Exponential stock models driven by tempered stable processes

Abstract.

We investigate exponential stock models driven by tempered stable processes, which constitute a rich family of purely discontinuous Lévy processes. With a view of option pricing, we provide a systematic analysis of the existence of equivalent martingale measures, under which the model remains analytically tractable. This includes the existence of Esscher martingale measures and martingale measures having minimal distance to the physical probability measure. Moreover, we provide pricing formulae for European call options and perform a case study.

Key words and phrases:

Exponential stock model, tempered stable process, bilateral Esscher transform, option pricing2010 Mathematics Subject Classification:

60G51, 91G201. Introduction

Tempered stable distributions form a class of distributions that have attracted the interest of researchers from probability theory as well as financial mathematics. They have first been introduced in [18], where the associated Lévy processes are called “truncated Lévy flights”, and have been generalized by several authors. Tempered stable distributions form a six parameter family of infinitely divisible distributions, which cover several well-known subclasses like Variance Gamma distributions [26, 25], bilateral Gamma distributions [20, 21] and CGMY distributions [6]. Properties of tempered stable distributions have been investigated, e.g., in [29, 33, 32, 3], and in [23], where some of the results of this paper have been announced. For financial modeling they have been applied, e.g., in [4, 7, 27, 16, 2], see also the recent textbook [28].

The purpose of this paper is to provide a systematic analysis of the existence of equivalent martingale measures for exponential stock price models driven by tempered stable processes, under which the computation of option prices remains analytically tractable. In particular, we are interested in martingale measures, under which the driving process remains a tempered stable process, or at least becomes a Lévy process for which the characteristic function is explicitly known.

Equivalent martingale measures of interest, under which the driving process remains a tempered stable process, are the Esscher martingale measure and bilateral Esscher martingale measures which minimize the distance to the original probability measure in a certain sense, for example the minimal entropy martingale measure or the -optimal martingale measure. We will examine the existence of these martingale measures in detail. Furthermore, we will treat the Föllmer Schweizer minimal martingale measure. In case of existence, the driving process is the sum of two independent tempered stable processes under this measure, and thus the model remains analytically tractable. For all the just mentioned martingale measures, we will derive option pricing formulae. Moreover, we will illustrate our findings by means of a case study.

The remainder of this text is organized as follows: In Section 2 we introduce the stock model. Afterwards, in Section 3 we study Esscher transforms, in Section 4 we study bilateral Esscher transforms, and in Section 5 we treat the Föllmer Schweizer minimal martingale measure. Section 6 is devoted to option pricing formulae, and in Section 7 we provide the case study.

2. Stock price models driven by tempered stable processes

In this section, we shall introduce the stock price model and review some results about tempered stable processes. The reader is referred to [23] for all results about tempered stable processes which we recall in this section.

Let be a filtered probability space satisfying the usual conditions. We fix parameters and . An infinitely divisible distribution on is called a tempered stable distribution, denoted

if its characteristic function is given by

where the Lévy measure is

| (2.1) |

2.1 Remark.

In [22] we have studied exponential stock models driven by bilateral Gamma processes, which would occur for .

We can express the characteristic function of as

| (2.2) | ||||

where the powers stem from the main branch of the complex logarithm. We call the Lévy process associated to a tempered stable process, and write

| (2.3) |

The cumulant generating function

exists on and is given by

| (2.4) | ||||

All increments of have a tempered stable distribution, more precisely

| (2.5) |

A tempered stable stock model is an exponential Lévy model of the type

| (2.8) |

where denotes a tempered stable process and is a dividend paying stock with deterministic initial value and dividend rate . Furthermore, is the bank account with interest rate . In what follows, we assume that . An equivalent probability measure is a local martingale measure (in short, martingale measure), if the discounted stock price process

| (2.9) |

is a local -martingale. The existence of a martingale measure ensures that the stock market is free of arbitrage, and the price of an European option , where is the time of maturity and the payoff profile, is given by

2.2 Lemma.

The following statements are true:

-

(1)

If , then is a martingale measure if and only if

(2.10) -

(2)

If , then is never a martingale measure.

3. Existence of Esscher martingale measures

In this section, we study the Esscher transform, which was pioneered in [9]. Throughout this section, let be a tempered stable process of the form (2.3).

3.1 Definition.

Let be arbitrary. The Esscher transform is defined as the locally equivalent probability measure with likelihood process

| (3.1) |

where denotes the cumulant generating function given by (2.4).

3.2 Lemma.

For every we have

under .

Proof.

This follows from Proposition 2.1.3 and Example 2.1.4 in [19]. ∎

We define the function as

where we have set

3.3 Theorem.

Proof.

Let be arbitrary. In view of Lemmas 3.2 and 2.2, the probability measure is a martingale measure if and only if , i.e. , and (3.4) is fulfilled. Note that if and only if (3.2) is satisfied. For the functions and we obtain the derivatives

for . Noting that , we see that on the interval . Hence, is strictly increasing on , which completes the proof. ∎

4. Existence of minimal distance measures preserving the class of tempered stable processes

In the literature, one often performs option pricing by finding an equivalent martingale measure which minimizes the distance

for some strictly convex function . Here are popular choices for the function :

-

•

For we call the minimal entropy martingale measure.

-

•

For with we call the -optimal martingale measure.

-

•

For we call the variance-optimal martingale measure.

We refer to [22, Section 5] for further remarks and related literature. While -optimal equivalent martingale measures do not exist in tempered stable stock models (which follows from [1, Example 2.7]), we have the following result concerning the existence of minimal entropy martingale measures:

4.1 Theorem.

The following statements are true:

-

(1)

If , then a minimal entropy martingale measure exists.

-

(2)

If , then a minimal entropy measure exists if and only if

This result, which has been indicated in [22, Remark 5.4], follows by adjusting the arguments of the proof of [22, Theorem 5.3] to the present situation, where the stock model is driven by a tempered stable process.

In this section, we shall minimize the relative entropy

within the class of tempered stable processes by performing bilateral Esscher transforms. Let be a tempered stable process of the form (2.3). We decompose the tempered stable process as the difference of two independent subordinators. Their respective cumulant generating functions are given by

| (4.1) | ||||

| (4.2) |

see [23]. Note that for .

4.2 Definition.

Let and be arbitrary. The bilateral Esscher transform is defined as the locally equivalent probability measure with likelihood process

Note that the Esscher transforms from Section 3 are special cases of the just introduced bilateral Esscher transforms . Indeed, we have

| (4.3) |

4.3 Lemma.

For all and we have

under .

Proof.

This follows from Proposition 2.1.3 and Example 2.1.4 in [19]. ∎

4.4 Proposition.

The following statements are true:

-

(1)

If we have

(4.4) then no pair with being a martingale measure exists.

-

(2)

If we have

(4.5) then there exist and a continuous, strictly increasing, bijective function such that:

-

•

For all there exists a unique with being a martingale measure, and it is given by .

-

•

For all no with being a martingale measure exists.

-

•

Proof.

We introduce the functions and as

By Lemmas 2.2 and 4.3, the measure is a martingale measure if and only if and

| (4.6) |

The function is continuous and strictly increasing on with

The function is continuous and strictly decreasing on with

Therefore, if we have (4.4), then for no pair equation (4.6) is satisfied. If we have (4.5), then let be the unique solutions of the equations

with the conventions

| if , | |||

| if , |

and define

| (4.7) |

Then is continuous and strictly increasing with , which finishes the proof. ∎

4.5 Remark.

The proof of Proposition 4.4 shows that the situation occurs if and only if and that the situation occurs if and only if

All equivalent measure transformations preserving the class of tempered stable processes are bilateral Esscher transforms; this follows from [23, Proposition 8.1], see also [7, Example 9.1]. Hence, we introduce the set of parameters

such that the bilateral Esscher transform is a martingale measure. The previous Proposition 4.4 tells us that for (4.4) we have , and that for (4.5) we have

| (4.8) |

Moreover, we remark that condition (4.5) is always fulfilled for .

4.6 Lemma.

For all we have

Proof.

4.7 Theorem.

Proof.

If (4.4) is satisfied, then by Proposition 4.4 we have . Now, suppose that (4.5) is satisfied, and let be the function from Proposition 4.4. Let be the function

By Proposition 4.4 and Lemma 4.6, for each the measure is a martingale measure and we have . The function is strictly increasing with

which gives us

Since is continuous, it attains a minimum and the assertion follows. ∎

4.8 Remark.

In contrast to bilateral Gamma stock models, it can happen that , i.e., there is no equivalent martingale measure under which remains a tempered stable process. Moreover, in contrast to bilateral Gamma stock models, the function from Proposition 4.4, which is defined in (4.7) by means of the inverse of , does not seem to be available in closed form, cf. [22, Remark 6.7].

Next, we consider the -distances

As mentioned at the beginning of this section, for tempered stable stock models the -optimal martingale measure does not exist. However, we can, as provided for the minimal entropy martingale measure, determine the -optimal martingale measure within the class of tempered stable processes. For this purpose, we compute the -distance of a bilateral Esscher transform. Since the subordinators and are independent, for and , the -distance is given by

| (4.10) | ||||

A similar argumentation as in Theorem 4.7 shows that, provided condition (4.5) holds true, there exists a pair minimizing the -distance (4.10), and in this case we also have , where minimizes the function

| (4.11) |

Numerical computations for concrete examples suggest that for , where for each the parameter minimizes (4.11), and minimizes

| (4.12) |

This is not surprising, since it is known that, under suitable technical conditions, the -optimal martingale measure converges to the minimal entropy martingale measure for , see, e.g. [10, 11, 30, 14, 1, 17].

5. Existence of Föllmer Schweizer minimal martingale measures

In this section, we deal with the existence of the Föllmer Schweizer minimal martingale measure in tempered stable stock models. This measure has been introduced in [8] with the motivation of constructing optimal hedging strategies. Throughout this section, we fix a finite time horizon and assume that . Then the constant

| (5.1) |

is well-defined. For technical reasons, we shall also assume that the filtration is generated by the tempered stable process of the form (2.3). As in [22, Lemma 7.1], we show that the discounted stock price process is a special semimartingale. Let be its canonical decomposition and let be the stochastic exponential

| (5.2) |

where we recall that for a semimartingale the stochastic exponential defined as

is the unique solution of the stochastic differential equation

see, e.g. [13, Theorem I.4.61]. The (possibly signed) measure with density

| (5.3) |

is the so-called Föllmer Schweizer minimal martingale measure (in short, FS minimal martingale measure).

5.1 Theorem.

The following statements are equivalent:

-

(1)

is a strict martingale density for .

-

(2)

is a strictly positive -martingale.

-

(3)

We have

(5.4) -

(4)

We have

(5.5) (5.6) and

If the previous conditions are satisfied, then under the FS minimal martingale measure we have

| (5.7) | ||||

Proof.

We only have to show the equivalence (3) (4), as the rest follows by arguing as in the proof of [22, Theorem 7.3]. We observe that (5.4) is equivalent to the two conditions

and, in view of the cumulant generating function given by (2.4), these two conditions are fulfilled if and only if we have (5.5) and (5.6). ∎

5.2 Remark.

Relation (5.7) means that under the driving process is the sum of two independent tempered stable processes. There are the following two boundary values:

- •

- •

As outlined at the end of [22, Section 7], under the FS minimal martingale measure we can construct a trading strategy which minimizes the quadratic hedging error. The arguments transfer to our present situation with a driving tempered stable process.

6. Option pricing in tempered stable stock models

In this section, we present pricing formulae for European call options. After performing a measure change as in Section 3 or 4, that is, or for appropriate parameters, we may assume that the driving process is a tempered stable process of the form (2.3) under the martingale measure . We fix a strike price and a maturity date . Then the price of a European call option with these parameters is given by

First, we shall derive an option pricing formula in closed form by following an idea from [15, Section 8.1]. In the sequel,

denotes the -distribution function and

6.1 Proposition.

Suppose that . Then, the price of the call option is given by

| (6.1) | ||||

Proof.

6.2 Remark.

Note that applying the option pricing formula (6.1) requires knowledge about the densities of tempered stable distributions, which are generally not available in closed form. Therefore, we will turn to the option pricing formula (6.2) below, which is based on Fourier transform techniques. However, we remark that formula (6.1) also holds true in the bilateral Gamma case , for which the densities are given in terms of the Whittaker function, see [20, Section 4].

In the sequel, we will use the following option pricing formula (6.2), which is based on Fourier transform techniques. Let is a tempered stable process of the form (2.3) under , let be a martingale measure as in Section 3, 4 or 5, that is, , or , and denote by the characteristic function of under the martingale measure .

6.3 Proposition.

Proof.

The stock prices are given by

where denotes the Lévy process given by for . Moreover, the Fourier transform of the payoff function is given by

see Table 3.1 in [24]. Furthermore, the characteristic function (2.2) is analytic on the strip by the analyticity of the power function on the main branch of the complex logarithm for . By our parameter restriction on , and possibly taking into account (5.7), we deduce that is analytic on a strip of the form with and . Consequently, [24, Theorem 3.2] applies and provides us with the call option price

which proves (6.2). ∎

6.4 Remark.

Proposition 6.3 does not apply for the boundary case (or , respectively), although might be a martingale measure in this situation, cf. Lemma 2.2. The point is that in this case the characteristic function is not analytic on a strip of the form with and , and hence, the option pricing formula from [24] does not apply.

7. A case study

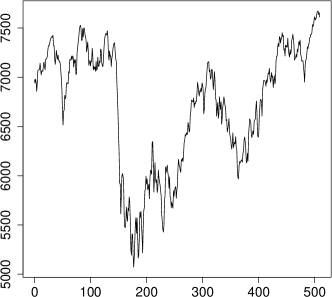

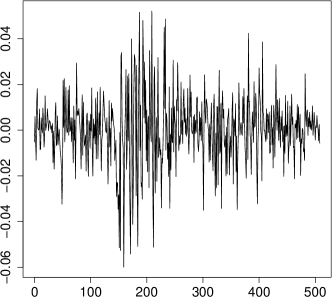

In order to illustrate our previous results, we shall perform a case study in this section. Figure 1 shows historical values of the German stock index DAX from January 3, 2011 until December 28, 2012, and the corresponding log returns. These data are available at http://www.finanzen.net/index/DAX/Historisch.

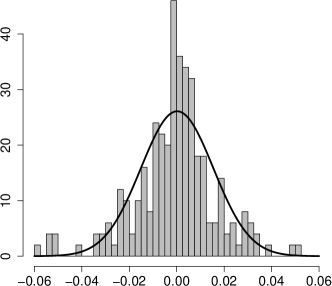

In the sequel, the time is measured in trading days. The data set consists of observations, which corresponds to a period of two years. Figure 2 below shows a histogram for the log returns. In order to estimate the parameters from these historical data by the method of moments, we determine the empirical moments up to order , which are given by

| (7.1) | ||||

| (7.2) | ||||

| (7.3) | ||||

| (7.4) |

Then the parameters with a driving Wiener process are estimated as

| (7.5) |

The fitted density is shown in the left plot of Figure 2.

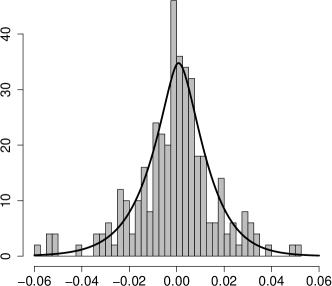

It has already been documented in several case studies that the Black Scholes model does not provide a good fit to observed log returns of financial data, and this also shows up here. Therefore, we consider a tempered stable process of the form (2.3). Recall that for we would have a bilateral Gamma process. We slightly deviate from this situation by choosing

| (7.6) |

In order to estimate the remaining parameters by the method of moments, we have to solve the system of equations

| (7.11) |

where are given by

see [23, Section 6] for further details. The solution of (7.11) is given by

| (7.12) |

The right plot in Figure 2 shows the fitted tempered stable density. Recall that the densities of tempered stable distributions are generally not available in closed form. For the right plot in Figure 2 we have used the inversion formula

which follows from (2.2) and [31, Lemma 28.5, Proposition 2.5.xii].

In the sequel, we suppose that under the real-world probability measure the process is a tempered stable process of the form (2.3) with (7.6) and estimated parameters (7.12). As the time is measured in trading days, the interest rate denotes the daily interest rate. We suppose that it is given by , which corresponds to an annualized interest rate of . Moreover, we suppose that , i.e., the stock does not pay dividends.

Based on these data, we will illustrate our results from Sections 3–5 concerning the existence of equivalent martingale measures.

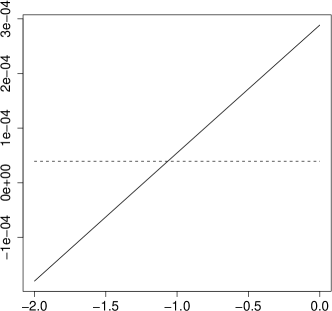

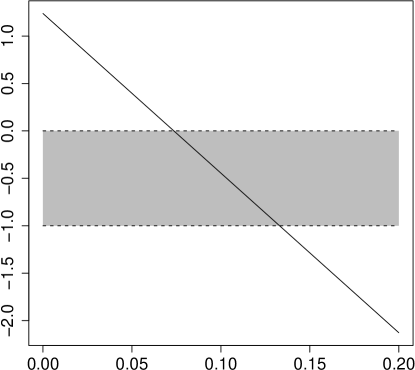

First, we consider the Esscher martingale measure from Section 3. The left plot in Figure 3 shows the function on the interval , together with the interest rate as dashed line. As this plot indicates, condition (3.3) is fulfilled and the solution of equation (3.4) is given by

| (7.13) |

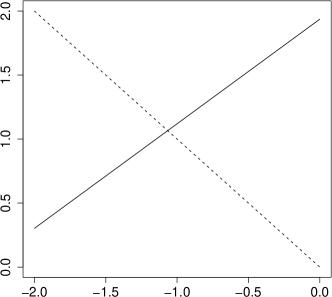

Therefore, the Esscher martingale measure exists. Alternatively, this can be seen by inspecting the right plot in Figure 3, which shows the function from Proposition 4.4 on the interval , together with the graph of as dashed line. The graph of represents all martingale measures which preserve the class of tempered stable processes, and the dashed line represents all Esscher transforms . Therefore, the intersection point corresponds to the just determined Esscher martingale measure .

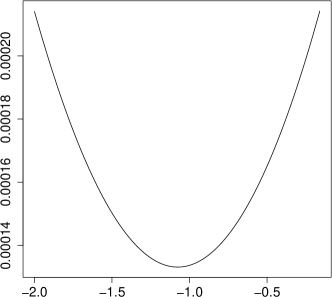

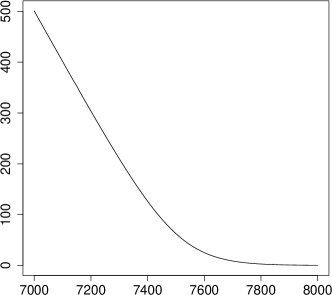

Next, we treat the existence of the minimal bilateral Esscher martingale measures from Section 4. The left plot in Figure 4 shows the relative entropies on the interval ; it indicates that the minimal entropy martingale measure within the class of bilateral Esscher transforms is attained for

| (7.14) |

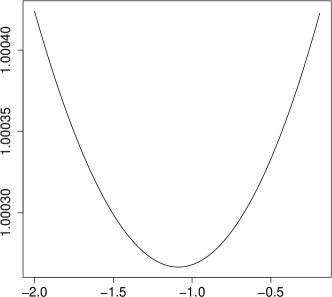

The right plot in Figure 4 shows the -distances on the interval ; it indicates that the variance-optimal martingale measure within the class of bilateral Esscher transforms is attained for

| (7.15) |

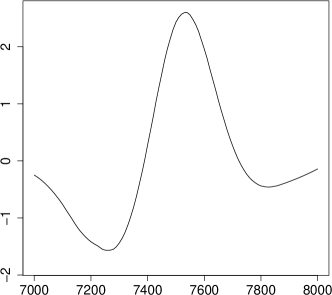

Finally, we treat the existence of the FS minimal martingale measure from Section 5. For this purpose, it will be useful to consider the annualized interest rate . Figure 5 shows the function

| (7.16) |

defined according (5.1) with varying annualized interest rate on the interval . According to Theorem 5.1, the FS minimal martingale measure exists if and only if , that is, the values of belong to the shaded area in Figure 5. We see that the FS minimal martingale measure exists if and only if , that is, the annual interest rate is between and . In particular, in our model with an annual interest rate of the FS minimal martingale measure does not exist.

In the sequel, we shall illustrate our results from Section 6 concerning option pricing formulae.

The left plot in Figure 6 shows the prices of European call options with current stock price , date of maturity and strike prices varying from to . We have computed these prices with the minimal entropy martingale measure, i.e. with formula (6.4), where is given by (7.14), and where the model parameters are given by (7.6) and (7.12). The right plot in Figure 6 shows the difference between these prices and the corresponding Black Scholes prices.

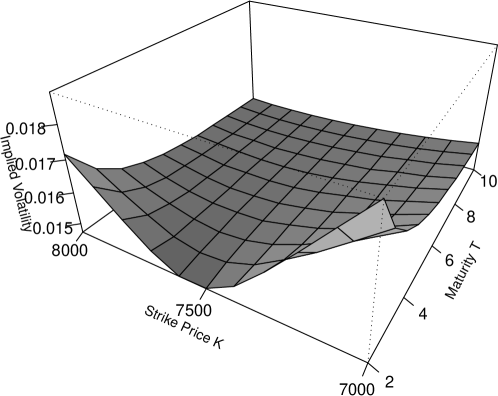

Figure 7 shows the implied volatility surface with current stock price , maturity dates varying from to , and strike prices varying from to . For this procedure, we have computed option prices with the minimal entropy martingale measure, i.e. with formula (6.4), where is given by (7.14), and where the model parameters are given by (7.6) and (7.12), and inverted the Black Scholes formula for the standard deviation . We observe a volatility smile for , which flattens out for longer times of maturity and converges to the standard deviation of the Black Scholes model, which we have estimated in (7.5). For the implied volatility curve shown in Figure 7 behaves almost like the constant function which is equal to estimated in (7.5); this flat behaviour does not change for larger times of maturity . Our empirical observation is not surprising, as we have shown in [23, Theorem 4.10] that, for a tempered stable process and a Brownian motion with the same mean and variance, the distributions of and are close to each other for large time points ; see also [29, Theorem 3.1.ii] for an investigation of the long time behaviour of tempered stable processes.

It is well known that, when estimating the model parameters, reasonable confidence intervals for the mean can only be achieved for a very large number of observations. Therefore, it is important that the model behaves stable with respect to calibration errors. In order to demonstrate the stability of our pricing rules, we have computed option prices for various values of the mean and the standard deviation . For this procedure, we have calculated the respective parameters by solving the system of equations (7.11) with given by (7.3), (7.4) and given by (7.6), and computed the option prices with the minimal entropy martingale measure, i.e. with formula (6.4) and . Figure 8 shows the computed option prices for varying from to , and varying from to , with current stock price , date of maturity and strike price . The surface behaves locally flat and shows that the model is stable with respect to minor calibration errors.

8. Conclusion

In this paper, we have provided a systematic analysis of the existence of equivalent martingale measures for exponential stock price models driven by tempered stable processes, under which the computation of option prices remains analytically tractable.

In this section, we shall review our results and provide a comparison with the results derived in [28]. The textbook [28] deals with financial models driven by several types of tempered stable processes. Its studies encompass the CTS, GTS, KRTS, MTS, NTS, and RDTS processes. We refer to [28] for further details, but point out that the tempered stable distributions considered in this paper correspond to the generalized classical tempered stable (GTS) distributions with mean

| (8.1) |

see formula (3.4) on page 68 in [28], which seems to have a small typo. Note that the calculation of the mean in (8.1) is also consistent with formula (2.12) in [23].

As pointed out in Remark 4.5, all measure transformations preserving the class of tempered stable processes are bilateral Esscher transforms. This is due to the result that for

under a probability measure and

under another probability measure , the measures and are equivalent if and only if , , and . In Section 5.3.3 in [28], such a result has also been shown for GTS-processes, and the characteristic triplet of the logarithm of the Radon-Nikodym derivative has been determined.

Using bilateral Esscher transforms, we have investigated several martingale measures under which the driving process remains a tempered stable process. These martingale measures have been the Esscher martingale measure in Section 3 (which later turned out to be a special case of bilateral Esscher martingale measures), and the minimal entropy martingale measure as well as the -optimal martingale measure in Section 4. Furthermore, we have provided a criterion for the existence of the Föllmer Schweizer minimal martingale measure in Section 5. In case of existence, the driving process turned out to be the sum of two independent tempered stable processes under the new measure, thus providing an analytically tractable model.

In Section 6, we have provided the option pricing formulae (6.3)–(6.5), which apply to the martingale measures that we have studied in the aforementioned sections. These formulae are based on Fourier transform techniques and follow from a result in [24], which has also been provided in [5]. An option pricing formula of this kind can also be found in Section 7.5 in [28]; see formula (7.10) on page 152.

In our case study in Section 7, we have estimated the parameters of the tempered stable process from historical data of the German stock index DAX. Based on our previous results, we have determined appropriate martingale measures and have used these in order to compute option prices and implied volatility surfaces. In Section 7.5.2 in [28], the authors have proceeded differently. Namely, they do not consider the real-world probability measure, they rather calibrate the risk-neutral parameters of the tempered stable process from available option price data. Thus, they assume that the driving process is also a tempered stable process under the martingale measure, which means that the martingale measure is a bilateral Esscher martingale measure. However, comparing our Figure 7 with Figure 7.1 on page 154 in [28], we observe similar results concerning the implied volatility surfaces: For short maturity dates we have a volatility smile, which flattens out for longer maturities.

The class of bilateral Gamma distributions, which occurs for , is a limiting case within the class of tempered stable distributions. Stock price models driven by bilateral Gamma processes have been examined in [22]. Comparing our results from this paper with those from [22], we see that for tempered stable processes with we obtain more restrictive conditions concerning the existence of appropriate martingale measures than for driving bilateral Gamma processes. This is not surprising, as our investigations in [23] have shown that, in many respects, the properties of bilateral Gamma distributions differ from those of all other tempered stable distributions.

Acknowledgement

The authors are grateful to two anonymous referees for valuable comments and suggestions.

References

- [1] Bender, C. and Niethammer, C. (2008): On -optimal martingale measures in exponential Lévy models. Finance and Stochastics 12(3), 381–410.

- [2] Bianchi, M. L., Rachev, S. T., Kim, Y. S. and Fabozzi, F. J. (2010): Tempered stable distributions and processes in finance: numerical analysis. Mathematical and statistical methods for actuarial sciences and finance 33–42, Springer Italia, Milan.

- [3] Bianchi, M. L., Rachev, S. T., Kim, Y. S. and Fabozzi, F. J. (2011): Tempered infinitely divisible distributions and processes. Theory of Probability and its Applications 55(1), 2–26.

- [4] Boyarchenko, S. I. and Levendorskii, S. Z. (2000): Option pricing for truncated Lévy processes. International Journal of Theoretical and Applied Finance 3(3), 549–552.

- [5] Carr, P. and Madan, D. B. (1999): Option valuation using the fast Fourier transform. Journal of Computational Finance 2(4), 61–73.

- [6] Carr, P., Geman, H., Madan, D. B. and Yor, M. (2002): The fine structure of asset returns: An empirical investigation. Journal of Business 75(2), 305–332.

- [7] Cont, R. and Tankov, P. (2004): Financial modelling with jump processes. Chapman and Hall / CRC Press, London.

- [8] Föllmer, H. and Schweizer, M. (1991): Hedging of contingent claims under incomplete information. In: M. H. A. Davis and R. J. Elliott (eds.), "Applied Stochastic Analysis", Stochastics Monographs, vol. 5, Gordon and Breach, London/New York, 389–414.

- [9] Gerber, H. U. and Shiu, E. S. W. (1994): Option pricing by Esscher transforms. Trans. Soc. Actuar. XLVI, 98–140.

- [10] Grandits, P. (1999): The -optimal martingale measure and its asymptotic relation with the minimal-entropy martingale measure. Bernoulli 5(2), 225-247.

- [11] Grandits, P. and Rheinländer, T. (2002): On the minimal entropy martingale measure. Annals of Probability 30(3), 1003–1038.

- [12] Hubalek, F. and Sgarra, C. (2006): Esscher transforms and the minimal entropy martingale measure for exponential Lévy models. Quantitative Finance 6(2), 125–145.

- [13] Jacod, J. and Shiryaev, A. N. (2003): Limit theorems for stochastic processes. Springer, Berlin.

- [14] Jeanblanc, M., Klöppel, S. and Miyahara, Y. (2007): Minimal -martingale measures for exponential Lévy processes. Annals of Applied Probability 17(5-6), 1615–1638.

- [15] Keller-Ressel, M., Papapantoleon, A. and Teichmann, J. (2013): The affine LIBOR models. Mathematical Finance 23(4), 627–658.

- [16] Kim, Y. S., Rachev, S. T., Chung, D. M. and Bianchi, M. L. (2009): The modified tempered stable distribution, GARCH models and option pricing. Probability and Mathematical Statistics 29(1), 91–117.

- [17] Kohlmann, M. and Xiong, D. (2008): The minimal entropy and the convergence of the -optimal martingale measures in a general jump model. Stochastic Analysis and Applications 26(5), 941–977.

- [18] Koponen, I. (1995): Analytic approach to the problem of convergence of truncated Lévy flights towards the Gaussian stochastic process. Physical Review E 52, 1197–1199.

- [19] Küchler, U. and Sørensen, M. (1997): Exponential families of stochastic processes. Springer, New York.

- [20] Küchler, U. and Tappe, S. (2008): Bilateral Gamma distributions and processes in financial mathematics. Stochastic Processes and their Applications 118(2), 261–283.

- [21] Küchler, U. and Tappe, S. (2008): On the shapes of bilateral Gamma densities. Statistics and Probability Letters 78(15), 2478–2484.

- [22] Küchler, U. and Tappe, S. (2009): Option pricing in bilateral Gamma stock models. Statistics and Decisions 27, 281–307.

- [23] Küchler, U. and Tappe, S. (2013): Tempered stable distributions and processes. Stochastic Processes and their Applications 123(12), 4256–4293.

-

[24]

Lewis, A. L. (2001):

A simple option formula for general jump-diffusion and other

exponential Lévy processes.

Envision Financial Systems and OptionCity.net

(http://optioncity.net/pubs/ExpLevy.pdf) - [25] Madan, D. B. (2001): Purely discontinuous asset pricing processes. In: Jouini, E., Cvitanič, J. and Musiela, M. (Eds.), pp. 105–153. Option Pricing, Interest Rates and Risk Management. Cambridge University Press, Cambridge.

- [26] Madan, D. B. and Seneta, B. (1990): The VG model for share market returns. Journal of Business 63, 511–524.

- [27] Mercuri, L. (2008): Option pricing in a Garch model with tempered stable innovations. Finance Research Letters 5, 172–182

- [28] Rachev, S. T., Kim, Y. S., Bianchi, M. L. and Fabozzi, F. J. (2011): Financial models with Lévy processes and volatility clustering. John Wiley & Sons, Inc., Hoboken, New Jersey.

- [29] Rosiński, J. (2007): Tempering stable processes. Stochastic Processes and their Applications 117(6), 677–707.

- [30] Santacroce, M. (2005): On the convergence of the -optimal martingale measures to the minimal entropy martingale measure. Stochastic Analysis and Applications 23(1), 31–54.

- [31] Sato, K. (1999): Lévy processes and infinitely divisible distributions. Cambridge studies in advanced mathematics, Cambridge.

- [32] Sztonyk, P. (2010): Estimates of tempered stable densities. Journal of Theoretical Probability 23(1), 127–147.

- [33] Zhang, S. and Zhang, X. (2009): On the transition law of tempered stable Ornstein-Uhlenbeck processes. Journal of Applied Probability 46(3), 721–731.