Contextual multi-armed bandit algorithms are widely used in sequential decision tasks such as news article recommendation systems, web page ad placement algorithms, and mobile health. Most of the existing algorithms have regret proportional to a polynomial function of the context dimension, . In many applications however, it is often the case that contexts are high-dimensional with only a sparse subset of size being correlated with the reward. We consider the stochastic linear contextual bandit problem and propose a novel algorithm, namely the Doubly-Robust Lasso Bandit algorithm, which exploits the sparse structure of the regression parameter as in Lasso, while blending the doubly-robust technique used in missing data literature. The high-probability upper bound of the regret incurred by the proposed algorithm does not depend on the number of arms and scales with instead of a polynomial function of . The proposed algorithm shows good performance when contexts of different arms are correlated and requires less tuning parameters than existing methods.

1 Introduction

Many sequential decision problems can be framed as the multi-armed bandit (MAB) problem (Robbins,, 1952; Lai and Robbins,, 1985), where a learner sequentially pulls arms and receives random rewards that possibly differ by arms. While the reward compensation mechanism is unknown, the learner can adapt his (her) decision to the past reward feedback so as to maximize the sum of rewards. Since the rewards of the unchosen arms remain unobserved, the learner should carefully balance between “exploitation", pulling the best arm based on information accumulated so far, and “exploration", pulling the arm that will assist in future choices, although it does not seem to be the best option at the moment. Application areas include the mobile healthcare system (Tewari and Murphy,, 2017), web page ad placement algorithms (Langford et al.,, 2008), news article placement algorithms (Li et al.,, 2010), revenue management (Ferreira et al.,, 2018), marketing (Schwartz et al.,, 2017), and recommendation systems (Kawale et al.,, 2015).

Contextual MAB algorithms make use of side information, called context, given in the form of finite-dimensional covariates. For example, in the news article recommendation example, information on the visiting user as well as the articles are given in the form of a context vector. In 2010, the Yahoo! team (Li et al.,, 2010) proposed a contextual MAB algorithm which assumes a linear relationship between the context and reward of each arm. This algorithm achieved a 12.5% click lift compared to a context-free MAB algorithm. Many other bandit algorithms have been proposed for linear reward models (Auer,, 2002; Dani et al.,, 2008; Chu et al.,, 2011; Abbasi-Yadkori et al.,, 2011; Agrawal and Goyal,, 2013).

The aforementioned methods require the dimension of the context not be too large. This is because in these algorithms, the cumulative gap between the rewards of the optimal arm and the chosen arm, namely regret, is shown to be proportional to a polynomial function of the dimension of the context, . In modern applications however, it is often the case that the web or mobile-based contextual variables are high-dimensional. Li et al., (2010) applied a dimension reduction method (Chu et al.,, 2009) to the context variables before applying their bandit algorithm to the Yahoo! news article recommendation log data.

In this paper, we introduce a novel approach to the case where the contextual variables are high-dimensional but only a sparse subset of size is correlated with the reward. We specifically consider the stochastic linear contextual bandit (LCB) problem, where the arms are represented by different contexts at a specific time , and the rewards are controlled by a single linear regression parameter , i.e., has mean for . The LCB problem is distinguished from the contextual bandit problem with linear rewards (CBL), where the context does not differ by arms but the the reward of the -th arm is determined by an arm-specific parameter , i.e., has mean for .

When the number of arms is large, the CBL approach is not practical due to large number of parameters. Methods for CBL are also not suited to handle the case where the set of arms changes with time. When we recommend a news article or place an advertisement on the web page, the lists of news articles or advertisements change day by day. In this case, it would not be feasible to assign a different parameter for every new incoming item. Therefore, when the number of arms is large and the set of arms changes with time, LCB approaches including the proposed method can be applied while the CBL approaches cannot.

In supervised learning, Lasso (Tibshirani,, 1996) is a good tool for estimating the linear regression parameter when the covariates are high-dimensional but only a sparse subset is related to the outcome. However, the fast convergence property of Lasso is guaranteed when data are i.i.d. and when the observed covariates are not highly correlated, the latter referred to as the compatibility condition (van de Geer and Bühlmann,, 2009). In the contextual bandit setting, these conditions are often violated because the observations are adapted to the past and the context variables for which the rewards are observed converge to a small region of the whole context distribution as the learner updates its arm selection policy.

In the proposed method, we resolve the non-compatibility issue by coalescing the methods from missing data literature. We start from the observation that the bandit problem is a missing data problem since the rewards for the arms that are not chosen are not observed, hence, missing. The difference is that in missing data settings, missingness is controlled by the environment and given to the learner while in bandit settings, the missingness is controlled by the learner. Since the learner controls the missingness, the missing mechanism, or arm selection probability is known in bandit settings. Given this probability, we can construct unbiased estimates of the rewards for the arms not chosen, using the doubly-robust technique (Bang and Robins,, 2005), which allows capitalizing on the context information corresponding to the arms that are not chosen. These data are observed and available, however, were not utilized by most of the existing contextual bandit algorithms.

We propose the Doubly-Robust Lasso Bandit algorithm which hinges on the sparse structure as in Lasso (Tibshirani,, 1996), but utilizes contexts for unchosen arms by blending the doubly-robust technique Bang and Robins, (2005) used in missing data literature. The high-probability upper bound of the regret incurred by the proposed algorithm has order where is the total number of time steps. We note that the regret does not depend on the number of arms, , and scales with instead of a polynomial function of . Therefore, the regret of the proposed algorithm is sublinear in even when and scales with .

Abbasi-Yadkori et al., (2012), Carpentier and Munos, (2012) and Gilton and Willett, (2017) considered the sparse LCB problem as well. While the high-probability regret bound of Abbasi-Yadkori et al., (2012) does not depend on , it is proportional to instead of , so is not sublinear in when scales with . Carpentier and Munos, (2012) used an explicit exploration phase to identify the support of the regression parameter using techniques from compressed sensing. Their regret bound is tight scaling with , but the algorithm is specific to the case where the set of arms is the unit ball for the norm and fixed over time. Gilton and Willett, (2017) leveraged ideas from linear Thompson Sampling and Relevance Vector Machines (Tipping,, 2001). The theoretical results of Gilton and Willett, (2017) are weak since they derived the regret bound under the assumption that a sufficiently small superset of the support for the regression parameter is known in advance.

Bastani and Bayati, (2015) addressed the CBL problem with high-dimensional contexts. They proposed the Lasso Bandit algorithm which uses Lasso to estimate the parameter of each arm separately. To solve non-compatibility, Bastani and Bayati, (2015) used forced-sampling of each arm at predefined time points and maintained two estimators for each arm, one based on the forced-samples and the other based on all samples. They derived a regret bound of order . For the same problem, Wang et al., (2018) proposed the Minimax Concave Penalized (MCP) Bandit algorithm which uses forced-sampling along with the MCP estimator (Zhang,, 2010) and improved the bound of Bastani and Bayati, (2015) to .

The regrets of Bastani and Bayati, (2015) and Wang et al., (2018) increase linearly with due to separate estimation for each arm. When the number of arms is bigger than , these algorithms should terminate before the forced-sampling of each arm is completed, thus may not be practical. In contrast, the proposed method allows to share information across arms so its performance does not depend on . In cases where all three methods are applicable, the proposed algorithm requires one less tuning parameter than Lasso Bandit and MCP Bandit, which is a significant advantage for an online learning algorithm as it is difficult to simultaneously tune the hyperparameters and achieve high reward.

We summarize the main contributions of the paper as follows.

-

•

We propose a new linear contextual MAB algorithm for high-dimensional, sparse reward models. The proposed method is simple and requires less tuning parameters than previous works.

-

•

We propose a new estimator for the regression parameter in the reward model which uses Lasso with the context information of all arms through the doubly-robust technique.

-

•

We prove that the high-probability regret upper bound of the proposed algorithm is , which does not depend on and scales with .

-

•

We present experimental results that show the superiority of our method especially when is big and the contexts of different arms are correlated.

1.1 Related Work

The fast convergence of Lasso for linear regression parameter was extenstively studied in van de Geer, (2007), Bickel et al., (2009), and van de Geer and Bühlmann, (2009). The doubly-robust technique was originally introduced in Robins et al., (1994) and extensively analyzed in Bang and Robins, (2005) under supervised learning setup. Dudík et al., (2014), Jiang and Li, (2016), and Farajtabar et al., (2018) are recent works that incorporate the doubly-robust methodology into reinforcement learning but under offline learning settings. Dimakopoulou et al., (2018) was the first to blend the doubly-robust technique in the online bandit problem. Their work, which focused on low-dimensional settings, proposed to use the doubly-robust technique as a way of balancing the data over the whole context space which makes the online regression less prone to bias when the reward model is misspecified.

2 Settings and Assumptions

In the MAB setting, the learner is repeatedly faced with alternative arms where at time , the -th arm () yields a random reward with unknown mean . We assume that there is a finite-dimensional context vector associated with each arm at time and that the mean of depends on , i.e., where is an arbitrary function. Among the arms, the learner pulls one arm , and observes reward . The optimal arm at time is . Let be the difference between the expected reward of the optimal arm and the expected reward of the arm chosen by the learner at time , i.e.,

Then, the goal of the learner is to minimize the sum of regrets over steps,

We specifically consider a sparse LCB problem, where is linear in ,

| (1) |

where is unknown and , denoting the -norm. Hence, only elements in are assumed to be nonzero. We also make the following assumptions, from A1 to A4.

A1.

Bounded norms. Without loss of generality,

A2.

IID Context Assumption. The distribution of context variables is i.i.d. over time :

where is some distribution over .

We note in A2 that given time , the contexts from different arms are allowed to be correlated.

A3.

Compatibility Assumption (van de Geer and Bühlmann,, 2009). Let be a set of indices and be a positive constant. Define

Then such that

where and denotes the support of .

A3 ensures that the Lasso estimate of converges to the true parameter in a fast rate. This assumption is weaker than the restricted eigenvalue assumption (Bickel et al.,, 2009).

A4.

Sub-Gaussian error. The error is -sub-Gaussian for some , i.e., for every

Assumption A4 is satisfied whenever .

3 Doubly-Robust Lasso Bandit

Lemma 11.2 of van de Geer and Bühlmann, (2009) shows that when the covariates satisfy the compatibility condition and the noise is i.i.d. Gaussian, the Lasso estimator of the linear regression parameter converges to the true parameter in a fast rate. We restate the lemma.

Lemma 3.1.

(Lemma 11.2 of van de Geer and Bühlmann,, 2009) Let and be random variables with where , , and ’s are i.i.d. Gaussian with mean zero and variance . Let be the Lasso estimator of based on the first observations using for the regularization parameter in the penalty, i.e.,

If for some , then for , with probability at least ,

| (2) |

Two hurdles that arise when incorporating Lemma 3.1 into the contextual MAB setting are that (a) (non-i.i.d.) the errors ’s are not i.i.d., and (b) (non-compatibility) the Gram matrix does not satisfy the compatibility condition even under assumption A3 because the context variables of which the rewards are observed do not evenly represent the whole distribution of the context variables. In the LCB setting, corresponds to . Since the learner tends to choose the contexts that yield maximum reward as time elapses, the chosen context variables ’s converge to a small region of the whole context space. We discuss on remedies to (a) and (b) in Section 3.1 and Section 3.2, respectively.

3.1 Lasso Oracle Inequality with non-i.i.d. noise

3.2 Doubly-robust pseudo-reward

To overcome the non-compatibility problem, in the CBL setting, Bastani and Bayati, (2015) proposed to impose forced-sampling of each arm at predefined time steps, which produces i.i.d. data. The following lemma shows that when ’s are i.i.d. and , then with high probability.

Lemma 3.3.

(Lemma EC.6. of Bastani and Bayati,, 2015) Let be i.i.d. random vectors in with for all . Let and Suppose that . Then if ,

| (4) |

where .

We derive the following corollary simply by setting the right-hand side of (4) larger than .

Corollary 3.4.

Suppose that the conditions of Lemma 3.3 are satisfied. Let for some . Then with probability at least ,

| (5) |

The setting of Bastani and Bayati, (2015) is different from ours in that they assume the context variable is the same for all arms but the regression parameter differs by arms. Bastani and Bayati, (2015) maintained two sets of estimators for each arm, the estimator based on the forced-samples and the one based on all samples. Whereas the latter is not based on i.i.d. data, using the forced-sample estimator as a pre-processing step of selecting a subset of arms and then using the all-sample estimator to select the best arm among this subset guarantees that there are i.i.d. samples for each arm, so the all-sample estimator converges in a fast rate as well.

We propose a different approach to resolve non-compatibility, which is based on the doubly-robust technique in missing data literature. We define the filtration as the union of the observations until time and the contexts given at time , i.e.,

Given , we pull the arm randomly according to probability , where is the probability of pulling the -th arm at time given . We specify the values of (t) later in Section 3.3. Let be the estimate given . After the reward is observed, we construct a doubly-robust pseudo-reward:

Whether or not is a valid estimate, this value has conditional expectation given that for all :

Thus by weighting the observed reward with the inverse of its observation probability , we obtain an unbiased estimate of the reward corresponding to the average context instead of . Applying Lasso regression to the pair instead of , we can make use of the i.i.d. assumption A2 and the compatibility assumption A3 with Corollary 3.4 to achieve a fast convergence rate for as in (3). We later show that when in Corollary 3.4 corresponds to , (5) holds with .

Since the allocation probability is known given , the simple inverse probability weighting (IPW) estimator also gives an unbiased estimate for the reward corresponding to the average context. We however show in the next paragraphs that the doubly-robust estimator has constant variance under minor condition on the weight while the IPW estimator has variance that increases with under the same condition. Constant variance is crucial for the performance of the algorithm, since it affects the convergence property of in (3) and eventually the regret upper bound in Theorem 4.1. We can make the IPW estimator have constant variance as well under stronger condition on , but this stronger condition is shown to result in regret linear in .

Let be the variance of given . We have,

| (6) |

Suppose satisfies the Lasso convergence property (3), i.e., for . Then we can bound the first and third terms of (6) by a constant under the following restriction,

| (7) |

Due to assumption A4 on the sub-Gaussian error , the second term of (6) is also bounded by a constant under (7). Hence, we have . Therefore if (7) holds and if all satisfy the Lasso convergence property (3), then the pseudo-rewards all have constant variance. Consequently, the estimate based on satisfies (3). Meanwhile, the restriction (7) leads to suboptimal choice of arms at each with probability that decreases with time. In Theorem 4.1, we prove that the regret due to this suboptimal choice is sublinear in .

The variance of given filtration is . As opposed to the first and third terms in (6), the term still increases with under (7). To achieve a constant variance, we need be larger than a predetermined constant value, . Simply replacing in with the truncated value will produce a biased estimate of when is actually smaller than , and the resulting estimate will not satisfy convergence property (3). If we instead directly constrain to be larger than , this will lead to suboptimal choice of arms at each with constant probability so the regret will increase linearly in .

3.3 Doubly-Robust Lasso Bandit algorithm

To make for all , we simply pull arms according to the uniform distribution when . Then to ensure for all , we randomize the arm selection at each step between uniform random selection and deterministic selection using the estimate of the last step, This can be implemented in two stages. First, sample from a Bernouilli distribution with mean where is a tuning parameter. Then if , pull the arm with probability , otherwise, pull the arm . Under this procedure, we have which satisfies (7). In practice, we treat as a tuning parameter.

The proposed Doubly-Robust (DR) Lasso Bandit algorithm is presented in Algorithm 1. The algorithm selects via two stages, computes , constructs the pseudo-reward and average context , and updates the estimate using Lasso regression on the pairs ’s. Recall that the regularization parameter should be set as to guarantee (3) for a fixed . To guarantee (3) for every , we impute instead of . Hence at time , we update where is a tuning parameter. The algorithm requires three tuning parameters in total, while Bastani and Bayati, (2015) and Wang et al., (2018) require four.

4 Regret analysis

Under (1), the regret at time is where We establish the high-probability regret upper bound for Algorithm 1 in the following theorem.

Theorem 4.1.

We provide a sketch of proof in the next section. A complete proof is presented in the Supplementary Material.

4.1 Sketch of proof for Theorem 4.1

In the DR Lasso Bandit algorithm, each of the decision steps corresponds to one of the following three groups.

-

(a)

: the arms are pulled according to the uniform distribution.

-

(b)

and : the arms are pulled according to the uniform distribution.

-

(c)

and : the arm is pulled.

We let . The strategy of the proof is to bound the regrets from each separate group and sum the results.

Due to assumption A1 on the norms of and is not larger than in any case. Therefore, the sum of regrets from group (a) is at most which corresponds to the first term in Theorem 4.1. We now denote the sum of regrets from group (b) and group (c) as and respectively. We first bound in Lemma 4.2, which follows from the fact that is a Bernouilli variable with mean and Hoeffding’s inequality.

Lemma 4.2.

With probability at least

To bound , we further decompose group (c) into the following two subgroups, where we set with .

(c-a) , : is pulled and

(c-b) , : is pulled and

We first show in Lemma 4.3 that the subgroup (c-b) is empty with high probability. Since is computed from the pairs where the average contexts ’s satisfy the compatibility condition (5) and the pseudo-rewards ’s are unbiased with constant variance, Lemma 3.2 can be applied on .

Lemma 4.3.

Finally when belongs to group (c-a), is trivially bounded by Hence we can bound as in the following lemma.

Lemma 4.4.

With probability at least

5 Simulation study

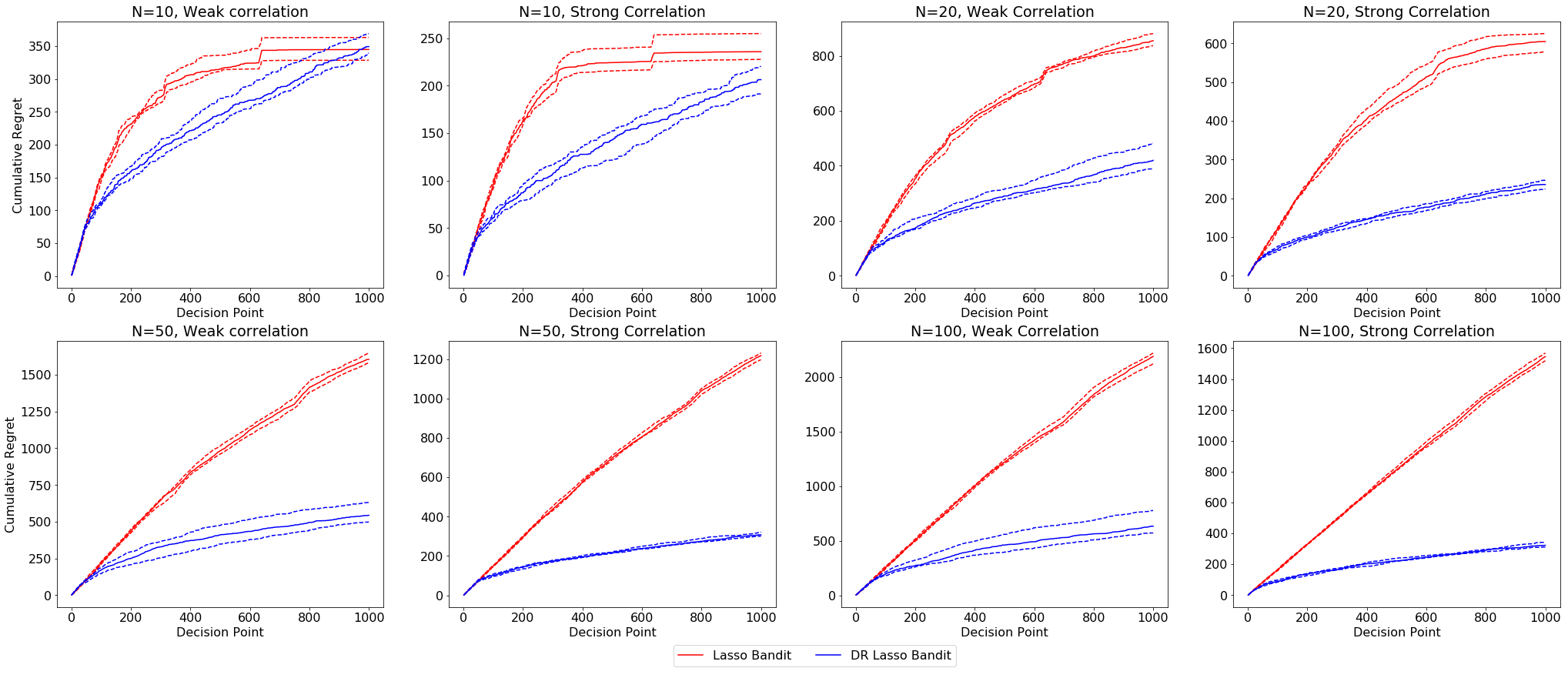

We conduct simulation studies to evaluate the proposed DR Lasso Bandit and the Lasso bandit (Bastani and Bayati,, 2015). We set or , , and . For fixed we generate from where for every and for every . We experiment two cases for , either (weak correlation) or (strong correlation). We generate and the rewards from (1). We set and generate the non-zero elements from a uniform distribution on .

We conduct 10 replications for each case. The Lasso Bandit algorithm can be applied in our setting by considering a -dimensional context vector and a -dimensional regression parameter for each arm where . For each algorithm, we consider some candidates for the tuning parameters and report the best results. For DR Lasso Bandit, we advise to truncate the value so that it does not explode.

Figure 1 shows the cumulative regret according to time . When the number of arms is as small as 10, Lasso Bandit converges faster to the optimal decision rule than DR Lasso Bandit. However, we notice that the regret of Lasso Bandit in the early stage is larger than DR Lasso Bandit, which is due to forced-sampling of arms. With larger number of arms, DR Lasso Bandit outperforms Lasso Bandit. Compared to Lasso Bandit, the regret of DR Lasso Bandit decreases dramatically as the correlation among the contexts of different arms increases. We also verify that the performance of the proposed method is not sensitive to , while the regret of Lasso Bandit increases with .

6 Concluding remarks

Sequential decision problems involving web or mobile-based data call for contextual MAB methods that can handle high-dimensional covariates. In this paper, we propose a novel algorithm which enjoys the convergence properties of the Lasso estimator for i.i.d. data via a doubly-robust technique established in the missing data literature. The proposed algorithm attains a tight high-probability regret upper bound which depends on a polylogarithmic function of the dimension and does not depend on the number of arms, overcoming weaknesses of the existing algorithms.

References

- Abbasi-Yadkori et al., (2011) Abbasi-Yadkori, Y., Pál, D. and Szepesvári, C. Improved algorithms for linear stochastic bandits. In Advances in Neural Information Processing Systems, pp. 2312–2320, 2011.

- Abbasi-Yadkori et al., (2012) Abbasi-Yadkori, Y., Pál, D. and Szepesvari, C. Online-to-confidence-set conversions and application to sparse stochastic bandits. In Artificial Intelligence and Statistics, pp. 1–9, 2012.

- Agrawal and Goyal, (2013) Agrawal, S. and Goyal, N. Thompson sampling for contextual bandits with linear payoffs. In Proceedings of the 30th International Conference on Machine Learning, pp. 127–135, 2013.

- Auer, (2002) Auer, P. Using confidence bounds for exploitation-exploration trade-offs. Journal of Machine Learning Research, 3:397–422, 2002.

- Bang and Robins, (2005) Bang, H. and Robins, J.M. Doubly robust estimation in missing data and causal inference models. Biometrics, 61(4):962-973, 2005.

- Bastani and Bayati, (2015) Bastani, H. and Bayati, M. Online decision-making with high-dimensional covariates. Available at SSRN 2661896, 2015.

- Bickel et al., (2009) Bickel, P., Ritov, Y. and Tsybakov, A. Simultaneous analysis of Lasso and Dantzig selector. Annals of Statistics, 37:1705–-1732, 2009.

- Carpentier and Munos, (2012) Carpentier, A. and Munos, R. Bandit theory meets compressed sensing for high dimensional stochastic linear bandit. In Artificial Intelligence and Statistics (AISTATS), pp. 190–198, 2012.

- Chu et al., (2009) Chu, W., Park, S.T., Beaupre, T., Motgi, N., Phadke, A., Chakraborty, S. and Zachariah, J. A case study of behavior-driven conjoint analysis on Yahoo!: front page today module. In Proceedings of the 15th ACM SIGKDD international conference on Knowledge discovery and data mining, pp. 1097-1104, 2009.

- Chu et al., (2011) Chu, W., Li, L., Reyzin, L. and Schapire, R.E. Contextual bandits with linear payoff functions. In Proceedings of the 14th International Conference on Artificial Intelligence and Statistics, pp. 208–214, 2011.

- Dani et al., (2008) Dani, V., Hayes, T. P. and Kakade, S. M. Stochastic linear optimization under bandit feedback. In Conference on Learning Theory, pp. 355–-366, 2008.

- Dimakopoulou et al., (2018) Dimakopoulou, M., Zhou, Z., Athey, S. and Imbens, G. Balanced Linear Contextual Bandits. arXiv preprint arXiv:1812.06227, 2018.

- Dudík et al., (2014) Dudík, M., Erhan, D., Langford, J. and Li, L. Doubly robust policy evaluation and optimization. Statistical Science, 29(4):485-511, 2014.

- Farajtabar et al., (2018) Farajtabar, M., Chow, Y. and Ghavamzadeh, M. More Robust Doubly Robust Off-policy Evaluation. In Proceedings of the 35th International Conference on Machine Learning, pp. 1446-1455, 2018.

- Ferreira et al., (2018) Ferreira, K., Simchi-Levi, D. and Wang, H. Online network revenue management using Thompson sampling. Operations Research, 66(6):1586–1602, 2018.

- Gilton and Willett, (2017) Gilton, D. and Willett, R. Sparse linear contextual bandits via relevance vector machines. In International Conference on Sampling Theory and Applications (SampTA), pp. 518–522, 2017.

- Jiang and Li, (2016) Jiang, N. and Li, L. Doubly Robust Off-policy Value Evaluation for Reinforcement Learning. In Proceedings of the 33rd International Conference on Machine Learning, pp. 652-661, 2016.

- Kawale et al., (2015) Kawale, J., Bui, H.H., Kveton, B., Tran-Thanh, L. and Chawla, S. Efficient Thompson sampling for online matrix-factorization recommendation. In Advances in Neural Information Processing Systems, pp. 1297–1305, 2015.

- Lai and Robbins, (1985) Lai, T.L. and Robbins, H. Asymptotically efficient adaptive allocation rules. Advances in Applied Mathematics, 6(1):4–22, 1985.

- Langford et al., (2008) Langford, J., Strehl, A. and Wortman, J. Exploration scavenging. In Proceedings of the 25th International Conference on Machine Learning, pp. 528–535, 2008.

- Li et al., (2010) Li, L., Chu, W., Langford, J. and Schapire, R. E. A contextual-bandit approach to personalized news article recommendation. In Proceedings of the 19th International Conference on World wide web, pp. 661–670, 2010.

- Robbins, (1952) Robbins, H. Some aspects of the sequential design of experiments. Bulletin of the American Mathematical Society, 58(5):527–535, 1952.

- Robins et al., (1994) Robins, J. M., Rotnitzky, A. and Zhao, L. P. Estimation of regression coefficients when some regressors are not always observed. Journal of the American statistical Association, 89(427):846-866, 1994.

- Schwartz et al., (2017) Schwartz, E.M., Bradlow, E.T. and Fader, P.S. Customer acquisition via display advertising using multi-armed bandit experiments. Marketing Science, 36(4):500–522, 2017.

- Tewari and Murphy, (2017) Tewari, A., and Murphy, S.A. From ads to interventions: contextual bandits in mobile health. In Mobile Health (pp. 495–517). Springer, Cham, 2017.

- Tibshirani, (1996) Tibshirani, R. Regression shrinkage and selection via the lasso. Journal of the Royal Statistical Society: Series B (Methodological), 58(1):267-288, 1996.

- Tipping, (2001) Tipping, M. E. Sparse Bayesian learning and the relevance vector machine. Journal of machine learning research, 1(Jun):211-244, 2001.

- van de Geer, (2007) van de Geer, S. The deterministic Lasso. In JSM proceedings, American Statistical Association, (see also http://stat.ethz.ch/research/research reports/2007/140), 2007.

- van de Geer and Bühlmann, (2009) van de Geer, S. A. and Bühlmann, P. On the conditions used to prove oracle results for the Lasso. Electronic Journal of Statistics, 3:1360–1392, 2009.

- Wang et al., (2018) Wang, X., Wei, M. M. and Yao, T. Minimax Concave Penalized Multi-Armed Bandit Model with High-Dimensional Convariates. In Proceedings of the 35th International Conference on Machine Learning, pp. 5187–5195, 2018.

- Yahoo, (2019) Yahoo! Webscope. Yahoo! Front Page Today Module User Click Log Dataset, version 1.0. http://webscope.sandbox.yahoo.com. Accessed: 09/01/2019.

- Zhang, (2010) Zhang, C. H. Nearly unbiased variable selection under minimax concave penalty. Annals of statistics, 38(2):894-942, 2010.

Supplementary Material:

Doubly-Robust Lasso Bandit

Gi-Soo Kim

Department of Statistics

Seoul National University

gisoo1989@snu.ac.kr

&Myunghee Cho Paik

Department of Statistics

Seoul National University

myungheechopaik@snu.ac.kr

A Proof of Lemma 4.2

Since is not larger than 1 in any case, , where is a sequence of independent Bernoulli variables with By Hoeffding’s inequality,

for any . Setting , we have Hence, with probability at least ,

Since ,

where the first inequality is due to Jensen’s inequality and the second is due to

B Proof of Lemma 4.3

Recall that we defined where . Due to assumptions A2 and A3 and Corollary 3.4, we have with probability at least ,

| (i) |

where . It remains to show that when (i) holds, the left-hand side of (8) is smaller than . In Section 3.2, we have shown that given the conditioning argument in (8) and the restriction (7) on , is -sub-Gaussian for all , with . Applying Lemma 3.2 with for , , and completes the proof.

C Proof of Lemma 4.4

Suppose corresponds to subgroup (c-a). Since for this subgroup, and

where the second inequality is due to Cauchy-Schwarz inequality and the third inequality is due to assumption A1. Hence, the sum of regrets from subgroup (c-a) is at most which we can bound as follows.

The derivation is analogous to that of the upper bound of because and have the same order in . Meanwhile, we proved in Lemma 4.3 that the subgroup (c-b) is empty with probability at least Therefore, with probability at least

D Proof of Theorem 4.1

Let be the sum of regrets from group (a). Due to , Lemma 4.2, and Lemma 4.4, we have with probability at least