Testing for time-varying properties under misspecified conditional mean and variance

Abstract

This study examines statistical performance of tests for time-varying properties under misspecified conditional mean and variance. When we test for time-varying properties of the conditional mean in the case in which data have no time-varying mean but have time-varying variance, asymptotic tests have size distortions. This is improved by the use of a bootstrap method. Similarly, when we test for time-varying properties of the conditional variance in the case in which data have time-varying mean but no time-varying variance, asymptotic tests have large size distortions. This is not improved even by the use of bootstrap methods. We show that tests for time-varying properties of the conditional mean by the bootstrap are robust regardless of the time-varying variance model, whereas tests for time-varying properties of the conditional variance do not perform well in the presence of misspesified time-varying mean.

Keywords time-varying properties; mean; variance; misspecified models; size distortions

1 Introduction

Many economic and financial time series data have time-varying properties. Their properties are roughly classified into two types. One is a property about the conditional mean. Constant and/or autoregressive parameters change with time as time-varying properties for the mean. Another time-varying property is the conditional variance of the error term for a regression model. Variance of the error term, that is, volatility, is frequently modeled by the autoregressive conditional heteroskedasticity (ARCH). As introduced by Dahlhaus and Rao (2006), a property of the time-varying model for volatility is that the parameters of volatility models change with time. Amado and Teräsvirta (2013) and Kim and Kim (2016) recently provided a time-varying volatility model and its applications.

Linearity tests are usually used to investigate time-varying properties. When we test for time-varying properties of the conditional mean, we assume a homoskedastic variance or a correctly specified linear variance process for the error term of the condtional mean. When we test for time-varying properties of the conditional variance, we assume a correctly specified linear process for a mean. However, it is difficult to know which time-varying property for the mean or variance is present a priori. This challenge implies that researchers may erroneously test for time-varying properties of the mean, although volatility actually has time-varying properties. Similarly, researchers might erroneously test for time-varying properties of the variance, although the mean actually has time-varying properties. In fact, Pitarakis (2004) and Perron and Yamamoto (2019) showed that a test for a change in regression coefficients (variance) ignoring or misspecifying the presence of change in variance (regression coefficients) causes poor statistical properties. For the influence of ARCH on inference of misspecified models, Lumsdaine and Ng (1999) showed over-rejection of ARCH tests in the presence of misspecified conditional mean models. Van Dijk, Franses, and Lucas (1999) demonstrated size distortions of ARCH tests when a process has additive outliers. Balke and Kapetanios (2007) pointed out that supurious ARCH effects appear when nonlinearity of the mean is ignored. If we were to perform erronous tests and fail to obtain reliability from the derived results, the correct model construction and evaluation are difficult. Accordingly, it is important to clarify the influence of tests on the misspecified models.

This study examines the influence of time-varying tests on misspecified conditional mean and variance. In particular, we clarify the statistical performance of tests for time-varying variance when a process has time-varying mean with homoskedastic variance. We also investigate statistical performance of tests for time-varying mean when a process has time-varying variance with a linear mean model. Some studies, including Lumsdaine and Ng (1999), van Dijk, et al. (1999), and Balke and Kapetanios (2007), investigated problems of misspecified models in ARCH tests. However, previous studies have not clarified the influence of time-varying tests on misspecified conditional mean and variance. As mentioned above, it is important to clarify time-varying properties correctly. This study uses a logistic smooth transition function to model time-varying mean and variance. This model smoothes threshold or structural break models in time. The time-varying tests used in this study are based on the method introduced by Luukkonen, Saikkonen, and Teräsvirta (1988a). They depeloped linearity tests using a Taylor series approximation to overcome the identification problem pointed out by Davies (1977, 1987).

The simulation results in this study provide evidence that the asymptotic test for time-varying mean has size distortions when the conditional variance model is misspecified. However, the wild bootstrap method introduced by Liu (1988) improves the size distortions. In fact, Becker and Hurn (2009) provided evidence that the wild bootstrap improves size properties when the conditional mean is being tested. We can test for time-varying mean by using the wild bootstrap without depending on the form of volatility. When we test for time-varying variance in the presence of a misspecified conditional mean, asymptotic tests have large size distortions. The properties are not improved by the use of the bootstrap ARCH test proposed by Gel and Chen (2012) and the wild bootstrap. The results show that the wild bootstrap tests for time-varying mean are robust regardless of the misspecified conditional variance, whereas tests for time-varying variance do not perform well in the presence of misspecified conditional mean.

The remainder of this paper is organized as follows. Section 2 presents the tests for time-varying mean and variance. Section 3 provides statistical properties of the tests for time-varying mean and variance in the presence of misspecified conditional models. Finally, Section 4 summarizes and concludes.

2 Tests for time-varying mean and variance

We assume the following regression model to test for time-varying mean1.

| (1) |

where and is a transition function to model time-varying properties of (1). (1) has a time-varying constant and slope for depending of the value of . Lin and Teräsvirta, T. (1994) provided the asymptotic theory for time-varying regression models. (1) reduces to a linear autoregressive model for and/or and . is denoted as

| (2) |

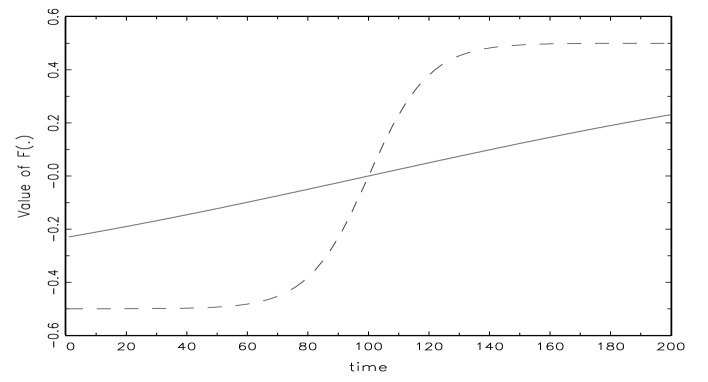

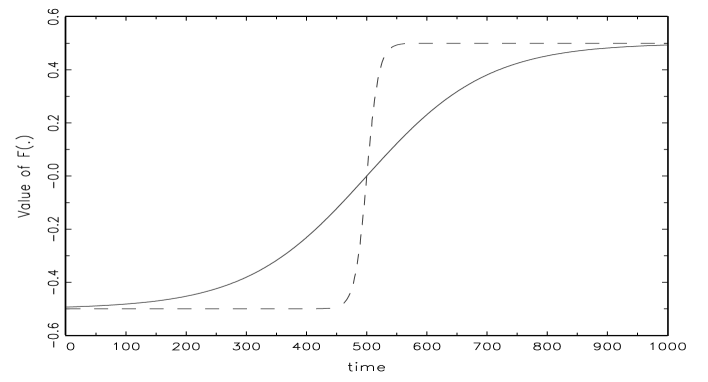

where is a parameter of smoothness and is a threshold parameter. We assume and . is bounded between and . moves toward when and small , and moves toward when and large . takes 0 for . with equals a structural break model, because with becomes the indicator function that takes the value -1/2 or 1/2. For example, Figures 1 and 2 demonstrate the values of . While Figure 1 depicts the graph of with , , and , Figure 2 depicts it with , , and . Figure 1 shows that with is almost linear, whereas with has a smooth change around For Figure 2, with has a smooth change around . By contrast, with has a rapid chagnge around The time-varying properties of (1) depend on the values of , , and .

The null and alternative hypotheses to test for time-varying mean in (1) are denoted as follows

| (3) |

(1) becomes a simple autoregressive (AR) model under and has a time-varying constant and slope under with and . Note that we cannot test for directly, because the null hypothesis has an identification problem about and , which are identified only under the alternative hypothesis with . Davies (1977, 1987) discussed the identification problem whereby a nuisance parameter is present only under the alternative hypothesis. A solution for the identification problem is to use the Taylor series approximation introduced by Luukkonen, Saikkonen, and Teräsvirta (1988a).

When we use a Taylor series approximation around , (1) with is given by

| (4) |

where is an error term for the new regression model. We can formulate the null and alternative hypotheses to test for time-varying mean in (4) as follows.

| (5) |

We rewrite (4) as

| (6) |

where and . The usual test for (5) uses the following Wald statisic.

| (7) |

where is the estimate of , is the estimate of the residual variance obrained from (4), and is the matrix such that . has an distribution with degrees of freedom under the null hypothesis.

Standard asymptotic tests for linearity often cause spurious nonlinearity when errors have heteroskedastic variance, including ARCH, generalized ARCH (GARCH), stochastic volatility, and structural breaks.

A method to relieve the influence is to use heteroskedasticity consistent covariance matrix estimator (HCCME) introduced by White (1980).

This is a popular method to test for linearity in the presence of heteroskedasticity,

since test statistics based on the HCCME asymptotically have the same distribution as the original test statistics under the null hypothesis.

However, linearity tests using HCCME do not perform well under the null hypothesis of linearity with ARCH and GARCH type errors particularly for finite samples.

HCCME cannot improve the influence of heteroskedastic variance on inference of the conditional mean sufficiently.

As pointed out by Pavlidis, Paya, and Peel (2013), the presence of ARCH errors complicate tests for lineality because ARCH errors are like nonlinear processes for conditional mean.

Some studies, including Pavlidis, Paya, and Peel (2010) and Maki (2014), demonstrated this problem.

An better method is the wild bootstrap proposed by Liu (1988).

This can resample data with unknown heteroskedastic variance and yeild better statistical performance than the asymptotic and the HCCME tests can.

The wild bootstrap test for time-varying mean takes the following procedure.

Step 1. Estimate regression model (4) and compute test statistic (6).

Step 2. Estimate the regression model under the null hypothesis with and obtain the parameter estimates and and residuals denoted as .

Step 3. Generate the bootstrapped sample as follows:

| (8) |

where .

We set to independent and identically distributed 2.

Step 4. Estimate regression model (4) using the generated bootstrap sample (7) and compute test statistic (6) denoted as .

Step 5. Repeat steps 3 and 4 many times.

Step 6. Compute the bootstrap -value as follows:

| (9) |

where is the number of bootstrap iterations and is an indicator function such that is 1 if is true and 0 otherwise. Usually, more than 1,000 times are enough for the number of bootstrap iterations. Andrews and Buchinsky (2000) and Davidson and MacKinnon (2000) discussed the problem of the number of bootstrap iterations. The null hypothesis is rejected if (8) is smaller than a significant level.

We next explain the test for time-varying smooth transition variance. Consider the following data generating process (DGP).

| (10) | |||

| (11) | |||

| (12) | |||

| (13) |

(9) has a linear AR model for mean and time-varying smooth transition ARCH process (11) for variance. While Hagerud (1996) proposed the smooth transition GARCH model with the transition variable , (12) has the transition variable . The transition function for time-varying ARCH is similar to that of time-varying mean3. Since (11) also has an identification problem, we use a Taylor series approximation around in order to test for time-varying smooth transition ARCH. (11) is rewritten as

| (14) |

where is an error term, including white noise and the remainder term from the Taylor approximation. The null hypothesis and alternative hypothesis of test for time-varying ARCH are given by

| (15) |

(14) nests ARCH test4. In order to test for (14), we first estimate (9) and obtain residuals. The test statistic is

| (16) |

where is the sum of the squared residuals obtained from the estimation of (13) with and is the sum of the squared residuals obtained from the estimation of (13). has an distribution with degrees of freedom under the null hypothesis5.

Gel and Chen (2012) introduced a new bootstrap test for ARCH to improve the size and power of the asymptotic test.

We use their approach to test for time-varying ARCH.

The procedure is denoted as follows.

Step 1. Estimate regression model (13) and compute test statistic (15).

Step 2. Estimate the regression model under the null hypothesis with and obtain the parameter estimates and residuals denoted as .

Step 3. Generate the bootstrapped sample as follows:

| (17) |

where is randomly selected from .

Step 4. Estimate regression model (13) using the generated bootstrap sample (16)

and compute test statistic (15) denoted as .

Step 5. Repeat steps 3 and 4 many times.

Step 6. Compute the bootstrap -value as follows:

| (18) |

The null hypothesis is rejected if the -value (17) is smaller than a significant level. We also use the wild bootstrap test for (14). This is almost smilar to the bootstrap test shown above. The main difference is Step 3. The wild bootstrap approach replace as , where . We denote the wild bootstrap test for time-varying ARCH as . The -value is given by

| (19) |

3 Statistical properties of time-varying tests

This section examines the statistical properties of the time-varying tests reviewed in section 2. We conduct Monte Carlo simulations to compare the size and power of the test statistics. The simulations are based on 10,000 replications, the nominal level at 5%, and sample sizes with , , , and . We show only nominal power properties and do not present size-corrected power because the purpose of the paper is to compare the tests and usual applied practitioners do not use size-corrected tests. Bootstrap tests have 1,000 replications. In order to avoid the effect of initial conditions, data with are generated. The initial 100 samples are discarded and we use the data with sample size . Tests compared in this section are denoted as , , , , and .

First, as a benchmark, autoregressive processes with homoskedastic error are generated.

| (20) |

where . is set to . The persistent parameter is set to and in order to investigate the influence of persistence of the process on time-varying tests. Since (19) has no time-varying properties in mean and variance, the rejection frequencies of each test demonstrate the empirical size for (19). Table 1 presents the rejection frequencies of each test. When the persistent parameter is , has slight under-rejection for , , and . Other tests have the empirical size near to 5% nominal level and reasonable size properties regardless of sample size. Although time-varying tests for mean, and , have over-rejection in small samples with , the over-rejection decreases with the increased sample size. Unlike time-varying tests for mean, time-varying tests for variance do not have size distortions, except for with , which has slight under-rejection.

Next, we consider the following DGP to examine the power properties of and and the size properties of , , and under the following time-varying mean model.

| (21) | |||

| (22) |

Parameters for the time-varying mean are set to and , respectively. moves from to . For , (20) has time-varying properties from to . We examine the effect of the magnitude of change for constant and AR parameters on performance of the tests. Smoothness parameter in is set to . means more smooth and slight change in than . In addition, the threshold parameter is set to . The simulation results are shown in Table 2. The powers of and are low for parameter sets with and . They increase rapidly with the large sample size. We can observe that the magnitude of and affects the powers of and . For example, the powers of and for with are 0.134 and 0.132, respectively, whereas those for with are 0.694 and 0.703, respectively. When the smoothness parameter is , and have sufficient power. has clear impact on the performance of and . Generally, we observe that and have ability to find time-varying mean properties in the presence of homoskedastic variance.

For , , and , the results in Table 2 show the empirical size properties of the tests, because (20) has homoskedastic variance. performs well in small samples. It has over-rejection for and . In particular, has a rejection frequency 0.325 and large size distortions when and We find that the increase in the time-varying AR parameter causes high rejection frequencies for the time-varying variance test under the null hypothesis of homoskecastic variance. Although the change of a constant of (20) also increases the rejection frecencies, the effect is not larger than the increase in the AR parameter. The rejection frecencies of for with and are 0.068 and 0.119, respectively. Similar properties are observed for . The results imply that the bootstrap time-varying ARCH test does not perform well under the null hypothesis of homoskedastic variance with a misspecified conditional mean. By contrast, the size properties of outperform those of and . does not have over-rejection even for . However, has size distortions for . Actually, the rejection frequencies of for with and are 0.253 and 0.113, respectively. does not improve the size properties when the DGP has time-varying mean with homoskedastic error. and for have larger size distortions than those for .

When we test for time-varying ARCH in the presence of a misspecified conditional mean, the tests cannot lead to reliable results, particularly for a large change in time-varying parameters with a large smoothness parameter As shown by Balke and Kapetanios (2007), neglected nonlinearity in the conditional mean cause spurious heteroskedasticity because the conditional variance includes extra nonlinearity and lags. This is more clear when increases7. If the mean is misspeficied, the residual includes nonlinearity of the mean. Large and sample size lead to stronger nonlinearity. This is the reason for poor performance of the time-varying variance test. Therefore, time-varying ARCH tests in the presence of a misspecified conditional mean have size distortions.

Table 3 reports rejection frequencies of the tests for the AR process with ARCH error. The DGP is the following.

| (23) | |||

| (24) | |||

| (25) |

We set a constant parameter for ARCH to . Persistence parameter for ARCH is set to , , and in order to examine the effect of persistence of variance on the performance of the tests. is the necessary and sufficient condition for a weak stationarity of a semi-strong process. For (22), (23), and (24), the rejection frequencies of and show the empirical size, because the process does not have time-varying mean. The performances of , , and show frequencies of finding ARCH properties. overrejects the null hypothesis at 5% significance and its over-rejection increases when the persistence parameter and/or sample size increases. is sensitive to persistence in the presence of the ARCH effect. has slight over-rejection only for with large samples. However, clearly outperforms and has reasonable and acceptable rejection frequencies in most cases. This is due to the property that the wild bootstrap can deal with heteroskedasticity of unknown form when the conditional mean is correctly specified. We observe the difference of power properties among , , and . and have sufficient power to find the ARCH effect. Their abilities to detect the ARCH effect increases for large and . The ability of is lower than that of and . For example, the powers of , , and for and are 0.937, 0.937, and 0.260, respectively. While the size properties of are superior to and under a misspecified conditional mean reported in Table 2, the powers of are clearly inferior to and . The higher powers of and are due to size distortions presented in Table 2. The comparison indicates that the use of these tests is not effective in the viewpoint of size and power because the size corrected tests are needed.

We finally investigate the statistical properties of the tests for the AR process with time-varying ARCH error. The DGP is given by

| (26) | |||

| (27) | |||

| (28) | |||

| (29) |

Time-varying parameters are set to and , respectively. We consider DGP with and These settings are similar to those in Table 2, in which the DGP has time-varying mean. The results are presented in Table 4. does not have over-rejection for all cases and is close to the nominal size at 5%. This means that is a reliable test for time-varying mean and does not lead to spurious time-varying mean. Although has size distortions under time-varying ARCH error, the rejection frequencies do not depend on the size of parameters , , and too much. The rejection frequencies mainly depend on sample size and slowly increase when the sample size increases. The results are similar to those of Zhou (2013) and Boldea, Cornea-Madeira, and Hall (2019). They show that the wild bootstrap is asymptotically valid for a change in mean or regression coefficients in the presence of conditional and unconditional heteroskedasticity8. The wild bootstrap can replicate unknown heteroskedasticity of the errors. The property brings valid tests for linearity of the mean.

The powers of are a little better than those of . These tests have sufficient power to find time-varying ARCH effects. Furthermore, the increase in the smoothness parameter brings higher power of time-varying ARCH tests. In particular, the effect is clear for . When the sample size is , the powers of and are 0.387 and 0.429 for , respectively, and 0.774 and 0.813 for , respectively. Note that the results of are clearly different from those of and . The powers of are lower than those of and in all cases. For example, when the process has and , the powers of , , and are 0.724, 0.744, and 0.154, respectively. and cause large over-rejections under the null hypothesis with time-varying mean, whereas they have higher power under the alternative hypothesis. By contrast, has better size properties than and do, whereas has clearly lower power than and do. The Monte Carlo simulation results provide evidence that tests yeild reliable results than do under ARCH and time-varying ARCH, and time-varying ARCH tests do not perform well in the presence of time-varying mean.

4 Summary and conclusion

This study examined the statistical performance of time-varying tests under misspecified conditional mean and variance. Although time-varying properties are frequently observed in various economic and financial data, it is difficult to know which time-varying property for mean or variance is present a priori. Researchers may employ misspecified conditional models and obtain unreliable results. Therefore, it is important to clarify the statistical properties of time-varying tests in misspecified conditional mean or variance models. Monte Carlo simulation results reveal that asymptotic tests for time-varying mean have size distortions when the variance model is misspecified, whereas the wild bootstrap method improves the size distortions. Wild bootstrap tests for time-varying mean are robust regardless of the misspecified variance, and can lead to reliable results of tests for time-varying mean. However, bootstrap tests in addition to asymptotic tests for time-varying variance have size distortions in the presence of the misspecified conditional mean. Tests for time-varying variance do not perform well and not provide reliable results in the presence of misspecified conditional mean. Robust time-varying variance tests in the presence of the misspecified conditional mean remain for further study.

Footnotes

1. Although (1) can take a general model with lags, we consider only a single-lag model to simplify the investigation in this study.

The same is true of variance.

2. Davidson and Flachaire (2008) discussed the method of the wild bootstrap, including other distributions for .

3. (12) includes conditional and unconditional heteroskedasticity.

While conditional heteroskedasticity has and/or with ,

unconditional heteroskedasticity has and/or with in addition to .

4. It is possible to test for the null hypothesis of .

This means that in the null hypothesis, there is an ARCH error and in the alternative hypothesis, there is a time-varying ARCH error.

However, it is difficult to know that the variance process has ARCH properties a priori.

When we have the null hypothesis ,

we have to test for the hypothesis whether variance has ARCH error before testing for .

This takes a two-step approach and cannot test for time-varying ARCH directly.

This may make comparisons among the tests difficult and lead to misleading results.

Therefore, we adopt hypothesese in (14) to avoid these problems and simply test for time-varying ARCH.

5. The test statistic is also expressed by , where is the coefficient of the determinantion of (13). asymptotically has distribution.

See Gel and Chen (2012)

6. We conduct Monte Carlo experiments under various other situations.

For example, while tests have larger rejection frequencies when is smaller than ,

they have smaller rejection frequencies when is larger than .

However, differences among the tests are similar to those of .

The results for other parameter sets are available from the author on request.

7. See Luukkonen et al. (1988b) for similar results.

8. Zhang and Wu (2019) proposes a nonparametric test for a change in regression coefficients in the presence of time-varying variance.

References

- [1] [Amado, C., Teräsvirta, T. (2013)] Modelling volatility by variance decomposition, Journal of Econometrics 175, 142-153.

- [2] [Andrews, D. W. K., Buchinsky, M. (2000)] A three-step method for choosing the number of bootstrap repetitions, Econometrica 68, 23-51.

- [3] [Balke, A. P., Kapetanios, G. (2007)] Testing for ARCH in the presence of nonlinearity of unknown form in the conditional mean, Journal of Econometrics 137, 472-488.

- [4] [Becker, R., Hurn, S. (2009)] Testing for nonlinearity in mean in the presence of heteroskedasticity, Economic Analysis & Policy 39, 313-326.

- [5] [Boldea, O., Cornea-Madeira, A., Hall, A.R. (2019)] Bootstrapping structural change tests, Journal of Econometrics (in press)

- [6] [Catani, P. S., Ahlgren, N. J. C. (2017)] Combined Lagrange multiplier test for ARCH in vector autoregressive models, Econometrics and Statistics 1, 62-84.

- [7] [Dahlhaus, R., Rao, S. S. (2006)] Statistical inference for time-varying ARCH processes, The Annals of Statistics 34, 1075-1114.

- [8] [Davidson, R., MacKinnon, J. G. (2000)] Bootstrap tests: how many bootstraps? Econometric Reviews 19, 55-68.

- [9] [Davidson, R., Flachaire, E. (2008)] The wild bootstrap, tamed at last, Journal of Econometrics 146, 162-169.

- [10] [Davies, R. B. (1977)] Hypothesis testing when a nuisance parameter is present only under the alternative, Biometrika 64, 247-254.

- [11] [Davies, R. B. (1987)] Hypothesis testing when a nuisance parameter is present only under the alternative, Biometrika 74, 33-43.

- [12] [Gel, Y. R., Chen, B. (2012)] Robust Lagrange multiplier test for detecting ARCH/GARCH effect using permutation and bootstrap, The Canadian Journal of Statistics 40, 405-426.

- [13] [Hagerud, G. (1996)] A new non-linear GARCH model, EFI Economic Research Institute, Stockholm School of Economics.

- [14] [Kim, K. H., Kim, T. (2016)] Capital asset pricing model: A time-varying volatility approach, Journal of Empirical Finance 37, 268-281.

- [15] [Lin, C.-F.J., Teräsvirta, T. (1994)] Testing the constancy of regression parameters against continuous structural change, Journal of Econometrics 62, 211-228.

- [16] [Liu, R. Y. (1988)] Bootstrap procedure under some non-i.i.d. models, Annals of Statistics 16, 1696-1708.

- [17] [Lumsdaine, R. L., Ng, S. (1999)] Testing for ARCH in the presence of a possibly misspecified conditional mean, Journal of Econometrics 93, 257-279.

- [18] [Luukkonen, R., Saikkonen, P., Teräsvirta, T. (1988a)] Testing linearity against smooth transition autoregressive models, Biometrika 70, 491-499.

- [19] [Luukkonen, R., Saikkonen, P., Teräsvirta, T. (1988b)] Testing linearity in univariate time series models, Scandinavian Journal of Statistics 15, 161-175.

- [20] [Maki, D. (2014)] A comparison of linearity tests based on wild bootstrap, Advances and Applications in Statistics 4(3), 93-107.

- [21] [Pavlidis, E., Paya, I, Peel, D. (2010)] Specifying smooth transition regression models in the presence of conditional heteroskedasticity of unknown form, Studies in Nonlinear Dynamics and Econometrics 14(3), 1-40.

- [22] [Pavlidis, E., Paya, I, Peel, D. (2013)] Nonlinear causality tests and multivariate conditional heteroskedasticity: a simulation study, Studies in Nonlinear Dynamics and Econometrics 17(3), 297-312.

- [23] [Perron, P., Yamamoto, Y. (2019)] Pitfalls of two-step testing for changes in the error variance and coefficients of a linear regression model, Econometrics 7(2), 22, 1-11.

- [24] [Pitarakis, J. Y. (2004)] Least squares estimation and tests of breaks in mean and variance under misspecification, Econometrics Journal 7, 32-54.

- [25] [van Dijk, D., Franses, P. H., Lucas, A., (1999a)] Testing for ARCH in the presence of additive outliers, Journal of Applied Econometrics 14, 539-562.

- [26] [van Dijk, D., Franses, P. H., Lucas, A., (1999b)] Testing for smooth transition nonlinearity in the presence of outliers, Journal of Business & Economic Statistics 17, 217-235.

- [27] [van Dijk, D., Teräsvirta, T., Franses, P. H. (2002)] Smooth transition autoregressive models - a survey of recent developments, Econometric Reviews 21, 1-7.

- [28] [White, H. (1980)] A heteroskedasticity-consistent covariance matrix estimator and a direct test for heteroskedasticity, Econometrica 14, 1261-1295.

- [29] [Zhang, E., Wu, J. (2019)] Testing for structural changes in linear regressions with time-varying variance, Communications in Statistics-Theory and Methods (in press)

- [30] [Zhou, Z. (2013)] Heteroscedasticity and autocorrelation robust structural change detection, Journal of the American Statistical Association 108, 726-740.

Table 1: Rejection frequencies under AR with homoskedastic error

| 0.049 | 0.051 | 0.034 | 0.046 | 0.051 | |

| 0.048 | 0.049 | 0.041 | 0.045 | 0.054 | |

| 0.053 | 0.054 | 0.040 | 0.050 | 0.051 | |

| 0.046 | 0.054 | 0.046 | 0.050 | 0.046 | |

| 0.106 | 0.104 | 0.035 | 0.047 | 0.048 | |

| 0.080 | 0.074 | 0.043 | 0.049 | 0.044 | |

| 0.054 | 0.061 | 0.045 | 0.049 | 0.051 | |

| 0.056 | 0.057 | 0.045 | 0.050 | 0.045 |

Table 2: Rejection frequencies under time-varying AR with homoskedastic error

| 0.056 | 0.061 | 0.036 | 0.043 | 0.048 | 0.380 | 0.382 | 0.036 | 0.046 | 0.042 | |

| 0.134 | 0.132 | 0.040 | 0.048 | 0.049 | 0.789 | 0.794 | 0.036 | 0.051 | 0.035 | |

| 0.625 | 0.630 | 0.049 | 0.053 | 0.041 | 0.986 | 0.988 | 0.042 | 0.067 | 0.035 | |

| 1 | 0.999 | 0.068 | 0.072 | 0.031 | 1 | 1 | 0.119 | 0.086 | 0.036 | |

| 0.091 | 0.090 | 0.035 | 0.043 | 0.048 | 0.943 | 0.941 | 0.055 | 0.071 | 0.029 | |

| 0.428 | 0.424 | 0.041 | 0.053 | 0.045 | 1 | 0.999 | 0.126 | 0.133 | 0.040 | |

| 0.996 | 0.997 | 0.064 | 0.076 | 0.027 | 1 | 1 | 0.286 | 0.296 | 0.083 | |

| 1 | 1 | 0.325 | 0.332 | 0.057 | 1 | 1 | 0.704 | 0.703 | 0.253 | |

| 0.085 | 0.091 | 0.036 | 0.042 | 0.044 | 0.880 | 0.875 | 0.038 | 0.046 | 0.034 | |

| 0.357 | 0.365 | 0.040 | 0.047 | 0.048 | 0.998 | 0.999 | 0.049 | 0.054 | 0.045 | |

| 0.990 | 0.992 | 0.046 | 0.055 | 0.038 | 1 | 1 | 0.068 | 0.077 | 0.044 | |

| 1 | 1 | 0.074 | 0.078 | 0.035 | 1 | 1 | 0.139 | 0.144 | 0.070 | |

| 0.121 | 0.129 | 0.036 | 0.042 | 0.042 | 0.994 | 0.994 | 0.040 | 0.052 | 0.031 | |

| 0.694 | 0.703 | 0.036 | 0.043 | 0.044 | 1 | 1 | 0.070 | 0.080 | 0.044 | |

| 1 | 1 | 0.042 | 0.052 | 0.034 | 1 | 1 | 0.127 | 0.132 | 0.058 | |

| 1 | 1 | 0.119 | 0.125 | 0.040 | 1 | 1 | 0.300 | 0.311 | 0.113 | |

Table 3: Rejection frequencies under AR with ARCH error

| 0.079 | 0.049 | 0.372 | 0.407 | 0.065 | |

| 0.086 | 0.052 | 0.681 | 0.705 | 0.120 | |

| 0.098 | 0.052 | 0.937 | 0.937 | 0.260 | |

| 0.100 | 0.053 | 0.999 | 0.999 | 0.558 | |

| 0.107 | 0.049 | 0.686 | 0.719 | 0.184 | |

| 0.144 | 0.057 | 0.946 | 0.956 | 0.323 | |

| 0.191 | 0.051 | 0.998 | 0.999 | 0.498 | |

| 0.231 | 0.055 | 1 | 1 | 0.674 | |

| 0.129 | 0.055 | 0.802 | 0.841 | 0.253 | |

| 0.201 | 0.057 | 0.976 | 0.985 | 0.366 | |

| 0.282 | 0.062 | 0.998 | 0.999 | 0.474 | |

| 0.401 | 0.060 | 0.999 | 1 | 0.561 |

Table 4: Rejection frequencies under AR with time-varying ARCH error

| 0.079 | 0.049 | 0.381 | 0.407 | 0.071 | 0.072 | 0.049 | 0.418 | 0.454 | 0.098 | |

| 0.091 | 0.055 | 0.692 | 0.706 | 0.128 | 0.088 | 0.053 | 0.738 | 0.756 | 0.175 | |

| 0.101 | 0.051 | 0.946 | 0.950 | 0.276 | 0.105 | 0.054 | 0.962 | 0.963 | 0.329 | |

| 0.116 | 0.056 | 0.999 | 0.999 | 0.576 | 0.117 | 0.050 | 0.999 | 1 | 0.597 | |

| 0.082 | 0.051 | 0.384 | 0.414 | 0.069 | 0.079 | 0.059 | 0.521 | 0.560 | 0.153 | |

| 0.091 | 0.055 | 0.712 | 0.733 | 0.144 | 0.095 | 0.059 | 0.863 | 0.875 | 0.298 | |

| 0.109 | 0.053 | 0.962 | 0.970 | 0.333 | 0.115 | 0.056 | 0.991 | 0.991 | 0.458 | |

| 0.151 | 0.054 | 1 | 1 | 0.627 | 0.146 | 0.061 | 1 | 1 | 0.645 | |

| 0.077 | 0.054 | 0.381 | 0.414 | 0.071 | 0.072 | 0.055 | 0.563 | 0.600 | 0.202 | |

| 0.086 | 0.054 | 0.724 | 0.744 | 0.154 | 0.083 | 0.052 | 0.910 | 0.922 | 0.384 | |

| 0.102 | 0.056 | 0.976 | 0.981 | 0.385 | 0.096 | 0.050 | 0.998 | 0.998 | 0.570 | |

| 0.125 | 0.055 | 1 | 1 | 0.725 | 0.118 | 0.052 | 1 | 1 | 0.746 | |

| 0.073 | 0.054 | 0.387 | 0.429 | 0.082 | 0.074 | 0.053 | 0.774 | 0.813 | 0.410 | |

| 0.091 | 0.055 | 0.752 | 0.790 | 0.196 | 0.081 | 0.057 | 0.992 | 0.995 | 0.595 | |

| 0.101 | 0.054 | 0.989 | 0.996 | 0.539 | 0.090 | 0.055 | 1 | 1 | 0.723 | |

| 0.118 | 0.052 | 1 | 1 | 0.813 | 0.117 | 0.053 | 1 | 1 | 0.816 | |

Solid line has . Dashed line has .