A Dimension-free Algorithm for Contextual Continuum-armed Bandits

Abstract

In contextual continuum-armed bandits, the contexts and the arms are both continuous and drawn from high-dimensional spaces. The payoff function to learn does not have a particular parametric form. The literature has shown that for Lipschitz-continuous functions, the optimal regret is , where and are the dimensions of contexts and arms, and thus suffers from the curse of dimensionality. We develop an algorithm that achieves regret when is globally concave in . The global concavity is a common assumption in many applications. The algorithm is based on stochastic approximation and estimates the gradient information in an online fashion. Furthermore, we generalize our algorithm to an adaptive scheme that takes advantage of sequentially arrived context without sacrificing the worst-case performance. Our results generate a valuable insight that the curse of dimensionality of the arms can be overcome with some mild structures of the payoff function.

1 Introduction

The multi-armed bandits (MAB) deal with a class of sequential decision making problems (Lai and Robbins, 1985; Auer et al., 2002a; Bubeck et al., 2012). Without knowing the payoff of each decision, the decision maker chooses a decision from a set of alternatives (arms) in each epoch based on the past history. The observed random payoff associated with the chosen decision can be used to learn in future epochs. The goal is to maximize the total payoff over a finite horizon. The MAB setting has been introduced in Robbins (1952) and studied intensively since then in statistics, computer sciences, operations research, and economics.

Recently, the contextual bandits problems have received attentions of many scholars. Before making decision in each epoch, the decision maker receives a context that can be used to infer the payoff and suggest which arm to pull. Contextual bandits are motivated by advertisement placement on webpages. Upon observing the user profile (context), the firm needs to decide which advertisement to place (arm) that may interest the user. The number of clicks is the payoff to maximize.

In this paper, we consider contextual continuum-armed bandits. Compared to the classic MAB setting, both decision and context are drawn from continuous spaces in our problem. This is motivated by personalized pricing in operations research and marketing. A firm sells multiple products over a finite selling season via dynamically adjusted prices. For each coming customer, the firm observes her profile such as education background, zip code, age and purchasing history. Then the firm decides a personalized price vector for the customer. The total payoff is the revenue extracted from a finite number of customers. The continuous nature and high dimensionality of the customer profile and pricing motivate the contextual continuum-armed bandit problem.

Prior Work. There is a body of literature on continuum-armed bandits (Agrawal, 1995; Pandey et al., 2007; Kleinberg and Slivkins, 2010; Maillard and Munos, 2010). Kleinberg (2005) studies the case that the mean payoff function satisfies a Hölder continuous property with constant . This work proves a worst-case lower bound for the regret of any algorithm when the arms set is one dimensional and proposes a uniform discretization algorithm achieving a regret of order , nearly tight with the lower bound. Auer et al. (2007) also study the one-dimensional arm set. Under the condition that payoff functions have finitely many maxima and a non-vanishing, continuous second-order derivative at all maxima, their algorithm achieves the regret order . Kleinberg et al. (2008) consider the multi-dimensional case and generalize the Lipschitz bandit problem to metric space. They present an algorithm obtaining the regret where is the covering dimension of arm space, kindly capturing the sparsity of arm space. The same regret is achieved by Bubeck et al. (2011), but is the packing dimension instead. They further demonstrate that the smoothness of the mean payoff function around its maximum can be used to reduce the packing dimension. Regret bounds independent of the dimension of the arm space are obtained by Cope (2009); Agarwal et al. (2013). Cope (2009) shows an asymptotic regret bound of size if the payoff functions are unimodal, three times continuously differentiable and its derivative is well behaved at its maximal. Agarwal et al. (2013) assume globally convex and Lipschitz payoff functions and achieving a regret with high probability.

Another stream of related literature is contextual bandits. Woodroofe (1979); Wang et al. (2005); Rigollet and Zeevi (2010); Perchet and Rigollet (2013) study contextual MAB with stochastic payoffs, under the name bandits with covariates: the context is a random variable correlated with the payoffs. They consider the case of finitely discrete arms. On the other hand, Slivkins (2014); Lu et al. (2009) consider continuous arms and assume Lipschitz continuity for both the arm and context space. They prove a lower bound for the regret of any algorithm where are the packing dimensions of the context and arms space respectively. Lu et al. (2009) presents a uniformly partition algorithm obtaining nearly tight regret upper bound where are covering dimensions of the context and arms space. The same regret bound can be achieved by the uniform partition and a bandit-with-expert-advice algorithm such as EXP4 (Auer et al., 2002b) or NEXP (McMahan and Streeter, 2009). The uniform partition is used to define an expert whose advise is simply an arbitrary arm for each set of the partition. Slivkins (2014) proposes an adaptive zooming algorithm so that frequently occurring contexts and high-paying arms structure can be used to improve practical performance. There other versions of contextual bandit problems, such as linear bandits (Auer, 2002; Dani et al., 2008; Rusmevichientong and Tsitsiklis, 2010; Abbasi-Yadkori et al., 2011), contextual bandits with policy sets (Auer et al., 2002b; Langford and Zhang, 2008; Agarwal et al., 2012; Dudik et al., 2011).

In operations research, many papers have focused on dynamic pricing and demand learning (Besbes and Zeevi, 2009, 2015; Broder and Rusmevichientong, 2012; den Boer and Zwart, 2013; den Boer, 2015). Recently Chen and Gallego (2018) consider personalized pricing of a single product to customers. Besides Lipschitz continuity in arms and context space, they further assume smoothness and local concavity at the unique maximizer of the payoff function. Their algorithm achieves the near-optimal regret in their setting, , slightly better than the when . In a recent paper, Chen and Shi (2019) consider multi-product pricing problem with inventory constraints. Similar to our setting, they assume global concavity and propose an algorithm which also depends on the online learning of gradients and achieves the regret bound of . The regret is independent of the dimension of the arm space, confirming the insights provided in this paper. However, the rate of regret bound does not seem to be optimal and the contextual information is not considered.

Main results and contributions. According to Slivkins (2014) and references therein, the optimal regret for the contextual continuum-armed bandits is , when the payoff function is Lipschitz continuous and are the dimensions of the context and arm space. After imposing the structure property that is globally concave in the decision variable when fixing , we provide an algorithm that achieves the regret . Compared to the previous bound, the dimensionality does not increase the regret exponentially when increases. The mitigation of the curse of the dimensionality can improve the performance of the algorithm significantly in practice. For example, in the context-free setting (), the regret of a ten-dimensional decision variable () is for previous algorithms, while a mere for our algorithm. On the other hand, global concavity is a mild assumption, which is commonly assumed in various applications. Therefore, the improvement in regret does not come with a substantial sacrifice in the generality of the formulation.

The algorithm is based on binning the contextual space and applying stochastic gradient descent or stochastic approximation in each bin to learn the optimal decision. Such algorithms are popular in machine learning (Bottou, 2010; Shalev-Shwartz and Srebro, 2008; Shalev-Shwartz et al., 2009; Duchi and Singer, 2009). In the case of concave functions, the classic algorithms in the learning literature such as UCB or Thompson sampling fail to take into account the special structure and do not seem to be able to achieve the optimal regret. Instead, gradient-based algorithms, which do not perform well for general functions due to multiple local maxima, can guarantee a surprising dimension-free regret in our setting. Our results thus convey the message that problem and domain-specific algorithmic design for learning problems may be helpful and beneficial.

Furthermore, we extend our algorithm to an adaptive binning framework. Such adaptive schemes are also adopted in Slivkins (2014); Chen and Gallego (2018); Perchet and Rigollet (2013). However, we the first one who design an algorithm combining stochastic approximation with adaptive partition of the context space. Although the new algorithm is much more challenging to analyze, we prove our algorithm achieves the optimal rate. The technical analysis also has important values to other areas, such as simulation optimization, stochastic programming. The adaptive algorithm outperforms the static one in practice, which is supported by the numerical experiment in Section 6.

2 Problem Formulation

The domain of the unknown payoff function is and . One can interpret and to be the normalization of some compact sets. Let denote the sequence of decision epochs faced by the decision maker. At the beginning of each epoch , the contextual information is revealed to the decision maker. The contextual information is drawn independently from some unknown distribution111Slivkins (2014) assumes that the context arrivals are fixed before the first round. We follow Perchet and Rigollet (2013) and assume that are i.i.d. and therefore denoted by . Then the decision maker chooses an arm in . The payoff in epoch is a random variable , whose mean is . We require to be independent across epochs given and .

Regret. If the payoff function were known, then the optimal decision and average payoff given context are

which is referred to as the oracle. Since the decision maker does not have access to the unknown function, the total payoff is always lower than that of the oracle in expectation. A standard performance metric of an algorithm is defined as the regret incurred compared to the oracle.

| (1) |

Note that the decision made in epoch , , is also random, even though the decision maker does not use active randomization. This is because at each epoch , the decision maker may rely on the information revealed so far to make decisions. Therefore, may depend on the observed contexts , the adopted decisions and the realized payoffs . Since is unknown to the decision maker, the objective is thus to design an algorithm that achieves small regret for a wide class of functions as . One can expect that if is an arbitrary function such as discontinuous ones, then no algorithm can achieve small regret. Next, we specify the assumptions that has to satisfy.

2.1 Assumptions

We now present a set of assumptions in our setting, which are required to guarantee the existence and good behavior of the gradient estimates. They are not required by Lipschitz bandits (Slivkins, 2014). Most assumptions are mild.

Assumption 1 (Twice differentiable).

For all , the function is twice continuously differentiable on the arm space .

Besides the existence of gradient, We assume strong concavity to ensure the global convergence of gradient descent and the uniqueness of the optimal solution.

Assumption 2 (Strong concavity).

There exists a constant such that for all and .

An immediate implication of Assumption 2 is the unique optimal solution for any context . The following assumption makes sure that is in the interior of , which implies that .

Assumption 3 (Interior optimal solution).

For any , the optimal solution satisfies .

Assumption 3 is imposed mainly for technical purposes. In practice, one may also extend the domain of to ensure an interior optimal solution. The next assumption imposes some regularity (Hölder condition) on the context space.

Assumption 4 (Hölder continuity of the context).

For every , the function is Hölder continuous in , i.e. with constant and .

Hölder continuity is a generalization of Lipschitz continuity. It is easy to see that for , it is equivalent to Lipschitz continuity. A Similar condition is also imposed in Perchet and Rigollet (2013). The next assumption makes sure that the random payoff behaves normally, which is standard in the literature.

Assumption 5 (Finite second moment).

For any given and , the random payoff has finite second moment, i.e., there exists a uniform constant such that .

At the beginning of the horizon, the following information is revealed to the decision maker: the domain of the context and the decision variable , the length of the horizon , and the constant defined in the Assumption 2.

3 Our Algorithm

There are two components of our algorithm. To deal with the contexts, we partition the context space into rectangular bins. When the partition is designed carefully, we are able to conduct context-free learning in each of the bin without significantly increasing the regret. That is, treat the contexts generated in the same bin equally. This idea is also adopted by Lu et al. (2009); Rigollet and Zeevi (2010); Perchet and Rigollet (2013); Chen and Gallego (2018). To find the optimal solution when the context falls into a particular bin, we use stochastic approximation and the estimated gradient to find the maximum. Next we elaborate on the two components separately.

Binning the context space. Discretization and local approximations are probably the most popular method to deal with nonparametric estimation. Utilizing Assumption 4, one can expect that and tend to behave similarly, including close maximal values and optimal solutions, when is small. Following this intuition, we partition the context space as follows. We divide each of the dimensions of the context space into equal intervals. As a result, the context space divided into identical hyper-rectangles, referred to as bins. The partition is thus a collection of bins of the following form: for ,

| (2) |

The algorithm thus keeps track of independent learning sub-problems. When a context is generated in at some epoch , the exact location of is no longer used as long as the knowledge of is preserved. The sub-problem then proceeds with one more epoch while the other sub-problems remain the same. Therefore, the sub-problem associated with is equivalent to a classic continuum-armed bandit problem without contextual information.

One can clearly see the trade-off in choosing a proper granularity of discretization, represented by . When is too small, the algorithm aggregates too much information into a bin and loses accuracy; when is too large, then there are too many bins and the learning horizon is short for each sub-problem. Later, we will choose an optimal to balance the trade-off and obtain small regret.

Stochastic Approximation (SA). To solve the sub-problem in a particular bin , the algorithm treats all contextual information equally as long as a context falls into . In this case, the oracle for the context-free problem can obtain the average payoff

| (3) |

with the following optimal solution

| (4) |

We develops an algorithm based on stochastic approximation (see Kushner and Yin (2003); Chau and Fu (2015) for a comprehensive review) to find . The basic idea is demonstrated below: Suppose at epoch a context is generated in bin . A decision is chosen and a random reward is observed. After a number of epochs, another context is observed in for some . If the gradient information of at is known, then stochastic approximation could be used to determine . In particular,

For a properly chosen step size , one can show that converges to the optimal solution .

However, there are two pitfalls of when applying SA directly. First, may be outside the domain . This issue can be addressed by projecting back to , denoted by the operator . Second, the function is not known to the decision maker, not to mention the gradient . Thus, we need to estimate the gradient from noisy payoffs . We use the Kiefer-Wolfowitz (KW) algorithm (Kiefer et al., 1952) as a subroutine. After applying and observing , the decision maker explores the neighborhood of and uses a finite-difference method to estimate the gradient. More precisely, suppose the contexts generated at fall into the same bin . Our algorithm applies decision in epoch , where is the unit vector with the th entry equal to 1 and 0 elsewhere. The step size will be specified later. The payoff can thus be regarded as an estimator for . After epoch , the KW algorithm suggests an estimator for

| (5) |

After more contexts generated in , the algorithm finally moves along the direction of the estimated gradient. Suppose in epoch , the context . Then the decision is chosen according to

Another contexts need to be observed in in order to estimate . The algorithm associated with a single bin is demonstrated in Algorithm 1. To simplify the notation, we only focus on the epochs when the contexts generated are in the same bin and re-order the index by .

Next we combine the two components for the contextual continuum-armed bandit problem. From the above description, we keep track of instances of Algorithm 1 and updates the number of epochs in each bin separately. The detailed steps are demonstrated in Algorithm 2.

Remark.

Technically speaking, the finite difference in Step 8 of Algorithm 1 may be outside the domain and the algorithm needs to adjust for that. In that case, we let which must be inside the domain . And then replace the corresponding difference in by its opposite. After that, all the following analysis remains the same.

4 Analysis of the Regret

In this section, we provide a roadmap of the analysis. We first bound the regret incurred in a single bin.

Proposition 1.

Let and , where and . Then the regret of Algorithm 1 in bin satisfies

| (6) |

where is a linear function of whose coefficients are independent of . Specifically,

Proposition 1 uses the standard convergence results of KWSA. However, we need to analyze the property of in (3) carefully. In particular, the assumptions imposed in Section 2.1 are for the function . First, we translate the assumptions in Section 2.1 of to obtain other crucial properties, including Lipschitz continuity, Lipschitz-continuous gradient and negative-definite Hessian matrix. Second, we prove the interchangeability of expectation and differentiation of to make sure the properties are extended to . Third, with the regulairty conditions of , we apply the asymptotic analysis in the stochastic approximation literature to derive finite time bound of Algorithm 1. More precisely, the left-hand side of (6) can be bounded by , because of bounded eigenvalues of the Hessian matrix. Then we bound by a decreasing sequence with convergence rate .

Remark.

According to Proposition 1, when there is not contextual information, Algorithm 1 achieves a bound for continuum-armed bandits. The problem is studied before in the literature and we compare to their results below. Cope (2009) shows a similar regret bound asymptotically. Our work has two improvements over his. First, we relax two critical assumptions in his paper, i.e., "the payoff function should be three times continuously differentiable" and "the set of optimal arms should be convex and contain an open ball in ". Second, our regret bound is a finite-time bound, while his is asymptotic. Bubeck et al. (2011) find that if the smoothness parameter of the payoff functions around the maxima were known, then the near-optimal regret could be achieved, independent of the dimension of the arm space. We do not require a certain degree of smoothness for the payoff function; instead, global convexity/concavity is imposed. In practice, knowing whether the unknown payoff function is convex seems to be more reasonable than knowing how smooth the function is. In a similar setting, Agarwal et al. (2013) propose an algorithm whose high-probability regret bound is . Comparing with Agarwal et al. (2013), we have three advantages. First, we eliminate the logarithmic terms in the bound. Second, we prove the bound with probability 1 instead of in their paper. Third, our algorithm is easy to implement.

From Proposition 1, we know that the regret incurred in one bin is bounded by if there are epochs to learn in that bin. This is because summing up leads to

To analyze the regret incurred by Algorithm 2, we need to aggregate the regret incurred in all the bins in the partition. Moreover, the optimal solution for the context-free problem in a bin is still not as good as the oracle . We expect to bound by the size the bin and the continuity of . We choose in Algorithm 2.

Theorem 1.

For the most common case of Lipschitz functions, we let and the regret bound becomes

It recovers the regret bound in Lipschitz bandit (Slivkins, 2014) with . Also notice the fact that when , . Therefore, no matter how large the dimension of the decision variable is, the dependence of the regret on is at most linear. Compared to the exponential dependence (i.e., ) in the literature, the mild dependence makes our algorithm more suitable for problems with high-dimensional decision variables. The significantly improved regret comes at the cost of a more restrictive form of , in particular, it has to be globally concave in . The additional assumption is still reasonable in various applications. Moreover, the algorithm eliminates the logarithmic terms commonly seen in the literature.

The main steps of the proof are described below. First, the regret incurred in epoch , is bounded by a constant multiplied by the mean square error , because of the global convexity. The distance between and is further bounded by and , where the bound of the first term is implied by Proposition 1. For the second term, the discretization error incurred by binning, is bounded by the diameter of bin . Second, after deriving the regret incurred in one epoch, the bound of total regret could be obtained by summing up the regret in all bins. The worst case in terms of the regret is when the covariates are generated evenly in the bins, and the best case is when the covariates are generated in a single bin. Therefore, suppose each of the bins observes covariates and we can compute the aggregate regret for this worst case. Finally, we need to minimize the regret over the number of bins . The tunable parameter can be regarded as a balance between exploration and exploitation. When the bin is large, there is enough observations in the bin that the selected arm is close to its optimum. However, due to the large diameter of the bin, its optimum may be far away from the optimum respect to one specific covariate in the bin. On the other hand, when the bin is small, the distance between the optimum of the bin and optimum of one covariate is quite small, but the arms chosen by Algorithm 1, may be far from the bin’s optimum. To balance the trade-off and obtain smallest regret, the number of bins is chosen to be .

Remark.

Another type of stochastic approximation is referred to as the Robbins-Monro (Robbins and Monro, 1951) algorithm. Different from KW, RM algorithm requires an oracle to return the unbiased estimators for the gradient of for any given . The unbiased estimator can be used to replace in (5). As a result, the convergence rate of RM is better than KW and the regret bound in Theorem 1 can be further improved. However, the information of an unbiased estimator for the gradient is a somewhat unrealistic scenario, and thus we do not present the regret for the RM algorithm in this paper.

5 Extension to Adaptive Binning

There is one potential pitfall in the binning algorithm proposed in Section 3. The size of the bins is predefined before the algorithm starts. So the bias due to binning will not decrease as more context observed in the bin. To remedy the pitfall, we propose an adaptive binning algorithm which reduces the binning bias by sequentially splitting the bin into smaller ones. More specifically, the adaptive algorithm has three advantages over the static one. First, taking advantage of sequentially arrived context, it partitions the space adaptively to the distribution of context to maintain a finer partition in popular regions of context. Second, when binning adaptively, the observations in a parent bin provide some information for all offspring bins. Such a pooling effect makes the exploration more effective. While in the setting of static binning, the information learned from observations is only restricted in its own bin. Third, as mentioned in Slivkins (2014), the adaptive algorithm can be applied to solve other MAB problem, such as MAB with stochastically evolving payoffs and sleeping bandits.

Adaptive binning the context space. Rather than fixing all bins at the beginning, the adaptive algorithm splits bins sequentially. When enough covariates are observed in the bin, we bisect it in all the dimensions to obtain child bins. Specifically, for a bin with boundaries and for , its children are indexed by and have the form

Our algorithm starts with a root bin , whose depth level is denoted by 0. When covariates are observed times in , it is split into level 1 bins. For such a bin , it will be split into level 2 bins once covariates are observed further times in the bin. So on so forth until the bin reaches the deepest depth . When a bin is at level , the algorithm no longer splits it and simply applies the decision of KW (Kiefer-Wolfowitz) algorithm whenever a covariate is generated in it.

There are two critical hyper-parameters required to be carefully designed before the beginning. First, —the maximal number of observations collected in a level- bin before partition—balances the trade-off between bias due to binning and learning horizon in each bin. When is too small, the learning horizon for bins in level k is too short that the solution obtained by KW algorithm may not be close to the optimum. When is too large, the bias is too large which makes the KW algorithm lose accuracy. Second, —the maximal level of bins—balances the trade-off between adding more child bins and the time horizons in the deepest bins. When a bin in the deepest level is split, the bias of the bin becomes smaller, but the total number of the bins increases by .

A crucial step in the algorithm is to determine what information to inherit when a bin is split into child bins. Since the last decision in parent bin is the best indicator for its optimum, we adopt it as the initial decision in child bins.

Next, we combine the adaptive binning algorithm with Algorithm 1 mentioned in section 3. The detailed steps are demonstrated in Algorithm 3.

Analysis of the regret. The adaptive binning algorithm is much more challenging to analyze because more hyper-parameters need to be carefully designed. Under the choice of and , we prove that the adaptive binning algorithm achieves the same order of regret upper bound as the static one.

Theorem 2.

Intuitively, the adaptive algorithm should outperform the static one because it refines more partitions in popular regions of context. However, Theorem 2 suggests that the adaptive and static algorithms achieve the same asymptotic rate of regret. That’s because the performance measure is an upper bound no matter for any distribution of covariates. So the worst-case performance is considered when counting the total regret. The worst-case for both the adaptive and static algorithm is that the covariates are distributed uniformly in the whole space, which exactly eliminates the advantage of adaptive binning. Thus, the benefit of the adaptive algorithm is not reflected in the asymptotic rate of regret. However, the adaptive algorithm performs better than the static one in practice (see Section 6).

Theoretical analysis is much more difficult than the static one

Remark.

As mentioned in Section 4, some prior work also attain the optimal regret rate in context-free setting. But their algorithms or analysis are difficult to extend to an adaptive scheme. Specifically, Cope (2009) assumes the set of optimal arms should be convex and contain an open ball in . This assumption may be violated easily when the context is restricted to a sub-area. Agarwal et al. (2013) propose an algorithm obtaining the optimal rate with a probability . When combining with static binning, their good-performance probability decreases with . It’s more challenging to make sure that their algorithm still attains the optimal bound with high-probability when extending to the adaptive one.

6 Numerical Experiment

In this section, we apply various algorithms to a numerical example with and . In the context space , there are two community centers: , corresponding to the two payoff functions and . For a context , its distance to the two centers are denoted and . The total payoffs are defined as

| (9) |

which could be checked satisfying the assumptions in Section 2.1 (details in supplementary material).

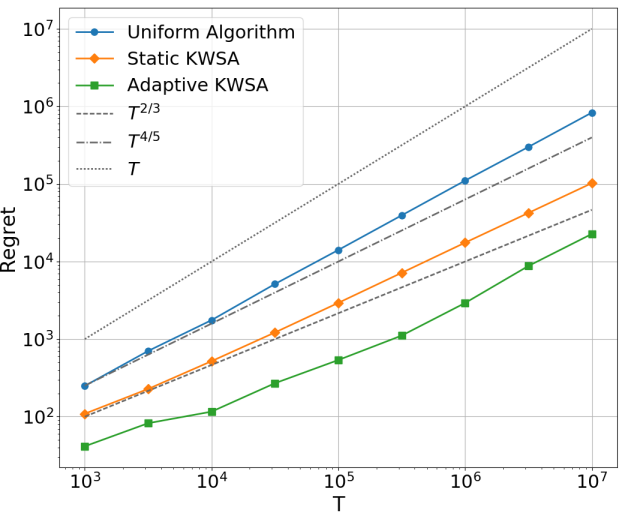

We compare our algorithms (KWSA with static and adaptive binning) with the "uniform algorithm" (Slivkins, 2014), which simply discretizes the covariate and arms space then apply UCB to sub-problems. With correctly tuned parameters, the "uniform algorithm" attains the regret bound ( in the example). While our algorithms attain the regret bound . The result shows in a log-log plot in Figure 1. We see that the "uniform algorithm" has a similar growth rate to and our algorithms have a similar growth rate to . So our algorithms perform much better than "uniform algorithm". Besides that, the adaptive algorithm shows significant improvement over the static one.

Remark.

Comparing to the existing work (Slivkins, 2014) using the adaptive partition scheme, our algorithms are more convenient to implement and show low computational complexity. In the numerical example, when total time horizon , the computing times for "uniform algorithm", Static KWSA, Adaptive KWSA are 12mins, 6mins and 7mins respectively, using a PC with 3.4GHz Intel Core i7 CPU and 8GB memory. That implies our algorithms reduce the computational burden even comparing to the simplest one. And using adaptive scheme only slightly increases the computing time.

7 Conclusion and Future Work

In this paper, we study the continuum-armed bandit problem under contextual information, where the context space and arms space are both continuous. After assuming the curvature of payoff functions, strong convexity and second-order smoothness, we propose a novel algorithm combining stochastic approximation with binning partition framework and obtain a much better regret than existing literature. Surprisingly, our method achieves a dimension-free result. Moreover, we generalize our algorithm to an adaptive one that maintains the asymptotic regret bound but performs much better in practice.

In the future, we will investigate how to reduce the effect incurred by context space. In other words, whether the curvature conditions corresponding to covariates can be utilized to improve the regret bound. If so, another nonparametric estimation framework other than binning partition is required to solve the curse of dimensionality problem. It’s an open problem that how to incorporate nonparametric statistic learning methods in reducing the growth rate of the regret with respect to the dimension of context space.

References

- Abbasi-Yadkori et al. [2011] Y. Abbasi-Yadkori, D. Pál, and C. Szepesvári. Improved algorithms for linear stochastic bandits. In Advances in Neural Information Processing Systems, pages 2312–2320, 2011.

- Agarwal et al. [2012] A. Agarwal, M. Dudík, S. Kale, J. Langford, and R. E. Schapire. Contextual bandit learning with predictable rewards. arXiv preprint arXiv:1202.1334, 2012.

- Agarwal et al. [2013] A. Agarwal, D. P. Foster, D. Hsu, S. M. Kakade, and A. Rakhlin. Stochastic convex optimization with bandit feedback. SIAM Journal on Optimization, 23(1):213–240, 2013.

- Agrawal [1995] R. Agrawal. The continuum-armed bandit problem. SIAM journal on control and optimization, 33(6):1926–1951, 1995.

- Auer [2002] P. Auer. Using confidence bounds for exploitation-exploration trade-offs. Journal of Machine Learning Research, 3(Nov):397–422, 2002.

- Auer et al. [2002a] P. Auer, N. Cesa-Bianchi, and P. Fischer. Finite-time analysis of the multiarmed bandit problem. Machine learning, 47(2-3):235–256, 2002a.

- Auer et al. [2002b] P. Auer, N. Cesa-Bianchi, Y. Freund, and R. E. Schapire. The nonstochastic multiarmed bandit problem. SIAM journal on computing, 32(1):48–77, 2002b.

- Auer et al. [2007] P. Auer, R. Ortner, and C. Szepesvári. Improved rates for the stochastic continuum-armed bandit problem. In International Conference on Computational Learning Theory, pages 454–468. Springer, 2007.

- Besbes and Zeevi [2009] O. Besbes and A. Zeevi. Dynamic pricing without knowing the demand function: Risk bounds and near-optimal algorithms. Operations Research, 57(6):1407–1420, 2009.

- Besbes and Zeevi [2015] O. Besbes and A. Zeevi. On the (surprising) sufficiency of linear models for dynamic pricing with demand learning. Management Science, 61(4):723–739, 2015.

- Bottou [2010] L. Bottou. Large-scale machine learning with stochastic gradient descent. In Proceedings of COMPSTAT’2010, pages 177–186. Springer, 2010.

- Broder and Rusmevichientong [2012] J. Broder and P. Rusmevichientong. Dynamic pricing under a general parametric choice model. Operations Research, 60(4):965–980, 2012.

- Bubeck et al. [2011] S. Bubeck, R. Munos, G. Stoltz, and C. Szepesvári. X-armed bandits. Journal of Machine Learning Research, 12(May):1655–1695, 2011.

- Bubeck et al. [2012] S. Bubeck, N. Cesa-Bianchi, et al. Regret analysis of stochastic and nonstochastic multi-armed bandit problems. Foundations and Trends® in Machine Learning, 5(1):1–122, 2012.

- Chau and Fu [2015] M. Chau and M. C. Fu. An overview of stochastic approximation. In Handbook of Simulation Optimization, pages 149–178. Springer, 2015.

- Chen and Gallego [2018] N. Chen and G. Gallego. Nonparametric learning and optimization with covariates. Working paper, 2018.

- Chen and Shi [2019] Y. Chen and C. Shi. Network revenue management with online inverse batch gradient descent method. Working paper, 2019.

- Cope [2009] E. W. Cope. Regret and convergence bounds for a class of continuum-armed bandit problems. IEEE Transactions on Automatic Control, 54(6):1243–1253, 2009.

- Dani et al. [2008] V. Dani, T. P. Hayes, and S. M. Kakade. Stochastic linear optimization under bandit feedback. In COLT, 2008.

- den Boer [2015] A. den Boer. Dynamic pricing and learning: Historical origins, current research, and new directions. Surveys in operations research and management science, 20(1):1–18, 2015.

- den Boer and Zwart [2013] A. V. den Boer and B. Zwart. Simultaneously learning and optimizing using controlled variance pricing. Management science, 60(3):770–783, 2013.

- Duchi and Singer [2009] J. Duchi and Y. Singer. Efficient online and batch learning using forward backward splitting. Journal of Machine Learning Research, 10(Dec):2899–2934, 2009.

- Dudik et al. [2011] M. Dudik, D. Hsu, S. Kale, N. Karampatziakis, J. Langford, L. Reyzin, and T. Zhang. Efficient optimal learning for contextual bandits. arXiv preprint arXiv:1106.2369, 2011.

- Kiefer et al. [1952] J. Kiefer, J. Wolfowitz, et al. Stochastic estimation of the maximum of a regression function. The Annals of Mathematical Statistics, 23(3):462–466, 1952.

- Kleinberg and Slivkins [2010] R. Kleinberg and A. Slivkins. Sharp dichotomies for regret minimization in metric spaces. In Proceedings of the twenty-first annual ACM-SIAM symposium on Discrete Algorithms, pages 827–846. Society for Industrial and Applied Mathematics, 2010.

- Kleinberg et al. [2008] R. Kleinberg, A. Slivkins, and E. Upfal. Multi-armed bandits in metric spaces. In Proceedings of the fortieth annual ACM symposium on Theory of computing, pages 681–690. ACM, 2008.

- Kleinberg [2005] R. D. Kleinberg. Nearly tight bounds for the continuum-armed bandit problem. In Advances in Neural Information Processing Systems, pages 697–704, 2005.

- Kushner and Yin [2003] H. Kushner and G. G. Yin. Stochastic approximation and recursive algorithms and applications, volume 35. Springer Science & Business Media, 2003.

- Lai and Robbins [1985] T. L. Lai and H. Robbins. Asymptotically efficient adaptive allocation rules. Advances in applied mathematics, 6(1):4–22, 1985.

- Langford and Zhang [2008] J. Langford and T. Zhang. The epoch-greedy algorithm for multi-armed bandits with side information. In Advances in neural information processing systems, pages 817–824, 2008.

- Lu et al. [2009] T. Lu, D. Pál, and M. Pál. Showing relevant ads via context multi-armed bandits. Technical report, Tech. rep, 2009.

- Maillard and Munos [2010] O.-A. Maillard and R. Munos. Online learning in adversarial lipschitz environments. In Joint European Conference on Machine Learning and Knowledge Discovery in Databases, pages 305–320. Springer, 2010.

- McMahan and Streeter [2009] H. B. McMahan and M. Streeter. Tighter bounds for multi-armed bandits with expert advice. In COLT, 2009.

- Pandey et al. [2007] S. Pandey, D. Agarwal, D. Chakrabarti, and V. Josifovski. Bandits for taxonomies: A model-based approach. In Proceedings of the 2007 SIAM International Conference on Data Mining, pages 216–227. SIAM, 2007.

- Perchet and Rigollet [2013] V. Perchet and P. Rigollet. The multi-armed bandit problem with covariates. Annals of Statistics, 41(2):693–721, 2013.

- Rigollet and Zeevi [2010] P. Rigollet and A. Zeevi. Nonparametric bandits with covariates. COLT 2010, page 54, 2010.

- Robbins [1952] H. Robbins. Some aspects of the sequential design of experiments. Bulletin of the American Mathematical Society, 58(5):527–535, 1952.

- Robbins and Monro [1951] H. Robbins and S. Monro. A stochastic approximation method. The annals of mathematical statistics, pages 400–407, 1951.

- Rudin et al. [1964] W. Rudin et al. Principles of mathematical analysis, volume 3. McGraw-hill New York, 1964.

- Rusmevichientong and Tsitsiklis [2010] P. Rusmevichientong and J. N. Tsitsiklis. Linearly parameterized bandits. Mathematics of Operations Research, 35(2):395–411, 2010.

- Shalev-Shwartz and Srebro [2008] S. Shalev-Shwartz and N. Srebro. Svm optimization: inverse dependence on training set size. In Proceedings of the 25th international conference on Machine learning, pages 928–935. ACM, 2008.

- Shalev-Shwartz et al. [2009] S. Shalev-Shwartz, O. Shamir, N. Srebro, and K. Sridharan. Stochastic convex optimization. In COLT, 2009.

- Slivkins [2014] A. Slivkins. Contextual bandits with similarity information. The Journal of Machine Learning Research, 15(1):2533–2568, 2014.

- Wang et al. [2005] C.-C. Wang, S. R. Kulkarni, and H. V. Poor. Bandit problems with side observations. IEEE Transactions on Automatic Control, 50(3):338–355, 2005.

- Woodroofe [1979] M. Woodroofe. A one-armed bandit problem with a concomitant variable. Journal of the American Statistical Association, 74(368):799–806, 1979.

8 Appendix

8.1 Proof of Proposition 1

Proposition 2.

Let and , where and . Then the regret of Algorithm 1 in bin satisfies

| (10) |

where is a linear function of whose coefficients are independent of . Specifically,

At a high level the proof first extends assumptions in section 2 to more properties of mean payoff function in Lemma 1. Then we prove theses assumptions and properties are also satisfied by the payoff function in Lemma 3. Finally, Proposition 1 can be proved using these properties.

Lemma 1 (Properties of ).

According to assumptions 1-3, we have that,

- (1)

-

is Lipschitz continuous in with a constant , i.e. .

- (2)

-

is Lipschitz continuous in with a constant , i.e. .

- (3)

-

For any and , the Hessian matrix is negative definite and all the eigenvalues are in the interval , i.e. .

- (4)

-

For every , the function has a unique maximizer , i.e. there exists a unique and .

Proof of Lemma 1.

- (1)

-

Since is a continuous function on a convex set , there exists a constant s.t . Then by generalized mean value theorem (Theorem 9.19 in Rudin et al. [1964]), for all and .

- (2)

-

Since is a continuous function on a convex set , there exists a constant s.t . Then by generalized mean value theorem, for all and .

- (3)

-

Notice that is a strongly concave function, for every and ,

By second order Taylor expansion, there exists a such that,

Thus,

and

Again by twice continuous differentiability of , we have

So for all ,

Recall that is a continuous function on a convex set and . Then for any ,

- (4)

-

Assuming there exists satisfying

By the strong concavity of ,

which contradicts with the definition of . Thus there only exists one maximizer .

Next, if , we can find a small step such that . Then which contradicts with the definition of . So .

Before proving the smoothness and convexity conditions of , we first provide condition for interchangeability of expectation and derivative in Lemma 2.

Lemma 2 (Pathwise Method).

Assume for every , is differentiable on and Lipschitz continuous with constant . Then .

Proof of Lemma 2.

Considering one certain dimension , if we can prove , then Lemma 2 is obvious.

In the first equality, denotes the unit vector with the i-th entry 1. The third equality is supported by dominated convergence theorem, where .

Lemma 3 (Optimal arm in hypercube).

For any hypercube , including a singleton , define the function . According to assumptions 1-3 ,we have that for any ,

- (1)

-

is twice continuously differentiable on the convex set . Additionally, expectation and gradient are exchangeable, i.e. and .

- (2)

-

is strongly concave in with the same constant of , i.e. for all

- (3)

-

maintains Lipschitz continuous property of with the same constant, i.e. for all

- (4)

-

maintains Lipschitz gradient property of with the same constant, i.e. for all .

- (5)

-

For all , the Hessian matrix of is negative definite and all the eigenvalues are in the interval , i.e. .

- (6)

-

The function has a unique maximizer , i.e. there exists a unique , and .

Proof of Lemma 3.

- (1)

-

Since are differentiable and are Lipschitz continuous with constant , according to pathwise method, . exists for the reason that exists for any . Similarly, as are differentiable and Lipschitz continuous with constant , we have

The continuity of is the consequence of continuous in .

- (2)

-

Strong concavity is obvious because expectation operator maintains linear relationship.

- (3)

-

- (4)

-

- (5)

-

Since has the twice continuous differentiable and strong concave property of , this property can be proved following the same way of Lemma 1(3).

- (6)

-

Assuming there exist satisfying

By the strong concavity of ,

Thus,

which contradicts with the definition of . Thus there is only one maximizer .

To prove the second part , we define that and . Recall that is a convex set , the lower bounds and upper bounds in each dimension are denoted by . In each dimension , we define the minimum distance between and as . Similarly, . , then and . Considering that is a strongly concave function in , for and and for . So for and for . Recall that is a continuous function. Then, there exists such that .

Lemma 4.

Suppose the sequence satisfies

Let , where

Then, by induction, we have .

Proof of Lemma 4.

We prove by induction. It is easy to see that it hold for . For any suppose that . Because due to ,

where the last inequality follows form the definition of that satisfies for any . Let . Then, . Notice that is convex. Then,

Then,

Therefore,

Then, we have . This concludes the induction proof.

Proof of Proposition 1. According to the dimension of arm space, the time epochs is divided into periods: period 1=, period 2= last period =. In each period, the gradient is estimated by finite-difference exactly once at the first epoch. Let denote the number of period, which is also the gradient estimation times. Then let . Notice that and , then

| (11) |

Let and . Then,

| (12) |

The first equality follows from tower law, second from the definition of and third from the definition of . According to strong concavity property of (Lemma 3(2)), we have

Add them together,

Note that strong concavity of implies that maximizer is unique. By optimality of , we have

which together with last equation implies that . Taking expectation of both sides,

| (13) |

Then by Lemma 3(5),

Then by Cauthy-Schwarz inequality,

Thus,

| (14) |

Furthermore, by Assumption 5,

| (15) |

Therefore, by equations ( 11),( 12),( 13),( 14),( 15),

Suppose that and with and , we have

Let , by induction (see Lemma 4), there exists such that

In each period, arms, required to be implemented. Notice that, by Lemma 3(6), and Lemma 3(5), . Then by Taylor expansion,

Taking expectation of both sides,

and for ,

Recall that is an affine function of , then there exist a function such that

for every epoch .

8.2 Proof of Theorem 1.

Theorem 3.

For any function satisfying the assumptions in Section 2.1, the regret by Algorithm 1 is bounded by

| (16) |

for a constant that is independent of .

We first prove a continuity result of maximizers in Lemma 5. It gives an error bound for the distance between the maximizer in one bin and optimum for a covariate. The error will disappear as the diameter of shrinks to zero.

Lemma 5 (Hölder continuous of and ).

For a hypercube , the diameter of arms space is and let be the diameter of bin . By Assumptions 1-4, there exists a uniform constant such that for any .

Proof of Lemma 5. From twice continuously differentiable and strongly concavity of function , we have that

Then add them together,

where . So we get the conclusion,

Proof of Theorem 1. According to the algorithm, denotes the partition formed by the bins. The regret associated with can be counted by bins into which falls. Therefore,

According to Lemma 1(3), we have . The distance between and can be bounded by and , where the first term is bounded by the error bound of stochastic approximation proved in Proposition 1 and the second term is bounded by the diameter of bin using Lemma 5. Therefore,

where is the function defined in Proposition 1 and denotes observation times in . After deriving the regret bound in one period, we can sum them together and obtain the bound of total regret.

Since forms a partition of the covariate space and always falls into one of the bins. The worst case is that all the covariates are uniformly distributed in the whole covariate space, for the regret incurred in each bin increases in the reciprocal order as observations increasing. Thus the total regret is less than the accumulative regret in bins when covariates occur times in each bin.

By the summation of series, , we have

Using the Cauchy inequality,

We separate in 2 cases to design the that minimizes the total regret.

- (1)

-

If , then

Hence, to minimize the total regret, by the choice of (satisfying ),

- (2)

-

If , then

Hence,

Hence, we choose and complete the proof of Theorem 1.

8.3 Proof of Theorem 2.

The adaptive algorithm is more challenging to analyze. That’s mainly because it split bins adaptively which cause expected randomness in determining the size of the bins. In the algorithm, we keep a dynamic partition of the covariate space consisting of all the bins in each period . The partition is mutually exclusive and collectively exhaustive. Specifically,

where denotes the level of bin . The partition will be gradually refined in the algorithm and updated at the end of each period.

Similar to the proof of Theorem 1, we first extend Lemma 5 to a result in bin of level .

Lemma 6 (Extension of Lemma 5).

For a bin in level , the diameter of arms space is and let be the diameter of bin . By Assumptions 1-4, there exists a uniform constant such that for any .

Proof of Lemma 6. In the bin of level , the diameter . So following the proof of Lemma 5, we have

Proposition 1 provides a finite-time convergence result of algorithm 1. It only gives an error bound in a single bin. So we generalize it to be applicable to the bins in different levels.

Proposition 3.

In a bin of level , let and , where and . Then the regret of Algorithm 1 in bin satisfies

where is the initial error in bin .

Proof of Proposition 2.

In the result of Proposition 1, we know that

where is a linear function of .

At the right-hand side, is the initial solution when context is observed in bin . According to the Algorithm 3, it’s a random variable defined as the last solution of the parent bin of . So depends on the information before the bin is generated. Let denotes the parent bin of , so the level of is . Then, let denotes the last solution in and denotes the true optimum of .

The last inequality follows from applying Proposition 1 to bin and Lemma 6.

Since all the bins in the same level are constructed in the same procedure, are all equal. Let , then . Thus, we have shown that

where and . According to the main part, . Therefore, the initial error forms a sequence.

where is the initial error in bin .

Thus, we conclude to prove Proposition 3.

Proof of Theorem 2. According to the algorithm, denotes the partition formed by the bins at time t when is generated. The regret associated with can be counted by bins into which falls. Meanwhile, the level of is at most . Therefore,

According to Lemma 1(3), we have . The distance between and can be bounded by and , where the first term is bounded by the error bound of stochastic approximation proved in Proposition 3 and the second term is bounded by the diameter of bin using Lemma 5. Therefore,

After deriving the regret bound in one period, we can sum them together and obtain the bound of total regret.

For the first term, note that occurs for at most times for given with . Moreover, there are bins with level except for . Total regret incurred in the first levels is bounded by the regret incurred in full tree of level .

For the second term, forms a partition of the covariate space and always falls into one of the bins. The worst case is that all the covariates are uniformly distributed in the whole covariate space, for the regret incurred in each bin increases in the reciprocal order as observations increasing. Thus the total regret incurred in the last level is less than the accumulative regret in bins when covariates occur times in each bin.

By the summation of series, , we have

Replace using Proposition 3,

Recall that , then and . Hence, can be further simplified as

Suppose is large enough that the level of tree , so the second term can be merged into the first term.

We separate in 2 cases to obtain the that minimizes the total regret.

- (1)

-

If , then , and

Hence, to minimize the total regret, by the choice of (satisfying ),

- (2)

-

If , then , and

Hence, to minimize the total regret, by the choice of (but ),

Hence, we complete our proof of Theorem 3.

8.4 Proof of Theroem 3.

Proposition 4.

We construct the example, for ,

The example satisfies assumptions.

Proof of Proposition 4

- (1,2)

-

The first order and second order derivative respect to are,

So the first and second assumptions are obviously satisfied.

- (3)

-

Then,

is in the interior of the decision space.

- (6)

-

Since the distance to boundary is a kind of infinity norm, its derivative to is less than 1. So the partial derivative

Assumption 6 is satisfied.

Proof of Theorem 3.

Where the total number of instances is . For a given bin , we focus on which only differs for . We rewrite the summation as .

Let , then

We complete the other side by the information theory. , then

In total we have,

The last equality follows by setting .

Combining these 2 bounds together,

To find a minimizing the right side, we use the first order condition.

Then,

Replacing by in the RHS,

Applying the first order condition again, we have

And finally,