Functional Models for Time-Varying Random Objects

Abstract

Functional data analysis provides a popular toolbox of functional models for the analysis of samples of random functions that are real-valued. In recent years, samples of time-varying object data such as time-varying networks that are not in a vector space have been increasingly collected. These data can be viewed as elements of a general metric space that lacks local or global linear structure and therefore common approaches that have been used with great success for the analysis of functional data, such as functional principal component analysis, cannot be applied. In this paper we propose metric covariance, a novel association measure for paired object data lying in a metric space that we use to define a metric auto-covariance function for a sample of random -valued curves, where generally will not have a vector space or manifold structure. The proposed metric auto-covariance function is non-negative definite when the squared semimetric is of negative type. Then the eigenfunctions of the linear operator with the auto-covariance function as kernel can be used as building blocks for an object functional principal component analysis for -valued functional data, including time-varying probability distributions, covariance matrices and time-dynamic networks. Analogues of functional principal components for time-varying objects are obtained by applying Fréchet means and projections of distance functions of the random object trajectories in the directions of the eigenfunctions, leading to real-valued Fréchet scores. Using the notion of generalized Fréchet integrals, we construct object functional principal components that lie in the metric space . We establish asymptotic consistency of the sample based estimators for the corresponding population targets under mild metric entropy conditions on and continuity of the -valued random curves. These concepts are illustrated with samples of time-varying probability distributions for human mortality, time-varying covariance matrices derived from trading patterns, and time-varying networks that arise from New York taxi trips.

KEY WORDS: Dynamic Networks, Fréchet Integral, Functional Data Analysis, Metric Covariance, Object Data, Principal Component Analysis, Stochastic Processes.

1 Introduction

Time-varying data where one collects an i.i.d. sample of random functions, which take values in a general object space that does not have a linear structure, are increasingly common, while the statistical methodology for the analysis of such data has been lagging behind. We aim to introduce techniques that will help to fill this gap. For the case where observations consist of samples of random trajectories that take values in , the methodology of choice is often Functional Data Analysis (FDA) (Ramsay and Silverman, 2005; Horvath and Kokoszka, 2012; Wang et al., 2016), where methodology for one-dimensional () functional data is readily available. Models for functional data that consist of vector-valued processes () have been studied more recently (Zhou et al., 2008; Berrendero et al., 2011; Chiou et al., 2014; Claeskens et al., 2014; Verbeke et al., 2014; Chiou et al., 2016) as well as the case where at each time point one records a random function, i.e. function-valued stochastic processes (Park and Staicu, 2015; Chen and Müller, 2012; Chen et al., 2017). In these models, the responses are situated in a linear space, either the Euclidean space or the Hilbert space . Functions of objects in spaces that can be locally approximated by linear spaces such as Riemannian manifolds including spheres have also been considered more recently (Lin et al., 2017; Dai and Müller, 2018). The major objective of this paper is to overcome the global or local linearity assumptions inherent in these previous approaches. The challenge is that existing FDA methodology relies on vector operations and inner products, which are no longer available.

Functional Principal Component Analysis (FPCA) (Kleffe, 1973; Dauxois et al., 1982) has emerged as the method of choice to represent and interpret samples of random functions that take values in linear spaces. It also provides dimension reduction by expanding an underlying random process into the basis functions given by the eigenfunctions of the auto-covariance operator and then truncating this expansion at a finite number of expansion terms. A related tool are the modes of variation, which enable exploration of the effects of single eigendirections (Castro et al., 1986; Jones and Rice, 1992) and are useful in practical applications (Dong et al., 2018). FPCA also provides a starting point for many theoretical investigations and FDA techniques such as functional clustering (Chiou and Li, 2007; Jacques and Preda, 2014; Suarez and Ghosal, 2016) or regression and classification (Yao et al., 2005a; Dai et al., 2017).

As we enter the era of big data, it has become increasingly common to observe more complex, often non-Euclidean, data on a time grid. Technological advances have made it possible to record and efficiently store time courses of image, network, sensor or other complex data. For example, neuroscientists are interested in dynamic functional connectivity, where one essentially observes samples of time-varying covariance or correlation matrices obtained from functional Magnetic Resonance Imaging (fMRI) data for each subject in a sample. Time-varying network data arise in various forms, e.g. road or internet traffic networks or time-evolving social networks, and it is of interest to extract structure and patterns from such data.

To obtain efficient and interpretable summaries of the information contained in samples of complex observations is a major task in modern statistics that has led for example to the development of methods such as Geodesic Principal Component Analysis (GPCA) in the space of probability distributions on (Bigot et al., 2017) and on more general Hilbert spaces (Seguy and Cuturi, 2015) that utilize optimal transport geometry and geodesic curves under the Wasserstein metric. These approaches utilize geodesics to connect the random distributions with the Wasserstein barycenters. We aim here at identifying dominant directions of variation in a sample of time-varying random object trajectories, where the random objects are indexed by time and are situated in a general metric space. The time-varying aspect provides for a novel and little explored setting, and to develop tools that are supported by theory and are useful for the further exploration and analysis of such data is the main motivation for this paper.

While FPCA for samples of functions taking values in smooth Riemannian manifolds has been studied both practically and theoretically (Anirudh et al., 2017; Dai and Müller, 2018), these approaches critically depend on the local Euclidean property of Riemannian manifolds and cannot be extended to functional data objects that take values in more general metric spaces that do not have a tractable and relatively simple Riemannian geometry. FPCA for doubly functional data, where the observations at each time point are functions rather than scalars (Chen et al., 2017), is based on a tensor product representation of the underlying function-valued stochastic process. The functions need to be Hilbert-space valued, so that this approach cannot be applied to non-Hilbertian data. Due to the lack of linear structure, developing a form of FPCA for random functions taking values in a metric space, which we refer to as functional random objects, is a major challenge.

Consider a totally bounded separable metric space and a random sample of fully observed -valued functional data. Aiming to extend key tools of FDA to cover such data, we first revisit the well-established FPCA for the case of real valued functional data. The essence of FPCA is contained in the auto-covariance structure of the underlying random functions, i.e. their covariance at different time points. This leads to the question how to quantify correlation between random objects in general metric spaces that correspond to the values of the random function at different time points. An example for such an extension of Pearson correlation to the case of multivariate data is the RV coefficient (Robert and Escoufier, 1976), which is zero if all of the vector components are uncorrelated and strictly positive otherwise.

In this article we introduce metric covariance, which is a novel association measure for paired data in general metric spaces. Metric covariance differs in key aspects from distance correlation, another measure of dependence between metric space data (Lyons, 2013; Székely and Rizzo, 2017), the latter being primarily suited to measure probabilistic independence rather than for quantifying the strength of ‘positive’ or ‘negative’ association, which is the primary goal of the former. Unlike distance covariance, the magnitude of metric covariance quantifies the degree of association between paired data objects. The key component of FPCA is to decompose the variation in a sample of trajectories into orthogonal directions. An important difference between metric covariance and distance covariance, which is specifically relevant in this context, arises when considering the associated notion of variance. In contrast to distance correlation, metric covariance of a random object with itself leads to an interpretable notion of variance for data objects, as we will demonstrate below. We also show that metric covariance is symmetric and non-negative definite whenever the squared distance is a semimetric of negative type (Sejdinovic et al., 2013; Lyons, 2013; Schoenberg, 1938). The notion of metric correlation can then be easily derived from metric covariance and random objects will be considered to be uncorrelated if they have a metric correlation of size 0.

In FPCA for -valued functional data, once the auto-covariance function has been determined, one defines a linear Hilbert-Schmidt operator whose eigenfunctions represent the orthonormal directions of variance for the functional data in the Hilbert space . The corresponding eigenvalues represent the fraction of variance explained by the respective functional principal components (FPCs), which are the lengths of the projections of the functional data in the direction of each eigenfunction. How can one extend these ideas to object-valued functional data, where one does not have a linear structure or inner product? We proceed by constructing a linear Hilbert-Schmidt operator using the proposed metric covariance as its kernel and utilize its eigenfunctions and eigenvalues. For real valued functional data, one obtains the FPCs by the Karhunen-Loève expansion of centered functional data in the eigenbasis, where the FPCs are the inner products of the centered functional data with respect to the eigenfunctions. Unfortunately it is not possible to ‘center’ object functional data living in general metric spaces and one also does not have an inner product. In the case of FDA in the Hilbert space , the inner products can be expressed as integrals. While due to the lack of linear structure there is no integral for functional random objects, the interpretation of inner products as integrals nevertheless provides a way forward that we develop in this paper. We propose two approaches for obtaining FPCs for object functional data, one in which the FPCs are scalar irrespective of the nature of the metric space in which the random objects live, and an alternative approach in which the FPCs themselves are random objects, i.e. valued.

To obtain FPCs in object space, we introduce the notion of a generalized Fréchet integral of an -valued curve with respect to a real valued function, where this integral resides in . Generalized Fréchet integrals depend on the underlying metric in and are defined under the constraint that the real valued function in the integrand integrates to one. We draw inspiration from the covariance integral for multivariate functional data that was previously introduced as a Fréchet integral (Petersen and Müller, 2016). This previous integral is a special case of the generalized Fréchet integral introduced here; it corresponds to the special case where is the space of covariance matrices and the real valued function in the integrand is the constant function one. We demonstrate that the resulting Object Functional Principal Components (Object FPCs), which reside in , provide useful insights about the structure of the underlying functional random objects.

For an alternative scalar approach, we extract relatively simple characteristics from the object functional data. A first step is to define a ‘mean’ function using the notion of Fréchet means (Fréchet, 1948). This mean function resides in the object function space and serves as a ‘central’ trajectory for the object functional data. To obtain a representative scalar FPC for a specific random object trajectory and eigenfunction, we utilize projections of the distance function between the specific random object trajectory and the Fréchet mean trajectory on each of the eigenfunctions. The resulting Fréchet scores encapsulate variation in the departures of functional random objects from the Fréchet mean trajectory. As we illustrate in simulations and data analysis, plotting these Fréchet scores against each other often illustrates meaningful patterns in the sample of object functional data that are generally hard to capture visually, due to their complexity and non-linearity. For example, such plots can aid in detecting the presence of clusters or outliers in functional random objects.

In this paper, we have three major objectives. First, we lay out a framework for extending FPCA to general metric space valued functional data. The population target parameters are the metric auto-covariance operator, its eigenvalues and eigenfunctions and the population Fréchet mean function, which are introduced in section 2; additionally, the object FPCs, which are generalized Fréchet integrals and the Fréchet scores (section 3). Second, we provide sample based estimators of these population targets and establish their asymptotic properties under mild restrictions on the metric entropy of the metric space and the continuity of the object functional data (section 4). Proofs of all results are in section S1 of the online supplement. Third, we illustrate our results through simulations (section 5) and various data examples (section 6), which include samples of time-varying probability distributions of age at death obtained from human mortality data of 32 countries, time-varying yellow taxi trip networks of different regions in Manhattan observed daily during the year 2016, and of changing trade patterns between countries that can be represented as time-varying covariance matrices, followed by a brief discussion (section 7).

2 Metric Covariance

2.1 Covariance and correlation for random objects

We consider a totally bounded separable metric space where is a metric and an -valued stochastic process on the interval . With denoting the probability measure of the random process , we are given a sample of random -valued functions on generated by . The simplest case is with the intrinsic Euclidean metric, where is a sample of real valued functional data. For general metric spaces , we refer to as a sample of functional random objects. Inspired by the approach to FPCA for real valued functional data, our first goal is to quantify the association between random objects and in , where and are two arbitrary points in the domain .

For motivation, consider first the case of real random variables with finite covariance. Imagine for a moment that we cannot add, subtract or multiply these r.v.s and are restricted to compute their distances . As is well known, one then can write the variance of using an i.i.d. copy of by .

Interestingly, this non-algebraic construction can be extended to the covariance of : Let be an i.i.d. copy of . We then obtain an alternate formulation of in terms of pairwise distances as follows,

If are -valued random variables with denoting the Euclidean distance in , a simple calculation shows that in this case,

which is the inner product in the Hilbert space of -valued random variables with finite . Next consider the case where are -valued random variables, where is a Hilbert space and is replaced by , the metric that arises from the inner product of the Hilbert space. If the metric is bounded then . One can show with some simple algebra and utilizing the Riesz representation theorem that

| (1) |

which is the inner product in , the Hilbert space of -valued random variables such that .

What happens if are -valued random variables and we replace by where is a general metric space with no vector space structure to rely on? Or, for which spaces does the function retain desirable properties? Proposition 3 of Sejdinovic et al. (2013) implies that whenever is a semi-metric of negative type, there exists a Hilbert space and an injective map, say , with

| (2) |

and therefore it follows from (1) that for some ‘remote’ Hilbert space and the unknown map ,

| (3) |

Here a space with a semi-metric is of negative type if for all , and with one has

These considerations motivate the following definition of a generalized version of covariance for paired random objects that take values in , where is a separable metric space,

| (4) |

where as above is an i.i.d. copy of . We refer to as metric covariance of and . Metric covariance is always finite if the underlying metric space is bounded and coincides with the usual notion of covariance in Euclidean spaces.

We also define metric correlation between two -valued random variables as follows,

By the Cauchy-Schwarz inequality one has . Metric covariance/correlation depends on the choice of the metric and different choices of might reveal different aspects of association between random objects, depending on the underlying geometry of the metric.

2.2 Metric auto-covariance operators

As in the real valued Euclidean case, we define the metric auto-covariance function for functional random objects as

for all . Obviously, is a symmetric kernel and therefore has real eigenvalues when used as the kernel of a linear Hilbert-Schmidt operator. The following result shows that for separable metric spaces for which the squared distance function is of negative type, the metric auto-covariance operator is positive semidefinite.

proposition 1

If is separable and is of negative type, then is a nonnegative definite kernel.

By Proposition 3 in Sejdinovic et al. (2013) and equation (2.1), implies that there exists an abstract Hilbert space and an injective map such that and are orthogonal in . Note that , which for real valued random variables equals .

Formally, one can define the metric auto-covariance operator as a linear Hilbert-Schmidt integral operator that operates on functions and utilizes the metric auto-covariance kernel,

We note that for example Theorem 4.6.4 of Hsing and Eubank (2015) implies the nonnegative definiteness of the kernel , in the sense that for all .

By Mercer’s theorem there is an orthonormal basis of consisting of eigenfunctions of such that the corresponding sequence of eigenvalues , which are ordered in declining order, is nonnegative, since is positive semidefinite. The eigenfunctions corresponding to non-zero eigenvalues are continuous on and has the representation

where the convergence is absolute and uniform; see, e.g. Lemma 4.6.1 and Theorems 4.5.2, 4.6.2, 4.6.5 and 4.6.7 of Hsing and Eubank (2015).

We thus accomplished the first step of extending FPCA from Euclidean valued functional data to general metric space valued functional data. The eigenfunctions can be interpreted as principal directions of variation of the functional object process and will be ordered according to the size of the associated eigenvalues. We can view the eigenvalues as representing a metric version of ‘fraction of variance explained’, which is their common interpretation in the real-valued case. The only requirement for this extension is that the squared metric is of negative type but this is not a severe restriction and in light of Proposition 3 of Sejdinovic et al. (2013) is true for the following examples:

-

1.

where is the space of univariate probability distributions on a common compact support in . Choices of include the popular 2-Wasserstein metric or the metric.

- 2.

- 3.

We conclude that in most cases of interest the auto-covariance operator and its eigenfunctions will be well defined.

2.3 Interpretation of metric covariance

When and are real valued, classical Pearson correlation captures the strength and sign of linear (also monotone) associations between and . From a geometrical perspective, Pearson correlation can be interpreted as the cosine of the angle between and . In , angles between vectors are defined using inner products, which can also be used for data in Hilbert space to characterize dependency. Specifically, for random functions in the metric space this idea leads to the notion of “dynamic correlation” in functional data analysis (Dubin and Müller, 2005), which was found to be useful for data analysis in genetics (Opgen-Rhein and Strimmer, 2006) and psychology (Liu et al., 2016). Dynamic correlation turns out to be equivalent to metric covariance when the random objects are in the Hilbert space , equipped with the usual metric. Metric covariance then provides a generalization beyond Hilbert spaces.

For general metric spaces, under the weak assumption that the squared metric is of negative type, the map from object to Hilbert space in (2) implies that metric covariance can be derived from the inner product in an abstract Hilbert space, while metric correlation is obtained by standardizing metric covariance, and is thus tied to the notion of an angle in an abstract space. Hence its magnitude can be interpreted as strength of association between random objects. While we use the existence of a map and an associated abstract Hilbert space, we do not require knowledge about . Metric covariance is thus a natural extension of Pearson covariance to general metric spaces.

In recent work (Petersen and Müller, 2019b), Wasserstein covariance for pairs of univariate probability distributions was introduced, and was shown to have an appealing interpretation as an expected value of an inner product of optimal transport maps. More specifically, if and are the components of a random bivariate density process and and the corresponding random quantile functions, the squared Wasserstein distance between and is given by

and Wasserstein covariance between and was introduced as

Wasserstein covariance is then easily seen to be a special case of metric covariance when the metric space-valued random objects are probability distributions and the Wasserstein metric is used. This Wasserstein version of metric covariance was found to quantify the degree of synchronization of the movement of probability mass from the marginal Fréchet means of the probability distributions to the random components of a multivariate density process. In applications to fMRI data, this Wasserstein version led to new findings and insights about differences in brain connectivity of normal versus Alzheimer disease patients, a topic of special interest in neuroimaging (Petersen and Müller, 2019b). The examples of dynamic correlation for Hilbert space valued random variables in functional data analysis and of Wasserstein covariance/correlation demonstrate the utility of metric covariance/correlation in non-standard spaces and its interpretability in applications. This provides evidence that metric covariance and metric correlation are indeed useful tools for data analysis in general metric spaces.

A word of caution is in order. While metric covariance covariance can be universally applied, and in the space of distributions with the Wasserstein metric has an interpretation as an inner product of transport maps, such interpretations hinge on the specific metric space in which the random objects are located and may not be available for all spaces. In practice, interpretations for specific scenarios can be important. The choice of the metric also matters and should be considered carefully, as it will affect the interpretation of metric covariance.

Apart from the interpretation of covariance as the expectation of an inner product, the diagonal elements of the metric auto-covariance surface reflect a natural notion of variance of metric-space valued objects, as

| (5) |

where is an independent copy of . This provides a variation measure that is tied to the average squared distance of objects that are independently sampled from the underlying population, which is a natural and interpretable measure of spread that is well known to coincide with conventional variance in the Euclidean case.

Since it is sensible to define variance for metric-space valued random objects as

it is then natural to extend this to a covariance measure between random objects that reflects the difference between squared distances when sampling independently from the marginal distributions of and and when sampling from the joint distribution of . This simple idea provides another avenue to suggest

Symmetrizing this expression and adding the factor .25 to match the usual definition of covariance in the Euclidean case then leads to formula (4). The above arguments also lead to an interpretation of the total variance that corresponds to the trace of the proposed metric covariance operator , as an integrated squared distance between the functional random objects and an independent copy ,

| (6) |

We find in our examples and applications that the eigenfunctions derived from metric covariance lead to useful and often well-interpretable modes of variation of the time-varying metric random objects in the sense of Jones and Rice (1992), adding to the practical appeal of metric covariance for the analysis of functional random objects.

To conclude this discussion, we note that metric covariance differs substantially from distance correlation (Székely et al., 2007; Lyons, 2013). A distinguishing feature of distance correlation is that it is equivalent to probabilistic independence between the distributions of and when it is 0, but we find that it is not suitable as a covariance or correlation measure for random objects in the situations that we study here. Specifically, the auto-covariance operator it generates is not useful for our purposes. For further details on this, see section S2 in the supplement.

3 Functional Principal Components: Generalized Fréchet Integrals and Fréchet Scores

3.1 Generalized Fréchet Integrals and Object Functional Principal Components

FPCs in the case of real valued functional data are projections of the centered process onto the directions of the eigenfunctions and therefore summarize how a function differs from the mean function along orthonormal eigenfunction directions. Formally the FPC of the process and the eigenfunction is

where is the mean process. The part of the score contributing to the variability of the functional data is , which is just a horizontal shift of the actual scores, so centering is not needed when our goal is to decompose the variability of the random processes , which is fortuitous as one cannot ‘center’ object data to obtain an analogue of , as algebraic operations such as subtraction are not feasible in metric spaces.

In the Euclidean case for any function on , whenever , one can obtain a scaled version of the integral of with respect to as follows,

This suggests to define an integral of an -valued function with respect to a real valued function which integrates to 1. For any real valued function with , we define the generalized Fréchet integral of with respect to as

| (7) |

provided that the integral exists as a limit of Riemann sums for all and the minimizer of the integrals over exists and is unique. A special case of the integral in (7) was introduced as Fréchet integral in Petersen and Müller (2016), where an integral for the space of covariance matrices was constructed for .

The Fréchet integrals defined here are far more general. Generalized Fréchet integrals can be interpreted as an extension of weighted Fréchet means (Fréchet, 1948). We omit the additional term “generalized” in the following and note that Fréchet integrals can be interpreted as projections of functional random objects onto functions , by weighing the elements according to the value of , in direct analogy to projections in the linear function space . This feature motivates to employ Fréchet integrals to obtain object FPCs.

For fixed consider the Fréchet integral function

which, if it exists, is the limit of Riemann sums. A sufficient condition for its existence is that is a continuous function of . If the metric is bounded and and are continuous for , the function is a continuous function of and the integral exists for all . Note that for any , is finite by the Cauchy Schwarz inequality whenever the metric space is bounded and the norm of the function is finite.

If the integrals exist as limits of Riemann sums, the question arises under which conditions the minimizers of the Riemann sums converge and whether the limit of the minimizers coincides with the Fréchet integral . Proposition 2 addresses this question. Let be a partition of , where the are the subintervals of the partition and the length of the subinterval is . The mesh size of the partition is given by . We select such that for each , . For each , the Riemann sum corresponding to the partition and is given by

and the Riemann integral is obtained as a limit of Riemann sums as the partition gets finer. Formally, .

We will invoke the following assumptions for the integral function . For ease of notation, we suppress in , writing in the following.

-

(I1)

The integrand function is uniformly equicontinuous in and .

-

(I2)

exists and is unique, and for all .

-

(I3)

There exist constants and such that

whenever .

Define .

proposition 2

-

1.

Under assumption (I1), converges to uniformly in as .

-

2.

Under assumptions (I1) and (I2), .

-

3.

If for a function with as , then under (I3), .

As a continuous function on a compact interval is uniformly continuous, whenever is continuous and is bounded and continuous, (I1) holds since for ,

Assumption (I1) is sufficient to guarantee that the Fréchet integrals are well defined, while Assumption (I3) is a restriction on the curvature of the function near its minimizer, implying convergence rates of the approximations of the Fréchet integrals. A few examples of spaces that satisfy assumptions (I2) and (I3) are as follows.

-

1.

Let be the space of univariate probability distributions on a common support . For any , denote the corresponding random distribution and quantile functions by . The squared 2-Wasserstein metric between distributions and is

For any taking values in , where we view as the quantile function of the distribution at time , writing for the quantile of the distribution at time , define . Since , a simple calculation shows that for any ,

therefore the minimizer exists and is unique by the convexity of the space of univariate quantile functions. By the orthogonal projection theorem the minimizer is uniquely characterized by

for all and therefore it is enough to choose and in (I3).

-

2.

Consider the space of graph Laplacians or graph adjacency matrices of connected, undirected and simple graphs with a fixed number of nodes , equipped with the Frobenius metric . For any ,

For any taking values in , let be the entry of the graph Laplacian or the graph adjacency matrix. Define . Since , it can be easily seen that for any ,

and so the minimizer exists and is unique by the convexity of the space of graph Laplacians (Ginestet et al., 2017) and the space of graph adjacency matrices. Again, by the orthogonal projection theorem, the minimizer is uniquely characterized by

for all and therefore it is enough to choose and in (I3).

-

3.

The same arguments also imply that satisfies assumptions (I2) and (I3) when is the space of correlation matrices of a fixed dimension .

As we have seen, for general metric spaces , under mild assumptions on the boundedness of the metric and continuity of the functions and , the Fréchet integral has nice properties if it exists and is unique. Moreover, when is bounded and ,

and therefore is a continuous function of . This ensures that the Fréchet integral always exists when is compact.

We now define the FPCs corresponding to the bounded continuous eigenfunctions of the metric auto-covariance operator in the object space using Fréchet integrals. For this, we assume that all trajectories have continuous sample paths almost surely and the metric space is bounded, and furthermore that

-

(A1)

-

(A2)

exists and is unique almost surely for all , where .

Then object functional principal components (object FPCs). for and are defined as the Fréchet integrals

| (8) |

which are random objects in . Similar to ordinary FPCA one can choose a number of basis functions aiming to explain a desired percentage of variation in the data utilizing the eigenvalues of the metric auto-covariance operator. If , the object FPCs correspond to a location and scale shifted version of the ordinary FPCs.

3.2 Fréchet Scores

Exploratory data analysis such as checking for clusters or outliers often benefits from plotting the FPCs against each other for the case of real valued functional data. FPCs defined using Fréchet integral live in the object space and therefore visualizing them is non-trivial. One approach is to obtain their projections to a lower-dimensional real space using multi-dimensional scaling or its variants (Kruskal, 1964; Belkin and Niyogi, 2002) and then visualizing the projections. Here we propose another approach for obtaining a scalar version of object FPCs. The resulting scalar FPCs are interpretable and can be plotted against each other and are thus useful for exploratory data analysis.

In the real valued case, one obtains projections of the deviations of the observed random curves from the mean curve onto dominant eigenfunctions. While the concept of a mean function can be generalized to object functional data using Fréchet means (Fréchet, 1948), one cannot ‘center’ object data and does not have directional information. Nevertheless, it is possible to study how distances of sample curves from the mean curve project onto a few dominant eigenfunctions, in analogy to the real valued case. Formally, given a random object process , the population Fréchet mean function is

where we assume existence and uniqueness of the minimizer. For real valued functional data under the Euclidean metric the Fréchet mean function coincides with the usual pointwise mean function. Defining distance functions

for sample trajectories , we represent the scalar functions in the eigenbasis of the metric auto-covariance operator, obtaining the coefficients

| (9) |

We refer to the scalars as the Fréchet scores.

The Fréchet scores can be interpreted as decomposition of the departures of the sample elements from the ‘central’ Fréchet mean curve in predominant directions of variation. They can be plotted against each other and have the potential to provide interesting insights, as we will illustrate in the data applications. Considering the existence of the Fréchet scores, with denoting as before the diameter of the totally bounded metric space , continuity of the Fréchet mean function implies that for any ,

Thus for continuous eigenfunction , the function is a continuous function of almost surely and therefore the Fréchet scores will exist. Proposition 3 shows that under assumption (A3) the Fréchet mean function is indeed continuous.

-

(A3)

For each , the pointwise Fréchet mean exists and is unique, and

for any .

proposition 3

If the random object process has almost surely continuous paths, then is continuous under (A3).

Assumption (A3) is satisfied for the space of univariate probability distributions with the 2-Wasserstein metric and also for the space , where is the space of covariance matrices or alternatively graph Laplacians of fixed dimension with the Frobenius metric (Dubey and Müller, 2017; Petersen and Müller, 2019a).

4 Estimation and Theory

Having defined suitable population targets, our goal now is to construct appropriate estimators, starting with a sample of functional random objects. An empirical estimator of the metric auto-covariance operator as defined in section 2 is given by

| (10) |

where

Observe that for each , is a -statistic and the class is a family of -statistics.

Noting that can be viewed as a stochastic process indexed by the function class , where allows us to apply the theory of -processes (Nolan and Pollard, 1987, 1988; Arcones and Giné, 1993) for weak convergence (Billingsley, 1968; Van der Vaart and Wellner, 1996). For the uniform convergence of , we need an assumption on the rate of continuity of the functional random objects.

-

(A4)

The process is almost surely -Hölder continuous for some , where the Hölder constant has a finite second moment, i.e. for some non negative function one has

where

Theorem 1

Under assumption (A4), the sequence of stochastic processes

converges weakly to a Gaussian process with mean 0 and covariance function

where is an i.i.d copy of .

Writing and for the eigenvalues and eigenfunctions of , uniform convergence and rates of convergence of these estimates of the eigenvalues and eigenfunctions of the metric auto-covariance operator to their targets are obtained as a direct consequence of Proposition 1 under the following assumption on the spacings of the eigenvalues.

-

(A5)

For each the eigenvalue has multiplicity 1, i.e it holds that , where .

Corollary 1

As in classical FDA, the eigenfunctions are uniquely identifiable only up to a sign change. For theoretical considerations such as the convergence in Corollary 1, we may always assume that true and estimated eigenfunctions are aligned in the sense that . Our next objective is to obtain sample estimators for the object FPCs (8) defined in section 3.1. For each , consider the following estimators of ,

A natural estimator for the Fréchet integral is then

| (11) |

To obtain convergence of to its population target, we make the following assumptions.

-

(A6)

For every and , and exist and are unique almost surely. Moreover for any , almost surely.

-

(A7)

There exist constants and such that almost surely,

whenever .

Assumption (A6) on the existence and uniqueness of the Fréchet integrals is used to establish consistency. Assumption (A7) is a restriction on the local behavior of the integrals around the minimizer and determines the rate of convergence.

Theorem 2

Under assumptions (A1), (A2), (A4) and (A6),

If additionally (A7) holds, then

Here we choose to be such that which ensures matching signs for the true and estimated eigenfunctions in the computation of and .

Next we provide estimates of the Fréchet scores and study their asymptotics. The starting point is the following estimator of the population Fréchet mean function,

| (12) |

We need the following assumptions:

-

(A8)

The Fréchet mean function estimate exists and is unique almost surely for all . Additionally, for every , there exists such that

-

(A9)

There exists a sufficiently small and constants and , such that for all -valued functions with , where , the functions are -Hölder continuous with Hölder constant bounded above by , i.e.

-

(A10)

For , it holds that as for all sufficiently small and for any constant . Here is the -ball around and is the covering number, i.e. the minimum number of balls of radius required to cover (Van der Vaart and Wellner, 1996).

-

(A11)

There exist and such that

proposition 4

Under assumptions (A3) and (A8),

Assumptions (A4) and (A9)-(A11) are required to obtain an entropy condition for the space of functional random objects (Lemma 1 below), which is used to establish the rate of convergence of the sample Fréchet mean function. We note that (A9), where we assume that in a sufficiently close neighborhood of the true Fréchet mean function all object functions have a common rate of Hölder continuity and a common Hölder constant, is weaker than assumptions that have been required in classical FDA (see e.g. Müller et al., 2006), where one deals with real-valued random functions. Assumption (A10) is a bound on the covering number of the object metric space and is satisfied by common instances for random objects that include the examples discussed at the end of section 3.2.

We write for -valued functions and define

Here is the minimizer of and is the minimizer of . We refer to and as and in the following. To derive the rate of convergence of , we first obtain a bound for for small , where . For this, we define function classes

| (13) |

It is easy to see that an envelope function for this class is the constant function , where is the diameter of . The -norm of this envelope function is . By Theorem 2.14.2 of Van der Vaart and Wellner (1996) we have

| (14) |

where is the bracketing integral of the function class ,

Here is the minimum number of balls of radius required to cover the function class under the norm. Lemma 1 provides the behavior of the bracketing integral of the function class , a key step for the proof of Theorem 3.

Lemma 1

Under assumptions (A4),(A9) and (A10), it holds for the function class as defined in (13) that as .

Theorem 3

Under assumptions (A3)-(A4) and (A8)-(A11),

Setting , an application is the convergence of the estimated Fréchet scores

| (15) |

Corollary 2

Under assumptions (A3)-(A5) and (A8)-(A11),

Following widely adopted convention, we assume throughout that true and estimated eigenfunctions are aligned in the sense that , as the scores are identifiable only up to a sign change.

5 Simulations

We illustrate the utility of the proposed methods through simulations for two settings: In the first setting, the space consists of univariate probability distributions equipped with the 2-Wasserstein metric and in the second setting, consists of networks with fixed number of nodes, represented as graph adjacency matrices and equipped with the Frobenius metric.

5.1 Time-varying probability distributions

We generated random samples of sizes and of ‘distribution’-valued curves on the domain , where for each , is a normal distribution with mean and variance with

with , , where and are orthonormal on . We use the 2-Wasserstein metric for the distribution space . For these specifications, the metric auto-covariance function is

| (16) |

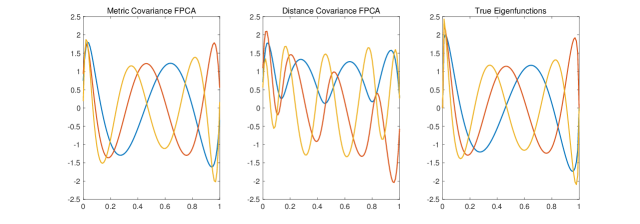

and and are the first 3 eigenfunctions.

We applied the proposed method to estimate the metric auto-covariance operator for the simulated data and obtained its eigenvalues and eigenfunctions. Denoting the estimated metric auto-covariance surface and the estimated -th eigenvalue and eigenfunction obtained at the simulation run by , respectively and , we computed mean integrated squared errors (MISE)

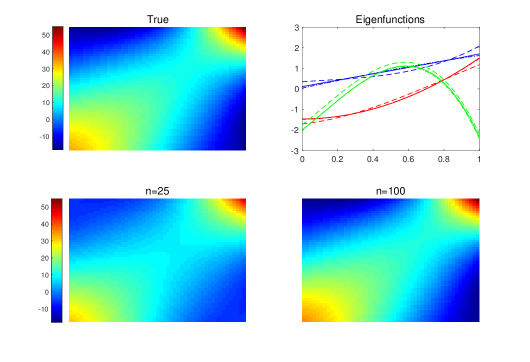

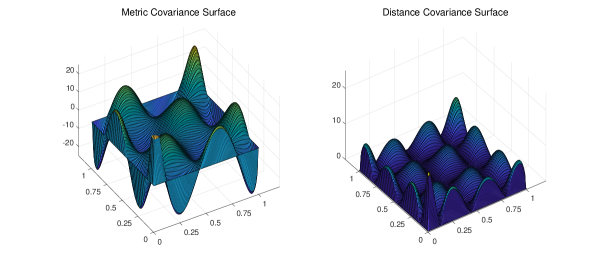

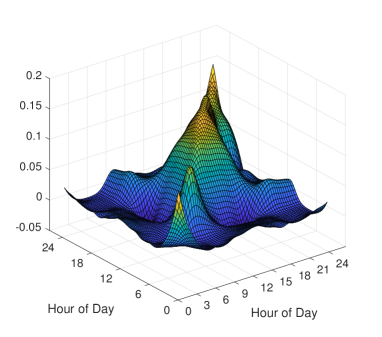

Figure 1 shows the true and estimated metric auto-covariance surfaces and their eigenfunctions for one randomly chosen simulation run for and . We find that the proposed method has negligible bias as sample size increases. The MISEs are reported in Table S6.1 Zones in Manhattan, New York and seen to decrease with increasing sample sizes.

| 25 | 12.2709 | 1.2841 | 1.5351 | 1.5202 | 10.8634 | 7.8471 | 3.5798 |

|---|---|---|---|---|---|---|---|

| 50 | 8.6598 | 0.0504 | 0.0201 | 0.0030 | 0.9748 | 0.6482 | 0.3680 |

| 100 | 4.0697 | 0.0158 | 0.0084 | 0.0047 | 0.1239 | 0.0607 | 0.0314 |

To illustrate the nature of the simulated random density trajectories, four density-valued random functions that are part of a sample of density-valued random functions as generated in one Monte Carlo run are displayed in Figure 2, reflecting variation in means and variances of the Gaussian distributions as a function of time for the four selected subjects. The estimated object FPCs, i.e. the Fréchet integrals of the object curves along the first two eigenfunctions, from one Monte Carlo run are in Figure 19 for sample size 50. Here the first object FPCs reflect variation in location of the distributions and the second object FPCs variation in the variance of the distributions, which is what we expect in view of how these data were generated. The object FPCs are found to be useful for discovering the underlying modes of variation for distributions as functional random objects.

5.2 Time-varying networks

In each iteration, we generated random samples of sizes and of time varying random networks with 10 nodes each in the time interval . For generating the edge weights, we followed the model described below. We assumed that the network has two communities, the first five nodes belonging to one community and the second five nodes to the other one. For each fixed time , the edge weights within each community and also those between the communities are the same, where the latter are smaller than the within community edge weights. Formally, if and denote the edge weight at time for the first community, the second community and between communities, for the network valued curve we generated

| (17) |

Here the , , and were generated from the uniform distributions , , and , respectively. The functions , and are orthonormal polynomials derived from Jacobi polynomials (Totik, 2005), which are classical orthogonal polynomials for . They are orthogonal with respect to the basis on . With a suitable change of basis, one can obtain a version of the Jacobi polynomials on which are orthonormal with respect to the weight function on . We selected , and as

The weighted networks are represented as graph adjacency matrices with the Frobenius metric. Here the true metric auto-covariance function is

| (18) |

and and are the first three eigenfunctions.

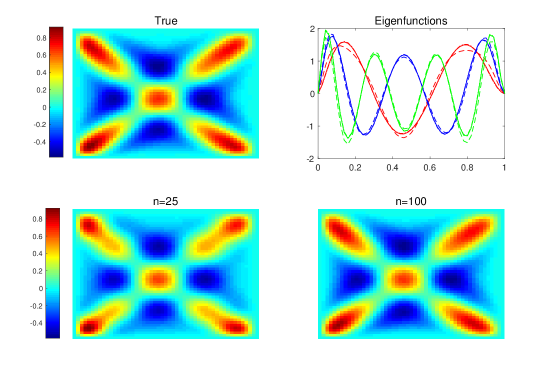

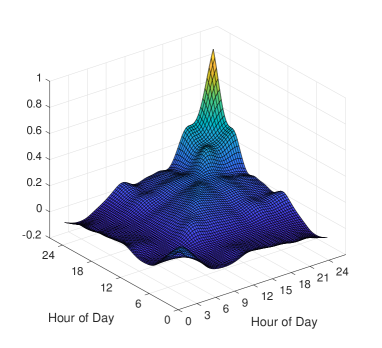

We estimated the metric auto-covariance operator from the simulated data and obtained its eigenfunctions for different sample sizes. Figure 4 displays the true and estimated metric auto-covariance surfaces and corresponding eigenfunctions for one randomly chosen simulation run for and . The MISEs were computed as described for the previous simulation setting and are reported in Table 2. They decrease with increasing sample sizes. The proposed method is seen to work very well.

| 25 | 0.0039 | 0.0039 | 0.0017 | 0.0007 | 0.0025 | 0.0010 | 0.0007 |

|---|---|---|---|---|---|---|---|

| 50 | 0.0017 | 0.0093 | 0.0046 | 0.0021 | 0.0007 | 0.0003 | 0.0001 |

| 100 | 0.0010 | 0.0130 | 0.0063 | 0.0028 | 0.0001 | 0.0001 | 0.0001 |

The object FPCs were obtained using Fréchet integrals (11). For visualization they are presented as a “networks.mov” in the supplementary materials. In the movie the leftmost plot corresponds to Fréchet integrals for the first eigenfunction which, as expected due to the true model, shows variation only in the edge weights of the first community. The middle plot corresponds to Fréchet integrals for the second eigenfunction and indicates variation only in the edge weights of the second community. The rightmost plot corresponds to Fréchet integrals for the third eigenfunction, where variation in both the first and the second community edge weights can be discerned.

6 Data Applications

6.1 Mortality data

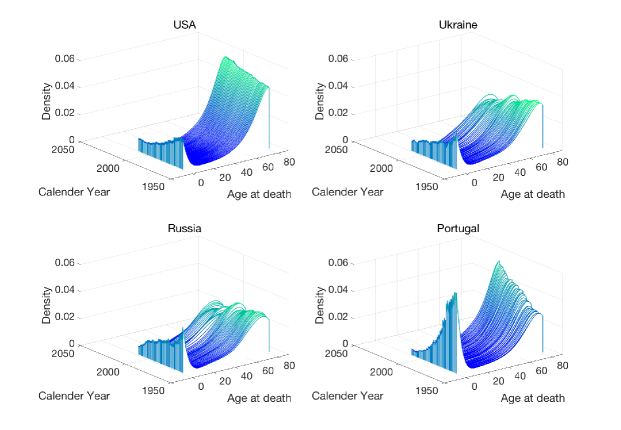

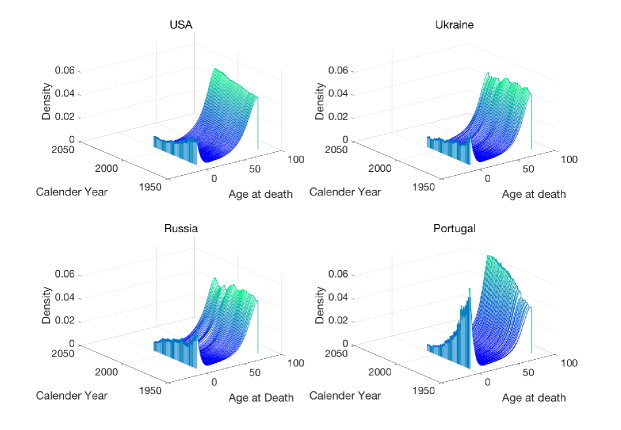

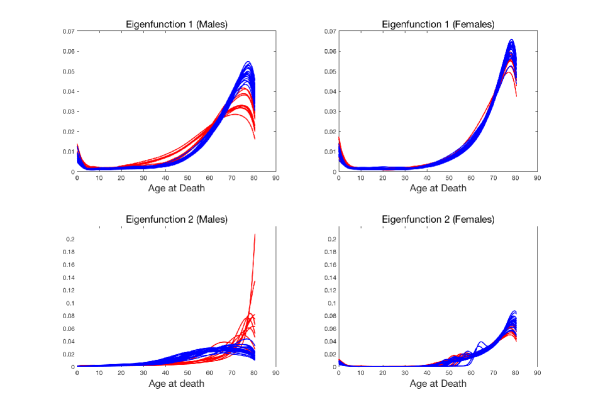

The Human Mortality Database provides life table data differentiated by gender and is available at www.mortality.org. Currently the mortality database contains life table data for 37 countries spanning over 5 decades. One can obtain histograms from life tables and smooth these with local least squares to obtain estimated probability density functions for age at death. We carried this out for the age interval . The mortality data can then be viewed as samples of time varying univariate probability distributions, for a sample of 32 countries, where the time axis corresponds to calendar years between 1960 and 2009 and the observation made at each calendar year for each country corresponds to the age at death distribution for that year. We included the 32 countries which had complete records over the entire calendar period. For each country and year, we used the Hades package available at https://stat.ucdavis.edu/hades/ for smoothing the histograms and used bandwidth to obtain the age-at-death densities. For illustration, the time-varying age at death distributions represented as density functions for the age interval and indexed by calendar year are displayed for four selected countries, USA, Ukraine, Russia and Portugal, for males in Figure 5 and for females in Figure 6.

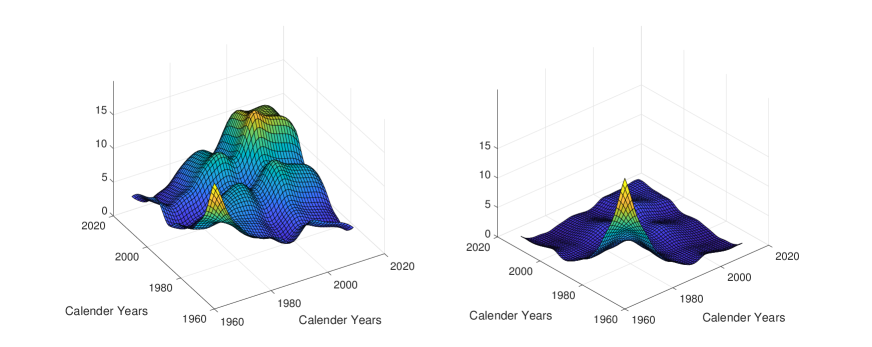

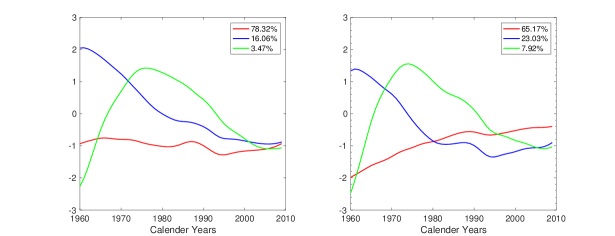

Choosing the 2-Wasserstein metric for the probability distributions space, the estimated metric auto-covariance surfaces for males and females can be inspected in Figure 7 and the eigenfunctions of the corresponding auto-covariance operators in Figure 8. The auto-covariance functions and eigenfunctions indicate that there are systematic differences between males and females.

The resulting object FPCs, i.e. the Fréchet integrals, are illustrated in Figure 9 for the first two eigenfunctions. The object FPCS are distributions that are represented as densities for males and females. The Eastern European countries included in the data base, namely, Belarus, Bulgaria, Czech Republic, Hungary, Latvia, Lithuania, Poland, Slovakia, Ukraine, Russia and Estonia underwent major political upheaval due to the end of Communist rule in these regions during the period between the late 1980s and early 1990. This is reflected in clear distinctions between the Eastern European countries (red) and the rest (blue) in the Fréchet integrals for the males but much less so for the females, which indicates that particularly male mortality was affected by the political upheavals.

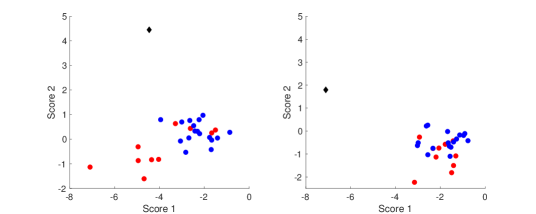

The sample Fréchet mean function at a particular calendar year corresponds to the sample average of the quantile functions of the different countries at that calendar year and is illustrated in the movies “mean_males.mov” and “mean_females.mov” in the supplementary materials. Figure 10 illustrates the scalar FPCs, i.e. the Fréchet scores for the second eigenfunction plotted against the Fréchet scores for the first eigenfunction for males and females. Russia is an outlier for the first eigenfunction for males and Portugal is an outlier for the second eigenfunction, even though it does not belong to the above list of Eastern European countries. One could speculate that this might be related to the fact Portugal in 1974 moved to a democratic government after four decades of authoritarian dictatorship. Figures 5 and 6 suggest higher infant mortality for both males and females in Portugal during the earlier era. Another interesting observation is that the order of outliers is reversed for females, as Russia turns out to be an outlier for females for the second eigenfunction and Portugal for the first. The plots of the Fréchet scores against each other indicate that there are clear distinctions between the two groups of countries and Portugal.

6.2 Time-varying networks for New York taxi data

New York City Taxi and Limousine Commission (NYC TLC) provides records on pick-up and drop-off dates/times, pick-up and drop-off locations, trip distances, itemized fares, rate types, payment types, and driver-reported passenger counts for yellow and green taxis available at http://www.nyc.gov/html/tlc/html/about/trip_record_data.shtml. The time resolution of these data is in the order of seconds. Of interest are networks which represent how many people traveled between places of interest and the evolution of these networks during a typical day. To study this, we constructed samples of time-varying networks where the sample elements are the recordings for each day in the year 2016. Three days (23 and 24 Jan and 13 March) were excluded from the study due to incomplete records.

We focus on the Manhattan area, which has the highest traffic and split the area according to the provided location shape files into 10 zones, which form the regions of interest. Details about the zones are in section S6.1 of the online supplement. Yellow taxis provide the predominant taxi service in Manhattan. We divided each day into 20 minute intervals, and for each interval constructed a network with nodes corresponding to the 10 selected zones and edge weights representing the number of people who traveled between the zones connecting the edges within the 20 minute interval. The edge weights were normalized by the maximum edge weight for each day so that they lie in . We thus have a time-varying network for each of the 363 days in 2016 for which complete records are available, where the time points at which the network-valued functions are evaluated correspond to the 20 minute intervals of a 24 hour day. The observations at each time point correspond to a 10 dimensional graph adjacency matrix which characterizes the network between the 10 zones of Manhattan for the particular 20 minute interval.

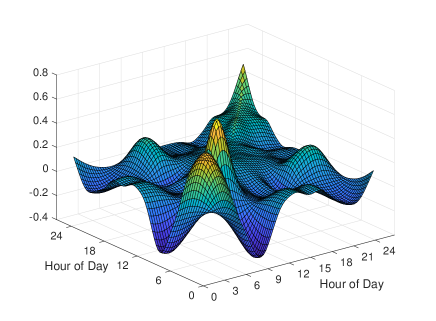

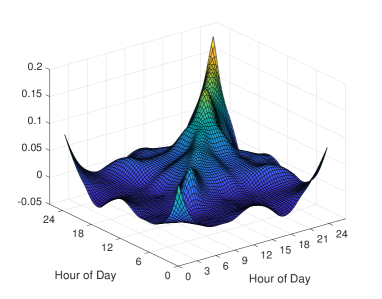

We choose the Frobenius metric as metric between the graph adjacency matrices. The sample Fréchet mean function at a particular time point therefore corresponds to the sample average of the graph adjacency matrices of 363 networks corresponding to different days for that time point. It is illustrated in the movie “mean_NY.mov” in the supplementary materials. Figure 11 illustrates the estimated auto-covariance function and associated eigenfunctions. The plots of the Fréchet scores for second, third and fourth eigenfunction against the scores for the first eigenfunction can be found in Figure 12, where the blue dots correspond to Mondays to Thursdays, the green dots to Fridays and the red dots to Saturdays and Sundays. Several interesting patterns emerge: Weekdays and weekends form clearly distinguishable clusters. Special holidays show similar patterns as weekends. Several outliers can be identified using the projection scores for the eigenfunctions, which turn out to be special days: For the first eigenfunction, the outliers correspond to New Year day and November 6, 2016, which is the day when daylight saving ends. March 13, 2016 is the day on which the daylight saving begins but was excluded as it did not have complete records. For the second eigenfunction, an outlying point is Independence Day, 4 July 2016, and for the third eigenfunction, 14 February 2016 which is Valentine’s day. Another day that stands out is 18 September 2016. On further investigating it was found that between 17 to 19 September 2016 three bombs exploded and several unexploded ones were found in the New York metropolitan area (https://en.wikipedia.org/wiki/2016_New_York_and_New_Jersey_bombings).

We then repeated the analysis separately for three groups of days, namely the weekdays Monday-Thursday (group 1), Fridays and weekends (group 2) and holidays (group 3). We present the results in Figure 17 (Supplement) and in several movies whose descriptions can be found in sections S3 and S5 of the online supplement.

6.3 World trade data

The Center for International Data at University of California, Davis (http://cid.econ.ucdavis.edu/nberus.html) provides detailed documentation of United Nations trade data for the years 1962-2000. The dataset, publicly available at https://cid.econ.ucdavis.edu/nberus.html, contains bilateral trade data during this time period for several commodities and countries. We studied the time period 1970 to 1999 for 46 actively trading countries and the 26 most common types of commodities. The list of chosen countries and commodities can be found in the section S6.2 of the online supplement. For each country, commodity and year, we represent current trade as the ratio of the amount of total trade, i.e. import export value (in thousands of US dollars), to the amount of total trade recorded for the same commodity and country in the year 2000, yielding a 26-dimensional vector of trade ratios.

Viewing the countries as sampling units, we obtain for each country and calendar year a -dimensional raw covariance matrix of commodities trade ratios as , where is the country-specific 26-dimensional vector of commodities trade ratios for year and the mean vector is obtained as cross-sectional average over all 46 countries. These raw time-varying raw covariances were then smoothed using local Fréchet regression with a Gaussian kernel (Petersen and Müller, 2019a; Petersen et al., 2019) to obtain samples of smooth time-varying 26-dimensional covariance matrices between the components of commodities trade for each of the 46 countries over the time period 1970 to 2000, yielding time-varying covariance matrices over the time period 1970 to 2000 as functional random objects.

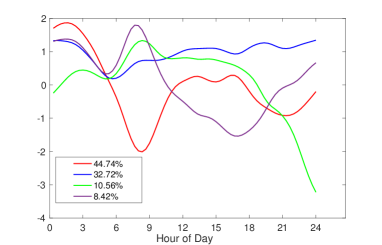

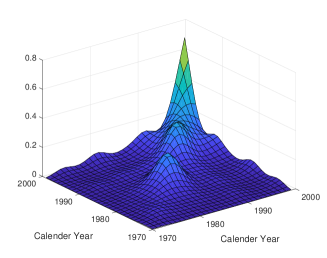

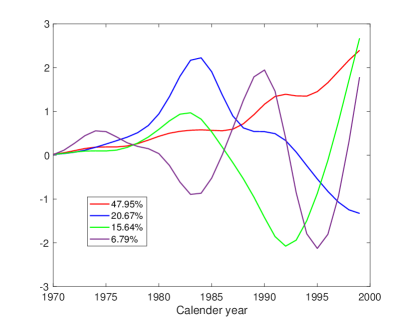

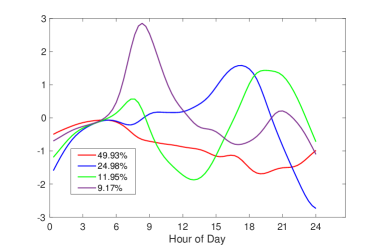

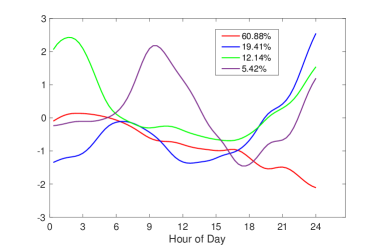

When adopting the Frobenius metric, the sample Fréchet mean function at calendar year corresponds to the sample average of the smoothed covariance across 46 countries for year . Figure 13(a) illustrates the estimated metric auto-covariance function and Figure 13(b) its eigenfunctions. The metric auto-covariance and its eigenfunctions provide insights about world trade patterns over the time period 1970 to 1999. The first eigenfunction represents increased variability due to overall expansion in world trade over the years from 1970 to 1999. The slope of the first eigenfunction is more gradual before 1985 but increases sharply starting 1985, stagnates a little around 1990 and then again picks up. This can be connected to the boom in world trade towards the last decade of the new millennium. The second eigenfunction corresponds to a contrast before 1990 and after 1990. The peak in the second eigenfunction between 1980-1985 could be related to a major economic downturn caused by recession affecting several countries in the dataset during the early 1980s. The recession began in USA in 1981 and continued until 1982 and affected many of the developed Western countries. The third eigenfunction captures effects of the early 1990s recession, which compared to the 1980s recession was much milder.

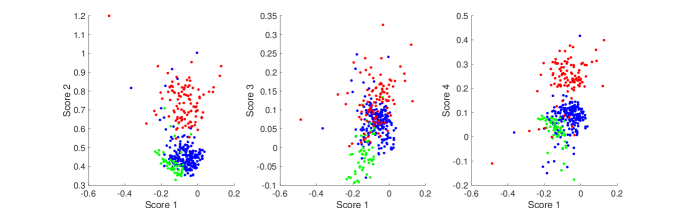

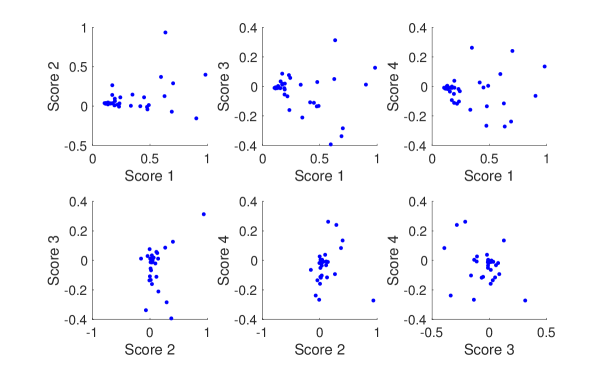

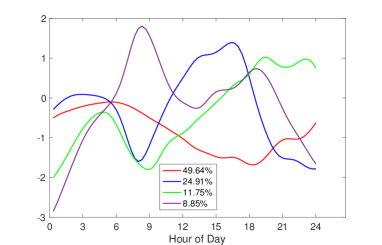

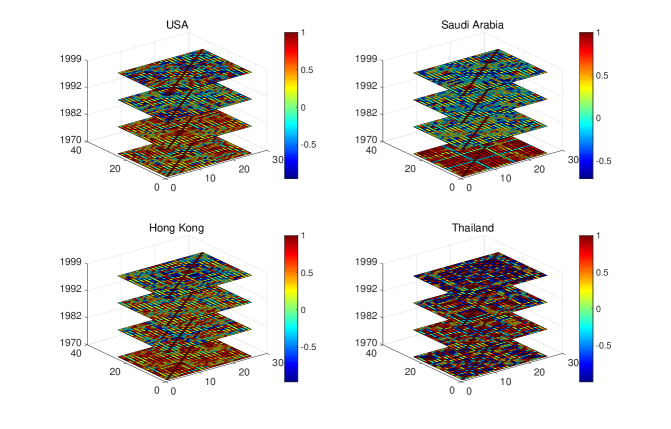

In Figure 14, the Fréchet scores for the first four eigenfunctions are plotted against each other. Thailand and Egypt have high Fréchet scores for the first eigenfunction and Saudi Arabia ranks the highest for the second eigenfunction. Chile, Israel, Hong Kong and Bulgaria turn out to figure prominently in the third eigenfunction. Further visualization can be found in section S4 of the online supplement, including a movie described in section S5 of the online supplement that demonstrates the object FPCs.

7 Discussion

We propose an extension of functional data methods to the case of functional random objects. The basis of our approach is metric covariance, a novel covariance measure for paired metric space valued data. Eigenfunctions of the metric covariance operator for time-varying object data aid in creating a version of object FPCA, where the object FPCs in the metric space are obtained as Fréchet integrals, a general and versatile concept. Alternatively, components of variation can be quantified by Fréchet scores, which are real numbers. For the precursor problem, where one has non-functional time-varying object data, i.e. one has observations for just one random object function over time, methods for metric-space valued regression have been considered previously (Steinke et al., 2010; Faraway, 2014; Petersen and Müller, 2019a), often under the special assumption that the regression responses are on a Riemannian manifold (Shi et al., 2009; Fletcher, 2013; Hinkle et al., 2012; Su et al., 2012; Yuan et al., 2012; Cornea et al., 2017). However the more general object function case, which is characterized by samples of random functions that are object-valued, is considerably more challenging, as the absence of a linear structure in the object space both globally and locally imposes serious limitations on the methods that can be applied.

The tools we propose here for functional random objects, namely metric covariance, the metric auto-covariance operator and its eigenfunctions, the Fréchet integrals and the Fréchet scores make it possible to obtain compact summaries, visualizations and interpretations of the observed samples of time-varying object data that in themselves are highly complex and difficult to quantify. These tools can provide insights into the patterns of variability of the object trajectories, as we demonstrated in the simulations and data examples. The quantification of functional random objects can also be used for other tasks. For example the object FPCs that we introduce reside in the object space and can serve as responses for a regression model, where predictors are Euclidean vectors and responses are random object trajectories, which are summarized by these object FPCs. Implementing such a regression approach is analogous to the principal component approach for function-to-function regression (Yao et al., 2005b). Various regression models can then be implemented through Fréchet regression (Petersen and Müller, 2019a). For the case where functional random objects feature as predictors in a regression setting, one can employ the vector of Fréchet scores that summarize each random object trajectory as predictors. The ensuing regression, classification and clustering models will be interesting topics for future research.

A core challenge that one faces when modeling and analyzing samples of random object trajectories is that in contrast to the situation for real-valued processes, one cannot expect to represent object-valued processes in terms of an analogue to the Karhunen-Loève expansion, due to the lack of a linear structure in the object space . In some special cases such expansions are possible, for example through a transformation method, whenever random objects can be transformed to a linear space, as exemplified for the case of objects that are probability distributions (Petersen and Müller, 2016) or for the case of Riemannian manifold-valued objects (Dai and Müller, 2018). Apart from such special cases, it is an open problem whether more general useful representations of functional random objectscan be found. Another open problem is inference for such data, e.g., comparing two groups or testing for structural features of auto-covariance. Here the metric auto-covariance operator that we introduce in this paper and also the Fréchet mean function could prove useful for the extension of tests that have been considered for real-valued functional data (for some recent examples, see Aston et al., 2017; Constantinou et al., 2017; Chen and Lynch, 2018; Choi and Reimherr, 2018). These and many other open problems in this area indicate that there is ample potential for future research.

Acknowledgements

We wish to thank the reviewers for their comprehensive and helpful comments that led to numerous improvements and new perspectives. This research was supported by NSF grant DMS-1712864 and NIH grant 5UH3OD023313.

References

- Anirudh et al. (2017) Anirudh, R., Turaga, P., Su, J. and Srivastava, A. (2017) Elastic functional coding of Riemannian trajectories. IEEE Transactions on Pattern Analysis and Machine Intelligence, 39, 922–936.

- Arcones and Giné (1993) Arcones, M. A. and Giné, E. (1993) Limit theorems for U-processes. The Annals of Probability, 1494–1542.

- Aston et al. (2017) Aston, J. A., Pigoli, D. and Tavakoli, S. (2017) Tests for separability in nonparametric covariance operators of random surfaces. The Annals of Statistics, 45, 1431–1461.

- Belkin and Niyogi (2002) Belkin, M. and Niyogi, P. (2002) Laplacian eigenmaps and spectral techniques for embedding and clustering. In Advances in Neural Information Processing Systems, 585–591.

- Berrendero et al. (2011) Berrendero, J., Justel, A. and Svarc, M. (2011) Principal components for multivariate functional data. Computational Statistics and Data Analysis, 55, 2619–2634.

- Bigot et al. (2017) Bigot, J., Gouet, R., Klein, T. and López, A. (2017) Geodesic PCA in the Wasserstein space by convex PCA. Annales de l’Institut Henri Poincaré B: Probability and Statistics, 53, 1–26.

- Billingsley (1968) Billingsley, P. (1968) Convergence of Probability Measures. Wiley, New York.

- Bosq (2000) Bosq, D. (2000) Linear Processes in Function Spaces: Theory and Applications. New York: Springer-Verlag.

- Castro et al. (1986) Castro, P. E., Lawton, W. H. and Sylvestre, E. A. (1986) Principal modes of variation for processes with continuous sample curves. Technometrics, 28, 329–337.

- Chen et al. (2017) Chen, K., Delicado, P. and Müller, H.-G. (2017) Modeling function-valued stochastic processes, with applications to fertility dynamics. Journal of the Royal Statistical Society, Series B (Theory and Methodology), 79, 177–196.

- Chen and Lynch (2018) Chen, K. and Lynch, B. (2018) A test of weak separability for multi-way functional data, with application to brain connectivity studies. Biometrika, 105, 815–831.

- Chen and Müller (2012) Chen, K. and Müller, H.-G. (2012) Modeling repeated functional observations. Journal of the American Statistical Association, 107, 1599–1609.

- Chiou et al. (2014) Chiou, J.-M., Chen, Y.-T. and Yang, Y.-F. (2014) Multivariate functional principal component analysis: A normalization approach. Statistica Sinica, 24, 1571–1596.

- Chiou and Li (2007) Chiou, J.-M. and Li, P.-L. (2007) Functional clustering and identifying substructures of longitudinal data. Journal of the Royal Statistical Society: Series B, 69, 679–699.

- Chiou et al. (2016) Chiou, J.-M., Yang, Y.-F. and Chen, Y.-T. (2016) Multivariate functional linear regression and prediction. Journal of Multivariate Analysis, 146, 301–312.

- Choi and Reimherr (2018) Choi, H. and Reimherr, M. (2018) A geometric approach to confidence regions and bands for functional parameters. Journal of the Royal Statistical Society: Series B (Statistical Methodology), 80, 239–260.

- Claeskens et al. (2014) Claeskens, G., Hubert, M., Slaets, L. and Vakili, K. (2014) Multivariate functional half-space depth. Journal of the American Statistical Association, 109, 411–423.

- Constantinou et al. (2017) Constantinou, P., Kokoszka, P. and Reimherr, M. (2017) Testing separability of space-time functional processes. Biometrika, 104, 425–437.

- Cornea et al. (2017) Cornea, E., Zhu, H., Kim, P. and Ibrahim, J. G. (2017) Regression models on Riemannian symmetric spaces. Journal of the Royal Statistical Society: Series B (Statistical Methodology), 79, 463–482.

- Dai and Müller (2018) Dai, X. and Müller, H.-G. (2018) Principal component analysis for functional data on Riemannian manifolds and spheres. Annals of Statistics, 46, 3334–3361.

- Dai et al. (2017) Dai, X., Müller, H.-G. and Yao, F. (2017) Optimal Bayes classifiers for functional data and density ratios. Biometrika, 79, 545–560.

- Dauxois et al. (1982) Dauxois, J., Pousse, A. and Romain, Y. (1982) Asymptotic theory for the principal component analysis of a vector random function: some applications to statistical inference. Journal of Multivariate Analysis, 12, 136–154.

- Dong et al. (2018) Dong, J. J., Wang, L., Gill, J. and Cao, J. (2018) Functional principal component analysis of glomerular filtration rate curves after kidney transplant. Statistical Methods in Medical Research, 27, 3785–3796.

- Dryden et al. (2009) Dryden, I. L., Koloydenko, A. and Zhou, D. (2009) Non-Euclidean statistics for covariance matrices, with applications to diffusion tensor imaging. Annals of Applied Statistics, 3, 1102–1123.

- Dubey and Müller (2017) Dubey, P. and Müller, H.-G. (2017) Fréchet analysis of variance for random objects. arXiv preprint arXiv:1710.02761.

- Dubin and Müller (2005) Dubin, J. A. and Müller, H.-G. (2005) Dynamical correlation for multivariate longitudinal data. Journal of the American Statistical Association, 100, 872–881.

- Faraway (2014) Faraway, J. J. (2014) Regression for non-Euclidean data using distance matrices. Journal of Applied Statistics, 41, 2342–2357.

- Fletcher (2013) Fletcher, P. T. (2013) Geodesic regression and the theory of least squares on Riemannian manifolds. International Journal of Computer Vision, 105, 171–185.

- Fréchet (1948) Fréchet, M. (1948) Les éléments aléatoires de nature quelconque dans un espace distancié. Annales de l’Institut Henri Poincaré, 10, 215–310.

- Ginestet et al. (2017) Ginestet, C. E., Li, J., Balachandran, P., Rosenberg, S. and Kolaczyk, E. D. (2017) Hypothesis testing for network data in functional neuroimaging. The Annals of Applied Statistics, 11, 725–750.

- Hinkle et al. (2012) Hinkle, J., Muralidharan, P., Fletcher, P. T. and Joshi, S. (2012) Polynomial regression on Riemannian manifolds. In Computer Vision–ECCV 2012, 1–14. Springer.

- Horvath and Kokoszka (2012) Horvath, L. and Kokoszka, P. (2012) Inference for Functional Data with Applications. New York: Springer.

- Hsing and Eubank (2015) Hsing, T. and Eubank, R. (2015) Theoretical Foundations of Functional Data Analysis, with an Introduction to Linear Operators. John Wiley & Sons.

- Jacques and Preda (2014) Jacques, J. and Preda, C. (2014) Model-based clustering for multivariate functional data. Computational Statistics and Data Analysis, 71, 92–106.

- Jakobsen (2017) Jakobsen, M. E. (2017) Distance covariance in metric spaces: Non-parametric independence testing in metric spaces. arXiv preprint arXiv:1706.03490.

- Jones and Rice (1992) Jones, M. C. and Rice, J. A. (1992) Displaying the important features of large collections of similar curves. The American Statistician, 46, 140–145.

- Kleffe (1973) Kleffe, J. (1973) Principal components of random variables with values in a separable Hilbert space. Statistics: A Journal of Theoretical and Applied Statistics, 4, 391–406.

- Kruskal (1964) Kruskal, J. (1964) Nonmetric multidimensional scaling: A numerical method. Psychometrika, 29, 115–129.

- Lin et al. (2017) Lin, L., St. Thomas, B., Zhu, H. and Dunson, D. B. (2017) Extrinsic local regression on manifold-valued data. Journal of the American Statistical Association, 112, 1261–1273.

- Liu et al. (2016) Liu, S., Zhou, Y., Palumbo, R. and Wang, J.-L. (2016) Dynamical correlation: A new method for quantifying synchrony with multivariate intensive longitudinal data. Psychological Methods, 21, 291–308.

- Lyons (2013) Lyons, R. (2013) Distance covariance in metric spaces. Annals of Probability, 41, 3284–3305.

- Monnig and Meyer (2018) Monnig, N. D. and Meyer, F. G. (2018) The resistance perturbation distance: A metric for the analysis of dynamic networks. Discrete Applied Mathematics, 236, 347–386.

- Müller et al. (2006) Müller, H.-G., Stadtmüller, U. and Yao, F. (2006) Functional variance processes. Journal of the American Statistical Association, 101, 1007–1018.

- Nolan and Pollard (1987) Nolan, D. and Pollard, D. (1987) U-processes: rates of convergence. The Annals of Statistics, 780–799.

- Nolan and Pollard (1988) — (1988) Functional limit theorems for U-processes. The Annals of Probability, 1291–1298.

- Opgen-Rhein and Strimmer (2006) Opgen-Rhein, R. and Strimmer, K. (2006) Inferring gene dependency networks from genomic longitudinal data: A functional data approach. REVSTAT - Statistical Journal, 4, 53–65.

- Park and Staicu (2015) Park, S. Y. and Staicu, A.-M. (2015) Longitudinal functional data analysis. Stat, 4, 212–226.

- Petersen et al. (2019) Petersen, A., Deoni, S. and Müller, H.-G. (2019) Fréchet estimation of time-varying covariance matrices from sparse data, with application to the regional co-evolution of myelination in the developing brain. arXiv preprint arXiv:1806.09690 Annals of Applied Statistics, in press.

- Petersen and Müller (2016) Petersen, A. and Müller, H.-G. (2016) Fréchet integration and adaptive metric selection for interpretable covariances of multivariate functional data. Biometrika, 103, 103–120.

- Petersen and Müller (2016) Petersen, A. and Müller, H.-G. (2016) Functional data analysis for density functions by transformation to a Hilbert space. Annals of Statistics, 44, 183–218.

- Petersen and Müller (2019a) — (2019a) Fréchet regression for random objects with Euclidean predictors. Annals of Statistics, 47, 691–719.

- Petersen and Müller (2019b) — (2019b) Wasserstein covariance for multiple random densities. arXiv:1812.07694 Biometrika, in press.

- Pigoli et al. (2014) Pigoli, D., Aston, J. A., Dryden, I. L. and Secchi, P. (2014) Distances and inference for covariance operators. Biometrika, 101, 409–422.

- Ramsay and Silverman (2005) Ramsay, J. O. and Silverman, B. W. (2005) Functional Data Analysis. Springer Series in Statistics. New York: Springer, second edn.

- Robert and Escoufier (1976) Robert, P. and Escoufier, Y. (1976) A unifying tool for linear multivariate statistical methods: the RV-coefficient. Journal of the Royal Statistical Society: Series C (Applied Statistics), 25, 257–265.

- Schoenberg (1938) Schoenberg, I. J. (1938) Metric spaces and positive definite functions. Transactions of the American Mathematical Society, 44, 522–536.

- Seguy and Cuturi (2015) Seguy, V. and Cuturi, M. (2015) Principal geodesic analysis for probability measures under the optimal transport metric. In Advances in Neural Information Processing Systems, 3312–3320.

- Sejdinovic et al. (2013) Sejdinovic, D., Sriperumbudur, B., Gretton, A. and Fukumizu, K. (2013) Equivalence of distance-based and RKHS-based statistics in hypothesis testing. Annals of Statistics, 41, 2263–2291.

- Shi et al. (2009) Shi, X., Styner, M., Lieberman, J., Ibrahim, J. G., Lin, W. and Zhu, H. (2009) Intrinsic regression models for manifold-valued data. In Medical Image Computing and Computer-Assisted Intervention–MICCAI 2009, 192–199. Springer.

- Steinke et al. (2010) Steinke, F., Hein, M. and Schölkopf, B. (2010) Nonparametric regression between general Riemannian manifolds. SIAM Journal on Imaging Sciences, 3, 527–563.

- Su et al. (2012) Su, J., Dryden, I. L., Klassen, E., Le, H. and Srivastava, A. (2012) Fitting smoothing splines to time-indexed, noisy points on nonlinear manifolds. Image and Vision Computing, 30, 428–442.

- Suarez and Ghosal (2016) Suarez, A. J. and Ghosal, S. (2016) Bayesian clustering of functional data using local features. Bayesian Analysis, 11, 71–98.

- Székely and Rizzo (2017) Székely, G. J. and Rizzo, M. L. (2017) The energy of data. Annual Review of Statistics and Its Application, 4, 447–479.

- Székely et al. (2007) Székely, G. J., Rizzo, M. L. and Bakirov, N. K. (2007) Measuring and testing dependence by correlation of distances. Annals of Statistics, 35, 2769–2794.

- Tavakoli et al. (2016) Tavakoli, S., Pigoli, D., Aston, J. A. and Coleman, J. (2016) A spatial modeling approach for linguistic object data: Analysing dialect sound variations across Great Britain. arXiv preprint arXiv:1610.10040.

- Totik (2005) Totik, V. (2005) Orthogonal polynomials. Surveys in Approximation Theory, 1, 70–125.

- Van der Vaart and Wellner (1996) Van der Vaart, A. and Wellner, J. (1996) Weak Convergence and Empirical Processes. Springer, New York.

- Verbeke et al. (2014) Verbeke, G., Fieuws, S., Molenberghs, G. and Davidian, M. (2014) The analysis of multivariate longitudinal data: A review. Statistical Methods in Medical Research, 23, 42–59.

- Wang et al. (2016) Wang, J.-L., Chiou, J.-M. and Müller, H.-G. (2016) Functional data analysis. Annual Review of Statistics and its Application, 3, 257–295.

- Yao et al. (2005a) Yao, F., Müller, H.-G. and Wang, J.-L. (2005a) Functional data analysis for sparse longitudinal data. Journal of the American Statistical Association, 100, 577–590.

- Yao et al. (2005b) — (2005b) Functional linear regression analysis for longitudinal data. Annals of Statistics, 33, 2873–2903.

- Yuan et al. (2012) Yuan, Y., Zhu, H., Lin, W. and Marron, J. (2012) Local polynomial regression for symmetric positive definite matrices. Journal of the Royal Statistical Society: Series B (Statistical Methodology), 74, 697–719.

- Zhou et al. (2008) Zhou, L., Huang, J. and Carroll, R. (2008) Joint modelling of paired sparse functional data using principal components. Biometrika, 95, 601–619.

Online Supplement

S1. Proofs

Proof of Proposition 1

It is clear that is a symmetric function. To prove that it is nonnegative definite we need to show that for any positive integer ,

for any in and in . Since is a semimetric of negative type, by Proposition 3 in Sejdinovic et al. (2013) there exists a Hilbert space and an injective map such that . We therefore have that for ,

which implies that for i.i.d copies and

Let and for where is an i.i.d copy of . Then

which leads to

The last step follows from the Cauchy-Schwarz inequality. This completes the proof.

Proof of Proposition 2

-

1.

For any , by (I1) there exists such that, whenever ,

For any partition as described above such that we find

which completes the proof for part (a).

-

2.

Observe that

and therefore by part (a), as .

Now assume that . Then there must exist a sequence of partitions and a such that but . For this sequence of partitions we observe that,

and therefore by (I2), which is a contradiction to part (a). Therefore the assumption that

cannot be true, which completes the proof for part(b). -

3.

Let be such that whenever , it holds that . Assume that . Then there exists a sequence of partitions and a such that , while . For this sequence of partitions we observe that

by (I3). Therefore , which results in a contradiction and completes the proof for part (c).

Proof of Lemma 3

Consider and a sequence such that . We aim to show that .

Observe that almost surely continuous sample curves on the compact interval are uniformly continuous and since is bounded, by bounded convergence, for all and sequences such that , there exists a for every such that whenever , it holds that for all but finitely many . For processes ,