1 Introduction

Sensitivity analysis, and particularly sensitivity indices, have became important tools in applied sciences. The aim of sensitivity indices is to quantify the impact of the input variables on the output of a model. This information improves the interpretability of the model. In global sensitivity analysis, the input variables are assumed to be random variables. In this framework, the Sobol indices [33] were the first suggested indices to be applicable to general classes of models. Nevertheless, one of the most important limitations of these indices is the assumption of independence between the input variables. Hence, many variants of the Sobol indices have been suggested for dependent input variables [22, 6, 23, 7].

Recently, Owen defined new sensitivity indices in [26] called "Shapley effects". These sensitivity indices have many advantages over the Sobol indices for dependent inputs [16]. For general models, [34] suggested an estimator of the Shapley effects. However, this estimation requires to be able to generate samples with the conditional distributions of the input variables. A consistent estimator has been suggested in [3], requiring only a sample of the inputs-output. This estimator uses nearest-neighbours methods to mimic the generation of samples with these conditional distributions.

In this paper, we focus on Gaussian linear models in large dimension. Gaussian linear models are widely used as numerical models of physical phenomena (see for example [19, 13, 29]). Indeed, uncertainties are often modelled as Gaussian variables and an unknown function is commonly approximated by its linear approximation around . Furthermore, high-dimensional Gaussian linear models are widely studied in statistics [5, 11].

In this particular case of Gaussian linear models, the theoretical values of the Shapley effects can be computed explicitly [27, 16, 4].

These values depend on the covariance matrix of the inputs and on the coefficients of the linear model.

In this paper, we assume that we observe an i.i.d. sample of the input Gaussian variables in high dimension and that the true covariance matrix and the vector are unknown. In this setting, the Shapley effects need to be estimated, replacing the true vector by its estimation and the theoretical covariance matrix by an estimated covariance matrix.

There exists a fair amount of work on high-dimensional covariance matrix estimation.

Many researchers took an interest in the empirical covariance matrix in high dimension [24, 37, 32, 1]. For particular covariance matrices, different estimators than the empirical covariance can be preferred. For some well-conditioned families of covariance matrices, [2] suggests a banded version of the empirical covariance matrix, and several works address the problem of estimating a sparse covariance matrix [14, 20, 10].

However, in general, given a high-dimensional covariance matrix, the computation cost of the corresponding Shapley effects grows exponentially with the dimension.

The only setting where a procedure to compute the Shapley effect with a non-exponential cost is the setting of block-diagonal matrices

[4].

Hence, in high dimension, block-diagonal covariance matrices are a very favorable setting for the estimation of the Shapley effects. Thus, we address the estimation of high-dimensional block-diagonal covariance matrices in this paper. In contrasts, we remark that the above methods

are not relevant for the estimation of the Shapley effects, since they do not provide block-diagonal matrices.

In our framework, we assume that the true covariance matrix is block-diagonal and we want to estimate this matrix with a similar structure to compute the deduced Shapley effects. Some works address the block-diagonal estimation of covariance matrices. [28] gives a numerical procedure to estimate such covariance matrices and [15] suggests a test to verify the independence of the blocks.

A block-diagonal estimator of the covariance matrix is proposed in [9]. The authors of [9] choose a more general framework, without assuming that the true covariance matrix is block-diagonal.

They obtain the estimated block-diagonal structure by thresholding the empirical correlation matrix. They also give theoretical guaranties by bounding the average of the squared Hellinger distance between the estimated probability density function and the true one. This bound depends on the dimension and the sample size . When converges to some constant , this bound is larger than and is no longer relevant as the Hellinger distance is always smaller than .

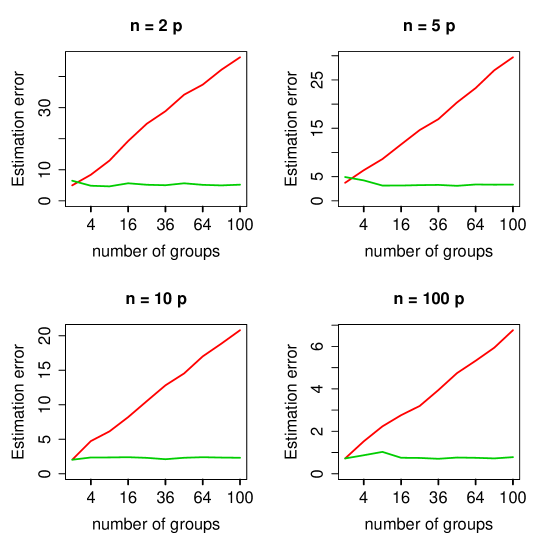

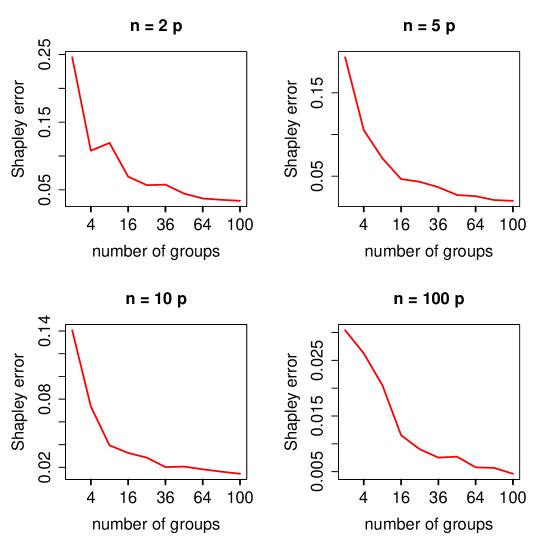

Here, we focus on the high dimension setting, when converges to some constant , and when the true covariance matrix is assumed to be block-diagonal. We give different estimators of the block-diagonal structure and we show that their complexity is small. Then, we provide new asymptotic results for these estimators. Under mild conditions, we show that the estimators of the block structure are equal to the true block structure, with probability converging to one. Furthermore, the square Frobenius distance between the estimated covariance matrices and the true one, normalized by , converge to zero at rate .

Thus, our work complements the one of [9]. We also study the fixed-dimensional setting, where we show that one of our suggested estimators is asymptotically efficient.

From the estimated block-diagonal covariance matrices, we deduce estimators of the Shapley effects in the high-dimensional linear Gaussian framework, with reduced computational cost. We recall that in high dimension, the computation of the Shapley effects requires that the corresponding covariance matrix be block-diagonal. We show that the relative estimation error of these estimators goes to zero at the parametric rate , up to a logarithm factor, even if the linear model is estimated from noisy observations.

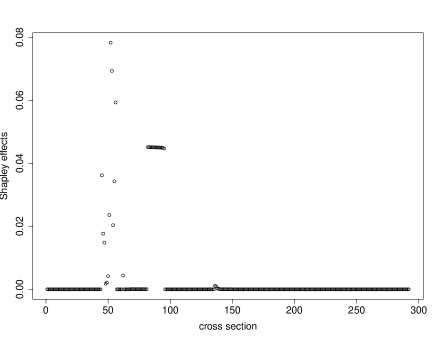

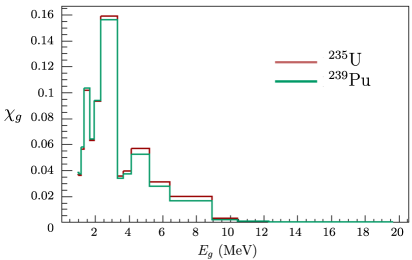

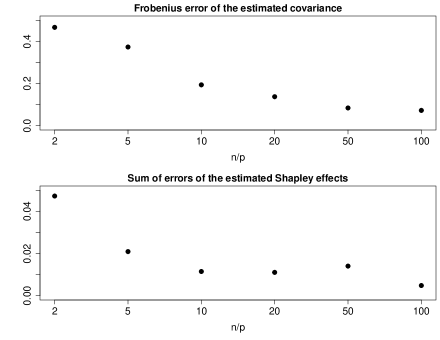

Our convergence results are confirmed by numerical experiments. We also apply our algorithm to semi-generated data from nuclear applications.

The rest of the paper is organized as follows. In Section 2, we focus on the block-diagonal estimation of the block-diagonal covariance matrix. In Section 3, we apply this block-diagonal estimation of the covariance matrix to deduce Shapley effects estimators. Section 4 is devoted to the numerical application on nuclear data, and the conclusion is given in Section 5. All the proofs are postponed to the appendix.

Appendix

We will write for a generic non-negative finite constant (depending only on , and in Conditions 2 and 3). The actual value of is of no interest and can change in the same sequence of equations. Similarly, we will write for a generic strictly positive constant.

If , and , we will wite if and , that is, if and are in the same group with the partition and are in different groups with the partition .

If , we define as the maximal partition such that and .

If (the set of the matrices of dimension ), and if , we define and .

Recall that is defined by .

If (the set of the symmetric positive definite matrices) and , let be the -th largest eigenvalue of . We also write (resp. ) for the largest (resp. smallest) eigenvalue of .

We define , the unbiased empirical estimator of . Let be the coefficients of and be the coefficients of .

Recall that when Condition 4 does not hold, we need to define as the partition given by thresholding by . We also define and write .

Proof.

Let us write

|

|

|

which is the closure of in .

First, let us show that, for all , is the minimum of on . If , we have

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

The function defined by has an unique minimum at . Thus, the function defined by has an unique minimum at . Thus

has an unique minimum at .

Now, the penalisation term is constant on each . Thus has a global minimum (not necessary unique) at , for some .

∎

Notation for Section 2.2

Here and in all the proofs of Section 2.2, we assume Conditions 1 to 3 of Section 2.2.1.

In the following, we introduce some notation.

We know that

|

|

|

where is the Wishart distribution with parameter and [12]. Thus, if we write i.i.d. with distribution , we have

|

|

|

Lemma 1.

For all ,

|

|

|

|

|

|

|

|

|

and

|

|

|

Moreover, that holds also for instead of .

Proof.

Let i.i.d. with distribution .

Using the result in [32] which states that

|

|

|

we have,

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

and

|

|

|

Thus,

|

|

|

The proof is the same for .

∎

We also verify the assumptions of Bernstein’s inequality (see for example Theorem 2.8.1 in [36]).

For all , let

|

|

|

(9) |

The random-variables are independent, mean zero, sub-exponential and we have , where is the sub-exponential norm (for example, see Definition 2.7.5 in [36]). So, we can use Bernstein’s inequality with : there exists such that, for all and ,

|

|

|

In this proof, we assume that Conditions 1 to 4 are satisfied. We first show several Lemmas.

Lemma 2.

For all symmetric positive definite and for all , if we write , we have:

-

•

decreases and so .

-

•

increases and so .

Proof.

Let us show that increases (the proof if the same for ).

For all , let , and an unit eigenvector of associated to . Let . Thus

|

|

|

If we show that , we proved that increases.

First, assume that . If we write the group of the largest eigenvalue of , then is equal to zero for all , so

is equal to zero for all , and so is equal to zero.

Assume now that and let us show that by contradiction. Assume that . Then

|

|

|

Furthermore, we have seen that . Thus, we have

|

|

|

that is in contradiction with .

∎

In the following, let for all .

Lemma 3.

For all , we have

|

|

|

(10) |

Moreover, for all , we have

|

|

|

(11) |

Proof.

First, we prove Equation (10).

Doing the Taylor expansion of and using the integral form of the remainder (as Equation (9) of [30] or in [20]), we have

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

where is the Kronecker product.

The trace is equal to zero. Now,

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

using Lemma 2 for the two last steps.

Now, we prove Equation (11) similarly. We have, using Lemma 2,

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

∎

Lemma 4.

|

|

|

Proof.

Using Lemma 3, we have

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

We show that the two terms go to .

The first term goes to with Lemma 1. For the second term, we have

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

using Bernstein’s inequality, where is defined in Equation (9). That concludes the proof.

∎

Lemma 5.

|

|

|

Proof.

Using Lemma 3, we have

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

The first term goes to 0 with Lemma 1. The second term is

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Now, for all and for all , let (with an implicit dependence on and ). Remark that

|

|

|

Thus,

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Now, by Condition 4, we know that , so, for large enough,

|

|

|

Thus, by Bernstein’s inequality, for large enough,

|

|

|

|

|

|

∎

Now, we can prove Proposition 2.

Proof.

We have

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

The two first terms go to 0 tanks to Lemmas 4 and 5. For the last term, we have

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

These two last terms go to 0 thanks to Lemmas 4 and 5.

In this proof, we assume that Conditions 1 to 3 hold.

Lemma 6.

For all , we have

|

|

|

(12) |

Moreover, for all , we have

|

|

|

(13) |

Proof.

Same proof as Lemma 3 replacing by .

∎

Lemma 7.

If , then,

|

|

|

Proof.

Following the proof of Lemma 4 (and using Lemma 6), it is enough to prove that the following term goes to 0:

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

using again Bernstein’s inequality. That concludes the proof.

∎

Lemma 8.

If , then,

|

|

|

Proof.

Following the proof of Lemma 5, it suffices to prove that

|

|

|

Now, by definition of , we know that , so, for large enough,

|

|

|

Thus, by Bernstein’s inequality, for large enough,

|

|

|

|

|

|

∎

We can now prove Proposition 3.

Proof.

We have

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

First,

|

|

|

|

|

|

|

|

|

|

from Lemma 8. Secondly,

|

|

|

|

|

|

|

|

|

|

from Lemma 7.

Finally,

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

from Lemmas 7 and 8.

∎

Proofs of Propositions 4, 5 and 6

Proof.

In the three cases, the computation of requires carrying out the BFS algorithm for and the computation of a determinant for . Recall that if is a graph (where is the set of vertices and the set of edges), the complexity of the BFS algorithm is . Recall that, if is a squared matrix of size , the complexity of is using the LU decomposition.

Now, we compute the complexity of the three estimators , and .

-

•

For all , the complexity of is , and the cardinal of is . Thus, the complexity of the computation of is .

Now, for all , the complexity of is and the cardinal of is (because the function decreases). Thus, the complexity of the evaluations is

So the complexity of is .

-

•

For the threshold , the complexity of is .

So the complexity of is .

-

•

One can divide the computation of into two steps.

For the first step, as we do not know the value of , we have to compute from to , verifying each time if the maximal size of group is smaller than or not.

First, for each value of from decreasing to , the complexity of the BFS algorithm to is , thus, the complexity of all these partitions if . Then, for , the complexity of is . So, the complexity of this first step is .

In the second step, we have to evaluate for all . The complexity of each evaluation

is , and the the number of evaluations is . Thus, the complexity of this second step is .

∎

To prove the convergence of in the three cases, we need the three following Lemmas.

Lemma 9.

For all sequence such that for all , (we assume that is large enough and that subset is not empty), we have

|

|

|

Proof.

Step 1: with probability which goes to 1.

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

using Lemma 1 and Bernstein’s inequality.

Step 2: with probability which goes to 1.

For all , and all , let and , where the dependency on and is implicit. Thanks to Condition 4, we have . Then, using Lemma 1,

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

by Bernstein’s inequality.

∎

Lemma 10.

Let . Let such that for all . Then,

|

|

|

Proof.

Thanks to Lemma 9, it suffices to show that, for large enough, there exists such that . By contradiction, let us assume that there does not exist such . Let such that and . Thus, we have

|

|

|

|

|

|

|

|

|

|

which is in contradiction with the definition of .

Lemma 11.

We have,

|

|

|

Proof.

Let be the set of the partitions of such that all their elements have cardinal smaller than . By assumption (Condition 3), . Let .

Thus verifies the assumption of in Lemma 10, so

|

|

|

Thus

|

|

|

To conclude, it suffices to prove that .

We have immediately . We have to prove the other inclusion. Assume that . We know that there exists such that . As , we know by definition of that and thus .

∎

Now, we prove Proposition 7.

Proof.

-

•

Using Lemma 9, Proposition 2, and the fact that , we have .

-

•

Using Lemma 9 and Proposition 2, we have .

-

•

Using Lemma 11 and Proposition 2, we have .

∎

Proof.

We follow the proof of Lemma 9.

Step 1: with probability which goes to 1.

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

using Lemma 1 and Bernstein’s inequality.

Step 2: with probability which goes to 1.

For all , and all , let and , where the dependency on and is implicit. Then, using Lemma 1,

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

by Bernstein’s inequality.

∎

Proof.

First, we prove the results for .

We have, using again the notation ,

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

By Markov’s inequality, that proves

|

|

|

Now, we want to prove that

|

|

|

First, we have

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Now, the variance is

|

|

|

Now,

|

|

|

|

|

Remark that if are random variables, we have

|

|

|

Thus

|

|

|

|

|

Let for some . We want to upper-bound . Let us define . We know that

|

|

|

So, using the independence of , we obtain

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

where we observed that .

Now, by Isserlis’ theorem and using the fact that is upper-bounded by , we have , and (and these bounds do not depend on ). So

|

|

|

Thus,

|

|

|

and

|

|

|

Thus, by Chebyshev’s inequality

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

So, we proved that is not an .

Now, we show that the same results hold for proving that . We have

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Yet, by Bernstein’s inequality,

|

|

|

|

|

|

and

|

|

|

That proves

|

|

|

Now, on the one hand, we have

|

|

|

and by Proposition 7,

|

|

|

On the other hand,

|

|

|

∎

Proof.

It suffices to prove that

|

|

|

(14) |

First,

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Secondly,

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

∎

Proof.

We follow the proof of Proposition 9.

Let , and .

We have

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Thus,

|

|

|

and thus

|

|

|

We conclude using Proposition 8 and using that .

∎

Proof.

The eigenvalues of are lower-bounded by and upper-bounded by , so verifies Condition 2. Condition 3 is verified by construction. It remains to prove the slightly modified Condition 4 given in Proposition 12. Let .

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

using an union bound and the fact that all the blocks have a size larger that 10. Then, by independence of , we have

|

|

|

Let for . Then, and are independent and uniformly distributed on . Thus

|

|

|

Let . The set is a subset of where and is an orthonormal basis of . The Lebesgue measure of this subset is . Furthermore, (conditionally to ) the probability density function of on this set is either or . So, for all ,

|

|

|

Thus

|

|

|

Then

|

|

|

Hence, it remains to prove that the conclusion of Proposition 2 holds. That will imply the same for Propositions 7 and 9. Let and , where the generation of is defined in Proposition 12. We have

|

|

|

|

|

|

|

|

|

|

Yet, for all , thanks to Proposition 2 (even in Condition 4 is not verified, the proof is still valid since the covariance matrix is in ). We conclude by dominated convergence theorem.

∎

Notation for the proofs of Section 2.3

For all , let be such that all coefficients are zero except the -th one which is equal to 1, and let be such that all coefficients are zero except the -th one which is equal to 1. Let be the -th coefficient of . Finally, as we use matrices of size , and vectors of size , we define and .

Proof of Proposition 13

We see that, for all , converges almost surely to . The following Lemma gives a central limit theorem for this convergence.

Lemma 12.

For all , we have

|

|

|

(15) |

with . In particular

|

|

|

Proof.

Let , where . We know that and .

Let , be such that .

Using the central limit Theorem,

|

|

|

and by Slutsky Lemma,

|

|

|

(16) |

where if and and otherwise.

Let us apply the Delta-method to (16) with the function , where is the inverse function of . If we write the Jacobian matrix of , we have:

|

|

|

Let us compute the linear map , that we identify with its matrix. Let us recall that, for the dot product , the gradient of on is . Thus, if , we have

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

So , then

|

|

|

Now,

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Indeed, as is symmetric positive definite, we have .

∎

Lemma 13.

For all and for all such that , we have .

Proof.

First, let us prove it for . We have .

|

|

|

Now, .

Thus, it suffices to show that . We then write which is symmetric positive definite (Schur’s complement), and which is also symmetric positive definite. Then, we have

|

|

|

because .

Now, we prove the lemma for any value of .

Let and such that . Let for all . We now define with the recurrence relation and with , we then have .

Thus

|

|

|

Furthermore, as , there exists such that . Thus, at least one of the previous inequality is strict, and so .

∎

Using Lemmas 12 and 13, we can prove Proposition 13.

Proof.

It suffices to show that, for all ,

|

|

|

We split the proof into two steps: for and for .

Step 1: .

Let , since . Thanks to Lemma 13, we know that .

Let . Using the convergence in probability of , we know that and .

Now, we know that for , the term of penalisation satisfies .

Thus,

|

|

|

Step 2: .

Let .

We know that

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

since for .

Let be equal to (which converges to ), to be equal to (which converges to a zero mean normal distribution) and to be equal to (which converges to a zero mean normal distribution). We have

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Thus, .

∎

Proof.

We follow the notation of [35].

An othonormal basis of is with the following total order on : we write if or if and . We define as the matrix which columns are the vectorizations of the components of this basis of . Thus , for all and .

Thus, is the Cramér-Rao bound, where is the standard Fisher information matrix in the model . As the sample is i.i.d, it suffices to prove if with . In the rest of the proof, we compute the Cramér-Rao bound, and we show that this bound is equal to . We split the proof into several Lemmas.

Lemma 14.

Recall that .

Let defined by

|

|

|

Then, .

Proof.

Deriving twice the log-likelihood with respect to and (for ) and taking the expectation, we get

|

|

|

|

|

|

|

|

|

|

Thus, for all , we have

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Now, if , we have

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

If , we have

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Finally,

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

∎

Lemma 15.

Let defined by

|

|

|

then, . Moreover for all .

Proof.

We compute the product . First of all, let and . We have

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

with

|

|

|

and

|

|

|

We then have

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Similarly,

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Now, if

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

If , then

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Finally,

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

We proved that . Let us show that for all . First of all, assume and . Assume for example and . Then we have

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

We apply the same method for and , for and , and for and . Then, let and , for example . We have

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

The other cases are similar.

∎

We thus have the component of the Cramér-Rao bound:

|

|

|

This matrix is equal to for and when the mean is known.

∎

Proof.

An orthonormal basis of is with the following total order on : we write if or if and . Thus, we define as the matrix which the columns are the vectorizations of the components of this basis of . We have , for all with and .

Thus, is the Cramér-Rao bound. As the sample is i.i.d, it suffices to prove the proposition with .

Lemma 16.

Let defined by

|

|

|

Then, .

Proof.

The proof is similar to the proof of Lemma 14, except that the values of and are more constraint.

First of all

|

|

|

|

|

|

|

|

|

|

Now, if ,

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

If and ,

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

If and , we have

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Finally,

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

∎

Lemma 17.

Let defined by

|

|

|

then, . Moreover for all and for all . Recall that we write if there exists such that .

Proof.

We introduce the following notation: if , let to be the index of in .

Step 1: Let us prove that .

We compute the product .

Assume that with and with and . We then have

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

using that if and because is block-diagonal, and using that if and because is block-diagonal.

Assume that with and . We have,

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

thanks to Lemma 15 applied to the matrix .

We proved that .

Step 2.A : We show that for all .

Assume that . First, assume that and . Assume for example that and (the other cases are similar).

We then have

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Let us take the case where with either , or . For example and . We then have

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

It is the same for and , then for and . We also can prove the equality similarly when and .

Step 2.B: Let us prove that for all .

Assume that . If , or if , we have

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

because if , the term is equal to 0. Similarly, if , the term is equal to 0.

It remains the case where and with . Then, .

∎

To conlude the proof, we remark that, if , then

|

|

|

Now, assume that . If or if , then because one of the two terms is zero. Assume that and with . Then

|

|

|

Thus, the covariance matrix of is equal to the Cramér-Rao bound.

∎

Proof.

Using the central limit Theorem and Proposion 15, we have

|

|

|

Then, by Proposition 13, we have

|

|

|

and by Slutsky,

|

|

|

∎

Lemma 18.

Under Conditions 1 to 4, for all

|

|

|

where is the operator norm, and it is equal to on the set of the symmetric positive semi-definite matrices.

Proof.

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Now, on the one hand,

|

|

|

|

|

|

|

|

|

|

by Bernstein’s inequality. On the other hand,

|

|

|

|

|

|

|

|

|

|

by Bernstein’s inequality.

∎

Lemma 19.

Under Conditions 1 to 5, for all ,

|

|

|

Proof.

We know that .

To simplify notation, let . Remark that and .

Now, we know that

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Thus, .

Now, by Lemma 1,

|

|

|

Let and . We have,

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

∎

Lemma 20.

Under Conditions 1 to 5, for all ,

|

|

|

Proof.

We have

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

by Lemmas 19 and 18. Now, with probability which goes to one , by Lemmas 1 and 19, we have . Moreover, . Thus, with probability which goes to one , we have

|

|

|

∎

We can now prove Proposition 17

Proof.

Let be the estimator of obtained replacing by and by in Equations (6) and (7).

For all and , we have

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

The term goes to 0 from Proposition 2. It remains to prove that

|

|

|

(17) |

For all and all , let us write

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Let, for all , ,

|

|

|

We then have

et .

As is linear, it is Lipschitz continuous from to , with constant (we can show that ). Let (we have in fact ). We then have,

|

|

|

It suffices to show that

|

|

|

Now,

|

|

|

|

|

|

|

|

|

|

The term is bounded from Conditions 2 and 5 and thanks to Lemma 20. The term is bounded in probability using Lemma 20, Conditions 2 and 5. Thus, it suffices to show that . We will use that the operator norm of a sub-matrix is smaller than the operator norm of the whole matrix.

For all and , we have

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Thus, we obtain a sum a three terms, and we have to prove that each term is .

The first term is thanks to Lemmas 1 and 19.

For the second term, so is from Lemma 18.

Finally, for the third term,

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

which do not depend on and .

Finally, remark that and are bounded from Condition 2, that are bounded in probability from Lemma 1, that from Lemma 18 and Proposition 2 and that

|

|

|

Thus, we proved that

|

|

|

∎

Lemma 21.

Under Conditions 1, 2 and 3, for all penalization coefficient and for all ,

|

|

|

where is the operator norm, and it is equal to on the set of the symmetric positive semi-definite matrices.

Proof.

Let .

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

that goes to 0 following the proof of 18.

∎

Lemma 22.

Under Conditions 1, 2, 3 and 5, for all penalization coefficient and for all ,

|

|

|

Proof.

The proof is similar to the proof of Lemma 20.

∎

We now can prove Proposition 18.

Proof.

For all , we define as the estimator of obtained replacing by , by and by in Equations (6) and (7). We also define .

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

By Proposition 8, .

Finally, we prove that

|

|

|

following the proof of Proposition 17.

∎

Proof.

Remark that verifies Conditions 1 to 3. Let .

Let if and otherwise.

Let and be defined as and in Proposition 17 but replacing by . As verify the Conditions 1 to 3 and the slightly modified Condition 4 given in Proposition 12, conditionally to

|

|

|

Thus, for all ,

|

|

|

so, by dominated convergence theorem,

|

|

|

unconditionally to .

We conclude saying that with probability which converges to 1 from Proposition 12, so and with probability which converges to 1.

∎