Decorrelated Local Linear Estimator: Inference for Non-linear Effects in High-dimensional Additive Models

Abstract

Additive models play an essential role in studying non-linear relationships. Despite many recent advances in estimation, there is a lack of methods and theories for inference in high-dimensional additive models, including confidence interval construction and hypothesis testing. Motivated by inference for non-linear treatment effects, we consider the high-dimensional additive model and make inference for the derivative of the function of interest. We propose a novel decorrelated local linear estimator and establish its asymptotic normality. The main novelty is the construction of the decorrelation weights, which is instrumental in reducing the error inherited from estimating the nuisance functions in the high-dimensional additive model. We construct the confidence interval for the function derivative and conduct the related hypothesis testing. We demonstrate our proposed method over large-scale simulation studies and apply it to identify non-linear effects in the motif regression problem. Our proposed method is implemented in the R package DLL available from CRAN.

1 Introduction

Additive models play an important role in modern data analysis [8, 55, 29]. The additive model is useful as it relaxes the stringent linearity assumption imposed in the multiple linear models and generalizes the nice interpretation of linear models. In the low-dimensional setting, additive models have been carefully investigated [8, 55, 29, 42, 32, 39, e.g.]. Recently, there has been a growing interest in the high-dimensional additive model, which generalizes the high-dimensional linear regression. Much progress has been made to understand the prediction performance of various proposals, including [40, 37, 46, 51, 52, 57, 58, 47]. However, the statistical inference problem in the high-dimensional additive model is far less understood from both methodological and theoretical perspectives.

Statistical inference in high-dimensional additive models is well-motivated from causal inference with observational studies. Causal conclusions from observational studies are invalidated due to unmeasured confounders [33, 43, e.g.]. A commonly used approach is to condition on a large number of measured covariates such that the conditional ignorability condition holds [4, 31, e.g.]. This idea has been carefully investigated by utilizing high-dimensional linear models. However, the linear model imposes a stringent assumption that the exposure has a constant effect on the outcome regardless of the exposure value. Such an assumption might not be plausible for various applications; see the application to motif regression in Section 5 for example. Non-linear effects have been commonly observed in scientific studies, including return to schooling [13], climate on crop yields [49], and the climate change on the economic outcomes [20, 19]. The additive model significantly relaxes the linearity assumption and better accommodates the possibly non-linear effect.

In this paper, we consider the additive model for the outcome variable ,

| (1) |

where is the variable of interest (e.g. the exposure or treatment variable), is the high-dimensional baseline covariates, and and for are unknown functions. The observed data are assumed to be independently and identically distributed. For a pre-specified and a small the ratio captures the exposure’s effect at . With approaching zero, the function derivative measures the exposure’s effect on the outcome [3]. The current paper is focused on statistical inference for with under the high-dimensional additive model (1).

1.1 Results and contributions

In the univariate setting, the local linear estimator is the state-of-the-art method to make inference for [23, 22, e.g.]. However, the inference problem under the high-dimensional additive model (1) is much more challenging due to the presence of the unknown high-dimensional function . With an accurate estimator , the estimated variables for can be used as proxies for . A natural idea is to estimate by applying the local linear method to with as the outcome variables. However, such a plug-in estimator suffers from large estimation bias due to the estimation error of ; see Table 1 in Section 4.1 for illustrations.

We propose a novel Decorrelated Local Linear (DLL) estimator of The classical local linear estimator can be expressed as a weighted average of the outcome variables, where the local linear kernel induces the weights. As the major novelty, we construct the decorrelation weights to mitigate the error inherited from the high-dimensional estimator . Meanwhile, the constructed decorrelation weights ensure that the standard error of our proposed DLL estimator is comparable to that of the classical local linear estimator. The decorrelation weights are constructed in a non-parametric way and designed for the bias correction of the local linear estimator.

In Theorem 1, we establish the asymptotic normality of our proposed DLL estimator as long as the estimator is consistent. We further show that the asymptotic variance of our proposed estimator matches with the optimal rate in the univariate setting [23]. We construct the confidence interval for and test for the hypothesis .

In Section 4, we demonstrate the validity of our theoretical results in moderate sample sizes, address practical issues on algorithm implementation, and provide practical recommendations. Our proposed method is implemented in the R package DLL, which is available from CRAN. The simulation results show that the DLL estimator significantly outperforms the plug-in estimator and the ReSmoothing estimator [27], in terms of the bias correction and coverage property. Regarding the empirical coverage and length, the confidence intervals (CIs) based on the DLL estimator are comparable to the oracle CIs, which are constructed with the oracle knowledge of the high-dimensional function .

In Section 5, we conduct a careful analysis of the motif regression problem [59] and observe a highly non-linear relationship between the gene expression level and the motif scores. Our results demonstrate the advantage of our proposed method over the statistical inference method assuming the linear outcome model.

1.2 Literature review and comparison

Two recent works [27] and [38] studied the inference problems in high-dimensional additive models. Specifically, [27] proposed a two-step ReSmoothing (RS) estimator: in the first step, a pre-smoothing estimator was obtained; in the second step, the pre-smoothing estimator was taken as the proxy outcome, and standard univariate non-parametric technique was then applied. In Section 4.2, we compare our proposed DLL estimator with the RS estimator and observe that the RS estimator suffers from a large bias of estimating the function derivative while our proposed DLL estimator corrects the bias effectively. Consequently, our proposed confidence interval has better empirical coverage than that based on the RS estimator; see Table 3 for the detailed comparison. In addition, [38] considered the confidence band construction problem under the high-dimensional sparse additive model, which is a different inference problem from the current paper.

Inference for function derivative has been actively studied in the non-parametric modeling, including local linear estimator [22], regression spline [61], kernel methods [26], empirical likelihood methods [44], and others cited therein. However, as discussed, the unknown high-dimensional function in the additive model poses great challenges to statistical inference for the function derivative at a local point. The paper [3] studied the inference for the function derivative in additive models without the sparsity structure. The penalty is essential to recovering the high-dimensional sparse model, which creates an additional bias to correct in the following inference step. The statistical inference problem with the sparsity structure requires extra innovation in terms of both method and theory.

A recent line of active research was focused on statistical inference in high-dimensional linear regression. Debiased estimators or Neyman’s Orthogonalization were proposed for inference for single regression coefficients [60, 54, 34, 5, 15, 24, 14]. The linear model is a special case of the additive model, where the function derivative is assumed to be a constant for any . Statistical inference for the non-linear effect in the additive model is a much more challenging problem, which requires novel methods and theories to address the non-linearity. Both the rate of convergence and the sufficient conditions for confidence interval construction are different from those established in the high-dimensional linear regression. A more detailed methodological comparison is presented in Remark 2. The real data analysis in Section 5 shows that a misleading scientific conclusion might be obtained without accounting for the possible non-linear effects.

Beyond the high-dimensional linear regression, [14] and [63] studied the inference procedure for the partially linear model. However, the focus is still on the inference problem for the linear component instead of the non-linear component addressed here.

Organization. In Section 2, we introduce the decorrelated local linear estimator. In Section 3, we establish the theoretical guarantee of the proposed estimator. In Section 4, we conduct a large-scale simulation study to demonstrate the finite-sample performance of the DLL estimator. In Section 5, we apply the DLL estimator to the motif regression problem. In Section 6, we provide conclusion and discussion.

Notations. For a sequence of random variables indexed by , we use and to represent that converges to in probability and in distribution, respectively. For a matrix , we use , , and to denote its entry, the -th row and -th column, respectively; for index sets and , denotes the sub-matrix of with row and column indices belonging to and , respectively. We use and to denote generic positive constants that may vary from place to place. For two positive sequences and , means for all and if and if and , and if and if .

2 Decorrelated local linear estimator

We consider the data being i.i.d. generated, where for the -th subject, denotes the outcome variable, denotes the variable of interest, and denotes the high-dimensional baseline covariates. We focus on the additive outcome model (1). Our goal is to make inference for the function derivative with denoting a pre-specified value belonging to the range of

2.1 Decorrelation for the local linear estimator

The local polynomial estimator [22, 50, 16, 21] has been developed under the univariate non-parametric regression for with denoting an unknown smooth function. By the Taylor expansion for we approximate by a linear function in a small neighborhood of and estimate by fitting a linear model within this small neighborhood. For a pre-specified bandwidth , define the kernel

| (2) |

The local linear estimator of has the following explicit form,

| (3) |

The local polynomial estimator is the state-of-the-art method for estimating in the univariate and also low dimensional setting. To illustrate the main idea, we focus on the uniform kernel and the local linear estimator, but our following proposed method is potentially useful for other kernels and higher-order local polynomial estimator.

For the high-dimensional sparse additive model in (1), the existing literature [40, 37, 51, 52, e.g.] was focused on accurately estimating the unknown functions and in (1). However, there is a lack of inference methods for .

In the following, we introduce the decorrelation idea and use to denote an initial estimator of ; see Section 2.4 for the detailed construction. With the estimator , we compute for which are proxies for the oracle outcome As a direct extension of the local linear estimator in (3), we replace by and have the following plug-in estimator,

| (4) |

is the same as the local linear estimator applied to the data with as the outcome variable. The simulation results in Section 4.1 demonstrate that the plug-in estimator suffers from a large bias due to the estimation error of . Consequently, the plug-in estimator is not ready for statistical inference; see Table 1 for details.

To correct the bias of the plug-in estimator, we consider the estimator of the form,

| (5) |

where are the weights to be specified. The error is decomposed as,

| (6) |

The first term of (6) appears in the univariate case, while the second term is the new addition in the high-dimensional setting, which results from the error of estimating the high-dimensional function . We construct the weights such that the second term of (6) is significantly reduced, but the first term in (6) is of the same scale as the univariate case.

To achieve this, we define the population decorrelation weights as

| (7) |

The population decorrelation weights ensure that the estimator in (5) is nearly unbiased and asymptotically normal. In the following Section 2.2, we propose a non-parametric estimator of the decorrelation weight defined in (7).

We provide intuitions on how the population decorrelation weights significantly reduce the second term in (6). The weights constructed in (7) guarantee

If is not used to construct , then the above equation implies

| (8) |

The zero mean of the estimation error guarantees the second term of the decomposition (6) converges to zero at a fast rate.

2.2 Construction of decorrelation weights

In the following, we construct non-parametric estimators of and defined in (7). We decouple the relationship between and by considering a high-dimensional sparse linear model,

| (9) |

where is a sparse vector and is independent of . Let denote the density function of Under the model (9), we obtain the following expression for ,

| (10) |

We also write for to highlight its dependence on . As a remark, the independence between and is important for establishing the simplified expression of in (10). In Section 2.6, we consider possibly non-linear relationship between and and generalize our procedure to the setting where the model between and is a sparse additive model. In Section 4.1, we demonstrate the robustness of our proposed method in finite samples when the independence assumption in the model (9) does not hold; see Settings 3 and 4 in Section 4.1 and Table 1 for details.

We utilize the expression (10) and construct a non-parametric estimator of . We will use sample splitting to create independence required for establishing the decorrelation property in (8). Our particular way of data splitting will not lead to the efficiency loss; see Remark 1 for details.

We randomly split the index set into two disjoint subsets and , with and With the data we estimate by the Lasso estimator , defined as

| (11) |

where is a tuning parameter. We estimate and by

For we respectively estimate and by

Then we estimate by

| (12) |

Our above construction ensures that the estimator is independent of the data points We can construct the estimators of in a similar way to (12) by switching the roles of and We construct the estimator by applying the Lasso algorithm in (11) to the data . We estimate by

and then estimate by

| (13) |

Then we apply the definition in (7) and define

| (14) |

where and are defined in (12) and (13), respectively. By centering , we construct the decorrelation weights as

| (15) |

With the data we construct the initial estimator of in the following equations (20) and (21); we construct the estimators by applying the same algorithm to the data For we compute

| (16) |

Remark 1

The construction in (14) and (16) uses the “data swapping” idea. That is, we swap the data and the initial estimators. Such a procedure is used to create the independence required for the proof but does not lead to loss of efficiency. The data swapping idea dated at least back to [48, 36] and was recently developed under the name of “cross-fitting” in the double machine learning literature [14, e.g.].

2.3 Decorrelated local linear estimator and inference for

By combining defined in (16) and the decorrelation weight defined in (15), we apply the generic form (5) and propose the Decorrelated Local Linear (DLL) estimator as

| (17) |

In Section 3, we show that is asymptotically normal if certain reasonably good estimator is used in our construction. Consequently, we construct the following confidence interval for

| (18) |

where denotes the upper quantile of the standard normal distribution and is the variance level estimator specified in Section 2.4. To test the null hypothesis we develop the following procedure,

| (19) |

Remark 2 (Comparison to debiasing methods in linear models.)

The debiased inference methods have been proposed in [60, 54, 34] about inference for the regression coefficients in high-dimensional regression models and extended to other high-dimensional parametric models [41, 54] or other inference targets in high-dimensional linear regression [10, 11, 1, 62]. These methods ultilize the fact that is nearly orthogonal to and then correct the bias with a linear function of In contrast, our proposed DLL estimator uses a non-linear transformation of to remove the high-dimensional error. Specifically, we construct the deccorelation weights based on certain kernel estimates with see (12) and (13). This new decorrelation idea is particularly designed for bias correction of the local linear estimator.

2.4 Initial estimators

We now specify the initial estimators and used in the construction of the DLL estimator in (17) and the related confidence interval in (18). In the existing literature [40, 47, 37, 51, 52], different types of penalty terms are imposed to ensure that only a small number of the unknown functions and are non-zero and these non-zero functions are smooth. We adopt the basis method in [40, 47] and generate a set of basis functions to approximate the smooth functions. In particular, for a positive integer we use to denote a set of B-spline basis functions for and for , to denote a set of B-spline basis functions for We write and for Following [47], we implement the following convex optimization problem,

| (20) |

where is a tuning parameter to be chosen. The choice of the tuning parameter and the number M of basis functions are discussed at the beginning of Section 4. Define

| (21) |

Similarly, we define as in (20) by replacing with and

Then we construct

| (22) |

and estimate the variance level by

| (23) |

In addition to the aforementioned basis method, we can also adopt the double penalization method [52] by generalizing the smoothing spline; see Section A.2 in the supplement. We also discuss the construction of additive models by firstly applying the quantile transformation to the observed covariates; see Section A.3 in the supplement.

2.5 Algorithm

We summarize our proposed DLL estimator (with data swapping) in Algorithm 1 and will present the DLL estimator without data swapping in Section A.1 in the supplement. We shall discuss the tuning parameter selection at the beginning of Section 4.

Input: Data ; the evaluation point , bandwidth , tuning parameters , the number of basis

Output: Point estimator and confidence interval .

2.6 Decorrelaction with the additive treatment model

This section generalizes the construction of decorrelation weights by considering non-linear models between and . Particularly, we consider the sparse additive model for

where for are unknown smooth functions. Instead of applying the Lasso algorithm (11), we implement another sparse additive model as in (20),

where is the tuning parameter to be chosen. We estimate by

By switching the data in and , we construct . With the estimates , we construct the decorrelation weights in the same way as in (12) and (13). In Section 4.3, we compare the finite-sample performance of Algorithm 1 and the generalized decorrelation method with the sparse additive model.

3 Theoretical justification

3.1 Technical conditions

Before presenting the main theorems, we present the technical conditions imposed on the outcome model (1) and the treatment model (9). Let denote the probability density function of evaluated at The first condition is on the function of interest , the regression error , and the bandwidth

- (A1)

Condition (A1) is standard for the analysis of the local polynomial estimator in the univariate case [23, 22, e.g.]. The smoothness condition on ensures a sufficiently small approximation error of by a linear function in a neighborhood near . The conditional moment conditions on are required to establish the asymptotic normality of our proposed DLL estimator. Since the expected number of observations is about , Condition requires that there are (asymptotically) infinitely many observations in the local neighborhood of with bandwidth . For a twicely differentiable function , the optimal choice of bandwidth for estimating is which satisfies

The second model assumption is imposed on the treatment model (9). Recall that denotes the probability density function of the regression error in (9) and for We use and to denote some high probability upper bounds, defined as: with probability larger than for some positive constant

| (24) |

where for some positive constant . The value (or ) defined in (24) captures the ratio of (or ) over near and are allowed to grow with and , but in general they grow to infinity at a slow rate; see Remark 3 for details. We now state the condition for the model (9) and and defined in (24).

- (A2)

For a constant is almost the weakest sparsity condition to identify for the high-dimensional linear model. The conditions on and the covariance matrix are standard for the high-dimensional analysis. The condition (25) is mild with and growing at the polynomial order of and see Remark 3. The independence assumption between and is stringent but we believe it is mainly imposed for the technical analysis. In numerical studies, we test the performance of our proposed method when the independence assumption between and is violated; see Settings 3 and 4 and Table 1 in Section 4.1 for details.

Remark 3 (Growth rates of and .)

We discuss the order of magnitudes for and over two examples. Firstly, consider the setting that there exist positive constant such that If for some positive constant , and is twicely differentiable for , then and are of constant orders. Secondly, we consider that is sub-gaussian and may be unbounded in this case. If is the Gaussian density, and , then with probability larger than for some positive constant ,

Finally, we require that the initial estimator estimates to certain accuracy. We use to denote the estimation accuracy of , which is defined as follows: with probability larger than for some positive constant , the initial estimator defined in (16) satisfies

| (26) |

where the expectation is taken with respect to the independent copy of The last assumption is on the rate of convergence of .

- (A3)

We discuss Condition (A3) by focusing on a commonly used regime with , being of a constant order, and If for some positive constant then any consistent estimator with will automatically satisfy the condition (27). Most estimators proposed in the high-dimensional sparse additive model can be shown to satisfy the assumption (A3). More discussion about (A3) can be found in Section A.4 in the supplement.

3.2 Asymptotic normality and inference properties

We establish the asymptotic limiting distribution for our proposed DLL estimator.

Theorem 1

With and and being of constant orders, our proposed DLL estimator achieves the optimal rate of convergence [53]. Furthermore, the DLL estimator is asymptotically normal and the asymptotic variance depends on the value through the density level . In finite samples, we compare the variance level of our DLL estimator to that of the oracle estimator by assuming the knowledge of ; See Table 1 for details.

As a Corollary of Theorem 1, we establish the properties of our proposed confidence interval defined in (18).

Corollary 1

Suppose that Conditions (A1), (A2) and (A3) hold and . For any our proposed confidence interval defined in (18) satisfies,

and

where denotes the length of the interval, is any positive constant, and denotes the upper quantile of the standard normal distribution.

Beyond Conditions (A1)-(A3), the above corollary requires a consistent estimator of such that our proposed variance estimator consistently estimates In Proposition 1 in Section A.5 in the supplement, we show that our proposed estimator in (23) satisfies if both and are consistent. Similarly, we can establish the validity of the proposed testing procedure in (19).

3.3 Theoretical reasoning of decorrelation

In the following, we explain why our constructed decorrelated weight is effective. With the estimation error of the DLL estimator is decomposed as

The stochastic error represents a random component with mean zero and, after rescaling, following an asymptotic normal limiting distribution. The approximation error is the error of approximating the non-linear function by a linear function at a local neighborhood of . The high-dimensional error is due to the estimation of the unknown function in high dimensions. Both the stochastic and approximation errors appear in the classical non-parametric regression, while the high-dimensional error is the new addition here.

The following theorem demonstrates that our proposed decorrelation method is effective in reducing the high-dimensional error.

Theorem 2

Our constructed decorrelation weights are instrumental in reducing the error due to estimating . This happens mainly due to the fact that the expectation of is zero. Condition (A3) and the upper bound (29) imply

The data swapping step creates the independence between the error function and the data which is required for the proof of (29). We believe that a more refined analysis might remove the data swapping step.

4 Simulation

We provide more details about the tuning parameter selection for Algorithm 1. For the high-dimensional sparse additive model, we compute the initial estimators and by applying the R package SAM [35] and choose the tuning parameter and the number M of basis functions in (20) by cross validation. We construct the Lasso estimator of in (11) by applying the R package glmnet [25] and choose the tuning parameter by cross validation. For local linear methods, choosing a good bandwidth is essential for the finite-sample performance. There are many methods for bandwidth selection. After exploration in the simulation study, we observe that the “Rule of Thumb” method proposed in [23] leads to the most stable performance. This bandwidth selection method is implemented in the R package locpol [9] with the thumbBw() function. The “Rule of Thumb” is used as our default bandwidth selection method. We demonstrate the performance of the DLL estimator with other bandwidth selection methods in Section F.2 in the supplement. The codes for replicating our proposed method can be found at https://github.com/zijguo/HighDim-Additive-Inference.

Since we believe that the data swapping is introduced for technical analysis, we mainly report the simulation results for the DLL estimator without the data swapping, which is described in Section A.1 in the supplement. We compare our constructed confidence intervals with and without data swapping in Section F.3 in the supplement. Both confidence intervals attain the desired coverage level. When the sample size is relatively large, they have similar performance; for relatively small sample size, the confidence interval without data swapping can be shorter than that with data swapping.

We demonstrate the finite-sample performance of our proposed DLL estimator across various settings and compare it with three other estimators described as follows,

- •

-

•

The oracle estimator (Orac) denotes the local linear estimator applied to the data with . The oracle estimator is used as the benchmark to compare with. For implementation of the local linear estimator and the related confidence interval, we follow the output of the package nprobust [12].

-

•

The ReSmoothing (RS) estimator is a two-step estimator proposed in [27]. In the first step, we implement the code available at https://github.com/gregorkb/spaddinf and obtain a pre-smoothing estimator of , denoted as ; in the second step, we apply the local polynomial estimator to the data where is used as the outcome. We fit the local linear estimator by the package nprobust [12].

We generate the outcome following the model (1) and consider both exactly sparse and approximately sparse settings.

Exactly sparse. We set the first six functions as follows and for ,

| (30) | ||||||||

More complicated relationships often exist in real life and the additive model might not be exactly sparse. We further introduce an approximately sparse setting.

Approximately sparse. We set and as in (30), generate as

and generate as linear functions with .

In addition, we explore the finite-sample performance for different non-linear functions by switching the role of and function; see the results in Section F.1 in the supplement.

4.1 Comparison with plug-in and oracle estimators

In the following, we compare our proposed DLL estimator with the plug-in(Plug) and oracle(Orac) estimators. We consider four different settings for generating and where the independence assumption between and in (A2) is violated in Settings 3 and 4.

Setting 1. We generate following the multivariate Normal distribution , where for and is a toeplitz covariance matrix with for and for

For , the correlation gradually decays from 0.1 to 0.

Setting 2. is generated in the same way as in Setting 1. With denoting the CDF of we generate the outcome model as

The main difference from Setting 1 is to apply a quantile transformation to and before applying the additive model transformation. The goal is to make inference for with We generate the additive model following (30) but set , , , and

Setting 3. We generate following with the same and as in Setting 1. We define and for , with denoting the CDF of . The marginal distributions of and are and is correlated with .

Setting 4. We generate following a centered multivariate t distribution with the same covariance matrix as in Setting 1. The degree of freedom is varied across

We fix the dimension and vary the sample size across {500, 1000, 1500, 2000}. The evaluation points are {-1.25, -0.5, 0.1, 0.25, 1}. For Setting 1, we generate the outcome using both exactly and approximately sparse models; for Settings 2 to 4, we only consider the exactly sparse outcome model. We generate the simulation data 500 times and then use the following metrics to compare these methods: 1. Bias, the absolute difference between the average of the 500 point estimates and the true value; 2. Root Mean Square Error (RMSE); 3. Standard Error (SE), the empirical standard deviation of the 500 point estimates; 4. Coverage, the empirical coverage out of 500 simulations; 5. Length, the average length of the constructed confidence interval (CI). In Table 1, we compare our proposed DLL with Plug, and Orac across four simulation settings and we take an average of the metrics across different sample sizes, evaluation functions, and evaluation points.

We summarize the results in Table 1. For the Plug estimator, the bias component is a dominating term in RMSE, while our DLL estimator is effective in bias correction. The RMSE of our proposed DLL estimator is similar to that of the oracle estimator, which is uniformly smaller than that of the Plug estimator. The coverage error is computed as the absolute difference between the empirical coverage and 95%; in most cases, the coverage error results from the undercoverage. The CIs based on the Plug estimator are in general undercoverage while our proposed CIs achieve the desired coverage level. Our proposed CI is of a similar length to the length of the oracle CI.

| Bias Percentage | RMSE Ratio | SE | Coverage Error | Length Ratio | |||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Setting | DLL | Plug | Orac | DLL | Plug | DLL | Plug | Orac | DLL | Plug | Orac | DLL | Plug |

| 1 | 0.128 | 0.407 | 0.090 | 1.152 | 1.248 | 0.293 | 0.286 | 0.269 | 1.05% | 4.19% | 0.88% | 1.157 | 1.103 |

| 2 | 0.133 | 0.563 | 0.045 | 1.057 | 1.267 | 0.350 | 0.344 | 0.337 | 1.06% | 7.46% | 0.80% | 1.045 | 1.010 |

| 3 | 0.065 | 0.280 | 0.037 | 1.049 | 1.080 | 0.502 | 0.497 | 0.479 | 0.77% | 1.94% | 0.81% | 1.050 | 1.031 |

| 4 | 0.151 | 0.520 | 0.049 | 1.034 | 1.213 | 0.320 | 0.316 | 0.316 | 1.15% | 6.72% | 0.91% | 1.037 | 0.986 |

In Table 2, we report the detailed simulation results for Settings 1 to 4 with and and the complete simulation results are presented in Section F.1 in the supplement. The results are consistent with the observations reported in Table 1: our proposed CI achieves the desired coverage and has a similar length to the oracle CI. In addition, the coverage improvement of our proposed CI over the Plug estimator can be quite substantial as our DLL estimator effectively corrects the bias. For Settings 3 and 4, our proposed method is still effective even if the independence assumption required in Condition (A2) is violated.

| Setting 1: approximately sparse | |||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Bias | RMSE | SE | Coverage | CI Length | |||||||||||||

| True | DLL | Plug | Orac | DLL | Plug | Orac | DLL | Plug | Orac | DLL | Plug | Orac | DLL | Plug | Orac | ||

| 500 | 0.21 | 0.46 | 0.02 | 0.44 | 0.60 | 0.39 | 0.39 | 0.38 | 0.39 | 0.91 | 0.72 | 0.94 | 1.51 | 1.45 | 1.49 | ||

| 1000 | 0.07 | 0.31 | 0.00 | 0.35 | 0.45 | 0.33 | 0.34 | 0.33 | 0.33 | 0.93 | 0.83 | 0.93 | 1.31 | 1.27 | 1.27 | ||

| 0.10 | 1.49 | 1500 | 0.05 | 0.26 | 0.01 | 0.31 | 0.39 | 0.29 | 0.31 | 0.30 | 0.29 | 0.94 | 0.86 | 0.95 | 1.18 | 1.15 | 1.15 |

| 500 | 0.20 | 0.45 | 0.00 | 0.45 | 0.60 | 0.39 | 0.41 | 0.39 | 0.39 | 0.91 | 0.77 | 0.94 | 1.56 | 1.50 | 1.55 | ||

| 1000 | 0.07 | 0.31 | 0.01 | 0.36 | 0.46 | 0.35 | 0.35 | 0.34 | 0.35 | 0.94 | 0.83 | 0.94 | 1.35 | 1.32 | 1.32 | ||

| 0.25 | 1.45 | 1500 | 0.07 | 0.27 | 0.03 | 0.32 | 0.41 | 0.30 | 0.31 | 0.31 | 0.30 | 0.96 | 0.84 | 0.96 | 1.22 | 1.19 | 1.18 |

| Setting 2: exactly sparse | |||||||||||||||||

| Bias | RMSE | SE | Coverage | CI Length | |||||||||||||

| True | DLL | Plug | Orac | DLL | Plug | Orac | DLL | Plug | Orac | DLL | Plug | Orac | DLL | Plug | Orac | ||

| 500 | 0.19 | 0.29 | 0.03 | 0.42 | 0.47 | 0.39 | 0.38 | 0.37 | 0.39 | 0.92 | 0.86 | 0.96 | 1.51 | 1.44 | 1.53 | ||

| 1000 | 0.15 | 0.25 | 0.06 | 0.36 | 0.40 | 0.32 | 0.32 | 0.31 | 0.32 | 0.93 | 0.88 | 0.95 | 1.30 | 1.24 | 1.28 | ||

| 0.10 | 0.74 | 1500 | 0.11 | 0.20 | 0.03 | 0.33 | 0.36 | 0.31 | 0.31 | 0.30 | 0.31 | 0.94 | 0.88 | 0.93 | 1.17 | 1.13 | 1.15 |

| 500 | 0.21 | 0.31 | 0.06 | 0.45 | 0.49 | 0.41 | 0.40 | 0.38 | 0.40 | 0.92 | 0.86 | 0.95 | 1.55 | 1.48 | 1.58 | ||

| 1000 | 0.18 | 0.28 | 0.09 | 0.37 | 0.42 | 0.33 | 0.32 | 0.31 | 0.32 | 0.92 | 0.87 | 0.95 | 1.34 | 1.28 | 1.33 | ||

| 0.25 | 0.94 | 1500 | 0.12 | 0.21 | 0.04 | 0.34 | 0.37 | 0.32 | 0.32 | 0.31 | 0.31 | 0.92 | 0.86 | 0.94 | 1.22 | 1.17 | 1.20 |

| Setting 3: exactly sparse | |||||||||||||||||

| Bias | RMSE | SE | Coverage | CI Length | |||||||||||||

| True | DLL | Plug | Orac | DLL | Plug | Orac | DLL | Plug | Orac | DLL | Plug | Orac | DLL | Plug | Orac | ||

| 500 | 0.12 | 0.24 | 0.01 | 0.72 | 0.74 | 0.69 | 0.71 | 0.70 | 0.69 | 0.94 | 0.92 | 0.93 | 2.81 | 2.73 | 2.60 | ||

| 1000 | 0.05 | 0.19 | 0.05 | 0.64 | 0.66 | 0.60 | 0.63 | 0.63 | 0.60 | 0.95 | 0.93 | 0.95 | 2.42 | 2.39 | 2.26 | ||

| 0.10 | 1.49 | 1500 | 0.04 | 0.15 | 0.02 | 0.57 | 0.58 | 0.55 | 0.57 | 0.56 | 0.55 | 0.96 | 0.94 | 0.95 | 2.19 | 2.16 | 2.05 |

| 500 | 0.08 | 0.21 | 0.00 | 0.73 | 0.74 | 0.68 | 0.72 | 0.71 | 0.68 | 0.94 | 0.93 | 0.94 | 2.79 | 2.73 | 2.59 | ||

| 1000 | 0.04 | 0.17 | 0.03 | 0.62 | 0.64 | 0.58 | 0.62 | 0.62 | 0.58 | 0.95 | 0.94 | 0.95 | 2.41 | 2.38 | 2.25 | ||

| 0.25 | 1.45 | 1500 | 0.03 | 0.15 | 0.02 | 0.56 | 0.57 | 0.52 | 0.56 | 0.55 | 0.52 | 0.95 | 0.93 | 0.94 | 2.18 | 2.14 | 2.04 |

| Setting 4: exactly sparse with df=10 | |||||||||||||||||

| Bias | RMSE | SE | Coverage | CI Length | |||||||||||||

| True | DLL | Plug | Orac | DLL | Plug | Orac | DLL | Plug | Orac | DLL | Plug | Orac | DLL | Plug | Orac | ||

| 500 | 0.17 | 0.36 | 0.04 | 0.38 | 0.49 | 0.33 | 0.34 | 0.33 | 0.32 | 0.92 | 0.78 | 0.95 | 1.33 | 1.27 | 1.32 | ||

| 1000 | 0.10 | 0.28 | 0.03 | 0.30 | 0.40 | 0.28 | 0.29 | 0.28 | 0.28 | 0.94 | 0.80 | 0.95 | 1.13 | 1.06 | 1.06 | ||

| 0.10 | 1.49 | 1500 | 0.06 | 0.23 | 0.02 | 0.25 | 0.34 | 0.23 | 0.24 | 0.24 | 0.23 | 0.96 | 0.83 | 0.97 | 1.00 | 0.94 | 0.92 |

| 500 | 0.18 | 0.38 | 0.05 | 0.40 | 0.51 | 0.36 | 0.35 | 0.35 | 0.35 | 0.89 | 0.76 | 0.94 | 1.34 | 1.28 | 1.34 | ||

| 1000 | 0.10 | 0.29 | 0.01 | 0.30 | 0.41 | 0.28 | 0.29 | 0.28 | 0.28 | 0.93 | 0.78 | 0.93 | 1.14 | 1.07 | 1.08 | ||

| 0.25 | 1.45 | 1500 | 0.06 | 0.24 | 0.01 | 0.25 | 0.35 | 0.24 | 0.24 | 0.24 | 0.24 | 0.96 | 0.83 | 0.96 | 1.01 | 0.95 | 0.94 |

4.2 Comparison with the ReSmoothing method

We compare DLL with the RS estimator [27] and generate the data as in Setting 1 with and . We construct two CIs centered at the RS estimator,

- (a)

-

(b)

OraRS confidence interval: we estimate the standard error of the RS estimator by the sample standard deviation of 500 RS estimates and then construct the confidence interval by assuming the asymptotic normality of the RS estimator.

The RS confidence interval does not necessarily achieve the correct coverage since are not i.i.d. The OraRS is not a practical inference procedure, but a favorable implementation of the confidence interval based on the RS estimator as its standard error is computed in an oracle way.

| Setting 1, exactly sparse: Comparison with ReSmoothing | |||||||||||||||

| Bias | SE | Coverage | Length | ||||||||||||

| DLL | RS | Orac | DLL | RS | Orac | DLL | RS | OraRS | Orac | DLL | RS | OraRS | Orac | ||

| 500 | 0.20 | 0.91 | 0.01 | 0.42 | 0.83 | 0.41 | 0.94 | 0.01 | 0.80 | 0.96 | 1.69 | 0.04 | 3.24 | 1.68 | |

| 750 | 0.07 | 0.69 | 0.01 | 0.40 | 0.90 | 0.39 | 0.93 | 0.01 | 0.88 | 0.95 | 1.55 | 0.02 | 3.53 | 1.51 | |

| -1.0 | 1000 | 0.05 | 0.53 | 0.01 | 0.35 | 0.89 | 0.35 | 0.96 | 0.01 | 0.92 | 0.95 | 1.46 | 0.02 | 3.48 | 1.42 |

| 500 | 0.20 | 0.97 | 0.02 | 0.42 | 0.78 | 0.41 | 0.92 | 0.01 | 0.78 | 0.95 | 1.69 | 0.04 | 3.06 | 1.68 | |

| 750 | 0.09 | 0.66 | 0.01 | 0.39 | 0.91 | 0.40 | 0.95 | 0.01 | 0.89 | 0.93 | 1.57 | 0.02 | 3.57 | 1.53 | |

| 0.5 | 1000 | 0.09 | 0.51 | 0.03 | 0.37 | 0.87 | 0.37 | 0.94 | 0.01 | 0.92 | 0.95 | 1.46 | 0.02 | 3.41 | 1.41 |

| Setting 1, approximately sparse: Comparison with ReSmoothing | |||||||||||||||

| Bias | SE | Coverage | Length | ||||||||||||

| DLL | RS | Orac | DLL | RS | Orac | DLL | RS | OraRS | Orac | DLL | RS | OraRS | Orac | ||

| 500 | 0.26 | 0.80 | 0.02 | 0.39 | 0.46 | 0.46 | 0.86 | 0.00 | 0.65 | 0.91 | 1.46 | 0.02 | 1.81 | 1.67 | |

| 750 | 0.18 | 0.73 | 0.01 | 0.35 | 0.63 | 0.38 | 0.94 | 0.00 | 0.80 | 0.95 | 1.42 | 0.01 | 2.46 | 1.51 | |

| -1.0 | 1000 | 0.12 | 0.66 | 0.01 | 0.35 | 0.73 | 0.38 | 0.94 | 0.00 | 0.86 | 0.93 | 1.37 | 0.01 | 2.87 | 1.42 |

| 500 | 0.29 | 1.08 | 0.02 | 0.40 | 0.44 | 0.46 | 0.86 | 0.00 | 0.26 | 0.93 | 1.47 | 0.02 | 1.72 | 1.68 | |

| 750 | 0.23 | 0.96 | 0.03 | 0.38 | 0.60 | 0.40 | 0.89 | 0.00 | 0.63 | 0.94 | 1.43 | 0.01 | 2.34 | 1.53 | |

| 0.5 | 1000 | 0.14 | 0.78 | 0.00 | 0.33 | 0.73 | 0.35 | 0.94 | 0.01 | 0.81 | 0.95 | 1.37 | 0.01 | 2.88 | 1.41 |

As reported in Table 3, our proposed DLL has a much smaller bias than the RS estimator. In terms of coverage, the OraRS confidence interval does not achieve the desired coverage level, even if its standard error is computed in an oracle way. In contrast, our proposed CI achieves the desired coverage level in most settings. The undercoverage of the OraRS method happens mainly because of the large bias of the RS estimator. We shall further point out that our proposed CI has a similar length to the oracle CI (the benchmark), but the OraRS confidence interval is much wider than our proposed CI and the oracle CI. See Section F.4 in the supplement for results with exchanging the roles of and .

4.3 Non-linear treatment model

In this section, we explore the performance of the generalized DLL estimator proposed in Section 2.6, which decorrelates with the sparse additive model. The estimator is referred to as DLL-S. As the main difference, DLL is using the Lasso algorithm to fit the treatment model while DLL-S is using the sparse additive model. We generate following the same distribution as in Setting 1 but generate as with . The outcome model is generated following the exactly sparse model. We also consider the setting with switching the roles of and here. The results are reported in Table 4.

| Non-linear Treatment Model, exactly sparse: | ||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Bias | Coverage | Length | ||||||||||||

| True | DLL | DLL-S | Plug | Orac | DLL | DLL-S | Plug | Orac | DLL | DLL-S | Plug | Orac | ||

| 500 | 0.31 | 0.23 | 0.37 | 0.01 | 0.84 | 0.91 | 0.78 | 0.95 | 1.40 | 1.44 | 1.34 | 1.50 | ||

| 1000 | 0.20 | 0.12 | 0.25 | 0.00 | 0.87 | 0.93 | 0.83 | 0.95 | 1.24 | 1.24 | 1.18 | 1.25 | ||

| 1500 | 0.18 | 0.10 | 0.23 | 0.03 | 0.92 | 0.95 | 0.88 | 0.96 | 1.12 | 1.14 | 1.07 | 1.12 | ||

| 0.10 | 1.49 | 2000 | 0.13 | 0.08 | 0.17 | 0.00 | 0.91 | 0.94 | 0.87 | 0.94 | 1.05 | 1.05 | 1.01 | 1.05 |

| 500 | 0.33 | 0.23 | 0.39 | 0.06 | 0.80 | 0.87 | 0.74 | 0.94 | 1.34 | 1.36 | 1.28 | 1.42 | ||

| 1000 | 0.19 | 0.12 | 0.24 | 0.01 | 0.90 | 0.92 | 0.85 | 0.95 | 1.17 | 1.18 | 1.12 | 1.19 | ||

| 1500 | 0.16 | 0.10 | 0.21 | 0.02 | 0.92 | 0.95 | 0.87 | 0.95 | 1.06 | 1.07 | 1.02 | 1.06 | ||

| 0.25 | 1.45 | 2000 | 0.13 | 0.08 | 0.18 | 0.00 | 0.91 | 0.95 | 0.87 | 0.95 | 1.00 | 0.99 | 0.95 | 0.99 |

| Non-linear Treatment Model, exactly sparse: | ||||||||||||||

| Bias | Coverage | Length | ||||||||||||

| True | DLL | DLL-S | Plug | Orac | DLL | DLL-S | Plug | Orac | DLL | DLL-S | Plug | Orac | ||

| 500 | 0.10 | 0.08 | 0.14 | 0.01 | 0.94 | 0.92 | 0.92 | 0.94 | 1.00 | 1.02 | 0.96 | 1.00 | ||

| 1000 | 0.08 | 0.06 | 0.12 | 0.00 | 0.92 | 0.95 | 0.90 | 0.94 | 0.85 | 0.87 | 0.83 | 0.84 | ||

| 1500 | 0.05 | 0.05 | 0.10 | 0.00 | 0.95 | 0.95 | 0.93 | 0.94 | 0.78 | 0.79 | 0.76 | 0.77 | ||

| 0.10 | -0.95 | 2000 | 0.05 | 0.03 | 0.10 | 0.01 | 0.95 | 0.94 | 0.92 | 0.95 | 0.73 | 0.74 | 0.71 | 0.72 |

| 500 | 0.11 | 0.10 | 0.15 | 0.00 | 0.92 | 0.92 | 0.88 | 0.95 | 0.94 | 0.96 | 0.91 | 0.94 | ||

| 1000 | 0.09 | 0.07 | 0.13 | 0.02 | 0.93 | 0.92 | 0.90 | 0.94 | 0.81 | 0.82 | 0.79 | 0.80 | ||

| 1500 | 0.04 | 0.06 | 0.09 | 0.01 | 0.94 | 0.93 | 0.91 | 0.93 | 0.74 | 0.75 | 0.72 | 0.73 | ||

| 0.25 | -0.88 | 2000 | 0.04 | 0.05 | 0.09 | 0.01 | 0.95 | 0.93 | 0.93 | 0.95 | 0.69 | 0.70 | 0.68 | 0.68 |

In Table 4, we observe that DLL-S improves the performance of DLL in terms of bias correction and empirical coverage. However, the regular DLL still corrects the bias of the plug-in estimator and achieves better coverage than the CI by the plug-in estimator. See Section F.1 in the supplement for results with additional evaluation points.

5 Real data analysis

The Motif Regression has important applications to biology, which studies the effect of the motif candidates’ matching scores on the gene expression level [59, 2, 17, 18]. Motifs are the DNA sequences bound to transcription factors, which control the transcription activities, e.g., gene expressions [59]. The matching score of a motif describes the abundance of occurrence, that is, how well the motif is represented in the upstream regions of the genes. A gene’s expression level can be well-predicted by the matching scores of a set of motifs [59, 2, 17, 18]. The data set consists of the expression values of genes and the scores of motifs. For our analysis, the outcome denote the gene expression level and are the matching scores of the 666 motifs.

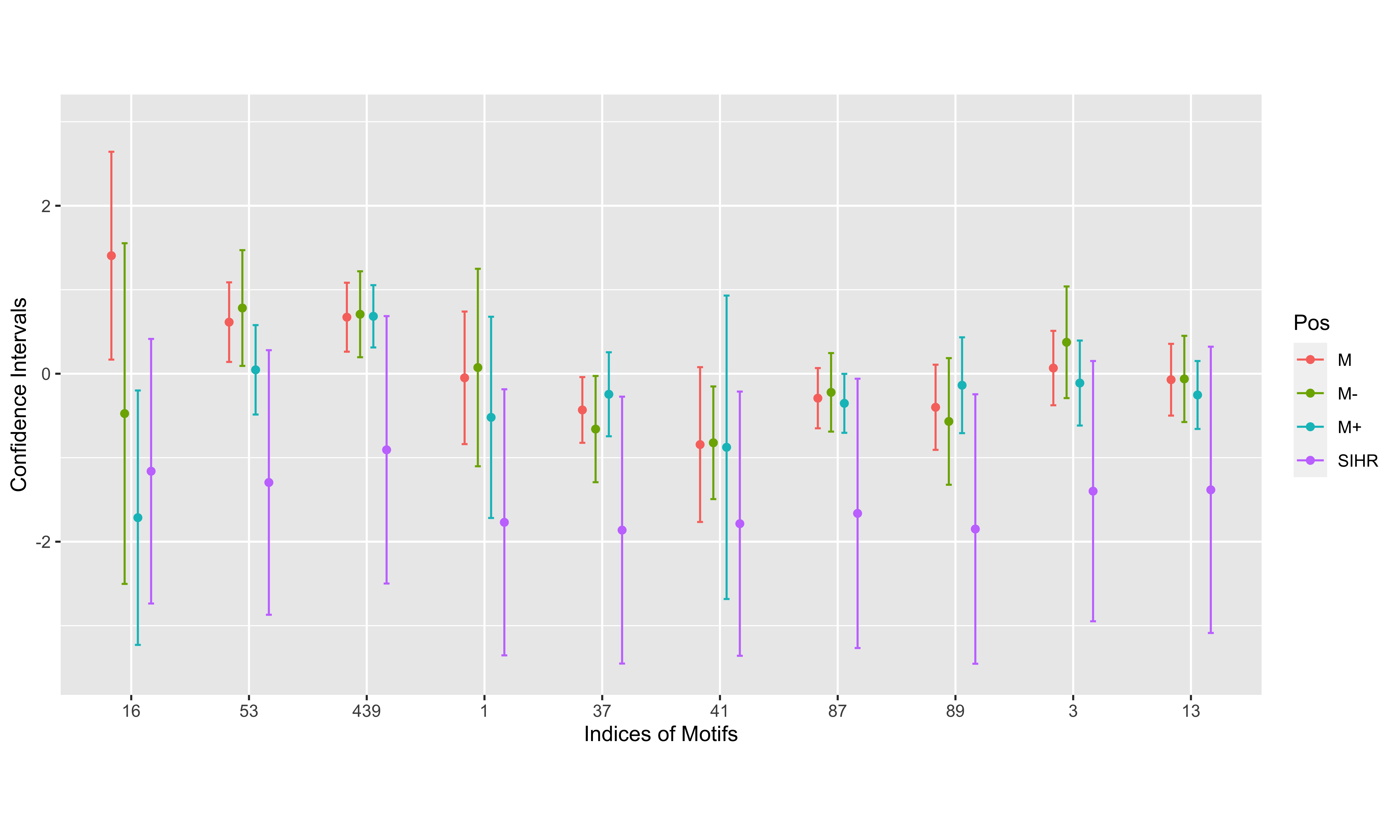

We define an index subset for the motifs To demonstrate our method, we choose one index from and set the corresponding motif score as the variable of interest and the remaining motif scores as the baseline covariates. We compute its sample mean and standard error for a chosen variable of interest. We choose three different evaluation points : mean, mean + standard error, mean - standard error. To demonstrate our method, we compare it with the existing inference method for the high-dimensional linear model, which assumes the linear and constant effect. Specifically, we apply the LF() function in the R package SIHR [45] and denote the corresponding estimator as SIHR. We report the comparison in Figure 1.

Figure 1 demonstrates several interesting observations. First of all, the CI lengths assuming the linear models are in general longer than those of DLL. This happens since the standard deviation of the regression error is about 2.5 by SIHR (assuming the linear model) but 1.45 by DLL (assuming the additive model). This indicates that the relationship between the gene expression levels and the motifs is highly non-linear. For constructing the local linear estimator, the DLL estimator only uses about 40% of the data while the SIHR estimator is computed with all data points.

Second, for the motifs with indexes 16, 53, and 439, we observe that those motifs do not have significant effects if we assume the effects to be linear. In contrast, our DLL estimator shows that they might have heterogeneous non-linear effects; for example, for motif 16, the CI at M- location is above zero while the CI at M+ is below zero. Lastly, the motifs with indexes 1, 37, 41, and 87 have significant linear effects, but their non-linear effects vary across different evaluation points.

We design a semi-real simulation study to further compare the finite-sample performance of our proposed DLL method and the SIHR method. We keep the data the same as the real data. After analyzing the original real data, we construct the noise level estimator and and . We simulate the synthetic response variable for with the i.i.d. regression error terms following . We repeat the simulation 500 times and evaluate DLL on the same three evaluation points as in the real data analysis.

We compare the results with SIHR and report the comparison in Table 5. The SIHR method, which assumes the linear outcome model, suffers from a large absolute bias and low empirical coverage. Our proposed CIs by the DLL estimators achieve the desired coverage levels in most settings. The lengths of our proposed CIs are, in general, shorter or comparable to the CI output by SIHR. This happens since the regression noise level by SIHR is much larger than the true noise level due to the model misspecification. This matches with the observations for the original real data.

| Bias | SE | Coverage | Length | |||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Motif | M | M+ | M- | SIHR | M | M+ | M- | SIHR | M | M+ | M- | SIHR | M | M+ | M- | SIHR |

| 1 | 0.08 | 0.15 | 0.14 | 1.37 | 0.23 | 0.45 | 0.32 | 0.41 | 0.93 | 0.87 | 0.94 | 0.45 | 0.94 | 1.73 | 1.19 | 2.66 |

| 3 | 0.00 | 0.01 | 0.05 | 1.39 | 0.22 | 0.39 | 0.32 | 0.43 | 0.96 | 0.95 | 0.93 | 0.45 | 0.93 | 1.34 | 1.09 | 2.70 |

| 13 | 0.06 | 0.09 | 0.02 | 1.35 | 0.27 | 0.41 | 0.31 | 0.42 | 0.96 | 0.96 | 0.97 | 0.59 | 1.12 | 1.61 | 1.18 | 2.88 |

| 16 | 0.24 | 0.26 | 0.00 | 1.30 | 0.36 | 0.71 | 0.45 | 0.40 | 0.87 | 0.94 | 0.98 | 0.53 | 1.03 | 2.28 | 2.07 | 2.66 |

| 37 | 0.09 | 0.15 | 0.33 | 1.44 | 0.20 | 0.55 | 0.53 | 0.42 | 0.93 | 0.95 | 0.95 | 0.44 | 0.77 | 2.20 | 2.16 | 2.75 |

| 41 | 0.15 | 0.06 | 0.07 | 1.36 | 0.42 | 0.36 | 0.85 | 0.41 | 0.97 | 0.96 | 0.95 | 0.47 | 1.86 | 1.45 | 3.31 | 2.66 |

| 53 | 0.22 | 0.12 | 0.08 | 1.35 | 0.25 | 0.36 | 0.27 | 0.41 | 0.89 | 0.94 | 0.96 | 0.49 | 0.93 | 1.30 | 1.02 | 2.66 |

| 87 | 0.06 | 0.03 | 0.18 | 1.49 | 0.22 | 0.33 | 0.27 | 0.43 | 0.95 | 0.95 | 0.90 | 0.36 | 0.88 | 1.31 | 1.01 | 2.70 |

| 89 | 0.04 | 0.07 | 0.12 | 1.50 | 0.27 | 0.43 | 0.34 | 0.41 | 0.95 | 0.95 | 0.93 | 0.35 | 1.06 | 1.54 | 1.21 | 2.78 |

| 439 | 0.01 | 0.05 | 0.05 | 1.46 | 0.29 | 0.44 | 0.29 | 0.43 | 0.92 | 0.92 | 0.96 | 0.39 | 0.99 | 1.51 | 1.19 | 2.69 |

6 Conclusion and discussion

We have proposed the decorrelated local linear estimator to mitigate the error caused by estimating the unknown nuisance functions in the high-dimensional additive model. We have established the asymptotic normality of our proposed estimator. We demonstrate the validity of the theoretical results in moderate samples sizes and provide practical recommendations for the algorithm implementation. Our proposed decorrelation idea is a novel and computationally efficient method designed for bias correction in non-parametric models. An interesting future research direction is extending our proposed method to accommodate other kernel functions and higher-order local polynomials. In addition to inference for there are other interesting statistical inference problems in the high-dimensional additive model, including confidence interval construction for and the significance test . We leave these problems for future research.

References

- [1] Susan Athey, Guido W Imbens, and Stefan Wager. Approximate residual balancing: debiased inference of average treatment effects in high dimensions. Journal of the Royal Statistical Society: Series B (Statistical Methodology), 80(4):597–623, 2018.

- [2] Michael A Beer and Saeed Tavazoie. Predicting gene expression from sequence. Cell, 117(2):185–198, 2004.

- [3] Alexandre Belloni, Victor Chernozhukov, Denis Chetverikov, and Kengo Kato. Some new asymptotic theory for least squares series: Pointwise and uniform results. Journal of Econometrics, 186(2):345–366, 2015.

- [4] Alexandre Belloni, Victor Chernozhukov, Ivan Fernández-Val, and Christian Hansen. Program evaluation and causal inference with high-dimensional data. Econometrica, 85(1):233–298, 2017.

- [5] Alexandre Belloni, Victor Chernozhukov, and Christian Hansen. Inference on treatment effects after selection among high-dimensional controls. The Review of Economic Studies, 81(2):608–650, 2014.

- [6] George Bennett. Probability inequalities for the sum of independent random variables. Journal of the American Statistical Association, 57(297):33–45, 1962.

- [7] Peter J Bickel, Ya’acov Ritov, and Alexandre B Tsybakov. Simultaneous analysis of lasso and dantzig selector. The Annals of statistics, 37(4):1705–1732, 2009.

- [8] Andreas Buja, Trevor Hastie, and Robert Tibshirani. Linear smoothers and additive models. The Annals of Statistics, 17(2):453–510, 1989.

- [9] Jorge Luis Ojeda Cabrera. locpol: Kernel Local Polynomial Regression, 2018. R package version 0.7-0.

- [10] T Tony Cai and Zijian Guo. Confidence intervals for high-dimensional linear regression: Minimax rates and adaptivity. The Annals of Statistics, 45(2):615–646, 2017.

- [11] Tianxi Cai, T Tony Cai, and Zijian Guo. Optimal statistical inference for individualized treatment effects in high-dimensional models. Journal of the Royal Statistical Society: Series B (Statistical Methodology), 83(4):669–719, 2021.

- [12] Sebastian Calonico, Matias D. Cattaneo, and Max H. Farrell. nprobust: Nonparametric kernel-based estimation and robust bias-corrected inference. Journal of Statistical Software, 91(8):1–33, 2019.

- [13] David Card. Estimating the return to schooling: Progress on some persistent econometric problems. Econometrica, 69(5):1127–1160, 2001.

- [14] Victor Chernozhukov, Denis Chetverikov, Mert Demirer, Esther Duflo, Christian Hansen, Whitney Newey, and James Robins. Double/debiased machine learning for treatment and structural parameters. The Econometrics Journal, 21(1):C1–C68, 2018.

- [15] Victor Chernozhukov, Christian Hansen, and Martin Spindler. Valid post-selection and post-regularization inference: An elementary, general approach. 2015.

- [16] William S Cleveland. Robust locally weighted regression and smoothing scatterplots. Journal of the American statistical association, 74(368):829–836, 1979.

- [17] Erin M Conlon, X Shirley Liu, Jason D Lieb, and Jun S Liu. Integrating regulatory motif discovery and genome-wide expression analysis. Proceedings of the National Academy of Sciences, 100(6):3339–3344, 2003.

- [18] Debopriya Das, Nilanjana Banerjee, and Michael Q Zhang. Interacting models of cooperative gene regulation. Proceedings of the National Academy of Sciences, 101(46):16234–16239, 2004.

- [19] Melissa Dell, Benjamin F Jones, and Benjamin A Olken. What do we learn from the weather? the new climate-economy literature. Journal of Economic Literature, 52(3):740–98, 2014.

- [20] Olivier Deschênes and Michael Greenstone. The economic impacts of climate change: evidence from agricultural output and random fluctuations in weather: reply. American Economic Review, 102(7):3761–73, 2012.

- [21] Jianqing Fan. Design-adaptive nonparametric regression. Journal of the American statistical Association, 87(420):998–1004, 1992.

- [22] Jianqing Fan. Local linear regression smoothers and their minimax efficiencies. The Annals of Statistics, 21(1):196–216, 1993.

- [23] Jianqing Fan and Irene Gijbels. Local Polynomial Modelling and Its Applications: Monographs on Statistics and Applied Probability 66, volume 66. CRC Press, 1996.

- [24] Max H Farrell. Robust inference on average treatment effects with possibly more covariates than observations. Journal of Econometrics, 189(1):1–23, 2015.

- [25] Jerome Friedman, Trevor Hastie, and Robert Tibshirani. Regularization paths for generalized linear models via coordinate descent. Journal of Statistical Software, 33(1):1–22, 2010.

- [26] Theo Gasser and Hans-Georg Müller. Estimating regression functions and their derivatives by the kernel method. Scandinavian Journal of Statistics, pages 171–185, 1984.

- [27] Karl Gregory, Enno Mammen, and Martin Wahl. Statistical inference in sparse high-dimensional additive models. The Annals of Statistics, 49(3):1514–1536, 2021.

- [28] Zijian Guo and Cun-Hui Zhang. Extreme nonlinear correlation for multiple random variables and stochastic processes with applications to additive models. arXiv preprint arXiv:1904.12897, 2019.

- [29] Trevor Hastie and Robert Tibshirani. Generalized additive models. Statistical Science, 1(3):297–318, 1986.

- [30] Tristen Hayfield and Jeffrey S. Racine. Nonparametric econometrics: The np package. Journal of Statistical Software, 27(5), 2008.

- [31] Miguel A Hernán and James M Robins. Causal inference, 2010.

- [32] Joel L Horowitz and Enno Mammen. Nonparametric estimation of an additive model with a link function. The Annals of Statistics, 32(6):2412–2443, 2004.

- [33] Guido W Imbens and Donald B Rubin. Causal inference in statistics, social, and biomedical sciences. Cambridge University Press, 2015.

- [34] Adel Javanmard and Andrea Montanari. Confidence intervals and hypothesis testing for high-dimensional regression. The Journal of Machine Learning Research, 15(1):2869–2909, 2014.

- [35] Haoming Jiang, Yukun Ma, Han Liu, Kathryn Roeder, Xingguo Li, and Tuo Zhao. SAM: Sparse Additive Modelling, 2021. R package version 1.1.3.

- [36] Chris AJ Klaassen. Consistent estimation of the influence function of locally asymptotically linear estimators. The Annals of Statistics, pages 1548–1562, 1987.

- [37] Vladimir Koltchinskii and Ming Yuan. Sparsity in multiple kernel learning. The Annals of Statistics, 38(6):3660–3695, 2010.

- [38] Junwei Lu, Mladen Kolar, and Han Liu. Kernel meets sieve: Post-regularization confidence bands for sparse additive model. Journal of the American Statistical Association, 115(532):2084–2099, 2020.

- [39] Enno Mammen, Oliver Linton, and J Nielsen. The existence and asymptotic properties of a backfitting projection algorithm under weak conditions. The Annals of Statistics, 27(5):1443–1490, 1999.

- [40] Lukas Meier, Sara Van de Geer, and Peter Bühlmann. High-dimensional additive modeling. The Annals of Statistics, 37(6B):3779–3821, 2009.

- [41] Yang Ning and Han Liu. A general theory of hypothesis tests and confidence regions for sparse high dimensional models. The Annals of Statistics, 45(1):158–195, 2017.

- [42] Jean D Opsomer. Asymptotic properties of backfitting estimators. Journal of Multivariate Analysis, 73(2):166–179, 2000.

- [43] Judea Pearl. Causality. Cambridge university press, 2009.

- [44] Gengsheng Qin and Min Tsao. Empirical likelihood based inference for the derivative of the nonparametric regression function. Bernoulli, 11(4):715–735, 2005.

- [45] Prabrisha Rakshit, T. Tony Cai, and Zijian Guo. Sihr: An r package for statistical inference in high-dimensional linear and logistic regression models, 2021.

- [46] Garvesh Raskutti, Martin J Wainwright, and Bin Yu. Minimax-optimal rates for sparse additive models over kernel classes via convex programming. Journal of Machine Learning Research, 13(Feb):389–427, 2012.

- [47] Pradeep Ravikumar, John Lafferty, Han Liu, and Larry Wasserman. Sparse additive models. Journal of the Royal Statistical Society: Series B (Statistical Methodology), 71(5):1009–1030, 2009.

- [48] Anton Schick. On asymptotically efficient estimation in semiparametric models. The Annals of Statistics, 14(3):1139–1151, 1986.

- [49] Wolfram Schlenker and Michael J Roberts. Estimating the impact of climate change on crop yields: The importance of nonlinear temperature effects. Technical report, National Bureau of Economic Research, 2008.

- [50] Charles J Stone. Consistent nonparametric regression. The Annals of Statistics, 5(4):595–620, 1977.

- [51] Taiji Suzuki and Masashi Sugiyama. Fast learning rate of multiple kernel learning: Trade-off between sparsity and smoothness. The Annals of Statistics, pages 1381–1405, 2013.

- [52] Zhiqiang Tan and Cun-Hui Zhang. Doubly penalized estimation in additive regression with high-dimensional data. The Annals of Statistics, 47(5):2567–2600, 2019.

- [53] Alexandre B Tsybakov. Introduction to nonparametric estimation., 2009.

- [54] Sara van de Geer, Peter Bühlmann, Yaacov Ritov, and Ruben Dezeure. On asymptotically optimal confidence regions and tests for high-dimensional models. The Annals of Statistics, 42(3):1166–1202, 2014.

- [55] Simon N Wood. Generalized additive models: an introduction with R. Chapman and Hall/CRC, 2017.

- [56] David A Wooff. Bounds on reciprocal moments with applications and developments in stein estimation and post-stratification. Journal of the Royal Statistical Society: Series B (Methodological), 47(2):362–371, 1985.

- [57] Yun Yang and Surya T Tokdar. Minimax-optimal nonparametric regression in high dimensions. The Annals of Statistics, 43(2):652–674, 2015.

- [58] Ming Yuan and Ding-Xuan Zhou. Minimax optimal rates of estimation in high dimensional additive models. The Annals of Statistics, 44(6):2564–2593, 2016.

- [59] Yuan Yuan, Lei Guo, Lei Shen, and Jun S Liu. Predicting gene expression from sequence: A reexamination. PLOS Computational Biology, 3(11):1–7, 11 2007.

- [60] Cun-Hui Zhang and Stephanie S Zhang. Confidence intervals for low dimensional parameters in high dimensional linear models. Journal of the Royal Statistical Society: Series B (Statistical Methodology), 76(1):217–242, 2014.

- [61] Shanggang Zhou and Douglas A Wolfe. On derivative estimation in spline regression. Statistica Sinica, pages 93–108, 2000.

- [62] Yinchu Zhu and Jelena Bradic. Linear hypothesis testing in dense high-dimensional linear models. Journal of the American Statistical Association, 113(524):1583–1600, 2018.

- [63] Ying Zhu, Zhuqing Yu, and Guang Cheng. High dimensional inference in partially linear models. In The 22nd International Conference on Artificial Intelligence and Statistics, pages 2760–2769. PMLR, 2019.

Appendix A Additional Discussions

A.1 Algorithm without Data Swapping

In this section, we present the DLL estimator without data swapping. Different from the DLL estimator with data swapping, we use all the samples, rather than half of them, when fitting the sparse additive model and constructing the decorrelation weights. Following the steps of Algorithm 1, we make a few changes to implement the DLL estimator without data swapping.

In Step 1, implement the sparse additive model as the following optimization problem with and :

| (31) |

In Step 2, construct the initial estimator as:

| (32) |

In Step 5, implement Lasso algorithm as follows with the tuning parameter :

and compute

In Step 6, construct and the weights as:

A.2 Double Penalization

In the following, we review the double penalization method [52] to construct initial estimators of and . This can be viewed as an alternative method to the estimators in (31) and (32). To construct the penalty term, we define the complexity measure of a univariate function as

| (33) |

where , , denotes the function’s empirical norm, and is a measure of the function’s smoothness.

Specifically, with the positive tuning parameters and , we define the initial estimators as

where the complexity measure is defined in (33).

A.3 Initial Estimators with Quantile Transformation

We consider the construction of the initial estimator by applying the quantile transformation to all variables. Particularly, we transform to , with

similarly, for we transform to , with

We construct the initial estimators and by applying the sparse additive algorithm to . Except for constructing the initial estimator differently, the other steps are the same as those in Algorithm 1. This DLL estimator with the extra quantile transformation is refered to as Trans and we do not apply the data swapping for Trans estimator. We compare the performance of Trans with the regular DLL estimator in Section F.3; see Tables S10 and S11 for details.

A.4 Further discussions on the Condition (A3)

In a more general setting, we may plug-in the existing convergence rate of and then the condition (27) is reduced to a simultaneous condition on and , where denotes the number of non-zero functions of Particularly, we follow [52] by assuming that the individual functions belong to the Sobolev space for and is continuous. We apply Proposition 4 and Theorem 2 in [52] and Corollaries 4 and 5 in [28] and establish that

Then the condition (27) is simplified as

If we set , then the above sparsity condition is much weaker than the one in [27], which requires and up to a polynomial order of

A.5 Consistent estimators of

Similar to the definition of in (26), we use to denote the accuracy measure of , which is defined as follows: with probability larger than for some positive constant

| (34) |

where and are defined in (22) and the expectation is taken with respect to the independent copy of

Proposition 1

Suppose that Condition (A1) holds and Then the estimator defined in (23) satisfies

Appendix B Notations, Events and Lemmas

We introduce some notations and events, which will be used throughout the proof. Let denote the conditional distribution of given and denote the density function of the error Since is independent of , we have

We express the density function of the random variable as

Define the following events,

| (35) | ||||

By the definitions of and in (24), we have for some positive constant Throughout the proof, we shall assume and this will automatically hold in our considered regime.

Define . Theorem 7.2 in [7] implies that the Lasso estimator satisfies

for some positive constant . Conditioning on the data in , the random variable is sub-gaussian random variable, which implies

for some positive constant Note that

The above two inequalities imply that, there exists a constant independent of and such that

for some positive constant Together with the definition in (24) and (26), we establish

| (36) |

The following lemma states the expectation of terms involved with , whose proof can be found in Section E.2.

Lemma 1

Suppose that Condition (A2) holds, then we have

| (37) |

| (38) |

| (39) |

| (40) |

| (41) |

| (42) |

| (43) |

| (44) |

The following lemma is about the concentration results for terms involved with , whose proof can be found in Section E.3.

Lemma 2

Suppose that Condition (A2) holds, then for a sufficiently large , with probability ,

| (45) |

| (46) |

| (47) |

| (48) |

| (49) |

| (50) |

Appendix C Proof of Theorem 2

Recall the definition of in (15). We define an accuracy measure of estimating the decorrelation weights as

| (52) |

We first introduce the following important intermediate results. With probability larger than for some and positive constants ,

| (53) |

| (54) |

and

| (55) |

A combination of (54) and (55) leads to the bound (29). We shall prove (53), (54), and (55) in Sections C.1, C.2, and C.3, respectively.

C.1 Proof of (53)

Recall the following notations,

-

•

and are two disjoint subsets with approximately equal sample size, with empty and

-

•

and denote the initial estimator of based on the data and , respectively.

The proof relies on the independence created by data swapping. Define the estimation error as and We write , and as the expectation, variance and probability conditioning on the sample respectively. Similarly, we define and conditioning on . For , we have the following decomposition

| (56) |

We will control the first term in the following and the second term can be controlled by a similar argument. Since

it is sufficient to analyze

where and are defined in (35). The above term has two sources of randomness: the initial estimator and the data . Since the randomness of is induced from the data , the estimation error is independent of the data .

C.2 Proof of (54)

We decompose as

| (58) |

By the Cauchy-Schwarz inequality, we have

| (59) |

where is defined in (52). Hence, it is sufficient to control Similar to (56), we have

| (60) |

and it is sufficient to control

Note that

where the last inequality follows from (37) and the bounded conditional density The above moment bound implies

By symmetry and the decomposition (60), we have

| (61) |

Combined with (59), we obtain

| (62) |

Note that

Together with (45), (51), and (61), we establish

Together with (53), (62) and the decomposition (58), we have

C.3 Proof of (55)

In the following, we first establish

| (63) |

Recall that the uncentered weight is defined in (14) and is the corresponding centered weight defined in (15). Note that

| (64) |

By Cauchy-Schwarz inequality

we have

By applying the above inequality and (64), we obtain

By the definitions and the above inequality implies (63).

Then the proof of (55) is reduced to establishing an upper bound for

We divide the above summation into two parts,

By symmetry, we focus on the first summation

| (65) |

and adopt the notation We note that

On the event defined in (35), we have

| (66) |

To facilitate the discussion, we introduce the following notations,

| (67) |

The estimator defined in (13) can be written as

| (68) |

The randomness of comes from the following three parts,

-

•

the noise

-

•

the variable with for the pre-fixed index

-

•

the estimation error , which depends on and the initial estimator computed on the data .

Note that is independent of the other two random sources. We shall write as the expectation with respect to but condition on the other two components and . We use to denote the conditional expectation by only considering the randomness of . Specifically, for , and are shorthanded for

We use to denote the conditional expectation of given the events by only considering the randomness of that is

We compute the following difference,

| (69) | ||||

Define

| (70) |

Note that

| (71) |

By (68), (69), and (71), we establish

| (72) | ||||

where the last component holds since defined in (70) does not depend on the index .

The decomposition (72) and the following two inequalities lead to an upper bound for (65).

| (73) |

and

| (74) | ||||

We establish (55) by combining (63), (72), (73), (74), and (36).

C.3.1 Proof of (73)

In the following proof, we fix and For with

and

By the above two expressions, we obtain

| (75) | ||||

We further take expectation with respect to (but conditioning on and ) in (75) and obtain that

| (76) |

Conditioning on and we define the conditional probability with respect to as

| (77) |

By change of variable , we have

for some constant Hence, we have

and then

Hence, we establish

| (78) |

We note that the non-negative random variable satisfies

and

Hence, we apply the equation (5) in [56] and obtain

| (79) | ||||

A combination of (76), (78) and (79) leads to

| (80) |

By taking expectation with respect to and we establish (73).

C.3.2 Proof of (74)

We calculate the expression of in (70) as

| (81) | ||||

Define

and

Then we can simplify the derivative of in (81) as

| (82) |

where is defined in (77). To bound the above terms, we introduce the following lemma to control all of the above terms.

Lemma 3

Suppose that is twice differentiable for there exists some positive constant such that

| (83) |

| (84) |

| (85) |

Appendix D Proof of Theorem 1

We start with the following error decomposition of

| (87) |

The high-dimensional error is controlled in Theorem 2. We shall control the stochastic error and the approximation error in Sections D.1 and D.2, respectively. We present the proof of (28) in Section D.3.

D.1 Analysis of the Stochastic Error

We shall establish the following limiting distribution,

| (88) |

with

| (89) |

D.1.1 Proof of (89)

We decompose the error between and its corresponding estimand,

| (90) | ||||

where the inequality follows from triangle inequality, and Cauchy-Schwarz inequality. We bound the difference between the sum of centered variables and that of uncentered variables,

By applying (45) and (46) in Lemma 50 and (51), we establish that, with probability larger than for

| (91) |

Note that

We apply (42), (50), and (91) and establish

| (92) |

We shall choose and establish that, with probability larger than

Combined with (90) and (92), we establish that, with probability larger than

| (93) |

For defined in (17), we approximate it by its corresponding estimand,

| (94) | ||||

D.1.2 Proof of (88)

Define . We rewrite the stochastic error as follows,

We use to denote the data Conditioning on , are independent random variables with

and

Define the event

The high probability inequality in (93) implies

| (98) |

By applying (93) and the fact that for a positive constant , we obtain that, on the event ,

| (99) |

It is sufficient to check the Linderberg condition

where the first inequality follows from (99) and the last inequality follows from the condition that for some positive constant and

D.2 Analysis of the Approximation Error

In the following, we show that, with probability larger than

| (101) |

and

| (102) |

with

By the continuity of at the point we combine (101) and (102) and establish that,

| (103) |

D.2.1 Proof of (101)

There exists some such that

Hence, we have

for some satisfying . The above inequality implies that

| (104) |

We now control the term

where the last inequality follows from the fact that . Together with (45) with , we establish that, with probability larger than

| (105) |

D.2.2 Proof of (102)

By the expression , we have

| (106) | ||||

By the Cauchy-Schwarz inequality, we have

| (107) | ||||

where the last inequality follows from the fact that . In addition, we have

| (108) |

and

| (109) | ||||

where the last inequality follows from the fact that . We now apply (45), (49), (51), the decomposition (106) with the error bounds in (107), (108), and (109). We establish that, with probability larger than

D.3 Proof of (28)

Appendix E Proofs of Extra Lemmas

E.1 Proof of Lemma 85

E.2 Proof of Lemma 44

E.2.1 Proof of (37) and (38)

We start with the expression of

By setting , we simplify the above expression as,

| (111) |

for some . We shall use as a generic function of throughout the proof and the specific function can vary from place to place. Hence, we have

| (112) |

E.2.2 Proof of (39) and (40)

E.2.3 Proof of (41) and (42)

By the iterated expectation, we have

We first analyze , by noting that

| (118) | ||||

where the last equality follows from the definition of .

E.2.4 Proof of (43)

E.2.5 Proof of (44)

Note that

For the first term, we apply the iterated expectation and obtain

with

Then it is sufficient to control the terms

and

| (122) |

Since

the term in (122) can be upper bounded by

It follows from (117) that

| (123) |

We control the term in the following.

and then have

Together with (123) and

we establish (44).

E.3 Proof of Lemma 50

The proofs rely on the Bernstein inequality [6], which is restated in the following lemma.

Lemma 4

Suppose that are independent zero mean random variables and almost surely. Then we have

Proof of (45)

We shall apply Lemma 4 by taking

By (38), there exists such that

| (124) |

Note that and

By (124) and Lemma 4 with , we establish (45).

Proof of (46)

By the definition of , the term satisfies

Note that By (42), we apply Lemma 4 with and establish (46).

Proof of (47)

It follows from (39) that

We apply (40) and establish

Note that we apply Lemma 4 with and establish (47).

Proof of (48)

It follows from (43) that

for some small positive constant Note that

and

We apply Lemma 4 with and establish (48).

Proof of (49)

The term satisfies

where the last inequality follows from (44). Note that

and We apply Lemma 4 with and establish (49).

Proof of (50). Note that both is upper bounded by a constant and

where the second inequality follows from the fact and the last inequality follows from (42). We apply Lemma 4 with and establish (50).

E.4 Proof of Lemma 85

E.5 Proof of Proposition 1

Note that

It is sufficient to show that

| (127) |

For the last hand side of (127), we have the decomposition

| (128) | ||||

By the law of large numbers, we have

| (129) |

Define the event

and by the definition of and we have

| (130) |

In the following analysis, we condition on the data in and take the conditional expectation as

| (131) |

By the Cauchy inequality, we have

where the least inequality follows from (131) and By the Markov inequality, we establish that, with probability larger than for some

Appendix F Additional Simulation Results

F.1 Setting 1-4 and Nonlinear Treatment Model

In this section, we present complete simulation results for Setting 1-4 and the nonlinear treatment model. The sample sizes are varied across {500,1000,1500,2000} and is varied across {-1.25,-0.5,0.1,0.25,1}. We consider two generating models for and as follows,

-

•

and ;

-

•

and .

The complete results for Setting 1 are summarised in Table S1 and Table S2. Similar to the results presented in the main paper, our DLL method achieves desired coverage, and the CI length is close to the confidence interval by the oracle estimator. Besides, our DLL method outperforms the plug-in method in terms of coverage since the DLL estimator has a smaller bias. The coverage for the plug-in estimator is relatively good at the boundary {-1.25,1} since only a few samples are used with the chosen bandwidth, and the standard error for the plug-in estimator is large, leading to a wide CI.

The summarized results for Setting 2 and 3 are in Table S3 and Table S4, respectively. The results for Setting 2 and Setting 3 are similar to those for Setting 1. For Setting 4, follows a t distribution and we vary the degree of freedom in {10,15}. The results are reported in Tables S5 and S6. In Settings 3 and 4, we test the robustness of our proposed method to the violation of assumption in (A2). The results demonstrate that our proposed DLL method still corrects the bias of the plug-in estimator and attains the desired coverage level, with the CI length similar to the confidence interval by the oracle estimator.

The results of the non-linear treatment model are presented in Table S7. We see that DLL-S correct more bias than the DLL estimator, and the coverage for DLL-S improves along with this additional bias-correction. However, the bias for DLL is still smaller than the plug-in estimator, and better coverage is obtained.

| Setting 1, exactly sparse: | |||||||||||||||||