Estimating the Algorithmic Variance of Randomized Ensembles via the Bootstrap

Abstract

Although the methods of bagging and random forests are some of the most widely used prediction methods, relatively little is known about their algorithmic convergence. In particular, there are not many theoretical guarantees for deciding when an ensemble is “large enough” — so that its accuracy is close to that of an ideal infinite ensemble. Due to the fact that bagging and random forests are randomized algorithms, the choice of ensemble size is closely related to the notion of “algorithmic variance” (i.e. the variance of prediction error due only to the training algorithm). In the present work, we propose a bootstrap method to estimate this variance for bagging, random forests, and related methods in the context of classification. To be specific, suppose the training dataset is fixed, and let the random variable denote the prediction error of a randomized ensemble of size . Working under a “first-order model” for randomized ensembles, we prove that the centered law of can be consistently approximated via the proposed method as . Meanwhile, the computational cost of the method is quite modest, by virtue of an extrapolation technique. As a consequence, the method offers a practical guideline for deciding when the algorithmic fluctuations of are negligible.

keywords:

[class=MSC]keywords:

t1This research was partially supported by NSF grant DMS 1613218.

1 Introduction

Random forests and bagging are some of the most widely used prediction methods (Breiman, 1996, 2001), and over the course of the past fifteen years, much progress has been made in analyzing their statistical performance (Bühlmann and Yu, 2002; Hall and Samworth, 2005; Biau, Devroye and Lugosi, 2008; Biau, 2012; Scornet, Biau and Vert, 2015). However, from a computational perspective, relatively little is understood about the algorithmic convergence of these methods, and in practice, ad hoc criteria are generally used to assess this convergence.

To clarify the idea of algorithmic convergence, recall that when bagging and random forests are used for classification, a large collection of randomized classifiers is trained, and then new predictions are made by taking the plurality vote of the classifiers. If such a method is run several times on the same training data , the prediction error of the ensemble will vary with each run, due to the randomized training algorithm. As the ensemble size increases with held fixed, the random variable typically decreases and eventually stabilizes at a limiting value . In this way, an ensemble reaches algorithmic convergence when its prediction error nearly matches that of an infinite ensemble trained on the same data.

Meanwhile, with regard to computational cost, larger ensembles are more expensive to train, to store in memory, and to evaluate on unlabeled points. For this reason, it is desirable to have a quantitative guarantee that an ensemble of a given size will perform nearly as well as an infinite one. This type of guarantee also prevents wasted computation, and assures the user that extra classifiers are unlikely to yield much improvement in accuracy.

1.1 Contributions and related work

To measure algorithmic convergence, we propose a new bootstrap method for approximating the distribution as . Such an approximation allows the user to decide when the algorithmic fluctuations of around are negligible. If particular, if we refer to the algorithmic variance

as the variance of due only the training algorithm, then the parameter is a concrete measure of convergence that can be estimated via the bootstrap. In addition, the computational cost of the method turns out to be quite modest, by virtue of an extrapolation technique, as described in Section 4.

Although the bootstrap is an established approach to distributional approximation and variance estimation, our work applies the bootstrap in a relatively novel way. Namely, the method is based on “bootstrapping an algorithm”, rather than “bootstrapping data” — and in essence, we are applying an inferential method in order to serve a computational purpose. The opportunities for applying this perspective to other randomized algorithms can also be seen in the papers Byrd et al. (2012); Lopes, Wang and Mahoney (2017, 2018), which deal with stochastic gradient methods, as well as randomized versions of matrix multiplication and least-squares.

Bootstrap consistency

From a theoretical standpoint, our main result (Theorem 3.1) shows that the proposed method consistently approximates the distribution as under a “first-order model” for randomized ensembles. The proof also offers a couple of theoretical contributions related to Hadamard differentiability and the functional delta method (van der Vaart and Wellner, 1996, Chapter 3.9). The first ingredient is a lifting operator , which transforms a univariate empirical c.d.f. into a multivariate analogue , where is a simplex. In addition to having interesting properties in its own right, the lifting operator will allow us to represent as a functional of an empirical process. The second ingredient is the calculation of this functional’s Hadamard derivative, which leads to a surprising connection with the classical first variation formula for smooth manifolds (Simon, 1983; White, 2016).111Further examples of problems where geometric analysis plays a role in understanding the performance of numerical algorithms may be found in the book Bürgisser and Cucker (2013).

To briefly comment on the role of this formula in our analysis, consider the following informal statement of it. Let be a smooth -dimensional manifold contained in , and let be a one-parameter family of diffeomorphisms , satisfying as , where denotes the identity map on . Then,

| (1.1) |

where is a volume measure, the symbol denotes the divergence of the vector field , and the symbol is a volume element on . In our analysis, it is necessary to adapt this result to a situation where the maps are non-smooth, the manifold is a non-smooth subset of Euclidean space, and the vector field is a non-smooth Gaussian process. Furthermore, applying a version of Stokes’ theorem to the right side of equation (1.1) leads to a particular linear functional of , which turns out to be the Hadamard derivative relevant to understanding . A more detailed explanation of this connection is given below equation (B.1) in Appendix B.

Related work

In the setting of binary classification, a few papers analyze the bias , and show that it converges at the fast rate of under various conditions (Ng and Jordan, 2001; Lopes, 2016; Cannings and Samworth, 2017). A couple of other works study alternative measures of convergence. For instance, the paper Lam and Suen (1997) considers the probability that the majority vote commits an error at a fixed test point, and the paper Hernández-Lobato, Martínez-Muñoz and Suárez (2013) provides an informal analysis of the probability that an ensemble of size disagrees with an infinite ensemble at a random test point, but these approaches do not directly control . In addition, some empirical studies of algorithmic convergence may be found in the papers Oshiro, Perez and Baranauskas (2012); Latinne, Debeir and Decaestecker (2001).

Among the references just mentioned, the ones that are most closely related to the current paper are Lopes (2016) and Cannings and Samworth (2017). These works derive theoretical upper bounds on or , where is the error rate on a particular class (cf. Section 4). The paper Lopes (2016) also proposes a method to estimate the unknown parameters in such bounds. In relation to these works, the current paper differs in two significant ways. First, we offer an approximation to the full distribution , and hence provide a direct estimate of algorithmic variance, rather than a bound. Second, the method proposed here is relevant to a wider range of problems, since it can handle any number of classes, whereas the analyses in Lopes (2016) and Cannings and Samworth (2017) are specialized to the binary setting. Moreover, the theoretical analysis of the bootstrap approach is entirely different from the previous techniques used in deriving variance bounds.

1.2 Background and setup

We consider the general setting of a classification problem with classes. The set of training data is denoted , which is contained in a sample space . The feature space is arbitrary, and the space of labels has cardinality . An ensemble of classifiers is denoted by , with .

Randomized ensembles

The key issue in studying the algorithmic convergence of bagging and random forests is randomization. In the method of bagging, randomization is introduced by generating random sets , each of size , via sampling with replacement from . For each , a classifier is trained on , with the same classification method being used each time. When each is trained with a decision tree method (such as CART (Breiman et al., 1984)), the random forests procedure extends bagging by adding a randomized feature selection rule (Breiman, 2001).

It is helpful to note that the classifiers in bagging and random forests can be represented in a common way. Namely, there is a deterministic function, say , such that for any fixed , each classifier can be written as

| (1.2) |

where , is an i.i.d. sequence of random objects, independent of , that specify the “randomizing parameters” of the classifiers (cf. Breiman (2001, Definition 1.1)). For instance, in the case of bagging, the object specifies the randomly chosen points in .

Beyond bagging and random forests, our proposed method will be generally applicable to ensembles that can be represented in the form (1.2), such as those in Ho (1998); Dietterich (2000); Bühlmann and Yu (2002). This representation should be viewed abstractly, and it is not necessary for the function or the objects to be explicitly constructed in practice. Some further examples include a recent ensemble method based on random projections (Cannings and Samworth, 2017), as well as the voting Gibbs classifier (Ng and Jordan, 2001), which is a Bayesian ensemble method based on posterior sampling. More generally, if the functions are i.i.d. conditionally on , then the ensemble can be represented in the form (1.2), as long as the classifiers lie in a standard Borel space (Kallenberg, 2006, Lemma 3.22). Lastly, it is important to note that the representation (1.2) generally does not hold for classifiers generated by boosting methods (Schapire and Freund, 2012), for which the analysis of algorithmic convergence is quite different.

Plurality vote

For any , we define the ensemble’s plurality vote as the label receiving the largest number of votes among . In the exceptional case of a tie, it will simplify technical matters to define the plurality vote as a symbol not contained in , so that a tie always counts as an error. We also use the labeling scheme, , where , and is the th standard basis vector for . One benefit of this scheme is that the plurality vote is determined by the average of the labels, . For this reason, we denote the plurality vote as .

Error rate

Let denote the distribution of a test point in , drawn independently of and . Then, for a particular realization of the classifiers , trained with the given set , the prediction error rate is defined as

| (1.3) |

where . (Class-wise error rates , with will also be addressed in Section 4.1.) Here, it is crucial to note that is a random variable, since is a random function. Indeed, the integral above shows that is a functional of . Moreover, there are two sources of randomness to consider: the algorithmic randomness arising from , and the randomness arising from the training set . Going forward, we will focus on the algorithmic fluctuations of due to , and our analysis will always be conditional on .

Algorithmic variance

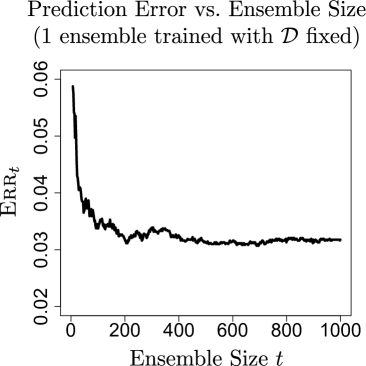

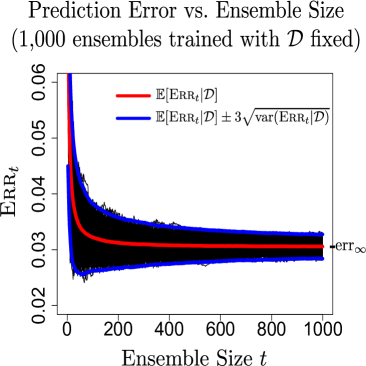

At first sight, it might not be obvious how to interpret the algorithmic fluctuations of when is held fixed. These fluctuations are illustrated below in Figure 1. The left panel shows how changes as decision trees are added incrementally during a single run of the random forests algorithm. For the purposes of illustration, if we run the algorithm repeatedly on to train many ensembles, we obtain a large number of sample paths of as a function of , shown in the right panel. Averaging the sample paths at each value of produces the red curve, representing with averaged out. Furthermore, the blue envelope curves for the sample paths are obtained by plotting as a function of .

Problem formulation

Recall that the value represents the ideal prediction error of an infinite ensemble trained on . Hence, a natural way of defining algorithmic convergence is to say that it occurs when is large enough so that the condition holds with high probability, conditionally on , for some user-specified tolerance . However, the immediate problem we face is that it is not obvious how to check such a condition in practice.

From the right panel of Figure 1, we see that for most , the inequality is highly likely to hold — and this observation can be formalized using Theorem 3.1 later on. For this reason, we propose to estimate as a route to measuring algorithmic convergence. It is also important to note that estimating the quantiles of would serve the same purpose, but for the sake of simplicity, we will focus on . In particular, there are at least two ways that an estimate can be used in practice:

-

1.

Checking convergence for a given ensemble. If an ensemble of a given size has been trained, then convergence can be checked by asking whether or not the observable condition holds. Additional comments on possible choices for will be given shortly.

-

2.

Selecting dynamically. In order to make the training process as computationally efficient as possible, it is desirable to select the smallest needed so that is likely to hold. It turns out that this can be accomplished using an extrapolation technique, due to the fact that tends to scale like (cf. Theorem 3.1). More specifically, if the user trains a small initial ensemble of size and computes an estimate , then “future” values of for can be estimated at no additional cost with the re-scaled estimate . In other words, it is possible to look ahead and predict how many additional classifiers are needed to achieve . Additional details are given in Section 4.2.

Sources of difficulty in estimating

Having described the basic formulation of the problem, it is important to identify what challenges are involved in estimating . First, we must keep in mind that the parameter describes how fluctuates over repeated ensembles generated from — and so it is not obvious that it is possible to estimate from the output of a single ensemble. Second, the computational cost to estimate should not outweigh the cost of training the ensemble, and consequently, the proposed method should be computationally efficient. These two obstacles will be described in Sections 3.2 and 4.2 respectively.

Remarks on the choice of error rate

Instead of analyzing the random variable , a natural inclination would be to consider the “unconditional” error rate , which is likely more familiar, and reflects averaging over both and the randomized algorithm. Nevertheless, there are a few reasons why the “conditional” error may be more suitable for analyzing algorithmic convergence. First, the notion of algorithmic convergence typically describes how much computation should be applied to a given input — and in our context, the given input for the training algorithm is . Second, from an operational standpoint, once a user has trained an ensemble on a given dataset, their actual probability of misclassifying a future test point is , rather than .

There is also a sense in which the convergence of may be misleading. Existing theoretical results suggest that converges at the fast rate of , and in the binary case, , it can be shown that , for some number , under certain conditions (Lopes, 2016; Cannings and Samworth, 2017). However, in Theorem 1 of Section 3, we show that conditionally on , the difference has fluctuations of order . In this sense, if the choice of is guided only by (rather than the fluctuations of ), then the user may be misled into thinking that algorithmic convergence occurs much faster than it really does — and this distinction is apparent from the red and blue curves in Figure 1.

Outline

Our proposed bootstrap method is described in Section 2, and our main consistency result is given in Section 3. Practical considerations are discussed in Section 4, numerical experiments are given in Section 5, and conclusions are stated in Section 6. The essential ideas of the proofs are explained in Appendices A and B, while the technical arguments are given Appendices C-E. Lastly, in Appendix F, we provide additional assessment of technical assumptions. All appendices are in the supplementary material.

2 Method

Based on the definition of in equation (1.3), we may view as a functional of , denoted

From a statistical standpoint, the importance of this expression is that is a functional of a sample mean, which makes it plausible that is amenable to bootstrapping, provided that is sufficiently smooth.

To describe the bootstrap method, let denote a random sample with replacement from the trained ensemble , and put In turn, it would be natural to regard the quantity

| (2.1) |

as a bootstrap sample of , but strictly speaking, this is an “idealized” bootstrap sample, because the functional depends on the unknown test point distribution . Likewise, in Section 2.1 below, we explain how each value can be estimated. So, in other words, if denotes an estimate of , then an estimate of would be written as

and the corresponding bootstrap sample is

Altogether, a basic version of the proposed bootstrap algorithm is summarized as follows.

Algorithm 1 (Bootstrap estimation of )

For

-

•

Sample classifiers with replacement from .

-

•

Compute .

Return: the sample standard deviation of , denoted .

Remark

While the above algorithm is conceptually simple, it suppresses most of the implementation details, and these are explained below. Also note that in order to approximate quantiles of , rather than , it is only necessary to modify the last step, by returning the desired quantile of the centered values , with .

2.1 Resampling algorithm with hold-out or “out-of-bag” points

Here, we consider a version of Algorithm 1 where is estimated implicitly with hold-out points, and then later on, we will explain how hold-out points can be avoided using “out-of-bag” (oob) points. To begin, suppose we have a hold-out set of size , denoted . Next, consider an array of size , whose th row is given by the predicted labels of on the hold-out points. That is,

| (2.2) |

and

| (2.6) |

The estimated error rate is easily computed as a function of this array, i.e. . To spell out the details, let ) denote the th column of , and with a slight abuse of our earlier notation, let denote the plurality vote of the labels in . Then, the estimated error rate is obtained from simple column-wise operations on ,

| (2.7) |

In other words, is just the proportion of columns of for which plurality vote is incorrect. (Note that equation (2.7) is where is implicitly estimated.) Finally, since there is a one-to-one correspondence between the rows and the classifiers , the proposed method is equivalent to resampling the rows , as given below.

Algorithm 2 (Bootstrap estimation of with hold-out points)

For

-

•

Draw a array whose rows are sampled with replacement from .

-

•

Compute .

Return: the sample standard deviation of , denoted .

Extension to OOB points

Since the use of a hold-out set is often undesirable in practice, we instead consider oob points — which are a special feature of bagging and random forests. To briefly review this notion, recall that each classifier is trained on a set of points obtained by sampling with replacement from . Consequently, each set excludes approximately 37% of the points in , and these excluded points may be used as test points for the particular classifier . If a point is excluded from , then we say “the point is oob for the classifer ”, and we write , where the set indexes the classifiers for which is oob.

In this notation, the error estimate in Algorithm 2 can be given an analogous definition in terms of oob points. Define a new array whose th row is given by

Next, letting be the th column of , define to be the plurality vote of the set of labels . (If this set of labels is empty, then we treat this case as a tie, but this is unimportant, since it occurs with probability .) So, by analogy with , we define

| (2.8) |

Hence, the oob version of Algorithm 2 may be implemented by simply interchanging and , as well as and . The essential point to notice is that the sum in equation (2.8) is now over the training points in , rather than over the hold-out set , as in equation (2.7).

3 Main result

Our main theoretical goal is to prove that the bootstrap yields a consistent approximation of as becomes large. Toward this goal, we will rely on two simplifications that are customary in analyses of bootstrap and ensemble methods. First, we will exclude the Monte-Carlo error arising from the finite number of bootstrap replicates, as well as the error arising from the estimation of . For this reason, our results do not formally require the training or hold-out points to be i.i.d. copies of the test point — but from a practical standpoint, it is natural to expect that this type of condition should hold in order for Algorithm 2 (or its oob version) to work well.

Second, we will analyze a simplified type of ensemble, which we will refer to as a first-order model. This type of approach has been useful in gaining theoretical insights into the behavior of complex ensemble methods in a variety of previous works Biau, Devroye and Lugosi (2008); Biau (2012); Arlot and Genuer (2014); Lin and Jeon (2006); Genuer (2012); Scornet (2016a, b). In our context, the value of this simplification is that it neatly packages the complexity of the base classifiers, and clarifies the relationship between and quality of the bootstrap approximation. Also, even with such simplifications, the theoretical problem of proving bootstrap consistency still leads to considerable technical challenges. Lastly, it is important to clarify that the first-order model is introduced only for theoretical analysis, and our proposed method does not rely on this model.

3.1 A first-order model for randomized ensembles

Any randomized classifier may be viewed as a stochastic process indexed by . From this viewpoint, we say that another randomized classifier is a first-order model for if it has the same marginal distributions as , conditionally on , which means

| (3.1) |

Since takes values in the finite set of binary vectors , the condition (3.1) is equivalent to

| (3.2) |

where the expectation is only over the algorithmic randomness in and . A notable consequence of this matching condition is that the ensembles associated with and have the same error rates on average. Indeed, if we let be the error rate associated with an ensemble of independent copies of , then it turns out that

| (3.3) |

for all , where is the error rate for , as before. (A short proof is given in Appendix E.) In this sense, a first-order model is a meaningful proxy for with regard to statistical performance — even though the internal mechanisms of may be simpler.

3.1.1 Constructing a first-order model

Having stated some basic properties that are satisfied by any first-order model, we now construct a particular version that is amenable to analysis. Interestingly, it is possible to start with an arbitrary random classifier , and construct an associated in a relatively explicit way.

To do this, let be fixed, and consider the function

| (3.4) |

which takes values in the “full-dimensional” simplex , defined by

For any fixed , there is an associated partition of the unit interval into sub-intervals

such that the width of interval is equal to for . Namely, we put , and for ,

Lastly, for , we put

Now, if we let be fixed, and let Uniform, then we define to have its th coordinate equal to the following indicator variable

where . It is simple to check that the first-order matching condition (3.2) holds, and so is indeed a first-order model of . Furthermore, given that is defined in terms of a single random variable Uniform, we obtain a corresponding “first-order ensemble” via an i.i.d. sample of uniform variables , which are independent of . (The th coordinate of the th classifier is given by .) Hence, with regard to the representation in equation (1.2), we may make the identification

when the first-order model holds with .

Remark

To mention a couple of clarifications, the variables are only used for the construction of a first-order model, and they play no role in the proposed method. Also, even though the “randomizing parameters” are independent of , the classifiers still depend on through the function .

Interpretation of first-order model

To understand the statistical meaning of the first-order model, it is instructive to consider the simplest case of binary classification, . In this case, is a Bernoulli random variable, where . Since almost surely as (conditionally on ), the majority vote of an infinite ensemble has a similar form, i.e. . Hence, the classifiers can be viewed as “random perturbations” of the asymptotic majority vote arising from . Furthermore, if we view the number as score to be compared with a threshold, then the variable plays the role of a random threshold whose expected value is . Lastly, even though the formula might seem to yield a simplistic classifier, the complexity of is actually wrapped up in the function . Indeed, the matching condition (3.2) allows for the function to be arbitrary.

3.2 Bootstrap consistency

We now state our main result, which asserts that the bootstrap “works” under the first-order model. To give meaning to bootstrap consistency, we first review the notion of conditional weak convergence.

Conditional weak convergence

Let be a probability distribution on , and let be a sequence of probability distributions on that depend on the randomizing parameters . Also, let be the bounded Lipschitz metric for distributions on (van der Vaart and Wellner, 1996, Sec 1.12), and let be the joint distribution of . Then, as , we say that in -probability if the sequence converges to 0 in -probability.

Remark

If a test point is drawn from class , then we denote the distribution of the random vector , conditionally on , as

which is a distribution on the simplex . Since this distribution plays an important role in our analysis, it is worth noting that the properties of are not affected by the assumption of a first-order model, since for all . We will also assume that the measures satisfy the following extra regularity condition.

Assumption 1.

For the given set , and each , the distribution has a density with respect to Lebesgue measure on , and is continuous on . Also, if denotes the interior of , then for each , the density is on , and is bounded on .

To interpret this assumption, consider a situation where the class-wise test point distributions have smooth densities on with respect to Lebesgue measure. In this case, the density will exist as long as is sufficiently smooth (cf. Appendix F, Proposition F.1). Still, Assumption 1 might seem unrealistic in the context of random forests, because is obtained by averaging over all decision trees that can be generated from , and strictly speaking, this is a finite average of non-smooth functions. However, due to the bagging mechanism in random forests, the space of trees that can be generated from is very large, and consequently, the function represents a very fine-grained average. Indeed, the idea that bagging is actually a “smoothing operation” on non-smooth functions has received growing attention over the years (Buja and Stuetzle, 2000; Bühlmann and Yu, 2002; Buja and Stuetzle, 2006; Efron, 2014), and the recent paper Efron (2014) states that bagging is “also known as bootstrap smoothing”. In Appendix F, we provide additional assessment of Assumption 1, in terms of both theoretical and empirical examples.

Theorem 3.1 (Bootstrap consistency).

Suppose that the first-order model holds for all , and that Assumption 1 holds. Then, for the given set , there are numbers and such that as ,

| (3.5) |

and furthermore,

Remarks

In a nutshell, the proof of Theorem 3.1 is composed of three pieces: showing that can be represented as a functional of an empirical process (Appendix A.1), establishing the smoothness of this functional (Appendix A.2), and employing the functional delta method (Appendix A.3). With regard to theoretical techniques, there are two novel aspects of the proof. The problem of deriving this functional is solved by introducing a certain lifting operator, while the problem of showing smoothness is based on a non-smooth instance of the first-variation formula, as well as some special properties of Bernstein polynomials. Lastly, it is worth mentioning that the core technical result of the paper is Theorem A.1.

To mention some consequences of Theorem 3.1, the fact that the limiting distribution of has mean 0 shows that the fluctuations of have more influence on algorithmic convergence than the bias (as illustrated in Figure 1). Second, the limiting distribution motivates a convergence criterion of the form , since asymptotic normality it indicates that the event should occur with high probability when is large, and again, this is apparent in Figure 1. Lastly, the theorem implies that the quantiles of agree asymptotically with their bootstrap counterparts. This is of interest, because quantiles allow the user to specify a bound on that holds with a tunable probability. Quantiles also provide an alternative route to estimating algorithmic variance, because if denotes the interquartile range of , then the theorem implies where .

4 Practical considerations

In this section, we discuss some considerations that arise when the proposed method is used in practice, such as the choice of error rate, the computational cost, and the choice of a stopping criterion for algorithmic convergence.

4.1 Extension to class-wise error rates

In some applications, class-wise error rates may be of greater interest than the total error rate . For any , let denote the distribution of the test point given that it is drawn from class . Then, the error rate on class is defined as

| (4.1) |

and the corresponding algorithmic variance is

In order to estimate , Algorithm 2 can be easily adapted using either hold-out or oob points from a particular class. Our theoretical analysis also extends immediately to the estimation of (cf. Section A.1).

4.2 Computational cost and extrapolation

A basic observation about Algorithm 2 is that it only relies on the array of predicted labels (or alternatively ). Consequently, the algorithm does not require any re-training of the classifiers. Also, with regard to computing the arrays or , at least one of these is typically computed anyway when evaluating an ensemble’s performance with hold-out or oob points — and so the cost of obtaining or will typically not be an added expense of Algorithm 2. Thirdly, the algorithm can be parallelized, since the bootstrap replicates can be computed independently. Lastly, the cost of the algorithm is dimension-free with respect to the feature space , since all operations are on the arrays or , whose sizes do not depend on the number of features.

To measure the cost of Algorithm 2 in terms of floating point operations, it is simple to check that at each iteration , the cost of evaluating is of order , since has columns, and each evaluation of the plurality voting function has cost . Hence, if the arrays or are viewed as given, and if , then the cost of Algorithm 2 is , for either the hold-out or oob versions. Below, we describe how this cost can be reduced using a basic form of extrapolation (Bickel and Yahav, 1988; Sidi, 2003; Brezinski and Zaglia, 2013).

Saving on computation with extrapolation

To explain the technique of extrapolation, the first step produces an inexpensive estimate by applying Algorithm 2 to a small initial ensemble of size . The second step then rescales so that it approximates for . This rescaling relies on Theorem 3.1, which leads to the approximation, . Consequently, we define the extrapolated estimate of as

| (4.2) |

In turn, if the user desires for some , then should be chosen so that

| (4.3) |

which is equivalent to .

In addition to applying Algorithm 2 to a smaller ensemble, a second computational benefit is that extrapolation allows the user to “look ahead” and dynamically determine how much extra computation is needed so that is within a desired range. In Section 5, some examples are given showing that can be estimated well via extrapolation when .

Comparison with the cost of training a random forest

Given that one of the main uses of Algorithm 2 is to control the size of a random forest, one would hope that the cost of Algorithm 2 is less than or similar to the cost of training a single ensemble. In order to simplify this comparison, suppose that each tree in the ensemble is grown so that all nodes are split into exactly 2 child nodes (except for the leaves), and that all trees are grown to a common depth . Furthermore, suppose that , and that random forests uses the default rule of randomly selecting from features during each node split. Under these conditions, it is known that the cost of training a random forest with trees via CART is at least of order (Breiman et al., 1984, p.166). Additional background on the details of random forests and decision trees may be found in the book Friedman, Hastie and Tibshirani (2001).

Based on the reasoning just given, the cost of running Algorithm 2 does not exceed the cost of training trees, provided that

where the factor arises from the extrapolation speedup described earlier. Moreover, with regard to the selection of , our numerical examples in Section 5 show that the modest choice allows Algorithm 2 to perform well on a variety of datasets.

The choice of the threshold

When using a criterion such as (4.3) in practice, the choice of the threshold will typically be unique to the user’s goals. For instance, if the user desires that is within 0.5% of , then the choice would be appropriate. Another option is to choose from a relative standpoint, depending on the scale of the error. If the error is high (say is 40%), then it may not be worth paying a large computational price to ensure that is less than 0.5%. Conversely, if is 2%, then it may be worthwhile to train a very large ensemble so that is a fraction of 2%. In either of these cases, the size of could be controlled in a relative sense by selecting when , where is an estimate of obtained from a hold-out set, and is a user-specified constant that measures the balance between computational cost and accuracy. But regardless of the user’s preference for , the more basic point to keep in mind is that the proposed method makes it possible for the user to have direct control over the relationship between and , and this type of control has not previously been available.

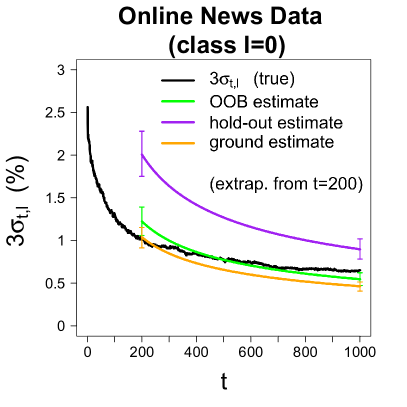

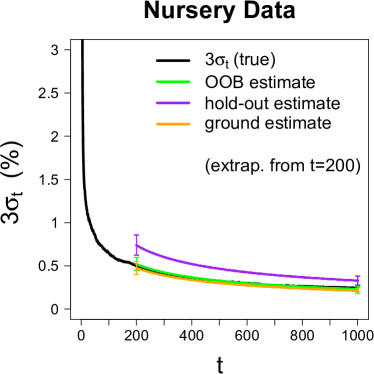

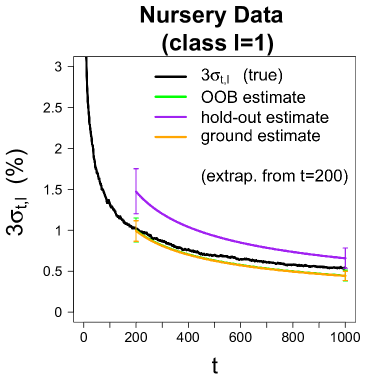

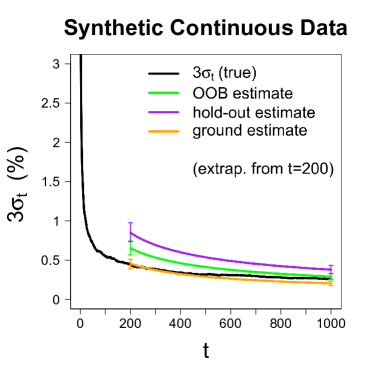

5 Numerical Experiments

To illustrate our proposed method, we describe experiments in which the random forests method is applied to natural and synthetic datasets (6 in total). More specifically, we consider the task of estimating the parameter 3, as well as . Overall, the main purpose of the experiments is to show that the bootstrap can indeed produce accurate estimates of these parameters. A second purpose is to demonstrate the value of the extrapolation technique from Section 4.2.

5.1 Design of experiments

Each of the 6 datasets were partitioned in the following way. First, each dataset was evenly split into a training set and a “ground truth” set , with nearly matching class proportions in and . (The reason that a substantial portion of data was set aside for was to ensure that ground truth values of and could be approximated using this set.) Next, a smaller set with cardinality satisfying was used as the hold-out set for implementing Algorithm 2. As before, the class proportions in and were nearly matching. The smaller size of was chosen to illustrate the performance of the method when hold-out points are limited.

Ground truth values

After preparing , , and , a collection of 1,000 ensembles was trained on by repeatedly running the random forests method. Each ensemble contained a total of 1,000 trees, trained under default settings from the package randomForest (Liaw and Wiener, 2002). Also, we tested each ensemble on to approximate a corresponding sample path of (like the ones shown in Figure 1). Next, in order to obtain “ground truth” values for with , we used the sample standard deviation of the 1,000 sample paths at each . (Ground truth values for each were obtained analogously.)

Extrapolated estimates

With regard to our methodology, we applied the hold-out and oob versions of Algorithm 2 to each of the ensembles — yielding 1,000 realizations of each type of estimate of . In each case, the number of bootstrap replicates was set to , and we applied the extrapolation rule, starting from . If we let and denote the initial hold-out and oob estimators, then the corresponding extrapolated estimators for are given by

| (5.1) |

Next, as a benchmark, we considered an enhanced version of the hold-out estimator, for which the entire ground truth set was used in place of . In other words, this benchmark reflects a situation where a much larger hold-out set is available, and it is referred to as the “ground estimate” in the plots. Its value based on is denoted , and for , we use

| (5.2) |

to refer to its extrapolated version. Lastly, class-wise versions of all extrapolated estimators were computed in an analogous way.

5.2 Description of datasets

The following datasets were each partitioned into , and , as described above.

Census income data

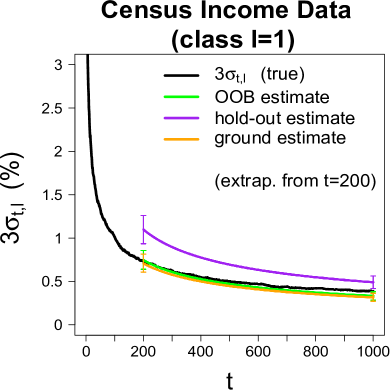

A set of census records for 48,842 people were collected with 14 socioeconomic features (continuous and discrete) (Lichman, 2013). Each record was labeled as 0 or 1, corresponding to low or high income. The proportions of the classes are approximately (.76,.24). As a pre-processing step, we excluded three features corresponding to work-class, occupation, and native country, due to a high proportion of missing values.

Connect-4 data

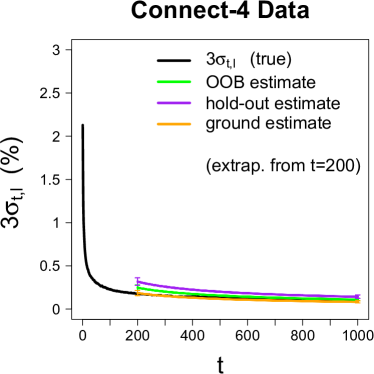

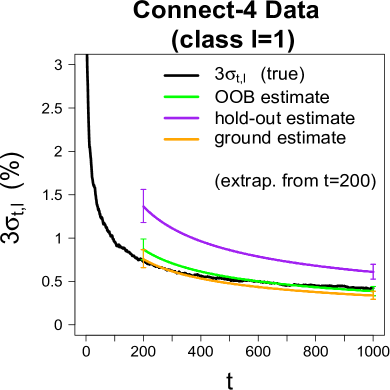

The observations represent 67,557 board positions in the two-person game “connect-4” (Lichman, 2013). For each position, a list of 42 categorical features are available, and each position is labeled as a draw , loss , or win for the first player, with the class proportions being approximately .

Nursery data

This dataset was prepared from a set of 12,960 applications for admission to a nursery school (Lichman, 2013). Each application was associated with a list of 8 (categorical) socioeconomic features. Originally, each application was labeled as one of five classes, but in order to achieve reasonable label balance, the last three categories were combined. This led to approximate class proportions .

Online news data

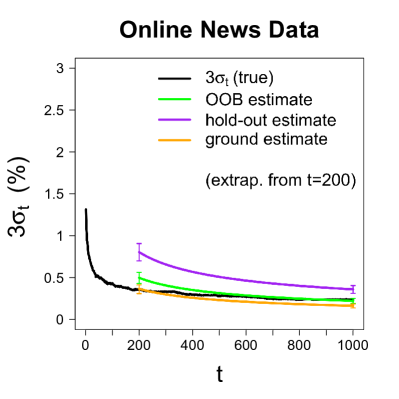

A collection of 39,797 news articles from the website mashable.com were associated with 60 features (continuous and discrete). Each article was labeled based on the number of times it was shared: fewer than 1000 shares , between 1,000 and 5,000 shares (), and greater than 5,000 shares (), with approximate class proportions .

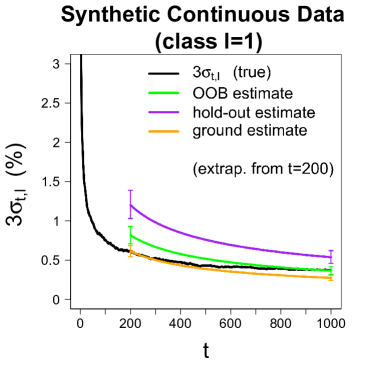

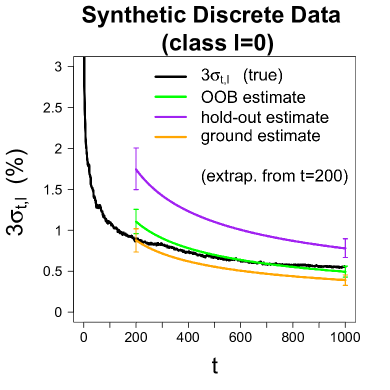

Synthetic continuous data

Two classes of data points in , each of size 10,000, were obtained by drawing samples from the multivariate normal distributions and with a common covariance matrix . The first mean vector was chosen to be , and the second mean vector was constructed to be a sparse vector in the following way. Specifically, we sampled 10 numbers without replacement from , and the coordinates of indexed by were set to the value (with all other coordinates were set to 0). Letting denote the spectral decomposition of , we selected the matrix of eigenvectors by sampling from the uniform (Haar) distribution on orthogonal matrices. The eigenvalues were chosen as .

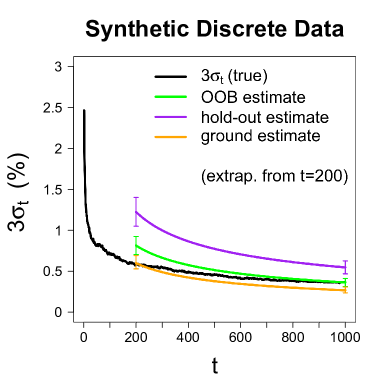

Synthetic discrete data

Two classes of data points in , each of size 10,000, were obtained by drawing samples from the discrete distributions Multinomial and Multinomial, where refers to the number of balls in 100 cells, and the cell probabilities are specified by . Specifically, we set , and . The vector was obtained by perturbing and then normalizing it. Namely, letting be a vector of i.i.d. variables, we defined the vector , where refers to coordinate-wise absolute value.

5.3 Numerical results

Interpreting the plots

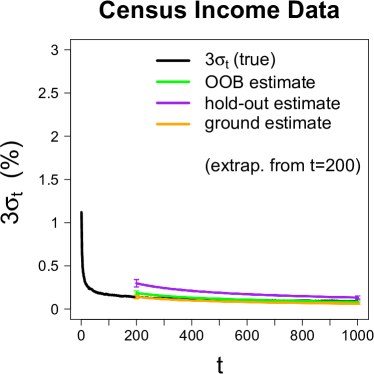

For each dataset, we plot the ground truth value as a function of , where the y-axis is expressed in units of %, so that a value is marked as 1%. Alongside each curve for , we plot the averages of (green) , (purple), and (orange) over their 1,000 realizations, with error bars indicating the spread between the 10th and 90th percentiles of the estimates. Here, the error bars are only given to illustrate the variance of the estimates, conditionally on , and they are not proposed as confidence intervals for . (Indeed, our main focus is on the fluctuations of , rather than the fluctuations of variance estimates.) Lastly, we plot results for the class-wise parameters in the same manner, but in order to keep the number of plots manageable, we only display the class with the highest value of at . This is reflected in the plots, since the values of for the chosen class are generally larger than .

Walking through an example (Figure 2)

To explain the plots from the user’s perspective, suppose the user trains an initial ensemble of classifiers with the ‘census income’ data. (The following considerations will apply in the same way to the other datasets in Figures 3-7.) At this stage, the user may compute either of the estimators or . In turn, the user may follow the definitions (5.1) to plot the extrapolated estimators for all at no additional cost. These curves will look like the purple or green curves in the left panel of Figure 2, up to a small amount of variation indicated by the error bars.

If the user wants to select so that is at most, say 0.5%, then the purple or green curves in the left panel of Figure 2 would tell the user that 200 classifiers are already sufficient, and no extra classifiers are needed (which is correct in this particular example). Alternatively, if the user happens to be interested in the class-wise error rate for , and if the user wants to be at most 0.5%, then the curve for the oob estimator accurately predicts that approximately 600 total (i.e. 400 extra) classifiers are needed. By contrast, the hold-out method is conservative, and indicates that approximately 1,000 total (i.e. 800 extra) classifiers should be trained. So, in other words, the hold-out estimator would still provide the user with the desired outcome, but at a higher computational cost.

Comments on numerical results

Considering all of the datasets collectively, the plots show that the extrapolated oob and ground estimators are generally quite accurate. Meanwhile, the hold-out estimator tends to be conservative, due to an upward bias. Consequently, the oob method should be viewed as preferable, since it is both more accurate, and does not require data to be held out. Nevertheless, when considering the hold-out estimator, it is worth noting that the effect of the bias actually diminishes with extrapolation, and even if the initial value has noticeable bias at , it is possible for the extrapolated value to have relatively small bias at .

To understand where the bias of the hold-out estimator comes from, imagine that two ensembles have been trained on the same data, and suppose their accuracy is compared on a small hold-out set. In this situation, it is possible for their observed error rates on the hold-out set to noticeably differ — even if the true error rates are very close. For this reason, the small size of leads to greater variation among the estimated values generated in the hold-out version of Algorithm 2, which leads to an inflated estimate of . By contrast, the ground estimator suffers less from this bias because it relies on the much larger ground truth set in place of . Similarly, the oob estimate of is less susceptible to this bias, because it will typically use every point in the larger training set as an “effective test point”, preventing excess variation among the values . (Even for small choices of , all training points are likely to be an oob point for at least one classifier.)

One last point to mention is that many of the datasets have discrete features, which may violate the theoretical conditions in Assumption 1. Nevertheless, the presence or absence of discrete features does not seem to substantially affect on the performance of the estimators. So, to this extent, the bootstrap does not seem to depend too heavily on Assumption 1. (See Appendix F.2 for further empirical assessment of that assumption.)

6 Conclusion

We have studied the notion of algorithmic variance as a criterion for deciding when a randomized ensemble will perform nearly as well as an infinite one (trained on the same data). To estimate this parameter, we have developed a new bootstrap method, which allows the user to directly measure the convergence of randomized ensembles with a guarantee that has not previously been available.

With regard to practical considerations, we have shown that our bootstrap method can be enhanced in two ways. First, the use of a hold-out set can be avoided with the oob version of Algorithm 2, and our numerical results show that the oob version is preferable when hold-out points are scarce. Second, the extrapolation technique substantially reduces the cost of bootstrapping. Furthermore, we have analyzed the cost of the method in terms of floating point operations to show that it compares favorably with the cost of training a single ensemble via random forests.

From a theoretical standpoint, we have analyzed the proposed method within the framework of a first-order model for randomized ensembles. In particular, for a generic ensemble whose classifiers are conditionally i.i.d. given , there is a corresponding first-order model that matches the generic ensemble with respect to its average error rate . Under this setup, our main result shows that the proposed method consistently approximates as . Some extensions of this result could include generalizations to other models of randomized ensembles (e.g., along the lines of Biau, Devroye and Lugosi (2008); Biau (2012); Scornet, Biau and Vert (2015); Scornet (2016b)), as well as corresponding results in the context of regression ensembles, which we hope to pursue in future work. More generally, due to the versatility of bootstrap methods, our approach may also be relevant to measuring the convergence of other randomized algorithms, as in Lopes, Wang and Mahoney (2017, 2018).

Acknowledgements

The author thanks Peter Bickel, Philip Kegelmeyer, and Debashis Paul for helpful discussions. In addition, the author thanks the editors and referees for their valuable feedback, which significantly improved the paper.

References

- Arlot and Genuer (2014) {barticle}[author] \bauthor\bsnmArlot, \bfnmS.\binitsS. and \bauthor\bsnmGenuer, \bfnmR.\binitsR. (\byear2014). \btitleAnalysis of purely random forests bias. \bjournalpreprint arXiv:1407.3939. \endbibitem

- Biau (2012) {barticle}[author] \bauthor\bsnmBiau, \bfnmG.\binitsG. (\byear2012). \btitleAnalysis of a random forests model. \bjournalJournal of Machine Learning Research \bvolume13 \bpages1063–1095. \endbibitem

- Biau, Devroye and Lugosi (2008) {barticle}[author] \bauthor\bsnmBiau, \bfnmG.\binitsG., \bauthor\bsnmDevroye, \bfnmL.\binitsL. and \bauthor\bsnmLugosi, \bfnmG.\binitsG. (\byear2008). \btitleConsistency of random forests and other averaging classifiers. \bjournalJournal of Machine Learning Research \bvolume9 \bpages2015–2033. \endbibitem

- Bickel and Yahav (1988) {barticle}[author] \bauthor\bsnmBickel, \bfnmP. J.\binitsP. J. and \bauthor\bsnmYahav, \bfnmJ. A.\binitsJ. A. (\byear1988). \btitleRichardson extrapolation and the bootstrap. \bjournalJournal of the American Statistical Association \bvolume83 \bpages387–393. \endbibitem

- Breiman (1996) {barticle}[author] \bauthor\bsnmBreiman, \bfnmL.\binitsL. (\byear1996). \btitleBagging predictors. \bjournalMachine Learning \bvolume24 \bpages123–140. \endbibitem

- Breiman (2001) {barticle}[author] \bauthor\bsnmBreiman, \bfnmL.\binitsL. (\byear2001). \btitleRandom forests. \bjournalMachine Learning \bvolume45 \bpages5–32. \endbibitem

- Breiman et al. (1984) {bbook}[author] \bauthor\bsnmBreiman, \bfnmL.\binitsL., \bauthor\bsnmFriedman, \bfnmJ.\binitsJ., \bauthor\bsnmStone, \bfnmC. J.\binitsC. J. and \bauthor\bsnmOlshen, \bfnmR. A.\binitsR. A. (\byear1984). \btitleClassification and regression trees. \bpublisherCRC press. \endbibitem

- Brezinski and Zaglia (2013) {bbook}[author] \bauthor\bsnmBrezinski, \bfnmC.\binitsC. and \bauthor\bsnmZaglia, \bfnmM. R.\binitsM. R. (\byear2013). \btitleExtrapolation methods: theory and practice. \bpublisherElsevier. \endbibitem

- Bühlmann and Yu (2002) {barticle}[author] \bauthor\bsnmBühlmann, \bfnmP.\binitsP. and \bauthor\bsnmYu, \bfnmB.\binitsB. (\byear2002). \btitleAnalyzing bagging. \bjournalThe Annals of Statistics \bpages927–961. \endbibitem

- Buja and Stuetzle (2000) {barticle}[author] \bauthor\bsnmBuja, \bfnmA.\binitsA. and \bauthor\bsnmStuetzle, \bfnmW.\binitsW. (\byear2000). \btitleSmoothing effects of bagging. \bjournalPreprint, AT&T Labs-Research. \endbibitem

- Buja and Stuetzle (2006) {barticle}[author] \bauthor\bsnmBuja, \bfnmA.\binitsA. and \bauthor\bsnmStuetzle, \bfnmW.\binitsW. (\byear2006). \btitleObservations on bagging. \bjournalStatistica Sinica \bpages323–351. \endbibitem

- Bürgisser and Cucker (2013) {bbook}[author] \bauthor\bsnmBürgisser, \bfnmP.\binitsP. and \bauthor\bsnmCucker, \bfnmF.\binitsF. (\byear2013). \btitleCondition: The geometry of numerical algorithms \bvolume349. \bpublisherSpringer. \endbibitem

- Byrd et al. (2012) {barticle}[author] \bauthor\bsnmByrd, \bfnmR. H.\binitsR. H., \bauthor\bsnmChin, \bfnmG. M.\binitsG. M., \bauthor\bsnmNocedal, \bfnmJ.\binitsJ. and \bauthor\bsnmWu, \bfnmY.\binitsY. (\byear2012). \btitleSample size selection in optimization methods for machine learning. \bjournalMathematical programming \bvolume134 \bpages127–155. \endbibitem

- Cannings and Samworth (2017) {barticle}[author] \bauthor\bsnmCannings, \bfnmT. I.\binitsT. I. and \bauthor\bsnmSamworth, \bfnmR. J.\binitsR. J. (\byear2017). \btitleRandom projection ensemble classification (with discussion). \bjournalJournal of the Royal Statistical Society Series B. \endbibitem

- Dietterich (2000) {barticle}[author] \bauthor\bsnmDietterich, \bfnmT. G.\binitsT. G. (\byear2000). \btitleAn experimental comparison of three methods for constructing ensembles of decision trees: Bagging, boosting, and randomization. \bjournalMachine learning \bvolume40 \bpages139–157. \endbibitem

- Efron (2014) {barticle}[author] \bauthor\bsnmEfron, \bfnmB.\binitsB. (\byear2014). \btitleEstimation and accuracy after model selection. \bjournalJournal of the American Statistical Association \bvolume109 \bpages991–1007. \endbibitem

- Friedman, Hastie and Tibshirani (2001) {bbook}[author] \bauthor\bsnmFriedman, \bfnmJ.\binitsJ., \bauthor\bsnmHastie, \bfnmT.\binitsT. and \bauthor\bsnmTibshirani, \bfnmR.\binitsR. (\byear2001). \btitleThe Elements of Statistical Learning. \bpublisherSpringer. \endbibitem

- Genuer (2012) {barticle}[author] \bauthor\bsnmGenuer, \bfnmR.\binitsR. (\byear2012). \btitleVariance reduction in purely random forests. \bjournalJournal of Nonparametric Statistics \bvolume24 \bpages543–562. \endbibitem

- Hall and Samworth (2005) {barticle}[author] \bauthor\bsnmHall, \bfnmP.\binitsP. and \bauthor\bsnmSamworth, \bfnmR. J.\binitsR. J. (\byear2005). \btitleProperties of bagged nearest neighbour classifiers. \bjournalJournal of the Royal Statistical Society: Series B \bvolume67 \bpages363–379. \endbibitem

- Hernández-Lobato, Martínez-Muñoz and Suárez (2013) {barticle}[author] \bauthor\bsnmHernández-Lobato, \bfnmD.\binitsD., \bauthor\bsnmMartínez-Muñoz, \bfnmG.\binitsG. and \bauthor\bsnmSuárez, \bfnmA.\binitsA. (\byear2013). \btitleHow large should ensembles of classifiers be? \bjournalPattern Recognition \bvolume46 \bpages1323–1336. \endbibitem

- Ho (1998) {barticle}[author] \bauthor\bsnmHo, \bfnmT. K.\binitsT. K. (\byear1998). \btitleThe random subspace method for constructing decision forests. \bjournalIEEE transactions on pattern analysis and machine intelligence \bvolume20 \bpages832–844. \endbibitem

- Kallenberg (2006) {bbook}[author] \bauthor\bsnmKallenberg, \bfnmO.\binitsO. (\byear2006). \btitleFoundations of Modern Probability. \bpublisherSpringer. \endbibitem

- Lam and Suen (1997) {barticle}[author] \bauthor\bsnmLam, \bfnmL.\binitsL. and \bauthor\bsnmSuen, \bfnmC. Y.\binitsC. Y. (\byear1997). \btitleApplication of majority voting to pattern recognition: an analysis of its behavior and performance. \bjournalIEEE Transactions on Systems, Man, and Cybernetics-Part A: Systems and Humans \bvolume27 \bpages553–568. \endbibitem

- Latinne, Debeir and Decaestecker (2001) {binproceedings}[author] \bauthor\bsnmLatinne, \bfnmP.\binitsP., \bauthor\bsnmDebeir, \bfnmO.\binitsO. and \bauthor\bsnmDecaestecker, \bfnmC.\binitsC. (\byear2001). \btitleLimiting the number of trees in random forests. In \bbooktitleMultiple Classifier Systems. \bpublisherSpringer. \endbibitem

- Liaw and Wiener (2002) {barticle}[author] \bauthor\bsnmLiaw, \bfnmA.\binitsA. and \bauthor\bsnmWiener, \bfnmM.\binitsM. (\byear2002). \btitleClassification and regression by randomForest. \bjournalR News \bvolume2 \bpages18-22. \endbibitem

- Lichman (2013) {bmisc}[author] \bauthor\bsnmLichman, \bfnmM.\binitsM. (\byear2013). \btitleUCI Machine Learning Repository. \endbibitem

- Lin and Jeon (2006) {barticle}[author] \bauthor\bsnmLin, \bfnmY.\binitsY. and \bauthor\bsnmJeon, \bfnmY.\binitsY. (\byear2006). \btitleRandom forests and adaptive nearest neighbors. \bjournalJournal of the American Statistical Association \bvolume101 \bpages578–590. \endbibitem

- Lopes (2016) {barticle}[author] \bauthor\bsnmLopes, \bfnmM. E.\binitsM. E. (\byear2016). \btitleA sharp bound on the computation-accuracy tradeoff for majority voting ensembles. \bjournalpreprint arXiv:1303.0727. \endbibitem

- Lopes, Wang and Mahoney (2017) {barticle}[author] \bauthor\bsnmLopes, \bfnmM. E.\binitsM. E., \bauthor\bsnmWang, \bfnmS.\binitsS. and \bauthor\bsnmMahoney, \bfnmM. W.\binitsM. W. (\byear2017). \btitleA bootstrap method for error estimation in randomized matrix multiplication. \bjournalpreprint arXiv:1708.01945. \endbibitem

- Lopes, Wang and Mahoney (2018) {binproceedings}[author] \bauthor\bsnmLopes, \bfnmM. E.\binitsM. E., \bauthor\bsnmWang, \bfnmS.\binitsS. and \bauthor\bsnmMahoney, \bfnmM. W.\binitsM. W. (\byear2018). \btitleError estimation for randomized least-squares algorithms via the bootstrap. In \bbooktitleInternational Conference on Machine Learning (to appear). \endbibitem

- Mentch and Hooker (2016) {barticle}[author] \bauthor\bsnmMentch, \bfnmL.\binitsL. and \bauthor\bsnmHooker, \bfnmG.\binitsG. (\byear2016). \btitleQuantifying uncertainty in random forests via confidence intervals and hypothesis tests. \bjournalJournal of Machine Learning Research \bvolume17 \bpages1–41. \endbibitem

- Ng and Jordan (2001) {binproceedings}[author] \bauthor\bsnmNg, \bfnmA. Y.\binitsA. Y. and \bauthor\bsnmJordan, \bfnmM. I.\binitsM. I. (\byear2001). \btitleConvergence rates of the voting Gibbs classifier, with application to Bayesian feature selection. In \bbooktitleInternational Conference on Machine Learning \bpages377–384. \endbibitem

- Oshiro, Perez and Baranauskas (2012) {binproceedings}[author] \bauthor\bsnmOshiro, \bfnmT. M.\binitsT. M., \bauthor\bsnmPerez, \bfnmP. S.\binitsP. S. and \bauthor\bsnmBaranauskas, \bfnmJ. A.\binitsJ. A. (\byear2012). \btitleHow many trees in a random forest? In \bbooktitleMachine Learning and Data Mining in Pattern Recognition \bpages154–168. \bpublisherSpringer. \endbibitem

- Schapire and Freund (2012) {bbook}[author] \bauthor\bsnmSchapire, \bfnmR.\binitsR. and \bauthor\bsnmFreund, \bfnmY.\binitsY. (\byear2012). \btitleBoosting: Foundations and Algorithms. \bpublisherThe MIT Press. \endbibitem

- Scornet (2016a) {barticle}[author] \bauthor\bsnmScornet, \bfnmE.\binitsE. (\byear2016a). \btitleOn the asymptotics of random forests. \bjournalJournal of Multivariate Analysis \bvolume146 \bpages72–83. \endbibitem

- Scornet (2016b) {barticle}[author] \bauthor\bsnmScornet, \bfnmE.\binitsE. (\byear2016b). \btitleRandom forests and kernel methods. \bjournalIEEE Transactions on Information Theory \bvolume62 \bpages1485–1500. \endbibitem

- Scornet, Biau and Vert (2015) {barticle}[author] \bauthor\bsnmScornet, \bfnmE.\binitsE., \bauthor\bsnmBiau, \bfnmG.\binitsG. and \bauthor\bsnmVert, \bfnmJ. P.\binitsJ. P. (\byear2015). \btitleConsistency of random forests. \bjournalThe Annals of Statistics \bvolume43 \bpages1716–1741. \endbibitem

- Sexton and Laake (2009) {barticle}[author] \bauthor\bsnmSexton, \bfnmJ.\binitsJ. and \bauthor\bsnmLaake, \bfnmP.\binitsP. (\byear2009). \btitleStandard errors for bagged and random forest estimators. \bjournalComputational Statistics & Data Analysis \bvolume53 \bpages801–811. \endbibitem

- Sidi (2003) {bbook}[author] \bauthor\bsnmSidi, \bfnmA\binitsA. (\byear2003). \btitlePractical Extrapolation Methods: Theory and Applications. \bpublisherCambridge University Press. \endbibitem

- Simon (1983) {bbook}[author] \bauthor\bsnmSimon, \bfnmL.\binitsL. (\byear1983). \btitleLectures on Geometric Measure Theory. \bpublisherThe Australian National University, Mathematical Sciences Institute, Centre for Mathematics & Its Applications. \endbibitem

- van der Vaart and Wellner (1996) {bbook}[author] \bauthor\bparticlevan der \bsnmVaart, \bfnmA. W.\binitsA. W. and \bauthor\bsnmWellner, \bfnmJ. A.\binitsJ. A. (\byear1996). \btitleWeak Convergence and Empirical Processes. \bpublisherSpringer. \endbibitem

- Wager, Hastie and Efron (2014) {barticle}[author] \bauthor\bsnmWager, \bfnmS.\binitsS., \bauthor\bsnmHastie, \bfnmT.\binitsT. and \bauthor\bsnmEfron, \bfnmB.\binitsB. (\byear2014). \btitleConfidence intervals for random forests: the jackknife and the infinitesimal jackknife. \bjournalJournal of Machine Learning Research \bvolume15 \bpages1625–1651. \endbibitem

- White (2016) {binproceedings}[author] \bauthor\bsnmWhite, \bfnmB.\binitsB. (\byear2016). \btitleIntroduction to Minimal Surface Theory. In \bbooktitleGeometric Analysis \bvolume22. \bpublisherAmerican Mathematical Society. \endbibitem

Supplementary Material

Outline of appendices and the proof of Theorem 3.1

Here we explain how the the main components of the proof of Theorem 3.1 fit together. First, in Appendix A.1, we show that under a first-order model, there is an explicit functional such that

| (1) |

where is the empirical c.d.f. of independent Uniform[0,1] random variables , and id is the identity function on . Also note that under the first-order model, the set of variables plays the role of the randomizing parameters . It follows that bootstrapping the classifier functions corresponds to bootstrapping the variables . More specifically, if we let

where are drawn with replacement from , then the bootstrap counterpart of (1) is given by

| (2) |

Due to the relations (1) and (2), the remainder of the proof deals with converting “bootstrap consistency for ” into “bootstrap consistency for ”, and this is handled with the functional delta method. In this way, the proof boils down to establishing the Hadamard differentiability of , which is done in Theorem A.1 of Appendix A.2, and this should be viewed as the core technical result of the paper. In turn, the details of applying the functional delta method, as well as the conclusion of the proof, are given in Appendix A.3.

The remainder of the appendices are organized as follows. Appendices B, C, and D contain the arguments for proving Theorem A.1 on Hadamard differentiability. Throughout these arguments, we will refer to various technical lemmas that are stated and proved in Appendix E. Also, we henceforth assume that the first-order model holds, so that for , and the sets and are synonymous. Lastly, Appendix F discusses the theoretical and empirical assessment of Assumption 1.

Notation

If is a generic subset of Euclidean space, we write for the interior and for the boundary. The identity function on is denoted , or just id when there is no ambiguity. The spaces , , , and respectively denote the following sets of real-valued functions on [0,1], all equipped with the supremum norm: continuous functions, càdlàg functions, distribution functions with no point mass at 0, and bounded functions. Hence, if we write as for functions and in these spaces, it is implicit that the convergence is uniform. (The analogous definitions apply when the open interval replaces .) Lastly, we use to denote the space of coordinate-wise bounded functions from to , with norm , where

Appendix A Proof of Theorem 3.1

A.1 Representing as a functional of the empirical process

Working under the first-order model, our aim in this subsection is to construct an explicit functional such that

(Later on, we will formally define , which will turn out to be the limit of as .) To construct this functional, consider the basic relation , where is the th class proportion, and is defined in equation (4.1). Hence, for each , it is enough to construct a functional such that

| (A.1) |

which implies that may be written as .

The lifting operator

As a first step in deriving the relation (A.1), we will show that the stochastic process can be obtained from a linear operator that “lifts” the univariate function on to a multivariate map on the simplex . The relationship between and is unraveled by noting that for any , the definition of the interval gives

| (A.2) |

and also . Due to the formula above, it is natural to consider an operator, denoted , that lifts a generic function to a new function whose th coordinate is given by

| (A.3) |

where is understood as 0 when . In particular, the definition of , and the calculation in equation (A.2), show that can be expressed by lifting and then evaluating at ,

| (A.4) |

Since many of our arguments will rely on special properties of , we briefly summarize these properties below.

Properties of the lifting operator

If we let and denote generic real-valued functions on , and let denote a scalar, then the following conditions hold.

-

•

Linearity.

-

•

Composition.

-

•

Identities.

-

•

Simplices.

If is non-decreasing and maps to , then maps to . -

•

Inverses.

If is invertible, then is invertible and .

The fact that respects composition of functions is the only property that takes some care to verify, but we omit the calculation for brevity. In turn, the “Inverses” property follows by combining the “Composition” and “Identities” properties.

Deriving the relation

To finish the derivation of as a functional of , it is helpful to consider a certain subset of . Namely, observe that if a test point is drawn from class , then an error occurs for the plurality vote if and only if

| (A.5) |

where the set is defined as

where . Consequently, we have

Next, the formula from equation (A.4) implies

where the set is the pre-image of under the map . Finally, if we recall the definition of , then is the -probability of the pre-image,

| (A.6) |

which provides us with the desired representation of as a functional of . More precisely, we obtain the relation by defining the functional according to

| (A.7) |

where , and we note that lies in almost surely.

A.2 Hadamard differentiability of

Since the random distribution function approaches as , the asymptotic behavior of is closely linked to the smoothness of at the “point” . Specifically, we will use the standard notion of Hadamard differentiability, as reviewed below (van der Vaart and Wellner, 1996).

Definition 1 (Hadamard differentiability222The added generality of letting B be a normed space, rather than just , will be needed in Appendix E.).

Let B be a normed space. A map is Hadamard differentiable at tangentially to , if there is a continuous linear map such that as ,

for all converging sequences of positive numbers and functions , such that for every , and . In particular, the linear map is referred to as the Hadamard derivative of at .

The following result (Theorem A.1) is the core technical result of the paper. It provides conditions under which the functionals are Hadamard differentiable at , tangentially to . Likewise, the theorem implies that the same differentiability property holds for the linear combination , for which .

Although each functional is defined in terms of the particular set and the particular measure , the Hadamard differentiability of is only mildly dependent on their structure. For each measure , the only property we need is that it satisfies Assumption 1. Regarding the set , it is simple to check that its complement in is a convex set with non-empty interior. In other words, the functional may be written as for some convex set with non-empty interior. So, given that the Hadamard derivative of is that same as that of , up to a sign, we state the result in terms of a generic functional that arises from such a set , and such a measure .

Theorem A.1 (Hadamard differentiability of ).

Let be a convex set with non-empty interior, and let be a distribution on satisfying the conditions of Assumption 1. Also let be defined for any according to

Then, the functional is Hadamard differentiable at tangentially to . Furthermore, the Hadamard derivative is given by

| (A.8) |

where is the outward normal to at the point , and is Hausdorff measure on .

Remark

A.3 Functional delta method

Recall that the bootstrap works for in the sense that the law converges weakly in probability to the same limit as . The following well-known fact shows that bootstrap consistency is preserved when and are composed with a Hadamard differentiable functional.

Lemma A.1 (Functional delta method (vaart), Sec. 23.2.1).

Let be Hadamard differentiable at , tangentially to . Also, let be a standard Brownian bridge on . Then, as ,

and

Concluding the proof of Theorem 3.1

With this lemma in hand, Theorem 3.1 on bootstrap consistency follows quickly from Theorem A.1. Specifically, if we consider , with each as in equation (A.7), and define , then the relations (1) and (2) lead to

| (A.9) | ||||

| (A.10) |

where we recall that in the first-order model, as explained on p.3.1.1 of the main text. Note also that implicitly depends on through the function .

It follows from Theorem A.1 and Lemma A.1 that the right hand sides of (A.9) and (A.10) tend to the same weak limit, namely . The only remaining detail to be proven in Theorem 3.1 is that has a centered Gaussian distribution. This follows from the fact that is a centered tight Gaussian process in , and the fact that is a continuous linear functional on (van der Vaart and Wellner, 1996, Lemma 3.9.8).

Appendix B A high-level proof of Theorem A.1

Here we give a proof of Theorem A.1 that focuses on the key ideas and delegates the technical pieces to Appendices C, D, and E. Consider a sequence of positive numbers and functions such that for every , and . Define the distribution function by

and define its lifted version by

The fact that the range of is contained in follows from the properties of listed earlier. Our aim is to evaluate the limit of the following difference as ,

| (B.1) |

Here, we have used the fact that , which follows from . Since approaches as , we may view the preimage as a perturbed version of the set . From this perspective, it is natural to interpret the right side of equation (B.1) through the lens of the first variation formula, introduced in Section 1.1, with playing the role of a volume, playing the role of a manifold, and playing the role of the map with .

In its classical form, the first variation formula deals with smooth maps on smooth manifolds. However, since the map need not be smooth, our proof proceeds by constructing a smoothed version of . In order to do this, it is enough to smooth the univariate function and apply the linear operator . The smoothing will be done using the linear Bernstein smoothing operator, denoted , where is an integer-valued smoothing parameter (lorentz; devoreconstructive).

For any function , the Bernstein smoothing operator returns a new function defined by

where is the th Bernstein basis polynomial where , and ranges over . Below, we will use of some special properties of this operator. First, when is a cumulative distribution function, it turns out that is also a cumulative distribution function. Second, when is continuous, we have the uniform limit as . The details of all the properties of we will use are summarized in Lemma E.1 of Appendix E.

When applying the operator , the smoothed version of will be denoted by

Likewise, the smoothed version of will be denoted by

| (B.2) |

which is a map from to itself. (It is not immediately obvious that takes values in , and this follows from being a cumulative distribution function, by Lemma E.1, as well as the “Simplices” property of .)

The remainder of the proof involves two essential parts. First, we prove a special version of the first variation formula for the smoothed maps . Second, we show that this smoothing leads to negligible approximation error. To quantify the approximation error from smoothing, define the remainder according to the following equation

| (B.3) |

Due to the smoothness of , the difference quotient on the right may be represented with a change of variable formula

where is the Jacobian matrix of at the point . This step is justified by Lemmas E.4, E.6, and E.7, which also prove invertibility of . From the above integral formula, Proposition C.1 in Appendix C provides the following limit

Next, Proposition D.1 in Appendix D shows that replacing with its smoothed version leads to negligible approximation error, i.e.

Consequently, by separately applying the operations and to equation (B.3), and then taking in each case, it follows that

Lastly, it is simple to check that the right side is a continuous linear functional of , as required by the definition of Hadamard differentiability. ∎

Appendix C A first variation formula

Proposition C.1.

Proof.

For any , let

| (C.2) |

and

| (C.3) |

Using an expansion for given in Lemma E.5 of Appendix E, as well as the boundedness of on , the integral on the left side of equation (C.1) may be written as

| (C.4) |

where is the divergence of evaluated at , and is a sequence of numbers not depending on . (In addition, note that lies in whenever , which follows from Lemma E.4, and the invariance of domain principle (Hatcher, Theorem 2B.3).)

We now evaluate the limits of the two integrals in line (C.4) separately. Due to the multivariate mean value theorem, for each fixed , there is a point on the line segment between and such that

| (C.5) |

Also, the points may be taken to satisfy as , since for every fixed and fixed , which follows from Lemma E.9. By the Cauchy-Schwarz inequality, the inner product in equation (C.5) is dominated by a number depending only on , since is bounded on by assumption, and is finite by Lemma E.9. Furthermore, Lemma E.9 gives the convergence for every , where we define

| (C.6) |

Hence, the continuity of and the dominated convergence theorem lead to

Turning our attention to the second integral in line (C.4), Lemma E.3 ensures that the divergence

converges uniformly to on as . Combining this with the facts that for every (Lemma E.9) and that is continuous (since is smooth), it follows that

Furthermore, it is simple to check that this pointwise limit is dominated by a constant (using Lemma E.3), and so

The preceding calculations may now be combined using the basic differential identity

which shows that the quantity in line (C.4) tends to as with held fixed. In turn, Stokes’ theorem may be applied to this divergence integral. To be specific, an applicable version of the Stokes’ theorem that holds for convex domains may be found in Leoni. (When referencing that result, note that bounded convex domains have Lipschitz boundaries (Grisvard, Corollary 1.2.2.3), and also, that the regularity assumptions on imply that is a Lipschitz vector field on .) Hence, for every ,

| (C.7) |

Appendix D Smoothing error is negligible

Proposition D.1.

Proof.

It is simple to check that may be written as

| (D.1) |

We will argue that both terms on the right side are small. Note that the set consists of the points such that and . Now consider a particular point , and note that if the Euclidean distance between the points and is written as , then both of the points and must be within a distance from the boundary . In other words, both of the points and lie within the tubular neighborhood of of radius . (The same reasoning applies to the other set .)

To express the previous paragraph more formally, let denote the tubular neighborhood of of radius ,

where is the Euclidean distance from a point to the boundary . Also, for any , recall that

| (D.2) |

Consequently, applying the reasoning above to both terms on the right side of equation (D.1) gives,

| (D.3) |

Furthermore, if is a random vector distributed according to , then this upper bound may be written as

To modify the last bound somewhat, let

| (D.4) |

and put

| (D.5) |

(This definition of will be used later on for handling the formal possibility that may be zero. Note that is positive for all and .) Clearly, the definition of gives

Next, we obtain an upper bound on this probability using a volume argument. Lemma E.6 in Appendix E shows that has a density, say , with respect to -dimensional Lebesgue measure. Also, Lemmas E.4 and E.7 imply that the random vector lies in with probability 1 for all and . Therefore,

| (D.6) |

where denotes Lebesgue measure on .

To control the volume of the right side of the bound (D.6), it is convenient to consider the Hausdorff measure of . Specifically, it is a fact from geometric measure theory that the -dimensional Hausdorff measure of , denoted , can be expressed as

| (D.7) |

(See the beginning of Section 3.2.37 and Theorem 3.2.39 in the book (federer) for additional details. In addition, that result depends on the fact that bounded convex sets in have -rectifiable boundaries (ambrosio, p.743).) In order to make use of the expression above, we will rely on Lemma E.8 in Appendix E, which states that for every , there is a number such that

In particular, is a sequence of positive numbers with as , and so when is fixed, this means

| (D.8) |

We now turn our attention to the factor in the bound (D.6). Lemma E.6 ensures there is a constant , such that the following bound holds for every ,

| (D.9) |

Combining lines (D.6), (D.8), and (D.9), we conclude that for every ,

Finally, the proof is completed using the fact that as , which is shown in Lemma E.8.∎

Appendix E Technical lemmas

Remark

To simplify the statements of the lemmas in this section, the notation in the previous appendices will be generally assumed without comment.

Proof of equation (3.3)

Recall and that we may express and as

By Fubini’s theorem,

Consequently, the claim will follow if we can verify the equation

for every fixed . This holds because when is fixed, we have , due to the first-order matching condition (3.1).∎

Lemma E.1 (Properties of Bernstein polynomials).

The Bernstein smoothing operator satisfies the following properties.

-

1.

For any function , the following limit holds

-

2.

If is linear, then for all , and in particular .

-

3.

If is non-decreasing and non-constant, then for every , the function is strictly increasing on .

Proof.

We refer to the book (devoreconstructive) for general background on these properties. The first property is given in Theorem 2.3 of (devoreconstructive, Chapter 1). The second property is proven after equation 1.7 of (devoreconstructive, Chapter 1).

Regarding the third property, if we let be arbitrary, it is enough to show that the derivative is strictly positive. To this end, it is shown in equation 2.2 of (devoreconstructive, Chapter 10) that satisfies

| (E.1) |

where we put . If is non-decreasing and non-constant then

So, because all the terms are non-negative, at least one of them must be positive. In turn, equation (E.1) implies that must be positive, since all the values are positive for all . ∎

Remark

Let denote the differentiation operator on univariate functions. If this operator is applied to a function with domain , then the domain of the derivative is taken to be .

Lemma E.2.

Let be the indicator function of . Then, for any fixed , we have the identity,

| (E.2) |

and the uniform limit,

| (E.3) |

Proof.

The identity (E.2) is a direct consequence of from Lemma E.1. To prove the limit, first note that because the functions are polynomials on , the supremum is finite. Hence, for fixed ,

∎

Lemma E.3.

For any fixed , there is a number not depending on such that the inequality

| (E.4) |

holds for all . Furthermore, as , we have the uniform limit

| (E.5) |