Three algorithms for solving high-dimensional fully-coupled FBSDEs through deep learning

Abstract

Recently, the deep learning method has been used for solving forward-backward stochastic differential equations (FBSDEs) and parabolic partial differential equations (PDEs). It has good accuracy and performance for high-dimensional problems. In this paper, we mainly solve fully coupled FBSDEs through deep learning and provide three algorithms. Several numerical results show remarkable performance especially for high-dimensional cases.

Keywords deep learning fully-coupled FBSDEs high-dimensional equation stochastic control

1 Introduction

In 1990, Pardoux and Peng proved the existence and uniqueness of the adapted solution for nonlinear BSDEs [1] and then found important applications of BSDEs in finance. When a BSDE is coupled with a (forward) stochastic differential equation (SDE), the system is usually called a forward-backward stochastic differential equation (FBSDE). The FBSDE is an important tool for a wide range of application areas. For example, it can be used to solve the stochastic optimization problems, and meanwhile the stochastic optimization provides a very important way for solving many AI applications such as robotics and aerospace. In financial fields, when constructing a derivatives pricing model, it is necessary to consider the credit value adjustment (CVA) and the funding value adjustment (FVA) in many cases. However, the computation of CVA and FVA greatly increase the difficulty for financial derivatives pricing. In this instance, the FBSDE appears as an effective tool for the modeling of this kind of complex derivatives pricing.

In most situations, it is impossible to obtain an explicit solution of a FBSDE. Therefore, it is necessary to find the approximate solution. In this paper, we aim to obtain the numerical solution of the following fully-coupled FBSDE through deep learning:

| (1.1) |

There are several ways to find the numerical solution of FBSDE (1.1). Based on the relationship between FBSDEs and PDEs (see [2]), numerical methods for solving the PDEs, such as the finite element method, the finite difference method, or the sparse grid method, can be applied to solve the FBSDEs. Ma et al studied the solvability of coupled FBSDEs and proposed a four-step approach [3]. Moreover, some probabilistic methods, which approximate the conditional expectation with numerical schemes, were developed to solve the FBSDEs. For example, [4] proposed a theta-scheme numerical method with high accuracy for coupled Markovian FBSDEs. [5] introduced a numerical scheme for coupled FBSDEs when the forward process does not depend on .

As is known, there is a significant difficulty for solving high dimensional BSDEs and FBSDEs, namely "curse of dimensionality". The computational complexity grows exponentially when the dimension increases, while the accuracy declines sharply. Therefore most of the aforementioned numerical methods can not deal with high-dimensional problems.

Recently, deep-learning method has achieved great success in many application areas [6], such as computer vision, natural language processing, gaming, etc. It provides a new point of view to approximate functions and shows optimistic performance in solving problems with high-dimension features. This poses a possible way to solve the "curse of dimensionality" although the reason why deep-learning has so remarkable performance has not been proven completely.

In a recent breakthrough paper of E et al [7], they solved the BSDEs from a control perspective by regarding the term as a control. A neural network was constructed to solve high dimensional BSDEs and related PDEs. Their method has shown superior performance and accuracy on comparing with the traditional numerical methods. Lately, Han and Long [8] extended this method to solve FBSDEs where and in the forward SDE do not depend on the term and gave a posteriori error estimation.

In this paper, we solve fully-coupled FBSDEs (1.1) by the above optimal control approach through deep neural network. Different from [7, 8], we systematically explore the dependence of the term on state precesses and even itself (in the following Algorithm 3) and propose three algorithms corresponding to different kinds of state feedback. In order to do this, we should design different cost functionals which make it possible to solve FBSDEs (1.1) by the optimal control approach. In the first algorithm (Algorithm 1), we adopt the same state feedback form as that in Han and Long [8]: the control is supposed to be dependent on the states of the forward SDE and of the BSDE. We generalize it to solve (1.1) in which and depend on the term. In the second algorithm (Algorithm 2), we take the state as the feedback. Besides the control , in the forward SDE should be regarded as a new control and denoted as . Both the controls and are supposed to be dependent on the state of the forward SDE. The price of doing this is that we must change the form of the cost function in Algorithm 1. A new penalty term is added to the cost function to punish the difference between the control and the solution of the backward SDE. The third algorithm (Algorithm 3) is inspired by the idea of the Picard iteration (see [2]). Given the initial pathes , the next iteration pathes are dependent on the current pathes in Picard iteration. is supposed to be dependent on . Different from the state variable feedback in Algorithm 1 and 2, Algorithm 3 is a path-dependent iteration one which has potential applications in the calculation of FBSDE (1.1) with random coefficients.

These three methods for solving FBSDE (1.1) can also be widely applied to solving high-dimensional BSDEs. It is well-known that Feynman-Kac formula gives the probabilistic interpretation of the solution of linear PDEs. [9] and related literatures obtained generalized Feynman-Kac formulas which establish the relationship between FBSDEs and nonlinear PDEs. The corresponding PDE of FBSDE (1.1) is

with terminal condition .

Consequently, from the numerical results, all the three algorithms can approximate the solution of the FBSDE (1.1) and perform well in high-dimensional cases. As shown in the examples in Section 5, the relative errors of these algorithms are less than 1%.

The remainder of this paper is organized as following. In Section 2, we firstly present some preliminaries on FBSDEs and in particular, give the existence and uniqueness conditions of fully-coupled FBSDEs. In Section 3, the relationship between FBSDEs and an optimal control problem are presented, which indicates that the FBSDEs can be solved from a control perspective. According to different kinds of state feedback, we propose three optimal control methods for solving FBSDE (1.1). In Section 4, we present our numerical schemes and the corresponding algorithms and show the neural network architecture. Section 5 gives some examples and shows the comparison among different algorithms for solving coupled FBSDEs.

2 Preliminaries on FBSDEs

In this section, we mainly introduce the form of FBSDEs and the existence and uniqueness conditions of fully-coupled FBSDEs [10].

Let and be a filtered probability space, where is a -dimensional standard Brownian motion on , is the natural filtration generated by the Brownian motion . is the initial condition for the FBSDE.

Considering the fully-coupled FBSDE (1.1), where are -adapted stochastic processes taking value in , respectively. The functions

are deterministic globally continuous functions. and are the drift coefficient and diffusion coefficient of respectively, and is referred to as the generator of the coupled FBSDE. If there is a triple satisfies the above FBSDE on , -almost surely, square integrable and -adapted, the triple are called the solutions of FBSDE (1.1). When functions and are independent of both and , FBSDE (1.1) is called a decoupled FBSDE.

It is well known that in BSDE theory, even if all coefficients satisfy Lipschitz condition, fully coupled FBSDE does not necessarily have solutions. So we have to give some more assumptions.

Given a full-rank matrix , we define

where .

Firstly, we give two assumptions as the following,

Assumption 1.

-

(i)

is uniformly Lipschitz with respect to ;

-

(ii)

is in , ;

-

(iii)

is uniformly Lipschitz with respect to ;

-

(iv)

is in , .

Assumption 2.

where and are given nonnegative constants with

Theorem 1.

Readers are referred to Theorem 2.6 of [10] for the proof in detail.

For convenience, in this article, we assume that is the Lipschitz constant satisfying Assumption 1 , that is

where represents one of the functions among and .

3 Solving FBSDEs from an optimal control perspective

Essentially, a deep neural network considered in this paper can be regarded as a control system, which is used to approximate the mapping from the input set to the label set. The parameters in the network can be seen as the control, and the cost function can be seen as the optimization objective. Thus, we firstly transform the problem of solving FBSDE into three optimal control problems with different kinds of feedback control.

3.1 Case 1: Feedback control based on

In the first case, we extend the method in [7, 8] for solving FBSDE (1.1). Consider the following variational problem:

| (3.1) |

where is -measurable random variable valued in and is a -adapted and square-integrable process. The couple is regarded as the control of variational problem (3.1) and is a feedback control based on .

Proposition 2.

Proof.

Thanks to Assumption 1 and 2 hold, the FBSDE (1.1) has a unique solution . Regarding as the control of the variational problem (3.1), we have

and then the optimal control can be achieved. The corresponding triple is the solution of FBSDE (1.1). Because of Assumption 1 and 2 hold, the solution is unique. ∎

The detailed iteration algorithm will be given in Section 4.

3.2 Case 2: Feedback controls based on

In (3.1), the initial value of process is regarded as a control. Now we regard the whole process in the forward SDE as a control, then we have the following control problem

| (3.3) |

where and are two -adapted and square-integrable processes. The are the controls of the variational problem (3.3). Both are feedback controls based on .

Proposition 3.

3.3 Case 3: Feedback control based on with Picard iteration method

Before introducing the Picard iteration with feedback , we first give an assumption to make sure the Picard iteration is convergent [2].

Assumption 3.

-

(i)

There exist such that for all and a.s.,

-

(ii)

There exist , such that for all and a.s.,

-

(iii)

There exist , such that for all and a.s.,

-

(iv)

There exists , such that for all and a.s.,

-

(v)

The processes and are -adapted, and the random variable is -measurable, for all . Moreover, the following holds:

The notations and are denoted as the square-root of the sum of squares of the components of a vector and a matrix, respectively. Under Assumption 3 and , FBSDE (1.1) has a unique solution . Pardoux and Tang’s results [2] have shown that (1.1) can be constructed via Picard iteration

| (3.5) |

when are given, is denoted as the iteration step. Therefore, the solution of the decoupled FBSDE (3.5) converges to to the solution of (1.1) when tends to infinity, i.e.

| (3.6) |

where , .

Regarding and as controls, we consider the following control problem

| (3.7) |

| (3.8) | ||||

where and are taking valued in and , respectively. The couple is regarded as the controls and is a feedback control based on . In the following, we will show that control problem (3.7) is equivalent to FBSDE (3.5).

When are known, we consider the SDEs (3.8) in (3.7), which has infinite number of solutions because both the initial value and the process are uncertain. Given and the process , (3.8) is a system of forward stochastic differential equations with initial condition . Under Assumption 3 and , the equations (3.8) has a unique solution [12] determined by and .

In the following Theorem 4, we will show that the solution of (3.8) converges to the solution of FBSDE (1.1) when goes to zero as tends to infinity, which means that solving the control problem (3.7) is equivalent to solving the FBSDE (1.1).

Theorem 4.

Proof.

The proof of this theorem is divided into two steps.

-

Step 1:

Supposing the following equation

(3.10) has a solution . Let

whose differential form is

Plugging Ito’s formula into ,

integrating from to ,

and taking the expectation

then we have

(3.11) based on the Gronwall inequality.

Similarly, we have

Integrating from to ,

and taking the expectation

then we have

(3.12) thus

Based on the Gronwall inequality, we get

(3.13) then

(3.14) Similarly, we get

and

Note that

then

As

we have

then we get

-

Step 2:

Given and , we have

(3.15) with its solution . By using the similar method of proof with Step 1, we get

(3.16) for a constant . Then

∎

Remark.

Remark.

In case 1, we regard as the feedback control of the state processes and only consider the initial value as the control. In case 2, in order to get the optimal approximation for the whole process , we introduce a new control and add a new error term in the cost function. When the final cost function approximate to 0, is exactly the state process . It means that we can directly get at any time through the trained network. Both of case 1 and case 2 do not consider the effect of process , while case 3 takes it into consideration. In case 3, the value of in the last iteration is used as the input of the current iteration.

4 Numerical schemes and algorithms for fully-coupled FBSDEs

In Section 3, FBSDE (1.1) is transformed to different optimal control problems. Inspired by [7] and [8], we use forward neural networks to simulate the control process and mentioned in Section 3. The universal approximation theorem [13] has shown that a feed-forward network containing a finite number of neurons can approximate continuous functions for a given accuracy.

In this section, we propose three algorithms. In the first algorithm, the inputs of the network are states and , and the output is . In the second algorithm, double control processes are employed, the state is taken as the input of the networks, the controls and are taken as the output of the networks, respectively. In the third algorithm, the three items are taken as the input of the network and the output of network is . Here we uniformly define the feedback function as and assume that has some good properties to ensure that the discrete-time scheme of the stochastic process is convergent, according to the work of Kloeden [14]. In our future work, we will establish concrete assumptions that needs to satisfy.

We firstly give the notations of the discrete time and the Brownian motion. Let be a partition of the time interval , where . We define and , where , for . For different optimal control problems in Section 3, we can give their corresponding discrete-time schemes.

We construct a fully connected neural network at each time point to approximate the control . We use to represent the parameters of the feed-forward neural network at time . We denote and define as a parameter. The ReLU activation function and Adam stochastic gradient descent-type algorithm are adopted in the neural network. The definitions of the loss function are different according to different control problems. The network parameters are updated by back propagation (BP), and then the optimal parameters can be found. The algorithms first update the parameters from the last layer to the first layer of the network at time point , and then update the parameters in the reverse direction of time until time .

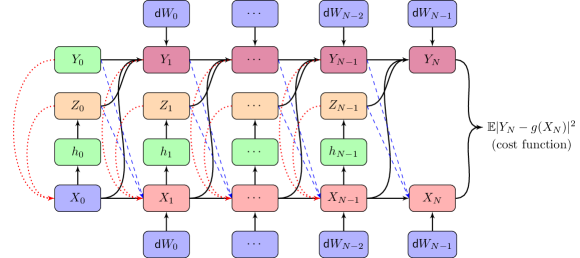

Here we take Algorithm 3 as an example, and show the neural network architecture in Figure 1. As shown in Figure 1, the solid lines represent the data flow generated in the current iteration, the dashed blue lines and dotted red lines represent respectively the data flow and neural network inputs that use the data of the previous iteration. represents the hidden layers and represents the outputs. and the weights of the hidden layers are trainable parameters.

For convenience, the time interval is partitioned evenly, i.e. for all . We define and denote the iteration step by which is marked by superscript in the algorithm. In the following subsections, we present these three algorithms for different kinds of feedback control in detail.

4.1 Algorithm 1: Feedback control based on

In [8], coupled FBSDEs where the forward SDE does not depend on have been studied. The values are calculated step by step in time, i.e. the triple of the current time-step is used to calculate the triple of the next time-step. We extend this idea to solve FBSDE (1.1).

For the control problem (3.1), the discrete-time scheme is

| (4.1) |

because the process is Markovian, should be represented as a function of

| (4.2) |

However, when simulating the function by the neural network, , cannot be used as both input and output of the network. Notice that (4.2) is an implicit function, assuming that its explicit form is

| (4.3) |

which only depends on and . Though both of the functions and are unknown , the objective of network estimation changes from approximating to approximating . The network contains four layers including one -dim input layer, two hidden -dim layers and a -dim output layer. The loss function is defined as

where is the number of samples.

According to Proposition 2, the triple converges to the true solution when the loss goes to zero. The corresponding algorithm is given above.

4.2 Algorithm 2: Feedback controls based on

As discussed in subsection 3.2, we consider and as controls. The corresponding discrete-time scheme of control problem (3.3) is

| (4.4) |

solving functions and , we can get

| (4.5) |

Thus we need to construct two networks at the same time, one for simulating and another for simulating . The network simulating at each time point consists of four layers including one -dim input layer, two hidden -dim layers and a -dim output layer. The network layers simulating is the same as that of except that the output layer is -dim. All parameters of the two networks are represented as .

The lost function is denoted as

According to Proposition 3, the triple converges to the solution of (1.1) when the loss tends to zero. The detailed algorithm is shown as follows.

4.3 Algorithm 3: Feedback control based on

For control problem (3.7), the corresponding discrete-time scheme can be written as

| (4.6) |

where and are time discretization schemes of , respectively, and the values of and for are given. The network at each time point consists of four layers including one -dim input layer, two hidden -dim layers and a -dim output layer. The loss function is defined as

where is the number of samples.

According to Theorem 4, the triple converges to the true solution when the loss tends to zero.

The detailed algorithm based on the conclusions of section 3 is given as following.

Remark.

In this algorithm, the Brownian motion is denoted as . The initial paths and are generated randomly, and they do not influence the convergence of and the process . As the aim of the algorithm is to find the optimal parameters to approximate the map in equations (4.6), the gradient descent method is used in line 8 of the algorithm which makes approximate to after times of iterations. The numerical results shown in Section 5 confirm the convergence of the algorithm. Besides, when the function in (4.6) only depends on , the numerical results also demonstrate good convergence for the neural network approximation.

5 Numerical results

In this section, we present the numerical results of our algorithms for different cases including partially-coupled cases and fully-coupled cases. If not mentioned, the results in the examples are the results of algorithm 3. All the examples of this section are implemented with 256 sample-paths of the Brownian motion , learning rate , the number of time-points if not specifically noted. The numerical experiments are performed in PYTHON on a LENOVO computer with a 2.40 Gigahertz (GHz) Inter Core i7 processor and 8 gigabytes (GB) random-access memory (RAM).

5.1 Example 1. Partially-coupled case (BSDE)

We consider an example in [15] for solving of partially-coupled FBSDEs.

Assume and the functions in (1.1) satisfy

where represents a diagonal matrix where the value of the th diagonal element is , and the explicit solution of this FBSDE is

We set for different dimensions, and the explicit solution of is 0.5.

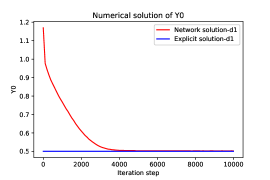

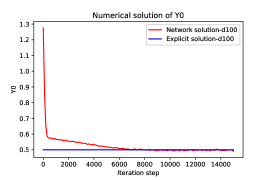

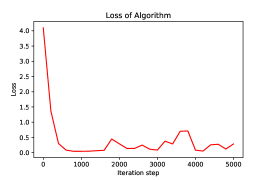

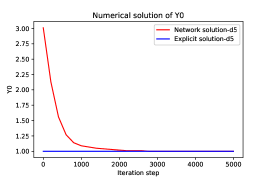

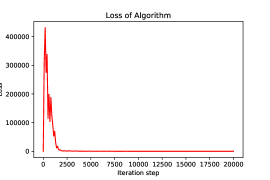

Figure 2 shows that in the case of , the network solution is close to the explicit solution when the number of iteration steps increases. After 10000 steps, the value of is 0.50496 and has a relative error of comparing to the explicit solution.

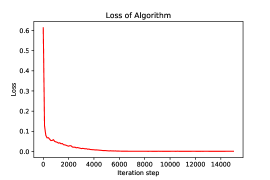

For case, the value of is 0.50413 after 15000 steps. The network has a rather optimistic performance with a relative error of to the explicit solution, see figure 3 in detail.

The initial value of is selected randomly in the interval and the numerical algorithm is performed 10 times independently. Table 1 shows the detailed numerical results.

| Step | Mean of | Variance of | Relative error of | Mean of runtime(s) |

|---|---|---|---|---|

| 3000 | 0.54501 | 3.540E-02 | 0.0900 | 4715.6 |

| 6000 | 0.50970 | 6.803E-04 | 0.0194 | 8751.3 |

| 9000 | 0.49882 | 5.049E-06 | 0.0024 | 12693.2 |

| 12000 | 0.49658 | 3.752E-07 | 0.0068 | 16615.4 |

| 15000 | 0.49602 | 4.369E-07 | 0.0080 | 20528.8 |

5.2 Example 2. The forward SDE not containing term

We adopt the example of [16] which does not contain term in the forward SDE. Consider the following FBSDE,

where

and

The explicit solution of this FBSDE is

[16] has shown the results of different dimensions for . In the case , [16] has achieved a relative error of in 134 seconds, and we get an approximated result of 1.0002 for with a relative error of comparing with the explicit solution of 1.0. Figure 4 shows the details.

Similarly, we perform 10 independent runs for the case . Detailed results are shown in Table 2.

| Step | Mean of | Variance of | Relative error of | Mean of runtime(s) |

|---|---|---|---|---|

| 1000 | 1.09393 | 6.445E-02 | 9.393E-02 | 279.9 |

| 2000 | 1.02127 | 1.046E-04 | 2.127E-02 | 461.4 |

| 3000 | 1.00247 | 7.194E-06 | 2.470E-03 | 658.2 |

| 4000 | 1.00025 | 8.857E-06 | 2.538E-04 | 880.9 |

| 5000 | 1.00020 | 8.000E-06 | 1.996E-04 | 1077.4 |

For high dimensional cases, the method of [16] is not applicable while our neural network method shows satisfactory results. For the case , our network demonstrates remarkable performance and the relative error of is . See Figure 5 in detail.

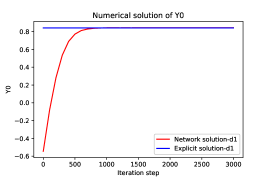

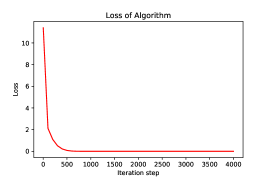

5.3 Example 3. 1-dim fully-coupled case

We adopt the example of [4] for the fully-coupled case. Considering the following FBSDE,

the solutions of this FBSDE are and . The numerical solution for this kind of FBSDEs is much more difficult as its diffusion coefficient is dependent on

We set , and the explicit solution . The numerical results are shown in Figure 6 which are close to the results of [4], and the relative error is .

In this example, we also use Algorithm 1 and 2 to solve the FBSDE. We use the same time partition, learning rate, number of iteration steps and samples as in Algorithm 3. In order to compare the results of the three algorithms more throughly, we calculate the variance of 1000 iteration steps before the current iteration. When the variance is less than or the number of iteration steps achieves the upper limit 10000, the loop iteration is terminated. We record the number of iteration steps and the running time when the algorithm terminate. As expected, all the results are convergent. The comparison of the three algorithms are shown in Table 3. We run each algorithm 10 times independently.

| Method | Mean of | Variance of | Relative error of | Steps | Time(s) |

| Alg 1 | 0.8381 | 1.262E-05 | 4.32E-03 | 2588.7 | 390.9 |

| Alg 2 | 0.8334 | 5.367E-06 | 9.86E-03 | 10000 | 2160.0 |

| Alg 3 | 0.8421 | 5.742E-08 | 4.24E-04 | 2030.4 | 1076.4 |

From Table 3, we can see that Algorithm 3 is more accurate and stable for this example. It requires the least number of iteration steps to achieve a smooth convergence result but it takes the longest time for each iteration step. Algorithm 1 and 2 takes less running time for each iteration step, but Algorithm 2 can not get a stable convergence result up to the maximum iteration step.

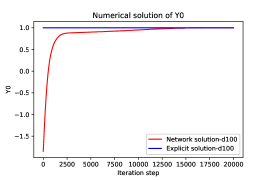

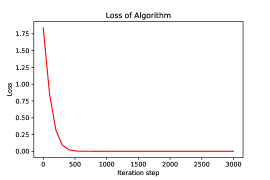

5.4 Example 4. 100-dim nonlinear generator for the FBSDE

Assume , consider this following FBSDE,

| (5.1) |

where takes value in . We can check that the explicit solution of this FBSDE is

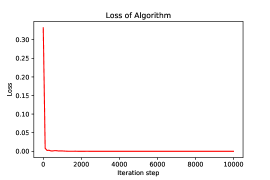

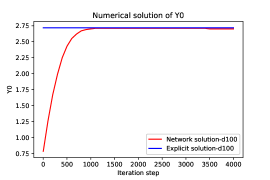

We set for , the explicit solution of is , and the number of time points is . The loss curve and the numerical solution of are shown in Figure 7.We can see from Figure 7 that in the case of , the result of the network solution is closer to the explicit solution when the number of iteration steps increases. After 4000 steps, the value of is 2.71662 and has a relative error of .

We show the results with different initial values for in Table 4. The neural network demonstrates satisfactory results. For the case of and , we compare the three algorithms with the same stopping condition as mentioned in Example 3. The comparison results of the three algorithms are shown in Table 5 for and Table 6 for respectively.

| Explicit solution | 1.00000 | 1.10517 | 1.22140 | 1.64872 | 2.71828 |

| Network solution | 0.99777 | 1.10390 | 1.22103 | 1.64780 | 2.71662 |

| Absolute error | 2.23E-3 | 1.27E-3 | 3.71E-4 | 9.21E-4 | 1.66E-3 |

| Relative error | 2.23E-3 | 1.15E-3 | 3.03E-4 | 5.58E-4 | 6.11E-4 |

| Method | Mean of | Variance of | Relative error of | Steps | Time(s) |

| Alg 1 | 1.6481 | 4.851E-07 | 3.93E-04 | 1518.2 | 1000.8 |

| Alg 2 | 1.6487 | 1.262E-09 | 1.94E-05 | 2049.0 | 423.6 |

| Alg 3 | 1.6478 | 9.335E-08 | 5.57E-04 | 1087.8 | 1957.8 |

| Method | Mean of | Variance of | Relative error of | Steps | Time(s) |

| Alg 1 | 2.7154 | 3.562E-07 | 1.07E-03 | 3516.8 | 2205.3 |

| Alg 2 | 2.7182 | 4.456E-10 | 1.21E-05 | 2557.7 | 503.4 |

| Alg 3 | 2.7164 | 1.282E-07 | 6.76E-04 | 1589.2 | 2768.4 |

From the running results of Example 3 and 4, we can get the following phenomenon. Algorithm 3 needs least number of iteration steps to get a stable convergence rate, but takes the longest time for a given step. Algorithm 2 computes as fast or faster than Algorithm 1, probably because it has fewer network parameters. In terms of accuracy, the three algorithms show different performance results for different problems. For example, Algorithm 2 has the best variance in Example 4, but for Example 3 it can not meet the requirement of stable convergence.

6 Conclusions

In this paper, based on different kinds of feedback controls, we propose three algorithms for solving high-dimensional FBSDEs and construct corresponding neural networks. From the numerical results, all the three algorithms perform well for solving FBSDEs, and the relative error are less than 1%. Algorithm 3 takes only a few steps to achieve convergence results, but each iteration may take more time. Although Algorithms 1 and 2 are computationally fast, they may require more steps to converge.

References

- [1] Etienne Pardoux and Shige Peng. Adapted solution of a backward stochastic differential equation. Systems and Control Letters, 14(1):55–61, 1990.

- [2] Etienne Pardoux and Shanjian Tang. Forward-backward stochastic differential equations and quasilinear parabolic pdes. Probability Theory and Related Fields, 114(2):123–150, 1999.

- [3] Jin Ma and Jiongmin Yong. Forward-Backward stochastic differential equations and their applications. Springer, 2007.

- [4] Yu Fu, Weidong Zhao, and Tao Zhou. Multistep schemes for forward backward stochastic differential equations with jumps. Journal of Scientific Computing, 69(2):1–22, 2016.

- [5] Christian Bender and Jianfeng Zhang. Time discretization and markovian iteration for coupled fbsdes. Annals of Applied Probability, 18(1):143–177, 2008.

- [6] Ian Goodfellow, Yoshua Bengio, and Aaron Courville. Deep Learning. MIT Press, 2016. http://www.deeplearningbook.org.

- [7] Weinan E, Jiequn Han, and Arnulf Jentzen. Deep learning-based numerical methods for high-dimensional parabolic partial differential equations and backward stochastic differential equations. Communications in Mathematics and Statistics, 5(4):349–380, 2017.

- [8] Jiequn Han and Jihao Long. Convergence of the deep bsde method for coupled fbsdes. arXiv:1811.01165, 2018.

- [9] Shige Peng. Probabilistic interpretation for systems of quasilinear parabolic partial differential equations. Stochastics and Stochastic Reports, 37(1):61–74, 1991.

- [10] Shige Peng and Zhen Wu. Fully coupled forward-backward stochastic differential equations and applications to optimal control. Siam Journal on Control and Optimization, 37(3):825–843, 1999.

- [11] Ying Hu and Shige Peng. Solution of forward-backward stochastic differential equations. Probability Theory and Related Fields, 103(2):273–283, 1995.

- [12] Bernt Oksendal. Stochastic differential equations. The Mathematical Gazette, 77(480):65–84, 1985.

- [13] George Cybenko. Approximation by superpositions of a sigmoidal function. Mathematics of Control, Signals, and Systems, 2(4):303–314, 1989.

- [14] Peter E. Kloeden and Eckhard Platen. Numerical Solution of Stochastic Differential Equations. Springer, 1992.

- [15] Jean-Francois Chassagneux. Linear multi-step schemes for bsdes. SIAM Journal on Numerical Analysis, 52(6):2815–2836, 2014.

- [16] Yu Fu, Weidong Zhao, and Tao Zhou. Efficient spectral sparse grid approximations for solving multi-dimensional forward backward sdes. American Institute of Mathematical Sciences, 22(9):3439–3458, 2017.