Distributions of Historic Market Data – Relaxation and Correlations

Abstract

We investigate relaxation and correlations in a class of mean-reverting models for stochastic variances. We derive closed-form expressions for the correlation functions and leverage for a general form of the stochastic term. We also discuss correlation functions and leverage for three specific models – multiplicative, Heston (Cox-Ingersoll-Ross) and combined multiplicative-Heston – whose steady-state probability density functions are Gamma, Inverse Gamma and Beta Prime respectively, the latter two exhibiting ”fat” tails. For the Heston model, we apply the eigenvalue analysis of the Fokker-Planck equation to derive the correlation function – in agreement with the general analysis – and to identify a series of time scales, which are observable in relaxation of cumulants on approach to the steady state. We test our findings on a very large set of historic financial markets data.

keywords:

Stochastic Mean-Reverting Models , Correlations , Relaxation , Steady-State Distribution , Generalized Beta Prime1 Introduction

Questions about correlations between and relaxation of quantities described by stochastic differential equations (SDE) have a very long history in physics applications [1], [2]. More recently, they found a new urgency in areas related to economics [3, 4, 5, 6, 7] and finance [8, 9, 10, 11], some of which utilized models originally found in physics. In the most general formulation, one is interested in correlations in the time series generated by a stochastic process, described by an SDE, and in the time scales for relaxation to its steady state. Ideally, one would obtain an analytical expression for the correlation function in terms of the parameters of an SDE and would identify quantities that analytically describe relaxation.

A common purpose of an SDE is to model empirical time series, such as stock prices. Stochastic models for stock returns use stochastic volatility as one of their inputs. In this paper we concentrate on a class of models for stochastic variance – squared stochastic volatility – which are characterized by the Generalized Beta Prime steady-state probability density function and its limits corresponding to their mean-reverting subset: Inverse Gamma, Gamma and Beta Prime distributions. We use readily-available historic stock prices data to test our predictions with respect to the correlation functions and leverage, which we derive analytically for these models. In particular, we study both daily and multi-day correlations and leverage.

This paper is organized as follows. In Section 2, we identify equations for the covariance of stochastic variance and for the leverage for a general form of stochastic term. We show that the correlation function of stochastic variance depends only on the relaxation parameter. We relate correlations of realized variance for daily and multi-day returns to correlations of stochastic variance. In Section 3, we proceed to apply general equations obtained in Section 2 to specific stochastic terms of mean-reverting models – multiplicative, Heston, and combined multiplicative-Heston – and derive their parameters from the historic market data. In A, we continue the discussion of correlations of multi-day returns introduced in Section 2. In B, we discuss Heston model in greater detail: we find correlations of stochastic variance using eigenvalues analysis of the Fokker-Planck equation as well as study the relaxation of cumulants and the distribution of relaxation times.

2 Correlations of Stochastic Variance and Leverage

Equation for de-trended stock log returns can be written as [12]

| (1) |

where is a normally distributed Wiener process and is the stochastic volatility which is related to the stochastic variance by . A general mean-reverting model for the stochastic variance can be written as

| (2) |

and rewritten as

| (3) |

It is assumed that and are cross-correlated, with the coefficient , as

| (4) |

where is independent of . In (2), is the relaxation parameter: is the time scale for achieving the steady-state distribution of [6], whose mean value is ,

| (5) |

| (6) |

which directly relates to stock returns data.

2.1 Correlation Function of Stochastic Variance

Using (3), we find the covariance of stochastic variance as

| (7) |

where

| (8) |

so that the correlation function (Pearson correlation coefficient) depends only on the relaxation parameter

| (9) |

To obtain from stock returns we observe that from (1)

| (10) |

which yields

| (11) |

for and

| (12) |

for . The factor of 3 in (12) is purely combinatorial and is model-independent. (In general, [12]). In (11) and (12) we replaced with – the number of days accumulation of returns. In what follows we will use and interchangebly. Specifically for daily returns, , the second equation in (11) is the one obtained in [10]. It follows then from (6) and (9)-(12) that for daily returns

| (13) |

|

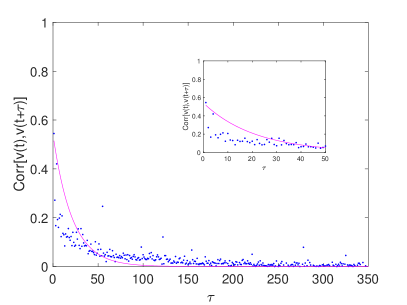

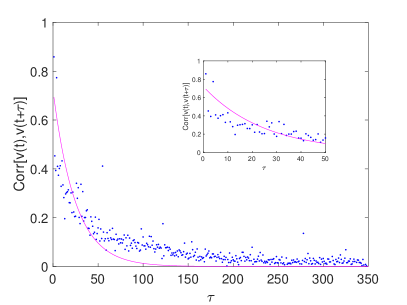

Fig. 1 show plots and their fits for the l.h.s. of (13) for daily returns. It is obvious that the fit is rather poor relative to the analytical prediction. This is mostly likely because mean-reverting, continuous stochastic volatility models are not appropriate for daily returns. On the other hand, such models are more relevant to multi-day returns. Consequently, it is of interest to investigate correlations of multi-day returns. Toward this end, we first discuss the consequences of (11). From the latter, we find that for , that is ,

| (14) |

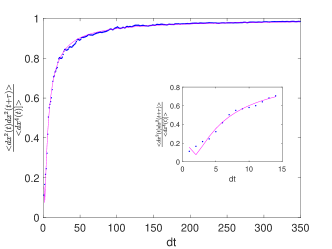

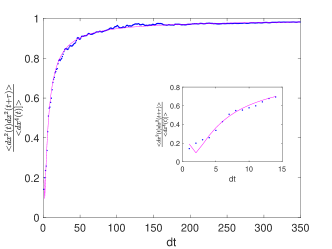

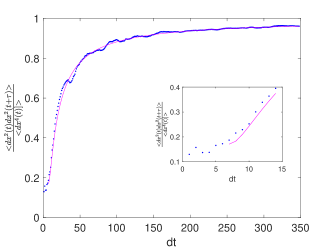

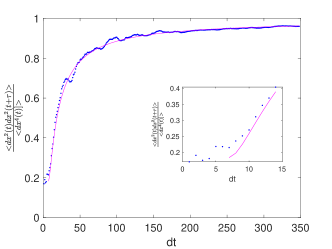

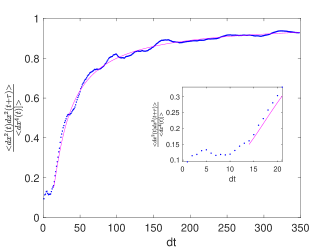

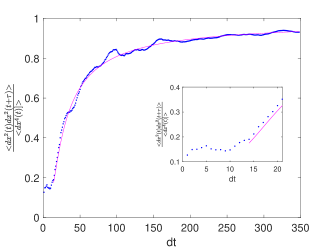

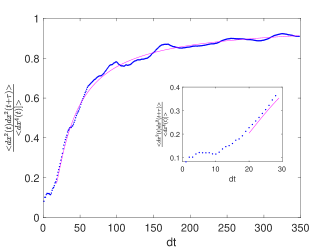

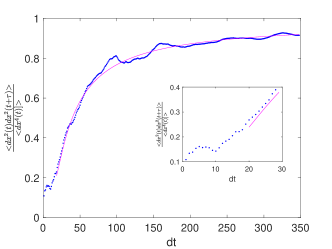

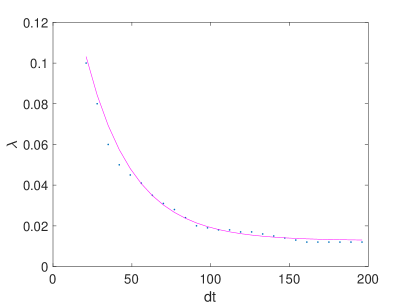

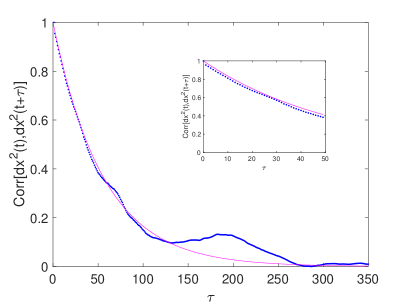

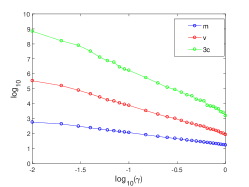

Fig. 2 shows the dependence of the l.h.s. of (14) as a function of the number of days of accumulation for respectively and their fits for with with the values of fitting parameters and statistics collected in Table 1. Clearly, predictions of (14) hold up quite well.

|

|

|

|

| DJIA | ||||

|---|---|---|---|---|

| a | b | c | ||

| 1 | 0.99 | 4.92 | 6.48 | 0.99 |

| 7 | 0.99 | 1.65 | 0.83 | 0.99 |

| 14 | 0.98 | 1.40 | 0.56 | 0.99 |

| 21 | 0.98 | 1.34 | 0.53 | 0.99 |

| S&P500 | ||||

|---|---|---|---|---|

| a | b | c | ||

| 1 | 0.99 | 4.87 | 6.52 | 0.99 |

| 7 | 0.99 | 1.61 | 0.79 | 0.99 |

| 14 | 0.98 | 1.35 | 0.54 | 0.99 |

| 21 | 0.98 | 1.30 | 0.53 | 0.99 |

Due to the complicated nature of relationship between and in (11), it is unclear how to express the result for in (9) in terms of market quantities for multi-day returns. Instead we surmised that may have a similarly clean dependence on time

| (15) |

In A we empirically investigate the dependence of on the number of days of return.

2.2 Leverage

We now turn to leverage effect, whose main ”prize” is the cross-correlation , but which also allows to independently evaluate . Leverage is defined as

| (16) |

A priori, it is clear that should be negative as upward fluctuations of volatility should lead to downward fluctuations in returns and that it should decay exponentially in time. Market leverage was studied in great detail in [8, 9, 10]. We believe that functional derivative in (7) of [9] can be greatly simplified – to in our notations – so that the (16) reduces to

| (17) |

3 Multiplicative, Heston and Combined Models of Stochastic Variance

3.1 Analytical results

Expressions 8 and 17 in Section 2 did not specify the form of and it is a priori clear that relaxation of the covariances should depend only on the single relaxation time parameter in the model, . A very general model of stochastic volatility is given by

| (18) |

Its steady-state distribution (probability density function – PDF) is a Generalized Beta Prime, or GB2, distribution given by [13, 14, 15, 16]

| (19) |

where is a beta function. GB2’s scale parameter is

| (20) |

and its shape parameters are ,

| (21) |

and

| (22) |

The steady-state distribution of (18) is Generalized Inverse Gamma (GIGa) for [5, 11] and Generalized Gamma (GGa) for .

For we return to the mean-reverting – multiplicative-Heston [12] – model

| (23) |

Its steady-state distribution is Beta Prime (BP)

| (24) |

with the scale parameter

| (25) |

and shape parameters,

| (26) |

and

| (27) |

It is required that , since PDF must be zero at . (This condition also assures that the distribution has a bell shape.) We also require that , that is which assures that variance exists. For multiplicative model, , the steady-state distribution of (23) is Inverse Gamma (IGa) and for Heston model (Cox-Ingersoll-Ross model of volatility), , it is Gamma (Ga) [17, 18, 19, 20, 21].

In this Section we will consider ”reduced” covariance , that is (compare with (9)). The reason is that we want to use the market data to determine model parameters. In what follows, the discussion will be limited to the mean-reverting models. Using (7) and 8, we find for the multiplicative-Heston model

| (28) |

The result for multiplicative and Heston models can be recovered by setting and respectively:

| (29) |

| (30) |

To find leverage, we use (17). For multiplicative-Heston model we find

| (31) |

The result for multiplicative and Heston models can be recovered by setting and respectively or by calculating directly with (17) (for Heston model, see also [9]). We find

| (32) |

where is the gamma function, and

| (33) |

for multiplicative and Heston model respectively.

3.2 Numerical Fitting

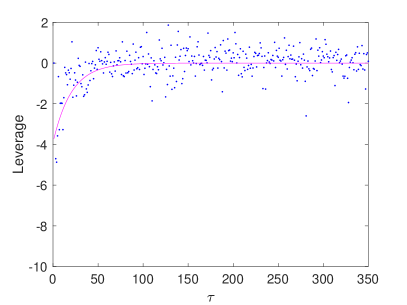

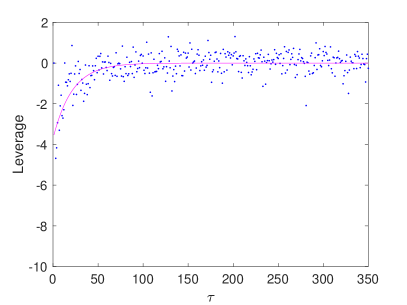

We use market data for daily returns. For our numerical fitting we adopt the following procedure:

-

1.

We use obtained in Sec. 2.1;

-

2.

We use (6) to obtain ( that is, );

-

3.

We use the second of (11) to obtain ;

-

4.

We fit with to determine ;

- 5.

- 6.

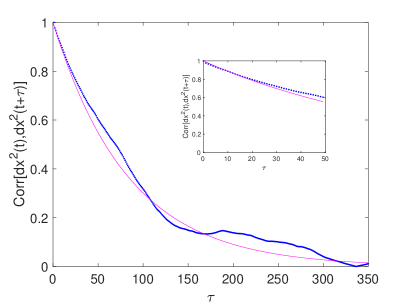

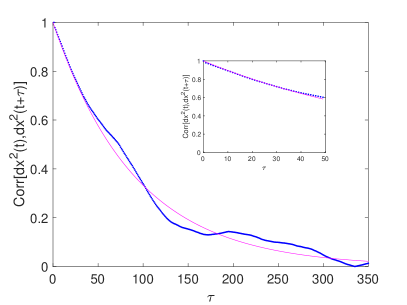

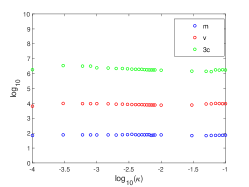

Fig. 3 shows plots of and leverage and their fits and the results of the above fitting procedure are summarized in Table 3.2. Notice that we use only multiplicative and Heston models since for the combined multiplicative-Heston model we can not independently find and using this procedure. However, we can determine those for the combined multiplicative-Heston model as a function of the number of days of returns, beginning with daily returns, using the stocks returns distribution function associated with this model and its BP steady-state distribution [12].

|

|

| DJIA Parameters | |

|---|---|

| Parameters | |

| S&P Parameters | |

|---|---|

| Parameters | |

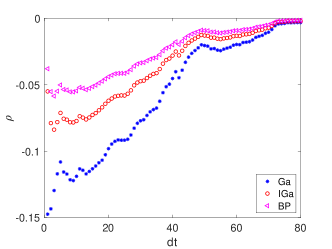

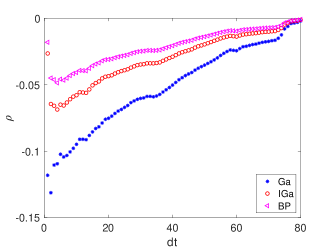

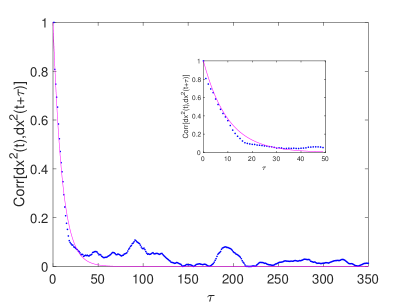

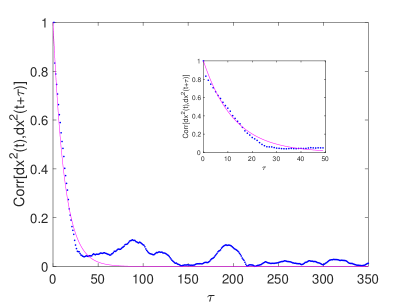

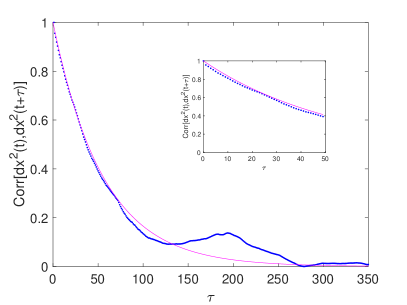

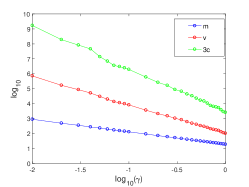

We also conducted a study of the leverage for multi-day returns. Towards this end we used (31)-(33) with the values of , , and obtained in [12]. The results for cross-correlation are shown in Fig. 4. Obviously, decays rapidly with the number of days of accumulation of returns.

|

4 Conclusions

We found that the correlation function (Pearson correlation coefficient) of stochastic variance (9) in mean-reverting models depends only on one - relaxation – parameter and that the variance of the variance can be found from a general, model independent formula (8). We also argued that leverage can be found from a general, model independent formula (17).

We investigated the relationship between the correlation functions of stochastic variance and of realized variance for multi-day returns, (11), and investigated the latter as a function of the number of days of accumulation of returns. We also empirically investigated the correlation function of realized variance and showed that it can be described by a single-parameter exponent, with inverse time parameter itself exponentially decreasing to its finite asymptotic values with the increase of the number of days of returns accumulation. We were unable to propose an explanation of this behavior.

For two specific volatility models – multiplicative and Heston – we used the correlation function and leverage to determine model parameters and cross-correlation between stochastic volatility and stock returns. We also showed that cross-correlation decays rapidly for multi-day returns.

We examined correlations and relaxation specifically for Heston model and showed that it displays a progression of relaxation times that are reflected in cumulants’ relaxation. Finally, we proposed that the distribution of relaxation times is best described by an Inverse Gaussian.

Appendix A Correlation Function of Multi-day Realized Variance

In Section 2 we argued that for the mean-reverting models, (2), the correlation function of stochastic variance is given, per (9), by . The problem with this prediction is relating to actual market quantities. For daily returns it is given by the l.h.s. of (13), however its fit with the in Fig. 1 is rather poor. The latter may be attributed to that continuous, mean-reverting models of stochastic variance are not a good match for daily returns. On the other hand, they may be more appropriate for multi-day returns [12, 21]. Unfortunately, the relationship between multi-day realized 222Notice that multi-day realized variance, that is variance calculated for multi-day accumulation of stock returns, is different from realized variance related to realized volatility, which is calculated by addition of daily realized variances [14]. and stochastic variances is complicated, per (11), and so is determining dependence on in presence of two time scales, and .

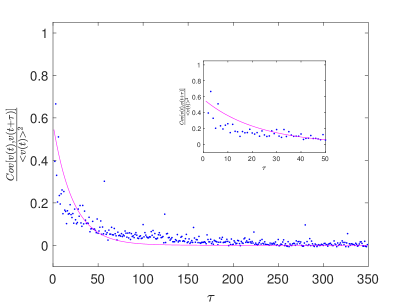

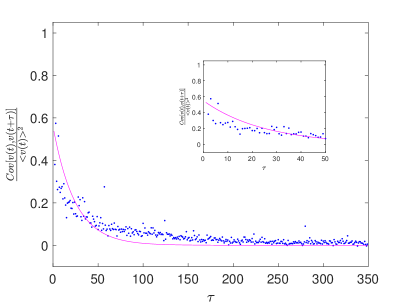

Consequently, we surmised, per(15), that the correlation function of multi-day realized variance is expressed by a pure exponent, . We fitted with for multi-day S&P returns (DJIA is very similar) and summarized our empirical findings, including statistics, in Table 2

| t | a | ||

|---|---|---|---|

| 7 | 0.57 | 0.09 | 0.71 |

| 14 | 0.80 | 0.11 | 0.75 |

| 21 | 0.95 | 0.10 | 0.78 |

| 28 | 0.97 | 0.08 | 0.80 |

| 35 | 0.96 | 0.06 | 0.84 |

| 42 | 0.96 | 0.05 | 0.87 |

| 49 | 0.98 | 0.045 | 0.89 |

| 56 | 0.99 | 0.041 | 0.90 |

| 63 | 0.99 | 0.035 | 0.92 |

| 70 | 0.99 | 0.031 | 0.93 |

| 77 | 1.00 | 0.028 | 0.93 |

| 84 | 1.00 | 0.024 | 0.94 |

| 91 | 1.00 | 0.020 | 0.94 |

| 98 | 1.00 | 0.019 | 0.95 |

| 105 | 1.00 | 0.018 | 0.95 |

| 112 | 1.00 | 0.018 | 0.96 |

| 119 | 1.00 | 0.017 | 0.96 |

| 126 | 1.00 | 0.017 | 0.97 |

| 133 | 1.00 | 0.016 | 0.97 |

| 140 | 1.00 | 0.015 | 0.98 |

| 147 | 1.00 | 0.014 | 0.98 |

| 154 | 1.00 | 0.013 | 0.98 |

| 161 | 1.00 | 0.012 | 0.98 |

| 168 | 1.00 | 0.012 | 0.98 |

| 175 | 1.00 | 0.012 | 0.97 |

| 182 | 1.00 | 0.012 | 0.97 |

| 189 | 1.00 | 0.012 | 0.98 |

| 196 | 1.00 | 0.012 | 0.98 |

In Fig. 5 we show exponential fit of itself as a function of days of accumulation. In Fig. 6 we show sample fits for 21, 28, 105, 112, 189 and 196 days of accumulation with parameter values from Table 2. At present, we do not have plausible interpretation of our empirical findings.

|

|

|

|

Appendix B Correlations and Relaxation in Heston (Cox-Ingersoll-Ross) Model

B.1 Eigenvalue Solution of Fokker-Planck Equation

We have previously investigated correlations and relaxation in multiplicative model [6]. Here we will apply the same approach to Heston (Cox-Ingersoll-Ross) model. To remain consistent with notations of [6], we replace with (not to confuse with stock returns), drop superfluous indices and write the model as

| (34) |

Obviously, via rescaling and , this equation can be reduced to that with the unity mean

| (35) |

For now, however, we will proceed with (34).

The Fokker-Planck equation for this process is given by

| (36) |

To find correlations and relaxation, we use an eigenvalue approach [2] to solving it. Namely, we seek the solution in the following form:

| (37) |

where and is a Ga steady-state distribution of (34)

| (38) |

where the latter assures that . describe relaxation to the steady state and we should also have

Substitution of (37) into (36) yields

| (39) |

which has two solutions

| (40) |

and

| (41) |

where is Tricomi’s confluent hypergeometric function and L is Laguerre polynomial function. Condition cannot be satisfied by and for it leads to quantization of , , where is an integer. Consequently, the eigenfunctions of (39) are given by

| (42) |

The correlation function can be found as [2]

| (43) |

where

| (44) |

Using (42), we find

| (45) |

Clearly, the only non-zero is . Using normalization condition [2]

| (46) |

We find

| (47) |

so that

| (48) |

and

| (49) |

that is

| (50) |

which is the same result as we already found in (30). The value of eigenvalue approach, however, is to establish multiple relaxation (time) scales, which we address next.

B.2 Cumulant Relaxation

As is for multiplicative model, the easiest way to observe multiple relaxation times predicted using eigenvalue method, is through relaxation of cumulants [6]. As was observed in B.1, the mean can always be set to unity, , and in what follows we will use (35). We will also use two sets of initial conditions, and . For the former, the expressions for the mean and the cumulants are given by

| (51) |

and in particular

| (52) |

For the latter, we have

| (53) |

and in particular

| (54) |

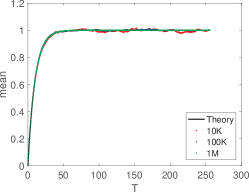

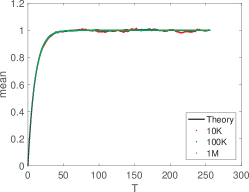

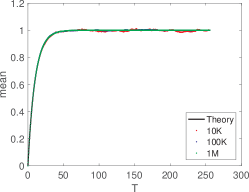

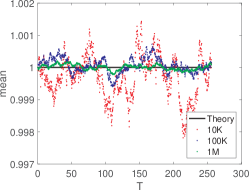

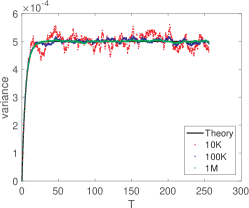

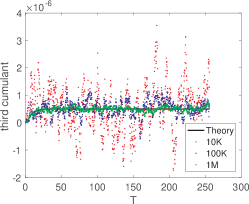

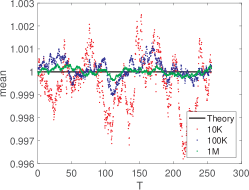

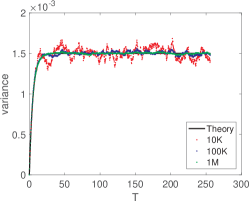

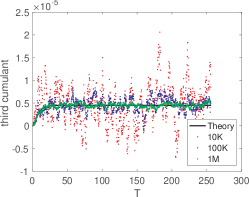

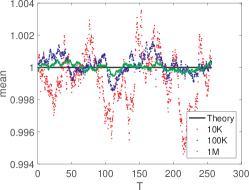

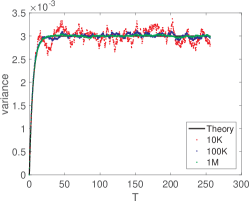

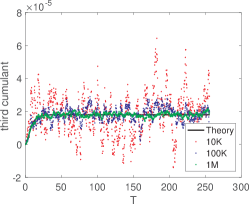

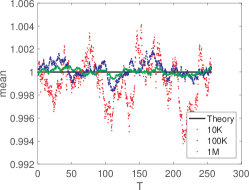

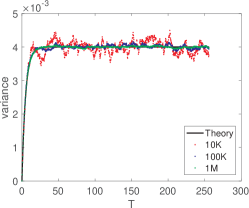

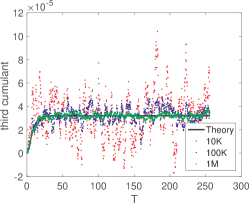

The behavior of the mean starting with is shown in Fig. 7 and the behavior of the mean and cumulants and starting with in Fig. 8. Time series of various durations were used, as well as different values of . Clearly, theory describes the mean and cumulants approach to equilibrium values very well.

|

B.3 Distribution of Relaxation Times

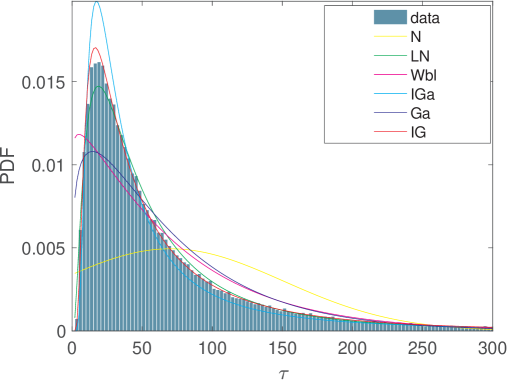

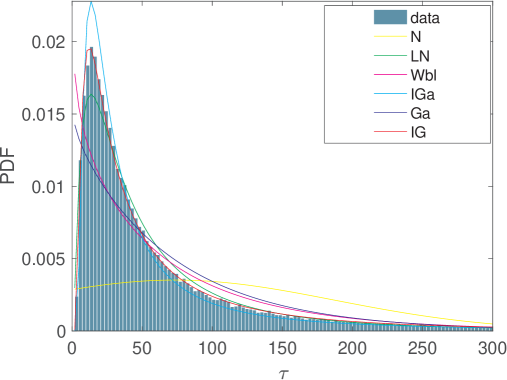

In the same manner as was done for multiplicative model [6], we investigate the distribution of relaxations times. Namely, we generate a time series (35) and observe how quickly its distribution approaches the steady-state distribution (38). The relaxation time is determined by saturation of the Kolmogorov-Smirnov (KS) statistic for comparison between numerical and theoretical distribution to its lowest value. We generated relaxation times and studies their distribution function. We fitted with Normal (N), Lognormal (LN), InverseGamma (IGa), Gamma (Ga), Weibull (Wbl) and Inverse Gaussian (IG) distributions using maximum likelihood estimation (MLE) and evaluated KS statistics for this fits (lower KS numbers indicate better fits.) The results are summarized in Table 3 and fits, for the same as in Table 3 and two values of from it, are shown in Fig. 9.

| parameters | KS test | parameters | KS test |

| N(70.0421,80.7143) | 0.2071 | N(70.4884,86.8047) | |

| LN( 3.8031, 0.9317) | 0.0175 | LN( 3.7814, 0.9532) | 0.0198 |

| IGa( 1.3787, 41.2501) | 0.0455 | IGa( 1.3383, 38.6621) | 0.0437 |

| Gamma( 1.2618, 55.5088) | 0.0806 | Gamma( 1.1940, 59.0379) | 0.0859 |

| Weibul( 71.9396, 1.0601) | 0.0703 | Weibul( 71.2892, 1.0235) | 0.0746 |

| IG( 70.0421, 52.2334) | 0.0083 | IG( 70.4884, 48.9500) | 0.0066 |

| parameters | KS test | parameters | KS test |

| N(71.0994,93.2400) | 0.2350 | N(70.7593, 89.8287) | 0.2281 |

| LN( 3.7596, 0.9759) | 0.0226 | LN( 3.7699, 0.9652) | 0.0211 |

| IGa( 1.2983, 36.1767) | 0.0418 | IGa( 1.3162, 37.2958) | 0.0431 |

| Gamma( 1.1286, 62.9993) | 0.0922 | Gamma( 1.1599, 61.0050) | 0.0889 |

| Weibul( 70.6876, 0.9888) | 0.0783 | Weibul( 70.9619, 1.0057) | 0.0764 |

| IG( 71.0994, 45.8257) | 0.0088 | IG( 70.7593, 47.2629) | 0.0070 |

| parameters | KS test | parameters | KS test |

| N(73.3633,113.5198) | 0.2678 | N(73.8387,117.0505) | 0.2723 |

| LN( 3.6953, 1.0479) | 0.0291 | LN( 3.6839, 1.0612) | 0.0304 |

| IGa( 1.1737, 29.1487) | 0.0387 | IGa( 1.1534, 28.0570) | 0.0381 |

| Gamma( 0.9659, 75.9566) | 0.1058 | Gamma( 0.9409, 78.4754) | 0.1078 |

| Weibul( 69.0188, 0.9031) | 0.0863 | Weibul( 68.7421, 0.8900) | 0.0877 |

| IG( 73.3633, 37.5457) | 0.0136 | IG( 73.8387, 36.2745) | 0.0142 |

|

|

As was the case with the multiplicative model, IG distribution

| (55) |

provided by far the best fit. It should be noted that for (55), cumulants and are independent of the coefficient . Fig. 10 shows excellent agreement with numerical results.

|

References

- [1] G. E. Uhlenbeck, L. S. Ornstein, On the theory of the brownian motion, Physical Review 36 (1930) 813–841.

- [2] A. Schenzle, H. Brand, Multiplicative stochastic processes in statistical physics, Physical Review A 20 (4) (1979) 1628–1647.

- [3] J.-P. Bouchaud, M. Mézard, Wealth condensation in a simple model of economy, Physica A: Statistical Mechanics and its Applications 282 (3) (2000) 536–545.

- [4] J.-P. Bouchaud, On growth-optimal tax rates and the issue of wealth inequalities, Journal of Statistical Mechanics: Theory and Experiment (2015) doi:10.1088/1742–5468/2015/11/P11011.

- [5] T. Ma, J. G. Holden, R. Serota, Distribution of wealth in a network model of the economy, Physica A: Statistical Mechanics and its Applications 392 (10) (2013) 2434–2441.

- [6] Z. Liu, R. A. Serota, Correlation and relaxation times for a stochastic process with a fat-tailed steady-state distribution, Physica A: Statistical Mechanics and its Applications 474 (2017) 301–311.

- [7] Z. Liu, R. A. Serota, On absence of steady state in a bouchaud-mezard network model, Physica A: Statistical Mechanics and its Applications 491 (2018) 391–398.

- [8] J. Masoliver, J. Perello, A correlated stochastic volatility model measuring leverage and other stylized facts, International Journal of Theoretical and Applied Finance 5 (05) (2002) 541–562.

- [9] J. Perello, J. Masoliver, Random diffusionand leverage effect in financial markets, Physical Review E 67 (2003) 037102.

- [10] J. Perelló, J. Masoliver, J.-P. Bouchaud, Multiple time scales in volatility and leverage correlations: a stochastic volatility model, Applied Mathematical Finance 11 (1) (2004) 27–50.

- [11] T. Ma, R. Serota, A model for stock returns and volatility, Physica A: Statistical Mechanics and its Applications 398 (2014) 89–115.

- [12] M. Dashti Moghaddam, R. Serota, Combined mutiplicative-heston model for stochastic volatility, arXiv:1807.10793 (2018).

- [13] G. Hertzler, ”classical” probability distributions for stochastic dynamic models, in: 47th Annual Conference of the Australian Agricultural and Resource Economics Society, 2003.

- [14] M. Dashti Moghaddam, J. Liu, R. Serota, Implied and realized volatility: A study of distributions and distribution of difference, arXiv:1906.02306 (2019).

- [15] M. Dashti Moghaddam, J. Mills, R. A. Serota, Generalized beta prime distribution: Stochastic model of economic exchange and properties of inequality indices, arXiv:1906.04822 (2019).

- [16] M. Dashti Moghaddam, J. Liu, R. A. Serota, Modeling response time distributions with generalized beta prime, arXiv:1907.00070, to be published in Discontinuity, Nonlinearity and Complexity (2019).

- [17] P. D. Praetz, The distribution of share price changes, Journal of Business (1972) 49–55.

- [18] D. Nelson, Arch models as diffusion approximations, Journal of Econometrics 45 (1990) 7.

- [19] S. L. Heston, A closed-form solution for options with stochastic volatility with applications to bond and currency options, The Review of Financial Studies 6 (2) (1993) 327–343.

- [20] A. A. Dragulescu, V. M. Yakovenko, Probability distribution of returns in the heston model with stochastic volatility, Quantitative Finance 2 (2002) 445–455.

- [21] Z. Liu, M. Dashti Moghaddam, R. Serota, Distributions of historic market data – stock returns, European Physics Journal B 92: 60 (2019) 1–10.