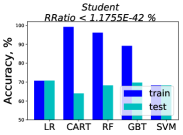

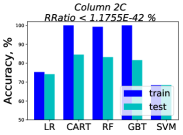

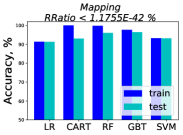

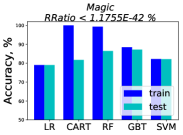

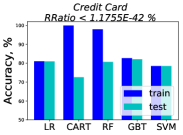

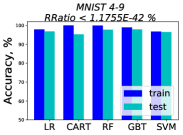

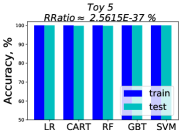

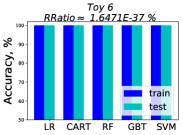

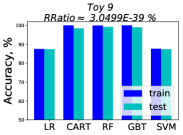

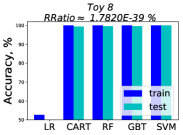

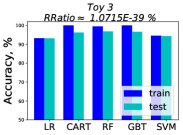

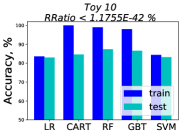

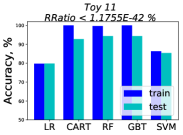

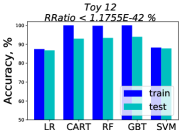

|

|

|

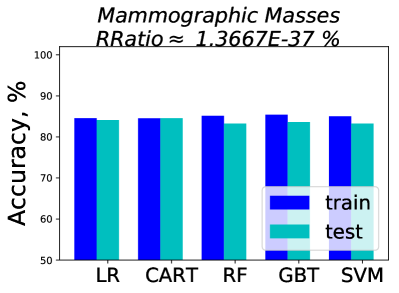

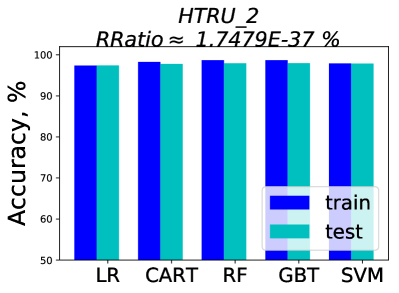

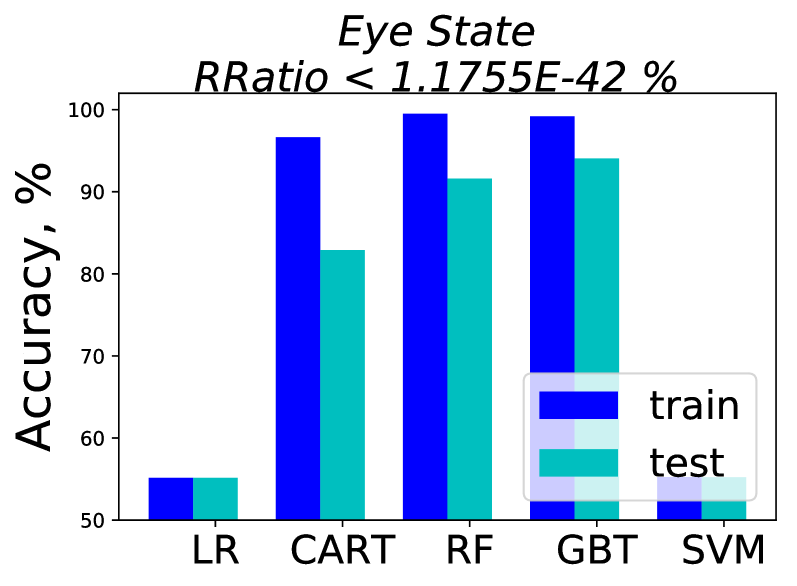

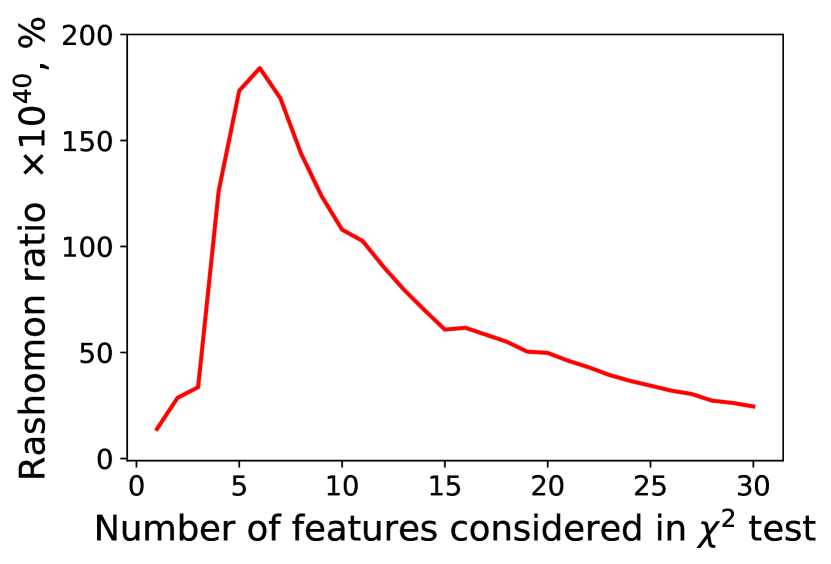

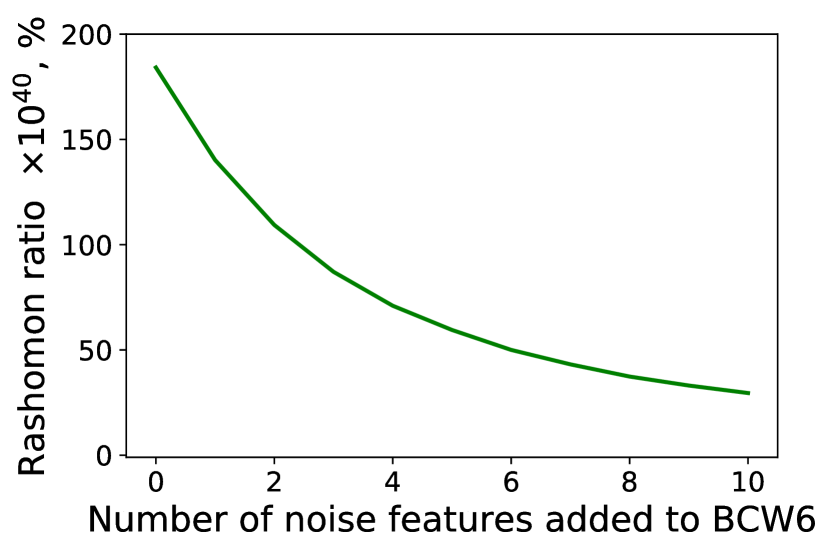

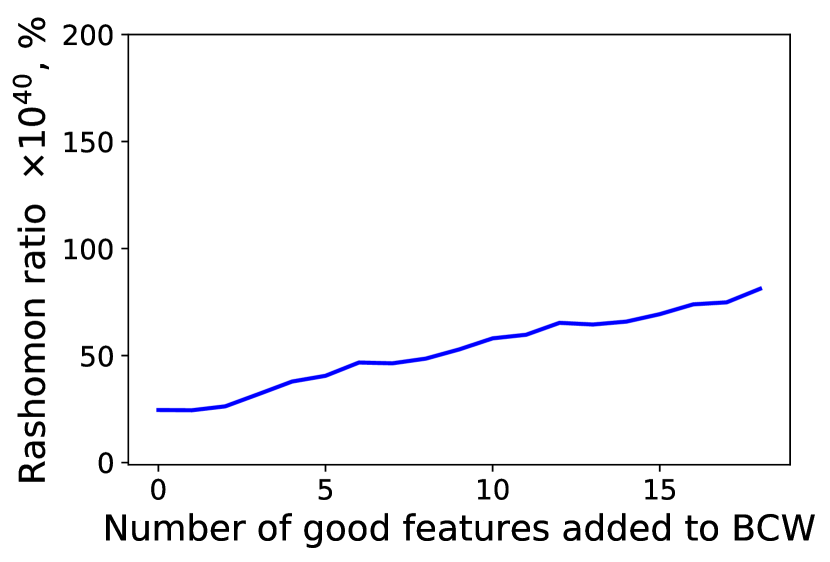

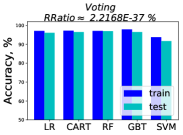

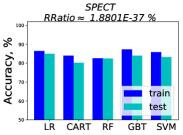

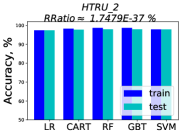

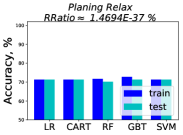

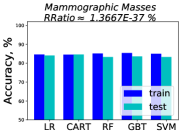

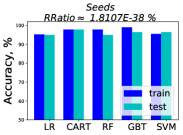

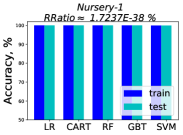

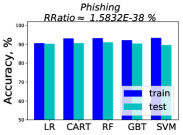

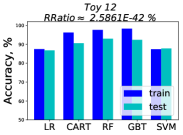

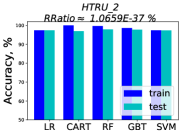

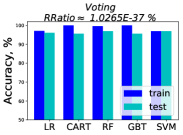

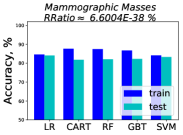

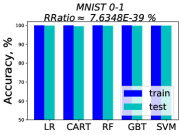

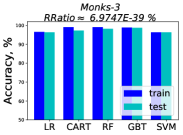

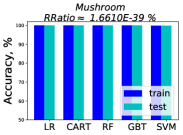

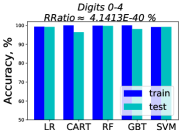

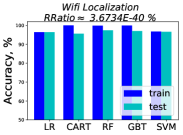

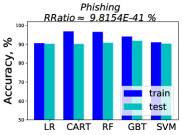

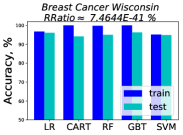

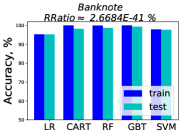

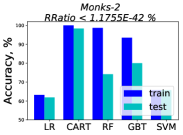

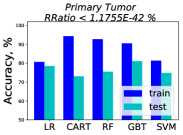

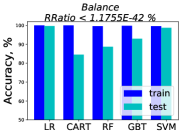

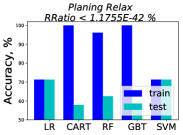

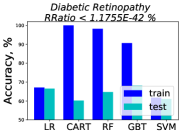

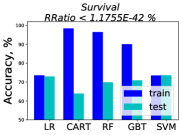

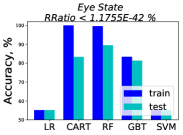

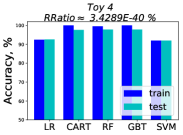

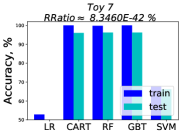

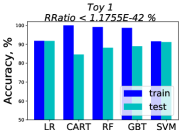

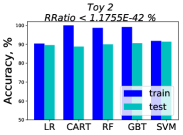

Figure 5(a) shows the performance of the five machine learning algorithms on data sets for which the Rashomon ratio was largest, as measured in the space of decision trees of depth 7. Performance for all data sets is shown in Figures 17 and 18 in Appendix E. Across the 38 data sets considered, we observe larger Rashomon ratios led to approximately similar training results across all algorithms (within difference between algorithms). Here, large Rashomon ratios are on the order of or , whereas small Rashomon ratios are or less222For other data sets and other metrics of measuring the Rashomon set, the results might be different.. Moreover, all of the models chosen by the algorithms, including simpler type models, generalized well (the differences between training and test errors are within ). These results are consistent with our thesis that larger Rashomon sets lead to the existence of accurate-yet-simpler models (in agreement with the theory in Section 5.1), and that larger Rashomon sets lead to better generalization. The results also imply that large Rashomon sets do occur in many data sets, with the Rashomon effect being large enough to include simpler models in practice (in agreement with Section 5.2).

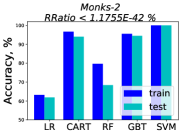

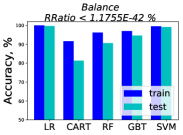

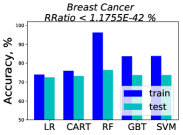

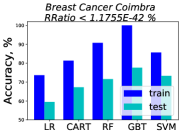

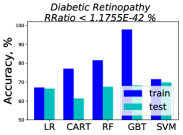

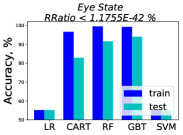

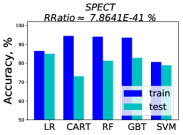

Interestingly, the converse statement, that similar performance across different algorithms should lead to large Rashomon sets, does not always hold; sometimes, generalization occurs with small Rashomon ratios (see Figure 5(b)). This observation could be explained in several different ways. Mainly, the Rashomon ratio is not the only driver of good generalization performance. The amount of data is one obvious additional driver. Appendix F discusses this further. Quality of features is another driver, as discussed in Appendix G.

Our second main result is that in all cases where large Rashomon ratios were observed, test performance was consistent with training performance across algorithms of varying complexity. This correlation between the size of the Rashomon ratio and consistent generalization performance suggests an indirect means of assessing the size of the Rashomon ratio as an alternative to the computationally intensive approach of sampling. When consistent training and test performance across algorithms is observed, this may indicate a large Rashomon ratio.

One thing we notably did not observe were cases where algorithms did not generalize, performance differed across algorithms, and the Rashomon set was large. Across all 38 data sets, we did not observe cases where the Rashomon set was large and performance differed among algorithms.

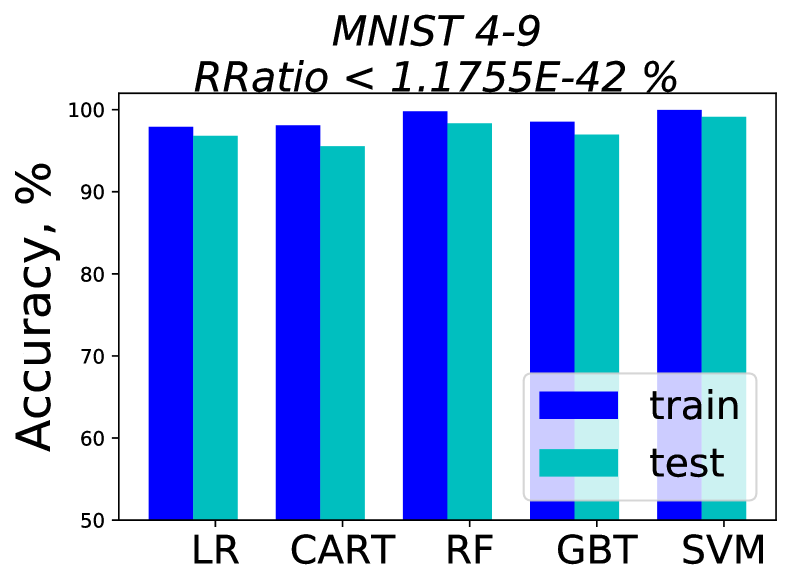

Figure 5(c) shows small Rashomon sets, where we observe wildly different performance across algorithms, where sometimes the models generalize and sometimes they do not. We show one example of each of these cases in Figure 5(c). Our theory does not apply to the case of small Rashomon sets, and thus there is no guarantee for such data sets.

7 Rashomon Sets in the Presence of Noise

We have seen that we can empirically determine whether a data set is likely to have a large Rashomon set: as we showed, we simply run many algorithms, and if they all perform similarly and generalize, there could be a large Rashomon set. But what about before examining the data? Could we know, just from understanding what kind of data set it is, whether it is likely to have a large Rashomon set? We aim to answer this now.

A typical reason given for “underspecification” D’Amour et al. (2020) (i.e., a large number of approximately-equally good models, a large Rashomon set) is the presence of substantial noise in the data. Intuitively, for data whose outcomes are essentially a random guess, it makes sense that no model would perform well, and many models would be equally poor. But what about more interesting cases? Does this intuition still hold? First, as we have shown above, large Rashomon sets exists for non-noisy data sets as well (see Figure 5 Voting and HTRU 2 data sets); it is not just noise that determines the Rashomon set. Second, it is not true that the Rashomon set always gets much larger under noise. In fact, if we add random classification noise Angluin and Laird (1988); Natarajan et al. (2013) (each label is flipped independently with some small probability), it is possible that the Rashomon set does not change at all. This is because the error rate of all models in the Rashomon set (assuming they are all better than random guessing) increases by the same amount in expectation. At least, as we show in Theorem 8, the size of the true Rashomon set does not decrease if we add random classification noise.

Theorem 8 (Expected size of the true Rashomon set cannot decrease under random classification noise).

Consider hypothesis space , data distribution , where, as before, , and . Let be a probability with which each label is flipped independently, and denotes the noisy version of . If the loss function is , then in expectation, the true Rashomon set over is a subset of the true Rashomon set over , .

In Theorem 8 we have shown that the size of the true Rashomon set does not decrease when adding random classification noise, but to prove that , we would need at least one model such that , yet , and such a model may not actually exist; in fact, if all models have increased error rates when noise is added, it does not.

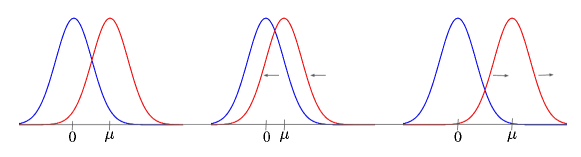

We still are left with finding a scenario where noise does impact the size of the Rashomon set in order to provide some proof to the intuition. Let us consider the setting of linear (Gaussian) discriminant analysis, where the data arise from two Gaussians, one with positive labels and one with negative labels. Instead of increasing label noise, we will increase feature noise by increasing the variances or changing the means of the Gaussians, making the two distributions overlap. In this case, will the Rashomon set increase in size? The answer to this question is conjectured in Conjecture 9.

Conjecture 9 (The Rashomon set can increase with feature noise).

Consider data distribution , where, , , and classes are balanced and generated by Gaussian distributions , , where . For the hypothesis space , where , , and , and the Rashomon parameter :

-

(I)

The volume of the Rashomon set is , where and are the two solutions to Eqn. (2), where is the CDF of the standard normal:

(2) -

(II)

We conjecture that333The hypothesis space for Part II conservatively includes all reasonable candidates for the empirical risk minimizer. In other words, we assume that decision boundary can be anywhere between the means of the two distributions. for , as we add feature noise to the data set by increasing the standard deviation , for all such that , the volume of the Rashomon set increases as a function of .

-

(III)

Consider the setting where for both Gaussians, and we add or remove noise by moving the means and of the Gaussians towards or away from each other. For any , the volume of the Rashomon set is minimized when . Moving the Gaussians either away from or towards each other increases the volume of the Rashomon set.

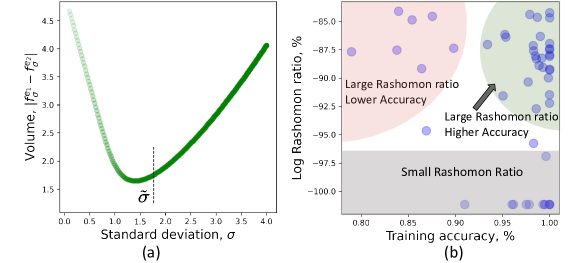

This conjecture is not a theorem because there is no analytical solution to the minimizer of the volume of the Rashomon set; the calculations are quite complex, involving differences of the CDF values of different Gaussians. However, all parts of the conjecture have been fully checked numerically. In part (II), we use an analytical derivation and exhaustive numerical computations to show that the derivatives of the left side of Eqn. (2) are either positive or negative sign. For part (III), we transpose the left Gaussian to to form a canonical problem in which all possible solutions can be computed numerically. We exhaustively search over the range of , finding the optimal and volume of the Rashomon set for each . We find that is very close to 2 for all . We discuss this in Appendix I.

This conjecture suggests that data that are approximately distributed according to two normal distributions, where the positive and negative normal distributions substantially overlap, will have a large Rashomon set. Figure 6(a) shows the dependence of the Rashomon set on the noise level for and . Figure 6(b) plots maximum accuracy versus Rashomon ratio for 38 data sets considered in Section 6. These figures indicate that large Rashomon sets occur both in noisy and non-noisy data.

There can be many data sets with characteristics as in Conjecture 9. For example, let us consider criminal recidivism data, whose Rashomon sets have been studied Fisher et al. (2019); Dong and Rudin (2020) and that admit simple-yet-accurate models Zeng et al. (2017); Rudin et al. (2020). Each data point is generated based on a set of random events happening in the world; whether someone enters a job training program, whether someone associates with criminal associates after release, and whether someone commits a crime each day are all random variables whose random effects are cumulative over time, and thus could be modeled by Gaussians by the central limit theorem. By this logic, we would expect many criminal recidivism prediction problems to admit large Rashomon sets. Other high-stakes predictions such as loan defaults may have similar characteristics.

In a sense, this full analysis paints a much clearer picture as to why such problems admit simple yet similarly accurate models: their distributions are approximately Gaussian with significant overlap, such overlap leads to large Rashomon sets, and large Rashomon sets lead to the existence of simple yet similarly accurate models.

8 Conclusion and Implications

We have proposed Rashomon sets and ratios as another perspective on the relationship between hypothesis spaces and data sets, and we have provided initial theoretical and experimental results showing that this is a unique perspective that may help explain some phenomena observed in practice. More specifically, the main conclusions include: (1) Large Rashomon sets can embed models from simpler hypothesis spaces (Section 5); (2) Similar performance across different machine learning algorithms may correlate with large Rashomon sets (Section 6); (3) Large Rashomon sets correlate with existence of models that have good generalization performance (Section 6); (4) The Rashomon ratio is a measure of a learning problem’s complexity (Section 4), and that data that approximately arise from overlapping Gaussian distributions tend to have large Rashomon sets (Section 7).

Consider a researcher conducting a standard set of machine learning experiments in which the performance of several different algorithms are compared, and generalization is assessed. In the possible scenario where all algorithms perform similarly, and when their models tend to generalize well on validation data, the learning problem is likely to have a large Rashomon set. Based on the result in Section 5, simpler models are likely to exist in a large Rashomon set. If the researcher is interested in simpler models, they can search the simpler function class , a subset of the larger class , to locate simpler models within it. While optimizing for simplicity or interpretability constraints is usually much more computationally expensive than running standard machine learning algorithms, our thesis is that this search would be likely to succeed in the presence of a large Rashomon set. In the converse case, if the researcher’s algorithms perform differently from each other, the researcher might then select a more complex model class that achieves better performance yet does not overfit. Further, if the researcher knows that the data are likely to have arisen from overlapping Gaussian distributions, the researcher could assume that it is worthwhile to search for a simple model that performs well.

References

- (1)

- Angluin and Laird (1988) Dana Angluin and Philip Laird. 1988. Learning from noisy examples. Machine Learning 2, 4 (1988), 343–370.

- Bartlett et al. (2005) Peter L Bartlett, Olivier Bousquet, Shahar Mendelson, et al. 2005. Local Rademacher complexities. The Annals of Statistics 33, 4 (2005), 1497–1537.

- Bartlett and Mendelson (2002) Peter L Bartlett and Shahar Mendelson. 2002. Rademacher and Gaussian complexities: Risk bounds and structural results. Journal of Machine Learning Research 3, Nov (2002), 463–482.

- Belkin et al. (2019) Mikhail Belkin, Daniel Hsu, Siyuan Ma, and Soumik Mandal. 2019. Reconciling modern machine-learning practice and the classical bias–variance trade-off. Proceedings of the National Academy of Sciences 116, 32 (2019), 15849–15854.

- Bousquet and Elisseeff (2002) Olivier Bousquet and André Elisseeff. 2002. Stability and generalization. Journal of Machine Learning Research 2, Mar (2002), 499–526.

- Breiman et al. (2001) Leo Breiman et al. 2001. Statistical modeling: The two cultures (with comments and a rejoinder by the author). Statist. Sci. 16, 3 (2001), 199–231.

- Burges (1998) Christopher JC Burges. 1998. A tutorial on support vector machines for pattern recognition. Data Mining and Knowledge Discovery 2, 2 (1998), 121–167.

- Cao et al. (2008) Feilong Cao, Tingfan Xie, and Zongben Xu. 2008. The estimate for approximation error of neural networks: A constructive approach. Neurocomputing 71, 4-6 (2008), 626–630.

- Chaudhari et al. (2019) Pratik Chaudhari, Anna Choromanska, Stefano Soatto, Yann LeCun, Carlo Baldassi, Christian Borgs, Jennifer Chayes, Levent Sagun, and Riccardo Zecchina. 2019. Entropy-SGD: Biasing gradient descent into wide valleys. Journal of Statistical Mechanics: Theory and Experiment 2019, 12 (2019), 124018.

- Coker et al. (2021) Beau Coker, Cynthia Rudin, and Gary King. 2021. A theory of statistical inference for ensuring the robustness of scientific results. Management Science 67 (2021), 5969–6627. Issue 10.

- Cortes and Vapnik (1995) Corinna Cortes and Vladimir Vapnik. 1995. Support-vector networks. Machine learning 20, 3 (1995), 273–297.

- Coston et al. (2021) Amanda Coston, Ashesh Rambachan, and Alexandra Chouldechova. 2021. Characterizing fairness over the set of good models under selective labels. In Proceedings of the 38th International Conference on Machine Learning (Proceedings of Machine Learning Research).

- D’Amour et al. (2020) Alexander D’Amour, Katherine Heller, Dan Moldovan, Ben Adlam, Babak Alipanahi, Alex Beutel, Christina Chen, Jonathan Deaton, Jacob Eisenstein, Matthew D Hoffman, et al. 2020. Underspecification presents challenges for credibility in modern machine learning. arXiv preprint arXiv:2011.03395 (2020).

- Davydov (2011) Oleg Davydov. 2011. Algorithms and error bounds for multivariate piecewise constant approximation. In Approximation Algorithms for Complex Systems. Vol. 3. Springer, Berlin, Heidelberg, 27–45.

- DeVore (1998) Ronald A DeVore. 1998. Nonlinear approximation. Acta Numerica 7 (1998), 51–150.

- Dinh et al. (2017) Laurent Dinh, Razvan Pascanu, Samy Bengio, and Yoshua Bengio. 2017. Sharp minima can generalize for deep nets. In Proceedings of the 34th International Conference on Machine Learning (Proceedings of Machine Learning Research, Vol. 70). 1019–1028.

- Dong and Rudin (2020) Jiayun Dong and Cynthia Rudin. 2020. Exploring the cloud of variable importance for the set of all good models. Nature Machine Intelligence 2, 12 (2020), 810–824.

- Dua and Graff (2019) Dheeru Dua and Casey Graff. 2019. UCI Machine Learning Repository. University of California, Irvine, School of Information and Computer Sciences.

- Fisher et al. (2019) Aaron Fisher, Cynthia Rudin, and Francesca Dominici. 2019. All models are wrong, but many are useful: Learning a variable’s importance by studying an entire class of prediction models simultaneously. Journal of Machine Learning Research 20, 177 (2019), 1–81.

- Hochreiter and Schmidhuber (1997) Sepp Hochreiter and Jürgen Schmidhuber. 1997. Flat minima. Neural Computation 9, 1 (1997), 1–42.

- Kakade et al. (2008) Sham M. Kakade, Karthik Sridharan, and Ambuj Tewari. 2008. On the complexity of linear prediction: risk bounds, margin bounds, and regularization. In Proceedings of the 21st International Conference on Neural Information Processing Systems (Vancouver, British Columbia, Canada) (NIPS’08). Curran Associates Inc., Red Hook, NY, USA, 793–800.

- Kearns and Ron (1999) Michael Kearns and Dana Ron. 1999. Algorithmic stability and sanity-check bounds for leave-one-out cross-validation. Neural Computation 11, 6 (1999), 1427–1453.

- Keskar et al. (2016) Nitish Shirish Keskar, Dheevatsa Mudigere, Jorge Nocedal, Mikhail Smelyanskiy, and Ping Tak Peter Tang. 2016. On large-batch training for deep learning: Generalization gap and sharp minima. arXiv preprint arXiv:1609.04836 (appeared at ICLR 2017) (2016).

- Koltchinskii and Panchenko (2002) Vladimir Koltchinskii and Dmitry Panchenko. 2002. Empirical margin distributions and bounding the generalization error of combined classifiers. The Annals of Statistics 30, 1 (2002), 1–50.

- Langford and Shawe-Taylor (2002) John Langford and John Shawe-Taylor. 2002. PAC-Bayes & margins. In Proceedings of the 15th International Conference on Neural Information Processing Systems (NIPS’02). MIT Press, Cambridge, MA, USA, 439–446.

- Lecué (2011) Guillaume Lecué. 2011. Interplay between concentration, complexity and geometry in learning theory with applications to high dimensional data analysis. Ph.D. Dissertation. Université Paris-Est.

- Letham et al. (2016) Benjamin Letham, Portia A. Letham, Cynthia Rudin, and Edward Browne. 2016. Prediction uncertainty and optimal experimental design for learning dynamical systems. Chaos 26, 6 (2016).

- Lugosi and Wegkamp (2004) Gábor Lugosi and Marten Wegkamp. 2004. Complexity regularization via localized random penalties. The Annals of Statistics 32, 4 (2004), 1679–1697.

- Madras et al. (2019) David Madras, James Atwood, and Alex D’Amour. 2019. Detecting underspecification with local ensembles. arXiv preprint arXiv:1910.09573 (appeared at ICLR 2020 under the title “Detecting Extrapolation with Local Ensembles”) (2019).

- Manwani and Sastry (2013) Naresh Manwani and PS Sastry. 2013. Noise tolerance under risk minimization. IEEE Transactions on Cybernetics 43, 3 (2013), 1146–1151.

- Marx et al. (2020) Charles Marx, Flavio Calmon, and Berk Ustun. 2020. Predictive Multiplicity in Classification. In Proceedings of the 37th International Conference on Machine Learning (Proceedings of Machine Learning Research, Vol. 119). PMLR, 6765–6774.

- Meinshausen and Bühlmann (2010) Nicolai Meinshausen and Peter Bühlmann. 2010. Stability selection. Journal of the Royal Statistical Society: Series B (Statistical Methodology) 72, 4 (2010), 417–473.

- Mendelson (2003) Shahar Mendelson. 2003. A few notes on statistical learning theory. In Advanced Lectures on Machine Learning. Springer, 40 pages.

- Nakkiran et al. (2021) Preetum Nakkiran, Gal Kaplun, Yamini Bansal, Tristan Yang, Boaz Barak, and Ilya Sutskever. 2021. Deep double descent: Where bigger models and more data hurt. Journal of Statistical Mechanics: Theory and Experiment 2021, 12 (2021), 124003.

- Natarajan et al. (2013) Nagarajan Natarajan, Inderjit S Dhillon, Pradeep K Ravikumar, and Ambuj Tewari. 2013. Learning with noisy labels. In Advances in Neural Information Processing Systems, C. J. C. Burges, L. Bottou, M. Welling, Z. Ghahramani, and K. Q. Weinberger (Eds.), Vol. 26. Curran Associates, Inc.

- Nevo and Ritov (2017) Daniel Nevo and Ya’acov Ritov. 2017. Identifying a minimal class of models for high-dimensional data. The Journal of Machine Learning Research 18, 1 (2017), 797–825.

- Newman and Rivlin (1976) DJ Newman and TJ Rivlin. 1976. Approximation of monomials by lower degree polynomials. Aequationes Mathematicae 14, 3 (1976), 451–455.

- Paturi (1992) Ramamohan Paturi. 1992. On the degree of polynomials that approximate symmetric boolean functions (preliminary version). In Proceedings of the Twenty-Fourth Annual ACM Symposium on Theory of Computing (Victoria, British Columbia, Canada) (STOC ’92). Association for Computing Machinery, New York, NY, USA, 468–474.

- Rogers and Wagner (1978) William H Rogers and Terry J Wagner. 1978. A finite sample distribution-free performance bound for local discrimination rules. The Annals of Statistics 6, 3 (1978), 506–514.

- Rudin (2019) Cynthia Rudin. 2019. Stop explaining black box machine learning models for high stakes decisions and use interpretable models instead. Nature Machine Intelligence 1, 5 (2019), 206–215.

- Rudin et al. (2020) Cynthia Rudin, Caroline Wang, and Beau Coker. 2020. The Age of Secrecy and Unfairness in Recidivism Prediction. Harvard Data Science Review 2, 1 (31 1 2020).

- Schapire et al. (1998) Robert E Schapire, Yoav Freund, Peter Bartlett, Wee Sun Lee, et al. 1998. Boosting the margin: A new explanation for the effectiveness of voting methods. The Annals of Statistics 26, 5 (1998), 1651–1686.

- Srebro et al. (2010) Nathan Srebro, Karthik Sridharan, and Ambuj Tewari. 2010. Smoothness, Low Noise and Fast Rates. In Advances in Neural Information Processing Systems, Vol. 23. Curran Associates, Inc., 2199–2207.

- Tulabandhula and Rudin (2013) Theja Tulabandhula and Cynthia Rudin. 2013. Machine learning with operational costs. The Journal of Machine Learning Research 14, 1 (2013), 1989–2028.

- Tulabandhula and Rudin (2014a) Theja Tulabandhula and Cynthia Rudin. 2014a. On combining machine learning with decision making. Machine Learning (ECML-PKDD journal track) 97, 1-2 (2014), 33–64.

- Tulabandhula and Rudin (2014b) Theja Tulabandhula and Cynthia Rudin. 2014b. Robust optimization using machine learning for uncertainty sets. arXiv preprint arXiv:1407.1097 (2014).

- Ustun and Rudin (2016) Berk Ustun and Cynthia Rudin. 2016. Supersparse linear integer models for optimized medical scoring systems. Machine Learning 102, 3 (2016), 349–391.

- Vapnik and Chervonenkis (1971) VN Vapnik and A Ya Chervonenkis. 1971. On the Uniform Convergence of Relative Frequencies of Events to Their Probabilities. Theory of Probability and its Applications 16, 2 (1971), 264.

- Vapnik (1995) Vladimir N Vapnik. 1995. The Nature of Statistical Learning Theory. Springer.

- Wallace and Boulton (1968) Christopher S Wallace and David M Boulton. 1968. An information measure for classification. Comput. J. 11, 2 (1968), 185–194.

- Zeng et al. (2017) Jiaming Zeng, Berk Ustun, and Cynthia Rudin. 2017. Interpretable classification models for recidivism prediction. Journal of the Royal Statistical Society: Series A (Statistics in Society) 180, 3 (2017), 689–722.

- Zhou (2002) Ding-Xuan Zhou. 2002. The covering number in learning theory. Journal of Complexity 18, 3 (2002), 739–767.

Appendix A Difference between flat minima and Rashomon set

Figure 7 illustrates differences between volume -flatness and the Rashomon set.

Appendix B Connection to Simplicity Measures

We will use demonstrations to show the differences between the Rashomon ratio and other complexity measures mentioned in Section 4. However, first we discuss how to analytically compute the Rashomon ratio for ridge regression since the demonstration of the difference between algorithmic stability and Rashomon ratio relies on it.

B.1 Analytical Calculation of Rashomon Ratio for Ridge Regression

A special case of when the Rashomon ratio can be computed in closed form in a parameter space is ridge regression. For a space of linear models , ridge regression chooses a parameter vector by minimizing the penalized sum of squared errors for a training data set :

| (3) |

where the optimal solution of the ridge regression estimator is

Geometrically, the optimal solution to ridge regression will be a parameter vector that corresponds to the intersection of ellipsoidal isosurfaces of the sum of squares term and a hypersphere centered at the origin, with the regularization parameter determining the trade off between the loss and the radius of the sphere. More generally, isosurfaces of the ridge regression loss function are ellipsoids, and the volume of such an ellipsoid corresponds to the volume of the Rashomon set. For a hypothesis space with uniform prior and volume function , the Rashomon ratio is . Using the geometric intuition above, we compute the Rashomon ratio in the parameter space by the following theorem:

Theorem 10 (Rashomon ratio for ridge regression).

For a parametric hypothesis space of linear models with uniform prior and a data set , the Rashomon set of ridge regression is an ellipsoid, containing vectors such that:

and the Rashomon ratio can be computed as:

| (4) |

where are singular values of matrix , and is the gamma function.

Proof.

Consider all models from the Rashomon set . Then by Definition 1 we get:

| (5) |

Using from the optimal solution of the ridge regression estimator , and expanding the difference between empirical risks we have:

Therefore the Rashomon set is an ellipsoid centered at :

By the formula of the volume of a p-dimensional ellipsoid, the volume of the Rashomon set can be computed as:

where are singular values of .

Since we assume a uniform prior on , is the volume of a box (or other closed region) containing the plausible values of . Therefore, the Rashomon ratio is , where . ∎

Interestingly, from Theorem 10, it follows that for ridge regression, the Rashomon ratio depends on the feature space only and does not depend on the regression targets . Indeed, assume that every parameter vector such that can be represented as . By a simple transformation, we have that , meaning that if we take a step in parameter space, the empirical risk difference will depend only on the feature space and the step itself, and not on the targets of the problem. This observation can help us choose the parameter as if we want to ensure some dependence between the optimal model and a model of interest . Then, by choosing the direction as , we can compute the Rashomon parameter .

For other algorithms, the Rashomon ratio generally depends on the targets; in that sense, ridge regression is unusual.

B.2 Algorithmic Stability

The main motivation for algorithmic stability theory is to ensure robustness of a learning algorithm. Following Bousquet and Elisseeff (2002), we define the hypothesis stability of a learning algorithm as follows.

Definition 11 (Hypothesis stability).

A learning algorithm has hypothesis stability with respect to the loss if for all ,

where , hypothesis is learned by an algorithm on a data set , loss for , data set , and is modified from the training data by removing the th element of the data set: .

The Rashomon ratio is fundamentally different from hypothesis stability, in case of linear least squares regression (which is discussed in Section B.1). This is formalized in Theorem 2.

Theorem 2 (Rashomon ratio is not algorithmic stability).

Consider a distribution over a discrete domain and a learning algorithm that minimizes the sum of squares loss : . for a linear hypothesis space . For any , there exist joint distributions and where for drawn i.i.d. from , drawn from over , and drawn from over , the expected Rashomon ratios are the same:

yet hypothesis stability constants are different by our arbitrarily chosen value of : where and denote data sets and , is the hypothesis stability coefficient of algorithm for distribution and is the hypothesis stability coefficient for distribution .

Proof.

Let us create our distribution. Consider the least squares regression , where , and loss for . For the marginal distribution and drawn i.i.d. from , we design distributions and as:

where is some fixed point with a positive probability and we define later. That is, the two conditional distributions have except when for , when it is with probability 1/2.

As a first part of the proof, we show that the algorithmic stability constants are different. According to the definition of algorithmic stability, for we have:

and for distribution :

where is a special draw such that , and where includes one point at , one point at , and the rest at other values . Since the domain is discrete, the probabilities of a special draw are:

where is a binomial coefficient, namely the probability of getting exactly successes from trials, where each trial has a probability of success . Denote as the probability of getting a special draw, then .

If contains only two points and , the loss difference evaluated at for all will be at least . To see this, note that the optimal function’s value at is: , the optimal function’s value at after we remove the first point is , and the optimal function’s value at after removing the second point is . Therefore, , , . And we get that , . As we add the rest of the points to the data set , the loss difference (from changing to ) in the special draw case will only increase. Therefore for all :

If we choose such that , then from the definition of algorithmic stability we have:

Therefore for any given we get that . This proves that the hypothesis stability constants are different and completes the first part of the proof.

We now need to prove that the expected Rashomon ratios are the same, which will constitute the second part of the proof. The Rashomon ratio for the hypothesis space of linear models does not depend on targets and can be calculated as in (4) for both and . Therefore the expected Rashomon ratios are the same:

Thus, both halves of our proof are complete. ∎

B.3 Geometric Margin

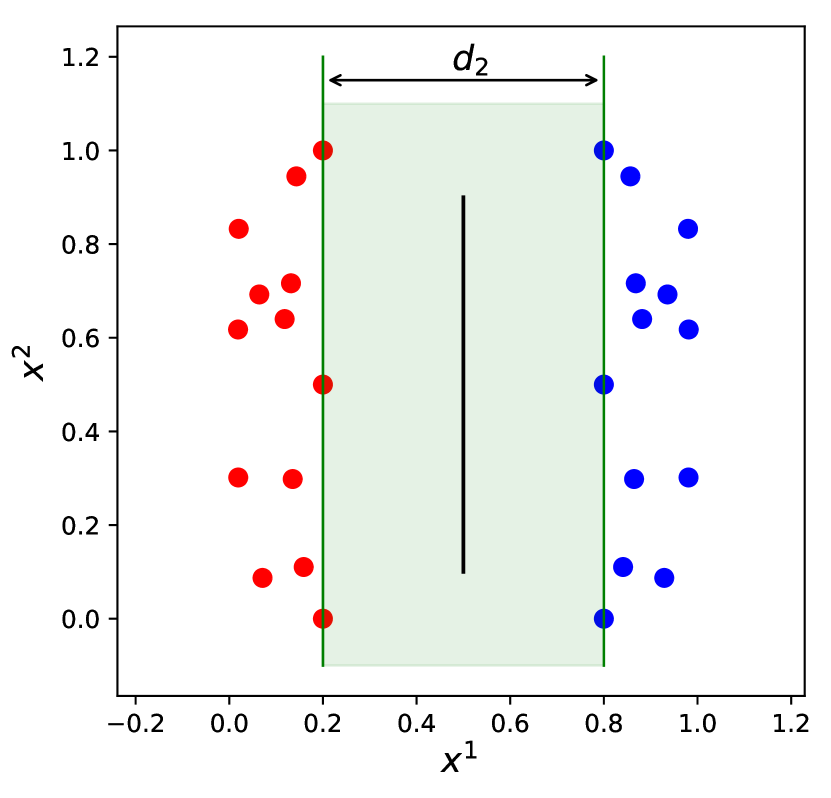

For the parametric hypothesis space of linear models and binary classification, denote and as the shortest distances from a decision boundary to the closest points with targets and respectively. Then the margin is a sum of these distances (Burges, 1998). Moreover, for the model that maximizes the margin, the margin width is .

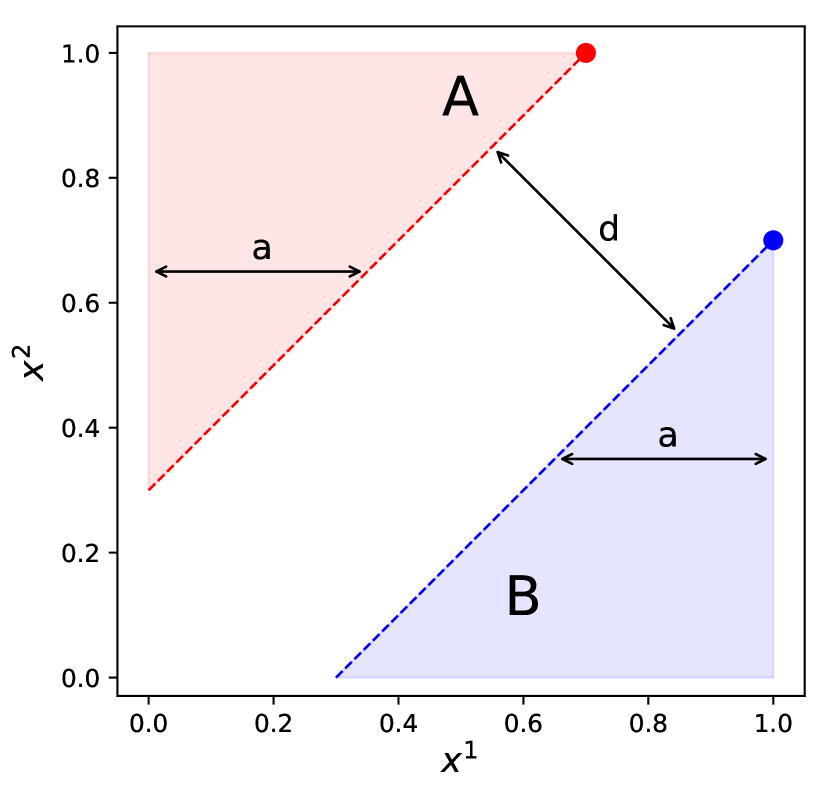

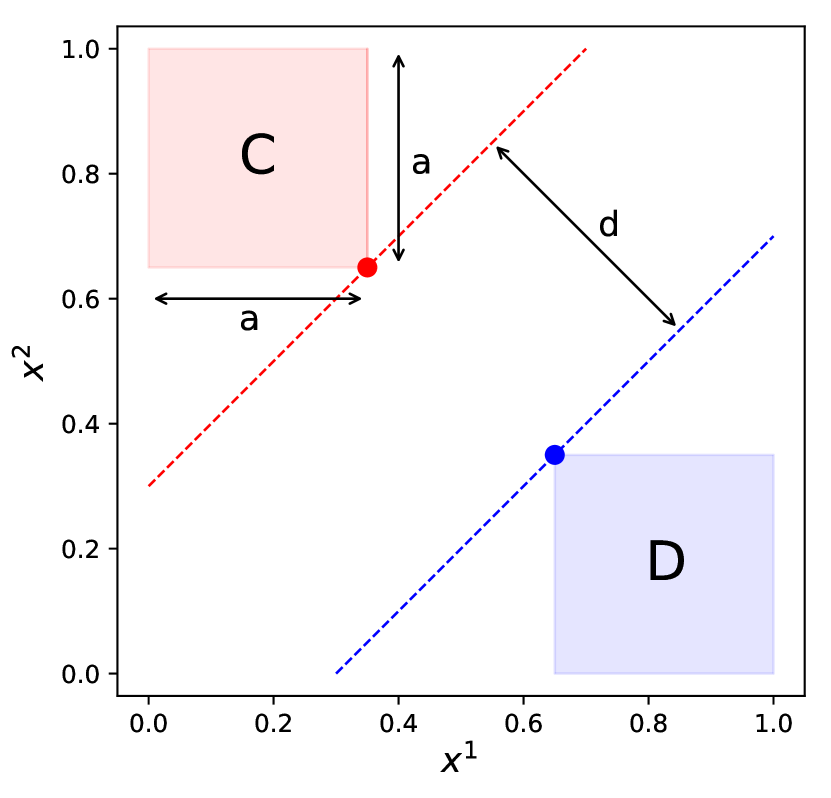

Intuitively both the Rashomon ratio and the width of the geometric margin are data-dependent and show how expressive the hypothesis space is with respect to a given data set. However, the margin depends on support vectors while the Rashomon set depends on the full data set. Theorem 3 summarizes this idea.

Theorem 3 (Rashomon ratio is not the geometric margin).

For any fixed , there exists a fixed hypothesis space , a Rashomon parameter , and there exist two data sets and with the same empirical risk minimizer such that the geometric margin is the same for both data sets, yet the Rashomon ratios are different:

Proof.

Consider two-dimensional separable data, , and a parametrized hypothesis space of origin-centered linear models: . Consider also 0-1 loss and an empirical risk minimizer that maximizes the geometric margin. Since the data are populated in a hypercube, as a hypothesis space we will consider all models that intersect the unit-hypercube.

For some positive constant that we choose later, consider the following regions of the feature space:

Construct data set , such that , where is any sample from the region , is any sample from the region , and are special points for the data set such that and . Please see Figure 8(a) for details.

Construct data set , such that , where is any sample from the region , is any sample from the region , and are special points for the data set such that and . Please see Figure 8(b) for details.

Note that the data sets we considered have the same width for the geometrical margin (see Figures 8(a), 8(b)). Now, we are left to show that the Rashomon ratios are different.

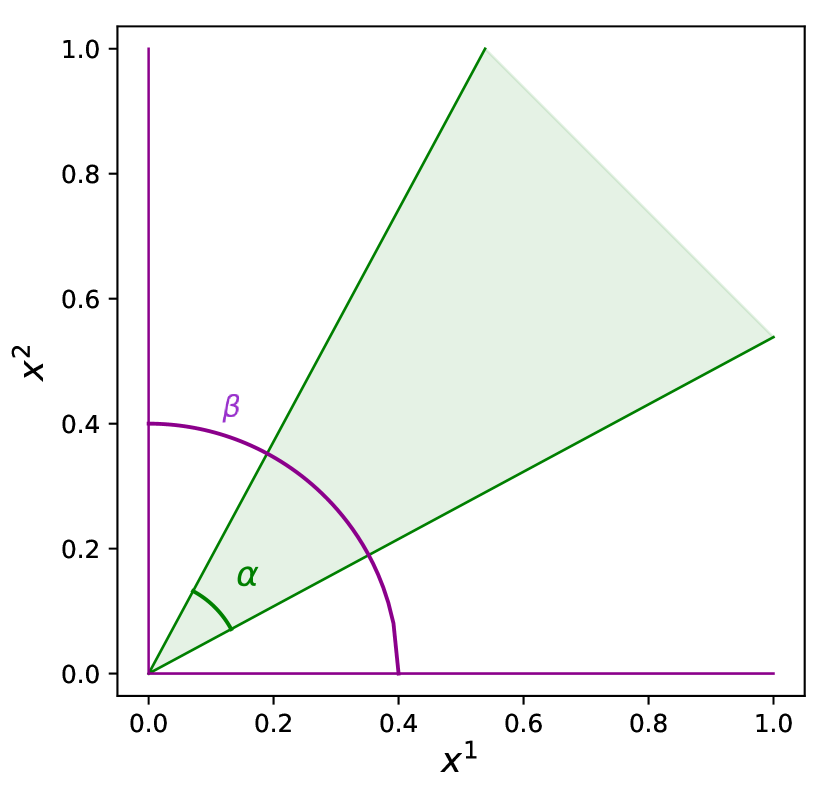

For the hypothesis space of origin-centered lines we have a unique parameterization and a one-to-one correspondence between an actual model and its parameterization. Therefore, if the Rashomon set is a single connected component, an angle between the two most distant models in the Rashomon set gives us some information about the size of the Rashomon set. In particular, we can compute the Rashomon ratio as a ratio of the angle that represents the Rashomon set and the angle that corresponds to the hypothesis space as shown on Figure 8(c). Since the hypothesis space is defined on the unit-hypercube, and for the Rashomon parameter the Rashomon ratio is:

For data sets and Figures 8(d) and 8(e) show the Rashomon set and angles and that represent the volume of the Rashomon set. Given the special points in the data sets we can compute and exactly: and . Then the Rashomon ratios difference is:

Now if we choose and such that , then the Rashomon ratio difference is at least .

∎

B.4 Empirical Local Rademacher Complexity

The empirical Rademacher complexity is another complexity measure of the hypothesis space. Following Bartlett et al. (2005), for binary classification we define it as follows.

Definition 12 (Empirical Rademacher complexity).

Given a data set , and a hypothesis space of real-valued functions, the empirical Rademacher complexity of is defined as:

where are independent random variables drawn from the Rademacher distribution i.e. for .

Since we are interested only in models that are inside the Rashomon set, we will consider local empirical Rademacher complexity (Bartlett et al., 2005), which is defined using the Rashomon set . In the following theorem, we provide a simple example to show the discrepancy between the two measures.

Theorem 4 (Rashomon ratio is not the local Rademacher complexity).

For , there exist two data sets and , a hypothesis space , and a Rashomon parameter such that the local Rademacher complexities defined on the Rashomon sets for and are the same: yet the Rashomon ratios are different:

Proof.

Consider two-dimensional separable symmetric data, , , 0-1 loss with empirical risk minimizer , and a hypothesis space of decision stumps based on the first feature, where for : if , , otherwise. We have a one-to-one correspondence between a function and its threshold parameter . Therefore, if the Rashomon set is a single connected component, we can compute the volume of the Rashomon set in parameter space by computing the difference between the largest and smallest threshold values of models within the Rashomon set, as illustrated in Figure 9(a). For , the difference between the largest and the smallest threshold values will be equivalent to the minimal distance between points of opposite classes projected onto the first feature , where is the projection of point onto first feature.

For the hypothesis space, we consider all decision stumps in the first dimension that are in the segment , where data are populated. The difference in thresholds for the hypothesis space is and therefore . For , the volume of the Rashomon set will be equivalent to —the projected minimal distance between points of opposite classes, and have that and . Now consider any two separable symmetric data sets , with different projected minimal distances and , such that . (Please see Figure 9(c) and 9(d) for details of the data sets and .) Consequently we get that:

For a separable symmetric data and 0-1 loss function, the Rashomon set contains all models that separate data in the same way. Therefore the Rademacher complexity of the Rashomon set is is:

where in the penultimate equality we have used the fact that, in the case of separable data and , all models in the Rashomon set will perform identically on any permutation of the labels.

Equality of the empirical Rademacher complexity of the optimal model to zero follows from the symmetric data considered and symmetrical patterns of all possible target assignments. For example, for the toy data set in Figure 9(b): .

Since both and are separable and symmetric we get that:

∎

Appendix C Proofs for Generalization Results

C.1 Proof of Theorem 5

Given a parameter , we call the Rashomon set with restricted empirical risk an anchored Rashomon set:

We define also the true anchored Rashomon set based on the true risk as follows:

Proposition 13 (True anchored Rashomon set is close to empirical).

For a loss bounded by and for any , and for a fixed , if then with probability at least with respect to the random draw of training data,

Proof.

For a fixed by Hoeffding’s inequality:

Therefore, with probability at least with respect to the random draw of data, .

Since , then by definition of the Rashomon set, . Combining this with Hoeffding’s inequality, we get that with probability at least :

therefore ∎

Proposition 13 is based on the same intuition as Lemma 23 in the work of Fisher et al. (2019), which is used to bound the probability with which a given model is not in the empirical Rashomon set; this is used in a proof of a bound for model class reliance. We use the proposition to indicate the probability with which the empirical anchored Rashomon set is as close as possible to the true anchored Rashomon set for a given model.

Theorem 5 (The advantage of a true Rashomon set).

Consider finite hypothesis spaces and , such that . Let the loss be bounded by , . Define an optimal function . Assume that the true Rashomon set includes a function from , so there exists a model such that . (Note that we do not know .) In that case, for any with probability at least with respect to the random draw of data:

where . (Unlike , we do know because we can calculate it.)

Proof.