Singularities and Catastrophes in Economics: Historical Perspectives and Future Directions

Abstract

Economic theory is a mathematically rich field in which there are opportunities for the formal analysis of singularities and catastrophes. This article looks at the historical context of singularities through the work of two eminent Frenchmen around the late 1960s and 1970s. René Thom (1923-2002) was an acclaimed mathematician having received the Fields Medal in 1958, whereas Gérard Debreu (1921-2004) would receive the Nobel Prize in economics in 1983. Both were highly influential within their fields and given the fundamental nature of their work, the potential for cross-fertilisation would seem to be quite promising. This was not to be the case: Debreu knew of Thom’s work and cited it in the analysis of his own work, but despite this and other applied mathematicians taking catastrophe theory to economics, the theory never achieved a lasting following and relatively few results were published. This article reviews Debreu’s analysis of the so called regular and crtitical economies in order to draw some insights into the economic perspective of singularities before moving to how singularities arise naturally in the Nash equilibria of game theory. Finally a modern treatment of stochastic game theory is covered through recent work on the quantal response equilibrium. In this view the Nash equilibrium is to the quantal response equilibrium what deterministic catastrophe theory is to stochastic catastrophe theory, with some caveats regarding when this analogy breaks down discussed at the end.

1 Introduction: A key point in the history of economics “in the mathematical mode”

To single out a specific point in the history of a field of study and to say: Here is where it all began oversimplifies the complicated relationships between competing paradigms. However we can look at specific lines of research that have, with hindsight, become the dominant paradigm and look to what those authors wrote at the time to justify their specific view point in order to understand how an influential researcher framed their point of view. One such researcher is Gérard Debreu, an economist who was the sole recipient of the 1983 Nobel Prize in Economics111Formally: The Swedish National Bank’s Prize in Economic Sciences in Memory of Alfred Nobel. for “having incorporated new analytical methods into economic theory and for his rigorous reformulation of general equilibrium theory”. His work was an important step in the mathematisation of economics [15] and his Nobel speech was titled: Economic Theory in the Mathematical Mode [14]. Debreu acknowledged [13, 14] the importance of Thom’s work on catastrophe theory [40, 41], but chose not to incorporate these ideas into his axiomatic treatment of economics. At the same time applied mathematicians were using catastrophe theory in many fields in a qualitative fashion that would ultimately lead to a backlash against catastrophe theory. The debate within the field of economic applications of catastrophe theory has been thoroughly reviewed in [33]

A common approach to simplifying the complexities of an entire economy is to reduce to a simplified form and study the local behaviour of that economy [12]: It suffices to construct an … economy with two commodities and two consumers … and having several equilibria. There is a neighbourhood of that economy in which every economy has the same number of equilibria. Simplifications like this allow us to use game theory with two economic agents each having two choices each, see [11] for a recent treatment and discussion.

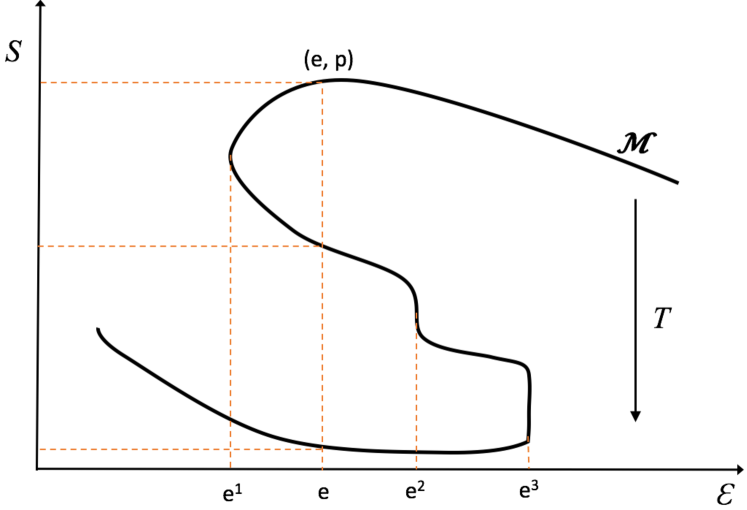

An important contribution of Debreu was the distinction between regular and critical economies. In Figure 1 the different configurations of an economy are labelled , , , and with the corresponding equilibrium states lying on the equilibrium surface . is the projection of the equilibrium surface onto , the space of all economic configurations. Debreu showed that, apart from a subset of with Lebesgue measure zero, there is an inverse mapping and in particular if is a locally unique equilibrium point then is a regular economy with at least one equilibrium point . This follows from the inverse function theorem when the determinant of the Jacobian is away from 0. The special cases where the Jacobian is degenerate, i.e. , , and , are the critical economies. To quote Debreu [13, pg. 284]: For instance the economy has a discrete set of (two) equilibria, but a continuous displacement of the economy in a neighbourhood of produces a sudden change in the set of equilibria. The parallels with singularity theory are apparent and were known to Debreu.

The purpose of this article is to introduce some of the formal aspects of game theory, equilibrium theory, and their stochastic variations and to place these in the context of catastrophe theory. The article is laid out as follows. Section 2 establishes the key equilibrium result of Nash and reviews an important method for the explicit computation of Nash equilibria. Section 3 introduces singularities from the perspective of catastrophe theory, its extension to stochastic catastrophe theory, and their relation to bifurcations in game theory. Section 4 is a discussion of these results in the context of other related approaches and results.

2 Nash Equilibrium

Optimisation leads naturally to singularities [2] and the Nash equilibrium is a solution to an optimisation problem. As such the appearance of singularities is expected to be a generic property of game theory solutions. This aspect of optimisation has been explored by Arnol’d [3]: … suppose we have to find such that the value of a function is maximal … On smooth change of the function the optimum solution changes with a jump, transferring from one competing maxima (A) to the other (B). From this, singularities are expected to be a fundamental property of economic theory which is at its core a study of optimising the allocation of scarce resources. In this section we introduce the basic elements of game theory as a decision problem and the Nash equilibrium as an optimal solution.

2.1 Basic definition and existence theorem

Economics is concerned with situations in which there are agents, where each agent has a discrete set of finite choices . An economic game is a function from the choices agents make to a real valued payoff, one for each agent:

| (1) |

where , the element of , is the payoff to agent . A strategy for agent is a probability distribution over :

such that

To simplify notation we refer to as . The definition of agent ’s expected payoff in the game , which takes discrete choices as its arguments, can be extended to take the strategies of the agents as arguments:

| (2) |

where denotes all indexed elements excluding element . This definition of is an extension in the sense that it contains each discrete strategy as a special case in which one probability and otherwise. These are called pure strategies. A strategy that is not a pure strategy is called a mixed strategy. Nash’s equilibrium theory establishes the following result,

Theorem 2.1.

Nash Equilibrium: There exists at least one -tuple such that:

| (3) |

Proof.

(verbatim from Nash’s original article [32]) Any -tuple of strategies, one for each agent, may be regarded as a

point in the product space obtained by multiplying the strategy spaces of the agents. One such -tuple counters another if the strategy of each agent in the countering -tuple yields the highest obtainable expectation for its agent against the -1 strategies of the other agents in the countered -tuple. A self-countering -tuple is called an equilibrium point.

The correspondence of each -tuple with its set of countering -tuples gives a one-to-many mapping of the product space into itself. From the definition of countering we see that the set of countering points of a point is convex. By using the continuity of the pay-off functions we see that the graph of the mapping is closed. The closedness is equivalent to saying: if and are sequences of points in the product space where , and counters then counters .

Since the graph is closed and since the image of each point under the mapping is convex, we infer from Kakutani’s theorem that the mapping has a fixed point (i.e. point contained in its image). Hence there is an equilibrium point. ∎

Using the notation above this can be rephrased more formally [11]: Given an agent , for every (-1)-tuple of the strategies of the other agents, there is a best response function:

| (4) |

This function consists of the set of strategies that maximise agent ’s payoff given the other agents’ strategies . Define as the product space:

| (5) |

Then is an upper-hemicontinuous, convex valued, and non-empty-valued correspondence that maps the set of -tuples to itself. Kakutani’s fixed point theorem provides proof of the existence of a fixed point such that: that also satisfies Equation 3.

2.2 Computational methods

This subsection briefly reviews some of the methods for explicitly computing Nash equilibria. The main focus will be on two-agent games, which is the special case of the setting introduced in the previous subsection. We shall suppose that agent 1 has pure strategies available, and agent 2 has pure strategies. We put and , and let and denote the matrices and , respectively. To simplify the notation for the probability distributions we put , for , and , for , and we let and denote the column vectors and , respectively. We have

| (6) |

Then the expected payoffs to agents 1 and 2 are expressed succinctly

as and , respectively, where denotes the transpose of .

A Nash equilibrium for such a game is then a pair satisfying (6)

and, for all satisfying (6), and

.

That is, a Nash equilibrium point is a pair of mixed strategies that are best

responses to each other.

An equivalent characterization of a Nash equilibrium point is that must satisfy (6) and

| (7) |

| (8) |

This characterization is proved in [31] (see Equation 4).

It could be roughly expressed as follows: a mixed strategy is a best response to an

opponent’s strategy if and only if it uses pure strategies that are best

responses amongst all pure strategies. See also [10] (Lemma 4.17).

The following result summarizes a further useful transformation of the problem of finding a Nash equilibrium point.

Theorem 2.2.

Assume that all elements of and are positive. Then there is a bijection between the set of all Nash equilibrium points and the set of all pairs of non-zero vectors and , such that

| (9) |

| (10) |

| (11) |

Proof.

Let be a given Nash equilibrium point for the game , . Then and are positive, by assumption that all elements of and are positive. So we may put for each , for each , and define . It is not difficult to verify that satisfies relations (9-11), and each component of this ordered pair is non-zero. Conversely, suppose that non-zero vectors and are given which satisfy relations (9-11). We put , , and define . Then satisfies relations (6-8). It is straightforward to check that the mappings and are inverses of each other. Hence is a bijection as claimed (as is its inverse ). ∎

We remark that the assumption of the above theorem that all elements of and are

positive is not too restrictive. For, if the given payoff matrices

and do not satisfy this assumption, then we could add to all entries of and

a sufficienty large positive constant to ensure and become positive,

without changing the essential nature of the game.

We now focus on describing a method due to Lemke and Howson [27]

for finding a pair of non-zero vectors which satisfy relations (9-11).

We shall also call such a pair of vectors a Nash equilibrium point.

Hereafter we shall use and to denote and , respectively,

and similarly for the corresponding starred variables.

This slight abuse of notation is to ensure consistency with most of the literature

on this subject. Consider the polyhedral sets

and

in and , respectively.

The method of Lemke and Howson is conveniently described in terms of

a labelling process for the vertices of and , originally proposed by Shapley

[37].

Let and be label sets

for agent 1 and agent 2, respectively, and put .

With each vertex of we associate a set of labels from

as follows. For , is given the label if .

For , is given the label if .

With each vertex of we associate a set of labels from as follows.

For , is given the label if .

For , is given the label if .

We say that is nondegenerate if each vertex of satisfies exactly

equations from amongst the

, with , and the

, with .

Similarly, is nondegenerate if each vertex

of satisfies exactly equations from amongst the

, with , and the

, with .

So, if and are both nondegenerate then each vertex of has exactly labels

and each vertex of has exactly labels.

A vertex pair has at most different labels taken altogether, and this number

could be less than if and have nonempty intersection.

A two-agent game defined by and is also called nondegenerate if

the corresponding polyhedral sets and are nondegenerate.

The description of the Lemke-Howson method is simplest in case the game under consideration

is nondegenerate, and we shall assume this hereafter.

Consider pairs of vertices .

We say that is completely labelled if

. The importance of this concept is due to the fact that

is completely labelled if and only if either

or is a Nash

equilibrium point for and (by Equations 10 and 11, and the definition of the

labelling scheme). To avoid the special case, the origin is

termed the artificial equilibrium.

Now let . We say that is -almost completely labelled

if if . A -almost completely labelled vertex

has exactly one duplicate label, that is, exactly one label which belongs to .

The Lemke-Howson algorithm is succinctly, abstractly, but not quite explicitly, described in terms of following a certain path through a graph related to . Indeed, let be the graph comprising the vertices and edges of . Fix some . An equilibrium point (which is completely labelled, as mentioned above) is adjacent in to exactly one -almost completely labelled vertex , namely, that vertex obtained by dropping the label . Similarly, a -almost completely labelled vertex has exactly two neighbours in which are either -almost completely labelled or completely labelled. These are obtained by dropping in turn one component of the unique duplicate label that and have in common. These two observations imply the existence of a unique -almost completely labelled path in from any one given equilibrium point to some other one. (The end points of such a path are completely labelled, but all other vertices on the path are -almost completely labelled.) The Lemke-Howson algorithm starts at the artificial equilibrium . Choosing arbitrarily, it then follows the unique -almost competely labelled path in from , step by step, until it reaches a genuine equilibrium point whereupon it terminates. The following result summarizes the conclusions we may draw from this description.

Theorem 2.3.

Let and represent a nondegenerate game and let be a label in . Then the set of -almost completely labelled vertices together with the completely labelled ones, and the set of edges joining pairs of such vertices, consist of disjoint paths and cycles. The endpoints of the paths are the Nash equilibria of the game, including the artificial one . The number of Nash equilibria of the game is therefore odd.

The above result provides an alternative and constructive proof of Theorem 2.1 in the special case of two-agent nondegenerate games. The algorithm can be described in a computationally explicit way using certain concepts and techniques of the well known simplex method of linear programming.

Lemke and Howson [27] proposed perturbation techniques for dealing with degenerate games. Eaves [17] provided an explicit computational procedure based on these ideas. A clear exposition of this procedure is contained in [28].

For -agent games, with , the problem of finding a Nash equilibrium is no longer of linear character. Thus the Lemke-Howson algorithm cannot be applied directly. Now a Nash equilibrium for an -agent game can be characterized as a fixed point of a certain continuous function from a product of unit simplices into itself. A tractable approach to computing an equilibrium point for such a game can then be based on a path finding technique related to an algorithm of Scarf [36] for finding fixed points of a continuous function defined on a compact set. An exposition of such an approach, known as a simplicial subdivision method, is found in [28].

The methods recalled in this subsection concern computation of a single, so called sample, equilibrium point for a game. Such methods are generally not adaptable to the construction of all equilibria of a given game, however. Methods for locating all equilibria exist – see section 6 of [28].

Homotopy methods for computing equilibria have also been developed [24].

3 Singularities in Economics

In the introduction to Section 2 it was pointed out that a core element of economics is the study of applied problems in optimisation. Here this notion is made explicit by introducing catastrophe theory and its stochastic extension and then game theory and its stochastic extension emphasising the role of singularities in each.

3.1 Catastrophe theory

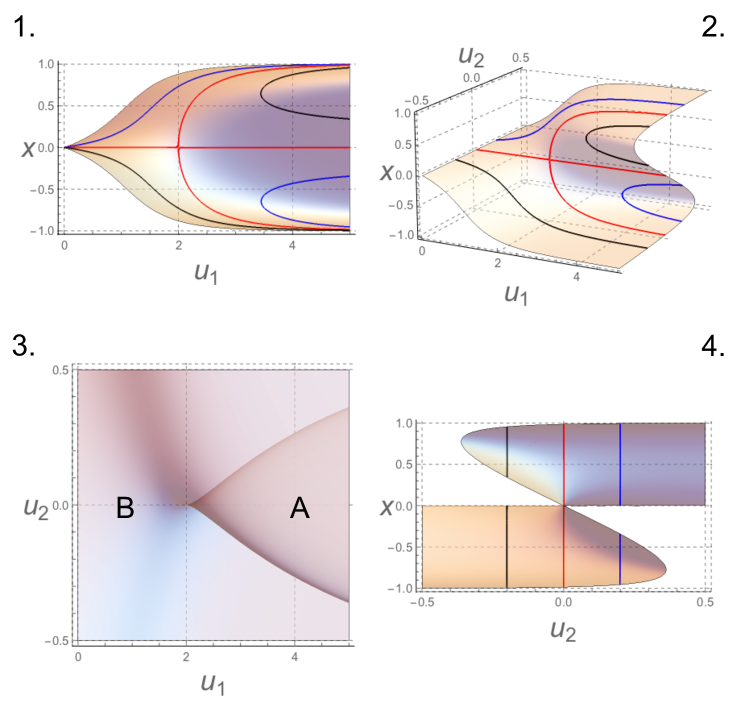

Catastrophe theory was introduced as an approach to economic equilibria through the work of Zeeman in the 1970s [47] in which the attempt was made to explain the dynamics of financial markets using qualitative arguments based on Thom’s earlier work in catastrophe theory. We follow [16] in establishing our general framework. We posit a potential function of a vector of state variables and a vector of control parameters [38]. One of the simplest examples is a system in which there is one (time dependent) state variable and two control parameters and . The dynamics of such a system are given by the ordinary differential equation:

| (12) |

for which the stationary solutions of the system are given by: . The following example is the starting point of recent analyses of asset markets [6, 16]:

| (13) |

The stationary states of the system are the specific that solve the equation:

| (14) |

Figure 2 shows the time independent stationary points as an equilibrium surface that is functionally dependent on the control parameters and .

One of the most important results of Thom’s work was the classification of catastrophes into one of seven elementary catastrophes, catastrophes for families of functions having no more than two state variables and no more than four codimensions. Following Stewart [38] we first give two key definitions needed to state Thom’s theorem, then the theorem is given, and an illustrative example then follows.

Right equivalence: Two smooth () functions and are said to be right equivalent if there is a local diffeomorphism with ( the zero vector) such that for all in some neighbourhood of the origin.

Codimension: If (the germ in the following) is smooth then the codimension of is the smallest for which there exists a -dimensional smooth unfolding

| (15) |

with

| (16) |

which is stable. If no such unfolding exists, the codimension is defined to be . In this way the codimension measures the “degree of instability” of the function .

Theorem 3.4.

[39] Let be a smooth stable family of functions each of which has a critical point at the origin, and suppose that . Set for all in near the origin. Then is right equivalent, up to a sign, to one one of the germs in Table 1.

| Catastrophe name | Germ () | Codimension | Unfolding () |

|---|---|---|---|

| Fold | 1 | ||

| Cusp | 2 | ||

| Swallow tail | 3 | ||

| Butterfly | 4 | ||

| Hyperbolic umbilic | or | 3 | |

| Elliptic umbilic | 3 | ||

| Parabolic umbilic | 4 |

The terms are control variables and the and are state variables. Further, is right equivalent, up to sign, to the expression on the same line as in Table 1 (where right equivalence of function families is defined in a similar sense to that of functions). In this table the catastrophes describe the geometry of the projection onto control parameter space of the surface defined by the partial derivative: .

The unfolding of results in the cusp catastrophe. A surprising result is that the Taylor series does not need to converge on or indeed any function and so the importance of this proof lies in the fact that a truncated Taylor series expansion provides a qualitatively (topologically) correct description of a system given by Equation 12. This is the case because this family, as do all of the elementary catastrophes, has the stability property that for sufficiently small perturbations of the topology is left unaffected.

Thom’s approach can be illustrated with a simple example from [38]. Suppose we are given a smooth stable potential function with one state variable and two control variables , . Regarding as a function family parametrised by and , suppose that each member of the family has a critical point at the origin, and that higher order terms in . Then, according to Thom’s theorem, the function is right equivalent to , and the function family is right equivalent to the unfolding , for (possibly) adjusted state and control variables , and .

When catastrophe theory is applied to specific problems in the applied fields, the following interpretation of Thom’s theorem is very useful (after [38, pg. 151]. The germ , when observed in applications, might be topologically unstable in the sense that small perturbations to the system might result in qualitatively different behaviours. So in practice, if we observe we should also expect to see the rest of its unfolding as well, and this unfolding will be a topologically stable and qualitatively complete description of the system. We note that Berry [7] has made the rather fascinating observation that a ‘battle of the catastrophes’ emerges as a parameter varies through the catastrophe set on the singularity surface. That this generates power-law tails in a very specific fashion may have applications not yet explored.

3.2 Stochastic Catastrophe Theory

Catastrophe theory is a deterministic approach to modelling a system’s dynamics but Cobb [9] was the first to extend catastrophe theory to stochastic differential equations which was later improved upon by Wagenmakers et al. [43]. The approach is to add noise to the evolutionary dynamics:

| (17) |

where is the drift function, is a diffusion process and parameterises the strength of the diffusion process. The stationary probability distribution is given by [43]:

| (18) | |||||

| (19) | |||||

| (20) |

Here normalises the probability distribution, in Equation 18: , Equation 19 is a simplification in which: constant in , and is the stochastic potential for the special case of being constant.

A potential function is necessary for catastrophe theory in order for there to be a gradient dynamic in Equation 12, this is equivalent to the symmetry of the Slutsky matrix [1] of economics. This symmetry is known to hold for potential games [35] and so a potential function exists. The existence of a potential function is also equivalent to the existence of a Lyapunov function. If a (local) Lyapunov function does not exist then this is a significant obstacle to the use of catastrophe theory, however Thom has answered this objection [41] by pointing out that near any attractor of any dynamical system there exists a local Lyapunov function. In evolutionary game theory, a dynamical extension to (static) economic game theory, a Lyapunov function can always be found for linear fitness functions that are of the type in Equation 2. The principal problem then is to confirm whether or not such a local Lyapunov function exhibits the bifurcation behaviour of catastrophe theory, and in general the answer is no [20]. Although this article covers what is properly called ‘elementary catastrophe theory’, Thom hinted [41] that there may be ways to accommodate these issues within the larger set of catastrophe theory that his methods encompass. It appears to still be an open question as to what extent catastrophe theory can be extended to accommodate these issues.

3.3 Bifurcations in Nash equilibria

To illustrate how bifurcations in the number of fixed points occur in the Nash equilibria of games we will use games, these games are described by two payoff matrices, one for each agent. Specifically, we consider normal form, two agent, non-cooperative games in which the agents select between one of two possible choices (pure strategies): . We refer to these games as . The joint choices determine the utility for each agent , . The choices available to the agents and their subsequent payoffs are given by agent 1’s payoff matrix:

| agent | |||

|---|---|---|---|

| agent | |||

and agent 2’s payoff matrix:

| agent | |||

|---|---|---|---|

| agent | |||

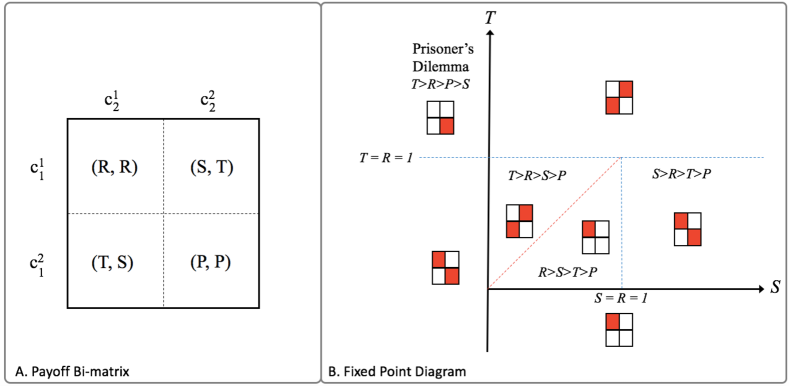

Both matrices are often more compactly written as a single bi-matrix, for example the following bi-matrix is the well known Prisoner’s Dilemma game where the vectors of joint payoffs are written :

| agent | |||

|---|---|---|---|

| cooperate | defect | ||

| agent | cooperate | ||

| defect | |||

In the extended form of , in which:

| (21) |

is an upper-hemicontinuous space222Upper-hemicontinuity does not hold if only discrete strategies can be used, and in order to use Kakutani’s fixed point theorem it is a necessary condition that the agent’s strategies are upper-hemicontinuous, the bi-matrix representation is only useful in describing the discrete valued payoffs.

In order to see how singularities can occur in game theory we parameterise the payoff values in each agent’s payoff matrix in such a way that allows for two control parameters and one state variable for each agent, i.e. the expected utility , at each Nash equilibrium, this approach is shown in Figure 3. Note that generally there are either one or three Nash equilibrium and Figure 3 only shows the pure strategy Nash equilibria of the games. In the case where there are two pure strategy Nash equilibria then there is also a third mixed strategy Nash equilibria that is not shown in Figure 3.

To illustrate the change in the number of fixed points, begin by looking at the Prisoner’s Dilemma game in the top left of the diagram. At this point but as increases and passes through two new pure strategy Nash equilibria form at the and pure strategies and a third mixed strategy equilibria forms that is not shown. Alternatively, beginning again from the Prisoner’s Dilemma but decreasing from to the original pure strategy at remains but a new pure strategy equilibrium forms at , as well as a mixed strategy equilibrium that is not shown. From this region of the game space, providing , then letting increase from to we see that there remains three equilibrium points but the two pure strategy equilibria at and switch to and . Other transitions in the state space follow similar patterns.

3.4 Quantal Response Equilibrium

The quantal response equilibrium (QRE) is an extension of the Nash equilibrium concept developed by McKelvey and Palfrey [29] in which agents do not perfectly optimise their choices, as in the Nash equilibrium, but instead there is some error in the choice they make, represented by stochastic uncertainty in their choices. The Nash equilibrium is recovered as a parameter representing the uncertainty in the decision tends to infinity, and so the Nash equilibria are a subset of the fixed points given by the QRE.

There are several different methods by which the QRE can be arrived at, McKelvey and Palfrey used differential topology and recent work by one of the authors used the method of maximising the entropy [46, 22]. For our purposes we will simply define the relevant terms and state the Logit functional form of the QRE. We note that there is nothing special in this form of the QRE correspondence. It is to be expected that all of the work in the current article, in particular the analysis of bifurcations parameterised by a noise term , will carry across to any regular QRE functional form.

Agent ’s expected utility can be said to be conditional on ’s discrete choice : . The interpretation of is that it is the expected utility to agent if they choose , i.e. they fix , while all of the other agents maintain a (possibly mixed) joint strategy . The definition of the equilibrium points given by the QRE are then the joint distributions given by:

| (22) |

This satisfies the criteria of a probability distribution over agent ’s space of choices and the exponentiated function is the product of a control parameter specific to each agent and a gradient , cf. Equations 18-20. The parameter controls the level of noise or uncertainty the agent has in selecting each strategy, when the agent selects uniformly across their choices and when the Nash equilibria of the game are recovered. For intermediate values of the agent prefers (up to some statistical uncertainty) one strategy over another only if it has a higher payoff, assuming all other agents are playing a known distribution over their own strategies. The probability is conditional on to remind us that the distribution has one free control parameter.

Bifurcations in the QRE were first analysed by McKelvey et al [30] (the chicken game discussed next) and a pitchfork bifurcation in the battle of the sexes game is covered in [18, Figure 6.3, page 153]. The equilibrium points in these plots were computed using the symbolic mathematics package Mathematica, however we note that there is also some very interesting work on computation of (Logit) QRE using homotopy methods. These methods can also be used to compute Nash equilibria, as limit points of the QRE, see [42], cf. Section 2.2. For our purposes the battle of the sexes serves to illustrate the bifurcations that can occur in the QRE as a covector of parameters are varied. The payoff bi-matrix for discrete strategies is given by:

| agent | |||

|---|---|---|---|

| Swerve | Straight | ||

| agent | Swerve | ||

| Straight | |||

This game represents interactions between two people, such as the game often seen in movies where drivers of two cars are heading directly towards one another. The challenge is for each driver to choose either straight or swerve, the driver who chooses straight wins and the driver who swerves loses. If they both choose to swerve the game is a draw, if they both choose straight both drivers crash into each other and lose. There are two pure strategy Nash equilibria: one where agent 1 swerves while agent 2 goes straight, the other where agent 1 goes straight while agent 2 swerves. These can be identified immediately by noting that, for either swerve, straight or straight, swerve neither agent can achieve a higher payoff by unilaterally changing their choice while the other agent’s choice remains fixed. There is also a mixed strategy equilibrium.

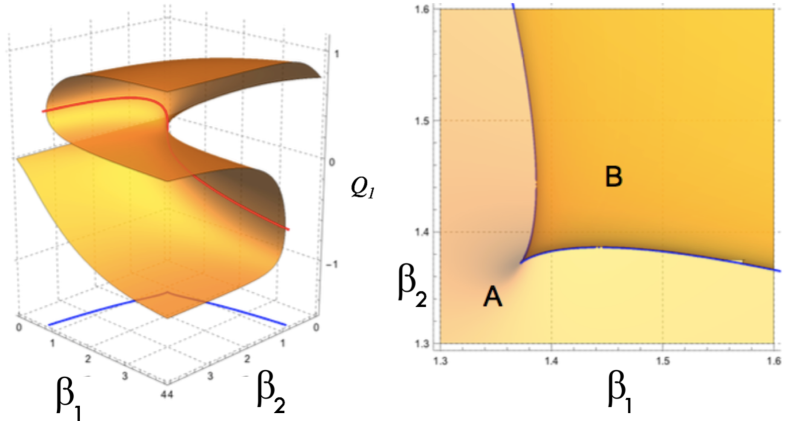

When these game parameters are put into the QRE it can be shown that there is one fixed point for and three fixed points for , these three fixed points correspond to the Nash equilibria of the Chicken game. In varying these parameters away from zero and towards there is necessarily some values of these parameters at which new fixed points emerge, a subset of these are shown in Figure 4. This bifurcation diagram was hinted at in McKelvey and Palfrey’s original work and recent work by Wolpert and Harré has explored some of the variety of this system of equations [45, 46, 21, 22].

To show this for games, first we rescale the probabilities so that: for the probability of one of agent ’s choices so that we can work with a single variable for each agent and we write the QRE as the functional relationships:

| (23) | |||||

| (24) | |||||

| (25) | |||||

| (26) |

To find the set of singular points of the QRE surface we compute the Jacobian of the system by first finding all four terms of the form , for example [45]:

| (27) | |||||

| (28) | |||||

| (29) |

The simplification in notation at equation 28 uses the subscript to denote either the first or the second argument of in equations 23 and 25 that differentiation is with respect to. A similar set of computations results in the Jacobian:

| (30) |

which is singular when . This set of solutions is shown as the red curve in the left plot of Figure 4 and the projection of this set onto the control plane is shown in the right plot. When game theory is used as the basis for the construction of macroeconomic models of an economy this set is called the critical set of the economy. Sard’s theorem allows us to conclude that the critical set of economies has measure zero [13, 14]

.

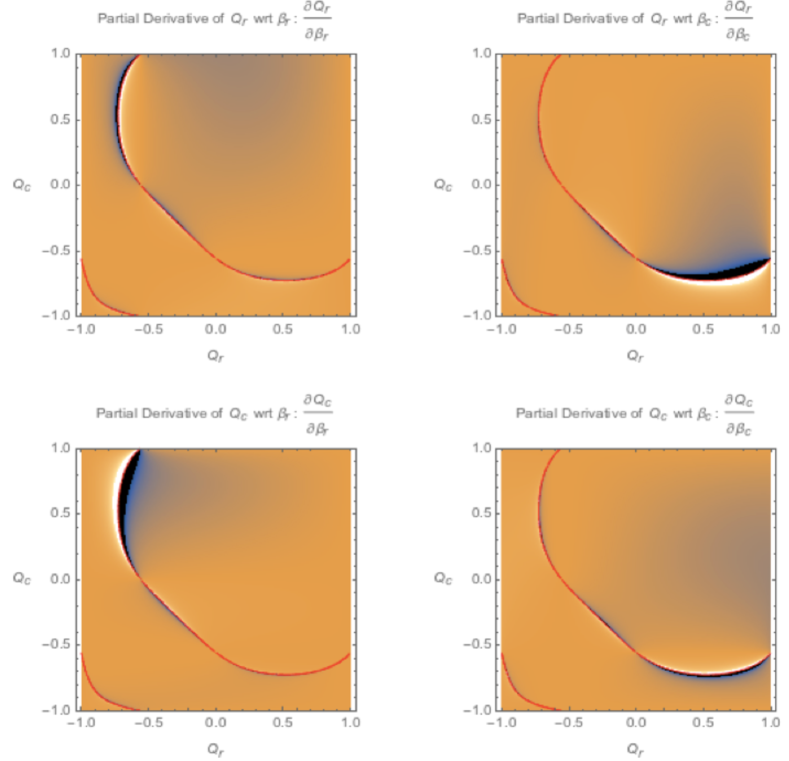

Figure 4 is one of the two mappings . An alternative representation is to consider the map where is the family of matrices of partial derivatives for games. This can be plotted directly as shown in Figure 5 where we have used the Chicken game as an example. In order to generate these plots, a large number of explicit values for were calculated and plotted, the results generate the background (golden-tan) colouring of the plots. Then the singularity set was calculated by implicitly solving the equation and overlaying these results on the plot of . It can be seen that where diverges is where .

One of the interesting points that arises in the representation of Figure 5 is that, except possibly at finite and isolated points, the critical economic states partitions the space into three parts. An interpretation of this is that, if all you can observe of an economy is its distribution over states (the ’s) then moving smoothly about this space is restricted by the partitions, there are states of the economy that are not accessible from a regular economy without passing through a critical state of the economy.

4 Discussion

The application of deterministic catastrophe theory to economics has a fraught history that has been well documented [33] but there are a number of articles that have been published recently that have begun a counter-swing in applications [34, 44, 25, 16, 26, 5] as well as some theoretical work [26]. In this article we have sought to briefly cover some of the recent material that has not elsewhere been collected in the hope that it might stimulate theoretical work to complement recent applied research.

We note that the original catastrophe theory, either deterministic or stochastic, is somewhat limited for direct economic application. The singularities that are traditionally studied require a priori assumptions on the potential function that may not be easily justified in an economic context. In particular, there is no agent-agent interaction explicit in the formulations of the potential function, and these interactions are central to economics.

On the other hand, the QRE has notable similarities with stochastic catastrophe theory. The similarities in the structures of equations 20 and 22 are notable, but their interpretation is not equivalent. Equation 20 is a single equation with a non-linear potential function whereas Equation 22 is a set of equations with linear interaction terms.

It might be tempting to assume that the exponentiated terms in these equations are both potentials, and a potential function is a necessary condition for the use of catastrophe theory, however this is also not immediately obvious. Ay et al [4] derived a potential function for game theory of the general form:

| (31) |

where is a (constant valued) payoff matrix that describes all of the interactions between agents and the are the strategies of the agents. In this case, in order for to be a potential function the following relationship needs to hold:

| (32) |

This condition is met if the matrix is symmetric. The relationship between these equations and their interpretations has yet to be explored.

These considerations have restricted the family of games to which catastrophe theory can be applied to those with symmetric payoff matrices. In economic theory, this is known to be satisfied by only a few games, in particular the potential games of Sandholm [35] and a few other examples given in Rosser Jr. [33]. In general, the adoption of catastrophe theory in economics has been infrequent and very few examples beyond the cusp catastrophe have been studied (see [8] for a notable exception using the Butterfly catastrophe applied to housing markets). However, as Rosser Jr. has pointed out, there is considerable value to be had in adding catastrophe theory to the tool box of methods that economists use. More generally, there is a great deal of untouched territory in the formal analysis of the dynamics of economic systems near market crashes (singularities) in which there have been rapid and at times uncontrolled transitions between stable economic states in recent times.

Acknowledgement: We are very thankful for the support of Laurentiu Paunescu and the diversity of people who were brought together for the JARCS workshop. M.S. Harré was supported by ARC grant DP170102927.

Addendum: Some elementary remarks on the analytical foundations of Quantal equilibrium theory for -games.

This section will reiterate in the simplest possible terms the thread of mathematical ideas running through sections 3.3 and 3.4, connecting Game Theory as represented by elementary -games to singularities, via the quantal approach to equilibria proposed by McKelvey and Palfrey. Hence we will consider only two players, each with the freedom to choose two strategies. The terms player and strategy (not to mention game) have always been interpreted somewhat abstractly. The first of these could easily be replaced by agent or particle ensemble without any loss of information. Similarly the word “strategy” could easily be replaced by state. We will see that an appropriate choice of terms has everything to do with the manner in which equilibrium is defined in relation to a specific mathematical model. Every -game corresponds to a unique pair of utility matrices over the real numbers. The “pure” strategies for each player are unit vectors and whereas “mixed” strategies are pairs such that and . The utility functions are then defined as a standard inner product

Since , these formulae reduce to a pair of quadratic functions whose domain is restricted to the unit square , such that and . Now define

and introduce non-decreasing, piecewise-continuous functions , such that

Finally, let , , and define a map such that . An equilibrium strategy (or equilibrium state) will then correspond to a fixed point

Two special cases are of particular interest here. First, suppose the are defined in terms of the Heaviside function with parameter :

so that

This in fact defines the “best response” map in Nash’s theory of equilibria. Note that

and

Since the are linear functions, these relations indicate that apart from the pure-strategy Nash-equilibria to be found among the vertices of , a unique mixed-strategy Nash equilibrium occurs precisely when . The choice of is well-suited to the classical conception of game theory, in which equilibria are “rationally optimized” strategies available to both players.

We turn now to a second model, in which players do not rationally fix their strategy in response to that of their opponent. Instead, strategies are governed by a smooth probability distribution. Applied to a large sample space of random trials of a specific game, this model may or may not realistically reflect the behaviour of human populations, though it is naturally adapted from numerically large particle-ensembles of the kind encountered in statistical thermodynamics. A standard probability distribution associated with the partition function which lies at the foundation of this theory is given as

where the parameters are strictly positive real numbers. Note that

and similarly

may be interpreted as the probability that ensemble 2 lies in state 1, given that the probability of ensemble 1 lying in the same state is . Conversely represents the probability that ensemble 1 lies in state 1, given a probability that ensemble 2 lies in the same state. Given two events and , the symmetry between the classical definitions of conditional probabilities and simply occurs when , where in general the probability of one event is construed as conditional on the actual occurrence of the other, as implied by Bayes’ Theorem. By contrast, the model above estimates the probability of one event as conditional on a given probability of the other, as is traditionally postulated in the world of quantum interactions. Symmetry occurring in the relations and is then another way of characterizing points of equilibrium. Since is a closed and bounded subset of , and in the present situation is a continuous map, the existence of fixed points is implied by the fact that any sequence of iterations where , must have a convergent subsequence. This is essentially the Fixed Point Theorem of Brouwer. Note, however, that if the distributions are not strictly continuous, as in the case of Nash equilibria, then the more general theorem of Kakutani may still be applied. With respect to an appropriately chosen norm on function-space, the Heaviside distribution may in fact be recovered as an asymptotic -limit of the smooth distribution above. For generic values of the number and location within of the fixed points of (for a given choice of the matrices ) will depend smoothly on these parameters, which suggests that the set of fixed points for each will generate a possibly branched topological covering of the parameter-plane, corresponding to the surface

where . Now let

According to the Implicit Function Theorem,

implies the existence of a function in a neighbourhood of . Similarly,

implies the existence of a function in a neighbourhood of . Hence, in a neighbourhood of any regular equilibrium point , the surface is parametrized smoothly by functions .

Conversely, for every belonging to the critical locus

the standard projection maps to the “branch locus”

In this formulation of equilibrium without reference to a potential function, there is no apparent classification of critical loci in terms of Thom’s elementary catastrophes. The projection above suggests rather that the branch locus might be understood via normal forms of generic mappings between smooth surfaces, as in the classic Theorem of Whitney (cf., e.g. [19]). This would seem to be the case for games of the sort represented in Fig. 4, but the general situation is not immediately clear. In particular, it must be asked whether all mappings which arise in the context above for -games are in fact generic, in the sense that their first jet extension is always transversal to the corank-one submanifold inside the jet space .

References

- [1] Sydney N Afriat. Demand Functions and the Slutsky Matrix.(PSME-7), volume 7. Princeton University Press, 2014.

- [2] Vladimir I Arnol’d. Catastrophe theory. Springer Science & Business Media, 2003.

- [3] Vladimir Igorevich Arnold. Singularities in optimization problems, the maxima function. In Catastrophe Theory, pages 43–46. Springer, 1984.

- [4] Nihat Ay, Jürgen Jost, Hông Vân Lê, and Lorenz Schwachhöfer. Information geometry, volume 64. Springer, 2017.

- [5] Jozef Barunik and Jiri Kukacka. Realizing stock market crashes: stochastic cusp catastrophe model of returns under time-varying volatility. Quantitative Finance, 15(6):959–973, 2015.

- [6] Jozef Baruník and M Vosvrda. Can a stochastic cusp catastrophe model explain stock market crashes? Journal of Economic Dynamics and Control, 33(10):1824–1836, 2009.

- [7] MV Berry. Universal power-law tails for singularity-dominated strong fluctuations. Journal of Physics A: Mathematical and General, 15(9):2735, 1982.

- [8] John Casti and Harry Swain. Catastrophe theory and urban processes. In IFIP Technical Conference on Optimization Techniques, pages 388–406. Springer, 1975.

- [9] Loren Cobb. Stochastic catastrophe models and multimodal distributions. Systems Research and Behavioral Science, 23(4):360–374, 1978.

- [10] Bruno Codenotti. Computational game theory, 2011.

- [11] Partha Sarathi Dasgupta and Eric S Maskin. Debreu’s social equilibrium existence theorem. Proceedings of the National Academy of Sciences, 112(52):15769–15770, 2015.

- [12] Gerard Debreu. Economies with a finite set of equilibria. Econometrica: Journal of the Econometric Society, pages 387–392, 1970.

- [13] Gerard Debreu. Regular differentiable economies. The American Economic Review, 66(2):280–287, 1976.

- [14] Gerard Debreu. Economic theory in the mathematical mode. The Scandinavian Journal of Economics, 86(4):393–410, 1984.

- [15] Gerard Debreu. Theory of value: An axiomatic analysis of economic equilibrium. Number 17. Yale University Press, 1987.

- [16] Cees Diks and Juanxi Wang. Can a stochastic cusp catastrophe model explain housing market crashes? Journal of Economic Dynamics and Control, 69:68–88, 2016.

- [17] B Curtis Eaves. The linear complementarity problem. Management science, 17(9):612–634, 1971.

- [18] Jacob K Goeree, Charles A Holt, and Thomas R Palfrey. Quantal response equilibria. Springer, 2016.

- [19] Martin Golubitsky and Victor Guillemin. Stable mappings and their singularities, volume 14. Springer Science & Business Media, 2012.

- [20] John Guckenheimer. Catastrophes and partial differential equations. Ann. Inst. Fourier, 23(2):31, 1973.

- [21] Michael S Harré, Simon R Atkinson, and Liaquat Hossain. Simple nonlinear systems and navigating catastrophes. The European Physical Journal B, 86(6):1–8, 2013.

- [22] Michael S Harré and Terry Bossomaier. Strategic islands in economic games: Isolating economies from better outcomes. Entropy, 16(9):5102–5121, 2014.

- [23] Ch Hauert. Fundamental clusters in spatial 2 2 games. Proceedings of the Royal Society of London B: Biological Sciences, 268(1468):761–769, 2001.

- [24] P Jean-Jacques Herings and Ronald Peeters. Homotopy methods to compute equilibria in game theory. Economic Theory, 42(1):119–156, 2010.

- [25] A Jakimowicz. Catastrophes and chaos in business cycle theory. Acta Physica Polonica, A., 117(4), 2010.

- [26] AN Kudinov, VP Tsvetkov, and IV Tsvetkov. Catastrophes in the multi-fractal dynamics of social-economic systems. Russian Journal of Mathematical Physics, 18(2):149–155, 2011.

- [27] Carlton E Lemke and Joseph T Howson, Jr. Equilibrium points of bimatrix games. Journal of the Society for Industrial and Applied Mathematics, 12(2):413–423, 1964.

- [28] Richard D McKelvey and Andrew McLennan. Computation of equilibria in finite games. Handbook of computational economics, 1:87–142, 1996.

- [29] Richard D McKelvey and Thomas R Palfrey. Quantal response equilibria for normal form games. 1995.

- [30] Richard D McKelvey and Thomas R Palfrey. A statistical theory of equilibrium in games. The Japanese Economic Review, 47(2):186–209, 1996.

- [31] John Nash. Non-cooperative games. Annals of mathematics, pages 286–295, 1951.

- [32] John F Nash. Equilibrium points in n-person games. Proceedings of the national academy of sciences, 36(1):48–49, 1950.

- [33] J Barkley Rosser. The rise and fall of catastrophe theory applications in economics: Was the baby thrown out with the bathwater? Journal of Economic Dynamics and Control, 31(10):3255–3280, 2007.

- [34] J Barkley Rosser. From catastrophe to chaos: a general theory of economic discontinuities. Springer Science & Business Media, 2013.

- [35] William H Sandholm. Potential games with continuous player sets. Journal of Economic theory, 97(1):81–108, 2001.

- [36] Herbert Scarf. The approximation of fixed points of a continuous mapping. SIAM Journal on Applied Mathematics, 15(5):1328–1343, 1967.

- [37] Lloyd S Shapley. A note on the lemke-howson algorithm. In Pivoting and Extension, pages 175–189. Springer, 1974.

- [38] Ian Stewart. Catastrophe theory. Math. Chronicle, 5:140–165, 1977.

- [39] Rene Thom. Structural stability and morphogenesis, 1975. Trans. by D. Fowler. Reading, Mass.: Benjamin, 1975.

- [40] René Thom. Structural stability and morphogenesis, 1976.

- [41] René Thom. Structural stability, catastrophe theory, and applied mathematics. SIAM review, 19(2):189–201, 1977.

- [42] Theodore L Turocy. A dynamic homotopy interpretation of the logistic quantal response equilibrium correspondence. Games and Economic Behavior, 51(2):243–263, 2005.

- [43] Eric-Jan Wagenmakers, Peter CM Molenaar, Raoul PPP Grasman, Pascal AI Hartelman, and Han LJ van der Maas. Transformation invariant stochastic catastrophe theory. Physica D: Nonlinear Phenomena, 211(3):263–276, 2005.

- [44] Alan Wilson. Catastrophe Theory and Bifurcation (Routledge Revivals): Applications to Urban and Regional Systems. Routledge, 2012.

- [45] David Wolpert, Julian Jamison, David Newth, and Michael Harré. Strategic choice of preferences: the persona model. The BE Journal of Theoretical Economics, 11(1), 2011.

- [46] David H Wolpert, Michael Harré, Eckehard Olbrich, Nils Bertschinger, and Juergen Jost. Hysteresis effects of changing the parameters of noncooperative games. Physical Review E, 85(3):036102, 2012.

- [47] E Christopher Zeeman. On the unstable behaviour of stock exchanges. Journal of mathematical economics, 1(1):39–49, 1974.