∎ \pstVerbrealtime srand

22email: Noonanj1@cf.ac.uk 33institutetext: Anatoly Zhigljavsky 44institutetext: School of Mathematics, Cardiff University, Cardiff, CF24 4AG, UK

44email: ZhigljavskyAA@cardiff.ac.uk

Approximations for the boundary crossing probabilities of moving sums of random variables

Abstract

In this paper we study approximations for the boundary crossing probabilities of moving sums of i.i.d. normal random variables. We approximate a discrete time problem with a continuous time problem allowing us to apply established theory for stationary Gaussian processes. By then subsequently correcting approximations for discrete time, we show that the developed approximations are very accurate even for a small window length. Also, they have high accuracy when the original r.v. are not exactly normal and when the weights in the moving window are not all equal. We then provide accurate and simple approximations for ARL, the average run length until crossing the boundary.

Keywords:

moving sum boundary crossing probability moving sum of normal change-point detectionMSC:

Primary: 60G50, 60G35; Secondary:60G70, 94C12, 93E201 Introduction: Statement of the problem

Let be a sequence of i.i.d. normal random variables (r.v.) with mean and variance . For a fixed positive integer , the moving sums are defined by

| (1.1) |

The sequence of the moving sums (1.1) will be denoted by so that .

The main aim of this paper is development of accurate approximations for the boundary crossing probability (BCP) for the maximum of the moving sums:

| (1.2) |

where is a given positive integer and is a fixed threshold. Note that the total number of r.v. used in (1.2) is and as , for all and . We will mostly be interested in deriving accurate approximations when . The case of is much simpler and is comprehensively covered in (AandZ2019, , Section 3), see Section 4.6 for discussion.

Developing accurate approximations for the BCP for generic parameters , and is very important in various areas of statistics, predominantly in applications related to change-point detection; see, for example, papers Bau2 ; Chu ; Glaz2012 ; MZ2003 ; Xia and especially books glaz2001scan ; glaz2009scan2 . Engineering applications of MOSUM (moving sums charts) are extremely important and have been widely discussed in literature; see e.g. Chu ; eiauer1978use ; glaz2001scan ; glaz2009scan2 ; waldmann1986bounds . The BCP is an ()-dimensional integral and therefore direct evaluation of this BCP is hardly possible even with modern software.

To derive approximations for the BCP (1.2) one can use standard tools and approximate the sequence of moving sums with a continuous-time process and then use some continuous-time approximations, see e.g. Haiman ; these approximations, however, are not accurate especially for small window length ; see discussion in Section 4.7. There is, therefore, a need for derivation of specific approximations for the BCP (1.2). Such a need was well understood in the statistical community and indeed very accurate approximations for the BCP and the Average Run Length (ARL) have been developed in a series of quality papers by J. Glaz and coauthors, see for example Glaz_old ; Glaz2012 ; wang2014variable ; wang2014multiple (the methodology was also extended to the case when are integer-valued r.v., see glaz1991tight ). We will call these approximations ‘Glaz approximations’ by the name of the main author of these papers; they will be formally written down in Sections 2.2 and 7.

The accuracy of the approximations developed in the present paper is very high and similar to the Glaz approximations; this is discussed in Sections 6 and 7. The methodologies of derivation of Glaz approximations and the approximations of this paper are very different. The practical advantage of our approximations (they require approximating either a one-dimensional integral or an eigenvalue of an integral operator) is their relative simplicity as to compute the Glaz approximations one needs to numerically approximate and dimensional integrals. This is not an easy task even taking into account the fact of existence of a sophisticated software; see references in Section 2.2.

The paper is structured as follows. In Section 2 we reformulate the problem, state the Glaz approximation and discuss how to approximate our discrete-time problem with a continuous-time problem. In Section 3 we provide exact formulas for the first-passage probabilities (in the continuous-time setup) due to L. Shepp Shepp71 and give their alternative representation which will be crucial for deriving some of our approximations. In Section 4 we adapt the methodology of D. Siegmund to correct Shepp’s formulas for discrete time and define a version of the Glaz approximation which we will call Glaz-Shepp-Siegmund approximation. In Section 5 we develop continuous-time approximations based on approximating eigenvalues of integral operators and subsequently correct them for discrete time. In Sections 4.7 and 6 we present results of large-scale simulation studies evaluating the performance of the considered approximations (also, in the cases when the original r.v. are not normal and the weights in the moving window are not equal). In Section 7, we develop an approximation for ARL and compare its accuracy to the one developed in Glaz2012 .

2 Boundary crossing probabilities: discrete and continuous time

2.1 Standardisation of the moving sums

The first two moments of are and Define

| (2.1) |

which are the standardized versions of . All r.v. are ; that is, they have the probability density function and c.d.f.

| (2.2) |

Unlike the original r.v. , the r.v. are correlated so that for all we have and

| (2.5) |

Proof of (2.5) is straightforward, see (AandZ2019, , Lemma 1).

Set and

| (2.6) |

Define the BCP for the sequence of r.v. :

| (2.7) |

From (2.1) and (2.6), the BCPs and are equal:

Note also that , where

| (2.8) |

In accordance with the terminology of Shepp71 and slepian1961first we shall call ‘first-passage probability’. In the following sections, we derive approximations for (2.7). These approximations will be based on approximating the sequence of r.v. by a continuous-time random process and subsequently correcting the obtained approximations for discreteness. Before doing this, we formulate the approximation which is currently the state-of-the-art.

2.2 Glaz approximation for

The approximation for the BCP developed in Glaz_old ; Glaz2012 ; wang2014variable ; wang2014multiple and discussed in the introduction is as follows.

Approximation 1. (Glaz approximation) For ,

| (2.9) |

where to approximate the first-passage probabilities and , which are

and dimensional integrals respectively, it is advised to use the so-called ‘GenzBretz’ algorithm for numerical evaluation of multivariate normal probabilities; see genz2009computation ; GenzR .

Unless is large (say, ), Approximation 1 is very accurate. However, its computational cost is also high, especially for large . Moreover, the main option in the ‘GenzBretz’ package requires the use of Monte-Carlo simulations so that for reliable estimation of high-dimensional integrals one needs to make a lot of averaging; see Section 6.1 and 7 for more discussion on these issues.

2.3 Continuous-time (diffusion) approximation

For the purpose of approximating the BCP , we replace the discrete-time process with a continuous process , , where (we will then correct the corresponding first-passage probabilities for discreteness). We do this as follows.

Set and define Define a piece-wise linear continuous-time process

By construction, the process is such that . Also we have that is a second-order stationary process in the sense that and the autocorrelation function do not depend on .

Lemma 1

Assume . The limiting process = , where , is a Gaussian second-order stationary process with marginal distribution for all and autocorrelation function .

This lemma is a simple consequence of (2.5).

2.4 Diffusion approximations: definition and their role in this study

The above approximation of a discrete-time process with a continuous process , allows us to approximate the BCP by a continuous-time analogue as follows.

By the definition of a diffusion approximation, the BCP is approximated by

| (2.10) |

Note that approximating the discrete process of moving sums by a continuous-time process and subsequent approximation of the BCP by is by no means new. This has been done, in particular, in Haiman .

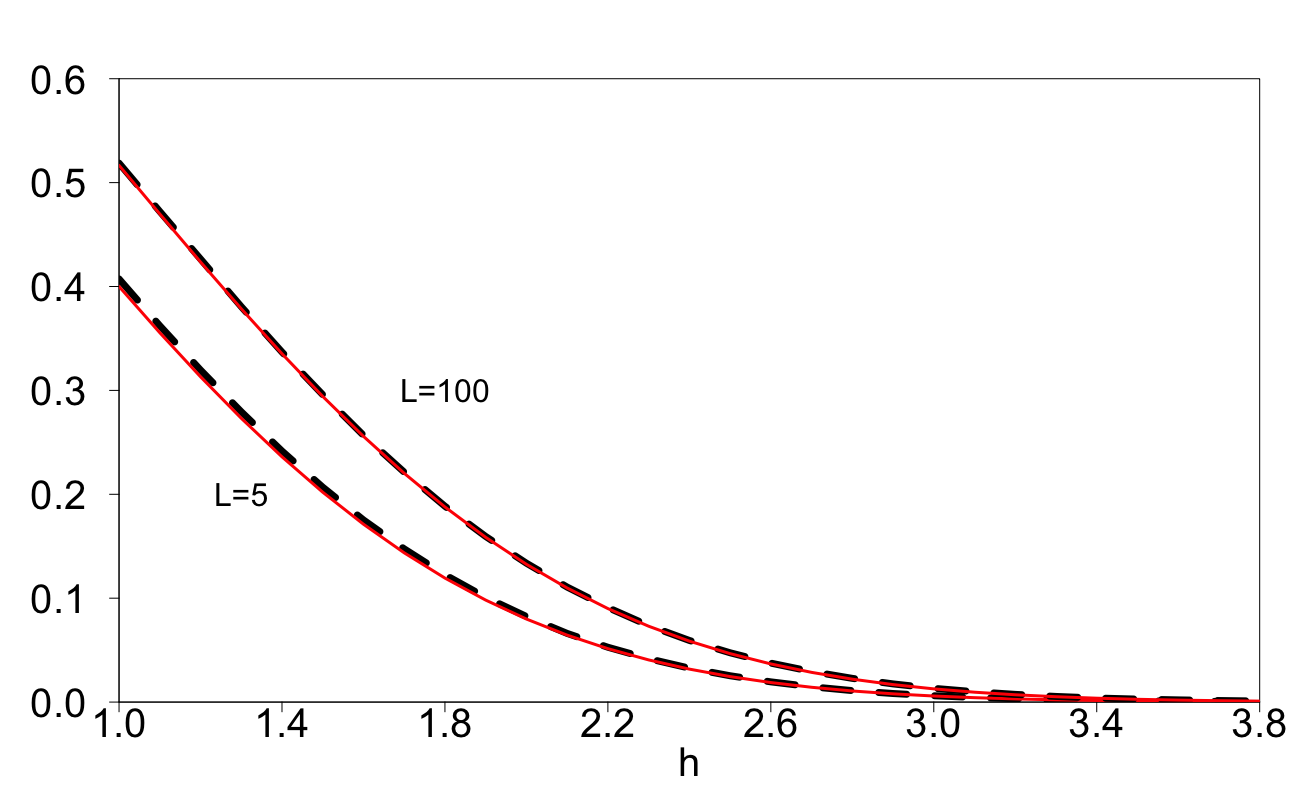

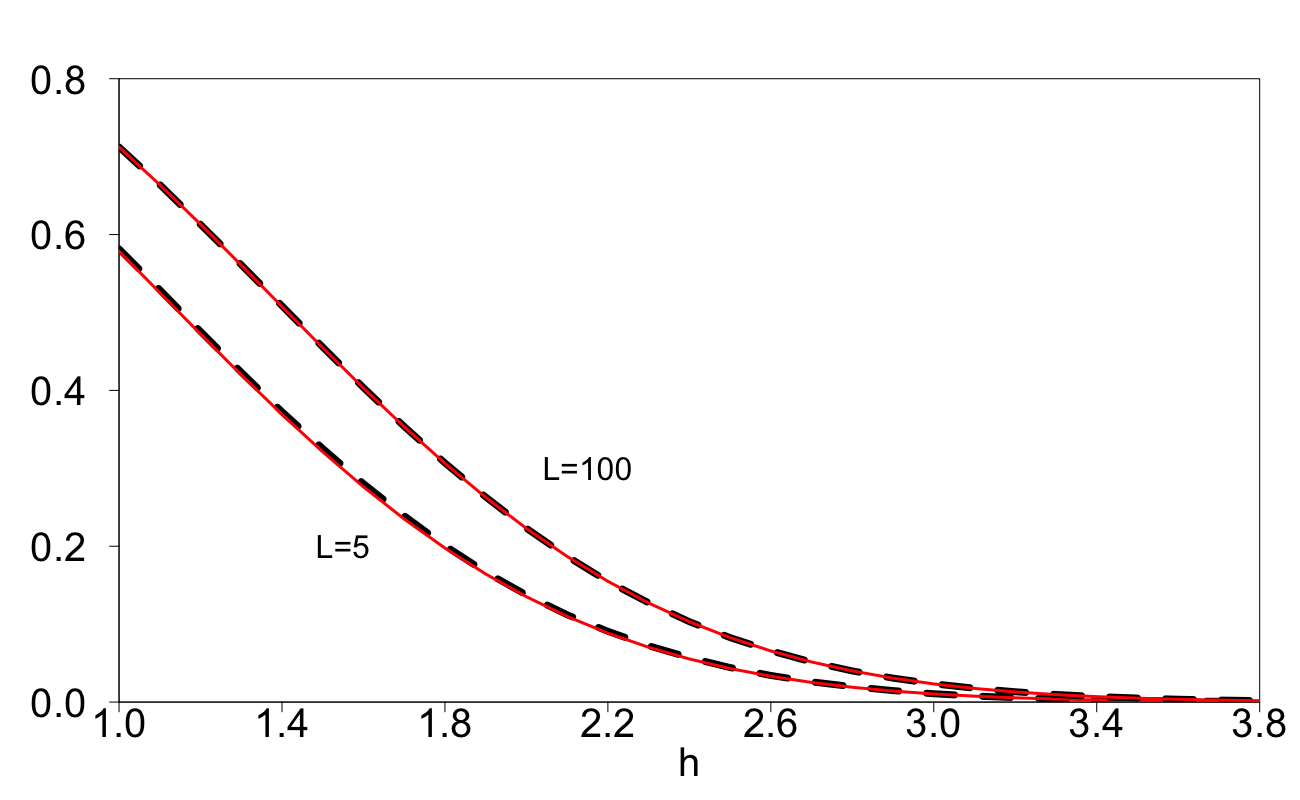

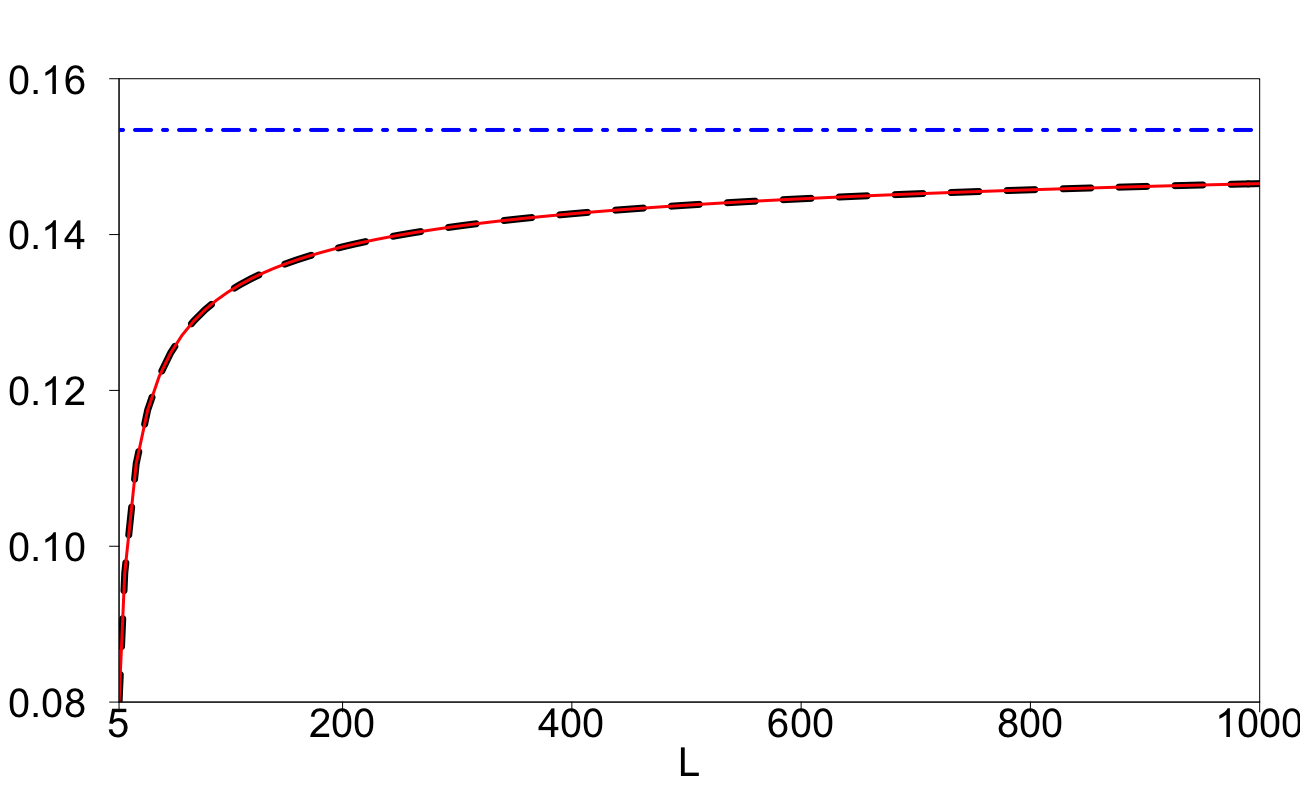

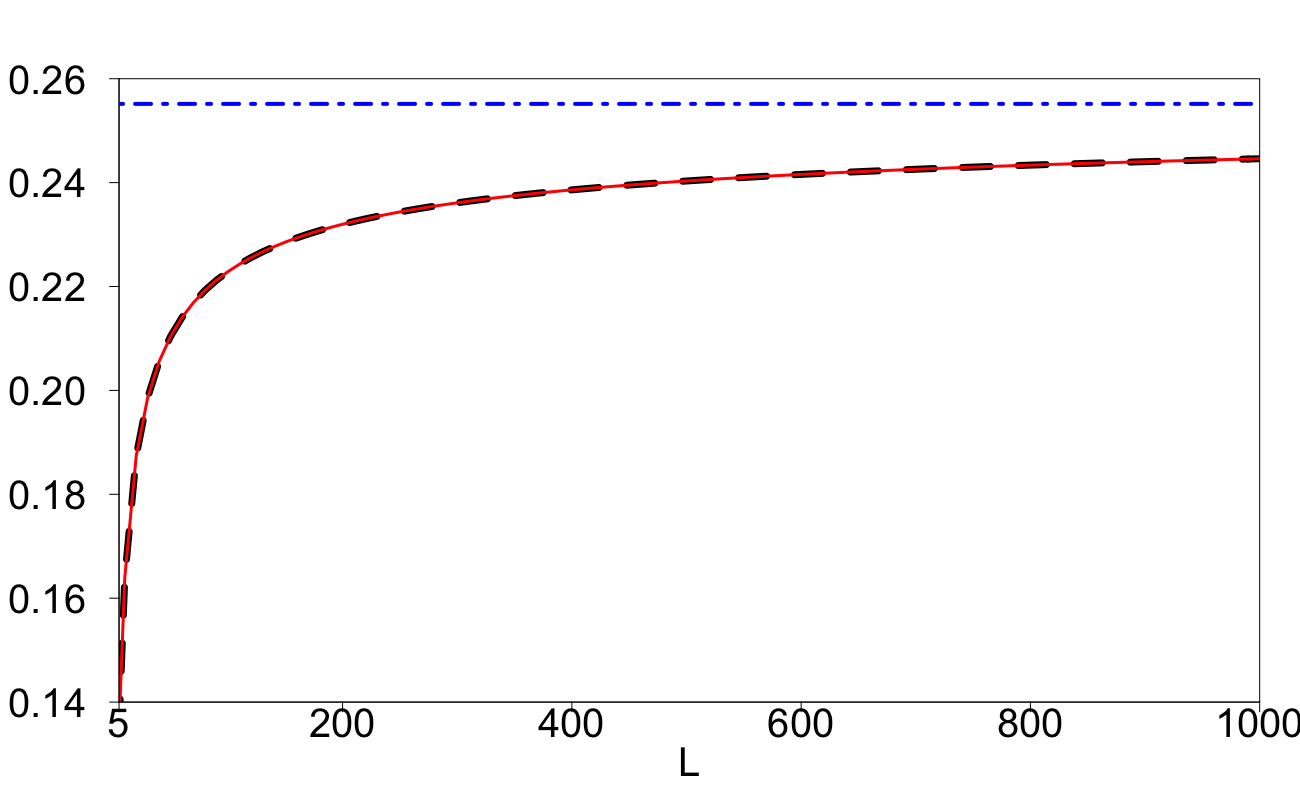

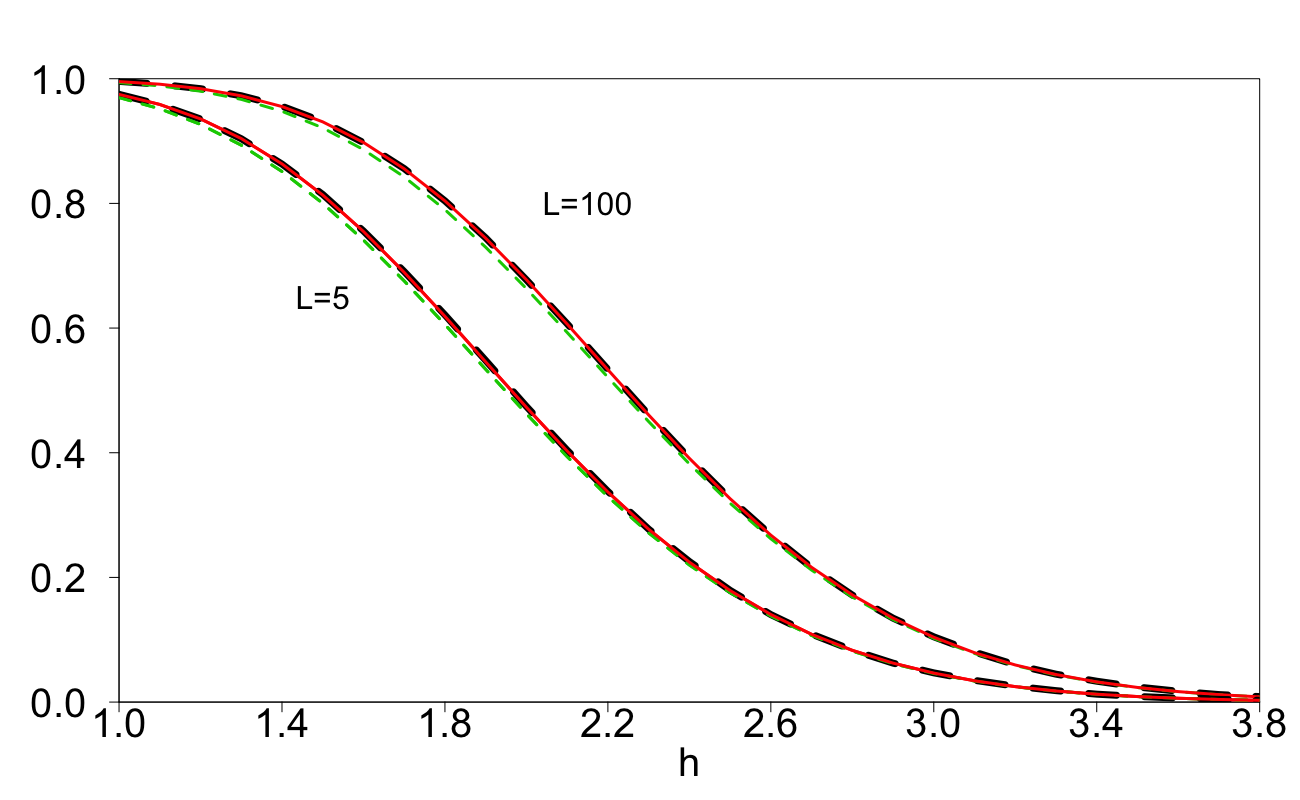

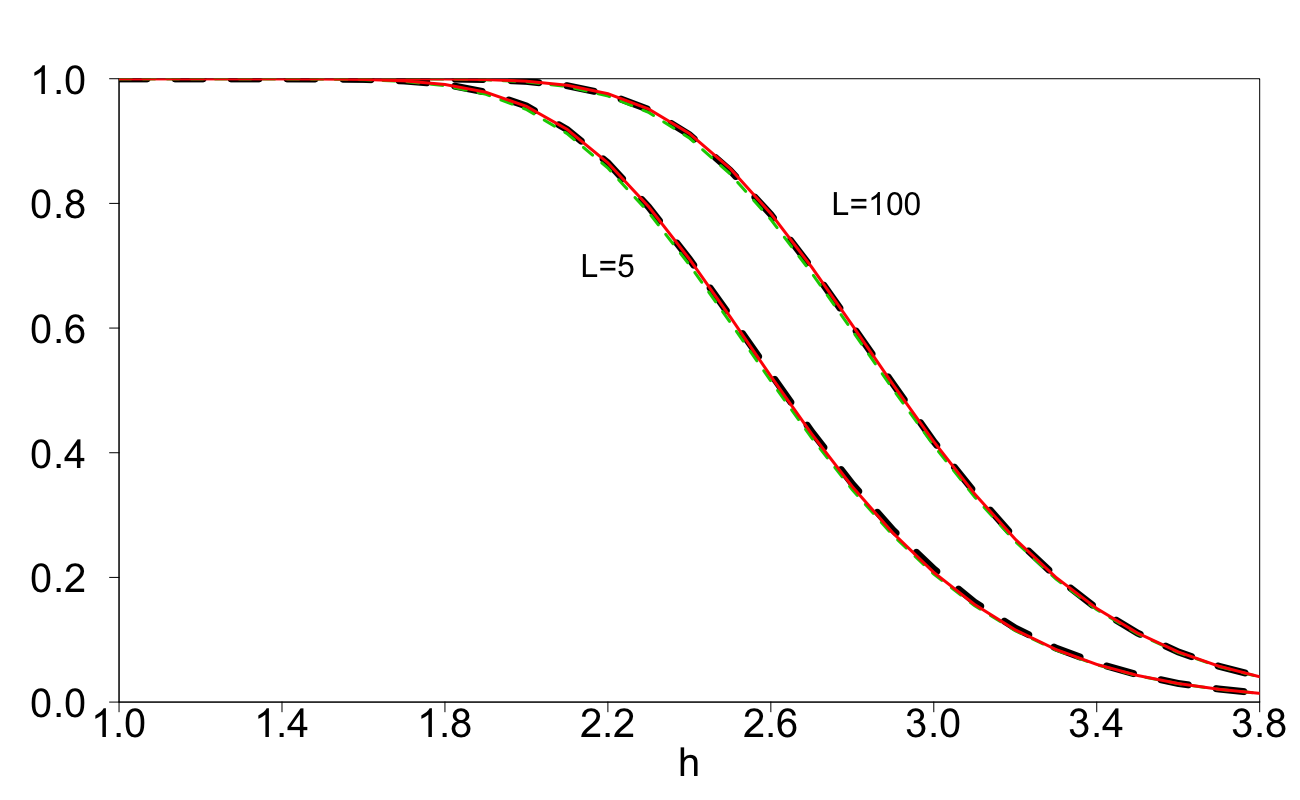

We will call (2.10) and any approximation to (2.10), which does not involve the knowledge of , ‘diffusion approximation’. These approximations can be greatly improved with the help of the methodology developed by D.Siegmund and adapted to our setup in Section 4. The importance of the discrete-time correction is illustrated by Figures 1 and 2, where for a fixed and we can see a significant difference in values of the BCPs for different values of . As seen from Figure 2, even for very large , the discrete-time correction is still needed. Hence we are not recommending to use any approximation for (including rather sophisticated ones like the one developed in Haiman ) as an approximation for . In the next section we will discuss a diffusion approximation that, after correcting for discrete time, will be a cornerstone for all approximations developed in this paper.

In what follows, it will also be convenient to use the first-passage probability

Since , we have .

3 Exact formulas for the first-passage probabilities in the continuous-time case

3.1 Shepp’s formulas

Define the conditional first-passage probability

| (3.1) |

Since for , for the unconditional first-passage probability we have .

3.2 An alternative representation of the Shepp’s formula (3.2)

3.3 Joint density for the values and associated transition densities

From (3.5), we obtain the following expression for the joint probability density function for the values under the condition for all :

| (3.7) |

From this formula, we can derive the transition density from to conditionally :

| (3.8) |

For this transition density, . Moreover, since , the non-normalized density of under the condition for all is

| (3.9) |

with and . In the case , (3.8) gives

| (3.10) |

From this and (3.9) we get

with and .

4 Correcting Shepp’s formula (3.2) for discrete time

4.1 Rewriting (3.2) in terms of the Brownian motion

Let be the standard Brownian Motion process on with and Recall the conditional probability defined in (3.1). Suppose is an integer and define the event

If , , we obtain from (Shepp71, , p.948)

It follows from the proof of (3.2) that to correct (4.1) for discrete time, one must correct the following probability for discrete time

| (4.2) | |||||

where , . Due to the conditioning on the rhs of (4.2), the processes can be treated as independent Brownian motion processes. Therefore, the independent increments of the Brownian motion means correcting formula (3.2) for discrete time is equivalent to correcting the probability for discrete time.

4.2 Discrete-time correction for the BCP of cumulative sums.

Let be i.i.d. r.v’s and set . Consider the sequence of cumulative sums and define the stopping time for and . Consider the problem of evaluating

| (4.3) |

Exact evaluation of (4.3) is difficult even if is not very large but it was accurately approximated by D.Siegmund see e.g. (Sieg_paper, , p.19). Let be the standard Brownian Motion process on . For and , define so that

| (4.4) |

In Sieg_paper , (4.4) was used to approximate (4.3) after translating the barrier by a suitable scalar . Specifically, the following approximation has been constructed:

where the constant approximates the expected excess of the process over the barrier . From (Sieg_book, , p. 225)

| (4.5) |

4.3 Discretised Brownian motion

Define = and let Let be i.i.d. r.v’s and set For define the stopping time

| (4.6) |

and consider the problem of approximating

| (4.7) |

As , the piecewise linear continuous-time process , , defined by:

converges to on as so we can refer to as discretised Brownian motion. We make the following connection between and the random walk :

Then by using (4.5), we approximate the expected excess over the boundary for the process by

We have deliberately rounded the value to as for small and small it provides marginally better approximation (4.9).

4.4 Corrected version of (3.2)

Set . To correct (3.2) for discrete time we substitute the barrier with . From this and the relation , the discrete-time corrected form of is

where and

4.5 A generic approximation involving corrected Shepp’s formula

Approximation 2. For integral , the discrete-time correction for the BCP (2.7) is

| (4.9) |

where is given in (4.4).

Whilst Approximation 2 is very accurate (see the next subsection), computation of requires numerical evaluation of a dimensional integral which is impractical for large . To overcome this, in Section 5.2 we develop approximations that can be easily used for any (which is not necessarily integer).

4.6 Particular cases: and

For , evaluation of (4.4) yields

| (4.10) |

In our previous work AandZ2019 we have derived approximations for the BCP with . The approximations developed in AandZ2019 are also discrete-time corrections of the continuous-time probabilities but they are based almost exclusively on the fact that the process is conditionally Markov on the interval ; hence the technique of AandZ2019 cannot be extended for intervals with . The approximation of AandZ2019 is different from of (4.10). It appears that is more complicated and less accurate approximation than .

For , (4.4) can be expressed (after some manipulations) as follows:

| (4.11) | |||||

Only a one-dimensional integral has to be numerically evaluated for computing .

4.7 Simulation study

In this section, we assess the quality of the approximations (4.10) and (4.11) as well as the sensitivity of the BCP to the value of . In Figures 1 and 2, the black dashed line corresponds to the empirical values of the BCP (for ) computed from 100 000 simulations with different values of and (for given and , we simulate normal random variables 100 000 times). The solid red line corresponds to Approximation 2. The axis are: the -axis shows the value of the barrier in Figure 1 and value of in Figure 2; the -axis denotes the probabilities of reaching the barrier. The graphs, therefore, show the empirical probabilities of reaching the barrier (for the dashed line) and values of considered approximations for these probabilities. From these graphs we can conclude that Approximation 2 is very accurate, at least for . We can also conclude that the BCP is very sensitive to the value of . From Figure 2 we can observe a counter-intuitive fact that even for very high value , the BCP is not even close to from (2.10). This may be explained by the fact that for any fixed and , the inaccuracy decreases with the rate const as .

4.8 The Glaz-Shepp-Siegmund approximation

5 Approximations for the BCP through eigenvalues of integral operators

5.1 Continuous time: approximations for

Let be a positive integer, and be the transition density defined by (3.10) for (3.15) for and (3.11) for .

Let us approximate the distributions of the values for integral in the following way. Let be the density of under the condition that does not reach for . By ignoring the past values of in , the non-normalized density of under the conditions that and does not reach for is

| (5.1) |

We can then define where . We then replace formula (5.1) with

| (5.2) |

where is an eigenfunction of the integral operator with kernel (3.10) corresponding to the maximum eigenvalue :

| (5.3) |

This eigenfunction is a probability density on with for all and Moreover, the maximum eigenvalue of the operator with kernel is simple and positive. The fact that such maximum eigenvalue is simple and real (and hence positive) and the eigenfunction can be chosen as a probability density follows from the Ruelle-Krasnoselskii-Perron-Frobenius theory of bounded linear positive operators, see e.g. Theorem XIII.43 in ReedSimon .

Using (5.2) and (5.3), we derive recursively: (). By induction, for any integer we then have

| (5.4) |

The approximation (5.4) can be used for any which is not necessarily an integer. The most important particular cases of (5.4) are with and . In these two cases, the kernel and hence the approximation (5.4) will be corrected for discrete time in the next section.

5.2 Correcting approximation (5.4) for discrete time

To correct the approximation (5.4) for discrete time we need to correct: (a) the first-passage probability and (b) the kernel . The discrete-time correction of can be done using from (4.4) so that what is left is to correct the kernel and hence .

5.2.1 Correcting the transition kernels for discrete time

As explained in Section 4, to make a discrete-time correction in the Shepp’s formula (3.2) we need to replace the barrier with in all places except for the upper bound for the initial value . Therefore, using the notation of Section 3.2, the joint probability density function for the values under the condition for all corrected for discrete time is:

| (5.5) |

with , ,

This gives us the discrete-time corrected transition density from to conditionally :

| (5.7) |

which is exactly (3.8) with is substituted for . In a particular case , the corrected transition density is

| (5.10) |

with .

Let us now make the discrete-time correction of the transition density . Denote by , the non-normalized density of under the condition for all corrected for discrete time; it satisfies . Using (5.10), we obtain

From (5.5) and (5.10), the transition density from to under the condition for all corrected for discrete time (the corrected form of (3.15)) is given by

| (5.14) | |||||

| (5.18) |

Unlike the transition density (5.7) (and (5.10) in the particular case ), which only depends on and not on , the transition density depends on both and and hence the notation. The dependence on has appeared from integration over the .

5.2.2 Approximations for the BCP

With discrete-time corrected transition densities and , we obtain the corrected versions of the approximations (5.4).

Approximation 4:

where is given in (4.10) and

is the maximal eigenvalue of the integral operator with kernel defined in (5.10).

Approximation 5:

where is given in (4.11) and

is the maximal eigenvalue of the integral operator with kernel defined in (5.14).

Similarly to from (5.3), the maximum eigenvalues and of the operators with kernels and are simple and positive; the corresponding eigenfunctions can be chosen as probability densities. Both approximations can be used for any .

In numerical examples below we approximate the eigenvalues () using the methodology described in Quadrature , p.154. This methodology is based on the Gauss-Legendre discretization of the interval , with some large , into an -point set (the ’s are the roots of the -th Legendre polynomial on ), and the use of the Gauss-Legendre weights associated with points ; and are then approximated by the largest eigenvalue and associated eigenvector of the matrix where and with the respective kernel . If is large enough then the resulting approximation to is arbitrarily accurate. With modern software, computing Approximations 4 and 5 (as well as Approximation 3) with high accuracy takes only milliseconds on a regular laptop.

As discussed in the next section, Approximation 5 is more accurate than Approximation 4, especially for small ; the accuracies of Approximations 3 and 5 are very similar. Note also that a version of Approximation 4 has been developed in our previous work AandZ2019 ; this version was based on a different discrete-time approximation (discussed in Section 4.6) of the continuous-time BCP probability .

6 Simulation study

6.1 Accuracy of approximations for the BCP

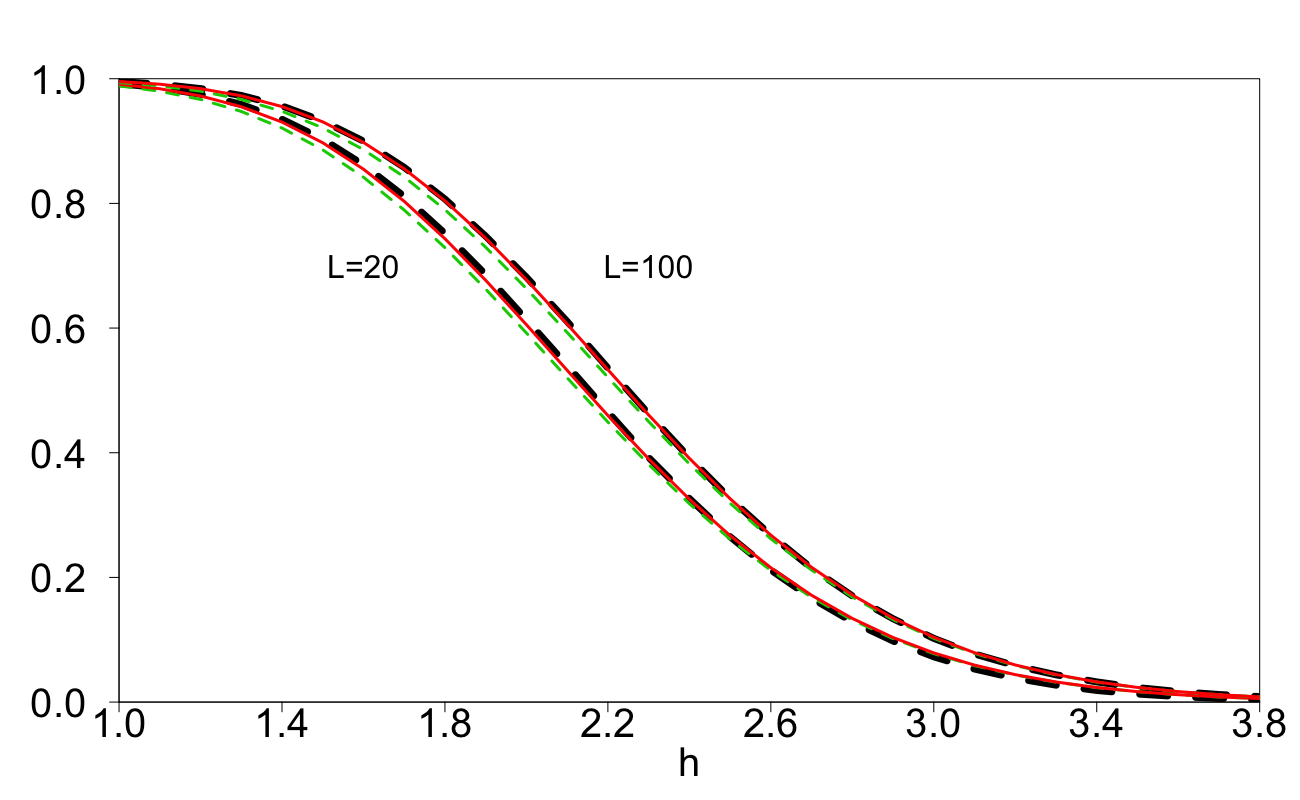

In this section we study the quality of Approximations 4 and 5 for the BCP defined in (2.7). Approximation 3 is visually indistinguishable from Approximation 5 and is therefore not plotted (see Table 1). Without loss of generality, in (1.1) are normal r.v.’s with mean and variance . The style of Fig. 3 is exactly the same as of Fig. 1 and is described in the beginning of Section 4.7. In Fig. 3, the dashed green line corresponds to Approximation 4 and the solid red line corresponds to Approximation 5.

From Figure 3 we see that the performance of Approximations 4 and 5 is very strong even for small . For small , Approximation 5 is more precise than Approximation 4 in view of its better accommodation to the non-Markovian nature of the process .

| =0 | =0.5 | =1 | =1.5 | =2 | =2.5 | =3 | =3.5 | =4 | |

|---|---|---|---|---|---|---|---|---|---|

| | 0.28494 | 0.46443 | 0.65331 | 0.81186 | 0.91687 | 0.97090 | 0.99209 | 0.99835 | 0.99974 |

| | 0.25744 | 0.43811 | 0.63472 | 0.80239 | 0.91348 | 0.97005 | 0.99195 | 0.99833 | 0.99974 |

| | 0.25527 | 0.43677 | 0.63432 | 0.80241 | 0.91353 | 0.97007 | 0.99195 | 0.99833 | 0.99974 |

In Table 1, we display the values of , and with for a number of different . From this table, we see only a small difference between and ; this difference is too small to visually differentiate between Approximations 3 and 5 in Fig. 3.

In Tables 2, 3 and 4 we numerically compare the performance of Approximations 1 and 3 for approximating across different values of and . Since Approximation 1 relies on Monte-Carlo methods, we present the average over 100 evaluations and denote this by . We have also provided values for the standard deviation and maximum and minimum of the 100 runs to illustrate the randomised nature of this approximation. These are denoted by , and respectively. The values of presented in the tables below are the empirical probabilities of reaching the barrier obtained by simulations. We have not included Approximation 5 in these tables as results are identical to Approximation 3 up to four decimal places.

| =2.5 | =2.75 | =3 | =3.25 | =3.5 | =3.75 | =4 | |

|---|---|---|---|---|---|---|---|

| | 0.855957 | 0.627299 | 0.376337 | 0.191122 | 0.086253 | 0.033769 | 0.013156 |

| | 0.004127 | 0.008588 | 0.013805 | 0.015181 | 0.012826 | 0.008510 | 0.005131 |

| | 0.010665 | 0.023748 | 0.029819 | 0.027066 | 0.025629 | 0.016208 | 0.011609 |

| | 0.012176 | 0.021268 | 0.033211 | 0.041322 | 0.041350 | 0.022650 | 0.018146 |

| Approximation 3 | 0.854844 | 0.625113 | 0.373863 | 0.188933 | 0.083981 | 0.033833 | 0.012551 |

| | 0.855429 | 0.627463 | 0.376681 | 0.191625 | 0.085697 | 0.034675 | 0.013116 |

| =2.5 | =2.75 | =3 | =3.25 | =3.5 | =3.75 | =4 | |

|---|---|---|---|---|---|---|---|

| | 0.952007 | 0.802073 | 0.554613 | 0.315085 | 0.155331 | 0.066113 | 0.025608 |

| | 0.001479 | 0.004856 | 0.012540 | 0.015050 | 0.015160 | 0.011647 | 0.008129 |

| | 0.004746 | 0.013360 | 0.027078 | 0.030940 | 0.033991 | 0.024111 | 0.030014 |

| | 0.003662 | 0.010894 | 0.031463 | 0.037715 | 0.041021 | 0.043283 | 0.016997 |

| Approximation 3 | 0.952475 | 0.802100 | 0.555109 | 0.316076 | 0.153803 | 0.066438 | 0.026143 |

| | 0.952818 | 0.803078 | 0.555530 | 0.315784 | 0.153446 | 0.066642 | 0.026244 |

| =2.5 | =2.75 | =3 | =3.25 | =3.5 | =3.75 | =4 | |

|---|---|---|---|---|---|---|---|

| | 0.979027 | 0.878031 | 0.661247 | 0.402887 | 0.211894 | 0.093329 | 0.039110 |

| | 0.000884 | 0.005502 | 0.014418 | 0.021283 | 0.018493 | 0.020459 | 0.015536 |

| | 0.001995 | 0.009243 | 0.039695 | 0.040615 | 0.063578 | 0.064306 | 0.037958 |

| | 0.002414 | 0.020613 | 0.025530 | 0.093876 | 0.038484 | 0.05694 | 0.033748 |

| Approximation 3 | 0.979119 | 0.878481 | 0.660662 | 0.405674 | 0.209313 | 0.094517 | 0.038529 |

From Tables 2, 3 and 4 we see that with this choice of , the errors of approximating and via the ’GenzBretz’ algorithm can accumulate and lead to a fairly significant variation of Approximation 1. This demonstrates the need to average the outcomes of Approximation 1 over a significant number of runs, should one desire an accurate approximation. This may require rather high computational cost and run time, especially if is large. On the other hand, evaluation of Approximation 3 is practically instantaneous for all . Even for a very small choice of , Table 2 shows that Approximation 3 still remains very accurate. As increases from 5 to , Table 3 shows that the accuracy of Approximation 3 increases. The averaged Approximation 1 is also very accurate but a larger appears to produce a larger range for and when is large; this is seen in Table 4. Note we have not included empirical values of in Table 4 due to the large computational cost.

6.2 Approximation for the BCP in the case of non-normal moving sums

Approximations 3, 4 and 5 remain very accurate when then the original in (1.1) are not exactly normal. We consider two cases: (a) are uniform r.v’s on [0,1] and (b) are Laplace r.v’s with mean zero and scale parameter 1. Simulation results are shown in Figure 4; this figure has the same style as figures in Sections 4.7 and 6.1.

Some selected values used for plots in Figure 4 are:

Emp: Ap. 4(5): 0.5921(0.6054);

Emp: Ap. 4(5): 0.6633(0.6775);

Emp: Ap. 4(5): 0.0777(0.0789);

Emp: Ap. 4(5): 0.1022(0.1034).

Here we provided means and 95% confidence intervals for the empirical (Emp) values of the BCP (with ) computed from 100 000 Monte-Carlo runs of the sequences of the moving sums (1.1) with normal (no brackets), uniform (regular brackets) and Laplace (square brackets) distributions for in (1.1). Values of Approximations (Ap.) 4 and 5 are also given.

From Figure 4 and associated numbers we can make the following conclusions: (a) the BCP for the case where in (1.1) are uniform is closer to the case where are normal, than for the case where have Laplace distribution; (b) as increases, the probabilities in the cases of uniform and Laplace distributions of become closer to the BCP for the case of normal and hence the approximations to the BCP become more precise; (c) accuracy of Approximation 5 is excellent for the case of normal and remains very good in the case of uniform ; it is also rather good in the case when have Laplace distribution; (d) Approximation 4 is slightly less accurate than Approximation 5 (and Approximation 3) for the case of normal and uniform (this is in a full agreement with discussions in Sections 5.2.2 and 6.1); however, Approximation 4 is very simple and can still be considered as rather accurate.

6.3 Approximation for the BCP in the case of moving weighted sums

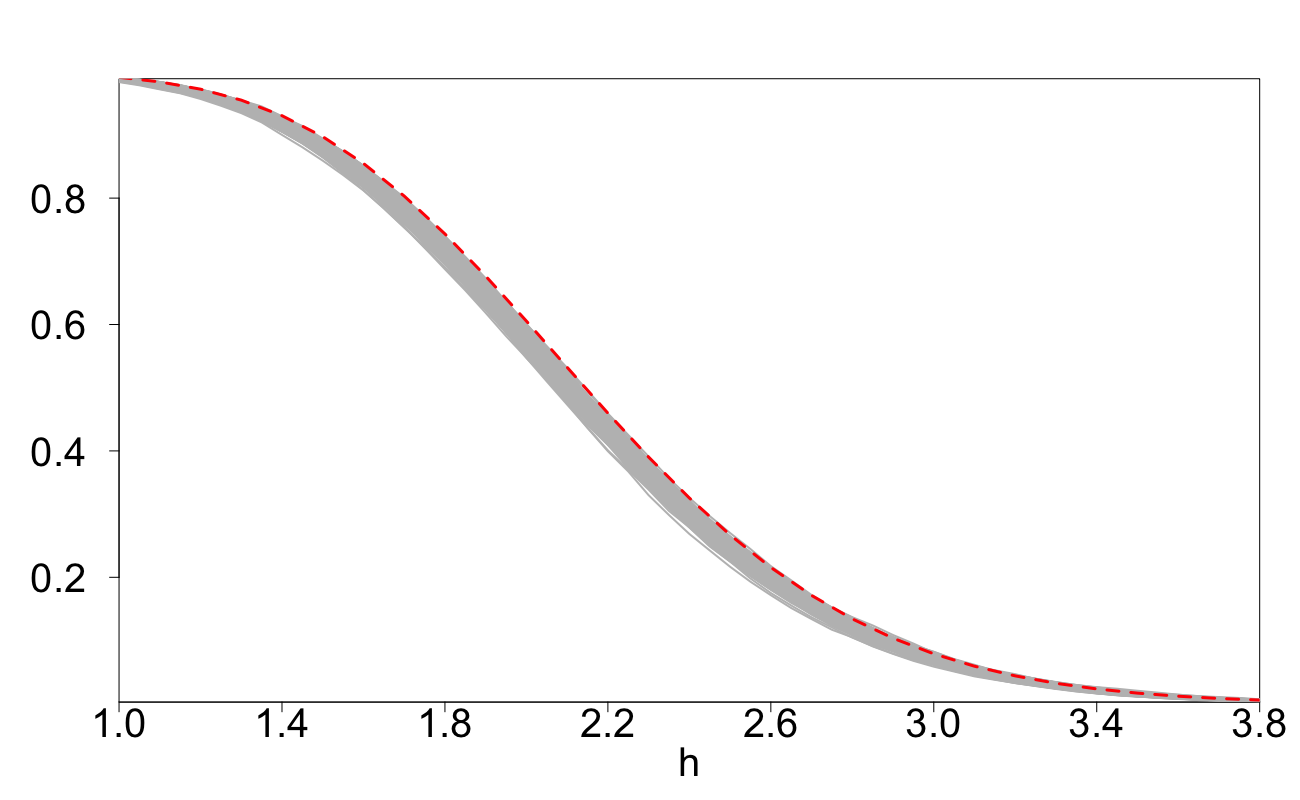

We have also investigated the performance of Approximation 5 (and 3) after introducing particular weights into (1.1). We explored the following two ways of incorporating weights:

-

(i)

random weights , with i.i.d. uniform on , are associated with a position in the moving window; this results in the moving weighted sum

-

(ii)

random weights are associated with r.v. ; here are i.i.d. uniform r.v’s on [0,2]; this gives the moving weighted sum

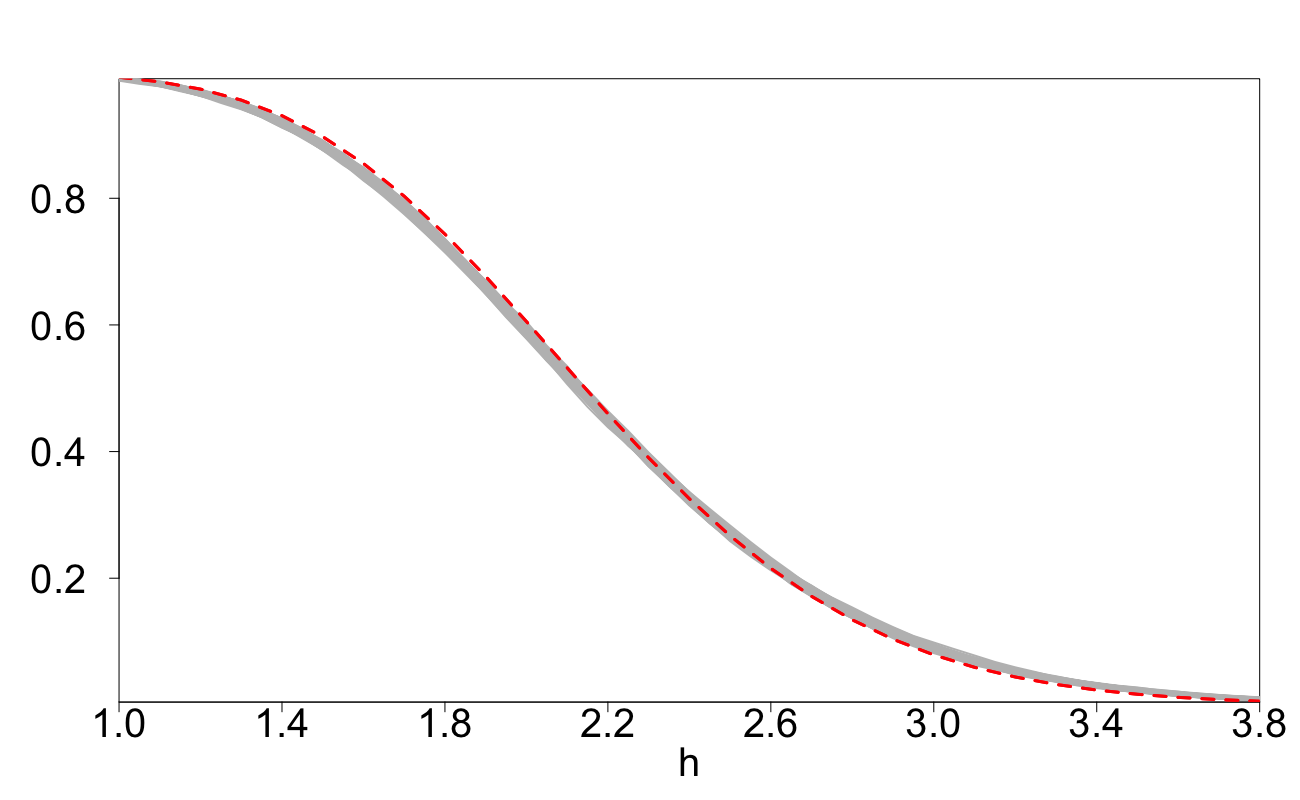

Simulations results are shown in Fig. 5. In both cases, we have repeated simulations 1,000 times and plotted all the curves representing the BCP as functions of in grey colour and Approximation 5 for the BCP for the non-weighted case (when all weights ) as red dashed line. We can see that for both scenarios the Approximation 5 for the BCP in the non-weighted case gives fairly accurate approximation for the weighted BCP. Similar results have been observed for other values of and .

7 Approximating Average Run Length (ARL)

In this section, we provide approximations to the probability distribution of the moment of time when the sequence reaches the threshold for the first time. Note that , where and . The BCP , considered as a function of , is the c.d.f. of this probability distribution: . The average run length (ARL) until reaches for the first time is

| (7.1) |

Note that . The diffusion approximation to the time moment is , which is the time moment when the process reaches . The distribution of has the form:

where is the delta-measure concentrated at 0 and

| (7.2) |

The function , considered as a function of , is a probability density function on since

From this, the diffusion approximation for is

| (7.3) |

The diffusion approximation (7.3) should be corrected for discrete time; otherwise it is poor, especially for small . As shown in Section 6, Approximations 3 and 5 are very accurate approximations for and can be used for all . We shall use Approximation 3 to formulate our approximations but note that the use of Approximation 5 would give very similar results.

We define the approximation for the probability density function of by

The corresponding approximation for is

| (7.4) |

The standard deviation of , denoted , is approximated by:

| (7.5) |

In this paper, we define ARL in terms of the number of random variables rather than number of random variables . This means we have to modify the approximation for ARL of Glaz2012 by subtracting . The standard deviation approximation in Glaz2012 is not altered.

The Glaz approximations for and are as follows:

| (7.6) |

| (7.7) | |||||

where .

In Tables 5 and 6 we assess the accuracy of the approximations (7.4) and (7.5) and also Glaz approximations (7.6) and (7.7). In these tables, the values of and have been calculated using simulations. Since the Glaz approximations rely on Monte Carlo methods, in the tables we have reported value -confidence intervals computed from 150 evaluations.

Tables 5 and 6 show that the approximations developed in this paper perform strongly and are similar, for small or moderate , to the Glaz approximations. For , the Glaz approximation produces rather large uncertainty intervals and the uncertainty quickly deteriorates with the increase of . This is due to the fairly large uncertainty intervals formed by Approximation 1 when approximating with large and hence small , as discussed in Section 6.1. The approximations developed in this paper are deterministic and are much simpler in comparison to the Glaz approximations. Moreover, they do not deteriorate for large .

Acknowledgment

The authors are grateful to the referees for careful reading of the manuscript and useful comments.

References

- (1) Bauer, P., Hackl, P.: An extension of the MOSUM technique for quality control. Technometrics 22(1), 1–7 (1980)

- (2) Chu, C.S.J., Hornik, K., Kaun, C.M.: MOSUM tests for parameter constancy. Biometrika 82(3), 603–617 (1995)

- (3) Eiauer, P., Hackl, P.: The use of MOSUMS for quality control. Technometrics 20(4), 431–436 (1978)

- (4) Genz, A., Bretz, F.: Computation of Multivariate Normal and t Probabilities. Lecture Notes in Statistics. Springer-Verlag, Heidelberg (2009)

- (5) Genz, A., Bretz, F., Miwa, T., Mi, X., Leisch, F., Scheipl, F., Hothorn, T.: mvtnorm: Multivariate Normal and t Distributions (2018). URL https://CRAN.R-project.org/package=mvtnorm. R package version 1.0-8: ‘https://CRAN.R-project.org/package=mvtnorm’

- (6) Glaz, J., Johnson, B.: Boundary crossing for moving sums. Journal of Applied Probability 25(1), 81–88 (1988)

- (7) Glaz, J., Naus, J., Wang, X.: Approximations and inequalities for moving sums. Methodology and Computing in Applied Probability 14(3), 597–616 (2012)

- (8) Glaz, J., Naus, J.I.: Tight bounds and approximations for scan statistic probabilities for discrete data. The Annals of Applied Probability 1(2), 306–318 (1991)

- (9) Glaz, J., Naus, J.I., Wallenstein, S., Wallenstein, S., Naus, J.I.: Scan statistics. Springer (2001)

- (10) Glaz, J., Pozdnyakov, V., Wallenstein, S.: Scan Statistics: Methods and Applications. Birkhäuser, Boston (2009)

- (11) Haiman, G.: First passage time for some stationary processes. Stochastic Processes and their Applications 80(2), 231–248 (1999)

- (12) Mohamed, J., Delves, L.: Computational Methods for Integral Equations. Cambridge University Press (1985)

- (13) Moskvina, V., Zhigljavsky, A.: An algorithm based on Singular Spectrum Analysis for change-point detection. Communications in Statistics—Simulation and Computation 32(2), 319–352 (2003)

- (14) Noonan, J., Zhigljavsky, A.: Approximations for the boundary crossing probabilities of moving sums of normal random variables. Communications in Statistics-Simulation and Computation, 1–22 (2019)

- (15) Reed, M., Simon, B.: Methods of Modern Mathematical Physics: Scattering theory Vol. 3. Academic Press (1979)

- (16) Shepp, L.: First passage time for a particular Gaussian process. The Annals of Mathematical Statistics 42(3), 946–951 (1971)

- (17) Siegmund, D.: Sequential Analysis: Tests and Confidence Intervals. Springer Science & Business Media (1985)

- (18) Siegmund, D.: Boundary crossing probabilities and statistical applications. The Annals of Statistics 14(2), 361–404 (1986)

- (19) Slepian, D.: First passage time for a particular Gaussian process. The Annals of Mathematical Statistics 32(2), 610–612 (1961)

- (20) Waldmann, K.H.: Bounds to the distribution of the run length in general quality-control schemes. Statistische Hefte 27(1), 37 (1986)

- (21) Wang, X., Glaz, J.: Variable window scan statistics for normal data. Communications in Statistics-Theory and Methods 43(10-12), 2489–2504 (2014)

- (22) Wang, X., Zhao, B., Glaz, J.: A multiple window scan statistic for time series models. Statistics & Probability Letters 94, 196–203 (2014)

- (23) Xia, Z., Guo, P., Zhao, W.: Monitoring structural changes in generalized linear models. Communications in Statistics—Theory and Methods 38(11), 1927–1947 (2009)